Embed Size (px)

Citation preview

Metropolitan Area Advisory Committee and Affiliates

Report to the Audit Committee and Board of Directors

Years Ended December 31, 2012 and 2011

Table of Contents

EXECUTIVE SUMMARY 1

STATEMENT ON AUDITING STANDARDS NO. 114 COMMUNICATION LETTER 2

ADJUSTING JOURNAL ENTRIES REPORT 4

RECLASSIFYING JOURNAL ENTRY REPORT 4

TREND AND RATIO ANALYSIS 5

MANAGEMENT REPRESENTATION LETTER 7

1

EXECUTIVE SUMMARY To assist you in your responsibilities as a member of the Audit Committee and Board of Directors, this section summarizes the most significant conclusions reached and issues addressed during our audit of Metropolitan Area Advisory Committee and Affiliates (collectively the Organization) for the year ended December 31, 2012. Significant Conclusions and Issues

We have completed our audit and issued our report, dated August 20, 2013. Based on our work performed:

Our audit scope was in accordance with that communicated in our engagement letter dated January 4,

2013.

We rendered an unmodified opinion on the December 31, 2012 consolidated financial statements.

We identified no conditions which we consider to be material weaknesses in internal controls.

Audit areas designated as greater than normal risk have been addressed and resolved to our satisfaction,

in the context of the overall fairness of the presentation of the consolidated financial statements.

We received the full cooperation of management and staff throughout the Organization and were kept

informed as to developments and plans affecting our audit scope.

The following report includes required communications and additional information for the benefit of the Audit Committee and Board of Directors.

August 20, 2013 To the Board of Directors Metropolitan Area Advisory Committee and Affiliates Chula Vista, California We have audited the consolidated financial statements of Metropolitan Area Advisory Committee and Affiliates (collectively the Organizations) for the year ended December 31, 2012, and have issued our report thereon dated August 20, 2013. Professional standards require that we provide you with information about our responsibilities under generally accepted auditing standards and Government Auditing Standards and OMB Circular A-133, as well as certain information related to the planned scope and timing of our audit. We have communicated such information in our letter to you dated January 4, 2013. Professional standards also require that we communicate to you the following information related to our audit.

Significant Audit Findings

Qualitative Aspects of Accounting Practices

Management is responsible for the selection and use of appropriate accounting policies. The significant accounting policies used by Metropolitan Area Advisory Committee and Affiliates are described in Note 1 to the consolidated financial statements. No significant new accounting policies were adopted and the application of existing policies was not changed during 2012. We noted no transactions entered into by the Organizations during the year for which there is a lack of authoritative guidance or consensus. All significant transactions have been recognized in the consolidated financial statements in the proper period.

Accounting estimates are an integral part of the consolidated financial statements prepared by management and are based on management’s knowledge and experience about past and current events and assumptions about future events. Certain accounting estimates are particularly sensitive because of their significance to the consolidated financial statements and because of the possibility that future events affecting them may differ significantly from those expected. The most sensitive estimates affecting the consolidated financial statements were:

Management’s estimate of the accounts receivable allowance for doubtful accounts is based on management’s estimate from prior experience. We evaluated the key factors and assumptions used to develop the accounts receivable allowance for doubtful accounts in determining that it is reasonable in relation to the consolidated financial statements taken as a whole.

Management’s estimate of the useful lives of property and equipment and rental property is based on the anticipated useful life of the assets using IRS tables as a guideline. We evaluated the key factors and assumptions used to develop the useful lives of property and equipment and rental property in determining that it is reasonable in relation to the consolidated financial statements taken as a whole.

Certain financial statement disclosures are particularly sensitive because of their significance to financial statement users. The consolidated financial statement disclosures are neutral, consistent, and clear.

Difficulties Encountered in Performing the Audit

We encountered no significant difficulties in dealing with management in performing and completing our audit.

Corrected and Uncorrected Misstatements

Professional standards require us to accumulate all misstatements identified during the audit, other than those that are clearly trivial, and communicate them to the appropriate level of management. Management has corrected all such misstatements. In addition, the misstatements detected as a result of audit procedures and corrected by management were material, either or in the aggregate, to the consolidated financial statements taken as a whole. The adjustments are attached to this letter for your reference.

3

Disagreements with Management

For purposes of this letter, a disagreement with management is a financial accounting, reporting, or auditing matter, whether or not resolved to our satisfaction, that could be significant to the consolidated financial statements or the auditors’ report. We are pleased to report that no such disagreements arose during the course of our audit.

Management Representations

We have requested certain representations from management that are included in the management representation letter dated August 20, 2013.

Management Consultations with Other Independent Accountants

In some cases, management may decide to consult with other accountants about auditing and accounting matters, similar to obtaining a “second opinion” on certain situations. If a consultation involves application of an accounting principle to the Organizations’ consolidated financial statements or a determination of the type of auditors’ opinion that may be expressed on those statements, our professional standards require the consulting accountant to check with us to determine that the consultant has all the relevant facts. To our knowledge, there were no such consultations with other accountants.

Other Audit Findings or Issues

We generally discuss a variety of matters, including the application of accounting principles and auditing standards, with management each year prior to retention as the Organizations’ auditors. However, these discussions occurred in the normal course of our professional relationship and our responses were not a condition to our retention.

During the course of our audit we noted matters involving internal control and other operational matters that do not meet the definitions of significant deficiency or material weakness that are presented for your consideration. Our comments and recommendations are intended to improve internal control, or result in other operating efficiencies. Our comments are summarized as follows:

As noted in prior years, Metropolitan Area Advisory Committee’s internal policies and procedures require staff to maintain current CPR certification, however it is not an explicit requirement of Head Start. During our testwork we identified 8 selections out of 40 where the teacher’s file did not contain evidence that the teacher was CPR certified. We recommend that Metropolitan Area Advisory Committee adhere to its internal policies and procedures.

AKT noted that the Organization stopped using software to record in-kind expenses during the year which resulted in packets of support without detailed lists of contributions. The donation totals on summary sheets are manually recalculated before being entered into the accounting system, but the lack of a listing could lead to errors. We recommend that the Organization input all in-kind donations into a schedule that can be reviewed and recalculated more easily.

Other Matters

With respect to the supplementary information accompanying the consolidated financial statements, we made certain inquiries of management and evaluated the form, content, and methods of preparing the information to determine that the information complies with accounting principles generally accepted, the method of preparing it has not changed from the prior period, and the information is appropriate and complete in relation to our audit of the consolidated financial statements. We compared and reconciled the supplementary information to the underlying accounting records used to prepare the consolidated financial statements or to the consolidated financial statements themselves.

This information is intended solely for the use of Board of Directors and management of Metropolitan Area Advisory Committee and Affiliates and is not intended to be, and should not be, used by anyone other than these specified parties.

Very truly yours,

AKT LLP

4

Adjusting Journal Entries

Account Description Debit Credit

Adjusting Journal Entries JE # 1To adjust beginning net assets to agree to prior year ending net assets.

7800 Miscellaneous 31.003000 Fund Balance 31.00

Total 31.00 31.00

Adjusting Journal Entries JE # 2Client entry.

1112 Accounts Receivable 58,813.001250 Accounts Receivable 93.007200 Administrative Expense 255.002220 Working Capital Advance 93.006000 Grant Revenue 58,813.006500 Indirect Admin Income 255.00

Total 59,161.00 59,161.00

Adjusting Journal Entries JE # 3

2250 Loans Payable 354,000.001250 Accounts Receivable 354,000.00

Total 354,000.00 354,000.00

Adjusting Journal Entries JE # 6

1205 Investment in Partnership 29.001257 AR - Rental Properties 10,968.006860 Partnership & Asset Management Fees (Properties) 10,968.006950 Gain on Investment 29.00

Total 10,997.00 10,997.00

To eliminate charter school note payable to MAAC and related MAAC receivable.

(Client) To make adjustments related to Mercado

Reclassifying Journal Entry

Account Description Debit Credit

Reclassifying Journal Entries JE # 1

2250 Loans Payable 712,211.002245 Current Loans Payable 712,211.00

Total 712,211.00 712,211.00

To reclassify loans payable as current.

5

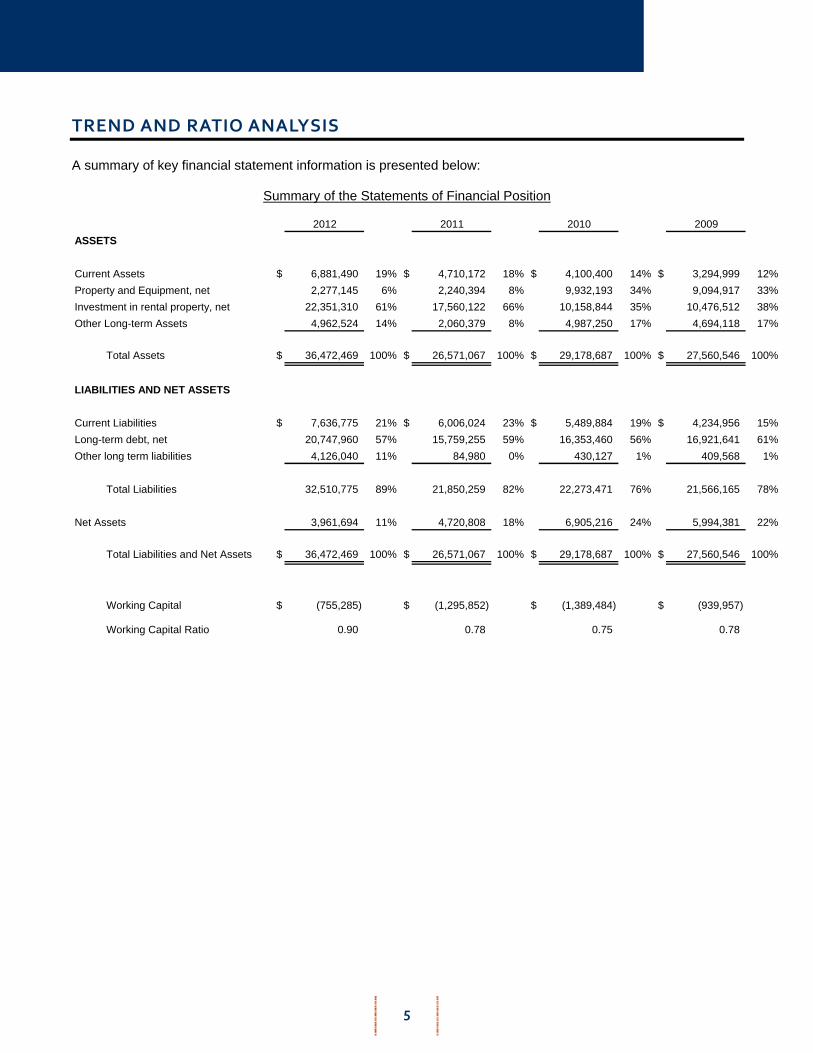

TREND AND RATIO ANALYSIS A summary of key financial statement information is presented below:

Summary of the Statements of Financial Position

2012 2011 2010 2009

ASSETS

Current Assets $ 6,881,490 19% $ 4,710,172 18% $ 4,100,400 14% $ 3,294,999 12%

Property and Equipment, net 2,277,145 6% 2,240,394 8% 9,932,193 34% 9,094,917 33%

Investment in rental property, net 22,351,310 61% 17,560,122 66% 10,158,844 35% 10,476,512 38%

Other Long-term Assets 4,962,524 14% 2,060,379 8% 4,987,250 17% 4,694,118 17%

Total Assets $ 36,472,469 100% $ 26,571,067 100% $ 29,178,687 100% $ 27,560,546 100%

LIABILITIES AND NET ASSETS

Current Liabilities $ 7,636,775 21% $ 6,006,024 23% $ 5,489,884 19% $ 4,234,956 15%

Long-term debt, net 20,747,960 57% 15,759,255 59% 16,353,460 56% 16,921,641 61%

Other long term liabilities 4,126,040 11% 84,980 0% 430,127 1% 409,568 1%

Total Liabilities 32,510,775 89% 21,850,259 82% 22,273,471 76% 21,566,165 78%

Net Assets 3,961,694 11% 4,720,808 18% 6,905,216 24% 5,994,381 22%

Total Liabilities and Net Assets $ 36,472,469 100% $ 26,571,067 100% $ 29,178,687 100% $ 27,560,546 100%

Working Capital $ (755,285) $ (1,295,852) $ (1,389,484) $ (939,957)

Working Capital Ratio 0.90 0.78 0.75 0.78

6

TREND AND RATIO ANALYSIS

Summary of the Statements of Activities

2012 2011 2010 2009

Revenue and Support $ 38,530,582 $ 37,498,358 $ 30,596,420 $ 24,991,221

Program Services 36,326,251 92% 36,889,796 93% 27,198,908 92% 22,677,578 91%Supporting Services:

Management and general 2,915,710 7% 2,749,360 7% 2,204,424 7% 1,936,296 8%Fundraising 47,733 0% 43,610 0% 238,809 1% 174,699 1%Cost of direct benefit to donors - 0% - 0% 43,444 0% - 0%

Total Supporting Services 2,963,443 8% 2,792,970 7% 2,486,677 8% 2,110,995 9%

Total Expenses 39,289,694 100% 39,682,766 100% 29,685,585 100% 24,788,573 100%

Net Income (Loss) $ (759,112) $ (2,184,408) $ 910,835 $ 202,648

A summary of the allocation of functional expenses is presented below:

‐

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Program Services Supporting Services

2012

2011

2010

2009

1355 3rd Avenue, Chula Vista, CA 91911 / P 619.426.3595 / F 619.426.2173 / www.maacproject.org

August 20, 2013

AKT LLP 7676 Hazard Center Drive, Suite 1300 San Diego, CA 92108

This representation letter is provided in connection with your audits of the consolidated financial statements of Metropolitan Area Advisory Committee and Affiliates (collectively the Organizations), which comprise the statements of financial position as of December 31, 2012 and 2011, and the related statements of activities, changes in net assets, and cash flows for the years then ended, and the related notes to the consolidated financial statements, for the purpose of expressing an opinion as to whether the consolidated financial statements are presented fairly, in all material respects, in accordance with accounting principles generally accepted in the United States (U.S. GAAP).

Certain representations in this letter are described as being limited to matters that are material. Items are considered material, regardless of size, if they involve an omission or misstatement of accounting information that, in light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would be changed or influenced by the omission or misstatement. An omission or misstatement that is monetarily small in amount could be considered material as a result of qualitative factors.

We confirm, to the best of our knowledge and belief, as of August 20, 2013, the following representations made to you during your audit.

Consolidated financial statements

• We have fulfilled our responsibilities, as set out in the terms of the audit engagement letter dated January 4, 2013, including our responsibility for the preparation and fair presentation of the consolidated financial statements.

• The consolidated financial statements referred to above are fairly presented in conformity with U.S. GAAP.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

• We acknowledge our responsibility for the design, implementation, and maintenance of internal control to prevent and detect fraud.

• Significant assumptions we used in making accounting estimates, including those measured at fair value, are reasonable.

• Related party relationships and transactions have been appropriately accounted for and disclosed in accordance with the requirements of U.S. GAAP.

• All events subsequent to the date of the consolidated financial statements and for which U.S. GAAP requires adjustment or disclosure have been adjusted or disclosed.

• The effects of all known actual or possible litigation, claims, and assessments have been accounted for and disclosed in accordance with U.S. GAAP.

• Material concentrations have been appropriately disclosed in accordance with U.S. GAAP.

AKT LLP Page 2 of 5

• Guarantees, whether written or oral, under which the organization is contingently liable, have been properly recorded or disclosed in accordance with U.S. GAAP.

Information Provided

• We have provided you with:

o Access to all information, of which we are aware, that is relevant to the preparation and fair presentation of the consolidated financial statements, such as records, documentation, and other matters.

o Additional information that you have requested from us for the purpose of the audit.

o Unrestricted access to persons within the entity from whom you determined it necessary to obtain audit evidence.

• All material transactions have been recorded in the accounting records and are reflected in the consolidated financial statements.

• We have disclosed to you the results of our assessment of the risk that the consolidated financial statements may be materially misstated as a result of fraud.

• We have no knowledge of any fraud or suspected fraud that affects the organization and involves:

o Management,

o Employees who have significant roles in internal control, or

o Others where the fraud could have a material effect on the consolidated financial statements.

• We have no knowledge of any allegations of fraud or suspected fraud affecting the organization’s consolidated financial statements communicated by employees, former employees, grantors, regulators, or others.

• We have no knowledge of any instances of noncompliance or suspected noncompliance with laws and regulations whose effects should be considered when preparing consolidated financial statements.

• We have disclosed to you all known actual or possible litigation, claims, and assessment whose effects should be considered when preparing the consolidated financial statements.

• We have disclosed to you the identity of the organization’s related parties and all the related party relationships and transactions of which we are aware.

• The organization has satisfactory title to all owned assets, and there are no liens or encumbrances on such assets nor has any asset been pledged as collateral.

• We are responsible for compliance with the laws, regulations, and provisions of contracts and grant agreements applicable to us; and we have identified and disclosed to you all laws, regulations and provisions of contracts and grant agreements that we believe have a direct and material effect on the determination of financial statement amounts or other financial data significant to the audit objectives.

• Metropolitan Area Advisory Committee is an exempt organization under Section 501(c)(3) of the Internal Revenue Code. Any activities of which we are aware that would jeopardize the Organization’s tax-exempt status, and all activities subject to tax on unrelated business income or excise or other tax, have been disclosed to you. All required filings with tax authorities are up-to-date.

• We acknowledge our responsibility for presenting the consolidating schedules I and II, as well as the Weatherization Program information, in accordance with U.S. GAAP, and we believe this information, including its form and content, is fairly presented in accordance with U.S. GAAP. The methods of measurement and presentation of the supplementary information have not changed

AKT LLP Page 3 of 5

from those used in the prior period, and we have disclosed to you any significant assumptions or interpretations underlying the measurement and presentation of the supplementary information.

• With respect to federal award programs:

a. We are responsible for understanding and complying with, and have complied with the requirements of OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, including requirements relating to preparation of the schedule of expenditures of federal awards.

b. We have prepared the schedule of expenditures of federal awards in accordance with OMB Circular A-133 and have identified and disclosed in the schedule expenditures made during the audit period for all awards provided by federal agencies in the form of grants, federal cost-reimbursement contracts, loans, loan guarantees, property (including donated surplus property), cooperative agreements, interest subsidies, insurance, food commodities, direct appropriations, and other assistance.

c. We acknowledge our responsibility for presenting the schedule of expenditures of federal awards (SEFA) in accordance with the requirements of OMB Circular A-133 §310.b, and we believe the SEFA, including its form and content, is fairly presented in accordance with the Circular. The methods of measurement and presentation of the SEFA have not changed from those used in the prior period, and we have disclosed to you any significant assumptions and interpretations underlying the measurement and presentation of the SEFA.

d. If the SEFA is not presented with the audited consolidated financial statements, we will make the audited consolidated financial statements readily available to the intended users of the supplementary information no later than the date we issue the supplementary information and the auditor’s report thereon.

e. We have identified and disclosed to you all of our government programs and related activities subject to OMB Circular A-133, and included in the SEFA expenditures made during the audit period for all awards provided by federal agencies in the form of grants, federal cost-reimbursement contracts, loans, loan guarantees, property (including donated surplus property), cooperative agreements, interest subsidies, insurance, food commodities, direct appropriations, and other assistance.

f. We are responsible for understanding and complying with, and have complied with the requirements of laws, regulations, and the provisions of contracts and grant agreements related to each of our federal programs and have identified and disclosed to you the requirements of laws, regulations, and the provisions of contracts and grant agreements that are considered to have a direct and material effect on each major program.

g. We are responsible for establishing and maintaining, and have established and maintained, effective internal control over compliance requirements applicable to federal programs that provide reasonable assurance that we are managing our federal awards in compliance with laws, regulations, and the provisions of contracts and grant agreements that could have a material effect on our federal programs. We believe the internal control system is adequate and is functioning as intended.

h. We have made available to you all contracts and grant agreements (including amendments, if any) and any other correspondence with federal agencies or pass-through entities relevant to federal programs and related activities.

i. We have received no requests from a federal agency to audit one or more specific programs as a major program.

j. We have complied with the direct and material compliance requirements (except for noncompliance disclosed to you), including when applicable, those set forth in the OMB Circular A-133 Compliance Supplement, relating to federal awards and have identified and disclosed to you all amounts questioned and all known noncompliance with the requirements of federal awards including those resulting from other audits or program reviews.

AKT LLP Page 4 of 5

k. We have disclosed to you any communications from grantors and pass-through entities concerning possible noncompliance with the direct and material compliance requirements, including communications received from the end of the period covered by the compliance audit to the date of the auditor’s report.

l. We have disclosed to you the findings received and related corrective actions taken for previous audits, attestation engagements, and internal or external monitoring that directly relate to the objectives of the compliance audit, including findings received and corrective actions taken from the end of the period covered by the compliance audit to the date of the auditor’s report.

m. Amounts claimed or used for matching were determined in accordance with relevant guidelines in OMB Circular A-122, Cost Principles for Nonprofit Organizations, and Subpart C, “Cost Sharing and Matching,” of OMB Circular A-110, Grants and Agreements with Institutions of Higher Education, Hospitals, and Other Non-Profit Organizations.

n. We have disclosed to you our interpretation of compliance requirements that may have varying interpretations.

o. We have made available to you all documentation relating to compliance with the direct and material compliance requirements, including information related to federal program financial reports and claims for advances and reimbursements.

p. We have disclosed to you the nature of any subsequent events that provide additional evidence about conditions that existed at the end of the reporting period affecting noncompliance during the reporting period.

q. There are no known instances of noncompliance with direct and material compliance requirements that occurred subsequent to the period covered by the auditor’s report.

r. No changes have been made in internal control over compliance or other factors that might significantly affect internal control, including any corrective action we have taken regarding significant deficiencies in internal control over compliance (including material weaknesses in internal control over compliance), have occurred subsequent to the date as of which compliance was audited.

s. Federal program financial reports and claims for advances and reimbursements are supported by the books and records from which the basic consolidated financial statements have been prepared.

t. The copies of federal program financial reports provided you are true copies of the reports submitted, or electronically transmitted, to the respective federal agency or pass-through entity, as applicable.

u. We have monitored subrecipients to determine that they have expended pass-through assistance in accordance with applicable laws and regulations and have met the requirements of OMB Circular A-133.

v. We have taken appropriate action, including issuing management decisions, on a timely basis after receipt of subrecipients’ auditor’s reports that identified noncompliance with laws, regulations, or the provisions of contracts or grant agreements and have ensured that subrecipients have taken the appropriate and timely corrective action on findings.

w. We have considered the results of subrecipient audits and have made any necessary adjustments to our books and records.

x. We have charged costs to federal awards in accordance with applicable cost principles.

y. We are responsible for and have accurately prepared the summary schedule of prior audit findings to include all findings required to be included by OMB Circular A-133 and we have provided you with all information on the status of the follow-up on prior audit findings by federal awarding agencies and pass-through entities, including all management decisions.

![~Welcome~ [] · 2013-04-17 · – internal accounting controls, including the nature, extent and results of the ... of Directors. Audit Committee Report • Guided by the Audit Committee](https://img.dokumen.tips/doc/110x75/5f8fda185018013b0376d1d2/welcome-2013-04-17-a-internal-accounting-controls-including-the-nature.jpg)