Embed Size (px)

Citation preview

Report on

Public Universities and TAFE Colleges

and of other

Ministerial Portfolio Agencies for 2001

Report No. 2

August 2002

AUDITOR GENERALfor

Western Australia

SERVING THE PUBLIC INTEREST

AUDITOR GENERAL FOR WESTERN AUSTRALIA

2

THE SPEAKER THE PRESIDENTLEGISLATIVE ASSEMBLY LEGISLATIVE COUNCIL

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHERMINISTERIAL PORTFOLIO AGENCIES FOR 2001

I submit to Parliament the Report on Public Universities and TAFE Colleges and of other Ministerial Portfolioagencies for 2001, pursuant to section 95 of the Financial Administration and Audit Act 1985 (FAAA). ThisReport summarises the results of the 21 financial statement and 16 performance indicator audits of WesternAustralian public universities, vocational education and training colleges and their subsidiaries, for the yearended December 31, 2001. (The subsidiaries are not subject to the FAAA and are not required to submitperformance indicators).

In addition, the Report summarises the results of the 25 financial statement and nine performance indicatoraudits of agencies with a June 30, 2001 reporting date, that were completed after my Report on MinisterialPortfolios at November 30, 2001 was finalised.

This Report also brings to the attention of Parliament the more significant operational, legislative complianceand management issues that have been raised with agencies.

D D R PEARSONAUDITOR GENERALAugust 14, 2002

AUDITOR GENERALfor

Western Australia

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

3

Foreword 4

Overview of the Tertiary Sector 5

Tertiary Organisations that Receive Government Funding 5

Key Financial Statistics 5

Performance Indicators 7

Summary of Audit Results 11

Audit Opinions 11

Reasons for Audit Qualifications 12

Quality of Financial Statements and Performance Indicators 13

Management Control Issues 14

Progress on Issues Previously Reported 20

Other Ministerial Portfolio Agencies for 2001 22

Summary of Audit Results 22

Reasons for Audit Qualifications 23

Management Control Issues 24

Previous reports of the Auditor General 25

Contents

AUDITOR GENERAL FOR WESTERN AUSTRALIA

4

In discharging the public sector audit mandate, there is a responsibility to provide Parliament withindependent and impartial advice regarding public sector accountability and performance. This Reporttherefore provides:

a summary of the results of the annual financial statement and performance indicator audits of publicuniversities and TAFE colleges in Western Australia for the 2001 academic year;

a summary of the results of the financial statement audits for subsidiary companies of theseinstitutions for the year ending December 31, 2001;

summaries of selected financial statement balances and key performance indicators, to providereaders with an indication of performance trends over time;

a summary of the results of the annual financial statement and performance indicator audits of thoseagencies with a June 30, 2001 reporting date, that were completed after my Report on MinisterialPortfolios at November 30, 2001 was finalised; and

commentary on significant control issues that have been identified concurrently with the annualaudits.

Issues included in this Report have arisen from the conduct of audit procedures that are primarilyintended to enable the formation of an opinion on the controls, financial statements and performanceindicators of individual agencies and subsidiary companies. Not all matters of significance will beidentified during the course of such routine financial statement and performance indicator audits. Othermatters may be detected during the course of additional and complementary audit procedures, such ascontrol, compliance and accountability audits and performance examinations and are reported separatelyto Parliament.

It is important to note that agency management remains responsible for keeping proper accounts andmaintaining adequate systems of internal control, preparing and presenting the financial statements,complying with the Financial Administration and Audit Act 1985 (FAAA) and other relevant written law,and for developing and maintaining proper records and systems for preparing and presenting relevantand appropriate performance indicators. The primary responsibility for the detection, investigation andprevention of irregularities rests with agency management.

Foreword

This section summarises key financial and operational statistics for the sector. It also includes summariesof selected financial information and key performance indicators for each of the 16 institutions in thissector.

Tertiary Organisations that Receive Government FundingIn 2001 the public tertiary education sector comprised four universities, Curtin University of Technology(Curtin); Edith Cowan University (Edith Cowan); Murdoch University (Murdoch) and The Universityof Western Australia (UWA) and 12 colleges providing TAFE courses (five metropolitan and sevencountry colleges).

Other private training organisations, including a private university and private training providers ofVocational Education and Training (VET) courses, also receive Federal funds or State funding under theState Training Strategy, however these organisations are beyond the scope of this report.

The public universities and colleges provided education and training to more than 151 000 students(universities 66 000 and colleges 85 000) and employed some 10 700 full-time equivalent staff in 2001.

State Government funding totalled $318 million (universities $57 million and colleges $261 million1).Revenue from other sources, including funding received directly from the Commonwealth totalled $1.06billion (universities $980 million and colleges $80 million).

Key Financial StatisticsTables one to four provide an overview of selected assets, liabilities, equity, expenditure and revenue ofuniversities and colleges and the extent of their dependence on Government funding.

Table 1: Universities’ assets, liabilities and equity.* Curtin University’s working capital is overstated by $4.1 million because current receivables are overstated by

that amount. In addition, Equity is overstated by $76.7 million (see Reasons for Audit Qualifications at page 12).

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

5

Overview of the Tertiary Sector

UNIVERSITY ASSETS LIABILITIES EQUITY

Investments Land & Employee Leaveand Working Buildings and

Capital SuperannuationEntitlements

$ Million $ Million $ Million $ Million2000 2001 2000 2001 2000 2001 2000 2001

Curtin 69 50* 396 455 112 118 396 510*

Edith Cowan 7 19 324 329 52 52 310 325

Murdoch 6 11 244 285 9 11 271 311

UWA 516 509 512 535 50 50 1 101 1 133

TOTAL 598 589 1 476 1 604 223 231 2 078 2 279

1 Includes Australian National Training Authority (ANTA) funding received from the Western Australian Department of Training.

Table 2: Universities’ expenditure and revenue.(1) For 2000, Curtin, Edith Cowan and Murdoch Universities, due to a change in reporting requirements, changed

their accounting policies to recognise grants received in advance for 2001 as a liability as at December 31, 2000rather than as revenue upon receipt.

Had this change in accounting policy not occurred, Revenue From Government (excluding HECS) for 2000would have been $8 million higher for Curtin, $5.7 million higher for Edith Cowan and $4.2 million higher forMurdoch than the reported figures.

In addition, HECS revenue for 2000 would have been $3.6 million higher for Curtin, $3.1 million higher forEdith Cowan and $1.7 million higher for Murdoch than the reported figures.

UWA did not change its accounting policy in relation to revenue, as the University was already recognisinggrants received in advance, as a liability.

(2) Includes $5.7 million from the State Government for development of the Academy Stagehouse.(3) Curtin University’s revenue from other sources is overstated by $76.7 million (see Reasons for Audit

Qualifications at page 12).

Table 3: Colleges’ working capital, assets and equity.* C Y O’Connor College was established as a statutory authority on January 1, 2001.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

6

UNIVERSITY EXPENDITURE REVENUE

Staffing Costs Other From HECS From OtherGovernment Sources

(excluding HECS)$ Million $ Million $ Million $Million $Million

2000 2001 2000 2001 2000(1) 2001 200 2001 2000 2001

Curtin 182 206 145 146 114 135 51 54 136 232(3)

Edith Cowan 104 114 62 64 79 100(2) 41 46 42 48Murdoch 79 85 52 67 65 73 23 27 42 50UWA 186 198 125 133 145 155 40 43 149 152TOTAL 551 603 384 410 403 463 155 170 369 482

TAFE College Working Capital Land & Buildings Equity$ Million $ Million $ Million

2000 2001 2000 2001 2000 2001

Central -0.8 -2.2 122.8 135.0 125.7 134.3

Central West 3.0 1.6 11.8 19.6 21.4 23.0

Challenger 0.3 1.4 48.4 55.5 58.4 60.7

C Y O’Connor * - 0.3 - 7.4 - 9.2

Eastern Pilbara 2.2 0.6 26.8 25.6 29.0 26.0

Great Southern 1.9 1.9 8.4 11.8 12.5 15.0

Kimberley 1.7 1.7 8.6 10.7 12.6 13.1

Midland 2.7 1.7 26.8 34.4 29.6 35.4

South East Metropolitan 2.6 0.0 38.3 55.4 42.7 56.3

South West Regional 2.8 3.0 20.8 21.4 24.2 25.1

West Coast 2.0 1.7 51.2 58.1 52.9 58.0

West Pilbara 2.7 2.4 10.8 10.9 14.4 14.1

TOTAL 21 14 375 446 423 470

OVERVIEW OF THE TERTIARY SECTOR (continued)

Table 4: Colleges’ expenditure and revenue from services. * C Y O’Connor College was established as a statutory authority on January 1, 2001.

Performance IndicatorsKey performance indicators of universities and colleges include student satisfaction surveys, thepercentage of graduates who were employed or proceeded to further study, the ratio of researchpublications to academic staff and the cost per student or student hour. In addition to theseaudited key performance indicators, detailed operational and financial indicators are reported toCommonwealth funding organisations2 and the Department of Training.

The selected audited key indicators listed in Tables 5a and 5b provide an indication of trends overtime for each institution. Due to significant variations in courses offered between bothuniversities and colleges, different student demographics and differing costs and economicconditions across geographic regions and use of different rating scales for measuringperformance, direct comparisons between institutions should not be made on the basis of thisdata alone.

For further discussion and explanation of the indicators for individual institutions, referenceshould be made to the annual reports of those institutions.

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

7

TAFE College EXPENDITURE REVENUEFROM SERVICE

Staffing Costs Other$ Million $ Million $ Million

2000 2001 2000 2001 2000 2001

Central 47.0 51.8 22.3 28.3 17.9 19.5

Central West 9.0 10.1 5.4 7.8 3.7 3.4

Challenger 30.5 32.1 14.1 16.8 12.1 11.6

C Y O’Connor * - 6.6 - 3.3 - 1.2

Eastern Pilbara 9.8 10.5 6.9 7.5 2.2 1.6

Great Southern 8.1 8.3 3.6 4.8 2.2 2.2

Kimberley 6.3 7.2 4.1 4.3 0.9 1.1

Midland 14.1 14.9 5.6 7.7 4.5 3.6

South East Metropolitan 27.6 29.9 13.6 15.4 12.5 11.2

South West Regional 12.9 13.0 7.1 8.0 3.9 3.9

West Coast 34.0 34.6 14.0 14.6 19.1 17.2

West Pilbara 5.6 6.1 4.6 5.4 2.6 3.4

TOTAL 205 225 101 124 83 80

2 Universities report performance to the Department of Education, Science and Training (DEST - formerly DETYA) and summarisedcollege information is reported to the Australian National Training Authority (ANTA).

Key Performance Indicators for Universities

Selected key performance indicators for universities are included in Table 5a. Graduate Satisfaction andGraduate Destination are measured as part of a national survey of all university undergraduate studentsin the year after they complete their studies. Graduate Satisfaction measures the percentage of graduatesthat were satisfied with the quality of their course. Graduate Destination represents the percentage ofstudents who were employed in their mode of choice (part-time or full-time) at the time of the surveys.It should be noted that survey questions and timing of the surveys for universities differ from those ofcolleges.

Teaching Expenditure per EFTSU (Equivalent Full-Time Student Unit) is calculated by dividing thenumber of equivalent full-time undergraduate students into the total expenditure on teaching relatedactivities.

Table 5a: Selected Audited Key Performance Indicators for Universities – 1997 to 2001.

UNIVERSITIES 1997 1998 1999 2000 2001

CURTIN

Graduate Satisfaction (% satisfied) N/A 90% 91% 90% 88%

Graduate Destination (% employed) 83% 82% 80% 83% 84%

Teaching Expenditure per EFTSU($ per Equivalent Full-time Student Unit) $12 423 $13 444 $12 695 $14 422 $15 110

EDITH COWAN

Graduate Satisfaction (% satisfied) 88% 88% 87% 90% 88%

Graduate Destination (% employed) 78% 76% 76% 77% 81%

Teaching Related Expenditure per EFTSU($ per Equivalent Full-time Student Unit) N/A N/A $10 833 $10 039 $10 079

MURDOCH

Graduate Satisfaction (% satisfied) N/A N/A 91% 92% 93%

Graduate Destination (% employed) 74% 74% 75% 76% 78%

Teaching Related Expenditure per EFTSU($ per Equivalent Full-time Student Unit) $13 468 $13 665 $13 166 $13 073 $14 741

UWA

Graduate Satisfaction (% satisfied) 88% 88% 89% 90% 91%

Graduate Destination (% employed) 82% 82% 84% 85% 85%

Teaching Expenditure per EFTSU($ per Equivalent Full-time Student Unit) $17 916 $18 424 $18 914 $19 654 $19 911

NATIONAL AVERAGES

Graduate Satisfaction (% satisfied) 89% 90% 89% 89% 89%

Graduate Destination (% employed) N/A 81% 82% 84% 84%

AUDITOR GENERAL FOR WESTERN AUSTRALIA

8

OVERVIEW OF THE TERTIARY SECTOR (continued)

Key Performance Indicators for Colleges

Selected key performance indicators for colleges are included in Table 5b. Graduate Satisfaction andGraduate Destination are measured as part of a national survey of all college students in the year afterthey complete their studies. Graduate Satisfaction measures the percentage of graduates that hadachieved their main reason for undertaking the course. Graduate Destination represents the percentageof students who were employed at the time of the surveys.

Cost per SCH (Student Curriculum Hour) is calculated by dividing the total SCH of training provided,by related college expenditure. In addition, to maintain comparability, the six month effect of the capitaluser charge, introduced on July 1, 2001, has been excluded.

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

9

TAFE COLLEGE 1997 1998 1999 2000 2001

Central

Graduate Satisfaction (% satisfied) 78% 81% 78% 76% 73%

Graduate Destination (% employed) 71% 70% 70% 71% 65%

Cost per SCH $8.70 $10.47 $10.39 $9.96 $10.77

Central West

Graduate Satisfaction (% satisfied) 78% 81% 80% 77% 75%

Graduate Destination (% employed) 63% 70% 68% 68% 69%

Cost per SCH $13.64 $15.48 $15.34 $15.47 $17.21

Challenger

Graduate Satisfaction (% satisfied) 80% 80% 80% 80% 78%

Graduate Destination (% employed) 65% 70% 70% 69% 64%

Cost per SCH $11.79 $13.17 $12.85 $12.56 $11.50

C Y O’Connor

Graduate Satisfaction (% satisfied) N/A N/A N/A N/A 78%

Graduate Destination (% employed) N/A N/A N/A N/A 76%

Cost per SCH N/A N/A N/A N/A $15.25

Eastern Pilbara

Graduate Satisfaction (% satisfied) N/A 90% 89% 88% 88%

Graduate Destination (% employed) N/A 78% 89% 82% 84%

Cost per SCH $36.08 $29.23 $31.43 $34.92 $32.66

Great Southern

Graduate Satisfaction (% satisfied) 78% 76% 82% 79% 75%

Graduate Destination (% employed) 57% 63% 62% 76% 68%

Cost per SCH $11.56 $12.70 $11.45 $12.48 $12.12

Kimberley

Graduate Satisfaction (% satisfied) N/A N/A N/A 78% 85%

Graduate Destination (% employed) N/A N/A N/A 86% 86%

Cost per SCH N/A N/A N/A $25.45 $27.78

Table 5b: Selected Audited Key Performance Indicators for Colleges – 1997 to 2001.(1) 1997 figures for Central TAFE do not include the Advanced Manufacturing Technology Centre and 1997

figures for Eastern Pilbara College do not include Pundulmurra College which were separate reportingentities in 1997.

(2) Figures for C Y O’Connor and Kimberley Colleges are only listed for periods after they became statutoryauthorities.

TAFE COLLEGE 1997 1998 1999 2000 2001

Midland

Graduate Satisfaction (% satisfied) 81% 84% 82% 81% 78%

Graduate Destination (% employed) 67% 72% 66% 70% 66%

Cost per SCH $10.94 $11.85 $11.12 $11.34 $10.80

South East Metropolitan

Graduate Satisfaction (% satisfied) 84% 86% 86% 82% 79%

Graduate Destination (% employed) 76% 85% 82% 76% 71%

Cost per SCH $10.30 $11.70 $11.50 $11.82 $11.94

South West Regional

Graduate Satisfaction (% satisfied) 79% 78% 81% 79% 78%

Graduate Destination (% employed) 69% 72% 75% 80% 72%

Cost per SCH $10.72 $11.79 $11.22 $11.60 $11.65

West Coast

Graduate Satisfaction (% satisfied) 83% 81% 84% 77% 76%

Graduate Destination (% employed) 67% 72% 68% 74% 67%

Cost per SCH $10.12 $10.53 $11.47 $11.09 $10.55

West Pilbara

Graduate Satisfaction (% satisfied) 82% 84% 88% 83% 84%

Graduate Destination (% employed) 74% 68% 81% 92% 90%

Cost per SCH $31.63 $31.75 $30.79 $34.93 $30.44

WESTERN AUSTRALIAN AVERAGES

Graduate Satisfaction (% satisfied) 81% 81% 82% 79% 76%

Graduate Destination (% employed) 69% 72% 71% 73% 68%

NATIONAL AVERAGES

Graduate Satisfaction (% satisfied) 79% 80% 80% 80% 79% Graduate Destination (% employed) 71% 73% 73% 76% 73%

AUDITOR GENERAL FOR WESTERN AUSTRALIA

10

Continued from page 9

OVERVIEW OF THE TERTIARY SECTOR (continued)

This section summaries the results of the financial statement and performance indicator audits for theuniversities (including their subsidiaries) and colleges in the tertiary sector, for the 2001 annualreporting cycle.

Audit OpinionsThe audit opinions for financial statements, controls and performance indicators of universities, collegesand their subsidiaries for the year ended December 31, 2001 are summarised in Table 6.

Table 6: Dates and types of opinions.Denotes an unqualified opinion.

(1) The opinions of subsidiaries are given pursuant to the Corporations Act and relate to financial statements only.

* Advanced Powder Technology has a reporting date of June 30, and this opinion related to the year ending June 30, 2001.

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

11

Summary of Audit Results

Financial Statements Performance(1) Date Opinionand Controls Indicators Issued

UNIVERSITIES AND SUBSIDIARIES

Curtin University of Technology Qualification July 4, 2002Curtin Consultancy Services Ltd N/A May 30, 2002Uniservices Kalgoorlie Pty Ltd N/A May 30, 2002

Edith Cowan University May 02, 2002ECU Resources for Learning Ltd N/A May 23, 2002

Murdoch University Qualification May 02, 2002The University Company Pty Ltd N/A March 25, 2002Murdoch Retirement Services Ltd N/A March 27, 2002

The University of Western Australia May 02, 2002Advanced Powder Technology Pty Ltd * N/A October 17, 2001

TAFE COLLEGES

Central May 28, 2002

Central West April 22, 2002

Challenger April 29, 2002

C Y O’Connor May 06, 2002

Eastern Pilbara May 29, 2002

Great Southern April 23, 2002

Kimberley April 23, 2002

Midland May 08, 2002

South East Metropolitan May 14, 2002

South West Regional May 02, 2002

West Coast April 23, 2002

West Pilbara April 30, 2002

AUDITOR GENERAL FOR WESTERN AUSTRALIA

12

The following audits of university subsidiaries for periods ending December 31, 2000 were completedafter the report on Western Australian Public Universities and TAFE Colleges for the 2000 reportingcycle was tabled in Parliament. These opinions were unqualified.

Table 7: Dates of opinions for 2000 reporting cycle.

Reasons for Audit Qualifications

Curtin University of Technology

Unfunded Superannuation

After the University’s financial statements were submitted to the Minister and to Audit, managementmade several major changes to the statements during the audit process. Some of these changes related toproposals by management to retrospectively amend accounting policies. In late May 2002, theUniversity decided to discontinue the recognition of its unfunded superannuation liability of $76.7million in the Statement of Financial Position and instead report this amount as a contingent liability inthe notes to the financial statements. This late amendment occurred close to the May 31 deadline for theAuditor General to issue the opinions. As there was insufficient time to properly consider this latechange, an interim audit report was issued on May 31, 2002 under the provisions of Section 94 of theFAAA.

The University subsequently reconsidered its position and resolved to reinstate this liability, and insteadrecognise expected future Commonwealth Government funding associated with the liability, as part ofReceivables in the Statement of Financial Position. Audit considers that the University does not exercisecontrol over future Commonwealth Government funding, and that these funds should not have beenrecognised as an asset. Consequently, the audit opinion on the financial statements was qualified.

The effect on the financial statements was that Net Assets and Revenue were overstated by $76.7 million.If revenue had been correctly reported, the University would have reported a net loss of $8 millioninstead of the $68.7 net profit that has been reported.

It is recommended that, in future, accounting policies be determined at the beginning of the reportingperiod to which they are to apply and that significant accounting issues be resolved prior to year end.

Subsidiary Date Unqualified Opinion Issued

MS Biotechnology Pty Ltd October 26, 2001

The University Company Pty Ltd October 23, 2001

WANMTC Pty Ltd November 29, 2001

SUMMARY OF AUDIT RESULTS (continued)

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

13

Murdoch University

Student Debtors

The opinion for Murdoch University was qualified due to inadequacies in manual and computerisedcontrols associated with a new student management system, implemented in January 2001. Inconsequence, it was not possible to provide reasonable assurance that student debtor transactions werecompletely and accurately processed. This, together with the lack of adequate reconciliations betweenthe student management system and the general ledger, resulted in a large number of errors in theaccounting records, and difficulties in determining outstanding student debtors in a timely manner.Subsequent to year end, a reconciliation was completed and the errors corrected, so that the financialstatements are considered to fairly represent the University’s financial position as at December 31, 2001.However, due to the control inadequacies during 2001, the audit opinion on the University’s controls wasqualified.

Quality of Financial Statements and PerformanceIndicators

As reported in the 2000 report on Western Australian Public Universities and TAFE Colleges, thefinancial statements for that annual reporting cycle required several amendments during the auditprocess. For 2001, audit staff provided advice, in advance of the year end, to universities and collegesregarding a variety of reporting requirements of the Australian Accounting Standards and the Treasurer’sInstructions. This advice, together with enhanced quality assurance processes implemented bymanagement, resulted in a significant reduction in the number of errors detected during the auditprocess, at most universities and colleges.

The performance indicators submitted for audit were generally satisfactorily prepared and wereconsidered relevant, appropriate and fairly represented performance. Audit is however consulting withuniversities regarding opportunities to further enhance the content of their performance indicators forfuture reporting periods.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

14

The following were the more significant control related matters identified in the course of the audits.These, together with other issues have been referred for particular management attention:

Offshore Projects of Universities

All universities are, to a varying extent, providing teaching services overseas. These services aredelivered primarily in the Asian region and, in most cases, universities contract partners to provideadministrative management services in the offshore country. These operations carry additional risks tothose of established onshore operations, including less developed administrative arrangements due to therelative “newness” of the ventures, the challenge of maintaining successful relationships with offshorepartners, and differing local law and customs.

At two universities, the agreements between the universities and offshore partners were considered byAudit to be inadequate and at another, a contract with a partner was only finalised after programscommenced. In addition, the following specific issues and control shortcomings were noted:

Contracts between Curtin University and offshore partners provide, in some cases, for revenue onoffshore projects to be a percentage of the partner’s profits, whereas on other contracts the Universityreceives a fee per student. However, contracts do not provide for independent verification of studentnumbers and related revenue due from partners. Consequently, the University is unable, for someprograms, to reliably determine the amount of offshore revenue to which it is entitled.

When one of Murdoch University’s offshore partners ceased remitting revenue to the University, itbecame apparent that the provisions in the contract were inadequate to ensure recovery of moneysthat were due to the University. As a consequence the University has provided for a doubtful debt of$2.2 million in its 2001 financial statements due to fee revenue that is expected to be uncollectible.A significant portion of this amount was in respect of students who have completed individualmodules but discontinued their studies. In these cases, agreements provided for the offshore partnerto only remit revenue upon completion of a whole course.

Except at UWA, management and monitoring of aspects of offshore programs is decentralised.Although this approach is not in itself an issue of concern, Audit found that systems and proceduresoperating were not adequate for management to monitor overall debt levels and to ensure appropriateand timely responses to adverse trends for this class of debtors.

In response, senior management of the universities have initiated significant action to improve controlsover offshore operations. It is recommended that management continue to enhance controls over theseoffshore operations, to ensure that:

All programs are comprehensively assessed for risk, approved in advance and comprehensiveenforceable contracts are in place prior to commencement of operations;

Management Control Issues

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

15

Management be provided with regular financial reports for offshore programs and closely monitorthe academic and financial performance of these operations;

All revenue is recognised and reliably measured in a timely manner when due; and

Debtors are monitored, regularly reported to management and followed up in a timely manner.

Calling of Quotations for Purchases

Purchasing policies should be designed to obtain value for money while ensuring equal opportunities forpotential suppliers. The key principle is to seek competitive quotations or tenders unless there arepredefined situations where this is not practicable, for example where:

there is a sole source of supply;

an emergency situation exists;

a pre-qualification process has occurred;

a similar requirement has been recently sourced, and it is reasonably expected that the market hasnot changed.

Colleges are required to comply with State Supply Commission purchasing requirements and, althoughthe universities are exempt from these requirements, it is generally accepted that equivalent competitiveprinciples are applicable to these publicly funded institutions.

The policies of universities and colleges generally require that written quotes (preferably three) berequested from potential suppliers, but that for smaller readily available items, verbal quotations mayinstead be requested. In the course of auditing university and college expenditure, audit samples wereused to test compliance with these requirements. The audit covered renewal of existing service contractsas well as procurement of new goods and services.

At several of the larger institutions where purchasing is devolved, Audit noted that record managementpractices were inadequate. As a result, it took management up to six weeks to determine whether recordsexisted to demonstrate that appropriate purchasing procedures had been followed. Due at least toinadequate documentation if not procedures, management at eight of the 12 universities and collegeswhere specific audit tests were performed, were unable to demonstrate that fair competition or value formoney were achieved for purchases. Non-compliance ranged from one out of a sample of 15 to 18 outof a sample of 40.

It is recommended that universities and colleges adopt rigorous business-like purchasing procedures,to ensure equal opportunity for all suppliers so that achievement of value for money is demonstrable.Sufficient quotes should be obtained and adequate records maintained to demonstrate that the market hasbeen tested. When contracts are extended, appropriate tendering and quotation processes should befollowed.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

16

Asset Management

The annual attest audit of all agencies required under the FAAA is directed at forming an opinion oncontrols, financial statements and performance indicators, without necessarily testing every area in detailevery year. Audit tests are performed to the extent necessary under auditing standards to obtain sufficientappropriate evidence to support each opinion.

Recognising the higher probity and fiduciary obligations associated with utilisation of public resources,further complementary reviews of the reliability of the operations of systems and procedures are fromtime to time undertaken over groups of selected agencies. This also provides added assurance that theindividual professional judgements and conclusions reached during the course of annual attest audits aresoundly based and consistent.

In the 2001 audit cycle, Asset Management was chosen for review across the Tertiary Sector. The reviewaddressed controls over assets other than land and buildings, including plant, equipment and computingassets. A standard audit test plan was performed at all universities and at all colleges except South WestRegional.

Issues Addressed by the Audit

At December 31, 2001 universities and colleges collectively reported plant, vehicles, furniture,computing equipment and assets, other than land and buildings, totalling $418 million with a depreciatedvalue of $219 million. Potential risks associated with these significant asset holdings, that wereaddressed by the review included:

purchased assets not being recognised and recorded in asset records, leading to subsequentinefficiencies in management of those assets and potentially avoidable write-offs;

disposal of assets without management approval, resulting in disposals below market value oravoidable costs in replacing assets;

inappropriate use of or loss of assets, leading to avoidable replacement costs;

incorrect accounting treatment of assets, resulting in errors in management reports and externalreporting.

MANAGEMENT CONTROL ISSUES (continued)

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

17

What We Found

Control shortcomings were noted at all 15 institutions, including significant issues at 12 institutions. Thefollowing were the more significant matters identified:

Asset Records

Maintaining complete and accurate records of assets assists in ensuring that all assets can beaccounted for. These records are usually maintained in an asset register, and should include sufficientdetails to enable periodic identification to minimise theft and enable appropriate accountingtreatment.

At eight institutions, the audit found that asset registers were not being updated when assets werepurchased, moved or disposed of and that asset registers were not being regularly reconciled togeneral ledger accounts. This renders stocktake procedures less effective and can result in inaccurateand incomplete accounting records resulting in unreliable financial and management information.

In addition, the review highlighted that items of value below the asset capitalization threshold, werenot always being recorded in a separate property register to enable management to properly managethe custody of assets. Some of these assets, such as video and digital cameras, sound and televisionequipment, and other specialized training equipment, are either infrequently used or are shared bydifferent departments, increasing the risk of them being misappropriated without detection.

Maintaining Control over Assets

Periodically, organisations should perform a stocktake of all assets. Benefits include theidentification of errors in asset records, any unrecorded losses, destruction or misappropriation andinstances where assets could be better used elsewhere in the organisation.

The review highlighted that several universities and colleges placed a low priority on the stocktakeprocess. A common issue was that branches and faculties did not respond to the instructions/requestsof asset management staff and many outstanding stocktake listings and untraced assets were onlyfollowed up when Audit inquired as to the status. At three institutions, assets of significant numberand value were only located or identified for write-off in March and April 2002, more than sixmonths after the stocktake process commenced. This caused lengthy delays in confirming theexistence of assets reported in the annual financial statements.

Accounting for Assets

At several colleges, instances were identified where assets were incorrectly treated as an expenseinstead of being capitalised in accordance with accounting policies and standards. This results inunderstatement of asset balances, which may result in the colleges’ capital user charge beingunderstated, as well as errors in financial reports.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

18

What Should be Done

It is recommended that colleges and universities:

review procedures for the timely update of asset registers and property registers for acquisitions,movements and disposals;

perform thorough periodic stocktakes of assets on the asset register and the property register andfollow up all discrepancies immediately;

regularly reconcile asset registers to general ledger accounts; and

review expenditures to ensure all asset acquisitions have been identified and capitalised inaccordance with their accounting policies.

Corporate Governance - College Governing Councils

Statutory authorities are usually governed by a board that oversees management and is the accountableauthority of the organisation. The main reasons for having boards are:

to provide a governing body with operational independence from government to achieve definedoutcomes;

to provide an additional pool of expertise, often from members with distinguished and extensiveexperience in related industries, and/or;

to provide a channel for the views of interest groups to be voiced.

Colleges are statutory authorities that have Governing Councils as their accountable authorities. Section39 of the Vocational Education and Training Act 1996 (VET Act), requires each college to have aGoverning Council of not less than nine members, including the managing director. Ten of the 12colleges did not have a fully constituted Council from January 1, 2002 to March 2002 as, due toresignations and the expiry of some members’ terms of appointment, the number of members droppedbelow the minimum requirements of the VET Act. At two colleges, the number of members was reducedas low as four. As the remaining appointed members did not represent a fully constituted Council, theyeither did not hold Council meetings or, continued to serve their college in an unofficial capacity.

Although the period during which this constitutional issue existed, coincided with a period of relativelylow activity for most Governing Councils, some significant resolutions were delayed. One commonconsequence was that some colleges were not able to comply with the requirements of the FinancialAdministration and Audit Act to submit their annual estimates for 2002 to the Minister by January 31,2002 and to submit their annual financial statements and performance indicators for 2001 to the Ministerand the Auditor General by February 28, 2002. Although colleges prepared and certified financial

MANAGEMENT CONTROL ISSUES (continued)

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

19

statements and performance indicators to enable the annual audit process to proceed, in some instancesthe issuing of audit opinions needed to be delayed because Governing Council approvals of thestatements and indicators were outstanding.

It was also noted that C Y O’Connor and Kimberley Colleges, which were established on January 1,2001 and July 1, 1999 respectively, were still operating under Interim Governing Councils, comprisingseven members as at December 31, 2001. The VET Act provides for an Interim Governing Council tobe appointed for the period from when a college is established until a Governing Council is constituted.Advice from the Crown Solicitor’s Office indicates that it is not the intent of the VET Act that a collegeshould operate under an Interim Governing Council for such lengthy periods.

It is recommended that steps be taken to:

ensure that in future, appointments are made in a timely manner so that properly constituted CollegeGoverning Councils exist and provide effective management expertise at all times; and

replace the Interim Governing Councils at C Y O’Connor and Kimberley Colleges with fullyconstituted Councils that comply with the VET Act.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

20

Progress by colleges and other agencies in addressing issues raised in previous Reports to Parliament isas follows:

Resource Fees Charged by Colleges

In addition to a standard tuition fee that is charged for each course/module, colleges set resource fees tobe paid by students which support the college in meeting a range of costs associated with trainingdelivery. It is important that these fees are soundly based, to ensure that colleges recover related costsand that students receive fair value for their fees. The 1999 report on Western Australian PublicUniversities and TAFE Colleges reported that:

there was not a clear and consistent understanding between colleges regarding which costs should becovered by resource fees;

most colleges were not in a position to demonstrate that students were charged an appropriateresource fee; and

resource fees were in most cases not formally assessed by senior management or approved by theGoverning Council on an annual basis.

A working party including representatives of the Department of Training and college managers has sincereviewed resource fee policy and revised guidelines were introduced for 2001. During the current auditcycle, the implementation of these new guidelines was reviewed and it was noted that significantprogress had been made by most colleges. However, audit sampling identified instances whereindividual training areas had not provided estimates of their resource costs as input to the resource feesetting process. Reliable estimates of the cost of providing resources to students are an essential inputfor determining appropriate resource fees to be charged to students.

It is recommended that management implement monitoring processes to assure compliance with theenhanced procedures they have implemented.

Business Continuity - Disaster Recovery Testing of Computer Systems

The 1999 report on Western Australian Public Universities and TAFE Colleges reported that mostcolleges had not tested recovery of their key systems at an alternate site to ensure continuity ofoperations in the event that a college’s computing facilities were damaged by fire, storms, flooding orother disasters. The Department of Training, in conjunction with the colleges, subsequently establisheda testing schedule, which was ready for implementation in January 2001.

Progress on Issues Previously Reported

It is of concern that disaster recovery has still not been satisfactorily addressed by testing the recoveryof key systems. At February 2002, of 48 key college databases and their related systems, only 15 hadbeen tested for recoverability at the recovery site. The 15 databases tested were the centralised payrollfor all 12 colleges and one other system at three colleges. Uncertainty therefore remains regarding theability to restore normal business operations in a timely manner in the event of regular computingfacilities being unavailable.

In addition to the exposure at colleges, universities are also at risk of business interruption, as it has nowbeen several years since universities last tested the disaster recovery of several key systems.

It is recommended that universities and colleges test, as a matter of priority, the recoverability of keysystems at an appropriate alternate location.

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

21

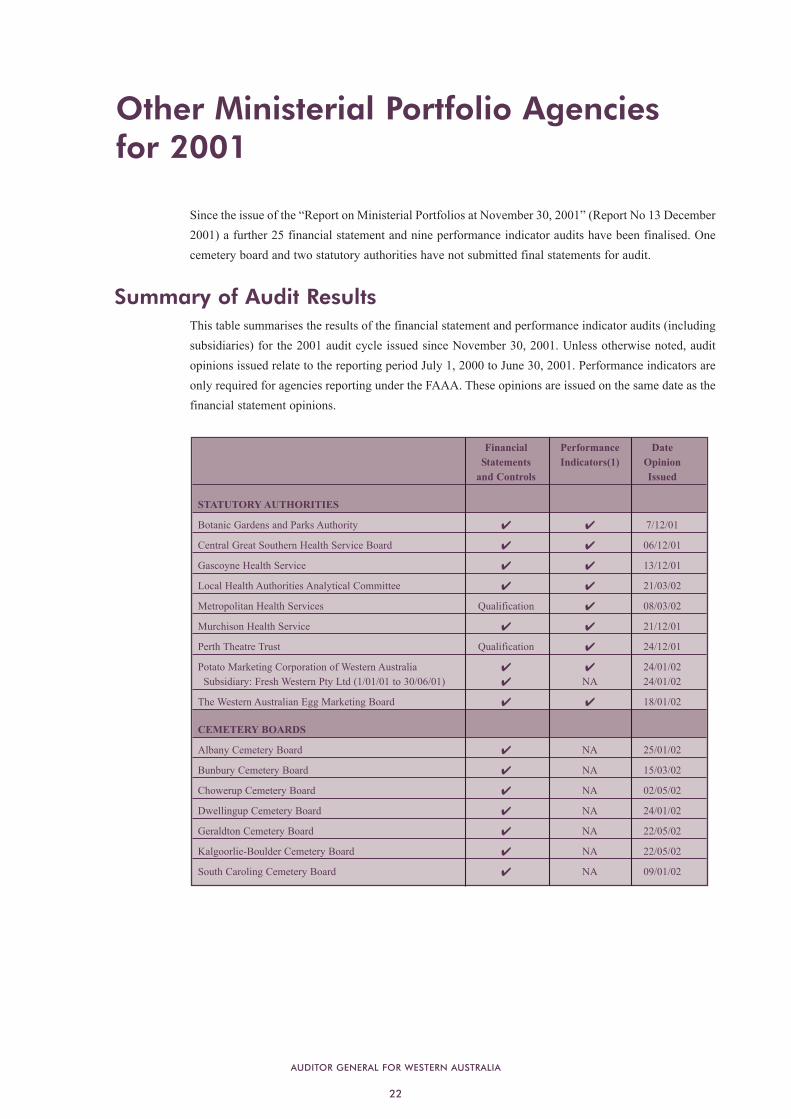

Since the issue of the “Report on Ministerial Portfolios at November 30, 2001” (Report No 13 December2001) a further 25 financial statement and nine performance indicator audits have been finalised. Onecemetery board and two statutory authorities have not submitted final statements for audit.

Summary of Audit ResultsThis table summarises the results of the financial statement and performance indicator audits (includingsubsidiaries) for the 2001 audit cycle issued since November 30, 2001. Unless otherwise noted, auditopinions issued relate to the reporting period July 1, 2000 to June 30, 2001. Performance indicators areonly required for agencies reporting under the FAAA. These opinions are issued on the same date as thefinancial statement opinions.

AUDITOR GENERAL FOR WESTERN AUSTRALIA

22

Financial Performance Date Statements Indicators(1) Opinion

and Controls Issued

STATUTORY AUTHORITIES

Botanic Gardens and Parks Authority 7/12/01

Central Great Southern Health Service Board 06/12/01

Gascoyne Health Service 13/12/01

Local Health Authorities Analytical Committee 21/03/02

Metropolitan Health Services Qualification 08/03/02

Murchison Health Service 21/12/01

Perth Theatre Trust Qualification 24/12/01

Potato Marketing Corporation of Western Australia 24/01/02Subsidiary: Fresh Western Pty Ltd (1/01/01 to 30/06/01) NA 24/01/02

The Western Australian Egg Marketing Board 18/01/02

CEMETERY BOARDS

Albany Cemetery Board NA 25/01/02

Bunbury Cemetery Board NA 15/03/02

Chowerup Cemetery Board NA 02/05/02

Dwellingup Cemetery Board NA 24/01/02

Geraldton Cemetery Board NA 22/05/02

Kalgoorlie-Boulder Cemetery Board NA 22/05/02

South Caroling Cemetery Board NA 09/01/02

Other Ministerial Portfolio Agenciesfor 2001

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

23

Table 8: Dates and types of opinions.Denotes an unqualified opinion.

(1) The opinions of subsidiaries are given pursuant to the Corporations Act and relate to financial statements only.

NA means that an opinion is not applicable, as performance indicators are not required to be submitted.

Reasons for Audit Qualifications

Metropolitan Health Services

Postal Remittances - Special Purpose Accounts

Controls over the opening of postal remittances relating to Special Purpose Accounts were not adequateas the remittances were not opened and recorded by the central mailroom prior to being forwarded topersons responsible for these accounts. As a consequence, all postal remittances may not have beenreceipted and properly brought to account.

Financial Performance Date Statements Indicators(1) Opinion

and Controls Issued

REQUEST AUDITS

Consolidated Financial Statements for the State of Western Australia NA 28/03/02

Friends of the KEMH Inc NA 22/03/02

Foundation for Advanced Medical Research Inc NA 19/02/02

Curtin University Superannuation Scheme 1968-1993- July 1, 1998 to June 30, 1999 NA 17/07/02- January 1, 1999 to December 31, 1999 NA 17/07/02- July 1, 1999 to June 30, 2000 NA 17/07/02- January 1, 2001 to December 31, 2000 NA 17/07/02- July 1, 2000 to June 30, 2001 NA 17/07/02

IN PROGRESS

The Aberdeen Unit Trust

Tarolinta Pty Ltd

NOT SUBMITTED

Beverley Frail Aged Lodge (Inc) (Final Audit)

Parliamentary Superannuation Board (Final Audit)

Rottnest Island Railway Trust

Upper Preston -Lowden Cemetery Board

Numbers Investments Pty Ltd

AUDITOR GENERAL FOR WESTERN AUSTRALIA

24

Bank Account

As noted in my December 19, 2001 Report to Parliament (No. 13 of 2001), duringthe year management became aware of an unauthorised bank account that hadbeen opened without their knowledge and without the prior authorisation of theTreasurer as required by section 21 of the Financial Administration and Audit Act1985. The bank account has now been closed.

Perth Theatre Trust

Plant and Equipment

The Trust had not reconciled the asset register to the general ledger and had notundertaken regular stocktakes. As a consequence the controls exercised by theTrust over computer equipment, furniture, fittings and equipment were notadequate to ensure compliance with legislative provisions.

Management Control Issues

Metropolitan Health Services

In addition to the qualification matters, a number of issues have been raised byinternal audit and other reviews over the past two years in relation to the operationof Special Purpose Accounts commonly referred to as "Trust Accounts". Asummary of these issues was also raised in the Office of the Auditor General(OAG) management letter to Metropolitan Health Services. As a result acomprehensive review into the administration of these accounts is beingconducted by the OAG, which will be subject to a separate report to Parliament.

Central Great Southern Health Service

The financial statements originally submitted for audit contained numerouserrors, which required considerable audit effort being expended to ensure the finalfinancial statements were complete and accurate. Significant changes were madeto most of the line items in the financial statements as a result of weaknesses inthe Health Service's reporting processes and shortcomings with the level offinancial expertise at the agency.

It was recommended that in future, a structured monthly and annual reportingprocess be developed and implemented to overcome the problems experienced aspart of this reporting cycle. In addition, the financial statements to be subject torigorous quality review prior to being submitted to the Minister and Audit.

OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001 (continued)

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

25

1996

Improving Road Safety – Speed and Red Light Cameras – The Road Trauma Trust Fund May 1, 1996

First General Report – On Departments, Statutory Authorities, (including Hospitals),Subsidiaries and Request Audits May 8, 1996

The Internet and Public Sector Agencies June 19, 1996

Under Wraps! – Performance Indicators of Western Australian Hospitals August 28, 1996

Guarding the Gate – Physical Access Security Management within the Western Australian Public Sector September 24, 1996

For the Public Record – Managing the Public Sector’s Records October 16, 1996

Learning the Lessons – Financial Management in Government Schools October 30, 1996

Order in the Court – Management of the Magistrates’ Court November 12, 1996

Second General Report for 1996 – On Departments, Statutory Authorities, Subsidiaries and Request Audits November 20, 1996

1997

On Display – Public Exhibitions at: The Perth Zoo, The WA Museum and the Art Gallery of WA April 9, 1997

The Western Australian Public Health Sector June 11, 1997

Bus Reform – Competition Reform of Transperth Bus Services June 25, 1997

First General Report 1997 – covers financial statements and performance indicators of departments, statutory authorities (excluding hospitals other than Wanneroo Hospital) and subsidiary bodies August 20, 1997

Get Better Soon – The Management of Sickness Absence in the WA Public Sector August 27, 1997

Waiting for Justice – Bail and Prisoners in Remand October 15, 1997

Report on Controls, Compliance and Accountability Audits – Public Property Management – Management of Information Technology Systems – Payroll and Personnel Management– Purchasing Goods and Services November 12, 1997

Public Sector Performance Report 1997 – Examining and Auditing Public Sector Performance – Follow-ups of Previous Performance Examinations – Sponsorship in the Public Sector November 13, 1997

Private Care for Public Patients – The Joondalup Health Campus November 25, 1997

Previous Reports of the AuditorGeneral

AUDITOR GENERAL FOR WESTERN AUSTRALIA

26

1998

Report on Ministerial Portfolios – Audit Results – Consolidated Financial Statements– Summary of the Results of Agency Audits April 8, 1998

Selecting the Right Gear – The Funding Facility for the Western Australian Government’s Light Vehicle Fleet May 20, 1998

Report on the Western Australian Public Health Sector May 20, 1998

Sale of the Dampier to Bunbury Natural Gas Pipeline (Special Report) May 20, 1998

Weighing up the Marketplace – The Ministry of Fair Trading June 17, 1998

Listen and Learn – Using customer surveys to report performance in the Western Australian public sector June 24, 1998

Report on the Western Australian Public Tertiary Education Sector August 12, 1998

Do Numbers Count? – Educational and Financial Impacts of School Enrolment August 19, 1998

Report on Controls, Compliance and Accountability Audits 1998 – Control of Agency Expenditure – Human Resource Management – Administration of Superannuation Systems October 14, 1998

Public Sector Boards – Boards governing statutory authorities in Western Australia November 18, 1998

Send Me No Paper! – Electronic Commerce – purchasing of goods and services by the Western Australian public sector November 18, 1998

Accommodation and Support Services for Young People Unable to Live at Home November 26, 1998

Public Sector Performance Report 1998 – Monitoring and Reporting the Environment– Recruitment Practices in the WA Public Sector – The Northern Demersal Scalefish Fishery December 9, 1998

Report on Audit Results 1997-98 – Financial Statements and Performance Indicators December 9, 1998

1999

Report on the Western Australian Public Health Sector – Matters of Significance– Summary of the Results of Agency Audits April 21, 1999

Proposed Sale of the Central Park Office Tower – by the Government Employees Superannuation Board April 21, 1999

Lease now – pay later? The Leasing of Office and Other Equipment June 30, 1999

Getting Better All The Time – Health sector performance indicators June 30, 1999

REPORT ON PUBLIC UNIVERSITIES AND TAFE COLLEGES AND OF OTHER MINISTERIAL PORTFOLIO AGENCIES FOR 2001

27

Report on the Western Australian Public Tertiary Education Sector – 1998 Annual Reporting Cycle June 30, 1999

Fish for the Future? Fisheries Management in Western Australia October 13, 1999

Public Sector Performance Report 1999 – Controls, Compliance and Accountability Audits – Follow-up Performance Examinations November 10, 1999

A Stitch in Time – Surgical Services in Western Australia November 24, 1999

Report on Ministerial Portfolios to November 5, 1999 – Issues Arising from Audits – General Control Issues - Summary of the Results of Agency Audits November 24, 1999

2000

Public Sector Performance Report 2000 – Emerging Issues – Management Control Issues April 5, 2000

Report on the Western Australian Public Health Sector and of Other Ministerial Portfolio Agencies for 1999 April 5, 2000

A Means to an End – Contracting Not-For-Profit Organisations for the Delivery of Community Services June 14, 2000

Private Care for Public Patients – A Follow-on Examination of the Joondalup Health Campus Contract June 21, 2000

Report on Western Australian Public Universities and TAFE Colleges– 1999 Annual Reporting Cycle June 21, 2000

Bus Reform: Further down the road – A follow-on examination into competition reform of Transperth bus services June 28, 2000

Surrender Arms? Firearm Management in Western Australia September 13, 2000

Second Public Sector Performance Report 2000 – Administration of Legislation – Financial and Management Control Issues October 11, 2000

A Tough Assignment – Teacher Placements in Government Schools October 18, 2000

Report on Ministerial Portfolio at December 1, 2000 – Summary of Audit Results– Accountability Issues (Corporate Governance, Accounting for GST Transitional Loan) December 20, 2000

AUDITOR GENERAL FOR WESTERN AUSTRALIA

28

2001

Sale of the Gas Corporation’s Businesses (Special Report) February 14, 2001

On-line and Length? Provision and use of learning technologies in Government schools May 23, 2001

Implementing and Managing Community Based Sentences May 30, 2001

Public Sector Performance Report, 2001 June 20, 2001

Report on Public Universities and TAFE Colleges - 2000 annual reporting cycle June 20, 2001

Lifting the Rating - Stroke Management in Western Australia August 22, 2001

Good Housekeeping: Facilities Management of Government Property and Buildings August 29, 2001

Second Public Sector Performance Report 2001 September 19, 2001

Righting the Wrongs: Complaints Management in the Western Australian Public Sector October 17, 2001

Third Public Sector Performance Report 2001 November 7, 2001

Life Matters: Management of Deliberate Self-Harm in Young People November 28, 2001

First Byte: Consortium IT Contracting in the Western Australian Public Sector December 5, 2001

Report on Ministerial Portfolios at November 30, 2001 December 19, 2001

2002

Level Pegging: Managing Mineral Titles in Western Australia June 19, 2002

The above reports can be accessed on the Office of the Auditor General’s Homepage on the Internet athttp://www.audit.wa.gov.au/

On request these reports may be made available in an alternative format for those with visual impairment.