Embed Size (px)

Citation preview

Internship Report on working of

Office of the ACCOUNTANT GENERAL N-WFP

PESHAWAR

Submitted byMeh

MBA (HRM)

INSTITUTE OF MANAGEMENT STUDIES UNIVERSITY OF PESHAWAR

RESEARCH & DEVELOPMENT DIVISIONINSTITUTE OF MANAGEMENT STUDIES

UNIVERSITY OF PESHAWAR

SIGNATURE : ____________________

NAME : MUHAMMAD AHMED KHAN

DESIGNATION : PROFESSOR

COORDINATOR RESEARCH & DEVELOPMENT DIVISION:

SIGNATURE : _____________________

NAME : PROF. ZIA UD DIN

DESIGNATION : PROFESSOR

An internship Report On Pre Audit AG Office Peshawar

ACKGROUND OF THE STUDY

The conditions of service of the Auditor-General have been prescribed by the

Pakistan, (Audit and Accounts) Order, 1952, hereinafter referred to as the” the

Audit and Accounts Order”

Article 123 & 197 of the 1956 & 1962 Constitution, preceded more or less on

the pattern of the 1953 Act, for keeping the accounts of the Federation and of

the provinces and the form to be prescribed by the Comptroller and the

Auditor General with the approval of President.

Articles 168 & 171 of the 1973 Constitution determine the entity, it’s factions,

powers and reports of the Auditor General. Existing constitutional Provisions

as shown at Annexure-1 in Section 3.

As per Ordinance 2001, Controller General of Accounts has transferred the

Accounting Functions of the Auditor-General to the Controller General of

Accounts Since July 2001.

Thus the objectives of A.G (N.W.F.P) Peshawar are as follows:

To prepare and maintain the accounts of the federation and the Provinces. To authorize payments and withdrawals from the Consolidated Fund and

Public Accounts of the Federal and Provincial Governments. Provide

information as such Governments may from time to time require, render

advice on accounting procedure for new scheme Programmes of activities,

Develop and maintain efficient system of pension, provident funds and

other retirement’s benefits in consultation with the concerned government.

1.2 PURPOSE OF THE STUDY

The report is presented for the fulfillment of the degree requirement of Master

in Business Administration at the Institute of Management of Studies,

Peshawar. The purpose of the study was also to analyze the organization, its

day-to-day operations.

Page No. 1

An internship Report On Pre Audit AG Office Peshawar

SECTION-2

ORGANIZATIONAL REVIEW

2.1 ORGANIZATION

Organization is defined as “group of people working together in some

concerted or coordinated effort to attain objectives”1.

2.2 MANAGEMENT

It is defined as “the process of designing and maintaining an environment in

which individuals work together in groups to accomplish efficiently selected

aims”2

The Accountant General is a competent, well-qualified senior executive and

has a vast experience.

The accountant General has a team of well qualified senior executives of the

Accounts Group like Add. A.G, D.A .G (SR) & A.A.G. These executives have

been selected by F.P.S.C by conducting C.S.S Exam.

2.3 OFFICE NETWORK

The Accountant General of Pakistan Revenues has a network of four main

offices in each provincial capital including Karachi, Lahore, Peshawar , Quetta

and a sub- office at Gilgat and Head office at Islamabad.

The accountant General office (N.W.F.P) Peshawar has a network of different

D.A.O in different Distric i.e (Kohat, Charsadda , Nowshera , Dir, Abbotabad ,

Bannu , Kohat )

2.4 ORGANIZATIONAL STRUCTURE

It is defined as “A framework that defines the boundaries of the formal

organization and within which the organization operates” 3rd .

Page No. 2

An internship Report On Pre Audit AG Office Peshawar

Its objectives, size and nature of its operations determine the organizational

structure of an entity. A clear-cut division of work at appropriate levels in the

hierarchy is created to avoid duplication and overlapping

2.5 DEPARTMENTALIZATION

Departmentalization is ‘grouping the jobs into related work units”4

2.5.2 Gazetted Audit Department

The GAD is responsible for pre-audit of claims of the gazetted government

servants, maintenance of their service record, fixation of their pay, per-audit of

T.A. Bills, re-imbursement of Medical Charges, preparation of Broadsheets

etc.

2.5.2 Treasury Audit Department

The TAD is responsible of pre-audit of claims of the non-gazetted government

servants, maintenance of their service record, fixation of their pay, pre-audit of

T.A. Bills etc.

Re-imbursement of Medical charge, preparation of Broadsheets etc. All the

contingency bills of department are pre-audit as per rules and regulations.

2.5.3 Central Fund

This department is responsible for the preparation and maintenance of G.P.

Fund A/cs of the Federal & Provincial employees. It calculates interest on

annual basis.

It arranges the final payment of GP Fund to the employee on his retirement. It

also makes disbursement of advances from GP Fund A/c on different grounds

to employees if opted during their service but prior to retirement.

2.5.4 Court Cases Cell /Legal cell

This department is responsible for preparing the legal replies on behalf of the

A/G/A.G.P.R and presenting them in Supreme Court, High Courts, F.S.T etc.

if initiated by any aggrieved employee or any third party in relation to

governmental rules and procedures especially in service matters.

Page No. 3

An internship Report On Pre Audit AG Office Peshawar

2.55 Pension Department

It deals with preparation of pension cases of all the retiring Federal/Provincials

Government Employees.

It calculates their monthly pension admissible and net payable in lump sum on

their retirement. It prepares the pension payment books for the retired

employees and makes enhancement if there is any change from Government.

2.5.6 Computer Department

Computers have become an important element of the modern office system.

This department of the office is responsible for the computerization of payroll

of all the federal & provincial employees being paid by A.G /A.G.P.R. It

makes deductions and payments if duly suggested by department and

approved by the A.G/A.G.P.R in the monthly payroll of the departments

concerned.

2.5.7 Personnel and Establishment Department

This department is responsible for the administration and service matters of all

the employees of the office.

It deals with all issues related to its employees like Recruitment, pay ,

promotions, penalty, training, leave etc. It maintains and controls the office

work & makes sure that the office achieves its goals.

2.5.8 Foreign Aid

This section is engaged in accounting of all foreign receipts in the form of

loans of grants and of all payments on account of principal and interest there

on. It is engaged in accounting of re-lending loans to financial/ non-financial

institutions And autonomous bodies and then recoveries of principal and

interest. Amounts receivable from provinces on account of US AID in local

currency loans. It also deals in adjustment of foreign aid directly disbursed to

foreign funded/aided projects, reconciliation of receipts and payments with

Economic Affairs Divisions.

Page No. 4

An internship Report On Pre Audit AG Office Peshawar

2.5.9 Book and Compilation

This section is responsible for booking head wise receipts and head wise

payment of F.T.O A/c, Income Tax, Sales Tax and coding and classifying

them. Making payments form sub-offices and passing general entries and

transfer entries and preparing monthly account. It also maintains civil a/c,

combined civil a/c and adjusting the direct payment made by federal govt.

through ministries.

2.5.10 Accounts Department

This section is responsible for making releases from Development demand in

the form of authorities or bills. It reconciles the expenditures, passes transfer

entry due to wrong booking and difference in reconciliation.

2.5.11 Computer Account Department

It presents the accounts in published form of all the local A/c and F.T.O.A/c

i.e. all the receipts and payment of F.T.O which have been duly booked and

submitted by Book & Compilation section.

2.5.12 Report Appropriation

This department is responsible for preparing report showing the Appropriation

Account which contains a comparison of original budgetary provision, all

subsequent modifications by ways of cuts, withdrawals, surrenders, re-

appropriations etc. with actual expenditure incurred and indicating all excesses

and savings in respect of each object head under a Grant or Appropriation. The

excesses and savings are required to be explained by the executive before the

Public Accounts Committee.

Page No. 5

An internship Report On Pre Audit AG Office Peshawar

2.5.13 Budget Section

It issues F.A.Cs. for loans and advances to Govt. Servants and provides budget

to provincial Govt. by authority. Provides assistance to Finance Division for

the Appropriation of Annual Budget.

2.5.14 Cheque Section

It prepares the pre-audited cheques drawn on State Bank of Pakistan or

National Bank Of Pakistan for disbursement to govt. departments for their pre-

audited claims.

2.6 CONTINGENCY APPROACH TO ORGANIZATION STRUCTURE

It stated, “ The most appropriate structure depends on the technology used, the

rate of environmental change, and other dynamic forces”

2.7 ORGANIZATIONAL CHART

The Accountant General OF Pakistan revenues is centralized organization. In

a centralized organization little authority is given to the lower levels of

management. As against in decentralized organization structure is tall and the

top Management undertakes the major decisions. Tall structure is defined as

‘Organization with many levels and relatively small spans of Management’

(Annexure-A)

2.8.1 HUMAN RESORUCE PLOCES

2.8.1 SELECTION AND RECURITMENT

“Selection is the process of choosing from among candidates from within the

organization or from the outside, the most suitable person for current position

or for further positions”5

2.8.2 RECRUITMENT POLICY

Non-gazetted staff up to BPS 11 is recruited by the office itself following

departmental rules of business under instructions of Federal Government. The

office conducts exams for different announced and advertised posts and after

announcing the results the qualified candidates are called for the interviews. If

Page No. 6

An internship Report On Pre Audit AG Office Peshawar

they clear the inter view they can then be appointed in the required office i.e.

whether at Head Office or to any other office in provincial offices.

2.8.3 TRAINING

“A learning experience that seeks a relatively permanent change in an

individual that will improve his or her ability to perform on the job” 7

2.8.4 TRAINING PROGRAM

A separate wing called HRM wing has been established in the Department of

auditor General. Under this wing there are five training institutes working at

Islamabad, Karachi , Lahore, Peshawar and Quetta. These are called the Audit

& Accounts Training Institutes.(AATI)

2.8.5 PROBATIONER OFFICERS’ TRAINING

The Probationer Officers’ Training annually runs from July to March. The

programs meant for probationary officers who join the Accounts Group under

the national scheme of recruitment for superior services and aims at imparting

essential skill in the field of accounting, auditing and management to enable

the officers to function efficiently and effectively in various constituent units

of the Accounts Group.

2.8.6 TRAINING OF SAS

The main responsibilities of the AATI are to impart training to staff of the

department regarding accounting matters. For this purpose a comprehensive

training in the shape of SAS examination is provided.

2.8.7 SAS PART-1

During the 1st stage of the SAS examination 6 month training is provided to

staff of various field offices. The subjects taught at this level are during this

training the staff is treated to be on duty and they get salary but temporarily

they are posted to AATI for study. After completion of training an exam is

Page No. 7

An internship Report On Pre Audit AG Office Peshawar

taken by the department of the Auditor General of Pakistan in different centers

in Pakistan.

2.8.8 SAS PART-II

The individuals who qualify the SAS Part-I examination are again deputed for

SAS Part-II training at AATI, Lahore, Karachi, Quetta and Peshawar. At the

finalization of training of six months again the exam is taken by the

department of the Auditor General of Pakistan.

2.8.9 SAS REFRESHER COUSE

Two weeks refresher coursed for SAS Part-I and SAS Part-II will be

conducted for the trainees of previous years. The dates are announced later on,

in accordance with the schedule of their respective examinations.

2.8.10 PROMOTIONOF SUCCESSFUL CANDIDATES

The trainees who qualify the SAS Part-II examination are awarded with

promotion. The trainees are promoted from a non-gazetted post to gazetted

post of A.A.O.

2.8.11 FINANCE MANGER’S COURSE (FMC)

These courses are available to Middle Level Manger’s (BPS-17-18) of the

various constituent units of Accounts Group and other Government

Organizations. Fifteen to twenty officers are accommodated in each course.

The office of the Auditor-General makes nominations of officers of Inter-

Departmental Cadres of Accounts Group and those from Departmental cadres

are nominated by the respective Heads of Department.

2.8.12 PIPFA (AAT)/SAS TRAINIG

The following preparatory coursed have been planned for Foundation &

Intermediate Stages of AAT Examination. The course is designed to prepare

the participants of the course for foundation and intermediate stage of AAT

Examination. It will help the department of Auditor General to have a cadre of

B-16 officer continues to remain available.

Page No. 8

An internship Report On Pre Audit AG Office Peshawar

2.8.13 ON-JOB TRAINING

Normally, given by a senior employee or supervisor, the trainee is shown how

to perform the job and allowed to do it under the trainer’s supervisor. The

Institute provides them with on job training, as exposure to advance coursed

and seminars conducted by the Audit and Accounts Training Institute.

2.8.14 JOB ROTATION

Job rotation is defined as” the practice of periodically rotating job assignment”

it enables the employees to work on different positions and get an overall

picture of the Office operations.

2.8.15 OFF-THE JOB TRAINING

Off-the job training in the office includes refresher coursed and meetings

organized by the AATI. This mode of training is done to enable employees to

upgrade their knowledge to new developments in Accounting and also to

broaden their outlook and train them in new techniques.

2.8.17 PERSONNEL APPRAISAL AND MOTIVATIONAL METHODS

The management of the A.G.P.R evaluates and motivates their employees time

to time. The methods used are:

Performance Report

Inspection

Promotion to B-16 On Passing The SAS Exam

2.9 LEAVE POLICIES:

Granting leaves is one of the duties of the personnel department. Leaves are

categorized as follows:

Casual Leave

Recreational Leave

Earned Leave

Leave Without pay

Page No. 9

An internship Report On Pre Audit AG Office Peshawar

2.9.1 CASUAL LEAVE

Casual leaves are granted for unforeseen circumstances and cannot be

combined with any other kind of leave. Each employee is entitled to 20 casual

leave in a calendar year.

2.9.2 RECREATIONAL LEAVE

Such leaves are granted to all the employees once during a year for

recreational purpose. The leave is approved by the concerned authority for a

period of 15 days and counted as 10 days leave.

2.9.3 EARNED LEAVE

Such type of the leave is given only after one year of service. Earned leave of

48 days are permitted each year. These can be accumulated and availed at

once to get maximum benefit out of it.

2.9.4 LEAVES WITHOUT PAY

As the name suggest, leaves are granted without giving the pay subject othe4

approval of the concerned department. Such leaves are granted only after the

exhaustion of the earned leaves.

Page No. 10

An internship Report On Pre Audit AG Office Peshawar

REFERENCES

1. Rue, Leslie W. and Lloyd L. Byers, (1992).Management: Skills and

Applications, Boston, Richard D.Irwin, P.567

2. Ibid.p.364

3. DECenzo, David A. and Stephen P. Robbins, (1996). Human Resource

Management, USA John Wiley & Sons Inc.,p.382.

4. Rue, Leslie W. and Lloyd L. Byers, (1992) Management: Skills and

Applications, Boston, Richard D. Irwin, p.487.

5. DeCenzo,David A. and Stephen P. Robbins, (1996). Human Resource

Management, USA, John Wiley & sons Inc.,p.111.

6. AGPR, (2000). Service Rules, Islamabad

7. DeCenzo, David A. and Stephen P.Robbins, (1996). Human Resource

Management, USA, John Wiley & sons Inc.,p.182.

Page No. 11

An internship Report On Pre Audit AG Office Peshawar

SECTION-3

FUNCTIONAL ANALYSIS

3. AUDITOR GENERAL

“Means the Auditor-General of Pakistan appointed under Article 168 of the

Constitution of the Islamic Republic of Pakistan.” 1

3.1 AUDITOR GENERAL FUNCTIONS IN RELATION TO ACCOUNTS

The Auditor General has been made responsible for Audit and Accounts

maintenance for at both the Federal and Provincial Governments levels

under Article 168/169 of 1973 Constitution of Pakistan. The extract of

same is at Annexure-1

3.2 REPORTS PRESENTATION TO THE PRESIDENT

The Auditor General presents his reports on accounts to the President of

Pakistan or Governor of a Province, as the case my be, who causes the same to

be laid before the National Assembly or Provincial Assembly.

3.3 ORGANIZATION

The functions of payment, at both the Federal and Provincial Government’s

levels and their accounts keeping are performed by the Pakistan Audit

Department through a system of Accountant General and a mix of District

Accounts Offices and treasuries. Since February 1997, a separate office of

Controller General of Accounts was created under the Auditor General.

3.4 A.G.P.R/A.G

The AGPR / A.G has been performing the payments and accounts keeping

functions on behalf of the Auditor General Of Pakistan.

Page No. 12

An internship Report On Pre Audit AG Office Peshawar

3.5 ACCOUNTANT GENERAL

“Means the head of an office of Accounts subordinate to the comptroller and

Auditor General of Pakistan whether known as Accountant General,

Comptroller or by any other designation. Provincial Accountant General

means as Accountant General who keeps the accounts of a Province” 2

MAIN FUNCTIONS OF ACCOUNTANT GENERAL N.W.F.P, PESHAWAR

1. General supervision of various sections of main office at Peshawar,

Monitoring and coordination of 24-District and 7- Agency Accounts

Offices in NWFP

2. Finalization of Pension Cases

Issue of Pension payment orders (PPO’s to the Treasury office

Peshawar and various District/ Agency Accounts offices in NWFP as

well as other AG’s

Post audit of pension payments Provincial Government Servants.

3. Maintenance of G.P. Fund Accounts

Monthly posting, yearly closing.

Issue of balance sheets / annual Account statements.

Temporary/Non-refundable Advances and issue of cheques to State

Bank of Pakistan

Transfer of G.P. Fund Accounts on transfer of subscriber to other

DAO/AAO.

Final payment of G.P Fund on retirement, removal, dismissed or death

of subscribers

Receipt of Bills on account of G.P. Fund Final payment of

Government servants of Non-Devolved Departments and serving in

Peshawar District and issue of Cheques at State Bank of Pakistan

Peshawar.

4. Pre-Audit of personal claims of all gazetted/ Non Gazetted Govt: Servants

of Government servants of non-devolved departments and serving in

Peshawar District on account of pay and allowances and contingent

Page No. 13

An internship Report On Pre Audit AG Office Peshawar

charges and issue of cheques on this account at State Bank of Pakistan

Peshawar.

5. Maintenance of Deposit register, Personal Ledger Accounts and refund of

lapsed deposit of Non-Devolved Departments Peshawar District.

6. Payment of various loans and advances, Civil advances and permanent

advances of Non-Devolved Departments at Peshawar and issue of cheques

after processing claims on this account at State Bank of Pakistan at

Peshawar.

7. Compilation of monthly accounts of Provincial transactions of Peshawar

District from the list of payments for which cheques have been issue by

this office as well as from the cash Accounts/ list of payment made by the

Treasury Office(DAO) Peshawar.

8. Consolidation of account (Budget head wise) prepared by this office as at

S.No.7 and those submitted by the DAOs/AAOs Public Works Divisions

as well as Forest Department in NWFP.

9. Preparation of monthly Civil accounts after consolidation (S.No.8) and its

submission to Finance Department, Government of NWFP.

10. Preparation of Finance Accounts of Provincial Government of NWFP of

each financial year and their submission to finance Department as well as

Controller General of Accounts Islamabad

Preparation of Appropriation Accounts of Provincial Government of NWFP of

each financial year and their submission to Finance Department as well as

Controller General of Accounts Islamabad

11. Discussion of Finance Accounts and Appropriation Accounts in the

meeting of Public Accounts Committee Govt: of NWFP.

12. Earmarking o Funds, allocated by Finance Department for House Building

Advance, Motor Car Advance, Scooter Advance and Cycle Advance.

Processing of Claims of Govt: Servant serving at Peshawar District, and

issue of cheque at Sate Bank of Pakistan, Peshawar.

13. Issue of NOC and to authorize opening of Assignment Accounts at

National Bank of Pakistan and PLA’s at District/ Agency Accounts

Offices in NWFP.

14. Receipt of Bank Scrolls from State Bank of Pakistan and their

reconciliation with cheques issued by this office.

Page No. 14

An internship Report On Pre Audit AG Office Peshawar

15. Monitoring of District Government Accounts and Devolution Plan and

submission of various M.I.S reports to Controller General of Accounts and

Auditor –General of Pakistan.

Maintenance of Financial Rules and Regulations and their circulation

among District/ Agency accounts Offices in NWFP, and Various section

of Main Office at Peshawar.

16. Court Cases.

17. Maintenance of Computer cell at Peshawar as will as in some District/

Agency Accounts Offices established for Computerization of Pay Rolls,

G.P.Fund and Accounts.

18. Introduce of New Accounting Models (NAM) as well as computerization

under project for improvement of Financial Reporting and Auditing

(RIFRA)

3.6 FUNCTIONS OF AGPR AT A GLANCE

3.6.1 PRE-AUDIT

Claims on governments in the form of bills with all supporting documents to

the AG/DAOs for payment.

The pre-payment audit function helps the Accounts offices to independently

check the appropriations and classification required for proper and accurate

accounting and control on unauthorized/irregular disbursements.

3.6.2 Payment/ disbursement

In Ags Offices/DAOs the passed/ admitted bills are transferred to the cheque

section for writing the pre-audited cheques.

These cheques are collected by the Ministries/Departments for either

encashment or handling over to the concerned agencies in case of third party

cheques.

3.6.3 Accounting

In AG office every bill passed for payment is booked against a particular grant

under proper function-cum-object classification as given in the Chart of

Classification. These accounts are incorporated in the monthly civil accounts

prepared by the AG Offices.

Page No. 15

An internship Report On Pre Audit AG Office Peshawar

3.7 Auditor General’s Accounts Related Reports

The AGPR prepares the Monthly Accounts in the form of civil A/c of Federal

and Provincial Governments, compiles the departmentalized accounting

entries both at Federal and Provincial levels for merger in Monthly Civil A/c.

These monthly accounts provide basis for preparation of Annual Accounts.

Monthly Accounts

Annual Accounts

3.8 Monthly Accounts

Federal Government

Departmentalized Accounting Entities (Federal)

Provincial Government

Departmentalized Accounting Entities (Provincial)

3.8.1 Federal Government

The AGPR prepares Monthly Civil Accounts which contain an Account of all

the transaction of the Federal Govt: brought to Account by him and by other

Civil Accounts Officers, for submission to the Federal Government.

3.8.2 Departmentalized Accounting Entities (Federal)

“The Accounts relating to Defence, Railways and other Departmentalized

accounting entities are complied by the departmental accounting authorities

and submitted monthly to the AGPR for posting in the Monthly Civil Account

of the Federal Government.

3.8.3 Provincial Government

Each Provisional Accountant General, as soon as the accounts of a month are closed,

prepares monthly Civil Account, in the form prescribed in Accounts Code Volume-

IV, which contains an Account of all the transactions of the provincial government

brought to account by him and by other Civil Accounts Officer/Treasuries, for

submission to the provincial Government.

Page No. 16

An internship Report On Pre Audit AG Office Peshawar

3.8.4 Departmentalized Accounting Entities (Provincial)

Complied accounts of the provincial departmentalized accounting entities are

submitted by their departmental accounting authorities to the concerned

Provincial Accountants General and are merged in the Provincial Monthly

Civil Account.3

3.9 ANNUAL ACCOUNTS

Appropriation Accounts

Finance Accounts

3.9.1 Appropriation Accounts

“The Appropriation Account contains a comparison of original budgetary

provision, all subsequent modifications by way of cuts, withdrawals,

surrenders, re-appropriations etc. with actual expenditure incurred and

indicating all excesses and savings in respect of each object head under a

Grant or Appropriation. The excesses and savings are required to be explained

by the executive before the Public Accounts Committee.”4

3.9.1.1 Federal Government

The Appropriation Accounts of the Federal Civil Departments are prepared by

the A.G.P.R., and submitted by the Auditor General to the President in

pursuance of the provisions of paragraph 9(4) of the Pakistan Audit and

Accounts Order 1973.

3.9.12 Departmentalized Accounting Entities

“Appropriation Accounts are prepared by the Accounting Authorities of

Departmentalized Accounting Entities and are submitted to the President by

the Auditor – General Of Pakistan along with an Audit Certificate there

upon”5

3.9.1.3 Appropriation Accounts to the Provisional Governments

“The Appropriation Accounts of provincial governments are prepared by their

respective Account General and submitted by the Auditor –general of Pakistan

Page No. 17

An internship Report On Pre Audit AG Office Peshawar

to the Governors of the respective provinces in pursuance of the provisions of

paragrah3(4) of the Pakistan Audit and Accounts Order1973”6

3.9.2 Finance Accounts

“These accounts exhibit the annual receipts and disbursements as well as

balance of assets and liabilities of the Federal Government as on June 30, of

financial year. The Finance Accounts cover transactions of both the

Consolidated Fund and the public accounts. Finance Accounts are based on

actual chase transactions and do not include accrued receipts and liabilities.

These accounts are submitted by the Auditor General of Pakistan to the

Federal / Provincial Government” 7

These accounts with the Auditor General’s reports on them form a single

document.

3.9.2.1 Federal Government

“Finance Accounts of the federal government are prepared by the Accountant

General of Pakistan Revenues and comprise transactions of the federal

government, brought into account in the books of accountant General of

Pakistan and all Federal Government’s departmentalized accounting entities.

3.9.2.2 Provincial Governments

The finance Accounts are prepared by Provincial Accountant General, in the form

prescribed by the Auditor General with the approval of the President, and submitted

to the Auditor General for approval and transmission to the Governor of the Province

concerned. These accounts comprise transaction of the each provincial government,

brought into account in the books of respective Accountants General and all

provincial governments’ depar4tmentalezed accounting entities e.g. Forest

Department.” 8

4.1 TRANSFER OF ACCOUNTING FUNCTIONS

With the promulgation of C.G.A. Ordinance 2001 the accounting function of

the Auditor General has been transferred to C.G.A and the Auditors General

has been vested with the Auditing Function only`.

Page No. 18

An internship Report On Pre Audit AG Office Peshawar

4.2 CONTROLLER GENERAL OF ACCOUNTS

“There shall be a controller General of Accounts who shall be appointed by

the President from amongst the officers of the Accounts Group and Shall be

BPS-22 Officer.” 9

4.1.1 Administrative Head

“The Controller General has been the administrative head of all the offices

subordinate to him with full authority for transfer and posting within his

organization.

4.2 Offices Under C.G.A

The following accounting organizations shall work under the Controller

General namely:-

i. The AGPR and its Sub-Offices

ii. The MAG and its sub-offices

iii. The offices of the provincial Accountants General of each province

and the offices subordinate to them.

iv. The Chief Accounts Officers of the departmentalized accounting

offices.

v. Any other departmentalized accounting organization as well as their

sub-offices.

4.3 FUNCTIONS OF THE CONTROLLER GENERAL “The functions of the Controller General shall be:-

a) To prepare and maintain the accounts of the Federation, the provinces

and district governments in such forms and in accordance with such

methods and principles as the Auditor-General may, with the approval

of the President, prescribe from time to time.

b) To authorize payments and withdrawals from the Consolidated Fund

and Public Accounts of the Federal and Provincial Governments

against approved budgetary provisions after pre-audited checks as the

Auditor-General may, from time to time, prescribe.

Page No. 19

An internship Report On Pre Audit AG Office Peshawar

c) To prepare and maintain accounts of such organizations and authorities

established, set up or controlled by the Federation or Provinces as may

be assigned to him by the President or as the case may be, the

Governor of a Province.

d) To lay down the principles governing the internal financial control for

Government departments in constitution with the Ministry of Finance

and the Provincial Finance departments as the case may be..

e) To render advice on accounting procedure for new scheme

Programmes or activities undertaken by the Government concerned.

f) To submit accounts complied by him or any other person responsible

in that behalf, after the close of each finical year the Auditor-General,

showing under the respective heads the annual receipts and

disbursements for the purpose of federation and of each Province

within the time-frame prescribed by the Auditor General.

g) To provide, is so far as the accounts complied by him permit, to the

Federal Government or as the case may be, the Provincial or District

Government such information as such Government such information as

such Governments may from time to time required

h) Develop and maintain efficient system of pension, provident funds and

other retirement benefits in consultation with the concerned

government.

i) To prescribe syllabus, schedule and provide facilities for the training of

officers and staff under his administrative control.”10

`

4.4 FEDERAL CONSOLIDATED FUND

“All revenue received and all loans raised by the Federal Government in

respect of nay loan, shall form part of a consolidated fund to be known as

Federal Consolidated Fund” 11

4.5 PUBLIC ACCOUNT

“All other money received by or on behalf or Federal Government or Received

by or deposited with the Supreme Court or any other Court established under

Page No. 20

An internship Report On Pre Audit AG Office Peshawar

the authority of the federation should be credited to the Public Account of the

Federation.” 11

4.5 PUBLIC ACCOUNT

“All other money received by or on behalf of Federal Government or received

by or deposited with the Supreme Court or any other Court established under

the authority of the Federation should be credited to the public account of the

Federation.”12

Page No. 21

An internship Report On Pre Audit AG Office Peshawar

ANNEXURE-I(Extracts from the 1973 constitution of Pakistan)

Article 168. Auditor-General of Pakistan

1) There shall be an Auditor-General of Pakistan, who shall be

appointed by the President.

2) Before entering upon office, the Auditor-Gen shall take before

the Chief Justice of

3) Pakistan oath in the form set out in the Third Schedule.

4) The terms and condition of service, including the term of

office, of the Auditor Gen shall be determined by the Act of Parliament

and, until so determined, by order of the President.

5) A person who has held office, as Auditor General shall not be

eligible for further appointment in the service of Pakistan before the

expiration of two years after he has ceased to hold that office.

6) The Auditor Gen shall not be removed from office except in the

like manner and on the like grounds as a Judge of the Supreme Court.

7) At any time when the office of the Auditor Gen is vacant or the

Auditor is absent or is unable to perform the functions of his office due

to any cause, such other person as the President may direct, shall act as

Auditor Gen and perform the functions of that office.

Article 169.Function and powers of Auditor General

The Auditor Gen shall, in relation to;

a) The accounts of Federation and of the Provinces; and

b) The accounts of any authority or body established by the Federation or a

Province, perform such functions and exercise such powers as may be

determined by or under Act of Parliament and until so determined, by

order of the President.

Article 170. Power of Auditor General to give Direction as to Account

The accounts of the Federation and of the Provision shall be kept in such form

and in accordance with such principles and methods as the Auditor General

may, with the approval of the President, prescribe.

Page No. 22

An internship Report On Pre Audit AG Office Peshawar

Article 171. Reports of Auditor General

The reports of the Auditor General relating to the accounts of the Federation

shall be submitted to the President, who shall cause them to be laid before the

National Assembly and the reports of the Auditor Gen relating to the accounts

of Province shall be submitted to the Governor of the Province, who shall

cause them to be laid before the Provincial Assembly”.13

`.

Page No. 23

An internship Report On Pre Audit AG Office Peshawar

REFERENCES

1. The Gazette of Pakistan, Extra, (May 17,2001) Ordinance No XXIII OF

2001 part-I Islamabad: Ministry of Law, Justice, Human Rights and

Parliamentary Affairs,p.290

2. Salam, Abdus. (1990).Audit Code 2nd Edition.

Lahore: Audit & Accounts Training Institue,p.1

3. Department of the Auditor General OF Pakistan. (2000) Reform Process

leading to functional separation between Audit & Account, Government of

Pakistan. Part-II Islamabad.p-74

4. Ibid p.74

5. Ibid p.75

6. Ibid p.75

7. Ibid p.76

8. Ibid p.76

9. The Gazette of Pakistan, Extra, (May 17,2001) Ordinance No XXIV Of

2001 part-I Islambad: Ministry of Law, Justice, Human Rights and

Parliamentary Affairs,p.297

10. Ibid p.298

11. Dr. Khan, M.J.R (1982). A Hand Book for Drawing & Disbursing Officers

Revised Edition Islamabad: O & M Division Public Administration

Research Centre,p.28

12. Ibid p.28

13. Department of The Auditor General OF Pakistan, (2000) Reform Process

Leading to functional Separation between Audit & Account, Government

OF Pakistan, Part-II Islamabad.p.53

Page No. 24

An internship Report On Pre Audit AG Office Peshawar

SECTION-4

GENERAL PROVIDENT FUND

(CENTRAL SERVICES) RULES

SHORT TITLE AND DEFINITIONS:

1. a) These rules may be called the General Provident Fund (Central Services )

Rules.

b) They shall come into force on the 1st April 1934.

2. In these rules:-

a) Account Officer means such officer as may be appointed in this behalf by

the Auditor-General of Pakistan.

b) Except where otherwise expressly provided emoluments means pay, leave

salary or subsistence grant as defined in the fundamental Rules and

includes **{ Pay in foreign exchange } converted at official rate of

exchange.

c) Family means:-

i.) In the case of a male subscriber, the wife or wives and children

of a subscriber, and the widow, or widows, and children of a

deceased son of the subscriber. Provided that if a subscriber

proves that his wife has been judicially separated from him or

has ceased under the customary law of the community to which

she belongs to be entitled to maintenance, she shall henceforth

be deemed to be no longer a member of the subscriber’s family

in matters to which these rules relate, unless the subscriber

subsequently indicates by express notification in writing to the

Account Officer that she shall continue to be so regarded;

ii.) in the case of a female subscriber, the husband and children of

a subscriber, and the widow of windows and children of a

subscriber, and the widow or windows and children of a

deceased son of a subscriber.

Page No. 25

An internship Report On Pre Audit AG Office Peshawar

Provided that if a subscriber by notification in writing to the Account

Officer expresses her desire to exclude her husband form her family,

the husband shall henceforth be deemed to be no longer a member of

the subscriber’s family in matters to which these rules relate, unless the

subscriber subsequently cancels formally in writing her notification

excluding him.

d) Fund means the General Provident fund.

e) Leave means any variety of leave recognized by the Fundamental Rules or

the Civil service Regulations.

f) Year means a financial year.

g) Continuous service means service which includes all kinds of leave with or

without pay and foraging service.

(2) Any other expression used in these Rules which is defined either in the

Provident Funds Act ( XIX of 1925) or in the fundamental rules is used in the

sense therein defined.

(b) Nothing in these rules shall be deemed to have the effect of terminating

the existence of the General Provident fund as heretofore existing or of

constituting any new fund.

Constitution of the Fund

3. The Fund shall be maintained in Pakistan in rupees.

4. All Government servants in permanent, temporary of officiating

service (including probationary service) irrespective of the class to

which they belong. Whose conditions of service the President is

competent to determine, shall be eligible to join the Fund:

Provided that no such Government servant as has been required or permitted

to subscribe to a contributory provident fund shall be eligible to join or

continue as a subscriber to the fund while he retains his right to subscribe to

such a fund.

Provided further that any Government servant not qualified for membership

under this rules who has been duly admitted to membership under rules or Page No. 26

An internship Report On Pre Audit AG Office Peshawar

orders heretofore in force shall continue to be member and shall be governed

by any special provision relating to obligation for and rates of , subscription

from time to time contained in those rules or orders for so long as his

conditions of service continue to be determined by the President.

5. Deleted.

6. 1) All eligible government servants in permanent pension able and non-

pension able service and those temporary or officiating Government servants

who have completed 2 years @ continuous temporary and/or officiating

service shall join the fund as compulsory subscribers.

2) All other eligible Government servants may elect to join the fund as

optional subscribers.

( G.P.M.F., O.M. No. F.17 (27)-RI/53, dated 30-12-1953)

1. (i) A Government servant who exercises the option

allowed by rule 6 (2) may discontinue subscription shall lapse if he

discontinue subscribing to the fund at any time, but his right of renewing

subscription shall lapse if he discontinues subscribing except when on leave,

more than three times.

2. (ii) If a Government servant’s right to resume

subscription lapses under sub-rule (i) of this rule he shall nevertheless retain

his other rights and liabilities as a subscriber to the fund; and no final

withdrawal of his deposits shall be allowed except on the happening of one or

other of the contingencies provided for in rules 29 , 30 and 31.

Nominations

8. (I) A subscriber shall , as soon as may be after joining the fund, send to the

Account Officer a nomination conferring on one or more persons the right

to receive the amount that may stand to his credit in the fund, in the event

of his death before that amount has become payable, or having become

payable has not been paid:

Provided that if , at the time of making the nomination, the subscriber has

a family, the nomination shall not be in favour of any person or persons

other that the members of his family.

Page No. 27

An internship Report On Pre Audit AG Office Peshawar

(2) If a subscriber nominates more than one person under sub-rule (1) , he

shall specify in the nomination the amount or share payable to each of the

nominees in such manner as to cover that whole of the amount that may

stand to his credit in the fund at any time.

(3) Every nomination shall be in such one of the forms set forth in the first in

the first schedule as is appropriate in the circumstances.

(4) A subscriber may at any time cancel a nomination by sending a notice in

writing to the Account Officer:

Provided that the subscriber shall, along with such notice, send a fresh

nomination made in accordance with the provisions of sub-rules (I) to (3).

(5) Without prejudice to that provisions of sub-rule (4) a subscriber shall

along with every nomination made by his under this rule send to the

account officer a contingent notice of cancellation which shall be in such

one of the forms set forth in the second schedule as is appropriate in the

circumstances.

(6) Immediately on the occurrence of any event by reason of which the

contingent notice of cancellation referred to in sub-rule ( 5) becomes

operative and the nomination to which the be in such one of the form set

forth.

(7) Every nomination made, and every notice of cancellation given, by

subscriber shall, to the extent that it is valid, take effect on the date on

which is received by the Account Officer.

(8) Nothing is sub-rules (1) to (3) shall be deemed to invalidate or to

required the replacement by a nomination there under of, a nomination

duly made before and subsisting on the 4th September, 1941. Provided

that in respect of every such nomination, the subscriber shall, as soon as

Page No. 28

An internship Report On Pre Audit AG Office Peshawar

may be after the said date send to the Account Officer a contingent

notice of cancellation in such one of the Forms set forth in second

Schedule as is appropriate in the circumstances.

Subscribers Accounts

9. An account shall be prepared in the name of each subscriber and shall

show the amount of his subscriptions with interest thereon calculated as

prescribed in sub-rule (2) of Rule 14.

Conditions and Rates of subscriptions

10. (1) Except as provided in rule 7, a subscriber shall subscribe monthly to

the fund except during a period of suspension.

Provided that a subscriber may, at his option, elect not to subscribe

during leave.

Provided further that a subscriber on reinstatement after a period passed

under suspension shall be allowed the option of paying in one sum, or in

installments, any sum not exceeding the maximum amount of arrear

subscription permissible for that period.

(2) The subscriber shall intimate his election not to subscribe during leave in the

following manner:-

(a) If he is an officer who draws his own pay bills, by making no deduction on

account of subscription in his first pay bill drawn after proceeding on leave.

(b) If he is not an officer who draws his own pay bills, by written communication

to the head of his office before he proceeds on leave. Failure to make due and

timely intimation shall be deemed to constitute an election to subscribe.

The option of a subscriber intimated under this sub-rule shall be final.

(3) A subscriber who has, under rule 30, withdrawn the amount standing to his

credit in the fund shall not subscribe to the fund after such withdrawal unless

and until he returns to duty.

Page No. 29

An internship Report On Pre Audit AG Office Peshawar

11. (1) The amount of subscription shall be fixed by the Subscriber himself, subject

to the following Conditions:-

(a) It shall be expressed in whole rupees.

(b) Except in the case of class IV Government servants, it may be any sum so

expressed but not less than the rates as indicated below:-

Pay range Minimum rates of subscription

(1) Up to Rs. 500 P.M Six paisa in the rupee

(2) Rs. 501 to Rs. 1,000 p.m Nine paisa in the rupee

(3) Above Rs. 1,000 p.m Twelve paisa in the rupee

The minimum rate of subscription in the case of class IV Government servants

shall be one rupee.

(2) For the purposes of sub-rule (1) the emoluments of a subscriber shall be.

(a) in the case of a subscriber who was in Government service on the 30 th June of

the preceding year, the emoluments to which he was entitled on that date

provided as follows:-

(i) If the subscriber was on leave on the said date and elected not to subscribe

during such leave or was under suspension on the said date, his emoluments

shall be the emoluments to which he was entitled on the first day after his

return to duty.

(ii) if the subscriber was on deputation out Pakistan on the said date or was on

leave on the said date and continues to be on leave and has elected to

subscribe during such leave, his emoluments shall be the emoluments to which

he would have been entitled had he been on duty in Pakistan;

(iii) If the subscribe joined the fund for the first time under the operation of

rule 6 on a day subsequent to the said date, his emoluments shall be the

emoluments to which he was entitled on such subsequent date.

(b) In the case of a subscriber who was not in Government service on the 30 th

June of the preceding year, the emoluments to which he was entitled on the

first day of his service or, if he joined the Found for the first time under the

operation of rule 6 on a date subsequent to the first day of his service, the

emoluments to which he was entitled on such subsequent date.

Page No. 30

An internship Report On Pre Audit AG Office Peshawar

3) The subscribe shall intimate the fixation of the amount of his monthly

subscription in each year in the following manner:-

(a). If he was on duty on the 30th June of the preceding year, by the deduction

which he makes in this behalf from his pay bill for that month:

(b) If he was on leave on the 30th June of the preceding year and elected not

to subscribe during such leave, or was under suspension on that date , by

the deduction which he makes in this behalf from his first pay bill after

his return to duty.

(c) If he has entered Government service for the first time during the year,

or if he is compulsorily required to join the fund from a particular date

under rule 6, or joins the und for the first time, by the deduction which

he joins the fund.

(d) If he was on leave on the 30th June of the preceding year, and continues

to be on leave and has elected to subscribe during such leave, by the

deduction which he causes to be made in this behalf from his salary bill

for that month;

(e) If he was on foreign service on the 30th June of the preceding year, by

the amount credited by him into the treasury on account of subscription

for the month of July in the current year.

4. The amount of subscription so fixed shall remain unchanged throughout the

year:

Provided that if a subscriber is on duty for a part of a month and on leave for

the remainder of that month and if he has elected not to subscribe during

leave, the amount of the subscription payable shall be proportionate to the

number of days spent on duty in the month.

Provided further that if the emoluments of a subscriber are increased or

reduced during the currency of a financial year by not less than 20 per cent,

the subscriber shall have the option to refix his subscription under sub-rule (1)

during the currency of that year.

12 When a subscriber is transferred to foreign service or

sent on deputation out of Pakistan, he shall remain subject to the rules of the

fund in the same manner as if he were not so transferred or sent on

deputation.

Page No. 31

An internship Report On Pre Audit AG Office Peshawar

Realization of Subscription

13. When emoluments are drawn from a Government

treasury in Pakistan or when the Government servant is on foreign service

outside Pakistan the recovery of subscriptions on account of these emoluments

and of the principal and interest of advances shall be made from the

emoluments themselves, and recovery on the above account from Government

servants on foreign service outside Pakistan shall be made in foreign exchange

through the Embassy of Pakistan in the country concerned in such manner as

the Federal Government may, from time to time, direct.

(2) When emoluments are drawn from any other source the subscriber shall

forward his dues monthly to the Account Officer.

(3) If a Government servant fails to subscribe with effect from the date on which

he is required to join the fund under rule 6, the total amount due to the fund

on account of arrears of subscription shall, with interest thereon at the rate

provided in rule 14 forthwith be paid by the subscriber to the fund, or in

default be ordered by the Account Officer to be recovered by deduction from

the emoluments of the subscriber by installments or otherwise, as may be

directed by the authority competent to sanction an advance for the grant of

which special reasons are required under clause (c )of sub-rule 15.

Interest

14. Subject to the provisions of sub-rule (5) below, Government shall pay to the

credit of the account of a subscriber interest at such rate as may be determined

for each year according to the method of calculation prescribed from time to

time by the Government of Pakistan:

Provided that, if the rate of interest determined for a year is less than 4 per

cent, all existing subscribers to the fund in the year preceding that for which

the rate has for the first time been fixed at less than 4 per cent, shall be

allowed interest at 4 per cent.

Page No. 32

An internship Report On Pre Audit AG Office Peshawar

2. Interest shall be credited with effect from last day in each year in the following

manner:-

(i) On the amount at the credit of a subscriber on the last day of the preceding

year, less any sums withdrawn during the current year- interest for twelve

months;

(ii) On sums withdrawn during the current year- interest from the beginning of the

current year up to the last day of the month preceding the month of

withdrawal;

(iii) On all sums credited to the subscriber’s account after the last day of the

preceding year—interest from the date of deposit up to the end of the current

year;

(iv) The total amount of interest shall be rounded to the nearest whole rupee, fifty

paisa counting as the next higher rupee;

Provided the when the amount standing at the credit of a subscriber has

become payable, interest shall thereupon be credited under this sub-rule in

respect only of the period from the beginning of the current year or from the

date of deposit, as the case may be, up to the date on which the amount

standing at the credit of the subscriber became payable.

In this rule, the date of deposit shall, in the case of a recovery from

emoluments, be deemed to be the first day of the month in which it is

recovered ; and in the case of an amount forwarded by the subscriber, shall be

deemed to be the first day of the month of receipt if

it is received by the Account Officer before the fifth day of that month, but it

is received on or after the fifth day of that month, the first day of the next

succeeding month.

In addition to any amount to be paid under rules 29, 30 or 31 interest thereon

up to the end of the month preceding that in which the payment is made shall

be payable to the person to whom such amount is to be paid:

Page No. 33

An internship Report On Pre Audit AG Office Peshawar

Provided that where the Account Officer has intimated to that person (or his

agent) a date on which he is prepared to make payment in cash, or has posted a

cheque in payment to that person interest shall be payable only up to the end

of the month preceding the date so intimated, or the date of posting the

cheque, as the case may be:

Provided further that if the person claiming the payment does not send an

application in that behalf within six months of the date on which the amount

standing at credit of the subscriber has become payable under rule 29, interest

shall be payable upto the end of sixth month after the month in which the

amount became payable.

Advance from the fund

A temporary advance may be granted to a subscriber from the mount that he

have in his a/c. the following conditions are:

1) No advance shall be granted unless the sanctioning authority is satisfied that

really the subscriber has the specific problem.

2) To pay for the overseas passenger for reasons of health or education of the

applicant or any person actually depend on him.

3) To pay expenses incurred in connection with the prolonged illness.

4) To pay for his marriage or the marriage of any member of his family.

Provided that an advance for the purchase of a motor car , motor cycle or

bicycle may be granted term and condition laid down in Para 254 to263-A of

the General Financial Rules. Volume-I

1) The sanctioning authority shall record in writing its reason for granting the advance.

2) An advance shall not, except for special reasons.

a) Exceed three months, pay or half the amount at the

credit of the subscriber in the fund. Whichever is

Page No. 34

An internship Report On Pre Audit AG Office Peshawar

less.

b) Unless the amount already advanced does not exceed two – thirds of the

amount admissible under sub-rule ( C ) ( I) be granted until at least twelve

months after the final repayment of all previous advances together with

interest

15-A an advance for construction of a (house any where in Pakistan) for occupation

by a the subscriber himself or change or completely reconstructing or for

extending or renovating house already owned by the children or by any of

thin.

a) Advance will be given under Para 253.A. of General Financial Rules.

b) An advance shall not be exceed then 80% of the total credit of the subscriber.

c) The sanctioning authority shall see the land and the house for issuing the

sanction.

d) Mortgage deed shall be registered within four months of its execution. No

reasons are required to be given for the advances after the subscriber has

attained the age of 50 years.

The amount of each advance shall not exceed eighty per cent of the balance in

the account of the subscriber on the date of application for the grant of

advance.

An advance drawn from G.P fund account of refundable advance if subscriber

has in the meanwhile attained the age of 45 year.

An advance shall be recovered from the subscriber in such number of equal

monthly installments as the sanctioning authority may direct; but such number

shall not be less than twelve unless the subscriber so elects. Or in any case,

more than forty-eight} A subscriber may, at his option, repay more than one

installment in a month. Each installment shall be a number of whole rupees the

amount of the advance being raised or reduced, if necessary, to admit of the

fixation of such installments.

Page No. 35

An internship Report On Pre Audit AG Office Peshawar

Recovery shall be made in the manner prescribed in rule 13, for realization of

subscriptions, and shall commence on the first occasion after the advance is

made on which the subscriber draws pay, or remuneration on foreign service.

Final withdrawal of Accumulations in the fund

When a subscriber quits the service, the amount standing to his credit in the

fund shall become payable to him.

Provided that a subscriber, who has been dismissed form the service and is

subsequently reinstated in the service shall, if required to do so by

Government, repay any amount paid to him form the fund in pursuance of this

rule , with interest thereon at the rate provided in rule 14 in the manner

provided in the proviso to rule 30. the amount so repaid shall be credited to his

account in the fund.

G.P.F.D.,O.M No. F.1 (3)-R.7/82-317, dated 9-5-1982)

When a subscriber-

a) Has proceeded on leave preparatory to retirement, or ,if he is employed in a

vacation department , on leave preparatory to retirement combined with

vacation, or

b) While on leave has been permitted to retire or been declared by a competent

medical authority to be unfit for further service.

The amount standing to his credit in the fund shall, upon application made by

him in that behalf to the Account Officer, become payable to the subscriber.

Provided that the subscriber, if he returns to duty, shall, if required to do so by

Government, repay to the fund, for credit to his amount, the whole or part of

any amount paid to him from the fund in pursuance of this rule with interest

thereon at the rate provided in rule 4, in cash or securities or partly in cash and

partly in securities, by installments or otherwise by recovery from his

emoluments or otherwise,

Page No. 36

An internship Report On Pre Audit AG Office Peshawar

as may be directed by the authority competent to sanction an advance for the

grant of which special reasons are required under clause © of sub-rule (1) of

rule 15.

Provided that no share shall be payable to.

1). Sons who have attained legal majority:

2). Sons of a deceased son who have attained legal majority:

3) Married daughters whose husbands are alive:

4) married daughters of a deceased son whose husbands are alive :

Transfer to Pension able service

33. (a) If a Government servant who is a subscriber to any other

Government provident fund, which is a non- contributory provident fund, is

permanently transferred to pension able service under the president, the

amount of subscriptions, together with interest thereon, standing to his credit

in such other fund at the date of transfer shall, with the consent of the other

Government concerned, be transferred to his credit in the fund.

(b) If a Government servant who is a subscriber to the State Railway Provident fund

or the Contributory Provident fund (Pakistan) or a provincial contributory

provident fund is permanently transferred to pension able service under in

President and elects or is required to calm pension in respect of such pension

able service-

(i) The amount of subscription, with interest thereon, standing to his credit in

such contributory provident fund at the date of transfer shall with the consent

of the other Government, if any, be transferred to his credit in the fund;

(ii) The amount of Government contributions, with interest thereon, standing to

his credit in such contributory provident fund shall, with the consent of the

other Government if any, be repaid to Government and credited to central

revenues ( civil) and

Page No. 37

An internship Report On Pre Audit AG Office Peshawar

(iii) He shall in exchange be entitled to count to wards pension such part of the

period during which he subscribed to such contributory provident fund as the

president may determine.

Page No. 38

An internship Report On Pre Audit AG Office Peshawar

Procedure Rules

34. All sums paid into the fund under these rules shall be credited in the books of

Government to an account named “ The General Provident Fund” Sums of

which payment has not been taken within six months after they become

payable under these rules shall be transferred to “Deposits” at the end of the

year and treated under the ordinary rules relating to deposits.

35. When paying a subscription in Pakistan either by deduction from emoluments

or in cash, a subscriber shall quote the number of his account in the fund,

which shall be communicated to him by the Account Officer. Any change in

the number shall similarly be communicated to the subscriber by the Account

Officer.

36. (I) As soon as possible after the close of each year, the Account Officer shall

send to each subscriber a statement of his account in the fund showing the

opening balance as on the 1st July of the year, the total amount credited or

debited during the year, the total amount of interest credited as on the 30th June

of the year the closing balance on that date. The Account Officer shall attach

to the statement of account an enquiry whether the subscriber.

(a) Desires to make any alteration in any nomination made under rule 8, or under

the corresponding rule heretofore in force.

(b) Has acquired a family in cases where the subscriber has made no nomination

in favour of a member of his family under the proviso to sub-rule ( I) of rule 8.

PROBLEM IN GP FUND FACED BY SUBSCRIBERS

TOKEN NUMBER

a) The first problem face by a subscriber in time of with drawal of G.P. fund

advance.

b) In the time of token number if any mistake found the concern auditor may

return this bill to the department for correction. Token register is maintain

for this purpose to write No. some time, the junior auditor has not enter

this bill, and it may lost.

Page No. 39

An internship Report On Pre Audit AG Office Peshawar

a) Name of the subscriber is checked if there is any mistake in the name

the bill will be returned to that concern department.

b) Sanction may also be checked if this sanction is not properly signed by

the concern DDO.

c) Account number will also be checked. If any figure miss the bill will

be return.

d) Source (V) will also be checked. If any mistake found the bill will be

returned.

e) Account code will also be checked. If A/C code has not written on the

bill the bill will be retuned to deptt.

f) Overdrawn by the subscriber.

g) The bill has not prepared according to Roll 16(a).

h) The balance has not covered the 80% of bill.

i) The signature of DDO is correct or not.

j) Amount to be checked.

After auditing of the above points. If the bill has no mistake the bill

will be passed.

k) Bill signed by the auditor & others officer. When the bill passed by the

senior auditor it will be send to the supertendant. He checked and

signed. Then the bill will send to the account officer for signature if the

AO satisfied from the bill he signed it:-

CHEQUE

After the auditing process the cheque will be made, and signed by different

officers and computer sanction. Then the cheque will be made and send to the

concerned department.

Page No. 40

An internship Report On Pre Audit AG Office Peshawar

SUMMARY OF N.W.F.P GENERAL PROVIDENT FUND RULES

Compulsory saving scheme:-

Monthly deduction are made according to BPS from pay bills w.e.f 01-12-

2001(Rule-4)

Scale Rate

(Rs)

Scale Rate

(Rs)

Scale Rate

(Rs)Scale Rate

(Rs)

B-1 85 B-8 215 B-15 585 B-22 2100

B-2 145 B-9 230 B-16 660

B-3 160 B-10 245 B-17 870

B-4 170 B-11 265 B-18 1120

B-5 180 B-12 455 B-19 1485

B-6 195 B-13 495 B-20 1710

B-7 205 B-14 540 B-21 1905

ACCOUNTING BY DAO/AG.

Ledger Account for each employee (Rule-7)

Balance Sheet is issued before the third month of every financial year.

Interest = Progressive Balance X Rate of Interest/ 100x1/12.Rule-7-)

Page No. 41

An internship Report On Pre Audit AG Office Peshawar

Admittance to Fund

Apply to DAO/AG through DDO for allotment of A/C No.

Send nomination forms specifying share(Rule-3)

Temporary Advances (Refundable Advances).

S.# Purpose Amount

Advance

Recover GPF

Rules.

1 Illness, Education,

Health, Marriage

for self dependent

3 months pay,

or ½ of the

balance, which

ever is less

12-36 installments

15

2 Construction/

purchases of

House/addition &

alteration in House

for himself and

family member

36 months pay

or 80 % of

balance which

ever is less -DO- 16

Interest is recovered in one or two installments at the following rate: Amount

of Advance X No. of installments/500. (Rule-14)

Page No. 42

An internship Report On Pre Audit AG Office Peshawar

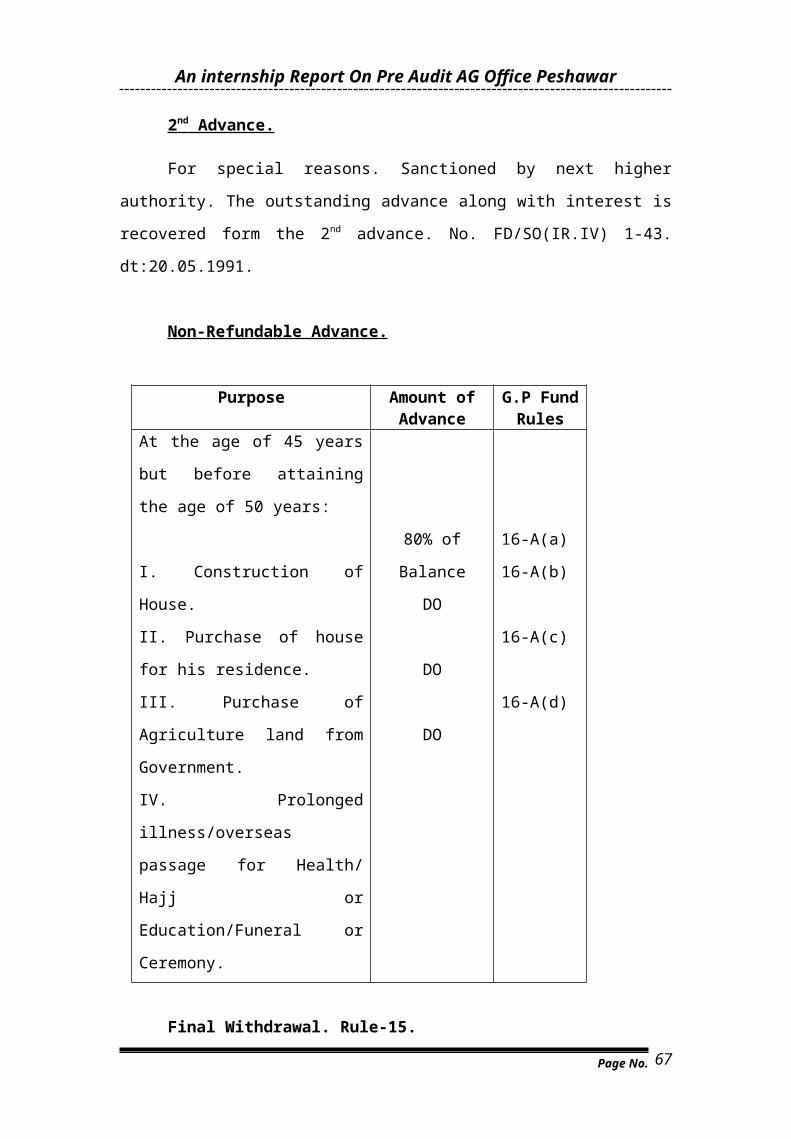

2 nd Advance.

For special reasons. Sanctioned by next higher authority. The outstanding

advance along with interest is recovered form the 2nd advance. No. FD/SO(IR.IV) 1-

43. dt:20.05.1991.

Non-Refundable Advance.

Purpose Amount of Advance

G.P Fund Rules

At the age of 45 years but before

attaining the age of 50 years:

I. Construction of House.

II. Purchase of house for his

residence.

III. Purchase of Agriculture land

from Government.

IV. Prolonged illness/overseas

passage for Health/ Hajj or

Education/Funeral or Ceremony.

80% of Balance

DO

DO

DO

16-A(a)

16-A(b)

16-A(c)

16-A(d)

Final Withdrawal. Rule-15.

When Quits Service. Dies in Service-paid to nominees or family members

Proceeds on L.P.R Zakat @ 2 ½ % deducted

Protection of accumulations. Rule-I

It cannot be paid towards fine or attachment under any decree of any court of

law. Amount over paid cannot be record from the GP fund unless he gives his

consent.

ILLUSTRATION ------ G.P.FUND BALANCE SHEETPrepare G.P.Fund Balance Sheet for the year 2001-2002 from the following

particulars:-

Opening Balance on 01.07.2001 Rs.10000/-

Page No. 43

An internship Report On Pre Audit AG Office Peshawar

Rate of monthly subscription Rs.180/-

Drawl of Refundable/ Non-Refundable Advance on 1.9.2000 Rs.2000/-

Recovery of G.P Fund Advance per month Rs.100/-

Rate of interest for the year Rs.14.5 %

G.P. Fund Balance Sheet For The Year

Payroll Month

Monthly Subscription

Refund of Advance

Total Total with drawls

Progre:ssive Balance

July 180 -- 180 Rtfg

August 180 -- 180 10360

Sep 180 -- 180 (A) 2000 5840

Oct 180 100 280 8820

Nov 180 100 280 9100

Dec 180 100 280 9380

January 180 100 280 9660

February 180 100 280 9940

March 180 100 280 10220

April 180 100 280 10500

May 180 100 280 10780

June 180 100 280 11060

TOTAL 2160 900 3060 118540

Opening Balance Rs. 10000Total Deposits Rs. 3060Interest ____% Rs. 1482Total Rs. 14542Withdrawals Rs. 2000Closing Balance Rs. 12542Irregular Formula=Sum of Progressive Balance X Rate of Interest X 1 /12

100Regular Formula = O/B x2x13 Credit X Formula

Page No. 44

An internship Report On Pre Audit AG Office Peshawar

REFERENCES

1. The G.P Fund Rules by Federal Govt.,

2. Salam, Abdus. (1990).Audit Code 2nd Edition.

Lahore: Audit & Accounts Training Institue,p.1

3. Department of the Auditor General OF Pakistan. (2000) Reform Process

leading to functional separation between Audit & Account, Government Of

Pakistan. Part-II Islamabad.p-74

4. Ibid p.74

5. Ibid p.75

6. Ibid p.75

7. Ibid p.76

8. Ibid p.76

9. The Gazette of Pakistan, Extra, (May 17,2001) Ordinance No XXIV Of

2001 part-I Islambad: Ministry of Law, Justice, Human Rights and

Parliamentary Affairs,p.297

10. Ibid p.298

11. Dr. Khan, M.J.R (1982). A Hand Book for Drawing & Disbursing Officers

Revised Edition Islamabad: O & M Division Public Administration

Research Centre,p.28

12. Ibid p.28

13. Department of The Auditor General OF Pakistan, (2000) Reform Process

Leading to functional Separation between Audit & Account, Government

OF Pakistan, Part-II Islamabad.p.53

Page No. 45

An internship Report On Pre Audit AG Office Peshawar

CHAPTER-1GAZETTED AUDIT DEPARTMENT

INTRODUCTION

The Gazetted Audit Department is working at six places, namely, Islamabad ,

Karachi , Lahore , Peshawar, Quetta and Gilgit and is divided into sections

known as GA.II, GA.III,GA.IV, GA.V, GA.VI and GA .VII at Islamabad.

AREAS OF WORK

The main areas of work for which the department is responsible are:-

(a) Audit of pay and allowances of Gazetted Officers including audit of

sanctions.

(b) Posting of Gazetter Notifications in the Audit Registers.

(c) Issue of pay slips, leave salary certificates and last pay certificate.

(d) Maintenance of leave accounts including reports on applications for

leave.

(e) Maintenance of Scale Audit Registers.

(f) Maintenance, compilation and issue of the History of Services.

(g) Maintenance of Board Sheets of House Building Advances, Motor Car

Advances and Advances for other conveyances.

(h) Arrangement for the payment of pay and allowances including leave

salary of Gazetted Officers not under the audit control of this

department, when so required.

(i) “Preparation and issue of statements showing the names of Gazetted

Officers due to retire”(Annexure-B)

Work Distribution

Each section is under the charge of a B.O or A.A.O in control. The B.O is

responsible for carrying out the day to day duties under the supervision of an

Addl. A.G or a D.A.G.

A.A.O’s Job

The A.A.O generally supervises the work of the section related with

correspondence, all non-routine cases and is personally responsible for

Page No. 46

An internship Report On Pre Audit AG Office Peshawar

maintenance of the sectional Calendar of Returns, pay slips, review of audited

bills in accordance with the prescribed procedure and the work relating to the

payment of salary. He is also responsible to see that all returns are issued on

due dates and that no unnecessary delay occurs in the disposal of cases in his

section.

Auditor’s Job

The work of the sections is divided, according to load of work. Each seat is

under the charge of an auditor. He is responsible for initiating all the audit

work regarding payment of a claim, recording it in the relevant register

classifying the charges, recording them in objection book, maintenance of

leave accounts, preparation and issue of last pay certificates, pay slips, leave

salary certificates, correspondence etc. some of them deal with compilation of

periodical returns.

Junior Auditor’ Job

A Junior Auditor works as a diarist and is responsible for other routine duties.

Letters’ Disposal Procedure

Following procedure is outlined for the receipt and disposal of all letters either

of common interest to all the sections or not concerned to any particular

section, as in the case of advice sought for by outside authorities in respect of

gazetted audit matters:-

Co-Ordination Section

GAD.I is the coordination section at Islamabad. The cases of general nature

relating to fixation of pay, admissibility of allowances, leave interpretation of

rules, procedure and other controversial subjects are received and dealt with in

these sections.

Payment Authorities

Payment authorities received from other accounts offices on behalf of gazetted

officers not under the audit control of this office are dealt with by GA. I at

Islamabad.

Page No. 47

An internship Report On Pre Audit AG Office Peshawar

Preparation of History of Service

Coordination work in connection with the preparation of the History of

Services is done by GAD-I. This section is required to collect the History of

Services from all the GAD section compile it and make necessary

arrangements for its printing and publication.

General Letter Circulation

“When only single copy of general letters concerning all the sections received

in one of the section at Karachi, Islamabad, the section should get the letters

typed; or, if they be lengthy, printed or cyclostyle copy, should obtain extra

copies from the departments concerned and supply copies to other section at

Karachi and Islamabad so that the case of each section may be self-contained

and prompt action on its parts may be taken” 2

General Cases Intimation

The section responsible for receipt and disposal of general cases concerning

all the section should intimate to other sections the orders passed thereon. In

non-routine cases the dealing section may, with the consent of the Branch

Officer concerned, consult other sections.

Page No. 48

An internship Report On Pre Audit AG Office Peshawar

PRE-ADUDIT SECTION WORK FLOW CHART

.GAZATTED GOVERNMETN SERVANTS’ AUDIT

List of Registers

“Besides the checks prescribed in the preceding Article the duty of Audit in

case of the pay bill of an effective gazetted Government Servant is-

a. to record the payment as a check on any second claim;