Embed Size (px)

Citation preview

March 2011

United StatesDepartment ofAgriculture

Report of the

Submitted to theSecretary of Agriculture

Dairy IndustryAdvisory Committee

1

Recommendations for Public Policy to Improve Dairy Farm Profitability and Reduce Milk Price Volatility

Foreword

The U.S. Department of Agriculture (USDA) established the Dairy Industry Advisory Committee

(Committee) in August 2009, under the rules of the Federal Advisory Committee Act (FACA). Secretary

Tom Vilsack appointed 17 members to serve on the Committee on January 6, 2010. The Committee

Charter is “to review the issues of: 1) farm milk price volatility and 2) dairy farmer profitability. The

Committee will provide suggestions and ideas to the Secretary on how USDA can best address these

issues to meet the dairy industry’s needs.” The Committee Charter further explains, “The exchange of

views and information between industry representatives and USDA should result in improved

understanding of the impact of USDA programs on the dairy industry and contribute to those programs’

effective and efficient administration”.

The Committee Bylaws state that “Members will be selected from a cross section of the dairy

industry representing producers and producer organizations, processors and processor organizations,

handlers, academia, retailers, consumers, and State agencies involved in organic and non-organic dairy at

the local, regional, national, and international levels.” Individuals serving on the Committee are as

follows1:

1 All members, except Dr. Novakovic, are considered under FACA to be serving as Representative Members and are appointed to obtain the perspectives of public sector stakeholders. Dr. Novakovic serves as a Special Government Employee under appointment by Secretary Vilsack.

2

Members Affiliation

Paul Bourbeau Paboco Farms, Inc., Vermont

Jay Bryant Maryland and Virginia Milk Producers Cooperative

Association, Virginia

Erick Coolidge Le-Ma-Ra Farm, Pennsylvania

Timothy den Dulk Den Dulk Dairy Farm, LLC, Michigan

Debora Erb Springvale Farms & Landaff Creamery, LLC, New Hampshire

James Goodman Northwood Farm, Wisconsin

James Krahn Oregon Dairy Farmers Association, Oregon

Edward Maltby Northeast Organic Dairy Producers Alliance, Massachusetts

Andrew Novakovic Cornell University, New York

Randy Romanski (replacing Rodney

Nilsestuen, dec. July 2010)

Department of Agriculture, Trade and Consumer Protection,

Wisconsin (formerly)

Robert Schupper Ahold USA Retail, Pennsylvania

Manuel (Ray) Souza Mel-Delin Dairy, California

Patricia Stroup Nestle USA, California

Sue Taylor Leprino Foods Company, Inc., Colorado

Edward Welch Associated Milk Producers Inc., Minnesota

James (Ricky) Williams Williams Dairy & Williams Dairy Trucking, Inc., Georgia

Robert Wills Cedar Grove Cheese Inc., Wisconsin

3

Executive Summary

The Federal Government has a number of programs to intervene when dairy prices fall to low

levels. For example, the Dairy Product Price Support Program (DPPSP) is designed to prevent wholesale

and farm prices from falling below a certain level. The Milk Income Loss Contract (MILC) Program is

designed similarly to the countercyclical payments used for agricultural crops and provides a cash income

supplement to partially offset the impact of low milk prices.

During 2009, MILC income supplements were triggered from February through November 2009.

Just short of $1 billion was spent on MILC in the 2 fiscal years (FYs) from October 2008 to

September 2010. The Agricultural Appropriations bill for FY 2010 provided an additional $290 million

as direct payments to farmers through the Dairy Economic Loss Assistance Payment (DELAP) Program.

These direct payments to farmers were by far the most significant and costly of the existing program

activities in the last 2 years.

Surplus butter and nonfat dry milk (NDM) were sold to the Government, at supported price

levels, under the DPPSP as well. The magnitude of DPPSP sales was quite small. In FY 2009,

Government purchases as a percentage of all commercial disappearance was 0.03 percent on a milkfat

basis and 1.7 percent for nonfat solids. The FY 2010 special Agricultural Appropriation also provided

$60 million for the purchase of cheese to be used in domestic food assistance programs. Of this total, $43

million was spent in FY 2010. In that year, the purchases enabled by the special appropriation amounted

to about 0.3 percent of total cheese production. For FY 2009, $230 million was spent to acquire surplus

dairy products under the DPPSP. These Government purchases and expenditures were not large enough

to mitigate the drop in commercial sales.

In addition to these core dairy programs, the Government made $108.6 million in direct loans to

dairy farmers through the Farm Loan Program (FLP), loan guarantees, concessions, and options for

restructuring, rescheduling, or deferring payments on existing FLP loans. The Dairy Export Incentive

Program (DEIP) was activated after several years of dormancy. Existing programs were implemented

and even augmented in 2009 and 2010 but those efforts did not prevent 2009 from being the worst year

for dairy farm profitability in decades.

The Committee makes 23 recommendations that are listed in the table at the end of the summary.

The order in which the recommendations are presented is not intended to connote importance or priority.

They are grouped thematically. The first set of recommendations relate to existing programs. These are

recommendations that do not require Congressional action.

4

The Committee finds that existing Federal programs and legislation had a limited impact on

mitigating the massive impact of recent market events. Some laws provide no flexibility to the Secretary,

while others allow some or even considerable discretion. When a proposed action has or is likely to have

an impact on Government expenditures, even programs that offer discretion to the Secretary cannot be

used without approval of the OMB. Meanwhile, Federal Milk Marketing Orders (FMMOs) are designed

for longer-term regulation of markets and are not readily amenable to mitigating shorter-term price

events.

Considering existing programs alone, if the Secretary can identify funding sources, he can use the

DPPSP and one or more food assistance programs to stimulate demand and lift prices. In this report, the

Committee suggests guidelines for using these programs (cf. recommendation 5).

Allocating part of the U.S. Government’s budget to dairy programs necessarily involves tradeoffs

with other programs. The Committee suggests that using objective measures of sector hardship can

reduce political pressures in the allocation process. The Committee recommends that the Secretary

implement trigger levels based on the difference between average milk prices and a new measure of feed

costs (cf. recommendation 1). The Secretary can then objectively determine when dairy farmers face

extreme hardship by examining whether the difference between revenues and costs falls below specific

trigger levels. Extreme hardship would justify shifting Governmental resources from other uses. Within

this framework, the first trigger would indicate use of a food assistance program to increase demand for

dairy products. At the second trigger, the DPPSP purchase prices may be raised. The Committee

recommends applying these responses cautiously.

The Committee also recommends that the Secretary review existing program administration to

examine its impact on exacerbating price volatility or delaying the Government’s response to dairy

farmers’ economic distress (cf. recommendation 2). For example, there are some delays in using the

DPPSP because of extra grading and other requirements and slower payment than is typical with

commercial accounts. Comments made to the Committee indicated that, despite significant

improvements in the Order amendment process, the FMMO program is difficult to change and could still

be improved. Moreover, the FMMO milk pricing formulas may be transferring volatility in narrow

subsectors of the dairy market into wider milk prices. Changes can be made to FMMOs without new

legislation.

USDA also is authorized to offer certain programs to help dairy farmers manage price, margin,

and/or income risk and to facilitate obtaining operating loans, especially for farmers whose circumstances

5

make it difficult to get conventional, commercial loans. The Committee offers one recommendation for

each type of program (cf. recommendations 4 and 5).

The Committee has also reviewed and considered alternative actions that would require new

legislation or regulation. In so doing, it was guided by the charge from the Secretary to focus attention on

dairy farm profitability and milk price volatility (cf. recommendations 6-9). Thus, the second set of

recommendations relates to actions that primarily address issues of milk price protection, stabilization, or

regulation. In a sense, they approach the problems of milk price volatility from the perspective of can this

be prevented or reduced. The third set take the perspective that, if price volatility cannot be avoided,

what can be done to reduce its impacts on the industry (cf. recommendations 10-12). This section is

referred to as income protection or stabilization. The fourth and last section combines a variety of

recommendations that seek to improve dairy farm profitability or enhance the development of dairy

markets, using strategies different from price or income stabilization (cf. recommendations 13-23).

It should also be noted that, while there was widespread DIAC support for most of these

recommendations, some recommendations were harder to reconcile across the entire group. Indications

of support among DIAC members are listed with each recommendation as a vote tally.

This report has three main sections. In the first, the justification for existing and new dairy policy

is reviewed, with an emphasis on the Committee’s charge to focus on dairy farm profitability and milk

price volatility. In the second section, existing programs, laws, and authorities are discussed. Lastly,

proposals and recommendations for modifications to existing programs or the creation of new programs

are reviewed and discussed.

6

NUMBER RECOMMENDATION PAGEEXISTING PROGRAMS AND AUTHORITIES

1

DEVELOP A SYSTEM THAT PROVIDES AN ACCURATE ASSESSMENT OF DAIRY FARM PROFITABILITY IN THE DAIRY INDUSTRY. USDA should develop a data gathering and reporting system that expresses farm profitability in the dairy industry using an index to provide an impartial overview of the general level of profitability at the farm level based on the milk price-feed cost margin.

12 in favor, 5 opposed, 0 abstaining

19

2

REVIEW FEDERAL MILK MARKETING ORDERS (FMMOs). The Secretary should appoint a committee to review implications of FMMOs, including, but not limited to, end-product pricing’s impact on milk price volatility and impact of classified pricing and pooling on processing investment, competition and dairy product innovation.

17 in favor, 0 opposed, 0 abstaining

31

3

SIMPLIFY AND IMPROVE RISK MANAGEMENT PRODUCTS FOR DAIRY FARMERS. Continue to simplify and improve Livestock Gross Margin (LGM)-Dairy and overhaul Adjusted Gross Revenue-Lite (AGR-Lite) in order to make them more accessible and easier for dairy farmers to use and adapt Livestock Risk Protection for use by dairy farmers. Expand risk management education.

17 in favor, 0 opposed, 0 abstaining

35

4

USE OF USDA Farm Loan Programs (FLPs). The Secretary should work with the Farm Service Agency (FSA) in Washington and all State FSA Executive Directors and State Committee members, particularly those in States with significant numbers of dairy operations, to promote efficient and effective use of the FLP for dairy farmers. We especially encourage the use of the Guaranteed Loan Program with existing commercial lenders. Apparently, some States leverage FLPs more effectively than others. We recommend that the Federal FSA examine any disparities and develop strategies to share best practices across regions.

17 in favor, 0 opposed, 0 abstaining

45

5

EMERGENCY INTERVENTIONS. The Secretary should develop a system of triggers and actions to guide his choices for special and emergency interventions, using existing programs.

17 in favor, 0 opposed, 0 abstaining

50

PRICE PROTECTION, STABILIZATION AND REGULATION

6

BEST USE OF FUNDS: Explore elimination of the Dairy Product Price Support Program (DPPSP) and the Dairy Export Incentive Program (DEIP) and use budget savings to enhance the safety net for producers.

16 in favor, 0 opposed, 1 abstaining

52

7

STRONGLY CONSIDER THE ELIMINATION OF END PRODUCT PRICING. Explore alternative measures to the current end product pricing system, such as competitive pricing and mandatory price reporting.

17 in favor, 0 opposed, 0 abstaining

53

7

NUMBER RECOMMENDATION PAGE

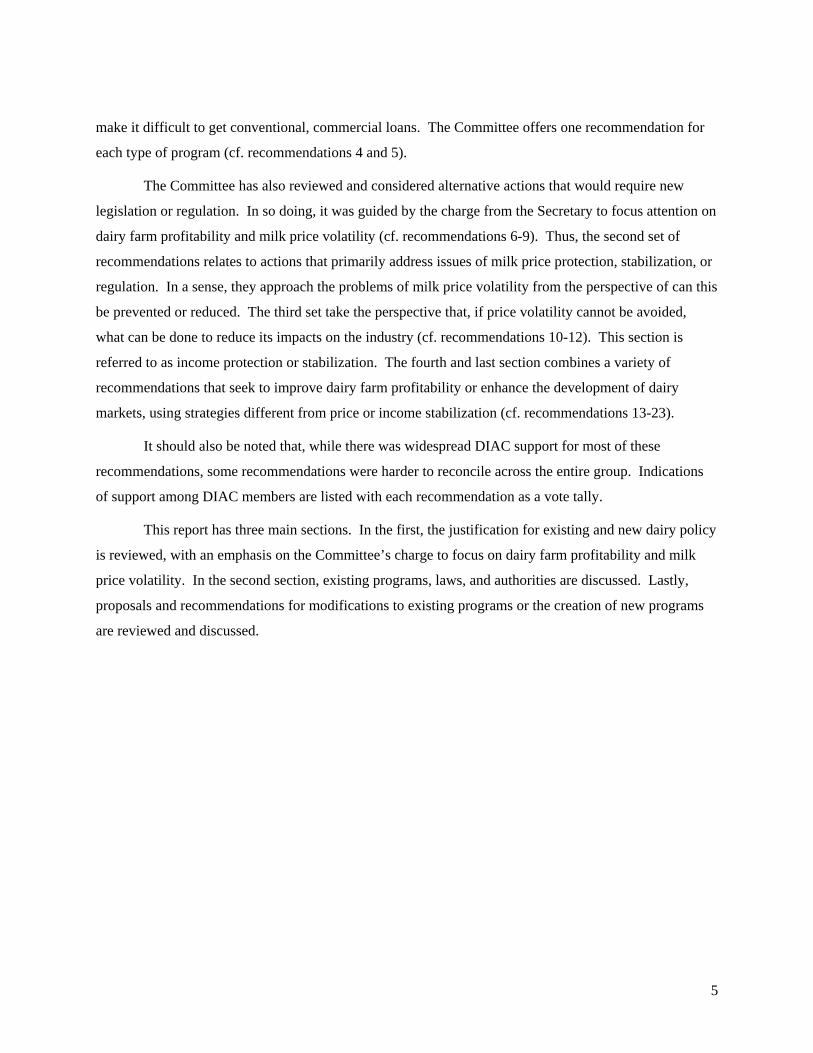

8

COLLECT AND PUBLISH PRICE DATA. Collect and publish data on alternative measures of a competitive pay price, considering but not limited to the proposals of the National Milk Producer Federation and Maine Dairy Industry Association.

15 in favor, 2 opposed, 0 abstaining

54

9

ADOPT A GROWTH MANAGEMENT PROGRAM. The Federal Government should adopt a growth management program that allows new producers to enter and allows producers to expand production.

9 in favor, 8 opposed, 0 abstaining

54

INCOME PROTECTION AND STABILIZATION

10

ESTABLISH RISK MANAGEMENT MARGIN LINES OF CREDIT. USDA should develop a credit mechanism (direct lending or credit guarantee) for first buyers of milk (cooperative or proprietary) to cover the margin deposits required on contracts for risk management between first buyers and producers of raw milk.

17 in favor, 0 opposed, 0 abstaining

58

11

MODIFY MILK INCOME LOSS CONTRACT (MILC) PROGRAM AND PROVIDE A MARGIN INSURANCE OPTION using funds from the elimination of the DPPSP and DEIP. Continue MILC, with a production cap based on available funds, with two important modifications: (1) use an all-milk income/feed cost margin trigger, and (2) provide an insurance program for production excluded by the cap to provide protection for larger producers.

15 in favor, 2 opposed, 0 abstaining

60

12

ADOPT TAX-DEFERRED FARM SAVINGS ACCOUNTS. Federal tax law should be amended to allow dairy farm operators to create special tax-deferred savings accounts. These accounts should not be subject to matching Government contributions and should not have a limit on dollars deferred per year. To be eligible, contributions must remain in the account for a minimum of 6 months; the account-holder can withdraw their funds at their own discretion thereafter. Payment of income taxes on contributions and interest would occur in the tax year in which the funds are withdrawn.

17 in favor, 0 opposed, 0 abstaining

63

PROFITABILITY AND MARKET IMPROVEMENT

13

SUPPORT COMPETITIVE MARKET STRUCTURES. USDA, through its regulatory authority and in cooperation with the Federal Trade Commission (FTC) and Department of Justice (DOJ), should continue to monitor and support competitive marketing structures throughout the supply and marketing chain of the dairy industry.

17 in favor, 0 opposed, 0 abstaining

66

14

MAINTAIN AND EXPAND PROGRAMS FOR EXPORT MARKET DEVELOPMENT. Continue and expand programs like the Market Access Program (MAP) and the Foreign Market Development Program (FMDP).

17 in favor, 0 opposed, 0 abstaining

67

8

NUMBER RECOMMENDATION PAGE

15

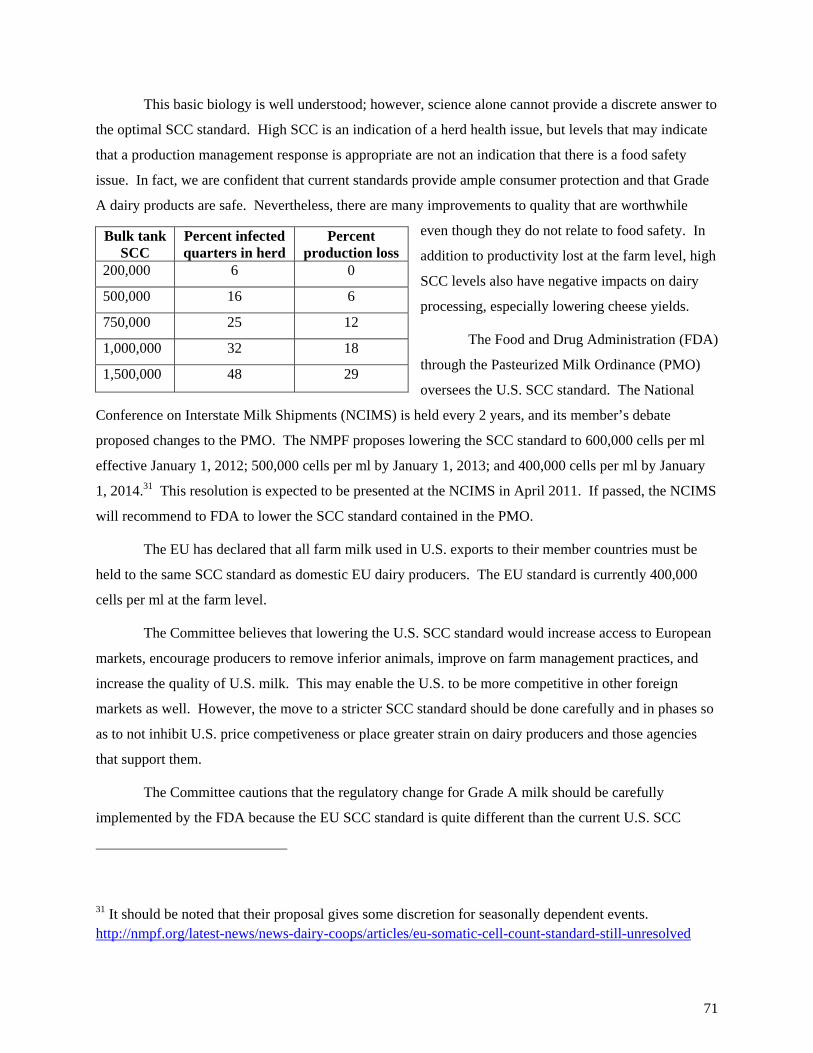

SUPPORT REDUCTION OF SOMATIC CELL COUNT STANDARD. Recommend that the Secretary support the adoption of a maximum somatic cell count of Grade A milk in the amount of 400,000 cells per milliliter at the farm level at the Interstate Milk Shippers Conference. The implementation should occur over a period of time not to exceed 48 months.

17 in favor, 0 opposed, 0 abstaining

70

16

ENHANCED FLUID MILK SOLIDS STANDARDS. Encourage the Secretary to explore the impacts of California-type fortification standards for U.S. beverage milk.

17 in favor, 0 opposed, 0 abstaining

72

17

RESTRICT USE OF DAIRY DESCRIPTORS ON PRODUCT LABELS. Recommend that USDA support restriction of dairy descriptors, including terms such as milk, cheese, yogurt, butter, for use on products made from milk.

17 in favor, 0 opposed, 0 abstaining

75

18

SUPPORT FOR VALUE-ADDED DAIRY. The Secretary should support programs that enhance value-added market development for dairy farms and dairy products. Opportunities include, but are not limited to, the development of educational training programs and technical assistance for farms, inspectors, and regulatory personnel to accommodate unique value-added dairy farm operations. A study should be made to examine the impact of user fees on value-added dairy product operations.

15 in favor, 0 opposed, 2 abstaining

77

19

PROVIDE INCENTIVE PAYMENTS FOR ENVIRONMENTAL PRACTICES. The Secretary should increase the amount of money available for incentive payments to dairy farmers for environmental practices that address social, economic, and environmental benefits to dairy farm communities.

16 in favor, 1 opposed, 0 abstaining

78

20

CONTINUE THE ENVIRONMENTAL QUALITY INCENTIVES PROGRAM (EQIP) AND GRANT PROGRAMS. Continue EQIP and give dairy farmers preference in grant programs for implementation of energy audits, infrastructure development for value-added processing and distribution facilities, construction of facilities to meet food safety regulations and farmland protection, and to allow beginning farmer loans for farm transfers between generations.

15 in favor, 1 opposed, 1 abstaining

80

21 PHASE OUT ETHANOL SUBSIDIES. Support the rapid phase out of the blender’s credit and tariff on imported ethanol.

16 in favor, 1 opposed, 0 abstaining82

22 DAIRY HERD HEALTH. Create a program to rapidly eradicate bovine tuberculosis (TB) and Johne's from the U.S. dairy herd.

17 in favor, 0 opposed, 0 abstaining84

23

DAIRY LABOR. The Secretary should use his influence with other agencies and Congress to provide a legal means for dairy farms to employ year-around long-term immigrant labor. Provide assurance that existing farm laborers have the opportunity to obtain permanent resident status.

13 in favor, 1 opposed, 3 abstaining

87

9

Approving:

Signature on File ____________________________________ Paul Bourbeau

Signature on File ____________________________________ Andrew Novakovic

Signature on File ____________________________________ Jay Bryant

Signature on File ____________________________________ Randy Romanski

Signature on File ____________________________________ Erick Coolidge

Signature on File ____________________________________ Robert Schupper

Signature on File ____________________________________ Timothy den Dulk

Signature on File ____________________________________ Manuel Souza

Signature on File ____________________________________ Debora Erb

Signature on File ____________________________________ Patricia Stroup

Signature on File ____________________________________ James Goodman

Signature on File ____________________________________ Sue Taylor

Signature on File ____________________________________ James Krahn

Signature on File ____________________________________ Edward Welch

Signature on File ____________________________________ Edward Maltby

Signature on File ____________________________________ James Williams

Dissenting:

Signature on File

____________________________________

Robert Wills

10

Table of Contents

Foreword ......................................................................................................................................................... 1

Executive Summary ........................................................................................................................................ 3

Approving: ...................................................................................................................................................... 9

Dissenting: ...................................................................................................................................................... 9

Table of Contents ............................................................................................................................................ 10

Introduction ..................................................................................................................................................... 13

Milk Price Volatility ....................................................................................................................................... 13

Causes of Price Volatility in the Dairy Sector ........................................................................................ 14

Dairy Farm Profitability .................................................................................................................................. 17

Measures of Profitability ......................................................................................................................... 19

The Status of Dairy Farm Profitability .................................................................................................... 22

Current Legislative and Regulatory Authorities ............................................................................................. 24

The Office of Management and Budget (OMB) ..................................................................................... 25

Comments on Possible Unintended Consequences ................................................................................. 26

The Dairy Product Price Support Program (DPPSP) ...................................................................................... 26

Milk Income Loss Contract (MILC) Program ................................................................................................ 28

Federal Milk Marketing Orders (FMMOs) ..................................................................................................... 31

Dairy Export Incentive Program (DEIP) ........................................................................................................ 34

Risk Management Programs ........................................................................................................................... 35

Livestock Gross Margin (LGM)-Dairy ................................................................................................... 36

Adjusted Gross Revenue Lite (AGR Lite) .............................................................................................. 37

Use and Participation in LGM-Dairy and AGR-Lite .............................................................................. 37

Commodity Credit Corporation (CCC) Charter Act, Section 5 ...................................................................... 38

Domestic Food Assistance Programs .............................................................................................................. 40

International Food Assistance Programs ......................................................................................................... 42

11

Section 32, Public Law 74-320 ....................................................................................................................... 44

Farm Loan Programs (FLPs)........................................................................................................................... 45

Wisconsin FSA FLP Example ................................................................................................................ 46

Market News, Research, and Promotion Programs ........................................................................................ 49

Recommendation for the Use of Existing Programs in Times of Severe Economic Distress......................... 50

Concluding Comments About Existing Programs .......................................................................................... 51

New Programs, Legislation, and Regulation .................................................................................................. 52

Programs to Stabilize and Regulate Milk Prices ..................................................................................... 52

Dairy Product Price Support Program (DPPSP) and Dairy Export Incentive Program (DEIP) ........ 52

Federal Milk Marketing Orders (FMMOs) ........................................................................................ 53

Growth Management ......................................................................................................................... 54

Programs to Protect and Stabilize Farm Incomes ................................................................................... 58

Price and Income Risk Management ................................................................................................. 58

Modified MILC and Margin Insurance .............................................................................................. 60

Farm Savings Accounts ..................................................................................................................... 63

Programs to Improve Profitability and Dairy Markets .......................................................................... 66

Export Markets .................................................................................................................................. 67

Farm Milk Quality ............................................................................................................................. 70

Enhanced Fluid Milk Solids Standards .............................................................................................. 72

What are the regional disparities? ................................................................................................... 74

Dairy Management Practices and Production Costs – Value-Added Dairy Operations .................... 77

Dairy Management Practices and Production Costs – Environmental Practices ............................... 78

Promoting Dairy Farm Development – EQIP and Other Grants ....................................................... 80

Dairy Management Practices and Production Costs – Corn Based Ethanol Subsidies ...................... 82

Dairy Herd Health Programs ............................................................................................................. 84

Johne’s Disease ............................................................................................................................... 86

Dairy Labor ........................................................................................................................................ 87

Summary and Conclusions ............................................................................................................................. 90

12

Appendix A - Farm Financial Performance Measures .................................................................................... 92

Liquidity .................................................................................................................................................. 92

Solvency .................................................................................................................................................. 92

Profitability ............................................................................................................................................. 92

Repayment Capacity ............................................................................................................................... 93

Financial Efficiency ................................................................................................................................ 93

Appendix B – Summary Information About Existing Dairy Programs .......................................................... 94

13

Introduction

With the ink barely dry on the 2008 Food Conservation and Energy Act (FCEA or 2008 Farm

Bill), the U.S. economy descended into the worst recession since the Great Depression of the 1930s. The

dairy industry suffered a combination of recession-driven demand effects and more sector-specific supply

effects. Dairy exports, which had been a primary contributor to dairy farm prosperity in 2007 and 2008,

collapsed as global demand declined. Domestic demand, especially in foodservice, also shrank as

consumers trimmed household budgets. On the supply side, feed costs, the single largest expense of milk

production, hit record highs. This created the worst margin squeeze since the early 1970s and pushed

most dairy farm businesses into the red, eliminating years of growth in dairy farm balance sheets.

Although net income for dairy farmers improved in 2010, weakened balance sheets leave farmers

vulnerable to any near-term negative margins.

This report reviews current and possible new Federal laws and programs intended to assist dairy

farmers, and discusses their potential application and impacts in various market environments. Milk and

dairy product markets begin with industries that provide products and services to dairy farmers and end

with consumers of traditional dairy products and other products containing significant dairy ingredients.

This report will attempt to highlight significant implications and considerations along the entirety of the

supply chain, but its orientation is defined by the Secretary’s charge to focus on the twin issues of milk

price volatility and dairy farm profitability.

Milk Price Volatility

A Working Definition of Price Volatility

Since the collapse of prices in 2009, it is common to hear milk prices described as “volatile”. The

image this connotes is negative, but beyond that it is not a well-defined concept. Prices can be considered

to have three fundamental dynamic characteristics: certainty, stability, and adequacy.

Certainty means that a future price is predictable. The more confident a prediction is, in amount

and distance, the greater the price certainty. Certainty can be measured by the difference between the

future price one expects at a future time and the actual price that is realized.

Stability refers to how much price changes over time. This involves the frequency and size of

change. A price that never changes is stable and predictable, but otherwise the two concepts are

independent. For example, a highly seasonal price pattern might be quite predictable while still being

“unstable”. Stability can be measured statistically in several ways, involving either amplitude or

frequency. Adequacy is a more subjective assessment, but it concerns whether a price returns positive net

revenue to the seller.

14

With this in mind, the Committee used the following description of volatility to consider and

evaluate policy solutions to the problem of volatility:

Prices that are volatile over time are unpredictable, unstable, and at least occasionally, inadequate.

This, of course, does not preclude the possibility of prices being very advantageous to a seller at other

times.

Causes of Price Volatility in the Dairy Sector

Before the Agricultural Act of 1949 established the Dairy Price Support Program (DPSP), farm

milk prices exhibited a high degree of instability. The relative spread from high to low was generally as

great as or greater than the dispersion in milk prices known today. The frequency was quite different as

the earlier fluctuations were entirely seasonal, whereas today one or more cyclical components

overwhelm a seasonal component. This instability had its effects, but these fluctuations were primarily

seasonal and generally predictable.

From 1950 to 1989, milk price variability was considerably dampened compared to the first half

of the 20th century. During the 1970s, the primary price mover was inflation, which affected the entire

U.S. economy. To offset surpluses generated by aggressive support price policies of the late 1970s, from

1981 to 1990, dairy markets were affected by a variety of significant Government programs, including

large product purchases and two new, temporary supply management programs. Beginning in 1983, the

support price for milk used in manufacturing was gradually reduced from over $13.00 per cwt to under

$10.00, where it has more or less remained. Government purchases have been infrequent at this low level

of support. While there clearly were price issues in the 1970s and 1980s, volatility, as defined in this

report, would probably not be the word used to describe them.

Since 1990, the farm milk price has become highly variable and unpredictable. The causes of this

increased volatility are debatable, but likely involve policy or regulatory issues and economic factors. As

a policy matter, the reduction of the Federal support price for milk during the 1980s may have revealed an

underlying susceptibility to volatility.

Price volatility in the last decade also corresponds to significant changes in administration of

Federal dairy programs. The base price for FMMO formulas was changed from a competitive pay price

survey of prices paid to a subset of dairy farmers producing unregulated milk (the Minnesota-Wisconsin

[M-W] price and then the so-called Basic Formula Price [BFP]) to class prices derived from the wholesale

prices of four dairy commodities (product price formulas or end product pricing). This change had the

effect of directly tying farm price volatility to the volatility of wholesale prices for dairy commodities,

15

which had always been more volatile than the previous competitive pay price series for milk. The switch

to a product formula price occurred in 2000.

Another significant policy event that seems to have changed dairy markets was the conclusion of

the Uruguay Round negotiations under the General Agreement on Tariffs and Trade, now referred to as

the World Trade Organization (WTO). In the U.S., the Uruguay Round Agreements Act was passed

in 1994. Under the Agreement on Agriculture (AoA), the U.S. and other developed countries agreed to

provide access to its dairy markets by foreign competitors equal to about 5 percent of total U.S. sales with

relatively low levels of tariff protection (this roughly doubled U.S. imports from about 2.5 percent to

5 percent of sales). Above this level, the U.S. replaced its strict import quota system with a tariff-based

system that generally provides a high degree of protection for most dairy commodities but greater access

to value added products, such as European-style cheeses. In exchange for increasing access to foreign

marketers, the U.S. dairy industry gained greater access to foreign markets. Increased trade subjected

U.S. dairy markets to the effects of changes in world supply and demand conditions, including weather,

political shocks, and foreign food safety issues. This increased trade opportunity may also have

contributed to increased price instability.

The somewhat unusual position of the U.S. among world dairy product traders may be a

compounding factor. The U.S. is among the largest producers of milk and milk products in the world. Its

cost structure puts it in the rather unusual position of being either a potential net importer or net exporter.

U.S. buyers tend to import high-value cheeses and other specialized products and sell low-value

commodities, especially dry powders. As such, the U.S. has tended to be a net importer on a dollar value

basis since the WTO, but on a milk equivalent basis it has often been a net exporter. This has been

increasingly true in the last several years. Periods of net export have been the result of a combination of

factors, including strong world demand, weak supplies by more consistent exporters, and favorable

exchange rates. While the U.S. is hardly unique in being susceptible to swings in world markets, its

vacillation between being a net importer or net exporter is unusual and perhaps puts it in a more volatile

position.

Another policy element that may contribute to persistence in dairy farming and milk production,

despite economic stress on farms, is the pooling of returns under FMMOs and State milk marketing

orders. Marketwide pools, which have been the norm for milk pricing for the last century or so, represent

a system of average pricing whereby processors pay a much different price for milk than the individual

price that farmers receive. This is because processors pay minimum regulated classified prices based on

their product sector, whereas dairy farmers receive a weighted average of the various classified prices,

regardless of the products that are made from their own milk. While useful in ensuring that farmers do

16

not destructively compete2 with one another for the highest valued market, pooling mutes price signals

that would otherwise discourage production from individual producers or suppliers facing a down market

or subsector.

Although not a matter of public policy per se, a related element is that the vast majority of the

milk marketed in the U.S. is marketed via cooperatives, and the cooperative business model has long been

to accept responsibility to market whatever volume of milk a producer chooses or is able to produce.3 In

periods of stress, when markets are long, there is essentially no marketing risk for a producer, in the sense

that every pound of milk produced will be purchased. Cooperatives cannot simultaneously agree to

market every pound of milk and guarantee a favorable price. Prices must be able to adjust to clear the

market. Pooling, combined with the essentially unlimited cooperative guarantee to purchase all milk

produced, is likely to exacerbate price volatility because those practices tend to delay production

adjustments when prices are low. When the DPSP was more aggressively used, it essentially guaranteed

a Government outlet for surplus dairy commodities and many cooperatives invested in producing these

sorts of products, especially nonfat dry milk (NDM) and butter (which also happen to be highly tradable

products in world markets). This also helps to explain the relatively open-ended purchasing agreements

cooperatives have had with their members. This marketing and pricing system has been in place for about

a century; so modern price volatility cannot be blamed on pooling and market security, but those two

elements likely confound the ability of the marketplace to react to volatility caused by other factors.

In terms of the internal economics of the sector, dairy analysts have described dairy markets as

having low price elasticities of supply and demand for farm level milk, and inelastic price elasticity of

demand for many dairy products throughout the market chain. While analysts debate the degree of

elasticity, most agree that short-term elasticities are small. As such, small relative changes in quantities

are associated with relatively large changes in price. This has always been true for dairy markets, and

some have argued that it is less true today.

2 “Destructive” competition is a term used historically to describe competition between dairy farmers for high priced markets or buyers that results in lower average prices for all farmers. Competition between buyers and sellers can be difficult, but it is generally considered to be “constructive” provided the competitive conditions are fair and balanced.

3 Of course there are exceptions to this general rule. A few cooperatives have long operated a “closed membership”, to control growth by restricting entry. In recent years, it has become more common for cooperatives to institute short or longer-term restrictions on individual farm growth, especially when the cooperative is processing its member's milk directly.

17

Whatever its precise magnitude, supply and demand inelasticity in dairy markets means that the

reduction in price support exposes the industry to this kind of volatility more now than when the DPSP

was more important in establishing and constraining market prices. Product formula pricing may further

aggravate the volatility enhancing aspects of product supply and demand inelasticities. Because

wholesale dairy prices have always tended to be more volatile, product formula pricing tends to transmit

this wholesale volatility very quickly and completely. Volatile farm prices directly impact dairy farm

revenue, but this form of pricing tends to keep processor margins, and hence net revenue, less volatile.

Manufacturers have less margin risk as long as they produce those specific commodities or a product

whose price is highly correlated with one of them. The number of product classes, combined with

pooling, may also have an effect on milk price volatility. Demand factors can result in the wholesale

value of one product class rising dramatically, while another product class price rises more slowly or even

falls. The relative margin assurance under product formula pricing reduces the buyer’s incentives to

move farm milk from lower valued to higher valued uses and pooling tends to dilute the seller’s

incentives. The exact magnitude and importance of these possible effects is not known, but the

Committee believes these are issues that warrant more in depth analysis.

One reason for the low degree of milk supply elasticity is that dairy farming is a production

activity that is characterized by a high degree of asset fixity. An operating farm will endure a great deal

of short term stress (negative cash flow) as long as the operator believes that the farm will be profitable in

the long term and sufficient credit or reserves exist to get through the negative period. Moreover, the

generally high degree of fixed costs and the fact that cows are not machines that can be simply turned off

means that it generally makes sense in the short term to produce at full capacity. Thus, in periods of low

or negative margins, farmers will continue to produce until they decide to discontinue their business or

their access to credit is eliminated.

Dairy Farm Profitability

In addition to swings in milk price, dairy farmers have experienced significant changes in prices

of feed and other production inputs. Feed is the single largest milk production cost component

(40-50 percent). Thus, dairy farmers are especially sensitive to the prices of purchased feeds or to the

prices of inputs used in homegrown feed production. Key feedstuffs include corn, soybean meal, and

alfalfa hay. Other important production inputs are energy and labor and—for those who grow their own

feed—fuel, fertilizer and seed.

From Fall 2006 through Summer 2008, the price of corn increased from about $2.00 to about

$5.50 per bushel. The increase in soybean prices was equally dramatic. Among the causes of feed price

18

increases was expanded bio-fuel production which created a large and new demand for corn and

contributed to the price increase for soybeans and other crops. Weather and international grain demand

also contributed to high feed costs.

Milk prices were

moving to a cyclical low in

2006 even as feed prices were

beginning to increase. As a

result of the high feed costs that

in turn led to decreased milk

supply, the price of milk rose

from a low of $11.70 per cwt in

July 2006 to a high of $21.90 in

November 2007—the all time

record high for the nominal

price of milk. By the end of

2008 and through 2009, farm profitability began to decline dramatically. Although corn prices and other

input costs softened from their highs, milk prices fell even more. The problem in 2009 was not just the

low price of milk, which was no lower than the levels of the previous two cycles; it was extremely low to

negative margins. In many months, the milk check barely covered the cost of feed. This is illustrated in

the accompanying chart.4

Clearly, the low point in milk margin over feed costs ($/cwt) during 2009 is far lower than the

previous troughs in 2006 and 2002, although milk prices were approximately the same in the 3 years. The

distinction between prices and margins is important. Prices influence margins and financial outcomes,

but output price alone does not determine farmers’ well-being. Most dairy and other agricultural support

programs are based on or triggered by an output price, such as milk price. The usefulness of that simple

approach has been seriously challenged by the events of the last 2 years and is a concern looking forward.

4 This chart uses a margin methodology developed by the National Milk Producers Federation (NMPF), in its Foundation for the Future proposal, combined with USDA price data. There are several ways to measure margins or other indicators of the relationship between the price of milk and the prices or costs of feed, or farm returns, more generally. The methodology proposed by NMPF is reasonable; however, in using it in this paper, the Committee does not imply a formal endorsement of their methodology.

19

The experience of 2009 has sensitized industry members and analysts that a milk price that looks

good, or even high, by purely historical comparisons can easily be inadequate when input prices are high.

This has caused much attention to be focused on alternative measures of profitability in dairy farming.

The need for this is accentuated by a general feeling that grain prices have likely shifted to a new average

level and that recent “highs” may prove to represent a new “normal”.

Measures of Profitability

Recommendation 1:

DEVELOP A SYSTEM THAT PROVIDES AN ACCURATE ASSESSMENT OF DAIRY

FARM PROFITABILITY. A data gathering and reporting system should be developed that

expresses farm profitability in the dairy industry using an index to provide an impartial

overview of the general level of profitability at the farm level based on the milk price-feed

cost margin.

There is no single best way to describe or measure dairy farm profitability. Various concepts are

used, and each can lead to rather different perspectives on “profitability” of dairy farmers.

Two observations reveal a basic conundrum about the apparently simple concept of profitability.

In 1975, USDA estimates that 443,610 “operations” reported having milk cows and total milk production

that year was 115,398 million pounds. In 2009, USDA estimates that there were 65,000 operations

having dairy cows and annual production was 189,320 million pounds. Thus, the number of operations

declined 85 percent while production increased 64 percent.

It is tempting to use the data on number of dairy operations as evidence that there must be a long-

term problem with dairy farm profitability. Even from year to year, it is common to describe poor

profitability across the sector as the cause for dairy farms going out of business. On the other hand, if one

looks at the growth in milk production, it is just as logical to say that dairy farming must have been

profitable to support that level of growth over so many years.

Data on farm numbers and prices are simple facts about the U.S. dairy sector. Interpreting these

facts and translating their meaning for questions like “are dairy farms profitable” or “is dairy farm

profitability a long term problem” is less straightforward. Perhaps the simplest conclusion that can be

made from these data is the following: Farm milk prices have not kept pace with consumer price

20

inflation5, but apparently the lower rate of increase in farm milk prices has been adequate to support an

impressive long-term increase in milk production. However, it is equally clear that many farm operators

have found the increase in price to be “inadequate”. The decline in numbers of farm operations that milk

cows is testimony that these farmers have found better places to invest their equity, labor, and

management skills, and/or that farmers reached normal retirement decisions and those farms were

consolidated rather than passed on to a new generation. By the same token, the increase in milk

production means that there is a group of farmers who have found profits to be sufficient to justify

continuing and even expanding.

If nothing else, this simple exercise reveals the difficulty in using averages to explain complex

economic factors and outcomes related to dairy farming. Factors of a more social nature, or related to

personal values, are part of this complexity as well.

Whether looking at an average or results for a specific farm, another question is how one ought to

measure profitability. Operators use different criteria to measure profit depending on their goals, size,

business structure, location, etc. High prices do not ensure high farm level profitability, and prices that

are more modest do not condemn farms to a lack of profitability. It is the relationship between cash

revenue and cash costs that keeps farms in business in the short term (liquidity), and measures such as the

return on equity (ROE) or net farm income (NFI) that define the long-term profitability of the farm

operation. There are many different production practices and, as with many small businesses, plenty of

entrepreneurial initiative and innovation that make a single standard for farm profitability difficult to

define. Some farms may be unprofitable in the long term, even though they have positive cash flow from

most years to the next. Other farm families may be eligible for public assistance for health insurance and

food stamps, but still see dairy farming as the best place to invest their equity and labor. Commercial

lenders typically have their own preferred measures and benchmarks when assessing the profitability and

5 The U.S. average price paid for all milk went from $8.78 per cwt in 1975 to $12.83 per cwt in 2009. Given the instability of prices in both periods, as opposed to the steady trend in milk production and the number of farms, a better indication of trend is to consider the average prices in the early 1970s vs. the late 2000s. These values are approximately $8 per cwt. and $15, respectively. This is an increase of 88 percent. Over those same time periods, the Consumer Price Index for all goods increased from about 50 to 196, according to the Bureau of Labor Statistics. If the average farm price had increased by the same percentage, it would have been over $31 per cwt in the 21st Century. The “nominal” price of milk increased 88 percent but the “real” price decreased over 50 percent.

21

repayment capacity of a farm borrower. The USDA and other Federal agencies may choose different

criteria (for example, USDA Rural Development uses tangible net-worth).

In response to the economic crisis experienced by much of the agricultural sector in the early

1980s, the American Bankers Association decided that there was a need to standardize how farm financial

performance is measured. This ultimately led to the creation of an independent organization called the

Farm Financial Standards Council (FFSC). The FFSC is a voluntary, not for profit organization that

seeks “to create and promote uniformity and integrity in financial reporting and analysis for agricultural

producers”. It currently endorses 21 specific measures of financial performance. Different groups of

measures are deemed to be alternative and useful indications of liquidity, solvency, profitability,

repayment capacity, and financial efficiency. A description of each is provided in Appendix A.

The Committee discussed numerous aspects of these questions and issues as it considered the

concept of dairy farm profitability, the status of dairy farm profitability currently, and alternative ways to

assist farmers in improving profitability. While we recognized that it is very appealing to have one “best”

measure that could be used to gauge farm profitability over time or to guide public policy actions, in the

end we concluded that no single measure is “best” for all purposes. Some measures are appealing

because they can be calculated or estimated without a lot of variables or data. They are simple. Other

measures are more appealing conceptually, but they are complex and difficult to calculate.

Recognizing that there are appropriate times and applications for different measures, we conclude

that a margin measure, such as the average, per cwt net return from the sale of milk less the cost of

purchasing feed to produce 100 pounds of milk – the milk margin over feed costs – is a simple but useful

measure of short term financial performance of dairy farm businesses.6 The milk margin over feed cost

does not account for other production cost components, such as labor, energy, depreciation, capital,

6 USDA has reported a ratio of the all milk price to an index of feed prices for decades. The milk-feed price ratio is the pounds of 16 percent protein mixed dairy feed equal in value to 1 pound of whole milk. The higher the ratio, the more feed a dairy producer could buy with proceeds from the sale of a pound of milk. Reported monthly by USDA, feed prices used in the ratio are based on current U.S. prices received for corn, soybeans, and alfalfa hay. The milk: feed price ratio has been a familiar and easy tool for indicating net returns to dairying: however some recent research has highlighted that in times of great volatility this measurement is not accurate (Understanding the milk-to-feed price ratio as a proxy for dairy farm profitability: CA Wolf October 2010, Journal of Dairy Science.). While conceptually related, a composite index of prices of feed is not the same as the average cost of the same feeds used to produce 100 pounds of milk. The first is simply a ratio of prices; the second results in a margin per cwt of milk produced.

22

veterinary services, and nutritional supplements. These costs vary greatly across individual operations,

either by region or the structure of the farm business. These other costs are probably not as volatile as

feed costs; hence, the milk margin over feed cost remains a fairly reasonable short-term indicator of farm

financial performance. However, individual producers will need to take into account their own

circumstances when evaluating how well this simple national measure represents their financial status.

Later in the report, we recommend the use of milk margin over feed costs for policy purposes, but

it should be understood that we do not think it is the “best” measure of profitability. As a type of cash

flow measure, it falls in the financial category FFSC describes as a measure of liquidity. Alternatively,

NFI is an appealing measurement of profitability and can be especially useful in comparing the

profitability of different dairy farms. ROE, another measure of profitability endorsed by FFSC, is a

helpful measurement when comparing profitability in dairy to other agricultural or even non-agricultural

businesses.

The Status of Dairy Farm Profitability

The impact on business equity and liquidity for farmers in 2009 was at an unprecedented level

that will need many months, if not years, of higher net returns to remedy. Those dairy farms that are

under most pressure are farms that:

must purchase feed have highly leveraged assets rely heavily on cash flow from the farm business for household income.

Economists at the USDA, Economic Research Service (ERS) estimate returns and costs of

production on dairy farms across the U.S. 7 Their reports estimate total returns to the dairy operation,

including milk sales, sales of cull cows and calves, and income from other sources that pertain to the dairy

operation or can be allocated in part to the dairy enterprise. Operating costs included cash expenses for

variable and fixed inputs in the dairy operation. Costs for hired labor, family labor, depreciation, taxes

and insurance and general farm overhead are estimated and allocated to the dairy enterprise. From these

basic data and estimates, it is possible to calculate measures such as NFI. The accompanying chart

illustrates net returns over total cost or operating costs. The patterns of both measures are very similar;

however, there is a significant distance between the two. This illustrates that non-cash average costs are

significant but much less variable than cash costs and income. 7 USDA ERS: Commodity Costs and Returns Data, Dairy. http://www.ers.usda.gov/data/costsandreturns/testpick.htm#milkproduction

23

The dairy industry is very diverse in production practices, location, capital investment, overhead

costs, and

expectations.

Estimated

averages

certainly do not

describe every

farm situation,

some of which

are much worse,

some much

better, and many

of which follow

a somewhat

different pattern

over time.

Nevertheless, these estimates bear witness to the severe economic challenge experienced across the dairy

sector in 2009. Perhaps even more importantly for long-term policy, the chart also indicates that dairy

farms experience a considerable amount of margin volatility.

-10

-8

-6

-4

-2

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

$/cw

t

US Dairy Returns Over Costs, Operating vs Total Costs

Dairy Returns less Total Costs Dairy Returns less Operating Costs

24

Current Legislative and Regulatory Authorities8

Dairy programs are legal authorizations or mandates specified by Congress and implemented as

regulations by the USDA or another executive agency of the Federal Government. Some of these

programs exist under permanent law while others are temporary. Temporary programs may exist for

many years, but periodically Congress needs to reaffirm them. The so-called Farm Bill is “omnibus”

legislation that mostly codifies changes to laws and programs that exist in other statutes. Therefore, it is

usually a bill of amendments to existing law. Underlying laws, such as the Agricultural Adjustment Act

of 1933, the Agricultural Marketing Agreement Act of 1937 (AMAA of 1937), and the Agricultural Act

of 1949, contain the original authorizations for basic dairy programs. This chapter of the report focuses

on existing laws and programs and attempts to suggest how the existing programs might best be used in

those cases where the Secretary has some discretion and flexibility. It is also an objective to better inform

the dairy community about existing laws and the opportunities and limits that the Secretary faces in

working within existing statutes and regulations.

Congress has latitude in how strongly it directs an action of the Executive Branch. In many

cases, a law authorizes USDA or another agency to do something, but it does not require or even enable

that action. For example, under the old parity-based DPSP, USDA could announce a support price for

milk that was no less than 75 percent of the parity price but no more than 90 percent. Thus, USDA was

authorized to choose within a range. Sometimes USDA is permitted to do nothing at all. For example,

USDA is not required to implement a FMMO simply at the request of farmers or another market

participant. The Secretary has the authority to deny a request for a new Order or even suspend or

discontinue an existing Order. Lastly, Congress may give the Secretary authority to act, but not provide

necessary funding, so as a result, the policy is not implemented.

Current programs have direct effects on milk prices, dairy product sales, farm incomes, and other

direct aspects of dairy profitability and volatility. Many programs exist outside of USDA authority that

affect dairy markets, including tax policy, public borrowing, transportation, energy, environment, labor

policy, and food regulations. The primary focus in this report will be on dairy-specific programs that

could reasonably impact farm level dairy markets. Where a recommendation is made for an action not

under the direct purview of the Secretary, the Committee encourages the Secretary to exert influence and

resources at his disposal to encourage the appropriate agency or agencies to adopt the recommended

8 A tabular summary of the objectives and legislative authorities for major dairy programs is provided in Appendix B.

25

action. Where there are specific recommendations related to the operation of an existing program (as

opposed to creating new legislation to modify an existing program), that recommendation is made at the

beginning of each program section. A concluding recommendation is offered that spans several

programs.

The Committee offers its recommendations with awareness that the President’s Office of

Management and Budget (OMB) may constrain executive discretion and, therefore, policy

implementations. The Committee also acknowledges the risk of undesired and/or unanticipated

consequences of any policy choice. Individually and collectively, members of the Committee considered

the consequences of each recommendation along the dairy supply chain.

The Office of Management and Budget (OMB)

The Secretary may only initiate and operate programs 1) which he is authorized to administer and

2) which have a well-defined mandatory or discretionary source of funding. If a program is mandatory,

Congress provides authority to spend whatever money is required to achieve the purposes of that act. If

the program is discretionary, Congress may or may not provide funding to support the program. When

funding is limited, which is often, the OMB plays a crucial role in determining which programs may be

implemented.

OMB implements and enforces Presidential policy Government-wide through “budget

development and execution, agency management, coordination and review of all significant Federal

regulations by executive agencies, review, and clearance of all agency communications with Congress,

and executive orders and Presidential memoranda”.9

OMB has significant influence on the spending ability of any Federal agency, including USDA.

When Congress provides a clear mandate and sufficient funding to conduct a program, OMB’s primary

concern is the efficient execution of the required program. However, when an authorized program is

unfunded or underfunded, USDA must work with OMB to determine where funding might be available or

even whether any such funding can be found. Inasmuch as OMB reports to the President, OMB’s

priorities, both programmatically and from the standpoint of financial stewardship, are driven by the

President’s overarching priorities. In periods when budgets are tight, OMB toes a strict line on

discretionary spending. Even when budgets are not unusually stressed, OMB will and must evaluate

tradeoffs when an Executive agency, like USDA, makes a request.

9 http://www.whitehouse.gov/omb/organization_mission/

26

Comments on Possible Unintended Consequences

One of the challenges in any public policy is that few choices make everyone better off. Policies

involve tradeoffs. In the dairy sector, tradeoffs exist among producers and among dairy processors,

retailers, consumers, taxpayers, and alternate agricultural and food sectors. We recognize that policies

that are good for some dairy farmers may not be good for all dairy farmers. This is evident in the ongoing

public debates related to varying farm size, business models, and regions of the U.S.

While we have not been charged to address business or individual issues that derive primarily

beyond the farm sector, we cannot look at farm level policy solutions without considering their possible

downstream effects over time.

We also recognize that the Secretary has a responsibility to balance and represent a public interest

in the administration of USDA programs and acknowledge that this is a difficult task. The purpose of the

policies discussed here is to counter extreme market conditions, not to eliminate fundamental market

functions.

The Dairy Product Price Support Program (DPPSP)

Recommendation Note:

At the conclusion of the chapter on existing laws and programs, we offer a recommendation

that relates to the Secretary’s use of the DPPSP. We also make a recommendation

concerning legislative changes that impact the DPPSP.

The DPSP was authorized under the Agricultural Act of 1949 and has been reauthorized by

subsequent Farm Bills. The Agricultural Act of 1949 gave the Secretary discretion to establish a support

price that would cover 75-90 percent of “parity” (a measure of farmers’ purchasing power in comparison

to a base period in the early 20th century). Since 1981, Congress has suspended the requirement that the

Secretary establish support prices according to a parity price benchmark.

FCEA also altered the purchase price targets, replacing a “support price” for milk with “purchase

prices” for commodity cheddar cheese, butter, and NDM. This altered program was titled the DPPSP.

Purchase prices, specified in law by FCEA or announced by USDA prior to 2008, did not change

significantly and are listed in the following table.

27

Price Before FCEA After FCEA Support Price for Milk Used in Manufacturing, average fat test (per cwt)

$9.90 not specified

Purchase Price for Cheddar Cheese, blocks (per pound) $1.1314 $1.13 Purchase Price for Cheddar Cheese, barrels (per pound) $1.1014 $1.10 Purchase Price for Butter (per pound) $1.05 $1.05 Purchase Price for NDM (per pound) $0.80 $0.80

Dairy product manufacturers initiate the process of moving surplus product off the market to

Government storage. USDA is obliged to buy any and all quantities of eligible product offered at the

announced purchase prices. Typically, any such product so acquired will either be sold back into

commercial markets at the statutory sellback price or will be made available for use in an international

food assistance program (for example, under Sec. 416(b) or one of the domestic programs, such as The

Emergency Food Assistance Program (TEFAP) or School Lunch).

To the extent that manufacturers take advantage of this guaranteed price, wholesale market prices

should not fall below the Government offer price, or at least not by very much. In practice, sellers show

some reluctance to sell cheese and butter to the Government. USDA issues standards for product

purchases that do not match the standards required by commercial buyers and payment terms are outside

of industry norms. Many manufacturers refer to a “cost of selling” to the Federal Government, with

estimates of that cost in the neighborhood of 3-5 cents per pound of product. In January 2009, wholesale

cheddar cheese prices were 6 to 7 cents per pound less than the USDA purchase price for 3 weeks without

generating sales to the Commodity Credit Corporation (CCC). As an approximation, a 1-cent per pound

change in the price of cheese equates to a change of about 10 cents per cwt of milk. USDA has reasons

for each of these rules and requirements. Nevertheless, the Committee believes that USDA should

carefully examine its requirements in an effort to make program changes that minimize reluctance to

participate.

The USDA purchase prices assure manufacturers of listed commodities that they will have a

market for those products at those prices. Also, market prices of these products are the foundation for

class prices in FMMOs,10 so the effect of Government purchases is widespread. Some analysts suggest

10 The California Stabilization and Marketing Plan for Market Milk does not use the same classification and pricing scheme as FMMO, but they are similar. California, which represents over one-fourth of U.S. milk production, also has regulated minimum class prices that are determined by wholesale product price formulas.

28

that dairy price supports have resulted in too many resources being directed toward production of the

targeted commodities compared to other products that might have better or broader commercial market

opportunities. If this causes a distortion that leads to inefficient allocation of resources in dairy markets,

returns to farmers will eventually be reduced.

Although Congress specified a support price for milk that “shall be” fixed at a given level from

1981 to 2008, the FCEA mandated commodity purchase prices for cheese, butter, and non-fat dry milk

specifying that the purchase prices “shall be no less than” proscribed levels specified in the statute. While

this language gives the Secretary the authority to raise one or more of the three commodity purchase

prices, the Secretary's ability to do so is subject to the approval of the OMB.

USDA used this discretionary authority to increase the purchase prices for cheddar cheese and

NDM in August, September, and October 2009. Compared to the purchase prices listed in the previous

table, the Secretary increased the purchase price of cheddar cheese by 18 cents per pound (16 percent) and

NDM by 12 cents per pound (15 percent). This action resulted in little dairy support program purchases

of NDM or cheese by the CCC, as product prices increased over the same period. In November 2009,

purchase prices for cheddar cheese and NDM under the DPPSP reverted to the levels specified in the

FCEA. The Secretary’s authority to make changes in the DPPSP support prices is limited by available

funding as detailed in the previous discussion regarding the OMB.

Milk Income Loss Contract (MILC) Program

Recommendation Note:

In the chapter on alternative laws and programs, we offer a recommendation concerning

legislative changes that impact the MILC.

The MILC program provides a form of countercyclical income support that draws some elements

from the structure of the (discontinued) Northeast Dairy Compact and the ongoing countercyclical price

(CCP) subsidies established for program crops (food and feed grains, etc.) in the Farm Security Act

of 2002.

29

The Northeast Dairy Compact was a Congressionally sanctioned agreement between the 6 New

England states to coordinate a minimum price for Class I milk marketed in their jurisdiction. When

Congressional approval for this multi-State Compact expired, the calculation methodology was adapted to

a countercyclical income subsidy that would apply to all dairy farmers in the contiguous U.S. As such,

there are three key variables that determine payments to farmers: the price trigger, the payment rate, and

the marketings payment limit.

Following the methodology of the Northeast Dairy Compact, the Northeast FMMO, Boston city

zone Class I price serves as the price trigger. When the actual Boston Class I price falls below $16.94 per

cwt, the MILC program becomes active. In the FCEA, Congress modified the trigger price to include an

automatic adjustment for changes in the prices farmers pay for certain feeds used in a dairy ration.

USDA’s National Agricultural Statistics Service (NASS) calculates the national dairy ration cost each

month. When the monthly ration cost exceeds $7.35 per cwt, the trigger price is increased by 45 percent

of the difference between the ration-cost trigger and the estimated actual U.S. average cost. For example,

if the dairy ration cost is estimated to be 10 percent above $7.35 per cwt, the milk payment trigger rises

4.5 percent (or $16.94 times 1.045 = $17.70). The FCEA increases the automatic feed adjustment trigger

cost from $7.35 to $9.50 per cwt beginning on September 1, 2012.

A payment rate was originally set at 45 percent of the difference between the announced monthly

price and the trigger, approximately the same percentage as the Class I utilization in the Northeast

FMMO. The FCEA reduces the MILC payment rate from 45 to 34 percent of the difference between the

announced monthly price and the trigger price beginning on September 1, 2012. There have been other

periods when the payment rate has varied. These changes are made by Congress as a way to achieve

budget targets, not because of conceptual or philosophical changes about the MILC program.

Lastly, the MILC program limits on how much an individual farm operator can receive. The

concept of a payment limit is derived from countercyclical payment programs for other agricultural crops

and was not used in the old Compact. For major program crops, the CCP and other subsidies are

generally limited by a maximum dollar amount. In the case of the MILC program, the payment is limited

by the number of pounds of milk on which a subsidy payment can be received. Like the dollar limit, the

quantitative limit has two objectives. First, it limits Government exposure to budget costs. Second, it

targets limited budget dollars to provide greater assistance to smaller scale farmers, which Congress has

generally favored in the form of payment limitations and income eligibility rules for other agricultural

programs.

Through September 2012, dairy producers are eligible to receive payments on up to 2.985 million

pounds per FY. At the national average production per cow, this equates to a farm size of about 150

30

cows. Producers whose marketings exceed the cap can choose the month for which they want to start

receiving payments. Marketings prior to that month do not count toward the limit even if the MILC

program is active. From that month, they receive payments for all months in which the program is active

until they reach their limit. The calculation starts over at the beginning of a new FY. This means that

smaller farmers will receive a greater proportional benefit relative to their gross income than will a very

large farm.

Many large-scale producers for which the eligible volume represents a very small portion of their

total production or gross income have criticized the program as being unfair to them. Also, many

producers and analysts believe that the price of milk remains at lower levels for longer periods when

MILC payments are triggered. The economic logic for this begins with the recognition that low prices are

the result of excess supply. Normally, low prices tend to stimulate consumption and discourage

production, thereby bringing supply and demand back into balance. When producers receive a Federal

price supplement, the self-correcting mechanism of the market is necessarily thwarted. This tends to

lessen the supply response and put more burdens on the demand side to correct the imbalance. This leads

to questions about the extent to which retail prices reflect lower farm and wholesale prices, or how long it

takes to reflect a decline. If the demand side is slow to respond, or does not feel the full effect of the price

declines farther upstream, and the supply side is protected from low prices by a price subsidy, then it is

consistent that low prices would persist for a longer period. The extent to which this occurs is debated.

Regardless, payments and their volume limitations are the basis for both political support and criticism of

the MILC program.

The MILC program is administered by the USDA’s FSA and is a mandatory program over which

USDA has no discretionary authority. USDA does promulgate rules to interpret and enforce the program

as authorized by Congress. These rules define requirements for eligibility and compliance, but they do

not alter the fundamental parameters specified in legislation.

31

Federal Milk Marketing Orders (FMMOs)

Recommendation 2:

REVIEW FEDERAL MILK MARKETING ORDERS (FMMOs). The Secretary should

appoint a committee to review implications of FMMOs, including, but not limited to,