Embed Size (px)

Citation preview

Report of the

Comptroller and Auditor General of India

on

Compliance of Fiscal Responsibility

and Budget Management Act, 2003

for the year 2014-15

Union Government (Civil) Department of Economic Affairs

(Ministry of Finance)

Report No. 27 of 2016

i

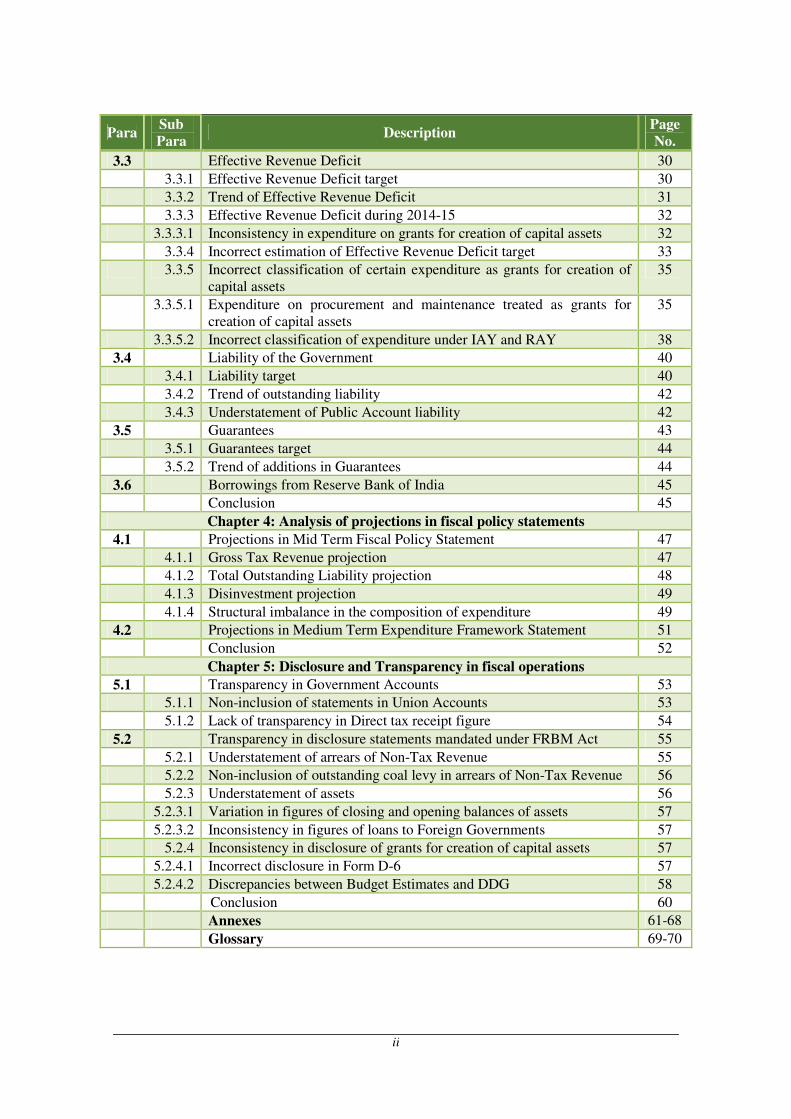

Para Sub

Para Description

Page

No.

Preface iii Executive Summary v-ix

Chapter 1: Introduction

1.1 Background 1

1.2 Fiscal Responsibility and Budget Management Act, 2003 and Rules 2004

1

1.3 Temporary hold of FRBM Act. 3 1.4 Introduction of renewed road-map under amended FRBM Act 4

1.5 Amended FRBM Act and obligations of the Union Government 5

1.6 Review of compliance of provisions of FRBM Act by the Comptroller and Auditor General of India (CAG)

6

1.7 Audit Objectives 7

1.8 Audit Scope and Methodology 7

1.9 Audit Criteria 8 1.10 Structure of the Report 9

Chapter 2: Deviation from the Act and Rules

2.1 Continuous deferment of targets 10

2.2 Non-adherence to annual reduction targets in 2014-15 10 2.3 Inconsistency in fiscal targets between MTFP Statement and FRBM

Act/Rules 12

2.4 Inconsistency in FRBM Act and Rules – on assumption of additional liabilities

14

2.5 Inconsistency in format of disclosure statement (D-6) 15 Conclusion 15

Chapter 3: Progress in achievement of FRBM targets

3.1 Revenue Deficit 16

3.1.1 Revenue Deficit target 16 3.1.2 Trend of Revenue Deficit 17

3.1.3 Revenue Deficit during 2014-15 18

3.2 Fiscal Deficit 18

3.2.1 Fiscal Deficit target 18

3.2.2 Trend of Fiscal Deficit 19

3.2.3 Fiscal Deficit during 2014-15 20

3.2.4 Revenue Deficit as a component of Fiscal Deficit 21 3.2.5 Transactions affecting the computation of deficit indicators 22

3.2.5.1 Understatement of Revenue Deficit due to misclassification of expenditure

22

3.2.5.2 Contraction of Revenue Deficit due to one-time receipts in 2014-15 23

3.2.5.3 Short/non transfer of levies/cess to earmarked funds 24

3.2.5.4 Non recognition of losses under NSSF in CFI 27

3.2.5.5 Net proceeds to States 28

3.2.5.6 Unpaid expenditure on subsidy 29

CONTENTS

ii

Para Sub

Para Description

Page

No.

3.3 Effective Revenue Deficit 30

3.3.1 Effective Revenue Deficit target 30 3.3.2 Trend of Effective Revenue Deficit 31

3.3.3 Effective Revenue Deficit during 2014-15 32

3.3.3.1 Inconsistency in expenditure on grants for creation of capital assets 32

3.3.4 Incorrect estimation of Effective Revenue Deficit target 33

3.3.5 Incorrect classification of certain expenditure as grants for creation of capital assets

35

3.3.5.1 Expenditure on procurement and maintenance treated as grants for creation of capital assets

35

3.3.5.2 Incorrect classification of expenditure under IAY and RAY 38 3.4 Liability of the Government 40

3.4.1 Liability target 40

3.4.2 Trend of outstanding liability 42

3.4.3 Understatement of Public Account liability 42 3.5 Guarantees 43

3.5.1 Guarantees target 44

3.5.2 Trend of additions in Guarantees 44

3.6 Borrowings from Reserve Bank of India 45 Conclusion 45

Chapter 4: Analysis of projections in fiscal policy statements

4.1 Projections in Mid Term Fiscal Policy Statement 47

4.1.1 Gross Tax Revenue projection 47 4.1.2 Total Outstanding Liability projection 48

4.1.3 Disinvestment projection 49

4.1.4 Structural imbalance in the composition of expenditure 49

4.2 Projections in Medium Term Expenditure Framework Statement 51

Conclusion 52

Chapter 5: Disclosure and Transparency in fiscal operations

5.1 Transparency in Government Accounts 53 5.1.1 Non-inclusion of statements in Union Accounts 53

5.1.2 Lack of transparency in Direct tax receipt figure 54

5.2 Transparency in disclosure statements mandated under FRBM Act 55

5.2.1 Understatement of arrears of Non-Tax Revenue 55 5.2.2 Non-inclusion of outstanding coal levy in arrears of Non-Tax Revenue 56

5.2.3 Understatement of assets 56

5.2.3.1 Variation in figures of closing and opening balances of assets 57

5.2.3.2 Inconsistency in figures of loans to Foreign Governments 57 5.2.4 Inconsistency in disclosure of grants for creation of capital assets 57

5.2.4.1 Incorrect disclosure in Form D-6 57

5.2.4.2 Discrepancies between Budget Estimates and DDG 58

Conclusion 60 Annexes 61-68

Glossary 69-70

iii

Section 7A of the Fiscal Responsibility and Budget Management (FRBM) Act,

2003, as amended in May 2012, provides that the Central Government may

entrust the Comptroller and Auditor General of India to review periodically as

required, the compliance of the provisions of this Act and such reviews shall be

laid before both House of Parliament. An amendment to the FRBM Rules 2004

was notified on 31 October 2015. Rule 8 of the FRBM (Amendment) Rules

provides that the Comptroller and Auditor General of India shall carry out an

annual review of the compliance of the provisions of the FRBM Act and the

Rules made thereunder by the Central Government, beginning with the

financial year 2014-15, and the Report shall be submitted to the President, who

shall cause them to be laid on the table of both Houses of Parliament.

This is the first report of the Comptroller and Auditor General of India relating

to review of the compliance of the provisions of the FRBM Act and the Rules

made thereunder by the Central Government for the year ended March 2015.

The report contains significant results arising from the review. The instances

mentioned in this report are those, which came to notice in the course of test

audit for the period 2014-15 as well as earlier years. Matters relating to the

period subsequent to 2014-15 have also been included, wherever necessary.

The audit has been conducted in conformity with the auditing standards issued

by the Comptroller and Auditor General of India.

PREFACE

Report No. 27 of 2016

v

Introduction

The Fiscal Responsibility and Budget Management (FRBM) Act, 2003 was

enacted by the Parliament in August 2003. The objective of introducing

FRBM Act, 2003 was to institutionalize fiscal discipline, reduce fiscal deficit,

improve macro-economic management and the overall management of the

public funds by moving towards a balanced budget. Due to global economic

crisis and adverse circumstances, the implementation of FRBM Act was put

on hold in February 2009. An amendment to the FRBM Act was made by the

Parliament in May 2012. An important aspect of the amendment was

introduction of Section 7A, which provides for entrustment to the Comptroller

and Auditor General of India, the periodical review of compliance of the

provisions of the Act by the Union Government.

What the Report covers

The present report discusses the compliance by the Union Government of the

provisions of FRBM Act, 2003 and the Rules made thereunder for the

financial year 2014-15. We have examined various amendments made in the

FRBM Act and Rules and analysed the trends and targets of various fiscal

indicators as set out in the Act/Rules from time to time. During the review

Audit examined (i) consistency of rules framed under the provisions of the

Act; (ii) achievement of targets by the Government as set out in the FRBM

Act and Rules; (iii) achievement of targets of receipts and expenditure as set

out in various fiscal statements; and (iv) issues of transparency and disclosures

made by the Government.

Major observations

Important audit observations relating to compliance of the provisions of the

Act and Rules made thereunder, and also on other related topics, are detailed

below:

EXECUTIVE SUMMARY

Report No. 27 of 2016

vi

Deviation from the Act and Rules

� For financial year 2014-15, in respect of effective revenue deficit and

revenue deficit, the annual reduction targets set out by the Government in

the Budget were not in accordance with the provisions of the Act.

(Para 2.2)

� There were inconsistencies in prescribed targets dates of fiscal indicators

under FRBM Act/Rules and target dates set out in Medium Term Fiscal

Policy Statement.

(Para 2.3)

� There was inconsistency between provisions contained in the FRBM Act

and Rules made thereunder in respect of assumption of additional

liabilities.

(Paras 2.4)

Progress in achievement of FRBM targets

� For financial year 2014-15, Government was able to achieve the targets

as set in Medium Term Fiscal Policy Statements in respect of revenue

and fiscal deficits. However, in respect of effective revenue deficit, the

target could not be achieved.

(Paras 3.1.3, 3.2.3 and 3.3.3)

� During the course of audit of accounts for FY 2014-15 of the Union

Government, certain transactions and financial eventualities were noticed

which had affected or had the bearing to affect the computation of

prescribed deficit indicators set out in the Act and the Rules made

thereunder.

(Para 3.2.5)

� Due to deficiency in the mechanism of estimating provisions on grants

for creation of capital assets, in certain test checked Ministries/

Departments, the resultant estimation of effective revenue deficit target in

FY 2014-15 was incorrect.

(Para 3.3.4)

� As a result of existence of varying practices in treatment of expenditure

on grants for creation of capital assets and incorrect classification of

Report No. 27 of 2016

vii

expenditure in certain welfare schemes, the effective revenue deficit was

understated during the financial year 2014-15.

(Paras 3.3.5.1 and 3.3.5.2)

� From FY 2011-12 onwards, the outstanding liability in terms of GDP

outstripped the targeted level as contained in the Medium Term Fiscal

Policy Statement. Further, due to understatement of liabilities of

` 6,70,210 crore in the Public Account, the total liabilities of the Union

Government were contained at 46.2 per cent of GDP, which otherwise

would have stood at 51.6 per cent of GDP in FY 2014-15.

(Paras 3.4.2 and 3.4.3)

Analysis of projections in fiscal policy statements

� Projection for FY 2014-15 included in Medium Term Fiscal Policy

Statement in respect of gross tax revenue, outstanding liabilities, and

disinvestment varied significantly from the actuals. Similarly, projection

under various heads of expenditure for FY 2014-15 included in Medium

Term Expenditure Framework Statements of 2013-14 varied significantly

in BE and RE of 2014-15.

(Paras 4.1 and 4.2)

Disclosure and Transparency in fiscal operations

� Recommendation of Twelfth Finance Commission relating to inclusion of

eight additional statements in the Union Government Accounts for

greater transparency, has not been acted upon, despite in-principle

acceptance of the recommendation by the Government.

(Para 5.1.1)

� Refunds of ` 1,17,495 crore (including interest on refunds of taxes) were

made from gross direct tax collection in FY 2014-15 but this aspect was

not disclosed in the Government accounts.

(Para 5.1.2)

� Disclosure statements mandated under the FRBM Act and the Rules

made thereunder placed before the Parliament for FY 2014-15 and earlier

years contained inconsistencies relating to understatement of non-tax

revenue; variations in closing and opening balances of physical and

Report No. 27 of 2016

viii

financial assets; overstatement of loans to foreign governments; and

discrepancies in the estimation of provision on grants for creation of

capital assets.

(Para 5.2)

Recommendations

Based on audit observations contained in the Report, the following

recommendations are made:

(i) To address the issues of inconsistency in the FRBM Act/Rules, the

Government may carry out suitable amendments.

(ii) The Government should follow the format of Form D-6 as prescribed

under the FRBM Rules.

(iii) Budgetary provisioning as well as their accountal need to be in

harmony with the codal provisions relating to classification structure

of accounts to avoid misclassification of expenditure.

(iv) The Government may transfer specific purpose levies/cess collected to

the funds earmarked for the purpose.

(v) A mechanism for recognizing the result of annual operations of NSSF

and its impact on the Government finances may be put in place.

(vi) To facilitate correct identification and booking of expenditure as

grants on creation of capital assets, the Government may consider

defining the criteria for classification of expenditure as grants for

creation of capital assets and its compliance by the

Ministries/Departments.

(vii) The Government may exclude such grants, which does not lead to

creation of assets owned by the grantee organisations, from

categorising as grants for creation of capital asset.

(viii) The Government may strengthen the process of making underlying

assumptions for projection of receipt and expenditure in various fiscal

policy statements to insulate them from frequent changes and to

seamlessly integrate the projection in the Budget.

Report No. 27 of 2016

ix

(ix) Necessary steps may be taken to append additional statements in the

Union Government Finance Accounts as suggested by the 12th

Finance

Commission to ensure greater transparency in the accounts.

(x) Disclosure statements prepared under the FRBM Act and Rules made

thereunder should be complete in all respect and transparent.

Report No. 27 of 2016

1

p

1.1 Background

The issue of management of fiscal deficit assumed importance in India in the

late eighties when the combined deficit of the Union and State Governments

rose to levels above 7 per cent of Gross Domestic Product (GDP). In the

year 1999-2000, the combined fiscal deficit of the Union and State

Governments stood at about 9.8 per cent of GDP, while revenue deficit was

about 6.8 per cent.

Fiscal deficit of the Union was over 6 per cent of GDP in the first half of the

eighties which widened further in the second half, reaching almost 9 per cent

at the end of financial year (FY) 1986-87. It was about 8.3 per cent in

FY 1990-91. During the period 1994-99, the average fiscal deficit of the

Union was over 6 per cent. Moreover, the total debt liability of the Union

increased from ` 6,30,071 crore in 1994-95 to ` 10,12,486 crore in 1998-99,

showing an increase of 61 per cent.

In view of the continuing fiscal stress on the economy and the need to contain

the fiscal deficit within a reasonable limit, the Union Government, in January

2000, set up a Committee to go into the various aspects of the fiscal system

and to recommend a draft legislation on fiscal responsibility. Based on

recommendation of the Committee, the Government, in December 2000,

introduced Fiscal Responsibility and Budget Management (FRBM) Bill,

which became Act in August 2003.

1.2 Fiscal Responsibility and Budget Management Act, 2003 and

Rules, 2004

The objective of FRBM Act, 2003 was to institutionalize fiscal discipline,

reduce fiscal deficit, improve macro-economic management and the overall

management of the public funds by moving towards a balanced budget. FRBM

Rules, 2004, framed under Section 8 of the Act came into force in July 2004.

FRBM Act was enacted to provide for following responsibilities of the Central

Government:

Chapter 1: Introduction

Report No. 27 of 2016

2

� to ensure inter-generational equity in fiscal management and long term macro-

economic stability by achieving sufficient revenue surplus and removing fiscal

impediments in the effective conduct of monetary policy;

� prudential debt management consistent with fiscal sustainability through limits on

the Central Government borrowings, debt and deficits;

� greater transparency in fiscal operations of the Central Government; and

� conducting fiscal policy in a medium-term framework and for matters connected

therewith or identical thereto.

To achieve the above, the Act and the Rules stipulated following targets to be

achieved by the Union Government in respect of major fiscal indicators as

indicated in Box-1.

Box-1: Targets for various fiscal indicators

Fiscal

Indicators Target

Revenue

Deficit (RD) Elimination of RD by 31 March 2008 and thereafter to build up adequate revenue surplus. To achieve the target of RD the Central Government shall reduce the RD by an amount equivalent to 0.5 per cent or more of the GDP1 at the end of each financial year beginning with 2004-05.

Fiscal Deficit

(FD) To bring down the FD to not more than three per cent of GDP at the end of 31 March 2008. To achieve the target of FD the Central Government shall reduce the FD by an amount equivalent to 0.3 per cent or more of the GDP at the end of each financial year beginning with 2004-05.

Guarantees The Government shall not give guarantee aggregating to an amount exceeding 0.5 per cent of GDP in any financial year beginning with 2004-05.

Liabilities The Government shall not assume additional liabilities (including external debt at current exchange rate) in excess of 9 per cent of GDP for FY 2004-05 and in each subsequent financial year, the limit of 9 per cent of GDP shall be progressively reduced by at least one percentage point of GDP.

Borrowings

from Reserve

Bank of India

The Act imposes restrictions on the borrowing by the Central Government from Reserve Bank of India (RBI).

Note: The position of the fiscal indicators from 2004-05 to 2014-15 are given in Annex 3.1. In respect of liabilities the figures are available at Table-7 and Graph-5 and in respect of

guarantees position is available in Graph-6.

1 As per FRBM Rules GDP means Gross Domestic Product at current price.

Report No. 27 of 2016

3

Besides, the Act and Rules require the Government to lay in both Houses of

Parliament three policy statements along with the Annual Financial Statement

and the Demands for Grants, as briefly narrated in Box-2 below.

Box-2: Fiscal Policy Statements

Medium Term

Fiscal Policy

(MTFP)

Statement

MTFP Statement containing three year rolling targets for fiscal indicators viz. RD, FD, Tax Revenue and Total Outstanding Liabilities as a percentage to GDP with specifications of underlying assumptions, including assessment of sustainability relating to balance between revenue receipt and revenue expenditure; use of capital receipts including market borrowings for generating productive assets.

Fiscal Policy

Strategy (FPS)

Statement

FPS Statement containing policies of the Central Government for the ensuing financial year, relating to taxation, expenditure, market borrowings and other liabilities, lending and investment, pricing of administered goods and services, securities and description of other activities etc., an evaluation of current policies vis-à-vis fiscal management principles, intra-year benchmarks for assessing trends in receipts and expenditure relating to annual targets and Budget Estimates (BE).

Macro-

economic

Framework

(MF)

Statement

MF Statement containing an assessment of growth in GDP, fiscal balance of the Union Government and external sector balance of economy as reflected in current account of balance of payment.

In the Budget speech of 8 July 2004, it was brought out that 2008-09 would be

a more credible terminal year, which would also coincide with the term of the

then Government. Accordingly, through the Finance Act 2004, amendment in

Section 4 of the FRBM Act was made, thereby the target dates for revenue

deficit and fiscal deficit were shifted to 31 March 2009.

1.3 Temporary hold of FRBM Act

Beginning from FY 2005-06, the fiscal deficit showed signs of improvement

and was reduced to a level of 2.7 per cent of GDP (as per Budget at a Glance)

in FY 2007-08 (refer Graph-2 of Para 3.2.2). In February 2009, the

Government put on hold temporarily the fiscal consolidation process citing

global economic crisis and adverse circumstances. During the two financial

years, i.e. FY 2008-09 and 2009-10, the fiscal deficit again rose to the level of

6.0 and 6.4 per cent of GDP (as per Budget at a Glance) respectively. The

outstanding liability of the Government during these two years’ period also

hovered around 49 to 50 per cent of GDP (refer Graph-5 of Para 3.4.2).

Report No. 27 of 2016

4

1.4 Introduction of renewed road-map under amended FRBM

Act

The 13th Finance Commission (FC) in its report (December 2009) for the

award period 2010-15 had presented renewed fiscal consolidation path for the

Centre. 13th FC recommended zero and three per cent targets of revenue and

fiscal deficit respectively to be achieved by the end of March 2014 followed

by revenue surplus of 0.5 per cent of GDP by 2014-15.

An amendment in the FRBM Act was passed by the Parliament in May 2012,

wherein a new fiscal indicator namely ‘effective revenue deficit’ was

introduced, to be worked out by excluding revenue expenditure incurred on

‘grants for creation of capital assets’ from the revenue deficit. In addition, it

envisaged elimination of effective revenue deficit by 31 March 2015 and

thereafter build up adequate effective revenue surplus and also to reach

revenue deficit of not more than two per cent of GDP by 31 March 2015,

among other measures. Further, in order to eliminate the effective revenue

deficit by 31 March 2015, the Central Government shall reduce such deficit by

an amount equivalent to 0.8 per cent or more of the GDP at the end of each

financial year beginning with FY 2013-14.

Subsequent to the amendment of May 2012 in the Act, the Government set up

a committee chaired by Dr. Vijay L. Kelkar, who was charged with the task of

introducing mid-term corrections for fiscal year 2012-13 and to chart a

medium term framework on this basis, for the remaining time horizon of the

13th FC. The Kelkar Committee in its report (September 2012) had

recommended fiscal roadmap of zero effective revenue deficit; two per cent

revenue deficit and 3.9 per cent fiscal deficit by the end of FY 2014-15.

Recommendations of the Committee with regard to proposed reforms on

expenditure and receipts were accepted by the Government (October 2012).

However, the Government decided (May 2013) to achieve the fiscal deficit

target of not more than 3 per cent of GDP by 2016-17. Accordingly,

amendments in FRBM Rules indicating new targets for fiscal consolidation

were notified in May 2013 whereby the target date for elimination of effective

revenue deficit, achieving the target of revenue deficit of not more than

two per cent of GDP was fixed as 31 March 2015 and for fiscal deficit of not

Report No. 27 of 2016

5

more than three per cent of GDP as 31 March 2017. The annual rates of

gradual reduction in the deficit parameters were also revised upwardly

(revenue deficit from 0.5 per cent or more of GDP to 0.6 per cent or more and

fiscal deficit from 0.3 per cent or more of GDP to 0.5 per cent or more). In

June 2015, the FRBM Rules were further amended to achieve the targeted

levels in respect of the three deficit indicators by 31 March 2018 and also the

annual rate of gradual reduction were relaxed in contrast to the upward

revision made in the Rules in May 2013 (revenue deficit from 0.6 per cent or

more of GDP to 0.4 per cent or more, fiscal deficit from 0.5 per cent or more

of GDP to 0.4 per cent or more and effective revenue deficit from 0.8 per cent

or more of GDP to 0.5 per cent or more).

1.5 Amended FRBM Act and obligations of the Union

Government

Since the enactment of the Act in 2003 and taking into account numerous

amendments made in the Act and Rules from time to time, including the latest

amendments in the Act (as of May 2015) and the Rules (as of June 2015), the

status of the target dates for various fiscal indicators stand as indicated in Box-

3 below:

Box-3: Revised targets for various fiscal indicators

Indicators Targets

Effective

Revenue

Deficit (ERD)

ERD is to be eliminated by 31 March 2018 with annual reduction by an amount equivalent to 0.5 per cent or more of GDP at the end of each financial year beginning with FY 2015-16.

Revenue

Deficit (RD)

RD of not more than two per cent of GDP by 31 March 2018 with annual reduction by an amount equivalent to 0.4 per cent or more of GDP at the end of each financial year beginning with FY 2015-16.

Fiscal Deficit

(FD)

FD of not more than three per cent of GDP at the end of 31 March 2018 with annual reduction by an amount equivalent to 0.4 per cent or more of GDP at the end of each financial year beginning with FY 2015-16.

Since the introduction of the Act, no change has been made in targets related

to guarantees, total liabilities and borrowings from RBI (shown in Box-1). The

amended FRBM Act and Rules2 also requires the Government to lay down

another Statement, viz. Medium Term Expenditure Framework Statement

2 Sections 6 and 7 of the FRBM Act and Rule 6 of FRBM Rules

Report No. 27 of 2016

6

before both Houses of Parliament, immediately following the Session of

Parliament in which the other three policy statements (shown in Box-2) were

laid, containing the following information:

Medium Term

Expenditure Framework

(MTEF) Statement

MTEF Statement containing three year rolling target for prescribed expenditure indicators, with specification of underlying assumptions and risks involved.

Further, the FRBM Act and Rules (as amended from time to time) requires

laying of quarterly review reports, in addition to certain disclosures in the

prescribed formats, which are indicated in Annex-1.1.

1.6 Review of compliance of provisions of FRBM Act by the

Comptroller and Auditor General of India (CAG)

13th FC had recommended that the Centre may institute a process of

independent review and monitoring of the implementation of FRBM process.

Accordingly, a new Section 7A was inserted through FRBM Amendment Act

(May 2012) which provides that the Central Government may entrust the

CAG to review periodically as required, the compliance of the provisions of

this Act and such reviews shall be laid before both Houses of Parliament.

An amendment in the Rules was further made in October 2015 to carry out the

effect of amendment in the Act made in May 2012. The amended Rules

provide that, the CAG shall carry out an annual review of the compliance of

the provisions of the Act and the Rules made thereunder by the Central

Government beginning with the Financial Year 2014-15. The review shall

include:

(i) analysis of achievement and compliance of targets and priorities set

out in the Act and the Rules made thereunder, Medium Term Fiscal

Policy Statement, Fiscal Policy Strategy Statement, Macro-

economic Framework Statement and Medium Term Expenditure

Framework Statement;

(ii) analysis of trends in receipts, expenditure and macro-economic

parameters in relation to the Act and the Rules made thereunder;

(iii) comments related to classification of revenue, expenditure, assets

or liabilities having a bearing on the achievement of targets set out

in the Act and the Rules made thereunder; and

Report No. 27 of 2016

7

(iv) analysis of disclosures made by the Central Government to ensure

greater transparency in its fiscal operations.

1.7 Audit Objectives

Audit objectives for the review of the compliance of the provisions of the Act

were to examine whether:

a) the Rules framed under the Act are consistent with the provisions of

the Act;

b) the Government achieved the targets of fiscal indicators set out in the

FRBM Act and Rules made thereunder effectively;

c) the classification of revenue, expenditure, assets and liabilities are in

line with established rules and principles;

d) the projections of components of receipts and expenditure in various

fiscal policy statements are based on concrete assumptions; and

e) the disclosures made by the Central Government to ensure

transparency in fiscal operations are adequate.

1.8 Audit Scope and Methodology

In terms of Government of India (Allocation of Business) Rules 1961, the

Ministry of Finance, Department of Economic Affairs is responsible for

preparation of Central Budget other than Railway Budget including

supplementary/excess grants; monitoring of budgetary position of the Central

Government; credit, fiscal and monetary policies; and administration of the

Fiscal Responsibility and Budget Management Act 2003, among other

business of the Government of India.

Accordingly, the field audit was conducted during the period December 2015

to February 2016. During this period, records of the Ministry of Finance,

Department of Economic Affairs were examined, including examination of the

FRBM Act and Rules made thereunder and various amendments carried out

from time to time, disclosures contained in prescribed Forms D-1 to D-6 for

the year 2014-15 presented along with the Budgets for the year 2015-16 and

2016-17, as well as other budget and accounts related publications.

Report No. 27 of 2016

8

As brought out in para 1.6, the CAG is mandated to carry out an annual review

of the compliance of the provisions of the Act and the Rules made thereunder

by the Central Government beginning with the financial year 2014-15.

Accordingly, the focus has been on the targets and transactions relating to this

particular financial year. However, matters relating to periods prior to 2014-15

as well as subsequent years were also examined wherever necessary. The

draft report was issued to the Ministry of Finance on 29 February 2016. An

exit conference with the officers of the Ministry of Finance, Department of

Economic Affairs was held on 13 April, 2016, wherein the audit findings and

recommendations were discussed. On receipt of replies from the Ministry, the

same together with rebuttal were incorporated and the revised draft report was

again made available to the Ministry on 23 May 2016. Subsequent replies of

the Ministry on the revised draft report received on 24 June 2016 have also

been incorporated in this report.

1.9 Audit Criteria

The main sources of audit criteria used for the purpose of review were drawn

from documents, such as the following:

• FRBM Act, 2003 as amended from time to time.

• FRBM Rules, 2004 as amended from time to time.

• Budget documents including various statements submitted by

Government under FRBM Rules and disclosures made to ensure

transparency in fiscal operations.

• Quarterly Review Reports submitted by the Ministry of Finance in

Parliament.

• Union Government Finance Accounts compiled by the Controller

General of Accounts under Ministry of Finance, Department of

Expenditure.

In addition, the reports of the Finance Commissions, High Level Expert

Committee on Efficient Management of Public Expenditure, and other

Committees on Fiscal Consolidation have also been consulted to determine the

audit criteria.

Report No. 27 of 2016

9

1.10 Structure of the Report

The present report is the first annual review by the CAG as per Rule 8 of

FRBM (Amendment) Rules 2015 to examine compliance of provisions of the

Act by the Government for FY 2014-15. The findings of Audit are discussed

in Chapters 2 to 5.

• Chapter 2 of this Report deals with the issues where deviations from

the Act and Rules were noticed.

• Chapter 3 analyses the extent of achievement of various fiscal

indicators during FY 2014-15 as compared to the targets set under the

Act and Rules.

• Chapter 4 examines the receipts and expenditure of the Union

Government for FY 2014-15 vis-à-vis projections contained in various

fiscal policy statements, Budget at a Glance, Annual Financial

Statement and Union Government Finance Accounts.

• Chapter 5 contains observations relating to adequacy and accuracy of

disclosures mandated under the Act and Rules and also issues of

transparency in fiscal operations.

Report No. 27 of 2016

10

In the FRBM Act 2003 and FRBM Rules 2004 (as amended from time to

time) various fiscal targets were set. In this chapter, we have discussed the

issues regarding deviations from provisions of the Act and the Rules and

inconsistencies between the Act and the Rules, followed by recommendations

wherever considered necessary.

2.1 Continuous deferment of targets

Fiscal targets prescribed in the original FRBM Act 2003 were to be achieved

by 31 March 2008 which were deferred to 31 March 2009 in 2004. However,

in 2009, the Government decided to put on hold temporarily the process of

fiscal consolidation citing reason of global meltdown necessitating adjustment

of fiscal policy to take care of exceptional circumstances through which the

economy was passing and promised to return to the FRBM target for fiscal

deficit at the earliest and as soon as the negative effects of the global crisis on

the economy have been overcome. Accordingly, the FRBM Act amended

through the Finance Act 2012 (May 2012) and rules made thereunder notified

in May 2013, contained revised targets for Revenue Deficit and Effective

Revenue Deficit, to be achieved by 31 March 2015. Further, in the MTFP

Statement placed along with Budget for FY 2014-15, the Government shifted

target for achievement of revenue deficit to March 2017 citing the reason

‘below five percent growth in GDP in the last two years’. Through Finance

Act 2015, amendment was made in the FRBM Act by which the target dates

for achievement of all the three deficit indicators were again extended to

March 2018. The reasons given were ‘emerging government priorities and

compositional shift in the fiscal relations between the Centre and States’

following the recommendations of the Fourteenth Finance Commission. Thus,

the Government has continuously been deferring the targets under the Act

immediately after its enactment.

2.2 Non-adherence to annual reduction targets in 2014-15

Rule 3 of amended FRBM Rules notified in May 2013 required that in order to

achieve the deficit targets as set out in Section 4 of the Act, the Central

Chapter 2: Deviation from the Act and Rules

Report No. 27 of 2016

11

Government shall reduce the effective revenue deficit, revenue deficit and

fiscal deficit targets by an amount equivalent to 0.8 per cent, 0.6 per cent and

0.5 per cent or more of the GDP respectively3 at the end of each financial year

beginning with FY 2013-14.

It may be mentioned that the Budget for FY 2013-14 was already placed in

February 2013, whereas the amended FRBM Rules were notified subsequently

in May 2013 setting out the amended annual reduction targets in respect of

three deficit indicators beginning with FY 2013-14. Taking into account the

amended annual reduction target of three deficit indicators, the Table-1 below

analyses the compliance of annual reduction in FY 2014-15 as set by the

Government in MTFP Statement for 2014-15 vis-à-vis RE for FY 2013-14.

Table-1: Annual Reduction Targets

(As percentage of GDP)

Fiscal Indicators RE

2013-14

Target in

BE 2014-15 Annual Reduction

Effective Revenue Deficit 2.0 1.6 0.4

Revenue Deficit 3.3 2.9 0.4

Fiscal Deficit 4.6 4.1 0.5

Source: MTFP Statement for 2014-15

The annual reduction target in respect of two deficit indicators, i.e. effective

revenue deficit and revenue deficit were only 0.4 per cent of GDP in Budget

of 2014-15 with reference to the revised estimates for FY 2013-14 as against

required reduction of 0.8 per cent and 0.6 per cent respectively as specified in

FRBM Rules applicable during that period. As such, the annual reduction

targets envisaged in the Budget of 2014-15 were not in accordance with

provisions contained in the Rules.

The Ministry stated (May 2016) that the MTFP Statement for the year 2014-15

had acknowledged an imbalance on revenue account and it was clarified that

the difficult macro-economic conditions in the international and domestic

market prevailing over the year resulted into lesser than mandated correction

in deficit. It further stated that later in the year 2015, in sync with the existing

macro-economic realities and need for creating additional fiscal space to

increase public investment, the FRBM Act was amended and new target date

was set for achieving deficit targets. It also added that annual reduction

targets have been re-calibrated. In Budget 2016-17, annual reduction in

3 These stipulations were further relaxed in June 2015 through amendment in the Act.

Report No. 27 of 2016

12

estimates of FD is in line with the FRBM Act, whereas, it is more than

mandated in respect of RD and ERD.

While taking into consideration the reply of the Ministry in the above para as

well as the position brought out in the MTFP Statement for FY 2014-15,

which bring out the impediments having a bearing on the achievement of the

annual reduction targets, it may be mentioned that the reduction targets as

specified in the FRBM Rules applicable during that period could not be

achieved. The subsequent recalibration of the reduction targets as mentioned

by the Ministry was brought into effect in June 2015 and the annual reduction

was to begin from FY 2015-16.

2.3 Inconsistency in fiscal targets between MTFP Statement and

FRBM Act/Rules

Section 4 of FRBM Act and Rule 3 of FRBM Rules specifies the targets for

the three fiscal indicators along with target date for their achievement. MTFP

Statement laid along with the Budget also contains three year rolling targets

for these fiscal indicators.

In this regard, following were observed in respect of target dates relating to

effective revenue deficit and revenue deficit after introduction of renewed

roadmap, which has also been summarized in Table-2 hereunder.

• FRBM Act as amended in May 2012 (through Finance Act 2012) set

the target of eliminating the effective revenue deficit and reach the

revenue deficit of not more than two per cent of GDP by 31 March

2015.

• MTFP Statement laid in Parliament in February 2013 along with

Budget 2013-14 indicated that this target will be achieved at the end of

FY 2015-16.

• FRBM Rules as amended and notified in May 2013 again set the said

targets of effective revenue deficit and revenue deficit as 31 March

2015.

• MTFP Statement laid in Parliament in July 2014 along with Budget

2014-15 showed that the targets of effective revenue deficit and

revenue deficit will be achieved at the end of FY 2016-17.

Report No. 27 of 2016

13

• In February 2015 through Finance Bill 2015, the Government proposed

changes in the FRBM Act and Rules and targets for achieving the

deficit indicators were shifted to 31 March, 2018. The Finance Bill

2015 became the Finance Act in May 2015.

Table-2: Inconsistency in target dates

As set out in

%age of

GDP

Amendment

Act of May

2012

MTFP

Statement of

February

2013

(in Budget

for FY 2013-

14)

FRBM

Rules

notified

in May

2013

MTFP

Statement of

July 2014

(in Budget for

FY 2014-15)

Finance Bill

2015

(in Budget

for FY

2015-16)

Effective

revenue

deficit

Nil To be achieved by

31 March 2015

31 March 2016

31 March 2015

31 March 2017 31 March 2018

Revenue

deficit

Not more than 2

Thus, between February 2013 and February 2015, different target dates were

set in respect of effective revenue deficit and revenue deficit. It may be seen

that MTFP Statements for 2013-14 and 2014-15 were having target dates

inconsistent with target dates set out in FRBM Act and Rules applicable

during that period.

The Ministry stated (May 2016) that the deferment of targets referred to in

audit observation was in respect of rolling targets/projections for next two

years (medium-term). It also stated that while preparing Budget for particular

financial year, the Government provides the rolling targets of specified fiscal

indicators viz., FD. RD, ERD, Tax-GDP ratio etc. in MTFP Statement. It

added that rolling targets are set on the basis of certain underlying

assumptions viz., GDP growth, receipts, expenditure etc. and variation in

these macro-economic parameters necessitates re-fixing of fiscal targets in the

budget year. Therefore, an advance amendment to the Act on the basis of

rolling targets is unwarranted, since situation may change by the time Budget

is presented.

The reply needs to be viewed in the light of the position that the MTFP

Statement which provides the underlying assumptions of fiscal indicators

along with rolling targets should have been aligned with the corresponding

fiscal targets stipulated in the FRBM Act/Rules.

Report No. 27 of 2016

14

2.4 Inconsistency in FRBM Act and Rules – on assumption of

additional liabilities

Rule 3(4) of the FRBM Rules requires that the Government shall not assume

additional liabilities (including external debt at current exchange rate) in

excess of 9 per cent of GDP for FY 2004-05 and in each subsequent financial

year, the limit of 9 per cent of GDP shall be progressively reduced by at least

one percentage point of GDP. Thus, according to application of this Rule, with

gradual reduction of one percentage point of GDP, from the level of

9 per cent, beginning from financial year 2004-05, the Government should not

assume any additional liabilities from the financial year 2013-14 onwards.

However, given the prevalence of deficit budgeting in the Union Government,

a significant portion of fiscal deficit is to be met from borrowings and hence

creation of additional liabilities cannot be ruled out. Thus, Rule 3(4) with

regard to assumption of additional liabilities is inconsistent and needs to be

aligned with the Rule 3(2) regarding fiscal deficit, which stipulates bringing

down fiscal deficit at the level of not more than of 3 per cent of GDP by

31 March 2018.

The Ministry stated (May 2016) that Rule 3(4) needs to be seen in the context

that with a fiscal deficit target of 3 per cent of GDP, creation of additional

liability cannot be avoided, but it will decline with reduction in fiscal deficit. It

also added that additional liability was to be progressively reduced by at least

one percentage point of GDP from the financial year 2005-06 onwards till the

ultimate fiscal deficit target of not more than 3 per cent of GDP is achieved,

and not that additional liability will be completely eliminated.

The reply of the Ministry does not address the issue. Subsequent amendments

in Rule 3(2) shifted the target of bringing down fiscal deficit at the level of not

more than of 3 per cent of GDP to 31 March 2018. Thus, with the shifting of

target dates for achieving the fiscal deficit, appropriate amendments could

have concurrently been brought in Rule 3(4) also to align the related

provisions in the Rules.

Recommendation: To address the issues of inconsistency in the FRBM

Act/Rules, the Government may carry out suitable amendments.

Report No. 27 of 2016

15

2.5 Inconsistency in format of disclosure statement (D-6)

Rule 6(1) of amended FRBM Rules requires that in order to ensure greater

transparency in its fiscal operation in the public interest, the Central

Government shall at the time of presenting the Annual Financial Statement

and the Demands for Grants, make disclosures in prescribed Form (D-6) with

regard to expenditure incurred on grants for creation of capital assets

(refer Annex 1.1). This disclosure statement is presented in the Expenditure

Budget Volume-I in a different format from FY 2011-12, although the Rule

6(1) was notified in May 2013. This disclosure statement appended in the

Expenditure Budget Volume-I from FY 2011-12 onwards has a different

format which varies from the prescribed Form (D-6). The disclosure does not

provide details of actual expenditure data for previous year (Y-1), as required

under the format prescribed by FRBM Rules.

The Ministry accepted (May 2016) the audit observation.

Recommendation: The Government should follow the format of Form D-6 as

prescribed under the FRBM Rules.

Conclusion

After introduction of FRBM Act, the Government had been continuously

deferring the fiscal targets. During 2014-15, in respect of effective revenue

deficit and revenue deficit, the annual reduction targets set out by the

Government were not in accordance with the provisions of the Act/Rules.

Between February 2013 and February 2015, the target dates set out in MTFP

Statement for effective revenue deficit and revenue deficit were inconsistent

with the FRBM Act and Rules. Further, there is inconsistency between

provisions made under the FRBM Act and Rules made thereunder on

assumption of additional liabilities.

Report No. 27 of 2016

16

The Government set the targets for various fiscal indicators in terms of

percentage of GDP. For FY 2014-15, the GDP figure was assumed by the

Government based on the GDP growth recorded in previous year viz. 2013-14

(old series with 2004-05 as the base year). Accordingly, in the Budget at a

Glance 2014-15 presented on 10 July 2014, GDP was projected at

` 128,76,653 crore assuming 13.4 per cent growth over the advance estimates

of 2013-14 (` 113,55,073 crore) released by the Central Statistical Office

(CSO), Ministry of Statistics and Programme Implementation. However, the

CSO on 30 January 2015 notified the new series of national accounts

containing the new series of GDP, revising the base year from 2004-05 to

2011-12. As a result of this revision, the GDP data for FY 2014-15 (old series

with 2004-05 as base year) was not available. Consequently, for analysis of

targets for FY 2014-15, the first revised estimates (R1) of GDP (new series

with 2011-12 as base year) released by CSO on 8 February 2016 has been

adopted in this report, and for earlier years the old series of GDP figures have

been adopted.

This chapter analyses the extent of achievement of various fiscal indicators

during FY 2014-15 as compared to the targets set in the FRBM Act/Rules

(as amended from time to time). Besides, the trend analysis from FY 2005-06

in respect of various fiscal indicators/parameters have also been made in this

chapter.

3.1 Revenue Deficit

Section 2(e) of FRBM Act defines revenue deficit as the difference between

revenue expenditure and revenue receipts, which indicates increase in the

liabilities of the Central Government without corresponding increase in the

assets of the Government.

3.1.1 Revenue Deficit target

The FRBM Act as notified in August 2003 had stipulated elimination of

revenue deficit by March 2008. Through Finance Act 2004 (September 2004),

Chapter 3: Progress in achievement

of FRBM targets

Report No. 27 of 2016

17

amendment was made in the FRBM Act and the target was shifted to

March 2009. In FRBM Act (amended through Finance Act 2012), the target of

elimination was modified with a new target to restrict revenue deficit to not

more than two per cent of GDP by 31 March, 2015. In the Union Budgets for

2013-14, through MTFP Statement, the target of restricting revenue deficit to

not more than two per cent of GDP was shifted to March 2016. This was

further shifted to March 2017 through the MTFP Statement placed along with

the Budget of 2014-15. This target was further extended to March 2018

through the Finance Act 2015.

3.1.2 Trend of Revenue Deficit

Following Graph-1 shows the trend of revenue deficit as a percentage of GDP

over the period from 2005-06 to 2014-15:

Graph-1: Trend of Revenue Deficit: 2005-15

Source: For BE/Target - MTFP Statement; For Actuals – Budget at a Glance (BAG) and

Union Government Finance Accounts (UGFA). For calculation of Actuals (UGFA), GDP (old

data series) upto 2013-14 has been adopted and for 2014-15, R1 GDP figure (new series)

released in February 2016 has been adopted.

Note: Data in absolute terms for deficits is at Annex 3.1. The actual deficit figures as per

Union Government Finance Accounts in some years differ from those shown in the Budget at

a Glance because the Budget at a Glance figures are not being computed exactly as per the

definition of revenue deficit provided in the FRBM Act.

The analysis of Graph4 and related data above reflects that up to FY 2007-08,

the Revenue Deficit was treading in line with fiscal consolidation path

envisaged in the FRBM Act/Rules. However, in FY 2008-09 a spike was

4 In Budget at a Glance, the figures of deficit are worked out by disregarding/netting certain transactions contrary to the definitions provided in the FRBM Act. In this context, para 3.2.3 further elucidates the background.

05-06 06-07 07-08 08-09 09-10 10-11 11-12 12-13 13-14 14-15

BE/Target 2.7 2.1 1.5 1.0 4.8 4.0 3.4 3.4 3.3 2.9

Actuals(BAG) 2.6 1.9 1.1 4.5 5.2 3.3 4.4 3.6 3.1 2.9

Actuals(UGFA) 3.0 3.1 1.7 6.3 5.4 3.3 4.4 3.6 3.1 2.9

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

As

pe

rce

nta

ge

to

GD

P

Report No. 27 of 2016

18

noticed, thereafter the revenue deficit as percentage of GDP showed a trend

converging towards the budgeted level.

3.1.3 Revenue Deficit during 2014-15

For FY 2014-15, the Government had set revenue deficit target at 2.9 per cent

of GDP which showed 0.4 per cent reduction from the level of 3.3 per cent for

the year 2013-14 (as discussed in Para 2.3). The calculation for computing the

revenue deficit is as under:

Table-3 : Revenue Deficit Estimate and Actuals: 2014-15

Component

Revenue

Expenditure

(1)

Revenue

Receipt

(2)

Revenue

Deficit (RD)

(1-2)

RD as % of

GDP

(As in Budget

at a

Glance/MTFP)

(`̀̀̀ in crore)

Budget Estimates 15,68,111 11,89,763 3,78,348 2.9

Actuals 14,66,992 11,01,472 3,65,520 2.9

Variation with reference to Budget Estimates

-1,01,119

(-6.45%)

-88,291

(-7.42%)

-12,828

(-3.39%)

-

Source: Budget at a Glance

Note: As per Union Government Finance Accounts, the revenue deficit for FY 2014-15 works

out at ` 3,66,228 crore (Difference between revenue expenditure of ` 16,95,137 crore and

revenue receipt of ` 13,28,909 crore).

The actual revenue deficit in 2014-15 was contained at the budgeted level, but

the required target under the FRBM Act/Rules, viz. not more than 2 per cent

of GDP by 31 March 2015 was breached. Further, the annual reduction target

equivalent to 0.6 per cent or more of GDP also could not be achieved, as the

reduction in 2014-15 was 0.4 per cent with reference to RE 2013-14, as

discussed in para 2.2.

3.2 Fiscal Deficit

Section 2(a) of FRBM Act, defines fiscal deficit as the excess of total

disbursements from the Consolidated Fund of India (CFI), excluding

repayment of debt, over total receipts into the Fund (excluding the debt

receipts), during a financial year.

3.2.1 Fiscal Deficit target

The FRBM Act as notified in August 2003 envisaged achieving fiscal deficit

of not more than three per cent of GDP by March 2008. However, through

Report No. 27 of 2016

19

Finance Act 2004 (September 2004), the target was shifted to March 2009. To

achieve this target, the fiscal deficit was to be reduced annually by an amount

equivalent to 0.3 per cent or more of the GDP beginning with FY 2004-05.

Further, the amended FRBM Rules notified in May 2013 stipulated that in

order to achieve the target of fiscal deficit of not more than three per cent of

GDP by 31 March 2017, the Central Government shall reduce such deficit by

an amount equivalent to 0.5 per cent or more of the GDP at the end of each

financial year, beginning with FY 2013–14. Subsequently, through Finance

Act, 2015, the fiscal deficit target under the FRBM Act was extended to

March 2018.

3.2.2 Trend of Fiscal Deficit

Graph-2 below presents the trend of fiscal deficit as a percentage of GDP

over the period from 2005-06 to 2014-15:

Graph-2: Trend of Fiscal Deficit: 2005-15

Source: For BE/Target - MTFP Statement; For Actuals – Budget at a Glance (BAG) and

Union Government Finance Accounts (UGFA). For calculation of Actuals (UGFA), GDP (old

data series) upto 2013-14 has been adopted and for 2014-15, R1 GDP figure (new series)

released in February 2016 has been adopted.

Note: Data in absolute terms for deficits is at Annex 3.1. The actual deficit figures as per

Union Government Finance Accounts in some years differ from those shown in the Budget at

a Glance because the Budget at a Glance figures are not being computed exactly as per the

definition of fiscal deficit provided in the FRBM Act.

Analysis of data in the above Graph reflects that up to the FY 2007-08, the

trend of fiscal deficit was in line with fiscal consolidation path envisaged in

the FRBM Act/Rules. However, from 2008-09 onwards, it started deviating

from the path. The estimate for fiscal deficit for FY 2008-09 was 2.5 per cent

of GDP, however, it ended up at 6.0 per cent of GDP. The estimate for

2009-10 was raised to the level of 6.8 per cent (5.5 per cent in the interim

Budget), in view of bleak outlook for the growth in the world economy. From

05-06 06-07 07-08 08-09 09-10 10-11 11-12 12-13 13-14 14-15

BE/Target 4.3 3.8 3.3 2.5 6.8 5.5 4.6 5.1 4.8 4.1

Actuals(BAG) 4.1 3.5 2.7 6.0 6.4 4.9 5.7 4.8 4.4 4.1

Actuals(UGFA) 4.5 4.3 3.3 7.7 6.7 4.9 5.7 4.9 4.4 4.1

0.0

1.02.03.0

4.05.06.0

7.08.0

As

pe

rce

nta

ge

to

GD

P

Report No. 27 of 2016

20

2011-12, fiscal deficit has shown a declining trend and it has come down from

5.7 per cent in 2011-12 to 4.1 per cent in 2014-15.

3.2.3 Fiscal Deficit during 2014-15

For FY 2014-15, the Government had set fiscal deficit target at 4.1 per cent of

GDP which showed 0.5 per cent reduction from the revised fiscal deficit target

of 4.6 per cent for the year 2013-14. The calculation for computing fiscal

deficit is as under:

Table-4: Fiscal Deficit-Budget Estimate and Actuals: 2014-15

Component

Actual

Expenditure

(1)

Non-debt

Receipts

(2)

Fiscal Deficit

(FD)

(1-2)

FD as % of

GDP

(As in Budget

at a Glance/

MTFP)

(` in crore)

Budget Estimates 17,94,892 12,63,715 5,31,177 4.1

Actuals 16,63,673 11,52,947 5,10,726 4.1

Variation with

reference to

Budget Estimates

-1,31,219 (-7.31%)

-1,10,768 (-8.77%)

-20,451

(-3.85%)

-

Source: Budget at a Glance

Note: As per Union Government Finance Accounts, the fiscal deficit for FY 2014-15 works out

at ` 5,15,948 crore (Excess of total disbursements from CFI excluding repayment of debt

amounting to ` 19,09,144 crore over total receipts into the CFI excluding the debt receipts

amount to ` 13,93,196 crore).

In 2014-15, fiscal deficit was contained at 4.1 per cent of GDP, i.e. at the

budgeted level and the Government also achieved the annual reduction target

of 0.5 per cent as discussed in para 2.2.

The figures of revenue and fiscal deficits reported in the Budget at a Glance of

the Union Budget differ, in some years, from those indicated/derived from

Annual Financial Statements/Union Government Finance Accounts of the

respective years. On this issue, the CAG of India in October 2007 had drawn

attention of the then Finance Minister. Apart from that, the matter was also

reported in the CAG’s Audit Reports on the accounts for FY 2004-05,

2005-06, 2007-08, 2008-09 and 2009-10 of the Union Government. The then

Finance Minister while explaining the difference in revenue and fiscal deficits,

in December 2007 had clarified that the procedure of depicting net

expenditure in the Budget at a Glance (Gross expenditure as reported in AFS

minus non-cash outgo item) had been followed over the years for budgeting

Report No. 27 of 2016

21

and accounting of Government transactions. Subsequently, in Budget speech

for FY 2008-09 the then Finance Minister acknowledged that significant

liabilities of the Government on account of oil, food and fertiliser bonds were

currently below the line, though the accounting arrangement was consistent

with the past practice. He further acknowledged that the fiscal and revenue

deficits were understated to that extent and there was need to bring these

liabilities into the fiscal accounting. However, the practice of netting certain

transactions for arriving at the figure of revenue and fiscal deficits in the

Budget at a Glance is still in practice in the Union Budget. Any netting of an

item of revenue or capital expenditure that affects the revenue or fiscal deficit

is inconsistent with the definition of these deficits under the FRBM Act.

3.2.4 Revenue Deficit as a component of Fiscal Deficit

Fiscal deficit necessitates additional borrowings, having an impact on inter-

generational fiscal management. Ideally, the borrowing should be undertaken

for investment purposes only. This requires the Government not to use

national savings to finance consumption. To quote 13th FC, “all items of

consumption expenditure need to be financed from current receipts, a practice

which is widely implemented in most countries that have successfully

addressed the issue of fiscal responsibility. While some allowances may be

made for revenue deficits during recessionary phases, the medium-term fiscal

framework must plan for all current expenditures to be financed entirely out of

current revenues”. Graph-3 depicts that the major portion of fiscal deficit

was on account of imbalance in current expenditure resulting into revenue

deficit averaging 67.8 per cent of fiscal deficit over the period from 2005-06

to 2014-15:

Report No. 27 of 2016

22

Graph-3: Trend of Revenue Deficit as component of Fiscal Deficit: 2005-15

Source: RD as %age of FD(BAG) - Budget at a Glance; and RD as %age of FD(UGFA) - Union

Government Finance Accounts.

Note: Data in absolute terms for deficits is at Annex 3.1.

The amended FRBM Act/Rules envisages fiscal deficit of not more than 3 per

cent of GDP and revenue deficit not more than 2 per cent of GDP, i.e. revenue

deficit should be two-thirds of fiscal deficit. Graph-3 shows that during the

post financial crisis period, the desired level (66 per cent or two-thirds of

fiscal deficit) of revenue deficit was achieved only in FY 2010-11. However,

from FY 2011-12 onwards, the position had deviated from the desired level.

3.2.5 Transactions affecting the computation of deficit indicators

During the course of audit of accounts for FY 2014-15 of the Union

Government, it was noticed that certain transactions and financial

eventualities, such as misclassification of expenditure, accruing of one time

receipts, short transfer of levies/cess to the designated funds, non-recognition

of losses in the operation of National Small Savings Fund (NSSF), short

assignment of net proceeds to States, and unpaid expenditure on subsidies, had

affected or had the bearing to affect the computation of prescribed deficit

indicators set out in the Act and the Rules made thereunder. These transactions

are discussed in succeeding paras.

3.2.5.1 Understatement of Revenue Deficit due to misclassification of

expenditure

During the audit of Union Government Accounts for FY 2014-15, a number of

instances of misclassification of expenditure of revenue nature as capital

expenditure and vice versa were noticed. These instances were reported in

Para 4.6 of CAG’s Report No.50 of 2015. As a result of obtaining budget

provisions under incorrect head of accounts, and subsequent booking of

05-06 06-07 07-08 08-09 09-10 10-11 11-12 12-13 13-14 14-15

RD as %age of FD(BAG) 63.0 56.3 41.4 75.2 81.0 67.5 76.4 74.3 71.0 71.6

RD as %age of FD(UGFA) 66.5 72.6 51.8 82.0 81.6 66.2 76.3 73.7 71.0 71.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

In p

er

cen

tRD as %age of FD(BAG)

RD as %age of FD(UGFA)

Report No. 27 of 2016

23

expenditure there against resulting in misclassifications, the capital

expenditure of the Union Government in FY 2014-15 was overstated by

` 748.43 crore and understated by ` 522.67 crore, leading to net overstatement

of capital expenditure by ` 225.76 crore. Correspondingly, revenue deficit for

FY 2014-15 was understated by an equivalent amount of ` 225.76 crore, as

detailed in Annex-3.2.

The Ministry stated (May 2016) that misclassification of expenditure, if any is

happening despite instructions issued to all Ministries/ Departments to

exercise extreme caution while booking expenditure. It added that the matter

may be taken up with the concerned Ministries / Departments by Audit.

The reply is in contravention to provision contained in Section 6(1) of FRBM

Act which requires that the Central Government shall take suitable measures

to ensure greater transparency in its fiscal operations. Being the administrative

Ministry for implementation of provisions of the Act, merely issuing

instructions to various Ministries to exercise due caution to avoid

misclassification do not absolve the Ministry of Finance from the

responsibilities mandated under the FRBM Act.

Recommendation: Budgetary provisioning as well as their accountal need to

be in harmony with the codal provisions relating to classification structure of

accounts to avoid misclassification of expenditure.

3.2.5.2 Contraction of Revenue Deficit due to one-time receipts in

2014-15

Levy on coal blocks: The Hon’ble Supreme Court had cancelled (September

2014) allocation of 204 captive coal blocks and imposed additional levy

@ ` 295 per ton on coal extracted since commencement of production in those

coal bocks till the date of its order (i.e. 24 September 2014) to be deposited in

Government account by 31 December 2014 and for the period from 25

September 2014 to 31 March 2015 @ ` 295 per ton to be deposited by 30 June

2015. Against the total additional levy of ` 9,518 crore to be received5 (for

coal extracted up to 24 September 2014) by 31 December 2014, ` 6,150 crore

were received by the Government till 31 March 2015.

5 Source: Reply/information received from Ministry of Coal

Report No. 27 of 2016

24

Receipt from spectrum auction: During 2014-15, the Government had

received ` 30,624 crore from ‘Other Communication Services’. On scrutiny of

the transactions, it was observed that out of ` 30,624 crore, receipts amounting

to ` 10,791 crore were collected from spectrum auction which had usage

rights of 20 years. Hence, ` 10,791 crore received by the Ministry was of the

nature of one-time receipt against the auctioned rights for 20 years.

Thus, one-time receipts of ` 16,941 crore helped the Government in

containing the revenue deficit, which would have been higher but for these

receipts. The fact that certain one-time receipts budgeted in 2014-15 would not

be available in 2015-16 and 2016-17 was also accepted by the Government in

its MTFP Statement for FY 2014-15.

The Ministry stated (May 2016) that the observation was factual in nature and

does not warrant any reply/action.

3.2.5.3 Short/non transfer of levies/cess to earmarked funds

Cesses are statutory levies whose proceeds are earmarked for utilisation for

specific purposes. The revenue from cess is therefore not shared by Central

Government with the States. In Para No. 2.3 of CAG’s Report No. 50 of 2015

on the accounts for FY 2014-15 of the Union Government, non-transfer of

` 8,123 crore, collected under different categories of levies and cess forming

part of tax/non-tax revenue, to the funds earmarked for the purpose have been

reported. Details of such cess/levy collected and transferred to designated

funds in the Public Account by the Government is at Annex-3.3. Such

collections were meant to be utilised for specific purposes. However, the

Government did not transfer the entire levy/cess collected to the designated

funds. Further, there is no disclosure in the annual accounts or in the Budget

documents with regard to the utilisation of cess collected for the intended

purpose and unutilised balances. This led to corresponding decrease of

revenue/fiscal deficit by ` 8,123 crore in 2014-15.

The Ministry stated (May 2016) that the audit observation has been made on

some selected Funds. Ministry offered following comments in support of its

stand:

(i) While it is true that the cesses/levies are levied for specific purposes, it

is also the responsibility of the Government, as custodian of public

Report No. 27 of 2016

25

money, that the resources realized are productively spent and deployed

for the purpose for which they were levied;

(ii) While rationally applying the resources, the capacity of the

Ministry/Department or the progress of the scheme/programme is also

required to be taken into account;

(iii) Funds parked in the reserve/corpus funds operated in the Public

Account without being utilized create a liability to the Government on

one hand, the scarce resources of the Government are held in the

Public Account without productive application;

(iv) Keeping the money in the Public Account unutilized would deprive the

sectors/schemes/programmes where resources are needed for effective

implementation;

(v) Prudent financial management requires distribution of scarce resources

among various competing needs of the Government depending on the

requirement/progress of the Government schemes;

(vi) Transfer to the dedicated fund such as Prarambhik Shiksha Kosh is

based on estimated collection of education cess, which is approved by

Parliament through Appropriation Act. In case of excess collection

over estimated collection, the difference in the estimated collection and

actual collection cannot be transferred to the account without valid

appropriation;

(vii) Universal access levy (UAL), which is transferred to Universal Service

Obligation Fund (USOF), is not a cess and UAL forms part of non-tax

receipt of the Government. USOF has a huge commitment towards

implementation of National Optical Fibre Network and Government

will finance the expenditure on NOFN as and when the scheme picks

up;

(viii) It has been explained to the Public Accounts Committee by Ministry of

Finance, vide this Ministry’s letter dated 30.1.2016, that Government

may credit such funds to USOF for being utilized exclusively for

meeting Universal Service Obligation;

Report No. 27 of 2016

26

(ix) In case of Cess on Tea, Cess on Films, there are no dedicated funds

created in the Public Account for regulating the flow of funds.

However, it is incorrect to state that Government has spent less on

development of these sectors. Government is, in fact, spending

sufficient funds commensurate with receipts in the form of cesses in

these sectors; and

(x) It is therefore incorrect to state that Government did not transfer the

cesses/levies to the designated funds in order to achieve the fiscal

deficit as this observation would be narrow in perspective.

Reply of the Ministry is not acceptable on following grounds:

(i) The levy/cess collected are for specific purpose usages and to

provide the intended service in return of the cess/levy charged.

Hence, the Government has a specific responsibility and liability as

well for providing the service. Till the service is not rendered fully,

the unspent collections need to be transparently reflected in the

accounts of the Union Government.

(ii) In case of excess collection of cess than estimated in the Budget,

the transfer of such collection to the designated funds through the

Appropriation Act could also have been augmented through the

available mechanism of proposing Supplementary Demands for

Grants.

(iii) In respect of levy/cess for which comment has been made in the

para above, there exists specific purpose Funds in the Public

Account as detailed in Annex-3.3.

(iv) The UAL is a levy collected as a percentage of the revenue earned

by the operators under various licenses, to be utilised by the

Government for providing access to basic telegraph services in

rural and remote areas. Thus, being a specific purpose levy

accounted for under non-tax revenue has to be utilised for the

purpose for which it was collected. For its transparent accountal, a

separate USO Fund has been opened in the Public Account.

However, the position of unspent amount of levy so far collected

Report No. 27 of 2016

27

for this purpose has not been appearing in the USO Fund

maintained in the Public Account.

Recommendation: The Government may transfer specific purpose

levies/cess collected to the funds earmarked for the purpose.

3.2.5.4 Non recognition of losses under NSSF in CFI

National Small Savings Fund (NSSF) was created in Public Account in April

1999 with the Central Government taking up the responsibility of servicing the

small savings deposits. The fund receives money from subscribers of various

small saving schemes, and invests the balance available with it in Central and

State Government Securities. Before the NSSF was constituted, the small

savings receipts mobilised by the Union Government and on-lent to the States

were treated as capital expenditure of the Union Government and, accordingly,

calculated in its gross fiscal deficit. Shortfall in returns from loans given out of

small savings proceeds and the interest paid on small savings were accounted

for under CFI and hence calculated under its revenue deficit. After the

constitution of the NSSF, however, the income/deficit of NSSF is not being

reflected as part of the Union Government’s revenue deficit. This is because

NSSF operations are being accounted for in the Public Account, and around

half of the outstanding balances under NSSF are accounted for as Public

Account liabilities, instead of being accounted for as internal debt in the CFI.

In this context, the 14th FC had observed that the off-budget nature of NSSF

operations renders them outside the regulatory framework of the FRBM Act,

raising concerns of fiscal transparency and comprehensiveness.

At the end of FY 2014-15, total accumulated deficit in the operation of NSSF

was ` 90,707.56 crore. These deficits are in the nature of loss to the

Government which will have to be borne on revenue account, whenever the

liabilities under NSSF are fully and finally repaid. By keeping the annual loss

in the operation of NSSF under Public Account, the deficit figure for the

relevant year are not reflected fairly.

The Ministry stated (May 2016) that since inception of NSSF in Public

Account, the reflection of deficit as a separate identity is being carried out as

a policy matter approved by Ministry of Finance. It added that the accounting

procedure of NSSF was got approved by the office of Controller General of

Accounts with the office of the CAG. It further stated that outstanding liability

Report No. 27 of 2016

28

of the Central Government on account of NSSF is understated in the accounts

due to netting of NSSF investments in Special State government

securities/other securities and accumulated deficit. A footnote is inserted in

Statement No. 2 of the Finance Accounts showing total outstanding liabilities,

investments and deficits separately.

The issue relating to surplus/deficit in the operation of NSSF was deliberated

amongst the offices of the CAG, the CGA and the Budget Division of the

Ministry of Finance in April 2000. During the deliberation, it was brought out

by the office of the CGA that the deficit which had arisen in the first year of

operation would get adjusted as and when there would be surplus. The

operational loss, which was ` 1681.68 crore at the end of FY 1999-2000,

has steadily increased year after year to ` 90,707.56 crore at the end of FY

2014-15 requiring urgent intervention. Under the present system, the

subscribers of the National Small Savings Schemes on maturity of their

investment are paid (principal/interest) out of the current/fresh subscriptions

flowing to the schemes and operational loss of the year is absorbed in the

scheme itself. Mere disclosure by way of footnote in the Finance Accounts is

not sufficient to mitigate the concern.

Recommendation: A mechanism for recognizing the result of annual

operations of NSSF and its impact on the Government finances may be put in

place.

In reply to the audit recommendation, the Ministry accepted (June 2016) that

administrative intervention is required for making good the accumulated

losses which occurred in NSSF. It further added that if administrative decision

is taken to make good the progressive deficit, this needs to be provided in CFI

(with due appropriation authorised by Parliament) and this will have an

adverse impact on revenue/fiscal deficit of the Government.

Reply of the Ministry underscores the audit contention that the losses in NSSF

affect the computation of prescribed deficit indicators set out in the Act.

3.2.5.5 Net proceeds to States

In terms of Article 279 of the Constitution, the Comptroller and Auditor

General of India is required to ascertain and certify the ‘net proceeds’

(any tax or duty the proceeds thereof reduced by the cost of collection),

whose certificate shall be final.

Report No. 27 of 2016

29

During the certification of ‘net proceeds’ by the CAG, based on the

recommendations of the successive Finance Commissions, it was noticed that

during the period 1996-97 to 2014-15 an aggregated amount of ` 81,647.70

crore was short devolved to the States.

The Ministry stated (June 2016) that the accuracy of the figures intimated by

CAG are required to be ascertained and need to be reconciled with that of

Budget Division, Department of Economic Affairs as the calculations for

State’ share of Central Taxes and Duties are based on set practices and norms

which have been meticulously followed year after year.

With regard to certification of net proceeds of taxes, it is pertinent to mention