Embed Size (px)

Citation preview

REPORT OF EXAMINATION

OF THE

ANTHEM BLUE CROSS LIFE AND HEALTH INSURANCE COMPANY

AS OF

DECEMBER 31, 2013

Filed on April 5, 2017

TABLE OF CONTENTS PAGE

SCOPE OF EXAMINATION ............................................................................................ 1

SUBSEQUENT EVENTS ................................................................................................ 2

COMPANY HISTORY: .................................................................................................... 7 Capitalization ............................................................................................................. 7 Dividends Paid to Parent ........................................................................................... 8

MANAGEMENT AND CONTROL:................................................................................... 8 Management Agreements ........................................................................................ 10

TERRITORY AND PLAN OF OPERATION ................................................................... 12

REINSURANCE: ........................................................................................................... 13 Assumed .................................................................................................................. 13 Ceded ...................................................................................................................... 13

ACCOUNTS AND RECORDS ....................................................................................... 14

FINANCIAL STATEMENTS: ......................................................................................... 15 Statement of Financial Condition as of December 31, 2013 .................................... 16 Underwriting and Investment Exhibit for the Year Ended December 31, 2013 ........ 17 Reconciliation of Surplus as Regards Policyholders from December 31, 2009

through December 31, 2013 ............................................................................... 19

COMMENTS ON FINANCIAL STATEMENT ITEMS: .................................................... 20 Claims unpaid .......................................................................................................... 20 Accrued medical incentives ..................................................................................... 20 Unpaid claims adjustment expense ......................................................................... 20 Aggregate health policy reserves ............................................................................. 20 Aggregate life policy reserves .................................................................................. 20 Aggregate health claim reserves.............................................................................. 20

SUMMARY OF COMMENTS AND RECOMMENDATIONS: ........................................ 20 Current Report of Examination ................................................................................ 20 Previous Report of Examination .............................................................................. 20

ACKNOWLEDGMENT .................................................................................................. 21

Los Angeles, California March 8, 2017

Honorable Dave Jones Insurance Commissioner California Department of Insurance Sacramento, California

Dear Commissioner:

Pursuant to your instructions, an examination was made of the

ANTHEM BLUE CROSS LIFE AND HEALTH INSURANCE COMPANY

(hereinafter also referred to as the Company) at the primary location of its books and

records at 120 S. Via Merida, Thousand Oaks, California 91362. The Company’s

statutory office is located at 21555 Oxnard Street, Woodland Hills, California 91367.

SCOPE OF EXAMINATION

We have performed our multi-state examination of the Company. The previous

examination of the Company was made as of December 31, 2009. This examination

covers the period from January 1, 2010 through December 31, 2013. The examination

was conducted in accordance with the National Association of Insurance

Commissioners’ Financial Condition Examiners’ Handbook (Handbook). The Handbook

requires the planning and performance of the examination to evaluate the Company’s

financial condition, to identify prospective risks, and to obtain information about the

Company, including corporate governance, identification and assessment of inherent

risks, and the evaluation of the system controls and procedures used to mitigate those

risks. The examination also included an assessment of the principles used and the

significant estimates made by management, as well as an evaluation of the overall

financial statement presentation, and management’s compliance with Statutory

Accounting Principles and Annual Statement instructions. All accounts and activities of

2

the Company were considered in accordance with the risk-focused examination

process.

The examination was a coordinated examination with Indiana as the Lead State, and

was conducted concurrently with examinations of other insurance entities within the

WellPoint Group of Companies (“WellPoint”).

In addition to those items specifically commented upon in this report, other phases of

the Company’s operations were reviewed including the following areas that require no

further comment: corporate records; fidelity bonds and other insurance; pensions, stock

ownership; growth of company; statutory deposits; and loss experience.

SUBSEQUENT EVENTS

During 2014, the Company’s ultimate parent, WellPoint, Inc., changed its name to

Anthem, Inc.

During February 2015, Anthem, and entities, were the target of a sophisticated external

cyber-attack. The attackers gained unauthorized access to certain information

technology systems and obtained personal information related to many individuals and

employees, such as names, birthdates, health care identification/social security

numbers, street addresses, email addresses, phone numbers and employment

information, including income data. To date, there is no evidence that credit card or

medical information, such as claims, test results or diagnostic codes, were targeted,

accessed or obtained, although no assurance can be given that they will not

identify additional information that was accessed or obtained.

Upon discovery of the cyber-attack, Anthem took immediate action to remediate the

security vulnerability and retained a cyber-security firm to evaluate the systems and

identify solutions based on the evolving landscape and has continued to implement

security enhancements since this incident. Anthem is providing credit monitoring and

3

identity protection services to those who have been affected by this cyber-attack.

Subsequent to the cyber-attack Anthem has incurred expenses to investigate and

remediate this matter and expects to continue to incur expenses of this nature in the

foreseeable future and will recognize these expenses in the periods in which they are

incurred.

Actions have been filed in various federal and state courts and other claims have been

or may be asserted against Anthem on behalf of current or former members, current or

former employees, other individuals, shareholders or others seeking damages or other

related relief, allegedly arising out of the cyber-attack. State and federal agencies,

including state insurance regulators, state attorneys general, the Health and Human

Services Office of Civil Rights and the Federal Bureau of Investigation, are investigating

events related to the cyber-attack, including how it occurred, its consequences and

Anthem’s responses. Although Anthem is cooperating in these investigations, Anthem

may be subject to fines or other obligations, which may have an adverse effect on how

they operate their business and their results of operations. With respect to the civil

actions, a motion to transfer was filed with the Judicial Panel on Multidistrict Litigation in

February 2015 and was subsequently heard by the Panel in May 2015. In June 2015,

the Panel entered its order transferring the consolidated matter to the U.S. District

Court for the Northern District of California. The U.S. District Court entered its case

management order in September 2015. Anthem filed a motion to dismiss ten of the

counts that are before the U.S. District Court. In February 2016, the court issued an

order granting in part and denying in part their motion, dismissing three counts with

prejudice, four counts without prejudice and allowing three counts to proceed. Plaintiffs

filed a second amended complaint in March 2016, and Anthem subsequently filed a

second motion to discuss. In May 2016, the court issued an order granting in part and

denying in part their motion, dismissing one count with prejudice, dismissing certain

counts asserted by specific named plaintiffs with or without prejudice depending on their

individualized facts, and allowing the remaining counts to proceed. In July 2016,

plaintiffs filed a third amended complaint which Anthem answered in August 2016. Fact

discovery is scheduled to be completed by December 2016. There remain two state

4

court cases that are presently proceeding outside of the Multidistrict Litigation. Anthem

has contingency plans and insurance coverage for certain expenses and potential

liabilities of this nature. While a loss from these matters is reasonably possible, Anthem

cannot reasonably estimate a range of possible losses because their investigation into

the matter is ongoing, the proceedings remain in the early stages, alleged

damages have not been specified, there is uncertainty as to the likelihood of a class

or classes being certified or the ultimate size of any class if certified, and there are

significant factual and legal issues to be resolved.

On July 24, 2015, the Company's ultimate parent company, Anthem, and Cigna

Corporation (Cigna) entered into an Agreement and Plan of Merger dated as of

July 23, 2015, by and among Anthem, Cigna, and Anthem Merger Sub Corp., a

Delaware corporation and a direct wholly-owned subsidiary of Anthem, pursuant to

which Anthem will acquire all outstanding shares of Cigna, or the Acquisition. The

Acquisition will further Anthem’s goal of creating a premium health benefits

company with critical diversification and scale to lead the transformation of health care

delivery for consumers. Cigna is a global health services organization that delivers

affordable and personalized products and services to customers through employer-

based, government-sponsored and individual coverage arrangements. All of Cigna’s

products and services are provided exclusively by or through its operating subsidiaries,

including Connecticut General Life Insurance Company, Cigna Health and Life

Insurance Company, Life Insurance Company of North America and Cigna Life

Insurance Company of New York. Such products and services include an integrated

suite of health services, such as medical, dental, behavioral health, pharmacy, vision,

supplemental benefits, and other related products including group life, accident and

disability insurance. Cigna maintains sales capability in 30 countries and jurisdictions.

Under the terms of the Merger Agreement, Cigna’s shareholders will receive $103.40 in

cash and 0.5152 shares of Anthem’s common stock for each Cigna common share

outstanding. The value of the transaction is estimated to be approximately $53.0 billion

based on the closing price of Anthem’s common stock on the New York Stock

Exchange on July 23, 2015. The final purchase price will be determined based on

5

Anthem’s closing stock price on the date of closing of the Acquisition. The combined

company will reflect a pro forma equity ownership comprised approximately 67%

Anthem shareholders and approximately 33% Cigna shareholders. Anthem expects to

finance the cash portion of the Acquisition through available cash on hand and the

issuance of new debt. Anthem entered into a bridge facility commitment letter and a

joinder agreement with a group of lenders which will provide up to $22.5 billion under a

364-day senior unsecured bridge term loan credit facility to finance the Acquisition in the

event that Anthem has not received proceeds from any combination of (i) senior

unsecured term loans, (ii) common or preferred equity or equity-linked securities

and/or (iii) senior unsecured notes in a public offering or private placement in an

aggregate principal amount of at least $22.5 billion prior to the consummation of the

Acquisition. In addition, in August 2015, Anthem entered into a term loan facility which

will provide up to $4.0 billion to finance a portion of the Acquisition. The commitment of

the lenders to provide the bridge facility and the term loan facility is subject to several

conditions, including the completion of the Acquisition. On July 21, 2016, the U.S.

Department of Justice, or DOJ, along with certain state attorneys general, filed a civil

antitrust lawsuit in the U.S. District Court for the District of Columbia seeking to block

the Acquisition. Trial commenced on November 21, 2016. On January 18, 2017,

Anthem provided notice to Cigna that Anthem had elected to extend the termination

date under the Merger Agreement from January 31, 2017 until April 30, 2017. Following

the conclusion of the trial, the Court ruled in favor of the DOJ, on February 8, 2017, and

Anthem promptly filed notice that Anthem would appeal the Court's ruling. On February

14, 2017, Cigna purported to terminate the Merger Agreement and commenced

litigation against Anthem in the Delaware Court of Chancery, or Delaware Court,

seeking damages and a declaratory judgment that its purported termination of the

Merger Agreement was lawful, among other claims. Anthem believes Cigna's

allegations are without merit. Also on February 14, 2017, Anthem initiated its own

litigation against Cigna in the Delaware Court seeking a temporary restraining order to

enjoin Cigna from terminating the Merger Agreement, specific performance compelling

Cigna to comply with the Merger Agreement and damages. On February 15, 2017, the

Delaware Court granted Anthem's motion for a temporary restraining order and issued

6

an order enjoining Cigna from terminating the Merger Agreement. The temporary

restraining order became effective immediately and will remain in place pending any

further order from the Delaware Court. Anthem intends to vigorously defend the

Acquisition in both the Circuit Court and the Delaware Court and remains committed to

completing the Acquisition as soon as practicable.

On December 1, 2016, a Regulatory Settlement Agreement, (RSA) was entered into by

Anthem and the California Department of Insurance, Indiana Department of Insurance

(INDOI), Maine Bureau of Insurance, Missouri Department of Insurance, New

Hampshire Insurance Department, North Dakota Department of Insurance, and South

Carolina Department of Insurance (collectively, the "Lead Regulators") and the

insurance regulatory departments, divisions, or offices of each of the remaining states

and U.S. jurisdictions that adopt, agree to, and approve this Agreement ( the

"Participating Regulators"). This RSA resulted from the targeted multi-state market

conduct and financial examination initially called by the lNDOI as lead domestic

regulator on February 26, 2015, as a result of Anthem's announcing of the cyber-

security breach noted above. The purpose of the examination was to assess Anthem's

state of cyber-security preparedness prior to the Data Breach, its post-Data Breach

response, the adequacy of measures taken by the Company to mitigate the harm to

consumers whose personally identifiable information (PIT) was compromised, and

determine the identity of the persons responsible for the breach. "The results of this

examination found that a) Anthem's pre-breach cyber-security was reasonable and

included the implementation of technologies and procedures consistent with or

exceeding those of a typical organization of its size and type; b) Anthem's preparations

to respond to a data breach began well before the incident occurred and included a

detailed Incident Response Plan (IR Plan); c) The Company's IR Plan allowed it to

timely and effectively respond to the Data Breach when it was discovered, removing

the attacker's ability to access the network within three days of identifying the Data

Breach; d) The examiners identified the attacker with high confidence and concluded

with medium confidence that the attacker was acting on behalf of a foreign

government. Attacks associated with this foreign government have not resulted in PIT

7

being transferred to non-state actors; e) Anthem promptly communicated and

cooperated with law enforcement and regulatory officials; f) Anthem provided affected

individuals with notice through direct mailing, emailing, news publications, website

notice, and working with state insurance departments; g) Within two weeks of

discovering the Data Breach, Anthem contracted with a vendor to provide credit

protection services for two years to breach-impacted consumers; and h)

Immediately following discover of the Data Breach, Anthem engaged expert consultants

to investigate the Data Breach and assist Anthem with its post-breach response. To

date, Anthem has already incurred significant costs related to the Data Breach: $2.5

million to engage expert consultants; $115 million for the implementation of security

improvements; $31 million to provide initial notification to the public and affected

individuals; and $112 million to provide credit protection to breach-impacted consumers.

In light of the facts set forth, the corrective actions already implemented by Anthem, and

the Additional Corrective Actions agreed to, the Lead Regulators find that administrative

fines or penalties are not warranted. Additional Corrective Actions include a) Continued

implementation of enhanced security measures at an estimated additional cost of at

least $30 million; b) Continuation of cyber-security monitoring; and c) Anthem Minor

Credit Protection Program at an estimated additional cost of at least $15 million.

COMPANY HISTORY

On October 4, 2007 the California Department of Insurance approved an amended

Certificate of Authority to change the Company’s name from BC Life & Health Insurance

Company to Anthem Blue Cross Life and Health Insurance Company.

Capitalization

The Company is authorized to issue 250,000 shares of Class A voting common stock

with a par value of $100 per share. As of December 31, 2013, there were 50,000

shares outstanding.

8

Dividends Paid to Parent

The Company paid the following ordinary cash dividends to its parent, WellPoint

California Services, Inc., during the examination period:

Year Amount 2012 $ 192,000,000 2013 321,300,000 Total $ 513,300,000

MANAGEMENT AND CONTROL

The Company is a member of an insurance holding company system. WellPoint, Inc.,

is one of the largest health benefits companies in the United States. WellPoint, Inc., is

the ultimate controlling entity. The following abridged chart, which is limited to the

Company’s ultimate parent and its affiliates, depicts the Company’s relationship within

the holding company system:

9

WellPoint, Inc. (Indiana)

Anthem Holding Corp. (Indiana)

WellPoint California Services, Inc. (Delaware)

Blue Cross of California (California)

(CA)

Anthem Blue Cross Life and Health Insurance Company

(California)

Golden West Health Plan, Inc.

(California)

Park Square I, Inc. (California)

Park Square Holdings, Inc. (California)

Park Square II, Inc. (California)

(*) all ownership is 100% unless otherwise noted.

Management of the Company is vested in a three-member board of directors elected

annually. A listing of the members of the board and principal officers serving on

December 31, 2013 follows:

10

Directors

Name and Residence Principal Business Affiliation

Wayne Scott DeVeydt Indianapolis, Indiana

Senior Vice President and Chief Financial Officer WellPoint, Inc.

Catherine Irene Kelaghan Carmel, Indiana

Vice President and Counsel WellPoint, Inc.

Mark James Morgan Newbury Park, California

President and Chief Executive Officer Anthem Blue Cross Life and Health Insurance Company

Principal Officers

Name Title

Mark James Morgan (*) President and Chief Executive Officer Cassie Shuang Kam (**) Chief Financial Officer Robert David Kretschmer Treasurer Kathleen Susan Kiefer Secretary George Lewis Chartrand Assistant Secretary Eric Kenneth Noble Assistant Treasurer

(*) Replaced by John Brian Ternan, effective May 26, 2015 as President and Chief

Executive Officer

(**) Replaced by Jay Reginald King, effective September 5, 2014

Management Agreements

Amended and Restated Master Administrative Services Agreement: Effective

January 1, 2004, the Company and its ultimate parent, WellPoint, Inc., entered into an

amended and restated Master Administrative Services Agreement. The initial term of

the agreement was for one year and continued for successive yearly renewal terms.

The agreement can be terminated by either party by providing a one year notice prior to

the expiration of any renewal. Under the terms of the agreement, WellPoint, Inc.

11

provides space and various administrative, management and support services to the

Company. The cost and expenses related to the services provided are allocated in an

amount equal to the direct and indirect costs and expenses incurred in providing such

services. The Company reimbursed WellPoint, Inc. for the actual cost of these services.

For 2010, 2011, 2012, and 2013, the Company paid $932,094,903, $956,091,251,

$914,692,907, and $955,190,143, respectively, in fees to WellPoint, Inc. under the

terms of this agreement. The California Department of Insurance (CDI) approved the

amended agreement on June 15, 2010.

Administrative Services Agreement: Effective August 1, 2003, the Company and its

affiliate, Worldwide Insurance Services, Inc. (WIS), a Virginia corporation, entered into

an Administrative Services Agreement. Under the terms of the agreement, WIS

provides a variety of administrative services, including: underwriting, pricing of risk,

premium and fee administration, policy and contract administration, policyholder and

customer services, claims administration, and management of third party vendors.

Third party vendors include preferred provider organizations and other vendors who

provide services with respect to reinsured policies of the Company under a coinsurance

agreement with HTH Re. Ltd., a Bermuda reinsurer. The Company paid WIS for the

actual cost of these services. For 2010, 2011, 2012, and 2013, the Company paid

$2,269,410, $2,242,762, $3,837,551 and $4,093,874, respectively, in fees to WIS under

the terms of this agreement. The CDI approved this agreement on

September 21, 2007.

Subcontractor Services Agreement: Effective August 1, 2003, the Company and its

affiliate, WIS, entered into a Subcontractor Services Agreement. Under the terms of the

agreement, the Company provides WIS the following services: claims adjudication

services, customer services, personnel, and management services. Fees charged by

the Company under this agreement are $9.30 per claim, with additional access fees

calculated based on claims experience. For 2010, 2011, 2012, and 2013, the Company

received $894,815, $991,470, $1,174,549, and $1,346,422, respectively, in fees from

WIS under the terms of this agreement. The CDI approved this agreement on

12

August 21, 2007.

Pharmacy Benefits Administrative Services Agreement: Effective December 1, 2009,

the Company entered into a Pharmacy Benefits Administrative Services Agreement with

its ultimate parent, WellPoint, Inc. The agreement replaces and supersedes the

previous Pharmacy Benefit Services Management Agreement between the Company

and NextRx Services, Inc. (previously Professional Claim Services, Inc. dba WellPoint

Pharmacy Management). Under the terms of the agreements, WellPoint, Inc. retained

Express Scripts, Inc. to provide certain pharmacy benefit management services to the

members of WellPoint, Inc.’s affiliated health plans, including the Company. The CDI

approved this agreement on October 6, 2009.

Consolidated Tax Allocation Agreement: Effective December 31, 2005, the Company

and its affiliates are part of a Consolidated Tax Allocation Agreement with its ultimate

parent, WellPoint, Inc., and its subsidiaries. Allocation of taxes is based upon separate

return calculations. The intercompany income tax balances are settled based on the

Internal Revenue Service due dates. The CDI approved this agreement on

April 26, 2007.

TERRITORY AND PLAN OF OPERATION

The Company is licensed to transact life and disability insurance solely in the State of

California. The Company offers traditional medical and dental coverage, as well as

preferred provider organization and indemnity coverage, and provides administrative

services relating to health plans for self-insured employers. The Company also writes

life insurance for individuals and group term life insurance for small and large employer

groups. The Company’s total direct written premium for the year ending 2013 was $5.3

billion. The written premium was comprised of group accident and health insurance,

$2.7 billion (51%), other accident and health insurance of $2.6 billion (48%) and group

and ordinary life, $46.5 million (1%).

13

The Company operates as a licensee of the Blue Cross Blue Shield Association. The

Company services approximately 3.4 million members. The Company does not have its

own employees. Services are provided to the Company by its affiliate, Blue Cross of

California. The Company markets its products through independent agents and direct

marketing.

REINSURANCE

Assumed

The Company has no reinsurance assumed.

Ceded

The following is a summary of the principal ceded reinsurance treaties in force as of

December 31, 2013:

Type of Contract Reinsurer’s Name Company’s Retention Reinsurer’s Maximum Limits

Health Coverage for International Students

HTH Re, Ltd. 80% and 100% Quota Share

20% and 0% Quota Share

Individual Long Term Care various years and plans

General Reins Corp (formerly Cologne Life Reinsurance Company)

80% Quota Share 20% Quota Share

Individual Long Term Care various years and plans

Gen Re Life Corp (formerly Cologne Life Reinsurance Company)

40% Quota Share 60% Quota Share

Individual Long Term Care various years and plans

Westport (formerly Employers Reinsurance Corporation)

60% Quota Share 40% Quota Share

Life and AD&D

Hartford Life and Accident Insurance Company

$300,000 per life Not to exceed $1,700,000 per person

Chiropractic Claims & Expenses for commercial PPO members

American Specialty Health Insurance Company

100% Quota Share 0% Quota Share

14

As of December 31, 2013, reinsurance recoverable for all ceded reinsurance totaled

$0.5 million or 0.04% of surplus as regards policyholders. The ceded reinsurance

recoverable was 100% from non-affiliated admitted reinsurers.

ACCOUNTS AND RECORDS

California Insurance Code (CIC) Section 735 states that the Company must inform the

board members of the receipt of the examination report. The board should be informed

of the report both in the form first formally prepared by the examiners and in the form as

finally settled and officially filed by the commissioner. The board must also enter that

fact in the board minutes. A review of the board minutes disclosed that, while the draft

was presented to the board, the officially filed report was not presented.

It is recommended that the Company implement procedures to ensure future

compliance with CIC Section 735.

15

FINANCIAL STATEMENTS

The financial statements prepared for this examination report include:

Statement of Financial Condition as of December 31, 2013 Underwriting and Investment Exhibit for the Year Ended December 31, 2013 Reconciliation of Surplus as Regards Policyholders from December 31, 2009 through December 31, 2013 Reconciliation of Examination Changes as of December 31, 2013

16

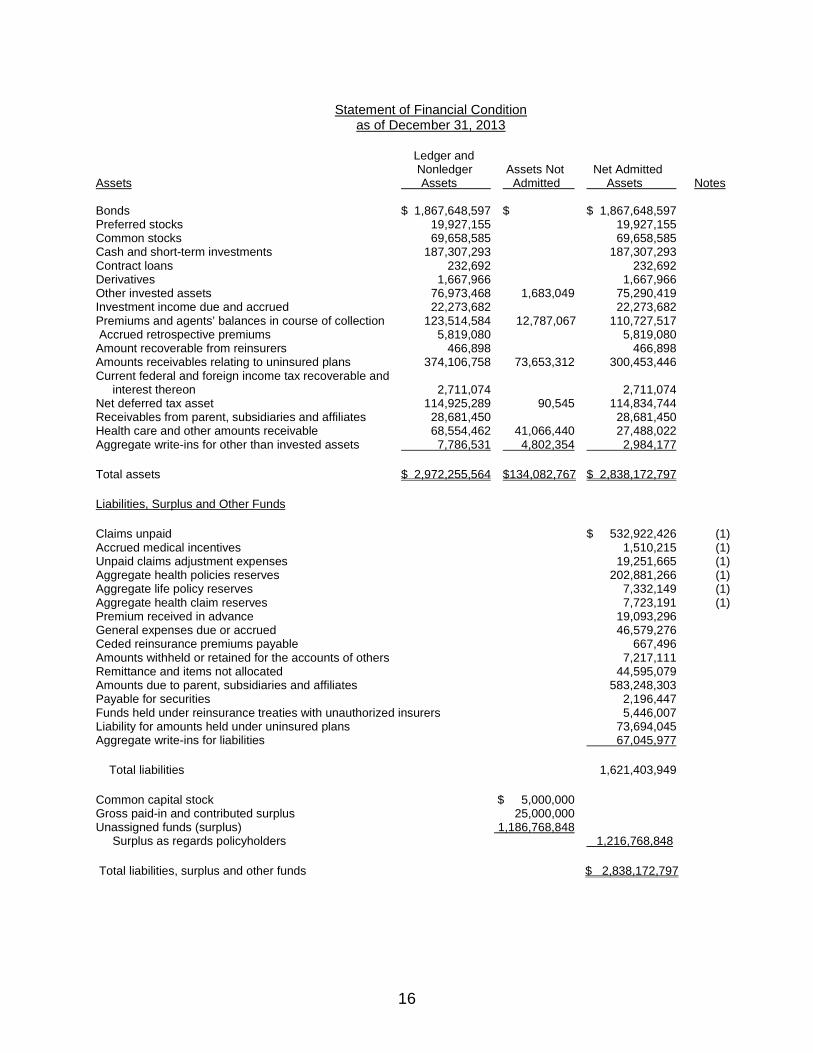

Statement of Financial Condition as of December 31, 2013

Ledger and Nonledger Assets Not Net Admitted Assets Assets Admitted Assets Notes Bonds $ 1,867,648,597 $ $ 1,867,648,597 Preferred stocks 19,927,155 19,927,155 Common stocks 69,658,585 69,658,585 Cash and short-term investments 187,307,293 187,307,293 Contract loans 232,692 232,692 Derivatives 1,667,966 1,667,966 Other invested assets 76,973,468 1,683,049 75,290,419 Investment income due and accrued 22,273,682 22,273,682 Premiums and agents’ balances in course of collection 123,514,584 12,787,067 110,727,517 Accrued retrospective premiums 5,819,080 5,819,080 Amount recoverable from reinsurers 466,898 466,898 Amounts receivables relating to uninsured plans 374,106,758 73,653,312 300,453,446 Current federal and foreign income tax recoverable and interest thereon 2,711,074 2,711,074 Net deferred tax asset 114,925,289 90,545 114,834,744 Receivables from parent, subsidiaries and affiliates 28,681,450 28,681,450 Health care and other amounts receivable 68,554,462 41,066,440 27,488,022 Aggregate write-ins for other than invested assets 7,786,531 4,802,354 2,984,177

Total assets $ 2,972,255,564 $134,082,767 $ 2,838,172,797

Liabilities, Surplus and Other Funds

Claims unpaid $ 532,922,426 (1) Accrued medical incentives 1,510,215 (1) Unpaid claims adjustment expenses 19,251,665 (1) Aggregate health policies reserves 202,881,266 (1) Aggregate life policy reserves 7,332,149 (1) Aggregate health claim reserves 7,723,191 (1) Premium received in advance 19,093,296 General expenses due or accrued 46,579,276 Ceded reinsurance premiums payable 667,496 Amounts withheld or retained for the accounts of others 7,217,111 Remittance and items not allocated 44,595,079 Amounts due to parent, subsidiaries and affiliates 583,248,303 Payable for securities 2,196,447 Funds held under reinsurance treaties with unauthorized insurers 5,446,007 Liability for amounts held under uninsured plans 73,694,045 Aggregate write-ins for liabilities 67,045,977

Total liabilities 1,621,403,949

Common capital stock $ 5,000,000 Gross paid-in and contributed surplus 25,000,000 Unassigned funds (surplus) 1,186,768,848 Surplus as regards policyholders 1,216,768,848

Total liabilities, surplus and other funds $ 2,838,172,797

17

Underwriting and Investment Exhibit for the Year Ended December 31, 2013

Statement of Income

Underwriting Income

Net Premium Income $5,314,570,413 Change in unearned premium reserve and reserves for rate credits 79,179,967 Aggregate write-ins for other non-health revenues 5,555 Total revenues $ 5,393,755,935

Deductions:

Hospital/Medical benefits $ 2,217,112,237 Other professional services 95,548,528 Outside referrals 261,595,408 Emergency room and out of area 1,046,739,495 Prescription drugs 724,898,436 Net incentive pools, withhold adjustments, and bonus amounts (509,349) Net reinsurance recoveries (12,704,988) Non-health claims (net) 25,055,952 Claims adjustment expenses including cost containment expenses 164,414,631 General and administrative expenses 628,000,242 Increase in reserve for life and accident and health contracts 69,112,680 Total underwriting deductions 5,219,263,272 Net underwriting gain 174,492,663

Investment Income

Net investment income earned $ 74,016,098 Net realized capital gain 20,231,806 Net investment gain 94,247,904

Other Income

Net loss from agents’ or premium balances charged off (amount charged off $594,588) $ (594,588) Aggregate write-ins for miscellaneous income 7,028,144

Total other income 6,433,556

Net income before federal income taxes 275,174,123 Federal and foreign income taxes incurred 106,271,175

Net income $ 168,902,948

18

Capital and Surplus Account

Surplus as regards policyholders, December 31, 2012 $ 1,361,040,897

Net income $ 168,902,948 Change in net unrealized capital losses (6,880,211) Change in net deferred income tax 25,406,696 Change in nonadmitted assets (10,401,482) Dividends to policyholders (321,300,000)

Change in surplus as regards policyholders for the year (144,272,049)

Surplus as regards policyholders, December 31, 2013 $ 1,216,768,848

19

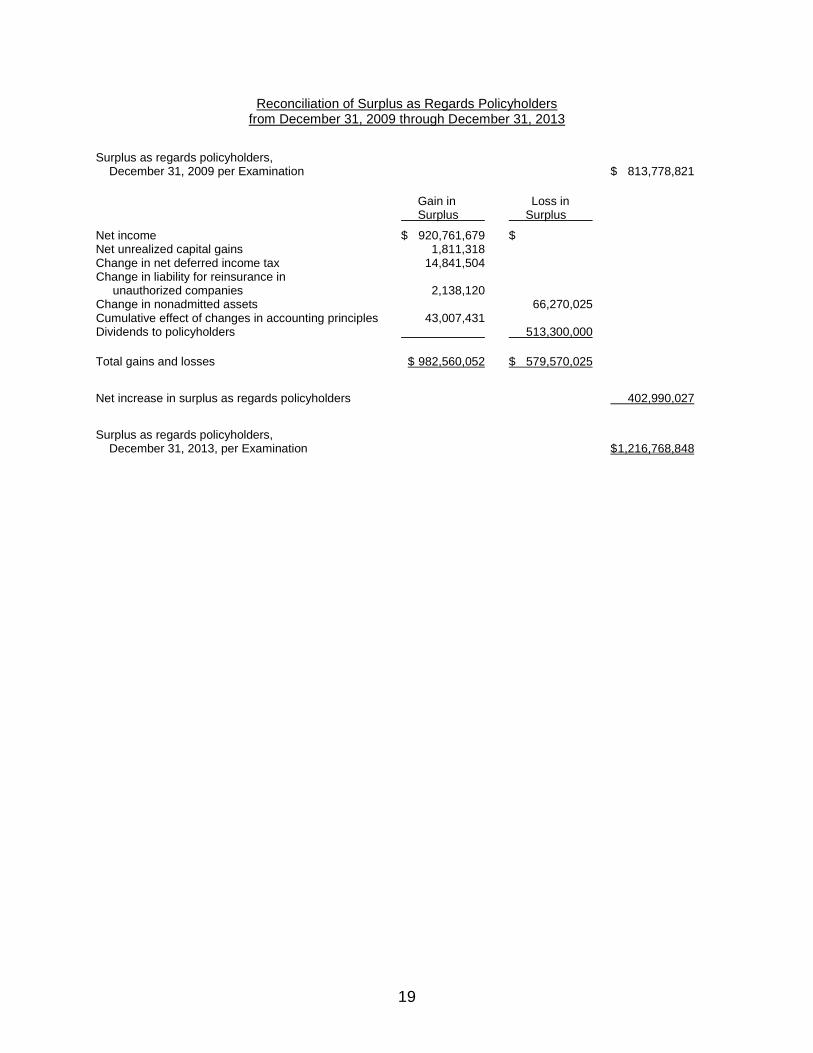

Reconciliation of Surplus as Regards Policyholders from December 31, 2009 through December 31, 2013

Surplus as regards policyholders, December 31, 2009 per Examination $ 813,778,821

Gain in Loss in Surplus Surplus

Net income $ 920,761,679 $ Net unrealized capital gains 1,811,318 Change in net deferred income tax 14,841,504 Change in liability for reinsurance in unauthorized companies 2,138,120 Change in nonadmitted assets 66,270,025 Cumulative effect of changes in accounting principles 43,007,431 Dividends to policyholders 513,300,000

Total gains and losses $ 982,560,052 $ 579,570,025

Net increase in surplus as regards policyholders 402,990,027

Surplus as regards policyholders, December 31, 2013, per Examination $ 1,216,768,848

20

COMMENTS ON FINANCIAL STATEMENT ITEMS (1) Claims unpaid (1) Accrued medical incentives (1) Unpaid claims adjustment expenses (1) Aggregate health policy reserves (1) Aggregate life policy reserves (1) Aggregate health claim reserves

The Company’s reserves were reviewed by the consulting actuarial firm of Merlinos and

Associates (Merlinos). The Indiana Department of Insurance retained Merlinos as part

of the coordinated examination of the WellPoint Group of Companies. Merlinos

concluded that the carried reserves as of December 31, 2013 were reasonable. In

addition, a Life Actuary from the California Department of Insurance (CDI) reviewed the

work of the consulting actuary and performed additional analysis as deemed

appropriate. The CDI actuary determined that the reserves were fairly stated.

SUMMARY OF COMMENTS AND RECOMMENDATIONS

Current Report of Examination

Accounts and Records – (Page 15): It is recommended that the Company implement

procedures in its board meetings to ensure compliance with CIC Sections 735.

Previous Report of Examination

None

21

ACKNOWLEDGMENT

Acknowledgment is made of the cooperation and assistance extended by the

Company’s officers and employees during the course of this examination.

Respectfully submitted,

_/S/__________________________

Cuauhtemoc Beltran, CFE Examiner-In-Charge Senior Insurance Examiner Department of Insurance State of California