Embed Size (px)

Citation preview

Report No. 5533-MAS

MauritiusAdjustment and GrowthCountry Economic MemorandumApril 11, 1985

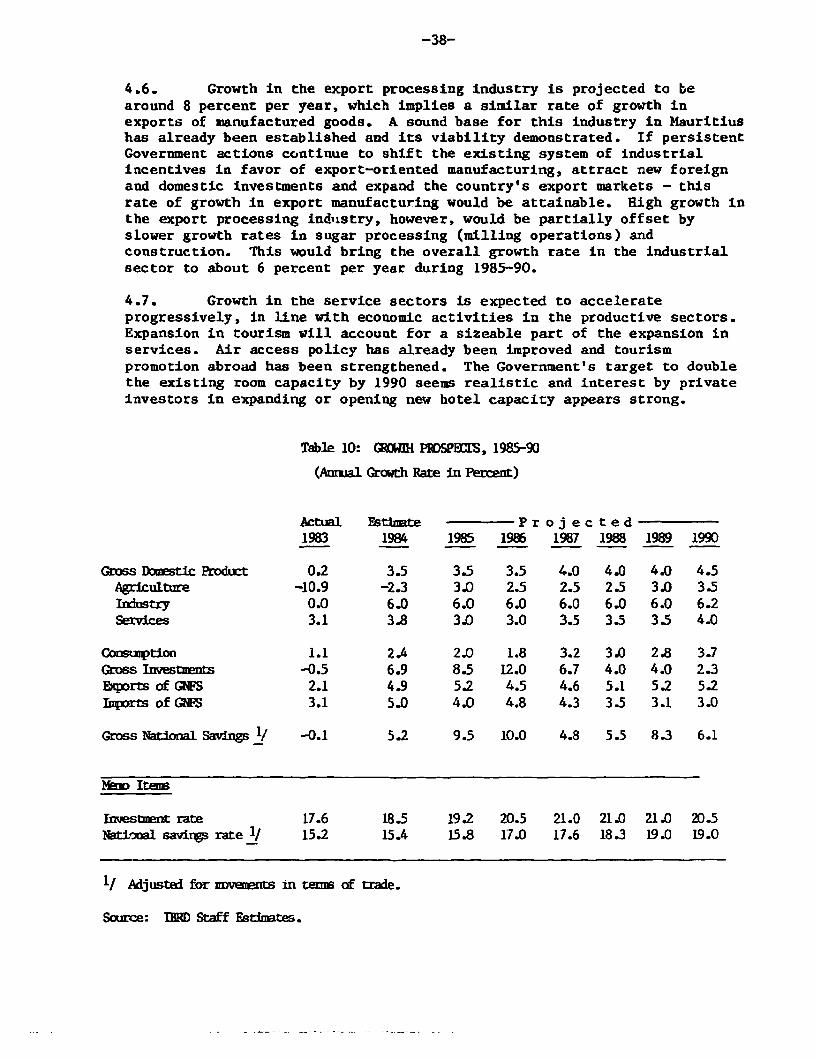

Country Programs Department 11Eastern and Southem Africa Region

FOR OFE iCIAL USE ONLY

~~~ ,J-~,,,-

:, * j F 7 2 _ g ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~--t--.0- - - i -

-~ ~ , . .-- - ' - ,- , - ,

- .. --

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performanceof theirofficial duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

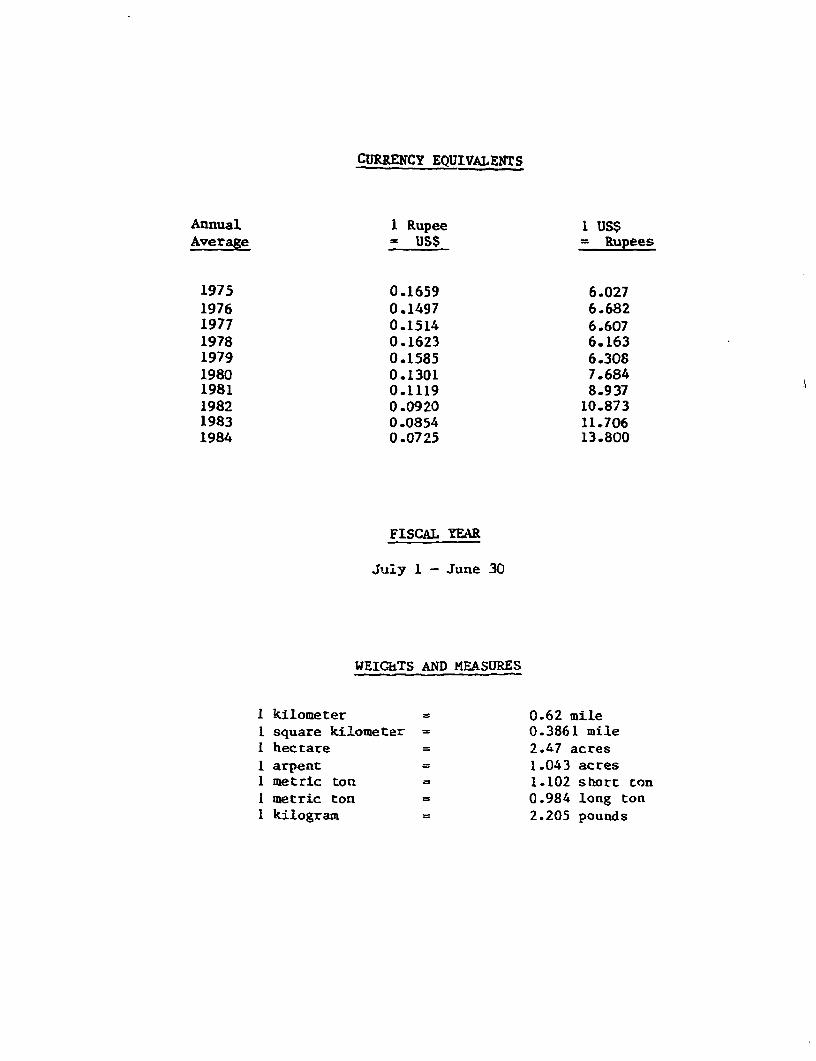

CURRENCY EQUIVALENTS

Annual 1 Rupee 1 US$Average = USS = Rupees

1975 0.1659 6.0271976 0.1497 6.6821977 0.1514 6.6071978 0.1623 6.1631979 0.1585 6.3081980 0.1301 7.6841981 0.1119 8.9371982 0.0920 10.8731983 0.0854 11.7061984 0.0725 13.800

FISCAL YEAR

july 1 - June 30

WEIGhTS AND MEASURES

1 kilometer = 0.62 mileI square kilometer = 0.3861 mileI hectare 2.47 acresI arpent 1.043 acres1 metric ton = 1.102 short ton1 metric ton 0.984 long ton1 kilogram = 2.205 pounds

(i) FOR OFFICIAL USE ONLY

MAIRTUS: AD TUSnfr AM GRa

wmxarmic Muu~

Tdae of Qxitens

axrN DMfge No

SU*M A IXUXUfSlOS

Fcsixc Strnktwe . . . . . . . . . . . . . . . . . . . . . 1iaormdc Pexfonrmame t 1979 . . . .*. . . .. . .. . . . . 2

-I. SnB.IZ SE 1979 AND ES= MOM=

St ai1i~.t1on Prcrw . . . . . . . . . . . ........ 3Structural Adjisnzt Progrm . . . . . . . . ....... 4Reent Ecmic Perfomnae (1979-1983) . . . . . . . . . . 6Deveioaets in 1984 . . . . . . . . . . . . . . . . . . . . 7Wage Poicy Arxl Bloyment . . . . . . . . . . . . . . . .. 9Fiscal PrUcy and PErfiormne . . . . . . . . . . .... . .. . 11Mnq anl Credit . . . . .. . . . . . . . . .* . . . . . .* . 13Bialae of Payments Derfornmme . . . . . . . . . . . . . . 16

125ctrnaldebt. . .. a. .. .. .. . .. .. ...... ................... 19

Ila. SAMEYKNR KUREM sSMUtRL AMD ELa! ADJSE

MIentaJming The Log Tern Viability of theipr SRh-Sector . . . . . . .. a ... .. . . ... . . . O 20

Agricxd.tra:L Diversification .. . .. . 26Refonn of Industrial Eblicies . . . . . . . . . . . 28Energy Ststivjtim, . . . . . . . . . . . .. 33

7macm1t Gnatliou ....... 33Population GCntrol . . . . . . . . . . . .. . . . 34

IV. FRSPE1S: AUJUSMEN! ANDGROM (1985-1990)

Growth Prospects . . . . . . . . . . . ... 36Pcblic Sector Investent Program . . . .. 38Finaring of the Piblic Setor lnvesbxmt PLgram. .. .. . 42Balaxe of PqEytj,ts Prospects . . . . . . . . . .. 44Thcternal Capitad Reqnrxe ts ....... .. . . . . . . 46Dlaside R1s And Creitworthirms . . . . .49

SIATI GNL Ae

This document has a restrited distribution and may be used by recipients only in the performance oftheir offcial duties Its contents may not otherwise be disclosed without World Bank authorization.

(i)

LIST OF M= TANS

1. wh of GDP by Main SCrs, 1979-19B4 6...... 62. Ire, Us6 Ard Savrgs, 1979-1984 9......093. Labor Farce. loyu2nt And Uimz1ouen . . .. ... . 104. OmatraJ Gaverrment Operatkm, 1980/81 - 1984/85. .. 125. Ymtr Eminn L97 - 1984 o........ 146. (oit EpmIion m Private Sector, 1979 - 1984 . . . 157. Balame of Paymews, 1981-194 .. . . ...... 168. iSports of Goods, 1979-18 . . -... . .. 0. 179. 1rport ByMjorCate,ries. 1979 -1984. *.... 18

10. GrowthProspecs, 1985 - 1990 .......... 3811. Pbl±c Sector Invtieznt Progg (PSP),

1984/85 - 1986/87 .0..0 ...... * *.... 4212. PSP An! its Fiz?rg, 1984/85 - 198889 . . . .0 . . 4413. Eqxort ProjectLoks, 1985 -1990 *. . . . . . . . 4614. Ba1 of paymmrs Ppro,ject1, 1985 - 1990 ..... 4715. a 1erid capital RePqxeimts, 1985 - 1990 . . . . . . 48

(ii)

LIS OF S1ATISML AN= MOM

I. Ebplaati and Bnployuft

1.1 1bPUJtioQ. 196O-641.2 Pobpulation by SEx and Age Group, Island of HMritlus1.3 Islad of Mzwitis: lBrth, Mortality and Fertility Rates1.4 eoyDet i Lage Estcbiss1.5 Re&stered U poyed

II. National Accotts

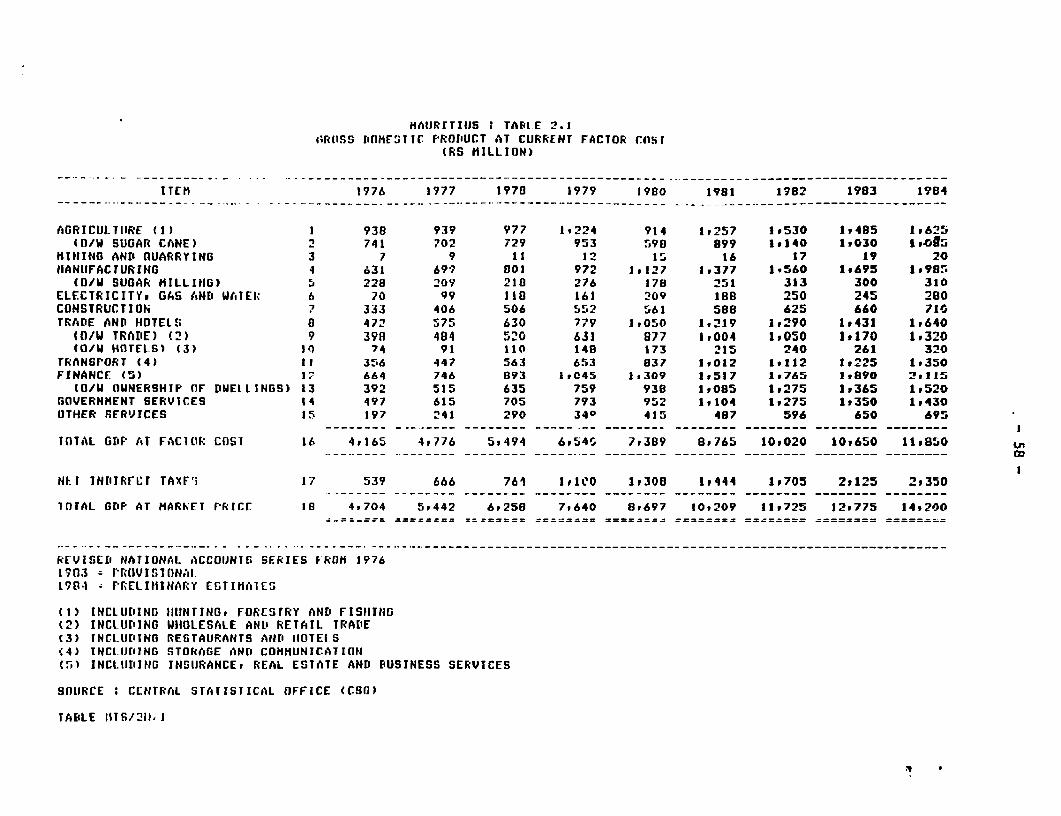

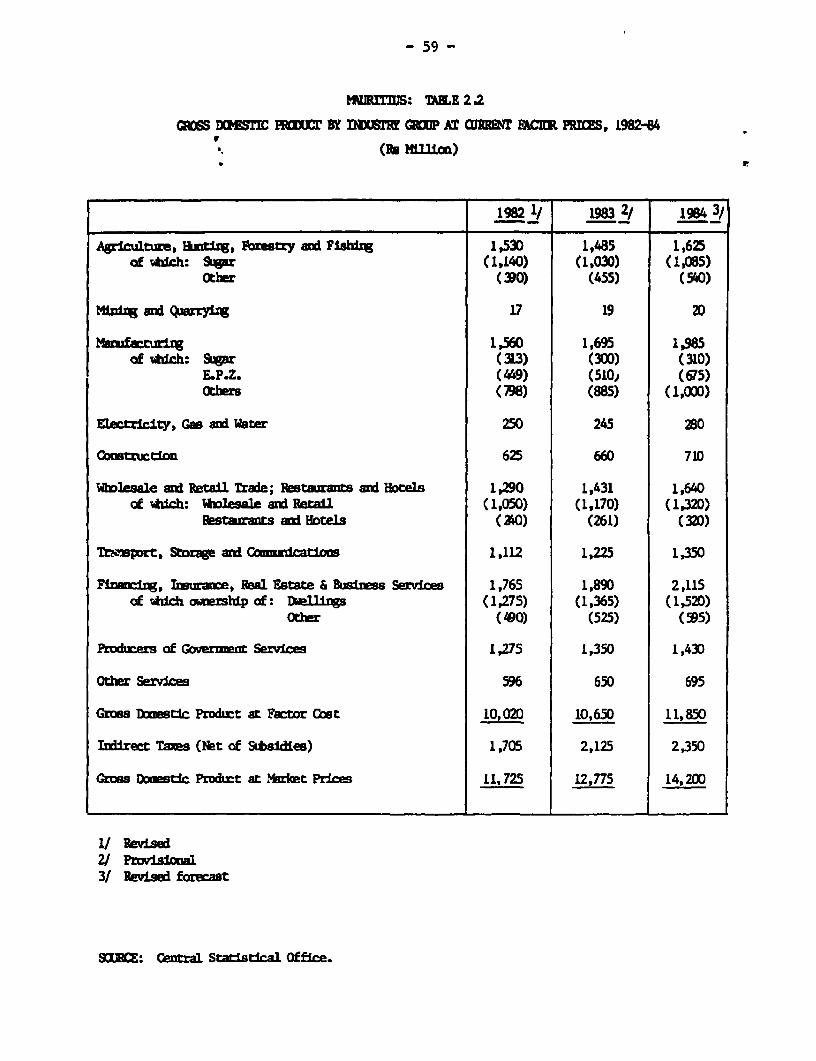

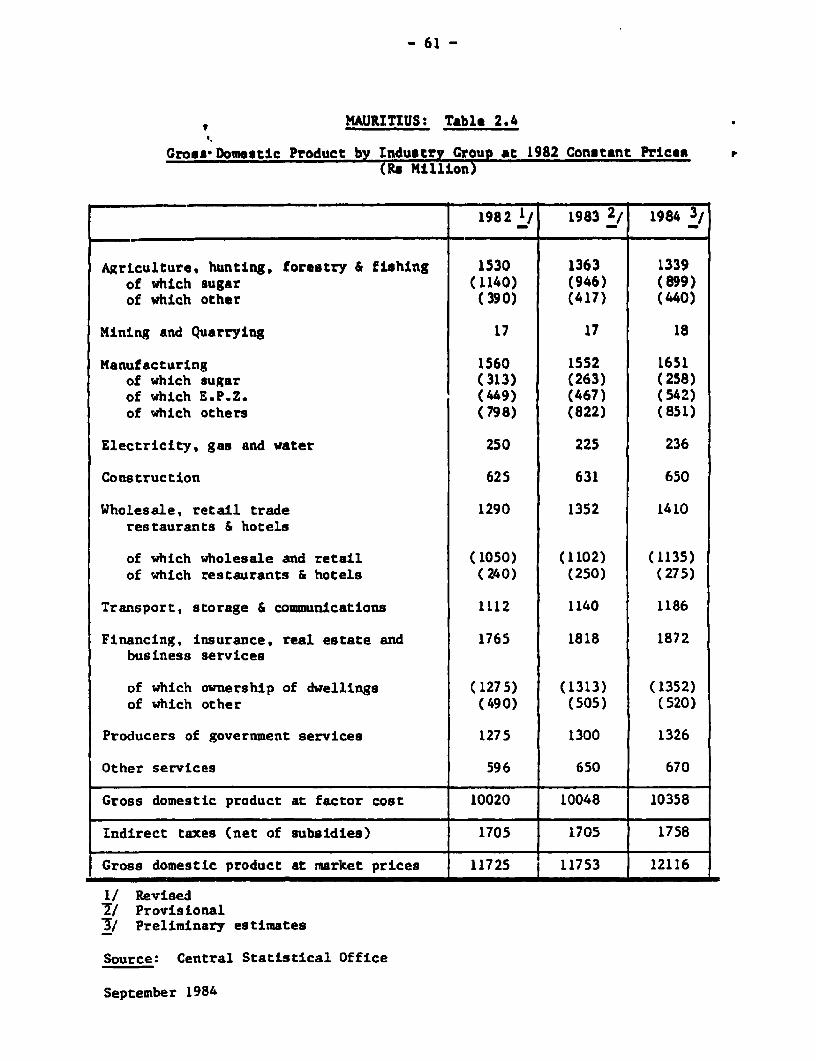

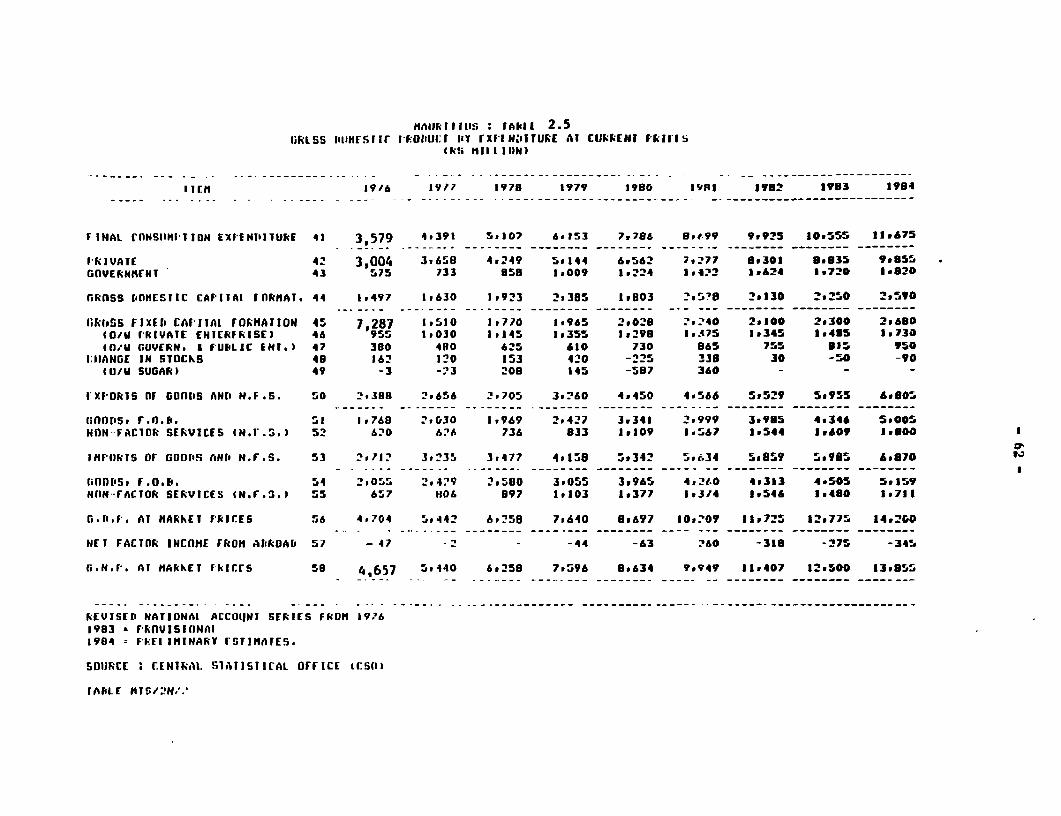

2.1 Gross Domestic prodlut at current Fawtr Cost, 1976-842.2 Gross 1ntic Product by Industry Group at Cwrreat Factor

Cost, 1982-842.3 Gross Dkmestic Product at 1976 Constant FactDr cost,

1976-822.4 Gross Ikmstic Rduct at 1982 Coostant FactOr Cost,

1982-842.5 Gross Jmestic Produc Expyaxiture at Qrert Erices,

1976-842.6 Gross lDomstlc Produrt by Expeiture at 1976 Cottnt

Plres, 1976-822.7 Gross Dkistic Product .by lptditure at 1982 Costant

Prices, 1982-842.8 Gcomasitioa of Gmoss Domestic Fied Cptal Fbnutin at

irrent and 1976 Coxtant PLces, 1976-822.9 Ccaposition. of Gross DoTstsic F1Ed Capital FEnition, at

1982 Ciostat Prices, 1982-84

MI. Balane of Payint and Eternal Trade

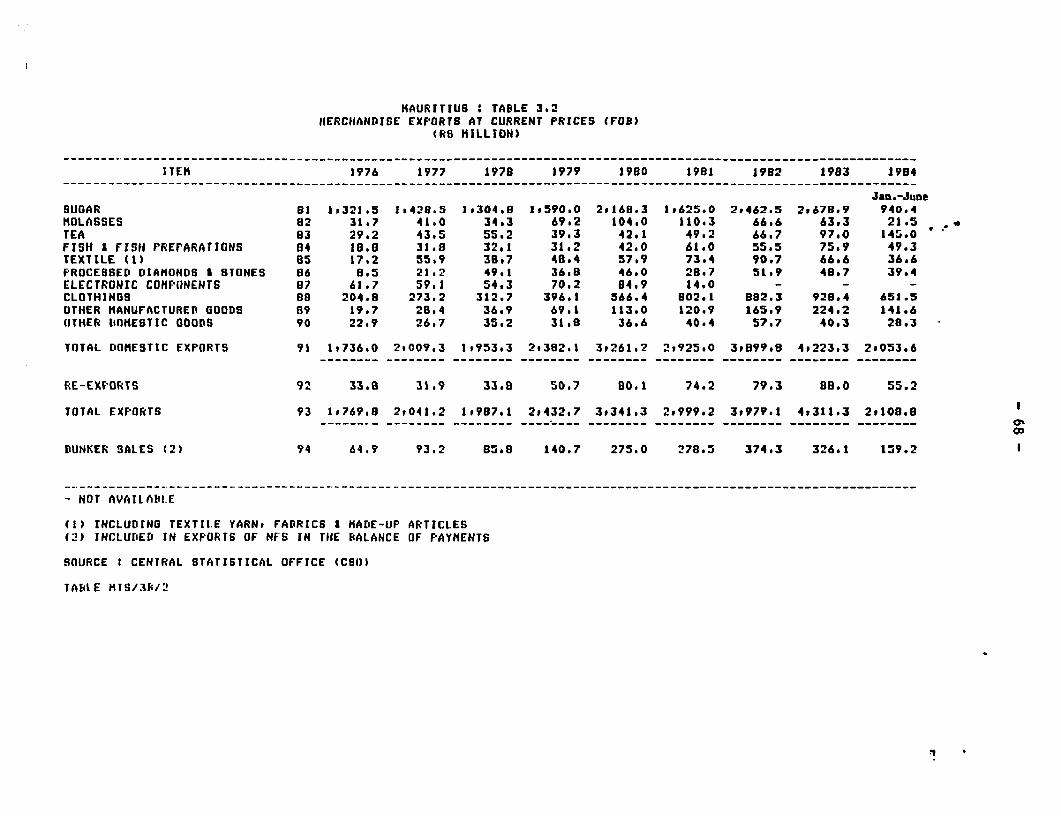

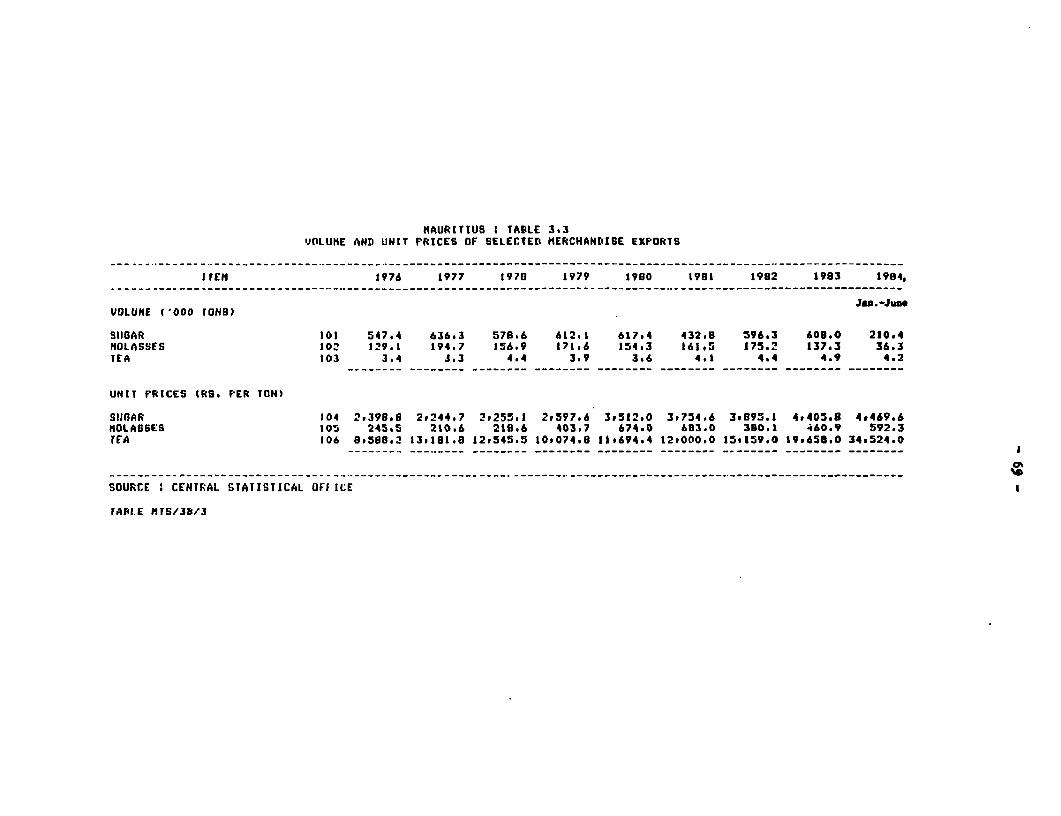

3.1 Ba of Payments, 1976843.2 trlhridise Exports at Qirrert Prices, 1976-843.3 Volum and Unit Prices cf Major Mechadise Exports,

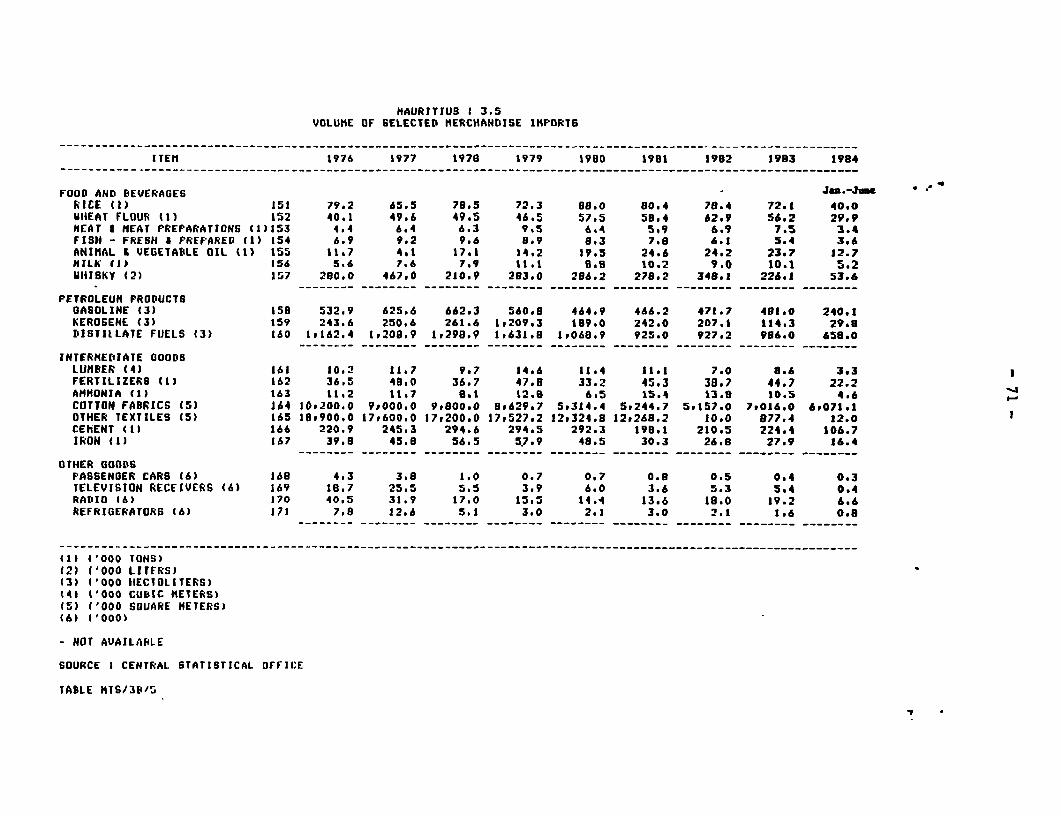

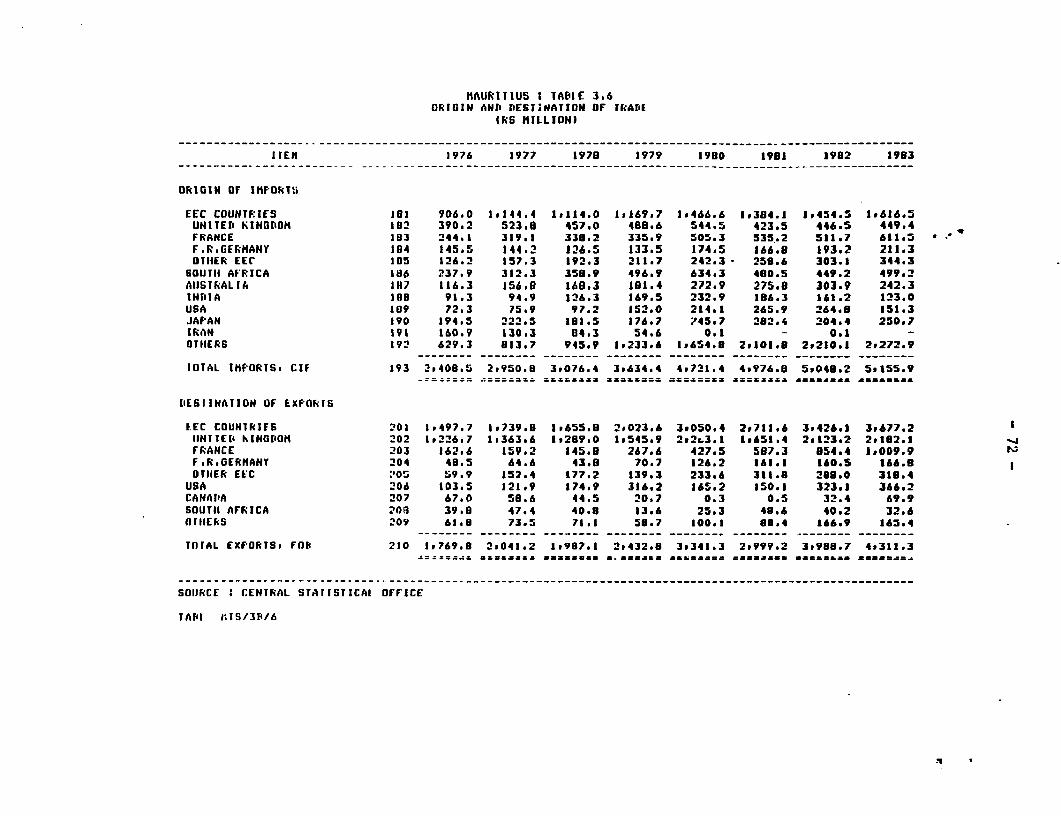

1976,843.'. sr dse bports at Qrren Praces, 1976-843.5 ol;re of Selted Merchaniise I1ports, 1976-843.L, OrigLn and Btinatim of frade, 1976-83

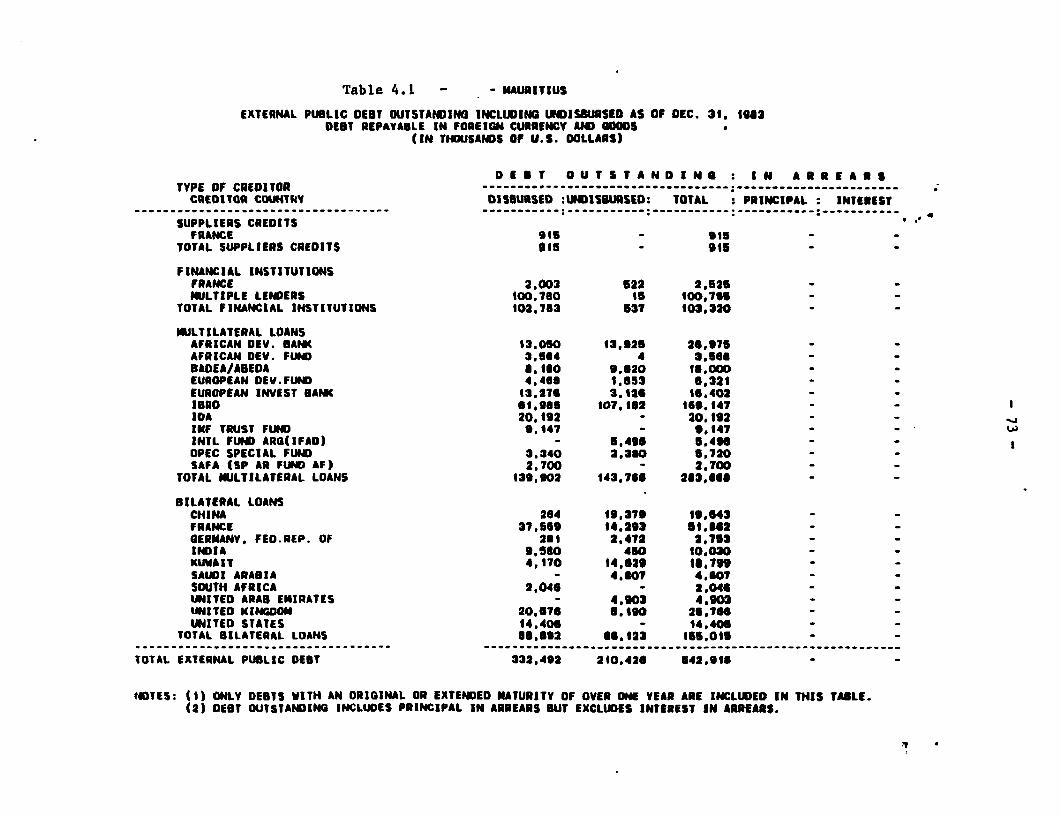

1NV7 Exteral DE!bt

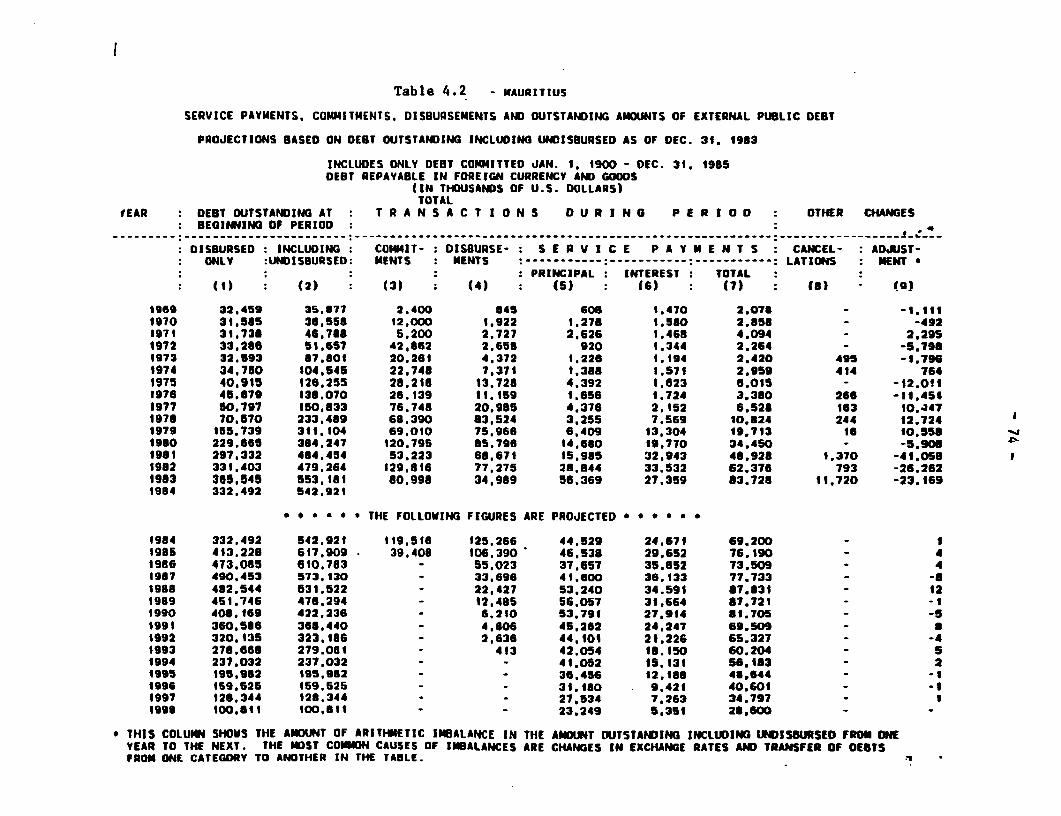

4.1 External Public Debt Outstandig as of Deeuber 31, 19834.2 External RPblic Debt - Service Payments, C=W tments,

Disbsnts ad Ourts tanig Anounts

(iv)

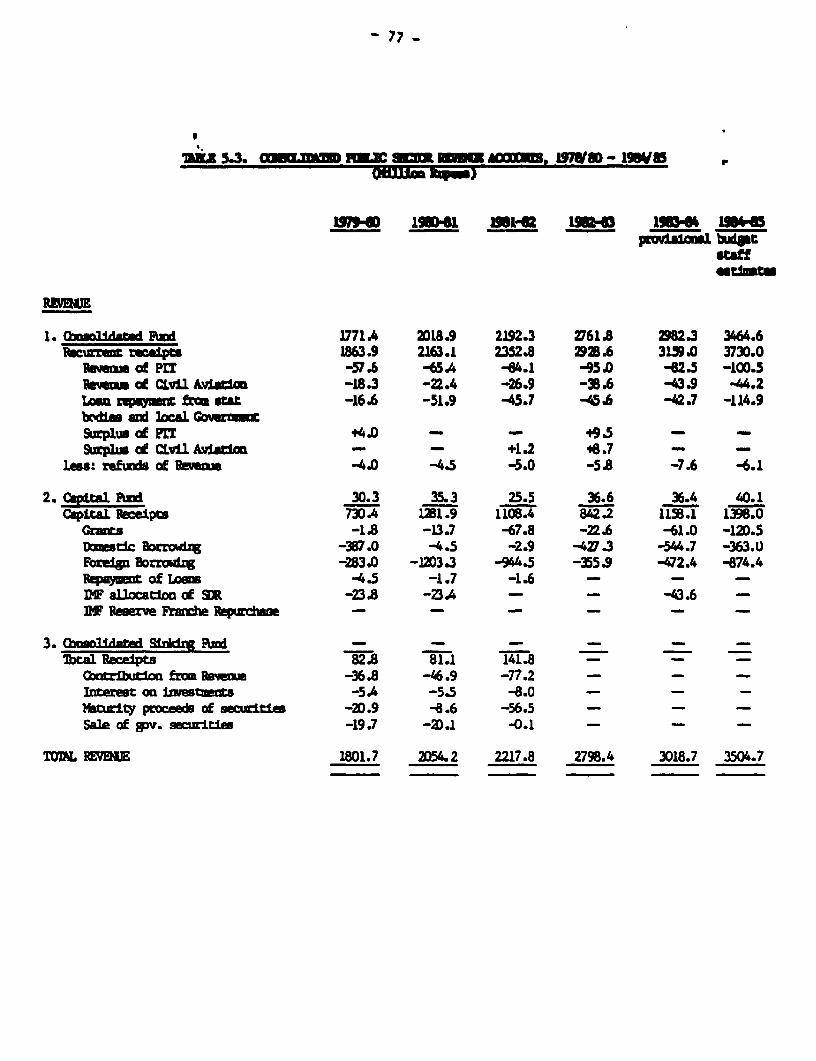

V. Public Fliexae

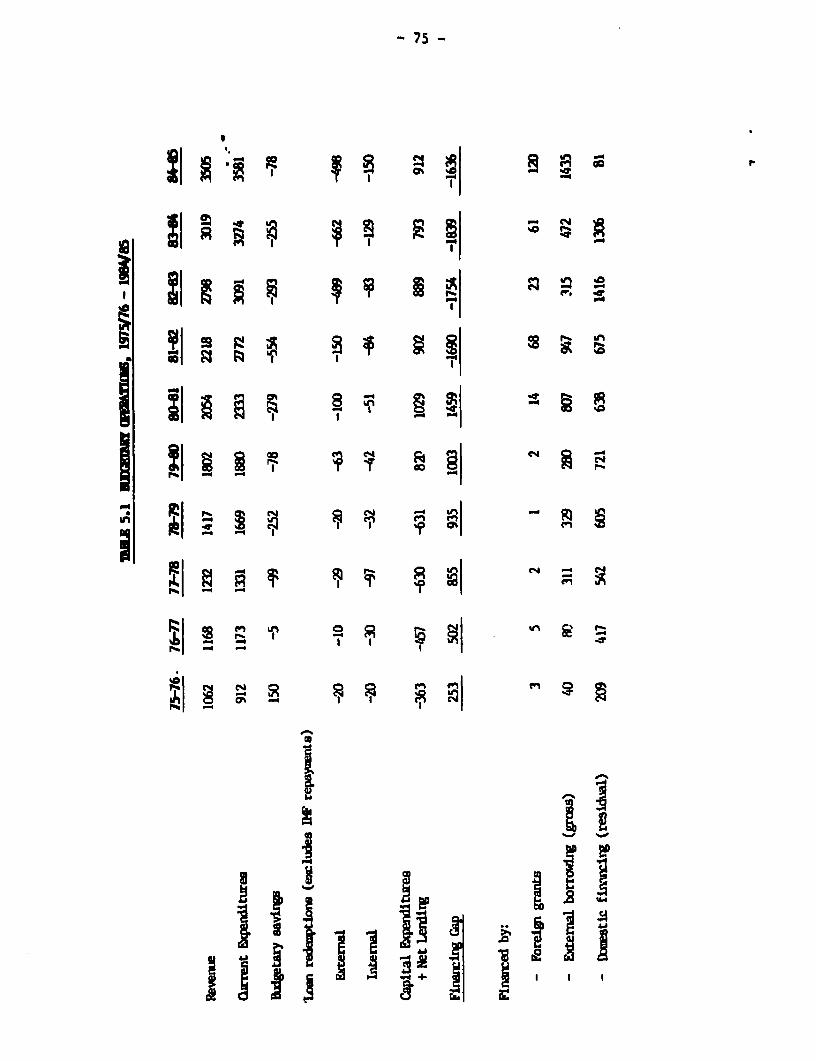

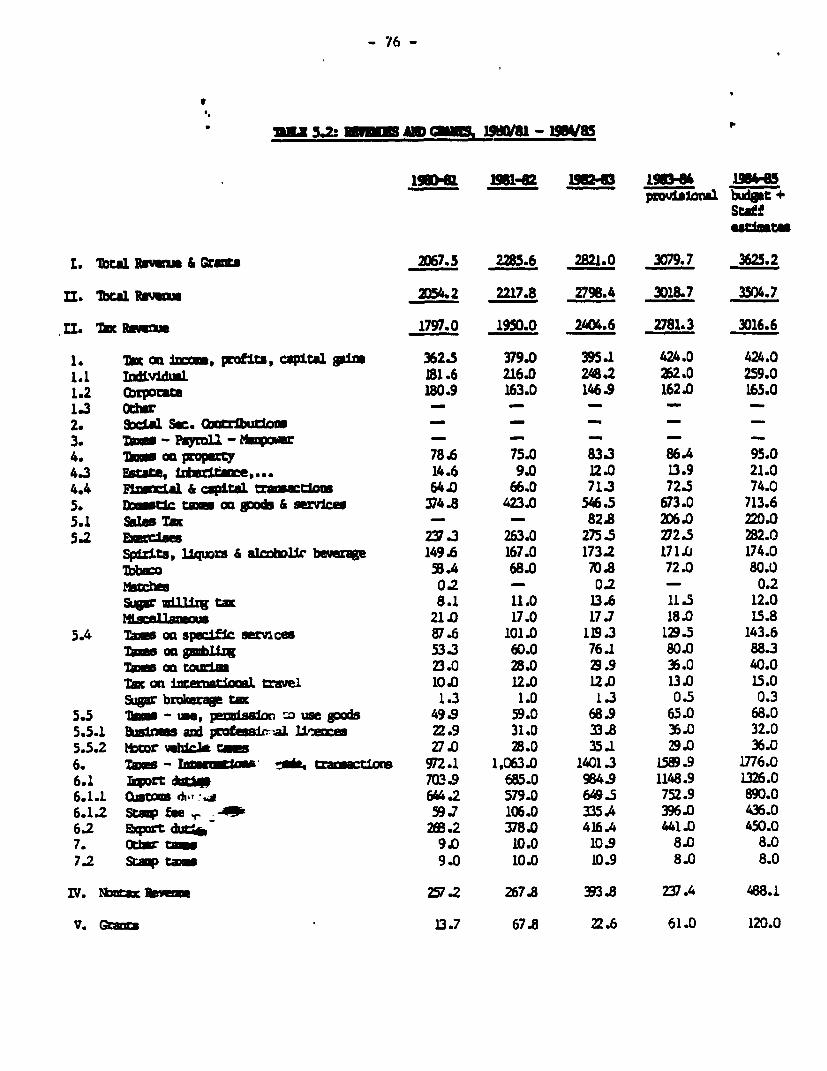

5.1 Budgetary Operatior, 1975/76 - 1984W855.2 Pem.e and Grants, 1980/81 - 1984/855.3 Cnolidated Public Sector Remem Aounts,

1978/80 - 1984/855.4 Econamic Classi.fcation of Bxgetary Expeditues,

1979/80 - 1984/855.5 Rmctlonal Classificaion of Recurrent Expeditur,

1979/80 - 1984/855.6 Public Sector Corolidate Firial Acounts, 1979/80 -

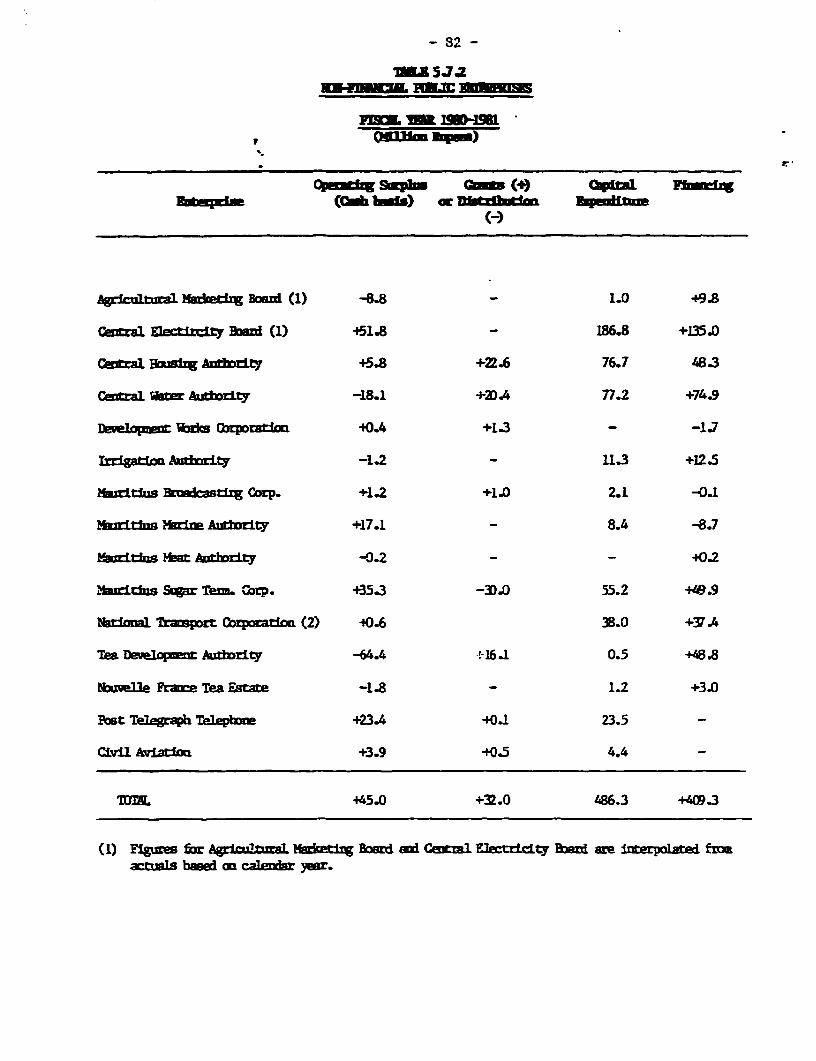

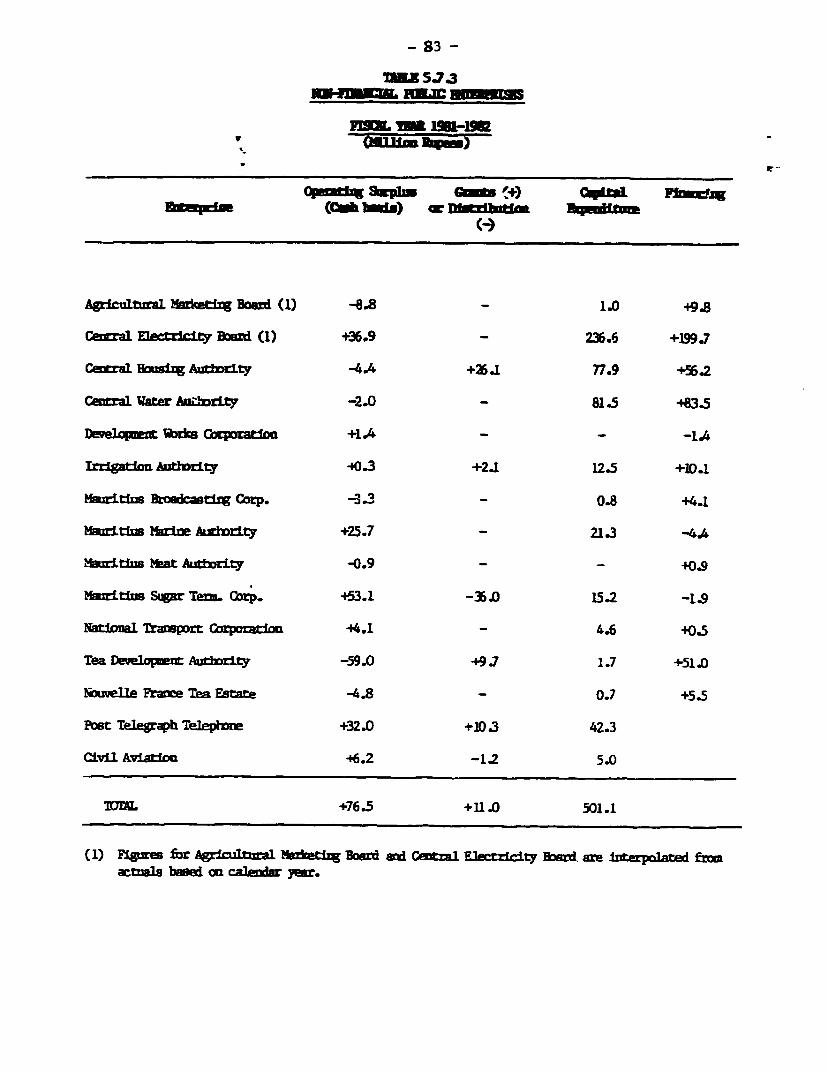

1984/855.7 Finaoial Accounts of Non4innocial. Public Enterprises,

1979/80 - 1984/85

VI. Monetary Statistics

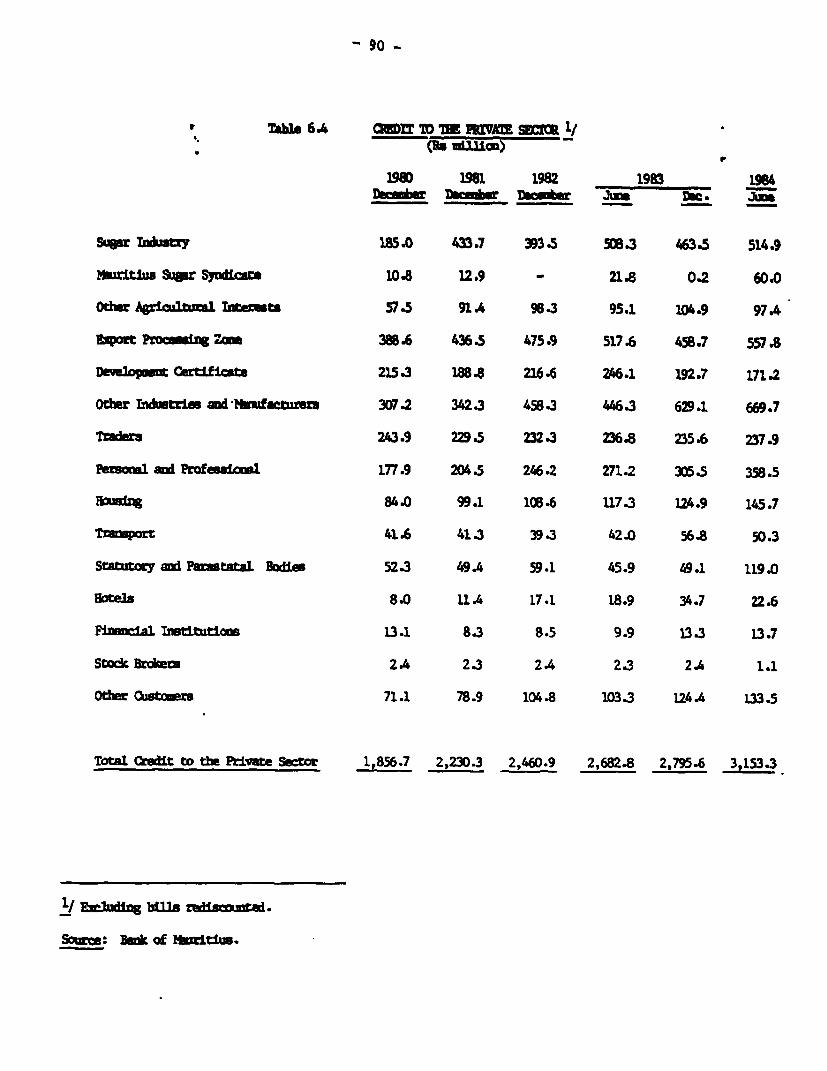

6.1 M,rtary Survey, 1979-846.2 Sunaxy Accounts of the Bark of Mauitius, 1979-846.3 Sumary Accouts of °mwmiia1 Ba*.s, 1979-46.4 Cedit to the Private Sector, 1980-846.5 Priuipal Interest Rates

II. Agrla tatistics

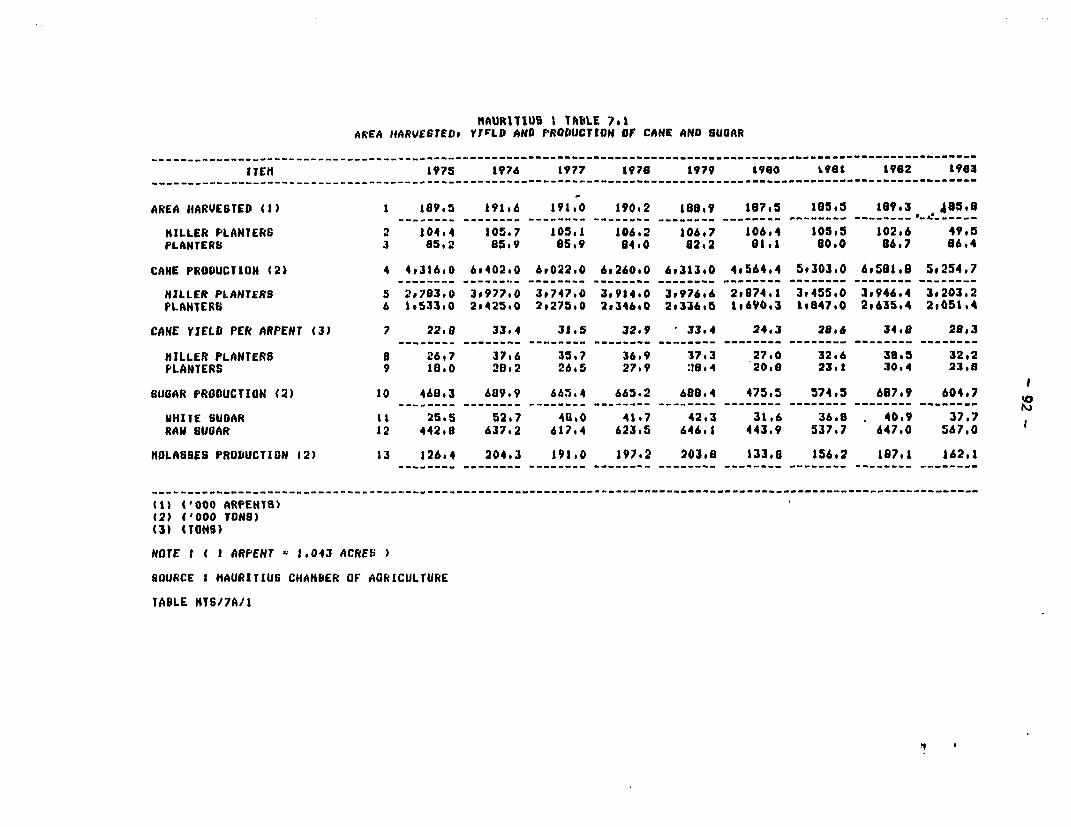

7.1 Area Harvested, Yield and Poduction of Cam and Sugar,1975-83

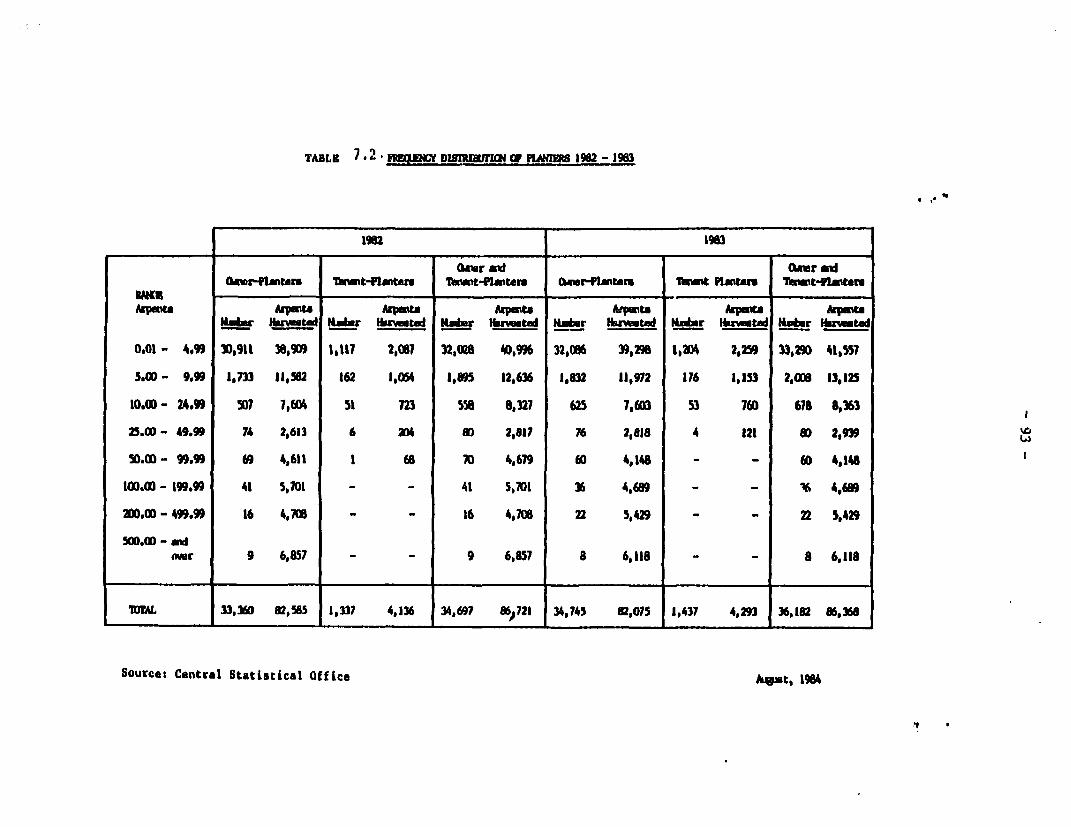

7.2 Frequency Distributim of Sugar Planters aid LandHoldirgs, 1974-84

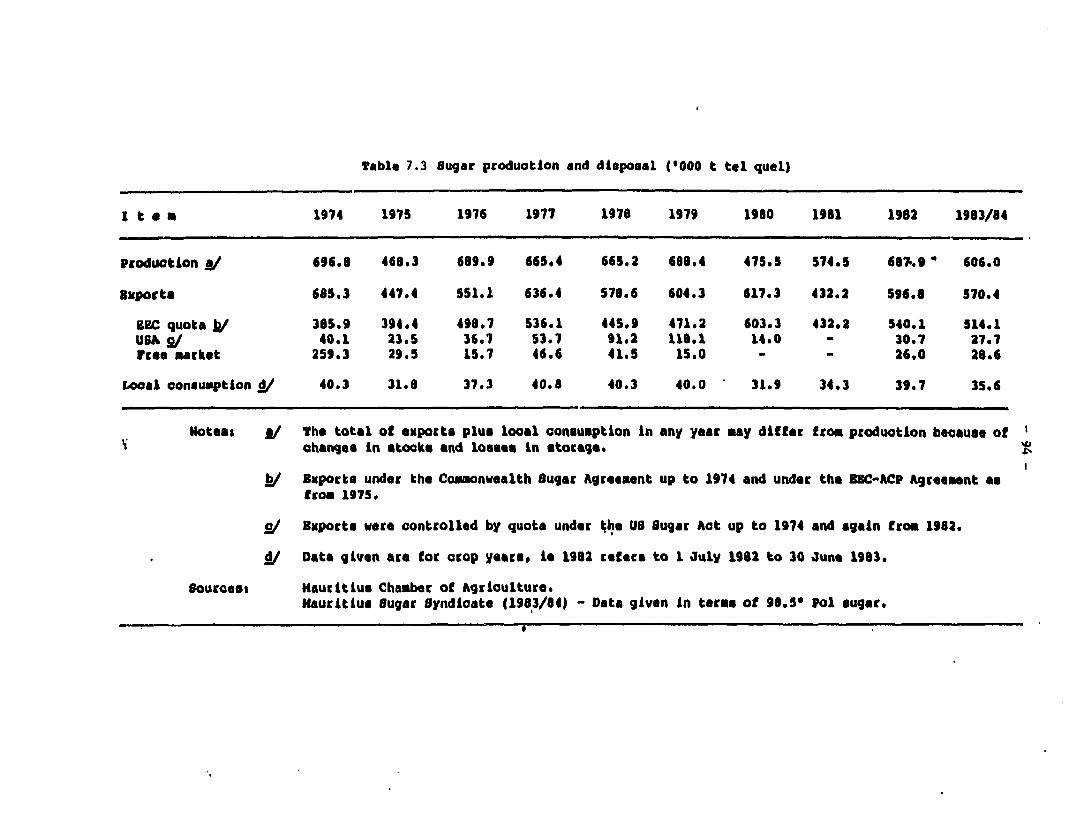

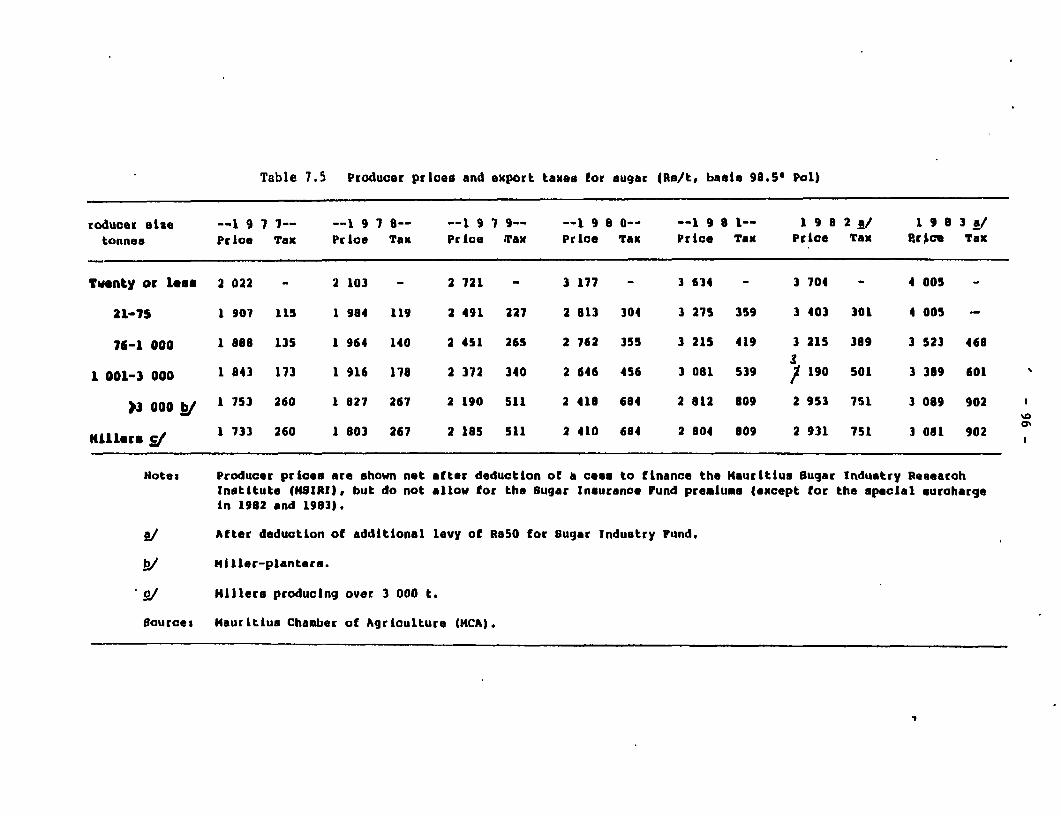

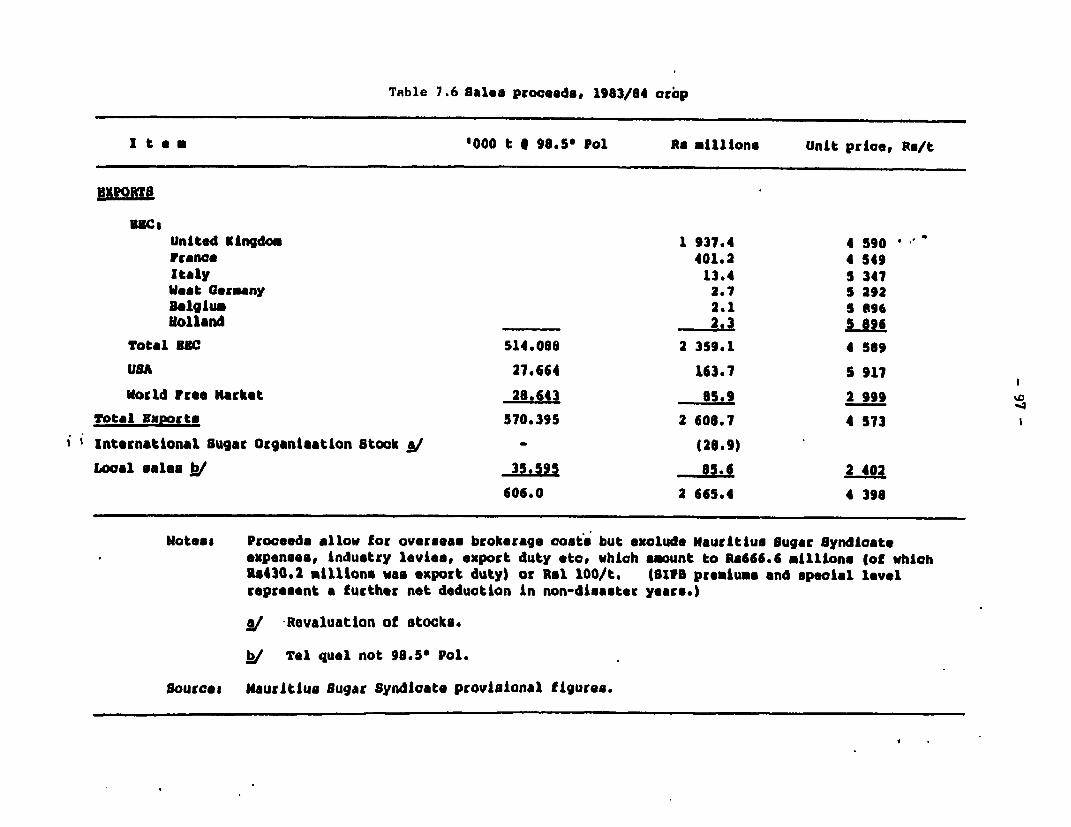

7.3 SWr Productiom and Dis l, 1974-847.4 Sr Pmduction by Mill and Regim, 1974-837.5 Producer Prices and Export Tmres for Sugar, 1977T837.6 Sgar Sales Proceeds, 19847.7 Foodcrop Producetion

II. Ocber

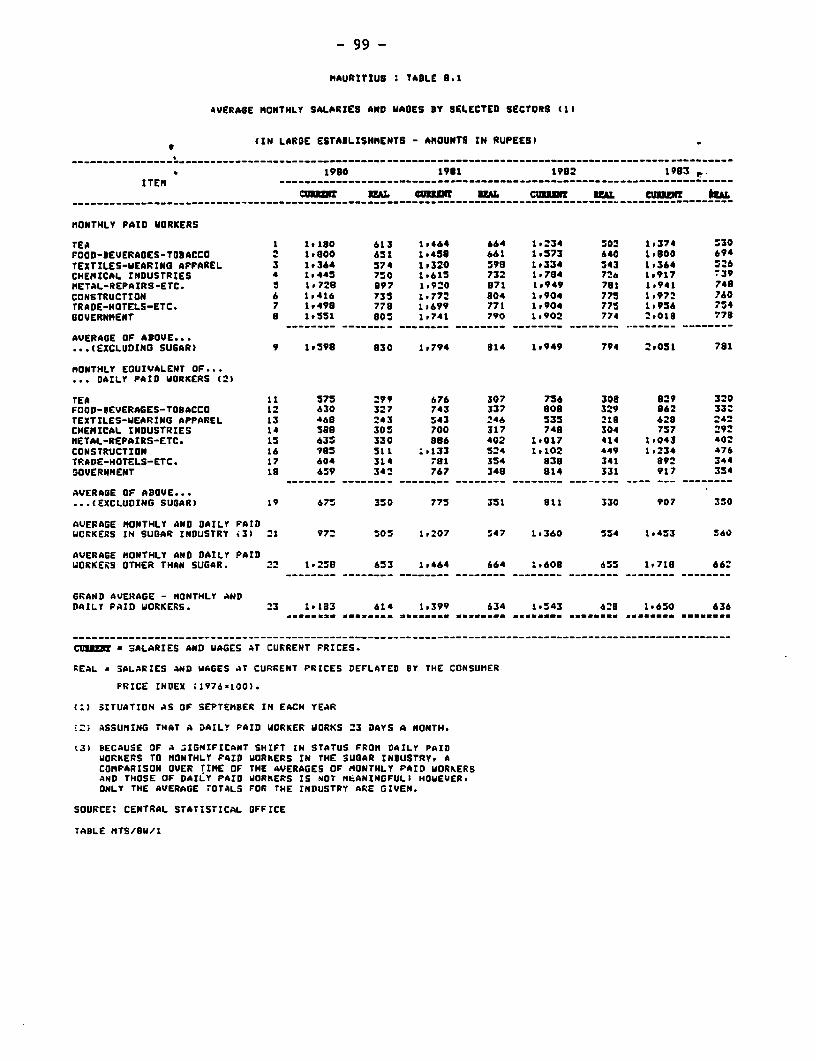

8.1 Average Pbnthly Salarles and Wages by Selected Sectors,1980-83

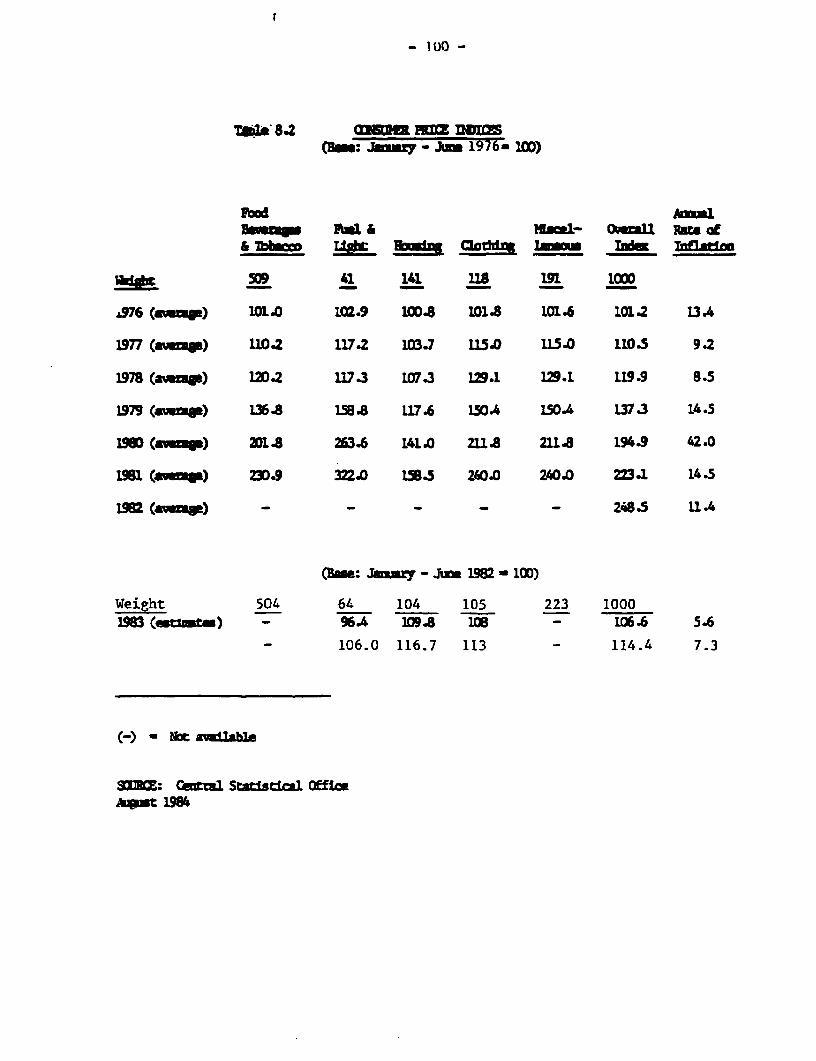

8.2 GDnsumer Price Tnlces, 1976-838.3 Distribution of Iuse]iold Ixra, 1979

(v)

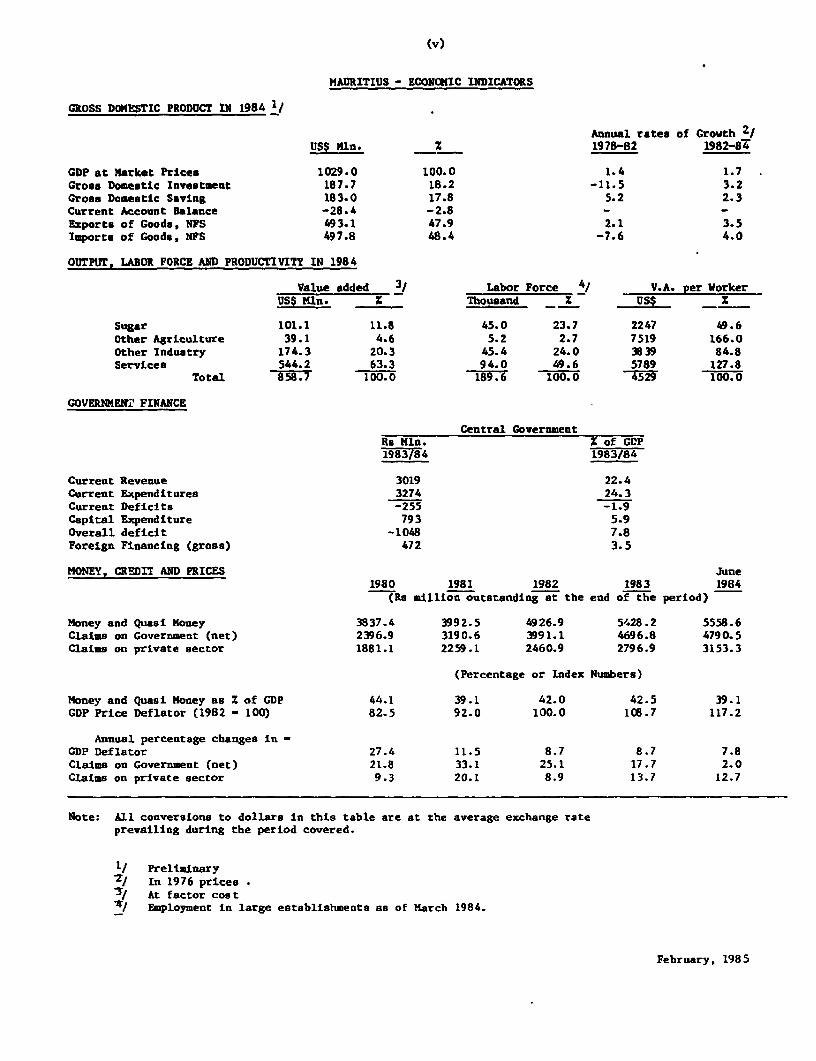

MAURITIUS - ECONCOIC INDICATORS

GROSS DOMESTIC PRODUCT IN 1984 1/

Annual rates of Grovth 2/USS Mln. % 1978-82 1982-84

GDP at Market Prices 1029.0 100.0 1.4 1.7Gross Domestic Investment 187.7 18.2 -11.5 3.2Gross Domestic Saving 183.0 17.8 5.2 2.3Current Account Balance -28.4 -2.8Exports of Goods, NFS 493.1 47.9 2.1 3.5Imports of Goods, NFS 497.8 48.4 -7.6 4.0

OUTPUT, LABOR FORCE AND PRODUCTIVITY IN 1984

Value added 3I Labor Force 4/ V.A. per WorkerUS$ Mln. Z Thousand _ US$ Z

Sugar 101.1 11.8 45.0 23.7 2247 49.6Other Agriculture 39.1 4.6 5.2 2.7 7519 166.0Other Industry 174.3 20.3 45.4 24.0 3839 84.8Services 544.2 63.3 94.0 49. 6 5789 127.8

Total 858 7 100.0 189.6 100.0 4529 100.0

GOVERNMEN'i' FINANCE

Central GovernmentRe Mln. Z of GDP1983/84 1983/84

Current Revenue 3019 22.4Current Expenditures 3274 24.3Current Deficits -255 -1.9Capital Expenditure 793 5.9Overall deficit -1048 7.8Foreign Financing (gross) 472 3.5

MONEY, CREDIT AND PRICES June1980 1981 1982 1983 1984

(Re million outstanding at the end of the period)

Money and Quasi Money 3837.4 3992.5 4926.9 5428.2 5558.6Claims on Government (net) 2396.9 3190.6 3991.1 4696.8 4790.5Claims on private sector 1881.1 2259.1 2460.9 2796.9 3153.3

(Percentage or Index Numbers)

Money and Quasi Money as Z of GDP 44.1 39.1 42.0 42.5 39.1GDP Price Deflator (1982 - 100) 82.5 92.0 100.0 10B.7 117.2

Annual percentage changes in -GDP Deflator 27.4 11.5 8.7 8.7 7.8Claims on Government (net) 21.8 33.1 25.1 17.7 2.0Claims on private sector 9.3 20.1 8.9 13.7 12.7

Note: All conversions to dollars in this table are at the average exchange rateprevailing during the period covered.

I/ Preliminary'Z/ In 1976 prices

At factor costt/ Employment in large establishments as of March 1984.

February, 1985

(vi)

MAURITIUS - TRADE, PAYT1NTS AND CAPITAL FLOWS

BALANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1980 - 83)

1961 1982 1983 1984 1ICUSS Million)

US$ ol. X

Excports of Coods, UPS 494.7 504.3 508.5 509.5 Sugar 229.8 61.1Imports of Goods, NFS 614.2 536.2 511.3 522.2 Molasses 9.3 2.5Resource Gap -119.5 -31.9 -26.0 -12.7 Tea 6.4 1.7

Clothing. 81.0 21.5Investment Income (net) -45.5 -45.7 -41.0 -41.9 Other products 41.4 11.0Net Transfers 17.3 30.7 19.4 27.4 Re-exports 6.4 2.2Current Account Balance -147.8 -46.9 -24.3 -27.2

Total 376.2 100.0Long-term Capital 7.8 1.5 0.9 5.9Net ItLT borrowing: 36.8 81.0 -21.4 68.8

Disbursements (49.1) (105.7) (31.6) (111.6) EXTERNAL DEST, DECEBUER 31, 1984Amortlzation (12.3) (24.7) (53.0) (42.8) (US$ million)

Other capital (net) 2/ 1.8 -16.5 0.8 -11.3Public Debt, outstanding and 413.2

Change in Reserves 101.4 -19.1 44.0 -36.2 disbursed( (-) - increase)

DEBT SERVICE RATIO FOR 1984Memo item

Use of-SDRe -7.3 - - - Public Debt, incl. guaranteed 17.8 3/Use of IMF credit 64.4 33.0 14.7 -9.8

1BRD/IDA LENDING (December 31, 1984)0SS million)

RATE OF EXCUANCE IBRD IDA

1981 1982 1983 1984 Outstanding & Disbursed 106.74 20.19US3l.08.937 US$1. 010.873 US01.0-11.706 US$1.0-13.801 Undisbursed 78.51 -R10-US$0.1119 R1.OU-S$0.92 RIlO.US$0085 R1 -U-S$O.073 Outstanding including 185.25 20.19

undisbursed

I/ Preliminary_/ Includes short-term private capital, SDR allocation and errors and omissionsi Debt service payments (excludlng IMF repayments) as percentage of estimated export earnings.

February 1985

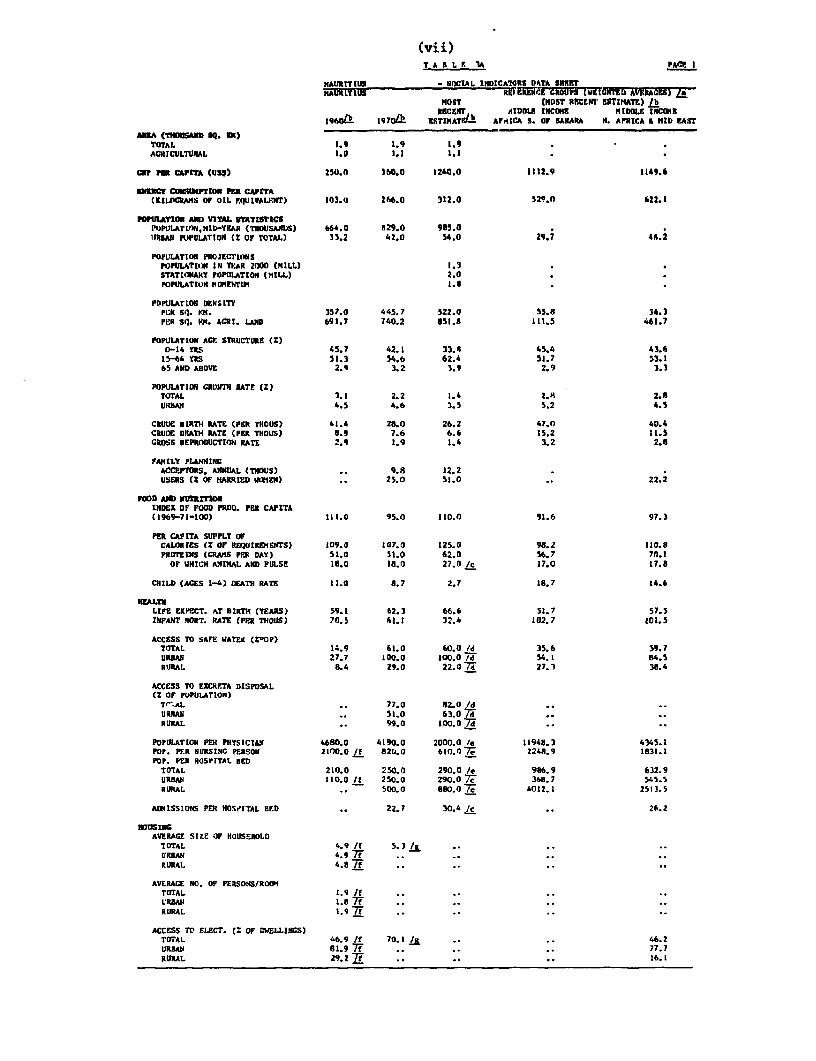

(vii)T A B L IUA PACE I

NAURITIUS - SOCIAL INDICATORS DNTA SHEETRAURITIUS RMORE u rLI3uPw-rICHTD AVur lsr-

MOST (MOST RECENT ESTIMATE) LbRECENr AlDnLE INCOME HIDOLE I NCORr

Iqeolk 1970To EsTtNATILi AFRICA S. OF SAHARA N. AFRICA A HID EAST

AMA (THUSD A . I S -)TOTAL I.9 1.9 1.9ACRICULTUIJAL 3.0 3.1 1.1

CGNPC CAPITA (US) 250.0 360.0 3240.0 1112.9 1149.6

Ymmc CmNSUMnION PE CAPITACSILOCMMs or OIL rQUIVALSNT) 103.a 266.0 312.0 529.n 622.1

rOPtHATOU AlD VITAL EtTATSTCSPOPlLATION,MHD-YEAR (THOUSANDS) 664.0 329.0 935.0IRSAN POPULATION (Z OF TOTAL) 31.2 42.0 54.0 29.7 4L2

POPULATtON PROJCTI(oNSPOPUIATION IN TEAR 2000 (MILL) .3.STATIONARY POPULATION (MILL) 2.0POPULATION II WFNTLH 1..

POPULATION DENSITYPC3 SQ. nK. 357.0 445.7 522.0 55.8 36.3PER Sq. M. ACRI. LAND 691.7 740.2 653.5 313.5 461.7

POPUlATION Ag: STRUCTUCE (Z)0-14 YRS 45.7 42.1 33.8 45.4 43.6

15-64 YI5 51.3 54.6 62.4 5s.7 53.165 AND ABOVE 2.9 3.2 3.9 2.9 3.3

POPUATION GROUt RATE (z)TOTAL 3.1 2.2 1.4 2.8 2.6URBAN 4.5 4.6 3.5 5.2 6.5

CRUDE BIRTH RATE (PER TubOS) 41.4 26.0 26.2 47,0 40.4CRUDE DEATH RATE (PR TrHOUS) E.9 7.6 6.6 15.2 1L.5CROSS REPRODUCTION RATE 2.9 1.9 1.4 3.2 2.6

FANtLY PLAPINGACCEPTORS. ANNUAL (THOUS) .. 9.8 12.2USERS (z OF HARRIED iZEN) . 25.0 51.0 .. 22.2

FOOD AND NUTRITIONINDEX OF FOOD PROD. PER CAPITA(1969-71-100) 133.0 1s.o 110.0 91.6 97.3

PER CAPITA SUPPLY OFCALORrEs (Z OF REquIRDIENTS) 109.0 107.0 L25.0 96.2 110.8PROTEINS (GRMS PER DAY) 51.0 51.0 62.0 56.7 70.3

or WHICH ANIMAL AND PULSE 1.0 38.0 27.0 7c 17.0 17.8

CHILD (ACES 1-4) DEATH RATF 11.0 6.7 2.7 13.7 14.6

HEALHLIFE EXPECT. AT BtRTH (YEARS) 59.1 62.3 66.6 51.7 57.5INFANr M1ORT. RATE (PER TH0OUS) 70.5 h1.1 32.4 102.7 101.5

ACCESS TO SArE WATER (Z-OP)TOTAL 14.9 61.0 60.0 Id 35.6 39.7URIAN 27.7 100.0 300.0 7d 54.1 84.5RURAL 6.4 29.0 22.077 27.3 38.4

ACCESS TO EXCRFTA DISPOSAL(Z OF POPULATION)

TrYAL .. t7,0 82.0 /dURuN .. 53.0 63.0 7d7RURAL .. 99.0 10o.O 7

POPULATION PER PHYSICIAN 4680.0 4190.0 2000.0 /a 11948.3 4345.1POP. PER NURSING PERSON 2100.0 Jf 820.0 ein.077 2248.9 1831.1POP. PER HOSPITAL BED

TOTAL 210.0 250.0 290.0 /e 9U6.9 632.9URBAJI 110.0 /f 250.0 290.0 7e 365.7 545.5RURAL .. 500.0 860.0 /c 4012.1 2513.5

ADHISSIONS PER NSTIqTAL BED .. 22.7 30.4 /c .. 26.2

AVERAGE SIZE OF HOUSEHOLDTOTAL 4.9 /J 5.3I / .URSAN 4.9 7W.RURAL 4. Jf ..

AVERAGE NO. OF PERSONS/ROOITOTAL 1.9 Jf ..URBA 1.5 77F ..RURAL 1.9 If ..

ACCESS TO ELECT. (: OF DWELLINGS)TOTAL 46.9 if 70.1 JR - .. 46.2URBAN 81.9 7F .. .. .. 77.7RURAL 29.27? .. .. .. 16.1

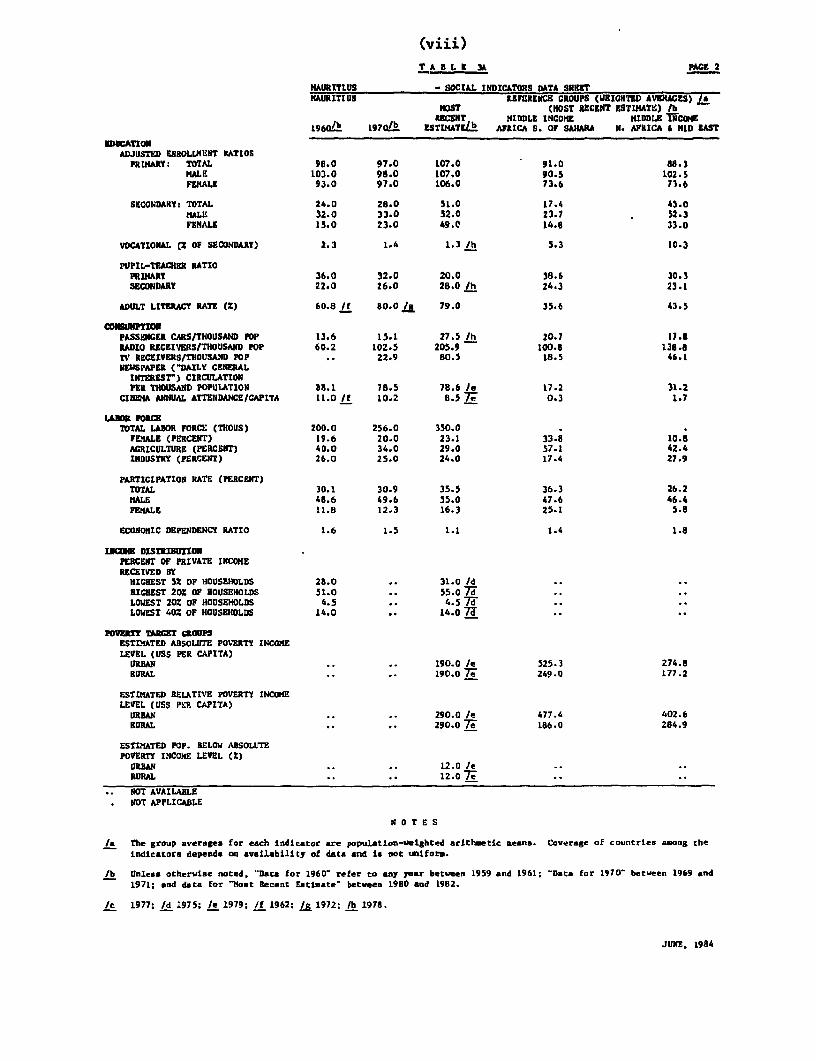

(viii)

T A E L C 3A PACE 2

NAURITIUS -SOCIAL INDICATORS DAT micrKAURIT US REFERENCE GROUPMS (lEIGNTED AVERAGES) 7j

MOST (HOST RECENT ESTIMATE) lbRECENT MIDDLE INCOME MIDDLE TNcQI

aLbk 1 9 .1 / ESTIMATILb AFRICA S. OF SAHARA N. AFlICA & NID AST

ADJUSTED ENROLLMENT RATIOSPRIMARY: TOTAL 98.0 97.0 107.0 91.0 68.3

MALE 103.0 98.0 107.0 90.5 102.5FEMALE 93.0 97.0 106.0 73.6 73.6

SECONDARYt TOTAL 24.0 28.0 51.0 17.4 43.0MALE 32.0 33.0 52.0 23.7 52.3FEMALE 15.0 23.0 49.0 14.8 33.0

VOCATIONAL Cl OF SECONDARY) 2.3 1.4 1.3 lh 5.3 10.3

PUPIL-TEACHER RATIOPRIMARY 36.0 32.0 20.0 38.S 30.3SECONDARY 2Z.0 26.0 28.0 /h 24.3 23.1

ADULT LITERACY RATE (Z) 60.8 If 80.0 j 79.0 35.6 43.5

CONSUIPTIONPASSENGER CARS/THOUSAND POP 13.6 15.1. 27.5 /h 20.7 17.8RADIO RECEIVERS/TNOUSAND POP 60.2 102.5 205.9 100.6 138.8TV RECEIVERS/THOUSAIND POP .. 22.9 80.5 18.5 46.1NEWSPAPER ("DAILY CENERAL

INTEREST") CIRCULATIONPER THOUSAND POPULiATION 8.1 78.5 78.6 le 17.2 31.2

CINEMIA ANNUAL ATTENDANCE/CAPITA 11.0 /f 10.2 8.5 7e 0.3 1.7

TOTAL LABOR FORCE (TEOUS) 200.0 256.0 350.0FEMALE (PERCENT) 19.6 20.0 23.1 33.8 10.8AGRICULTURE (PERCENT) 40.0 34.0 29.0 57.1 42.4INDUSTRY (PERCENT) 26.0 25.0 24.0 17.4 27.9

PARTICIPATION RATE (PERCENT)TOTAL 30.1 30.9 35.5 36.3 26.2M;ALE 45.6 49.6 55.0 47.6 46.4FEMALE 11.8 12.3 16.3 25.1 5.8

ECONOMIC DEPENDENCY RATIO 1.6 1.5 1.1 1.4 1.8

lUCOlE DISTRIBUTIONPERCENT OF PRIVATE INCOMERECEtVED BY

RICHEST 5% OF HOUSEHOLDS 28.0 .. 31.0 /dHIGHEST 20S OF HOUSEHOLDS 51.0 .. 55.0 7i *.LOWEST 20% OF HOUSEHOLDS 4.5 .. 4.5 7*-LOWEST 402 OF HOUSEHOLDS 14.0 .. 14.0 7..

POVERT TARGET sROUPSESTIMATED ABSOLUTE POVERTY INCOMELEVEL (USS PER CAPITA)

URBAN .. .. 190.0 /e 525.3 274.8RURAL .. .. 190.0 7e 249.0 177.2

ESTIMATED RELATIVE POVERTY INCOMELEVEL (USS PEP. CAPITA)

URBAN .. .. 290.0 /e 477.4 402.6RURAL .. .. 290.0 7e 186.0 284.9

ESTIMATED POP. BELOW ABSOLUTEPOVERTY INCOME LEVEL (2)

URBAN .. .. 12.0 /eRURAL .. .. 12.0o7

NOT AVAILABLENOT APPLICABLE

N O T E S

/a The group averages for each indicator are population-veighted arithmetic means. Coverage of countries among theindicators depends on availability of data and is not uniform.

lb Unless otherwise noted, "Data for 1960- refer to any year between 1959 and 1961; 'Data for 1970- between 1969 and1971; and data for -Most Recent Eattuate- between 1980 and 1982.

/c 1977; /d 1975; le 1979; /f 1962; /R 1972: lh 1978.

JUNE, 1984

(ix)

Seq.., iliha th. St. .. deem lts gape. Oodeersu lGotwer* as8 =mqelssmato psei .1is e id Snds hs seand enbs use ssss Us ie.rsm.stesdesuTbi tes... q Sb twit qt- e.tdssdhse 14pIlie adel seeep. sadd i dilltesS .sepssi elsatie it. is.. Th. dsp. en sersstaIses. at.. mado=eits epstm.tissdliSe. India. BtEads ss.d serseri elsel esge Aul lst.eadd busemns. sal .pi

lIsps see s.s an 155d ftI Sb Se a tde - If s.ee elf Oft t s assnlMMP Go. (ilt rapeN sie ish6 sadins 41hubs s..ftuu , Ifsedits. StSs.?. dooal SI sek:New:e am G55; issnp too lEgs lesse lii Sspresirl' Smadstpsodr Nlidfl SiReu rteP 51,. sed Miaddle Uss' is etss. tesses sosp.,fsi.sea

aElsiise. far lob nla 1nss s.l leE4 sh aesss 95 -shssseasSst spisteegi aness. as eseb lveilss s. s ofI ip sEw.,alpe ln.9 lbh sampese

st Gph 5 r ss isu.li. sesen 1esuse iu h rdlep .. d bsalbii di .du am smIler,. seitse ue'h

*ag I u.us.. dp.10 ol ni sasuels p...aural.p.ssJiloaln,n ieen.-I.55 5 Isi., sq:. P Pa .- ls.sser Itetss -A Ii aulsi. be 5...P it llo,s1.'Stu.arurLs3L - tes,els a esraeissrs11 ldps sea. tISepsrepss eP -- Iafesu I. -rei aP55 sense. Gasepis siVnes pes.1 ci rts setpssts.Ph.55iisissPsui s sIltw 55 .isqiS ss lep GS.

eIsm. 1590, eso usi dss.. he is MIses asg phrpeususe. hetshttesesst lpeetldu Prapielseusp l s.qeuuis

511. s.d uwi disS. ~ ~ ~ .N1 . d ~ Srt -d.d m Wus. tP; I 44.1 sd. sles ts*r isUes

- ~~~ ~e. te t nly s4 us6s1* tIle. ad lies i sait e. rissjj.s5 r..i ss

prs.u m eayer .Me. -F elIses saeslbiliie .4 is..l aibi -l. .. i.. A ttIdMd a kldssr -F 5P ..? esm te sesuede 5ass.esepu.u. soma. lels. asr Iona %s..sess"id lee esuius rplwam.

-taial.lpmein wr CirlsspIial prlsiedaswess aps Ussd ss seow L...~ 5 n 5 .. isp .sua nMee

is. p.1.1`p uS of sews a . sub steir altiustip *d First lutier eisuri. pesnisimi. Radit-len ssr5ed ss-mapeSe-I eurssisalnd

seals seemii Ills eeussy iila birth lanstes 1.111 o55

flfls ps eosa ssuigyleretn ttle . es-psef. lb I.-L5. PerF-1 kerits.ri elsef e." sista0 dssi .9. sirusi. s He. e phIps husie. rsN esisslq.11.lseis .e sum1 is -lendsH -VI sq ap sedie es" uses.. -Imnia k.Issent,.0.wm aArr1bliesport.,plsSSi P. setadas. Rsi sentre Is ite ssslkesd - ,atboos suea

pestlasiar .9 doislite add lsPsllist ireeds ise polsjsSst, Itilass.

is sesetus Ste est-Psu. l e indsPsir 5w sise= wsssse 55 sb sassP pi. 'tn eAPss eLe., it esuls meseed55p.,araSh nis is s. tim s555'P5 sees-.lb.l etc en, aumi s. soue msen e.sss seeod F u. diffftsast 5-1 555 .. lau se

eieaslstoo.heels -. .. * the mo5.5r? p1st lepiaLa" sanh 5 deiseims ppsiwelftdes sseth -. 01, bl. STe1o Is.after IraqIs ssssaleqS EseC..: -91tdIIT111L nrisae.sm spiltlss te t.S .1. s*as seeeg5 u.iee 5t .ass. *as oeetts..r apses.. as.is. o o.sass .slqs sise a rspe Idseale rats, Patehe ola'.K esis. e eeesil ssrqeis.6 01 -1 rod.. ~ 11

.5 pissi. elat laCaCc 159g1s5 iss 5, Shepe,teleIs le she sa. 1.,,i*lsssP 4- .I 5ea.l,qtps. iidsp. .... .s.ap.vs.e.s sgo, ..t5sl si e prlisre pteewles 1 5 pspaaas Go.1Es eII 4: teepiesl - Cs dsIssseS e-.deeie

sai 15 us -1es .dtl . % Mlld ' Isee.-.t,b Pt -e.ePs1. 45stwse-e. .. es s.ie-P.,IE ..sc Gs p rresp -- s...ps ep issiekiet4 :li.ssn ..Ms IS~!~j-su-resr rselssli rreq -Pe Slal-p iN t5ps '*.* -. W.tre..s ee

ssisapea liS, iJ s.es qq se. .`21`.qIeprplep.qttes ass ss aps it.,,

t1ji.l I .. l±kjPffl lseleis5 q- eeePeailhsn ea eeCeCEIsesIsests nslewsCcsep

_______ ______ _______ ______ C hl ipse- 1 -1. 1 ysani isp ses-e lie

Pielius175ss5h low. Ide.rent *" Al .. isedqshrseaisi -sI5iserc eshla5a-..

Psesrmopiush qg;y$r~sl-at.*Ms ss ass edEal tE dssssk sDlreess dse.9 sesltetP- sapsaIssism Isp Ise-o. es-s.7a 115-3. .eie1i ssqp qpseeeIssaS Is Sa ab Vs ssesimt. .5 raise

Pp.. snetes (sf Usi~pi -seaes lisbiles.f tbeal. nd S a Is *llst Lute Istr resos "n meaW. t Us teeardebla esse assa

______ ______ ______ _ Tool_ is es l Ga bla P s a e s ii S d- ra pI M C p its s s ps i s n s e s l 1 s t s Per -r Gd.a S

S.P sepal rapraiaeisa pepist il sa sepepisese 1t55at5 555-Ss.5itl. ___i__ t- __ -w_ p_ -4__ on _____a Q__ __ -94.,apsplqey rn. ans Mamra- (wr ase ssts tennl sag,le, a t. 1. ?:l1L1 sa Ifei esltea inP ppi

peespa.. Ii a.." spinsra ti dha, al a.sp. Ieadq .eseauusda-sel asrseiLr pla.esta - Sean (nines sq eereied isaql - Peleiseg .1 arpIst getS Is cite.~~~~~::.PIaL- f LIMal. aSI.I.- I

asses .t steAd-Usseleg as. a. an Irastalse ar Idea Peshei-Is ens J.. M. --f ... I1- IG Ii-spl na.napsI,as 55 t-t .ilstLetsa'si I'l J.setai Is.. sese. irese

easirl a pses! ia usas Ise) 4m.aseed s sdbroto eniPl '7

Sfla CS7eels.sci SWeees.1sS N5S,t!. neP VSbd-4 do -1-,M Pradood, P.L. Ilojeh..slwkalaq t sita.. s- ssiqes Se aise.rs.gti - ce -

sew efrellios assantles ICte, 11111 asegant lee: Se,Ss.-.-Wea Isssl t*l Isgi ame,iSrsa. Hs-Saaftis sP.l -Os PM seeB .9 Ma alate an Ene. qqpaprs5sea, Issers .ItS u.s

as"i. AMIs - eslaslu ftartess 1. dislss sedap waisred 55 es.. IOU.e1easereasesd.. ti%M is ae lpp a. IM,- IDr P.m..e Ci Iona-do!ta tsti .1 ssepi set.a sitis aSjd sense fawdisess 55.1 fl lotl,fl 5 M-. Les Pa.. SW -V,es IStatee Id-s aP-aerl .afltsaista and t.ul- PsedS3. S asendao, pt.beel.1,t awe mt- I. sls .. tIiloall. -tI - .a esss""tEtlib lpe f.eteed -usls d saflPA 115515d -Plap alMGee Iq laneesf t1. so,aetd SC"SI si see: is.. MN G .- I

dats. 1l.n5 -- sirse bihod,sftt- Itl -seel. adle.-sG Ast I. t.laSsaPer aert sssei 51 -seislas Wsp.eeq str osdesss -a basa. tp. s.e1 pa r e.ia eils,aa titaslbprp.

-seit esi" Se lad ePenweiss. is ;- Lsssse le alnlbls issi.- pi ilasa.I0stieiae-

Pain. seaL. sasen byl Pt. g-s b- pbrelsa-Isie TIM . spal ttm Scn A5 as.a etet dp I.iI ttwas ` SkIp eM ts 'h-ssm do seIpes Mm leleispe.: .teip Elt.- it"K-t..s Ess nd -to .d Pras islta. l an poaed, ieql.. owed. sslels5 b, TAPBi tgp ala0odb.["lG, Mdlb. ,I

Per s-s ef l -.1 eni as a ee se5 ea .1m ; pee peItS" ~ .s -1rrise tdesemW Ilst s.-Itee .eestsa- ssEe si -esibasdpM . i e P .aspelld5 isda b. .. pres.eass1 e.e

5peseS pne,sdlwetAtpPese

qanaas g alMesels siitb he les W,el Pt seqn tes,s

rep Pales enqiesale L pa asses isala -. P5.f1 see a r Pad Sheal esL Le saIIssatLa. pi m~aaIe s

C5ild~ ~ ~ ~ ~ ~~~~~:4 I.. a et se a tsse seldsbppIea I asiitIpaPsrsls a e see ta.ist11 -*Pb5 q .,e-oo. ase -"IT rats, i sPollase is- ewGn55e a slse as ssi.parps ts5 nsiis ensprLit --M."lE -te .Mn dap-n Cp Isp,sablesqe,il P.5 95 . sess a s.beee Pl.aIaw 5SldP. e It

- .- . pool. rallad.l. .. 7--p- La"a.."sUb ajaqs. er sete ass..-I.Iss_gapg.ss-_Ft:% h-. fty b. dooldnaS M b"o5sen1 Pa Isit bl ssske. 4Sse 4esala.5 ssnses- ah-

P-Moamea .ef perLes-e.&- sps tis.S Isi. atm Cd IsIIS det..ad

.qtSoel a idsnta es P Mom-Gqie Irwessea bre telse. ippsqs isIss asas It.e ses --- sain.Pse.e pei tpilel ltes ss

(x)

ABREVIATIONS AND ACRONYMS

ACP African Caribbean and PacificCEB Central Electricity BoardCSO Central Statistical OfficeCTO Central Training OfficeCOLA Cost of Living AdjustmentCHA Central Housing AuthorityDWC Development Works CorporationDC Development CertificateDRC Domestic Resource CostEPZ Export Processing ZoneEEC European Economic CommunityEEC Export Enterprise CertificateEEZ Exclusive Economic ZoneEP Effective ProtectionGNFS Goods and Non-factor ServicesICU Industrial Coordination UnitLDP London Daily PriceMEDIA Mauritius Export Development and

Investment AuthorityMGTO Mauritius Goveirnment Tourist OfficeMHC Mauritius Housing CorporationMSA Mauritius Sugar AuthorityNFP National Pensions FundNRB National Remuneration BoardNP Nominal ProtectionPSIP Pubic Sector Investment ProgramTDA Tea Development AuthorityTOE Tons of Oil EquivalentUHRS Unemployment Hardship Relief SchemeFY Fiscal Year

txi)

PREFACE

This report is based on the findingsof an economic mission which visited Mauritiusfrom July 23 - August 17, 1984. Tbis mission wascomposed of Ms. F. Aynur Sumer, (Mission Chiefresponsible for the preparation of this CEM),Mr. Hassan Imam (public investment program), Mr.Constantxao Lluch (wage policy and employmentissues), Ns. Pisei Eap (balance of payments andlong term economic projections), Mr. Ben Yates(Consultant on sugar subsector and agriculture),Itr. lan McDougall (Consultant on industry) andMr. Pierre Demangel (Consultant on public finance)

The section on energy is a summaryof the findings of the energy assessmentfollow-up mission which visited Mauritius in1983. The section on population draws on thePopulation Sector Review (4486 - MAS) publishedin grey cover in November 1983.

(xii)

MAURITIUS: ADJUSTMENT AMD GROWTH

COUNTRY ECONOMIC M1EMORANDUM

SUMMARY AND CONCLUSIONS

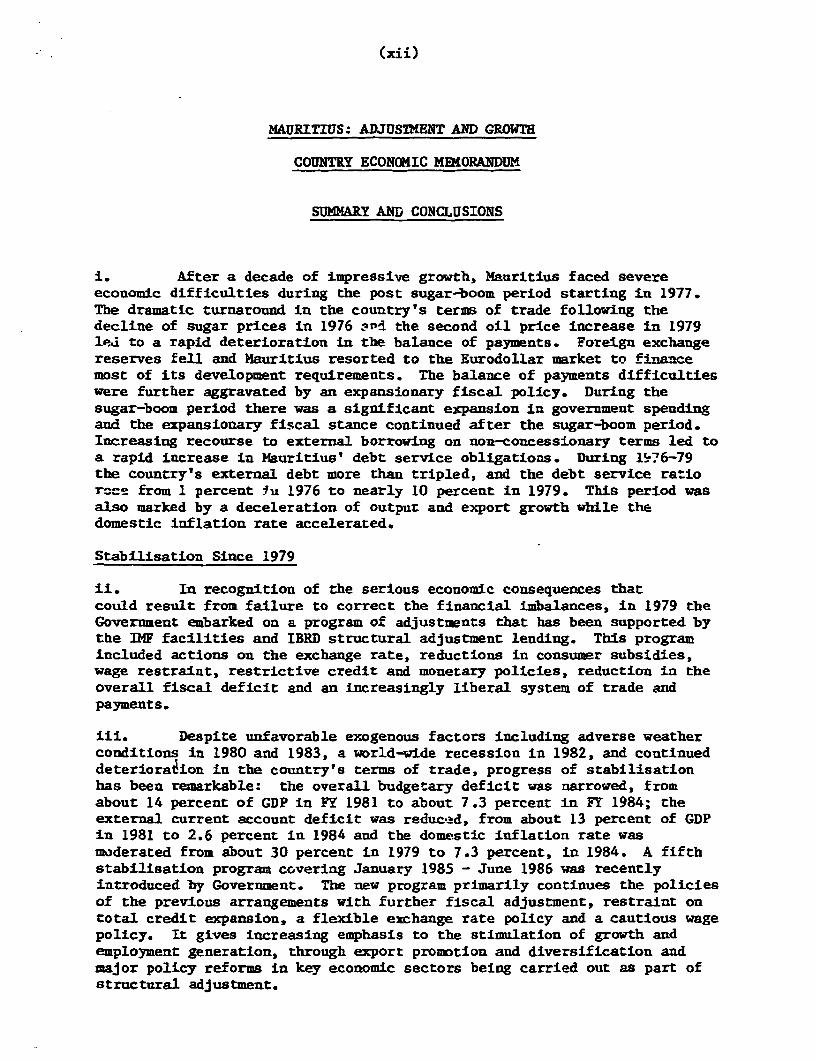

i. After a decade of impressive growth, Mauritius faced severeeconomic difficulties during the post sugar-boom period starting in 1977.The dramatic turnaround in the country's terms of trade following thedecline of sugar prices in 1976 onli the second oil price increase in 1979led to a rapid deterioration in the balance of payments. Foreign exchangereserves fell and Mauritius resorted to the Eurodollar market to financemost of its development requirements. The balance of payments difficultieswere further aggravated by an expansionary fiscal policy. During thesugar-boom period there was a significant expansion in government spendingand the expansionary fiscal stance continued after the sugar-boom period.Increasing recourse to external borrowing on non-concesslonary terms led toa rapid increase in Mauritius' debt service obligations. During 1X76-79the country's external debt more than tripled, and the debt service ratior-e- from 1 percent fu 1976 to nearly 10 percent in 1979. This period wasalso marked by a deceleration of output and export growth while thedomestic inflation rate accelerated.

Stabilisation Since 1979

ii. In recognition of the serious economic consequences thatcould result from failure to correct the financial imbalances, in 1979 theGovernment embarked on a program of adjustments that has been supported bythe IMF facilities and IBRD structural adjustment lending. This programincluded actions on the exchange rate, reductions in consumer subsidies,wage restraint, restrictive credit and monetary policies, reduction in theoverall fiscal deficit and an increasingly liberal system of trade andpayments.

iii. Despite unfavorable exogenous factors including adverse weatherconditions in 1980 and 1983, a world-wide recession in 1982, and continueddeterioration in the country's terms of trade, progress of stabilisationhas been remarkable: the overall budgetary deficit was narrowed, fromabout 14 percent of GDP in FY 1981 to about 7.3 percent in FY 1984; theexternal current account deficit was reduced, from about 13 percent of GDPin 1981 to 2.6 percent in 1984 and the domeistic Inflation rate wasmoderated from about 30 percent in 1979 to 7.3 percent, in 1984. A fifthstabilisation program covering January 1985 - June 1986 was recentlyintroduced by Government. The new program primarily continues the policiesof the previous arrangements with further fiscal adjustment, restraint ontotal credit expansion, a flexible exchange rate policy and a cautious wagepolicy. It gives increasing emphasis to the stimulation of growth andemployment generation, through export promotion and diversification andmajor policy reforms in key economic sectors being carried out as part ofstructural adjustment.

(xiii)

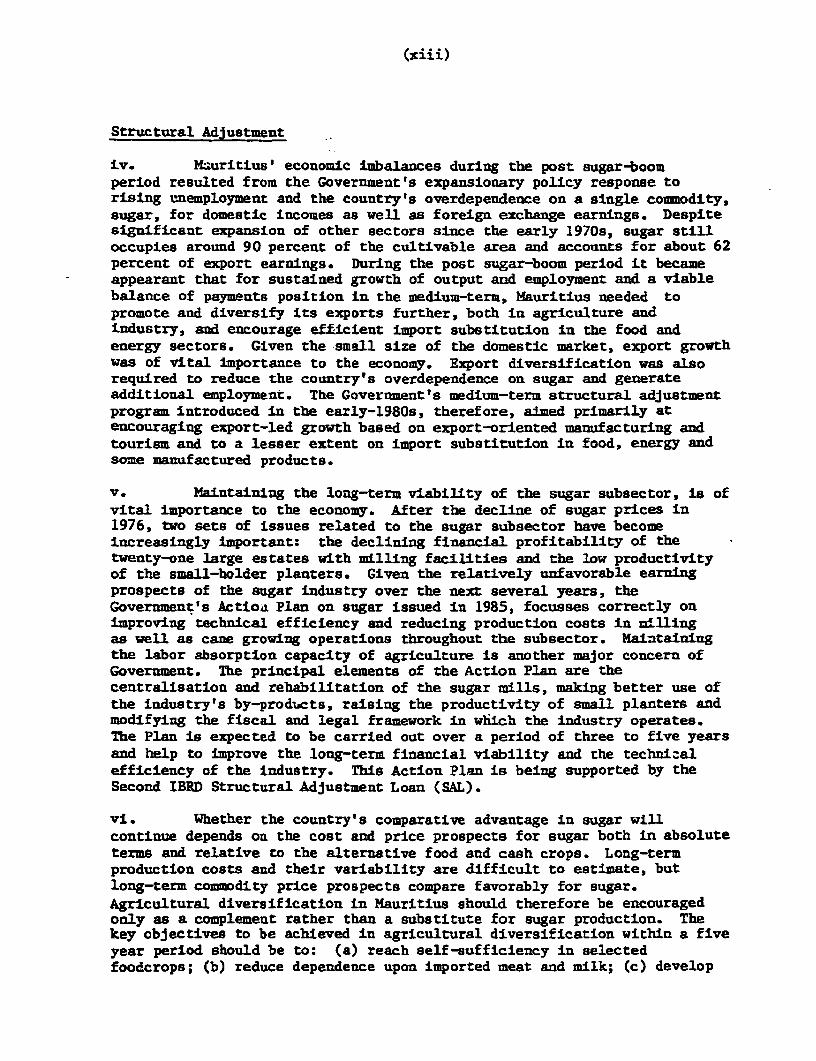

Structural Adjustment

iv. Mauritius' economic imbalances during the post sugar-boomperiod resulted from the Government's expansionary policy response torising unemployment and the country's overdependence on a single commodity,sugar, for domestic incomes as well as foreign exchange earnings. Despitesignificant expansion of other sectors since the early 1970s, sugar stilloccupies around 90 percent of the cultivable area and accounts for about 62percent of export earnings. During the post sugar-boom period it becameappearant that for sustained growth of output and employment and a viablebalance of payments position in the medium-term, Mauritius needed topromote and diversify its exports further, both in agriculture andindustry, and encourage efficient import substitution in the food andenergy sectors. Given the small size of the domestic market, export growthwas of vital importance to the economy. Export diversification was alsorequired to reduce the country's overdependence on sugar and generateadditional employment. The Government's medium-term structural adjustmentprogram introduced in the early-1980s, therefore, aimed primarily atencouraging export-led growth based on export-oriented manufacturing andtourism and to a lesser extent on import substitution in food, energy andsome manufactured products.

v. Maintaining the long-term viability of the sugar subsector, is ofvital importance to the economy. After the decline of sugar prices in1976, two sets of issues related to the sugar subsector have becomeincreasingly important: the declining financial profitability of thetwenty-one large estates with milling facilities and the low productivityof the small-holder planters. Given the relatively unfavorable earningprospects of the sugar industry over the next several years, theGovernment's Actioa Plan on sugar issued in 1985, focusses correctly onimproving technical efficiency and reducing production costs in millingas well as cane growing operations throughout the subsector. Maintainingthe labor absorption capacity of agriculture is another major concern ofGovernment. The principal elements of the Action Plan are thecentralisation and rehabilitation of the sugar mills, making better use ofthe industry's by-products, raising the productivity of small planters andmodifying the fiscal and legal framework in waich the industry operates.The Plan is expected to be carried out over a period of three to five yearsand help to improve the long-term financial viability and the techni:alefficiency of the industry. This Action Plan is being supported by theSecond IBRD Structural Adjustment Loan (SAL).

vi. Whether the country's comparative advantage in sugar willcontinue depends on the cost and price prospects for sugar both in absoluteterms and relative to the alternative food and cash crops. Long-termproduction costs and their variability are difficult to estimate, butlong-term commodity price prospects compare favorably for sugar.Agricultural diversification in Mauritius should therefore be encouragedonly as a complement rather than a substitute for sugar production. Thekey objectives to be achieved in agricultural diversification within a fiveyear period should be to: (a) reach self-sufficiency in selectedfoodcrops; (b) reduce dependence upon imported meat and milk; (c) develop

(xiv)

all lands to the limit of their maximum productivity; and (d) establish aframework of marketing facilities, institutions and price stabilisationmechanisms to provide improved support and security for producers.

vii. Continued promotion of export-oriented manufacturing remains amajor priority for Mauritius. Given the stagnant nature of the sugarsubsector, the small size of the domestic market and the sizeable backlogof unemployed, export-oriented manufacturing offers the strongest potentialto foster growth and add to foreign exchange earnings. The set ofmedium-term policy reforms for manufacturing industry, already adopted orbeing initiated by Government, focusses on improving Mauritius'competitiveness, extending the system of export incentives to all firmscapable of export activities and attracting new foreign investment andtechnology to export-oriented manufacturing. Go4ernment has been highlysuccessful in maintaining the country's export competitiveness throughappropriate exchange rate and wage policies. Beginning in 1981, under theFirst and Second SAL's Mauritius also began taking steps to improve theexport regime by strengthening and broadening fiscal incentives for exportpromotion and trading, improving export financing facilities, simplifyingand centralizing export procedures and strengthening institutions thatpromote exports and international trade. A reorientation of the externaltrade policy and the system of industrial protection is also underway.This is expected to improve capital efficiency and help channel investmentsinto more export-oriented and labor-intensive lines of manufacturing, bestsuited for Nauritius.

viii. In tourism, the Government's primary objectives are to Increaseforeign exchange earnings and generate additional employment. Thisexpansion would be obtained through promDtion and improved air access toMauritius, and increase in capacity by encouraging new privateinvestments.

ix. In energy, the great majority of investment has been and willcontinue to be in the power sub-sector. In the future, major expansion ofpower-system capacity and energy supply is likely to come from theutilisation of bagasse, a by product of sugar. Therefore, power-systemplanning and development is closely linked with the sugar restructuringprogram. Power generation by bagasse may grow from about 10 percent ofsupply now to 30 percent in 1990, displacing perhaps 25,000 tonnes orabout 15 percent of the country's oil import bill, by the end of tAedecade.

x. The policy reforms and programs in agriculture, industry, tourismand energy are further supported by a rolling three-year Public SectorInvestment Program (PSIP) which is geared primarily to the needs of thesesectors. The objectives of the new PSIP for FY 1985-87 are mostappropriate as regards their emphasis on basic infrastructure since mostproductive activities are left to private initiative. There are 21 newprojects, of which 11 are extension of on-going projects. The Governmenthas been successful in the past in resisting pressures to go forward withbig, politically attractive projects of low priority. The new PSIP doesnot include any such projects. lowever, given the fiscal constraint, whichwill continue to be binding at least over the next fiscal year, the overall

(xv)

size of the PSIP would need to be reduced somewhat in 1985 and be keptunder review, thereafter. Its implementation will also depend on theavailab'lity of external resources on terms and conditions geared toMauritius' needs.

Recent Economic Performance

xi. The economy showed signs of a strong recovery in 1984 afterdisappointing performance in the preceeding years. This reflectedthe expansion of economic activity abroad as well as the favorable impactof domestic economic policies pursued to stabilize the economy and supportexport-oriented industrialisation and tourism. In 1984 there was rapidgrowth in all productive sectors except sugar where output fell belawnormal production level. Gross domestic product increased by 3.1 percentin 1984 as compared to 0.3 percent in drought-affected 1983.

xii. The strongest recovery in 1984 has been observed in themanufacturing sector, especially in the Export Processing Zone (EPZ) wheregrowth has been estimated at 16 percent in real terms. In mDst of the EPZfirms new purchase orders extend as far as end-1985, and many firms areapproaching their capacity limits. A significant increase in newinvestments was also evident in 1984. This strong upsurge in output andinvestment in export manufacturing is attributable to a number of factors:expansion of export markets as a result of the global economic recovery,the promotional campaign undertaken by Government under its StructuralAdjustment Program, improved investment incentives to the private sectorand the emergence of the -Hong Kong factor: the majority of foreignprivate investments to start new export enterprises, mainly in the knitwearand textile are coming from Hong Kong. Most of these investors havealready established markets in the EEC countries, and others are interestedin establishing themselves in the North American market.

-iii. 1984 also witnessed a healthy recovery in tourist arrivals andcapacity use. The most recent estimates indicate a growth of 10 percent invalue added in tourism in 1984. Government has moved ahead effectivelywith measures to strengthen the promotion of Mauritius as a destination fortourists and to open up new air access points abroad, notably Zurich,Taipei and Jeddah. Consideration is also being given to air access fromSingapore, Dubai and Australia. Interest by private investors inexpanding or opening new hotel capacity also seems strong; 50 rooms haverecently been added to one hotel and 200 rooms will be opening up in newhotels in 1985. The target is to double the existing room capacity by1990.

xiv. The tea sub-sector has also shown remarkable progress, followingreforms in the ownership pattern of Tea Development Authority (TDA)plantations as well as favorable export prices.

xv. On the demand side, there was an upturn in capital formation in1983, which continued in 1984. Gross fixed investments in 1984 areestimated to have increased by about 8 percent in real terms.- Most of theincrease is attributable to higher investment in construction other thanresidential buildings, transport equipment and machinery. Private

(xvi)

investment seems to have risen substantially in 1983 and 1984, particularlyin manufacturing. Investment in construction has also shown, for the firsttime since 1980, an increase of 5.5 percent in 1984. This is due toconstruction in road infrastructure and industrial estates, and to hotelexpansion. Housing construction continues to remain stable, in line withGovernment policy to discourage investments in less productiveinfrastructure.

xvi. After a decline of 1.5 percent in 1982 domestic consumptionincreased by about 1.0 percent in 1983 and nearly 2.5 percent in 1984.Increase in real per capita consumption in 1984 was about 1.0 percent.Government consumption increased by 2.7 percent and it is expected that therestraint on government expenditure will continue in the future. With therecovery of domestic income, which rose faster than consumption, grossdomestic savings increased from 15.4 percent of GDP in 1982 to over 18.0percent in 1984.

Prospects: Adjustment and Growth

xvii. The key objectives of Mauritius's structural adjustment strategywill continue to be valid throughout this decade. This should enable thecountry to achieve a sustainable growth path and provide employment for theunemployed as well as new entrants to the labor force. Since 1979 economicgrowth has slowed down and the employment situation has deteriorated.Therefore, a transition to a more growth-oriented development strategywould be desirable within a viable financial framework. This frameworkshould take into account the heavy debt service obligations falling due forrepayment in 1985 and 1986 particularly. The most recent balance ofpayments estimates place Mauritius' debt service ratio, includingrepayments to the IMF, in the range of 26 percent in 1985. Providedfinancing is made availabe on relatively sof t terms, the debt service ratiois expected to decline thereafter. Beginning in 1986, Yauritius should beable to relax its restrictive economic policies gradually and acceleratethe implementation of the structural adjustment strategy.

xviii. The GDP growth for the medium term (1985-1990) could be around3.5 - 4.0 percent per annum. Growth in industrial output, primarily in theExport Processing Zone, would be the main impetus for GDP growth.Expansion in agriculture would remain constrained by the limited prospectsof the sugar subsector, notwithstanding the recovery from the low ou.pu;level of 1984. The continuous recovery of the economy calls for higherlevels of investment in productive sectors. Therefore the ratio ofinvestment to GDP is projected to increase somewhat to 20.5 percent in 1986and remain at around that level until 1989.

xix. Despite higher rates of growth during 1985-1990 the balance ofpayments situation would remain manageable, provided that the export drivewhich began in the early 1980s as part of the structural adjustmentstrategy continues throughout the projection period. Although the exportgrowth rate in 1984 cannot be sustained over the medium term, a 13 percentannual increase in exports of goods and in non-factor services (e.g.,tourism) in current prices should be feasible for the rest of this decade.The external current account deficit is projected to increase from aboutUS$28 million in 1984 to about US$30 million in 1985 and US$57 million in1990.

(xvii)

Externa. Capital Requirements

xx. These current account deficits, the external debt liabilities andthe minimal external reserve build up required would call for a totalinflow of foreign capital of about US$360 million during the 1985-87period. Taking into account the likelilevel of net direct foreigninvestment and expected disbursements from loans already contracted, thiswould call for about US$335 million in new commitments from theinternational community over the period. Multilateral and bilateral donorscould be expected to provide about US$300-315 million of this amount. Theremaining US$20-35 would have to be financed through borrowings fromcommercial sources. Given Mauritius' need for quick-disbursements, aboutUS$100-115 million should accordingly be in the form of program loans. Thedebt service ratio, excluding IMF repayments, should stabilize at around 15percent. Including IMF repayments the debt service ratio would be higherbut remain manageable at around 17 percent.

xxi. If the response of the aid community does not support theadjustment efforts of the Government, Maurttius may be led to borrow inamounts and on terms which would bring the future debt burden beyond safelimits in the 1990s. This is the risk which has to be faced in the nextfew years and which argues for a close monitoring of the economic situationby all parties involved. During the post-sugar boom period and since then,Mauritius has demonstrated excellent managerial capacity to protect itsinternational credit standing. There has never been a default or paymentsarrears on external debt. Under the SAL and stabilisation programs thegovernment has taken measures that many countries have not been able orwilling to take. Provided that the Government continues to be committed toa continued process of adjustment, Mauritius should remain creditworthy forthe projected amounts of non-project and project borrowing.

MAURITIUS: ADJUSTKENT AND GROWTH

COUNTRY ECONOMIC MEMORANDUM

I - INTRODUCTION

1.1. The last Country Economic Memorandum (CEM) on Mauritius waspublished in January 1983. That CEK and an updating economic note weredistributed to the Second Consultative Group meeting held in June 1983.Since then, a Population Sector Memo has been published in grey cover and anumber of studies commissioned by the Government have been completed.These include two reports prepared by the Sugar Commission of Inquiry andsector reports on Industry.

1.2. This Economic Memorandum reflects the findings of an economicmission which visited Mauritius between July 23 and August 17, 1984. Theobjective of the memorandum is to review Mauritius' economic performancesince the last Consultative Group meeting and discuss the country's growthand employment prospects to the end of this decade. The report covers thefollowing topics: a review of the stabilization efforts since 1979 andrecent economic performance; a review of the structural adjustment policiesalready undertaken and to be followed during the second half of the 1980sand finally, a discussion of the prospects of the Mauritian economy during1985-90 with a change in the emphasis of economic policies from austerityto a more growth-oriented strategy.

Economic Structure

1.3. Mauritius is an island with smaller outer islands situated in theIndian Ocean, densely populated and with an economy dominated by sugarproduction. Despite significant expansion of other sectors since the early1970s, sugar still occupies around 90 percent of the cultivable area andaccounts for about 60 percent of export earnings. The level of economicactivity, is therefore, highly sensitive to fluctuations in sugarproduction and exports. Overdependence on a single commodity also rendersthe economy highly vulnerable to e%ternal shocks and disturbances.

1.4. The main island of Mauritius has a population of 1 million on aland area of about 2,000 km2, just over half of which is cultivable. Theouter islands are dispersed and less developed. Despite the spectaculardrop in fertility during 1965-73, the population growth rate (currently at1.5 percent) has recently been rising and is a matter of concern toGovernment.

1.5. Mauritius enjoys a pleasant tropical climate which makes itattractive for tourists. however, the country is subject to cyclonesbetween late December and March which can cause severe damage. Major

-2-

cyclones occur on average at 12-15 year intervals. The absence of mineralresources and the distance of Mauritius from major markets (about 6thousand miles from Western Europe; 10 thousand miles from the U.S.) affectthe potential for economic development and condition the choice of economicactivities best suited to Mauritius. Furthermore, the country, does notlie on the main sea routes and thus maritime transport costs are higher inMauritius than in countries competing for similar markets.

Economic Performance to 1979

1.6. In the early years following independence (1968) the Mauritianeconomy was characterized by low economic growth, conservative economicmanagement and the emergence of a major unemployment problem. During thatperiod the GDP increased at an average rate of 1.1 percent per year whilethe investment level remained virtually constant at about 16 percent ofGDP. At the beginning of the 1970s Mauritius adopted a pragmaticdevelopment strategy with the twin objectives of growth and socialjustice. With an open and relatively free economy, the Governmentencouraged private initiative to assume an important role in thedevelopment process; itself providing infrastructure, institutional supportand incentives to the private sector. Social justice was to be achievedthrough alleviation of poverty and unemployment. The social objectiveswere pursued through public works programs, minimum wage regulations,public provision of health care and education, food subsidies and selectivecontrol over consumer prices.

1.7. The country's economic performance during most of the 1970s wasremarkably successful. With an open economy and an export-orienteddevelopment strategy the Goverrnment encouraged the production of cashcrops; sugar and tea for export, the development of export mauufacturingindustries and tourism and provided infrastructure for the growing needs ofthe economy. The unprecedented increase in sugar prices in 1973 and 1974helped the economy to grow by more than 10 percent per year between1972-77. During this period, gross domestic savings increasedsubstantially and helped accelerate the growth of manufacturing,construction and service sectors. The rapid growth in production andexports was also accompanied by a rapid increase in employment; in 1977 theunemployment rate was reduced to about half of its peak level at thebeginning of the 1970s. About a decade after independence, the GNP percapita was above $1,000; equivalent to the level of a middle-incomedeveloping country. The adult literacy rate was more than 80 percent andbasic needr of tne vast majority of the population were extensivelycovered.

1.8. During the post sugar-boom period, however, between 1976 and1979, serious economic difficulties emerged. The sharp turnaround inMauritius' international terms of trade following the decline of sugarprices in 1976 and the second price increase in petroleum led to a rapiddeterioration in the balance of payments. Foreign exchange reserves felland the country had to resort to the Eurodollar market to finance some of

its development requirements. The balance of payments difficulties werefurther aggravated by an expansionary fiscal policy. During 1975-1979 anambitious public investment program was initiated that increased capitalspending at an average annual rate of 40 percent while current expendituresgrew over 30 percent per year. Although the growth of government spendingmoderated after the end of the sugar boom, the fiscal deficit continued tomount, reflecting expansionary economic policies that were increasingly outof line with the reduced resource availabilities. Failure to take promptaction to revert to more austere economic policies when sugar pricesdeclined led to excessive budgetary deficits, strong domestic demand,rising domestic inflation and ultimately widening balance of paymentsdeficits.

1.9. Growing current account deficits of the balance of payments werefinanced largely by increasing recourse to external borrowing onnon-concessionary terms. This in turn resulted in a rapid increase inMauritius' debt service obligations. During 1976-79 the country's externaldebt more than tripled and the debt service ratio rose from a modest 1% in1976 to nearly 10% in 1979. This period was also marked by a decelerationof GDP and export growth. The domestic inflation rate rose dramaticallyand the unemployment rate reached a critically high level.

II. STABILIZATION SINCE 1979 AND RECENT PERFORMANCE

2.1. Beginning in 1979, the Government embarked on a stabilisation andstructural adjustment program that could be supported by the IMF facilitiesand World Bank Structural Adjustment lending.

Stabilization Programs

2.2. For short term adjustment focussed primarily on demand-managementpolicies, Mauritius has worked closely with the IMF. Since 1979, fourconsecutive stand-by arrangements covering 1979/80 - 1983/84, have beensuccessfully implemented. Central to these programs has been the adoptionof policies in the areas of the exchange rate, reductions in consumersubsidies, wage restraint, restrictive credit and monetary policies,reduction in the overall fiscal deficit, and the maintenance of a liberalsystem of trade and payments. Despite unfavorable factors including aworld-wide recession in 1982, adverse weather conditions and continueddeterioration in the country's terms of trade, progress under the stand-byarrangements has been good: the overall budgetary deficit has beennarrowed (from about 14 percent of GDP in FY1981 to about 7.3 percent in FY1984), Lhe external current account deficit has been reduced (from over 13percent of GDP In 1981 to an estimated 2.6 percent in 1984), and thedomestic inflation rate has been dampened (from about 27 percent in 1979 to7.3 percent, in 1984).

-4-

2.3 In 1979 and 1981, the Mauritian rupee was devalued by 30 percentand 20 percent, respectively, vis-a-vis the SDR. In February 1983 theGovernment changed the peg of the Mauritian rupee from the SDR to atrade-weighted basket of currencies more representative of Mauritius'external trade pattern. Since then, Mauritius has been pursuing a flexibleexchange rate policy which together with the wage policy has been highlyeffective in maintaining Mauritius' export competitiveness.

2.4. A fifth stand-by arrangement for a period of eighteen monthscovering January 1985-June 1986 in an amount equivalent to SDR 49.1 millionhas recently been approved by the IMF's Board (March 1, 1985). The newprogram primarily continues the policies of the previous stand-byarrangements with further fiscal adjustment, restraint on total creditexpansion, a flexible exchange rate policy and a cautious wage policy. Thenew program also gives increasing emphasis to the stimulation of growth andemployment generation through export promotion and diversification andmajor policy reforms in key economic sectors. In this respect, the newstand-by arrangement and the ongoing structural adjustment efforts aremutually reinforcing.

Structural Adjustment Program

2.5. Mauritius' economic imbalances during the post sugar-boom periodresulted from the Government's expansionary response to rising unemploymentand the country's overdependence on a single commodity. With the dramaticturnaround in the country's terms of trade during 1976-79 it becameapparent that, for sustained growth of output and employment and a viablebalance of payments position in the medium term, Mauritius had to furtherpromote and diversify its exports, both in agriculture and industry andencourage import-substitution of food and energy. Given the small size ofthe domestic market, export growth was of vital importance te the economy.Export diversification was also required to reduce the country'soverdependence on sugar and generate additional employment.

2.6. A Structural Adjustment Program focussing more on supply sidemeasures -was initiated in 1980. Concurrently, policy discussions beganwith the World Bank and the Program was supported by the First StructuralAdjustment Loan (SAL I). Despite shortcomings in implementation, the FirstStructural Adjustment Loan am proved timely and its results positive.Under SAL I, the country's energy planning capacity was strenghtened, themedium term public investment program was reduced and rationalized and aset of policy reforms in agriculture and industry was initiated. Theprogram contributed to the mobilization of a financing package at a timewhen Mauritius' foreign exchange reserves were completely exhausted. Italso helped to develop a dialogue both internally and with theinternational community - on a large number of sector issues whose adequatesolution are critical for the achievement of sustained growth of output andemployment. Also, the discussions on the different components of the FirstStructural Adjustment Loan helped the emergence of a general consensus

among different segments of political opinion in Mauritius on the urgencyand content of the future policy reforms required by the economy. This inturn set the stage for further action on the part of the Government, ascontemplated in the second Structural Adjustment Loan (SAL II).

2.7. The thrust of the Second Structural Adjustment Loan, introducedin late 1983, is basically in four areas: (a) restructuring of the sugarindustry and agricultural diversification (b) further promotion ofexport-oriented industrialization, (c) tourism development and (d)improvement in public resource management.

2.8. A first approach to a restructuring program for the sugarindustry was announced by the Government in July 1984 after the findings ofa Sugar Commission of Inquiry. The program, which Includes a major taxreform and factory rationalisation, aims at (a) maintaining the long termfinancial viability of the large estates, (b) rationalising millingoperations on a national scale and rehabilitating and modernising factoryequipment, (c) raising the productivity of small planters and (d) improvingthe utilisation of the industry's by-products and (e) diversifying theoutput in terms of food production and/or other agricultural activities.On the basis of the restructuration program, an Action Plan for themodernisation and rehabilitation of the industry has, more recently beendrawn up, which details the measures to be taken to achieve theseobjectives.

2.9. In the manufacturing sector continued promotion of export-oriented industries remains a major priority for Mauritius. Given thestagnant nature of the sugar sub-sector, the small size of the domesticmarket and the sizable backlog of unemployed, export-oriented manufacturingoffers the strongest potential to foster growth and add to foreign exchangeearnings. The set of medium term policy reforms for manufacturing industryfocusses on improving Mauritius' competitiveness, extending the system ofexport incentives to all firms capable of export activities and attractingnew foreign investment and technology to export manufacturing.

2.10. In tourism, the primary objectives are to increase foreignexchange earnings and generate additional employment. Infrastructure andhigh air fares constitute the two main constraints to a more rapid growthin tourism. The program for tourism aims at fuller utilization of existingcapacity through tourism promotion and improved air access to Mauritius andexpansion of capacity through encouragement of new private investments.

2.11. Energy policies were not dealt with explicitly in the SecondStructural Adjustment Loan. The Government has recently established anEnergy Planning Division in the Ministry of Energy and InternalCommunications in order to define and program the implementaiton ofeffective and comprehensive energy policies and projects. The greatmajority of energy sector investment in Mauritius has been, and willcontinue to be in the power sub-sector. Future major expansion of powersystem capacity and energy supply is likely to come from the utilisation ofbagasse; hence power system planning and development is now closely linkedwith the sugar restructuring program. Accordingly, displacement of oilwith bagasse as a fuel for power generation is becoming an important importsubstitution program. Power generation from baggasse may grow from about10 percent of supply now to 30 percent in 1990, displacing perhaps 25,000tonnes, or about 15 percent of the country's oil bill by the end of thedecade.

- 6 -

2.12. The policy reforms and programs in agriculture, industry, tourismand energy are further supported by a rolling three-year Public SectorInvestment Program (PSIP) which is geared primarily to the needs of thesesectors.

Recent Economic Performance (1979-1983)

2.13. After a decade of impressive growth performance followingindependence, expansion of Mauritius' economy slowed down significantlysince 1979. There was a major decline of around 10 percent in real outputin 1980 as a result primarily of a 30 percent drop in sugar production.Although this was followed by a strong recovery during the next two years,at a rate of 6 percent each year, the level of real GDP in 1982 was onlyslightly higher than that of 1979. In 1983 GDP stagnated once again (Table1). There were wide swings in sugar output from year to year after 1979,due primarily to adverse weather conditions. The sector's share in GDP,including sugar manufacturing, fell to little over 10 percent in 1980, theyear of extreme cyclone damage, and was only 12 percent in drought-affected1983.

Table 1 - RFI GXXTh OF GDP BY MIN MA2MR5, 1979-84

1983 Annual Gowth Rate (%)Rs million As % of GDP 1979-81 1982 1983 1984 '/

Agriculture 1485 13.9 -10.5 19.8 -10.9 -1.8of which sugar 1030 9.6 -13.6 28.5 -17.0 -5.0

other 455 4.3 0.0 -3.3 6.9 5.5

Marufacturii:g 1695 15.9 0.5 7.2 -0.5 6.4of *idch sugar 300 2.8 -15.0 12.0 -16.0 -1.9

EpZ 2/ 510 4.8 12.0 3.0 4.0 16.1DC, others 885 8.3 4.1 -2.0 3.0 3.5

Costruxtion 660 6.2 -11.5 -4.1 1.0 3.0

Services 6810 63.9 1.0 2.8 3.1 3.3of i*ch Utilities 245 2.3 - 10.3 -10.0 4.9

Tourias 261 3.8 -1.3 -1.0 4.2 10.0Transport 1225 11.5 -0.4 3.2 2.5 4.0Goverrmnt 1350 12.7 2.5 4.4 2.0 2.0

CDP at factor cost 10650 100.0 -2.3 6.0 0.3 3.1

Note: Growth rates for 1979-82 are based on data in 1976 prices and for1983-84 on data in 1982 prices.

1/ Preli-minary2, Import-substitution subsector.

Source: Statistical Annex Tables.

-7-

2.14. During 1979-1983, the setback in non-sugar activity was smaller.Nevertheless the real rate of growth In manufacturing (excluding sugarmanufacturing) averaged only 3 percent per annum as compared to 17 and 10percent per year achieved during 1972-76 and 1976-79, respectively. Fixedinvestment in manufacturing had risen steadily In real terms until 1979,following the establishment of the Export Processing Zone (EPZ) In 1970.It fell each year from 1979 to 1982. The slowdown in industrial growthreflected an actual decline in the import-substitution sub-sector while EPZgrowth also decelerated. Devaluations In 1979 and 1981 helped to restorecompetitiveness in the industrial sector; however, in 1981 Mauritius lostits preferential status for textile exports vis-a-vis the EEC market whentariff preferences were extended to other developing countries.Furthermore, in 1982 the country's major export markets were depressed as aresult of international recession and increased protectionism both in theEEC and the US. It was not until late-1983, that new orders for knitwearand textile products started to come in, as well as applications to opennew Export Processing Industries (see also para. 2.40). After declining by8 percent in 1982, investment in manufacturing recovered in 1983 andreached a level slightly above that of 1981.

2.15. By 1979, tourism had become the third largest foreign exchangeearner after sugar and manufacturing, and a major source of employmentproviding jobs directly and indirectly to about 10 percent of the laborforce. Between 1979-83 there was a serious setback in tourism; neither thenumber of tourist arrivals nor the nights spent regained their 1979 level.The downturn was mainly attributable to the second oil crisis in 1979 whichraised the air fares substantially, the cyclonic conditions and theirafter-effects in 1980, and the economic recession in 1982 in the majortourist generatirng countries.

2.16. Construction declined through 1983 in both real and relativeterms reflecting completion of one major project, the bulk sugar terminal,and the effects of restrictive demand management policies.

Developments in 1984

2.17. The economy shows signs of a modest recovery in 1984, aftervirtual stagnation in 1983. This reflects expansion of economic activityabroad as well as the favorable impact of domestic economic policiespursued to encourage export-led industrialization and tourism. Preliminaryestimates indicate that in 1984 there has been rapid growth in allproductive sectors except sugar.

2.18. The strongest recovery in 1984 has been observed in themanufacturing sector especially in the Export Processing Zone (EPZ). Basedon a firm-level survey carried out in 1984, the rate of growth ofmanufacturing output in the Export Processing Zone firms has been estimatedto be around 16 percent in real terms. Factual evidence indicates that inmost of the LPZ firms new purchase orders extend as far as end-1985 andthat many firms are approaching their capacity limits. A significantincrease in new investments is also evident in 1984. These new investmentsare expected to increase the production capacity in export manufacturing byabout 20 percent by end-1985.

- 8 -

2.19. A strong upsurge in output and investments in the ExportProcessing Zone is attributable to a number of factors: expansion ofeconomic activity abroad, the promotional campaign undertaken by Governmentunder its Structural Adjustment Program, improving investment incentives tothe private sector and the emergence of the Hong Kong syndrome. Themajority of applications to start new export enterprises, mainly inknitwear and textile industries, are coming from Hong Kong. Some of theseinvestors already have established markets in the EEC countries, and othersare interested in establishing themselves in the North American market.Push factors within Hong Kong due to political uncertainties have beenpartly responsible for the recent surge of private capital inflow from HongKong. However, the Government efforts to promote the export-led industryhave also been quite active, especially in the Far East. Severalincentives have attracted new investors, such as the provision of taxholidays, import duty exemptions, infrastructural facilities and evenMauritian nationality. Administrative procedures have also been greatlycentralized and simplified.

2.20. In 1984, there has also been a healthy recovery in touristarrivals and capacity use. From January to June 1984, tourist arrivalsreached 65,300 as compared to 56,700 in the same period of 1983. Touristsfrom Europe, notably France, Germany, Italy, and the United Kingdom,accounteA for more than one-third of total arrivals. The average touriststay has also increased to 11 days as compared to 9 days over the pastdecade Preliminary estimates indicate a growth of 10 percent in valueadded a 1984. The government has moved ahead effectively with measures tostreng..hen the promotion of Mauritius as a destination for tourists and toopen up new air access points abroad, notably Zurich, Taipei and Jeddah.Consideration is also being given to air access from Singapore, Dubai andAustralia. Interest by private investors in expanding or opening new hotelcapacity also seems strong. The target is to double the existing roomcapacity by 1990.

2.21. On the demand side gross capital formation which peaked in 1978fell steadily up to 1983. In real terms, total fixed investment declinedby almost 40 percent during 1978-1982, then rose by some 3 percent in1983 (Table 2). The decline was fairly even]y shared by all economicsectors except energy and water which recovered somewhat in 1982 due toconstruction of a major hydroelectric project. The rise in totalinvestment in 1983 was due mainly to a revival of investments inmanufacturing.

2.22. Upturn in capital formation in 1983 has continued in 1984. Grossfixed investments in 1984 are estimated to have increased by about 8percent in real terms. Most of the increase is attributable to higherinvestment in constri'ztion other than residential buildings, transportequipment and machinery. Private investment seems to have risensubstantially in 1983 and 1984, particularly in manufacturing. Investmentin construction has also shown for the first time since 1980 an increase of5.5 percent in 1984. This is due to construction in road infrastructure,industrial estates and hotel expansion. Housing construction continues toremain stable, in line with Government policy to discourage investments inless productive infrastructure.

- 9 -

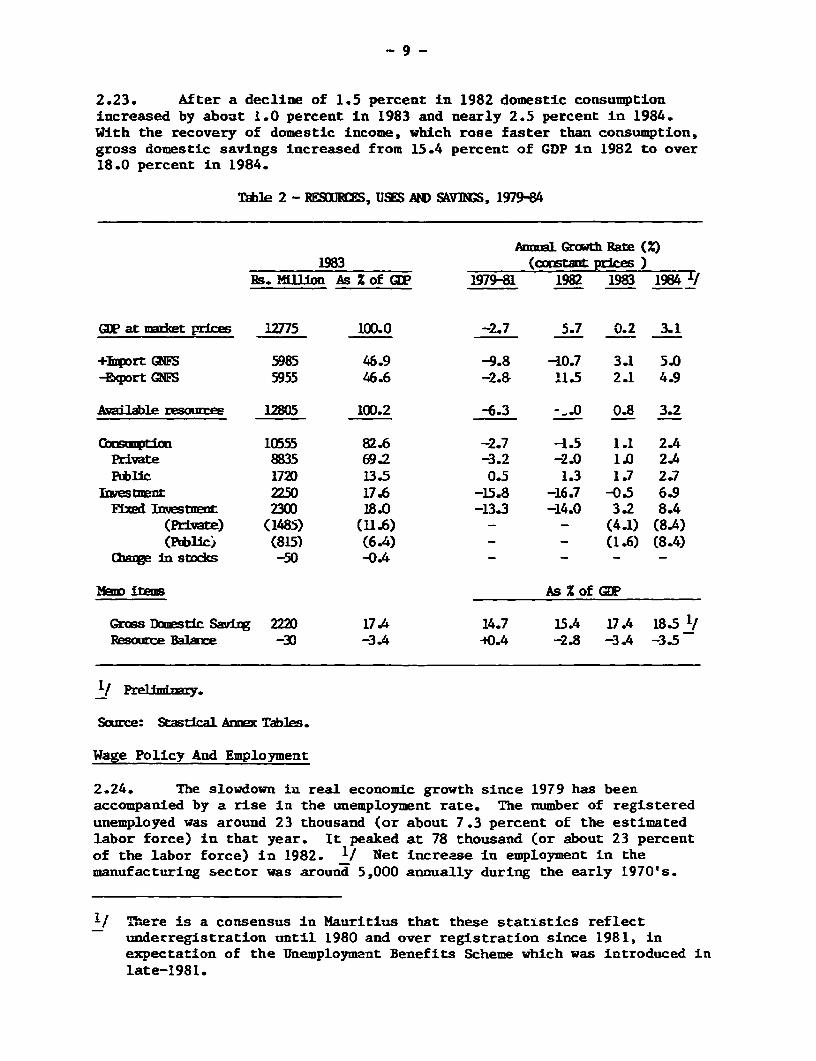

2.23. After a decline of 1.5 percent in 1982 domestic consumptionincreased by about 1.0 percent in 1983 and nearly 2.5 percent in 1984.With the recovery of domestic income, which rose faster than consumption,gross domestic savings increased from 15.4 percent of GDP in 1982 to over18.0 percent in 1984.

Table 2 - WRE9JRE, USES AND SkYI%S, 1979-84

Anmkl Grth Rate (X)1983 (constant prices )

Rs. Million As x of di 1979-81 1982 1983 1984 /

GOP at nmret prices 12775 100.0 -2.7 5.7 0.2 3.1

+bWiurt GNFS 5985 46.9 -9.8 -10.7 3.1 5.0-Export GNQE 5955 46.6 -2.8 11.5 2.1 4.9

Available resounces 12805 100.2 -6.3 - -. 0 0.8 3.2

10555 82.6 -2.7 -1.5 1.1 2.4Private 8835 69.2 -3.2 -2.0 1.0 2.4Fkblic 1720 13.5 0.5 1.3 1.7 2.7

Invest7wnt 2250 17.6 -15.8 -16.7 -0.5 6.9Fx Investment 2300 18.0 -13.3 -14.0 3.2 8.4

(Privat) (1485) (11.6) - - (4.1) (8.4)(Public} (815) (6.4) - - (1.6) (8.4)

CargeIn stocks -50 -0.4 - - - -

items As % of GIP

Gross Dowstic Sarrxg 2220 17.4 14.7 15.4 17.4 18.5 1/Resource Balance -30 -3.4 -0.4 -2.8 -3.4 -3.5

V Prelimidazy.

Source: Stastical Aex Tables.

Wage Policy And Employment

2.24. The slowdown in real economic growth since 1979 has beenaccompanied by a rise in the unemployment rate. The number of registeredunemployed was around 23 thousand (or about 7.3 percent of the estimatedlabor force) in that year. It peaked at 78 thousand (or about 23 percentof the labor force) in 1982. 1/ Net increase in employment in themanufacturing sector was around 5,000 annually during the early 1970's.

1/ There is a consensus in Mauritius that these statistics reflectunderregistration untll 1980 and over registration since 1981, inexpectation of the Unemployment Benefits Scheme which was introduced inlate-1981.

- 10 -

This trend tapered off gradually after 1979 and turned negative in 1982,when industry as a whole had to lay off a significant number of employees.With the recovery in economic activity, however, employment opportunities,particularly in export-manufacturing and tourism, expanded vigorously inthe latter part of 1983 and in 1984. There are indications that betweenSeptember 1983 and June 1984 some 8,200 additional jobs were created in theExport Processing Zone as a result of fuller utilization of existingcapacity. Including additional employment generated in tourism andconstruction it has been estimated that employment growth in 1984 hasslightly exceeded the increase of about 10,000 in the labor force for thefirst time in several years. Despite these improvements, however, thelevel of unemployment at 20 percent, still remains high and is a majorissue in Mauritius.

2.25. Wage policy has b.een an important part of adjustment policiessince 1979. The policy is implemented annually througn a national wageaward (the cost of living adjustment), which is based on the previousyear's inflation rate. The cost of living adjustment is also mandatory inthe private sector and is decided, at the beginning of each fiscal year,after national tripartite negotiations. During 1979-1984 wage awards inboth public and private sectors have been held considerably below cost ofliving increases. From 1979/80 through 1983/84, these awards have amountedto a cumulative increase of 55 percent, compared to 122 percent for theconsumer price index in the same period. The cost of living adjustment for1984/85 equaled about 3 percent, compared to the rise in the cost of livingindex in 1983/84 of 5.6 percent. The Government continues to view wagerestraint as vital to improve the country's export competitiveness.

Table 3: LABOR FORCE, EMPLOYMENT AND UNEMPLOYMENT, 1979-83(In thousands)

1979 1980 1981 1982 1983

Labor Force 313 324 332 339 355Employment 286 289 290 289 294Large Establishments 199 197 195 194 191Informal Sector 1/ 87 92 95 95 103

Unemployment (residual) 27 35 42 50 61

Registered Unemployment 2/ 23 31 57 78 73

Memo Items

Unemployment Rate (percent)Residual Unemployment 8.6 10.8 12.7 14.7 17.2Registered Unemployment 7.3 9.6 17.2 23.0 20.6

/ Estimated by the CSO based on assumptions made about labor/landratios in small scale agriculture and about the number of employeesper license issued to operate a small establishment.

2/ Unemployment registered in the official employment exchanges.

Source: Central Statistical Office.

- 11 -

Fiscal Policy and Performance

2.26. The drop in sugar prices after the sugar-boom, natural calamitieslike cyclones and drought and costly welfare state policies caused thebudget deficit to reach a peak of 14 percent of GDP in 1980/81. Followingthe end of the sugar boom the government did not retrench spending forseveral reasons. Some development projects necessitated outlays overseveral years and many projects had a high job-creation component and weredifficult to cut back at a time when private employment opportunities weredeteriorating. Current expenditure decisions, on the other hand, couldonly be reversed with great political difficulty.

2.27. Since 1979, however, there has been a sharp change in fiscalpolicy, which has become a key element of stabilisation. Despite a setback in 1980 due to severe cyclones, the fiscal adjustment since 1979 hasbeen substantial. The current budget deficit, which peaked at Rs. 554million in 1981/82, was reduced by one half to Rs. 255 million in 1983/84.The overall fiscal deficit at 12.6 percent of GDP continued to be alarmingin 1981/82. Through continuous efforts to postpone or slow down lowpriority capital spending, it was reduced substantially to about 7.3percent of GDP in 1983/84. The 1984/85 budget calls for additional cuts ingovernment spending and aims at reducing the fiscal deficit further toabout 6.0 percent of GDP.

2.28. On the revenue side discretionary tax measures taken since 1979to reduce the fiscal deficit included increases in the rates of importduties, across-the-board surcharges, and the introduction in 1983 of asales tax levied on wholesale trade. New tax measures introduced in1983/84 included a land development tax with a rate of 40 percent on theincreased value of land resulting from conversion of agricultural toresidential use; a tax on seasonal residences and vacation bungalows; and aland transfer tax of 5 percent on the value of land transferred. Thesetaxes were expected to bring about 45 million Rs. in 1983/84 but actuallybrought much less. Import duties were restored on some non-basic fooditems as well as luxury items. Several exemptions from import duties werewithdrawn. A withholding tax of 20 percent of dividends as an advancepayment on the income tax due was also introduced. As a result revenuesincreased by 2 percent in real terms during 1981/82-1983/84 while currentexpenditures were kept constant.

2.29. Current expenditures were restrained with substantial reductionsin budgetary subsidies to rice, wheat flour and to private educationalinstitutions. Retail prices of rice and wheat flour were raised in 1982/83and again in 1983/84 to curtail government spending and promote theproduction of domestically produced food stuffs. Primarily because ofthese measures but also as a result of the continued policy of wagerestraint which, allowed only partial compensation for inflation, thecurrent account deficit dropped to about 1.9 percent of GDP in 1983/84 fromabout 4.0 percent in 1981/82.

- 12 -

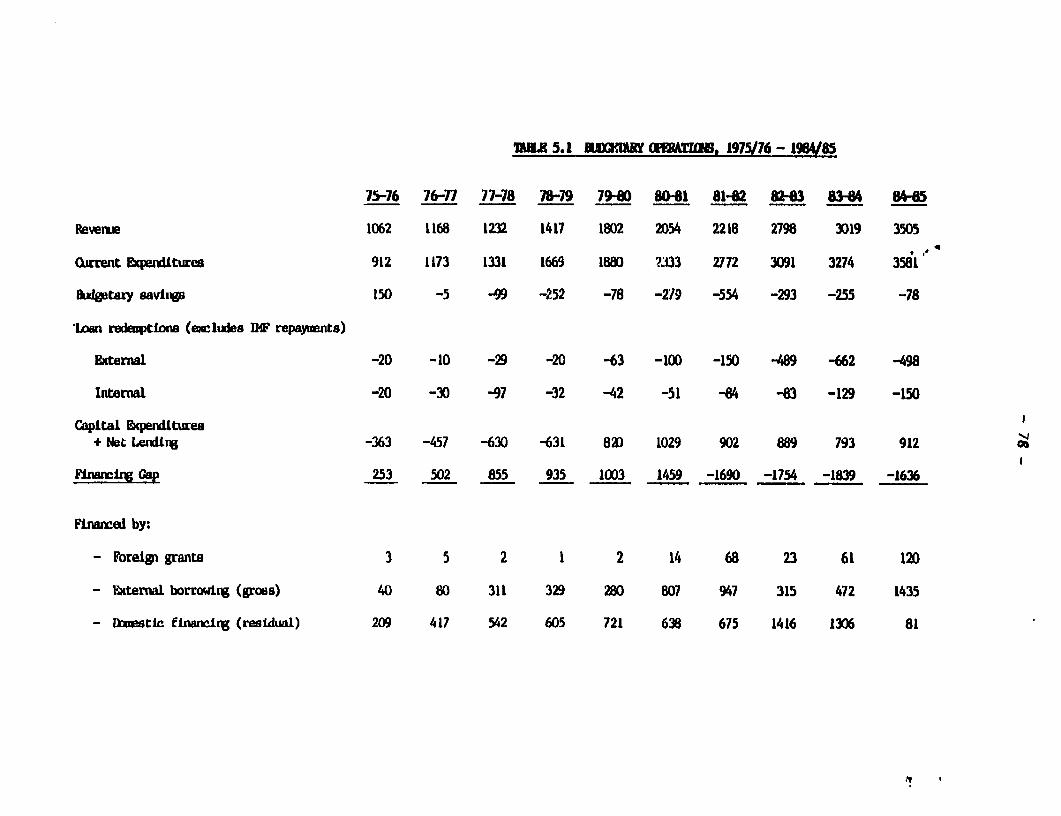

Table 4: CENTRAL GOVERNMENT OPERATIONS, FY81-85(Rs million)

1980/81 1981/82 1982/83 1983/84 1984/85(Prov.) (Budget)

Current revenue 2059 2278 2798 3019 3505Current expenditure 2318 2772 3091 3274 3581Current deficit -258 -554 -293 -255 -78

Capital expenditure 1048 902 889 793 912

Overall balance -1307 -1456 -1182 -1048 -988

Financed by:Grants 14 68 23 61 120External Borrowing 638 947 315 472 1435Debt Amortization -152 -234 -572 -791 -648Domestic Borrowing 807 675 1416 1306 81

Overall deficit aspercent of GDP 14.0 12.6 9.5 7.3 5.8

Source: Statistical Annex Tables.

2.30. Capital expenditures were cut sharply in 1981/82 from theirunsustainable high levels during the pre-stabilization period. Furtherreductions in capital spending also materialized in subsequent years due todelays in project execution. There was a modified pattern in deficitfinancing for both 1982/83 and 1983/84 marked by negative net foreignborrowing. This was due to a surge in capital repayments against a reducedlevel of new disbursements. This left the burden of financing on domesticsources in both years. Due to ceilings on total credit to the economy,fewer funds were available for private activity. This situation isexpected to reverse in 1984/85 with net foreign borrowing becoming positiveand domestic financing being substantially reduced.

2.31. The 1984/85 budget continues to reflect the restrictive fiscalobjectives of the ongoing stabilisation efforts. The principal new revenuemeasure introduced in 1984/85 is a 10 percent surcharge on customs andstamp duties, which is expected to yield an additional Rs 120 million (or 7percent of 1983/84 tax revenue). Grants are expected to nearly doublereflecting additional aid from European sources. The budget figures takeno account, however, of benefits that may arise from the June 1, 1984establishment of a Unifed Revenue Board, which will co-ordinate the effortsof the various revenue departments and work with the newly established TaxAppeals Tribunal, set up to expedite the adjudication of tax disputes.

- 13 -

2.32. Another important structural reform introduced by Government in1984/85 is a change in the company tax. The tax, which had been set at 55percent for public companies and 66 percent for private companies, wasformerly calculated on net profits after dividend distributions and henceencouraged the distribution of dividends. In tne 1984/85 budget thededuction for dividend distribution was eliminated, and the tax rate wasreduced to 35 percent for both public and private companies. In addition,the companies that are in nontraditional export sectors (i.e., other thansugar, molasses, and tea) will benefit by a 2 percentage point reduction inthe rate of company taxation for each 10 percent of their turnoverexported, subject to a minimum corporate tax rate of 25 percent. Thesemodifications, which have been introduced as part of the Government'sstructural adjustment strategy, are expected to encourage privateinvestment and promote export-oriented production.

2.33. On the expenditure side, the 1984/85 budget continues therestraint on current expenditures exercised in the previous three years.The wage bill is budgeted to increase by only 5.6 percent compared with 11percent in 1983/84. Total subsidies and transfers will remain virtuallystable, as slight increases in subsidies to local government, educationand pensions are expected to be offset by a further decline (of more than25 percent) in subsidies for rice and wheat flour. Capital expenditure isbudgeted to increase only slightly from the outturn of 1983/84 and toremain at a little over 5 percent of GDP. The Government expects that thework of the recently established Management Audit Bureau, in conjunctionwith spending agencies, will result in a much closer correspondence betweenthe capital budget and the actual outturn, with the former being based uponthe most realistic possible assumptions. The fiscal deficit in FY1984/85was Initially intended to be financed partly by external financing andpartly by domestic bank borrowing. However balance of payments problemsforced the government to raise an additional 500 million Rupees (US$40million) in Eurodollar loans, which should liberate most of the domesticfinancial resources for the private sector.

Money and Credit

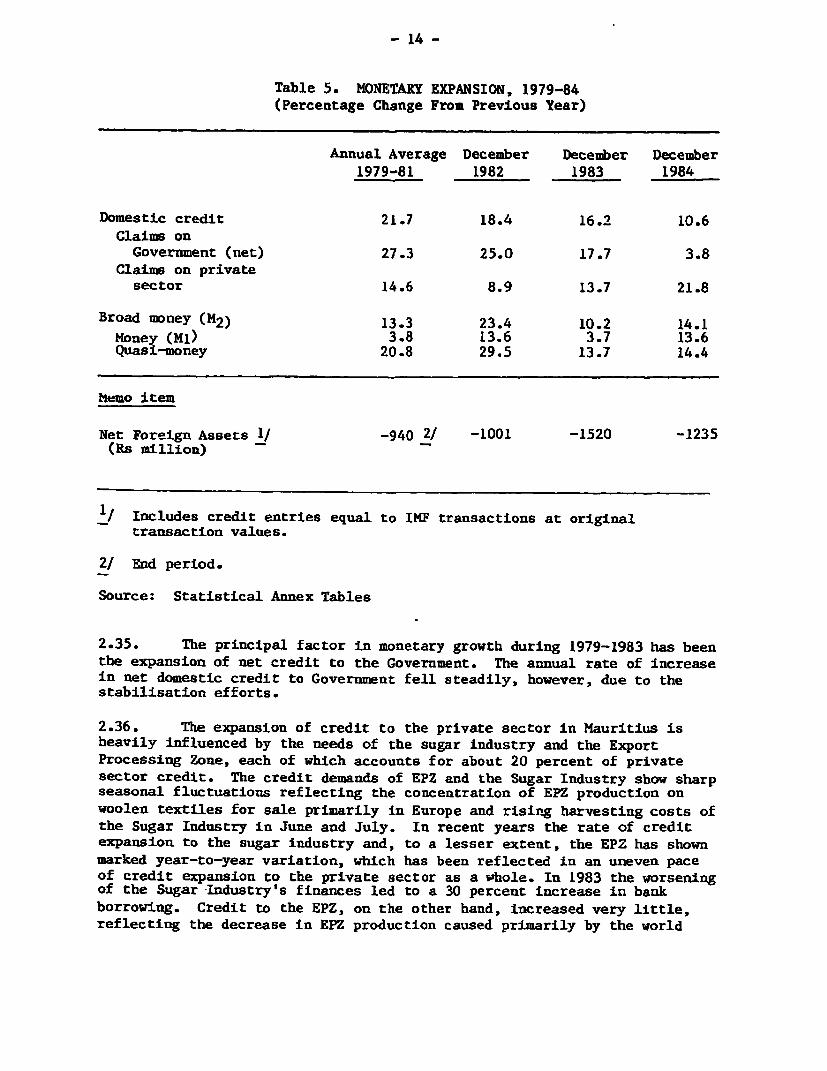

2.34. Since 1979 broad money has increased in line with the trend ofnominal GDP around 14 percent per year. In 1981 the deterioration in thebanking system's net foreign assets position contributed to the slow growthin money supply. In 1982 nominal deposit interest rates were raised andinflation declined, bringing an end to negative real interest rates. In1983, the money supply increased more slowly than GDP, in response to thedecline in real deposit rates and also reflecting some reluctance on thepart of banks to bid for deposits in view of ceilings on their lending tothe private sector and their excess liquidity. In 1984 the increase inprivate credit accelerated while a new US$ 40 million Eurocurrency credit,disbursed in September 1984. led to a sharp reduction in net domestic bankclaims on the Government.

- 14 -

Table 5. MONETARY EXPANSION, 1979-84(Percentage Change From Previous Year)

Annual Average December December December1979-81 1982 1983 1984

Domestic credit 21.7 18.4 16.2 10.6Claims onGovernment (net) 27.3 25.0 17.7 3.8

Claims on privatesector 14.6 8.9 13.7 21.8

Broad mDney (M2) 13.3 23.4 10.2 14.1Money (Ml) 3.8 13.6 3.7 13.6Quasi-money 20.8 29.5 13.7 14.4

Memo item

Net Foreign Assets 1/ -940 2/ -1001 -1520 -1235(Rs million)

,' Includes credit entries equal to IMF transactions at originaltransaction values.

2/ End period.

Source: Statistical Annex Tables

2.35. The principal factor in monetary growth during 1979-1983 has beenthe expansion of net credit to the Government. The annual rate of increasein net domestic credit to Government fell steadily, however, due to thestabilisation efforts.