Embed Size (px)

Citation preview

Level one Market Study Report

Report submitted to Geodetics

THE CONSULTANT

Martin Ombima, P.O.BOX 2696 40100 Kisumu Tel +254721710323/0786710323 Email: [email protected]

July 14, 2016

Page 2

Table of Contents A SUMMARY OF THE STUDY AND THE KEY OBSERVATIONS ...................................................................... 3

SECTION A: THE PROFILE OF THE RESPONDENTS ..................................................................................... 5

SECTION B: PRODUCTION ........................................................................................................................ 6

SECTION C: SELLING ............................................................................................................................... 12

SECTION D: AGRICS CLIENT SATISFACTION: ............................................................................................ 21

July 14, 2016

Page 3

A SUMMARY OF THE STUDY AND THE KEY OBSERVATIONS

This study was conducted among 249 respondents equally spread amongst four administrative

counties of Kakamega, Busia, Siaya and Bungoma but divided into six regions within the four

counties, one in each county, and three in Kakamega (Kakamega North, Kakamega East and

Butere). For the sake of this study, we will have six regions of Kakamega North, Kakamega East,

Butere, Busia, Bungoma and Siaya.

The study focused on broad areas including:

i. The profile of the responding farmer

ii. The production

iii. Selling of what is produced within the farm

iv. Agrics clients‟ certification

For each of the broad areas mentioned above data was collected, analyzed and conclusions made

on areas that interventions can be made by various stakeholders.

Under the profile of the respondents, researchers understanding of their characteristics have been

provided in tables and description made. A synopsis of the respondents reached from the six

regions have been provided, their gender, household characteristics, age, their land size, Agrics

products taken, household income, their wished and desire amongst others.

Under production, an understanding of the various crops that the respondents produce and the

farm inputs that are utilized has been established. An analysis on the agronomic services that

were utilized has also been made. An understanding on when various farming activities are

undertaken was also established. The following observations were made:

i. As an agronomic service, traction/mechanization in land preparation, most of the respondents

were not certified by the current service providers. This is an area that stakeholders and other

service providers can explore further on the possibility of providing this service. Note that the

respondents are ready to pay for it, and they are not satisfied by the current service providers

ii. On soil testing, 91% of the respondents seem not to understand the soil testing concept as an

agronomic service. This is a gap that stakeholders can come in to fill in the information gap, and

provide the soil testing service

iii. From the analysis, there doesn‟t seem to be a clear relation between climatic conditions/the

weather and land preparation. Majority of the farmers prepare their land in February, based on

experience alone. Stakeholders need to come in with very clear weather prediction information that can inform when land preparation should be done in relation to other factors.

iv. Scientifically, sowing should be informed by the availability/prediction of rain. There is need to

create a link between when the sowing is done and the actual climatic conditions. Stakeholders

need to come in to provide this accurate information on both short and long term weather forecast

to inform when sowing should be done. Stakeholders can also explore on a possibility of

providing information service using various means to inform when sowing should be done

Under selling, an understanding of various marketing components by the respondents was established.

The following observations were made:

July 14, 2016

Page 4

i. While analyzing responses, it was observed that there seem to be a gap in market information

awareness. The respondents don‟t seem to understand the value of selling their maize through a

buying centre. Stakeholder need to explore the possibility of sharing market information on the

best option for the farmers. There is a perception that small scale farmers cannot take their

products to the NC&PB stores, this needs to be demystified

ii. From the findings, exploitation and interference by the middle men emerged as a major issue in

the selling of the maize. The following suggestions can work towards reducing the problem

a. Work with the farmers to create more storage facilities at the household level

b. Encourage more farmers to form and join peer farmer organizations where they can

access information on markets and trends. Through these groups, they will have a higher bargaining power and reduce the interference by the middlemen

c. Strengthen the existing farmer groups/SACCOs which can act as selling and buying point

for the various products iii. On fertilizer advice, the analysis, indicates that Agrics is a major stakeholder on fertilizer

advisory service provision amongst the respondents. However, this stake is at 53%. There is need

to strategize on how the remaining 47% of the farmers in the region can be reached to improve

Agrics impact in the study area.

iv. On weather forecast, the study established that there is no major information service provider on

both short and long term weather forecast according to the respondents. This is an area that can be explored on how the farmers can benefit from this service

On Agrics clients‟ satisfaction, an understanding of Agrics clients‟ perception on various products was

established the following observations were made:

i. Most of the respondents value the quality of farm inputs that Agrics is providing. This was their

main motivating factor for joining the program.

ii. The analysis also observed that the major reason why former clients left is because they did not

receive the farm inputs and packages on time as they expected

Issues for follow on research:

From the study, a pattern is emerging on areas then need further interrogation. This mainly revolves

around the soil; where by the following questions need to be investigated further:

i. Soil Testing: Who is doing it? What are the costs involved? How well/effective can this be

delivered?

ii. Can a link be created between soil testing and mobile technology? Ie can a specific farmer‟s land/soil related information be able to be shared via an online/mobile platform? Are the farmers

willing to adopt this?

iii. Soil conditions advice-what is the best/effective mode of delivering this advice? Is there an opportunity for customizing this advice?

iv. How are soil conditions linked to the mode/technology used in land preparation? Farmers are

already paying for land preparation services, how can this be linked to soil testing and soil

condition information? v. How can soil testing and information on soil conditions be linked to fertilizer advice?

July 14, 2016

Page 5

SECTION A: THE PROFILE OF THE RESPONDENTS

The study reached out to a total of 247 respondents as broken down in the table below. Amongst the

respondents, the average number of individuals per household is 6.03. The household with the highest membership in this study was 15 and the least with 1.

On land ownership, the respondent with the smallest potion of land is 0.2 acres while the highest one

had 7.0 acres. The average land size amongst the respondents is 1.6 acres across the six counties.

A total of 96 current Agrics clients were interviewed. The study also reached out to 153 non Agrics

clients. Out of the 153 non Agrics clients, 58 were former Agrics clients

A total of 95 respondents are not current or former Agrics Clients.

Of the 96 current Agrics clients, 56% had been with the organization for one season, 37% for 2 seasons and 7% for 3

seasons. None of the respondents had been around for 4 sessions

Agrics product taken by the respondents:

55% of the respondents have taken the core package alone from

the Agrics, most of whom are grain farmers.

10% have taken the poultry package, mainly due to limitation on their land size most of them

have less than 0.5 acres of land.

38% have taken the core package, and another product

245 out of the 247 (98%) interviewed grow maize in their farms.

72% grow beans, where in most cases the beans and maize is intercropped

Household Income:

52% of the maize producers get 20-26 % of their household income from maize as a crop

Amongst the beans producers, 83% get 0-25% of their household income Vegetable contributes 0-25% of the household

income amongst 83% of the respondents who

grow vegetable Other sources of income at the household level

include: livestock (including Poultry), casual

labor, and other crops that have not been

mentioned above

Respondents Desire/Wish:

A total of 67% of the respondents wish to be involved in

land production activities by tilting their land. Out of this 67%, 31% would wish to increase their food production, 27% to

increase cash crop production, and 9% to increase the size of

their land for production.

Note that only 1% indicated that they wish to invest in storage facilities.

County Men Women Average acreage per household Average size of the Household

1. Kakamega N 16 28 1.7 6.5

2. Kakamega E 17 24 1.5 5.3

3. Butere 21 25 1.5 6.5

4.Bungoma 15 24 1.5 6.2

5. Busia 19 24 1.6 5.5

6. Siaya 11 23 1.3 6

Total 99 148

Age group % Interviewed

<20; 0

20-29; 8.90%

30-39; 30.20%

40-49; 33.20%

50-59; 16.90%

>60 10.10%

Maize Beans Vegetable Sugarcane Others

0-25% 28% 83% 54% 32% 28%

26-50% 52% 16% 38% 50% 53%

51-75% 16% 1% 9% 11% 13%

More than

76%

3% 0% 0% 7% 7%

Desire/Wish Respondents

Buy land 9%

Increase food crops 31%

Increase cash crops 27%

Cows and/or related facilities 16%

Poultry and/or related facilities 14%

Storage 1%

Other 3%

July 14, 2016

Page 6

SECTION B: PRODUCTION

A total of 98% of the respondents interviewed grow maize in their farms, with an average of 48% of their

land cultivated by maize.

72% of the respondents grow beans, this covering an average of 19% of their land. In most cases, beans

are intercropped with maize.

23% of the respondents indicated that they produce vegetable, covering an average of 21% of their total

land space

16% of the respondents indicated that they cultivate bananas, covering and average of 22% of their land

11% of the respondents who grow sugar cane, it covers an average of 41% of their land. It is also worth noting that all the respondent who cultivate sugarcane have at least 1 acre piece of land

82% of the respondents have allocated an average of 30% of their total land for livestock (including poultry) and living area

Most of the respondents indicated that they grow maize primarily for food/subsistence. Vegetable and sugarcane is mainly grown for cash.

Fertilizer utilization:

90% of the respondents use chemical fertilizer as key farm input. The highest amount of fertilizer

utilized by one farmer is 250kg, and the least is 2kgs.

6.4% of the farmers indicated that they had procured less than 10Kgs of fertilizers this season.

Most of these farmers (98%) have less than one acre of land

47.5% of the respondents utilize between 12-25kgs this season, each farmer utilizing an average

of 23.1 kgs this season alone

33.8% of the respondents procured between 26-50kgs

11.9% procured between 75 to 250 Kgs of fertilizer this season

Fertilizer quantity and supplier

Fertilizer supplier Number of farmers Average quantity in Kgs

1.Agrovet, 63 34.5

2.Agrics, 85 43.3

3.One Ace 19 37.4

4.Govt 44 47.2

5.other 5 32.5

Total 216

The Fertilizer supplier and the reasons for choosing:

The supplier where Fertilizer is bought

Agrovet Agrics One Acre Fund Government Others

Reason

for

choosing

supplier

1.Price, 30 5 1 34 3

2.Ease, 14 4 3 6 2

3.Quality, 12 72 12 3 0

4.Reputation 4 4 3 0 0

From the above table, most of the respondents (48%) who buy fertilizer from the Agrovet, do so

because of the price.

July 14, 2016

Page 7

For Agrics and One Acre Fund, their choice as a fertilizer supplier is informed by the quality of

the product, where 85% and 63% of the respondents indicated this for Agrics and Once Acre

Fund respectively. 77% of the respondents indicated that they chose the government as their fertilizer supplier

because of the price.

Certified seed (hybrid)

89% of the respondents indicated that they used

certified seeds this season. The average utilization

of certified seeds per respondent was 7.4Kgs.

The average utilization of certified seeds per acres

amongst the respondents is 1.6kgs per acre

The major suppliers of the certified seeds

amongst the respondents are Agrics (37%) and

the Agrovet (31%). From the study, 11.7% of the current Agrics clients interviewed buy seeds

from the Agrovet

The graph above, most of the respondents indicated that quality and price informs their choice of

certified seeds supplier. Their choice of sourcing certified seeds from the Agrovet and the government

is to a large extent informed by the price. The respondents who source their seeds from Agrics and

One Acre Fund, their decision is informed by the quality of the certified seeds

0

10

20

30

40

50

60

70

Agrovet Agrics One Acre Fund

Government Others

The supplier where Certified seeds are bought

Reason for chosing supplier 1.Price,

Reason for chosing supplier 2.Ease,

Reason for chosing supplier 3.Quality,

Reason for chosing supplier 4.Reputation

31%

37%

9%

16%

7%

Certified seeds supplier for the respondents

Agrovet Agrics One Acre Fund Government Others

July 14, 2016

Page 8

Agronomic services

Traction/mechanization (land Preparation) A total of 59.4% indicated that they used traction/mechanization as an agronomic service this season.

75.7% of the farmers who used this service paid for it, either as part of the core package, or

separately from other service providers

(individuals with tractors or ox drawn plough)

An average of Ksh 1,529.8 was paid for this

service per acre amongst the respondents who

paid cash money for this service

Most of the respondents (71%) indicated that

they get traction/mechanization services from other service providers.

On probing further on level of satisfaction for

the “other” land preparation service provider, it was established that 59% of the respondents are not satisfied by the kind of service that they are getting as

indicated in the figure below

Foll

The extension ad training courses are currently being offered by Agrics and other partners and most

of the respondents indicated that they are satisfied by this services.

Some respondents indicated that they pay ksh 200 for the trainings and extension services provided

by Agrics and One Acre Fund

5%

54%

31%

10%

Level of satisfaction on Traction/mechanization service provision by others

Very unsatisfied Unsatisfied Satisfied Very Satisfied

Agrics10%

One Acre Fund4%

Government

15%Others

71%

Traction/Mechanization (Land preparation) service providers

This is an area that stakeholders and other service providers can explore further on the possibility

of providing this service. Note that the respondents are ready to pay for it, and they are not

satisfied by the current service providers

Follow on studies need to focus on various technologies for adoption in land preparation

July 14, 2016

Page 9

Soil testing:

9.2% of the respondents indicated that they use soil testing as an agronomic service. 78.2% of the

respondents who used soil testing are from Busia County. 73.9% of the respondents who used the

soil testing agronomic service got it from Agrics and most of them indicated that they are satisfied by the service

No substantial reason was given for using this service

This service was also offered for free amongst the respondents

Land Preparation:

A summary on how the respondents prepare their land is provided in the table below:

How do the farmer know when to prepare land

Experience Community Extension services Training course Information service Others

when land

is

prepared

in

November 3 1 0 0 0 0

December 24 3 9 10 4 0

January 61 12 20 11 0 0

February 33 5 9 3 6 9

March 8 0 1 1 0 0

April 3 0 0 0 0 0

Total 132 21 39 25 10 9

This can be analyzed as in the graph below:

From the graph above, most of the respondents tilt their land in January (104), followed by

February (65) and December (50)

0

10

20

30

40

50

60

70

Experience Community Extension services

Training cource

Information service

Others

How do the farmer know when to prepare land

when land is prepared in November

when land is prepared in December

when land is prepared in January

when land is prepared in February

when land is prepared in March

when land is prepared in April

There seem to be a gap here: the respondents seem not to understand the soil testing concept as an

agronomic service. They don’t seem to see soil testing as an agronomic service, this is because they

could not give good reasons why they are using the service. This is a gap that stakeholders can come

in to fill in the information gap, and provide the soil testing service

July 14, 2016

Page 10

For most of the respondents, the decision on when to do land preparation is informed by

experience. Extension service and training comes in 2nd

and 3rd

in informing the decision on when

to prepare the land.

SOWING:

From the feedback that we got, 98% of the respondents sow their land in the months of March

and April this year.

The table below gives a summary on when the respondents indicated that they sow their land

compared to last year

Difference with last year

Same Early Late

Month when sowing

was done

March 103 26 33

April 4 8 35

From the table above, most of the respondents did the sowing of their farms in March, the same

period as last year

A significant number of respondents who sow in April indicated that this was late, thus, they were

meant to sow in March

A further analysis as to why most of the respondents indicated that they sow in march is given in

the graph below:

If the difference this year is:

Same Early Late

What informs the Farmers

decision on Sowing

Experience 48 9 12

Community 19 3 4

Extension services 23 4 8

Training course 12 10 2

Information Service 0 0 0

Other 1 0 7

From the table and graph above, you will notice that majority of the respondents are influenced

by experience while making the decision on when to sow their land.

0 10 20 30 40 50

Experience

Community

Extension services

Training course

Information Service

Other

Wh

at in

form

s th

e af

rmer

s d

ecis

ion

o

n S

ow

ing

If the differece this year is Late

If the differece this year is Early

If the differece this year is Same

From the above, there doesn’t seem to be a clear relation between climatic conditions/the weather

and when land is preparation. Majority of the farmers prepare their land in February, based on

experience alone. Stakeholders can come in with very clear weather prediction information that can inform when land preparation should be done in relation to other factors. This can be

provided inform of information

July 14, 2016

Page 11

This experience might not be based on any scientific data or understanding of whether patterns,

hence the farmers might be exposed to risks, considering the changes in climatic conditions-thus

relying on experience might not be accurate

It is worth noting that none of the farmers was influenced by information services in deciding

when to sow their land

Scientifically, sowing should be informed by the availability/prediction of rain. There is need

to create a link between when the sowing is done and the actual climatic conditions.

Stakeholders can come in to provide this accurate information on both short and long term

weather forecast to inform when sowing should be done. Stakeholders can also explore on a

possibility of providing information service using various means to inform when sowing

should be done

July 14, 2016

Page 12

SECTION C: SELLING

Out of all the 249 respondents who participated in this study, 209 are involved in maize production. 10%

of this number does not sell their maize. This 10% indicated that they produce

maize purely for subsistence purposes.

From the chat above, most of the respondents , 47%, indicated

that they sell their maize

between the 17-30th

week after harvest. The reason given for

this is cash need and price. You

will notice that this coincides with the time when the farmers

are preparing their land, and

procuring farm inputs for the

next season

Most of the respondents who

sell their maize within four weeks of harvest indicated that they do this because of need for cash and price. It is also worth

noting that most respondents sell their maize within four weeks but in tranches

Respondents who sell their maize between 5-16 weeks indicated that they do this for the cash need and price

From the respondents, less than 2% indicated that they sell their maize due to lower post-harvest

loss.

.

The respondents indicated that in

general their potential means of selling their surplus yield is as indicated in the

graph below:

The local market was identified to

be the most preferred option. This can be attributed to accessibility and ease of

access

Note that none of the respondents

indicated that they will have the online platform as a potential means of selling their yield

Regarding the options for selling their surplus yield (for maize) respondents ……. In the graph below:

18%

35%

47%

Period in weeks before selling maize

0-4 Weeks 5-16 Weeks 17-30 Weeks

0

20

40

60

80

100

120

Local market Buying center

Farm gate Online Not selling

where farmers expect to sell surplus yield

Option 1

Option 2

This implies that there is a gap

amongst the respondents when it

comes to understanding the market

systems

July 14, 2016

Page 13

A total of 50% of the respondents identified the local market as their preferred option for selling their

surplus produce

Selling at the farm gate was the most preferred second option for selling their surplus

As a second option, more respondents prefer not to sell

their surplus maize, than take it

to the local market and the

buying centre

The response patterns on the selection of the options for selling maize are the same for selling the bean.

Options for selling vegetable are slightly different where the majority of the respondents identified local

market as their option one and two.

0 50 100 150

Local market

Buying center

Buyers buying at farm gate

Online platform

Other: …..

Po

ten

tial

mea

ns

of

selin

g

surp

lus

yiel

d

Number of respondents

While analyzing at these responses, there seem to be a gap in market information awareness. The

respondents don’t seem to understand the value of selling their maize through a buying centre.

Geodetics can explore the possibility of sharing market information on the best option for the farmers.

There is a perception that small scale farmers cannot take their products to the NC&PB stores, this

need to be demystified

July 14, 2016

Page 14

PRICE:

The respondents shared their expected price per kilo of maize and beans as indicated in the chat below:

Price expectation for a big percentage of the respondents, for maize and beans, fall within the market

rate for these goods per kilo. This is an indication that most of the respondents are well informed about the current market rates for the goods that they are producing. This study queried further about

the sources of price information, and the results are indicated in the chat below:

Most of the respondents indicated the word of mouth and other buyers was their main sources of the expected market price.

The respondents who use the word of mouth, indicated that

they use it daily, and they find it to

be accurate and useful

Majority of the

respondents who use other buyers

as a source, indicated that they access this information both daily

and weekly. They find this source

to be accurate. A big percentage also indicated that this is a useful

source of the expected selling price

information. The table below

summaries this.

Frequency Accuracy Usefulness of the source

Word of Mouth Monthly 7 Very accurate 6 Very Useful 19

Weekly 67 Accurate 136 Useful 117

Daily 143 Not Accurate 34 Not so useful 34

Very Inaccurate 6 Very Unuseful 9

(Other) Buyer Monthly 16 Very accurate 1 Very Useful 7

Weekly 43 Accurate 75 Useful 68

Daily 63 Not Accurate 39 Not so useful 38

Very Inaccurate 5 Very Unuseful 7

The respondents were asked to rank their major marketing challenges that they experience in their areas. The findings are as indicated in the chat below:

0 20 40 60 80 100 120 140

15-40

45-70

75-100

120-160

Above 160

Don’t KnowEx

pec

ted

Pri

ce P

er K

g in

Ksh

Beans

Maize

4% 2%

18%

46%

30%

0%

Expected price information sources

News paper TV Radio

Word of Mouth (Other) Buyers Internet/App

July 14, 2016

Page 15

Most of the respondents indicated that middle men interference is the major marketing challenge that

they experience. This is in line with selling options that the farmers have, of selling at the local market and at the farm gate.

The interference by the middle men might have contributed to low

market price of crops, which the

respondents identified as the second

challenge in marketing their products

The study established that 48% of the respondents do not have grain storage

facilities. The lack of storage facilities can

press the farmer to sell their grain a few weeks after harvest since they fear the

post harvest loss due to lack of good

storage facilities. At this point, the market is usually flooded with maize, and the middlemen take

advantage and buy maize in bulk to sell to the millers

On farmer group or SACCO membership, only 38% of the respondents belong these groups. It was

established that only 4% of the respondents sell their produce through the organized farmer groups. This exposes them to exploitation by the middlemen

Regarding the selling price information, more than 70% of the respondents indicated that the reliability of the information and the frequency of updates need to be improved, while providing the

selling price information

12%

5%

45%

38%

0%

Marketing Challenges Experienced

Lack of transport to the market

Lack of road

Middle men interference

Low market price of crops

Lack of appropriate place in the market

From the above findings, exploitation and interference by the middle men is emerging as a major

issue in the selling of the maize. The following suggestions can work towards reducing the problem

i. Work with the farmers to create more storage facilities at the household level

ii. Encourage more farmers to form and join peer farmer organizations where they can

access information on markets and trends. Through these groups, they will have a

higher bargaining power and reduce the interference by the middlemen iii. Strengthen the existing farmer groups/SACCOs which can act as selling and buying

point for the various products

July 14, 2016

Page 16

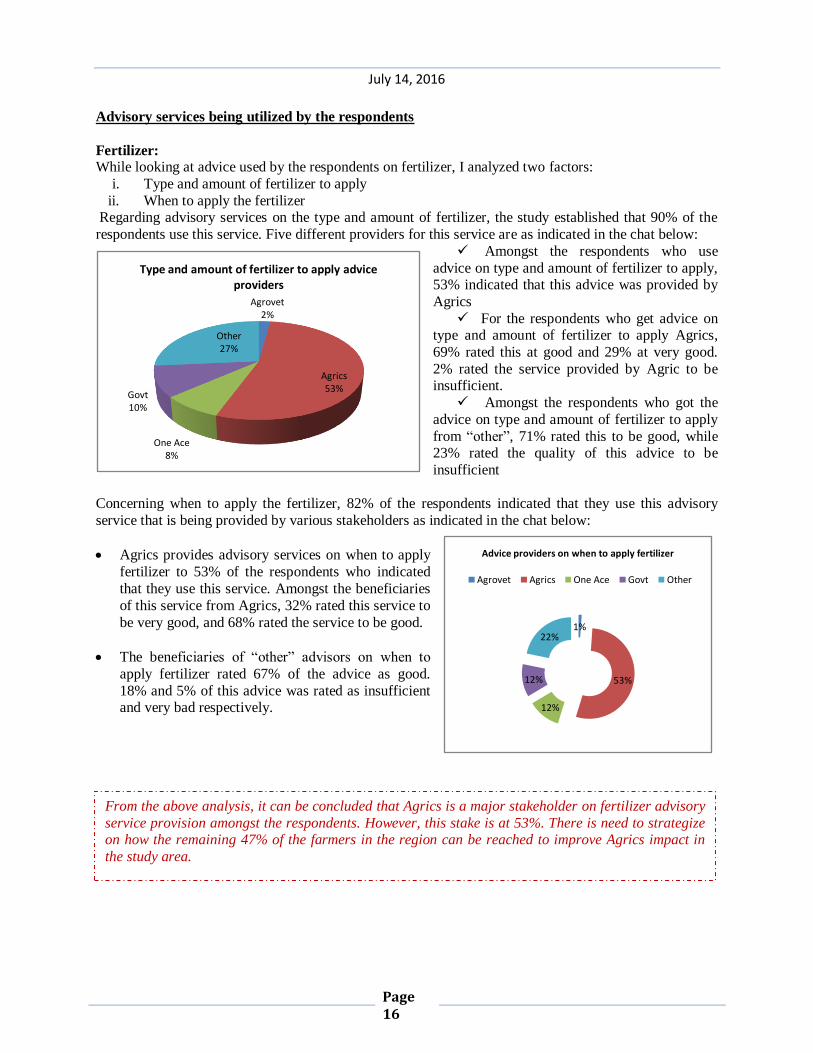

Advisory services being utilized by the respondents

Fertilizer: While looking at advice used by the respondents on fertilizer, I analyzed two factors:

i. Type and amount of fertilizer to apply

ii. When to apply the fertilizer Regarding advisory services on the type and amount of fertilizer, the study established that 90% of the

respondents use this service. Five different providers for this service are as indicated in the chat below:

Amongst the respondents who use

advice on type and amount of fertilizer to apply, 53% indicated that this advice was provided by

Agrics

For the respondents who get advice on type and amount of fertilizer to apply Agrics,

69% rated this at good and 29% at very good.

2% rated the service provided by Agric to be insufficient.

Amongst the respondents who got the

advice on type and amount of fertilizer to apply

from “other”, 71% rated this to be good, while 23% rated the quality of this advice to be

insufficient

Concerning when to apply the fertilizer, 82% of the respondents indicated that they use this advisory

service that is being provided by various stakeholders as indicated in the chat below:

Agrics provides advisory services on when to apply

fertilizer to 53% of the respondents who indicated

that they use this service. Amongst the beneficiaries

of this service from Agrics, 32% rated this service to

be very good, and 68% rated the service to be good.

The beneficiaries of “other” advisors on when to

apply fertilizer rated 67% of the advice as good.

18% and 5% of this advice was rated as insufficient and very bad respectively.

Agrovet2%

Agrics53%

One Ace8%

Govt10%

Other27%

Type and amount of fertilizer to apply advice providers

1%

53%

12%

12%

22%

Advice providers on when to apply fertilizer

Agrovet Agrics One Ace Govt Other

From the above analysis, it can be concluded that Agrics is a major stakeholder on fertilizer advisory

service provision amongst the respondents. However, this stake is at 53%. There is need to strategize on how the remaining 47% of the farmers in the region can be reached to improve Agrics impact in

the study area.

July 14, 2016

Page 17

Soil conditions

From all the respondents involved in this study (249), 28% indicated that they use this service. Among the

28% who use this service, 57% are from Busia county and 27% from Kakamega North. Advisory

service providers on soil conditions are provided in

the chat below:

Most of the clients from Busia who use advisory

service on soil conditions are not current Agrics

clients. Some of them are former Agrics clients

Amongst the respondents who got advisory service

on soil conditions from Agrics, 74% gives Agrics a rating of good, while 26% gives them a rating of

very good.

From the study, 79% of respondents who got this service, on soil conditions, from “other” service

providers, rated the advice as good.

Weather forecast

The respondents were asked if they use advisory service or information on both short and long term weather forecast. 27% of all the 249 respondents indicated that they use the short term weather forecast

advisory service. 26% indicated that they use long term weather forecast advisory service. A breakdown

on advisory services on long and short term weather forecast is provided in the chats below:

From the above chats, most of the respondents get information on weather from “other” sources not

included in the choices provided by this study. These include: Radio, Friends and relatives, amongst others.

55%

4%

7%

34%

Soil conditions advisory service providers

Agrics

One Ace

Govt

Other

The following needs to be taken into consideration:

There is need to interrogate further the advice that Agrics currently provide to farmers on soil conditions Need to map out other service providers on soil conditions to share lessons and experience

21%5%

3%71%

Information Provider on Short terms weather Forecast

Agrics One Acre Fund Government Others

21%5%

10%64%

Information Provider on long term weather forecast

Agrics One Acre Fund Government Others

July 14, 2016

Page 18

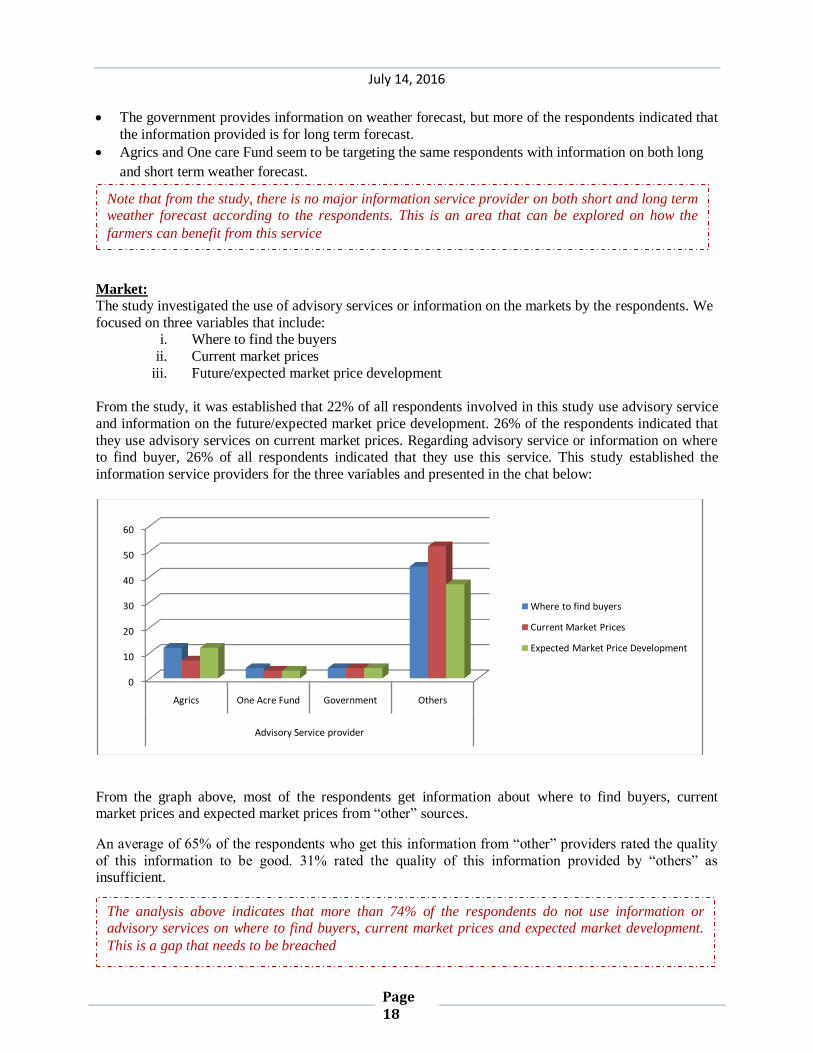

The government provides information on weather forecast, but more of the respondents indicated that

the information provided is for long term forecast.

Agrics and One care Fund seem to be targeting the same respondents with information on both long

and short term weather forecast.

Market:

The study investigated the use of advisory services or information on the markets by the respondents. We

focused on three variables that include: i. Where to find the buyers

ii. Current market prices

iii. Future/expected market price development

From the study, it was established that 22% of all respondents involved in this study use advisory service

and information on the future/expected market price development. 26% of the respondents indicated that

they use advisory services on current market prices. Regarding advisory service or information on where to find buyer, 26% of all respondents indicated that they use this service. This study established the

information service providers for the three variables and presented in the chat below:

From the graph above, most of the respondents get information about where to find buyers, current market prices and expected market prices from “other” sources.

An average of 65% of the respondents who get this information from “other” providers rated the quality

of this information to be good. 31% rated the quality of this information provided by “others” as insufficient.

0

10

20

30

40

50

60

Agrics One Acre Fund Government Others

Advisory Service provider

Where to find buyers

Current Market Prices

Expected Market Price Development

Note that from the study, there is no major information service provider on both short and long term weather forecast according to the respondents. This is an area that can be explored on how the

farmers can benefit from this service

The analysis above indicates that more than 74% of the respondents do not use information or advisory services on where to find buyers, current market prices and expected market development.

This is a gap that needs to be breached

July 14, 2016

Page 19

Information that the respondents would like to have: All the respondents were asked on the information that they would like to have, but don‟t have access to it

now, or they are not using it at the moment. All the 18 items on the questionnaire were availed to the

respondents and they were requested to select what they would like to have, rank by importance and suggest how much they are willing to pay for the service.

The table below gives a summary of responses and how the ranking was done by importance.

Information that respondent

would like to have, but are not

using it at the moment

Number of

respondents who

would like to use

it

Number of

respondents who

ranked 1st

Number of

respondents who

ranked 2nd

Number of

respondents who

ranked 3rd

Soil Conditions 130 98 15 4

Plant diseases/health (Pest

control)

76 29 24 8

Seed varieties 73 38 18 9

Short term weather forecast 73 21 16 12

Long term weather forecast 74 17 15 12

Animal disease/health (Pest

control)

72 16 16 16

From the list of 18 information items, respondents selected what they would or would not like to have. For all items that at least 28% of the respondents indicated that they would like to use, a further analysis

was done to establish how they ranked the items by importance.

From this analysis, soil conditions was ranked first as information that the respondents would like to have

bur don‟t have access at the moment.

The table above lists the order in which the six information services was ranked by the respondents

involved in this study

Amount of money that the respondents are willing to pay for information: For the six items that were ranked top as earlier explained, the study sought to establish how much the

respondents are willing to pay.

This was established by analyzing the amount that had been indicated by the respondents who ranked the

information service as their first by importance.

In this analysis, I looked at the highest and lowest amount in Kenyan shillings that had been suggested by the respondents. I also got the average of the amount that all the respondents who ranked the information

service first for each of the top six categories of information as identified by the respondents. This is

summarized in the table below Highest amount in Ksh

that is willing to pay for

the service

Lowest amount in Ksh

that is willing to pay

for the service

Average for respondents

who ranked this as 1st are

willing to pay

Soil Conditions 3,000 0 345

Plant diseases/health (Pest control) 1,000 0 218

Seed varieties 500 0 140

Short term weather forecast 300 0 133

July 14, 2016

Page 20

Long term weather forecast 300 100 123

Animal disease/health (Pest control) 500 50 120

From the above table, under soil conditions, we realize that the average amount for respondents who

ranked 1st are willing to pay is Ksh 345, although the highest respondent is willing to pay ksh 3,000.

Having and understanding of these, can help in determining the price at which this service can be offered.

What the farmer would do if the main crop fails:

The respondents were asked to share on what they would do if their main crop failed. Their responses are

provided in the chat below:

From the above graph, only 26% of the respondents indicated that they will claim from insurance if their

main crop fails. This group consists of the current Agrics and non Agrics clients.

2%

9%

31%

9%

15%

26%

7%

Action to be done when main crop fail

Not repay input credit

Take a loan

Reduce cost of living (spend less on food, phone, etc)

Turn to family for money

Use saved money

Claim from insurance

Other

Act

ion

to

be

do

ne

wh

en m

ain

cro

p f

ail

Action to be taken when main crop fails

Data information and findings on information that the respondents would like to use and what they are willing to pay for needs to be interrogated further to inform future service provision or business

opportunities in this sector by various players.

On crop insurance, the study indicates that only 26% have insured their crops. There is still a huge

market for crop insurance across the six counties. Various stakeholders involved in crop insurance

need to interrogate this opportunity further.

July 14, 2016

Page 21

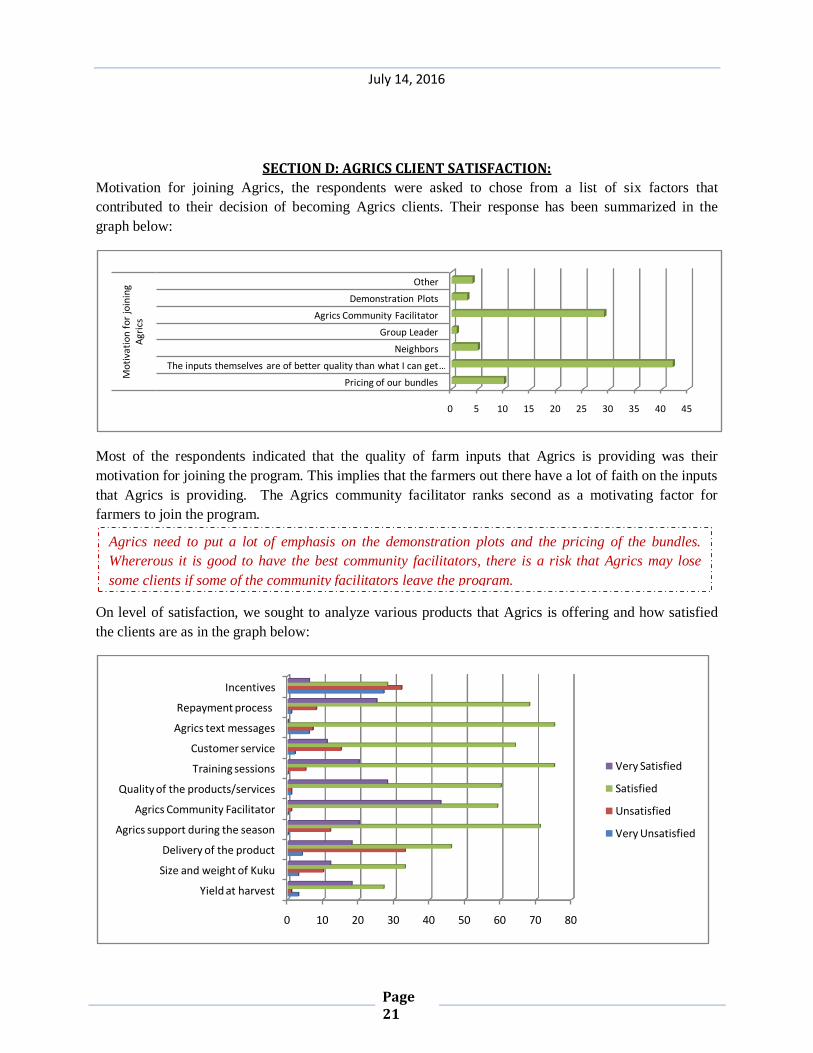

SECTION D: AGRICS CLIENT SATISFACTION:

Motivation for joining Agrics, the respondents were asked to chose from a list of six factors that

contributed to their decision of becoming Agrics clients. Their response has been summarized in the

graph below:

Most of the respondents indicated that the quality of farm inputs that Agrics is providing was their

motivation for joining the program. This implies that the farmers out there have a lot of faith on the inputs

that Agrics is providing. The Agrics community facilitator ranks second as a motivating factor for

farmers to join the program.

On level of satisfaction, we sought to analyze various products that Agrics is offering and how satisfied

the clients are as in the graph below:

0 5 10 15 20 25 30 35 40 45

Pricing of our bundles

The inputs themselves are of better quality than what I can get …

Neighbors

Group Leader

Agrics Community Facilitator

Demonstration Plots

Other

Mo

tiva

tio

n f

or

join

ing

Agr

ics

0 10 20 30 40 50 60 70 80

Yield at harvest

Size and weight of Kuku

Delivery of the product

Agrics support during the season

Agrics Community Facilitator

Quality of the products/services

Training sessions

Customer service

Agrics text messages

Repayment process

Incentives

Very Satisfied

Satisfied

Unsatisfied

Very Unsatisfied

Agrics need to put a lot of emphasis on the demonstration plots and the pricing of the bundles.

Whererous it is good to have the best community facilitators, there is a risk that Agrics may lose

some clients if some of the community facilitators leave the program.

July 14, 2016

Page 22

Most of the clients indicated that they are satisfied by Agrics products. The text messages, training

sessions and Agrics support during the season were the best offered services according to the respondents.

Incentives and the delivery of the product (trimming, process) had the highest number of respondents who indicated that they were unsatisfied.

Respondents were asked to give their opinion on their credit in relation to their yield as a result of interventions by Agrics. 43% believe that this is a good value worth about what they paid for. 32% think

that it is a poor value, worth less than what they paid for, while 25% believe that this is an exceptional

value, worth more than what they paid for.

On interaction with Agrics staff, respondents were asked how often they interact with Agrics‟ staff in the

field. 95% indicated that they interact on weekly basis, 4% on monthly, and 1% on daily basis.

On customer care, 16% of the respondents indicated that they had contacted the customer service.

Amongst the 84% that had not contacted customer service, 83% indicated that they are aware of the

customer service number.

From the 16% that had contacted the customer care, 75% indicated that their problems had been resolved

to complete satisfaction by the company or its representatives. 25% indicated that their problem was not

resolved.

From the study, 95% of the respondents indicated that they receive text messages from Agrics. Amongst

the text message recipients, 99% indicated that they find information from the text messages to be valuable.

Respondents were asked if they buy farm inputs on credit from other organizations. 46% of the respondents to this question indicated that they buy from other organizations on credit. Compared to

Agrics, 67% of the respondents who bought inputs from other organizations indicated that inputs from

Agrics were batter. 7% said that they were worse and 27% said that they are the same. Most of the

respondents mentioned quality a key factor that makes the Agrics products to be better than the rest.

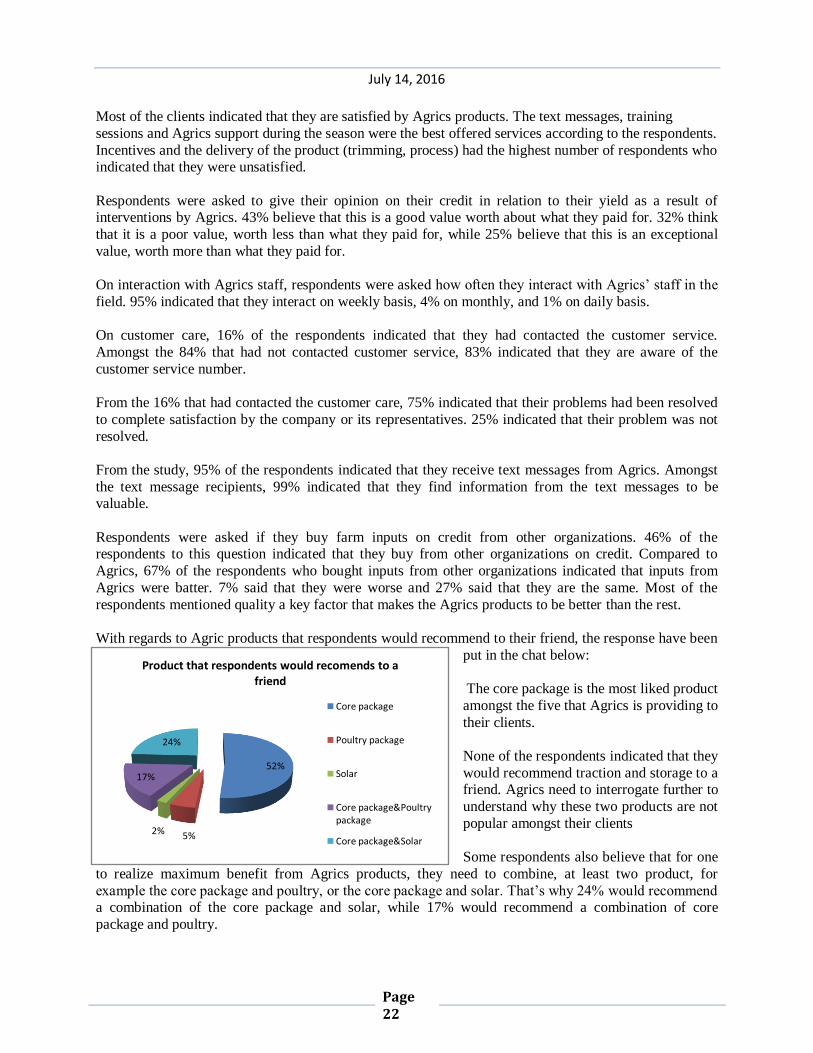

With regards to Agric products that respondents would recommend to their friend, the response have been

put in the chat below:

The core package is the most liked product

amongst the five that Agrics is providing to

their clients.

None of the respondents indicated that they

would recommend traction and storage to a friend. Agrics need to interrogate further to

understand why these two products are not

popular amongst their clients

Some respondents also believe that for one

to realize maximum benefit from Agrics products, they need to combine, at least two product, for

example the core package and poultry, or the core package and solar. That‟s why 24% would recommend a combination of the core package and solar, while 17% would recommend a combination of core

package and poultry.

52%

5%2%

17%

24%

Product that respondents would recomends to a friend

Core package

Poultry package

Solar

Core package&Poultry package

Core package&Solar

July 14, 2016

Page 23

Opinion of former Agrics Clients:

The study sought the opinion of the former Agrics clients to establish how they have progressed after parting ways with interventions that Agrics is currently implementing in the region.

We sought to establish why they exited from the program. The findings are summarized in the chat below:

From the chat above, you realize that the major reason why the clients left is because they did not receive

the farm inputs and packages on time as they expected.

Amongst the respondents, 19% had other reasons for exiting the program. This include: “I was new but

due to my delay of payment I was harassed” say Mebo from Butere; „I had more problems concerning

money‟; „I had my personal challenges/problems‟; „I was away during recruitment and had inadequate

land‟; „I had personal challenges will come back next year‟ amongst other reasons.

In comparison with other organizations, the former clients rated Agrics services as follows:

11%

6%

32%

7%4%

8%

13%

19%

Reasons for Exiting Agrics Program

I am happier on my own

I am better served by another organization

I did not receive inputs and packages on time

Your services and products were not at the standard I expected

I was unable to repay my debt

I thought it was too expensive

I had expected more yield increase

0 5 10 15 20 25 30 35 40

Yield at harvest

Delivery of the product (timing, process)

Agrics Community Facilitator

Training sessions

Agrics text messages

Incentives

Agr

ic p

rod

uct

Comparison of Agrics products with other programs by former clients

Very Satisfied

Satisfied

Usatisfied

Very Usatisfied