Embed Size (px)

Citation preview

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 1/39

SYED ZEESHAN HASSAN

060515

INTERNSHIP REPORT

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 2/39

BBA 08

ACKNOWLEDGEMENT

First of all thanks to Almighty Allah, who gave me the strength and courage to complete this

task, I am thankful to my parents for their prayers, their financial and moral support.

I am thankful to all my friends for their help and support. And at most I am grateful to the whole

crew of Askari Bank, who has been a source of learning and cooperation for me.

I have tried my level best to make this work thoughtful and precise, but it may have mistakes, I

will be more than pleased to have feedback, and suggestions to help me improve my work for my

future projects.

2

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 3/39

TABLE OF CONTENTS:

Executive summary Page

4

Introduction Page

5

1.1. History of Askari

Commercial Bank Ltd.

Page

6

1.2. Objectives of ACBL Page

8

1.3. Organizational Structure Page

10

1.4. Products and Services Page

13

2. Learning and experience Page

20

2.1. Rationale for selection Page

20

2.2. SWOT of ACBL Page

32

2.3. Recommendations Page

36

2.4. Conclusion Page

38

References Page

40

3

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 4/39

EXECUTIVE SUMMARY:

This is an explanatory report about my internship that I completed at Askari Bank from

13th July, 2009 to 22nd August; 2009.Askari Bank is one of the rapidly expanding banks of

Pakistan which has stretched over 200 branches all over the Pakistan. Along with my personal

account in Askari Bank, perhaps its dynamic progress was one of the main reasons of my joining

to this bank for my internship.

This report holds information about different departments of Askari bank. The purpose of this

report is to document the experience and learning which I gained during my internship. Although

I was not considered as a regular employee of the bank to whom bank may award a major

responsibility of banking but even then during my internship I was able to learn practical aspects

of the bank, and got a bird’s eye view of the banking activities in the departments I was assigned

to. I was placed in six departments from where I learned so many things.

During this whole process I gained information about Askari Bank which previously I did not

have any knowledge of i.e. the history of the bank, products and services it offers, the prevailing

departments of the bank and their functions and how the bank’s day to day activities are

conducted.

To conclude I may say that Askari Bank has aggressive growth plans in Pakistan. It has

developed a good reputation for good service and a quality bank. It offers a broad range of

products to target different market segments.

4

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 5/39

INTRODUCTION

According to Dr. Hart

“Banker or bank is a person or company carrying on business of receiving money and

collecting drafts for the customers subject to the obligation of honoring cheques drawn upon

them from time to time by customers to the extends of the amounts available on their currents

accounts”.

In the words of G W Gilbert

“A banker is a dealer in capital or more properly a dealer in money. He is an intermediate

party between the borrower and lender. He borrows one party and lends to the another”

According to Banking companies ordinance 1984

“Banking means the accepting, for the purpose of lending, or investment, of deposits of

money from the public, repayable on demand or otherwise, and withdraw able by cheque,draft, order or otherwise.”

“Banking companies mean companies which transact the business of banking in Pakistan.”

Commercial Bank:

“The commercial bank receives surplus money from the public and lend to others who needs

funds. Bank collects cheque, bills of exchange etc from customers. It transfers money from

one place to another. It provides agency and general utility services. Purpose of commercial bank is to earn profit.”

5

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 6/39

1.1. HISTORY OF ASKARI COMMERCIAL BANK

The banking sector has witnessed a dramatic change during the last ten years with the

development of Askari Bank, which is not only redefining priorities and focus of the banks,

but also threatening the domination of traditional players. The story begins with the

incorporation of Askari Commercial Bank limited in Pakistan on October 09, 1991, Askari

Bank Commenced (begin) to operations in April 1992, as a public limited company. The

bank is listed on the Karachi, Lahore and Islamabad Stock Exchanges and the initial public

offering was over subscribed by 16 times.

While capturing the target market share amongst the view banks, Askari has provided good

value to its shareholders. Its share price has remained approximately 12% higher than the

average share price of quoted banks during the last four years.

Askari Bank has expanded into a nation wide presence of 153 Branches, and an Offshore

Banking Unit in Bahrain. A shared network of over 800 online ATMs covering all major

cities in Pakistan supports the delivery channels for customer service. As on December 31,

2008, the Bank had equity of Rs. 11.016 billion and total assets of Rs. 207.168 billion, with

over 475,000 banking customers, serviced by a total staff of 2,118.

Askari Bank is the only bank with its operational head office in the twin cities of Rawalpindi-

Islamabad, which have relatively limited opportunities as compared to Karachi and Lahore.

This created its own challenges and opportunities, and forced as to evolve an outward-

looking strategy in terms of Askari market emphasis. As a result, Askari developed a

geographically diversified assets base instead of a concentration and heavy reliance on

6

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 7/39

business in the major commercial centers of Karachi and Lahore, where most other banks

have their operational Head offices.

Historically, Askari’s core marketing focus for its asset base has been the middle and upper

middle business houses (including wholesalers and manufacturers) operating in the large

urban centers of Pakistan, which are primarily oriented towards foreign trade. This segment

constitutes significant revenues to the bank. The liability side remains focused on the middle

and upper middle class retired and serving government and armed forces personal and mid-

size business houses.

Their corporate banking division was established in April 1999 with the primary focus on

servicing large corporate and multi-national companies (MNCs). Benefiting from the bank’s

growing balance sheet size, this division B now gaining momentum and their long-term aim

D to develop it into an independent.

Strategic business unit (SBU)… This would the bank to acquire, develop and specialized

abilities, and enhance their focus on serving the emerging needs of the corporate clients.

With this branch network of over 100 and further expected increase in future, the ATM’s

facility and internet Banking, Askari Bank’s reach is ever increasing. In recognition of this

reach, they have set up a retail-banking group in July 2000, the mobile ATM’s facility is first

time started by Askari commercial bank in 2005 dedicated to serving the urban consumer

market; Askari is committed to aggressively market this segment. The strategy is to provide

their customers with a basket of innovative products to meet their varying needs.

Askari Commercial Bank is the only Private Sector bank that has been approved by the

World Bank as a Participating Financial Institution for the US$ 200 million Line of Credit

sanctioned (authorized) to the Government of Pakistan for the Financial Sector Deepening

and Intermediation Project.

Askari's emphasis on further broadening its core foreign trade business translated into

handling a higher volume of Export and Import business of Rs. 36 billion registering a

growth of 42% over the pervious year. This enhanced foreign trade business was secured due

7

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 8/39

to excellent customer services and efficient international settlement arrangements with our

correspondent banks.

Askari Bank is operating throughout Pakistan. Most of the branches are connected through

our State of the Art, On-line Communications Network, which gives the bank a competitive

edge in providing instant services to its clientele. We also offer direct access to the latest

Foreign Exchange Rates through our Online Communications.

Mission:

To be the leading private sector bank in Pakistan, with an international presence,

delivering quality services through innovative technology and effective resource

management, in a modern and progressive organization culture of meritocracy, maintain

high ethical and professional standards, with providing enhance value to all our

stakeholders, and contributing to society.

Vision:

To be the leading bank in Pakistan.

Core values:

The intrinsic values, which are corner stones of Askari corporate behavior, are:

• Commitment

• Integrity

• Fairness

• Team-work

• Service

Objectives of ACBL:

As Askari Bank looks ahead to the future by moving through the decade its efforts are

guided by a broad framework of corporate objectives, which are as follows:.

8

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 9/39

• It will endure to provide its customers with as many creative financial services and

products, as is required. As today customer demands a package of services suited to

this particular business, Askari plans to develop different and new products to cater to

the customer's demand. Askari bank has they strength to be a market leader.

• Bank will keep standing and by and develop, its human capital base. It is planning to

provide all the required training to its staff towards achieving a higher level of

professionalism. Askari will continue striving to build a strong, motivated and

dedicated work force where total commitment will be towards customer's satisfaction

and wealthy growth of organization.

• Askari bank will endure to provide a competitive return to its shareholders and will

strive to maximize its share value. The enhancement in its capital and returns will be

a continuous process. Askari bank is interested in being one of the most financially

viable institutions. So it lays great emphasis on gradual building up to a healthy

deposit mix. In the years ahead, the bank will enhance its focus on growth through

operational efficiency, creating strategic alliances developing well-structured

networking system innovating new products, enhancing marketing and sales efforts

improving customer service, achieving greater employee motivation and providing

the best value to its stakeholders - will make it a leader in the corporate world.

How to deliver:

These objectives and guiding mission will be achieved through

• Focused objective

• Winning as a team

• Excellence in delivery

• Relentless quality

• Upward rising sales

9

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 10/39

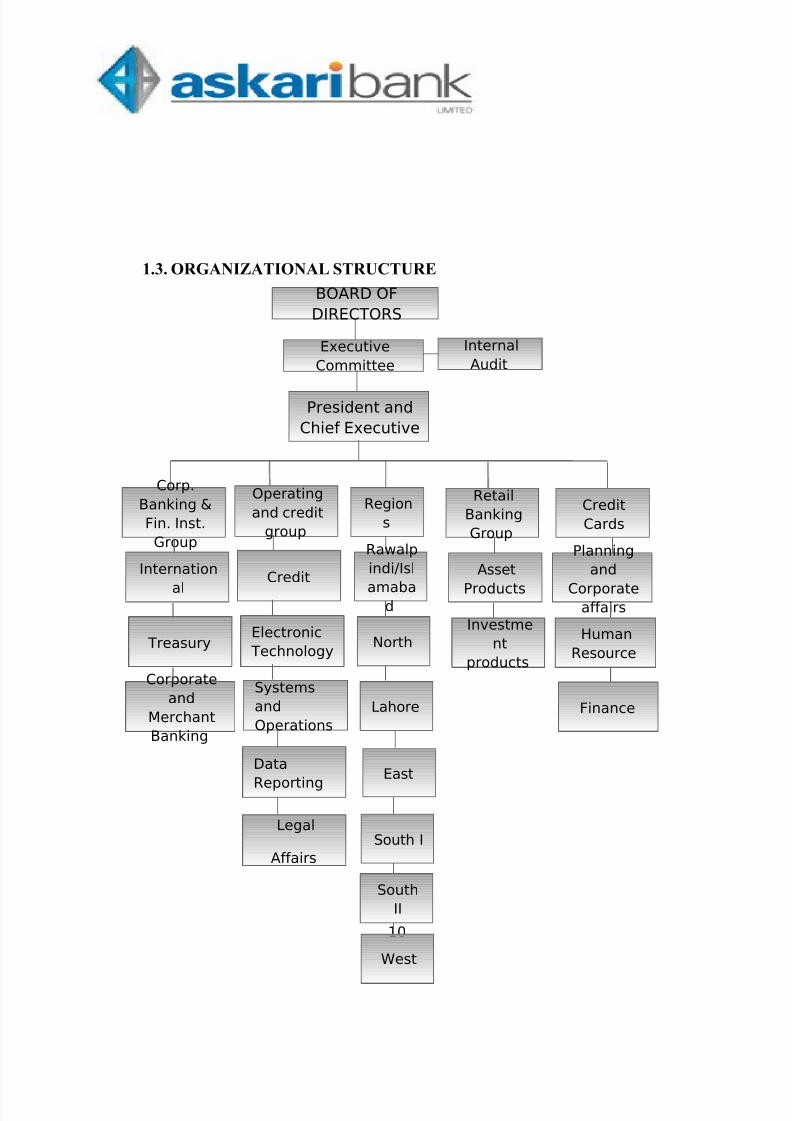

1.3. ORGANIZATIONAL STRUCTURE

10

BOARD OF

DIRECTORS

Executive

Committee

President and

Chief Executive

Internal

Audit

Corp.

Banking &

Fin. Inst.

Group

Operating

and credit

group

Region

s

Retail

Banking

Group

Credit

Cards

Internation

al

Credit

Rawalp

indi/Isl

amabad

Asset

Products

Planning

and

Corporateaffairs

TreasuryElectronic

TechnologyNorth

Investme

nt

products

Human

Resource

Corporate

and

Merchant

Banking

Systems

and

Operations

Lahore Finance

Data

Reporting

East

Legal

Affairs

South I

South

II

West

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 11/39

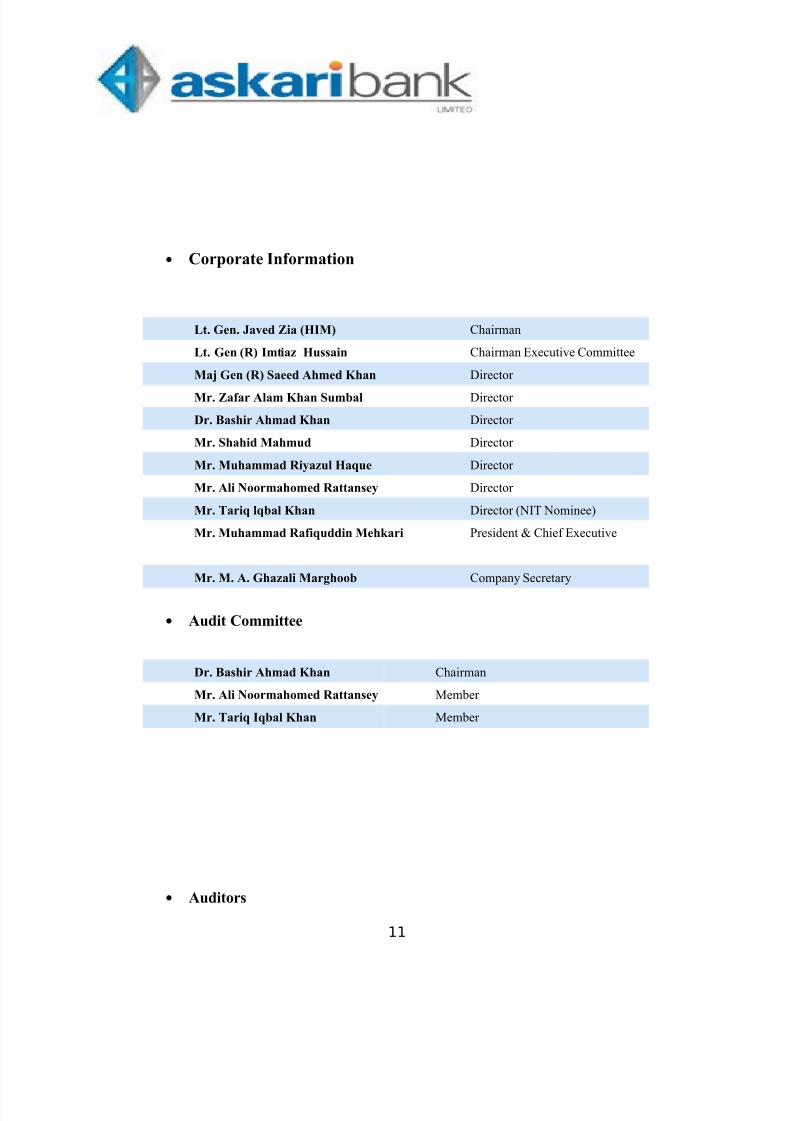

• Corporate Information

Lt. Gen. Javed Zia (HIM) Chairman

Lt. Gen (R) Imtiaz Hussain Chairman Executive Committee

Maj Gen (R) Saeed Ahmed Khan Director

Mr. Zafar Alam Khan Sumbal Director

Dr. Bashir Ahmad Khan Director

Mr. Shahid Mahmud Director

Mr. Muhammad Riyazul Haque Director

Mr. Ali Noormahomed Rattansey Director

Mr. Tariq lqbal Khan Director (NIT Nominee)

Mr. Muhammad Rafiquddin Mehkari President & Chief Executive

Mr. M. A. Ghazali Marghoob Company Secretary

• Audit Committee

Dr. Bashir Ahmad Khan Chairman

Mr. Ali Noormahomed Rattansey Member

Mr. Tariq Iqbal Khan Member

• Auditors

11

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 12/39

A.F.Ferguson & Co. Chartered Accountants

• Legal Advisors

Rizvi, Isa, Afridi & Angell

•

Registered Office /Head Office

AWT Plaza, The Mall,

P.O.Box 1084, Rawalpindi.

Tel : (051) 9063000

Fax: (051) 9272455

Website

:www.askaribank.com.pk

1.4. Products and Services

The product & services of Askari commercial bank limited are developed keeping in

view the customers needs & wants, & the expectation that the customer attaches with its

financial institutions.

12

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 13/39

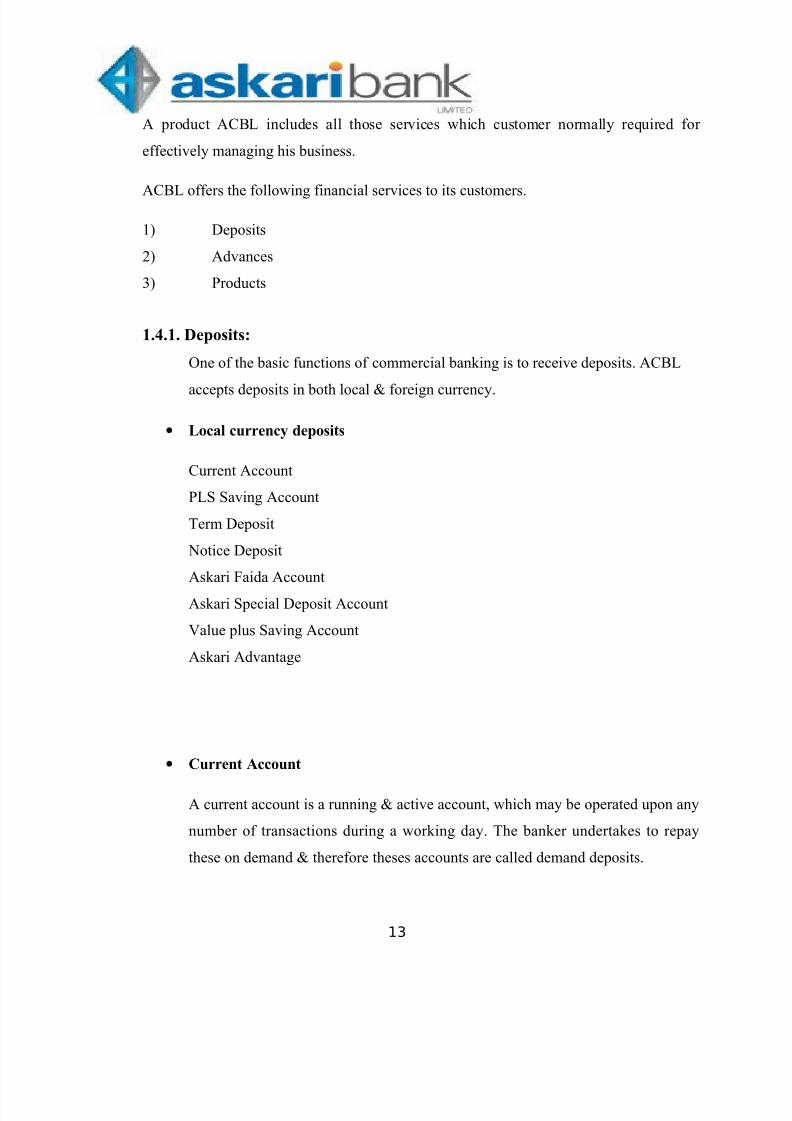

A product ACBL includes all those services which customer normally required for

effectively managing his business.

ACBL offers the following financial services to its customers.

1) Deposits

2) Advances

3) Products

1.4.1. Deposits:

One of the basic functions of commercial banking is to receive deposits. ACBL

accepts deposits in both local & foreign currency.

• Local currency deposits

Current Account

PLS Saving Account

Term Deposit

Notice Deposit

Askari Faida Account

Askari Special Deposit Account

Value plus Saving Account

Askari Advantage

• Current Account

A current account is a running & active account, which may be operated upon any

number of transactions during a working day. The banker undertakes to repay

these on demand & therefore theses accounts are called demand deposits.

13

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 14/39

• Transaction fee

The bank charges no transaction fees if the minimum balance requirement is met.

However, if the average balance falls below the min. balance then the fees ischarged at the rate of Rs. 10 per transaction.

• Saving Accounts

The saving account is usually opened by lower or middle class people so that they

can meet their future contingencies, as the objective of such account is to

promoting the habit of thrift among people, the bank impose certain restrictions

on withdrawals from the saving accounts.

• Transaction fees

Transaction fees are charged of Rs. 20 per transaction if the min balance is not

met.

1.4.2. Advances

Advances are major sources of earning of income for commercial banks. Banks attracts

surplus balances from the customers at low interest rates & makes advances at higher

interest rates to the individuals or business firms.

ACBL offer these facilities in two forms:

• Funded facilities

• Non- Funded facilities

• Funded facilities

14

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 15/39

In funded facilities the bank actually advances money against further repayment.

These facilities are known as cash credits.

•Non- Funded facilities

Non- Funded facilities are those in which bank substitutes its own credit for its

customers.

ACBL offers to its customers are large number of non-funded facilities.

These facilities include:

1. Guarantee

2. Letter of credit

1.4.3. Products

• Personal finance:

Personal Finance is a parameter driven product for catering to the needs of the

general public belonging to different segments. One can avail unlimitedopportunities through Askari Bank's Personal Finance. With unmatched finance

features in terms of loan amount, payback period and most affordable monthly

installments, Askari Bank's Personal Finance makes sure that one gets the most

out of his/her loan. Once a good credit history is established, the door to

opportunity opens much wider.

• Mortgage finance

Askari "Mortgage Finance" offers the convenience of owning a house of choice,

while living in it at its rental value. The installment plan has carefully designed to

suit both the budget & accommodation requirements. It has been designed for

enhancing financing facility initially for employees of corporate companies for

15

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 16/39

purchase/ construction/ renovation of house. The maximum financing amount is

Rs. 10 million with a repayment tenure upto 20 years.

• Business finance

In pursuance of the National objectives to review the economy of the country,

ACBL is providing loans to small and medium size business enterprises under

Askari Bank's Business Finance Scheme. Our goal is to offer a loan, which

enables business community to receive the financing required by them based on

their cash flows. Ore valued customers can enjoy the convenience of getting

financing on attractive terms with the minimum processing turnaround time.

• Askcar (Car Finance)

Yet another of our products, Askcar offers the most convenient and affordable

vehicle- financing scheme, which provides our valuable customers an opportunity

to own a brand new vehicle of their choice. With minimum down payment, lowest

insurance rates and widest range of available car makes and models, Askcar offers

the best value to our esteemed customers.

• Askcard

ASKCARD means freedom, comfort, convenience and security, so that you can

have retail transactions with complete peace of mind. ASKCARD is your new

shopping companion which enhances your quality of life by letting you do

shopping, dine at restaurants, pay your utility bills, transfer funds, withdraw and

deposit cash through ATM anywhere, anytime.

• Traveller cheques

The range of our products and value added services enhances with introduction of

Rupee Travellers Cheques (RTCs) launched in March 2002. In spite of our

constraint on issuing higher denomination of RTCs against restrictions imposed

by the Central Bank of Pakistan we have been striving to attain our shares with

16

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 17/39

sizeable portfolio. Total volume handled by the department during the year 2004

is Rs. 798 Million.

• Value Plus

The first liability product launched by this unit is showing a remarkable

acceptability in the market. The growth of this product is witnessed by its share,

which has presently reached at Rs. 1,079 Million even after lowering down the

profit rates due to sufficient liquidity in the market.

Askari master card

No joining fee

When you successfully apply for an Askari MasterCard, we will not

charge you any Joining Fee. It’s almost like you are getting it for FREE!

o Global acceptability

Your card provides you with service at thousands of locations in Pakistan, and

at over 23 million establishments worldwide. As an added convenience, you

will have the benefit of receiving your monthly billing in Pak Rupees,

regardless of the currency of purchase.

• 24-Hours customer service

With Askari MasterCard, you are always a phone call away from the assistance

you need. To speak to one of our friendly Customer Service representatives,

please call our UAN 111-000-787 for Karachi, Lahore or Rawalpindi/ Islamabad.

• Low service charges

17

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 18/39

Your Askari MasterCard provides you the experience of revolving your spending

at comparatively low service charges. In addition, the same rate also applies to

cash advance obtained on your Askari MasterCard

• Zero loss Liability

Please report loss or theft of your Askari MasterCard immediately at our

Customer Services UAN 111-000-787 for Karachi, Lahore and

Rawalpindi/Islamabad. Once you have registered the loss of your credit card, your

liability against its fraudulent use will be limited and we will send a replacement

card within 48 hours of reporting.

• Cash advance facility

Cash advance facility is available for Askari MasterCard holders. You can get up

to 80% of your sanctioned credit limit as cash advance in Pakistan or anywhere

else in the world. The facility is available at all ATMs displaying the Cirrus logo

around the world and in Pakistan. You may also avail this facility at designated

branches of Askari Commercial Bank, during banking hours.

• Balance Transfer facility

With Askari MasterCard, you can avail an incredible offer of a Balance Transfer

at the exclusive rate of just 1.5%* per month.

• Free travel insurance

Just purchase your travel tickets on Askari MasterCard and you are automaticallycovered under our Travel Insurance Plan (in case of personal accident resulting in

death or permanent disablement) for up to Rs.8,000,000/- on a Gold Card and

Rs.4,000,000/- on a Silver Card.

1.4.4. Agriculture Banking

18

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 19/39

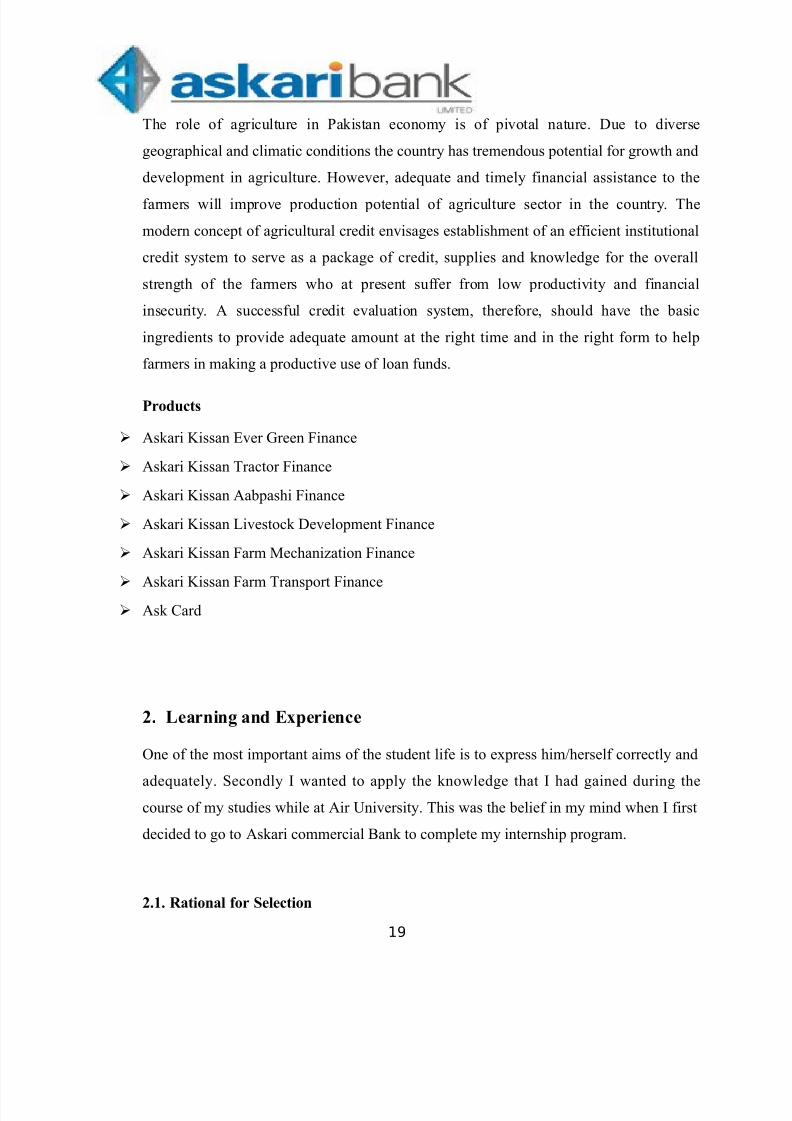

The role of agriculture in Pakistan economy is of pivotal nature. Due to diverse

geographical and climatic conditions the country has tremendous potential for growth and

development in agriculture. However, adequate and timely financial assistance to the

farmers will improve production potential of agriculture sector in the country. The

modern concept of agricultural credit envisages establishment of an efficient institutional

credit system to serve as a package of credit, supplies and knowledge for the overall

strength of the farmers who at present suffer from low productivity and financial

insecurity. A successful credit evaluation system, therefore, should have the basic

ingredients to provide adequate amount at the right time and in the right form to help

farmers in making a productive use of loan funds.

Products

Askari Kissan Ever Green Finance

Askari Kissan Tractor Finance

Askari Kissan Aabpashi Finance

Askari Kissan Livestock Development Finance

Askari Kissan Farm Mechanization Finance

Askari Kissan Farm Transport Finance

Ask Card

2. Learning and Experience

One of the most important aims of the student life is to express him/herself correctly and

adequately. Secondly I wanted to apply the knowledge that I had gained during thecourse of my studies while at Air University. This was the belief in my mind when I first

decided to go to Askari commercial Bank to complete my internship program.

2.1. Rational for Selection

19

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 20/39

I served Askari Bank Satellite town Rawalpindi as an internee for some six weeks. As

internship was a compulsory requirement for the completion of my BBA degree so I

observed feasibility of joining any organization of well repute. Before starting my

internship at Askari, I have bundle of ideas about different organizations to join. But the

point was which one to choose. And I choose Askari Bank Ltd. Most of the organizations

which I had idea about were banks. One reason of selecting banking industry was the

complete implementation of BBA courses under one roof.

I choose Askari Bank Ltd. because of some definite reasons:

• My account is held by Askari Bank Ltd, so I have been having regularly visiting

to the bank. That’s why I have a bit more attachment to this bank than else.

• During my visits to Askari Bank at different places, I observed that all the

branches have a harmony in the setup or physical outlook of the branch which

insisted me to think about management’s nationwide organization and planning.

• Up till my internship at Askari Bank, which ever branch I visited, all were having

an ATM machine because of which I came to the conclusion that the bank is

utilizing modern technology at a rapid speed.

2.1.1 First week

I started my internship from "General Banking" in the first week. The General banking is

basically divided into the following sub departments, which are as follows:

• Account opening

• Bills and remittances

• Clearing

• Term deposit

• Cash department

20

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 21/39

The first day of exposure to the practical field was at the (sub department) Account

opening.

The relationship of customer starts with this department. Every one is not allowed tocome and open an account in the bank, for this purpose there should be an introducer who

himself is the account holder in the same branch. He has to introduce the new client by

signing the opening account form and then his signatures are verified.

Applicant's fills the account opening form and provides it to the bank with photocopy of

I.D. card and signatures card.

Then the banker inquires the about the option of opening a joint account or individual. If

the customer wants to open joint account then either it is "either or survivor" (i.e. only

one persons signature is sufficient) or jointly (i.e. both should sign the cheque).

Account opening

Although the procedure of opening an account in a bank is a quite complicated job but I

am going to tell you only the basic necessities for opening the account, which are as

follows:

• Introduction

• National I.D. card

• Personal data

• Details of dealing with other banks.

These are some of the basic requirements for opening the account.

Issuance of chequebook

Once the account is opened, ACBL issues the cheque book to the customer so that they

could withdraw their money whenever they like. The producer of issuance of the

chequebook is as follows:

For the customer who already has an account with the bank, the lastly consumed

chequebook requisition slip with the help of which a new chequebook is issued. And the21

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 22/39

person who is going to open a new account for the first time gets the chequebook free

without any requisition slip.

For the new depositors the cheque book is not issued at the time of opening of account,rather it is issued after three days but, as the most of the customers are from the armed

forces so the usually get the cheque earlier. ACBL issues the cheque books for both the

local and foreign currency accounts.

I remained there in the account-opening department for one week and daily I learnt a new

thing

I come to know about the details of the account opened by the banks.

In the start I have stated the account opening procedure and issuance of cheque book in a

very comprehensive way, now let me tell u the further related detail of account opening

• First of all a customer come and gets the information regarding the opening of

account. After getting the proper information he gets an introducer and goes for

opening an account of any kind whatever he wants

• He fills the form regarding the opening of account which is in fact a request.

• S.S card is filled which contains the signature that will be used in future in order

to identify that you are the same particular person who perfectly eligible for

receiving the benefits.

• The S.S card and the application form is verified and the verification stamp is

imposed on it.

• After verification the application forms are pasted in the file with the serial, no

which is actually the account no. Allocated to the respective customers.

•The chequebook is issued to the customer after three days.

• A letter of thanks is posted to the customer as well as the introducer. The

introducer is thanked for the two perspectives. First he should be thanked that

because of him the bank get another customer and the second reason behind

sending the letter to him is that if the customer had fraudulently get the signature

22

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 23/39

of that person as an introducer then he should come to know that some one has

used his name as well as signature for his personal benefit and without the consent

of him (introducer).

• The procedure for opening the account comes to an end after sending the letter of

thanks.

Active and inactive Account

The account becomes Inactive if there is no debit transaction. Account becomes active if

there is credit transaction.

2.1.2 Second Week

In the second week I was shifted to the TDR (Term Depots Receipts) department. It was

again a good experience to work with the officer here. First of all he told me about the

basics of the TDR.

Deposit is lifeblood of a commercial bank. The main function of a commercial bank is to

channelize the saving from the savers to the ultimate users of the funds. This process of

collecting saving is called "deposit mobilization".

Deposits are of two types one is the demand deposit and the other one is time deposit

(these have been explained in detail in the "department" portion). As the name signifies

the demand deposit is payable on demand so no interest or benefit is given on such

deposits but the time deposit is a kind of deposit, which gives you a benefit in terms of

cash. Most of the people who have surplus money with them especially the landlords

deposit their money in such accounts.

Term deposits are payable on demand with certain maturity. Different percentages of

profit are given in the time deposit (the detail is given in the Marketing Mix)

These are called fixed deposit because they are fixed and no transaction is allowed till

maturity. In fix deposit you can open an A/c of the same title only than A/c number will

23

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 24/39

be changed. While in other accounts the A/c can't be opened under the same title even in

other branch of the same Bank.

Record keeping

The record of the TDR is although feed in the computer but there is also a hard copy of

the record. The verified TDR forms are pasted with serial number of receipt given to the

customer (the receipt of the form regarding the deposit of the amount).

Askari Bachat Certificates are attached or pasted in the file according to the date. The

date may be of any month and any year i.e. if there is a card of the 8th then on this card

you will find the only 8th date of any month and any year in which the card was issued.

2.1.3. Third Week

In the third week of my internship I was shifted to the Clearing section and Bills for

collection section as well. Three days I worked with the "Clearing" and then with the

"Bills for collection" section.

Clearing

This is a "Inter-city clearing" i.e. the cheques of Lahore city from different banks like

National Bank of Pakistan, Standard Chartered Bank, Muslim Commercial Bank are

deposited here. The deposited cheque is received carefully by checking the title of

cheque, date, amount, and signature on the cheque. All the cheques go to the State Bank

of Pakistan. Everyday NIFT receives all cheques and arranges them. By establishment of

NIFT a lot of time, cost and labor is saved. The cheques are stamped carefully. Two

stamps are required on the cheques

• Clearing stamp

24

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 25/39

• Payee's account will be credited

If any stamp is missed or unclear, SBP returned one the cheque with reason.

When the cheques are deposited they enter all the cheques on the computer with accountnumber and these figures go to SBP.

There are four types of Balances in the computer

• Available balance

• Float amount

• Block amount

•

Ledger balance

NIFT collects all the cheques at 2:00 pm. After that the computer department gives

clearing sheet that is checked in clearing.

Same day clearing

All the cheques are cleared in coming day. But same day cheques are cleared other same

day when it is deposited. The same day cheque amount is 50,000 below this amount thecheque, can't be cleared in the same day.

Clearing house

It is a place where representatives of all scheduled banks sit together and interchange

their claim against cash other with the help of controlling staff of "state Bank of

Pakistan" where there is no branch of State Bank of Pakistan, the designated branch of

State of Pakistan.

So, system by which banks exchange cheques and other negotiable instruments drawn on

each other within specific area and there by secure payment for their clients through the

clearing house at specific time In an efficient way.

Bills for collection

25

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 26/39

Two types of cheques are deposited here

• Outstation cheques

• Askari other branch cheques (local)

Outstation cheques mean different cities cheques are deposited and Local means Askari's

other Branches like cantt, circular road, defence, Gulberg etc. Are deposited. All cheques

account numbers on the computer and these figures go to SBP.

The cheques are cleared in 5-6 days. Because "NIFT" receives and delivered to SBP

where these cheques are cleared in 3 days and deliver to the banks, which mention on the

cheques.

The cheques require three stamps

• Askari crossing stamp

• OBC number

• Payee's account will be credited.

2.1.4. Fourth Week

In the fourth week of internship I was transferred to the "Remittances department". I met

there with a quite sophisticated personality, she tells me about the issuance, procedure

and the entries of the demand drafts and pay orders.

Demand Draft

It is an instrument payable on demand for which value has been received, issued by the

branch of the bank drawn. Demand draft is payable at some other branches of the same

bank. But Askari Bank contract with MCB so ACBL's demand draft is payable at MCB

also. Demand draft is very useful because there is no chance o fraud. The person deposit

cash and get demand draft. It is used for outstation payment.

Issuance of demand draft

26

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 27/39

On the application form following particulars are given:

• Name of beneficiary

• Amount

• Mode of payment

• The place where DD is drawn

• Signature

• Name and address of the beneficiary

Request shall be made on standard application form. The customer writes his name,

address, I.D number, and phone number on the backside of the application form.

Commission is charged as per schedule of charges. The issuance of DD is computerizedand the amount is automatically protect graphed drawing printing for the avoidance of

forgery.

The withholding tax and excise duty is deducted as per schedule. when the customer

depots cash in the cash department, he got voucher from the cash department and gave it

to the person who makes the DD.

Payment of DD

When a person brings DD (which have been drawn on you), you will check it from your

DD payable record and ask the customer to sign twice at the back of the DD so that it

could be confirmed that he is the eligible person for receiving the benefit, along with this

you obtain the ID of that person verify it and then make the payment. After making the

payment, entry is made in the register that this DD has been paid.

DD payable register

Every day you receive an IBCA from different banks and it contains a list of DDs, which

have been drawn on you. Banker records it in DD payable register. These DD are those,

which other branches have drawn on your bank.

Payment of DD from Suspense A/c

27

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 28/39

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 29/39

The transfer of funds from one branch to another branch of the same bank is called

telegraphic transfer. The bank apply test on telegraphic transfer. The applicant receives

Commission and charges, if the Applicant’s account is in ACBL, he pays no charge

above Rs. 100,000/-

If he has no account in the ACBL then he has to pay charges according to the amount e.g.

for Rs. 100,000/- the charges are Rs. 250/-

If the account of beneficiary is in another bank, his bank will present The TT to ACBL

through for payment.

Pay Order

Pay order issued from one branch can only be payable from the same branch. Pay order is

used for same city payment. E.g. If ACBL (Main Branch) issued pay order it is only

payable for Main Branch of ACBL.

Procedure

• Applicant fill the application

• After paying charges he gets voucher and pay order is issued

• All pay orders shall be crossed "payee's A/c only".

Cancellation

• The applicant give application for cancellation

• Charges are recovered from the applicant.

2.1.5. Fifth Week

In the second last week of my internship I worked in the "Accounts section".

Account Section

29

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 30/39

I worked in accounts department but as it is a confidential department so they did not

give me enough information regarding their working. First day I sorted out the cheques of

ACBL with the help of the serial number and the nature of the account and arrange them

in sequence. After that i checked the activity which contains the title of the cheque,

amount, date etc. Accounts department maintains the record of expenses of all the

departments, it also maintain the record of all the employees regarding their basic salary,

increment, benefits etc. It is the backbone of ACBL

On the next day I worked in the mail dispatch section, the person appointed here asked

me to arrange the letters and to write the mailing address on the envelopes and then to put

the letters into the envelops. It was an interesting job but, the single thing which I learned

from here was that, I learnt by heart the addresses of many branches of the ACBL, which

helped me to know the extensive branch network of the Bank. On the following day I

repeated the same job and did nothing else.

2.1.6. Sixth Week

In the last week I was shifted to the "foreign exchange" department. For the first three

days I worked there but in the last three days I was shifted again to the account-opening

department due to the absence of one of the Account opening officer. Therefore I was

sent back to the account-opening department.

30

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 31/39

2.2. Swot Analysis of Askari commercial Bank

Strengths

Leading Private sector Bank

Askari commercial bank is the leading private sector bank in the banking network

in Pakistan with many of them online branches in major cities of the country

• Full day Banking

One can avail the benefit of the services provided at the bank till 5:00 P.m. which

is highly useful for those customers who find it difficult to leave their officers in

the morning.

• Atm Network

The bank has the largest ATM Network cross the country. The customers of

ACBL withdraw access their funds any time at all the ATM Sites with

ASKCASH Logo.

• Customized solutions

The management of the bank believes in customer focused banking rather than the

product oriented banking. The products and services designed by the bank are

specifically tailored to the individual needs of its customers.

•Electronic Banking

The revolution in the banking in the form of electronic banking operations have

opened avenues of excellent, efficient and quick services saving the time and

costs of the customers and fortunately ACBL is among those few banks who are

already reaping the benefits of electronic transactions.

31

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 32/39

Electronic Funds Transfer

ACBL management is quite prepared to adopt the latest advancements in

technology resulting in revolution in the banking operations such as check

clearing process, computer based teller equipment, automatic teller machines, and

electronic funds transfers among the others.

Phone Banking

Phone banking service is very attractive for those classes of customers who don’t

have time to personally come to the bank i.e. banking on the phone line thus

saving the precious time of the customers.

Weaknesses

In my opinions these are the points that might be detrimental to the efficiency and

profitability of the bank.

Not Highly Automated

The bank has still some of the traditional ways of operations in this advanced

technological environment.

Manual Book Keeping

Although the bank has computerized accounting system but, still the bankers use

to make their entries in the accounting register.

Low Job Satisfaction

Understanding and the effective management of the human resources is the most

difficult challenge faced not only by the bank but by all the organizations. Even

though the people have been sacrificed in the new organizational developments, it

is becoming clear that the true lasting competitive advantage comes through

human resources and how they are managed. ACBL seems to not focusing on this

highly critical issue as the job satisfaction level of the employees working at

ACBL, was quite low.

32

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 33/39

Lack of Specialization

This famous and useful concept given by Adam Smith in 1776 seems to be

missing in the bank. The employees are constantly rotated from one job to another

job of totally different characteristic in the view of giving them the know-how of

the working in all the departments. But I think this is not a very good tactics used

by the management. Otherwise the situation might be like this ‘Jack of all and

master of none.’

Centralization

There is a high degree of centralization in the bank. Almost all the decision-

making is in the hands of the upper management. But centralization is effective upto a certain level otherwise it becomes inefficient and at times costly too. I

personally observed that delay occurred in the operations of the employees only

due to the fact that they had not got any instructions from the head office.

Lack of Training Facilities

Presently there is no specific training program arranged for the new recruiters.

They have to learn based on their observations and also their mistakes. It takes a

bit time for the fresh one to learn the banking the result is huge amount of

blunders, mistakes etc. resulting in monetary and non-monetary losses for the

bank. There is pressure not only on the new learner but also on the person placed

upon with this responsibility.

Opportunities

Apart from the ones discussed in External Factors Evaluation Matrix, the bank is facing

the following threats and opportunities currently:

These are positive external environmental factors effecting the organization.

• It deals in bulk business.

• A large amount of foreign investment is attracted.

• Strong potential for growth

33

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 34/39

• Steady increase in Customer Deposits

• Overseas Operations

• Branches In Remote Areas

• Islamic Banking

• Sharp increase in imports and exports

Threats

• High Employee turnover

As discussed above, the job satisfaction level of the employee is very low

resulting in high turnover, which is bad for any organization as there are hugemonetary and non-monetary costs involved in the fresh recruitments.

• High charges

• The schedules of charges indicate that the fees charged by the bank on the various

services it provides are extremely high. It may result in decrease in the number of

its exiting customers. Further more, this could be very alarming situation for the

bank in case some of the competitors grasped the opportunity and lowered its

rates.

• Less attractive rate of return

Commercial banks face considerable competition in attracting deposits from

individuals or small investors. In contrast, the Govt. of Pakistan national saving

scheme offers attractive rates of return (approx. 16 to 18 percent annually) on 10-

15 year fixed accounts, which banks find difficult to match.

2.3. R ECOMMENDATIONS

• All the departments should work as a team not as individuals, so, that the whole

branch would get benefit out of it. So, there is a lack of teamwork.

34

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 35/39

• As they lack international presence, so it’s better for them to take advantage from

international banks and try to adopt their policies and strategies to be in their line.

• I believe more incentives should be given to the human resource to keep them

committed to their bank. Such incentives can be in the form of bonuses for those who

performed really well for a time span of 2 or 3 consecutive months.Job rotation of

such capable employees is another good idea in which officers should be given

different tasks (job rotation) or multiple tasks (job enlargement) to ensure the officials

that they are an important asset for the multinational organization. Such measure

would also make them know where exactly do they stand and what exactly are they

doing for the Bank.

• If leadership to some extent becomes decentralized, employees would have a free

hand to make certain decisions according to their own work experience. Employees if

given a free hand can at times come up to certain procedures which are less time

consuming and more beneficial for the whole organization. Such procedures /

methods can later on be implemented for the whole bank to be followed which would

in turn increase the efficiency level of Askari Bank. Similarly, it would initiate other

employees to come onto certain measures which should be implemented amongst the

whole organization.

• The reference based criteria should not be followed for recruitment of employee.

Incompetent workers cause damage to bank’s repute and smooth flow of branch.

• Although technology, bank currently owns is in working condition, but it often

crashes so its better that Askari Bank adopts new and modern mechanisms for

maintaining its technology as some times systems get hanged. The software and

hardware, which is called as ‘System’, of the bank should be upgraded. Better

computer specialists should be hired to program a new system as I found out that

majority of the problems are occurring because of up gradation and changes in the

current system.

• Adopt more aggressive marketing strategy and should be proactive in social causes.

Right now the bank plays little or no role in social causes whereas its competitors are

actively participating.

35

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 36/39

• There should be some training system for internees and also some reward system for

internees so that to motivate them for high performance and low absentees.

2.4. CONCLUSION

This internship experience has been very much informative for me as it helped me in

numerous ways like in learning new things and ideas about official environment and now

I have the knowledge and experience of working in office environment. I have realized

my abilities and expertise of working in that kind of environment. Internship is a

36

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 37/39

supervised pre-professional career related experience paid or unpaid, part or full time,

with measurable learning objectives and formal evaluation.

Askari Bank Ltd will remain an aggressive and innovative financial institution andcontinue to adhere to the tradition of understanding its customer’s needs and looking for

new ways to serve them. Further integration and productivity gains will result in stronger

performance in terms of revenue as well as service quality in the coming years. The

strong leadership of Board and management and the relentless effort of the staff at Askari

Bank Ltd will be able to offer more superior products and services to customers and to

contribute more to economic and social development of Pakistan while developing a

bigger future for it.

Askari Bank views specialization and service excellence as the cornerstone of its

strategy. The people of bank innovation, creativity, reliability, customized services and

their execution are the key ingredients for their future growth. Based on this approach,

their Treasury Division and the Structured Finance Unit have been geared to provide

specialized services to the corporate customers. Revenues from these activities have

started yielding dividends and they expect significant growth in these areas in the coming

years. While building on their in-depth familiarity with their customers’ needs and

anticipated developments in the banking industry, the Retail and Corporate areas of their

operations will continue to provide a strong and stable base to the business of the Bank.

They are aware that they have stepped into the 21st century and they must meet its

challenges by acquiring the highest levels of Technology. They will thus be accelerating

their enable them distribute their products and services through most efficient and high-

tech means. They say that they will invest in the modern tools and substantial allocation

of resources will be made to achieve this objective during the current year. Their focus

would be to constantly seek out growth opportunities through increased quality assets and

by offering a wider range of products and services to their esteemed customers. There are

significant growth opportunities for ASKARI BANK and they are confident in their

37

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 38/39

ability to grasp them. They are committed to enhancing the shareholder’s value and look

forward with greater optimism to a prosperous future for ASKARI BANK.

REFERENCES:

1. http://www.askaribank.com/

2. http://www.google.com.pk/

38

8/4/2019 Report Ful n Final

http://slidepdf.com/reader/full/report-ful-n-final 39/39

3. www.askaribank.com/creditcards/index.asp

4. http://en.wikipedia.org/wiki/Askari

5. Brochure- ACBL Awards & Achievements

6. Economic Bulletin, Vol. 34, No.5 September – October 2008, published Bi-monthly by

Economic Research Wing, Askari Bank Ltd

7. Economic Bulletin, March-June 2008, published bi-monthly by Economic Research

Wing, Askari Bank ltd.

8. ACBL News lines, s Newsletter January 2008