Embed Size (px)

Citation preview

CR Common Practices Related Party Disclosures

1

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

Introduction

Under International Accounting Standards, the presentation of related party information is governed by IAS 24 “Related party disclosures”. Two versions of this standard currently exist with a revised version having been issued in November 2009 the application of which is mandatory for accounting periods beginning on or after 1 January 2011 although earlier application is permitted. This revision simplifies the definition of a related party, clarifying its intended meaning and eliminating inconsistencies as well as establishing a partial exemption from the disclosure requirements for government related entities. It does not, however, alter the fundamentals of related party disclosure requirements. The overall objective remains that an entity's financial statements contain the disclosures necessary to draw attention to the possibility that its financial position and profit and loss may have been effected by the existence of related parties and by transactions and outstanding balances with such parties. Under IAS 24 an individual is a related party of an entity in one of three main circumstances: (i) if they have control or joint control; (ii) if they can exert significant influence; and (iii) if they are a member of its key management personnel. Another entity is a related party if: (i) both it and the reporting entity are members of the same group; (ii) one entity is an associate or joint venture of the other; (iii) if the same third party can exert joint control or significant influence over both entities; (iv) the entity is a post- employment benefit plan for the benefit of the employees of the reporting entity; and (v) an individual qualifying as a related party controls, jointly controls or exerts significant influence over both entities (para 9).

Focusing on a sample of 30 large listed European companies that report under IFRS, supplemented by Company Reporting data and comment, this report analyses the types of related parties identified and the form that company disclosures take.

Key observations include the following. Key management compensation is widely disclosed with a number of companies going beyond what is required by IAS24. Related party information given by Italian companies goes beyond that of others due to national legislation. Financial institutions are most likely to identify governments as a related party. Financial institutions are more likely than other companies to identify a post-employment benefit plan as a related party.

Companies under examination

Our sample consists of 30 listed European company accounts, which feature in the Standard & Poor’s Europe 350 dataset with period ends of 31 December 2010 which have published recently their annual reports. The sample contains a spread of companies from different countries and industry classes. The companies of which the accounts have been analysed are as follows:

Company Period end Auditors Country Industry class

Accor 31 December 2010 Deloitte and Ernst & Young France Hotels

Aegon 31 December 2010 Ernst & Young The Netherlands Life Insurance

Anglo American 31 December 2010 Deloitte UK General Mining

ASML 31 December 2010 Deloitte & Touche The Netherlands Semiconductors

Assa Abloy 31 December 2010 PricewaterhouseCoopers Sweden Building Materials & Fixtures

Astra Zeneca 31 December 2010 KPMG UK Pharmaceuticals

BAE Systems 31 December 2010 KPMG UK Defence

BASF 31 December 2010 KPMG Germany Commodity Chemicals

BBVA 31 December 2010 Deloitte Spain Banking

Belgacom 31 December 2010 Deloitte Belgium Fixed Line

Telecommunications

BG 31 December 2010 PricewaterhouseCoopers UK Integrated Oil & Gas

BMW 31 December 2010 KPMG Germany Auto-mobiles

BNP Parabis 31 December 2010 Mazers and PricewaterhouseCoopers France Banking

Commerzbank 31 December 2010 PricewaterhouseCoopers Germany Banking

Drax 31 December 2010 Deloitte UK Conventional Electricity

Eni 31 December 2010 Ernst & Young Italy Integrated Oil & Gas

E.on 31 December 2010 PricewaterhouseCoopers Germany Multi-utilities

Fiat 31 December 2010 Deloitte & Touche Italy Auto-mobiles

Groupe Danone 31 December 2010 PricewaterhouseCoopers and Ernst &

Young

France Food Products

Iberdrola Renovables 31 December 2010 Ernst & Young Spain Alternative Electricity

ITV 31 December 2010 KPMG UK Broadcasting and Entertainment

L'air Liquide 31 December 2010 Ernst & Young and Mazars France Commodity Chemicals

Lloyd’s Banking Group 31 December 2010 PricewaterhouseCoopers UK Banking

Logica 31 December 2010 PricewaterhouseCoopers UK Computer Services

Nestle 31 December 2010 KPMG Switzerland Food Products

Novozymes 31 December 2010 PricewaterhouseCoopers Denmark Biotechnology

Royal DSM 31 December 2010 Ernst & Young The Netherlands Speciality chemicals

Smith & Nephew 31 December 2010 Ernst & Young UK Medical Equipment

TeliaSonera 31 December 2010 PricewaterhouseCoopers Sweden Fixed Line

Telecommunications

UBS 31 December 2010 Ernst & Young Switzerland Banking

Analysis

Early Adoption

Of the companies in our sample only two have chosen to early adopt the revised version of IAS 24. These are TeliaSonera and UBS. TeliaSonera continues to identify as related parties both the Swedish and Finnish governments which respectively hold 37.3% and 13.7% of the company's shares. Despite the revised version of IAS 24 offering a partial disclosure exemption in relation to government related entities there is no change to related party disclosures in comparison to last year. TeliaSonera further notes that commitments are added to the list of examples of related party transactions but again there is no change to the disclosures in comparison to last year. UBS states that it adopted the revised standard in its 2009 financial statements thus resulting in a CHF668 million reduction in loans to related parties and a CHF11 million reduction in fees receivable in relation to its 2008 financial year. Early adoption has not impacted the types of related parties reported by either company with both continuing to report a broad range. TeliaSonera's related party disclosures include information relating to: key management personnel compensation; joint ventures; associates; governments; and pensions. The information given by UBS relates to key management personnel compensation; associates; pension plans; entities in which key management have an interest; and loans to board members.

Types of Related Party Information

The types of related party identified by our sample companies mirror those outlined in IAS 24 with the most common type of information identified being compensation paid to key management personnel which is clearly disclosed by 29 of the 30 companies in our sample. The next two most commonly identified forms of related party are entities over which the reporting entity can either exert significant influence or holds joint control namely associates and joint ventures respectively. Of the companies in our sample 22 identify associates as related parties with 18 identifying joint ventures. A further common type of related party which is identified by 10 companies in our sample is an employee pension plan with others disclosed including: governments; entities in which key management personnel have an interest; non-consolidated companies; and companies with a material shareholding in the reporting entity. Under IAS 24 for related parties other than Key Management Personnel Compensation companies should disclose the nature of the related party relationship as well as any transactions and amounts outstanding at the yearend separately for each type of related party (para 18 & para 19)

Types of Related Party Number of Companies

Key Management Personnel Compensation 29

Key Management Personnel Loans 5

Entities by virtue of Key Management Personnel Interest 7

Associates 22

Joint Ventures 18

Government 6

Pension Schemes 10

Non-consolidated subsidiaries/Companies 5

Companies with material shareholding or Control 3

CR Common Practices Related Party Disclosures

3

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

Key Management Personnel Compensation

Key management personnel are defined by IAS 24 as those persons having authority and responsibility for planning, directing and controlling of the activities of the entity, directly or indirectly, including any director whether executive or otherwise of that entity (para 9). All companies in our sample have a group of individuals at their head which meet this definition but not all clearly identify such individuals as related parties using IAS 24 terminology. Of the companies in our sample 20 identify the compensation paid to key management personnel within their related parties note with such companies including BAE Systems, E.on and Royal DSM. A further three companies either include the information in a separate note referenced within the related parties note or use IAS 24 specific terminology by identifying the information given as key management personnel compensation. These companies are BG and Eni which both use the key management personnel terminology and BBVA which gives the information in a referenced note. For a further six companies information of the type required by IAS 24 is given in a note to the accounts but the link to related party information is less clear. These companies include BMW, ASML, Assa Abloy and BNP Parabis. In the case of BASF, however, there is no disclosure of key management personnel compensation in either a related parties or any other note to the accounts. Reference is instead made to a separate compensation report included within the corporate governance section of the annual report.

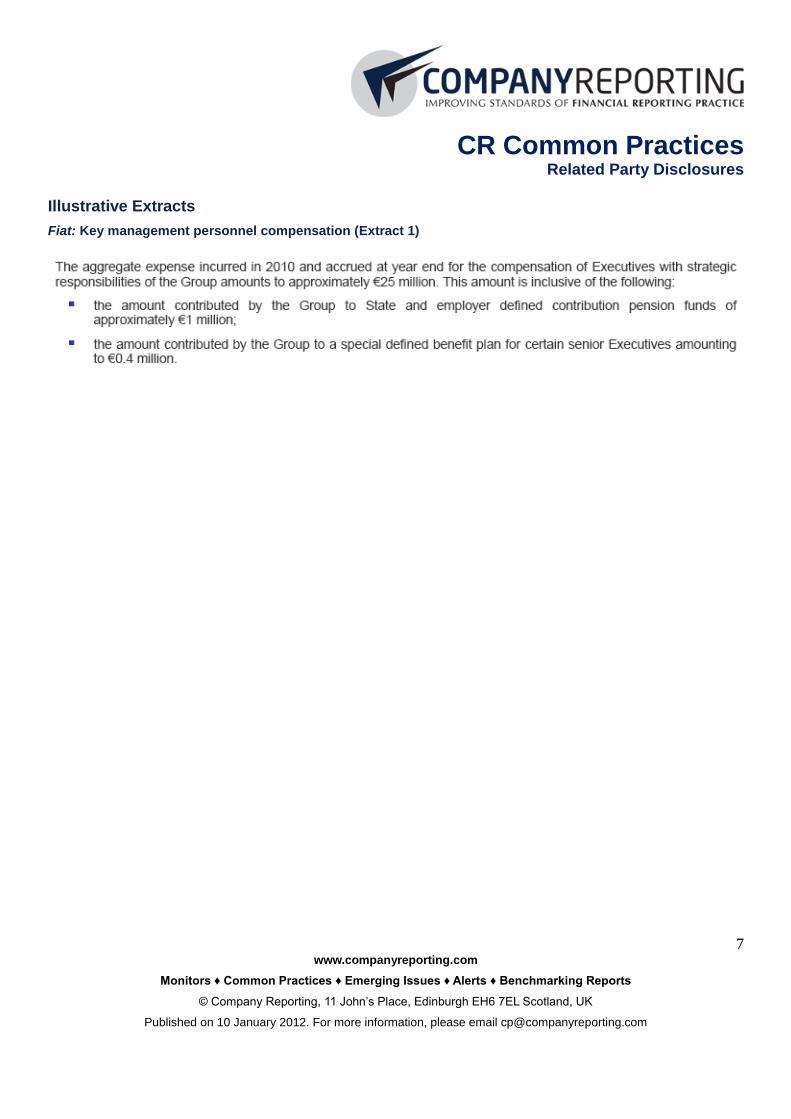

Under IAS 24 companies are required to disclose key management personnel compensation in total and for each of the following categories: short-term employee benefits; post-retirement benefits; other long-term benefits; termination benefits; and share-based payment (para 17). Of the companies in our sample disclosing key management personnel compensation in a note to the accounts all but one clearly discloses amounts in line with the IAS 24 defined categories. The exception to this is Fiat which identifies the total amount paid to directors without giving any breakdown, disclosing only that the total includes the notional cost of stock options and stock grants paid to the Chief Executive Officer without quantifying the amount. In addition, Fiat discloses separately the total compensation paid to executives with strategic responsibilities stating that this includes amounts in relation to both defined benefit and contribution pension plans (Extract 1). No mention is made of the other IAS 24 defined categories.

While all other sample companies giving key management personnel compensation information in a note follow IAS 24 the format of disclosures is varied. The vast majority of companies including Logica, Belgacom and Astrazeneca (Extract 2) choose to present the information in a tabular format although there are those such as E.on, Groupe Danone and Royal DSM which instead employ a narrative disclosure format.

Some companies opt to go beyond what is required by IAS 24. Companies do this by either including additional disaggregation when disclosing the types of remuneration or by giving information separately for each member of key management. Two additional types of remuneration disclosed by companies are benefits in kind and bonuses with companies identifying the former including Iberdrola Renovables, Anglo American, BNP Parabis and BG. Those to disclose the latter include Novozymes, BG and Nestle. BG makes reference to bonuses with Novozymes disclosing cash bonuses and Nestle identifying both cash and share bonuses separately. Further additional categories identified are social security costs which are disclosed by Iberdrola Renovables and Anglo American and Directors fees which are disclosed by Groupe Danone and BNP Parabis. The former opts to disclose an aggregate figure whereas the latter gives information separately for each director. The information given by BNP Parabis for each director is not limited to such fees, however, with other forms of key management personnel information disclosed in the same fashion (Extract 3). BNP Parabis, although not for each individual, gives a particularly detailed breakdown of post-retirement benefits disclosing information for separate pension schemes. BNP Parabis is not alone in presenting information separately for individual directors. Other companies to do so are ASML, TeliaSonera, Assa Abloy, Aegon and Commerzbank.

Key Management Personnel Transactions

In addition to receiving compensation from the organisations within which they work key management personnel and directors impact the related party disclosures of a number of sample companies in other ways. There are two main instances where this is the case. These are either where an individual has transacted with the company in their own right or where another party over which the individual may have influence has transacted with the company.

Each of the banks in our sample identifies key management personnel as related parties by virtue of the fact that loans have been made to such individuals. There are, however, differences between companies in relation to the format that disclosures take. Lloyd’s Banking Group, Commerzbank and UBS all disclose this information in a tabular format giving information in relation to movements during the year. Lloyd’s Banking Group and UBS both disclose additions and repayments separately whereas Commerzbank gives only a percentage change figure which combines both. In addition both Lloyd’s Banking Group and Commerzbank disclose the interest rates relevant to these loans. Within its related parties note to the accounts Commerzbank further analyses loans into those relating to its supervisory board and board of management. In contrast, UBS presents no such breakdown in a note, but does so in a separate corporate governance report within which it identifies amounts paid to separate individuals. BNP Parabis and BBVA instead disclose amounts outstanding in a narrative format with the latter identifying board of directors and management committee amounts separately. Lloyd’s Banking Group stands out from the others as it is the only company to also present deposit information again in common with loans identifying the relevant interest rates.

Of the sample companies six, across a range of different industries, identify as related parties entities within which members of key management personnel have an interest. The sample companies in question are Accor, UBS, Fiat, Eni, Drax and BMW. Of these, Fiat, Drax and BMW fully explain why a related party relationship exists by identifying the actual member of management concerned and their position within the related party. The other companies only state that a related party relationship exists by virtue of an interest held by an unnamed member of key management personnel. In each case, however, the entities transacted with, and the nature of the transactions undertaken, are identified. In addition, with the exception of BMW which states that amounts are not material all companies quantify transaction amounts including those outstanding at the year end.

Associates and Joint Ventures

Associates and joint ventures are both identified as related parties by a significant number of sample companies with 22 identifying the former and 18 the latter. Of the sample companies identifying associates and/or joint ventures as related parties Accor, Belgacom, Nestlé and L'air Liquide make reference to transactions not being significant. In the case of Nestle such a statement refers only to transactions with associates with no mention being made of joint venture transactions other than that they are eliminated on consolidation in line with the Nestlé's percentage holding. The relevance of such a statement is hard to fathom as under IAS 24 the full amount of any transaction should be disclosed. L'air Liquide also discloses superfluous and arguably misleading information within its related parties note by identifying the contribution made to the consolidated balance sheet and income statement by proportionately consolidated companies. Groupe Danone discloses only amounts outstanding at the yearend making no specific statement about the existence or not of current year transactions.

Related party transactions with associates and joint ventures can be split into two types: funding and trading with there being a cross over in relation to banks where the primary area of business is to provide financing. Each of the banks in our sample, provide funding to joint ventures and/or associates but there are differences in disclosure. BBVA and Commerzbank both identify associate and joint venture amounts in aggregate with each disclosing both income statement and balance sheet amounts in a tabular format. Lloyd’s Banking Group instead chooses to disclose the information in a narrative format giving separate information for its Sainsbury's Bank joint venture but in common with its peers, aggregate information for other joint ventures and associates. UBS and BNP Parabis in contrast to the other banks disclose associate and joint venture amounts separately with the latter including a detailed analysis of income statement and balance sheet amounts (Extract 4).

Non-financial companies to disclose the provision of loan finance to joint ventures or associates include TeliaSonera, Anglo American, BG, BMW and Eni. BG discloses only the total for loans to all associates and joint ventures in aggregate identifying a range of interest rates which attach to these loans. BMW and Anglo American also aggregate loan amounts but only in relation to joint ventures. The latter disclosing separately a significant loan to an individual associate. TeliaSonera also identifies a loan amount for an individual investment but the disclosures given by Eni are by far the most detailed. Eni identifies separately loans made to each of its investments giving some information in relation to the purpose of each loan. For each individual investment loan receivables, payables, charges and gains are identified. In addition, Eni states that it has acted as guarantor for a number of its associates and joint ventures disclosing the amounts involved. Another company to act as guarantor for associate loans is Royal DSM.

Each of the above non-financial companies also enters into trading transactions with its associates and joint ventures but again the format of the disclosures given varies. BG in common with its disclosure of loan amounts aggregates associate and joint venture incomes and expenses as well as payables and receivables (Extract 5). TeliaSonera in contrast discloses individual sales and purchases amounts but opts to aggregate payables and receivables. Anglo American while disclosing that transactions were not significant also aggregates related party trade receivables and

CR Common Practices Related Party Disclosures

5

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

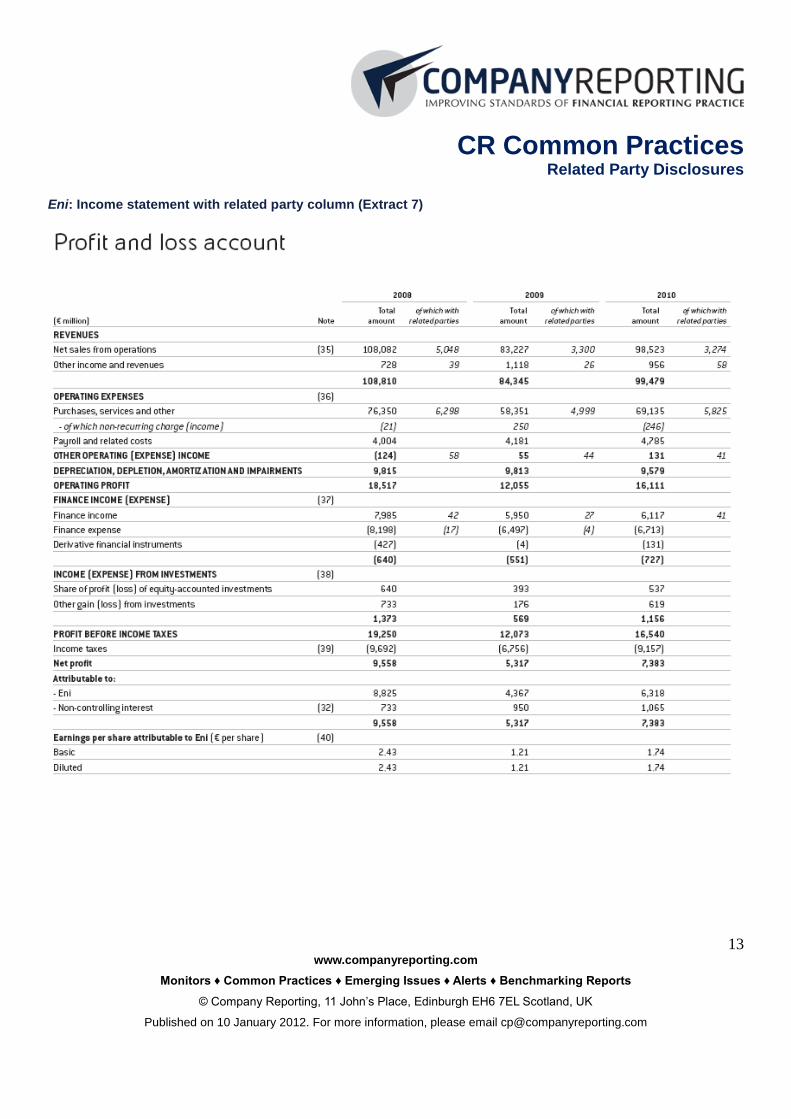

payable amounts. These aggregate totals are identified within the trade payables and receivables notes rather than the related parties note. Once again, however, the stand out company in relation to the disclosure of associate and joint venture related party transactions is Eni with individual sales, purchases, receivables and payables disclosed for each investment (Extract 6). In addition, Eni presents a narrative description of the most significant transactions. Eni goes further, however, by presenting a related parties income statement, balance sheet and cash flow statement impact analysis as well as including separate related party columns on the face of its primary financial statements (Extract 7).

Fellow Italian company Fiat discloses equally as detailed related party information but instead of including related party columns on the face of the primary financial statements publishes separate supplementary statements so as not to compromise an overall reading of the statutory statements (Extract 8). In addition Fiat presents in a note to the accounts an analysis of related party amounts as they relate to discontinued operations. The detailed related party information presented by both Italian companies is in respect of Italian legislation introduced in 2006. While the detail given by other companies is not so high there is variety in relation to the information disclosed. BAE Systems for example publishes a table which shows amounts in respect of individual equity accounted investments separately including sales, purchases, receivables, payables, lease amounts and management recharges (Extract 9). In addition to disclosing the figures involved ITV also explains the nature of related party transactions undertaken with associates and joint ventures. In contrast, Smith & Nephew and BASF while disclosing associate and joint venture related party information separately do not give amounts for individual joint ventures and associates.

Governments and other parties with a significant shareholding

Of the companies in our sample nine identify related party relationships in respect of either governments or other parties with a significant shareholding. Six sample companies identify related party information in relation to governments. Of these Aegon, Commerzbank and Lloyd’s Banking Group are financial institutions which due to current economic conditions have sought government support. In the case of Commerzbank and Lloyd’s Banking Group, this has led to the German government owning a 25% shareholding in the former and the UK government owning a 41% stake in the latter. Both banks state that transactions are carried out with government entities in the normal course of their business, however, only Commerzbank makes quantified disclosures in relation to such transactions (Extract 10). Lloyd’s Banking Group does, however, make reference to conditions that have been placed on it in return for government support. It has undertaken to loan a predetermined amount to businesses and to pay a fee so that the government would guarantee the issue of debt. Aegon gives a detailed breakdown of the financial support that it has received from the Dutch government in the form of convertible loans including terms and conditions. Under the support agreement dividends cannot be paid until the government loans are repaid.

Two further companies, Belgacom and TeliaSonera are government owned telecommunications providers with the Belgian government having a 53.5% stake in the former and the Swedish and Finnish governments having a 37.3% and 13.7% shareholding in the latter respectively. Although both companies state that telephony services are made available to the governments in question no quantified information is disclosed on grounds of materiality. TeliaSonera, however, does disclose a number of fees that it pays to the government such as for the use of numbers, radio frequencies and to fund measures to ensure electronic communications are not disrupted. The last company to disclose a government as a related party is Eni which gives a detailed breakdown of transactions with government controlled entities.

Companies to disclose related party transactions with significant or controlling shareholders other than governments are BBVA, Novozymes and Iberdrola Renovables. BBVA within its related parties note identifies transaction amounts in relation to significant shareholders in aggregate without identifying the parties in question. Analysis of the financial statements as a whole reveals that no party owns more than 5.07% of the shares. In the case of the other two companies a controlling shareholder is identified with 70.1% of Novozymes owned by the Novo Nordisk Foundation

and 80% of Iberdrola Renovables owned by Iberdrola. In both cases a detailed breakdown of income and expense amounts and transaction balances is presented showing transactions with the controlling party and fellow subsidiaries. In addition, Iberdrola Renovables gives a breakdown of financing received from its parent including a currency and maturity analysis and a disaggregation into fixed and floating (Extract 11). Iberdrola Renovables further gives a detailed description of agreements entered into with its parent and fellow subsidiaries.

Post-Employment Benefit Plan

Of the companies in our sample ten makes reference to a post-employment benefit plan being a related party. Of these five are financial institutions. The information disclosed by these companies varies with Commerzbank stating that external providers of occupational pensions for employees are considered related parties but give no further information. Aegon goes a stage further by disclosing that it provides reinsurance, asset management and administrative services to pension funds but stops short of giving any quantified information in relation to fees. Each of the other financial institutions which are Lloyd’s Banking Group, BNP Parabis and UBS also make reference to providing services for employee benefit funds but give quantified fee information. The information given by UBS, in terms of detail, surpasses that given by its peers as not only is reference made in the related parties note, a specific section exists within the post-retirement benefits note. Within this section UBS in addition to giving a breakdown of fees and services discloses details of a scheme whereby bank properties were sold to a pension fund and a transaction analysis of UBS securities held by the pension fund (Extract 12).

For the non-financial companies including BAE Systems, BMW and TeliaSonera that make reference to a pension plan being a related party on the whole the level of disclosure is less detailed. Nestlé however, outlines how one of its subsidiaries acts as an asset manager on behalf of a pension plan disclosing the fees that it receives in return for such services. There is also quantification in relation to the amount of assets under management. ITV also makes an interesting disclosure by identifying that a pensions funding partnership has been established. Under this arrangement, an interest in a partnership, which owns a company subsidiary, has been contributed to the pension fund. ITV makes it clear that it consolidates both the partnership and the subsidiary.

Stand out companies

Italian companies Eni and Fiat are worthy of praise for the sheer detail of the related party information that is presented. Both companies present a full analysis of related party transactions by type including separate quantified disclosure for transactions with each related party. The information disclosed is not confined to the related parties note with both companies presenting additional primary financial statement information so as to exhibit the impact of related party transactions as a whole. It should be noted that the information presented is largely as a result of national legislation but the fact remains that the information presented far outstrips that given by companies from other countries. Italy could easily be considered to be leading the way in terms of related party transaction disclosures. Other companies that are worthy of note are UBS which has early adopted revised IAS 24 and provides a detailed breakdown of transactions with post-employment benefit plans and BNP Parabis for the clarity of its disclosures in relation to key management personnel compensation, associates and joint ventures.

In contrast, companies which could improve the quality of related party transactions are BASF which does not disclose key management compensation in a related party or any other note to the accounts. Other companies which could improve their related party disclosures are BG which expresses associate and joint venture amounts in aggregate and L'air Liquide which within its related parties note includes information in relation to the impact that proportionately consolidated entities have on the income statement and balance sheet that could easily be deemed superfluous.

Summary - Conclusion

Our principal conclusions are that:

Key management compensation is widely disclosed with a number of companies going beyond what is required by IAS 24.

The most detailed related party information is given by Italian companies as a result of national legislation.

Financial institutions are the companies which are most likely to identify governments as related parties.

Financial institutions are more likely than other companies to identify a post-employment benefit plan as a related party.

CR Common Practices Related Party Disclosures

7

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

Illustrative Extracts

Fiat: Key management personnel compensation (Extract 1)

Logica: Key management personnel compensation tabular format (Extract 2)

CR Common Practices Related Party Disclosures

9

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

BNP Parabis: Key management personnel compensation per director (Extract 3)

BNP Parabis: Balance sheet analysis of associate and joint venture related party amounts (Extract 4)

CR Common Practices Related Party Disclosures

11

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

BG: Joint venture and associated undertakings related party amounts aggregated (Extract 5)

Eni: Joint venture and associate related party amounts by company (Extract 6)

CR Common Practices Related Party Disclosures

13

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

Eni: Income statement with related party column (Extract 7)

Fiat: Related party transactions supplementary balance sheet (Extract 8)

CR Common Practices Related Party Disclosures

15

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

BAE Systems: Related party transactions equity accounted investments (Extract 9)

Commerzbank: Government related party transactions (Extract 10)

Iberdrola Renovables: Analysis of related party financing (Extract 11)

CR Common Practices Related Party Disclosures

17

www.companyreporting.com

Monitors ♦ Common Practices ♦ Emerging Issues ♦ Alerts ♦ Benchmarking Reports

© Company Reporting, 11 John’s Place, Edinburgh EH6 7EL Scotland, UK

Published on 10 January 2012. For more information, please email [email protected]

UBS: Post employment benefit plan related party disclosures (Extract 12)