Embed Size (px)

Citation preview

© 2011 ACTEX Publications, Inc.. Regulation of Insurance & United States Insurance Law CAS Exam 6 – Peter J. Murdza

TABLE OF CONTENTS

REGULATION OF INSURANCE AND UNITED STATES INSURANCE LAW 1. Kucera ―NAIC Public Hearing on Credit-Based Insurance Scores‖ 1 2. McCarty ―Impact of Credit-Based Scoring on the Availability and Affordability of Insurance‖ 3 3. Harrington ―Insurance Rate Regulation in the 20th Century‖ 7 4. Musulin ―Issues in the Regulatory Acceptance of Computer Modeling‖ 15 5. Porter 2 ―Development of Insurance Regulation‖ 25 6. Porter 3 ―Federal and Other Influences on Insurance Regulation‖ 43 7. Porter 4 ―Roles of State Regulators and the NAIC in Insurance Regulation‖ 57 8. Porter 5 ―State Department of Insurance Operations 67 9. Porter 6/8 ―Licensing and Rate Regulation‖ 77 10. Porter 11 ―Solvency Regulation‖ 83 11. Porter 12 ―Insolvency Regulation‖ 99 12. Wagner ―Insurance Rating Bureaus‖ 117 13. NAIC IRIS ―Property/Casualty Ratios‖ 125 14. Feldblum RBC ―Property/Casualty Insurance Co. Risk-Based Capital Requirements‖ 159

15. A.M. Best Special ―Special Report: U.S. Surplus Lines—2007 Market Review‖ 205 16. GAO ―Common Regulatory Standards and Greater Member Protections Are Needed‖ 213 17. A.M. Best Annual ―Annual Review of the Excess and Surplus Lines Industry, September 2001‖ 215 18. AAA Asbestos ―Current Issues in Asbestos Litigation‖ 219 19. Legal Misc. Liability Insurance, Litigation Costs, and Expert Evidence 225

GOVERNMENT AND INDUSTRY INSURANCE PROGRAMS 20. AAA SS ―Social Security Reform Options‖ 229 21. Caulder ―Government Insurers Study Note‖ 241 22. Hamilton ―Residual Market Insurance‖ 247 23. Nyce ―Government Programs‖ 267 24. Wiening 10/12 ―Social Security, Social Security Disability Income Benefits, and Medicare‖ 277 25. Williams ―Ongoing Challenges Facing the National Flood Insurance Program‖ 293 26. Bartlett ―Attempts to Socialize Insurance Costs in Voluntary Markets‖ 297 27 CPCU ―Flood Insurance and Hurricane Katrina‖ 303

ACCOUNTING 28. AS–Page 2 Chapter 2: ―Assets‖ and Chapter 9: ―Investment Income‖ 311 29. AS–Page 3 Chapter 5: ―Other Liabilities, Capital, and Surplus‖ 359 30. AS–Page 4 Chapter 9 and Chapter 10: ―Other Income‖ 385 31. O‘Connell Chapter 8: ―Other Expenses‖ 425 32. Lynch Chapter 14: ―Generally Accepted Accounting Principles‖ 435 33. Scheid Chapter 15: ―SEC Reporting Requirements‖ 485 34. NAIC AS ―Annual Statement Blanks, Property and Casualty 2006‖ 493 35. Feldblum/Blanchard ―Notes to the NAIC Property/Casualty Annual Statement‖ 507 36. Feldblum Surplus ―Statutory Surplus: Computation, Pricing, and Valuation,‖ 517 37. Feldblum Schedule F ―Reinsurance Accounting: Schedule F‖ 525 38 Feldblum Schedule P ―Completing and Using Schedule P‖ 569 39. Feldblum IEE ―The IEE and the Allocation of Investment Income‖ 635 40. SSAP 5 ―Liabilities, Contingencies, and Impairment of Assets‖ 665 41. SSAP 9 ―Subsequent Events‖ 667 42. SSAP 53 ―Property and Casualty Contracts—Premiums‖ 669 43. SSAP 55 ―Unpaid Claims, Loss and Loss Adjustment Expenses‖ 673 44. SSAP 62 ―Property and Casualty Reinsurance‖ 677

45. SSAP 65 ―Property Casualty Contracts‖ 699 46. Blanchard Insurance ―Basic Insurance Accounting—Selected Topics‖ 707 47. NAIC Preamble Accounting Practices and Procedures Manual ―Preamble‖ 723 48. Feldblum Discounting ―Discounting Note to the Financial Statement‖ 731 49. DeFrain ―The Impact of International Financial Reporting Standards on U.S. Actuarial Practice‖ 740 50. Vaughan ―The Implications of Solvency II for U.S. Insurance Regulation 745 51. Feldblum IRS ―IRS Loss Reserve Discounting‖ 755 52. Feldblum Taxable ―Computing Taxable Income for P&C Insurance Companies‖ 763 53. Feldblum Strategy ―Federal Income Taxes and Investment Strategy‖ 793

© 2011 ACTEX Publications, Inc. Regulation of Insurance & United States Insurance Law CAS Exam 6 – Peter J. Murdza

PROFESSIONAL RESPONSIBILITIES OF THE ACTUARY IN FINANCIAL REPORTING

54. AAA Materiality ―Materiality, Concepts on Professionalism‖ 799 55. AAA Actuarial ―Practice Note on Statements of Actuarial Opinion‖ 807 56. ASOP 20 ―Discounting of P&C Loss and Loss Adjustment Expense Reserves‖ 857 57. ASOP 36 ―Statements of Actuarial Opinion Regarding P&C Loss and LAE Expense Reserves‖ 869 58. ASOP 41 ―Actuarial Communications‖ 873 59. ASOP 43 ―Property/Casualty Unpaid Claims Estimates‖ 877

REINSURANCE ACCOUNTING PRINCIPLES

60. Blanchard Reinsurance ―Basic Reinsurance Accounting—Selected Topics‖ 883 61. FASB 113 ―Accounting and Reporting for Reinsurance of Short-Duration and Long-Duration Contracts‖ 887 62. Freihaut ―Common Pitfalls and Practical Considerations in Risk Transfer Analysis‖ 901 63. Steeneck ―Commutation of Claims‖ 913

NOTES Questions and parts of some solutions have been taken from material copyrighted by the Casualty Actuarial Society. They are reproduced in this study manual with the permission of the CAS solely to aid students studying for the actuarial exams. Some editing of questions has been done. Students may also request past exams directly from the society. I am very grateful to this organization for its cooperation and permission to use this material. It is, of course, in no way responsible for the structure or accuracy of the manual. Exam questions are identified by numbers in parentheses at the end of each question. CAS questions have four numbers separated by hyphens: the year of the exam, the number of the exam, the number of the question, and the points assigned. SoA or joint exam questions usually lack the number for points assigned. W indicates a written answer question; for questions of this type, the number of points assigned are also given. A indicates a question from the afternoon part of an exam. MC indicates that a multiple choice question has been converted into a true/false question. Page numbers (p.) with solutions refer to the reading to which the question has been assigned unless otherwise noted. Please note that even though the section on the square root rule in Feldblum‘s ―NAIC Property/Casualty Insurance Company Risk-Based Capital Requirements,‖ has been deleted from the syllabus, problems that make use of that rule are still included in the manual. Although I have made a conscientious effort to eliminate mistakes and incorrect answers, I am certain some remain. I am very grateful to students who discovered errors in the past and encourage those of you who find others to bring them to my attention. Please check our web site for corrections subsequent to publication. I would also like to thank the following who in one way or another contributed to this manual: Ed Jordan, Laurrie Raida, and Joanne Spalla. Please note that because of the large number of past CAS exam questions that are relevant to this course, a Study Manual 7–S (a supplement) has also been published. It contains questions from older exams and their solutions. QUESTION NUMBERS RUN CONSECUTIVELY BEGINNING WITH STUDY MANUAL 7–S. Hanover, NH 6/29/11

PJM

AS–Page 3 359

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

D. Keith Bell, Chapter 5: "Other Liabilities, Capital, and Surplus,"

in Property-Casualty Insurance Accounting, Eighth Edition, pp. 5–1 to 5–15.

OUTLINE

I. LIABILITIES

A. Lines Not Discussed

1. Line 1 – Losses

2. Line 2 – Reinsurance payable on paid losses and loss adjustment expenses

3. Line 3 – Loss adjustment expenses

4. Line 6 – Taxes, licenses and fees (excluding federal and foreign income taxes)

5. Line 7.1 – Federal and foreign income taxes (including realized capital gains/losses)

6. Line 7.2 – Net deferred tax liability)

7. Line 9 – Unearned premiums (after deducting ceded reinsurance premiums)

8. Discussed items

a. Miscellaneous items that may comprise 5–15% of total liabilities

b. Categories

1) Accounts payable and accrued liabilities

2) Banking items

3) Dividends payable

4) Miscellaneous items

B. Postretirement Benefits Other Than Pensions

1. Postretirement benefits – "all forms of benefits, other than retirement income,

provided by an employer to retirees"

a. Specified benefits, e.g., health care

b. Monetary amounts

2. Treatment – overview

a. Accounted for on an accrual basis

b. Liability equals the actuarial PV of benefits expected to be received at

retirement by current retirees and fully eligible or vested employees

c. Allocated between LAE (line 3) and other expenses (line 5)

3. Initial obligation

a. Transition – initial adoption date of the accounting standard

b. Alternative treatments

1) Recognize the liability immediately

2) Amortize over a period up to twenty years

360 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

4. Subsequent periods

a. Accrual of costs for newly eligible or vested employees at the date of eligibility,

i.e., the estimated liability cost

b. Recognition of the interest cost of an obligation at the start of the period

c. Treatment of actuarial gains/losses from assumptions – immediate recognition

or amortization

1) Must recognize during the period if exceed 10% of the obligation or the

fair value of a plan's assets

2) If do not recognize, amortize over the average life expectancy of fully

vested and retiree groups

5. Plan assets

a. Segregate or restrict

b. Measure at fair value

c. Used to offset the accrued liability

C. Line 4 – Commission Payable, Contingent Commissions and Other Similar Charges

1. Agents and general agents

a. Contingent commissions may be based on

1) Profitability of the business produced

2) Persistency

3) Loss ratio developed

4) Other criteria

b. Agent receives a percentage of the net profit calculated as follows:

1) Agent's earned premium

2) Less incurred losses produced by his business

3) Less commissions (other than contingent)

4) Less policyholder dividends (the company's percentage)

5) Less overhead (the company's percentage)

c. Two variations

1) Graded contingent commission – agent's commission, the percentage

of which increases with profits

2) Growth contingent commission – agent's commission, the percentage

of which depends on both profitability and premium volume

d. Timing of the determination of a liability

1) On a calendar year basis for all agents

2) On a fiscal year basis on the anniversary date of the contract or the

agent's appointment

e. Additional allowances

1) Two types

a) Reimbursement of specific expenses

b) Award or bonus beyond contingent commission

2) Treatment

a) If premium based, include with contingent commissions

b) If not a percentage, included with other expenses (line 5)

AS–Page 3 361

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

2. Reinsurance commissions

a. General characteristics

1) Payment to the ceding company may reflect expense reimbursement or

both expenses and loss experience

2) Classified as commission, reducing acquisition expenses, even though

other expenses may be reimbursed

b. Straight profit contract – contract whose commission equals "a stipulated

percentage of the profits produced by the ceding company's business"

1) Calculated either on an annual basis or as a moving average

2) Calculation when cancellation

a) When contract terminated, runoff of the business before a final

calculation

b) When portfolio terminated, immediate calculation

c. Sliding scale contract – contract whose commission "depends largely on the

loss ratio or experience of the particular ceding company's business"

1) Most common arrangement

2) Provisional commission during the year with an adjustment at year end

3) Often limited by annual maximum and minimum with a carryover to the

next year if above or below the limiting ratios

4) Balance sheet treatment

a) As must reserve for any possible return commission during the

year, actual credit received or claimed limited to the minimum

b) At year end, must reserve for the carryforward and any

commission owed or due for the year

d. Guaranteed profit contract – contract that "usually includes a fixed

commission rate and a fixed reinsurer's fee or profit"

1) Very little risk to the reinsurer

a) Ceding company liable for losses that exceed the net premium

less a profit factor

b) Reinsurer must return the difference if losses less than the net

premium less the profit factor

2) Ceding company takes credit for commission only as earned

e. May show contingent commissions on a net basis, combining assumed and

ceded reinsurance

3. Company officers or management

a. Contract with a management group to manage a company in return for a

percentage of net written premium

1) Managers may pay all or part of general administrative expenses

2) In some cases, may not have payments reduced because of returns or

reinsurance

b. In some cases, payments based on the calendar year underwriting profit

362 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

D. Line 5 – Other Expenses (Excluding Taxes, Licenses and Fees)

1. Liabilities for all expenses listed in the Underwriting and Investment Exhibit –

Part 3 – Expenses, except

a. Claim adjustment services (line 1)

b. Commissions and brokerage – contingent (line 2)

c. Taxes, licenses and fees (line 20)

2. Represent general administrative expenses

E. Line 8 – Borrowed Money and Interest Thereon

1. Liabilities for loans other than loans secured by mortgages on a company's real estate

and surplus loans

2. Those secured by mortgages treated as reduction from asset values (Page 2, line 4)

3. Surplus loans

a. Money borrowed by mutual and cooperative insurers to satisfy capital and

surplus requirements

b. Treated as surplus

F. Line 10 – Advance Premiums

G. Line 11 – Dividends Declared and Unpaid

1. Stockholders (10a)

a. Usually paid in cash

b. If distributed as stock dividends, do not represent an actual distribution, but a

capitalization of part of unassigned surplus – no liability created

2. Policyholders (10b)

a. Paid either in cash or credit

b. If undeclared and merely anticipated, are a segregation of surplus

H. Line 12 – Ceded Reinsurance Premiums Payable (Net of Ceding Commissions)

I. Line 13 – Funds Held By Company Under Reinsurance Treaties

1. Listed in Schedule F – Part 3, column 19

2. Usually, by unauthorized companies as security for the payment of their obligations

3. Unauthorized reinsurers – "companies not authorized or licensed to do business in the

domiciliary state of the ceding company"

4. Cash or another highly liquid asset

5. Contract should stipulate whether to be applied against losses, unearned premium, or

both

6. Include premium balances withheld by a ceding company under a reinsurance contract

7. Reciprocal agreements with both sides holding security allows the offsetting of

payables against receivables

8. Funds held allow a company to take credit for amounts due from such reinsurers if

adequately secured

AS–Page 3 363

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

J. Line 14 – Amounts Withheld or Returned by Company for Account of Others

1. Deductions from employees or agents

a. Payroll taxes

b. Group insurance premiums

c. Pensions

d. Savings bonds

2. Policyholder or claimant funds

a. Uncashed or unclaimed checks

b. Premiums due another company

c. Policyholder taxes collected by the company

K. Line 15 – Remittance and Items Not Allocated

L. Line 16 – Provision for Reinsurance

1. Obtained from Schedule F – Part 7, line 6; known as the Schedule F penalty

2. Loss and unearned premium reserves are net of reinsurance (including unauthorized and

overdue)

3. But because insurance departments do not allow reduction of these reserves, an extra

liability must be created for premium and paid and unpaid losses due

4. But because the ceding company retains funds owned by or owed to the reinsurer, the

liability is reduced

M. Line 17 – Net Adjustments in Assets and Liabilities due to Foreign Exchange Rates

1. Involves the valuation of assets and liabilities maintained in a foreign country at year

end

2. Common to convert such assets or liabilities into U.S. dollars at the time of their

acquisition or incurrence and maintain this initial converted value as the book value

3. But because of currency fluctuations, this book value will differ from the real value and

thus an explicit adjustment is made based on the exchange rate published by the NAIC

4. Alternative to adjusting every individual asset

N. Line 18 – Drafts Outstanding

1. Draft-incurred basis

a. Not included in the regular issuance of checks so the bank balance has not yet

been reduced and thus a need for a reserve

b. Once issued, loss reserves reduced so no duplication of liability

c. Once cleared and accepted, this reserve reduced as well as assets

2. Draft-paid basis

a. Drafts recorded only when paid

b. No such liability for outstanding

c. Reduction in reserves and assets when cashed

3. Bank overdrafts reduce cash on Page 2

364 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

O. Line 19 – Payable to Parent, Subsidiaries and Affiliates

1. Expense reimbursement

2. Reflects services provided, e.g., data processing services

P. Line 20 – Derivatives

Q. Line 21 – Payable for Securities

1. Acquired prior to the statement date

2. Payment usually requires five days

R. Line 22 – Payable for Securities Lending

S. Line 23 – Liability for Amounts Held under Uninsured Accident and Health Plans

1. Administrative services or uninsured plans

2. Do not report income and disbursements under premium and losses

3. Funds held for such are liabilities

4. Comparable to but does not offset amounts receivable relating to uninsured A&H plans

(Page 2, line 17) as involve different plans

T. Line 24 – Capital Notes and Interest Thereon

1. Treated as capital for the RBC formula, though recorded as a balance sheet liability

2. Usually, no need for regulatory approval of principal or interest payments if capital and

surplus exceed a certain amount

U. Line 25 – Aggregate Write-Ins for Liabilities

(Details shown at bottom of Page 3)

1. Examples

a. Liability to return excess profits under a no-fault statute (MA)

b. Retroactive reinsurance – as company not able to offset loss and LAE reserves,

records as a negative liability

c. Reserve for uncashed checks if not included in line 14

d. General accounts payable

e. Unearned interest on premium notes

f. Liabilities for unexpired premiums on options

g. Agents' security fund reserve

h. Debt obligations of employee stock ownership plans, unless satisfied satisfy by

a source other than stock dividends, company contributions, or the

sale/exchange of company securities

2. Notes

a. Some are segregations of surplus

b. Many could be included in a larger category

V. Line 27 – Protected Cell Liabilities

AS–Page 3 365

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

II. CAPITAL AND SURPLUS

A. Overview

1. Initial financing ranges from 150,000 to $5M_

– minimum depends on

a. Lines of insurance to be written

b. Type of business organization

1) Stocks

a) Issue common and preferred stock

b) Control split between the board of directors and officers

2) Mutual surplus

a) No capital stock

b) Policyholders elect directors who appoint officers

c) Initial surplus may come from prospective policyholders, e.g.,

doctors organizing a medical malpractice company

d) Outside surplus contributions via interest bearing debentures

called guaranty fund certificates/surplus notes

i) Limited in their interest payments

ii) Must be evidenced by a written agreement approved by

the insurance commissioner

iii) Must not repay until excess surplus

e) Outside sources may also provide guaranty capital

i) Issued with a stated par value

ii) Also must not be repaid until have excess surplus

iii) If dissolution, can only be paid after the company has

paid its policy obligations, but holders of such take

preference over members

f) Demutualization – formation of a mutual holding company to

issue capital stock whose proceeds purchase less than a

majority of the mutual's voting rights

3) Reciprocals – "voluntary unincorporated business created to write

insurance for its subscribers," who insure each other and are both

policyholders and owners

a) Managed by an attorney-in-fact, which may be incorporated

b) Compensation to the attorney-in-fact is a percentage of

premiums

c) Attorney-in-fact normally provides initial financing in

exchange for

i) Debentures

ii) Surplus notes

iii) Guaranty fund notes

iv) Certificates of contribution

d) States regulate surplus

366 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

2. Ongoing financial requirements

a. Less than that required to obtain a certificate of authority

1) Initial surplus includes working capital for commencing business

2) Subtract unassigned surplus deficits from the original surplus

b. Components

1) Paid-in or contributed surplus for stocks

2) Guaranty fund surplus for mutuals

3) Subordinated surplus debentures, notes, or similar instruments

4) Certificates representing shares

5) Deposit and escrow requirements

6) Fractional shares

7) Liability of subscribers and shareholders for unpaid shares

8) Shareholders' preemptive rights

9) Organizational expenses and liability of incorporation

10) Treasury stock (reduction)

11) Unassigned funds (surplus)

c. Capital or surplus impairment – situation when assets less liabilities are less

than a prescribed amount

1) Statutes vary by state

2) Regulators usually issue a notice that correction is required

3) May require

a) New capital stock

b) Surplus or contribution notes

c) Subordinated dividends

d) Contribution to paid-in surplus

d. Insurers also required to satisfy risk-based capital (RBC) formula

1) Includes asset, credit, premium, and reserve risks

2) Insurer to file RBC supplement with the NAIC

3) Leads to issuance of capital notes

B. Line 29 – Aggregate Write-Ins for Special Surplus Funds

(Details shown at bottom of Page 3)

1. Transfer from unassigned surplus for special purposes to prevent the funds being

available for dividends

2. Also referred to as voluntary reserves

3. Reasons for segregation

a. Security fluctuations

b. Potential income taxes on unrealized capital gains

c. Policyholder dividends not yet declared

d. Extraordinary underwriting losses that may occur

e. Contingent assessments by state insolvency guaranty funds

f. Other types of contingencies

AS–Page 3 367

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C. Lines 30 and 31 – Capital Stock

Line 30 – Common capital stock

Line 31 – Preferred capital stock

1. Amount of initial capitalization and later changes in par values

2. Amount equals the number of common shares outstanding times the par (stated) value

3. No entries for a mutual company

D. Line 32 – Aggregate Write-Ins for Other than Special Surplus Funds

E. Line 33 – Surplus Notes

1. Includes subordinated surplus debentures as states may permit stock or mutual to

borrow

2. Characteristics

a. Incurred to meet minimum surplus requirements

b. Strict control by the domiciliary state as to interest rates and repayments

c. Subordinated to all other obligations

d. Must have stockholders approval if a stock company

F. Line 34 – Gross Paid In and Contributed Surplus

1. Dollars received from an initial sale of stock that differs from the par or stated value

2. Dollars received from the sale of treasury stock that differs from the par or stated value

3. No entries for a mutual company

G. Line 35 – Unassigned Funds (Surplus)

368 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

H. Line 36 – Less Treasury Stock at Cost

Line 36.1 Shares common

Line 36.2 Shares preferred

1. Treasury stock – stock "issued, fully paid for and subsequently reacquired" and held

for reissuance or cancellation

2. Restrictions on it vary by state

a. Amount held may be limited by law

b. Necessary conditions in some states

1) Only when net assets are greater than the paid-up capital and required

surplus, excluding the portion attributable to the unrealized

appreciation in the value or revaluation of assets and the increase

attributable to the surrender of the company's own shares

2) Only with regulatory permission

3) Only if approved by the directors or stockholders

c. Purposes not requiring approval by the directors or stockholders

1) Redemption of shares at a cost not to exceed the redemption price

2) Elimination of fractional shares

3) Collection or compromise of debt to the corporation

4) Payment to entitled dissenting shareholders

3. Reduces outstanding shares and surplus, but does not affect the number of total shares

issued or the amount of paid-in capital

4. If reissue stock at other than the repurchase cost, increase or reduce paid-in surplus

5. If cancel stock, must reflect this by reducing lines 36.1, 36.2, and 37 and reflecting on

Page 4, line 36 and 38

6. No entries for a mutual company

I. Line 37 – Surplus as Regards Policyholders

1. Sum of lines 29–35 less line 36

2. Includes mutual or reciprocal guaranty funds, guaranty capital, and accrued interest

AS–Page 3 369

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

PAST CAS EXAMINATION QUESTIONS

A. Liabilities: Accounts Payable, Accrued Liabilities, and Banking Items

A1. List two expense items that must be separately reserved because they are generally paid after policy

termination and are thus not covered by the unearned premium reserve. (77–7–38–1) A2. Loans secured by mortgages on company real estate are included as borrowed money in Page 3 –

Liabilities, Surplus and Other Funds. (78–7–31–1) A3. To provide for a more uniform reporting of liabilities frequently written in, the caption, drafts

outstanding, has been provided in the 1978 Annual Statement. (79–7–2–1) A4. Liability for agent reimbursement for administrative expenses that is paid as a percentage of premium is

considered contingent commission and entered on line 4, Page 3 of the Annual Statement. (80–7–2–1) A5. For reinsurance contracts that provide for contingent commissions, the NAIC requires the ceding

company to carry as a liability the maximum possible return commission. (80–7–3–1) A6. Under a sliding scale reinsurance arrangement, additional commission accrued on the basis of favorable

loss experience is a nonadmitted asset for the ceding company. (82–7–13–1) A7. Loans secured by mortgages on company real estate are reflected in the Annual Statement as a reduction

to the asset value of real estate. (85–7–8–.5) A8. The liability, contingent commission and other similar charges on Page 3 of the Annual Statement, can

reflect obligations related to which of the following? 1. Agents and general agents 2. Reinsurance agreements 3. Company officers A. 1,2 B. 1,3 C. 2,3 D. 1,2,3 E. None of these answers is correct. (85–7–23–1) A9. a. Contrast drafts-paid loss accounting and drafts-issued loss accounting.

b. What are the expected changes in the IBNR reserve, the reserve for reported claims, and the total reserve for a company that changes from a drafts-paid to a drafts-issued loss accounting basis? (85–7–49–1/2)

A10. According to Bell, liabilities for loans secured by mortgages on company real estate are included on line

8, borrowed money, of the Statement of Liabilities, Surplus and Other Funds. (87–7–23–MC)

A11. According to Bell, the corresponding case reserve always should be reduced when a paid loss draft is issued if the company records the draft outstanding as a liability. (87–7–23–MC)

A12. It is possible for an insurer to report negative net commission expenses consistently over time.

(94–7–16–.5) A13. A bonus based on realized profit paid to company officers under a management contract would appear

on Annual Statement Page 3, line 4, contingent commissions and other similar charges. (99–7B–5–.5)

370 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

A1. 1) Loss adjustment expenses (Page 3, line 3) 2) Contingent commissions (Page 3, line 4), pp. 5–1 to 5–3.

A2. F, pp. 5–5, 5–6 – They are "treated as a reduction from the asset value of the real estate." A3. T, p. 5–6 – They are included in Page 3, line 8. A4. T, p. 5–3. A5. F, p. 5–3 – For the ceding company, it is a reduction of commission expense, not a liability. A6. F, p. 5–4 – The ceding company may take credit for such. A7. T, pp. 5–5, 5–6. A8. 1. T, p. 5–2 2. T, p. 5–3 3. T, p. 5–4 Answer: D A9. a. Drafts-paid accounting requires that the draft issued is presented to the bank before funds are

transferred from the company's operating account to the bank. When the draft is issued, the draft payable liability is increased and when it is received, this liability is reduced. Drafts-issued accounting would treat drafts as if they were checks. Their issuance would represent a direct outgo, a charge to income as a loss paid.

b. There should be no change in the IBNR reserve since these have not entered the system. The

reserve for reported claims will be lower under the drafts-issued system as claims are classified as paid (and thus subtracted from the reserve) at an earlier date. The total reserve will also be lower under the drafts-issued system as there is no change to the IBNR reserve and the reserve for reported claims is lower, p. 5–6.

A10. F, pp. 5–5, 5–6 – These are "treated as a reduction from the asset value of the real estate." A11. T, p. 5–6 – Although the reference is to a paid loss draft, this describes a company using drafts

outstanding, which initially shifts the liability from case reserves to an account including such drafts.

A12. T, p. 5–3 – Reinsurance commissions may include the reimbursement of other expenses.

A13. T, p. 5–5.

AS–Page 3 371

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

A14. The Insurance Accounting and Systems Association's Property-Casualty Insurance Accounting addresses the impact of contingent commission contracts on the annual statement. Using the information below, calculate the impacts of the following contingent commission contract on lines 4, 5, and 6 of Page 3 of the 2001 Annual Statement.

Annual Statement, Page 3, Liabilities, Surplus and Other Funds

Line 4 Commission payable, contingent commission and other similar charges Line 5 Other expenses (excluding taxes, licenses and fees) Line 6 Taxes, licenses and fees (excluding federal and foreign income taxes)

Contingent Commission Contract Details i) If the agent's business results in a fiscal year ending November 30, 2001 loss ratio is less than

55%, the agent earns contingent commission equal to 2% of direct written premium. ii) The contingent commission agreement calls for a bonus of $25,000 if the agent's fiscal year

ending November 30, 2001 direct written premium is greater than $5,000,000. iii) Contingent commission earned is paid in two installments: 60% is paid December 31, 2001, the

remaining 40% is paid June 15, 2001.

Agent's Results for Fiscal Year Ending November 30, 2001 i) Direct written premium equals $7,500,000. ii) Calendar year loss ratio equals 50%. (00–7US–87–1.25) (00–7C–78–1.25)

A15. Small Town Insurance Agency has recently negotiated an agreement with Never Pay Insurance

Company. Under the agreement, Never Pay Insurance Company pays Small Town a flat 10% commission as well as a contingent commission of 30% of the profits generated by Small Town's business. Given the following assumptions and assuming no payments (loss or expense) have been made, calculate the incremental change to line 4, contingent commissions and other similar charges, on Page 3, Liabilities, of Never Pay Insurance Company's Annual Statement as a result of this agreement. Show all work.

Earned premium $1,000,000 Expected loss ratio 60% of earned premium Loss adjustment expense 8% of earned premium Other expenses 15% of earned premium

(02–7US–67–1.5) A16. Describe three types of reinsurance commission clauses that are often part of a reinsurance contract.

(05–7C–42b–.75)

372 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

A14. Contingent commissions that are a percentage of premium are included on Page 3, line 4. Ones that are flat amounts are included on Page 3, line 5. Page 3, line 6 is unaffected. Only 40% of the contingent commissions are unpaid as of year end. Thus we get:

Line 4: (.02)(7.5M

_ )(.40) = 60,000

Line 5: (25,000)(.40) = 10,000 Line 6: 0, pp. 5–2, 5–3.

A15. Contingent commissions that are a percentage of premium are included on line 4, Page 3. Ones that are

flat amounts are included on line 5, Page 3. Thus we get:

(.30)(1M_

)(1 .60 .08 .15 .10) = 21,000, pp. 5–2, 5–3.

A16. 1) Straight profit – The primary insurer receives a specified percentage of its reinsurer's profit. 2) Sliding scale – The primary insurer receives a commission that is related to the loss ratio or

experience of the ceded business, usually subject to a minimum and maximum. 3) Guaranteed profit – The primary insurer initially receives a commission based on a fixed rate

but the reinsurer is guaranteed a fixed profit. The primary insurer thus gains when losses are less than expected but loses when losses are greater than expected, pp. 5–3, 5–4.

AS–Page 3 373

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

B. Liabilities: Reinsurance and Miscellaneous

B1. Funds held or retained by a company for the account of an unauthorized reinsurer is included as a Page

2 asset, funds held by or deposited with ceding reinsurers. (77–7–5–MC)

B2. Net adjustments in assets and liabilities attributable to foreign exchange rates is shown on Page 3 of the

Annual Statement. (77–7–6–1) B3. The Annual Statement reserve for unpaid dividends generally includes a provision for anticipated but

undeclared dividends. (78–7–24–1) B4. With respect to expired policies, policyholder dividends that can be reasonably estimated from historical

experience but have not been declared by the board of directors can be reflected as a liability on Page 2 of the Annual Statement. (79–7–11–1)

B5. Your company withholds $100,000 of the premium balances due ABC Reinsurance Company,

representing unearned premiums and outstanding losses on business ceded to ABC. Your company would include this amount in its asset item, funds held by or deposited with reinsured companies. (80–7–20–1)

B6. If a payment on a mortgage loan to an insurance company includes an amount for real estate taxes not

yet due, then the insurer should include this portion of the payment in the liability account, amounts withheld or retained by company for account of others. (84–7–1–.5)

B7. The liability, dividends declared and unpaid to stockholders on Page 3 of the Annual Statement,

includes cash and stock dividends. (85–7–10–.5) B8. A liability should be established in the Annual Statement for declared but unpaid stockholder cash

dividends. (86–7–3–.5) B9. Net foreign assets are adjusted by the applicable rates of exchange prevailing at the statement date.

(86–7–21–MC) B10. Deferred taxes are not recognized under SAP. (96–7US–35–MC)

B11. You are given the following information from company X as of December 31, 1998.

Loss and LAE reserves 600 Reinsurance recoverable on loss payments 40 Unearned premium reserves 100 Mortgage loan on home office 45 Current federal income taxes 55 Deferred federal income taxes 25

What are company X's liabilities under Statutory Accounting Principles?

A. < $725 B. ≥ $725 but < $750 C. ≥ $750 but < $775 D. ≥ $775 but < $800 E. ≥ $800 (99–7US–20–1) B12. According to the Insurance Accounting and Systems Association's Property-Casualty Insurance

Accounting, ceded losses under a loss portfolio transfer are recorded as a negative liability. (01–7US–34–.5)

374 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

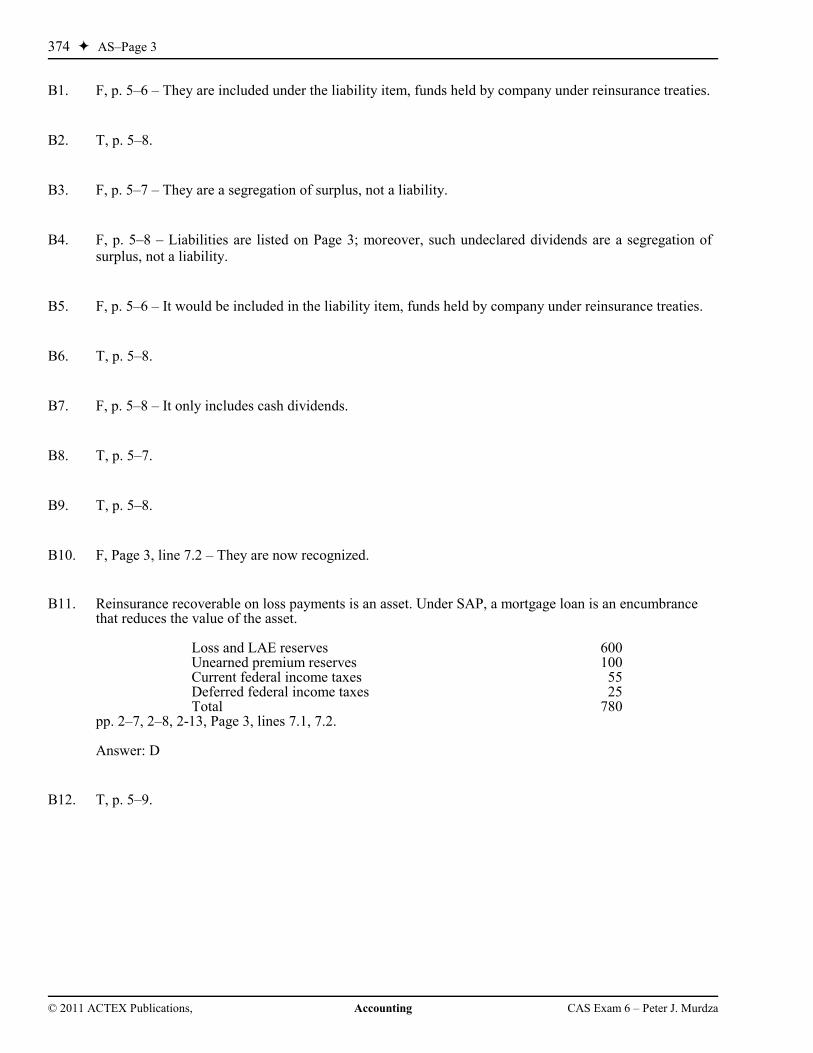

B1. F, p. 5–6 – They are included under the liability item, funds held by company under reinsurance treaties. B2. T, p. 5–8. B3. F, p. 5–7 – They are a segregation of surplus, not a liability. B4. F, p. 5–8 – Liabilities are listed on Page 3; moreover, such undeclared dividends are a segregation of

surplus, not a liability. B5. F, p. 5–6 – It would be included in the liability item, funds held by company under reinsurance treaties. B6. T, p. 5–8. B7. F, p. 5–8 – It only includes cash dividends. B8. T, p. 5–7. B9. T, p. 5–8. B10. F, Page 3, line 7.2 – They are now recognized. B11. Reinsurance recoverable on loss payments is an asset. Under SAP, a mortgage loan is an encumbrance

that reduces the value of the asset. Loss and LAE reserves 600 Unearned premium reserves 100 Current federal income taxes 55 Deferred federal income taxes 25 Total 780

pp. 2–7, 2–8, 2-13, Page 3, lines 7.1, 7.2. Answer: D

B12. T, p. 5–9.

AS–Page 3 375

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

B13. Given the following information from the 2003 Annual Statements of two reinsurers, ABC and XYZ, answer the following questions. Assume the companies are similar in line of business and geographic mix.

Reinsurer Reinsurer ABC ($000) XYZ ($000) Assets Bonds 15,000 20,000 Common stock (nonaffiliated) 0 5,000 Cash 5,000 5,000 Total invested assets 20,000 30,000 Agents balances or uncollected premiums 2,500 5,000 Funds held by or deposited with reinsured companies 10,000 0 Reinsurance recoverable on loss and LAE payments 5,000 2,500 EDP equipment 1,000 0 Total assets 38,500 37,500 Liabilities Loss reserves 15,000 10,000 LAE reserves 5,000 1,000 Contingent commissions 1,000 500 Unearned premium reserves 5,000 6,000 Provision for reinsurance 0 5,000 Ceded reinsurance balances payable 1,000 2,500 Total liabilities 27,000 25,000 Policyholders surplus 11,500 12,500

a. Compare and contrast the two companies with respect to reserve leverage. b. Compare and contrast the two companies with respect to reinsurance items. c. Which company has the stronger balance sheet? Explain your answer. (04–7US–57c-e–1ea.)

376 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

B13. a. ABC's ratio of loss and LAE reserves to surplus is higher reflecting a greater risk:

RatioABC = 15,000 + 5,000

11,500 = 1.74

RatioXYZ = 10,000 + 1,000

12,500 = .88

b. ABC is owed money from companies it reinsures. Such companies hold 10,000 of ABC's funds

(funds held or deposited with reinsured companies), whereas it owes such companies 1,000 (ceded reinsurance balances payable) for a net amount of 9,000, which is almost equal to its surplus of 11,500. XYZ, on the other hand, owes money to the companies it reinsures. Such companies hold none of ABC's funds, whereas it owes such companies 2,500.

In regard to ceded reinsurance, ABC has a positive balance. Assuming companies owe ABC

5,000 (reinsurance recoverable on loss and LAE payments) and there is no provision for reinsurance. XYZ, on the other hand, has a negative balance. Assuming companies owe XYZ

2,500 and there is 5,000 for a provision for reinsurance for a net amount of 2,500, pp. 2–11 to 2–13, 5–6, 5–7.

c. Because of its lower ratio of loss and LAE reserves to surplus, XYZ has the stronger balance

sheet. In addition, the provision for reinsurance results from a specific NAIC formula and may not reflect collectibility problems. If there are no such problems, XYZ's position is even stronger, Feldblum, "Schedule F," pp. 13, 43.

AS–Page 3 377

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C. Surplus

C1. From the following information, calculate total assets, total liabilities, and net worth on a statutory

basis. Your answer may be presented in algebraic form, using the alphabetic labels for each item. a. Loss and loss expense reserves $70,000,000 b. Other expense and tax reserves 4,000,000 c. Federal income tax reserves 2,000,000 d. Unearned premium reserves 60,000,000 e. Agents' balances or uncollected premiums 25,000,000 f. Bonds 100,000,000 g. Stocks 75,000,000 h. Real estate 5,000,000 i. Cash and bank deposits 2,000,000 j. Funds held or retained by company for reinsurance in unauthorized companies 100,000 k. Ceded reinsurance balances payable 500,000 l. Funds held by or deposited with reinsured companies 1,000,000 m. Amounts recoverable from reinsurers 300,000 n. Unearned premiums on reinsurance in unauthorized companies 100,000 o. Reinsurance on paid and unpaid losses due from unauthorized companies 200,000 p. Dividends declared and unpaid to stockholders 300,000 q. Other admitted assets 6,000,000 r. Other liabilities 1,500,000 (71–7–8–9) C2. Develop a formula for surplus as regards policyholders on a statutory basis using the letter references of

the following items: a. Funds held by company for account of unauthorized companies b. Reserve for unpaid losses and LAE c. Purchase price of currently owned stocks and bonds d. Cash on deposit in banks e. Company reserve for future catastrophe losses f. Paid-up capital g. Balances owed to company by its agents for less than 90 days h. Market value of stocks owned at year end i. Amortized value of bonds held at year end j. Dividends paid to policyholders k. Reserve for unpaid expenses (excluding LAE) l. Dividends declared and unpaid m. Reinsurance due from unauthorized companies n. Unearned premium reserve. (75–7–6–5) C3. Describe two types of funds shown by some insurers as special surplus funds and explain why insurers

may elect to segregate moneys into such funds. (77–7–47–2) C4. The initial capital and surplus requirements of an insurance company are generally greater than the

requirements after organization. (83–7–20–.5) C5. The XYZ Insurance Company had 750,000 shares of common stock, at $10 par value, outstanding at

December 31, 1981. In May 1982, XYZ issued 250,000 additional shares, also at $10 par value, all of which sold at $12 per share. In October 1982, the company issued a 100% stock dividend. What effects do these transactions have on Pages 2 and 3 of the Annual Statement? (83–7–55–2)

378 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C1. Total Admitted Assets (Page 2, line 28) = Bonds (line 1) + Stocks (line 2) + Real Estate (line 4) + Cash and Short-Term Investments (line 5) + Uncollected Premiums and Agents' Balances (line 15.1) + Amounts Recoverables from Reinsurers (line 16.1) + Funds Held by or Deposited with Reinsured Companies (line 16.2) + Other Admitted Assets (other lines)

TAA = f + g + h + i + e + l + m + q Provision for Reinsurance = Reinsurance on Paid and Unpaid Losses Recoverable from Unauthorized Companies + Unearned Premiums on Reinsurance in Unauthorized Companies Funds Held or Retained by Company for Account of Such Unauthorized Companies = o + n j Total Liabilities (Page 3, line 28) = Losses and Loss Adjustment Expenses (lines 1 & 3) + Other Expenses and Taxes, Licenses and Fees (lines 5 & 6) + Federal and Foreign Income Taxes (line 7) + Unearned Premiums (line 9) + Dividends Declared and Unpaid (line 11) + Ceded Reinsurance Premiums Payable (line 12) + Funds Held by Company under Reinsurance Treaties (line 13) + Provision for Reinsurance (line 16) + Other Liabilities (other lines) TL = a + b + c + d + p + k + j + (o + n j) + r

Statutory Net Worth (Page 3, line 37) = Total Admitted Assets Total Liabilities Note that item k is included as a subtraction in agents' balances, which is on a net basis, p. 5–7; Pages 2–3. C2. Total Admitted Assets (Page 2, line 28) = Bonds (line 1) + Stocks (line 2) + Cash and Short-Term

Investments (line 5) + Uncollected Premiums and Agents' Balances (line 15.1) TAA = i + h + d + g Provision for Reinsurance = Reinsurance Due from Unauthorized Companies Funds Held by

Company for Account of Unauthorized Companies PFR = (m a)*

Total Liabilities (Page 3, line 28) = Losses and LAE (lines 1 & 3) + Other Expenses and Taxes, Licenses and Fees (lines 5 & 6) + Unearned Premiums (line 9) + Dividends Declared and Unpaid (line 11) + Funds Held by Company under Reinsurance Treaties (line 13) + Provision for Reinsurance (line 16) TL = b + k + n + l + a + (m a)* Surplus as Regards Policyholders (Page 3, line 37) = Total Admitted Assets Total Liabilities

* Disregard if negative. Items e and f reflect segregations of surplus, and item j reflects a prior outgo, not a current asset or liability, pp. 5–7, 5–10, 5–14; Pages 2–3.

C3. Special surplus funds include: 1) a reserve for the excess of admitted values over market value of assets, 2) a reserve for taxes on unrealized gain, 3) a reserve for undeclared policyholder dividends, 4) a reserve for extraordinary underwriting losses, and 5) a reserve for contingent assessments by insolvency guaranty funds. Insurers may elect to create such reserves to restrict the amount of money available for stockholder or policyholder dividends, pp. 5–13, 5–14.

C4. T, p. 5–11. C5. The issuance of the stock dividend transfers 10M

_ from unassigned funds to capital.

Page 2, line 5 Cash 5/82 Add 3.0M

_

Page 3, line 30 Common capital stock 5/82 Add 2.5M_

Page 3, line 34 Gross paid-in and contributed surplus 5/82 Add .5M

_

Page 3, line 37 Surplus as regards policyholders 5/82 Add 3.0M_

Page 3, line 30 Common capital stock 10/82 Add 10M

_

Page 3, line 35 Unassigned funds (surplus) 10/82 Subtract 10M_

pp. 5–7, 9–13; Pages 2–3.

AS–Page 3 379

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C6. Money borrowed to satisfy statutory capital and surplus requirements is reported as part of the liability, borrowed money, on Page 3 of the Annual Statement. (85–7–4–.5)

C7. When a company acquires treasury stock, there is a reduction in the number of shares outstanding and in

total statutory surplus, but there is no effect on paid-in capital. (85–7–5–.5) C8. Smith and Jones organized a new stock insurance firm, which had minimum initial capital requirements

of one million dollars. They planned to issue 20,000 shares at a par value of $50 each, but the shares were actually sold as follows: the first 10,000 at $50 each, the next 5,000 at $55 each and the last 5,000 at $60 each. What entries on Page 3 of the Annual Statement would be affected, and by how much? (85–7–36–2)

C9. Statutory accounting requires that any value received from the sale of treasury stock in excess of its cost

be treated as a realized capital gain. (87–7–18–.5) C10. According to Property-Casualty Insurance Accounting, the state requirements for policyholder surplus

are usually less strict for the newly organized insurer than for one already in existence. (93–7–17–.5) C11. Treasury stock is shown on the balance sheet of the NAIC Annual Statement as a positive contribution

to surplus. (93–7–46–MC) C12. According to the IASA accounting text, state laws require a minimum amount of policyholder surplus

for a new insurer. Upon what two factors is this minimum dependent? (96–7B–68–1) C13. According to the IASA accounting text, how are estimates of undeclared dividends to policyholders

reported in the Annual Statement?

A. As dividends paid to policyholders on the Cash Flow Exhibit B. As a liability on Page 3 C. As dividends to policyholders on the statement of income D. As appropriated surplus (special surplus funds) on Page 3 E. The undeclared dividends are not reported in any of these locations. (98–7B–29–1)

C14. Overcap lnsurance Company has just repurchased 10,000 shares of its common stock at $10 per share.

You are given the following information immediately prior to the repurchase:

Outstanding shares of common stock 100,000 Paid-in capital $1,000,000 Issued shares of common stock 100,000 Total policyholder surplus $5,000,000

Which of the following statements are true immediately after the repurchase?

1. The number of outstanding shares is 90,000. 2. Paid-in capital is $900,000. 3. Policyholder surplus is $4,900,000.

A. 1 B. 2 C. 1,3 D. 2,3 E. 1,2,3 (98–7B–32–1) C15. In the Annual Statement, Page 3, line 29, aggregate write-ins for special surplus funds denotes liabilities

of the company. (99–7B–15–.5) C16. According to the Insurance Accounting and Systems Association's Property-Casualty Insurance

Accounting, special surplus funds restrict the amount of funds available for stockholder dividends. (00–7US–23–.5) (00–7C–37–.5)

380 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C6. F, p. 5–14 – Substitute "surplus" for "the liability, borrowed money." C7. T, p. 5–12. C8. Assume all the issued stock is common stock. Line 30 – Common capital stock shows the par value of stock, i.e., 1M

_ .

Line 34 – Gross paid-in and contributed surplus shows the difference between the par and sale values,

i.e., (55 60)(5,000) + (60 50)(5,000) = 75,000, p. 5–10. C9. F, p. 5–12 – Substitute "additional paid-in surplus" for "a realized capital gain." C10. F, p. 5–11 – Substitute "more" for "less." C11. F, p. 5–12 – Substitute "negative" for "positive." C12. It depends on "the type of business being formed (generally stock, mutual or reciprocal), and the lines of

insurance to be written," p. 5–9. C13. D, pp. 5–8, 5–14. C14. 1. T, p. 5–12 – The number of outstanding shares is reduced.

2. F, p. 5–12 – This does not change. 3. T, p. 5–12 – Policyholder surplus is reduced. Answer: C

C15. F, p. 5–14 – "segregations of surplus" for "liabilities of the company." C16. T, p. 5–14.

AS–Page 3 381

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C17. According to the Insurance Accounting and Systems Association's Property-Casualty Insurance Accounting, special surplus funds restrict the amount of funds available for policyholder dividends. (00–7US–24–.5) (00–7C–38–.5)

C18. Which of the following is not reflected in statutory policyholders' surplus? A. Unassigned funds B. Special surplus funds C. Surplus notes D. Treasury stock

E. Each of the above is reflected in statutory policyholders' surplus. (01–6–24–1) C19. During 2000, ABC Insurance Corporation reissued 100 shares of treasury stock for $50 a share. The par

value of the stock is $1 per share. ABC reacquired the stock in 1999 for $40 a share. Describe how this transaction impacts the various line items on Pages 2 and 3 of ABC Insurance Corporation's 2000 Annual Statement. Ignore all tax issues. (01–7US–81–1.25) (01–7C–76–.5/1)

C20. The following information includes all assets and liabilities for an insurance company. Use this

information to answer the questions below.

Amortized Cost ($000s) Actual Cost ($000s) Fair Market ($000s) Class 1 bonds 1,000 8,000 1,200 Class 2 bonds 500 600 400 Class 3 bonds 700 650 600 Class 6 bonds 200 150 250 Common stock n/a 700 1,000

Other Information ($000)

Loss reserve 2,000 Loss adjustment expense reserve 400 Cost of building and land 10,000 Depreciation of building/land 400 Total uncollected premium 400 Mortgage loan on building/land 5,600 Cash 200 Uncollected premium 31–90 days past due 250 EDP equipment 100 Uncollected premium > 90 days past due 50 Office furniture 50 Funds held with reinsured companies 1,200 Provision for reinsurance 700 Reinsurance payable on paid Losses 100 Treasury stock 900 Unearned premium reserve 750

a. Calculate the value of bonds held by the company as it would appear on the asset page of the

Annual Statement. Show all work. b. Calculate the value of real estate as it would appear on the asset page of the Annual Statement.

Show all work. c. Calculate total net admitted assets as it would appear on the asset page of the Annual Statement.

Show all work. d. Calculate policyholder surplus as it would appear on the liabilities, surplus and other funds page

of the Annual Statement. Show all work. (07–7US–26–1/.5/1.5/1.5)

382 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

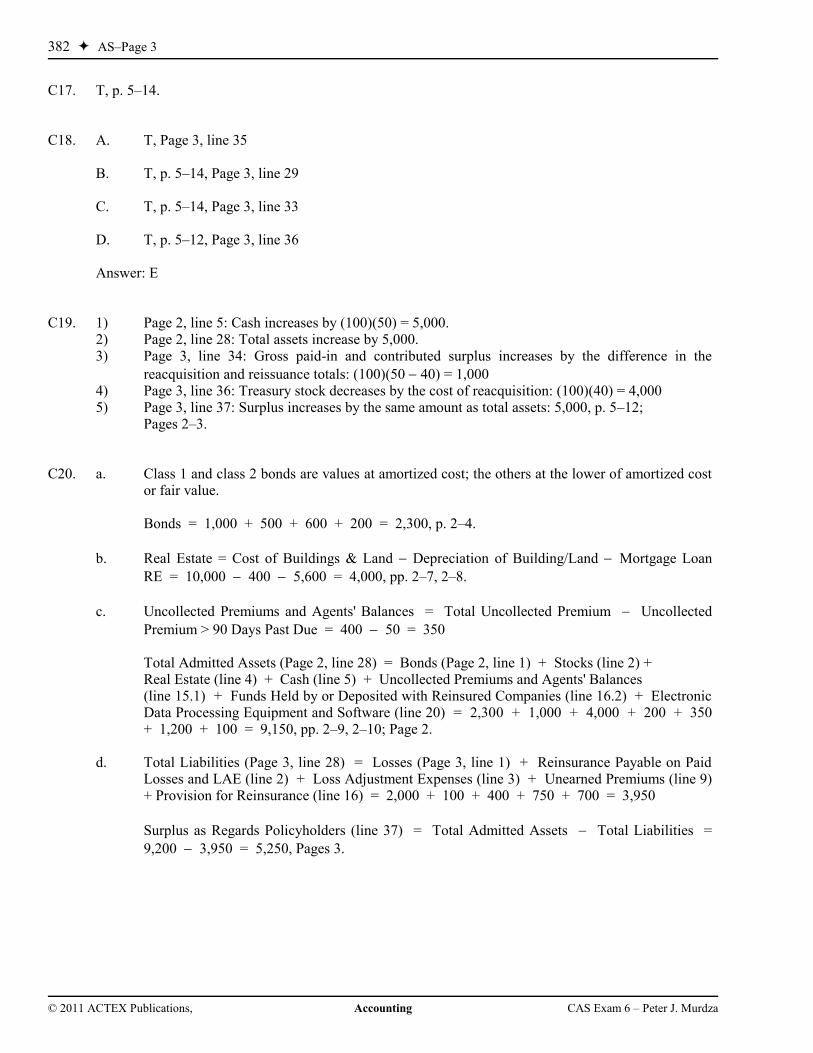

C17. T, p. 5–14. C18. A. T, Page 3, line 35

B. T, p. 5–14, Page 3, line 29 C. T, p. 5–14, Page 3, line 33 D. T, p. 5–12, Page 3, line 36

Answer: E

C19. 1) Page 2, line 5: Cash increases by (100)(50) = 5,000.

2) Page 2, line 28: Total assets increase by 5,000. 3) Page 3, line 34: Gross paid-in and contributed surplus increases by the difference in the

reacquisition and reissuance totals: (100)(50 40) = 1,000 4) Page 3, line 36: Treasury stock decreases by the cost of reacquisition: (100)(40) = 4,000 5) Page 3, line 37: Surplus increases by the same amount as total assets: 5,000, p. 5–12;

Pages 2–3. C20. a. Class 1 and class 2 bonds are values at amortized cost; the others at the lower of amortized cost

or fair value. Bonds = 1,000 + 500 + 600 + 200 = 2,300, p. 2–4.

b. Real Estate = Cost of Buildings & Land Depreciation of Building/Land Mortgage Loan

RE = 10,000 400 5,600 = 4,000, pp. 2–7, 2–8.

c. Uncollected Premiums and Agents' Balances = Total Uncollected Premium Uncollected

Premium > 90 Days Past Due = 400 50 = 350 Total Admitted Assets (Page 2, line 28) = Bonds (Page 2, line 1) + Stocks (line 2) +

Real Estate (line 4) + Cash (line 5) + Uncollected Premiums and Agents' Balances (line 15.1) + Funds Held by or Deposited with Reinsured Companies (line 16.2) + Electronic Data Processing Equipment and Software (line 20) = 2,300 + 1,000 + 4,000 + 200 + 350 + 1,200 + 100 = 9,150, pp. 2–9, 2–10; Page 2.

d. Total Liabilities (Page 3, line 28) = Losses (Page 3, line 1) + Reinsurance Payable on Paid

Losses and LAE (line 2) + Loss Adjustment Expenses (line 3) + Unearned Premiums (line 9) + Provision for Reinsurance (line 16) = 2,000 + 100 + 400 + 750 + 700 = 3,950

Surplus as Regards Policyholders (line 37) = Total Admitted Assets Total Liabilities =

9,200 3,950 = 5,250, Pages 3.

AS–Page 3 383

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

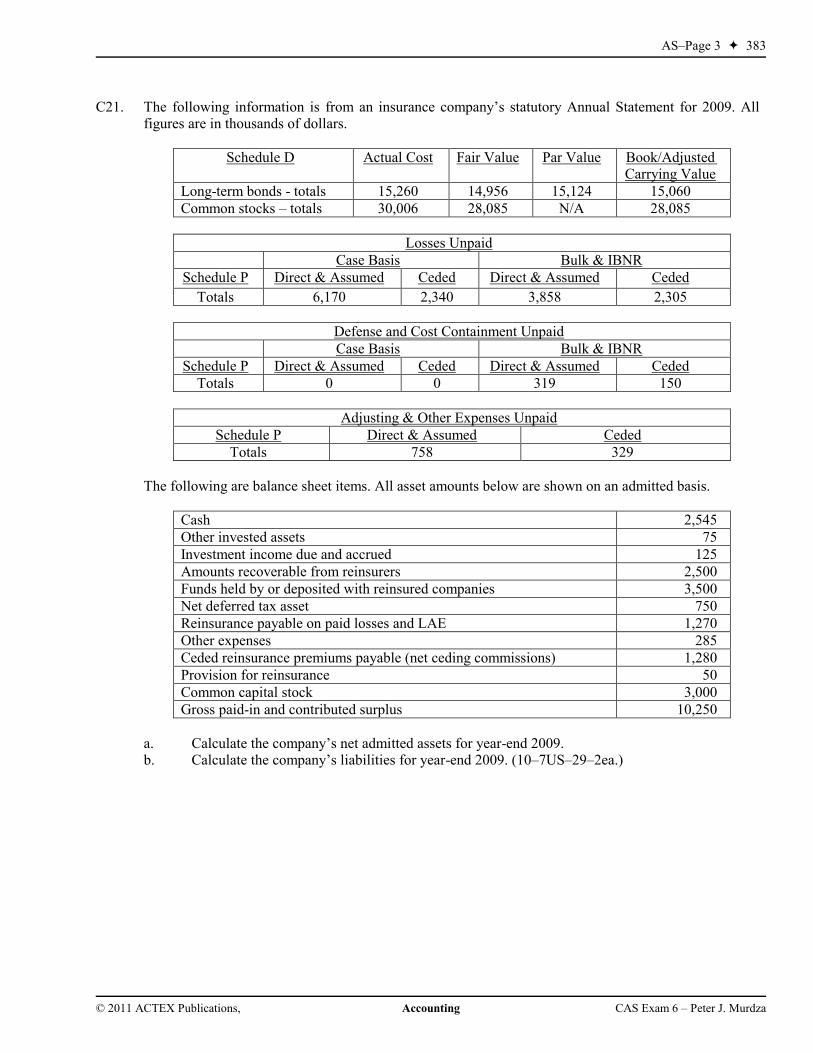

C21. The following information is from an insurance company’s statutory Annual Statement for 2009. All

figures are in thousands of dollars.

Schedule D Actual Cost Fair Value Par Value Book/Adjusted Carrying Value

Long-term bonds - totals 15,260 14,956 15,124 15,060

Common stocks – totals 30,006 28,085 N/A 28,085

Losses Unpaid

Case Basis Bulk & IBNR

Schedule P Direct & Assumed Ceded Direct & Assumed Ceded

Totals 6,170 2,340 3,858 2,305

Defense and Cost Containment Unpaid

Case Basis Bulk & IBNR

Schedule P Direct & Assumed Ceded Direct & Assumed Ceded

Totals 0 0 319 150

Adjusting & Other Expenses Unpaid

Schedule P Direct & Assumed Ceded

Totals 758 329

The following are balance sheet items. All asset amounts below are shown on an admitted basis.

Cash 2,545

Other invested assets 75

Investment income due and accrued 125

Amounts recoverable from reinsurers 2,500

Funds held by or deposited with reinsured companies 3,500

Net deferred tax asset 750

Reinsurance payable on paid losses and LAE 1,270

Other expenses 285

Ceded reinsurance premiums payable (net ceding commissions) 1,280

Provision for reinsurance 50

Common capital stock 3,000

Gross paid-in and contributed surplus 10,250

a. Calculate the company’s net admitted assets for year-end 2009. b. Calculate the company’s liabilities for year-end 2009. (10–7US–29–2ea.)

384 AS–Page 3

© 2011 ACTEX Publications, Accounting CAS Exam 6 – Peter J. Murdza

C21. a. Bonds are valued at book/adjusted carrying value and stocks at fair value. Total Admitted Assets (Page 2, line 28) = Bonds (Page 2, line 1) + Stocks (line 2) + Cash

(line 5) + Other Invested Assets (line 8) + Investment Income Due and Accrued (line 14) + Amounts Recoverable from Reinsurers (line 16.1) + Funds Held by or Deposited with Reinsured Companies (line 16.2) + Net Deferred Tax Asset (line 18.2) = 15,060 + 28,085 + 2,545 + 75 + 125 + 2,500 + 3,500 + 750 = 52,640, Page 2.

b. Losses = Direct & Assumed – Ceded = (6,170 + 3,858) – (2,340 + 2,305) = 5,383 LAE = Direct & Assumed – Ceded = (319 + 758) – (150 + 329) = 598 Total Liabilities (Page 3, line 28) = Losses (Page 3, line 1) + Reinsurance Payable on Paid

Losses and LAE (line 2) + Loss Adjustment Expenses (line 3) + Other Expenses (line 5) + Ceded Reinsurance Premiums Payable (line 12) + Provision for Reinsurance (line 16) = 5,383 + 1,270 + 598 + 285 + 1,280 + 50 = 8,866, Page 3.