Embed Size (px)

DESCRIPTION

legal issues in ISlamic banking and finances in India

Citation preview

Regulating Islamic Finance in Secular Countries:A Case Study of India

By Dr.Shariq Nisar and Syed Kamran Razvi

*Shariq Nisar, Ph.D. Economics, is Joint Editor Islamic Economics Bulletin, India and

works as consultant. He has worked in the banking sector in various capacities.

E:[email protected]; M;91-9980355403

*Syed Kamran Razvi, Legal consultant, and is also Director, Miftah Advisory India P Ltd. e: [email protected] m:91-9810078799 f: 91-11-41734987 a: Flat No.7,137B/12, Zakir Nagar, New Delhi-25

Regulating Islamic Finance in Secular Countries:A Case Study of India

By Dr.Shariq Nisar and Syed Kamran Razvi

ABSTRACT

Indian Muslims have always been trying to manage their economic affairs within the framework of Shariah. Their struggle against usury practices has been both religious and financial struggle. This paper aims to highlight the attempts made by Indian Muslims in this regard and how some of the recent developments since opening of Banking and financial sectors and FDI cap from 74% to 100% in various categories of banking and provides opportunity and poses regulatory challenge in establishing Islamic Finance and Sharia compliant-products affecting their functioning. The paper focuses on opportunities, events and regulatory changes facilitate and pose new and additional challenges to new entrants. It examines the potential segments including NBFCs,FII, Micro Finance and Mutual Funds as new source of proliferation in India and the regulatory mechanism existing and requisite for functioning at large scale. The paper also relates the causes of failures in past by the depressed economic scenario in early 1990s and the highly changing regulatory environment in the late 1990s. Some prominent Islamic NBFCs and new initiatives by UTI and others in India are taken for detailed case studies to identify the future aspects in the topic of the paper.

Terms;

Lac: One hundred thousand

Crore: 10 Million.

1: Introduction

Financial arrangements constitute an integral part of the process of economic

development. A growing economy requires a progressively rising volume of savings

and adequate institutional arrangements for the mobilisation and allocation of savings.

These arrangements must not only extend and expand but also adapt to the growing

and varying financial needs of the economy. A well-developed and efficient capital

market is an indispensable prerequisite for the effective allocation of savings in an

economy. A financial system1 consisting of financial institutions, instruments and

markets provides an effective payment and credit supply network and thereby assists

in channeling of funds from savers to the investors in the economy. The task of the

financial institutions or intermediaries is to mobilise the savings and ensure efficient

allocation of these savings to high yielding investment project so that they are in a

position to offer attractive returns to the savers.

1 Annxr.1 to paper

Islam’s teachings are not confined to the religious spheres but extend and

control every aspect of human endeavors including the economic activity. Islam

provides guidelines to regulate the economy and seeks to curb the unbridled race for

material pursuit. Concern for equity and justice, halal and haram and a sense of

responsibility towards the weaker sections of society and the need to share the

economic resources with them, are some of the principles which guide and control the

economic activity in Islam.

Keeping in view the Islamic aspirations, Indian Muslims have always been

trying to manage their economic affairs within the framework of the Shariah. The

present paper seeks to highlight the attempts made by Indian Muslims in this regard

and how some of the later developments in the form of changing regulatory

environment has affected their functioning.

Besides being the world’s second most populous country India also is Asia’s

third largest and one of the fastest growing economy. It has a huge Muslim population

between 150-200 million.2 There are several places where Muslims constitute

majority of the total population (Bagsiraj, 2002). There are a number of industries in

which Muslims traditionally have major stakes3.

Since the last two decades, India has continuously managed an average saving

rate at above 20 percent of the GDP (Bhandari, & Aiyar, 1999, p.29). Considering

their relative economic backwardness even 15 percent saving rates for Muslims would

fetch an enormous amount of annual savings to the community. Besides, there are

properties worth billions of Rupees lying in the form of Awqaf. Zakah potential of the

Indian Muslims still largely remains untapped and under utilized.

2: Non-feasibility of Islamic Banking in India

Indian banking laws do not explicitly prohibit Islamic banking but there are

provisions that put Islamic banking almost an unviable option. As the financial

institutions in India comprises of Banks and Non Bank Financial Institutions. Banks

in India are governed through Banking Regulation Act 1949, Reserve Bank of India

Act 1934, Negotiable Instruments Act 1881, and Co-operative Societies Act 1961.

2 Even a conservative estimate by Syed Shahabuddin in “Muslim India” puts Muslim population as 133.54 million in the year 2001. For details please see, www.milligazette.com/Archives/15092001/29.htm 3 Like leather, cotton, bronze, lock, sari, carpet, etc.

Despite these acts being amended several times, one of the distinguishable features

that still remain unaffected is that they define Banking in such a way that Banks can

accept deposits from public only for further lending. For example, Section 5 (b) and 5

(c) of the Banking Regulation Act, 1949 prohibit the banks to invest on PLS basis

(BR Act, 1949, 1999, pp. 6-7). Further, section 8 of the Banking Regulations Act (BR

Act, 1949, 1999, p. 12) reads, “No banking company shall directly or indirectly deal

in buying or selling or bartering of goods …”.

Besides India is among the countries that explicitly provides guarantee to its

depositors. Deposits of each account up to the value of Rs. 0.1 million are guaranteed

through the Deposit Insurance and Credit Guarantee Corporation (DICGC), a

subsidiary of the Reserve Bank of India established in 1962. Moreover, government

also interferes at the assets side by asking banks to provide concessional credit to

certain priority sector.4

Above all the Government of India explicitly clarified its position with respect

to the permissibility of Islamic banking in the country. Minister of State for Finance

Mr. Zulfiqarullah, informed the Indian parliament that the Government is not in

favour of its own or permitting the private sector to open an Islamic bank (Dalvi,

1999).

Some other factors that help stealing the shine of Islamic banking is

governments’ policy of large-scale pre-emption of banks’ resources through Cash

Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) requirements. These

together eat up over 35 percent of the banks’ total deposits. Counting another 40

percent of banks’ resources directed towards the priority sector leaves banks with very

little capital at their own disposal. Also, to increase the banking habit among people

and for the purpose of extending banking facilities to the larger sections of the

population, banks are asked to open branches in the rural and semi rural areas that

mostly are economically nonviable5 (Kanta, 1996, p.24).

Some of the other issues are stamp duty rates, Income Tax on income by

Financial institutions.

4 The Concept of priority sector lending was proposed by Prof. Gadgil Study Group (1967). Later on the Ghosh Committee (1981) recommended a target of 40 percent of the total credit to priority sector including 18 percent to Agriculture and 10 percent to weaker section.5 By the end of 1992-93, 171 Regional Rural Banks out of 196 were loss making.

3: Non-Banking Financial Institutions in India

Non Banking Financial Institutions in India comprise of Non Banking Financial

Companies (NBFCs), Mutual Funds, Insurance Companies and Developmental

Institutions. According to the nature of their business, NBFCs are further classified as

Equipment Leasing (EL), Hire Purchase (HP), Merchant Banking, Investment

Companies, and Mutual Benefits Companies etc.

A new set of companies called the Asset Finance Companies (AFC) has been

added to this classification, these are further sub-divided into those accepting deposits

and not accepting deposits.

Developmental institutions are mainly created to serve special purposes like

agriculture development, investments and export promotion etc. They are mainly

promoted and run by the Government and its maintained institutions. On the other

hand the insurance sector, which has recently been opened for the private sector, is

still beyond the reach of small capital holders. Entry norms and regulatory framework

makes it further difficult for the small capital owners to think entering this field.

Mutual funds are open to the private players. But they too are beyond the reach of

small capital holders. Besides the initial requirements of large capital and some other

stringent requirements are well beyond the reach of Islamic financial institutions.6

In short anybody going for Islamic alternatives in finance has the option of

choosing only the Non Banking Financial Companies format for its easy entry norms,

low capital requirements, lower regulations and flexibility in registration and

functioning.

However two newer option can be through the route of FII and Micro Finance.

4: Non-Banking Financial Companies (NBFCs)

The Non Banking Financial Corporations or Companies (interchangeably used in this

paper) are defined by the RBI Amendment Act, 1997 as financial institutions which

are registered as companies and which have as their principal business the receiving

6 The Tata Mutual Fund made a pioneering attempt when, at the instance of the Barkat and some other Islamic financial group, it launched Tata Core Sector Equity Fund in 1996 (IEB, 1996a). This scheme was specially tailored keeping in view the Muslims inhibition of dealing with interest bearing and haram investments. This scheme surprised many by being able to raise Rs. 230 million from the public. After initial hiccups the scheme did well for three years. After that the nomenclature was changed to the ‘Tata IT sector Fund’ (IEB, 2000a).

of deposits under any scheme or arrangement or in any other manner and lending in

any manner (http//: www.rbi.org.in).

In India, the Non Banking Financial Corporations (NBFCs) play an important

role in the mobilization and the deployment of financial resources. NBFCs are

popular because of their added advantage over banking institutions in terms of high

customer orientation, lower transaction costs, quick decision-making, easy

registrations, lesser regulations and higher flexibility. Flexibility in their structure also

allows NBFCs to un-bundle services provided by banks and market the components

on a competitive basis. These distinctive features armed with economic liberalization

contributed to great proliferation of NBFCs activities in India. The significant

increase in the domain of activities of NBFCs is evident by the fact that the share of

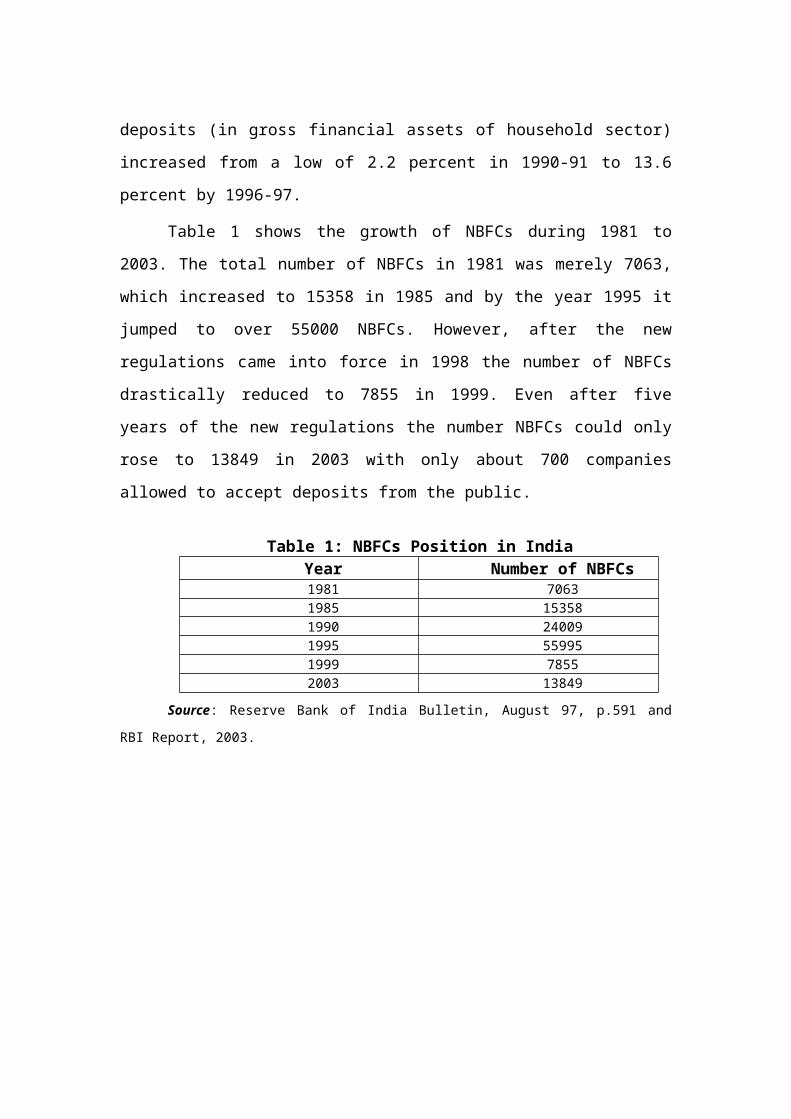

non-bank deposits (in gross financial assets of household sector) increased from a low

of 2.2 percent in 1990-91 to 13.6 percent by 1996-97.

Table 1 shows the growth of NBFCs during 1981 to 2003. The total number of

NBFCs in 1981 was merely 7063, which increased to 15358 in 1985 and by the year

1995 it jumped to over 55000 NBFCs. However, after the new regulations came into

force in 1998 the number of NBFCs drastically reduced to 7855 in 1999. Even after

five years of the new regulations the number NBFCs could only rose to 13849 in 2003

with only about 700 companies allowed to accept deposits from the public.

Table 1: NBFCs Position in IndiaYear Number of NBFCs1981 70631985 153581990 240091995 559951999 78552003 13849

Source: Reserve Bank of India Bulletin, August 97, p.591 and RBI Report, 2003.

In December 2006, NBFCs have been permitted to distribute and market

Mutual Funds, this has been permitted by RBI for two years subjected to certain

conditions including financial worth (NOF) of Rs.100 Crores. However, it is no

longer easy to take CoR( Certificate of Registration) and to run as Deposit taking

NBFC as Table 1A illustrates.

Table 1A: Status of NBFCs as on March 2007March 2007 CATEGORY Total Numbers

‘A’ Deposit Taking 403Non Deposit taking 748Banned in Delhi+Mumbai+Kolkata

238

Applications rejected as on October 1,2006

All over India NBFC+RNBC 20080

5: Islamic Financial Institutions in India – A Brief History

Even a cursory look at the economic history of Indian Muslims highlights the fact that

Muslims have always been conscious about the need to operate financial institutions

on Islamic pattern. Hamidullah (1944) traces back such efforts to the end of

nineteenth century. Another notable effort that still continues its operation was made

in 1938 in the form of Pattani Cooperative Credit Society at Surat, Gujrat (Bagsiraj,

2002). However, the Bait-un-Nasr of Mumbai, established in 1973, still remains one

of the most successful attempts so far.

The history of Muslim Funds (a very popular format devised by the Jamiat-e-

Ulema-e-Hind) is also as old as 1940 when the first Muslim Fund in the country was

established at the Rampur State of North India (Nasir, 1997). Partition of the country

in 1947 halted these efforts for almost one and half decade. After that the first major

attempt could be made possible in the form of Muslim Fund Deoband in the year

1961.

These Funds are arguably the most popular format adopted by Muslims in

India specially in the highly concentrated Muslim belt of North. According to a list

prepared by the Federation of Interest Free Organization (FIFO), there are more than

130 Muslim Funds in the country. Of them, thirty Muslim Funds as well as some

others are the founding members of the Federation of Interest Free Organizations

established in 1986. FIFO acts as an apex body of the member organisations for

policy making, liquidity arrangements, staff training and representing to the

Government.

Jamaat-i-Islami Hind also attempted, particularly in the southern states of

India, to establish welfare societies. The main purpose was to financially help the

poor and needy on Islamic principles. Bagsiraj (2002) reports about 200 such

institutions.

Muslim Funds, cooperative credit societies and welfare societies are all non-

profit institutions and have started either out of the need to rescue people from the

ruthless moneylenders or out of a concern for the economically backward and

downtrodden.

By 1980s, Muslims started venturing into profit oriented business as well. This

was made possible for three reasons; firstly, by that time, Indian Muslims had gained

some financial expertise through successful running of non-profit financial

businesses; secondly, the Islamic financial movement started in late seventies had

gained momentum throughout the Islamic world giving an impetus to the Indian

Muslims as well; lastly, the new economic policy initiated in early 1990s focussing on

privatisation, liberalisation and globalisation from the old controlled regime provided

new opportunities for the overall growth of the business.

The first NBFC claiming to do business on Islamic principles called Al-Mizan

was started in 1980 at Madras (Bagsiraj, 2002). This was a loose constituent of many

small partnership firms engaged in leather trading. This effort miserably failed in

1984-85. Some other notable NBFCs established in India since then are as follows.

Table 2: Prominent Islamic NBFCs in India

Name of Institution Year of Establishment1. Barkat Investment Group 19832. Al-Amin Islamic Financial & Investment Corporation of India 19863. Al-Barr Finance House Ltd. 19894. Syed Shariyat Finance 19895. Assalam Finance & Investment Ltd. 19906. Baitul Islam Finance Ltd. 1990

Source: Nisar, S. (1999, p.27)

6: Changing Regulatory framework for NBFCs in India

After more than four and a half decades of planned economy, India opted for a market

friendly economy when it faced a severe economic crisis in the early 1990s. These

policy changes were partly brought about out of the IMF/World Bank compulsion and

partly due to changing domestic politics. Large-scale policy and institutional changes

were brought in to make the country integrate with the global economy. Hence the

period witnessed large-scale regulatory changes in the entire financial system.

Regulations governing NBFCs were an integral part of these overall policy changes.

We would like to begin with the start of these regulations.

NBFCs regulation in India began in 1963 with a declared aim of safeguarding

depositors’ interest and to ensure healthy functioning of the NBFC sector. To begin

with, a new chapter, IIIB, was inserted in the RBI Act, 1934 to enable the central bank

to effectively supervise, regulate and control these institutions. Initially the directions

were restricted to the liability side of the balance sheet and that too, solely to the

deposit acceptance activities. However, after the reports of several expert committees

examining the functioning of NBFCs, the Chakravarty Committee (1985)

recommended a licensing based system for NBFCs. Narasimham Committee (1991)

outlined a detailed framework for streamlining the functioning of NBFCs and setting

up of a separate specialised department under the aegis of the RBI to control and

supervise the activities of NBFCs. Later on, Shah Working Group, 1992 (RBI, 1998-

99, p. 157), was appointed to make an in depth study of the role of NBFCs and to

suggest regulatory and control measures to ensure healthy growth of these companies.

Based on the recommendations of this group, the RBI initiated a series of measures

that included:

a. Widening the definition of regulated deposits;

b. Compulsory registration of NBFCs having Net Owned Funds7 of Rs. 5

million and above;

c. Guidelines on prudential norms to regulate the assets side of the NBFCs

as well.

To empower the RBI to enforce these regulations, the RBI Act, 1934 was

further amended in March 1997. Major highlights of the amendments were:

1. An entry norm of Rs. 2.5 million as minimum NOF (this was later raised

to Rs. 20 million),

2. Compulsory registration with the RBI and maintaining certain minimum

percentage of liquid assets,

7 NOF: Net Owned Fund is the aggregate of the paid-up capital and free reserves, reduced by the amount of accumulated balance of loss, deferred revenue expenditure and other intangible assets, if any, and further reduced by investments in shares and loans, and advances to subsidiaries, companies in the same group and other NBFCs in excess of 10 percent of owned fund.

3. Creation of reserve funds by transferring a minimum of 20 percent of the

net profit every year.

Besides, some other stringent provisions, those violating the regulations were

not allowed to access public deposits. Simultaneously, new set of regulatory measures

was announced in January 1998 (further amended in December, 1998) bringing an

entirely new set of regulations and supervision over the activities of NBFCs. Now the

NBFCs were broadly classified into three:

1) Those accepting public deposits; they were the subject of the entire gamut of

new regulations. The regulatory attention was specifically focused on this

category,

2) Those not accepting public deposits but engaged in financial business were

proposed to be regulated in a limited manner, and

3) The Core investment companies holding at least 90 percent of their assets as

investments in the securities of their groups/holding/subsidiary companies.

Since the major focus of these regulatory changes was on companies accepting

public deposits, Islamic NBFCs were among those affected most severely by the new

and sudden regulatory changes that mainly focused on the following:

Linking the quantum of deposit to Net Owned Fund (NOF),

Reducing the period of deposit between 12-60 months, from 24-120 months,

Ceiling on the rate of return not exceeding 16 percent.

Ceiling on brokerage fee and commission not exceeding 2 percent of the

deposit.

Changes in the content of application form as well as the advertisement

patterns for soliciting deposits only helped in tightening the situation.

The companies accepting public deposits were now asked to comply with all

the prudential norms of income recognition, assets classifications, accounting

standards, provisioning for bad and doubtful assets, capital adequacy, credit, and

investment concentration norms etc. The classification of assets and provisioning of

accounts have been laid down as follows: (Shah 1996, p.763)

Substandard: 10 percent of the total outstanding.

Bad and doubtful: Up to 1 year-20 percent of the outstanding.

1-3 years-30 percent of the outstanding.

Bad and doubtful uncovered-100 percent of the

outstanding

Total loss- 100 percent of the outstanding

The minimum capital adequacy ratio had been fixed at 12 percent while the

credit and investment concentration was fixed at 15 and 25 percent of the owned

funds to single borrower and group respectively. The total loans and investments were

subject to a ceiling of 25 and 40 percent of the NOF respectively for exposure to

single party or an industry group. Those soliciting public deposits were now asked to

specify their rating in the advertisements. Mobilizing public deposits was fixed not

more than 1.5 times of its NOF or Rs. 100 million whichever was lower.

Prohibiting NBFCs to invest more than 10 percent of NOF in real estate and

asking them not to invest in unquoted shares badly hampered the investment

opportunities of Islamic NBFCs. Moreover the companies were now required to

maintain liquid assets of not less than 15 percent of their public deposits into

commercial banks.

Table 3: Position of NBFCs for issue of Certificate of Registration

Criteria Number1. Total number of applications received 37,3902. Number of NBFCs having NOF of Rs. 2.5 million and above (i.e., fulfilling primary eligibility criteria)

10, 486

3. Number of approved applications: Number of NBFCs permitted to hold/accept public deposits

7,855624

4. Number of rejections 1,1675. Number of NBFCs whose applications are under process 1,4646. Number of NBFCs having NOF below Rs. 2.5 million 26,904

Source: RBI, 1998-99, p. 163. Note: Position as on August 31, 1999.

As is obvious from the table 3 that after the implementation of new

regulations, business prospects of NBFCs in the country including those of Islamic

were badly hurt. As per the direction for compulsory registration, the RBI received

37,390 applications. Out of these, 7,855 were approved and 11, 67 were rejected. Rest

of the applications were pending at different stages of processing. Strikingly only 624

of the total approved NBFCs, have been permitted to accept/hold public deposits.

7: Effects of Regulatory Changes on Islamic NBFCs

In the early liberalization phase, Islamic NBFCs like others grew rapidly. Major

factors responsible for this pull, besides the Islamic tag or interest-free, were their

highly customer oriented services and high returns made possible mainly due to the

bullish stock market and spiraling real estate prices, especially in the metros like

Mumbai, Delhi, Bangalore, and Hyderabad, etc.

By 1995, both the stock market and real estate had started crashing. These two

put a brake on the returns offered to the depositors who till now had been receiving

very handsome returns. Sliding economic conditions at a time of fast changing

regulatory requirements proved too much too soon for many of the Islamic NBFCs. In

a nutshell, shrinking business opportunities, increasing competition and highly

changing regulations culminated in closing down few very promising Islamic NBFCs

in the country.

Following sub-sections attempt to find out the effect of these regulations on

some of the selected Islamic NBFCs like Barkat, BUN, Al-Najib and the Al-Barr.

These four though come under the purview of the provisions of law governing and

regulating NBFCs but each company follows a different business format like Barkat,

a leasing company, Baitun Nasr a cooperative, Al Najib a Mutual Benefits Company

and Al Barr engaged in merchant and investment banking activities.

7.1: Barkat Investment Group (BIG)

Arguably it has been one of the brightest and most trusted Islamic financial

institutions in the country. Since the Bait-un-Nasr Urban Cooperative Credit Society

Ltd (BUN), Bombay was prohibited to invest its deposits under the Islamic option it

floated two partnership firms called Falah Investments Ltd. and Ittefaq Investments

Ltd. in 1983. These two later on were joined together to form the Barkat Investment

Group in 1988. In 1991, Barkat floated its flag bearing organization the Barkat

Leasing and Financial Services Ltd. (BLFSL) The total funds under its management

increased from about Rs. 1.6 million in March 1989 to about Rs. 270 million in March

1997. During all these years its returns to deposits remained a positive figure between

10 to 25 percent (Table 4), except one of its schemes Barkat Stocks that incurred

losses of 8.56 and 5.85 percent during the financial year 1995-96 and 1996-97. Due to

limited business options other than trading in stock and real estates all the schemes of

Barkat incurred losses of about 25 percent in the year 1997-98. The total loss to the

company was to the tune of Rs. 32.8 million which did not appear quite high in

comparison to Brakat’s past performance and the present financial standing. But

eventually it proved too much for the company. After two years of frenzy the Barkat

was finally closed by the government in May 2000. Liquidation of Barkat at a time

when it had assets worth Rs. 170 million (Table 5) was a major blow to the Islamic

financial activities in India.

As mentioned earlier that Barkat had heavily invested in the real estate and the

stock market. This was mainly because Islamically Barkat had little other options and

moreover the past performance of these two sectors had made Barkat able to meet the

expectations of its depositors. By the time the slump started in stock market in 1995,

Barkat had already invested a substantial part of its funds in the stock market. Tight

liquidity in the market had its impact on the Barkat which was forced to divest its high

performing shares at depressed prices. Recovery in the stock market by 1999 was too

late for the Barkat. On the other hand real estate market also went into an

unprecedented recession in 1996 that only helped increasing the despair.

Table 4: Summary of the Financial Performance of Barkat Investment Group(1988-1998- Rs. In Lakhs)

Year 1988-89 1989-90 1990-91 1991-92 1992-93 1993-94 1994-95 1995-96 1996-97 1997-98Gross Profit 8.88 13.141 27.833 56.512 79.358 158.76 286.378 313.433 401.241 -60.356Expenses 5.131 6.7 7.478 15.766 26.777 48.78 104.178 149.457 232.456 257.326Net Profit 3.749 6.441 20.355 40.746 52.581 109.98 182.2 163.98 168.79 -317.68Depositors Share 1.874 4.831 15.267 30.56 42.065 93.29 150.373 139.857 253.225 27.969Deposits Mobilized 9.865 27.6.5 85.96 151.58 262.317 567.75 970.664 1807.027 2262.484 1,135.38

Returns to Depositors

BIC 19 17.5 17.75 20 16 16.25 14 12 10 -25.45Stocks 25 14 -8.56 -5.85 -25.45Leasing 6 13.64 15.23 15 10.45 0Retained Fund 1.875 1.61 5.088 10.186 10.516 16.69 31.827 24.119 -84.44 -345.651Add/Less Retained Fund b/d 0 1.875 3.485 8.573 18.759 29.275 45.965 77.792 101.911 17.471

Net Retained Fund 1.875 3.485 8.573 18.759 29.275 45.965 77.792 101.91 17.471 -328.18Source: (Balance Sheets)

Table 5: Assets Held by Barkat Investment Group as on 30th September 1998

1= Real Estate Properties (Total 34 Properties) 116,834,3412= Other Assets

Fixed 2,389,792 Leased 24,407,095 Investments in Shares 2,685,000 Real Estate Receivables 12,608,075 PLS investments 3,730,000 Barkat Fisheries 3,200,000 Deposits 2,015,000 Other Receivables 2,967,000Total 1+ 2 170,836,303

Source: Barkat’s Assets List

Barkat’s self-imposed moratorium on Murabahah only added to its already

existing list of woes by limiting its investment basket. Though during later years

Barkat did try albeit unsuccessfully, to expand its investment portfolio by increasing

its presence in leasing based (Ijarah) activities.

Table 6: Returns on Working Capital and Total Investments of Barkat Leasing and Financial Services Ltd. during 1991-98

YearGross Returns on Working Capital

Net Returns on Working Capital

Gross Returns on Investment

Net Returns on Investment

% % % %1991-92 2.71 0.43 5 0.811992-93 11.64 3.2 13.94 3.831993-94 1.77 3.49 8.72 2.831994-95 17.97 1.73 16.8 1.621995-96 14.35 1.09 13.61 1.041996-97 15.81 0.75 13.4 0.641997-98 5.3 - 7.23 5.13 - 6.99

Source: Bagsiraj, M. I. (2000, p. 548)

Barkat Leasing and Financial Services Ltd. (BLFSL) returns on capital shows

that the strategy had worked except for the year 1997-98 when its net return on

working capital was down by 7.23 percent (Table 6) and its net return to investment

by 6.99 percent. That was the year of heavy regulatory changes brought in the NBFCs

sector in India.

New regulatory changes enforced in April 1997 completely banned all firms

involved in investment activities from accepting any fresh deposits. This led to a one-

way flow of funds (outflow) from the firms in the group causing tremendous pressure

on the already trembling operations. Barkat’s commitment to Shariah forced it not to

access the usual avenues available to others for addressing its liquidity needs. Had this

not been the case, temporary liquidity from conventional banks might have sufficed

its liquidity needs. Since there were no Shariah complaint options available or lender

of the last resort, Barkat kept waiting for some sort of external assistance either from

within or outside the country, which never reached and finally one of the very

promising Islamic NBFC in India was closed in May 2000. (IEB, 2000b, 2002).

7.2: Baitun Nasr Urban Cooperative Credit Society (BUN)

Started on a trial basis in 1973, it was regularized in 1976 as an Urban Cooperative

Credit Society under the Maharashtra Cooperative Credit Societies Act. The main

purpose of the society was to provide banking facility to its members on Islamic lines.

It accepted deposits from its members on interest free basis and extended it to the

same on actual service charges. Table 7 shows its financial performance from

beginning till 1999. Since September 2001 BUN has been forced to suspend its

operation due to its close association with the Barkat group.

Table 7: Financial Performance of Baitun Nasr (1977-1999).Share Capital, Total Deposits, Loan Turnover and Total Assets are in Rs. ‘000

Years 1977 1982 1987 1992 1997 1998 1999Branches 1 4 7 12 18 18 20Members 654 6820 20356 47186 120510 137797 155050Share Capital 26 126 584 2862 13035 12993 12762Total Deposits 36 171 6191 26302 108580 119184 124159Loan Turnover 49 3062 15977 58088 278995 324950 364810Total Assets 0 13 705 5497 25760 30405 34598

Source: (Balance Sheets)

Starting with a meager fund of Rs. 12000 the society became one of the most

successful Islamic societies in India with 20 branches in the city of Mumbai.

Membership of the society increased to more than 150,000. Total deposits of the

society also reached Rs. 120 million. It is pity that the BUN was not closed for any

bad investments (as it was not allowed at all) but because it had, once upon a time,

floated Barkat Investment Group (Nisar: 2003). It was a classic case of rumor and

contagion effect taking its toll on an otherwise smoothly functioning institution. BUN,

in fact, has purely been engaged in banking activities, accepting deposits from the

public (members) and lending it to the same. All its lending were secured by property,

gold and silver. The society had developed a scientific system of calculation of

service charges and all its 20 branches were computerized to keep pace with the

changing technological developments and keep overheads low.

The only solace for the society is that despite it being closed for so long, its

depositors, by taking a lesson from Barkat, have not taken the case to the court. Till

date, the society is in a dormant state.

7.3: Al-Najib Milli Mutual Benefits Limited (AMMB)

This is the largest financial institution in the country managed by Muslims. With 41

branches mainly spread in the northern India the company has deposits over Rs. 200

million. As far the Islamicity is concern its operation are ambiguous beyond any

doubt. The company, in fact, avoids calling itself an Islamic financial institution.

The prestigious Muslim Fund, Najibabad floated AMMB in 1993 (Nasir,

1997). Since AMMB was notified as the Mutual Benefit Finance Companies (Under

Section 620 A) of the Non Banking Financial Companies Act, hence it was kept

outside the purview of most of the new regulations. Because of this, even during the

recessionary years, it kept growing, albeit a bit slowly. This shows that even the

worse economic condition could have successfully been averted had there not been

the sudden regulatory changes. Another factor that provided greater flexibility to

AMMB’s operations was its mother organization MFN which is incorporated as a

trust through separate Act. Since the businesses of AMMB and MFN were run from

the same offices it gave the group a privilege of cross shifting its employees, assets

and liabilities. Because of this operational flexibility the group was able to promptly

counter some of the regulatory changes that might have affected its business

prospects. Moreover the AMMB also follows a policy of putting a large chunk of its

deposits in commercial banks, which provides the company a solid source of revenue

besides giving it a good cushion during the time of crisis. Table 8 shows the financial

position of AMMB, which is getting stronger by the day.

Table 8: Financial Performance of Al-Najib Milli Mutual Benefits Limited (1993-99)

(Figures in Rs. ‘000)

Year Deposits Loan Investments Profit after Tax1993 53,635.44 28,623.45 352.60 2.181994 66,953.61 37,306.80 1072.60 3.551995 91,050.83 44,834.90 1339.20 34.071996 112,307.37 53,401.38 1674.90 29.541997 120,763.01 66,568.84 1874.50 52.181998 140,330.79 72922.46 5660.15 96.411999 161,718.97 78,062.76 16,495.65 103.63

2000 193,285.05 80,518.04 15,875.50 51.71

Source: Annual Reports, 1992-93 to 1999-2000.

7.4: Al-Barr Finance House Ltd. (ABFL)

Formerly known as Al-Baraka Finance House Ltd. It was promoted by the Dallah Al

Baraka group in 1989. This is the only Islamic financial institution in the country with

a foreign stake. Throughout 1990s it was low profiled and largely unknown to the

public. However, since inception of the new regulations in 1998, it has succeeded in

accelerating its activities. It is registered under the NFBCs Act and unlike many other

Islamic NBFCs in the country it has thrived since the new regulations. The strongest

reason that seems to have favored this company during the new regulation was its

lower stretch. At the time of new regulations it operated with a very few branches and

with small public deposits. A foreign holding of 51 percent proved to be its major

source of strength, besides helping it earns a credit rating of adequate safety (IEB,

1999).

Table 9 shows the financial highlights of the company during 1990 to 1998. A

substantial part of companies resources are invested in short term Murabahah and at

the time of exigency the company is not hesitant in approaching interest based

commercial institutions. The total income of the company increased from merely 12

lakh in 1990 to 715 lakh by 1999. Specially the period since 1997 saw greater

proliferation in its total income. Irrespective of the economic condition the company

has managed to distribute dividend at the rate of 12 percent since 1996. Despite share

capital being constant since 1997 reserve surpluses of the company has increased

constantly. Fixed assets too witnessed greater jump since the new regulation.

Table 9: Financial Highlights of Al-Barr Finance House Ltd. (1990-1999)(Figures in Rs. 100,000)

Year 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Total Income

12.43 15.66 85.65 145.34 186.93 288.26 434.65 604.39 657.59 715.21

Profit 0.06 2.92 17.39 41.29 45.98 100.02 115.92 106.33 80.44 85.23Dividend 14 15 12 10 11 12 12 12 12

Fixed Assets

0.38 0.75 45.72 180.60 193.82 433.53 743.55 959.56 1232.351197.1

8Share

Capital15.00 21.56 300.00 300.00 400.00 400.00 400.00 430.00 430.00 430.00

Reserves and Surplus

0.06 0.60 5.15 12.87 25.17 81.19 149.10 233.18 261.26 289.40

Source: Balance Sheets

8: Second Wave of Islamic Finance and Financial Institutions:

The possible ‘second wave’ of Islamic Financial Institutions is not in the Banking Sector or NBFC but in the stock market or investment driven through the medium of FII, who are now attempting to register Mutual Funds, Real Estate investments,etc. This has permitted the entry without meeting out the challenge which RBI, the central Banker has posed for Shariah compliant products or interest free products.

Table 10: NSE Top Four Shariah Compliant Sectors

FII in India

FII in India are desired to be registered under the SEBI8 laws, they can also

create sub-accounts. FIIs are permitted to have their own brokers operate with

condition of account being maintained by custodian bank and transactions by the local

Stock-broker. Countries with whom, India has DTAA are advantaged in terms of tax

benefits which the investors can enjoy. However the most favourable DTAA structure

that India has is with Mauritius. Last two years have seen DTAA signing with UAE

and some other emerging economies in Middle East. The potential really lies in the

fact post 9/11, wherein the Gulf money has been craving for as alternative investment

destination to US. The investment opportunity in fast growing fairly well regulated

and organized Indian market is seen and duly recognized by many of the Islamic

Banks and Financial institutions. Sharia Complaint products (stocks and others like

real estate, infrastructure,etc) in India after deducting the interest component are

readily available. Indexing has been done by co-author Dr.Shariq Nisar and one of the

new entity Miftah Advisory India P Ltd, who is initiating this Index at BSE or NSE.

TABLE 11: FOREIGN INVESTMENT INFLOWSYear A. Direct Investment B.Portfolio Investment Total (A + B)

(Rs. crore) (US $ Million) (Rs. crore) (US $ Million) (Rs. crore) (US $ Million)1 2 3 4 5 6 71990-91 174 97 11 6 185 1031991-92 316 129 10 4 326 1331992-93 965 315 748 244 1713 5591993-94 1838 586 11188 3567 13026 41531994-95 4126 1314 12007 3824 16133 51381995-96 * 7172 2144 9192 2748 16364 48921996-97 * 10015 2821 11758 3312 21773 61331997-98 * 13220 3557 6696 1828 19916 53851998-99 * 10358 2462 -257 -61 10101 24011999-00 * 9338 2155 13112 3026 22450 51812000-01 * 18406 4029 12609 2760 31015 67892001-02 * 29235 6130 9639 2021 38874 81512002-03 * 24367 5035 4738 979 29105 60142003-04 * 19860 4322 52279 11377 72139 156992004-05* P 25395 5652 41854 9315 67249 149672005-06* P 34316 7751 55307 12492 89623 20243P: Provisional.* Includes acquisition of shares of Indian companies by non-residents under Section 6 of FEMA,1999.Data on such acquisitions are included as part of FDI since January 1996.Note: 1. Data on FDI have been revised since 2000-01 with expanded coverage to approach international best practices.Data from 2000-01 onwards are not comparable with FDI data for earlier years.2. Negative (-) sign indicates outflow.Source: RBI.

TABLE 12: TRENDS IN FII INVESTMENTYear Gross Gross Net Net Cumulative

Purchases Sales Investment Investment** Net Investment**

8 Securities Exchange Board of India body through enactment in 1992, regulator for Financial markets but in case of NBFC it shares as cross-regulator with RBI, the Central Bank in India. It has power to frame regulations. www.sebi.gov.in.

(Rs. crore) (Rs. crore) (Rs. crore) (US $ mn.) (US $ mn.)1 2 3 4 5 6

1992-93 17 4 13 4 41993-94 5593 466 5126 1634 16381994-95 7631 2835 4796 1528 31671995-96 9694 2752 6942 2036 52021996-97 15554 6979 8574 2432 76341997-98 18695 12737 5957 1650 92841998-99 16115 17699 -1584 -386 8898 1999-00 56856 46734 10122 2339 112372000-01 74051 64116 9934 2159 133962001-02 49920 41165 8755 1846 152422002-03 47061 44373 2689 562 158042003-04 144858 99094 45765 9950 257552004-05 216953 171072 45881 10172 359272005-06 346978 305512 41467 9332 45259

** Net Investment in US $ mn. at monthly exchange rate.Source: RBI.

The report in India times dtd.30 May 2007 is illustrative and is summarized below9:

"FIIs from Gulf countries should actively look at investing in the Indian stock markets," Union Commerce Minister Kamal Nath said in a presentation at the valedictory function of the 3rd India-Gulf Cooperation Council Industrial Forum.

India's stock markets were booming and registering as FIIs here would help Gulf banks deliver benefits to their high net-worth clients.

These are the indicative trends that what second wave of Islamic Investments would be. Although at least three FII from Gulf, like Taib Bank and others have tried to float the Sharia Compliant Mutual Fund, but there progress in terms of launching in India for more than one year has been partly challenged by regulations/regulators there.

Local Players:

There is raise in expectations by the Indian local players, who already have strong business presence in Middle East and launch of some Indian insurance companies in Middle East insurance sector are adding to expectations. It may be too early to predict the trends.

The biggest stumbling block for Sharia Compliant funds has been a specific mention for such products in Equity markets which is considered by regulators as community specific and too sensitive to handle.

However this perception or limitation imposed on Sharia compliant products by Indian regulators may be waning, if this circular by RBI is any indication which must be credited to Manmohan Singh’s government.

Vide Circular UBD.PCB.No.17/09.09.001/2006-07 dated October 17, 2006 on ‘Prime Minister’s 15 Point Programme for the Welfare of Minorities.’ In this connection a

9 http://timesofindia.indiatimes.com/articleshow/2086728.cms

list of 121 Minority Concentrated Districts has been identified by Government of India10.

By this circular RBI11 has issued instructions to controlling offices, branch offices advising them to specially monitor the credit flow to minorities in these 121 districts thereby ensuring that the minority communities receive an equitable portion of the credit within the overall target of the priority sector. The above requirement is to be kept in view for the purpose of earmarking of targets and location of development projects under the Prime Ministers New 15 Point Programme for the Welfare of the Minorities.

This circular itself is a major shift in terms of the way Indian Banking policy will be governed. This has not happened in the past 70 years of Indian independence.

In addition to this Micro Finance Bill of 2007 if and when passed by the Parliament can be another thrust area for Community Development initiative. The principles enumerated can be beneficial to direct entry for Islamic financial products.

RBI more recently, has agreed to the initiative by the Finance Ministry to directly permit the acceptance of ECB by those institutions who are already established in the field of micro-lending and help establish small enterprises. Institutions like IDB and other such development funds from Islamic Nations can gain entry to Indian finance market through this route without much changes warranted to their principles, as is in the existing Indian financial (including Banking) and tax laws and regulations therein.

In this sense it may widen the area of entry Islamic Financial products in Indian market.

8: Conclusion

The decade of 1980s and 1990s saw proliferation of Islamic NBFCs. India’s decision

to introduce large-scale regulatory changes in the non-banking financial sector at a

time when most of the South Asian countries were passing through severe economic

recession did not augur well for the non-banking finance sector. More so Islamic

NBFCs appears to have suffered more because of the distinct nature of their business

and other religious constraints like not being able to avail the conventional avenues

available to other financial institutions. In a fast changing regulatory environment like

this, a conventional NBFC would prefer keeping its money in commercial banks than

to go with risk associated ventures that are part and parcel of Islamic financial

institutions. On the other hand small size of Islamic NBFCs and a lack of the lender of

last resort besides naive and complacent attitude towards the regulation also had a fair

10 This issue was debated in one of the constituent assembly debates and was also part of scheme of governance for muslims under Government of India Act of 1935.11 Reserve Bank of India Act of 1934 but it became functional in 1935. Its existence pre-dates Indian independence in 1947 and becoming of Indian Republic in 1950.

share in their failures. Perhaps the recessionary economic phase could have easily

been tackled had the management been more alert and investors more informed.

The decades of 2000 onwards may be facilitating entry for Islamic financial Products

in India through Stock market, investments, Venture Capital finance,

micro-credit/finance and lastly Sukuks.

9: Suggestions and Recommendations

Experiences of the Islamic NBFCs in India underscore at least two points: (i)

Internally, Islamic NBFCs should be well capital adequate besides being highly

cautious in their business operations and (ii) In a secular democratic country like India

there is need for some sort of advocacy groups that work quietly in creating soothing

conditions for Islamic oriented businesses.

Islamic financial institutions constantly need to diversify their investment

basket through innovations and improvement in technology. In a secular country like

India it could be difficult due to non-recognition of Islamic principles but nevertheless

they are important and need to be conveyed to the regulators through all the legal

means.

Self imposed moratorium on certain qualified modes of finance by certain

Islamic finance house instead of increasing the reputation led to isolation and lopsided

investments. Therefore, more flexibility is needed to cope with the changing business

environment. Lack of the lender of last resort has been a major cause of concern for

Islamic financial institutions the worldwide. Therefore, the establishment of any such

institutions that could act as the lender of last resort should be the topmost priority by

Islamic economists and policy makers.

Another issue that needs immediate attention of the policy makers is to put a

check on tainted profit seekers who just fore the sake of their small profit vitiate the

whole environment for genuine concerns. Many institutions that operate on the basis

of interest disguising them as an Islamic financial alternative, either overtly or

covertly, only help in creating a crisis of confidence. People also need to be informed

about the Islamic finance principles so that at the time of crises they do not create

unnecessary panic and rumors leading to contagion.

****

*Shariq Nisar, Ph.D. Economics, is Joint Editor Islamic Economics Bulletin, India and

works as consultant. He has worked in the banking sector in various capacities.

E:[email protected]; M;91-9980355403

*Syed Kamran Razvi, Legal consultant, and is also Director, Miftah Advisory India P

Ltd. e: [email protected] m:91-9810078799 f: 91-11-41734987 a: Flat No.7,137B/12,

Zakir Nagar, New Delhi-25

References:

Bagsiraj, M. I. (2002). Islamic financial institutions of India: their nature, problems and prospects. In

Munawar Iqbal & David T. Llewellyn (Eds.), Islamic Banking and Finance – New perspectives on

profit sharing and risk (pp. 169-92). Edward Elgar Publishing, Cheltenham, UK.

Bagsiraj, M. I. (2000). Islamic Financial Institutions of India, their nature, problems and prospects: A

critical evaluation of selected representative units. In: Proceedings of the Fourth International

Conference on Islamic Economics and Banking. Loughborough University, U.K. August 13-15.

Bhandari, S.S & Aiyar, Sarita, Ed. (1999). Statistical Outline of India 1999-2000. Mumbai: Tata

Services Ltd.

Dalvi, A. M. (1999). “Random thoughts on some economic and legal challenges to Islamic banking

system”. Paper presented at the National Seminar on Islamic Economics – Issues and Challenges,

October 1999, New Delhi.

Hamidullah, M. (1944). Anjuman –e- Imdade Bahmi Qarze Bila Sud. Maarif, Urdu (pp. 211-16), Vol.

53. No. 3. Azamgarh.

IEB (1996a). Tata Core Sector Equity Fund – An Interest Free Investment Opportunity for Muslims

Institutions. Islamic Economics Bulletin (p. 2), March – April, Vol. 6, No.2. Aligarh.

IEB (1999). Letter to the Editor. Islamic Economics Bulletin (p. 2), September – October, Vol. 9, No. 5 .

Aligarh.

IEB (2000a). Tata Core Sector Equity Fund Rose Up. Islamic Economics Bulletin (p. 2). March –

April, Vol. 10, No. 2. Aligarh.

IEB (2000b), Barkat in Crisis, Islamic Economics Bulletin (p. 4), July – August, Vol. 10, No. 4. Aligarh.

IEB (2002), “The Future of Islamic Finance in India”, Islamic Economics Bulletin (pp. 3-4), September

– October, Vol. 12, No. 5. Aligarh.

Kanta, Ahuja (1996). The Banking Sector after the Reforms. Presidential Address, 79th Annual

Conference. Gwalior: Indian Economic Association.

Nasir, M. H. (1997), Muslim Fund Najibabad ka Pacchees Sala Safarnama. Delhi: Markazi Press.

Nisar, S. (1999), A Brief Profile of some Islamic Financial Institutions in India. Souvenir, National

Seminar on “Islamic Economics – Issues and Challenges”, 2-3 October, New Delhi.

Nisar, S. (2003), “Muslim Para Bank Crucified by Media”, The Milli Gazette, September 1-15. New

Delhi.

Reserve Bank of India at http://www.rbi.org.in

R.B.I. (1997). Report on trend and progress of banking in India 1997-98. Government of India:

Mumbai.

R.B.I. (1998). Report on trend and progress of banking in India 1998-99. Government of India:

Mumbai.

RBI Bulletin (1997, August) Government of India: Mumbai.

The Banking Regulation Act, 1949, (1999). New Delhi: Universal Law Publishing Co. Pvt. Ltd.