Embed Size (px)

Citation preview

Reflections On The Last 25 Years

Robert Martin

Managing Director & Chief Executive Officer

Growth Frontiers Asia Pacific Conference

30th October 2018

2

Summary

Corporate Social Responsibility

The BOC Aviation Journey since November 1993

Macro Environment

Airline Market

Supply Chain

Aircraft Financing

Operating Leasing

Conclusion

Corporate Social Responsibility

3

4

7.5 Magnitude Earthquake

6 Meter High Tsunami

200,000+ Displaced

2,000+ Fatalities

Airlink Regional Response Framework: Asia Pacific Region

Airlink Regional Response Framework: Asia Pacific Region

5

• Activated Regional

Response Plan

• Engaged 20+ Nonprofit

Partners

• Mobilized Regional

Aviation Community

Airlink Regional Response Framework: Asia Pacific Region

Support Airlink responses in Southeast Asia and around the globe

Sandra Walter [email protected]

6

The BOC Aviation Journey

7

The BOC Aviation Journey

All data as at the end of the relevant period

8

2009 >5

2006

>10

2000 >1

2013

>3

1997 >0.3

2017 16

30 Jun 2018 >17

Ownership Total assets

US$ billion1993

1997

SALE established with 50:50 joint

ownership between Singapore

Airlines and Boullioun Aviation

Services

Temasek and GIC each became

14.5% shareholders

2006 Bank of China acquired 100% of

SALE on 15 Dec 2006

2016Listed on HKEx on 1 June

- 70% by Bank of China

- 30% by public float

2018 Market capitalisation of US$5bn

Core Competencies: A 25-Year Track Record

Sales

Transitions

Repossessions

Purchasing

Leasing

Financing

320 aircraft sold

More than 70 transitions

36 aircraft in 13 jurisdictions1

More than 780 aircraft purchased totalling more than US$42 billion

More than 840 leases executed with > 150 airlines in 55 countries and regions

More than US$23 billion in debt raised since 1 January 2007

All data as at 30 September 2018, since inception unless otherwise indicated

Notes:

1. Includes repossessions and consensual early returns

2. Average value over last 11 years since 1 January 2008

3. As at 30 June 2018

Since inception in 1993:

9

US$3.4 billion3 in cumulative net profit after tax generated since inception

Fleet utilization2

Cashflow collection2

Average 99.9%

Average 99.6%3

10

Macro Environment

Global GDP Growth

-1

0

1

2

3

4

5

6

%

Global GDP Growth, By Year (%)

11

Source: World Bank, IMF, Public data sources

Central Bank Intervention Comes To An End

Developed economy and emerging economy central bank net purchases of G4 financial assets,

% of world GDP, rolling 12m

Source: JP Morgan

Note: The G4 is normally comprised of the US, the Eurozone, the UK and Japan; we also include

Switzerland. In the chart, we include G4 central bank purchases by looking at changes in their own

balance sheets, and include purchases of G4 assets by emerging economy central banks and by non-G4

developed country central banks by looking at changes in their foreign exchange reserves ex-gold.

Sources include individual central bank disclosures, the IMF’s International Financial Statistics database,

a 2014 analysis from Niall Ferguson and Moritz Schularick and J.P. Morgan Asset Management. 2018.

12

Lower USD Interest Rates Environment Recently

%

Source: Bloomberg, as at 22 October 2018

13

Interest rates have trended back to the 2009 levels but are still lower than pre-GFC

0

2

4

6

8

10

12

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

10Y USD SWAP 6M USD LIBOR

Average US 10-Year Swap Rate

10Y USD SWAP and 6M USD LIBOR

Jet Fuel Price – Creeping Up (Again)

14

US$/BBL

Source: Bloomberg, 22 October 2018

0

20

40

60

80

100

120

140

160

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

Jet Fuel Price

0

0.25

0.5

0.75

1

SARS Global Financial Crisis

European RecessionGPA restructuring starts

9/11

Irish Banking Crisis

Eurozone Debt Crisis

There’s Always a Downturn Somewhere!

15

Asia

Eu

rop

eU

SC

om

mo

dity

Eco

no

mie

s

Importance of having a counter-cyclical strategy

Asian Financial Crisis

Global Financial Crisis

Global Financial CrisisDotcom bubble

1St Gulf War 2nd Gulf War

Oil price bubble

Cypriot Financial Crisis

Spanish Banking Crisis

Icelandic Financial Crisis

Russian Financial Crisis

Commodity Crisis

Airline Market

16

Global

Economic

Crisis

9/11 &

Second

Gulf

War

First

Gulf

War

0

200

400

600

800

1,000

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

20

22

20

24

20

26

20

28

20

30

20

32

20

34

20

36

20

38

Ind

ex

ed

(1

99

0 =

10

0)

Global Real GDP Passenger Traffic (RPK)

17

Air Traffic Demand of 5.1% Drove Fleet Growth of 3.4%

Asia: ~x2

Source: Ascend FlightGlobal Fleet Forecast 2015, Oxford Economics, Boeing Current Market

Interactive Forecast 2018-2037

Middle class households (million)

Air traffic has grown by 5.1% since 1990 Annual fleet growth (by number of aircraft)

Fleet growth, %

Source: Ascend, 30 September 2018

-4%

-2%

0%

2%

4%

6%

8%

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Se

p-1

8

Average: 3.4%

1990 - 2017 2018 - 2037

Air Traffic +4.7%

Global GDP +2.6%

Air Traffic +5.1%

Global GDP +2.9%

Growing Global Connectivity and Falling Price of Airfares

18

Source: IATA Economics

Unique city pairs more than doubled over last two decades

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

US

$/R

TK

Nu

mb

er

of

un

iqu

e c

ity-p

airs

Unique city pairs

(LHS)

Cost of air transport, adjusted for CPI inflation

(RHS)

Unique City Pairs and Cost of Air Transport

9/11 and

Aftermath

Global

Financial

Crisis

Airline Industry Profitability Has Significantly Improved

Over The Last Decade

19

Source: IATA, October 2018

To

tal W

orld

Ne

t P

rofits

, U

S$

B

Airline Industry Net Profit

Indiv

idua

l Re

gio

ns’ N

et P

rofits

, US

$B

(LHS) (RHS) (RHS) (RHS)

-15

-10

-5

0

5

10

15

20

25

-30

-20

-10

0

10

20

30

40

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Thousands

Net profits, World Total Asia Europe North America

Weaker Airlines Exited

20

0

50

100

150

200

250

300

350

400

0

10

20

30

40

50

60

2000 2002 2004 2006 2008 2010 2012 2014 2016 Oct-18*

No. of opr No. of ac

No. of airline

operatorsNo. of aircraft

Source: Ascend, Innovata, BOC Aviation Risk Management, based on 100+ seat operators, includes airline

bankruptcies and suspensions

* Info updated as at 15 October 2018

9/11 effect –

impacted US carriers

most; few airlines but

many aircraft

Weaker airlines hit by high fuel

price followed by financial crisis;

many airlines

Big airlines affected

in 2017: Alitalia, Air

Berlin, Monarch,

VIM Avia, Niki

Total Airline Bankruptcies and Total Number of Aircraft Repossessed Per Annum

21

Number of airlines

0

5

10

15

20

25

30

35

40

45

50

Airlines with fleet >20 aircraft Airlines with fleet <20 aircraft

308 airlines left the market since 2000, of which 33 (11%) had more than 20 a/c in their fleet

Source: Ascend, Innovata, BOC Aviation Risk Management, based on 100+ seat operators, includes airline

bankruptcies and suspensions

* Info updated as at 15 October 2018

Predominantly Smaller Airlines Have Exited The Market

Number of Airlines That Left the Market, By Year

22

Number of airlines

with fleet >20 aircraft

0

1

2

3

4

5

6

No more than 5 airlines (fleet >20 aircraft) per year left the market

Source: Ascend, Innovata, BOC Aviation Risk Management, based on 100+ seat operators, includes airline

bankruptcies and suspensions

* Info updated as at 15 October 2018

Larger Airlines Show Greater Resilience

Airlines (Fleet >20 Aircraft) That Left the Market, By Year

23

Leasing: Customer Segmentation

794 airlines in service today

Focus on 147 airlines or only 19% of the airlines in the market – minimum credit score, above 20

aircraft

Credit above minimum,

fleet >20 aircraft

Credit above minimum,

fleet 10-20 aircraft

Credit above minimum,

fleet < 10 aircraft

Credit below minimum,

fleet >20 aircraft

Credit below minimum,

fleet 10-20 aircraft

Credit below minimum,

fleet < 10 aircraft

Source: Ascend, as at 30 September 2018

Only commercial aircraft with 100 seats and above

147 airlines, 19%

47, 6%

57, 7%58, 7%

85, 11%

400, 50%

17,016 aircraft, 75%

702, 3%

259, 1%

2,326, 10%

1,156, 5%

1,329, 6%

c.80% of

BOC Aviation’s

portfolio

Airline segmentation by credit score and fleet

sizeOur target 147 airlines operate 75% of the

current in-service aircraft

Supply Chain

24

25

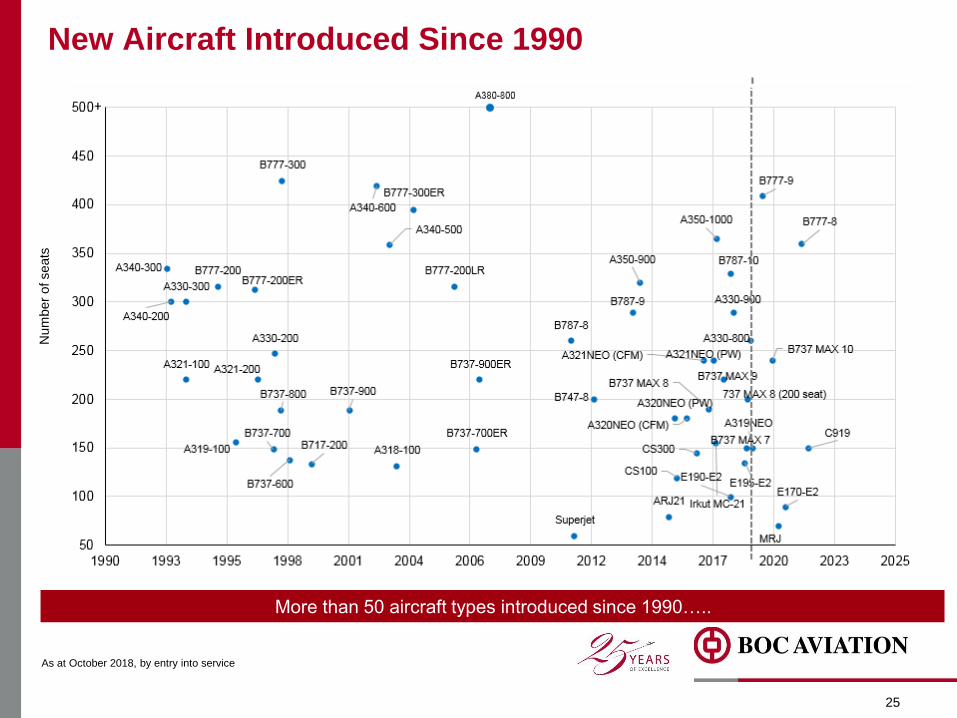

New Aircraft Introduced Since 1990

As at October 2018, by entry into service

A340-300

A340-500

A340-200

A321-100

A330-300

B777-200

A319-100

B777-200ER

A321-200

B737-700

A330-200

B737-800

B777-300

B737-600

B717-200

B737-900

A340-600

A318-100

B777-300ER

B777-200LR

B737-700ER

B737-900ER

B787-8

Superjet

B747-8

B787-9

A350-900

ARJ21

A320NEO (PW)

A320NEO (CFM)

CS100

CS300

A321NEO (CFM) A321NEO (PW)

B737 MAX 8

Irkut MC-21

A350-1000

B737 MAX 9

B787-10

E190-E2

A330-900

E195-E2

B737 MAX 7

A330-800

A319NEO

B777-9

B737 MAX 10

MRJ

E170-E2

B777-8

C919

737 MAX 8 (200 seat)

50

100

150

200

250

300

350

400

450

500

1990 1993 1995 1998 2001 2004 2006 2009 2012 2014 2017 2020 2023 2025

Num

ber

of seats

More than 50 aircraft types introduced since 1990…..

A380-800

+

26

Supply Chain Challenge Since 2014

As at October 2018, by entry into service

B787-9

A350-900

ARJ21

A320NEO (PW)

A320NEO (CFM)

CS100

CS300

A321NEO (CFM)

A321NEO (PW)

B737 MAX 8

Irkut MC-21

A350-1000

B737 MAX 9

B787-10

E190-E2

A330-900

E195-E2

B737 MAX 7

A330-800

A319NEO

B777-9

B737 MAX 10

MRJ

E170-E2

B777-8

C919

737 MAX 8 (200 seat)

50

100

150

200

250

300

350

400

450

2013 2014 2016 2017 2019 2020 2021 2023

Num

be

r o

f se

ats

… of which, more than 25 aircraft types were introduced in the last four years

Aircraft Financing

27

Operating Lessors’ Share Has Doubled Since 1990

28

23%

45%

20%

25%

30%

35%

40%

45%

50%

0

5,000

10,000

15,000

20,000

25,000

1990 1995 2000 2005 2010 2015 Sep 2018

Owned Fleet Operating Lease % provided by operating lessor

Source: Ascend, 30 September 2018

Num

be

r o

f a

ircra

ft

Pro

po

rtio

n p

rovid

ed

by o

pe

ratin

g lesso

rs

x2

Global fleet has grown from 8,794 to 22,788 aircraft since 1990

29

Changes in Bank Sizes

Source: Bloomberg - ‘China’s Too-Big-to-Fail Financial Firms Keep Getting Bigger “, 11 October 2018

0

10

20

30

40

50

Dec-08 2010 2011 2012 2013 2014 2015 2016 2017 2018

China US

US$ trillion

Total assets of Chinese banks vs US banks

30

Growing Importance of Chinese Banks

Source: Bloomberg - ‘China’s Too-Big-to-Fail Financial Firms Keep Getting Bigger “, 11 October 2018

0 2 4 6 8 10 12 14

Germany

Italy

Switzerland

France

Canada

Australia

UK

Japan

US

China

China has more mega-banks than any other country in the world

Number of banks with over US$500 billion of assets

31

Growing Importance of Chinese Banks

Source: Bloomberg - ‘China’s Too-Big-to-Fail Financial Firms Keep Getting Bigger “, 11 October 2018

Biggest banks by assets

US$ trillion

0

1

2

3

4

5

ICBC CCB AGBank BOC MitsubishiUFJ

BNPParibas

HSBC JPMorgan BofA Citigroup

32

The Operating Leasing Industry

33

The Operating Leasing Industry Today

5 key airframe manufacturers

3 key engine manufacturers

10,000+ supply chain partners

c.800 airlines globally

46,950 new aircraft required over

the next 20 years1

200+ active banks

1000+ capital market investors

350+ aircraft lessors

SuppliersCustomers

Funding Investors

Aircraft

Leasing

Industry

Notes:

1. Boeing CMO 2017-2036

34

Major Changes In The Operating Leasing Industry Since 1990

3 key airframe manufacturers

disappeared as individual OEMs

(McDonnell Douglas, Canadair,

Fokker)

489 airlines in 1990

300+ airlines filed for bankruptcy

since 2000

1990s: Japanese banks

2000s: European commercial banks

2010s: Asian banks; equity & debt

capital markets; ABS market

SuppliersCustomers

Funding Investors

Aircraft

Leasing

Industry

1990s: US, Japan

2000s: Middle East

2010s: Chinese; ABS investors

No of owned aircraft Market share (%) Current Status

GPA 352 19.7

Polaris 263 14.7

ILFC 139 7.8

GE Capital 111 6.2

AWAS 84 4.7

UAS 55 3.1

Electra 51 2.8

Aeronautics Leasing 46 2.6

GATX 40 2.2

Int’l Air Leases 39 2.2

35

Top 10 Lessors in 1992

Source: Hoare Govett – ‘GPA Group Plc’, 1 June 1992

36

What Happened To Them?

Export Credit

Bank Debt

Capital Markets

Cash

Source: Hoare Govett – ‘GPA Group Plc’, 1 June 1992

No of owned aircraft Market share (%) Current Status

GPA 352 19.7Partly acquired by GE Capital &

the rest by Aercap later

Polaris 263 14.7 Acquired by GE Capital

ILFC 139 7.8 Acquired by Aercap

GE Capital 111 6.2 Owns GECAS today

AWAS 84 4.7 Acquired by DAE

UAS 55 3.1 Bankrupt

Electra 51 2.8 Bankrupt

Aeronautics Leasing 46 2.6 Bankrupt

GATX 40 2.2 Acquired by Macquarie

Int’l Air Leases 39 2.2 Bankrupt

4

33

GPA Aercap

The Scale of the Industry Is Significantly Greater Today

37

Source: FlightGlobal, Company’s filings

Notes:

1. As at 31 March 1992

2. As at 30 June 2018

US$ billion, owned fleet NBV

Today’s largest aircraft lessor is at least eight times larger than 1990’s

19921 20182

GPA

Aercap =

8 x GPA

in 1992

38

Aircraft Lessor Strategic Landscape – Now

Source: Ascend, Company filingsData as of 31 December 2017 unless indicated otherwise

Notes:

1. As at 30 June 2018

2. As at 30 September 2018

3. As at 31 March 2018

4. As at 30 September 2017

5. Including finance leases

6. Completed the acquisition of SKY Leasing’s Irish subsidiary in Sep 2018

Top lessors by owned fleet value

Fleet value, US$ billion

33.0

30.0

18.5

14.9 14.312.9

12.0 11.3

9.27.9 7.6 7.4 6.8

5.6 5.44.0 4.0

2.9

1

3

4

5

5

1

1

1

1

1,5

1

6

Source: Bloomberg, October 2018; respective Company websites

Notes:

1. As at 30 June 2018 for BOCA, ALC, Aercap, Avolon, Aircastle and Aercap; as at 31 March 2018 for

SMBC, as at 30 September 2017 for ACG.

2. Calculated as annualised interest expense for the first six months of 2018 divided by average debt.

Actual 12 months for SMBC AC as at 31 March 2018, and ACG as at 30 September 2017.

3. Avolon announced the sale of 30% stake to ORIX in August 2018

4. Excluded IFRS9 adjustments of US$82.4m (BOC Aviation’s own calculations). Including, COF would

be 3.2%.

All top 10 lessors have credit ratings

Lessor Fitch S&P Global Moody’s Average cost of

funds1,2

ICBC Leasing A A A1 N.A

GECAS A A A2 N.A

BOC Aviation A- A- NR 3.1%

SMBC Aviation Capital A- BBB+ NR 3.6%

Aviation Capital Group BBB+ A- NR 4.1%

Air Lease Corporation BBB BBB NR 3.3%

Aercap Holdings BBB- BBB- Baa3 4.1%

Avolon3 BB BB+ Ba2 3.7%4

Aircastle BBB- BBB- Baa3 5.1%

Dubai Aerospace NR BB+ Ba2 N.A

39

Lessor Financing: Shift to Use Of Credit Ratings

40

• Airline market strong but reshaping in certain parts of world

• There are always new entrants and airlines leaving the market

• Shift to Asia Pacific

• Rising fuel prices and interest rates again

• Liquidity continues to be strong driving funding costs and aircraft trading

• The use of bond markets has significantly increased for lessors

• Shift to more Asian banks

• Supply side

• Record number of new aircraft types

• Stress on supply chain

• Competition in leasing is fierce

• Recent M&A hardly changes overall market concentration

• Most lessors in 1990 don’t exist today, but talent has just moved

around

Conclusions

Disclaimer

This presentation contains general background information about the activities of BOC Aviation Limited (“BOC Aviation”), current as at the date hereof. This document does notconstitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of BOC Aviation or any of its subsidiariesor affiliates in any jurisdiction or an inducement to enter into investment activity.

The information contained in this document has not been independently verified and no representation or warranty, expressed or implied, is made as to, and no reliance should beplaced on, the information or opinions contained herein. The information set out herein may be subject to revision and may change materially. BOC Aviation is not under anyobligation to keep current the information contained in this document and any opinions expressed in it are subject to change without notice. None of BOC Aviation or any of itsaffiliates, advisers or representatives (including directors, officers and employees) shall have any liability whatsoever for any loss whatsoever arising from any use of this documentor its contents or otherwise arising in connection with this document (whether direct, indirect, consequential or other).

No part of this document, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever.No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of theinformation or the opinions contained herein. None of BOC Aviation or any of its affiliates, advisors, agents or representatives including directors, officers and employees shall haveany liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in connection with thedocument. This document is highly confidential and is being given solely for your information and for your use and may not be shared, copied, reproduced or redistributed to anyother person in any manner.

This document may contain “forward-looking statements”, which include all statements other than statements of historical facts, including, without limitation, any statementspreceded by, followed by or that include the words “will”, “would”, “aim”, “aimed”, “will likely result”, “is likely”, “are likely”, “believe”, “expect”, “expected to”, “will continue”, “willachieve”, “anticipate”, “estimate”, “estimating”, “intend”, “plan”, “contemplate”, “seek to”, “seeking to”, “trying to”, “target”, “propose to”, “future”, “objective”, “goal”, “project”, “should”,“can”, “could”, “may”, “will pursue” or similar expressions or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and otherimportant factors beyond BOC Aviation’s control that could cause the actual results, performance or achievements of BOC Aviation to be materially different from future results,performance or achievements expressed or implied by such forward-looking statements. Neither BOC Aviation nor any of its affiliates, agents, advisors or representatives (includingdirectors, officers and employees) intends or has any duty or obligation to supplement, amend, update or revise any of the forward-looking statements contained in this document.

Any securities or strategies mentioned herein (if any) may not be suitable for all investors. Recipients of this document are required to make their own independent investigation andappraisal of the business and financial condition of BOC Aviation, and any tax, legal, accounting and economic considerations that may be relevant. This document contains datasourced from and the views of independent third parties. In replicating such data in this document, BOC Aviation does not make any representation, whether express or implied, asto the accuracy of such data. The replication of any views in this document should not be treated as an indication that BOC Aviation agrees with or concurs with such views.

The information contained in this document is provided as at the date of this document and is subject to change without notice.

41

42

www.bocaviation.com

BOC Aviation Limited 8 Shenton Way #18-01 Singapore 068811 Phone +65 6323 5559 Facsimile +65 6323 6962

Incorporated in the Republic of Singapore with limited liability

Company Registration No. 199307789K