Embed Size (px)

Citation preview

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

SustainabilityAccounting,ManagementandPolicyJournal;2015Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020

Reflectionsonnaturalcapitalaccountingatthenationallevel:Advancesinthesystemofenvironmental-economicaccountingCarlG.Obst11InstituteforDevelopmentofEnvironmental-EconomicAccounting1.Introduction

Naturalcapitalanditsincreasingscarcityhavebeenattheheartofconcernsoversustainabilityforwellover40years(Meadowsetal.,1972;MA,2005;Rockströmetal.,2009).Asthekeydriversofnaturalcapital’sscarcityareeconomicgrowthandtherelatedincreasingconsumptionofgrowingpopulations,therehaslongbeendiscussionthatthemeasureofeconomicgrowth,grossdomesticproduct(GDP),hasinappropriatelybecomethemostwidelyadoptedmeasureofprogress(Kennedy,1968;Costanzaetal.,2009;Stiglitzetal.,2010).

Alternativemeasuresofprogressthatincorporatearangeofnon-economicfactors,includingnaturalcapital,havebeendevelopedformanyyears.High-profileexamplesincludetheHumanDevelopmentIndex(HDI;UNDP,2014)andtheGenuineProgressIndicator(GPI;Cobbetal.,1995).ManybuildfromthepioneeringworkofNordhausandTobinintheearly1970s(NordhausandTobin,1972).Nonetheless,howeverwidelypublicizedorrecognized,thesealternativemeasureshavenotdisplacedGDPasthefocalindicatorforeconomicanddevelopmentpolicy.Costanzareinforcesthisrealityinmakingthecasethat“thechancetodethroneGDPisnowinsight”(Costanzaetal.,2014).

Thispaperpresentssomereflectionsontherelativelackof“success”indisplacingGDPastheleadingmeasureofprogress,well-beingand/oreconomicwelfareinpolicycircles.ItdoessobyreflectingontheroleofaccountingframeworksinthemeasurementofGDPandfromthispositiondiscussesthepotentialofextendingtheseframeworksvianaturalcapitalaccounting.Suchextensionwouldhelptomainstreamthediscussionofenvironmentalfactorsineconomicanddevelopmentpolicythroughanintegratedmeasurementframework,perhapsreplacingsomeaspectsofthebroadermeasuresofprogressthathavedeveloped.Atthesametime,thepaperisnotintendedtoprovideafulsomecriticalreviewofdifferentmeasuresofprogress.

Intermsofaccountingperspective,thepaperdoesnotcoverthevariouswaysinwhichthebroadbodyofaccountingknowledgeandresearchhastackledthequestionofnaturalcapitalandsustainability(Gray,1990;BebbingtonandLarrinaga,2014).Further,thispaperdoesnotaimtocritiquethebodiesofworkthatmaybegenerallyconsideredasgreen,environmentalorwealthaccountingthathaveemergedfromtheeconomicsprofession(HamiltonandClemens,1999;Dasgupta,2009;Mäleretal.,2009;Barbier,2013).Instead,thereflectionsonaccountingcomefromtheperspectiveoftheSystemofNationalAccounts(SNA),i.e.theUnitedNationsaccounting-basedstandardsystemofmacro-economicstatisticsthatunderpinsthederivationofGDP.

Asalong-timenationalaccountant,theauthorhasspentthepastfouryearsworkingontheUnitedNations-ledprojecttoestablishinternationalstatisticalstandardsthatextendtheSNAandintegrateenvironmentalinformationwithinanaccountingframework.ThestandardswereadoptedbytheUnitedNationsStatisticalCommissionin2012,andwhileworkcontinuestoimplementandfurther

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

advancethisareaofaccounting,substantialandmeaningfulprogresswillonlybepossiblebyexpandingtheawarenessofthesedevelopmentsandseekinginputfromabroadrangeofdisciplines.Thegoalofthispaperisthustoraiseawarenessofthepotentialofaccountinggenerally,butnationalaccountingspecifically,tocontributetothemeasurementofprogress.

Thepaperisstructuredasfollows.Section2describestheroleofaccountinginthemeasurementofGDPandpointstothepotentialbenefitsthatarisefromtakinganaccountingapproach.Section3summarizesthedevelopmentofinternationalstatisticalstandardsonnaturalcapitalaccountingoverthepast20yearsthathaveemergedfromextensionstotheSNA.Akeymessageofthissectionisthatthedevelopmentprocesshastendedtobequiteseparatefromdevelopmentsintheacademicliteratureoverthistime.

Section4providesanoverviewofthecurrentstateofplaybydescribingthecontentoftheSystemofEnvironmental-EconomicAccounting2012(SEEA2012)–thebodyofworkrecentlyreleasedundertheauspicesoftheUnitedNationsStatisticalCommission.Section5reviewsthedevelopmentsintheSEEA2012,notinglimitationsandareasofrequiredresearch.Section6concludeswithreferencetocurrentinitiativesandtheroleofaccounting.

2.Measuresofprogress,GDPandaccounting

Sincethe1930s,theassessmentofcountries’progresshasmostcommonlybeenlinkedtogrowthinthemeasureofeconomicactivityknownasGDP.ThemeasurementofGDPhasbeenprogressivelyrefinedsincetheearly1950s,withitsconceptualbasissetoutinameasurementframeworkknownastheSNA.ThelatestversionoftheSNAwasadoptedbytheUnitedNationsStatisticalCommissionin2008(EuropeanCommissionandInternationalMonetaryFund,2009).

TheSNAenshrinesafocusoneconomiccapital,i.e.thosephysicalentitiesorintellectualproductsthatprovideongoinginputstoproductionandthegenerationofincome,asdefinedfromaneconomicaccountingperspective.Initsaccountingapproach,theSNAexcludesthedirectmeasurementofhumanandsocialcapital,andhasacoverageofenvironmentalornaturalcapitalthatisessentiallylimitedtotheextractionofresources.Indeed,naturalprocessesareexplicitlyexcludedfromthedefinitionofproductionthatsetsthemeasurementboundaryforGDP(EuropeanCommissionandInternationalMonetaryFund,2009,6.24).

Thefocusoneconomiccapitalallowsacomprehensiveandinternallyconsistentaccountingforallmarket-basedflowsofincome,butitdoesnotpermitabroaderassessmentofthesustainablegenerationofthatincomeorrecognitionofotherbenefitsthatcontributetowell-beingwhicharegeneratedfromtheomittedformsofcapital.Theideathatthereisadirectconnectionbetweenoverallwell-beingandmultipleformsofcapital–suchaseconomic,natural,socialandhumancapital–hasbeenestablishedformanyyearsineconomics(PearceandAtkinson,1993;AsheimandWeitzman,2001;Dasgupta,2009)andprovidesthebasisfortheinvolvementofaccountinginthisfield.

GiventheseseeminglyobviouslimitationsaboutthescopeandbasisofGDP,whatisitaboutGDPthathasmadeitsoenduring?Therearemanyreasonsbut,intheviewoftheauthor,anoftenoverlookedoneisthatGDPisforgedfromanaccountingframeworkwithalloftheinternalchecksandbalancesthatanaccountingsystemcontains.Themajorityofalternativeindicatorsofprogressdonothavetheseinternalchecksandbalances,evenincaseswheretheyincorporateindicatorsofcapitalandincome.

TherearefourkeyfeaturesofthenationalaccountssystemthatprovideGDP’srobustness.First,thereisadefinedproductionboundarythatdeterminesthosegoodsandservicesconsideredtobeproducedwithintheeconomyandthussetsthesizeofGDP.Second,thereistheadoptionofsupply

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

anduseprinciplessuchthattheremustbeabalancebetweenthetotalgoodsandservicessupplied(throughproductionandimports)andthetotalgoodsandservicesused(byotherbusinesses,government,households,forinvestmentorexported).Third,thereisacloserelationshipbetweentheproductionboundaryandtheassetboundarysuchthatchangestotheproductionboundaryortheassetboundaryoftenimplychangesintheother.Forexample,expandingproductiontoincludeunpaidhouseholdworkwouldalsorequirethatequipmentusedtosupportthiswork(fridges,washingmachines,etc.)wouldbeconsideredassets,whereas,atpresent,theyareconsideredconsumptionitems.Fourth,changesinassetsoveranaccountingperiodmustreconcilewiththeopeningandclosingbalancesheets.

Whilethesemaybefairlystandardaccountingprinciplesandrelationships,thiscombinationoffeaturespermitsGDPtobemeasuredequivalentlyinthreeways–intermsofproduction,incomesorexpenditures.Further,thealignmentofincomeandassetmeasurementthroughthecarefuldefinitionofmeasurementboundariessupportsconsistentrecordingandanalysisofchangesintheassetbaseandchangesinGDPandincome.Combined,thesefeaturesprovideadegreeofrobustnessnotfoundinmostotherindicatorsofprogress.

Incontrast,measuressuchastheGPIortheHDIbringtogetherarangeofindicatorsfromtheeconomic,socialandenvironmentaldomainsandthenweighttogetherthedifferentindicatorsinsomeway.Whileclearlyprovidingaggregateindicatorswithabroader,andmoreappropriate,scopeinmeasuringprogress,thereareconcernsabouthowtheseindicatorsareconstructed(forashortsummary,seeBartelmus,2014).

Fromanaccountingperspective,themajorconcernishowthecomponentthemesandindicators“beyondGDP”areselected.MostmeasuresthatgobeyondGDPtendtoworkbottom-upinthesenseofaddinginindicatorsofthosethemesthatwouldseemmostappropriateinabroaderconceptualizationofprogressorwelfare.(Seee.g.theconstructionoftheGPIwhichuseshouseholdconsumptionexpenditurefromthenationalaccountsandadjustsfor24differentsocialandenvironmentalcomponents;Cobbetal.,1995).

GDP,ontheotherhand,isdefinedtop-downbyfirstdeterminingaconceptofproductionandincludinganygoodorserviceconsistentwiththatconcept.Thisisnottosaythatthedefinitionofproductioniscorrect,immutableorcompletelyobjective,buttheapproachdoesconferalevelofstabilityoverthescopeofGDPinthefaceofchangingcircumstancethatisunusualintheindicatorspace.Further,theadoptionofthesame,agreed-upondefinitionofGDPinallcountriesprovidesaverystrongcomparativeframework.

Someofthesefeaturesareonesthatotherindicatorframeworksaretakingon.TheHDIisnowregularlycompiledforallcountriesfollowinganagreed-uponmethodology(UNDP,2014),andrecently,estimatesoftheGPIhavebeenreleasedforalargernumberofcountries(Kubiszewskietal.,2013).

However,theimportantlessonhereisthatGDPshouldnotbeviewedasanindicatorthatsimplyweightstogetheradiverseselectionofgoodsandservices.Ifthatwerethecase,thenGDPwouldhavebeentoppledoramendedmanyyearsago.Itisnothardtothinkofthingsthatmightbeincludedorexcluded.GDP,howevernarrowlydefinedinscope,drawstremendousstrengthfromitsaccountingroots,inparticularthefundamentallinksbetweenincome,productionandassets.Itisinunderstandingtheserootsandthepotentialtoextendoramendthemthatthereexistspotentialtoderivemorerobustalternativemeasuresofwell-beingandprogress.

Oneareainwhichthepotentialofaccounting-basedapproacheshasbeenexploredisknownaswealthaccounting.ThisareaofresearchemergedfrominitialworkbySolow(1974)andHartwick(1977)inthe1970sconcerningtheeconomicsofusingnaturalresources(whichwasbasedoninitialworkofLindahl(1933)onthedefinitionofincome).Theworkhasbroadenedtoconsiderother

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

formsofcapitalunderthegenerallogicthatthereisastrongrelationshipbetweenthesustainabilityofacountry’sconsumptionanditsuseofcapital.Dasgupta(2009)providesathoroughexpositionoftheconceptsandrelationships.

Thewealthaccountingtheoryhasbeenactivelyappliedinrecentyearsintwodifferentbutsimilarlyfoundedworks.First,inthedevelopmentofmeasuresofgenuinesavingsandnationalwealthbytheWorldBank(2011).Second,intheworkonthedevelopmentoftheInclusiveWealthIndex(UNU-IHDPandUNEP,2012).

Anotherapproachreflectingthepotentialofaccounting-basedapproachestogobeyondGDPhasbeendevelopedintheSystemofEnvironmental-EconomicAccounting(SEEA),anditisthisapproachthatisthefocusofthispaper.Unlikethewealthaccountingapproach,theapplicationofaccountingprinciplesintheSEEAisnotappliedonlyinrelationtothevalueofthevariousformsofcapitalandtheassociatedincomeandconsumption.TheSEEAalsoappliesaccountingprinciplestotheorganizationofenvironmentalinformationinphysicalterms(e.g.flowsofwater,energyandemissions)tosupportthedevelopmentofmorecoherentdataontheenvironmentandfacilitatetheintegrationofthosedatawitheconomicinformation.ThescopeandapproachoftheSEEAareexplainedthroughSections3and4.

AkeymotivationfordevelopingtheaccountingextensionsoftheSEEAisthatbyextendingthestandardeconomicaccountingframework,itwillfacilitatemainstreamingenvironmentalinformationwithinregulardiscussionsoneconomicanddevelopmentpolicy.Thus,ratherthansettingupalternativeandcompetingmeasures,theintentistoworkwithinthecurrentaccountingconstructsandestablishcomplementarymeasurestoGDPthatenableabroaderstorytobeconveyed.Whethersuchanapproachwillbemorepersuasiveandsuccessfulinbroadeningthediscussionisyettobefullytested,butitshouldberecognizedasadifferentwayforward.

Ofcourse,intheabsenceofdefinitiveaccountingapproachesthatcoverallaspectsofprogress,thecompilationofbroadindicatorssuchastheHDIandGPIaddsimmeasurablytothepublicdiscussionoftheseimportantissues.Itissimplynotedherethataccounting-basedapproacheshavecertainfeaturesthatsuggestmovingbeyondGDPinmeasurementtermsisnotonlyacaseofreplacingonebroadindicatorforanother.

3.Backgroundtothedevelopmentofinternationalstandardsinnaturalcapitalaccounting

Thepotentialandneedtobetterintegratemeasuresrelatingtonaturalcapitalwithinthenationalaccountsframeworkemergedthroughthe1970sand80s(Bartelmus,1987;Ahmadetal.,1989).ConsistentwitharequestfromthefirstUnitedNationsConferenceonEnvironmentandDevelopmentheldinRiodeJaneiroin1992(UnitedNations,1993a),theUnitedNationsStatisticalDivisionledthedraftingofthefirstinternationaldocumentonenvironmental-economicaccounting(UnitedNations,1993b).Thisdocument,IntegratedEnvironmentalandEconomicAccounting,becameknownastheSystemofEnvironmental-EconomicAccountingorSEEA.Itwasaninterimdocumentpreparedbytheworld’sofficialstatisticscommunitytoproposewaysinwhichtheSNAmightbeextendedtobettertakenaturalcapitalintoconsideration.

Sincethatinitialworkin1993,workonenvironmental-economicaccounting(nowmorewidelyreferredtoas“naturalcapitalaccounting”)hascontinuedsteadilywithintheauspicesoftheofficialstatisticscommunity.CountriessuchasTheNetherlands(StatisticsNetherlands,2013),Canada(StatisticsCanada,2014),Australia(AustralianBureauofStatistics,2012)andDenmark(StatisticsDenmark,2013)areamongtheleadersinthefield,butmanyothercountries,bothdevelopedanddeveloping,haveexperienceinthedevelopmentofvariousenvironmental-economicaccounts.

Keydevelopmentssince1993haveincluded:

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

• TheestablishmentoftheLondonGroupofExpertsonEnvironmental-EconomicAccountinglargelycomprisingtechnicallevelrepresentativesfromnationalandinternationalstatisticalofficesandwhichhasnowmet20times.

• Aguidancedocumentreleasedin2000titledIntegratedEnvironmentalandEconomicAccounting–AnOperationalManual(UnitedNations,2000).

• Anupdatetothe1993SEEAreleasedin2003,theSEEA-2003(EuropeanCommissionandInternationalMonetaryFund,2003).

• TheestablishmentofanoverarchingUNbodyforthisfieldofworkin2005–theUnitedNationsCommitteeofExpertsonEnvironmental-EconomicAccounting(UNCEEA)–undertheauspicesoftheUnitedNationalStatisticalCommissionandgiventhetaskofprogressinginternationaleffortsinthisarea.

• AdoptionoftheSEEA2012CentralFramework(UnitedNationsandEuropeanUnion,2014)astheinternationalstatisticalstandardintheareaofenvironmental-economicaccounting.Thisadoptionplacesworkinthisareaonapar,atleastconceptually,withthelong-standingSNA[1].

• ReleaseofSEEA2012ExperimentalEcosystemAccounting(UnitedNationsetal.,2013)asasynthesisofapproachestothemeasurementofecosystemsthroughanationalaccountinglens.

Overthepast20years,therehasbeenanimportantbroadeningoffocusinSEEA-relatedwork.Throughthe1980sandearly1990s,theprimaryfocuswasonextensionsandadjustmentstoGDP,forexamplemeasuresofdepletionanddegradation-adjustedGDP,andrecordingenvironmentalexpenditures.Discussionconsideredtherangeofwaysinwhichdepletionanddegradationmightbeestimated,valuedand,subsequently,incorporatedwithinthestructureofthestandardnationalaccountsanditsvariousmeasuresofproduction,income,savingandwealth.

Throughthe1990s,thisspecificfocusstartedtobroadentoconsiderwaysinwhichaccountingapproachesandstructuremaybeusefulintheorganizationofphysicalinformationonenvironmentalstocksandflowssuchaswater,energyandwaste.Thisdirectionbuiltonworktomodeltheeconomyinphysicalterms(Meadowsetal.,1972).ThisbroadeningoftheSEEAdiscussionreflectedarecognitionthataccountingprinciplescouldbeappliedwithoutreferencetomonetaryunits.

Thisbroaderapplicationofaccounting,whichhasbeenexpandedfurtherinrecentyearsthroughthedevelopmentofecosystemaccounting,confrontsthecommonconceptionthatadoptionofaccountingapproachesnecessarilyreliesonvaluation(inmonetaryterms)ofnature.Certainlytherearequestionsthatcannotbeansweredunlessvaluationisundertaken,forexampleadjustingmeasuresofGDP,buttherearesomeimportantadvantagesofapplyingaccountingprinciplesintheorganizationofdatainphysicalterms(seeSection4).

Onthewhole,thedevelopmentofnaturalcapitalaccountingasdescribedintheSEEAhastakenplaceoutsideofacademiaandhasreflectedaprocessmanagedbytheinternationalofficialstatisticalcommunity.Overthe20yearsfromthereleaseofthe1993SEEA,therehasbeenrelativelylittleacademicliteraturewhichdebatesaccountingalternativesfromanationalaccountingperspective.ExceptionsincludeHarrison(1993),Vanoli(1995),deHaanandKeuning(1996),NordhausandKekkelenberg(1999),PeskinanddeLosAngeles(2001),Vardonetal.(2007)andEdensandHein(2013).Instead,thedevelopmentanddebateoftheworkisreflectedindocumentspublishedbyvariousinternationalagencies(particularlytheUnitedNationsStatisticsDivision[UNSD]andtheStatisticalOfficeoftheEuropeanCommunities[Eurostat])andindocumentspresentedtothemeetingsoftheLondonGroupandUNCEEA.Essentially,theacademicliterature

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

doesnotreflectthesubstantialthinkinganddebatethathastakenplaceoverthepast20yearsinnationalaccountingandSEEAcircles.

Itwouldbewrongtoconcludethatthesedocumentsandpaperswerenotsubjecttopeerrevieworwerereportsofconsultantsengagedonlyonspecifictopics.IndeedtheprocessoffinalizingtheSEEACentralFrameworkinvolvedwellover100expertsthroughmultipleroundsofconsultationandreviewoverfiveyears.Atthesametime,byandlarge,thetechnicalcontentoftheSEEA2012CentralFrameworkmaybebestdescribedasacodificationofliteratureandthinkingdevelopedbefore2000.Thedocumenthasthustendedtoclarifythelanguageandmakechoicesaboutthetechnicalapproachtonaturalcapitalaccounting.Significantly,bymakingthesechoicesandreflectinganagreed-uponposition,ithasprovidedastrongerfoundationforgovernmentsandinternationalagenciestosupportworkinnaturalcapitalaccountingandinturnformabasisforfurtherresearchandextension.

Unfortunately,theeffectofdiscussionontheSEEAresidinglargelywithintheinternationalstatisticalcommunityhasmeantthatawarenessoftheworkoutsideofthatcommunityhasbeenlimited.ThishasbothreducedthediscussionwithintheSEEAcommunityofotherdevelopmentstakingplaceoutsideandmeantthatsomeofthepositivedevelopmentstakingplaceintheSEEAwerenotinfluencingotherthinking.However,since2012,thisdynamichaschangedsignificantly,andwhileitisstillearlydays,thebreadthofconnectionsisincreasinglyrapidly.Section6providesadescriptionofthenatureanddirectionofsomeoftheseconnections.

Thechangeddynamichasbeendrivenbytwothings.First,theadoptionoftheSEEACentralFrameworkandtheprocessleadinguptoitsreleaseprovidedaplatformfortheinternationalstatisticalcommunitytopromoteitsapproach.ThisplatformwasreinforcedbytheSEEA’sjointpublicationbysixinternationalagencies(UnitedNations,EuropeanCommission,FoodandAgriculturalOrganizationoftheUnitedNations,InternationalMonetaryFund,OrganisationforEconomicCooperationandDevelopmentandtheWorldBank)andthetimingofadoption,justaheadoftheRio2012conferenceonsustainabledevelopment.

Second,inframingthescopeoftheSEEACentralFramework,themembersoftheUNCEEAdeterminedthatsometechnicalaspectsofnaturalcapitalaccountingwereunlikelytogetbroad-basedsupport,particularlythevaluationofenvironmentaldegradation(asdistinctfromvaluingthedepletionofindividualresourcessuchastimberandfishresources).They,therefore,splitthedraftingoftechnicalmaterialintwo–theSEEACentralFrameworkontheonehandandasecondvolumethatbecameknownastheSEEAExperimentalEcosystemAccounting.

Inthissecondvolume,avarietyofissueswerebroughttogether,and,withouttherequirementtodevelopaninternationalstatisticalstandard,abroaderframingofnaturalcapitalaccountinginanationalaccountscontextwasundertaken.Thetimingoftheworkwasespeciallyimportantinthiscontext,asitwaspossiblefortheSEEAdiscussiononecosystemaccountingtotakeintoconsiderationtheemergingworkonecosystemservicesandecologicaleconomics.Theadvancesintheseareas–whichgainedmomentumafter2000–providedaready-madeacademiccommunityinterestedininter-disciplinaryworkandwhowerealsomakingconnectionsbetweentheenvironmentandtheeconomy.

Thesetwofactors,combinedwiththeincreasingrecognitionofdecliningnaturalcapital,havemeantthat:

• thethinkingoutlinedinSEEAExperimentalEcosystemAccountinghasbenefitedfromsubstantialinputfrommanynon-statistical,non-nationalaccountingexperts,includingeconomists,ecologistsandgeographers;

• theprocessfordevelopingandadvancingSEEAExperimentalEcosystemAccountinghasprovidedaplatformfortheseexpertstoengage;and

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

• thereistheopportunityfornationalaccounting-basedapproachestobeconsideredinotherapproachesandprojectsonnaturalcapitalassessment.

AproductofthisbroaderengagementhasbeenanincreaseinthenumberofacademicpapersandrelatedwritingfromtheexistingSEEAcommunityadmittedlyfromalowbase.ThepapersbyEdensandHein(2013)andObstandVardon(2014)areexamplesofthisdirection.Inmanywaysthispaperisaimedatestablishingfurtherconnectionsinthisimportantareaofworkandreflectstheinter-disciplinarydynamicthatmustbenurtured.

4.TheSEEA2012

Inlightofthisshorthistoryofnaturalcapitalaccountingasdevelopedthroughthechannelofofficialstatisticsandnationalaccounting,thissectionbrieflysummarizesthekeyelementsoftheapproachdescribedintheSEEA2012.TheSEEA2012comprisesthreevolumes:

• theSEEA2012CentralFramework;

• SEEA2012ExperimentalEcosystemAccounting;and

• SEEA2012ApplicationsandExtensions(UnitedNations,2014).

ThethirdvolumefocusesonwaysinwhichdataorganizedfollowingtheaccountingframeworkdescribedintheSEEACentralFrameworkcanbeappliedtotheanalysisofvariouspolicyquestionsandlinkedtootherdatasets.Thisvolumeisnotdiscussedfurtherinthispaper.

Thefocushereisonadescriptionoftheaccountingcontentofthefirstandsecondvolumesthatcollectivelyprovideacomprehensiveapproachtotheintegrationofenvironmentalinformationwithinformationonthemeasurementofeconomicactivityandwealth.

ThissectionprovidesasummaryofthemainaspectsofSEEA2012,includingtheaccountingprinciplesthatareappliedandadescriptionofthemaintypeofaccountswithinscope,namely:

• physicalflowaccountsforsubstancessuchaswater,energyandemissions;

• assetaccountsforresources(suchasmineralandenergyresources,timberandfishstocks);

• accountsformeasuringchangesinlandandecosystems;

• accountingforenvironmentaltransactions(includingenvironmentalprotectionexpenditure,environmentalgoodsandservices,environmentaltaxesandsubsidies);and

• asequenceofaccountsandaccountingfordepletionanddegradation.

FurtherdetailsinalloftheseareasofaccountingareprovidedintherelevantSEEA2012volume.

4.1Accountingprinciples[2]

Tofacilitatetheintegrationofenvironmentalandeconomicinformation,theSEEAusesasitsbasetheaccountingprinciplesoftheSNA.Amongthekeyprinciplesarequadrupleentryaccounting(wherebyeachtransactionisrecordedintheaccountsofthesupplierandconsumerinboththeirrealandfinancialaccounts),recordingonanaccrualbasisandvaluationattransactionorexchangevalues.

TheSEEACentralFrameworkdescribeshowtheseprinciplescanbeappliedinaccountingforstocksandflowsmeasuredinphysicalquantities(e.g.tonnesoftimber,cubicmetersofwater)byrecognizingthatthereisanunderlyingphysicalrealitytoeconomicactivity.Inthiscontext,

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

accountingapproachesprovideasetofrelationshipsbetweeninformationonstocksandflowsthatcanbeappliedinsituationswheredataarenotavailableinmonetaryunits.

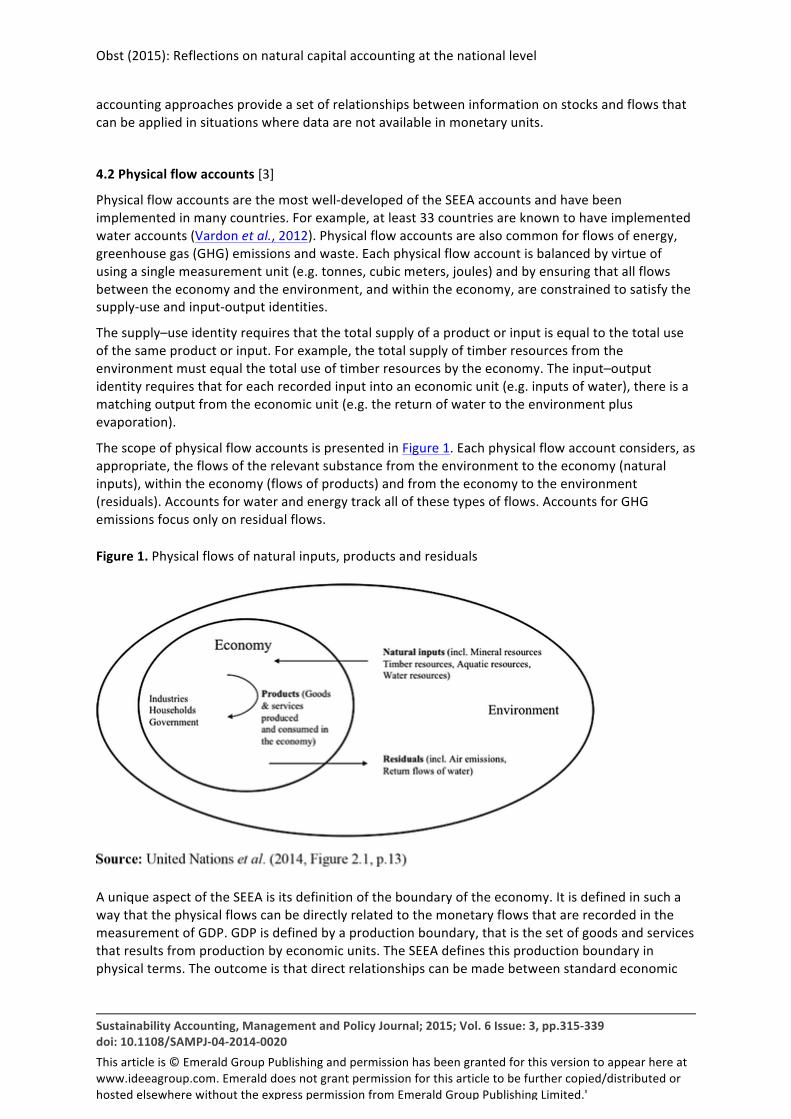

4.2Physicalflowaccounts[3]

Physicalflowaccountsarethemostwell-developedoftheSEEAaccountsandhavebeenimplementedinmanycountries.Forexample,atleast33countriesareknowntohaveimplementedwateraccounts(Vardonetal.,2012).Physicalflowaccountsarealsocommonforflowsofenergy,greenhousegas(GHG)emissionsandwaste.Eachphysicalflowaccountisbalancedbyvirtueofusingasinglemeasurementunit(e.g.tonnes,cubicmeters,joules)andbyensuringthatallflowsbetweentheeconomyandtheenvironment,andwithintheeconomy,areconstrainedtosatisfythesupply-useandinput-outputidentities.

Thesupply–useidentityrequiresthatthetotalsupplyofaproductorinputisequaltothetotaluseofthesameproductorinput.Forexample,thetotalsupplyoftimberresourcesfromtheenvironmentmustequalthetotaluseoftimberresourcesbytheeconomy.Theinput–outputidentityrequiresthatforeachrecordedinputintoaneconomicunit(e.g.inputsofwater),thereisamatchingoutputfromtheeconomicunit(e.g.thereturnofwatertotheenvironmentplusevaporation).

ThescopeofphysicalflowaccountsispresentedinFigure1.Eachphysicalflowaccountconsiders,asappropriate,theflowsoftherelevantsubstancefromtheenvironmenttotheeconomy(naturalinputs),withintheeconomy(flowsofproducts)andfromtheeconomytotheenvironment(residuals).Accountsforwaterandenergytrackallofthesetypesofflows.AccountsforGHGemissionsfocusonlyonresidualflows.

Figure1.Physicalflowsofnaturalinputs,productsandresiduals

AuniqueaspectoftheSEEAisitsdefinitionoftheboundaryoftheeconomy.ItisdefinedinsuchawaythatthephysicalflowscanbedirectlyrelatedtothemonetaryflowsthatarerecordedinthemeasurementofGDP.GDPisdefinedbyaproductionboundary,thatisthesetofgoodsandservicesthatresultsfromproductionbyeconomicunits.TheSEEAdefinesthisproductionboundaryinphysicalterms.Theoutcomeisthatdirectrelationshipscanbemadebetweenstandardeconomic

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

accountingmeasuressuchasoutputandvalueadded,andphysicalmeasuressuchaswaterandenergyuse,andGHGemissions.

Thisuniqueaspectmaybeparticularlyimportantwherethephysicaldatasets(e.g.GHGemissioninventories)arecommonlycollectedwithoutconsiderationoftheprecisemeasurementscopeoftheeconomy.

Importantly,thephysicalflowaccountsoftheSEEAapplystandardproduct,industryandinstitutionalsectorclassificationssuchthateconomicdataandenvironmentalinformationcanbereadilycompared.Thisallowsstraightforwardandcorrectdefinitionofproductivityandintensityindicatorswherephysicalflowsarecomparedtoeconomicvariablessuchasvalueaddedandoutput.Further,withphysicaldatastructureandscopefollowingtheSEEA,extensionstoinput–outputtablesaremorestraightforward,thussupportingthederivationoffootprintandsimilarcalculations.ThegenericstructureofSEEAphysicalflowaccountsisshowninTableI.

Table1.Basicformofaphysicalsupplyandusetable

4.3Accountingforenvironmentalassets[4]

AccountingforenvironmentalassetsisattheheartoftheSEEA.Fromameasurementperspectivehowever,environmentalassetscanprovedifficulttodefineand,commonly,varyingtermsanddefinitionsareusedwithoutaclearunderstandingofthelinkstostandardmeasuresofeconomicassetsasdefinedintheSNA.Doublecountingormeasurementgapsarethereforerealrisks.TheSEEACentralFrameworkaimstobringclaritytothisareaofaccounting.

Inthefirstinstance,environmentalassetsaredefinedbroadlytoencompassthewholeofthebiophysicalenvironment.Thus,“Environmentalassetsarethenaturallyoccurringlivingandnon-livingcomponentsoftheEarth,togetherconstitutingthebiophysicalenvironment,whichmayprovidebenefitstohumanity”(UnitedNationsetal.,2013,2.17,p.13).

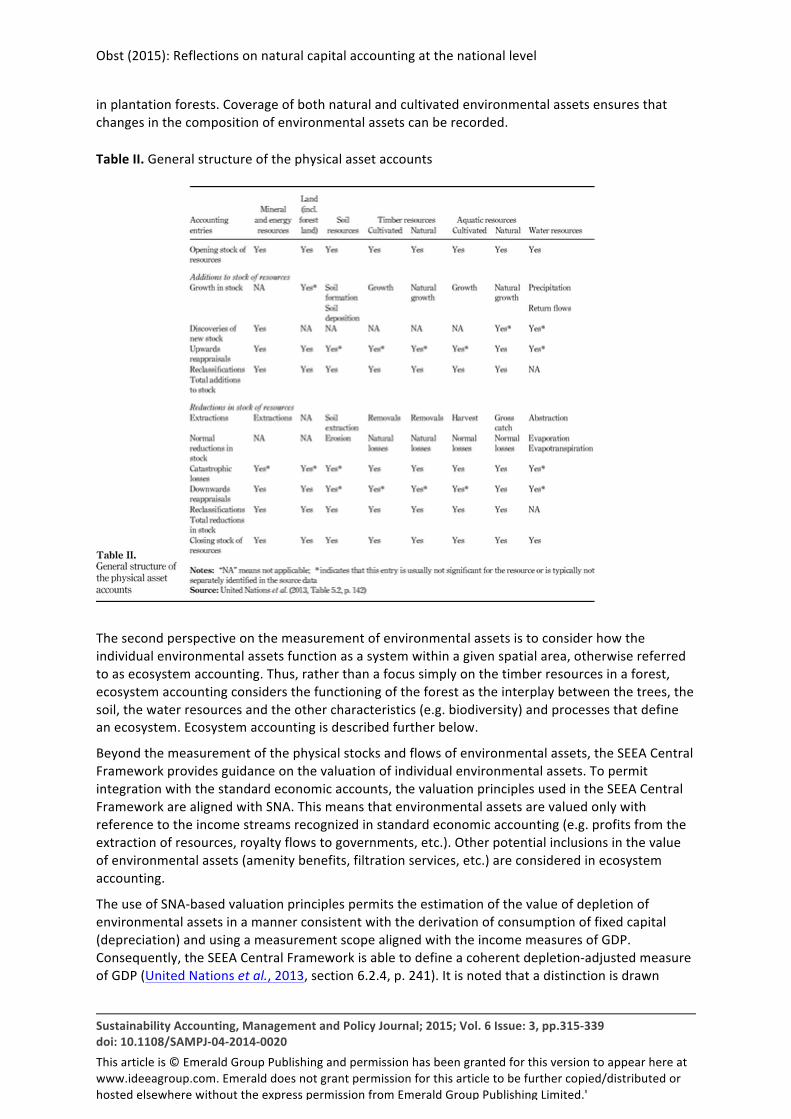

Itisthenrecognizedthatformeasurementpurposes,thisdefinitionmaybetackledfromtwodifferentbutcomplementaryperspectives.Inthefirstperspective,variouscomponentsofthebiophysicalenvironmentaremeasuredasindividualenvironmentalassets.Thesecomponentsincludemineralandenergyresources,soilresources,timberresources,fishandaquaticresources,otherbiologicalresourcesandwaterresources.AssetaccountsthatrecordtheopeningandclosingstocksoftheseresourcesandtheadditionsandreductionsinstockaredescribedintheSEEACentralFramework.ExamplesofthetypesofaccountingentriesareshowninTableII.

Importantly,themeasurementscopeofindividualenvironmentalassetsisnotlimitedtopurelynaturalresourcesandhenceincludes,forexample,fishinaquaculturefacilitiesandtimberresources

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

inplantationforests.Coverageofbothnaturalandcultivatedenvironmentalassetsensuresthatchangesinthecompositionofenvironmentalassetscanberecorded.

TableII.Generalstructureofthephysicalassetaccounts

Thesecondperspectiveonthemeasurementofenvironmentalassetsistoconsiderhowtheindividualenvironmentalassetsfunctionasasystemwithinagivenspatialarea,otherwisereferredtoasecosystemaccounting.Thus,ratherthanafocussimplyonthetimberresourcesinaforest,ecosystemaccountingconsidersthefunctioningoftheforestastheinterplaybetweenthetrees,thesoil,thewaterresourcesandtheothercharacteristics(e.g.biodiversity)andprocessesthatdefineanecosystem.Ecosystemaccountingisdescribedfurtherbelow.

Beyondthemeasurementofthephysicalstocksandflowsofenvironmentalassets,theSEEACentralFrameworkprovidesguidanceonthevaluationofindividualenvironmentalassets.Topermitintegrationwiththestandardeconomicaccounts,thevaluationprinciplesusedintheSEEACentralFrameworkarealignedwithSNA.Thismeansthatenvironmentalassetsarevaluedonlywithreferencetotheincomestreamsrecognizedinstandardeconomicaccounting(e.g.profitsfromtheextractionofresources,royaltyflowstogovernments,etc.).Otherpotentialinclusionsinthevalueofenvironmentalassets(amenitybenefits,filtrationservices,etc.)areconsideredinecosystemaccounting.

TheuseofSNA-basedvaluationprinciplespermitstheestimationofthevalueofdepletionofenvironmentalassetsinamannerconsistentwiththederivationofconsumptionoffixedcapital(depreciation)andusingameasurementscopealignedwiththeincomemeasuresofGDP.Consequently,theSEEACentralFrameworkisabletodefineacoherentdepletion-adjustedmeasureofGDP(UnitedNationsetal.,2013,section6.2.4,p.241).Itisnotedthatadistinctionisdrawn

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

betweenthedepletionofanindividualenvironmentalasset(e.g.thedepletionofoilandgasresources)andthedegradationofenvironmentalassetswherethebroaderdeclineinqualityandconditionofanecosystemisinevidence.Conceptually,themeasurementofdegradationisfarmorechallengingthanaccountingfordepletion.

Accountingforenvironmentalassetsmaybeofdirectuseinnaturalresourcemanagementandinassessmentofsustainableincomesandproductionofprimaryindustries.Further,asthevaluationapproachappliedisconsistentbetweendifferentnaturalresourcesandwithproducedassetssuchasbuildingsandequipment,itispossibletoaggregatethevaluesofdifferentassetstoobtainmeasuresofnetworthatthesectorandnationallevel.

4.4Accountingforlandandecosystems[5]

Accountingforlandisseenasdistinctfromthemeasurementofindividualenvironmentalassetssuchastimber,waterandsoil.IntheSEEA,landisseenasreflectingthespacewithinwhicheconomicactivitytakesplaceandenvironmentalassetsaresituated.IntheSEEACentralFramework,accountingforlandcomprisesaccountingforchangesinthecompositionoflanduseandlandcoverwithinacountry,notingthatchangesintheoverallareaofacountryarelikelytoberelativelyinfrequentaccountingconsiderations.

Accountingforecosystems,asintroducedabove,iseffectivelyanextensionoflandaccounting.Itaimstoaccountforthechangeinqualityorconditionofacountry’sspatialareas,wherethespatialareasmaybeclassifiedindifferentways:

• bytypeofecosystem(e.g.forests,wetlands,agriculturalland);

• byadministrativeunits;or

• bysomeothercriteria(e.g.rivercatchmentareas).

Declinesinecosystemconditionduetoeconomicorhumanactivitymaybeconsideredtoconstitutedegradation.

Inaddition,ecosystemaccountingcomplementsthemeasurementofecosystemassetsbyaccountingfortheecosystemservicesgeneratedbythoseassets.Ingeneralterms,thisisanapplicationofthestandardaccountingrelationshipbetweenincomeandcapital.Inlinewiththegeneraldirectionofworkonmeasuringecosystemservices,asinprojectssuchastheMillenniumEcosystemAssessment(MA,2005),TheEconomicsofEcosystemsandBiodiversity(TEEB,2010)andtheEuropeanUnion’sMappingandAssessmentofEcosystemsandtheirServices(Maesetal.,2013),SEEAExperimentalEcosystemAccountingrecognizesthatthescopeofecosystemservicesisbroaderthanthecontributionsthatecosystemsmaketothegenerationofgoodsandservicesmeasuredinGDP.Thus,thereareservices,suchascarbonsequestrationandstorage,floodprotection,waterpurificationandculturalservices(amongmanyothers),thatshouldberecognizedinacompleteaccountingsystem.ThecorollaryofextendingthescopeofecosystemservicesbeyondcontributionstoGDPisthattheproductionandincomeboundariesareenlargedcomparedtoGDPandthepotentialvalueofenvironmentalassetsisincreasedrelativetothestandardvaluationsofenvironmentalassetsdefinedfollowingtheSNAandtheSEEACentralFramework.

AlargenumberofaspectsofaccountingforecosystemsandecosystemserviceshavebeendescribedinSEEAExperimentalEcosystemAccountingbysynthesizingawiderangeofworkinthisarea.Nonetheless,thereremainmanymeasurementchallenges.Thesemeasurementchallengeslargelyreflectthefactthattherelationshipbetweentheincome(ecosystemservices)andthecapital(ecosystemassets)isfarmoremulti-facetedthanforstandardeconomicassetssuchasbuildingsand

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

machines.Thatis,ecosystemassetswilltendtohavemultipleownersandbeneficiariesandcangenerateavarietyofmixes(orbaskets)ofecosystemservices.

Thesecharacteristicsofecosystemshavetwoparticularaccountingimplications.First,itisnotstraightforwardtoassignthecostofanydegradationtoeconomicunits,asoneeconomicunit’suseofanassetmayhaveimpactsonmultipleeconomicunits.Second,forassetvaluationpurposes(andhencetoobtainestimatesofthevaluationofdegradation),itisnecessarytoassumeafuturepatternofuseoftheecosystembymultipleusersofmultipleecosystemservices.Bothimplicationsarenotconfrontedinstandardaccountingforproducedassetsthathavesingleowners/usersandsinglestreamsofincome.

Themainrationaleforlandandecosystemaccountingistheassessmentoftrade-offsinsituationswhereareasoflandmaybeusedfordifferentpurposes.Ifdecisionsaremadesolelyonthebasisofincomefromeconomicproduction,thetrade-offagainstotherbenefitsthatmaybeobtainedbutwhicharemoreofapublicgoodcharacterwillnotberecognized.Supportingtheassessmentoftrade-offsinforestrybetweentimberproductionandthebenefitsofcarbonsequestrationandwaterpurificationisanexampleofthetypeofdecisionthatmaybesupportedfromthistypeofaccounting.Landandecosystemaccountingshouldalsosupportmorestructuredreportingonoverallenvironmentalcondition.

4.5Accountingforenvironmentaltransactions[6]

Thepredominantfocusinnaturalcapitalaccountingisonintegratingenvironmentalinformationintostandardeconomicaccounts.However,alsoofinterestisthepotentialtogleaninformationfromstandardeconomicaccountsaboutactivitiesundertakenbyeconomicunitsthatmaybeconsidered“environmental”.

Tothisend,theSEEACentralFrameworkdefinestheenvironmentalactivitiesofenvironmentalprotectionandresourcemanagementasconstitutingascopethatcanbeusedtoclassifyvariousstandardeconomicflowssuchasoutput,valueadded,investmentandemployment.TheSEEACentralFrameworkdefinesenvironmentalprotectionexpenditureaccountstorecordexpendituresbygovernments,householdsandbusinessesthathavethepurposeofmaintainingorimprovingtheenvironment.TheSEEACentralFrameworkalsodefinestheEnvironmentalGoodsandServicesSectorandanassociatedsetofindicatorsthatmaybeusedtoprovideongoingestimatesofoutputandemploymentinenvironmentalactivitiesasashareofoveralleconomicactivity.

Tofurtheraidassessmentofthepolicyresponsetoenvironmentalissues,thisareaofaccountingprovidesdefinitionsforenvironmentaltaxesandenvironmentalsubsidiesandsimilartransfers.Particularlyataninternationallevel,consistentdefinitionofthesetypesofvariablespermitsanassessmentofalternativepolicyresponses.

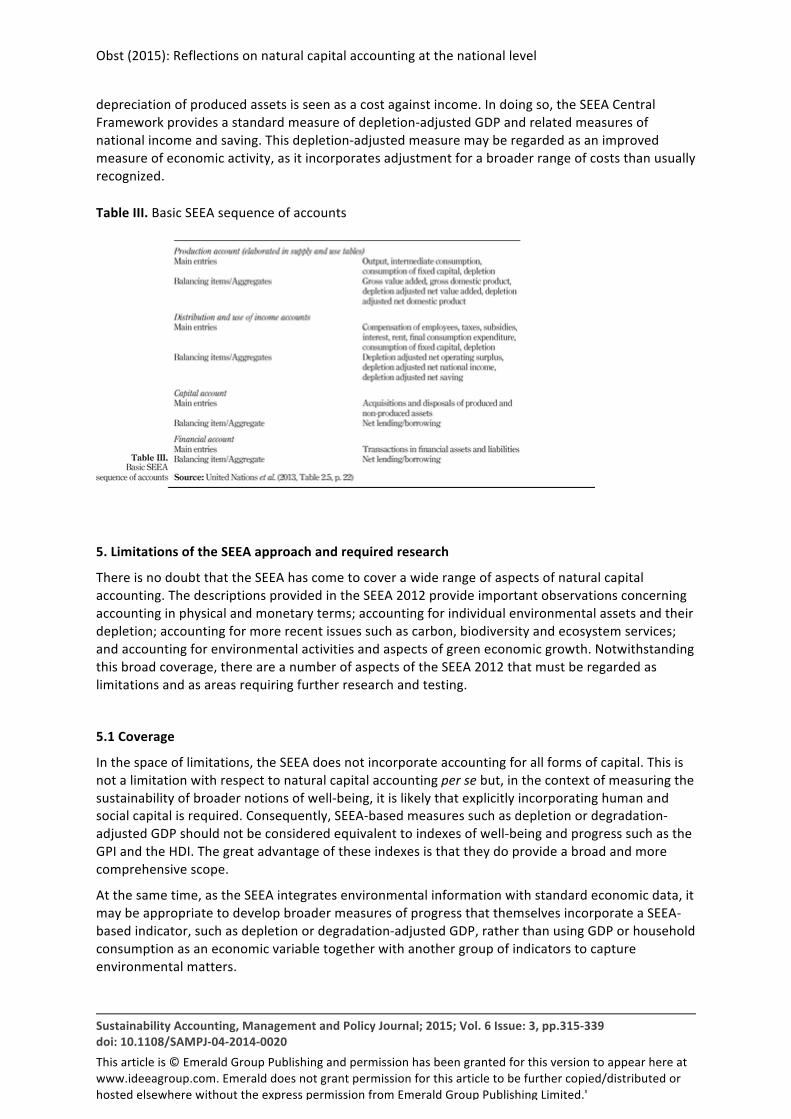

4.6Thesequenceofenvironmentalaccounts[7]

Oneofthestrengthsofaccountingframeworksistheirabilitytodrawtogetherawiderangeofinformationinacomplementaryandinternallyconsistentway.Thisstrengthisdemonstratedinthedescriptionoftheconnectionsbetweenthedifferenttypesofaccounts,knowninnationalaccountingasthesequenceofaccounts.Thetypicalsequenceofaccounts,asshowninTableIII,linksproduction,income,consumption,saving,capitalformation,financialtransactionsandbalancesheets.

TheSEEACentralFrameworkaugmentsthestandardsequenceofnationalaccountspresentedintheSNAbyrecordingdepletionofenvironmentalassetsasacostagainstincomeinthesamewayasthe

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

depreciationofproducedassetsisseenasacostagainstincome.Indoingso,theSEEACentralFrameworkprovidesastandardmeasureofdepletion-adjustedGDPandrelatedmeasuresofnationalincomeandsaving.Thisdepletion-adjustedmeasuremayberegardedasanimprovedmeasureofeconomicactivity,asitincorporatesadjustmentforabroaderrangeofcoststhanusuallyrecognized.

TableIII.BasicSEEAsequenceofaccounts

5.LimitationsoftheSEEAapproachandrequiredresearch

ThereisnodoubtthattheSEEAhascometocoverawiderangeofaspectsofnaturalcapitalaccounting.ThedescriptionsprovidedintheSEEA2012provideimportantobservationsconcerningaccountinginphysicalandmonetaryterms;accountingforindividualenvironmentalassetsandtheirdepletion;accountingformorerecentissuessuchascarbon,biodiversityandecosystemservices;andaccountingforenvironmentalactivitiesandaspectsofgreeneconomicgrowth.Notwithstandingthisbroadcoverage,thereareanumberofaspectsoftheSEEA2012thatmustberegardedaslimitationsandasareasrequiringfurtherresearchandtesting.

5.1Coverage

Inthespaceoflimitations,theSEEAdoesnotincorporateaccountingforallformsofcapital.Thisisnotalimitationwithrespecttonaturalcapitalaccountingpersebut,inthecontextofmeasuringthesustainabilityofbroadernotionsofwell-being,itislikelythatexplicitlyincorporatinghumanandsocialcapitalisrequired.Consequently,SEEA-basedmeasuressuchasdepletionordegradation-adjustedGDPshouldnotbeconsideredequivalenttoindexesofwell-beingandprogresssuchastheGPIandtheHDI.Thegreatadvantageoftheseindexesisthattheydoprovideabroadandmorecomprehensivescope.

Atthesametime,astheSEEAintegratesenvironmentalinformationwithstandardeconomicdata,itmaybeappropriatetodevelopbroadermeasuresofprogressthatthemselvesincorporateaSEEA-basedindicator,suchasdepletionordegradation-adjustedGDP,ratherthanusingGDPorhouseholdconsumptionasaneconomicvariabletogetherwithanothergroupofindicatorstocaptureenvironmentalmatters.

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

WhiletheSEEAdoesnotincorporatehumanandsocialcapital,fromanaccountingperspective,someimportantadvancesinthisareahavebeenmadethroughtheavenueofwealthaccounting,asnotedinSection2.ItshouldbepossibletoseeimprovedconnectionsbetweenthewealthaccountingworkandtheworkbeingundertakenfortheSEEA,asitpertainstothemeasurementofnaturalcapital.Inparticular,theorganizationofinformationonthestockandchangesinstockofenvironmentalassetsinnon-monetarytermsusingtheSEEAshouldbeofdirectuseinthecompilationofwealthaccountingestimates.

Broadeningaccountingframeworkstoencompassso-calledmultiplecapitalsisalsobeingpursuedatacorporatelevelthroughtheworkoftheIntegratedInternationalReportingCouncil(IIRC)(IIRC,2013).Ofnote,incomparisontotheworkoftheSEEA,theIIRC’sintegratedreportingframeworkdoesnotdefineexplicitmeasurementorreportingboundariesforeachofitssixformsofcapital.Thishighlightsthelikelychallengesinfullyaccountingforallformsofcapital,astherearelikelytobeimportanttrade-offsbetweencapitaltypes(e.g.betweenproducedandhumancapital)andinter-dependencies(e.g.betweennaturalcapitalandhumanhealth/capital).

Theseissuesbecomeclearwhendefiningthescopeofvaluationfordifferentformsofcapital,which,foraccountingpurposes,requiresaclearlinkbetweenaflowofbenefitsandanunderlyingasset.Itislikelythatsomebenefitswillreflectacombinationofinputsfromdifferentformsofcapital,andhence,thedefinitionandattributionofvaluetospecificcapitaltypesislikelytobechallenging.

5.2Spatialscale

TheSEEAhasbeendesignedforapplicationatanationallevel.Thenatureoftheapproachisthustoenableconsistentrecordingofdifferentenvironmentalstocksandflowsacrossmultiplelocationsandecosystemtypes.Forexample,theassetaccountsfordifferentenvironmentalassetstakethesameformandthesupplyandusetablesforenergy,waterandotherenvironmentalflowsallusethesameSNAproductionboundarytodelineatetheenvironmentandtheeconomy.WhilethisapproachworkswellinthecontextoftheSEEACentralFramework,itisfarmorechallengingtoapplyatthelevelofecosystemswhicharemuchhardertodefineinspatialterms.Importantly,oneissuethathasnotbeenresolvedintheSEEAExperimentalEcosystemAccountingmodelishowbesttorecordthemultipleandoftenunknownecologicaldependenciesbetweendifferentecosystems.Whileatoneleveltheeffectofnotfullyarticulatingthesedependenciesmaynetoutatnationallevel,thisisnotstrictlythecaseandalsomakestheapplicationofthemodeltocorporateandgloballevelschallenging.Thisisanimportantareaoffutureresearch.

5.3Valuation

Valuationiscommonlyacontentiousissueinnaturalcapitalaccountingwithsomeviewingvaluationofenvironmentalassetsandtheirservicesasthecommodificationofnatureandhencenotconducivetoimproveddecisionmaking(McAffe,1999;KosoyandCorbera,2010),whileothersconsiderthatunlessthereisvaluation,therecannotbeintegrationormainstreamingofnaturalcapitalconsiderations(Costanzaetal.,1997;TEEB,2010;WorldBank,2011).TheSEEAhasthereforetrodacarefulline.Itisundoubtedlythecasethatfullintegrationwiththestandardeconomicaccountsrequiresvaluationofenvironmentalstocksandflows.Atthesametime,thereisasignificantamountofinformationinphysicaltermsonenvironmentalstocksandflowsthatmaybebetterorganizedinamannerconsistentwitheconomicdata(e.g.usingstandardindustryclassifications).Informationinphysicalterms,compiledregularlyovertimewithinanaccountingframework,wouldsupporttheprocessofmainstreamingthisinformationintodecisionmaking.Thismightinclude,forexample,integrationofphysicalinformationonnaturalcapitalintoriskmanagementframeworks.

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

Whenvaluationisundertaken,thereisnodoubtthatitisadifficulttask,astransactionsinenvironmentalassetsandservicesarenotgenerallyobservable.Notwithstandingthepracticaldifficulties,theSEEAtakesaparticularviewonvaluationrequiringthatforintegrationpurposes(withthestandardeconomicaccounts),itisnecessarytouseexchangevalues–i.e.thepricesatwhichtheassetsorserviceswouldbeexchangedifamarketexisted(SEEAExperimentalEcosystemAccounting,5.9).Thisconceptionofvalueisdifferentfromthatusedforeconomicanalysiswherethefocusiscommonlyonthechangeineconomicwelfareassociatedwithdifferentusesoftheenvironment.Welfare-basedvaluesarerelatedtoexchangevaluesusedforaccountingbutalsoincludeconsumersurplus,i.e.theadditionalbenefitthatconsumers/purchasersobtainbypayinglessthantheywouldhavebeenwillingtopayfortheasset,goodorservice.

Whilethisdistinctionbetweenwelfareandexchangevaluesisrecognizedbypractitioners(Batemanetal.,2011),mostfocusinthedevelopmentofenvironmentalvalueshasbeenfromawelfareperspectiveandonlyasub-setofmethodsexplicitlytargettheestimationofexchangevaluesforenvironmentalgoodsandservices.

Eventhoughexchangevaluesmaybetheappropriatevaluesforaccountingpurposes,theexclusionofconsumersurplusmeansthattherearesomeaspectsoftheenvironmentthatarelesslikelytobecapturedinaccountingframeworks.Forexample,valuesincludingconsumersurplusarelikelytoberelevantinbetterunderstandingourextensiveculturalconnectionstotheenvironmentandvariousintrinsicenvironmentalvalues.Whetherandhowsuchaspectsmightbeincorporatedintoaccountingframeworksisanimportantquestion.

5.4ResearchagendasoftheSEEA

BoththeSEEACentralFrameworkandSEEAExperimentalEcosystemAccountingcontainresearchagendas.Theyhighlightimportantissuesrequiringfurtherinvestigationanddeliberation.Someissuesconcernmeasurementandintegration,suchastheneedforwidelyadoptedinternationalclassificationsoflanduse,landcoverandecosystemtypestosupporttime-seriesandcross-countrycomparisons.Otherissuesrelatetoparticulartopicareaswheretheapplicationofaccountingprinciplesisnotwell-establishedorhassomeparticularchallenges.Examplesofthisincludeaccountingforsoilresources,thevaluationofwaterresourcesandaccountingforbiodiversity.

Afinalsetofissuesrelatestoestablishingamorecompleteintegrationofenvironmentalstocksandflowswiththestandardeconomicaccounts.Aparticularchallengehereisthedefinitionandtreatmentofecosystemdegradation.Thisarearequiresadditionaldiscussiontoconsiderboththevaluationofnon-marketenvironmentalflowsandhowthewell-establishedareaofexternalitiesfromeconomicscanbeappliedmosteffectivelywithinanationalaccountingsetting.

Inadditiontothesetheoreticalandconceptualmatters,awidearrayofpracticalchallengesexist(suchasthemeasurementofecosystemservicesandtheconditionofecosystemassets),anditisessentialthateffortstotestthecurrentdescriptionsofSEEAandrelatednaturalcapitalaccountingstandardsaresupported.Oneofthelessonsoverthepast20yearsfromthosecountriesthathavebeentestingvariousiterationsoftheSEEAhasbeenthattherearesubstantialbenefitssimplyfromattemptingtheaccountingapproach.Learningbydoingisverytrueintheaccountingspace.

6.Futuredirectionsfornaturalcapitalaccounting

Fromanofficialstatisticsperspective,theadoptionoftheSEEACentralFrameworkasaninternationalstatisticalstandardhasprovidedrenewedenergytotheintegrationofenvironmentalinformationintostandardeconomicmeasurementandaccounting.Thisintegrationisseenascentraltotheprocessofmainstreamingthediscussionofnaturalcapital,particularlyineconomic

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

andplanningpolicydiscussion.TherearemanydirectandrelatedinitiativestowhichtheSEEAisrelated,andthissectionprovidesasenseofjustsomeofthenaturalcapitalaccountingworkthatisunderway.

TheSEEACentralFramework’sstatusasastatisticalstandardobligestheUnitedNationsandotherinternationalagenciestoencourageandfacilitatethedevelopmentofstatisticalprogramsthatintroduceandmaintainnaturalcapitalaccountingatthenationallevel.Atthisstage,thereisnomandatoryreporting,butcountriesareencouragedtoadoptaflexibleandmodularapproachtotheimplementationofthestandards,takingintoaccountrelevantpolicycontexts,dataavailabilityandstatisticalcapacity(UnitedNationsetal.,2013,p.9).

Inthissetting,theUNSDhascommencedaprogramofraisingawarenessandsupportfortheimplementationofSEEA,includingdraftinganoverarchingimplementationguide(UnitedNations,2013)anddevelopingtrainingmaterial.UNSDalsohasrecentlycommencedajointprogramofworkwiththeUnitedNationsEnvironmentProgram(UNEP)andtheSecretariatoftheConventiononBiologicalDiversity(CBD)toadvanceecosystemaccountinginsevencountries–Bhutan,Indonesia,Vietnam,SouthAfrica,Chile,MexicoandMauritius.

AnaturalcapitalaccountingprogramthatisbeingadvancedbytheWorldBankisitsWealthAccountingandValuationofEcosystemServices(WAVES)initiative.TheWAVESprogramisdirectedatministriesoffinanceandplanningencouragingthemtoadoptnaturalcapitalaccountingasacentralpartoftheirpolicydevelopment.Therearecurrentlyeightimplementingcountries(WorldBank,2014).TheWAVESprogramadoptstheSEEAasitstechnicalguidanceforaccounting.

Stillattheinternationallevel,closeconnectionsarebeingdrawnbetweenthenaturalcapitalaccountingoutlinedintheSEEAandthedevelopmentofindicatorsforthesustainabledevelopmentgoals(SDGs)beingestablishedaspartoftheUnitedNationsPost-2015DevelopmentAgenda.Theconnectionhereisthatnaturalcapitalaccountingcanprovidetheorganizingframeworkforinformationoneconomic-environmentallinkagesandthuscanserveasabaseforimprovedmeasurementandassessmentinrelationtoanumberofdifferentSDGs.ThisisaparticularlyrelevantdevelopmentintheambitiontogobeyondGDPinassessingwell-beingandprogress,andinmeetingoneoftheobjectivesoftheCBD’sAichitargetstointegratebiodiversityintonationalaccountingby2020.

Inthecorporatesector,thereisanincreasingappetiteforintegratingenvironmentalinformationincorporatemeasurement,assessmentandreporting.BroadinitiativesincludetheworkoftheGlobalReportingInitiative(GRI),andtheInternationalIntegratedReportingCouncil(IIRC).ThereisspecificworkonnaturalcapitalaccountingprotocolsbytheNaturalCapitalCoalitionandaspartoftheUnitedNationsEnvironmentProgram–FinanceInitiative(UNEP-FI).Overall,whiletherearesomedifferencesbetweenaccountingatthenationalandcorporatelevel,themajorityoftheaccountingprinciplesarethesameandmuchofthethinkingunderpinningtheestablishmentofaccountingstandardsintheSEEAmaywellprovideabasisforthedraftinganddiscussionofsimilarstandardsatthecorporatelevel.Inturn,theworkthathasbeencompletedonaccountingfornaturalcapitalatthecorporatelevel,forexampletheenvironmentalprofitandlossstatementofPuma(2011),mayprovideinsightsintothechallengesthatremainfortheSEEA.

Anassociatedconsiderationisthat,onceimplemented,theSEEAislikelytoprovideindustry-levelbenchmarkinformationonenvironmentalstocksandflows.Suchbenchmarking(andinternationalcomparability)mayprovidearelevanttoolforcomparisonofcorporateaccountsandreports.Fromtheoppositeperspective,standardizedcorporatereportingcouldprovideveryusefulinputtonational-levelaccountingfortheseenvironmentaldimensions.Anotheravenueofcollaborationmaybeinthedevelopmentofdecision-makingsupporttools–suchasriskmanagementframeworks–intowhichnaturalcapitalconsiderationsneedtobeincorporated.

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

Alongsidethesepositivepotentialconnections,itmustberecognizedthatcorporateinitiativessuchastheIIRCandGRIarethemselvessubjecttovariousconcerns.Flower(2015)raisesconcernsaboutthefocusoftheIIRCeffortsoverthepastfouryearsashavingbecomeoverlyfocusedonbroaderconceptionsofvaluefromtheperspectiveofcorporationsratherthanseekingtoembedbroadernotionsofsocietalvalueandcostsofcorporateactivitywithincorporateaccountingpractice.Adams(2014)rejectstheseconcerns,highlightingtheimportanceofcorporationsbuildingabroaderunderstandingoftheiroperationsanddependenciesonmultiplecapitals.Importantly,however,bothauthorsrecognizetherelevanceofaccountingmovingbeyonditstraditionalfinancialcapitalbase.

ItisinthisbroadeningoftraditionalaccountingthatconnectionsbeingmadebetweenSEEAandvariouscorporateaccountinginitiativescanbedevelopedfurtherandanalignmentofconcepts,terminologyandstandardsmightbefacilitatedtotheextentappropriate.

Fromanacademicperspective,therearesomeimportantconnectionsthatremaintobebetterestablished.Fromapurelydatasupplyside,afullypopulatedsetofSEEAdatawouldprovide,overtime,ahigherqualitysetofbaseinformationforalltypesofanalysisatnationalandinternationallevel,suchasinput–outputanalysis,computablegeneralequilibriumanalysisandlifecycleandsupplychainanalysis.Itwouldalsofacilitatecross-countrycomparisonsofenvironmentalsustainabilityissuesandhasthepotentialtolinktoarangeofsocialdata(e.g.accesstowaterandenergy,nutrition),thusfacilitatingenhancedassessmentofsustainabledevelopment.

Fromaresearchperspective,therearealsoarangeofpotentialareasofengagement.Particularlyintheareaofecosystemaccounting,thereismuchrequiredresearchandtestinginrelationtotheassessmentofecosystemcondition,integrationacrossspatialscales,themeasurementandvaluationofecosystemservices,thedefinitionofecosystemdegradationanditsallocationtoeconomicunitsandotherareas.TheSEEA’saccountingframeworkmightthusprovideawayinwhichthedifferentaspectsofecosystemresearchcanbeplacedincontextratherthanbeingseenasdistinct,andpossiblycompeting,approaches.

Finally,regardingimprovingmeasuresofprogress,Costanzaandcolleaguesintheirarticle“TimetoleaveGDPbehind”observethat:

ThesuccessortoGDPshouldbeanewsetofmetricsthatintegratescurrentknowledgeofhowecology,economics,psychologyandsociologycollectivelycontributetoestablishingandmeasuringsustainablewell-being(Costanzaetal.,2014).

Whiletherehavebeenmanyattemptstodevelopalternativemetricsbycombiningindicatorsfromvariousdomains,thesealternativeshavenotledtotheunderlyingintegrationofdatafromthesedifferentdomains.Consequently,theseindicatorsfindthemselvesstandingsomewhataloneandincompetitionwithGDPanditssupportingbodyofintegratedeconomicinformation.

TheworkonSEEAandotherrelateddevelopmentsinnaturalcapitalaccountinginrecentyearssuggeststhat,ingoingbeyondGDP,accountingapproachesmayprovideanotherwayforward.Thispotentialliesinthecapacityofaccountingapproachestointegratedifferenttypesofinformationinarigorousanddetailedway.Withtheintegrationofdatainplace,thederivationofalternativemeasuresthatcomplementGDPcanfollowandtherebyleadtothemainstreamingofbroadermeasuresofprogressusingwell-establishedandwell-acceptedmethods.Overall,accountingmaywellbeessentialinestablishingthenewmetricsthathavebeenrequiredforsolong.

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

References1.AdamsC.A.(2014),“Theinternationalintegratedreportingcouncil:acalltoaction”,CriticalPerspectivesonAccounting,Vol.27No.1.[GoogleScholar][Infotrieve]2.Ahmad,Y.,ElSerafy,S.andLutz,E.(Eds)(1989),EnvironmentalAccountingforSustainableDevelopment,TheWorldBank,Washington,D.C.[GoogleScholar]3.Asheim,G.B.andWeitzman,M.L.(2001),“DoesNNPgrowthindicatewelfareimprovement”,EconomicLetters,Vol.73No.2,pp.233-239.[GoogleScholar][CrossRef],[ISI][Infotrieve]4.AustralianBureauofStatistics(2012),“Completingthepicture–environmentalaccountinginpractice”,ABScat.no.4628.0.55.001.[GoogleScholar]5.Barbier,E.B.(2013),“Wealthaccounting,ecologicalcapitalandecosystemservices”,EnvironmentandDevelopmentEconomics,Vol.18No.2,pp.133-161.[GoogleScholar][CrossRef],[ISI][Infotrieve]6.Bartelmus,P.(1987),“BeyondGDP–Newapproachestoappliedstatistics”,ReviewofIncomeandWealth,Vol.33No.4,pp.347-358.[GoogleScholar][CrossRef][Infotrieve]7.Bartelmus,P.(2014),“What’sbeyondGDP?”,HumanDimensions,IHDP,Bonn,May.[GoogleScholar]8.Bateman,I.J.,Mace,G.M.,Fezzi,C.,Atkinson,G.andTurner,K.(2011),“Economicanalysisforecosystemserviceassessment”,EnvironmentalandResourceEconomics,Vol.48No.2,pp.177-218.[GoogleScholar][CrossRef],[ISI][Infotrieve]9.Bebbington,J.andLarrinaga,C.(2014),“Accountingandsustainabledevelopment:anexploration”,Accounting,OrganizationsandSociety,Vol.39No.6.[GoogleScholar][ISI][Infotrieve]10.Cobb,C.,Halstead,T.andRowe,J.(1995),“IftheGDPisup,whyisAmericadown?”,TheAtlanticMonthly,October,Vol.276,pp.59-78.[GoogleScholar]11.Costanza,R.,Arge,R.,deGroot,R.,Farberk,S.,Grasso,M.,Hannon,B.,Limburg,K.,Naeem,S.,O’Neill,R.V.,Paruelo,J.,Raskin,R.G.,Suttonkk,P.andvandenBelt,M.(1997),“Thevalueoftheworld’secosystemservicesandnaturalcapital”,Nature,Vol.387No.1,pp.253-260.[GoogleScholar][CrossRef],[ISI][Infotrieve]12.Costanza,R.,Hart,M.,Posner,S.andTalberth,J.(2009),“BeyondGDP:theneedfornewmeasuresofprogress”,ThePardeePapers,No4,January2009,TheFrederickS.PardeeCenterfortheStudyoftheLonger-RangeFuture,BostonUniversity.[GoogleScholar]13.Costanza,R.,Kubiszewski,I.,Giovannini,E.,Lovins,H.,McGlade,J.,Pickett,K.E.,Ragnarsdottir,K.V.,Roberts,D.,DeVogli,R.andWilkinson,R.(2014),“TimetoleaveGDPbehind”,Nature,Vol.505No.7483,pp.283-285.[GoogleScholar][CrossRef],[ISI][Infotrieve]14.Dasgupta,P.(2009),“Thewelfareeconomictheoryofgreennationalaccounts”,EnvironmentalandResourceEconomics,Vol.42No.1,pp.3-38.[GoogleScholar][CrossRef],[ISI][Infotrieve]

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

15.DeHaan,M.andKeuning,S.J.(1996),“Takingtheenvironmentintoaccount:theNAMEAapproach”,ReviewofIncomeandWealth,Vol.42No.2,pp.132-148.[GoogleScholar][Infotrieve]16.Edens,B.andHein,L.(2013),“Towardsaconsistentapproachforecosystemaccounting”,EcologicalEconomics,Vol.90No.1,pp.41-52.[GoogleScholar][CrossRef],[ISI][Infotrieve]17.EuropeanCommissionandInternationalMonetaryFund(2003),“Organisationforeconomicco-operationanddevelopment,UnitedNationsandWorldBank”,HandbookofNationalAccounting:IntegratedEnvironmentalandEconomicAccounting,StudiesinMethods,SeriesF,No61Rev1,whitecoveredition,UnitedNations,NewYork.[GoogleScholar]18.EuropeanCommissionandInternationalMonetaryFund(2009),“Organisationforeconomicco-operationanddevelopment,UnitedNationsandWorldBank”,SystemofNationalAccounts,UnitedNations,NewYork,NY.[GoogleScholar]19.Flower,J.(2015),“Theinternationalintegratedreportingcouncil:astoryoffailure”,CriticalPerspectivesonAccounting,Vol.27(March),pp.1-17.[GoogleScholar][CrossRef]20.Gray,R.(1990),TheGreeningofAccountancy:TheProfessionafterPearce,ACCA,London.[GoogleScholar]21.Hamilton,K.andClemens,M.(1999),“Genuinesavingsratesindevelopingcountries”,WorldBankEconomicReview,Vol.13No.2,pp.333-356.[GoogleScholar][CrossRef],[ISI][Infotrieve]22.Harrison,A.(1993),“ThedrafthandbookandtheUNSTATframework:comments”,inLutz,E.(Ed.),TowardImprovedAccountingfortheEnvironment,TheWorldBank,Washington,DC.[GoogleScholar]23.Hartwick,J.M.(1977),“Intergenerationalequityandtheinvestingofrentsfromexhaustibleresources”,AmericanEconomicReview,Vol.67No.5,pp.972-974.[GoogleScholar][ISI][Infotrieve]24.InternationalIntegratedReportingCouncil(2013),“Theinternationalframework”,IIRC,availableat:www.theiirc.org[GoogleScholar]25.Kennedy,R.F.(1968),“RemarksattheUniversityofKansas”,availableat:www.jfklibrary.org(accessed18March1968).[GoogleScholar]26.Kosoy,N.andCorbera,E.(2010),“Paymentsforecosystemservicesascommodityfetishism”,EcologicalEconomics,Vol.69No.1,pp.1228-1236.[GoogleScholar][CrossRef],[ISI][Infotrieve]27.Kubiszewski,I.,Costanza,R.,Franco,C.,Lawn,P.,Talberth,J.,Jackson,T.andAylmer,C.(2013),“BeyondGDP:measuringandachievingglobalgenuineprogress”,EcologicalEconomics,Vol.93No.1,pp.57-68.[GoogleScholar][CrossRef],[ISI][Infotrieve]28.Lindahl,E.R.(1933),“Theconceptofincome”,inBagge,G.(Ed.),EconomicEssaysinHonourofGustavCassel,Allen&Unwin,London.[GoogleScholar]29.McAffe,K.(1999),“Sellingnaturetosaveit?Biodiversityandgreendevelopmentalism”,EnvironmentandPlanningD:SocietyandSpace,Vol.17No.2,pp.133-154.[GoogleScholar][CrossRef],[ISI][Infotrieve]

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

30.MA(2005),MillenniumEcosystemAssessment.EcosystemsandHumanWell-Being:AFrameworkforAssessmentSummary,IslandPress,Washington,DC.[GoogleScholar]31.Maes,J.,Teller,A.,Erhard,M.,Liquete,C.,Braat,L.,Berry,P.andBidoglio,G.(2013),MappingandAssessmentofEcosystemsandtheirServices,AnAnalyticalFrameworkforEcosystemAssessmentsunderAction5oftheEUBiodiversityStrategyto2020,PublicationsOfficeoftheEuropeanUnion,Luxembourg.[GoogleScholar]32.Mäler,K.G.,Aniyar,S.andJansson,Å.(2009),“Accountingforecosystems”,EnvironmentalandResourceEconomics,Vol.42No.1,pp.39-51.[GoogleScholar][CrossRef],[ISI][Infotrieve]33.Meadows,D.H.,Meadows,D.L.,Randers,J.andBehrens,W.W.III(1972),TheLimitstoGrowth,UniverseBooks,NewYork,NY.[GoogleScholar]34.Nordhaus,W.D.andKokkelenberg,E.C.(Eds)1999),Nature’sNumbers:ExpandingtheNationalEconomicAccountstoIncludetheEnvironment,NationalAcademyPress,Washington,DC.[GoogleScholar]35.Nordhaus,W.D.andTobin,J.(1973),“Isgrowthobsolete?”,StudiesinIncomeandWealth,Vol.38No.2,pp.509-564.[GoogleScholar][Infotrieve]36.Obst,C.andVardon,M.(2014),“Recordingenvironmentalassetsinthenationalaccounts”,OxfordReviewofEconomicPolicy,Vol.30No.1,pp.126-144.[GoogleScholar][CrossRef],[ISI][Infotrieve]37.Pearce,D.andAtkinson,G.(1993),“Capitaltheoryandthemeasurementofsustainabledevelopment:anindicatorofweaksustainability”,EcologicalEconomics,Vol.8No.2,pp.103-108.[GoogleScholar][CrossRef][Infotrieve]38.Peskin,H.M.andDeLosAngeles,M.(2001),“Accountingforenvironmentalservices:contrastingtheSEEAandtheENRAPapproaches”,ReviewofIncomeandWealth,Vol.47No.2,pp.203-219.[GoogleScholar][CrossRef][Infotrieve]39.Puma(2011),“Puma’senvironmentalprofitandlossaccountfortheyearended31December,2010”,Puma,Germany,availableat:http://about.puma.com/damfiles/default/sustainability/environment/e-p-l/EPL080212final-3cdfc1bdca0821c6ec1cf4b89935bb5f.pdf[GoogleScholar]40.Rockström,J.,Steffen,W.,Noone,K.,Persson,A.,Chapin,F.S.,Lambin,E.F.,Lenton,T.M.,Scheffer,M.,Folke,C.,Schellnhuber,H.J.,Nykvist,B.,deWit,C.A.,Hughes,T.,vanderLeeuw,S.,Rodhe,H.,Sörlin,S.,Snyder,P.K.,Costanza,R.,Svedin,U.,Falkenmark,M.,Karlberg,L.,Corell,R.W.,Fabry,V.J.,Hansen,J.,Walker,B.,Liverman,D.,Richardson,K.,Crutzen,P.andFoley,J.A.(2009),“Asafeoperatingspaceforhumanity”,Nature,Vol.461No.7263,pp.472-475.[GoogleScholar][CrossRef],[ISI][Infotrieve]41.Solow,R.M.(1974),“Intergenerationalequityandexhaustibleresources”,ReviewofEconomicStudies,SymposiumontheEconomicsofExhaustibleResources,Vol.41,pp.29-46.[GoogleScholar]

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

42.StatisticsCanada(2014),“Canadiansystemofenvironmental-economicaccounts–physicalflowaccounts”,StatisticsCanada,Ottawa.[GoogleScholar]43.StatisticsDenmark(2013),“EnvironmentalaccountsforDenmark”,StatisticsDenmark,Copenhagen.[GoogleScholar]44.StatisticsNetherlands(2013),“EnvironmentalaccountsoftheNetherlands”,StatisticsNetherlands,DenHaag.[GoogleScholar]45.Stiglitz,J.,Sen,A.andFitoussi,J.P.(2010),MeasuringourLives:WhyGDPdoesn’tAddUp,TheNewPress,NewYork,NY.[GoogleScholar]46.TEEB(2010),TheEconomicsofEcosystemsandBiodiversity,MainstreamingtheEconomicsofNature,ASynthesisoftheApproach,ConclusionsandRecommendationsofTEEB,availableat:www.teeb.org[GoogleScholar]47.UnitedNations(1993a),ReportoftheUnitedNationsConferenceonEnvironmentandDevelopment,RiodeJaneiro,3-14June1992,Vol.1,ResolutionsAdoptedbytheConference,SalesNo.E.93.I.8andcorrigendum,ResolutionI,annexII(Agenda21),UnitedNations,NewYork,NY.48.UnitedNations(1993b),HandbookofNationalAccounting:IntegratedEnvironmentalandEconomicAccounting,InterimVersion,UnitedNations,NewYork,NY,StudiesinMethods,SeriesF.No.61,SalesNo.E.93.XVII.12.[GoogleScholar]49.UnitedNations(2000),HandbookofNationalAccounting:IntegratedEnvironmentalandEconomicAccounting–AnOperationalManual,UnitedNations,NewYork,NY,StudiesinMethods,SeriesF.No.78,SalesNo.E.00.XVII.17.[GoogleScholar]50.UnitedNations(2013),“Systemofenvironmental-economicaccounting2012–implementationguide”,DraftpresentedtotheLondonExpertGrouponEnvironmental-EconomicAccounting,November2013,availableat:http://unstats.un.org/unsd/envaccounting/londongroup/meeting19/LG19_6_1.pdf.[GoogleScholar]51.UnitedNations(2014),SystemofEnvironmental-EconomicAccounting2012–ApplicationsandExtensions,Whitecoverpublication,UnitedNations,NewYork,NY,pre-editedtextsubjecttoofficialediting.[GoogleScholar]52.UnitedNationsDevelopmentProgram(2014),HumanDevelopmentReport2014,UNDP,NewYork,NY.[GoogleScholar]53.UnitedNations,EuropeanCommissionandOrganisationofEconomicCo-operationsandDevelopmentandWorkBank(2013),SystemofEnvironmental-EconomicAccounting2012–ExperimentalEcosystemAccounting,Whitecoverpublication,UnitedNations,NewYork,NY,pre-editedtextsubjecttoofficialediting.[GoogleScholar]54.UnitedNationsandEuropeanUnion(2014),“Foodandagricultureorganizationoftheunitednations,internationalmonetaryfund,organisationforeconomicco-operationanddevelopmentandTheWorldBank”,SystemofEnvironmental-EconomicAccounting2012–CentralFramework,UnitedNations,NewYork,NY.[GoogleScholar]

Obst(2015):Reflectionsonnaturalcapitalaccountingatthenationallevel

SustainabilityAccounting,ManagementandPolicyJournal;2015;Vol.6Issue:3,pp.315-339doi:10.1108/SAMPJ-04-2014-0020Thisarticleis©EmeraldGroupPublishingandpermissionhasbeengrantedforthisversiontoappearhereatwww.ideeagroup.com.Emeralddoesnotgrantpermissionforthisarticletobefurthercopied/distributedorhostedelsewherewithouttheexpresspermissionfromEmeraldGroupPublishingLimited.'

55.UNU-IHDPandUNEP(2012),InclusiveWealthReport2012,MeasuringProgressTowardsSustainability,CambridgeUniversityPress,Cambridge.[GoogleScholar]56.Vanoli,A.(1995),“Reflectionsonenvironmentalaccountingissues”,ReviewofIncomeandWealth,Vol.41No.2,pp.113-137.[GoogleScholar][CrossRef][Infotrieve]57.Vardon,M.,Lenzen,M.,Peevor,S.andCreaser,M.(2007),“WateraccountinginAustralia”,EcologicalEconomics,Vol.61No.4,pp.650-659.[GoogleScholar][CrossRef],[ISI][Infotrieve]58.Vardon,M.,Andersen,O.,Becker,A.,Becker,R.,Clarke,D.,Csizmadia,M.,DiMatteo,I.,Edens,B.,Edwards,R.,Markhonko,V.,Martinez-Lagunes,R.,Singh,G.,Smith,H.andVako,S.(2012),“TheSystemofenvironmental-economicaccountingforwater:development,implementationanduse”,inGodfreyandChalmers(Eds)WaterAccounting:InternationalApproachestoPolicyandDecisionMaking,EdwardElgar,Cheltenham.[GoogleScholar]59.WorldBank(2011),TheChangingWealthofNations,TheWorldBank,Washington,DC.[GoogleScholar]60.WorldBank(2014),WAVESAnnualReport,WorldBank,WADC.[GoogleScholar]

Notes

1. FurtherdetailsonthehistoryofthedevelopmentoftheSEEAareprovidedinSEEACentralFrameworkChapter1.

2. Forfurtherdetails,seeUnitedNationsetal.(2013,Chapter2).3. Forfurtherdetails,seeUnitedNationsetal.(2013,Chapter3).4. Forfurtherdetails,seeUnitedNationsetal.(2013,Chapter5).5. Forfurtherdetails,seeUnitedNationsandEuropeanUnion(2014,Chapter5)andUnited

Nationsetal.(2013).6. Forfurtherdetails,seeUnitedNationsetal.(2013,Chapter4).7. Forfurtherdetails,seeUnitedNationsetal.(2013,Chapter6).