Embed Size (px)

Citation preview

Reducing Transatlantic Barriers to Trade and Investment

An Economic Assessment

Final Project Report

March 2013

Prepared under implementing Framework Contract TRADE10/A2/A16

Joseph Francois (project leader)

Centre for Economic Policy Research, London

Colophon

Reducing Trans-Atlantic Barriers to Trade and Investment

Primary authors: Joseph Francois, Miriam Manchin, Hanna Norberg, Olga Pindyuk, Patrick Tomberger

Client: European CommissionPrepared under implementing Framework Contract TRADE10/A2/A16

Date: March 2013

Contact:Centre for Economic Policy Research3rd Floor77 Bastwick StreetLondon, EC1V 3PZUKTel: +44 (0)20 7183 8801Email: [email protected]: www.cepr.org

Contents

Colophon ii

Key Findings vii

Executive Summary 1

1. Introduction 5

2. Economic and Policy Background 72.1. Current trade flows and FDI 82.1.1. Trade 82.1.2. FDI 102.2. Current patterns of tariffs 142.3. Non-tariff barriers 152.3.1. Indexes and econometrics 16

3. Technical Discussion on CGE Modelling Set Up 213.1. The model 213.2. Sectors and regions in the model 24

4. The Policy Options Considered 274.1. Scenarios 274.2. Spill-overs 284.3. Sectoral effects: Preliminary ranking 30

5. Results 335.1. Limited Scenarios 335.2. Full FTA 455.2.1. Macro Results 455.2.2. Output and Trade 495.2.3. Sustainability Impacts 705.2.4. Global Effects 81

6. FDI Barriers 856.1 Indexes and comparison of levels of openness 856.2 Impact of NTBs on foreign affiliates 91

7. Conclusions 95

8. References 97

Annex 1: Mapping of model sectors 103

Annex 2: CGE model technical overview 105

Annex 3: High tariff sectors, ranked by HS2 applied tariff rates 113

Annex 4: Derivation of foreign investment income equation 115

iv

List of FiguresFigure 1 EU trade in goods with the US by sector (in million euros), 2011 9Figure 2 The bilateral composition of trade in projected benchmark (2027) 9Figure 3 EU27 outward stocks of FDI, 2010 10Figure 4 Top ten hosts of EU outward FDI stocks, 2010 (in 1000 million euros) 11Figure 5 Top ten sources of EU inward FDI stocks, 2010 (in 1000 million euros) 11Figure 6 US outward and inward FDI to the EU and the rest of the World, 2010 (in 1000 million euros) 12Figure 7 EU’s direct investment flows to the US, 2004-2011 13Figure 8 EU’s direct investment flows from the US, 2004-2011 13Figure 9 Trade Weighted Applied (MFN) average tariff rates 2007 14Figure 10 Value added and impact rankings 32Figure 11 Decomposition of EU output changes, ambitious scenario 63Figure 12 Average Value of NTM Indexes for FDI 87Figure 13 Average NTM index values for FDI located in the EU 88Figure 14 Breakdown of NTBs for FDI by sector 89Figure 15 Income from FDI, market size, and openness, 2007-2009 90Figure 3 Representative nested production technology 106Figure 4 Representative household demand 108

List of TablesSummary of Macroeconomic Effect 3Table 1 Perceived NTB index by business (index between 0-100) 18Table 2 Total trade cost estimates from NTB reduction in per cent, Ecorys (2009) 20Table 3 Sectors and regions used in the CGE model 25Table 4 Scenario Summaries 28Table 5 Impact ranking indexes 31Table 6 Changes in GDP (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 34Table 7 Changes in GDP (in million euros), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 35Table 8 Changes in trade (in per cent), extra-EU trade for the EU, 2027 benchmark, limited agreement, 20 per cent direct spill-overs 36Table 9 Changes in trade (in million euros), extra-EU trade in case of the EU, 2027 benchmark, limited agreement, 20 per cent direct spill-overs 36Table 10 Changes in EU bilateral exports to US by sector (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 38Table 11 Changes in US bilateral exports to EU by sector, 2027 benchmark, limited agreement, 20 per cent direct spill-overs 39Table 12 Changes in EU trade by sector (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 40

v

Table 13 Changes in US trade by sector (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 42Table 14 Changes in EU output by sector (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 43Table 15 Changes in US output by sector (in per cent), 2027 benchmark, limited agreement, 20 per cent direct spill-overs 44Table 16 Changes in GDP (in per cent), 2027 benchmark, 20 per cent direct spill-overs 46Table 17 Changes in GDP (in million euros), 2027 benchmark, 20 per cent direct spill-overs 47Table 18 Household disposable income, million euro, 2027 benchmark 48Table 19 Changes in bilateral exports to the partner country (in per cent and million euros), 2027 benchmark, 20 per cent direct spill-overs 50Table 20 Changes in value of total exports (in per cent and million euros), extra-EU exports in case of the EU, 2027 benchmark, 20 per cent direct spill-overs 51Table 21 Changes in value of total imports (in per cent and million euros), extra-EU imports in case of the EU, 2027 benchmark, 20 per cent direct spill-overs 52Table 22 Changes in terms of trade (in per cent), 2027 benchmark, 20 per cent direct spill-overs 53Table 23 Change in EU tariff revenue (in million euros), 2027 benchmark 54Table 24 Trade diverted from intra-EU trade (in million euros), 2027 benchmark, 20 per cent direct spill-overs, ambitious experiment 55Table 25 Change in EU exports to non-US, extra-EU destinations (in million euros), 2027 benchmark, 20 per cent direct spill-overs, ambitious experiment 57Table 26 Change in EU imports from non-US extra-EU sources (in million euros), 2027 benchmark, 20 per cent direct spill-overs, ambitious experiment 59Table 27 Changes in EU output by sector (in per cent). 2027 benchmark, 20 per cent direct spill-overs 60Table 28 Changes in US output by sector (in per cent), 2027 benchmark, 20 per cent direct spill-overs 61Table 29 Changes in extra-EU exports and imports by sector (in per cent and million euros), 2027 benchmark, 20 per cent direct spill-overs 64Table 30 Changes in US exports and imports by sector (in per cent and million euros), 2027 benchmark, 20 per cent direct spill-overs. 66Table 31 Changes in bilateral exports from the EU to the US by sector (in per cent and million euros), 2027 benchmark, 20 per cent direct spill-overs 68Table 32 Changes in bilateral exports from the US to the EU by sector (in per cent and million euros), 2027 benchmark, 20 per cent direct spill-overs 69Table 33 Changes in wages for less and more skilled labour, total effects (in per cent), 2027 benchmark, 20 per cent direct spill-overs 71Table 34 Change in more skilled employment in the EU by sector (in per cent), 2027 benchmark, ambitious scenario, 20 per cent direct spill-overs 73Table 35 Change in more skilled employment in the US by sector (in per cent), 2027 benchmark, ambitious scenario 74Table 36 Change in less skilled employment in the EU by sector (in per cent), 2027 benchmark, ambitious scenario 75Table 37 Change in less skilled employment in the US by sector (in per cent), 2027 benchmark, ambitious scenario 76

vi

Reducing Transatlantic Barriers to Trade and Investment

Table 38 Displacement of less and more skilled labour in the EU and US, total effects (in per cent), 2027 benchmark, 20 per cent direct spill-overs 77Table 39 Changes in CO2-emissions (in thousand metric tons), 2027 benchmark, 20 per cent direct spill-overs 79Table 40 Changes in land use (in per cent), 2027 benchmark, 20 per cent direct spill-overs 80Table 41 Total effects on GDP for rest of the World (in million euros and per cent), 2027 benchmark, 20 per cent direct spill-overs 82Table 42 Change in exports by region (in per cent), 2027 benchmark, 20 per cent direct spill-overs 83Table 43 Regression estimates for NTMs and FDI 92Table A1 Mapping of Model Sectors to GTAP 103Table A2 Mapping of Model Sectors to ISIC rev 3.1 104Table A3 Annualized GDP growth rates 111Table A4 HS-2 Classification, top 2 per cent of tariff lines 113

vii

• An ambitious and comprehensive transatlantic trade and investment agreement

couldbringsignificanteconomicgainsasawholefortheEU(€119billionayear)

andUS(€95billionayear).Thistranslatestoanextra€545indisposableincome

eachyearforafamilyof4intheEU,onaverage,and€655perfamilyintheUS.

• ThebenefitsfortheEUandUSwouldnotbeattheexpenseoftherestoftheworld.

Onthecontrary,liberalisingtradebetweentheEUandtheUSwouldhaveaposi-

tiveimpactonworldwidetradeandincomes,increasingglobalincomebyalmost

€100billion.

• Incomegainsarearesultofincreasedtrade.EUexportstotheUSwouldgoupby

28%,equivalent toanadditional€187billionworthofexportsofEUgoodsand

services.Overall,totalexportswouldincrease6%intheEUand8%intheUS.

• Reducing non-tariff barrierswill be a key part of transatlantic liberalisation.As

muchas80%ofthetotalpotentialgainscomefromcuttingcostsimposedbybu-

reaucracyandregulations,aswellasfromliberalisingtradeinservicesandpublic

procurement.

• Theincreasedlevelofeconomicactivityandproductivitygainscreatedbytheagree-

mentwillbenefittheEUandUSlabourmarkets,bothintermsofoverallwagesand

newjobopportunitiesforhighandlowskilledworkers.Labourdisplacementwill

bewellwithinnormallabourmarketmovementsandeconomictrends.Thismeans

arelativelysmallnumberofpeoplewouldhavetochangejobsandmovefromone

sectortoanother(0.2to0.5percentoftheEUlabourforce.)

• TheagreementwouldhavenegligibleeffectsonCO2emissionsandonthesustain-

ableuseofnaturalresources.

Key Findings

1

TheeconomiesoftheEuropeanUnionandtheUnitedStatesareveryimportanttrading

partnersforeachother.Althoughaveragetarifflevelsarerelativelylowalready,various

non-tariffbarriersorNTBs(oftenintheformofdomesticregulations)onbothsides

oftheAtlanticconstituteimportantimpedimentstodeepeningtransatlantictradeand

investmentlinkages.Thisstudyexaminestheimpactofthereductionofsuchbarriers.

Evenwheretheymightnotbedirectlytargetingcross-borderactivities,domesticrules

andregulationsneverthelesscanplaceacostontradeandinvestment.However,unlike

tariffs,itshouldalsobestressedthatmanyregulationscannotsimplyberemovedwhen

theyservelegitimatedomesticpurposes.Yetinsuchcasesthecostsinvolvedmaystill

bemitigatedorreducedthroughpartialregulatoryconvergenceandcross-recognition

ofstandards.Whilethisislikelytobeadifficultprocess,thepotentialbenefitsinterms

ofproductivityandincomesaresubstantial.

Thisstudyreviewstheimportanceofthebilateraleconomicrelationshipandprovides

computablegeneralequilibrium(CGE)-basedestimatesfortheeconomy-wideimpact

of reducing both tariff and non-tariff barriers (NTBs). Estimates are providedwith

regardstoexpectedchangesinGDP,sectoroutput,aggregateandbilateraltradeflows,

wages, and labour displacement, amongother issues.The analysis uses theGTAP8

database(projectedto2027),inconjunctionwithNTBestimatesreportedintheEcorys

(2009)study.Thestudyinvestigatesdifferentpolicyoptionsforthedeepeningofthe

bilateraltradeandinvestmentrelationshipbetweentheEUandUS.Theserangefrom

partialagreementsthatarelimitedinthescopeofbarrierstheywouldaddress(tariffs

only, or services only, or procurement only) to a full-fledged free trade agreement

Executive Summary

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

2

(FTA) with a comprehensive liberalisation agenda covering simultaneously tariffs,

procurement, NTBs for goods, and NTBs for services. The comprehensive option

includestwoscenarios:alessambitiousagreementthatincludesa10percentreduction

intradecostsfromNTBsandnearlyfulltariffremoval(98percentoftariffs)andan

ambitiousscenariothatincludestheeliminationof25percentofNTBrelatedcosts

and100percentoftariffs.Inbothscenariosmoreambitionisimposedonthelowering

ofprocurement-relatedNTBsthanforotherNTBsaffectinggoodsandservices.Itis

assumedthatNTBslinkedtoprocurementarereducedby25percentor50percent,

inthe“lessambitious”andinthe“ambitious”scenariosrespectively.Theimpactof

partialalignmentofglobalrulesandstandardswithanewsetofEU-USstandardsand

cross-recognitionagreementsisalsoincludedintheassessment.

The results indicate positive and significant gains for both economies. Under a

comprehensiveagreement,GDPisestimated to increasebybetween68.2and119.2

billioneuros for theEUandbetween49.5and94.9billioneuros for theUS(under

the less ambitious and more ambitious scenarios). However, if the FTA would be

limitedtotariffliberalisationonly,orservicesorprocurementliberalisationonly,the

estimatedgainswouldbe significantly lower.For example, anFTA limited to tariff

liberalisationwouldleadtoalower(23.7billioneuro)increaseinGDPfortheEUand

a9.4billioneurosincreasefortheUS.Thestudyalsoquantifiespotentialbenefitsfrom

NTBreductionaffectingFDI.Theoverallmessageisthatnegotiatinganagreementthat

wouldbeofacomprehensivenaturewouldbringsignificantlygreaterbenefitstoboth

economies.

Anothercoremessagethatfollowsfromourresultsisthatfocusingeffortsonreducing

NTBsiscriticaltothelogicoftransatlantictradeliberalization.Differentapproaches

tothesameregulatorychallengeshavetheunintendedconsequenceofincreasingcosts

for firms,which have to complywith two regulatory environments, dragging down

labourproductivity.NegotiationonNTBsprovidestheopportunitytopursueamixof

cross-recognitionandregulatoryconvergencetoreducethesebarriers.Comparedtoa

focusonNTBS,justlimitingtheexercisetotariffswouldleadtomuchmorelimited,

Executive Summary

3

thoughpositive effects. Furthermore, thegains to the transatlantic economies from

NTBreductionarenotprojectedtobeattheexpenseoftherestoftheworld,thoughthe

rest-of-worldimpacthingescriticallyonthepotentialforglobalconvergencetoward

EU-US standards, which could then become de facto global standards and have a

knock-oneffectloweringNTBsmultilaterally.Suchaprocessimpliesimprovementof

marketaccessforthirdcountries,helpingtooffsettradediversion.

Finally, this study also reports estimates on sustainability impacts -- changes in

emissionsandinnaturalresourceutilization.EliminationofNTBsimpliesimproved

productivity(i.e.lessprimaryinputsarerequiredforcurrentactivity).Theresultspoint

tonegligibleeffectsontherateofCO2emissionsandutilisationofnaturalresources.

Summary of Macroeconomic Effect

Limitedagreement:tariffsonly

Limitedagreement:servicesonly

Limitedagreement:procurement

only

Comprehensiveagreement:lessambitious

Comprehensiveagreement:ambitious

ChangeinGDP

EU,millioneuros 23,753 5,298 6,367 68,274 119,212

US,millioneuros 9,447 7,356 1,875 49,543 94,904

Bilateralexportsf.o.b.

EUtoUS,millioneuros

43,840 4,591 6,997 107,811 186,965

UStoEU,millioneuros

53,777 2,859 3,411 100,909 159,098

Totalexportsf.o.b.

extra-EU,millioneuros

43,740 5,777 7,136 125,232 219,970

US,millioneuros 57,330 5,488 5,942 142,071 239,543

Note: estimatestobeinterpretedaschangesrelativetoaprojected2027globaleconomy.

5

Thetransatlantictraderelationshipisadeepone,rootedincenturiesofsharedeconomic

history. In thepost-warperiod, this facthasbeen reflectednotonly in early shared

steps leadingultimately to themodernmultilateral tradingsystem,butalsoperiodic

initiativestoformaregionaltradeagreement.1Withtherisingimportanceofglobaland

regionalproductionchainsandinternationalfirms,thelogicforaregional,transatlantic

agreement seemscompelling.Together, the twoeconomiesaccount for roughlyhalf

of world output and world trade. They are, mutually, each other’s most important

investmentpartnersaswell.

In 2012, a comprehensive dialoguewas initiated between the EuropeanUnion and

UnitedStates,regardingpossibilitiesfordeepeningoftransatlantictradeandinvestment

relations.Thediscussionsregardingthepossibledeepeningoftheselinksareon-going.

This report offers quantification of the effects of a trade and investment agreement

underarangeofpossiblepolicyoptions.BoththeEUandtheUShaverelativelylow

MFNtariffs.But,giventhemagnitudeofbothtradeandinvestmentflowsbetweenthe

EUandtheUS,removingevenrelativelyminorimpedimentstotheseflowswillhavea

significantimpact,withpotentialsubstantivebenefitsforbotheconomies.Inaddition,

sincetheexistingnon-tariffbarriersalsoactasimpedimentstotradeandinvestment,

therearegoodreasonstobelievethattherearesignificantuntappedgainsfromadeeper

tradeandinvestmentrelationship.

1 Past initiativeshave includedboth theNAFTA(NorthAtlanticFreeTradeArea)and theTAFTA(TransatlanticFreeTradeArea).SeeBaldwinandFrancois(1997a,1997,1999)forbackgroundonearlierinitiatives.SeeBaldwin(2012)andFrancois,Manchin,andTomberger(2012)ontheriseinvaluechainsandglobalproduction.

1. Introduction

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

6

This report builds on an important previous study benchmarking the current level

of transatlanticNTBs.That report found that thepotentialgains for theEUandUS

were substantial (Ecorys, 2009). Since the Ecorys study was published, economic

conditionshavechanged,whilethelikelyfocusofapossibleagreementisnowbetter

defined.Workingwith new data (including theGTAP8 database,more recent trade

and tariff information and new investment income data fromEurostat), the present

reportprovidesanupdatedandmoreaccuratesetofestimates.WeprovidenewCGE-

basedestimatesfortheeconomy-wideimpactofremovingnotonlyNTBs(quantified

onthebasisoftheestimatesinEcorys(2009),2butalsotariffsaffectingtransatlantic

tradeflows.Inaddition,wehaveexpandedtheanalysisbyprovidinganassessmentof

theimpactofremovingbarrierstoforeigndirectinvestment(FDI)ontheactivityof

multi-nationalenterprises(MNEs)acrossthetransatlanticmarketplace.BoththeCGE

andinvestmentassessmentsbuildonthesurveyandeconometricworkoftheoriginal

Ecorysstudy.Thereportisstructuredasfollows.Chapter2providesthebackground

fortheeconomicassessment.ThisincludescurrenttradeandFDIflows,aswellasa

technical discussion, providing an overviewof howNTBshavebeen identified and

measured,basedonthe2009Ecorysreport.InChapters3-5wesetoutandemploya

CGEmodeltoexaminebotheconomicandsocio-economic(sustainability)impactsof

trade-relatedmeasures.Chapter6focusesonforeigninvestment.InChapter7weoffer

someconcludingcomments.

2 InEcorys(2009)study,non-tariffbarriersaredefinedas“allnon-priceandnon-quantityrestrictionsontradeingoods,servicesandinvestment,atfederalandstatelevel.Thisincludesbordermeasures(customsprocedures,etc.)aswellasbehind-thebordermeasuresflowingfromdomesticlaws,regulationsandpractices”.

7

WestartthischapterwithanoverviewofcurrenttradeandFDIrelationshipsbetween

theEUandUS,aswellastariffsandNTBsthatarecurrentlyinplace.Indoingso,we

definethecontextinwhichweestimatetheeffectsofliberalisingtradeandinvestment

betweenthetwoeconomies.

TheEUandtheUSarerelativelyopentowardseachotherintermsofinvestmentand

trade,asreflectedinrelativelylowlevelsfortariffs.However,variousNTBs(oftenin

the formofdomestic regulations)onboth sidesof theAtlantic constitute important

impedimentstotransatlantictradeandinvestmentflows.Eventhoughtheymightnot

bedirectlytargetingcross-borderactivities theyneverthelessdobearacostontrade

andinvestment.ThereductionofsuchbarrierscouldpotentiallybenefitboththeEU

andtheUS.However,unliketariffs,manyregulationscannotsimplyberemoved,as

theyoftenserveimportantandlegitimatedomesticobjectiveslikeproductsafetyand

environmentalprotection. Yetsuchcostsmaybereduced throughpartial regulatory

convergence and cross-recognition of standards. Still, some amount of regulatory

divergenceisinevitableandwillremain,asregulationsreflectdifferencesingeography,

language,preferences,culture,andhistory.Thus,inarealisticanalyticalexercise,while

itcanbeassumedthatsomeNTBscanbeeliminatedbymutualagreementandeffort,

their100percenteliminationshouldnotbeconsideredasarealisticoutcome.3

3 Atthesametime,asbothregionsarehighincomewithhighstandardsfordomesticobjectives,neithershouldregulatoryconvergencebeseenasaprocessforbilateralloweringofstandards,butratherasamechanismforreinforcementofcomparableobjectivesotherwisereachedthroughdifferentregulatorymeans.

2. Economic and Policy Background

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

8

2.1. CurrenttradeflowsandFDI

2.1.1. Trade

TheUS is themost important trade partner for theEU asmeasured by exports. In

2011,around17percentoftotalEUexportsweredestinedtotheUSmarket.TheUS

isalsoanimportantsourceofEUimports.Itisthethirdmostimportant(11percent

of total imports)afterChinaandRussia4.For theUS, theEUisalsoakeybilateral

tradepartner.TheEUwasthesecondmostimportantdestinationforUSexports(after

Canada),representing19percentoftotalexports.Itisalsothesecondmostimportant

importpartner(afterChina),supplying17percentoftotalUSimports.5

ThemagnitudeofthetraderelationshipbetweentheEUandtheUS,andtheimportance

of the two economies as bilateral partners, suggests that anFTA thatwould reduce

obstaclesandcoststotradebetweenthetwocouldhavesignificantimpactsontradeand

ontheireconomicperformance.

Figure1showsEUmerchandisetradewiththeUSdividedbymainsectorsfortheyear

2011.Mostimportsandexportstakeplaceinthemachineryandtransportequipment

sector.Thisamountedto70,850millioneurosofEUimportsfromtheUS,and104,429

millioneurosworthofEUsalestotheUS.Thesecondmostimportantsectorforgoods

tradebetweentheEUandtheUSischemicals.AlsointhissectortheEUexportsmore

thanitimports(around50percentmore).

4 Source:Eurostat.5 Source:Eurostat.

Economic and Policy Background

9

Figure 1 EUtradeingoodswiththeUSbysector(inmillioneuros),2011

Source: Eurostat

Giventhatgoods tradeaccountsforroughly65percentof totalbilateral trade, (see

Figure2), liberalisationefforts (if thesameacross theboard)are likely to lead toa

morepronouncedimpactintermsofexchangesofgoodsratherthanservicesbetween

theUSandEU.

Figure 2 Thebilateralcompositionoftradeinprojectedbenchmark(2027)

Source: modelbenchmarkdatabase.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

10

2.1.2. FDI

NorthAmericaisthemostimportantdestinationforEUoutwardFDI,ascanbeseen

inFigure 3.The region hosts about one-third of totalEUoutwardFDI stocks.The

secondmost important region forEU’s outwardFDI stock is the so-called non-EU

EuroperegionthatincludestheformerSovietUnioncountries,Switzerland,Norway

andTurkey.Theseeconomiesholdaboutone-fourthofEUFDIstocks.Thethirdmost

important region forEU’sFDI isAsia,whichaccounts for14percentof totalFDI

outwardstocks.

Figure 3 EU27outwardstocksofFDI,2010

Source: Eurostat.

While inFigure 3we focused on regions, Figure 4 andFigure 5 (below) show the

breakdown of EU FDI partners by major country (instead of regions).Again, this

confirmstheimportanceoftheUS.Onacountrybasis,theUSstandsoutevenmoreas

themostimportantbilateralinvestmentpartnerfortheEU.EUoutwardFDIstocksin

theUSaremorethantwiceaslargeastothesecondmostimportanthostcountryfor

EUFDI,whichisSwitzerland.TherelativeimportanceoftheUSassourceofFDIin

Economic and Policy Background

11

theEUisevenmorepronouncedwhenviewedonacountrybasis,withtheUSowning

almostfourtimesmoreofEUinwardstocksofFDIthanthesecondmostimportant

partnercountry,Switzerland.GiventhemagnitudesoftheFDIbetweentheEUandthe

USanypolicyinfluencingthefurtherflowscouldhaveasignificantimpactonthese

economies.

Figure 4 ToptenhostsofEUoutwardFDIstocks,2010(in1000millioneuros)

Source: Eurostat

Figure 5 ToptensourcesofEUinwardFDIstocks,2010(in1000millioneuros)

Source: Eurostat

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

12

Figure6depictstheevolutionofoutwardandinwardFDItoandfromtheUS.Forthe

US,theEUisalsothemostimportantFDIpartner.ThestockofinwardFDIfromthe

EUexceedsthatfromtherestoftheworld.However,thestockofUSoutwardFDIto

theEUrepresentsanevenhigheramountthaninwardstockfromtheEU.

Figure 6 USoutwardandinwardFDItotheEUandtherestoftheWorld,2010(in

1000millioneuros)

Source: OECDandowncalculations

FDIactivitybetweenEUandUSsufferedtheconsequencesofthefinancialcrisisbutis

nowrebounding.Justbeforethefinancialcrisis,EUinvestmentflowstotheUSpeaked,

withalmost178,510millioneurosofEUinvestmentflowsgoingto theUSin2007

(seeFigure7).Thisrepresentedabout14percentofthetotaloftheEU’sinvestment

flowsgoingabroad.Duringthecrisis,EUinvestmentflowstotheUSdroppeddown

toalmost2004levels,withthelowestamountofbilateralflowstakingplacein2010.

Nevertheless,in2011,bilateralinvestmentflowspickedupagain,althoughnotreaching

yetpre-crisislevels.

Economic and Policy Background

13

Figure 7 EU’sdirectinvestmentflowstotheUS,2004-2011

Source: Eurostatandowncalculations.

InvestmentflowsfromtheUS(andfromtherestoftheworld)totheEUalsodropped

dramaticallyduringthecrisis(seeFigure8).Thehighestamountofinvestmentfrom

theUStookplacein2007,amountingto195,660millioneuros.In2010,theincoming

FDIflowswereonly114,763millioneuros.However,whilethevolumeofFDIinflows

fromtheUSisstillbelowthepre-crisislevel,theshareofinvestmentcomingfromthe

UShasreacheditspre-crisislevelasof2010.

Figure 8 EU’sdirectinvestmentflowsfromtheUS,2004-2011

Source: Eurostatandowncalculations.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

14

GiventheimportanceandattractivenessoftheNorthAmericanregionforEUinvestors

andoftheEuropeanmarketforUSinvestorsanypolicyaimingtoremoveregulatory

barriers to transatlantic investmentscanbeexpected tohaveapotentiallyvery large

impact.

2.2. Current patterns of tariffs

Inthissectionwefocusonexistingtariffbarriers.Figure9showsthatthereissome

heterogeneityintermsoftariffprotectionsbetweentheEUandtheUS.Whileinmost

sectors, EU tariffs are slightly higher than those imposed by theUS, they are still

relativelylow.However,therearetwomainexceptions:motorvehicles,andprocessed

foods.TheEUaveragetariffsontheseproductsaresubstantiallyhigherthantheUS

tariffs.Formotorvehicles6theEUappliesanaveragetariff(8.0percent)thatisalmost

eighttimeshigherthantheUS.Forprocessedfoodproducts,EUaveragetariffs(14.6

per cent) aremore than four times higher thanUS average tariffs. For agriculture,

forestryandfisheriesaveragetariffsarealsorelativelyhigh(about3.7percent)butfor

theseproductsthereisnodifferencebetweentheEUandtheUS.

Figure 9 TradeWeightedApplied(MFN)averagetariffrates2007

Source: WTO,CEPII,UNCTADmappedtoGTAP8

6 Motorvehiclessectorinthiscaseincludesalsopartsandcomponents.

Economic and Policy Background

15

Giventhecurrenttariffstructure,thescopefortariffreductionstohaveasignificant

impactontradeflowsislimited.Indeed,formostsectors,afurtherreductionintariffs

impliesverysmallabsolutechangesinthelevelofprotection.Nevertheless,insome

sectors,suchasprocessedfoods,agriculture,forestryandfisheries,andmotorvehicles,

the impact is likely tobemoresubstantial.Forothersectors,NTBsare theprimary

driverofpotentialimpactaswillbeshowninthenextsection.

2.3. Non-tariff barriers

NTBs and regulatory divergence are complex issues to dealwith analytically.Even

the measurement of the importance of these barriers for trade and investment is a

difficultexercise.ThisstudyreliesontheearlierworkonthistopicintheEcorys(2009)

study.TheEcorys study remains themost comprehensive and detailed to date.The

methodologyincorporatedinthatstudyusedamulti-prongedapproachthatcombined

literaturereviews,businesssurveys,econometricanalyses(gravitymodellingtogether

with CGEmodelling), as well as consultations with regulators and businesses and

inputs by sector experts aiming to obtain a qualitative andquantitative estimates of

transatlanticNTBs.WhiletheEcoryssurveyfocusedonbothtradeandFDI,wefocus

hereontrade-relatedbarriers.WewillreturntoFDIbarriersinChapter6.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

16

2.3.1. Indexes and econometrics

Toestimatethead-valoremequivalentofNTBs(theimpactonpricesandcosts)and

toquantifytowhatextentthoseareremovablebetweenthetwoeconomies,theEcorys

(2009)studyundertookacomplexsetofassessments.Wesummarizethosestepsbriefly

here.Theassessmentinvolvedsurveyscombinedwithgravity-basedeconometrics.7

7 ForfurtherdiscussiononthemethodologiesusedforNTBquantification,whichtechnicallyareknownasgravitymodelsseebothEcorys(2009)Chapter3.4,andalsoAnderson,Bergstrand,Egger,andFrancois(2008).Forgoods,selectionbasedgravitymodellingwasused. Servicesbarrierswerebasedon theNTBelasticityestimates fromFrancoisandHoekman(2010).

Box 1 NTBSandtheconceptsofcostandrents

NTBs and regulatory differences can have two main effects. NTBs can either

increase thecostofdoingbusinessfor firms,or theycanrestrictmarketaccess.

TraditionalNTBs,likeimportquotas,areanexamplewhereNTBsmarketaccess.

In contrast, regulations that require expensive reconfiguration of products (like

changing voltage or reconfiguration of an exhaust system) for export are an

exampleofcostraisingNTBs.Bothcanhavedifferentimpactsbychangingmarket

concentration and economic power (and thus profits) of companies. In order to

beabletomakeadistinctionbetweenthosetwotypesofNTBs,theconceptsof

‘cost’and‘rent’areincludedhereinmodellingofNTBs,followingthefindings

ofthefirmsurveys(andrelatedliterature)intheEcorys(2009)study.Thatstudy

foundthatabout60percentof theprice impactofNTBscouldbeclassifiedas

following from actual cost increases on average, while the creation of market

power(economicrent)wasresponsiblefortheother40percentofpriceincreases.

Thisisanaverage,andthereissomevariationacrossbothsectorsandcountries

inthisregard.InthecaseofNTB-relatedcostincreases,thisconstitutesawelfare

losstosociety.Incaseofanincreaseinmarketconcentration,consumerpricesmay

alsogoup.Howeverpartoftheincreaseisthenappropriatedbycompaniesasthey

reapincreasedrevenuesandprofits.Thusthereisaredistributionofwelfare,and

notsimplyareductionineconomicefficiency.

Economic and Policy Background

17

TheNTBestimatesinvolvedatwo-partsurveyasafirststep.Thesurveywasconducted

on firms in theEUandUSengaged in trade, and firms in theEUandUSengaged

in FDI.Theywere asked both detailed questions aboutNTBs, and amore general

setofquestionsaboutoverallmarketaccessconditions.8 IncaseswhereNTBswere

identified,companieswereaskedabouttherelativeimportanceofsuchbarriers.Firms

also provided a comprehensive generalmeasure ofNTB-relatedmarket access (the

combinedimpactofallbarriers)intheformofarankingscaledfrom0to100.With

theoverall rankingquestion, 0 indicated that therewerenoNTBsof any type, and

100meant therewere prohibitively highNTBs.The business survey restrictiveness

indicators were then crosschecked against OECD (2007) restrictiveness indicators

and against the ProductMarket Regulation (PMR) indexes. For the service sectors

the combinationof theOECD restrictiveness indicators and the survey resultswere

used.TheresultingmeasuresaresummarisedinTable1below.Thefirmrankingsare

bilateral(forexampleanAmericanfirminFrancemightgiveadifferentrankingthan

aGermanfirminFrance).

ThereportedNTBrankings(theNTBindex)ongoodsonbothsidesoftheAtlanticare

generallyhigherthanonservices,rangingfrom20percentto56percent.Thehighest

perceived NTB levels were found on the aerospace and space industry. On goods

exported to theUS,machinery also exhibits high levels ofNTBs,while the lowest

levelsarereportedforpharmaceuticals.ForgoodsexportedfromtheUS,highlevels

ofNTBswerereportedforchemicals,cosmeticsandbiotechnology.Lowerlevelsof

NTBswerereportedforelectronics,iron,steelandmetalproducts.

Ofcourse,thefirmrankingsofgeneralopennessarerelative.Theydonottranslateinto

actualimpactsoncostsandprices.Forthis,thesurveydatawasthenintegratedwith

asetofeconometricmodels(knownasgravitymodels)toestimatethecorresponding

ad-valoremofpercentpriceimpactofthevariationsinNTBlevels.Onthatbasis,the

8 Thegeneralrankingquestionsarereproducedasanannextothisreport.SeetheannextotheEcorys(2009)reportformoreinformationonthemoredetailedquestions.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

18

Ecorys (2009) report alsoprovidesprice/cost estimatesof existingNTBs for traded

goodsandservicesinapercentageformthatcanbeinterpretedsimilarlytoad-valorem

tariffs.TheseestimatesarereportedinTable2below.Theyreflectthehigherpricesthat

resultbecauseofNTBs.9

Table 1 PerceivedNTBindexbybusiness(indexbetween0-100)

Sector EUexportstotheUS USexportstotheEUServices Sectors:Travel 35.6 17.6Transport 39.9 26.3FinancialServices 29.7 21.3ICT 20.0 19.3Insurance 29.5 39.3Communication 44.6 27.0Construction 45.0 37.3OtherBusinessServices 42.2 20.0Personal,CulturalandRecreationalServices

35.8 35.4

Goods Sectors:Chemicals 45.8 53.2Pharmaceuticals 23.8 44.7Cosmetics 48.3 52.2Biotechnology 46.1 50.2Machinery 50.9 36.5Electronics 30.8 20.0Office,InformationandCommunicationEquipment

37.9 32.3

Medical,MeasuringandTestingAppliances

49.3 44.5

AutomotiveIndustry 34.8 31.6AerospaceandSpaceIndustry 56.0 55.1FoodandBeverages 45.5 33.6Iron,SteelandMetalProducts 35.5 24.0Textiles,ClothingandFootwear

35.6 48.9

WoodandPaper,PaperProducts

30.0 47.1

Source: Ecorys(2009)

9 Thereadermaynotesomedifferencebetweenthesectorsinthetablesinthissection.WehavestartedinTable1withthefullsetofsectorsfromtheoriginalECORYSsurvey.Thesehavebeenconsolidatedwhenwemovetosectorsforthemodelling,bothintheoriginalECORYSstudyandinthisreport.

Economic and Policy Background

19

AccordingtotheestimatesinTable2,non-tariffbarriersarethehighestforfoodand

beverageproducts,withimportsfromtheUSfacinga56.8percenttariffequivalent,

whileEUexportstotheUSoftheseproductsfacea73.3percentextracost.Among

services,financialservicesareoneofthesectorswiththehighestestimatedNTBs.In

thissector,EUbarriersagainstUSexportsamountto11.3percent,whileUSbarriers

againstEUexports areestimated tobeabout31.7per cent.Barriers in the services

sectors arehigheron theEU side for thebusiness and ICT sector, communications

sector,construction,andpersonal,cultural,otherservices.OntheotherhandtheUS

barriersforEUexportersintheservicessectorsarehigherthanintheEUinthefinance

andinsurancesectors.

Itshouldbestressedthatincontrasttoreducingtariffs,theremovalofNTBsisnotas

straightforward.Infact,itisunlikelythatallareasofregulatorydivergenceidentified

actuallycanbeaddressed.Aspreviouslypointedout,therearemanydifferentsources

of NTBs and thus removing them may require constitutional changes, unrealistic

legislative changes, or unrealistic technical changes. Removing NTBsmay also be

difficultpolitically,e.g.becausethereisalackofsufficienteconomicbenefittosupport

theeffort;becausethesetofregulationsistoobroad;becauseofconsumerpreferences,

language and geography; or due to other political sensitivities. In recognition of

thesedifficulties,intheassumptionsofthescenarios,thedegreetowhichanNTBor

regulatorydivergencecan,potentiallyandrealistically,bereducedistakenintoaccount

whichisdiscussedinmoredetailsinthefollowingsubchapter.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

20

Table 2 TotaltradecostestimatesfromNTBreductioninpercent,Ecorys(2009)

Sector Totaltradebarriers:EUbarriersagainstUSexports

Totaltradebarriers:USbarriersagainstEUexports

Foodandbeverages 56.8 73.3Chemicals 13.6 19.1Electricalmachinery 12.8 14.7Motorvehicles 25.5 26.8Othertransportequipment 18.8 19.1Metalsandmetalproducts 11.9 17.0Woodandpaperproducts 11.3 7.7Othermanufactures N/A N/A average goods 21.5 25.4TransportAir 2.0 2.0Water 8.0 8.0Finance 11.3 31.7Insurance 10.8 19.1BusinessandICT 14.9 3.9Communications 11.7 1.7Construction 4.6 2.5Personal,cultural,otherservices

4.4 2.5

average services 8.5 8.9

Source: Ecorys(2009),AnnexTableIII.1

At this stage, therearepatterns inTable2 thatwill carry forward in themodelling.

FollowingfromtheEcorys(2009)study,businessesperceivedtransatlanticNTBsas

substantiallylowerforservicesthanforgoods.Thismeansthat,forcomparablecuts

inbarriers inpercent terms, thedifferences inbarriers(combinedwith theabsolute

importanceingoodstraderelativetoservicestrade)implythatwecanexpectgreater

impactfromNTBreductionsingoodsthaninservices.

21

Thepurposeofthischapteristopresentanddiscussthemodelusedasbasisforthe

policyexperiments,includingthesectorandregionalaggregationthatwereused.

Inthisreport,theeconomicassessmentofatradeagreementbetweentheEUandUS

isbasedonacomputablegeneralequilibrium(CGE)modelofglobalworldtrade.The

CGEmodellingexerciseismeanttoestimatetheeffectsontheEUandUSeconomies.

CGEmodelsliketheonesusedherehelpanswerwhat-ifquestionsbysimulatingthe

price,incomeandsubstitutioneffectsinmarketequilibriumunderdifferentassumptions

aboutchangesinpolicy.Theeconomicoutcomesofthe“baseline”scenario(withno

policy change) can be compared to the different scenario associated with changes

in tradepolicy.The“baseline” for themodel is thus the equilibriumwithoutpolicy

change,andthe‘scenario’istheequilibriumafterthepolicychange.Theeffectofthe

policychangecanthenbebenchmarkedbythedifferencebetweenthetwo.

3.1. The model

TheCGEmodelemployedisbasedonthewidelyusedGTAPmodel(Hertel,1997),

with added features from theFrancois, vanMeijl, and vanTongeren (2005)model.

Moretechnicaldetailsofthemodelareprovidedintheannex.

Themostimportantaspectsofthemodelcanbesummarisedasfollows:

• Itcoversglobalworldtradeandproduction

• Itallowsforscaleeconomiesandimperfectcompetition

3. Technical Discussion on CGE Modelling Set Up

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

22

• Itincludesintermediatelinkagesbetweensectors

• It allows for trade to impact on capital stocks through investment effectswhich

allowstoobtainlonger-runimpactontheeconomy

ImperfectcompetitionintheFrancois,vanMeijl,andvanTongeren(2005)model,as

implementedhere,isexplainedinFrancois,Manchin,andMartin(2012).Itinvolves

firm level competition and supply of varieties of goods and services to both final

consumersanddownstreamfirmsunderwhatisknownasmonopolisticcompetition.

ThemodellingofinvestmenteffectsisbasedonFrancoisandMcDonald(1996).This

doesnotinvolvegrossforeigndirectinvestmentflows,butratherchangesinregional

andglobalcapitalstocks(machineryandequipment)asaresultofchangesinlevelsof

savingsandinvestment.

Box 2 Keyfeaturesofthemodel

Modelsimulationsarebasedonamulti-region,multi-sectorglobalCGEmodel.

Sectorsarelinkedthroughintermediateinputcoefficients(basedonnationalsocial

accountsdata)aswellascompetitioninprimaryfactormarkets.Themodelincludes

imperfectcompetition,short-runandlong-runmacroeconomicclosureoptions,as

wellasthestandardstatic,perfectcompetition,Armington-typeset-upasasubset.

Onthepolicyside,itofferstheoptiontoimplementtariffreductions,exporttax

and subsidy reduction, trade quota expansion, input subsidies, output subsidies,

andreductionsintradecosts.Internationaltradecostsincludeshippingandlogistic

services(thesourceoffob-cifmargins),butcanalsobemodelledasSamuelson-

typedeadweightcosts.Thiscanbeusedtocapturehighercostswhenproducingfor

exportmarkets,duetoregulatorybarriersorNTBsthatdonotgeneraterents(or

wheretherentsaredissipatedthroughrent-seeking).

Technical Discussion on CGE Modelling Set Up

23

In theCGEmodel, there is a single representative or composite household in each

region. Household income is allocated to government, personal consumption, and

savings. In each region the composite household owns endowments of the factors

of production and receives incomeby selling the services of these factors to firms.

It also receives income from tariff revenue and rents accruing from import/export

quotalicenses.Partoftheincomeisdistributedassubsidypaymentstosomesectors,

primarilyinagriculture.

Taxes are included at several levels in the model. Production taxes are placed on

intermediateorprimaryinputs,oronoutput.Tariffsareleviedattheborder.Additional

internal taxes are placed on domestic or imported intermediate inputs, andmay be

applied at differential rates that discriminate against imports.Where relevant, taxes

arealsoplacedonexports,andonprimaryfactorincome.Finally,whererelevant(as

indicatedbysocialaccountingdata)taxesareplacedonfinalconsumption,andcanbe

applieddifferentiallytoconsumptionofdomesticandimportedgoods.

Ontheproductionside,inallsectors,firmsemploydomesticproductionfactors(capital,

labourandland)andintermediateinputsfromdomesticandforeignsourcestoproduce

outputsinthemostcost-efficientwaythattechnologyallow.Inmostsectors,perfect

competition isassumed,withproducts fromdifferent regionsmodelledas imperfect

substitutes.

Heavymanufacturingsectorsaremodelledwithimperfectormonopolisticcompetition.

Monopolistic competition involves scale economies that are internal to each firm,

depending on its own production level.An important property of themonopolistic

competitionmodelisthatincreasedspecialisationatintermediatestagesofproduction

yields returns due to specialisation, where the sector as a whole becomes more

productivethebroadertherangeofspecialisedinputs.Inmodelsofthistype,partof

theimpactofpolicychangesinfinalconsumptionfollowsfromchangesinavailable

choices(thevarietyofgoodstheycanchoosefrom).Similarlyfirmsareaffectedby

changes in available choices (varieties)of intermediate inputs.Changes in available

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

24

varieties also involve changes in available foreign varieties, in addition to domestic

one.Asaresult,changesinconsumerandfirminputchoiceswill“spill-over”between

countriesastheytradewitheachother.

TariffsandtariffrevenuesareexplicitinthestandardGTAPdatabase,andthereforecan

bedirectlyincorporatedintothemodelusedheredirectlyfromthestandarddatabase.

However,NTBsaffectinggoodsandservicestrade,aswellascostsavingslinkedto

tradefacilitationarenotexplicitinthedatabaseandweneedtotakestepstocapture

these effects.Where NTBs leads to higher costs, we follow the standard approach

tomodelling icebergordead-weight tradecosts in theGTAP framework,originally

developedbyFrancois(1999,2001)withsupportfromtheECtostudytheMillennium

Round (nowknownas theDohaRound).10 Ithas featured in the jointEC-Canadian

governmentstudyonanEU-CanadaFTA,aswellasthe2009EcorysstudyonEU-US

non-tariffbarriers.Informalterms,wemodelchangesintheefficiencyofproduction

forsale inspecificmarkets. In thissense,wecancapture the impact thatNTBscan

haveinraisingcostswhenservingforeignmarkets.WhereNTBsinsteadinvolvehigher

pricesbecauseofrents,wemodelthisasadditionalmark-ups(higherprices)accruing

tofirms.AshighlightedalreadyinthediscussioninChapter2,thereisanapproximate

60:40splitbetweencostgeneratingNTBsandrentgeneratingNBTs,intermsofimpact.

3.2. Sectors and regions in the model

WhileintheGTAPdataabout60sectorsand130differentregionsareavailable,forthe

purposeofthisstudywehaveaggregatedsectorsandregionstoallowustoconcentrate

onthekeyresults.ThesectorandregionalaggregationsarepresentedinTable3.

10 TheoriginalFrancoisapproachhasgrownfromaspecializedextensioninearlyapplicationstoanowstandardfeatureoftheGTAPmodel,followingitsincorporationbyHertel,WalmsleyandItakura(2001).

Technical Discussion on CGE Modelling Set Up

25

Table 3 SectorsandregionsusedintheCGEmodel

Sectors RegionsAgrforestryfisheries EuropeanUnionOtherprimarysectors UnitedStatesProcessedfoods OtherOECD,highincomeChemicals EastEuropeElectricalmachinery MediterraneanMotorvehicles ChinaOthertransportequipment IndiaOthermachinery ASEANMetalsandmetalproducts MERCOSURWoodandpaperproducts LowIncomeOthermanufactures RestofWorldWatertransportAirtransportFinanceInsuranceBusinessservicesCommunicationsConstructionPersonalservicesOtherservices

27

In thischapterwesummarize thepolicyscenariosused in theCGEassessment that

followsinChapter5.Thisincludessomeexplanationofconcepts,suchas“policyspill-

overs,”thatareincludedinthescenarios.

4.1. Scenarios

Asdiscussed inChapter2,while it isconceivableforall tariffs toberemoved, it is

not realistic to assume that all NTBs and costs from regulatory divergence can be

removed.Thisisbecauseoftheunderlyingdifferencesinthenatureofthesemeasures.

AsaresultwhenmodellingtheliberalisationofNTBswemusttakeintoaccountthe

degree towhichNTB-related costs can realistically be reduced (via variousmeans

and techniques).On thebasis of theEcorys (2009) survey, a reasonableunderlying

ruleofthumbisthatapproximately50percentofthecost/priceimpactofNTBscan

beremoved–i.e. theyare“actionable.”While there issomevariationbysector, the

mappingfromoverallprice/costdifferencestothosethatcanbenegotiatedonreflects

thisfinding,whichisbasedonexpertopinions,cross-checkswithregulators,legislators

andbusinessessupportedbythebusinesssurveyfromtheEcorys(2009)study.Against

thisbackground,thestudyissetuparoundscenariosdifferingwithrespecttolevelsof

ambitionandscopeofcoverage.ThescenariosaresummarizedinTable4below.

Thescenariossummarizedinthetablearerelativelymodest.Startingfromthelevelof

barriersreportedinTable2,onlyabouthalfofthebarriersareconsideredasnegotiable

oractionable.Ofthese,halfarereducedinthemostambitiousscenario(or25percent

4. The Policy Options Considered

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

28

oftotalNTBsinTable2).Thisisthemostambitiousscenario.Themodestscenarios

assumeevenlessreductioninNTBs.Underboththeambitiousandmodestscenarios,it

isassumedthatmoreaggressiveliberalizationisappliedtoprocurement.Thescenarios

reported here are therefore far less ambitious than under the original Ecorys study,

wherefulleliminationofactionableNTBswasassumed.

Table 4 ScenarioSummaries

Narrow(limited)FTAScenariosTariffsonly 98percentoftariffseliminatedServicesonly 10percentofservicesNTBseliminatedProcurementonly 25percentofprocurementNTBseliminatedComprehensiveScenarios

Lessambitious

98percentoftariffseliminated

10percentofNTBseliminatedonbothgoodsandservices(20percentofactionable)

25percentofprocurementNTBseliminated

Ambitious

100percentoftariffseliminated

25percentofNTBseliminatedonbothgoodsandservices(50percentofactionable)

50percentofprocurementNTBseliminated

4.2. Spill-overs

Thesimulationsthatarecarriedoutalsotakeintoaccountconceptsofbothregulatory

convergenceandregulatoryspill-overs.Morespecifically,insettinguptheexperiments,

wehaveincludedtwosetsofpossibleeffectsbeyondbilateralliberalization.Theseare

definedasfollows.First,wehaveincludeddirect spill-overs.Thesearebasedonthe

assumptionthatimprovedregulatoryconditionsnegotiatedbetweentheEUandtheUS

willalsoresultinalimitedfallinrelatedtradecostsforthirdcountriesexportingtothe

EUandUS.Inotherwords,thiscapturestheextenttowhichthebilateralstreamlining

of regulationsandstandards,and reduction in regulatoryburdens,alsobenefitother

exporterstotheEUandUS.Thispositivemarketaccesseffectforthirdcountriesis

modelledasbeingaround20percentofthebilateralfallintradecostrelatedtoNTBs

forthecorescenarios.(Wehavealsoexamined10percentspill-oversasarobustness

The Policy Options Considered

29

check.)ThisconceptwasintroducedintheEU-JapanstudybyCopenhagenEconomics

(2009).Inpractice,itmeansthatifthereis5percentNTB-relatedtradecostreduction

betweentheEUandUS,therewillalsobea1percenttradecostreductionforthird

countriesexportingtotheEUandUS.Thelogicisthatfirmsinthirdcountriesmayfind

iteasiertomeeteitherEUorUSregulatoryrequirementsifbilateralnegotiationslead

to simplifications thatarenot inherentlydiscriminatory.KoxandLejour (2006), for

example,provideevidencethatdifferencesinregulationscanincreaseoperatingcosts

indifferentmarkets,reducingbilateraltrade.

Asecondindirecteffectinvolvingthirdcountriesisconsideredaswell:theindirect spill-

overs.Thesearemeanttogaugetheeconomicimplicationsifthirdcountriesadoptsome

ofthecommonstandardsagreedbetweentheEUandtheUS.Giventhat,collectively,

theEUandtheUSwouldstandastheworld’sbiggesttradingblock,thereisavery

realpossibilitythatmutualagreementonregulationsandstandardswouldbeadopted,

partially,alsobythirdcountries.Thus,wheretheEUandtheUSactasaregulatory

hegemon,thereisscopeforsettingdefactocommon,globalstandards.Thisimplies

thatthebilateralagreementwillgiveEUandtheUSimprovedmarketaccessinthird

marketsfromreducedNTBs.Inaddition,therewillbescopeforreductionsinNTBs

amongst third countries, as they converge further on common standards.Therefore,

indirectspill-overswillleadtolowercostsandgreatertradebetweenthirdcountriesas

well.Wehavemodelledindirectspill-oversas50percentofthedirectspill-overrate.

Thismeansthatforexamplefora5percenttradecostreductionbetweentheEUand

US,andwith20percentcorrespondingdirectspill-overs,wewillhavea1percent

(directspill-over)reductionforthirdcountriesexportingtotheUSorEU,anda0.5per

cent(indirectspill-over)reductionforEUandUSexportcoststothirdcountries,and

fortradebetweenthirdcountries.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

30

4.3. Sectoral effects: Preliminary ranking

Atthisstage,wehavespelledout tradeflows, tariffbarriers,andnon-tariffbarriers.

InwhatfollowsinChapter5,wewillfocusoneffects.Beforedoingso,itisusefulto

benchmarkexpectations.Whatwemeanisthat,beforeweturntomodellingresults,

wewant toprovideanon-modelbased rankingof some important sourcesof likely

effects. This involves the data summarized inTable 5 below. In theTable, column

Asummarizes the totalvalueof tariffsandactionableNTBs(asdefinedbyEcorys)

appliedbytheUSagainstEUexports.Thenexttwocolumnssummarizetheimportance

ofeachsectortototalEUexportstotheUS.ColumnBisbasedongrossvalues,while

columnCisbasedinsteadonthevalueaddedcontainedinexports.11IncolumnC,we

seethatwhilechemicalsare12.38percentofexportsonagrossvaluebasis,theyare

somewhatlessimportantonavalueaddedbasis,accountingfor11.21percentofEU

valueaddedcontainedinexportstotheEU.Asacrudefirstpassatpossibleeffects,

columnEprovidesanimpact-rankingindex.Thisisbasedonthevalueaddedcontained

in exports by sector (C), the scope for liberalization (A), and theprice elasticityof

demandforimports(D).Together,theseprovidearoughestimateofincreasedexports,

onavalueaddedbasis,followingfromimprovedmarketaccesstotheUSforEUfirms.

Forexample,ofthetotalvalueaddedcontainedinEUexportstotheUS,columnEsays

thatfullliberalizationinchemicalscouldyieldan8.39percentincreaseintotalexports

totheUSonavalueaddedbasis.AsitisvalueaddedthattranslatesintoGDP,theindex

alsoprovidesacruderankingofoverallGDPimpactsofsector-specificliberalization.

11 SeeFrancois,Manchin,andTomberger(2012)forexplanationofthevalueaddedcalculations,whicharebasedonourCGEmodeldatabase

The Policy Options Considered

31

Table 5 Impactrankingindexes

A B C D E=.01*A*C*D

actionable

NTBs+tariffsgrossexport

shareexportvalueaddedshare

priceelasticity index

Agrforestryfisheries

3.70 1.73 2.09 4.77 0.37

Otherprimarysectors

0.00 1.36 1.70 12.13 0.00

Processedfoods 48.93 4.42 4.71 2.46 5.67Chemicals 14.69 12.38 11.21 5.09 8.39Electricalmachinery

9.91 1.09 0.94 9.65 0.89

Motorvehicles 22.49 8.81 7.11 10.00 15.99Othertransportequipment

8.63 5.31 4.94 7.14 3.04

Othermachinery 0.80 16.92 16.25 9.71 1.26Metalsandmetalproducts

6.69 2.75 2.53 13.91 2.36

Woodandpaperproducts

5.76 2.42 2.61 7.99 1.20

Othermanufactures

3.20 7.32 4.90 6.56 1.03

Watertransport 0.65 0.05 0.04 3.80 0.00Airtransport 2.35 3.12 2.41 3.80 0.22Finance 6.46 6.20 7.45 2.04 0.98Insurance 3.84 6.02 7.10 3.18 0.87Businessservices 1.58 10.07 12.28 3.18 0.62Communications 0.65 0.85 1.01 3.18 0.02Construction 0.90 0.35 0.36 4.21 0.01Personalservices 0.66 1.49 1.76 8.71 0.10Other(public)services

0.00 7.36 8.59 3.92 0.00

Source: CGEcalculations.

TheestimatesincolumnEofTable5areofcoursepartialequilibrium.Theymisscross-

sectoreffects,includinglabourmarketinteractionandintermediatelinkages.Theyalso

missconsumerbenefitsfromaccesstomoregoodsandservices.Evenso,theyprovide

aclearrankingoflikelyeffects.Thisrankingcarriesthroughtheestimatesinthenext

chapter, and so it isworth discussing the pattern for the impact indexes briefly, as

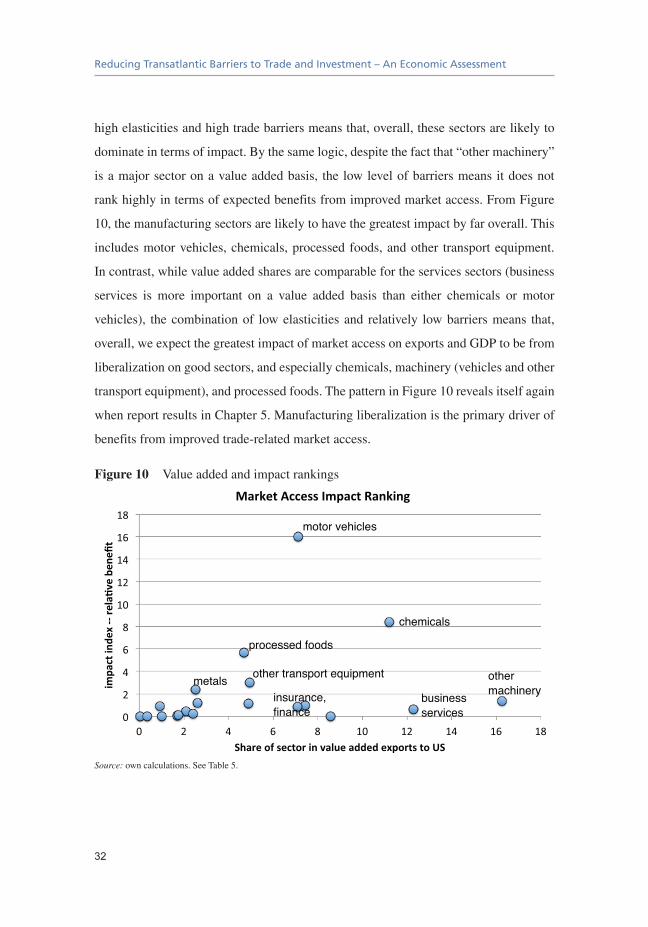

showninFigure10.Fromthefigure,wecanseethatforsomesectors,especiallymotor

vehicles, though they are not dominant on a value added basis, the combination of

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

32

highelasticitiesandhightradebarriersmeansthat,overall,thesesectorsarelikelyto

dominateintermsofimpact.Bythesamelogic,despitethefactthat“othermachinery”

isamajorsectoronavalueaddedbasis, the lowlevelofbarriersmeansitdoesnot

rankhighlyintermsofexpectedbenefitsfromimprovedmarketaccess.FromFigure

10,themanufacturingsectorsarelikelytohavethegreatestimpactbyfaroverall.This

includesmotorvehicles,chemicals,processedfoods,andother transportequipment.

Incontrast,whilevalueaddedsharesarecomparablefortheservicessectors(business

services is more important on a value added basis than either chemicals or motor

vehicles), thecombinationof lowelasticitiesand relatively lowbarriersmeans that,

overall,weexpectthegreatestimpactofmarketaccessonexportsandGDPtobefrom

liberalizationongoodsectors,andespeciallychemicals,machinery(vehiclesandother

transportequipment),andprocessedfoods.ThepatterninFigure10revealsitselfagain

whenreportresultsinChapter5.Manufacturingliberalizationistheprimarydriverof

benefitsfromimprovedtrade-relatedmarketaccess.

Figure 10 Valueaddedandimpactrankings

Source: owncalculations.SeeTable5.

33

In this chapter we focus on the results of the CGE modelling of bilateral trade

liberalization.Theresultsarereportedwithrespecttoaneconomicbenchmarkprojected

outtotheyear2027,whichimpliesthatthattheycapturetheimpactoftheagreement

afulltenyearsaftertheimplementationoftheagreement,providingthelonger-term

impactofpolicychanges.First,wepresentresultsforthelimitedscenarios.Wethen

examinethecomprehensivescenarios,assumingthatanagreementwouldcollectively

covertariffs,services,andprocurement.Wethenmoveontoreportingestimatedeffects

on output and trade, first on an aggregate and then on amore disaggregate, sector

specific level.Wealsoprovideadiscussionof the effectsof removalofbarrierson

sustainability,i.e.effectsonlabour,CO2emissionsandtheuseofnaturalresources.

Thelastpartofthischaptersummarisestheresultingeffectsontherestoftheworld.

5.1. Limited Scenarios

Inthissection,wepresentresultsassumingthatalessambitious,limitedFTAwouldbe

implemented.Weanalysetheimpactassumingthatonlyasinglepolicypillar,i.e.only

tariffliberalisation,oronlyservicesliberalization,oronlyprocurementliberalisation

wouldbe implemented.Note that the liberalisationefforts thatarebeingconsidered

for each pillar are similar to those envisaged in the less ambitious scenario of the

comprehensiveFTAoption(seeTable4),including20percentspill-overs.12Forthe

tariffonlyagreementthereareobviouslynospill-overs.

12 Resultswith10percentspill-oversarereportedinseparateannextables.

5. Results

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

34

Thefirstconclusiontotakefromtheresultsofthepartialagreementsisthatliberalising

eachpolicypillarsseparatelyleadstorelativelysmall increasesinGDPforboththe

USandtheEU(seeTable6andTable7below).FortheEU,thetariffscutsleadtoa

GDP increaseof0.10percent (23,753millioneuros),while the reductionofNTBs

inservicesandinprocurementincreaseGDPbyonly0.02percent(5,298and6,367

millioneuros).FortheUS,thesechangesareevensmaller(rangingfrom0.01to0.04

percent).

Table 6 ChangesinGDP(inpercent),2027benchmark,limitedagreement,20per

centdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnlyEuropeanUnion 0.10 0.02 0.02UnitedStates 0.04 0.03 0.01Other -0.01 0.00 0.00OtherOECD,highincome

-0.03 0.00 0.00

EastEurope -0.04 0.00 0.00Mediterranean -0.04 0.00 0.00China 0.01 -0.01 -0.01India -0.01 0.00 0.00ASEAN -0.02 0.01 -0.01MERCOSUR -0.01 0.00 0.00LowIncome -0.02 0.00 0.00RestofWorld -0.02 0.00 0.00

Source: CGEcalculations.

Results

35

Table 7 ChangesinGDP(inmillioneuros),2027benchmark,limitedagreement,

20percentdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnlyEuropeanUnion 23,753 5,298 6,367UnitedStates 9,447 7,356 1,875Other -7,903 -117 -1,595OtherOECD,highincome

-5,065 726 -668

EastEurope -292 26 4Mediterranean -580 60 -8China 2,289 -1,713 -856India -489 137 79ASEAN -832 337 -263MERCOSUR -363 182 -5LowIncome -228 39 47RestofWorld -2,344 90 75

Source: CGEcalculations.

Therelativesizeoftheservicesimpactislinkedbothtothemagnitudeofunderlying

bilateralbarriersthatarereduced(seeTable2)andalsototherelativetradevolumes

(seeFigure2).NTBsareperceivedbybusinessesasroughly2.5timeshigheringoods

thanservices,asappliedintheexperiments.ThiscapturesthefactthatboththeEUand

USarerelativelyopen,byglobalstandards,intheservicesectors.Atthesametime,

goodstradeistwicethevalueofservicestrade.Thustherelativemagnitudesforgoods

andservicesNTBsareconsistentwiththebenchmarklevelsofprotectionandtrade.

Next,welookattheexpectedchangesintradefortheEUandtheUS.Theresultsare

presentedforeachmeasureseparatelyinTable8andTable9below.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

36

Table 8 Changesintrade(inpercent),extra-EUtradefortheEU,2027benchmark,

limitedagreement,20percentdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnlyExportsEuropeanUnion 1.18 0.16 0.19UnitedStates 1.91 0.19 0.23

ImportsEuropeanUnion 1.00 0.13 0.18UnitedStates 1.13 0.57 0.14

Terms of tradeEuropeanUnion -0.01 0.00 0.00UnitedStates 0.04 -0.01 -0.02

Source:CGEcalculations.

Table 9 Changesintrade(inmillioneuros),extra-EUtradeincaseoftheEU,2027

benchmark,limitedagreement,20percentdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnlyExportsEuropeanUnion 43,740 5,777 7,136UnitedStates 57,330 5,488 5,942

ImportsEuropeanUnion 44,338 5,742 7,881UnitedStates 47,775 4,655 5,869

Source:CGEcalculations.

Amongthepartialagreementoptions, the tariffcutsareshowntodeliver thelargest

increase in trade flows. Here, both exports and imports are shown to increase by

between 1 and 2 per cent. Extra-EU exports are estimated to increase by 1.18 per

cent(correspondingto44billioneuros)whileimportsfromoutsideEUareexpected

toriseby1.00percent(correspondingalso toabout44billioneuros increase).The

changesareestimatedtobeslightlyhigherfortheUS.Liberalisingprocurementand

serviceswill leadtorelativelysmall, less than0.5percent(about6-7billioneuros)

increases inexportsand imports.Theresultingchanges in termsof tradeareshown

tobe insignificant.While theprocurementandservicesoptions leadtosimilarGDP

effects, the trade effects are larger overall for procurement.This traces back to the

Results

37

underlying trade elasticities.Goods are estimated to bemoreprice sensitive overall

(seethediscussioninChapter4)andthistranslatesintosomewhatlargertradevolume

effects.However,bothsetsoftradevolumeeffectsaremuchsmallerthantheestimates

discussedbelowlinkedtoamorecomprehensiveagreement.

ThetablesbelowshowtheimpactofthelimitedFTAonbilateralsectoraltradebetween

theEUandtheUS.Limitingtheliberalisationtoservicesorprocurementonlywould

haveaverymarginalimpactonsectoraltrade,withtheexceptionofsomeoftheservices

exportsand imports increasingasbarriers removedunder theservices liberalisation.

Nevertheless,onaverage,bothbilateralexportsandimportswouldincreasebyabout

1per centor less if only servicesorprocurement is liberalised.On theotherhand,

thecutsintariffswouldleadto6.6percentincreaseofEUexportstotheUSandto

a12.4percentincreaseinimports.Thedifferenceinthemagnitudeofchangeisdue

totheinitialtariffstructuresbetweenthetwoeconomies,withtheEUhavinghigher

barrierstowardstheUS.Thusthedifferenceintheseaveragechangesismainlydriven

bymotorvehicles.Inthissectortheimportswouldsignificantlyincreaseastariffsare

removedforUSexporters.Inabsoluteterms,thegreatestincreaseinbilateralservices

exportsunderservices-onlyliberalizationisinfinance,insurance,andbusinessservices

inthecaseoftheEU,andinfinanceandbusinessservicesinthecaseoftheUS.With

procurement only,we see bilateral trade growth primarily in goods (chemicals and

vehiclesexportsfortheEU,chemicalsandmetalsandfabricatedmetalproductsforthe

US).Thebilateraltradeeffectsoftariffsoutweighboththeprocurementandservices

only scenarios.There is substantial growth in bilateral trade in chemicals, vehicles,

machinery, and othermanufactures.Total trade (EU exports to theUS,US exports

totheEU)expandsbyalmost100billioneurosinthetariffonlyscenario.Thesector

patternreflectsthebasicpatternoftariffsinthetariffs-onlyscenario,asdiscussedin

Chapter2,alongwiththeunderlyingelasticitiesasdiscussedinChapter3.Forexample,

USmanufacturing tariffs are relatively low, and highest on othermanufactures and

processedfoods(Figure9).

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

38

Table 10 Changes in EU bilateral exports to US by sector (in per cent), 2027

benchmark,limitedagreement,20percentdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnly

PercentMillioneuros

PercentMillioneuros

PercentMillioneuros

Agrforestryfisheries

17.53 2,024 0.00 0 -0.15 -17

Otherprimarysectors

0.37 33 0.05 4 0.00 0

Processedfoods 8.15 2,402 0.00 0 1.50 442Chemicals 5.46 4,509 -0.09 -77 2.59 2,140Electricalmachinery

3.08 225 -0.19 -14 -0.22 -16

Motorvehicles 13.70 8,048 -0.05 -29 5.69 3,345Othertransportequipment

1.84 653 -0.01 -4 1.50 531

Othermachinery 8.60 9,705 -0.11 -123 -0.11 -126Metalsandmetalproducts

20.40 3,744 0.01 2 4.13 757

Woodandpaperproducts

2.23 359 -0.02 -4 -0.19 -30

Othermanufactures

23.35 11,402 -0.02 -12 -0.05 -27

Watertransport 0.32 1 3.35 12 0.26 1Airtransport 0.24 50 0.79 164 0.03 7Finance 0.22 93 4.32 1,787 -0.03 -13Insurance 0.27 107 4.35 1,746 -0.06 -24Businessservices 0.43 288 1.23 825 0.13 87Communications 0.20 11 0.73 41 0.07 4Construction 0.45 10 1.73 40 0.48 11Personalservices 0.46 46 2.49 247 -0.26 -25Otherservices 0.27 130 -0.03 -13 -0.10 -50total 6.57 43,840 0.69 4,591 1.05 6,997

Source:CGEcalculations.

Results

39

Table 11 ChangesinUSbilateralexportstoEUbysector,2027benchmark,limited

agreement,20percentdirectspill-overs

TariffsOnly ServicesOnly ProcurementOnly

PercentMillioneuros

PercentMillioneuros

PercentMillioneuros

Agrforestryfisheries

19.33 978 0.03 1 0.15 8

Otherprimarysectors

0.50 51 -0.04 -4 0.00 0

Processedfoods 39.82 2,173 0.03 2 0.11 6Chemicals 12.45 9,927 0.16 129 0.54 430Electricalmachinery

3.39 639 0.91 171 1.07 201

Motorvehicles 109.50 20,808 0.11 20 0.67 127Othertransportequipment

7.61 2,823 0.05 18 0.32 118

Othermachinery 12.10 5,659 0.16 75 0.28 129Metalsandmetalproducts

23.43 4,995 0.03 6 9.29 1,980

Woodandpaperproducts

3.74 257 0.07 5 0.73 50

Othermanufactures

15.80 5,836 0.04 16 0.06 22

Watertransport -0.25 -1 2.90 17 0.11 1Airtransport -0.17 -29 0.74 125 0.08 14Finance -0.14 -35 2.16 546 0.66 166Insurance -0.24 -9 3.25 116 0.09 3Businessservices -0.36 -130 2.41 862 0.09 32Communications -0.18 -12 4.60 300 0.11 7Construction -0.31 -7 2.76 65 1.14 27Personalservices -0.42 -29 5.07 355 0.30 21Otherservices -0.23 -116 0.07 35 0.14 69total 12.36 53,777 0.66 2,859 0.78 3,411

Source:CGEcalculations.

Table12belowshowsthecorrespondingestimatedchangesintheEU’stotalexternal

trade (extra-EU). Overall, the tariff cuts are expected to cause total imports and

exports to increaseby1.18and1.00percentrespectively.Theinducedeffectsfrom

liberalisingtradeinservicesandprocurementaresmaller,rangingfrom0.13to0.19

per cent respectively.Nevertheless, exports in the insurance and finance sectors are

estimatedtoincreasebyabout2percentifservicesareliberalised.Meanwhile,finance,

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

40

communications,andpersonalservicesimportsareestimatedtoincreaseby1-1.8per

cent due to services liberalisation. Under tariff liberalisation, the highest increase

in importswould takeplace inmotorvehicleswitha9.21percent,while regarding

exportsthemostpronouncedincreaseisestimatedtotakeplaceinothermanufactures

witha5.50percentincrease.

Table 12 Changes in EU trade by sector (in per cent), 2027 benchmark, limited

agreement,20percentdirectspill-overs

Totalexports Totalimports

Tariffsonly ServicesonlyProcurement

onlyTariffsonly Servicesonly

Procurementonly

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Agrforestryfisheries

0.58 1,303 0.00 3 -0.05 -102 2.64 1,342 0.10 52 0.17 85

Otherprimarysectors

-0.27 -363 0.03 35 0.01 11 0.52 3,643 0.01 98 0.01 47

Processedfoods 1.33 2,360 0.03 45 0.27 481 2.66 2,282 0.07 64 0.12 100

Chemicals 1.23 4,707 -0.01 -47 0.65 2,478 2.46 7,972 0.08 268 0.13 419

Electricalmachinery

-0.03 -26 -0.02 -15 -0.31 -292 0.39 1,357 0.01 23 0.01 24

Motorvehicles 3.70 8,399 -0.02 -43 1.47 3,340 9.21 16,799 0.11 193 0.22 404

Othertransportequipment

0.56 914 -0.02 -38 0.27 442 2.54 2,345 0.06 55 0.16 151

Othermachinery 1.73 10,359 -0.08 -487 -0.10 -611 0.82 3,969 0.14 685 0.03 126

Metalsandmetalproducts

2.70 3,720 -0.01 -18 1.15 1,589 1.18 4,156 0.06 214 1.45 5,111

Woodandpaperproducts

0.16 222 -0.01 -17 -0.05 -72 0.67 438 0.11 74 0.29 189

Othermanufactures

5.50 11,957 0.02 34 -0.02 -36 -0.03 -250 0.05 523 0.04 412

Watertransport 0.10 47 0.22 100 0.03 14 -0.02 -8 0.31 118 0.05 21

Airtransport 0.14 110 0.21 162 0.01 9 -0.09 -84 0.21 203 0.05 51

Finance 0.09 87 2.00 1,864 0.00 2 0.09 63 1.02 695 0.32 221

Insurance 0.09 86 2.03 1,849 -0.03 -27 0.12 20 0.94 160 0.07 12

Businessservices 0.04 183 0.36 1,500 0.02 77 -0.08 -144 0.62 1,127 0.06 103

Communications 0.00 0 0.47 127 0.02 6 0.09 35 1.15 420 0.08 29

Construction -0.02 -13 0.27 176 0.00 -1 0.09 20 0.47 110 0.22 52

Personalservices -0.13 -138 0.50 552 -0.11 -117 0.15 41 1.84 487 0.21 55

Otherservices -0.06 -173 0.00 -4 -0.02 -53 0.12 341 0.06 173 0.10 267

Total 1.18 43,740 0.16 5,777 0.19 7,136 1.00 44,338 0.13 5,742 0.18 7,881

Source:CGEcalculations.

Results

41

ThereductionoftariffswillleadUSimportsandexportstoincreaseby1.91and1.13

percentrespectively(Table13).Thebiggestincreasesareestimatedtotakeplacein

theexportofmotorvehicles (15.43percent),chemicals (4.05percent),metalsand

metalproducts(4.33percent).AscanbeseenfromtheTable,theestimatedeffectsof

theliberalisationofservicesandprocurementontradearemuchsmaller.Thebiggest

changes in imports are also attributable to the reduction of tariffs,with the highest

sectorspecificincreasesexpectedtotakeplaceinprocessedfoodsandmetalsandmetal

productions(2.37percentand2.43percentrespectively)andmotorvehicles(2.13per

cent).Theliberalisationoftheservicessectorsishoweverestimatedtoincreaseimports

offinanceandinsuranceservicesbyaround3percent.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

42

Table 13 Changes inUS trade by sector (in per cent), 2027 benchmark, limited

agreement,20percentdirectspill-overs

Totalexports Totalimports

TariffsOnly ServicesOnlyProcurement

OnlyTariffsOnly ServicesOnly

ProcurementOnly

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Percent

Mlneuros

Agrforestryfisheries

0.29 1,386 0.00 -16 0.03 140 1.74 1,814 0.03 35 -0.08 -82

Otherprimarysectors

-0.09 -166 0.00 8 0.01 18 0.14 696 0.05 265 0.00 -2

Processedfoods 2.39 2,556 0.02 16 0.03 31 2.37 2,490 0.01 14 0.58 608

Chemicals 4.05 13,363 0.11 375 0.11 362 1.06 2,857 -0.06 -167 1.00 2,678

Electricalmachinery

-1.10 -1,534 0.76 1,061 0.59 826 0.94 3,994 -0.26 -1,106 -0.35 -1,467

Motorvehicles 15.43 23,826 0.05 80 0.31 477 2.13 8,879 0.01 25 0.91 3,773

Othertransportequipment

1.55 2,688 0.02 34 0.18 305 1.08 929 0.02 18 0.55 473

Othermachinery 1.77 4,854 0.08 220 0.17 466 1.46 10,363 0.01 72 -0.14 -1,012

Metalsandmetalproducts

4.33 5,171 0.01 10 2.14 2,553 2.43 4,716 0.08 165 0.69 1,339

Woodandpaperproducts

0.00 0 0.02 14 0.13 96 0.82 1,088 0.03 40 -0.11 -143

Othermanufactures

3.40 6,989 0.03 69 0.04 84 1.06 8,190 0.03 213 -0.03 -237

Watertransport 0.07 3 0.09 4 0.03 1 0.22 6 0.63 18 0.04 1

Airtransport 0.04 19 0.18 96 0.04 19 0.12 66 0.34 182 0.01 7

Finance -0.10 -78 0.98 736 0.27 203 0.26 156 3.14 1,903 -0.02 -13

Insurance -0.26 -85 0.68 222 0.03 9 0.31 191 2.81 1,716 -0.04 -26

Businessservices -0.29 -398 0.90 1,240 0.04 55 0.39 609 0.55 861 0.05 79

Communications -0.18 -36 2.07 411 0.05 11 0.24 36 0.32 48 0.02 3

Construction -0.33 -42 0.82 105 0.27 35 0.45 26 0.80 47 0.23 13

Personalservices -0.57 -429 0.95 712 0.13 98 0.60 124 1.43 298 -0.18 -38

Otherservices -0.28 -758 0.03 90 0.06 152 0.35 544 0.01 9 -0.06 -88

Total 1.91 57,330 0.19 5,488 0.23 5,943 1.13 47,775 0.57 4,655 0.14 5,868

Source:CGEcalculations.

Wenowturntoanalysingtheestimatedeffectsontheoutputofthedifferentsectors.

TheunderlyingchangesfortheEUandtheUSarepresentedinTable14andTable15

below.

Results

43

Table 14 Changes inEUoutputbysector(inpercent),2027benchmark, limited

agreement,20percentdirectspill-overs

Baselinesharesinvalueadded

TariffsOnly ServicesOnly ProcurementOnly

Agrforestryfisheries

0.040 0.03 0.00 0.00

Otherprimarysectors

0.019 0.00 0.00 0.00

Processedfoods 0.030 0.06 0.01 0.04Chemicals 0.028 -0.11 -0.01 0.12Electricalmachinery

0.004 -0.31 0.02 0.06

Motorvehicles 0.015 -0.65 -0.01 0.30Othertransportequipment

0.007 -0.26 -0.02 0.09

Othermachinery 0.037 0.35 -0.04 0.03Metalsandmetalproducts

0.021 0.03 -0.03 -0.39

Woodandpaperproducts

0.023 0.06 0.00 -0.01

Othermanufactures

0.029 0.60 -0.01 0.01

Watertransport 0.003 0.14 -0.04 0.03Airtransport 0.003 0.15 -0.01 0.01Finance 0.032 0.06 0.11 -0.02Insurance 0.010 0.06 0.32 0.01Businessservices 0.222 0.05 0.01 0.02Communications 0.023 0.05 -0.03 0.01Construction 0.083 0.12 0.03 0.02Personalservices 0.035 0.04 0.02 0.00Otherservices 0.338 0.05 0.01 0.01

Source:CGEcalculations.

AscanbeseenintheTable14,thecorrespondingestimatedchangesinsectorspecific

outputareverysmall.Noneofthesectorswillexpandorcontractbymorethan1per

centinthecaseoftheEU,andinmostsectorsoutputwillbasicallyremainunchanged.

Similarly,onlyslightchangesareexpectedtotakeplaceinUSsector-leveloutputasa

consequenceofthenon-comprehensiveFTAsthatweresimulated.Inonlytwosectors

theoutputisestimatedtochangebymorethan1percent:intheelectricalmachinery

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

44

sectoritisestimatedtodecreaseby1.40percent,whileinmotorvehiclesitisexpected

toincreaseby1.76percent(oncetariffsarecut).

Table 15 Changes inUSoutputbysector (inpercent),2027benchmark, limited

agreement,20percentdirectspill-overs

Baselinesharesin

valueaddedTariffsOnly ServicesOnly

ProcurementOnly

Agrforestryfisheries 0.031 -0.02 0.00 0.00Otherprimarysectors 0.023 -0.01 0.00 0.00Processedfoods 0.017 0.06 0.02 -0.06Chemicals 0.021 0.81 0.07 -0.27Electricalmachinery 0.003 -1.40 0.64 0.73Motorvehicles 0.010 1.76 0.05 -0.56Othertransportequipment

0.009 0.38 0.03 -0.07

Othermachinery 0.027 -0.38 0.07 0.13Metalsandmetalproducts

0.014 0.15 0.05 0.07

Woodandpaperproducts

0.023 -0.05 0.03 0.02

Othermanufactures 0.010 0.05 0.02 0.00Watertransport 0.002 0.04 0.03 0.02Airtransport 0.004 0.00 0.00 0.02Finance 0.074 0.00 -0.11 0.01Insurance 0.020 -0.04 -0.27 0.01Businessservices 0.099 -0.01 0.01 0.00Communications 0.019 0.00 0.06 0.01Construction 0.080 0.09 0.04 0.01Personalservices 0.036 -0.01 0.04 0.02Otherservices 0.480 -0.02 0.00 0.00

Source:CGEcalculations.

Whilethenon-comprehensiveFTAoption,whichwouldbelimitedtoeithertariff,or

servicestrade,orprocurementliberalization,wouldresultinpositivechangesinsector-

leveloutputandtradepatterns,thesebenefitswouldberelativelysmall.Atanaggregate

level,thechangeswouldbeevensmaller.Whencomparingtheimpactofthesenon-

comprehensiveFTAswithacomprehensiveFTAthatwillbediscussedinthefollowing

section,itisclearthattheoverallbenefitswouldbeofmuchlargermagnitudeinthe

caseofatradeagreementthatcoversmorepolicypillarssimultaneously.

Results

45

5.2. Full FTA

5.2.1. Macro Results

Here,weturntothediscussionofeffectsonmacroeconomicvariables,resultingfrom

a reductionofbarriers to tradeand investmentbetween theEUand theUSundera

comprehensiveFTA(seeTable4fordetails).Insodoing,wepresenttheresultswith

regards to GDP.13As indicated above two FTA scenarios are considered: one less

ambitiousandonemoreambitious(asdescribedinTable4).

Table16andTable17belowshowtheestimatedeffectonGDPbothfortheambitious

andlessambitiousscenariosfortheEUandtheUS.Theresultsarepresentedforthe

totalimpactandalsodecomposedintothedifferentsubcomponentsthatcorrespondto

theseveralpolicypillars,namelytariffs,totalNTBsongoods,totalNTBsonservices,

directandindirectspill-overs,andprocurement.Procurementrelatedbarriersareinfact

capturedbytheNTBsingoodsandinservices.Aprocurementcolumnisintroduced

inthetablebelowinordertohighlighttheimportanceofthistypeofbarriersinthe

negotiations.However,itisimportanttonotethattheimpactofreducingprocurement

barriersshouldnotbeaddedtotheeffectsfromotherpillarsasitwouldmeandouble-

counting.

AscanbeseenTable16,theestimatedimpactonGDPfortheEUandUSrangebetween

0.2 and 0.5 per cent, for the less ambitious and ambitious scenarios respectively.

BecausewearedealingwithNTBsratherthantariffs,changesintradevolumesalone

arenotnecessarilyindicativeofthenetimpactonGDP,andsothereaderiscautioned

whencomparingTable16toTable20(changesinexports)below.Thisisbecause,as

13 Theannextablesalsoreportchangesinrealnationalincome.GDPisreportedherebecauseitisaconceptthatwillbemorefamiliartothereader.GDPisthevalueofafixedbasketoffinalgoodsandservicesproducedbytheeconomy.Realnationalincome,ontheotherhand,isameasureoftheactualpurchasingpoweravailableforfinalconsumption,givenchangesinbothoutputandprices. Realnational incomebettercapturesshifts in theeconomytowardamoreefficientbasketofgoodsandservices,aswellaschanges in finalconsumptionprices. Usually these twomeasurestrackeachotherclosely.However,whenthecurrentpatternofGDPreflectsstrongunderlyingdistortions,realnationalincomeisabettermeasureofthebenefitstotheagentsintheeconomy.

Reducing Transatlantic Barriers to Trade and Investment – An Economic Assessment

46

discussedearlierinthereport(seeChapters2and3),NTBsinvolvehighercostsand

solowerproductivity.TheimpactonGDPwillthereforehinge,inpart,oncostsavings

linkedtoremovingNTBs.Basically,withNTBsthatraisecoststheopportunitycosts

ofnewexportsresultingfromNTBreductionarelowerthanwithtariffs,sothatthecost

sideofthecost-benefitanalysisofincreasedtradeislower.TheimpactonGDPwill

alsohingeonthevalueaddedcompositionofexports.Assuch,eveniftradevolume

effects arenot relatively large in aparticular sector (recall ourdiscussionofFigure

10), theymaystillyield relatively largegainsoverall.The indirectspill-overeffects

aremorecomplexstill(thoughsmallinabsoluteterms).Therewillbebothincreased