Embed Size (px)

Citation preview

DEPARTMENT OF COMMERCEDEPARTMENT OF COMMERCE

NIZAM COLLEGENIZAM COLLEGE (AUTONOMOUS-NAAC ACCREDITED-CPE STATUS)

OSMANIA UNIVERSITY HYDERABAD.

C e r t i f i c a t eC e r t i f i c a t e

This is to certify that Mr./Ms.______________________________

studying in the B.Com (E.Com) I year, bearing a Hall Ticket no__________

has successfully completed computer Practical in the subject Financial

Accounting, as prescribed in the syllabus, during the Semester, ‘II’ for

the Academic Year 2010-2011.

External Examiner Internal Examiner

Name: Name:

Date: Date:

Rectification of Accounting ErrorsEvery businessman is interested in finding out the true profit and correct financial

position of his business at the close of the trading period. The effort of the

accountant is to prepare the final accounts in such a fashion which exhibits true

picture of the business. Accounts are considered to be authentic proof of true

financial position of a concern. But in spite of best efforts there are certain

transactions which are omitted to be recorded or entered wrongly in the books. Such

errors affect the final accounts. An accountant should, therefore, try to locate such

errors and rectify them before the preparation of final accounts.

Accountants prepare trial balance to check the correctness of accounts. If total of

debit balances does not agree with the total of credit balances, it is a clear-cut

indication that certain errors have been committed while recording the transactions

in the books of original entry or subsidiary books. It is our utmost duty to locate these

errors and rectify them, only then we should proceed for preparing final accounts. We

also know that all types of errors are not revealed by trial balance as some of the

errors do not effect the total of trial balance. So these cannot be located with the

help of trial balance. An accountant should invest his energy to locate both types of

errors and rectify them before preparing trading, profit and loss account and balance

sheet. Because if these are prepared before rectification these will not give us the

correct result and profit and loss disclosed by them, shall not be the actual profit or

loss.

All errors of accounting procedure can be classified as follows:

1. Errors of Principle

When a transaction is recorded against the fundamental principles of accounting, it is

an error of principle. For example, if revenue expenditure is treated as capital

expenditure or vice versa.

2. Clerical Errors

These errors can again be sub-divided as follows:

(i) Errors of omission

When a transaction is either wholly or partially not recorded in the books, it is an

error of omission. It may be with regard to omission to enter a transaction in the

books of original entry or with regard to omission to post a transaction from the

books of original entry to the account concerned in the ledger.

(ii) Errors of commission

When an entry is incorrectly recorded either wholly or partially-incorrect posting,

calculation, casting or balancing. Some of the errors of commission effect the trial

balance whereas others do not. Errors effecting the trial balance can be revealed by

preparing a trial balance.

(iii) Compensating errors

Sometimes an error is counter-balanced by another error in such a way that it is not

disclosed by the trial balance. Such errors are called compensating errors.

From the point of view of rectification of the errors, these can be divided into two

groups :

(i) Errors affecting one account only, and

(ii) Errors affecting two or more accounts.

Errors affecting one account

Errors which affect can be :

(a) Casting errors;

(b) error of posting;

(c) carry forward;

(cl) balancing; and

(e) omission from trial balance.

Such errors should, first of all, be located and rectified. These are rectified either with

the help of journal entry or by giving an explanatory note in the account concerned.

Rectification

Stages of correction of accounting errors

All types of errors in accounts can be rectified at two stages:

(i) before the preparation of the final accounts; and

(ii) after the preparation of final accounts.

Errors rectified within the accounting period

The proper method of correction of an error is to pass journal entry in such a way

that it corrects the mistake that has been committed and also gives effect to the

entry that should have been passed. But while errors are being rectified before the

preparation of final accounts, in certain cases the correction can't be done with the

help of journal entry because the errors have been such. Normally, the procedure of

rectification, if being done, before the preparation of final accounts is as follows:

(a) Correction of errors affecting one side of one account Such errors do not let the

trial balance agree as they effect only one side of one account so these can't be

corrected with the help of journal entry, if correction is required before the

preparation of final accounts. So required amount is put on debit or credit side of the

concerned account, as the case maybe. For example:

(i) Sales book under cast by Rs. 500 in the month of January. The error is only in sales

account, in order to correct the sales account, we should record on the credit side of

sales account 'By under casting of. sales book for the month of January Rs.

500".I'Explanation:As sales book was under cast by Rs. 500, it means all accounts

other than sales account are correct, only credit balance of sales account is less by

Rs. 500. So Rs. 500 have been credited in sales account.

(ii) Discount allowed to Marshall Rs. 50, not posted to discount account. It means that

the amount of Rs. 50 which should have been debited in discount account has not

been debited, so the debit side of discount account has been reduced by the same

amount. We should debit Rs. 50 in discount account now, which was omitted

previously and the discount account shall be corrected.

(iil) Goods sold to X wrongly debited in sales account.

This error is effecting only sales account as the amount which should have been

posted on the credit side has been wrongly placed on debit side of the same account.

For rectifying it, we should put double the amount of transaction on the credit side of

sales account by writing "By sales to X wrongly debited previously."

(iv) Amount of Rs. 500 paid to Y, not debited to his personal account. This error of

effecting the personal account of Y only and its debit side is less by Rs. 500 because

of omission to post the amount paid. We shall now write on its debit side. "To cash

(omitted to be posted) Rs. 500.

Correction of errors affecting two sides of two or more accounts

As these errors affect two or more accounts, rectification of such errors, if being done

before the preparation of final accounts can often be done with the help of a journal

entry. While correcting these errors the amount is debited in one account/accounts

whereas similar amount is credited to some other account/ accounts.

Correction of errors in next accounting period

As stated earlier, that it is advisable to locate and rectify the errors before preparing

the final accounts for the year. But in certain cases when after considerable search,

the accountant fails to locate the errors and he is in a hurry to prepare the final

accounts, of the business for filing the return for sales tax or income tax purposes, he

transfers the amount of difference of trial balance to a newly opened 'Suspense

Account'. In the next accounting period, as and when the errors are located these are

corrected with reference to suspense account. When all the errors are discovered and

rectified the suspense account shall be closed automatically. We should not forget

here that only those errors which effect the totals of trial balance can be corrected

with the help of suspense account. Those errors which do not effect the trial balance

can't be corrected with the help of suspense account. For example, if it is found that

debit total of trial balance was less by Rs. 500 for the reason that Wilson's account

was not debited with Rs. 500, the following rectifying entry is required to be passed.

Difference in trial balance

Trial balance is affected by only errors which are rectified with the help of the

suspense account. Therefore, in order to calculate the difference in suspense account

a table will be prepared. If the suspense account is debited in' the rectification entry

the amount will be put on the debit side of the table. On the other hand, if the

suspense account is credited, the amount will be put on the credit side of the table.

In the end, the balance is calculated and is reversed in the suspense account. If the

credit side exceeds, the difference would be put on the debit side of the suspense

account.

Effect of Errors of Final Accounts

1. Errors effecting profit and loss account

It is important to note the effect that an error shall have on net profit of the firm. One

point to remember here is that only those accounts which are transferred to trading

and profit and loss account at the time of preparation of final accounts effect the net

profit. It means that only mistakes in nominal accounts and goods account will effect

the net profit. Error in these accounts will either increase or decrease the net profit.

How the errors or their rectification effect the profit-following rules are helpful in

understanding it :

(I) If because of an error a nominal account has been given some debit the profit will

decrease or losses will increase, and when it is rectified the profits will increase and

the losses will decrease. For example, machinery is overhauled for Rs. 10,000 but the

amount debited to machinery repairs account -this error will reduce the profit. In

rectifying entry the amount shall be transferred to machinery account from

machinery repairs account, and it will increase the profits.

(il) If because of an error the amount is omitted from recording on the debit side of a

nominal account-it results in increase of profits or decrease in losses. The

rectification of this error shall have reverse effect, which means the profit will be

reduced and losses will be increased. For example, rent paid to landlord but the

amount has been debited to personal account of landlord-it will increase the profit as

the expense on rent is reduced. When the error is rectified, we will post the

necessary amount in rent account which will increase the expenditure on rent and so

profits will be reduced.

(iil) Profit will increase or losses will decrease if a nominal account is wrongly

credited. With the rectification of this error, the profits will decrease and losses will

increase. For example, investments were sold and the amount was credited to sales

account. This error will increase profits (or reduce losses) when the same error is

rectified the amount shall be transferred from sales account to investments account

due to which sales will be reduced which will result in decrease in profits (or increase

in losses).

(iv) Profit will decrease or losses will increase if an account is omitted from posting in

the credit side of a nominal or goods account. When the same will be rectified it will

increase the profit or reduce the losses.

For example, commission received is omitted to be posted to the credit of

commission account. This error will decrease profits ( or increase losses) as an

income is not credited to profit and loss account. When the error will be rectified, it

will have reverse effect on profit and loss as an additional income will be credited to

profit and loss account so the profit will increase ( or the losses will decrease).

If due to any error the profit or losses are effected, it will have its effect on capital

account also because profits are credited and losses are debited in the capital

account and so the capital shall also increase or decrease. As capital is shown on the

liabilities side of balance sheet so any error in nominal account will effect balance

sheet as well. So we can say that an error in nominal account or goods account

effects profit and loss account as well as balance sheet.

2. Errors effecting balance sheet only

If an error is committed in a real or personal account, it will effect assets, liabilities,

debtors or creditors of the firm and as a result it will have its impact on balance sheet

alone. because these items are shown in balance sheet only and balance sheet is

prepared after the profit and loss account has been prepared. So if there is any error

in cash account, bank account, asset or liability account it will effect only balance

sheet.

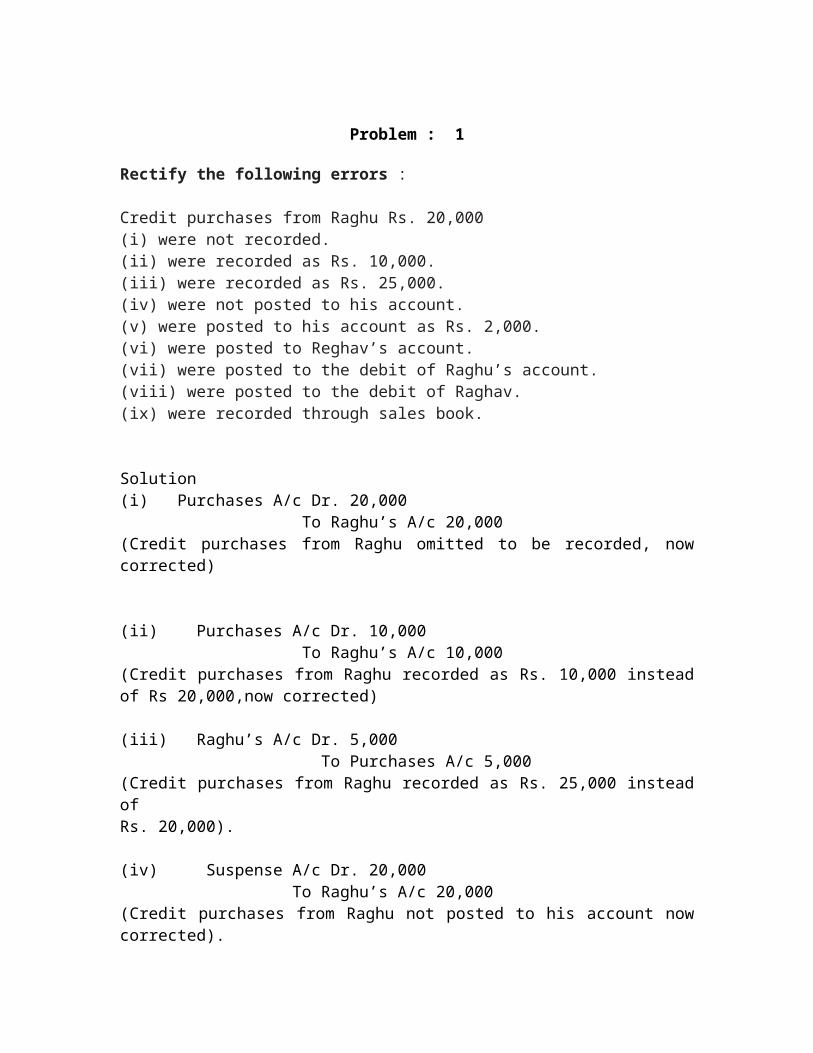

Problem : 1

Rectify the following errors :

Credit purchases from Raghu Rs. 20,000(i) were not recorded.(ii) were recorded as Rs. 10,000.(iii) were recorded as Rs. 25,000.(iv) were not posted to his account.(v) were posted to his account as Rs. 2,000.(vi) were posted to Reghav’s account.(vii) were posted to the debit of Raghu’s account.(viii) were posted to the debit of Raghav.(ix) were recorded through sales book.

Solution(i) Purchases A/c Dr. 20,000 To Raghu’s A/c 20,000(Credit purchases from Raghu omitted to be recorded, now corrected)

(ii) Purchases A/c Dr. 10,000 To Raghu’s A/c 10,000(Credit purchases from Raghu recorded as Rs. 10,000 instead of Rs 20,000,now corrected)

(iii) Raghu’s A/c Dr. 5,000 To Purchases A/c 5,000(Credit purchases from Raghu recorded as Rs. 25,000 instead ofRs. 20,000).

(iv) Suspense A/c Dr. 20,000 To Raghu’s A/c 20,000(Credit purchases from Raghu not posted to his account now corrected).

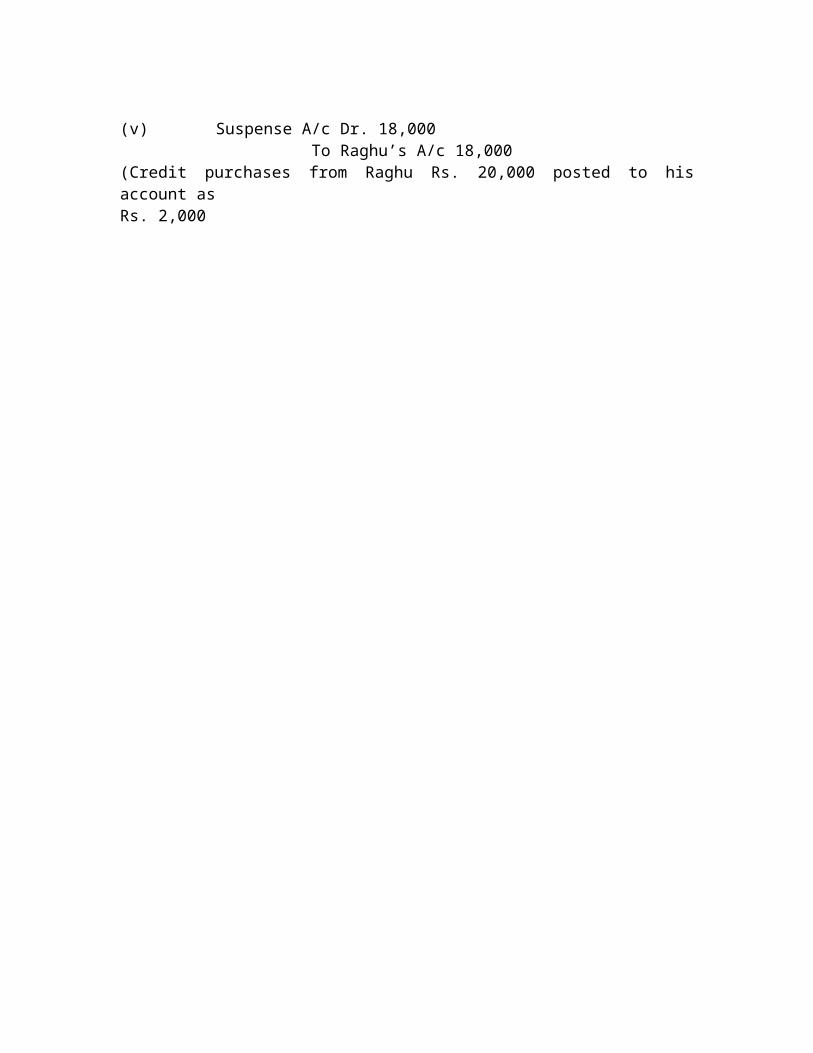

(v) Suspense A/c Dr. 18,000 To Raghu’s A/c 18,000(Credit purchases from Raghu Rs. 20,000 posted to his account asRs. 2,000

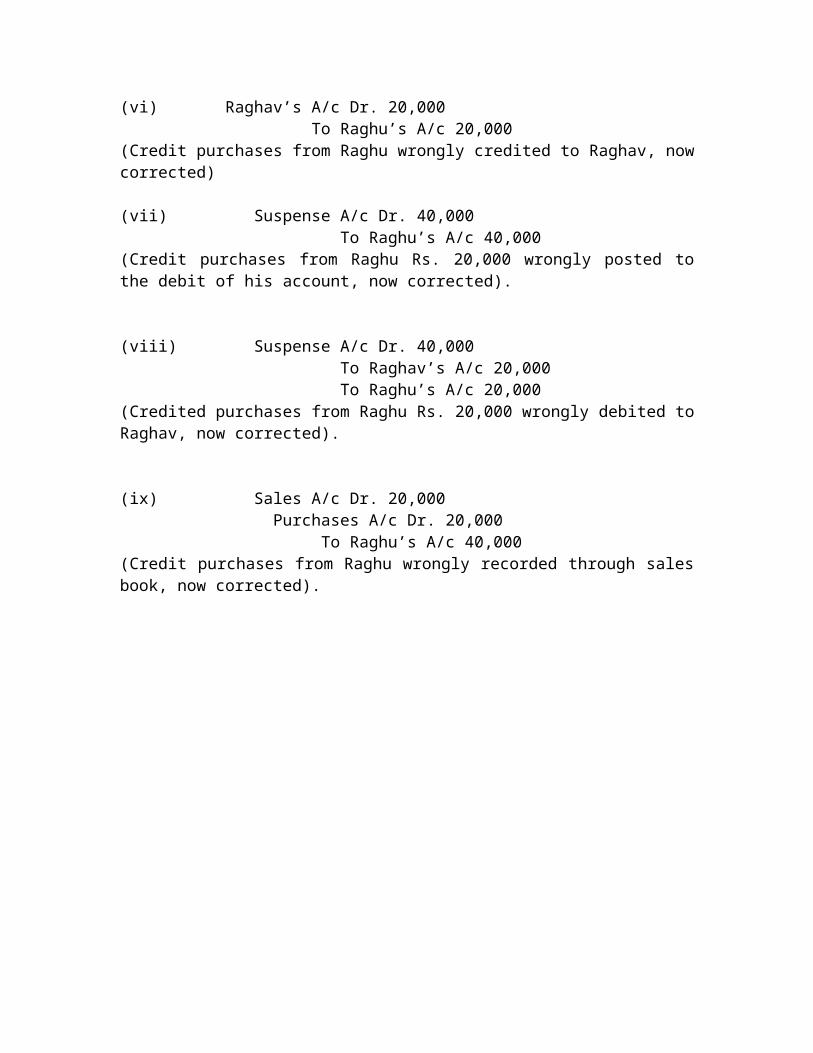

(vi) Raghav’s A/c Dr. 20,000 To Raghu’s A/c 20,000(Credit purchases from Raghu wrongly credited to Raghav, now corrected)

(vii) Suspense A/c Dr. 40,000 To Raghu’s A/c 40,000(Credit purchases from Raghu Rs. 20,000 wrongly posted to the debit of his account, now corrected).

(viii) Suspense A/c Dr. 40,000 To Raghav’s A/c 20,000 To Raghu’s A/c 20,000(Credited purchases from Raghu Rs. 20,000 wrongly debited to Raghav, now corrected).

(ix) Sales A/c Dr. 20,000 Purchases A/c Dr. 20,000 To Raghu’s A/c 40,000(Credit purchases from Raghu wrongly recorded through sales book, now corrected).

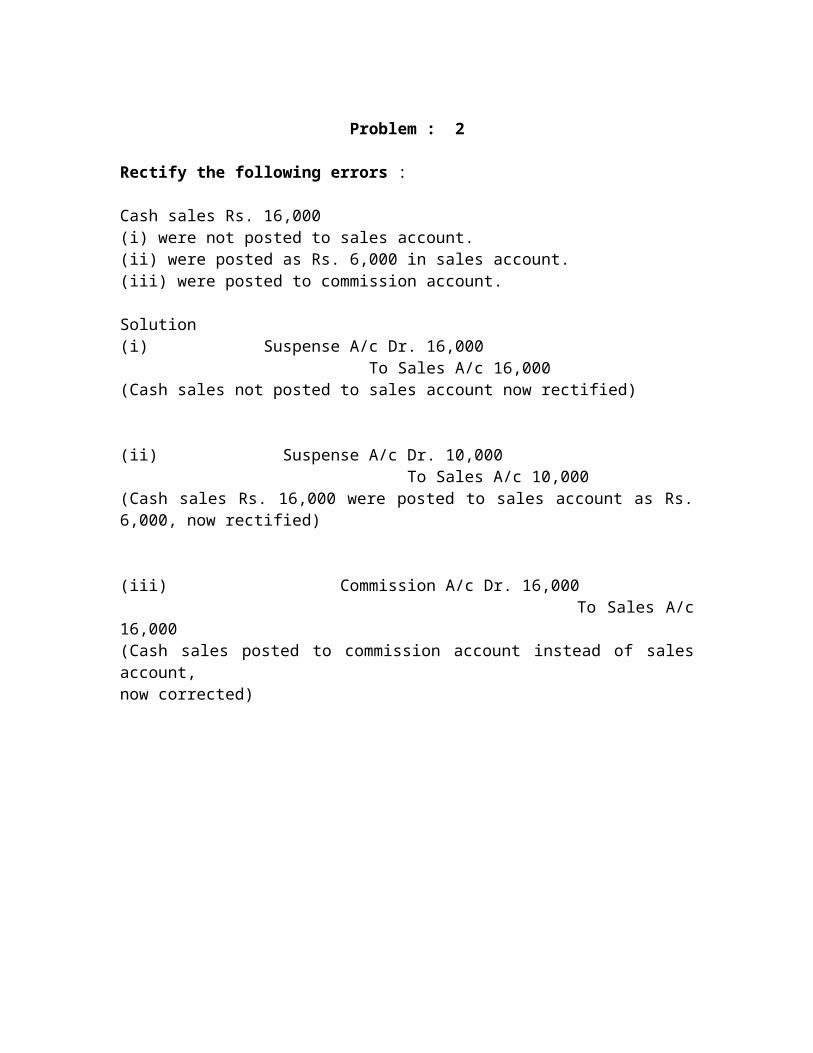

Problem : 2

Rectify the following errors :

Cash sales Rs. 16,000(i) were not posted to sales account.(ii) were posted as Rs. 6,000 in sales account.(iii) were posted to commission account.

Solution(i) Suspense A/c Dr. 16,000 To Sales A/c 16,000(Cash sales not posted to sales account now rectified)

(ii) Suspense A/c Dr. 10,000 To Sales A/c 10,000(Cash sales Rs. 16,000 were posted to sales account as Rs. 6,000, now rectified)

(iii) Commission A/c Dr. 16,000 To Sales A/c 16,000(Cash sales posted to commission account instead of sales account,now corrected)

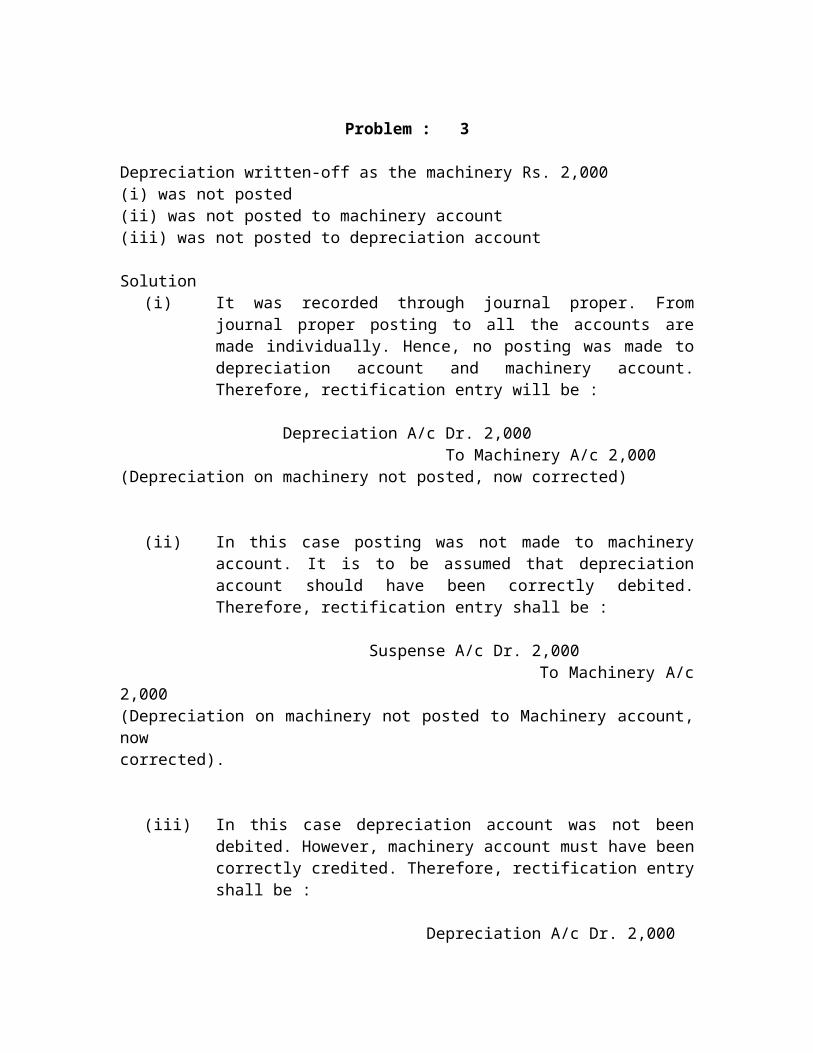

Problem : 3

Depreciation written-off as the machinery Rs. 2,000(i) was not posted(ii) was not posted to machinery account(iii) was not posted to depreciation account

Solution(i) It was recorded through journal proper. From journal

proper posting to all the accounts are made individually. Hence, no posting was made to depreciation account and machinery account. Therefore, rectification entry will be :

Depreciation A/c Dr. 2,000 To Machinery A/c 2,000(Depreciation on machinery not posted, now corrected)

(ii) In this case posting was not made to machinery account. It is to be assumed that depreciation account should have been correctly debited. Therefore, rectification entry shall be :

Suspense A/c Dr. 2,000 To Machinery A/c 2,000(Depreciation on machinery not posted to Machinery account, nowcorrected).

(iii) In this case depreciation account was not been debited. However, machinery account must have been correctly credited. Therefore, rectification entry shall be :

Depreciation A/c Dr. 2,000 To Suspense A/c 2,000(Depreciation on machinery not posted to Depreciation account, nowcorrected).

Problem : 4

Trial balance of Anurag did not agree. It showed an excess credit Rs. 10,000. Anurag put the difference to suspense account. He located the following errors :(i) Sales return book over cast by Rs. 1,000.(ii) Purchases book was undercast by Rs. 600.(iii) In the sales book total of page no. 4 was carried forward to page 5 as Rs. 1,000 instead of Rs. 1,200 and total of page 8 was carried forward to page 9 as Rs. 5,600 instead of Rs. 5,000.(iv) Goods returned to Ram Rs. 1,000 were recorded through sales book.(v) Credit purchases from M & Co. Rs. 8,000 were recorded through sales book.(vi) Credit purchases from S & Co. Rs. 5,000 were recorded through sales book. However, S & Co. were correctly credited.(vii) Salary paid Rs. 2,000 was debited to employee’s personal account.

Solution(i) Suspense A/c Dr. 1,000 To Sales Return A/c 1,000(Sales returns book overcast by Rs. 1,000, now corrected).

(ii) Purchases A/c Dr. 600 To Suspense A/c 600(Purchases book undercast by Rs. 600, now corrected)

(iii) Sales A/c Dr. 400 To Suspense A/c 400(Error in carry forward of sales book, now corrected).

Note : Errors in carry forward the total of one page to another duringa period finally affects the total of that book resulting in error of under/overcastting.

In this case, carry forward from page 4 to 5 resulted in undercasting of Rs. 200 and carry forward from page 8 to page 9 resulted in overcasting of Rs.600.Overall overcastting being Rs. 600–200 =Rs. 400.

(iv) Sales A/c Dr. 1,000 To Return Outwards A/c 1,000(Return Outwards wrongly recorded through sales book, now rectified).

(v) Purchases A/c Dr. 8,000 Sales A/c Dr. 8,000 To M & Co.’s A/c 16,000(Credit purchases wrongly recorded through sales book, now rectified).

(vi) Purchases A/c Dr. 5,000 Sales A/c Dr. 5,000 To Suspense A/c 10,000(Credit purchases wrongly recorded through sales book, however suppliers account correctly credited, now rectified).

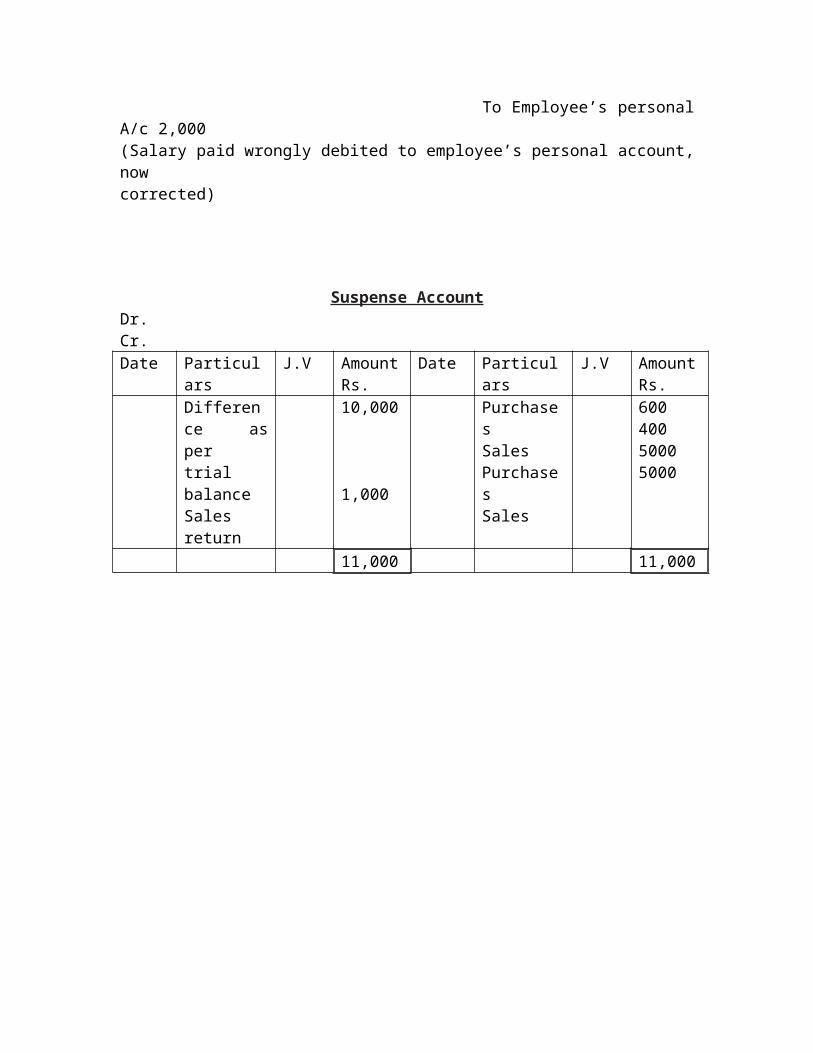

(vii) Salary A/c Dr. 2,000 To Employee’s personal A/c 2,000(Salary paid wrongly debited to employee’s personal account, nowcorrected)

Suspense AccountDr. Cr.Date Particular

sJ.V Amoun

tRs.

Date Particulars

J.V AmountRs.

Difference as per trial balanceSales return

10,000

1,000

PurchasesSalesPurchasesSales

60040050005000

11,000 11,000

Problem : 5

Trial balance of Rahul did not agree. Rahul put the difference to suspense account. Subsequently, he located the following errors :(i) Wages paid for installation of Machinery Rs. 600 was posted to wages account.(ii) Repairs to Machinery Rs. 400 debited to Machinery account.(iii) Repairs paid for the overhauling of second hand machinery purchased Rs. 1,000 was debited to Repairs account.(iv) Own business material Rs. 8,000 and wages Rs. 2,000 were used for construction of building. No adjustment was made in the books.(v) Furniture purchased for Rs. 5,000 was posted to purchase account as Rs. 500.(vi) Old machinery sold to Karim at its book value of Rs. 2,000 was recorded through sales book.(vii) Total of sales returns book Rs. 3,000 was not posted to the ledger.

Rectify the above errors and prepare suspense account to ascertain the original difference in trial balance.

Solution

(i) Machinery A/c Dr. 600 To Wages A/c 600(Wages paid for installation of machinery wrongly debited to wages account, now rectified)

(ii) Repairs A/c Dr. 400 To Machinery A/c 400(Repairs paid wrongly debited to machinery account now rectified)

(iii) Machinery A/c Dr. 1,000 To Repairs A/c 1,000(Repairs for overhauling of second hand machinery purchased, wronglydebited to repairs account, now rectified).

(iv) Building A/c Dr. 10,000 To Purchases A/c 8,000 To Wages A/c 2,000(Material and wages used for construction of Building, not debited tobuilding account).

(v) Furniture A/c Dr. 5,000 To Purchases A/c 500

To Suspense A/c 4,500(Furniture purchased for Rs. 5,000 wrongly debited to purchases account as Rs. 500, now rectified).

(vi) Sales A/c Dr. 2,000 To Machinery 2,000(Sale of machinery wrongly recorded in sales book, now rectified).

(vii) Sales Return A/c Dr. 3,000 To Suspense A/c 3,000(Total of sales returns book not posted to ledger, now rectified).

Suspense AccountDr CrDate Particular

sJ.V Amoun

tRs.

Date Particulars

J.V AmountRs.

Difference as per trial balance

7,500 FurnitureSales return

4,5003.000

7,500 7,500

Hence, original difference in Trial Balance was Rs. 7,500 excess credited.

Problem : 6

Trial balance of Anant Ram did not agree. It showed an excess credit of Rs. 16,000. He put the difference to suspense account. Subsequently the following errors were located:(i) Cash received from Mohit Rs. 4,000 was posted to Mahesh as Rs. 1,000.(ii) Cheque for Rs. 5,800 received from Arnav in full settlement of his account of Rs. 6,000, was dishonoured. No entry was passed in the books on dishonour of thecheque.(iii) Rs. 800 received from Khanna, whose account had previously been written off as bad, was credited to his account.(iv) Credit sales to Manav for Rs. 5,000 was recorded through the purchases book as Rs. 2,000.(v) Purchases book undercast by Rs. 1,000.(vi) Repairs on machinery Rs. 1,600 wrongly debited to Machinery account as Rs. 1,000.(vii) Goods returned by Nathu Rs. 3,000 were taken into stock. No entry was recorded in the books.

Solution

(i) Mahesh’s A/c Dr. 1,000 Suspense A/c Dr. 3,000 To Mohit’s A/c 4,000(Cash received from Mohit Rs. 4,000 wrongly posted to Mahesh asRs.1,000, now rectified)

(ii) Arnav’s A/c Dr. 6,000 To Bank A/c 5,800 To Discount Allowed A/c 200(Cheque received from Arnav for Rs. 5,800 in full settlement of his account of Rs. 6,000, dishonoured but no entry made in books, now rectified)

(iii) Khanna’s A/c Dr. 800 To Bad debts recovered A/c 800(Bad debts recovered wrongly credited to Khanna’s account, now rectified)

(iv) Manav’s A/c Dr. 7,000 To Purchases A/c 2,000 To Sales A/c 5,000(Credit sales to Manav Rs. 5,000 wrongly recorded through purchasesbook as Rs. 2,000, now rectified)(v) Purchases A/c Dr. 1,000

To Suspense A/c 1,000(Purchases book undercast by Rs. 1,000)

(vi) Repairs A/c Dr. 1,600 To Machinery A/c 1,000 To Suspense A/c 600(Repairs on machinery Rs. 1,600 wrongly debited to machinery account as Rs. 1,000, now rectified)

(vii) Sales Return A/c Dr. 3,000 To Nathu’s A/c 3,000(Sales return from Nathu not recorded)

Suspense Account

Date Particulars J.V Amount Rs.

Date Particulars J.V Amount Rs.

Difference as per trial balanceMohit

16,000

3,000

PurchasesRepairsBalance c/d

1,000 60017,400

19,000 19,000

Note : Even after rectification of errors suspense account is showing a debit balance of Rs. 17,400. This is due to non-detection of errors affecting trial balance. Balance of suspense account will be carried forward to the next year and will be eliminated as and when all the remaining errors affecting trial balance are located.

Rectification of error in Tally

Rectification of error in Tally is very simple and prompt effective on your final

accounts of company. You can easily rectify your voucher entry with only two

easy steps

1st step

reaching on voucher entry alteration mode :-

Display >> Daybook >> select the date >> Select The Voucher

Entry

2 nd step

Correct the mistake of voucher entry in it :-

Mistake may be wrong journal entry or mistake may be wrong choosing of voucher . Or mistake of feature or configuration setting .All these are corrected here and accept this .