Embed Size (px)

Citation preview

CFA Institute

Reconsidering the Affirmative Obligation of Market MakersAuthor(s): Hans R. StollSource: Financial Analysts Journal, Vol. 54, No. 5 (Sep. - Oct., 1998), pp. 72-82Published by: CFA InstituteStable URL: http://www.jstor.org/stable/4480111 .

Accessed: 14/06/2014 19:03

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

CFA Institute is collaborating with JSTOR to digitize, preserve and extend access to Financial AnalystsJournal.

http://www.jstor.org

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation

of Market Makers

Hans R. Stoll

Market makers on exchanges regulated by the U.S. SEC are subject to an affirmative obligation to make 'fair and orderly markets," and in return, they receive certain benefits. Financial economists have long been skeptical, however, of the efficacy of a legal requirement to "do good" and havefound little evidence that the requirement contributes to the quality of markets. Moreover, competition across markets reduces the willingness of market makers to stabilize markets, and electronic trading reduces the importance of market makers.

"~~~~~~~~~~~~~~~~ ilLa di.j

T_ he affirmative obligation to "maintain fair and orderly markets" dates to the 1950s and 1960s and reflects the interventionist regulatory policy common at that time. In

recent years, competition and market transparency have become important guiding principles of reg- ulation; yet, the affirmative obligation remains. This article traces the evolution of the affirmative obligation from a negative obligation, presents an analysis of the rationales for an affirmative obliga- tion, and discusses the efficacy of an affirmative obligation in today's highly automated and com- petitive markets.

From Negative to Affirmative The NYSE, founded in 1792, was established as a call auction market where members would trade each security at particular times. In 1870, after a merger with certain other exchanges, the NYSE adopted a system of continuous auction trading, where trading in each security took place at a spe- cific location continuously throughout the day. Members of the exchange acted as brokers for cus- tomers or traded for their own accounts as floor traders. The NYSE specialist, who emerged in the early 1900s, flourished particularly after World War I, when the increase in volume motivated busy brokers to leave customer limit orders with other brokers specializing in particular securities. These specialists, acting as brokers' brokers, executed the

orders left with them against incoming market orders. Over time, specialists also began to trade for their own accounts to satisfy incoming market orders when no appropriate customer limit orders existed.

When the Securities Exchange Act of 1934 was being enacted, the evolution of specialists into dealers for their own accounts was viewed with suspicion-a suspicion fueled by a series of investigations culminating with the Pecora hear- ings of 1934 and by reports of pools in which specialists participated.' Critics pointed to the inherent conflict of interest in the specialist func- tion as it had by then evolved: Specialists acted as dealers for their own accounts and as brokers for customer limit orders. In Section 11(e) of the Securities Exchange Act, Congress directed the SEC to investigate "... the feasibility and advis- ability of the complete segregation of the functions of dealer and broker...."

The SEC investigation concluded that the func- tions of broker and dealer need not be segregated. Instead, it specified a statutory standard-the Saperstein Interpretation-under which specialists were permitted to trade for their own accounts. The standard, embodied in NYSE Rule 204, states that no specialist should undertake transactions unless they are ". . . reasonably necessary to permit such specialist to maintain a fair and orderly market...."

By the 1960s, a dramatic change had occurred in the role of the specialist (Oesterle, Winslow, and Anderson 1992). The Saperstein Interpretation, which imposed a negative duty on specialists-a duty not to trade for their own accounts unless necessary-was supplemented by an affirmative obligation to improve markets. SEC Rule llb-1, promulgated in 1965, mandates that exchange rules

Hans R. Stoll is the Anne Marie and Thomas B. Walker Professor of Finance and director of the Financial Mar- kets Research Center at the Owen Graduate School of Management, Vanderbilt University.

72 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation of Market Makers

include "requirements, as a condition of a special- ist's registration, that a specialist engage in a course of dealings for his own account to assist in the maintenance, so far as practicable, of a fair and orderly market. . . ." The rule, in other words, requires that specialists trade for their own accounts. This change in the perceived role of the specialist is reflected in a comparison of congres- sional testimony by Richard Whitney, NYSE pres- ident in 1933, and Keith Funston, NYSE president in 1961. In response to the question, "What is a specialist?" Whitney replied, "one who executes orders for other brokers," but Funston replied, "The essence of being a specialist is dealing for his own account."2

The change in the role of the specialist, espe- cially in light of the suspicion with which the spe- cialist was viewed, was furthered by the Special Study of Securities Markets, which was authorized, in part, to examine the market break of May 28, 1962, and was completed under the direction of Milton Cohen (U.S. Securities and Exchange Com- mission 1963). The authors of the Special Study doubted that the specialist had turned altruistic and could thus be relied on to assure that markets were orderly. They believed that more-specific legal requirements would produce desirable behavior. The Special Study recommended estab- lishment of an affirmative obligation for specialists and a series of other requirements, which included specialist capital, specific rules on permitted trades by specialists, requirements for specialists to main- tain continuity with depth, reports of specialists' trades, surveillance of specialists, and increased SEC authority to discipline specialists.3 Most of these recommendations were implemented either as part of SEC Rule llb-1 or as part of exchange rules.

The NYSE, in turn, implemented certain tests of specialist performance to evaluate the degree to which specialists met their affirmative obligation. These tests included the degree to which special- ists' trades were made on stabilizing ticks (buying on a minus tick and selling on a plus tick) and the specialist's participation rate, price continuity, and willingness to carry inventory overnight.

Stigler (1964) castigated the Special Study for concluding that more regulation was needed. He noted that the study provided no theory or evi- dence why additional regulations would make markets better than they were or better than some alternative proposal. And, on the ground that news sometimes warrants rapid changes in prices, he questioned the implication that continuous mar- kets and stable prices are desirable.

The SEC's Institutional Investor Study (IIS)

Report, completed in 1971 (see U.S. Securities and Exchange Commission 1971), heeded Stigler's crit- icisms. The report, written by a staff of economists, developed an analytical framework for assessing regulation and provided empirical evidence for its conclusions. It favored the elimination of fixed commissions and greater competition in the securi- ties markets. Chapter XII of the IIS Report found that market makers tended to act in a stabilizing manner even in the case of market makers in third markets or regional markets, who are under no affirmative obligation. This result is not surprising because stabilizing trading-buying on a minus tick and selling on a plus tick-is also profitable. The study examined NYSE specialists in detail and found that profits from market making were not related to the liquidity provided by a specialist unit. The wide variations in liquidity provided by different spe- cialists suggested that individual specialists have the leeway to act capriciously in accord with their own risk preferences. In a competitive market, such individualistic behavior would not be possible.

The IIS Report's recommendations for greater competition in securities markets were reflected in the Securities Acts Amendments of 1975. These amendments eliminated fixed commissions and unnecessary anticompetitive exchange rules. They also called for the development of a national mar- ket system within which competition among bro- kers and dealers could take place. Despite the increased reliance on competition rather than rules as a regulator, no corresponding change occurred in the affirmative obligation approach to regulating market makers.

For many years, the affirmative obligation was applied only to exchange specialists. The OTC mar- ket was not subject to Rule 1 lb-1 because it was not a national securities exchange under the 1934 act. Furthermore, the OTC market relied on competi- tion among dealers in a stock rather than on an affirmative obligation to assure a fair and orderly market. Following the development of the Nasdaq Stock Market, however, and particularly in reaction to the crash of October 1987, Nasdaq imposed var- ious obligations on its market makers, including the obligation to quote continuously, to limit the size of the spread relative to the average spread of all dealers, and to quote a minimum depth.

The Chicago Board Options Exchange (CBOE), established in 1973, designed its trading system to separate the dealer and broker functions. The limit- order book is maintained by an order book official (OBO), and the dealer function is carried out by competing market makers in the crowd. In this framework, neither a negative nor an affirmative obligation seemed necessary or desirable. The CBOE did establish an affirmative obligation for its

September/October 1998 73

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

competing market makers, although it was loosely written and gave market makers wide latitude. In 1987, the CBOE created the Designated Primary Market Maker (DPM), who performed the function of OBO and market maker in certain classes of options. DPMs resemble specialists in stocks because they act as both dealers and as brokers, but the genesis of the DPM was different. Although an affirmative obligation was implicit in the DPM's dealer activities, the DPM was created not to stabilize prices but to develop active and well- functioning markets in those options that would face competition from other exchanges as the SEC allowed multiple listing of options. In return for building up a market, the DPM received support from the exchange for acting as OBO and received the right to execute a certain proportion of the trades.

Stimulated by regulatory concerns and by the IIS Report, financial economists began in earnest to study the behavior of dealers and to provide the the- ory that Stigler found wanting in the Special Study. Stoll (1978a) and Ho and Stoll (1981) developed a model of dealers and the bid-ask spread based pri- marily on inventory considerations. Glosten and Milgrom (1985) and Copeland and Galai (1983) developed models of dealers based on adverse- information considerations and dealers' concerns that they will be "picked off" by informed investors. What have the economic analyses revealed about the affirmative obligation's success in meeting its main goals-to maintain price stability and to achieve low-cost trading and efficient markets?

Price Stability One rationale for an affirmative obligation is the need to stabilize prices and reduce stock-price vol- atility. Particularly when stock prices drop dramat- ically, as in 1987, regulators and exchanges have responded by imposing additional requirements on market makers. This reaction reflects a belief that free competitive markets are too volatile and disor- derly, but little evidence has been found for this view or for the conclusion that an affirmative obli- gation stabilizes prices. Friedman (1953) pointed out long ago, in criticizing governmental attempts to stabilize exchange rates, that private speculators naturally tend to stabilize prices in their search for trading profits.

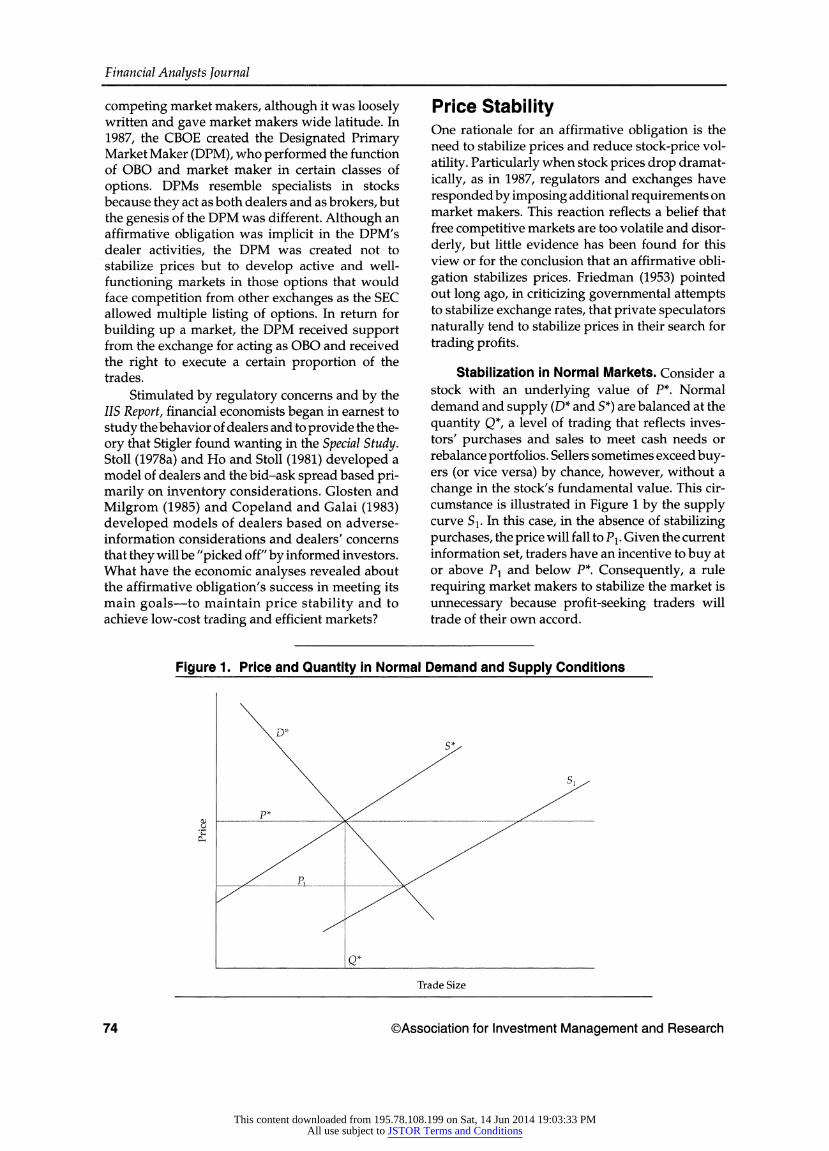

Stabilization in Normal Markets. Consider a stock with an underlying value of P*. Normal demand and supply (D* and S*) are balanced at the quantity Q*, a level of trading that reflects inves- tors' purchases and sales to meet cash needs or rebalance portfolios. Sellers sometimes exceed buy- ers (or vice versa) by chance, however, without a change in the stock's fundamental value. This cir- cumstance is illustrated in Figure 1 by the supply curve S1. In this case, in the absence of stabilizing purchases, the price will fall to P1. Given the current information set, traders have an incentive to buy at or above P1 and below P*. Consequently, a rule requiring market makers to stabilize the market is unnecessary because profit-seeking traders will trade of their own accord.

Figure 1. Price and Quantity in Normal Demand and Supply Conditions

0)~ ~ D

X P*. _ __ _

Trade Size

74 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation of Market Makers

Economic forces, not an affirmative obligation, drive dealers' behavior. Specialists perform well on the tick test, which measures the percentage of times the specialist buys on down ticks and sells on up ticks, but so do market makers without an affir- mative obligation. In an analysis of OTC market makers at a time when they faced little or no affir- mative obligation, Stoll (1976) found that they have the same tendency to buy after price declines and sell after price increases as specialists who are sub- ject to an affirmative obligation. Stabilizing dealer behavior, in other words, is not the result of an affirmative obligation but, rather, a result of the incentive any trader has to buy low (that is below P* in Figure 1) and sell high. Hasbrouck and Sofi- anos (1993) and Madhavan and Smidt (1991, 1993), in sophisticated analyses of specialist behavior, confirmed the importance of economic forces, although they found that the trading behavior of the specialist is a complicated process.

The role of economic forces is also evident in the fact that the bid-ask spreads of stocks are strongly related to the economic characteristics of stocks-volume, stock price, volatility of return, competition-independently of any affirmative obligation. For example, Tinic (1972) and Branch and Freed (1977) showed that economic character- istics explain cross-sectional differences in spreads on the NYSE, which imposes an affirmative obliga- tion, but Benston and Hagerman (1974) and Stoll (1978b) showed that economic characteristics explain differences in spreads on the Nasdaq,

which does not impose an affirmative obligation. The important role of underlying economic forces in the behavior of market makers and other traders implies that elimination of the affirmative obliga- tion would have little effect on the degree of market stabilization or the pattern of bid-ask spreads.

Although dealers with an affirmative obliga- tion and traders with no such obligation have sim- ilar incentives to buy low and sell high, a market structure that relies on one or a few dealers to stabilize prices is not necessarily superior to a struc- ture that gives access to many competing traders. In a free market, those traders most willing to pro- vide liquidity will do so, whereas under the rule of affirmative obligation, the approach is to rely on the willingness of designated dealers to provide liquid- ity. Stoll (1978a) showed that the willingness of a dealer to absorb inventory and the bid price set by the dealer depend on the dealer's degree of risk aversion and wealth. A risk-averse and poorly cap- italized dealer requires a larger return and a lower bid price than a risk-loving and highly capitalized dealer. On the other hand, if the wealth of many traders each taking relatively small positions could be harnessed, the return required to stabilize prices might be quite low and the bid price higher than when a market relies on a single or relatively few dealers. The reason is that the risk associated with absorbing excess supply is spread across more traders.

For illustration of this point, consider Figure 2, where P* again represents the underlying value of

Figure 2. Demand Curve for a Single Market Maker versus Demand Curve for a Group of Traders

,,Bm

Trade Size

September/October 1998 75

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

the stock and S represents the excess supply of the stock. The demand curve DM represents the prices a single market maker with wealth WM would bid to buy shares, and the curve DC represents the prices a group of competing traders with aggregate wealth Wc would bid to buy shares. The equation for the demand curves, based on Stoll (1978a), is

Zi cx2p* Bi = P 2W Q,with i = M,C (1)

where

Bi = the bid price of trader i

Zi = the coefficient of relative risk aver- sion of trader i

G2 = the stock's variance of return

Wi = the wealth of trader i

Q = the transaction size

i = M = case for a single market maker

i = C = case for a group of competing traders

If the aggregate wealth of the competing traders, WC, exceeds that of a single dealer, WM, the demand of competing traders in Figure 2 is more elastic than the demand of a single dealer. The result is that the bid price at which a group of competing traders would buy, Bc, is higher and the depth greater than would be the case for the bid price, BM, and depth of a single market maker.

Wealth committed to market making is impor- tant, but regulators cannot require the use of wealth. Market makers must possess greater mini- mum capital today than in earlier years, which would increase the elasticity of DM in Figure 2 if the wealth were committed. But a dealer may possess large amounts of capital and be unwilling to use it. For example, the IIS Report (Ch. 12) and Smidt (1971) found that specialists' willingness to provide liquidity in similar stocks varies considerably, something that can be interpreted as different risk preferences in the Stoll (1978a) model. For example, in Equation 1, a higher value of z lowers the bid price at any depth.

Two recent studies found that the quality of market making differs among specialists, which is consistent with this analysis and with the findings of Smidt. Corwin (1997) showed that transitory volatility in stock prices and the use of trading halts differ significantly, after differences in stock char- acteristics were controlled for, among specialist units. Cao, Choe, and Hathaway (1997) found that specialist units differ in the efficiency with which they execute transactions, which suggests that reg- ulation does not necessarily bring the most able dealers to the fore.

If the buying power of many value traders can quickly be harnessed, the market will be more sta- ble than if relatively few market makers are relied on to supply liquidity. Because the same investors are not likely to always be the most willing suppli- ers of liquidity, a market that makes it easy for any buyer to provide liquidity is most desirable. In the past, news of temporary imbalances was slow to be disseminated and the ability to harness groups of traders was limited, but today, with high-speed communications technology, these problems are not significant. Most markets now allow investors to compete directly with the market maker by quickly placing (or canceling) limit orders.

Stabilization in Periods of Stress. Periods of stress are typically periods in which the funda- mental values of securities drop dramatically. The objective of a fair and orderly market is not to impede a warranted change in fundamental values but to bring the change about quickly and in an orderly manner. Regulatory requirements often run counter to this objective. For example, the NYSE evaluates specialists on the degree of conti- nuity in prices. Although price continuity is easy to adhere to in most instances, it should be ignored when new information warrants a change in stock price, as Stigler first noted. For a specialist to main- tain an existing price when new information war- rants a lower price is not only unprofitable for the specialist but undesirable for society. In efficient markets, prices quickly adjust to the new equilib- rium, and the arbiter of that equilibrium is the entire market. The idea that the specialist can-or should-slow down a change that the market views as desirable ascribes too much foresight to the specialist and too little to the market. Fortu- nately, specialists are not interested in losing money, so sudden price changes are allowed to occur.

Research suggests that the affirmative obliga- tion plays little role in dampening price change. Roll (1988, 1989) analyzed stock-price behavior in 23 countries on October 19, 1987, a period of stress in stock markets around the world. After account- ing for each country's beta coefficient vis-a-vis the world market portfolio, he found that the degree of price decline in various countries was not related to differences in regulations, such as whether a market designated an official specialist. This result implies that an affirmative obligation has no dis- cernible effect on price volatility in periods of stress. Stock prices reflect fundamental market forces that cannot easily be altered by market mak- ers with or without an affirmative obligation. Christie and Schultz (1997) analyzed the behavior

76 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation of Market Makers

of Nasdaq market makers in the less stressful mar- ket break of November 15, 1991, when stock prices fell 4 percent. They concluded that the regulatory obligations imposed after the crash of 1987 had a beneficial effect, in that market makers did not widen spreads, abandon the inside spread, or fail to trade. Their results are also consistent, however, with a widening of spreads between 1987 and 1991. That is, spreads may have already been so wide that the stress associated with the 4 percent break of 1991 was insufficient to cause a further widening.

Periods of stress in individual stocks are often accompanied by trading halts and discontinuous price changes. Trading halts may be initiated by the company (in the case of news) or by the specialist, with approval of a floor governor (in the case of order imbalances). Trading halts occur when the specialists recognize the need for discontinuous price changes.4 A trading halt is an efficient mech- anism that allows time for the specialists to find the other side and allows fair treatment of limit orders on the book. The behavior of specialists is not uni- form, however. When Corwin analyzed the behav- ior of specialist units around trading halts, he found significant differences among units as to the prob- ability that they would call a halt because of trading imbalances and differences in the duration of those halts.5 He did not find differences for trading halts arising from news announcements.

Given the historical evolution of the NYSE, it is appropriate that specialists have a say in when a trading halt is called. The variations in the frequency and duration of trading halts among specialist units (after stock characteristics have been controlled for) implies that specialists' will- ingness to provide liquidity depends on character- istics of the specialist and suggests that liquidity and price stability could be improved in certain stocks if the most willing traders could be attracted to those stocks.

The opening after a trading halt and the daily opening are clearly periods of market volatility, if not stress. Market makers tend to have a greater influence on prices in these periods than at other times, so information on how the market performs at these times is of interest. Lee, Ready, and Sequin (1994) concluded that the reopening after. a halt is inefficient. Bhattacharya and Spiegel (1997) found a difference in reopenings after suspensions resulting from news and those resulting from order imbalances. Stoll and Whaley (1990a) inves- tigated stock-price behavior around openings and closings on the NYSE. They concluded that stock prices are more likely to overshoot at the opening than at other times, which is an indication that suppliers of liquidiity-mnarket makers and limit-

order traders-are exacting a premium. A more competitive and more transparent opening than at present would probably lead to even better opening prices and less volatility.

After the opening and in the absence of trading halts, trading is supposed to be continuous and price changes between trades are supposed to be small. This continuity requirement also seems to introduce some inefficiencies, as Stigler noted and Miller (1991, Ch. 11) reiterated. Miller pointed out that the requirement for price continuity hampers specialists in adjusting their quotes to reflect changes in stock index futures prices. The resulting price divergence is a source of the much maligned, but economically beneficial, practice of index arbi- trage. Stoll and Whaley (199Gb) showed that returns on stock index futures lead returns on the stock index, which implies that stock returns are slow to adjust to new information and is consistent with Miller's argument. Lags in the adjustment of stock prices relative to index futures prices were particularly evident during the October 1987 mar- ket break, as noted by the report of the Presidential Task Force on Market Mechanisms (1988). Huang and Stoll (1994) showed that the five-minute return on actively traded stocks can be predicted on the basis of the previous five-minute stock index futures return, which also implies that stock prices are slow to adjust.6

Taken together, the evidence on the behavior of stock prices suggests that exchange market mak- ers have little ability to dampen large price changes although the obligation to maintain price continu- ity may slow price adjustments. At the same time, volatility appears to be greatest around exchange openings and after trading halts, when market makers have the most influence. Exchange market makers also display substantial variations in their willingness and/or ability to provide liquidity. In summary, the effect of an affirmative obligation to stabilize prices is decidedly mixed.

Low-Cost Trading and Market Efficiency A second rationale for an affirmative obligation is that such an obligation is necessary to achieve low- cost trading and to keep markets functioning efficiently. Under SEC rules, market makers must continuously quote two-sided markets. Because such an obligation can be shirked by quoting a wide spread, markets monitor spreads and sometimes impose a maximum spread and/or a minimum depth. Nasdaq, apparently attempting to distin- guish itself as the most demanding market, has set both a minimum depth and a mnaximnum spread.

September/October 1998 77

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

The minimum depth for the more active stocks, instituted after the 1987 crash, is 1,000 shares. The maximum spread was set at 125 percent of the average spread of the three market makers with the lowest spreads. Because the maximum spread is defined in relation to the average spread of all dealers, the maximum spread rule may have had the perverse effect of contributing to the widening of all dealer spreads. That is, if all dealers have wide spreads, there is less danger that any one of then is violating the maximum spread rule. That spreads are indeed excessive in Nasdaq is documented in, for example, Christie and Schultz (1994) and Huang and Stoll (1996).7

The NYSE does not specify a maximum spread, although spreads are monitored together with other measures of specialist performance, nor does it require a minimum depth, although it does require that specialists have sufficient capital to trade 15,000 shares of their specialty stocks. The CBOE establishes limits on the spreads that its competing market makers may quote, but the depth requirement is simply that market makers make markets in "a reasonable number of con- tracts."

The objective that there always be a reasonable bid and offer at which the public can trade is comr mendable, but the idea that it is to be achieved by rule is, at best, curious. Either the rule is effective and imposes costs on market makers, in which case they will seek to avoid the rule or leave market making, or the rule is ineffective and imposes no costs, in which case the rule is needless.

Suppose a dealer's bid quotes for alternative depths are given by demand schedule D in Figure 3. At a depth of 1,000 shares, then, a dealer might set a bid quote of $49.75 for a security that has a funda- mental value of $50. A requirement to bid $49.875 at a depth of 1,000 would place the dealer at Point A in the figure, which is off the demand curve because the bid price does not cover all costs. One response of the market maker would be to shirk the require- ment. In the context of Figure 3, the market maker could avoid the requirement either by reducing the bid (back to $49.75) or by decreasing the depth (to 500 shares). In practice, shirking of the affirmative obligation is possible because the obligation is not usually clearly defined, because monitoring is costly and difficult, and because a profit-seeking dealer's behavior is usually consistent with the affir- mative obligation. Consequently, an exchange will have difficulty identifying behavior that is contrary to the affirmative obligation.

A second market-maker response, one that is possible if the market maker is granted market power, is to cross-subsidize the losses on some trades that have resulted from a costly affirmative obligation with excess profits on other trades. Cohen et al (1977) argued that stabilization by the specialist has social benefits that justify granting a quiasi-monopoly position and special privileges to the specialist. Glosten (1989) developed an adverse-information model in which a monopolist specialist helps avoid market failure. Regulators have accepted grants of special privilege to market

Figure 3. Dealer's Bid Quotes for Alternative Depths

$50 Fundamental Value

wwwww ww wwww ww w . . ....... . .. . ... ... . .. . . .. . .

$49.875 A.-

500 1,000 Shares Shares

Trade Size

78 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation of Market Makers

makers in return for the affirmative obligation. Unfortunately, the private benefits arising from the market maker's special position seem to outweigh the costs of the affirmative obligation.8 Furthermore, those market makers who do not shirk their affirmative obligation are finding it difficult to earn excess profits on some trades to subsidize losses on others as competition from proprietary traders, from market makers in competing markets, and from other investors in their own markets increases.

A third market-maker response, if the affirma- tive obligation requirement is binding and if com- petition limits the market maker's ability to earn offsetting profits, is for market makers to leave market making and become proprietary traders. Given speedy electronic access to many markets, a proprietary trader can act as a market maker with- out the obligations of a market maker. To regula- tors, this outcome would threaten the established order in which market makers are held responsible for orderly markets. Others, however, have two reasons to embrace such an outcome. First, it is inevitable because of competition. Second, it is effi- cient because liquidity is provided by those traders that have an economic incentive to provide it. The resulting bid-ask spread is likely to be tighter if many traders have access to markets than if a few designated dealers are required to post quotes.

Competition Black (1971a, 1971b, 1995) predicted the demise of market makers because public traders can provide liquidity at lower cost. He wrote,

Dealers have no role in this equilibrium. Trad- ers do not use market orders. If they did use market orders, limit orders would provide the market's depth. Exchanges would not need dealers to provide depth. (1995, p. 28)

What Black had in mind, I believe, is that innova- tions in the types of orders that traders place allow all traders to act like dealers and, thereby, make dealers unnecessary. In a similar vein, Glosten (1994) noted that a computerized limit-order book is the most efficient market structure and will tend to dominate other forms of trading.

Black's world is at hand. Market makers are no longer necessary because public investors-the ultimate purveyors of liquidity-can enter orders directly.9 Under SEC order-handling rules, limit orders will have standing in Nasdaq and can be expected in the future to be a source of greater liquidity for market orders (U.S. Securities and Exchange Commission 1997). Market makers are likely to reduce trading for their own accounts and increase the extent to which they represent limit

orders. When a public limit order and a market- maker quote have the same right and can be placed with the same speed, the distinction between mar- ket makers and public investors is blurry. In this environment, the argument for an affirmative obli- gation applies no more to the dealer than to the public investor who trades like a dealer.

Even without the demise of market makers that Black predicted, competition among market makers and market centers is making it difficult for any market maker to earn excess profits on some trades to subsidize other trades. Modern high-speed communications technology has increased the competition among stock market centers. On the NYSE, 85 percent of the trades are entered via the Designated Order Turnaround system, and the turn of a switch can divert that order flow to another market. The NYSE handles less than 75 percent of the trades in its stocks. The third market and the regionals "cream-skim" the easy trades. To retain the easy trades, the NYSE would have to lower the cost of executing those trades, which would leave no excess revenues to subsidize the hard trades. Similar trends have affected Nasdaq as Instinet has grown dramati- cally and attracted substantial volume. The ineffi- ciencies and high spreads of Nasdaq have caused it to lose market share.

In the four options markets, competition has not reached the level observable in the stock mar- kets.10 Although equity options may be listed on multiple exchanges, most equity options are traded on only one exchange. Judging by past trends in stocks, however, the lack of direct competition in options trading is likely to change in the future, particularly if inefficiencies in an option market attract competitors. Increased competition will put increased pressure on option market makers.

The effect of automation and limit-order competition on the affirmative obligation can be further illustrated by two examples. The first deals with the changes in Nasdaq brought about by the SEC's recently adopted order-handling rules (U.S. Securities and Exchange Commission 1997). Under these rules, dealers must display their customer limit orders and the Nasdaq quote montage must display quotes of electronic communications net- works (ECNs) that compete with Nasdaq. In this new market organization, therefore, limit orders and ECNs compete directly with dealer quotes, which poses several issues. First, Nasdaq, as a market, apparently cannot require a minimum depth at the inside quote because the inside quote could be made by a limit order that offers less than the minimum depth. As a result, one of the objectives of an affirmative obligation-that there

September/October 1998 79

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

be a minimum depth-cannot be met. There is a minimum depth at some price, of course, but that is true without an affirmative obligation. Second, although requiring market makers to display a minimum depth for their quotes is possible, such a requirement (if binding and costly) seems unfair because limit orders directly compete with market makers and have no obligation. Third, ECN quotes may represent market makers (who have an affirmative obligation) or customers (who do not); it is impossible to tell without going into the audit trail. Must an affirmative obligation be imposed on the ECN as a market, or can rules and monitoring procedures be established that limit the affirmative obligation to certain traders within an ECN? Given the questionable benefit of the affirmative obliga- tion, eliminating it would appear to be the simplest solution.

A second example is the recent proposal by Interactive Brokers Inc. (IBI) to send customer orders and proprietary orders to handheld termi- nals on the floors of options exchanges.11 This order flow would make two-sided markets, as does a market maker on the floor, but without a market maker's affirmative obligation. IBI would be similar to an ECN on Nasdaq, and the issues are the same. Should affirmative obligations be imposed on IBI?

Recent regulatory policy and technological change give customers greater standing in the mar- kets and allow customers to compete with market makers if they wish. In this more competitive envi- ronment, affirmative obligation is less important, less effective, and less fair than in the past. It is less important because the affirmative obligation is not effective and thus not the best method to increase liquidity and because customers can fend for them- selves by placing limit orders. It is less effective because dealers cannot afford to act "affirmatively" in a competitive environment. And it is less fair because market makers and customers have nearly the same access to markets.

Conclusion Ironically, the securities markets-those bastions of speculation and free competition-deem it neces- sary to impose an affirmative obligation on their market makers. Rather than encouraging participa- tion of additional speculators to stabilize prices, a la Friedman, the equity exchanges assign specific responsibilities to market makers in return for

specific privileges. It has not always been so. Initially, markets were thought to be gathering places in which traders would meet; none of them would have a special role. Only over time, as some traders evolved from brokers to dealers, did the function of a designated market maker become institutionalized on U.S. equity exchanges. And only over time did a negative obligation that limited dealers' trading to what was necessary turn into an affirmative obligation to improve markets. Domestic bond markets, domestic currency mar- kets, and the stock markets in other countries-all operate without an affirmative obligation and without adverse consequences.

The time has come to reconsider the affirma- tive obligation, certainly as a regulatory obligation. That an affirmative obligation reduces volatility or makes markets more efficient is not evident. The costs to the public of the privileges granted to market makers-such as a quasi-monopoly posi- tion and access to trading information-probably outweigh any benefits. And finally, the cross- subsidization between easy trades and hard trades implicit in the affirmative obligation is increasingly impractical in today's competitive markets.

Rather than imposing obligations, markets would do better to provide incentives for all inves- tors, not solely dealers, to supply liquidity. Improved access to markets for all investors would reduce the need to impose negative or affirmative obligations on market makers. Indeed, as access to markets is equalized by technology, the distinction between market makers and other investors is dis- appearing.

Markets will function well without an affirma- tive obligation. Market makers need no regulatory obligations and should not receive special privi- leges. The existence of market makers should depend on the quality of their market-making ser- vices, not on some privileged position provided in return for an ephemeral affirmative obligation.

This study was supported by the Dean's Fundfor Fac- ulty Research, by the Financial Markets Research Cen- ter, and by a grant from Timber Hill Inc. I gratefully acknowledge the comments of William Christie, Donald Langevoort, and Robert Seijas without ascribing to them the views expressed in this article, which are my own.

80 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Reconsidering the Affirmative Obligation of Market Makers

Notes 1. A fine description of this evolution can be found in U.S.

Securities and Exchange Commission (1963), Ch. VI, pp. 61-67.

2. Quotations from U.S. Securities and Exchange Commission (1963), Ch. VI, p. 64.

3. U.S. Securities and Exchange Commission (1963), Ch. VI, pp. 167-71. See also Robbins (1966), pp. 191-201, for a general discussion of the specialist.

4. According to Corwin, 1,044 trading halts occurred in 1992. 5. See Hopewell and Schwartz (1978) for earlier work on

trading suspensions. 6. Transaction costs, however, eliminate any profits for most

investors. 7. Neither the minimum depth nor the maximum spread

requirement has been directly linked to odd-eighth avoid-

ance or excessive spread. These requirements may have helped induce a less-than-competitive environment, how- ever, as dealers try to protect themselves from the effects of the requirements.

8. See Stoll (1985, p. 18) for data on specialist revenues. 9. That an affirmative obligation is unnecessary is also part of

Peake's (1978) vision of a national market system in which investors can trade directly with each other.

10. The four equity options markets are the CBOE and the Pacific, American, and Philadelphia stock exchanges. The CBOE recently purchased the NYSE options market.

11. U.S. Securities and Exchange Commission (1996) summa- rizes the CBOE response to the IBI proposal and gives the SEC's views on the proposal.

References

Bhattacharya, Uptal, and Matthew Spiegel. 1997. "Anatomy of a Market Failure: NYSE Trading Suspensions (1974-1988)." Journal of Business and Economic Statistics, vol. 16, no. 2 (April):216-226.

Benston, G.J., and R.L. Hagerman. 1978. "Risk, Volume and Spread." Financial Analysts Journal, vol. 34, no. 1 (January/ February):46-49.

Bernstein, Peter L. 1987. "Liquidity, Stock Markets, and Market Makers." Financial Management, vol. 16, no. 2 (Summer):54-62.

Black, Fischer. 1971a. "Toward a Fully Automated Exchange." Financial Analysts Journal, vol. 27, no.4 (July/August):28-35,44.

- . 1971b. "A Fully Computerized Stock Exchange-II." Financial Analysts Journal, vol. 27, no. 6 (November/ December):24-28, 86-37.

. 1995. "Equilibrium Exchanges." Financial Analysts Journal, vol. 51, no. 3 (May/June):23-29.

Branch, Ben, and W. Freed. 1977. "Bid-Asked Spreads on the AMEX and the Big Board." Journal of Finance, vol. 32, no. 1 (March):159-63.

Cao, Charles, Hyuk Choe, and Frank Hathaway. 1997. "Does the Specialist Matter? Differential Execution Costs and Inter- Security Subsidization on the NYSE." Journal of Finance, vol. 52, no. 4 (September):1615-40.

Christie, William G., and Paul Schultz. 1994. "Why Do Nasdaq Market Makers Avoid Odd-Eighth Quotes?" Journal of Finance, vol. 49, no. 5 (December):1813-40.

.1997. "Dealer Markets under Stress: The Performance of Nasdaq Market Makers during the November 15, 1991 Market Break." Working paper. Owen Graduate School of Management, Vanderbilt University.

Cohen, K., S. Maier, W. Ness, Jr., H. Okuda, R. Schwartz, and D. Whitcomb. 1977. "The Impact of Designated Market Makers on Security Prices." Journal of Banking and Finance, vol. 1, no. 3 (December):219-35.

Copeland, T.C., and D. Galai. 1983. "Information Effects of the Bid-Ask Spread." Journal of Finance, vol. 38, no. 5 (December):1457-69.

Corwin, Shane. 1997. "Differences in Trading Behavior across NYSE Specialist Firms." Working paper. Terry College of Business, University of Georgia.

Friedman, Milton. 1953. "The Case for Flexible Exchange Rates." In Essays in Positive Economics. Chicago, IL: University of Chicago Press.

Glosten, Lawrence R. 1989. "Insider Trading, Liquidity and the Role of the Monopolist Specialist." Journal of Business, vol. 62, no. 2 (April):211-36.

. 1994. "Is the Electronic Open Limit Order Book Inevitable?" Journal of Finance, vol. 49, no.4 (September):1127-61. Glosten, Lawrence R., and Paul R. Milgrom. 1985. "Bid, Ask and Transaction Prices in a Specialist Market with Heterogeneously Informed Traders." Journal of Financial Economics, vol. 14, no. 1 (March):71-100. Hasbrouck, Joel, and George Sofianos. 1993. "The Trade of Market Makers: An Empirical Analysis of NYSE Specialists." Journal of Finance, vol. 48, no. 5 (December):1565-93. Ho, Thomas, and Hans Stoll. 1981. "Optimal Dealer Pricing under Transactions and Return Uncertainty." Journal of Financial Economics, vol. 9, no. 1 (March):47-73. Hopewell, Michael, and Arthur Schwartz. 1978. "Temporary Trading Suspensions in Individual NYSE Securities." Journal of Finance, vol. 33, no. 5 (December):1355-73. Huang, Roger D., and Hans R. Stoll. 1994. "Market Microstructure and Stock Return Predictions." Review of Financial Studies, vol. 7, no. 1 (Spring):179-213.

. 1996. "Dealer versus Auction Market: A Paired Comparison of Execution Costs on Nasdaq and the NYSE." Journal of Financial Economics, vol. 41, no. 3 (July):313-57.

Lee, Charles, Mark Ready, and Paul Sequin. 1994. "Volume, Volatility, and New York Stock Exchange Trading Halts." Journal of Finance, vol. 49, no. 1 (March):183-214. Madhavan, Ananth, and Seymour Smidt. 1991. "A Bayesian Model of Intraday Specialist Pricing." Journal of Financial Economics, vol. 30, no. 1 (November):99-134.

. 1993. "An Analysis of Daily Changes in Specialists' Inventories and Quotations." Journal of Finanice, vol. 48, no. 5 (December):1595-1628. Miller, Merton H. 1991. Financial Innovations and Market Volatility. Cambridge, MA: Blackwell. Oesterle, Dale A., Donald A. Winslow, and Seth C. Anderson. 1992. "The New York Stock Exchange and Its Outmoded Specialist System: Can the Exchange Innovate to Survive?" Journal of Corporation Law, vol. 17 (Winter):223-310.

September/October 1998 81

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions

Financial Analysts Journal

Peake, Junius W. 1978. "The National Market System." Financial Analysts Journal, vol. 34, no. 4 (July/August):25-33.

Presidential Task Force on Market Mechanisms (Brady Commission). 1988. Report submitted to the President, Secretary of the Treasury, and Chairman of the Federal Reserve Board, January 8.

Robbins, Sidney. 1966. The Securities Markets. New York: Free Press.

Roll, Richard. 1988. "The International Crash of October 1987." Financial Analysts Journal, vol. 44, no. 5 (September/ October):19-35.

. 1989. "Price Volatility, International Market Links, and Their Implications for Regulatory Policies." Journal of Financial Services Research, vol. 3, no. 2/3 (December):211-46.

Smidt, S. 1971. "Which Road to an Efficient Stock Market?" Financial Analysts Journal, vol. 27, no. 5 (September/ October):18-20.

Stigler, George J. 1964. "Public Regulation of the Securities Markets." Journal of Business, vol. 37, no. 2 (April):117-42.

Stoll, Hans R. 1976. "Dealer Inventory Behavior: An Empirical Investigation of NASDAQ Stocks." Journal of Financial and Quantitative Analysis, vol. 11, no. 3 (September):359-80.

. 1978a. "The Supply of Dealer Services in Securities Markets." Journal of Finance, vol. 33, no. 4 (September):1133-51.

. 1978b. "The Pricing of Security Dealer Services: An Empirical Study of NASDAQ Stocks." Journal of Finance, vol. 33, no. 4 (September):1153-72.

. 1985. "The Stock Exchange Specialist System: An Economic Analysis." Monograph Series in Finance and Economics, 1985-2. New York University, Salomon Center.

Stoll, Hans R., and Robert E. Whaley. 1990a. "Stock Market Structure and Volatility." Review of Financial Studies, vol. 3, no. 1 (Spring):37-71.

. 1990b. "The Dynamics of Stock Index and Stock Index Futures Returns." Journal of Financial and Quantitative Analysis, vol. 25, no. 5:441-68.

Tinic, S. 1972. "The Economics of Liquidity Services." Quarterly Journal of Economics, vol. 86, no. 1 (February):79-93.

U.S. Securities and Exchange Commission. 1963. Report of the Special Study of Securities Markets, Part 2. 88th Congress, 1st Session. Washington, DC: U.S. Government Printing Office.

. 1971. Institutional Investor Study Report. 92nd Congress, 1st Session. Washington, DC: U.S. Government Printing Office.

. 1996. Release No. 34-38054 ("CBOE Release") (December 16), 61 FR 67365 (December 20).

.1997. Order Execution Obligations. Release No. 34-37619A (January 10).

v

~~~~~- A

jjTI4 Over 24,000 investment professionals from 63 countries have earned the CFAW designation -

Chartered Financial Analyst. And that speaks volumes in any language. It says that the standards represented by the CFA charter are a constant in an ever-changing world of international investments. That the designation's stringent Code of Ethics and advanced curriculum provide charterholders with the competitive edge so vital to their success.

A universal symbol for high professional standards and principles, the CFA charter is sponsored by the Association for Investment Management and Research. AIMR also offers other professional development programs designed to achieve higher standards for CFA charterholders, their employers and their clients.

For more information and a free brochure, call 1-800- 247-8132. Or visit our Web site at www.aimr.org. tEW 9lIM R

SETTING A HIGHER STANDARD

82 ?Association for Investment Management and Research

This content downloaded from 195.78.108.199 on Sat, 14 Jun 2014 19:03:33 PMAll use subject to JSTOR Terms and Conditions