Embed Size (px)

Citation preview

Recession and Recovery: A New England Perspective

Yolanda KodrzyckiVice President and Director, NEPPC

Federal Reserve Bank of Boston

Presented atRegional and Community Bankers Conference

October 21, 2010

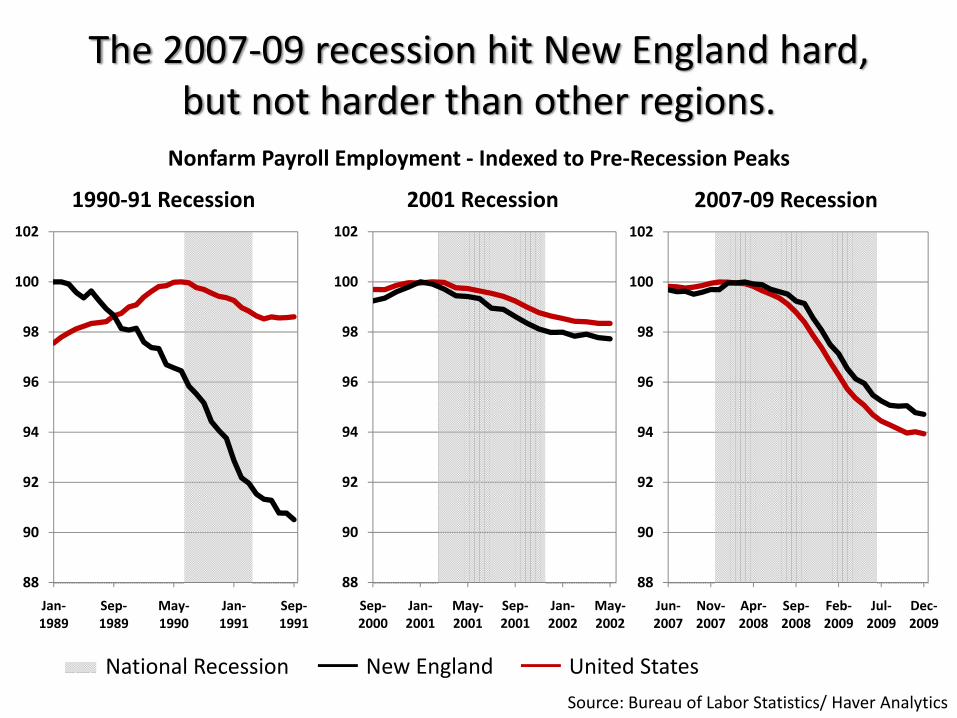

The 2007‐09 recession hit New England hard, but not harder than other regions.

Nonfarm Payroll Employment ‐ Indexed to Pre‐Recession Peaks

National Recession United States

Source: Bureau of Labor Statistics/ Haver Analytics

88

90

92

94

96

98

100

102

Jan‐1989

Sep‐1989

May‐1990

Jan‐1991

Sep‐1991

1990‐91 Recession

88

90

92

94

96

98

100

102

Sep‐2000

Jan‐2001

May‐2001

Sep‐2001

Jan‐2002

May‐2002

2001 Recession

88

90

92

94

96

98

100

102

Jun‐2007

Nov‐2007

Apr‐2008

Sep‐2008

Feb‐2009

Jul‐2009

Dec‐2009

2007‐09 Recession

New England

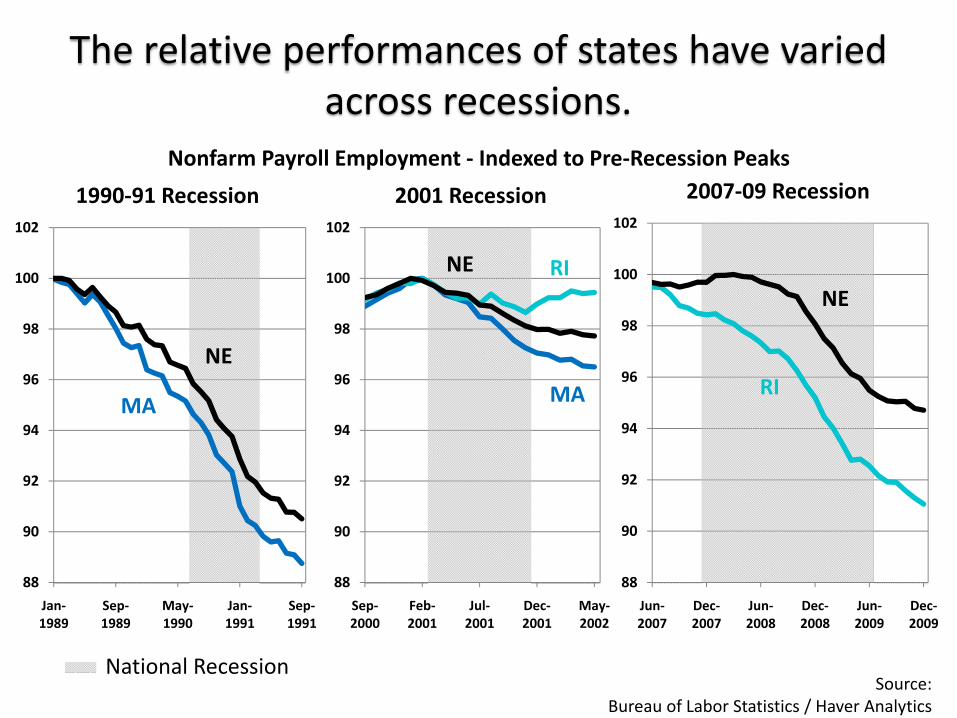

The relative performances of states have variedacross recessions.

Nonfarm Payroll Employment ‐ Indexed to Pre‐Recession Peaks

Source: Bureau of Labor Statistics / Haver Analytics

88

90

92

94

96

98

100

102

Jan‐1989

Sep‐1989

May‐1990

Jan‐1991

Sep‐1991

1990‐91 Recession

88

90

92

94

96

98

100

102

Sep‐2000

Feb‐2001

Jul‐2001

Dec‐2001

May‐2002

2001 Recession

RI

88

90

92

94

96

98

100

102

Jun‐2007

Dec‐2007

Jun‐2008

Dec‐2008

Jun‐2009

Dec‐2009

2007‐09 Recession

MA MA RI

National Recession

NE

NE

NE

Among the New England states, MA and NH had the smallest job losses in the 2007‐09 recession …

‐12%

‐10%

‐8%

‐6%

‐4%

‐2%

0%

RI CT VT ME NE MA NH

Change in Nonfarm Employment from Peak to Trough

Source: Calculations Based on Bureau of Labor Statistics Data

… and the strongest job gains in the expansion to date

0%

2%

4%

6%

8%

10%

12%

ME VT CT RI NE NH MA

Change in Nonfarm Employment from Trough to August 2010

Source: Calculations Based on Bureau of Labor Statistics Data

By sector, construction and manufacturinghad the steepest job losses in 2007‐09.

New England United States

Source: Calculations Based on Bureau of Labor Statistics Data

Construction

Manufacturing

Professional and Business Services

Trade, Transportation, and Utilities

Financial Activities

Leisure and Hospitality

Government

Educational and Health Services

Percentage Change from Peak to Trough

Government and financial servicesare still shedding jobs.

New England United States

Source: Calculations Based on Bureau of Labor Statistics Data

Construction

Manufacturing

Professional and Business Services

Trade, Transportation, and Utilities

Financial Activities

Leisure and Hospitality

Government

Educational and Health Services

Percentage Change From Trough to Present

Four New England sectors have shed50,000 or more jobs since 2007.

Source: Calculations Based on Bureau of Labor Statistics Data

Construction

Manufacturing

Professional and Business Services

Trade, Transportation, and Utilities

Financial Activities

Leisure and Hospitality

Government

Educational and Health Services

Thousands

Change in NE Employment from Peak to August 2010

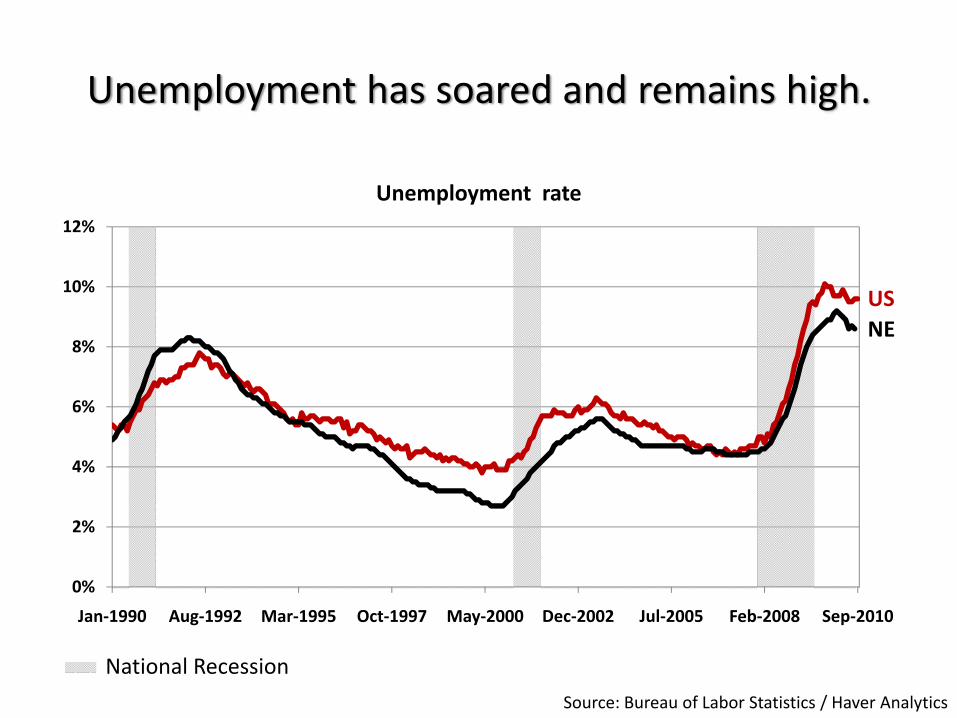

Unemployment has soared and remains high.

Source: Bureau of Labor Statistics / Haver Analytics

0%

2%

4%

6%

8%

10%

12%

Jan‐1990 Aug‐1992 Mar‐1995 Oct‐1997 May‐2000 Dec‐2002 Jul‐2005 Feb‐2008 Sep‐2010

Unemployment rate

USNE

National Recession

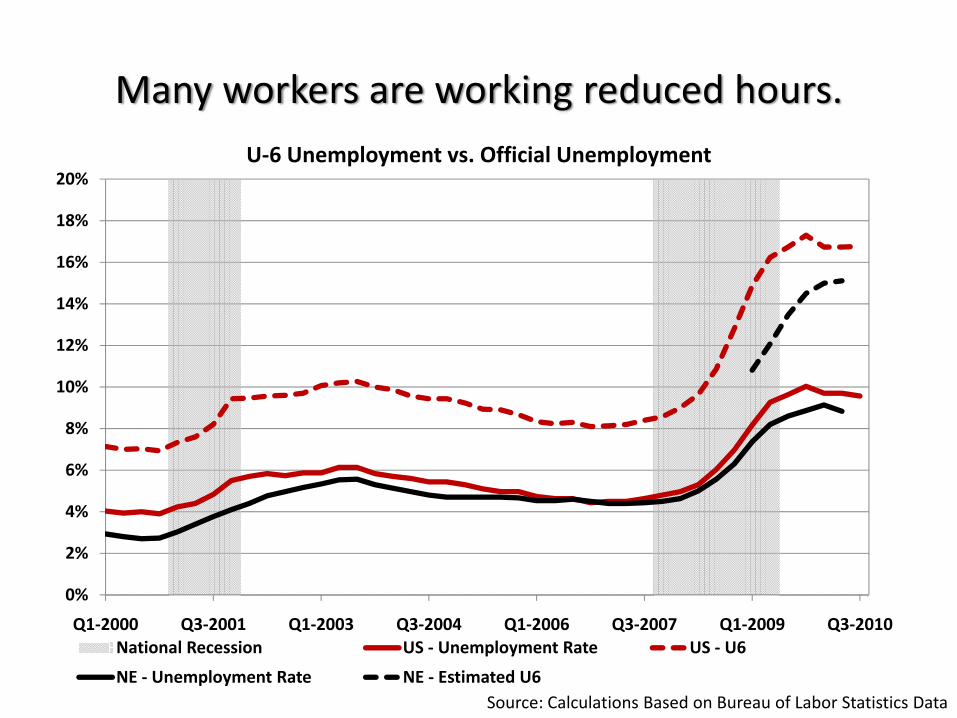

Many workers are working reduced hours.

Source: Calculations Based on Bureau of Labor Statistics Data

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Q1‐2000 Q3‐2001 Q1‐2003 Q3‐2004 Q1‐2006 Q3‐2007 Q1‐2009 Q3‐2010

U‐6 Unemployment vs. Official Unemployment

National Recession US ‐ Unemployment Rate US ‐ U6

NE ‐ Unemployment Rate NE ‐ Estimated U6

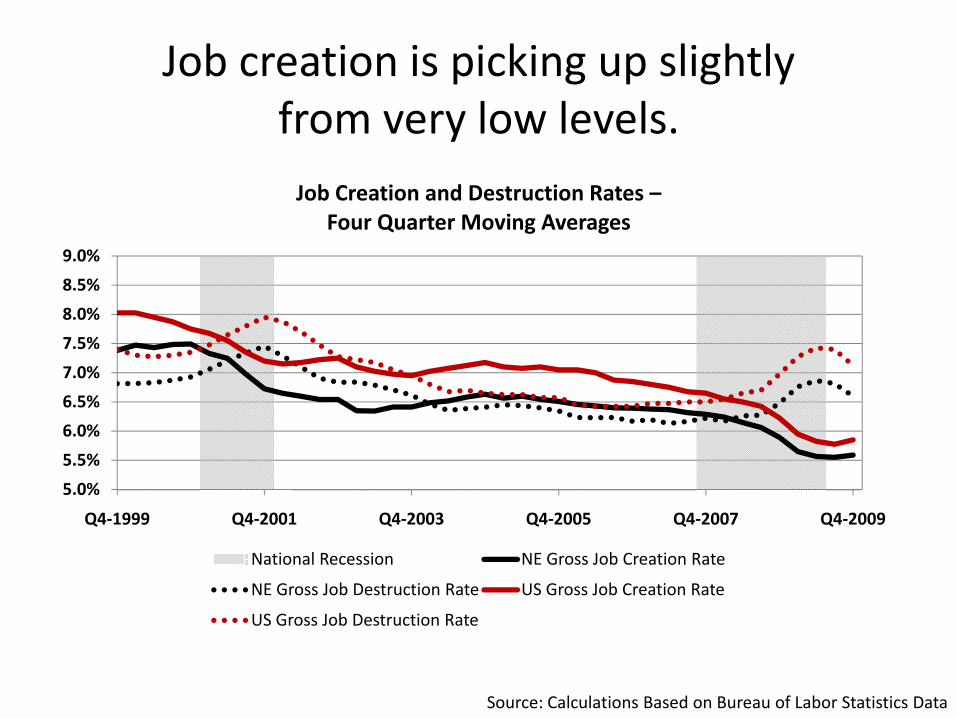

Job creation is picking up slightly from very low levels.

Source: Calculations Based on Bureau of Labor Statistics Data

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

Q4‐1999 Q4‐2001 Q4‐2003 Q4‐2005 Q4‐2007 Q4‐2009

Job Creation and Destruction Rates –Four Quarter Moving Averages

National Recession NE Gross Job Creation Rate

NE Gross Job Destruction Rate US Gross Job Creation Rate

US Gross Job Destruction Rate

House prices have fallen 19 percent in RI, more than in neighboring states.

Source: Federal Housing Finance Authority/Haver Analytics

0

100

200

300

400

500

600

700

800

Q2‐1990 Q2‐1994 Q2‐1998 Q2‐2002 Q2‐2006 Q2‐2010

Southern New England FHFA House Price Index (1980 = 100)

Percent Change From Peak to PresentCT MA RI US

‐12.7% ‐12.9% ‐19% ‐11.2%MA

US

RICT

National Recession

House prices in Vermont have been remarkably stable throughout the downturn.

Source: Federal Housing Finance Authority/Haver Analytics

0

100

200

300

400

500

600

700

800

Q2‐1990 Q2‐1994 Q2‐1998 Q2‐2002 Q2‐2006 Q2‐2010

Northern New England FHFA House Price Index (1980 = 100)

Percent Change From Peak to PresentME NH VT US‐9.2% ‐14.1% ‐3.4% ‐11.2%

MEVTNHUS

National Recession

Foreclosure starts in RI have fallen,and are now in line with neighboring states.

Source: Mortgage Bankers Association/Haver Analytics

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

Q2‐1990 Q2‐1994 Q2‐1998 Q2‐2002 Q2‐2006 Q2‐2010

Southern New England Foreclosure Starts ‐Percentage of All Home Loans

MA

USRICT

National Recession

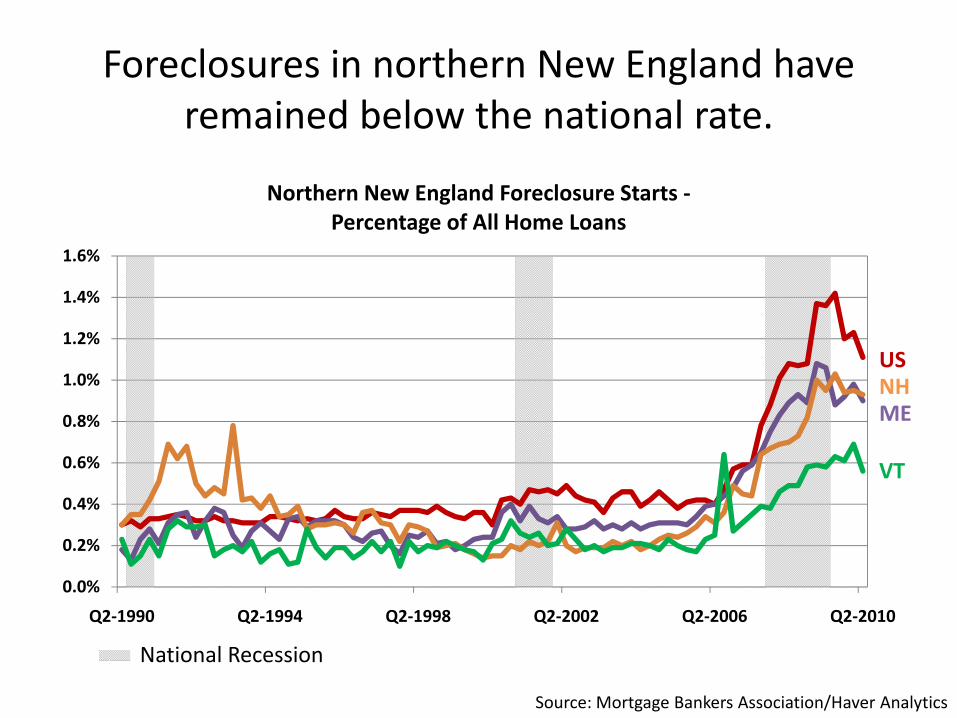

Foreclosures in northern New England have remained below the national rate.

Source: Mortgage Bankers Association/Haver Analytics

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

Q2‐1990 Q2‐1994 Q2‐1998 Q2‐2002 Q2‐2006 Q2‐2010

Northern New England Foreclosure Starts ‐Percentage of All Home Loans

ME

US

VT

NH

National Recession

Homeowner vacancy rates in New England have remained well below the national average.

Source: Bureau of the Census/Haver Analytics

MA

US

RI

CT

National Recession

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Q2‐1999 Q1‐2002 Q4‐2004 Q3‐2007 Q2‐2010

Southern New England Homeowner Vacancy RateFour Quarter Moving Average

Homeowner vacancy rates have been higher in Maine than in other northern New England states.

Source: Bureau of the Census/Haver Analytics

NH

US

VT

ME

National Recession

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

Q2‐1999 Q1‐2002 Q4‐2004 Q3‐2007 Q2‐2010

Northern New England Homeowner Vacancy RateFour Quarter Moving Average

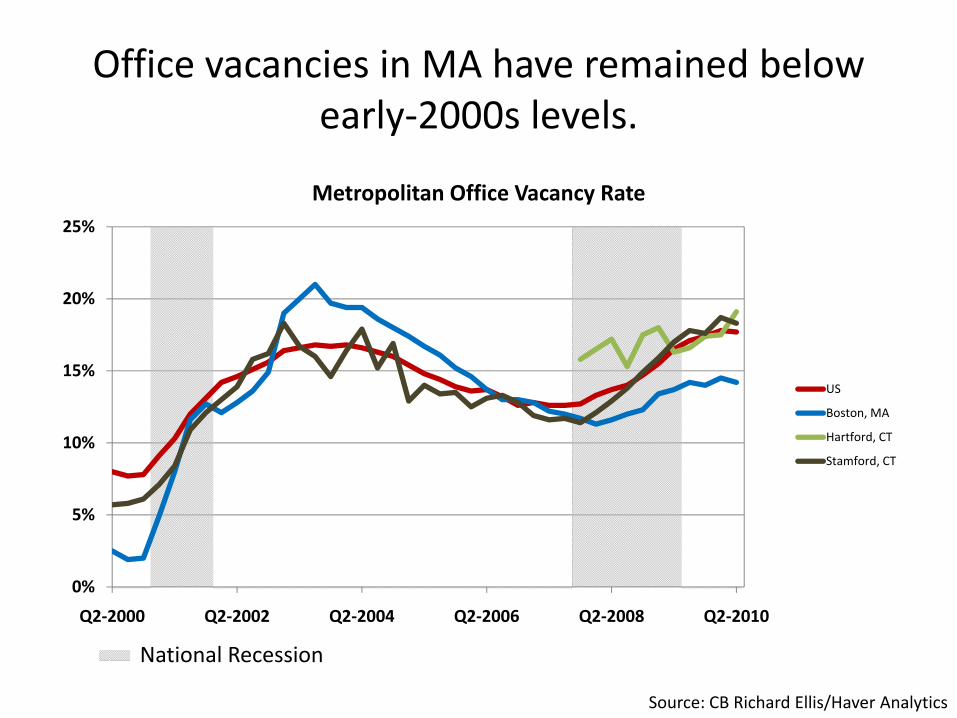

Office vacancies in MA have remained below early‐2000s levels.

Source: CB Richard Ellis/Haver Analytics

0%

5%

10%

15%

20%

25%

Q2‐2000 Q2‐2002 Q2‐2004 Q2‐2006 Q2‐2008 Q2‐2010

Metropolitan Office Vacancy Rate

US

Boston, MA

Hartford, CT

Stamford, CT

National Recession

Small businesses are reporting few job openings and little interest in expanding headcount.

0%10%20%30%40%

Jan‐1989 May‐1993 Sep‐1997 Jan‐2002 May‐2006 Sep‐2010

Percent of Small Businesses with One or More Jobs Open(Four Quarter Moving Average)

‐10%0%10%20%30%

Jan‐1989 May‐1993 Sep‐1997 Jan‐2002 May‐2006 Sep‐2010

Net Percent of Small Businesses Planning to Increase Employment(Four Quarter Moving Average)

National Recession

Source: National Federation of Independent Business

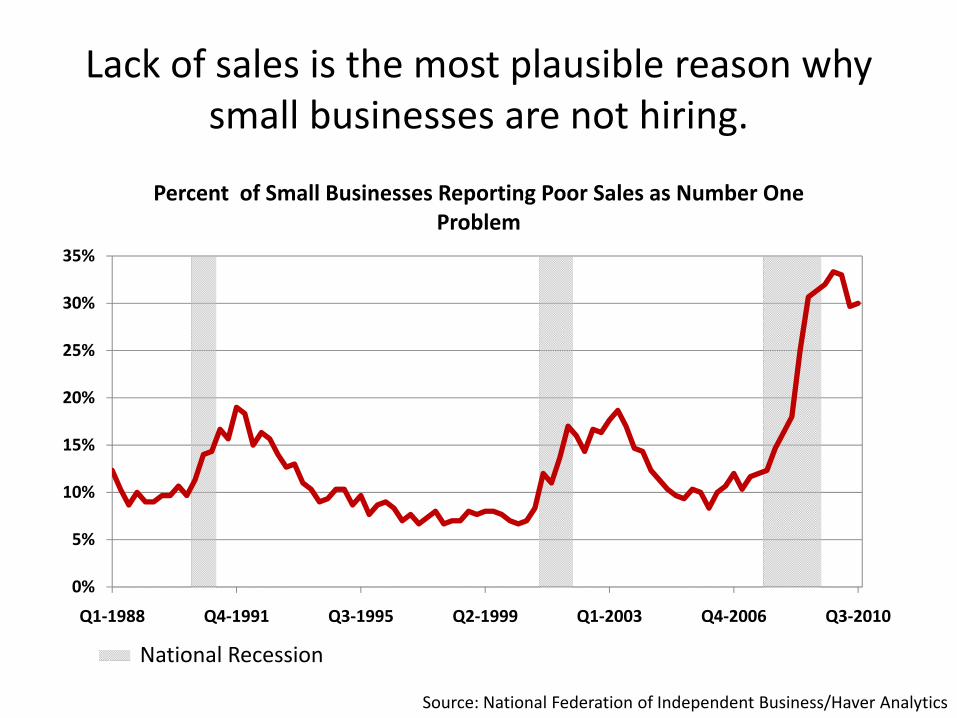

Lack of sales is the most plausible reason why small businesses are not hiring.

Source: National Federation of Independent Business/Haver Analytics

0%

5%

10%

15%

20%

25%

30%

35%

Q1‐1988 Q4‐1991 Q3‐1995 Q2‐1999 Q1‐2003 Q4‐2006 Q3‐2010

Percent of Small Businesses Reporting Poor Sales as Number One Problem

National Recession

Poor sales have replaced taxes as the biggest concern to small businesses.

1st 2nd 3rd 4th 5th

1990‐91 Recession

TaxesGovernment Requirements

Poor Sales OtherCompetition from Large Corporations

23.1% 16.9% 13.2% 11.8% 9.0%

2001 Recession

Taxes Quality of Labor Poor SalesGovernment Requirements

Insurance Cost or Availability

22.5% 16.7% 13.4% 11.3% 11.0%

2007‐09 Recession

Poor Sales TaxesInsurance

Cost/AvailabilityInflation

Government Requirements

21.2% 19.0% 11.1% 10.0% 9.6%

Source: National Federation of Independent Business/Haver Analytics

Top Average Responses During Past Three Recessions

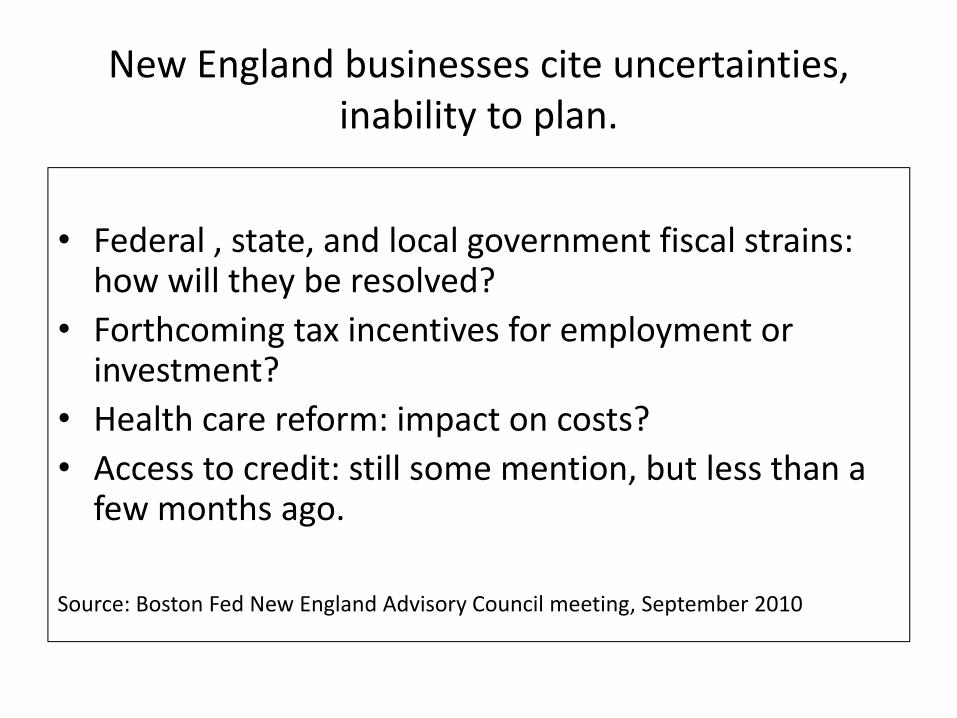

New England businesses cite uncertainties, inability to plan.

• Federal , state, and local government fiscal strains: how will they be resolved?

• Forthcoming tax incentives for employment or investment?

• Health care reform: impact on costs?• Access to credit: still some mention, but less than a few months ago.

Source: Boston Fed New England Advisory Council meeting, September 2010

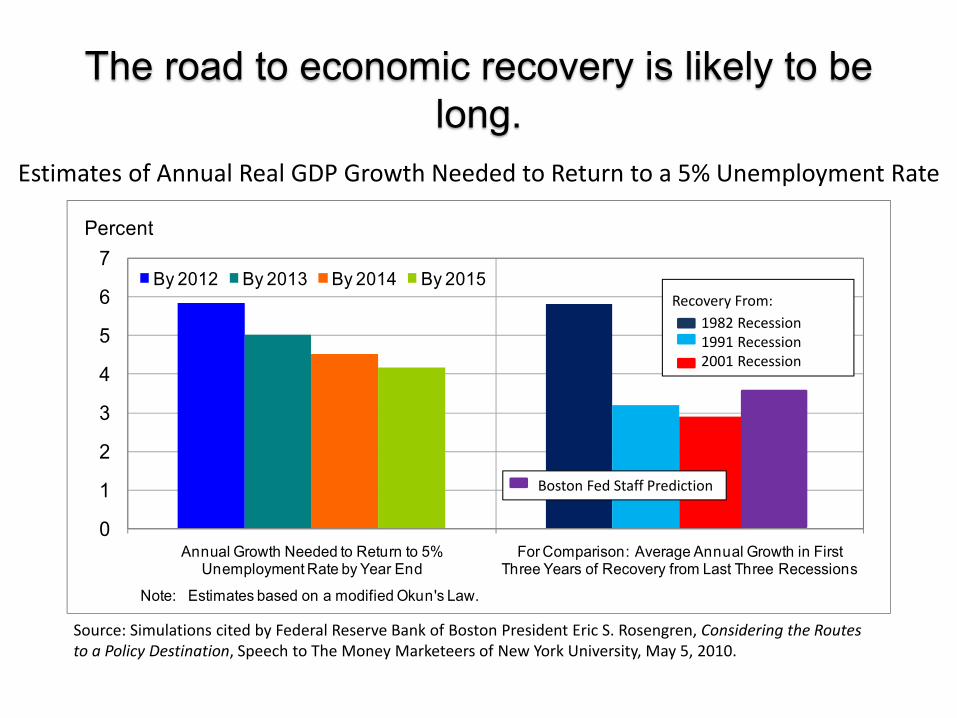

The road to economic recovery is likely to be long.

0

1

2

3

4

5

6

7

Annual Growth Needed to Return to 5% Unemployment Rate by Year End

For Comparison: Average Annual Growth in First Three Years of Recovery from Last Three Recessions

By 2012 By 2013 By 2014 By 2015

Percent

1982 Recession

1991 Recession

2001 Recession

Recovery from:

Note: Estimates based on a modified Okun's Law.

Recovery From:1982 Recession1991 Recession2001 Recession

Estimates of Annual Real GDP Growth Needed to Return to a 5% Unemployment Rate

Boston Fed Staff Prediction

Source: Simulations cited by Federal Reserve Bank of Boston President Eric S. Rosengren, Considering the Routes to a Policy Destination, Speech to The Money Marketeers of New York University, May 5, 2010.

Economic recovery won’t feel like fiscal recovery for the states.

• ARRA money goes away.• Rainy day funds have been drawn down.• Employment and wages are lagging GDP recovery.• Enrollments in Medicaid / SCHIP rise when economy is weak.

• Pension and other retirement‐related contributions continue to rise.

• Local governments seek more state aid as property tax revenues weaken.

Summary

• New England economy hit hard, but not quite as hard as U.S. economy.

• Slow recovery taking hold.

• Many opinions on what can and should be done to accelerate the improvement.

• Fiscal problems of state and local government will exert a drag on the recovery unless federal aid comes to the rescue.