Embed Size (px)

Citation preview

RECENT TRENDS AND CHALLENGESIN THE FIELD OF VALUATION

Organised byCentre for Valuation Studies

Institution of Science and Technology for Advanced Studies & Research,Vallabh Vidyanagar

14th December, 2013

BY

JIGESH J. MEHTAB.E. (Civil), LL.B., M.S.(USA), F.I.V.

(Govt. Approved Valuer)

Office :A-302, Tirupati Plaza,

Near Collector’s Office,Athwa Gate, Surat - 395 001.

Tel. no. : +91-261-2472637

Any challenge implies an opportunity….Infact, a prospect is associated with every problem of valuation. Every challenging situation can usually be addressed primarily by the application of ten commandments of valuation. viz.

4 factors – legal, economic, social, physical/technical;

4 ingredients – utility, scarcity, transferability, demand/supply;

Value means Present Worth of Future Benefits, and

In any valuation exercise of tangible assets what is valued is not the tangible thing but rights and interests arising out of ownership of tangible assets.

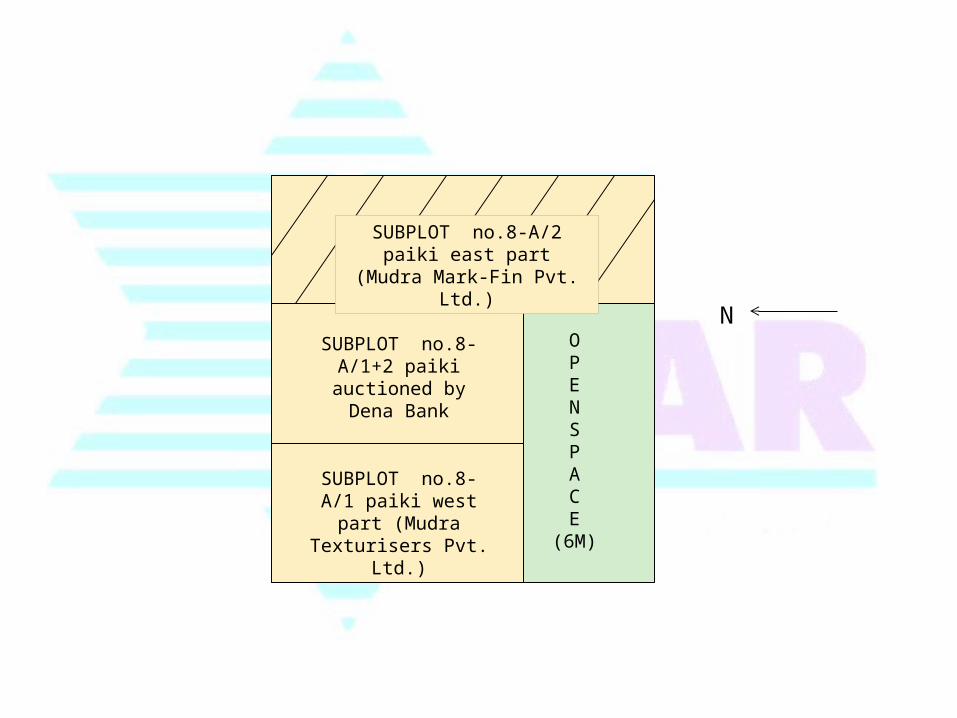

NON-AVAILABILITY OF APPROVED SUBDIVISION PLANS

OPENSPACE

(6M)

SUBPLOT no.8-A/1+2 paiki

auctioned by Dena Bank

SUBPLOT no.8-A/1 paiki west part (Mudra Texturisers Pvt. Ltd.)

SUBPLOT no.8-A/2 paiki east part (Mudra Mark-Fin

Pvt. Ltd.)

N

COMBINED CONSTRUCTION ON TWO ADJOINING PLOTS BUT ONLY ONE OFFERED AS LOAN SECURITY

Two brothers had purchased two adjoining plots. Instead of constructing duplex-type bungalow with two independent units, they had constructed only one(1) two-storeyed building covering both plots in such a way that the ground floor was occupied by one brother and 1st floor was occupied by another brother. The brother occupying ground floor wanted loan facility against mortgage of his one plot. On inspection, it was found that 1st owner’s ground floor was on his plot but the 1st floor portion above it was under the possession of 2nd brother. We could not inspect 1st floor occupied by 2nd brother as relations between two brothers had strained and they were not on talking terms. After the loan officer was informed about his fact, the bank decided to reject this property as security.

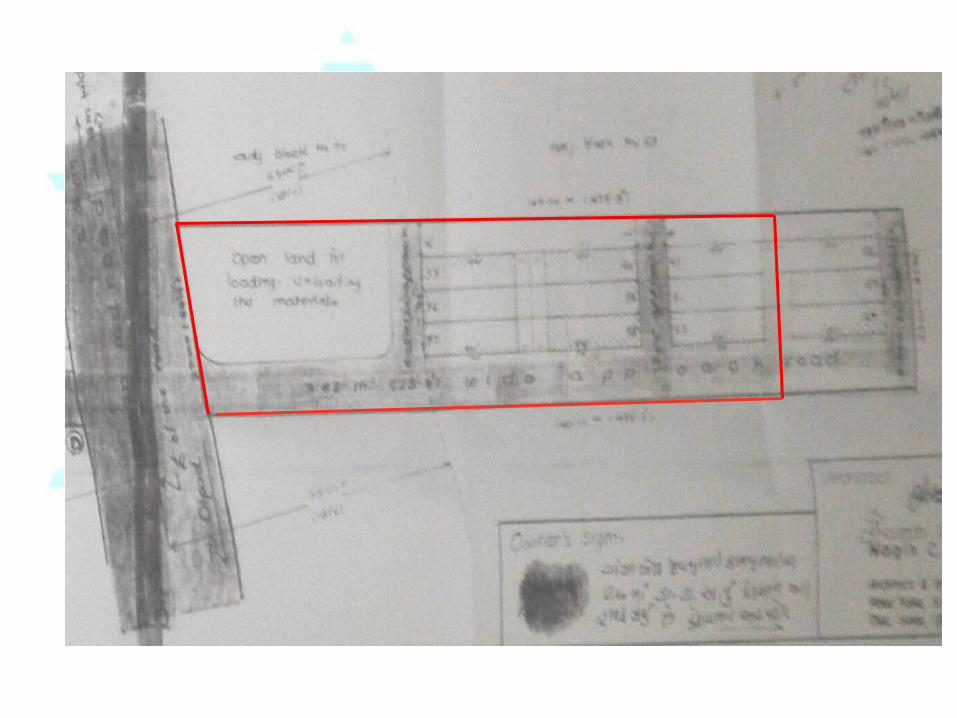

AREAS OF COMMON USE SUCH ROADS, COP AND LOADING/UNLOADING TRANSFERRED IN FAVOUR OF SOME SPECIFIC PLOTHOLDER(S) IN A LAYOUT

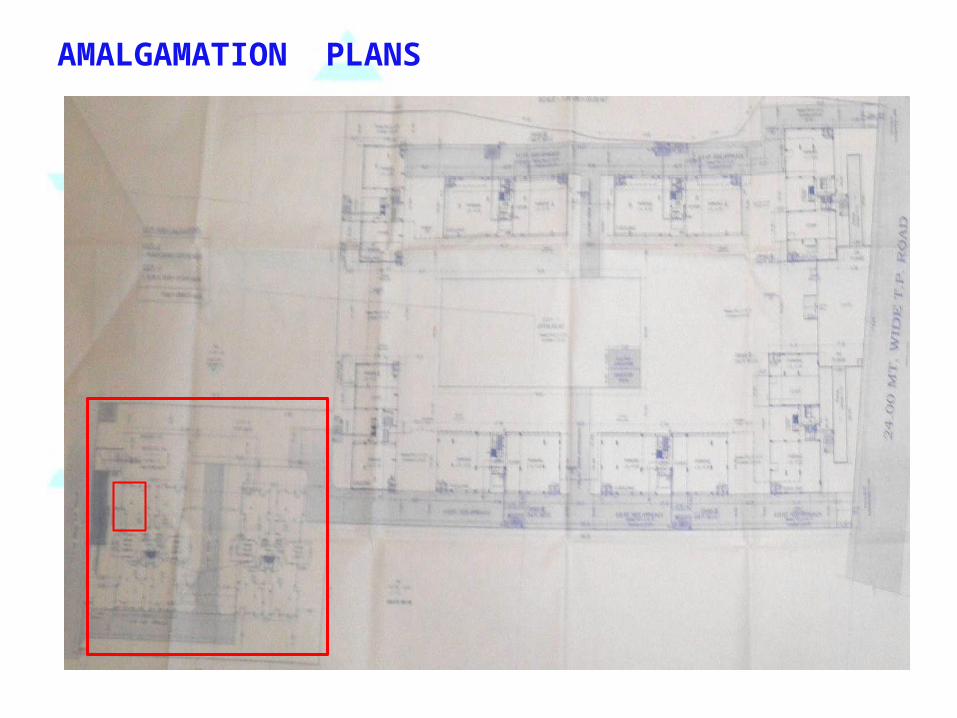

AMALGAMATION PLANS

5 shops on an upper floor of commercial building developed on 2060.50 sq. m. land area out of the overall plot area of 4331.77 sq. m. including a twin-theatre

Age of Building ~ 25 years; Future Life ~ 30 years

Leasehold land for 60 year period from 1971

Due to non-availability of lease deed for land, it could not be verified whether there is provision (or not) for further extension of lease on the expiry of lease period in year 2031.

Non-transfer clause of leasehold rights in land mentioned in sale deeds for shops for transfer of superstructure only

Parent lease deed for land does not allow the leaseholder/developer of this building to transfer or assign leasehold rights in land and therefore, the developer of the land have the responsibility to pay the lease rent during the period of lease

Prima facie, this appears to be a case of defective title. Careful study of the sale deeds hints that these shops are virtually transferred on sublease (atleast for unexpired lease period ~ 18 years as on date of valuation) without any ground rent, at 100% premium.

Market Value basis will hold good only if advocate’s title report confirms that the shopholders in this building are entitled to leasehold rights for undivided land corresponding to the shops by virtue of their possession/occupation because what is being valued is the “shopholders’ interests in the shops” and NOT the shop itself. ELSE, the lender Bank will be not be able extend charge to the undivided land area as only the superstructure will be mortgaged

It is noteworthy that out of the prevailing composite rate of Rs.5500-6000 per sq. ft. ASSUMING THAT GROUND LEASE IS FURTHER RENEWABLE AFTER EXPIRY OF PRESENT LEASE TERM (considering lease in perpetuity equivalent to freehold land), the construction component would not exceed 20-25% while the remaining 75-80% is attributable to the FSI value for corresponding undivided land.

What would happen if the building is wholly destroyed or becomes permanently unfit for use due to fire or flood or earthquake or other such irresistible force duering loan period? Insurance is taken only for construction but if the developer does not agree to give land for re-construction, a dead-lock will be created and one does not know the final outcome if the matter is taken to court as the developers will argue that only construction was sold and that the land right was never transferred. This interpretation could be very harmful. Once this submission is clearly made by the developer, any challenge to counter him in court of law would be a tedious matter.

SHARE OF UNDIVIDED LAND AREA NOT TRANSFERRED ALONGWITH BUILT-UP UNITS

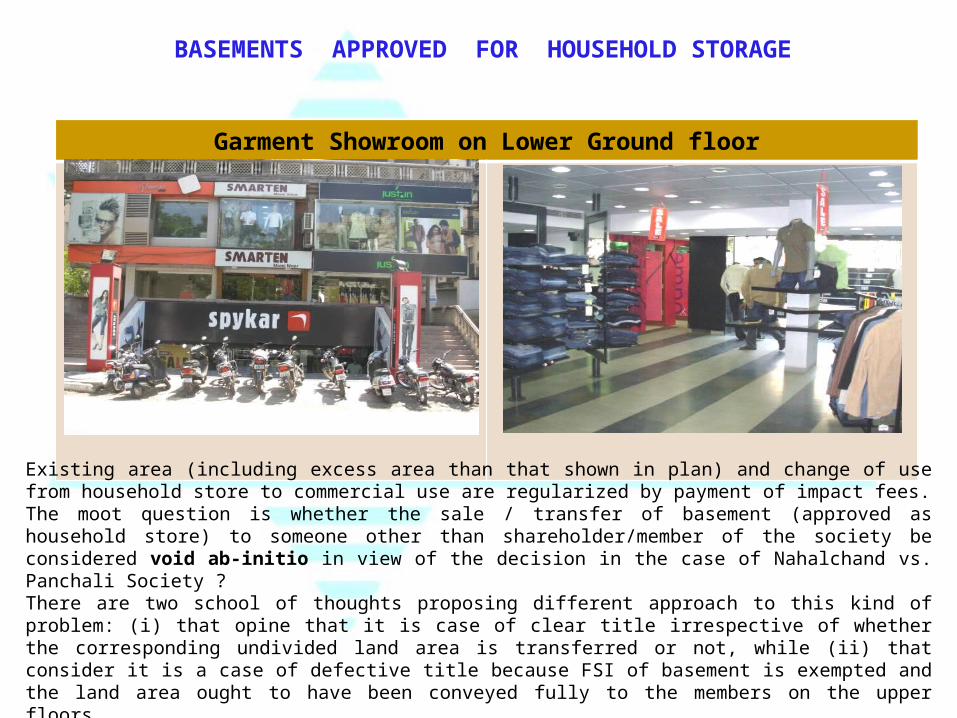

BASEMENTS APPROVED FOR HOUSEHOLD STORAGE

Garment Showroom on Lower Ground floor

Existing area (including excess area than that shown in plan) and change of use from household store to commercial use are regularized by payment of impact fees.The moot question is whether the sale / transfer of basement (approved as household store) to someone other than shareholder/member of the society be considered void ab-initio in view of the decision in the case of Nahalchand vs. Panchali Society ?There are two school of thoughts proposing different approach to this kind of problem: (i) that opine that it is case of clear title irrespective of whether the corresponding undivided land area is transferred or not, while (ii) that consider it is a case of defective title because FSI of basement is exempted and the land area ought to have been conveyed fully to the members on the upper floors.

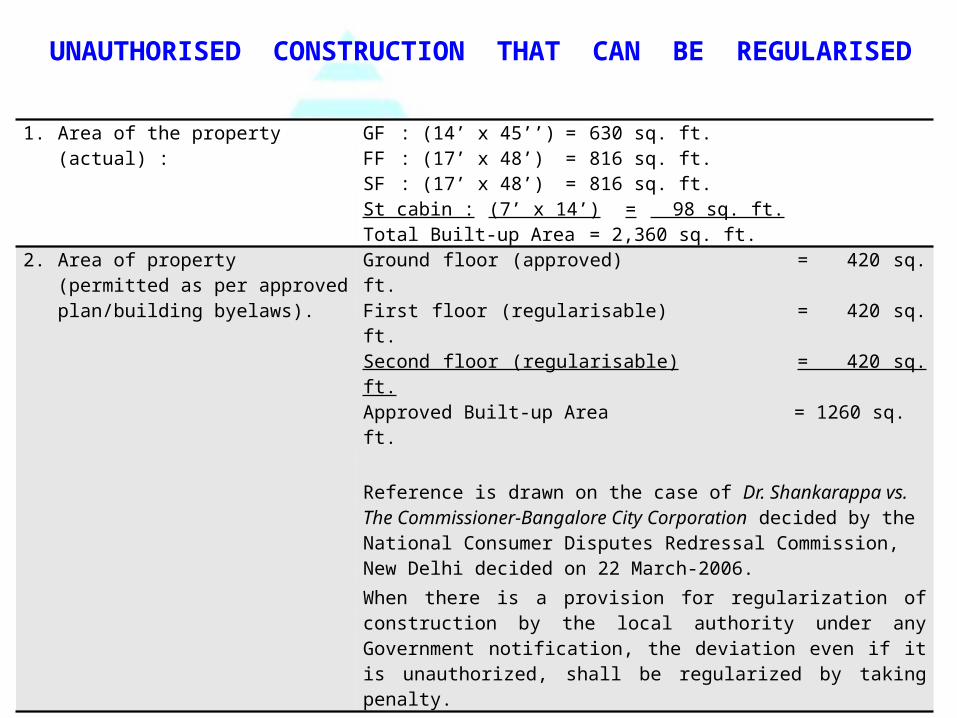

UNAUTHORISED CONSTRUCTION THAT CAN BE REGULARISED

1. Area of the property (actual) : GF : (14’ x 45’’) = 630 sq. ft.FF : (17’ x 48’) = 816 sq. ft.SF : (17’ x 48’) = 816 sq. ft.St cabin : (7’ x 14’) = 98 sq. ft.Total Built-up Area = 2,360 sq. ft.

2. Area of property (permitted as per approved plan/building byelaws).

Ground floor (approved) = 420 sq. ft.First floor (regularisable)= 420 sq. ft.Second floor (regularisable) = 420 sq. ft.Approved Built-up Area = 1260 sq. ft.

Reference is drawn on the case of Dr. Shankarappa vs. The Commissioner-Bangalore City Corporation decided by the National Consumer Disputes Redressal Commission, New Delhi decided on 22 March-2006.When there is a provision for regularization of construction by the local authority under any Government notification, the deviation even if it is unauthorized, shall be regularized by taking penalty.

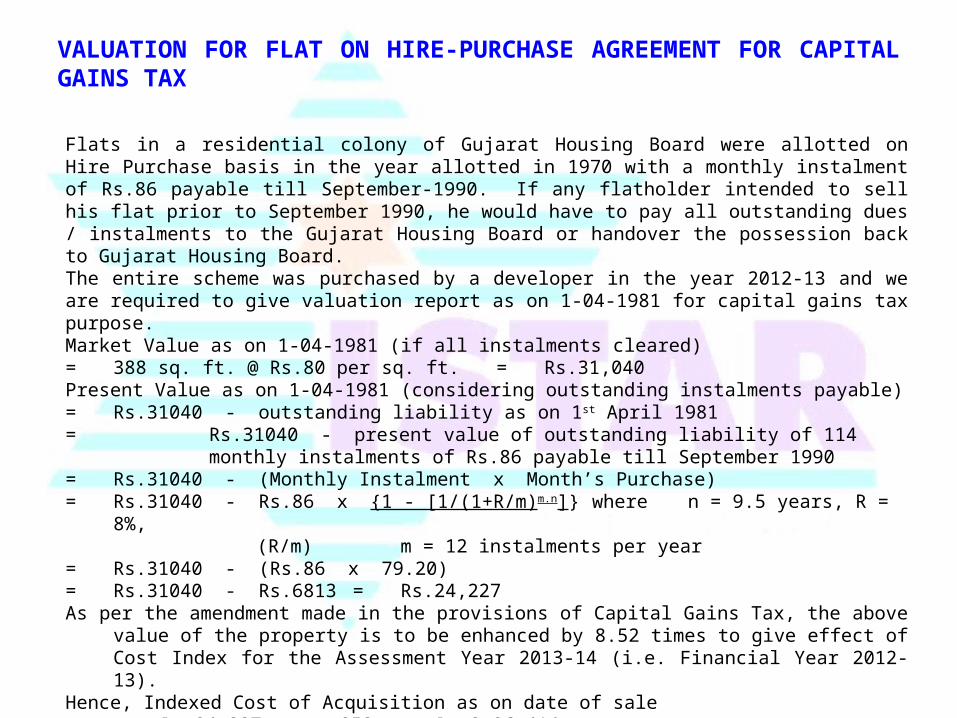

VALUATION FOR FLAT ON HIRE-PURCHASE AGREEMENT FOR CAPITAL GAINS TAX

Flats in a residential colony of Gujarat Housing Board were allotted on Hire Purchase basis in the year allotted in 1970 with a monthly instalment of Rs.86 payable till September-1990. If any flatholder intended to sell his flat prior to September 1990, he would have to pay all outstanding dues / instalments to the Gujarat Housing Board or handover the possession back to Gujarat Housing Board.The entire scheme was purchased by a developer in the year 2012-13 and we are required to give valuation report as on 1-04-1981 for capital gains tax purpose.Market Value as on 1-04-1981 (if all instalments cleared)= 388 sq. ft. @ Rs.80 per sq. ft. = Rs.31,040Present Value as on 1-04-1981 (considering outstanding instalments payable)= Rs.31040 - outstanding liability as on 1st April 1981= Rs.31040 - present value of outstanding liability of 114 monthly instalments of

Rs.86 payable till September 1990= Rs.31040 - (Monthly Instalment x Month’s Purchase)= Rs.31040 - Rs.86 x {1 - [1/(1+R/m)m.n]} where n = 9.5 years, R = 8%,

(R/m) m = 12 instalments per year= Rs.31040 - (Rs.86 x 79.20)= Rs.31040 - Rs.6813 = Rs.24,227As per the amendment made in the provisions of Capital Gains Tax, the above value of the property is

to be enhanced by 8.52 times to give effect of Cost Index for the Assessment Year 2013-14 (i.e. Financial Year 2012-13).

Hence, Indexed Cost of Acquisition as on date of sale= Rs.24,227 x 852 = Rs.2,06,414

100

PROPERTIES UNDER COASTAL REGULATION ZONE (CRZ)

Part Plan of Draft Town Planning Scheme

Survey no

Documented Area Effect under proposed Draft T.P.Scheme

(sq. m.) Final Plot no.

Area Deduction (sq. m.)

Net Area (sq.m.)

30 13861 (Old tenure, N.A.) 3 611 13,250

32 4654 (Old tenure, N.A.) 5/1 920 3,734

38 40165 (Old tenure)Subject to verification of N.A. permission granted by Collector u/s 65B of Bombay Land Revenue Code (for industrial use)

8/1 + 8/2 14,055 26,110

41 paiki 13658 (New Tenure)

Pending premium for conversion to old tenure and subsequently N.A. permission

18 paiki 3,902 9,756

72,338 sq. m. (-) 19,488 sq. m. 52,850 sq. m.

APPROACH TO VALUATION (NOTIFIED INDUSTRIAL AREA)

Land Value (i) Net Area of land = 52850 sq. m. – 8528 sq. m. under erosion in river from R.S. no.38 = 44322 sq. m. @ Rs.15000 per sq. m. = Rs.66,48,30,000

(ii) Add, Area under erosion in river = 8528 sq. m. @ Rs.5000 per sq. m. = Rs.4,26,40,000

(iii) Less, outstanding liability of premium payable for tenure conversion of R.S. no.41 paiki

= 13658 sq. m. @ 80% of Rs.6450 per sq. m. guideline rate = Rs.7,04,75,280TOTAL VALUE OF FREEHOLDER’S INTEREST IN LAND = Rs.63,69,94,720

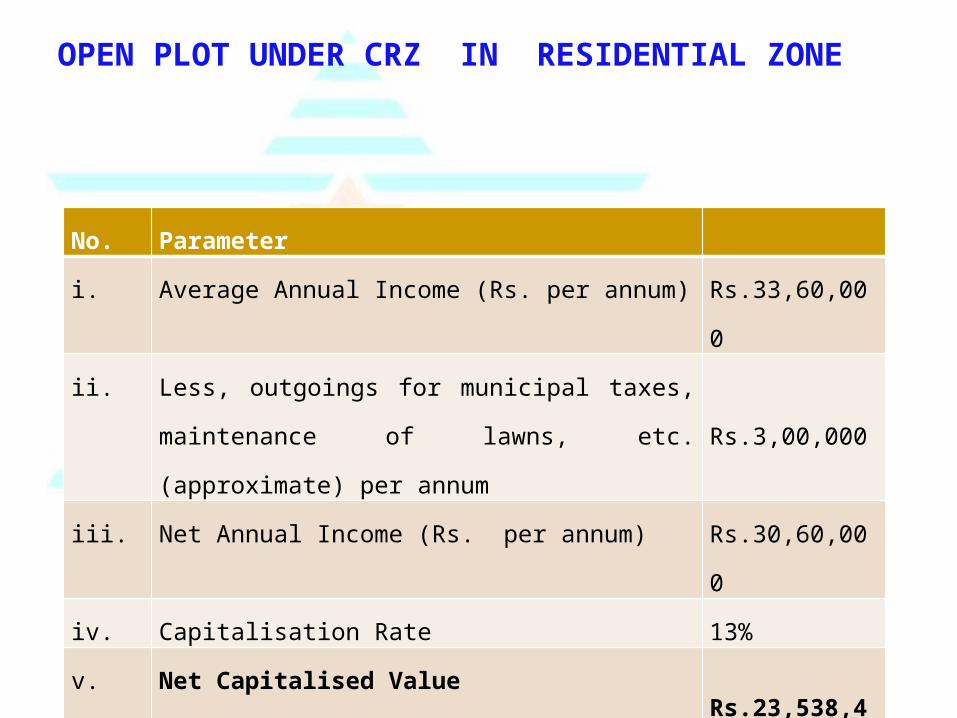

OPEN PLOT UNDER CRZ IN RESIDENTIAL ZONE

No. Parameter

i. Average Annual Income (Rs. per annum) Rs.33,60,000

ii. Less, outgoings for municipal taxes, maintenance

of lawns, etc. (approximate) per annumRs.3,00,000

iii. Net Annual Income (Rs. per annum) Rs.30,60,000

iv. Capitalisation Rate 13%

v. Net Capitalised Value

= Net Annual Income / Capitalization RateRs.23,538,461

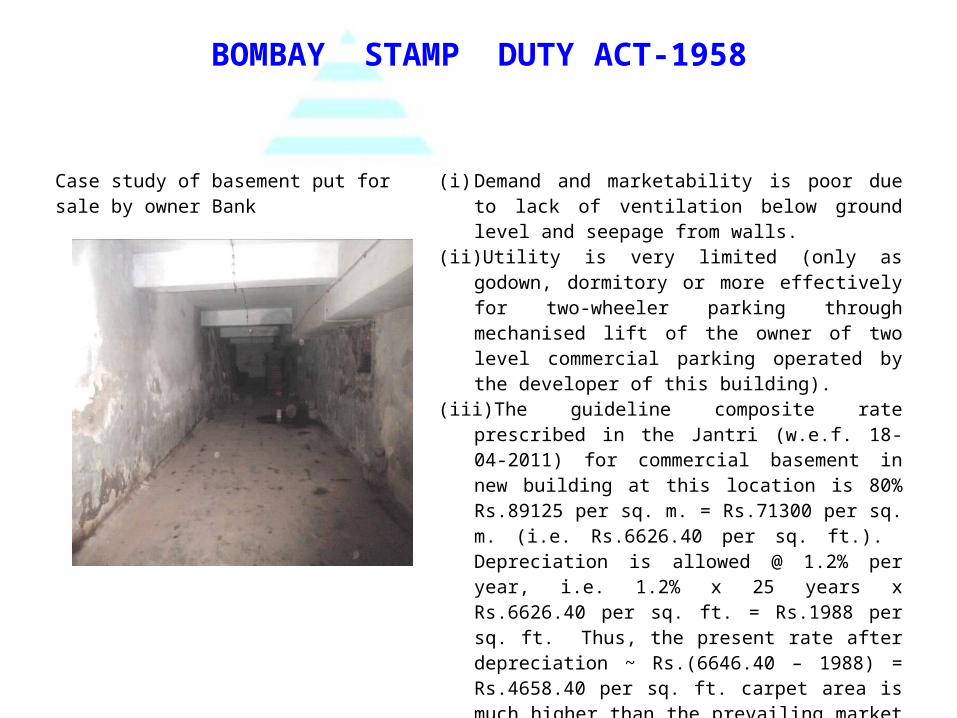

BOMBAY STAMP DUTY ACT-1958

Case study of basement put for sale by owner Bank

(i) Demand and marketability is poor due to lack of ventilation below ground level and seepage from walls.

(ii) Utility is very limited (only as godown, dormitory or more effectively for two-wheeler parking through mechanised lift of the owner of two level commercial parking operated by the developer of this building).

(iii) The guideline composite rate prescribed in the Jantri (w.e.f. 18-04-2011) for commercial basement in new building at this location is 80% Rs.89125 per sq. m. = Rs.71300 per sq. m. (i.e. Rs.6626.40 per sq. ft.). Depreciation is allowed @ 1.2% per year, i.e. 1.2% x 25 years x Rs.6626.40 per sq. ft. = Rs.1988 per sq. ft. Thus, the present rate after depreciation ~ Rs.(6646.40 – 1988) = Rs.4658.40 per sq. ft. carpet area is much higher than the prevailing market rate. However, as per the provisions of Jantri, the conveyance deed for this property will have to be executed paying a stamp duty on Jantri rate eventhough the auction value may be lesser. Alternatively, the seller Bank should get prevaluation / adjudication done under section 31 of the Bombay Stamp Duty Act.

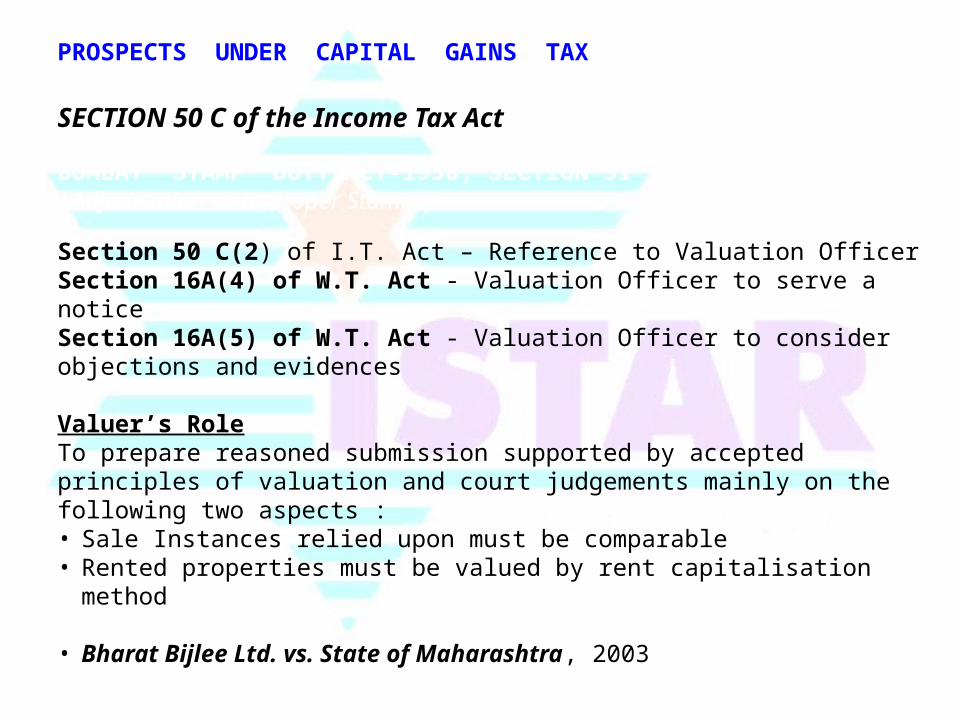

SECTION 50 C of the Income Tax Act

PROSPECTS UNDER CAPITAL GAINS TAX

BOMBAY STAMP DUTY ACT-1958, SECTION 31 (Adjudication as to Proper Stamps)

Section 50 C(2) of I.T. Act – Reference to Valuation OfficerSection 16A(4) of W.T. Act - Valuation Officer to serve a notice Section 16A(5) of W.T. Act - Valuation Officer to consider objections and evidences

Valuer’s RoleTo prepare reasoned submission supported by accepted principles of valuation and court judgements mainly on the following two aspects :• Sale Instances relied upon must be comparable• Rented properties must be valued by rent capitalisation method

• Bharat Bijlee Ltd. vs. State of Maharashtra, 2003

PROSPECTS UNDER WEALTH TAX ACT

Exemptions are covered under Section 2(ea) and Section 5

(A) Any house that the assessee may occupy for the purpose of business or profession carried on by him.(B) Any residential property that has been let out for a minimum period of three hundred days in the previous year.(C) Any property in the nature of commercial establishments or complexes.(D) Urban Land such as land on which construction of a building is not permissible under any law for the time being in force or the land occupied by any building constructed with the approval of the appropriate authority or any unused land held by assessee for industrial purposes for a period of two years from the date of acquisition by him.

According SECTION 5(VI), one house or part of a house or a plot of land (not exceeding 500 sq. m.) belonging to an individual or H.U.F. is exempted.Concessional valuation for a house can be worked out by applying provisions of Schedule-III of Wealth Tax Act.

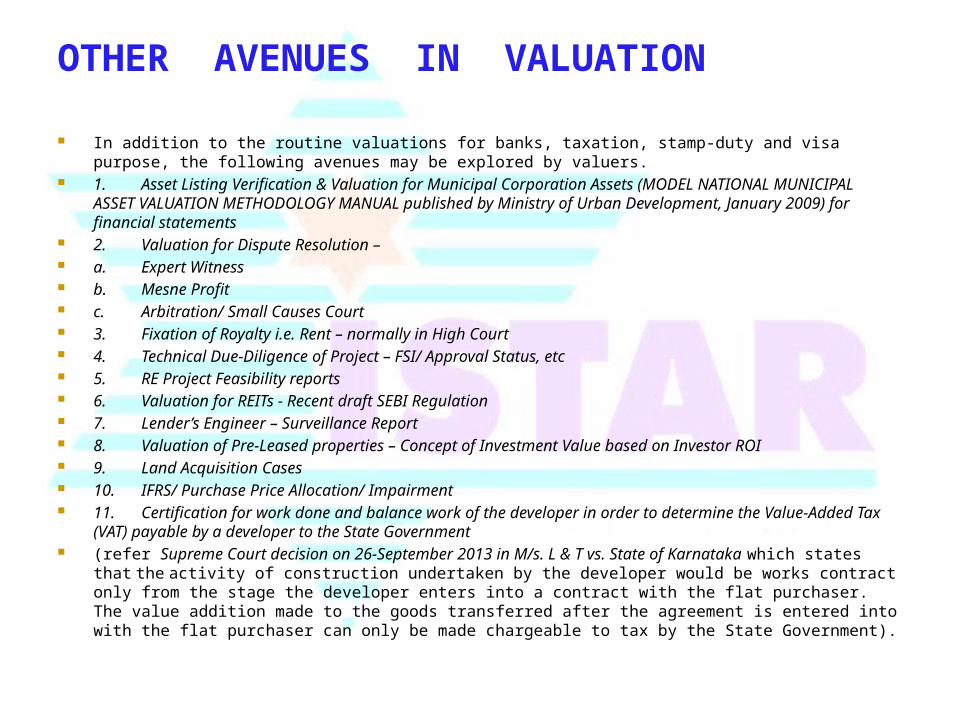

OTHER AVENUES IN VALUATION

In addition to the routine valuations for banks, taxation, stamp-duty and visa purpose, the following avenues may be explored by valuers.

1. Asset Listing Verification & Valuation for Municipal Corporation Assets (MODEL NATIONAL MUNICIPAL ASSET VALUATION METHODOLOGY MANUAL published by Ministry of Urban Development, January 2009) for financial statements

2. Valuation for Dispute Resolution – a. Expert Witness b. Mesne Profit c. Arbitration/ Small Causes Court 3. Fixation of Royalty i.e. Rent – normally in High Court 4. Technical Due-Diligence of Project – FSI/ Approval Status, etc 5. RE Project Feasibility reports 6. Valuation for REITs - Recent draft SEBI Regulation 7. Lender’s Engineer – Surveillance Report 8. Valuation of Pre-Leased properties – Concept of Investment Value based on Investor ROI 9. Land Acquisition Cases 10. IFRS/ Purchase Price Allocation/ Impairment 11. Certification for work done and balance work of the developer in order to determine the Value-

Added Tax (VAT) payable by a developer to the State Government (refer Supreme Court decision on 26-September 2013 in M/s. L & T vs. State of Karnataka which states that the

activity of construction undertaken by the developer would be works contract only from the stage the developer enters into a contract with the flat purchaser. The value addition made to the goods transferred after the agreement is entered into with the flat purchaser can only be made chargeable to tax by the State Government).

Thank You

![Opening the blackbox of [e]valuation in private equity ... · ‘social studies of finance’ and the ‘sociology of valuation and evaluation’ literatures by investigating the](https://img.dokumen.tips/doc/110x75/5d4b7b6f88c993e76c8b5a21/opening-the-blackbox-of-evaluation-in-private-equity-social-studies.jpg)