Embed Size (px)

Citation preview

1

Recent Healthcare Mergers & Acquisitions - Business and Legal Trends

John Callahan Partner and Head of International Healthcare M&A

MCDERMOTT WILL & EMERY LLP

312.984.7553

Michael A. Crabb, III (Trey) Managing Director and Hospital M&A Practice Leader

ZIEGLER INVESTMENT BANKING

312.705.7272

Twitter: healthbanker

2

Discussion Topics

1. The Big Picture

2. Trends in Healthcare and Hospital M&A

3. Healthcare Reform

4. Bogies, Blunders and Bombs

5. Emerging Models

Appendix

3

Learning Objectives

1. Increase members’ familiarity with mergers, acquisitions and joint ventures

2. Bring members’ knowledge current in healthcare M&A

3. Help members position their organizations to thrive in a changing marketplace

4

Discussion Topics

1. The Big Picture

5

Polling Question #1

6

The Big Picture

7

The Big Picture

8

$2,500,000,000,000

The Big Picture

9

The Big Picture

10

The Big Picture

11

Discussion Topics

2. Trends in Healthcare and Hospital M&A

Year-to-Date Performance

12

Healthcare Investing

Buy – Hospitals – low valuations make this a great time to jump in and achieve great arbitrage

multiples in the next 5 years • Standalone NFP experiencing increased pressure

• NFP systems up for grabs if reimbursement pressure grows

– Senior Housing – private pay increases the strength of this sector in uncertainty

– PBMs – minimal government exposure

Hold – Hospice – uncertain reimbursement

– Skilled Nursing

– Home Health

– Diagnostic Imaging

13

Increased M&A Activity

14

• 51 hospital deals announced YTD 2012

*Source: Irving Levin Associates, Inc.

82

56

37

59

5055

61 60

52

77

86

51

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

0

10

20

30

40

50

60

70

80

90

100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 YTD(Sept)

Transactions Dollars Committed (Billions)

Consolidation in Greater Chicago Market

Centegra Health and Mercy Alliance Filed for New Hospital CON

National Health Systems Enters Chicago Market Through Acquisitions

Merger of Two Large Catholic Health Systems

Merger of Two Hospitals in Western Suburbs

20 miles

More than 30%20% - 30%10% - 20%0% - 10%Less than 0%

Vanguard Acquires Additional Hospitals in Market

1

2

++

Adventist MidwestNorthwestern MemorialAcademic Medical CenterAdvocateAlexian Brothers (Ascension)Loyola (Trinity)RHC - ProvenaCentegraCDH – DelnorVanguardOther

Population Growth 2000-2004

15

Greater Chicago Market Recent M&A Activity

Centegra Health & Mercy Alliance each filed CONs for new hospitals in 12/2010, both were denied in 6/2011; revised applications submitted and denied in 12/2011; CON granted to Centrgra in 7/2012

Ascension (Alexian Brothers) & Trinity (Loyola and Mercy) enter Market through acquisitions • Ascension/Alexian signed a

letter of intent in 4/2011; approved by IHF 12/2011

• Trinity acquisition of Loyola closed in 6/2011

• Trinity acquisition of Mercy reported in 9/2011; closed in 3/2012

Merger of Provena & Resurrection Health Care (closed 11/2011)

Merger of Delnor & Central DuPage Hospital (closed 3/2011)

Vanguard acquires West Suburban & Westlake Hospital from Resurrection Health Care (closed 8/2010)

More than 30%20% - 30%10% - 20%0% - 10%Less than 0%

Population Growth 2000-2007

16

Northwestern terminated diligence with Elmhurst; also in discussions with Northwest Community and Roseland Community Hospital • Elmhurst – announced 10/2011 • Roseland – reported 11/2011 • Northwest Community –

rumored in early 2011

MetroSouth Medical Center (FP) acquired by Community Health Systems (FP) - definitive agreement announced 12/2011

Centegra Health discussions with Froedtert (Winter 2011)

Academic Medical Centers

Advocate

Alexian Brothers (Ascension)

Loyola (Trinity)

RHC - Provena

Centegra

CDH – Delnor

Vanguard

Other

1

2

+ +

Sherman rejects Centegra merger proposal (2/2011); Sherman undertaking merger RFP process (5/2012)

17

Polling Question #2

18

Discussion Topics

3. Healthcare Reform

19

Health Care Reform a/k/a Putting Out Fire with Gasoline

Election 2012

Repeal of material provisions of the Affordable Healthcare Act will grow increasingly difficult to accomplish as: – Benefits of PPACA begin to be available to the currently uninsured – Providers and payors reconfigure themselves for governmental and commercial value and/or budget-based payment

arrangements – Providers can no longer rely on the fee-for-service model

Who will Win as a Result – Transformation, and not just another reimbursement model, will allow big wins for those who partake – Robust IT and monitoring capabilities necessary – Those with a track record of collaborating on patient care – Providers with a stable primary care patient base – Providers that have standardized clinical processes and protocols – Providers with aligned incentives – Providers with strong governance and change management structures

On November 20, 2012, the Obama Administration issued guidance for insurance companies

– Pre-existing conditions / Market reform – Essential health benefits – Wellness incentives

20

21

– Cost

– Quality

– Accountability

21

Recurrent Themes

22

– Hospital Value Based Purchasing Program

– Accountable Care Organizations

– Pilot Program on Payment Bundling

– Readmission Reduction Program

– Payment Adjustments for Hospital-Acquired Infections

22

Cost and Quality Initiatives

23

Coordination/Integration of health care services across treatment settings

Reduction:

– in the cost of health care services

– of preventable hospitalizations

– of emergency room visits

– of hospital readmissions

– of hospital-acquirement infections

Improvements:

– in quality and health outcomes

– in patient and family-caregiver satisfaction

– in the efficiency of care

Doing More with Less

24

New Technology Costs

A need, no longer an option, for a strong IT infrastructure to support:

– The coordination of care

– Quality of care measurement, improvement and reporting

– New payment models and Policies

– Expanded Benchmarking Functions

– Data Capturing, Reporting, Counseling

– Electronic Medical Records

– Performance Based Compensation

– Community Need Initiatives

25

Physician Alignment

A need for strong physician platforms, both primary care and specialists

A willingness to change governance and share control with physicians and to align economic incentives to incentivize quality care

A buy-in to evidence based medicine and an adherence to clinical protocols

The capital necessary to build satellite facilities and support vertical integration

A recognition that defensive practice acquisitions can be as or more important than strategic ones that are planned in advance

26

Scale, Scale, Scale

Size really does matter and can shape strategic direction in that it can provide:

– An ability to achieve economic and operational efficiencies

– Access to Capital

– Healthy relationships with payors

– An ability to respond to unexpected market or industry changes nimbly

– Capital to support further strategic alignment initiatives

– A broader knowledge base to leverage

27

Discussion Topics

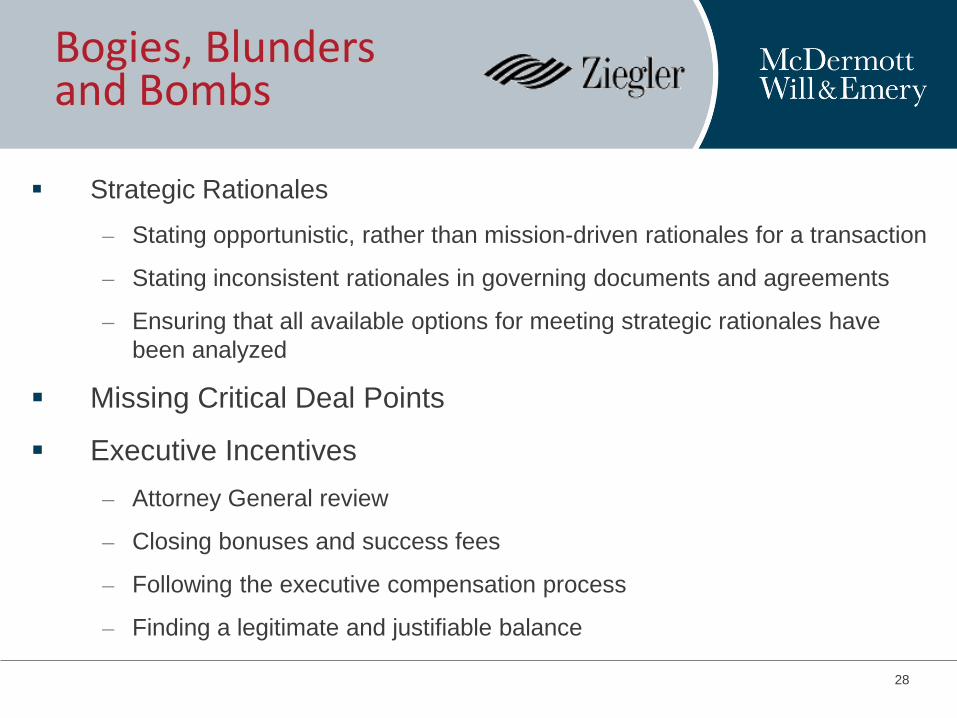

4. Bogies, Blunders and Bombs

28

Strategic Rationales

– Stating opportunistic, rather than mission-driven rationales for a transaction

– Stating inconsistent rationales in governing documents and agreements

– Ensuring that all available options for meeting strategic rationales have been analyzed

Missing Critical Deal Points

Executive Incentives

– Attorney General review

– Closing bonuses and success fees

– Following the executive compensation process

– Finding a legitimate and justifiable balance

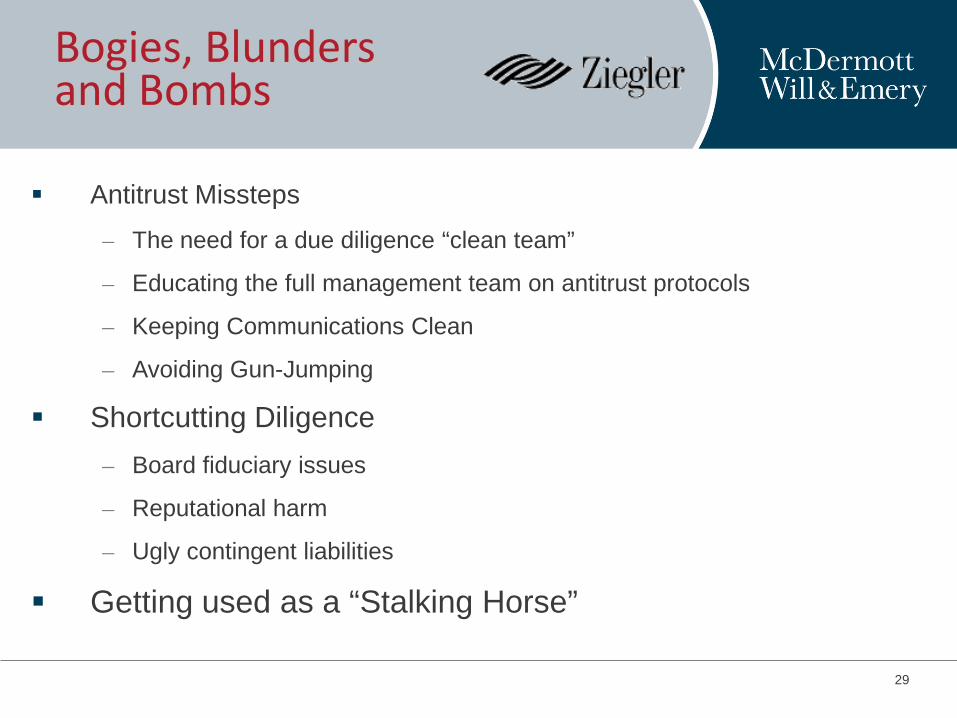

Bogies, Blunders and Bombs

29

Antitrust Missteps

– The need for a due diligence “clean team”

– Educating the full management team on antitrust protocols

– Keeping Communications Clean

– Avoiding Gun-Jumping

Shortcutting Diligence

– Board fiduciary issues

– Reputational harm

– Ugly contingent liabilities

Getting used as a “Stalking Horse”

Bogies, Blunders and Bombs

30

Polling Question #3

31

Discussion Topics

5. Emerging Models

Recent joint ventures

32

DLP Ventures – Duke-LifePoint – Two systems have had a cardiovascular affiliation in place for four years in Danville,

VA

– 4 Transactions together announced

LHP – St. Mary’s Hospital and The Waterbury Hospital* (both in Waterbury, CT)

– Bay medical Center (Panama City, FL) and Sacred Heart Health System (Pensacola, FL)

Aurora Health Care and IASIS Healthcare form Aurora IASIS Health Partners

Aggressive For-Profits

Acquisition of non-profits beyond the traditional rural and suburban markets into urban non-profit hospitals

– Vanguard Health System acquisition of Detroit Medical Center and two Chicago-area Resurrection Health Care hospitals

– Creation of Ascension Health Care Network with Oak Hill

– Healthcare reform driving increased returns for investments that formerly did not seem profitable

Providing ongoing capital commitments post-acquisition

18% of US hospitals

33

Joint Ventures Between not-for-profit and for-profit hospitals in the US

34

LHP management has been involved in 70.6% of these structures.

Source: LHP Proposal for Marion County Hospital District. Feb. 2012

Other groups pursuing joint ventures

35

• Duke LifePoint (DLP)

• Health Management Associates

• Hospital Corporation of America

• Tenet Healthcare

• Not-for-profits

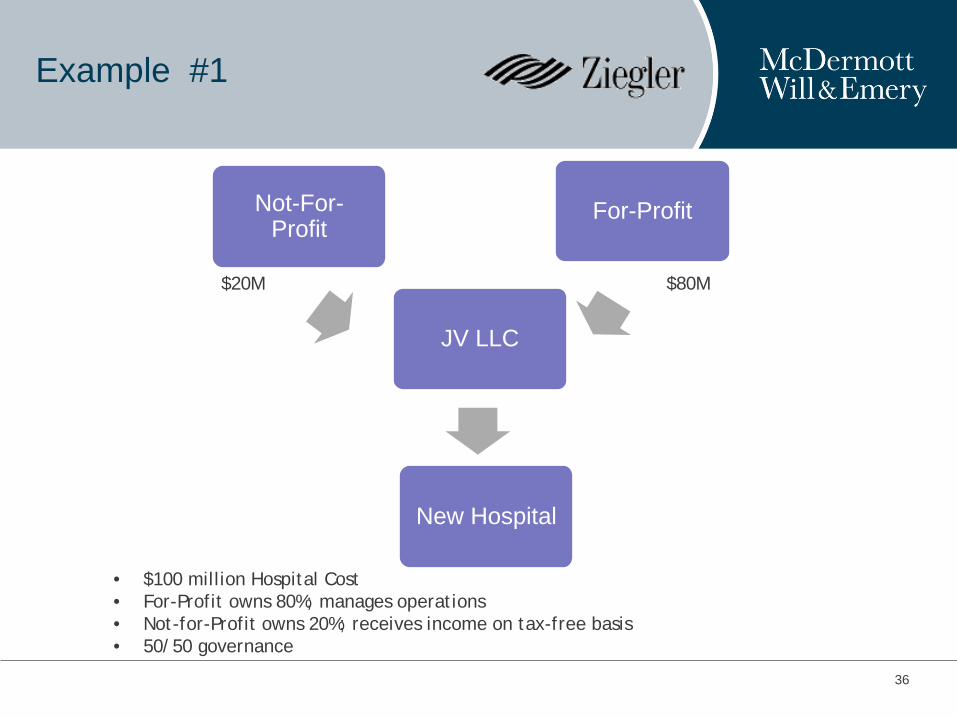

Example #1

36

Not-For-Profit

For-Profit

JV LLC

New Hospital

$20M $80M

• $100 million Hospital Cost • For-Profit owns 80%; manages operations • Not-for-Profit owns 20%; receives income on tax-free basis • 50/50 governance

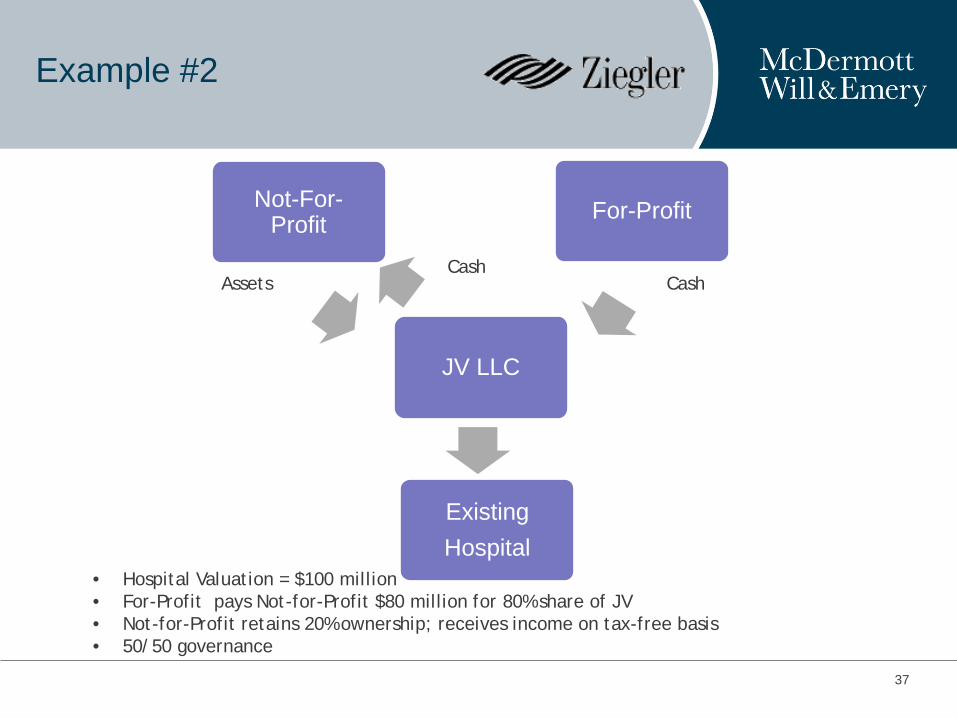

Example #2

37

Not-For-Profit For-Profit

JV LLC

Existing Hospital

Assets Cash

• Hospital Valuation = $100 million • For-Profit pays Not-for-Profit $80 million for 80% share of JV • Not-for-Profit retains 20% ownership; receives income on tax-free basis • 50/50 governance

Cash

The Rise of the Non-Profit

Emergence of aggressive acquisition programs in not-for-profits – Trinity Health merger with Catholic Health East

– Partners Healthcare’s acquisition of South Shore Memorial

Increased experience in strategy by hospital executives – Use of strategic consultants and internal M&A personnel allows not-for-profit hospitals to

take a proactive approach to transactions, looking for deals themselves

Availability of new strategies and structures – Duke LifePoint joint venture

– LHP Hospital Group (+ others) • 80/20 ownership, but 50/50 governance

38

39

Clinical Branding and Management Arrangements

– Use and Protection of Brands

– Measuring effectiveness, economically and clinically

– Clearly defining obligations and expectations

– Rights of first refusal and non-competition provisions

– Watching out for the Trojan Horse

Emerging Deal Structures (Service Line Branding and Affiliation Transaction)

Opportunities Beyond Hospitals

Buying physician practices – “Under-the-radar” deals

– Primary care vs. hospital based physicians

– Non-traditional companies looking to enter physician practice management

Service line activity – Inpatient rehabilitation

– Psychiatry

– Dialysis

Back office functions

40

What is Next?

Critical Access Hospitals

Hospitals with <$100 million NPR

Consolidation within cities

For profit hospital company bandwidth

41

42

Polling Question #4

43

QUESTIONS?

44

Recent Healthcare Mergers & Acquisitions - Business and Legal Trends

John Callahan Partner and Head of International Healthcare M&A

MCDERMOTT WILL & EMERY LLP

312.984.7553

Michael A. Crabb, III (Trey) Managing Director and Hospital M&A Practice Leader

ZIEGLER INVESTMENT BANKING

312.705.7272

Twitter: healthbanker

45

Appendix

Acute Care Hospital Comparative Valuations

46

Post-Acute Comparative Valuations

47

Other Healthcare Comparative Valuations

48

Healthcare REIT Comparative Valuations

49