Embed Size (px)

Citation preview

RECENT DEVELOPMENTS IN THE TAXATION OF DERIVATIVES AND

FINANCIAL PRODUCTS

Chris Van Loan

Partner

Blake, Cassels & Graydon LLP

September 27, 2013

10TH Taxation of Financial Products & Derivatives Course

Federated Press

Introduction

• Focus of presentation will be on recent legislative developments

affecting the Canadian income taxation of derivatives and financial

products

• 2013 Federal budget included two significant proposed changes:

– Character conversion transaction proposals

– Synthetic disposition arrangement proposals

• On July 11, 2013, the Department of Finance released a

backgrounder extending the grandfathering relating to the character

conversion proposals

• Legislative proposals released on September 13, 2013 include draft

provisions implementing the grandfathering discussed in the July 11,

2013 Backgrounder

2

Character Conversion

Transactions

• The proposed character conversion rule would treat

the gain (or loss) realized on a purchase or sale of

capital property under a “derivative forward

agreement” as ordinary income (or loss) rather than

capital gain (or loss)

• The new rules will significantly affect many

investment funds that have used forward contracts

or derivative contracts to convert ordinary income

into capital gains

3

Character Conversion

Transactions (cont’d)

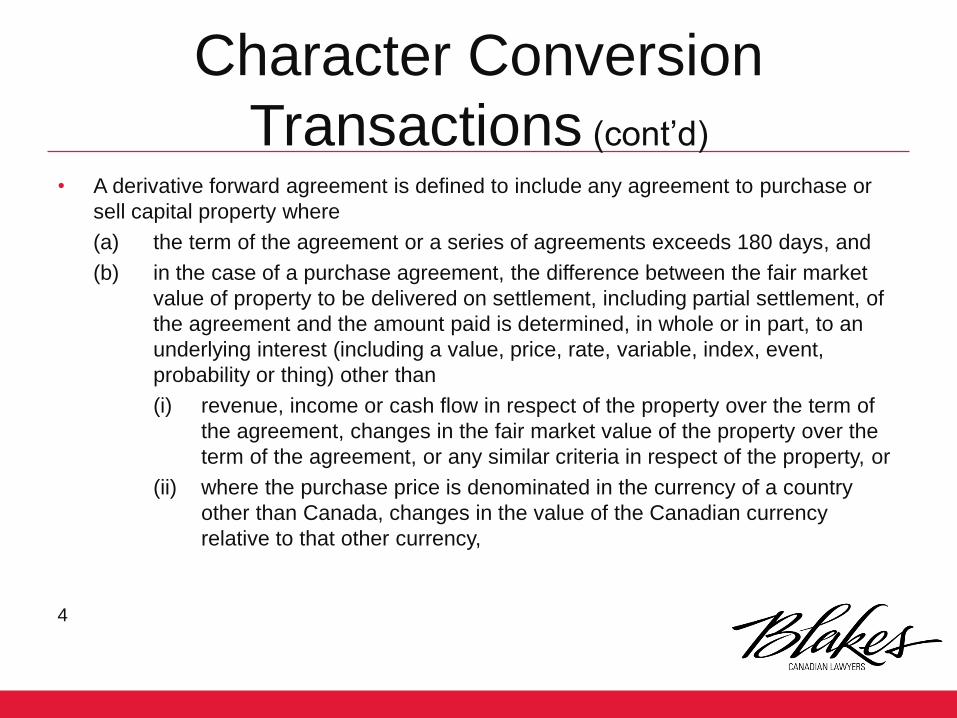

• A derivative forward agreement is defined to include any agreement to purchase or

sell capital property where

(a) the term of the agreement or a series of agreements exceeds 180 days, and

(b) in the case of a purchase agreement, the difference between the fair market

value of property to be delivered on settlement, including partial settlement, of

the agreement and the amount paid is determined, in whole or in part, to an

underlying interest (including a value, price, rate, variable, index, event,

probability or thing) other than

(i) revenue, income or cash flow in respect of the property over the term of

the agreement, changes in the fair market value of the property over the

term of the agreement, or any similar criteria in respect of the property, or

(ii) where the purchase price is denominated in the currency of a country

other than Canada, changes in the value of the Canadian currency

relative to that other currency,

4

Character Conversion

Transactions (cont’d)

(c) in the case of a sale agreement,

(i) the difference between the sale price of the property and the fair market value of the property at

the time the agreement is entered into by the taxpayer is attributable, in whole or in part, to an

underlying interest (including a value, price, rate, variable, index, event, probability or thing)

other than

(A) revenue, income or cash flow in respect of the property over the term of the agreement,

changes in the fair market value of the property over the term of the agreement, or any

similar criteria in respect of the property, or

(B) where the sale price is denominated in the currency of a country other than Canada,

changes in the value of the Canadian currency relative to that other currency,

and

(ii) the agreement is part of an arrangement that has the effect — or would have the effect if the

agreements that are part of the arrangement and that were entered into by persons or

partnerships not dealing at arm’s length with the taxpayer were entered into by the taxpayer

instead of non-arm’s length persons or partnerships — of eliminating a majority of the taxpayer’s

risk of loss and opportunity for gain or profit in respect of the property for a period of more than

180 days;

5

Character Conversion

Transactions (cont’d)

• Proposed paragraph 12(1)(z.7) includes amounts in income

– For a sale, the amount by which the sale price of the property exceeds the fair

market value of the property at the time that the agreement is entered into

– For a purchase, include the amount by which the fair market value of the

property exceeds the cost to the taxpayer of the property

• Proposed paragraph 20(1)(xx) provides for a deduction equal to (subject to certain

restrictions)

– For a sale, the amount by which the fair market value of the property at the time

the agreement is entered into exceeds the sale price of the property

– For a purchase, the amount by which the cost of the property exceeds its fair

market value at the time it is acquired by the taxpayer

• Corresponding adjustments to adjusted cost base to prevent double tax

6

Example: Mutual Fund That Sells

Canadian Securities Forward

• The forward price is based on a reference basket of securities

• In this example, the mutual fund holds Canadian securities and agrees to sell them forward. The

fund has made an election under subsection 39(4) of the Income Tax Act (Canada) to obtain

guaranteed capital gains/capital losses treatment

• Prior to the derivative forward agreement proposal, the mutual fund was able to obtain a return

that is economically linked to the reference basket of securities in the form of capital gains or

capital losses

7

Mutual Fund

Trust

Financial

Product

Provider

Reference Bond

Portfolio Canadian Securities

Forward Sale

Example: Application of the Character

Conversion Transaction Proposal

• This transaction would fit within the definition of a “derivative forward agreement”, as the sale price of the

Canadian securities is determined by reference to a basket of securities that is not related to the value of the

Canadian securities sold forward

• The proposed character conversion rule would thus treat the gain or loss as ordinary income rather than as a

capital gain or capital loss

• I

8

Mutual Fund

Trust

Financial

Product

Provider

Reference Bond

Portfolio Canadian Securities

Forward Sale

Character Conversion

Transactions • The new rules will apply to agreements entered into on or after

March 21, 2013 and to existing agreements that are extended on or

after March 21, 2013

• On July 11, 2013, the Department of Finance released a backgrounder

setting out changes to the character conversion proposals and

extending grandfathering of derivative forward agreements entered into

before March 21, 2013

• The September 13, 2013 legislative proposals contain two sets of

transitional rules

– for series of short-term agreements, grandfathering may be available until the

end of 2014

– for a longer-term agreement, grandfathering may be available until the earlier of

its termination date or March 21, 2018

9

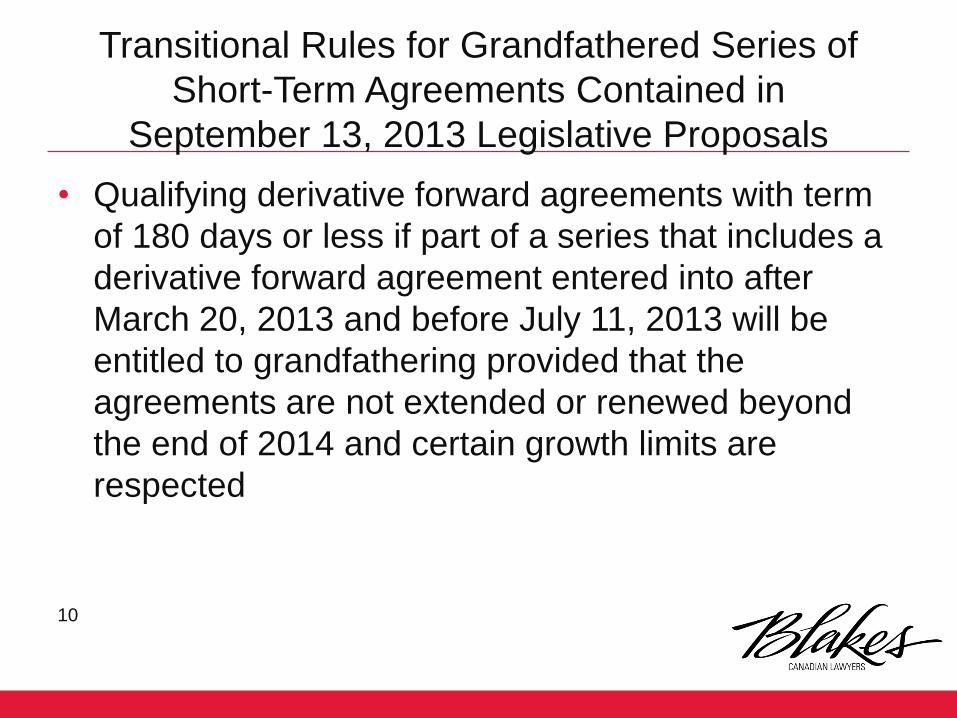

Transitional Rules for Grandfathered Series of

Short-Term Agreements Contained in

September 13, 2013 Legislative Proposals

• Qualifying derivative forward agreements with term

of 180 days or less if part of a series that includes a

derivative forward agreement entered into after

March 20, 2013 and before July 11, 2013 will be

entitled to grandfathering provided that the

agreements are not extended or renewed beyond

the end of 2014 and certain growth limits are

respected

10

Transitional Rules for Grandfathered Series of

Short-Term Agreements Contained in

September 13, 2013 Legislative Proposals (cont’d)

• Pursuant to these growth limits, the notional amount of a

derivative forward agreement eligible for grandfathering

cannot exceed the total of the following: 1. its notional amount when the agreement is entered into;

2. the total increase in the notional amount that is attributable to the underlying interest;

3. the amount of cash that was held by the taxpayer immediately prior to March 21, 2013 that was

committed to be invested under the derivative forward agreement;

4. the total increase in the notional amount of the derivative forward agreement that is attributable to the final

settlement of a qualifying terminated derivative forward agreement;

5. certain other permitted increases in the notional amount;

less

6. any total decrease in the notional amount attributable to the underlying interest; and

7. the total of partial settlements to the extent that they are not reinvested

11

Transitional Rules for Grandfathered

Long-Term Agreement Contained in

September 13, 2013 Legislative Proposals

• A qualifying derivative forward agreement entered into

before March 21, 2013 will be entitled to grandfathering

until the earlier of the termination date of the agreement

and before March 22, 2018 provided that the agreement

is not extended or renewed beyond the end of 2014 and

certain growth limits are respected

• Grandfathering will be permitted if an agreement is

extended to a date before 2015

12

Transitional Rules for Grandfathered

Long-Term Agreement Contained in

September 13, 2013 Legislative Proposals (cont’d)

• Pursuant to these growth limits, the notional amount of a

derivative forward agreement eligible for grandfathering

cannot exceed the total of the following: 1. its notional amount prior to March 21, 2013;

2. the total increase in the notional amount that is attributable to the underlying interest;

3. the amount of cash that was held by the taxpayer immediately prior to March 21, 2013 that was

committed to be invested under the derivative forward agreement;

4. the total increase in the notional amount of the derivative forward agreement as a consequence of the

exercise of an over-allotment option granted to March 21, 2013;

5. the total increase in the notional amount of a derivative forward agreement that is attributable to the final

settlement of a qualifying terminated derivative forward agreement;

6. certain other increases in the notional amount up to the lesser of 5% and total increases in the notional

amount after March 20, 2013 and before July 11, 2013;

less

6. any total decrease in the notional amount after March 20, 2013 attributable to the underlying interest; and

7. partial settlements after March 20, 2013 to the extent that they are not reinvested

13

Transitional Rules in September 13, 2013

Legislative Proposals

• One of the provisions included in the transitional rules is

intended to provide relief where a derivative forward

agreement is terminated, but another increased in notional

amount by no more than that of the terminated agreement

• This will allow grandfathering to continue to be available

where there is a merger of investment funds

• The term of the surviving derivative forward agreement cannot

exceed the term of the terminated derivative forward

agreement

14

Practical Implications

• Explanatory Notes accompanying the

September 13, 2013 Legislative Proposals

include a number of examples – a sale of property pursuant to a covered call option should

not, in and of itself, be a derivative forward agreement

– a sale of property pursuant to a put/call strategy could be a

derivative forward agreement

– exchangeable shares with an embedded exchange right

should not be caught

15

Practical Implications

• What are the implications for fixed forward

price contracts?

• What are the implications for currency

forward purchase and sale transactions?

16

Synthetic Disposition

Arrangement Proposal • The synthetic disposition arrangement proposal is aimed

at transactions that allow a taxpayer to defer the tax from

disposing of property by entering into transactions that

would put the taxpayer in the same economic position as

if it had sold a property with an accrued gain while

retaining ownership for tax purposes until a later date

• The new measures will deem a taxpayer to have

disposed of the property at fair market value at the time it

enters into a “synthetic disposition arrangement”

17

Synthetic Disposition

Arrangement Proposal (cont’d)

• A “synthetic disposition arrangement” is defined as one or more

agreements or other arrangements that (a) have the effect of

eliminating “all or substantially all” of the taxpayer’s risk of loss and

opportunity for gain or profit in respect of the property for more than

one year; and (b) do not otherwise result in a disposition of the

property within one year

• The explanatory notes that accompanied the budget proposal stated

that the rule is intended to apply to a wide range of monetization

structures, including forward sales, put-call collars, exchangeable

debt transactions, total return swaps, and securities borrowing

transactions used to facilitate a short sale of property that is

economically similar to the property of the taxpayer

18

Synthetic Disposition

Arrangement Proposal (cont’d)

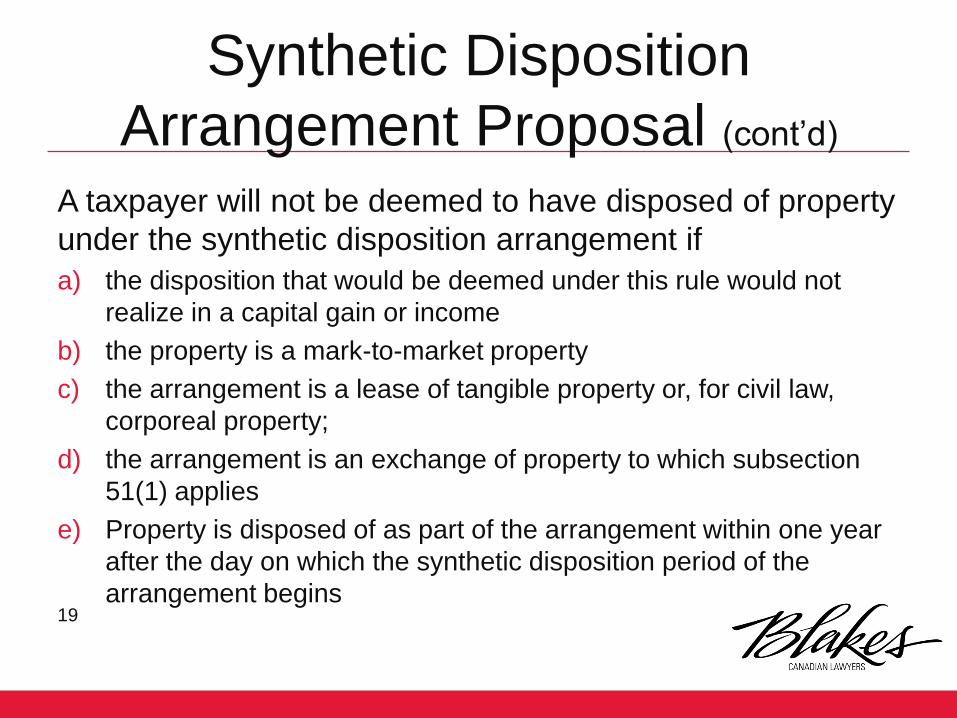

A taxpayer will not be deemed to have disposed of property

under the synthetic disposition arrangement if

a) the disposition that would be deemed under this rule would not

realize in a capital gain or income

b) the property is a mark-to-market property

c) the arrangement is a lease of tangible property or, for civil law,

corporeal property;

d) the arrangement is an exchange of property to which subsection

51(1) applies

e) Property is disposed of as part of the arrangement within one year

after the day on which the synthetic disposition period of the

arrangement begins 19

Synthetic Disposition

Arrangement Proposal (cont’d)

• The notes accompanying the September 13, 2013 legislative

proposals provide a number of examples of transactions that would

or would not be considered to be subject to the synthetic disposition

arrangement proposal

• The following are included as transactions that would be considered

to be subject to the synthetic disposition proposal:

– put-call arrangements where all or substantially all of the risk of loss and

opportunity for gain has been given up

– sale of a very deep in the money call option

– a secured loan where the loan was in an amount approximately equal to the

value of the property provided as security and both the lender and borrower had

a right to settle the loan with the property

– the entering of a total return swap where the taxpayer owns the reference share

20

Synthetic Disposition

Arrangement Proposal (cont’d)

• The following are included in the notes accompanying the

September 13, 2013 legislative proposals as examples of

transactions that would not be considered to be subject to the

synthetic disposition arrangement proposal

– a put-call arrangement where the strike price on the call option was significantly

higher than the current value of the property and the strike price on the put

option was significantly less than the value of the property

– a loan which is simply secured by property, even if the borrower has the right to

settle the loan with the property

– a sale of property for a fixed price, but subject to the purchaser obtaining

regulatory approval

– a swap whereby the owner of the property only pays an amount equal to

dividends on the reference share and not changes in price

21

Synthetic Disposition

Arrangement Proposal (cont’d)

• In the budget documents, it was stated that the rule is not

intended to apply to “ordinary hedging” which the Department

of Finance seems to view as dealing only with potential risk of

loss

• The provision also does not require that the taxpayer actually

received a loan or was otherwise put into funds

• The new rules will apply to transactions entered into on or

after March 21, 2013 and also to existing agreements that are

extended on or after March 21, 2013 as if the agreement was

entered into at the time that it was extended

22

Example: Monetization

23

• Inception of Transaction

• The financial product provider has agreed to purchase the reference shares from the client at a point in the future for the forward price

• The financial product provider also makes a loan to the client with the same term as the forward

• Shares are pledged to the financial product provider as security for the transactions

Securities

Lender

Financial

Product

Provider

Client

Borrowing

of Shares

Market

Sale of share and

investment of sales

proceeds

Loan

Forward purchase

contract

on reference share

Example: Monetization

24

• Conclusion of Transaction

• The financial product provider’s payment obligation under the forward contract is generally set off against the client’s obligation to repay the loan

• The share purchased by the financial product provider is used to close out the securities borrowing transaction

Securities

Lender

Financial

Product

Provider

Client

Return of

Shares

Payment of forward purchase price

(generally applied to repay the loan

owed by the client)

Sale of share pursuant to forward

Repayment of Loan

Practical Implications

• An inherent level of uncertainty will be involved in

determining whether the taxpayer has eliminated “all or

substantially all” of the risk of loss and opportunity for gain

or profit

• CRA generally interprets “all or substantially all” as

meaning 90% or more

• Case law, however, has taken an approach which requires

that the particular facts and circumstances be considered

and has contemplated a lower threshold (see Wood v.

MNR, 87 DTC 312 and McDonald v. The Queen, 98 DTC

2151)

25

Synthetic Disposition Arrangement –

Application to “Dividend Stop-Loss Rules”

• Generally, the Income Tax Act (Canada) includes rules

that deny a corporation the ability to claim losses on the

disposition of a share of a Canadian corporation to the

extent that such corporation has received dividends on

the share that qualified for the inter-corporate dividend

deduction

• An exception to the rule is available if the share has

been owned for at least 365 days (and no more than 5%

of the class of shares were owned by the taxpayer and

non-arm’s length persons)

26

Synthetic Disposition Arrangement –

Application to “Dividend Stop-Loss Rules” (cont’d)

• The synthetic disposition arrangement definition (with the one year

threshold replaced by a 30-day threshold) will apply for purposes of

the dividend stop-loss rule

• Where this rule applies, for purposes of the 365-day ownership

requirement threshold, the taxpayer will be deemed not to own the

share during the “synthetic disposition period”

• This rule will not apply where the taxpayer owned the relevant

property throughout the 365-day period preceding the synthetic

disposition period

• Not clear which shares are affected where the taxpayer owns more

than what are subject to the synthetic disposition arrangement

27

Synthetic Disposition Arrangement –

Application to “Dividend Stop-Loss Rules” (cont’d)

• A corresponding rule will apply in the context of claiming

foreign tax credits for non-Canadian taxes on foreign

securities held for less than a year

• These proposals will have wide-ranging implications

• For example, the rule would apply to an equity derivative

transaction where a taxpayer hedges its obligations by

purchasing the underlying shares or securities

• Would the rule apply where the “hedge” is entered into

prior to the relevant shares having been acquired?

28