Embed Size (px)

Citation preview

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 1 —

RECENT AMENDMENTS UNDERBST, CST AND ALLIED ACTS

Ms. Rupa GamiChartered Accountant

Para No. Chapter No., Subject / Topic of the Amendment Page Nos.

Introduction……………………………………………………………………… ...................... 1

Chapter-I

1 to 18 AMENDMENTS TO THE BOMBAY SALES TAX ACT, 1959 ...................................... 3-18

19 to 20 AMENDMENTS TO SCHEDULE ENTRIES ................................................................. 18-19

Chapter-II

AMENDMENTS TO BOMBAY SALES TAX, RULES

21 to 27 The Bombay Sales Tax (Third Amendment) Rules, 2004 dated 30th July, 2004 ... 20-25

28 to 30 The Bombay Sales Tax (Fourth Amendment) Rules, 2003 dated 31st March, 2003 ... 25

Chapter-III

Notifications ........................................................................................................................ 26

Chapter-IV

AMENDMENTS TO THE CENTRAL SALES TAX ACT, 1956

31 to 32 The Finance Act, 2003 .................................................................................................. 29-30

33 to 38 The Finance Act, 2004 .................................................................................................. 30-32

39 The Central Sales Tax (Registration and Turnover) Amendment Rules, 2003 ............ 32

40 AMENDMENTS RELATING TOSPECIAL ECONOMIC ZONE UNDER BST ACT, 1959 ................................................... 32

Chapter-V

41 to 42 Amendments to Maharashtra State Tax on Right to Use Act, 1985 ............................ 33

Chapter-VI

43 to 45 Amendments to the Maharashtra Sales Tax on transfer of propertyin goods involved in the execution of Works Contract (Re-enacted) Act, 1989 ........ 34

Chapter-VII

46 to 50 AMENDMENTS TO MAHARASHTRA TAX ON LUXURIES ACT, 1987 ...................... 35

Chapter-VIII

51 to 54 AMENDMENTS TO PROFESSION TAX ACT, 1975 .................................................. 36-37

Conclusion ........................................................................................................................... 37

Annexures ............................................................................................................................ 39

INDEX

10th Non Residential Refresher Course

— 2 —

INTRODUCTION

The story of mankind is punctuated by progress and retrogression. Empires have risen andcrashed into the dust of history. Civilizations have flourished, reached their peak and passed away.

The law exists to serve the needs of the society, which is governed by it. If the law is to playits allotted role of serving the needs of the society, it must reflect the ideas and ideologies of thatsociety. It must keep time with the heartbeats of the society and with the needs and aspirations of thepeople. As the society changes, the law cannot remain immutable. The early nineteenth centuryessayist and wit Sydney Smith, said: “When I hear any man talk of an unalterable law, I amconvinced that he is an unalterable fool.” The law must, therefore, in a changing society march intune with the changed ideas and ideologies.

The life of the law has not been logic: it has been experience. The felt necessities of the time,the prevalent moral and political theories, intuitions of public policy, avowed or unconscious, eventhe prejudices which judges share with their fellowmen, have had a good deal more to do than thesyllogism in determining the rules by which men should be governed. The law embodies the story ofa nation’s development through many centuries, and it cannot be dealt with as if it contained onlythe axioms and corollaries of a book of mathematics. In order to know what it is, we must know whatit has been, and what it tends to become. We must alternately consult history and existing theoriesof legislation. But the most difficult labour will be to understand the combination of the two into newproducts at every stage. The substance of the law at any given time pretty nearly corresponds, so faras it goes, with what is then understood to be convenient; but its form and machinery, and the degreeto which it is able to work out desired results, depend very much upon its past.

Before I advert to the actual provisions of law as amended, it is quite apt and appropriate thatwith a view to find out the real object, intent and purpose for which the amendment is so made, itbecomes imperative to look to the rules of interpretation or construction of law such as to cite aninstance, the one popularly known in the legal parlance as “ rule in Heydon’s case”.

The rule which is also known as ‘purposive construction or ‘mischief rule’, enablesconsideration of four matters in construing an Act:

(i) What was the law before the making of the Act,

(ii) What was the mischief or defect for which the law did not provide,

(iii) What is the remedy that the Act has provided, and

(iv) What is the reason of the remedy?

The rule then directs that the courts must adopt that construction which ‘shall suppress themischief and advance the remedy’. The rule has been explained in the Bengal Immunity Co. vs. Stateof Bihar, 6 STC 446 (SC).

Such rules of interpretation for the use to be made by the readers are given in the Annexurehereto with a view to avoid verbosity in the Paper.

While dealing with the subject proper, as to ‘Recent Amendments in the BST Act, CST Act &other Allied Laws’, it is quite imperative to look to the speech of Honourable the Finance Minister,Mr. Jayant Patil delivered on 27-5-2004 while laying the budget before the House. He has referred tothe tax policy, its objectives and the ultimate goal to be achieved through his finance proposals. Theproposals revolve around the philosophy that moderate tax rates not only improve thecompetitiveness of manufacturing in the state by reducing costs but also encourage growth in

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 3 —

consumption by reducing prices. The twin objectives are to generate an employment and increase therevenue receipts and improve finances. The economic laws of the fiscal policy should attempt torationalize the tax structure and rate, and simplify the procedure, to reduce both the transaction timeand transaction costs which has a direct bearing on productivity and competitiveness.

Thus ‘Recent Amendments’ that I have dealt with in this Paper requires to be tested on theabove objectives and the fiscal policy so laid down.

The paper to be discussed today is fraught with a number of major amendments that wouldaffect the fiscal revenue of the State on one hand and the business of the dealer on the other hand.

Further, the relevancy of the amendments has to be considered in the background of VAT Actwhich is likely to get the Presidential assent in the near future and come into force w.e.f. April 2005.

In today’s paper, I shall be initially dealing with the Maharashtra Act No. XIII of 2004 whichreceived the assent of the Governor in the “Maharashtra Government Gazette” on 29th June, 2004.The other amendments would be dealt with later.

The L.A. Bill No. XXI of 2004 dated 7-6-2004 along with errata dated 9-6-2004 to amendcertain tax laws in operation in the State of Maharashtra was placed before the Assembly on 9th June,2004. The Amending Act is called the ‘Maharashtra Laws (Levy, Amendment and Validation) Act,2004.

The paper today would cover amendments to BST Act, Rules, Notifications, CST Act and otherAllied laws.

CHAPTER - I

IMPORTANT AMENDMENTS TO THE BST ACT, 1959 BYMAHARASHTRA ACT NO. XIII OF 2004

The amendments to Section 1 relating to short title and Section 25 relating to lotteries cameinto effect on the date of publication of the Act in the Official Gazette. The remaining amendmentsto sections came into force with effect from 1st July, 2004.

1. Amendments to Section 2 — Definitions

1.1 Clause (11) Explanation Para (ii) — An auctioneer as a Deemed Dealer

1.1.1 Section 2(11) defines a dealer and the Explanation thereto was added by MaharashtraAct 24 of 1985 w.e.f 16-8-1985 to provide for a deeming fiction specifying certainpersons as deemed dealers.

Explanation Para (ii) was inserted by Maharashtra Act No.9 of 1988 w.e.f. 22-4-1988by which the “auctioneer” was deemed to be a dealer. This explanation explicitlyincluded the auctioneer under the term ‘dealer’ although earlier he was hithertoimplicitly covered. The new amendment was required in light of the judgment of theHon’ble Tribunal in the case of M/s Ashwin & Co. (Appeal No. 35 of 1994 decided on25-1-2002) where it was held that an auctioneer who merely organises an auction, nothaving possession of the goods and there being no transfer of property in goods by wayof a sale as so construed in law, would not render himself liable to tax as a deemeddealer under Explanation Para (ii) to Section 2(11).

10th Non Residential Refresher Course

— 4 —

The scope of the amendment is widened by addition of the words, ’whether acting as

an agent or otherwise’ and merely by organising the sale of goods or conducting the

auction of goods for which either he has an authority or not to sell the goods, he

becomes a deemed dealer.

In my view, even the expanded definition may not render an auctioneer liable as a

dealer while looking to the liabilities arising under the civil law as to the defaults, if

any, that the party to the auction commits in performing the mutual obligations arising

under the auction.

The Bombay High Court in 97 STC 55 in case of Varun Polymol Organics Ltd. vs. State

of Maharashtra has held that it is not open to the State Legislature to enact a legislation

to the effect that a particular transaction shall be deemed to be a sale even though it

cannot actually be a sale if by creating the said fiction it transgresses its legislative

jurisdiction. The power of the State Legislature to enact a law for levy of sales tax or

purchase tax is restricted to Article 246(3) of the Constitution read with entry 54 in List

II of the Seventh Schedule thereto. The expression ‘sale’ used in entry 54 in List II

must be interpreted so as to be applicable only to transactions where there is transfer of

property in goods by one party to another for consideration.

An auctioneer is more a service provider than a seller. Honourable the Supreme Court

in 9 STC 353 in the case of Gannon Dunkerley has specifically observed that a sale is

to be understood in terms of Sale of Goods Act, 1930 for the purpose of levy of sales

tax. Thus the deeming provision of treating the mere disposal of goods by an auctioneer

as a sale as per clause (b)(i) of Explanation to Section 2(28), thereby treating every

disposal of goods referred to in the Explanation to clause (11) as a deemed sale may not

be constitutionally valid.

1.1.2 Consequential amendments have been made by insertion of sub-sections (3) and (4) to

Section 16 with a view to fix the liability of the auctioneer to pay tax, on such sale;

i.e., on mere disposal of goods as referred to in clause (11) to section 2 by considering

the same to be a deemed sale. The liability so discharged by the auctioneer relieves the

principal on the principles of joint and several tax liability.

1.1.3 Poser: Whether even after the amendment of section 2(11) read with section 16(3) an

auctioneer can be held liable to pay tax as a dealer under the BST Act, 1959?

1.1.4. Poser: Whether the state legislature has competence to levy tax by considering the

disposal of goods by an auctioneer as a deemed sale as understood in law as per sec. 2

(28), explanation there under?

1.2 Clause12B — Eligibility Certificate

By an amendment to this section, two new agencies have been added for the grant of eligibility

certificates under the package scheme of incentives by way of exemption or deferral of

payment of tax liability. These are Maharashtra Energy Development Agency effective from

24-8-1998 to implement Wind Mill Power Generation Scheme and Directorate of Industries

effective from 26-2-2003.

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 5 —

2. Sections 3(4) — Incidence of Tax

2.1 Sales Tax is a tax on sale which is levied on a dealer. Section 3(4) is a charging section whichclassifies the dealers into three categories so far as their liability arises under the provisions ofthe BST Act, 1959. They are:

1) Importer, 2) Manufacturer,3) Reseller and others.

The Amending Act, 2004 has added one more category that of Liquor Vendor and increasedthe limit of turnover in case of resellers from Rs. 2.5 lacs to Rs. 5 lacs for the purpose of attracting taxliability. The limits of turnover prescribed for attracting tax liability, before amendment and afteramendment, are as follows:

CATEGORY BEFORE AMENDMENT AFTER AMENDMENT

(1) (2) (3)

Importer 1. Total turnover limit Rs. 100000/- 1. As per Column (2).

2. Value of taxable goods sold or 2. As per Column (2)purchased by him is not less thanRs.10000/-.

3. Value of goods, taxable or not, 3. Value of goods whetherbrought into the State or despatched taxable or not, brought by himto him from outside the State is not into the State or despatched toless than Rs.10000/-. him from outside the State is

not less than Rs.25000/-.

Manufacturer 1. Total turnover limit Rs. 100000/- 1. As per Column (2)

2. Value of taxable goods sold or 2. As per Column (2)purchased is not less than Rs.10000/-

3. Value of goods, taxable or not, 3. Value of goods, taxable or not,manufactured during the year is not less manufactured during the year isthan Rs. 10000/-. not less than Rs. 25000/-.

Liquor As per ‘Resellers’ given below 1. Total turnover limitDealer Rs. 250000/-.

2. It applies to a dealer whoholds liquor vendor licence inForm FL-I, FL-II, FL-III or FL-IVunder the Bombay ForeignLiquor Rules, 1953 or Licence inForm E under the SpecialPermits & Licence Rules, 1952or Licence in Form CL-II, CL-IIIor CL/FL/TOD/III theMaharashtra Country LiquorRules, 1973.

Resellers 1. Total turnover limit Rs. 250000/- 1. Total turnover limit Rs 500000/-& Others 2. Value of taxable goods sold or 2. As per Column (2)

purchased during the year is not lessthan Rs. 10000/-.

10th Non Residential Refresher Course

— 6 —

The dealer whose turnover of sales or purchases exceeds the above limits shall have to applyfor registration under the BST Act within 30 days. However, with the threshold limit of turnoverbeing increased to Rs. 5 lacs for resellers and other dealers, a number of small dealers would comeout of the purview of BST Act. They would be saved of the various hassles involved in complyingwith the Sales Tax provisions. The Department, too, would benefit since it would reduce the paperwork as well as time involved in catering to small dealers who do not contribute much to therevenue. This is with a view to be in consonance with the objectives as outlined by the FinanceMinister.

This also will be consistent with the provisions made in the Value Added Tax Act, 2002where the threshold limit is provided at Rs. 10 lacs.

2.2 Poser: Where the turnover of a dealer who is a reseller exceeds Rs. 2.5 lacs on 20th June,2004, whether he would be liable for registration?

3. SECTION 7 — Levy of Sales Tax on (Schedule B) Declared Goods

3.1 The amendment deletes the words “other than those covered by Schedule Entry B-6" underSection 7 w.e.f. 1-5-2003. This is in accordance with VAT on Iron and Steel being withdrawnw.e.f. 1-5-2003. This would result in all resale of declared goods including Iron and Steelbeing allowed as a deduction under section 7. The earlier exemption provided underthe notification entry Group A-154 need not be resorted to.

3.2 Earlier, VAT had been introduced on Iron & Steel w.e.f. 1-10-2002 consequent to theamendment made to clause (a) of Section 15 of the Central Sales Tax Act, 1956 by the FinanceAct, 2002 (20 of 2002) dated 11-5-2002.

Section 15(a) is to the effect that every sales tax law of a State in respect of tax on sale ofdeclared goods shall be subject to two conditions:

(i) the tax payable under such law shall not exceed 4%, and

(ii) that the tax would not be levied at more than one stage.

By the Finance Act, 2002, the second condition regarding single point levy on declared goodshad been withdrawn w.e.f. 11-5-2002 and as a result the State of Maharashtra had exercisedthe power to levy value added tax on Iron and Steel w.e.f. 1-10-2002.

3.3 However, it is apprehended that since the present amendment has been made withretrospective effect from 1-5-2003, dealers who had already paid VAT on Iron and Steel for theperiod 1-5-2003 upto 30-6-2003 following the concession granted by the Commissioner ofSales vide Trade Circular No 17T dated 10th July, 2003, instead of claiming resale would be atthe loser’s end since the sales tax collected by them would be forfeited on the one hand andthe set off claim on purchases under Rule 42M or reduction in sales price under Rule 46Cwould not be allowed on the other hand.

However, in view of clarification issued vide Trade Circular No 11T dated 8th July, 2004, thebenefit of VAT would be available up to 30-6-2004 and there should not be forfeiture of tax ordenial of set off up to 30-6-2004.

4. SECTION 9 — Levy of Turnover Tax on Schedule C goods

4.1 Under Section 9 turnover tax is levied on turnover of sales of Schedule C goods at 1% w.e.f.1-4-1999, and w.e.f. 1-5-2002, when the tax liability exceeds 1 crore either in the previous year

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 7 —

or in the current year, turnover tax is levied at 1.5%. The Explanation to Section 9 defines taxliability as sales tax and purchase tax ‘leviable’ without adjustment of set off, drawback orrefund. The Explanation has been amended whereby the term tax liability would now meansales tax and purchase tax ‘payable’. This amendment would be effective from 1-5-2002. Theamendment is clarificatory in nature and has been made to provide for determination of therate of turnover tax on the basis of the tax payable before adjustment of set off.

4.2 As for instance, the rate of tax on sports goods as provided in Schedule Entry C-II-54 is 8% onthe basis of tax ‘leviable’ whereas by notification u/s 41, the tax ‘payable’ is reduced to 4% asper entry 71 of Group A and hence the amendment.

5. SECTION 13AA — Purchase Tax payable on Schedule C-I goods

5.1 Section 13AA provides for levy of additional purchase tax at the rate of 2 % in addition tothe sales tax or purchase tax leviable in case of Schedule C-I goods. The tax is so levied whengoods are purchased locally and used by the dealer in the manufacturing of taxable goodswhich are despatched by him to his branch or agent at a place situated outside the statewithin India.

Under the amendment, a proviso has been added whereby no purchase tax shall be leviedunder this section w.e.f. 1-7-2004.

5.2 Poser: Whether in case of goods manufactured by a dealer prior to 30-6-2004 and despatchedby him to his branch or agent outside the state after 1-7-2004 would attract the purchase taxliability under Section 13AA?

5.3 It has been clarified by the Commissioner vide Circular No. 11T dated 8th July, 2004 thatwhere a dealer purchases goods on or before 30-6-2004 and after manufacturing sends thefinished goods to his branch outside the state on or after 1-7-2004, purchase tax u/s. 13AAwould be attracted.

5.4 In keeping with the objective of providing employment and generating wealth, as laid out bythe Finance Minister in his budget speech certain benefits have been granted to themanufacturers under the set off rules. The tax on raw materials is an element of cost. Toreduce the costs, the retention percentage under Rule 41D in case of branch transfers, has beenreduced from 6% to 3% under the amending Act and therefore an amendment has beennecessitated in this section also.

5.5 In case of Hotel Balaji and Others vs. State of Andhra Pradesh 88 STC 98 (SC) it has been heldthat Section 13AA is intended to encourage the industry and at the same time derive revenue.The tax imposed by this section is a purchase tax levied on the purchase price of rawmaterials purchased by a manufacturer and that it is well settled that taxing power can beutilized to encourage commerce and industry. It can also be used to serve the interests ofeconomy and promote social and economic planning.

5.6 The amendment so made is with a view to serve the interests of economy and promote socialand economic planning.

6. SECTION 14 — Purchase Tax payable on contravention of the terms of declaration

6.1 An amendment to second proviso to Section 14(1) has been made whereby set off ofpurchase tax paid under both sections 13A or 13AA would now be available againstpurchase tax payable under Section 14. Earlier the proviso provided only for set off ofpurchase tax paid u/s. 13A. The inadvertent mistake of non-provision of set off of purchase taxunder Section 13AA is set right by this amendment.

10th Non Residential Refresher Course

— 8 —

6.2 This is done with the purpose of bringing on par such a dealer with other manufacturers. The

amendment is retrospective and takes effect from 1st October, 1995. Earlier these dealers were

carrying additional burden of 2% purchase tax due to non-availability of consequential set off.

A beneficial provision in the form of amendment to Section 14, second proviso thereto,

the set off of the purchase tax paid or payable under Section 13AA will now be allowed

along with the set off of the purchase tax under Section 13A.

6.3 Under the unamended provision, the proviso to sub-section (1) provides that where a dealer is

holding an entitlement certificate and he purchases Schedule C-I goods on Form 15-EC and

uses them in the manufacture of goods which are despatched by him to his branch or agent

outside the State, purchase tax at the rate of 6% is payable.

Although there has been an amendment to Rule 41D for reduction of retention, there has been

no corresponding amendment to Section 14 to reduce the rate of tax from 6% to 3% in order

to equal the new retention rate under the amended set off rules. This amendment remains to

be carried out.

7. Section 15-1A — Levy of surcharge

The levy of surcharge under Section 15-1A during the period 31-3-1999 to 31-3-2001 has been

amended so as to make it applicable only in respect of periods commencing from 1-4-1999. In

view of the introduction of this Section from 5.00 PM on 31-3-1999 there had been some

controversy regarding levy of surcharge even for the F.Y. 1998-99. This amendment has been

made to enforce levy only with effect from 1-4-1999.

8. Section 22 — Registration

8.1 A number of amendments have been made to the section whereby registration of a dealer has

become a complex issue. A number of circulars have been issued to explain the amendments

or clarify the same which too, has resulted in a number of controversies.

8.2 Any dealer liable to tax under Section 3 or Section 19(6) shall have to get himself registered.

Further Section 22(3) has been amended whereby the Government can now prescribe

conditions to be fulfilled by the dealer before granting of the Registration Certificate.

8.3 Rule 7 — Application for registration by dealers liable to tax

8.3.1 The conditions have been prescribed under the amended Rule 7 of the BST Rules,

1959. Under the first proviso to sub-rule 3 the dealer is required to make a separate

application for registration for the place of business for which he has obtained a

certificate of entitlement under the Package Scheme of Incentives. Exception has been

provided to Package Scheme of Incentive Units under 1998 Power Generation Policy

where no such separate certificate is required.

8.3.2 Under sub-rule 7 renumbered as Clause (a), the furnishing of Permanent Account

Number, if any, in the application for registration has become necessary in the case of

individuals, each of the partners of the firm, members of HUF and members of the

managing committee of unincorporated association and of persons having any interest

in the business. Form 1 has been amended accordingly. This is with respect to

individuals / entity becoming liable for compulsory registration on exceeding the

threshold limits prescribed under section 3(4) of the Act.

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 9 —

8.3.3 Another clause (b) has been inserted under sub-rule 7 whereby a dealer applying for

voluntary registration after 1-7-2004 shall have to obtain Permanent Account Number

before making the application. He will also have to furnish a proof of current bank

account and will have to be introduced either by a registered dealer continuously

registered for the last five years or an advocate, Tax Practitioner, Chartered Accountant

or a Cost Accountant.

8.3.4 Accordingly Rule 17 has been amended by adding sub-rule 4 whereby the dealer who

is registered on or before 1-7-2004 should furnish his PAN No. in Form N-13-1 before

29-8-2004. For dealers applying for registration after 1-7-2004 the PAN Number has to

be furnished at the time of application for registration. For those dealers whose

certificate is in force on 1-7-2004 and who do not have a PAN Number, they have to

inform the same within 15 days of obtaining the number.

8.4.1 Sub-section (8) Automatic cancellation of Registration with effect from 1-7-2004

A new sub-section (8) is inserted whereby all dealers whose Registration Certificates are

in force on 31-3-2004 and 30-6-2004 would automatically be liable for cancellation

w.e.f. 1-7-2004 unless.

1. the dealer is a manufacturer or an importer during the period 2003-04,

2. he holds liquor vendor licence at any time during the period 2003-2004.

3. he holds an authorization or permit or any other certificate under any entry of

notification u/s. 41 at any time during 2003-04.

4. the dealer falls under Explanation to Section 2(11) as deemed dealer.

5. the turnover of the dealer exceeds the prescribed limits of Rs. 5 lacs during the

period 2003-2004.

This procedural section creates a number of anomalies since cancellation of

Registration Certificate is based on the dealer’s position during the period 2003-04.

Practical difficulties are encountered by dealer whose Registration Certificate gets

cancelled automatically and whose turnover exceeds the limits during the period

1-4-2004 to 30.6.2004 since he would have to apply for registration once again.

8.4.2 While considering the issue of automatic cancellation of Registration Certificate, the

question of levy of purchase tax on the stocks held on that date is provided for by

amending Section 15(2) of the principal Act. Thus the purchase tax will be levied on

the stock of taxable goods purchased against declarations under Section 11 or 12 of the

Act, treating the same as contravention liable to levy of purchase tax u/s. 14.

8.4.3 Poser: Whether in case of a dealer liable to pay tax under Section 4 of the BST Act,

1959, on his registration certificate under the BST Act being automatically cancelled

under section 22(8) w.e.f. 1.7.2004, does he become liable to tax on other local

purchases after 1-7-2004 as a deemed registered dealer?

8.4.4 Poser: Where a dealer is having a place of business in a Special Economic Zone with a

turnover exceeding 5 lacs and also a place outside SEZ with turnover not exceeding the

threshold limits, then whether his registration certificate for the outside SEZ unit isliable for automatic cancellation?

10th Non Residential Refresher Course

— 10 —

8.4.5 The automatic cancellation of registration certificate as provided under Section 22(8)(a)shall not affect the registration under the other laws viz., Central Sales Tax Act, WorksContract Act, Lease Tax Act, etc. The registration under the other laws would begoverned by those laws.

8.4.6 A number of administrative concessions have been granted by issue of trade circularswhich are as specified hereunder:

8.4.7 In case of a dealer whose registration certificate is cancelled but whose turnover hasexceeded the limit of Rs. 500000/- in the period 1-4-2004 to 30-6-2004, the dealerwould have to apply in Form 1 to the registration authority. In such a case the newregistration certificate number will bear the same number and will be issued with effectfrom 1-7-2004. (Trade Circular 18T dated 19-8-2004).

8.4.8 In the case of a dealer who has obtained new registration certificate during the year2003-2004, either under Section 19(6) or on account of shifting of place of business, theturnover of the full financial year 2003-2004 would be considered for determiningwhether the dealer’s turnover has exceeded Rs. 5 lacs or not for the purposes of Section22(8). (Trade Circular 18T dated 19-8-2004)

8.4.9 Certain concessions are available to dealers whose registration certificates are cancelledunder Section 22(8) and who have applied for registration afresh under Section 22(2A)on or before 30th October, 2004. These are:

(i) The new registration number would bear the number of the certificate held bythem on 30th June 2004.

(ii) The date of effect of the new registration certificate would be 1st July, 2004.

(iii) A dealer who was granted voluntary registration prior to 1st April, 2004 onpayment of a deposit of Rs.5000/- will not have to make the payment onceagain. Even a dealer whose turnover exceeded the limits during the period 1stApril, 2004 to 30th June, 2004 will not have to pay the deposit amount.

(Trade Circular 25T dated 4-9-2004)

8.5 Clause (b) of sub-section (8) Surrender of Registration Certificate for defacing

Section 22(8)(b) requires the dealers whose registration certificate is automatically cancelled tosurrender their certificates to the assessing authority before 30-9-2004 for defacement by theauthority who shall deface the said certificate and its own copy and return the dealer’s copyduly defaced.

8.6 Clause (c) of sub-section (8) Filing of Special return

8.6.1 Section 22(8)(c) provides for filing of a special return in case of all dealers whoseregistration certificate is in force on 31-3-2004 as well as on 30-6-2004, in Form N-18D,including those dealers whose registration certificate is automatically cancelled underSection 22(8)(a). The return is to be filed within the extended time before 30thSeptember, 2004. If the return is not filed within the extended time, the registrationcertificate of the dealer would be liable to be cancelled w.e.f. 1-7-2004.

8.6.2 Clause (b) of sub-rule (4) of Rule 10 has been inserted to provide forsurrender of the copy of registration certificate to the assessing authority within 15days of the date of receipt of the order cancelling the registration certificate where thedealer has failed to file a special return. This is to give effect to cancellation ofregistration certificate under section 22(8)(c)(ii).

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 11 —

8.6.3 Poser: The extended date for filing of special return has been provided by theCommissioner’s Circular No. 17T dated 19-8-2004 to be 30th September, 2004. WhenSection 22(8)(c) specifically provides for filing of the special return on or before 31stJuly, 2004, whether the Commissioner of Sales Tax is justified in extending the date forfiling of such return as on or before 30-9-2004 ?

8.6.4 Poser: As a corollary to this, whether a dealer renders himself liable for any actionunder the law for any default committed by not filing the return during the extendedperiod from 1-8-2004 to 30-9-2004 ?

8.6.5 The above return is to be filed in addition to the annual return. This would result inunnecessary duplication of work for revenue and the assessee as the annual return isalready being filed and the same data would have to be provided in the special return.A very harsh measure of cancellation of registration certificate in case of non-filing ofsuch special return has been prescribed.

8.7 Sub rule (4) of Rule 22 — Filing of Annual Return

8.7.1 Under this rule, every dealer is required to file an annual return in Form N-18A, N-18Bor N-18C depending upon his tax liability, entitlement certificate etc. A proviso hasbeen added w.e.f. 1-7-2004 whereby a dealer whose annual turnover of sales orpurchases has exceeded Rs. 40 lacs shall have to attach Annex 1 to the annual return.For the purpose of computing the turnover of sales or purchases of Rs. 40 lacs, sales orpurchases of taxable as well as tax-free goods will have to be included.

8.7.2 Under Annexe 1, information in respect of purchases from suppliers in excess of Rs. 1lac during the year is to be provided with details of local and interstate purchases aswell as of highseas and other import purchases during the year. This requirement isapplicable for the period 2003-04 onwards.

8.7.3 Poser: In case of dealers who have filed their Annual Return before thisamendment, whether they will be required to submit Annexe 1 separately ?

8.8 Sub-rule (6) of Rule 22 - Form of Special Return

The rule has been added to provide for separate form for Special Return in Form N-18D asprescribed under section 22(8)(c).

9. SECTION 33 — Assessment

9.1 Section 33(4A) — Limit for time barring assessment

9.1.1 Section 33(4A) has been amended whereby assessments would become timebarred after the expiry of three years from the end of the year when all the returns(except annual return) are filed within one month from the end of the year. If, for anyreason, the order of assessment is not made within this period it shall be presumed thatthe returns are accepted as correct and complete. This provision would be effectivefrom 1-7-2004.

9.1.2 Under this amended section, for the purpose of period of limitation, the filing of annualreturn would be excluded. Whereas in case of M/s DGP Windsor (I) Ltd. vs. State of

Maharashtra, S.A. Nos 295 and 495 of 2003 decided on 31-1-2004, the annual return

was considered as the last return which if filed within the prescribed time was

considered for the period of limitation for the time barring assessment.

10th Non Residential Refresher Course

— 12 —

9.1.3 Where any single return whether monthly or quarterly is not filed within onemonth from the end of the year, the time barring period for completing theassessment shall not be three years but shall be eight years from the end of the year.

9.1.4 By virtue of the amendment by Maharashtra Act VIII of 2003, Section 33(4-1B) wasinserted whereby for returns relating to the period 1st April, 1999 to 31st March, 2003,the period of limitation for making assessment would be five years and not three years.Thus on reading Section 33(4A) with Section 33(4-1B) it could be inferred that theamendment under this section would apply for the period 2003-04 onwards.

9.1.5 Poser : Whether the amendment is a substantive amendment in which case it wouldapply prospectively; i.e., from the period 2004-2005 onwards or it is a proceduralamendment which would apply to the period 2003-04 onwards ?

9.1.6 Poser : Whether the amendment would apply to all pending assessments also, say, forperiod 2001-2002 ?

9.2 Section 33(6B) — Transaction wise assessment by the Enforcement Officer

9.2.1 Sub-section (6B) has been substituted w.e.f. 1-7-2004. The amended section providesfor deemed jurisdiction to the enforcement officer to assess the transaction related tosales or purchase or any claim or deduction during the course of proceedingsundertaken under Section 49. The earlier sub-section was operative from 6-2-1999.

9.2.2 Whereunder the search proceedings, if it is found that the dealer has evaded tax on anytransaction of sale or purchase or any claim or deduction has been wrongly made,the Enforcement Officer shall have the jurisdiction to assess the dealer in respectof only such transactions without the requirement of transfer of assessmentproceedings from the regular assessing authority to the Enforcement Officer asotherwise contemplated by Section 70 of the Act.

9.2.3 Such a transaction based assessment will be without prejudice to the assessmentproceedings under any other provisions of the Act, by any authority in respect of othertransactions. Once the tax has been assessed by the Enforcement Officer on aparticular transaction, it shall not be taxed again at the time of assessment of othertransactions under the other provisions of the Act.

9.2.4 The assessment shall be made after giving notice to such a dealer. Under Rule 32,sub-rule (2) is added which provides for notice of assessment to be issued in FormN-27-E. A minimum period of 15 days is required to be given in the notice forcompliance by the dealer.

9.2.5 Poser: Whether in a case where an action is taken under Section 49 by the STOEnforcement Branch before 1-7-2004 and the finding that the assessee has evaded orsought to evade tax on any transaction of purchase or sale is made after 1-7-2004,whether such an action for assessing the dealer under section 33(6B) without a TOPOrder u/s. 70 will be justified?

9.3 Section 33D — Cancellation of Assessment

9.3.1 Where a dealer is assessed ex parte for any period on account of his non-attendance atthe time of hearing when the assessment order is passed, the dealer can apply to theComissioner for cancellation of the assessment in Form N-30AA under Rule 36Awithin 30 days from the date of service of the order. The Commissioner shall, after

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 13 —

verification, cancel the order of assessment including any penalty and interest. Theorder for cancellation of the assessment order shall be in Form N-30-E as prescribedunder Rule 36B.

9.3.2 The section permits only one application to be made for a given assessment period. Thesection shall be applicable for the assessments made after 1-7-2004 for any period ofassessment, before or after the notified date of amendment.

9.3.3 The authority concerned shall have to make a fresh assessment order within a periodof 18 months from the date of service of the cancellation order.

9.3.4 It can be seen that although the time limit has been prescribed for applying forcancellation of the order, there is no limit prescribed for passing of the orderfor cancellation of the assessment by the concerned authority. Thus the section givesauthoritative powers to the officer to postpone the passing of order for cancellingof assessment indefinitely and thereby extending the time for passing of fresh orderof assessment. It is therefore required that the time limit for passing of cancellationorder be prescribed in the section or the rule. This will also help the authority tocomplete time barring assessments which may otherwise be prolonged

9.3.5 Again this would go against the Finance Minister’s objective as laid down in hisspeech, that of reducing time and costs involved in assessments being challenged inappeal and reducing the number of appeals and expediating the finalisation ofassessment.

9.3.6 While the dealer may apply for cancellation of assessment, it is preferred that he takesrecourse to filing of appeal to safeguard against the rejection of cancellation and non-availability of alternative remedy.

9.3.7 Further there is no provision in the amended section for stay of recovery of demandraised in the assessment. As a result, the officer can initiate recovery proceedingsdespite the fact that an application for cancellation of the assessment order has beenmade.

9.3.8 Poser: Whether pending the application for cancellation of assessment, the dealer canapply for stay of recovery before the AC/ DC (Adm) or the Additional Commissioner ofSales Tax?

9.3.9 Poser: Whether pending the application for cancellation of assessment, the assessee canfile the first appeal against the ex parte order and obtain the stay of demand?

10. Section 36 — Interest and Penalty provisions

10.1 Clause (3)(a) and Clause (3)(b) — Rate of interest

10.1.1 The interest is leviable under Section 36(3)(a) on late payment of dues as per the returnso filed by the dealer and under Section 36(3)(b) on differential dues on assessment @2% per month for the period of default. The rate of interest has now been reduced to1.25% per month w.e.f. 1-7-2004.

10.1.2 The lower rate would apply for defaults made or continued after 1-7-2004. Thus only

the period of default after 1-7-2004 would attract a lower rate although the default may

have been committed prior to 1-7-2004.

10th Non Residential Refresher Course

— 14 —

For instance if the tax due for March, 2004 was paid on 31-8-2004 interest would beleviable at 2% per month for the period 26-4-2004 to 30-6-2004 and at 1.25% permonth for the period 1-7-2004 to 31-8-2004.

10.1.3 The third proviso to Section 36(3)(b) is amended. The amendment clarifies that whena dealer has filed all the returns within one month from the end of the year (otherthan the annual return) he would get the benefit of non-levy of interest under thisproviso. This amendment would be effective from 1-4-2000.

10.1.4 In case of M/s Ador Fontech Limited vs. State of Maharashtra in S.A. No. 1780 of 2002decided on 31-3-2003, for Section 36(3) the ‘last return’ would cover only those returnswith which payment is required to be made and which is specifically provided withchallans. Since the annual return does not provide for payment of taxes but is only aconsolidation of all sales and purchases of the whole year, it would not be consideredfor the purpose of Section 36(3)(b).

10.2 Clauses 4A, 4B, 4C — Penalty Provisions

10.2.1 In place of existing sub-section 4A, three new sub-sections 4A, 4B and 4C have beenintroduced.

10.2.2 Sub-section (4A)

Under Section 22(8), a dealer who holds a valid Registration Certificate on 31-3-2004as well as on 30-6-2004 as well as those dealers whose Registration Certificates areautomatically cancelled on 1-7-2004 are required to file a special return. In case offailure to file such a return, penalty of Rs. 2000/- under sub-section (4A) wouldbecome leviable on the defaulting dealer.

10.2.3 Sub-section (4B)

Where the annual return is not filed by the prescribed date, penalty would be leviable undersub-section (4B) on the basis of the annual tax liability of the dealer which would be as follows:

Sr. No. Annual tax Liability Quantum of Penalty

1 does not exceed 20000/- 1500

2 exceeds 20000 but does not exceed 4 lakhs. 10000

3 exceeds 4 lakhs 25000

The expression ‘tax liability’ has been explained as:

(i) in case of a dealer holding eligibility certificate and a certificate of entitlement underthe notification issued under Section 41, the cumulative quantum of benefits in respectof that year.

(ii) In any other case, the total of all taxes payable for all places of business in the stateunder the CST Act and BST Act less the set off claimed by him.

10.2.4 Sub-section (4C)

If a dealer fails to file any return for any period, without sufficient cause, within theprescribed time, penalty under sub-section (4C) would be leviable at Rs. 2000/-. Thissub-section would be applicable where penalty under sub-sections (4A) and (4B) arenot applicable.

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 15 —

10.2.5 The only disturbing fact regarding imposition of the above penalties is that thequantum of penalty is fixed by law and the assessing officer has discretion to levyor not to levy the penalty and this may lead to unhealthy practices.

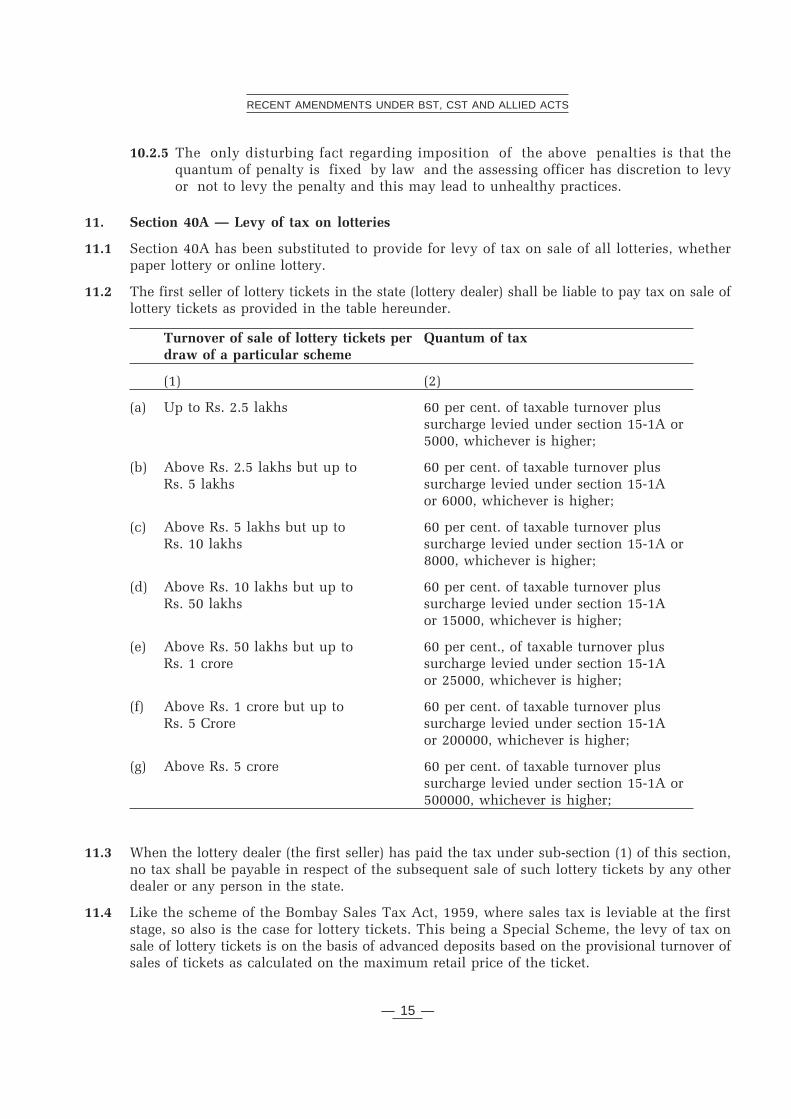

11. Section 40A — Levy of tax on lotteries

11.1 Section 40A has been substituted to provide for levy of tax on sale of all lotteries, whetherpaper lottery or online lottery.

11.2 The first seller of lottery tickets in the state (lottery dealer) shall be liable to pay tax on sale oflottery tickets as provided in the table hereunder.

Turnover of sale of lottery tickets per Quantum of taxdraw of a particular scheme

(1) (2)

(a) Up to Rs. 2.5 lakhs 60 per cent. of taxable turnover plussurcharge levied under section 15-1A or5000, whichever is higher;

(b) Above Rs. 2.5 lakhs but up to 60 per cent. of taxable turnover plusRs. 5 lakhs surcharge levied under section 15-1A

or 6000, whichever is higher;

(c) Above Rs. 5 lakhs but up to 60 per cent. of taxable turnover plusRs. 10 lakhs surcharge levied under section 15-1A or

8000, whichever is higher;

(d) Above Rs. 10 lakhs but up to 60 per cent. of taxable turnover plusRs. 50 lakhs surcharge levied under section 15-1A

or 15000, whichever is higher;

(e) Above Rs. 50 lakhs but up to 60 per cent., of taxable turnover plusRs. 1 crore surcharge levied under section 15-1A

or 25000, whichever is higher;

(f) Above Rs. 1 crore but up to 60 per cent. of taxable turnover plusRs. 5 Crore surcharge levied under section 15-1A

or 200000, whichever is higher;

(g) Above Rs. 5 crore 60 per cent. of taxable turnover plussurcharge levied under section 15-1A or500000, whichever is higher;

11.3 When the lottery dealer (the first seller) has paid the tax under sub-section (1) of this section,no tax shall be payable in respect of the subsequent sale of such lottery tickets by any otherdealer or any person in the state.

11.4 Like the scheme of the Bombay Sales Tax Act, 1959, where sales tax is leviable at the firststage, so also is the case for lottery tickets. This being a Special Scheme, the levy of tax onsale of lottery tickets is on the basis of advanced deposits based on the provisional turnover ofsales of tickets as calculated on the maximum retail price of the ticket.

10th Non Residential Refresher Course

— 16 —

11.5 The other amendments which relate to definitions, procedure for filing returns and penalprovisions are not detailed here.

12. Section 41-A1 — Refund of tax to certain class of dealers

12.1 Section 41-A1 has been introduced w.e.f. 1-7-2004 which gives powers to the Government togrant refund of tax in such exigencies arising in the public interest to any class or classes ofdealers or the persons as the case may be. This provision is contradistinguished with that ofsection 41 which provides for grant of exemptions by way of notification. This amendment ismade in light of the proposed VAT being introduced which may provide for such granting ofrefund when VAT is levied.

13. Section 42 — Set off of Entry Tax

13.1 An amendment is made in Section 42 whereby the State Government by rules is empoweredto grant set off or refund of tax paid or levied under the Maharashtra Tax on Entry of Goodsinto Local Areas Act, 2002 to a dealer. This amendment is made with retrospective effect from1-10-2002.

13.2 In case of Eurotex Industries and Exports Ltd. & Anr. vs. State of Maharashtra, 135 STC 25(Bom) it has been held that where the goods entering the local area from within the State donot bear sales tax, levy of entry tax on goods entering the local area from outside the Statewould be unconstitutional. The direct and immediate consequence of the levy of entry tax isthat for a manufacturer the cost of raw materials becomes cheaper within the state and costlierif purchased from outside the state.

13.3 The amendment so made would correct this defect.

14. Sections 43A and 44A — Interest on refund and delayed refunds.

14.1 The applicable rate of interest on refund was 12% p.a. and on delayed refunds was 9% p.a.The said rate has been reduced to 6% p.a. both on refunds and delayed refunds with effectfrom 1-7-2004.

14.2 As a result of the amendment, if refund is due, say, for the period 2003-04, then interest onrefund would be calculated under section 43A at 12% p.a. up to 30-6-2004 and at 6% p.a.from 1-7-2004 onwards.

15. Section 55 — Appeal provisions

15.1 Sub-section (7)(a) has been substituted to provide that the departmental appellate authorityshall have the power to confirm, reduce, enhance or annul the assessment. By thisamendment, the powers of the appellate authority to remand the assessment are withdrawn.This means that the appellate authority would have to pass the final order in appeal. Thesame does not apply in the case of the Tribunal and the Tribunal can remand the matter tothe assessing authority or the appellate authority to make a fresh order as per its directions.The amendment is effective from 1-7-2004.

15.2 Poser: The right of appeal being a substantive right vested in an assessee, arises on the dateof passing of the order. Then in such a case, where the order is passed on or before 1-7-2004and the appeal is filed thereafter, whether the appellate authority can exercise the power ofremand or not?

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 17 —

15.3 Poser: Where appeal has been filed before 1-7-2004, whether the appellate authority canexercise the power of remand or not ?

15.4 A second proviso is added to sub-section (7) after the first proviso to Section 55 wherebythe appellate authority other than the Tribunal have also been given powers to pass anorder in appeal even in such a case where a point has been decided by the Tribunalagainst the State or the Commissioner and against which further proceedings are initiatedbefore a higher forum. The appellate authority can pass an order notwithstanding that sucha point has been decided against the state but in that event the recovery proceedings for tax,penalty and interest, if any, shall be stayed, relating to the point in dispute, until the higherforum decides the issue, and thereafter modify the order when the higher forum decides theissue.

15.5 Under Sub-section (8) all the appellate authorities including the Tribunal have to decide theappeals on the basis of the priorities for hearing and disposal of cases prescribed underRules 61(3) and 61(4). Under these sub-rules.

(a) Every Appellate Authority and the Tribunal are required to maintain a register showingthe chronological order of filing of appeal and the quantum of relief sought.

(b) Every Appellate Authority and the Tribunal are required to fix dates of hearing of theappeals in such a way that half the cases fixed for hearing during a month are caseswhere appeals are filed against order passed under section 52 of the Bombay Sales TaxAct, 1959 or where appeals are filed earlier to all other appeals and the remaining halfout of the balance appeals are those involving highest quantum of relief sought.

16. Section 62 — Rectification of mistakes

16.1. A new sub-section (1A) is inserted which provides that where any dealer or a person hasrecorded sale of goods on a declaration or a certificate and who could not produce suchdeclaration or certificate before the passing of the assessment order, then such a dealer canapply to the authority within a period of 2 years for rectification of the order, on the groundthat he has received such declaration or certificate. He shall produce before the authority thesaid declaration or certificate and such authority, on being satisfied, shall rectify theorder.

16.2 Such an application for rectification can be made only once in respect of any assessmentsought to be rectified.

16.3 Under the second proviso where the dealer in his application for rectification has specifiedthe quantum of tax to be reduced and filed the necessary evidence, in support thereof, theconcerned authority shall stay the recovery of tax including interest, if any, so levied underthe said order, till the rectification application is finally heard and disposed of.

16.4 Poser: The second proviso to section 62(1A) contemplates the authorities to stay the recoveryproceedings relating to the disputed tax and the interest, if any, but not the penalty. Can theauthority even stay the recovery of penalty?

16.5 The rectification remedy to be pursued is in addition to the remedy by way of appeal. Sincethe period of filing of appeal expires after 60 days, it is always preferable to file an appealalong with the application for rectification. On the remedy of rectification being availed, theappeal filed can be withdrawn.

10th Non Residential Refresher Course

— 18 —

17. Section 63 — Offenses and penalties

17.1 Under sub-section (10) of Section 63, clause (b-2) is inserted to provide for failure to surrenderthe certificate of registration under clause (b) of sub-section (8) of section 22 without sufficientcause, as an offence which is, on conviction, punishable with an imprisonment up to 1 yearwith fine.

17.2 A new sub-section (10B) is inserted to provide for failure to file a special return under clause(c) of sub-section (8) of section 22, without sufficient reasons, as an offense which is, onconviction, punishable with a simple imprisonment up to one month and a fine of Rs. 1,000/- ormore.

18. Section 67 — Cognizance of offences

18.1 By virtue of the deletion of sub-section (1) of section 67 effective 1st of July, 2004, now thecourt can take cognizance of a complaint by any authority for the alleged offence said to havebeen committed by any person under the Act or the Rules. Prior to the amendment, onlythe Commissioner or his authorised representative, if any, was entitled to make a complaint, towhich the court could take cognizance of and not otherwise.

AMENDMENTS TO SCHEDULE ENTRIES

19.1 Amendment of Schedule entry A-8

19.1.1 Schedule entry A-8(1) has been amended to exclude ‘deoiled cakes’ along with oilcakes. This amendment is clarificatory as oil cakes and de-oiled cakes are taxed onlyunder C-I-5 with effect from 1.10.1995.

19.2 Amendment of Part II Schedule C

19.2.1 Entry C-II-5A regarding farsan powder has been amended to exclude mixture of maizepowder with lakh or khesari dal powder. Mixture of maize powder with gram dalpowder will continue to be taxed at 4%.

For the betterment of the human lives and welfare and to restrict the extensive use oflakh or khesari dal powder by its consumption in the form of farsan powder, thisamendment seems to have been carried out.

19.2.2 In case of Jayshree Industries vs. State of Maharashtra, S.A. Nos. 331 & 332 of 1995decided on 13-2-2004, the Tribunal held farsan powder as a tax free item althoughmaize flour formed an ingredient of the said product since the flour was meant forhuman consumption and was not sold as maize flour for industrial purposes.

19.2.3 Rate of tax on kerosene other than that sold for household purpose through publicdistribution system covered under entry C-II-56(2) has been reduced from 20% to 13%.

This is with a view to reduce the cost of consumption of kerosene under the publicdistribution system.

19.2.4 Rate of tax on wires and cables of all kinds used in the generation, transmission,distribution or in connection with the consumption of electricity has been reduced from13% to 8% under Schedule entry C-II-112(1). All other goods used in the generation,transmission, distribution or in connection with the consumption of electricity such asall kinds of holders, plugs, switches, casings, cappings, reapers, bends, junction boxes,meter boards, switch boards, electrical earthenware and porcelainware would continueto be taxed at 13% under Schedule entry C-II 112(2).

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 19 —

The weeding out of the goods like wires and cables of all kinds by reducing the ratefrom 13% to 8% seems to be with the avowed object of extending the distribution ofelectrical energy to the underdeveloped areas at a lesser cost. Wires and cables ‘of allkinds’ signifies the scope of the definition of the goods namely ‘wires and cables’ asduly expanded and such terminology can be found in the various other scheduleentries such as :

Entry 66 — sanitaryware of all kinds

Entry 53 — all kinds of industrial, commercial and domestic receptacles

Entry 69 — all kinds of greeting cards

Entry 87 — all kinds of synthetics

Entry 88 — all kinds of paints

19.2.5 The rate of tax on domestic and commercial electrical and electronic appliances that iscooking ranges, microwave ovens, washing machines and vacuum cleaners andcomponents, parts and accessories of any of them covered under entry C-II-118 hasbeen reduced from 20% to 13%.

There is no other change in the entry.

19.2.6 Schedule entry C-II-151A for lottery tickets has been deleted in light of the amendmentof section 40A, where the scheme of levy of tax has been changed.

20. Amendment of the notification issued under section 8A of Bom. LI of 1959

20.1 Section 8A provides for levy of tax at the last stage on such goods as may be specified fromtime to time by notification in section 41 of the Act. By a retrospective amendment to entry 1so appended to the said notification dated 15-5-1996, the goods like precious stones etc. havebeen subjected to tax at the last stage. However, the specific entries with the numbers as givenin Schedule C Part II have now been specifically referred to by mentioning Entries 98A and 99of the said Schedule and such amendment is made effective from 1st January, 2000.

10th Non Residential Refresher Course

— 20 —

CHAPTER - II

AMENDMENTS TO BOMBAY SALES TAX RULES, 1959

The Bombay Sales Tax (Third Amendment) Rules, 2004 were published on 30th July, 2004and came into effect from 1st July, 2004.

21. Rule 2 Definitions

21.1 Sub-rule (f) Government Treasury

21.1.1 Under rule 2 clause (f) the definition of ‘Government Treasury’ is widened to includein its fold many more branches of banks and the mode of payment is specifiedseparately for.

i. dealers who fall within the jurisdiction of the assessing authority in BrihanMumbai,

ii. dealers within the jurisdiction of an assessing authority outside BrihanMumbai, where the principal place of business is situated in the districtheadquarters and at a place outside the district headquarters and.

iii. in the case of a non-resident dealer.

21.2 Sub-rule (f-1) 100% EOU

21.2.1 This is a clarificatory amendment which defines a 100% export oriented unit as anundertaking approved as such by the Board appointed in this behalf by the CentralGovernment. This is in exercise of the powers conferred by Section 14 of Industries(Development and Regulation) Act, 1951 and the rules made under that Act.

21.2.2 The term ‘100% EOU’ is referred to in set-off rules 41D and 42AD which now wouldinclude a unit approved by the Board and not merely a unit which exports 100% ofits goods. On this issue of ‘100% EOU’, Hon’ble the Maharashtra Sales Tax Tribunalhad an occasion to deal with, in the case of Karsandas Exports (Appeal No. 102 of 2001 decided on 17-10-2003), where the Tribunal held that 100% EOU wouldmean a unit exporting 100% of its goods even if not certified. This decision would no longer apply.

21.2.3 Poser: Whether in the absence of any definition of the term ‘EOU’ under the provisionsof the Sales Tax Act and the Rules thereunder, can resort be made to the provisions ofany other statute like Import Export Regulation Act or the policy thereunder made bythe Central Government? And if so, whether the amendment can be consideredclarificatory?

21.3 Sub rule (f-a) Package Scheme of Incentives

21.3.1 Three more schemes have been included in the definition of “Package Scheme ofIncentives”.

1. The 1993 Package Scheme of Incentives for Tourism

2. The 1998 Power Generation Promotion Policy

3. The 1999-New Package Scheme of Incentives for Tourism Projects

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 21 —

21.4 Sub-rule (f-aa) Permanent Account Number

21.4.1 Permanent Account Number is defined as the Permanent Account Number allottedunder the Income-tax Act, 1961.

It has become compulsory to furnish the permanent account number by every dealerliable to pay tax under the newly inserted sub-section (2) of section 50. Thisinformation is required to be furnished in Form N-13-I

22. Rule 3 Processes not included in manufacture

22.1 By an amendment to this rule, clause (xv) relating to the process of preparing butter fromcream and ghee from butter is deleted w.e.f. 1-7-2004. By notification, the Government ofMaharashtra, in exercise of the powers conferred by section 2(17)(a) has specified the ‘processof preparing butter from cream and ghee from butter’ as manufacture. The result of theamendment to the rule and notification would be that the process of preparing of butter fromcream and ghee from butter would now amount to manufacture and the resale claim on suchprocess would not be admissible with effect from 1-7-2004.

In fact the preparing of butter from cream was not considered to be a distinct commercialcommodity as so clarified by Supreme Court as well as the other High Courts in its variousjudgments such as:—

1. 52 STC 117 (Bom) CST vs. Agarwal & Co.

2. 86 STC 105 (Guj) Chunilal Mayachand vs. State of Gujarat

3. 81 STC 67 (WBTT) Milk Food Ltd. & Anr. vs. Commercial Tax Officer.

4. 81 STC 332 (Mad) State of Tamil Nadu vs. Bharat Dairy Farm

5. 46 STC 63 (SC) Dy. Commr. of Sales Tax vs. Pio Food Packers

In view of the amendment now, when butter is manufactured from cream, the same shall besubjected to tax and so also ghee from butter. This raises an issue whether in light of thevarious ratio decisions of the Supreme Court, such levy of tax would be justified?

As per the ratio decision in the case of 81 STC 332 (Mad) cream and butter are not separatecommodities. They are two forms of the same commodity and no process of manufacture isinvolved in the conversion of cream into butter.

The Supreme Court in 42 STC 433 in the case of Porritts & Spencer Asia (Ltd) has observedthat while interpreting a word in an entry, one should bear in mind that it does not embody astatic concept, it may change its hue with new developments in technology and emergence ofnew processes.

22.2 By The Bombay Sales Tax (Fourth Amendment) Rules, 2003 notified on 31-3-2003, Clause(xx) is added to Rule 3 by which the process of conversion of whole grain of pulses into splitform of pulses is not to be considered as manufacturing activity. As per the provisions ofsection 15(d) of the Central Sales Tax Act, 1956 the whole grain of pulses and split form ofpulses constitute the same commodity.

22.3 In the case of Khandelwal Dal Mill vs. STO, 106 STC 312 (MP) it has been stated that by virtueof section 15(d) of the CST Act, 1956 whole and split pulses are treated as one itemirrespective of the fact that on being split they lose their original identity. Therefore where aregistered dealer purchases whole pulses from an unregistered dealer and utilizes them in themanufacture of split pulses, no purchase tax was leviable.

10th Non Residential Refresher Course

— 22 —

22.4 Due to the process of conversion of whole grain of pulses into split form not being considered

as manufacture, the units undertaking such process would not be eligible for grant of sales tax

incentives under the package scheme of incentives by way of exemption or deferral.

22.5 By The Bombay Sales Tax (Sixth Amendment) Rules, 2004 notification dated 19.8.2004,

Clause (xxi) is inserted whereby the following process shall not be considered as a

manufacturing activity.

(xxi) the process consisting of conversion of:—

a. Unginned cotton to ginned cotton,

b. Unginned cotton to cotton seed,

c. Ginned cotton to baled cotton.

22.6 In keeping with the objective of providing benefits to the above processing industry

Explanation VI is inserted under Rule 31B to include the above processes as manufacture for

the purpose of availing benefit under package scheme of incentives by way of deferment under

rules 31B and 31C.

The above amendments to Rules 3, 31B and 31C are effective from 1-8-2004.

23. Rule 41D Drawback, set off, etc. of tax paid by a manufacturer in respect of purchases

made after the notified day

23.1 By insertion of sixth proviso to Rule 41D, the Government has tried to reduce the

revenue loss in light of the fact that a manufacturer either of taxable or tax free goods

was earlier eligible to get full set-off of tax on their inputs subject to the retention so

provided in Rule 41D. As for example, a manufacture of books and magazines being a tax

free commodity was entitled to get full set off under rule 41D though on the sales side no

sales tax was recoverable on the goods being tax free. This way the state was losing revenue,

as sales tax was leviable at first stage only. However with the introduction of sub-rule 3A to

Rule 41D, the retention percentage have been kept at 2% on taxable goods and 3% on tax

free goods and therefore to be in consonance with this provision, the sixth proviso now

inserted provides for grant of set off on inputs in proportion of taxable and tax free sales

so that retention at different rates of 2% and 3% can be applied accordingly.

23.2 A new sub-rule (3A) has been added to provide for the set-off to be claimed under sub-rule (1)

in respect of purchases made after 1-7-2004 to be reduced by

a. 3 per cent of the purchase price where goods are despatched by the claimant dealer to

his own place of business or agent outside the State.

b. 2 percent of the purchase price where the goods manufactured are taxable goods.

c. 3 percent of the purchase price where the goods manufactured are tax free goods.

The new sub-rule (3A) has been inserted with a view to give incentives to the manufacturers

by improving their competitive strength in the market and making the price cost effective.

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 23 —

23.3 Poser: Whether the ratio proportion method relating to retention of the tax paid on rawmaterials as provided for under sixth proviso to Rule 41D can be applied in the case of capitalassets purchases which are used in manufacture of tax free and taxable goods?

23.4 The provisos (i) and (ii) of the newly inserted rule (3A) gives exemption from such reductionto a dealer holding a registration certificate as on 30.9.1995 and whose turnover does notexceed 12 lacs in the immediately preceding year and also to a 100% EOU on its export salescovered under sub-section (1) of section 5 of CST Act, 1956.

23.5 The aggregate sum of set-off shall be calculated in terms of Rule 44D and the formulathereunder.

23.6 Under sub-rule (2), clause (iii), a dealer despatching goods to his own place of business or tohis agent outside the state was required to produce certificate in Form 31C for such a claim.This condition has been dispensed with since production of Form F under the Central SalesTax Act, 1956 has become mandatory with effect from 11-5-2002 in respect of suchtransactions. The amendment to the rule however, is applicable from 1-7-2004.

24. Rule 41F Drawback, set off, etc. of tax paid by a manufacturer of certain goods

24.1 The amendment to the Rule 41F provides for grant of drawback or set-off of tax paid bya manufacturer of certain specific goods as mentioned in Column 3 of the statement soappended to Rule 41F. The second proviso so added by the amendment lays down thatwhere manufacture results in scrap, whether it is covered under entry 23 of Part I ofSchedule C or Entry 100C of Part II of Schedule C and also the goods not being scrap socovered in the said entries, the dealer shall be eligible for grant of set-off of tax to the extentof manufactured goods only and not on scrap based on the proportional method being appliedto the sale price of scrap as well as the goods so produced.

24.2 Under The Bombay Sales Tax (Amendment) Rules, 2004 notified on 27-3-2004, the rule wasamended by making addition of one more proviso in the rule after the second original provisowhereby set-off under the rule was restricted to taxable manufactured goods. The set-offadmissible under this rule was calculated in the proportion of taxable to total value ofmanufactured goods. The non taxable goods included goods covered by Section 41 exemption.The rule was made retrospective from 1-5-2000.

24.3 Due to retrospective effect being given to the rule, the Government has issued a resolution forgrant of administrative relief for the period 1-5-2000 to 29-2-2004. The difference in amount ofset off as per the unamended rule 41F and amended rule 41F would be admissible by way ofadministrative relief. The power of granting administrative relief would be exercised by theassessing authority.

24.4 The provision of the amended rule is applicable from 1-3-2004. Administrative relief shall begranted in the following situations:

1) Where assessments are already completed as per the pre-amended rule 41F, actionwould be initiated under section 62 or section 57 and on such completionadministrative relief would be granted.

2) Where action for rectification or revision is already initiated, the same shall becompleted, final figures worked out and then administrative relief would be granted.

3) Where rectification or revision orders are already passed under the amended provisionsthe administrative relief would be granted.

10th Non Residential Refresher Course

— 24 —

25.1 Rules 42M, 46A and 46C — Set off and reduction in price in case of B-6 goods

The amendment to Rule 42M is on account of the fact that the levy of tax on iron and steel;

i.e., Schedule B-6 goods was based on the VAT method and as the levy of VAT has been

discontinued w.e.f. 1-5-2003, the corresponding effect on discontinuation of grant of set-off

and allowing of resale claim has been made effective retrospectively from 1-10-2002 and

ending on or before 30-4-2003.

Thus even the corresponding Rules 46A and 46C have been duly amended to be in

consonance with the above amendments in Rule 42M.

25.2 Amendment to The Bombay Sales Tax Rules, 1959 vide Gazette Notification dated 11th

August 2004

Rule 42AE is inserted in the BST Rules. As per Notification Entry G-6, units situated in

Special Economic Zones (SEZ) can purchase goods from local dealers without payment of tax

by issuing them Form GE. However, in a case when the goods are purchased without issue of

Form GE, sales tax is charged by the vendors. There was no provision for grant of set-off in

such cases. Now, above Rule is inserted in the Rules, with retrospective effect from 1.5.2002.

The setoff will be available for purchases effected without issue of Form GE, if the said

purchases are for following purposes:

(i) for use in the manufacture of goods for export out of the territory of India,

(ii) for use of the manufacture of goods for sale to other Certified Registered Dealers,

(iii) for resale in the course of export out of the territory of India,

(iv) for use in the packing of goods so sold or resold as above, or

(v) for the purpose of development, expansion and maintenance of the SEZ.

Under this Rule, full set off will be available calculated as per Rule 44D(a)/(c)

26. Rule 44D — Computation of aggregate tax for grant of set off

Rule 44D has been re-numbered as Rule 44D(1). While computing the aggregate tax so

admissible in the various setoff rules as mentioned in Rule 44D, the words ‘other than the

purchase tax paid or payable as per the first proviso to sub-section (1) of section 14’ are now

being deleted so that the 6% additional purchase tax so levied on account of the

contravention of section 14 where the manufactured goods are transferred to the branches

shall be admissible by way of set off subject to the retention of 3% as so provided for in the

respective rules.

By addition of sub-rule(2), while aggregating the total sum of set off admissible to a

manufacturing dealer under the various rules like 41D, 41F, etc., the amount of entry tax so

paid by the claimant dealer under the Entry Tax Act of 2002 shall be entitled to such grant

of set off. The rule also provides that if the claimant dealer himself has not imported the

goods on his own but such goods are purchased from a local registered dealer, then in

that event also, the necessary set off shall be admissible subject to reduction as so provided in

the respective rules.

The second proviso to the rule provides that no set off of entry tax, if levied on Schedule A

goods or where the whole of tax is exempt by virtue of notification under section 41 will be

admissible to the claimant dealer.

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 25 —

27. In light of the various amendments so carried out both in the Act as well as in the Rules,corresponding amendments have been duly carried out in the respective forms asprescribed from time to time.

THE BOMBAY SALES TAX (FOURTH AMENDMENT) RULES, 2003By Notification dated 31-3-2003

28. Clause (k) of Rule 2 — Definition of very Large Project

Clause (k) is inserted whereby ‘Very Large Project’ has been defined to mean Eligible IndustrialUnit in respect of which the Eligibility Certificate is issued in terms of the GovernmentResolution, Industries, Energy and Labour Department, No. IDL-1098/(121)/IND-8, dated 11thAugust, 1998.

29. Rule 31AA - Calculation of cumulative quantum of benefits

29.1 The rule refers to the computation of the CQB which a backward area unit holding a certificateof entitlement is entitled to avail of under the respective scheme of exemption or deferral.With the coming into force of levy of turnover tax and surcharge u/ss. 9 and 15-1A respectively,such tax so borne by the claimant unit shall also be available for the computation of CQB.

29.2 Rule 3B has been added to Rule 31AA which provides for computation of such benefits to amega project under 1999 PSI not only on the finished product but also by-products or scrapgenerated during the process of manufacture. And even the benefits so available on the capitalassets in sub-rule (c) of rule (3B) as now provided for, shall be available, subject to the non-availability of set off under rule 42AC or 41D as so provided therein.

29.3 Similar provisions are made in Rule 31B for grant of CQB in regard to surcharge and turnovertax as effective from 1-4-1999.

30. Rule 31B — Deferment of tax for a specified period

By amending clause (d) of Rule 31B, the period for such benefits has been specifically statedto be 12 years and 10 years respectively instead of the provision of not exceeding 12 years or10 years as it originally stood in the rule.

The period for deferral of benefit under this rule shall commence from the date of furnishingof last return and not the annual return. This is made effective from 1-9-1995.

Similarly the instalments also are classified as six annual instalments and five annualinstalments instead of equal annual instalments not exceeding six such instalments or five asthe case may be.

But in case of mega project or very large project located in Vidarbha and Marathwada Regions,the period for deferral is provided for 18 years and repayment in seven equal instalmentswhereas in the case of other regions, the period is for 14 years and five equal instalments.

10th Non Residential Refresher Course

— 26 —

CHAPTER - III

NOTIFICATIONS

Notification Group / Entry Description

SEZ 2001/(152)/IND-2 — Explains Govt. policy regarding setting up of Specialdtd. 12-10-2001 Economic Zones in Maharashtra

CST 2001/CR-77/Tax-2 Sale of Purefied Terepthalic acid by a dealer in Maharashtradtd. 9-12-2002 — to a Registered dealer or Government inter-state. CST reduced

to 2% subject to production of ‘C’ Form

STA 1097.CR-194/ Group G, Entry 3 Relating to sale of gold bullion covered by C-I-10 and C-I-23,Taxation 2 by specified dealers whole of tax exempt.dated 28-12-2002

STA 2000/CR-123/ Group B, Entry 2 Provides for exemption of tax on sale to diplomatic officers,Taxation 2 consular offices etc. where the price of goods sold through adtd. 29-12-2002 single invoice shall not be less than Rs. 1500/-

STA 2002/CR-27/ Group C, Entry 48 Sales by Muk Badhir Vidyalaya of any printed material andTaxation 2 sale of raw material to such Vidyalaya exempt from taxdtd. 4-1-2003 period 1-4-2002 to 31-3-2003

STA 2002/CR-51/ Group A, Entry 47 Sales or purchases by Registered Dealer of bullion and specieTaxation 2 and gold jewellery (Entry C-I-10, Entry C-II-97), tax exempt indtd. 30-1-2003 excess of 1% and whole of surcharge and turnover tax

w.e.f. 1-4-2002.

STA 2002/CR-109/ Group G, Entry 6 Form GE substitutedTaxation-2dtd. 3-2-2003

STA 2002/CR-12/ Group E, Entry 8 Sale of newsprint to publisher of newspapers byTaxation 2 M/s. Murti Agro Products, Nagpur, exempt in excess of 2%.dtd. 6-2-2003

STA 2002/CR-110/ Group H, Entry 24 Sale of milk powder by the Government Milk Scheme,Taxation 2 Nagpur to the Chief Minister Aid Fund, Orissa for thedtd. 24-3-2003 period 1st April, 1999 to 31st March 2000 whole of

tax exempt.

STA 2001/38/ Group A, Entry 15 Sale or purchase of country liquor covered by C-II-20 andTaxation 2 foreign liquor covered by C-II-22dtd. 28-3-2003

STA 1097/194/ Group G, Entry 3 Sale of bullion substituted for only gold bullion and platinumTaxation 2 covered by C-I-10, C-I-23, by specified categories wholedtd. 29-3-2003 of tax exempt

STA 2000/123/ Group B, Entry 1, 4, 5 Sale by registered dealer to various UN Agencies, whole of taxTaxation 2 exempt where the price of goods in a single invoice is not lessdtd. 29-3-2003 than Rs. 1500/- (Rs. 5000 up to 28-12-2002)

RECENT AMENDMENTS UNDER BST, CST AND ALLIED ACTS

— 27 —

Notification Group / Entry Description

STA 2002/121/ Group L, entry 7 M/s. Swati Asbestos for National Programme on improvedTaxation 2 chulha run by Dept. of Non conventional energy in respect ofdtd. 29-3-2003 sales for the period from 1-10-1995 to 31-3-2003 whole of tax

exempt.