Embed Size (px)

Citation preview

Part of the CBRE affiliate network

Philippine

s

Real Estate Boon or Bane:

Analysis and Prognosis of the

Property Market

CREBA 21st ANNUAL NATIONAL CONVENTION

Presented by

VICTOR J. ASUNCIONExecutive Director for Retail Investments,

Global Research & Consultancy

CB Richard Ellis Philippines | Page 2

Is Real Estate Boon or Bane?

Real estate cannot be lost or stolen, nor can it be

carried away. Purchased with common sense,

paid for in full, and managed with reasonable

care, it is about the safest investment in the

world. — Franklin D. Roosevelt

Owning a piece of real estate in the Philippines

fullfills a dream. Progress and development

move the country further ahead as the place to

live, retire or invest. Being an OFW or Filipino

immigrant abroad gives you an edge on prime

spots.— Overseas-Filipinos.Com

Part of the CBRE affiliate network

Philippine

s

Real Estate Boon or Bane:

Analysis and Prognosis of the

Property Market

CB Richard Ellis Philippines | Page 4

Property Market Indicator/ Macro Level

GDP - is the market value of all officially recognized final goods and services

produced within a country in a given period

GVA of Real Estate is made up of services produced in real estate buying, selling,

subdividing, renting, leasing, operating of self-owned/leased apartment buildings, non-

residential and dwellings, cemetery developments and real estate activities on a fee

and contract basis.

CB Richard Ellis Philippines | Page 5

Property Market Indicator/ Macro Level

GDP/ GVA of Real Estate/ GVA of Construction – public and private construction

CB Richard Ellis Philippines | Page 6

Property Market Drivers

OFW (Dollar Remittance) - Filipinos working

abroad sent home $20.1 billion in 2011 up by

7.2 percent higher than in 2010.

BPO (Business Process Outsourcing) -

the industry grew by approximately 22

percent to $10.9 billion in 2011, employing

640,000.

TOURISM - 2011 foreign tourist receipts

grew approximately 18.34 percent to P129

billion ($2.8 billion) from 2010’s P109 billion

($2.4 billion) revenues.

Part of the CBRE affiliate network

Philippine

s

OFW Remittances

CB Richard Ellis Philippines | Page 8

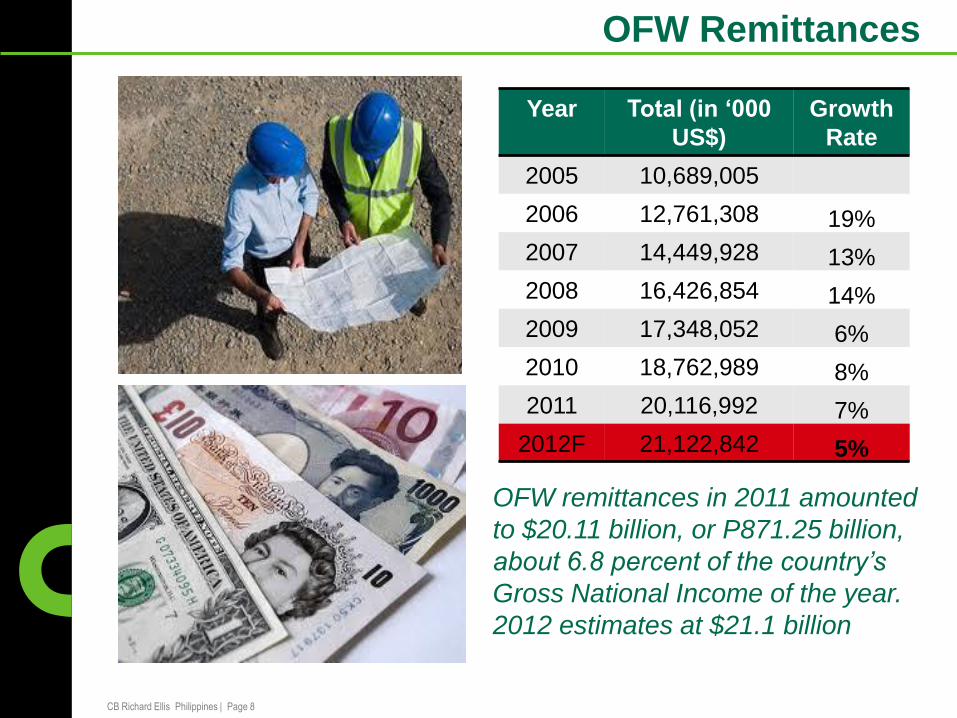

OFW Remittances

Year Total (in ‘000

US$)

Growth

Rate

2005 10,689,005

2006 12,761,308 19%

2007 14,449,928 13%

2008 16,426,854 14%

2009 17,348,052 6%

2010 18,762,989 8%

2011 20,116,992 7%

2012F 21,122,842 5%

OFW remittances in 2011 amounted

to $20.11 billion, or P871.25 billion,

about 6.8 percent of the country’s

Gross National Income of the year.

2012 estimates at $21.1 billion

CB Richard Ellis Philippines | Page 9

OFW by Origin

Total OFWs OCWs Other OFWs Total OFWs OCWs Other OFWs

Philippine

Number (In thousands) 2,158 2,057 100 2,043 1,940 104

Percent 100 95.3 4.7 100 94.9 5.1

Total 100 100 100 100 100 100

National Capital Region 12.5 12.9 3.5 13.8 14 9.6

Cordillera Administrative Region 1.9 1.9 2.4 1.8 1.8 1.1

I - Ilocos Region 9.2 9.2 8 9.5 9.8 3.8

II - Cagayan Valley 6.3 6.6 1.2 6.1 6.4 1.4

III - Central Luzon 14.3 14.3 14.8 14.4 14 22.3

IVA - CALABARZON 16.5 16.7 12.2 16 16 15.7

IVB - MIMAROPA 1.9 1.9 2.6 1.7 1.7 2.2

V - Bicol Region 3.3 3.5 0 3.1 3.2 1.5

VI - Western Visayas 8.5 8.8 2.7 8.3 8.5 3.1

VII - Central Visayas 6.9 7.1 4.2 6.6 6.8 2.6

VIII - Eastern Visayas 2 2 2.7 2 2 1

IX - Zamboanga Peninsula 1.9 1.5 9.2 2.3 2.1 5.6

X - Northern Mindanao 3.5 3.5 3.8 3 3 2

XI - Davao Region 2.3 2.3 2.1 2.8 2.9 2.4

XII - SOCCSKSARGEN 4.4 4.3 5.4 4.2 4.1 5

XIII - Caraga 1.6 1.6 1.9 1.4 1.4 2.5

Autonomous Region in Muslim Mindanao 3 2 23.2 3.1 2.3 18

2011 2010

OFW DEPLOYMENT - The top three (3) regions that deploys the most OFWs are

Region IVA (Calabarzon); Region III (Central Luzon) and the National Capital Region

(Metro Manila).

CB Richard Ellis Philippines | Page 10

OFW Remittances

IMPACT to HOUSEHOLD DISPOSABLE INCOME

REMITTANCE RECEIPIENT

HOUSEHOLDREMITTANCE NON-RECEIPIENT

HOUSEHOLD

Source: Ang, A., Sugiyarto G. & Jha S. (2009, December). Remittances and Household Behavior in the Philippines (ADB Economics Working Paper Series No. 188).

Retrieved August 15, 2010, from http://www.adb.org/Documents/Working-Papers/2009/Economics-WP188.pdf

OFW REMITTANCE RECEIPIENT HOUSEHOLD - Spends at

approximately 43.30% on Food directly impacting the Retail Sector (about $

7.5 billion in 2009); and 2.1% or $364 million for the Housing Sector

CB Richard Ellis Philippines | Page 11

OFW Remittances

BOON for the RETAIL/ SERVICE SECTOR

OFW Household – fuels the regional

expansion of major retailers and mall

developers; more quick service restaurants

OFW Remittances - will continue to provide

ample support for the consumption-driven

economy

CB Richard Ellis Philippines | Page 12

OFW Remittances

BOON for the HOUSING SECTOR

HUDCC estimates the housing backlog at

3.6 million units,

TO BUY OWN HOUSE – major reason why

Filipinos seek employment abroad. OFW is

the major market of housing developers

nationwide

Housing Segment DefinitionSurplus (Shortage)

of Housing Units

Socialized 400k below (624, 200)

Economic 401k – 1.25M (2M)

Low Cost 1.25M – 3M (484, 325)

Mid end 3M – 6M 247, 611

High end 6M up 200, 000

Source: SHDA and UA&P Center for Research and Communication 2012.

CB Richard Ellis Philippines | Page 13

OFW Remittances/ BPO/ Tourism

BOON for the RESIDENTIAL

CONDOMINIUM SECTOR

New Generation – condominium dwellers in

urban centers

Impact of Population Demographics –

more visible in the residential condominium

sector given higher disposable income of a

younger populace

CB Richard Ellis Philippines | Page 14

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Manila

CB Richard Ellis Philippines | Page 15

OFW Remittances/ BPO/ Tourism

More than 2/3 of

upcoming supply located

in Quezon City, Makati

City, Mandaluyong City,

and City of Manila

QC, Makati, Mandaluyong

and Manila

Biggest concentration of

upcoming supply is in

Quezon City

Upcoming Residential Condominium Supply – Metro Manila

CB Richard Ellis Philippines | Page 16

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Manila

Upcoming residential condominium supply shifting to the >80K to

100K price range with less focus on projects priced above 100K .

CB Richard Ellis Philippines | Page 17

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Manila

Share of upcoming residential condominiums with the >80K to 100K

price range increased from 34.1% to 42.5% while share of projects

priced above 100K declined from 29.3% to 17.4%.

CB Richard Ellis Philippines | Page 18

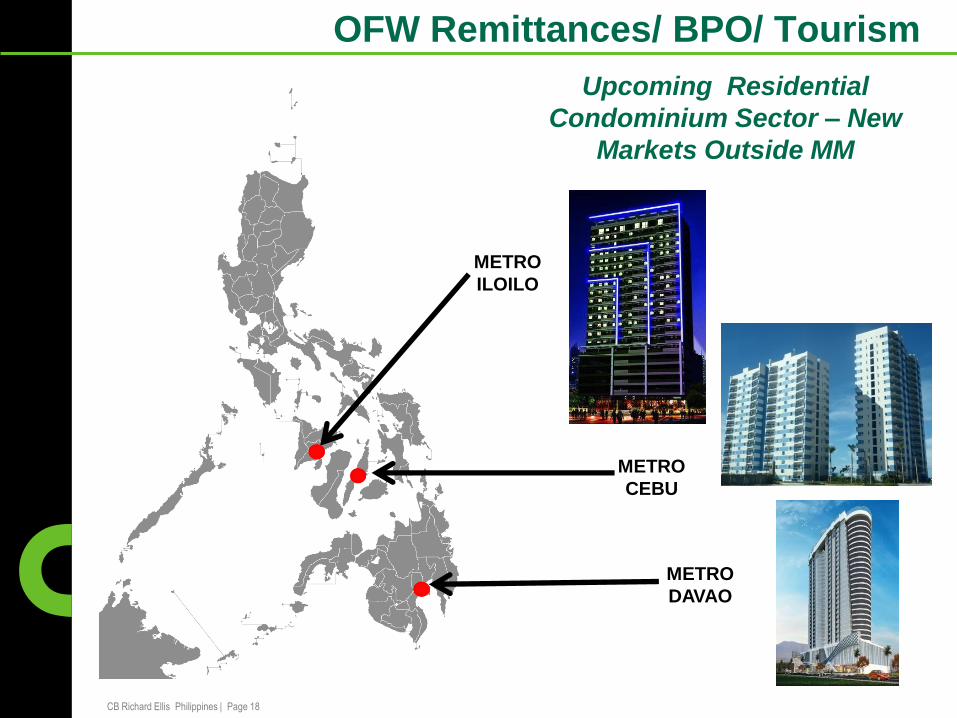

OFW Remittances/ BPO/ Tourism

Upcoming Residential

Condominium Sector – New

Markets Outside MM

METRO

CEBU

METRO

DAVAO

METRO

ILOILO

CB Richard Ellis Philippines | Page 19

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Cebu

CB Richard Ellis Philippines | Page 20

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Davao

CB Richard Ellis Philippines | Page 21

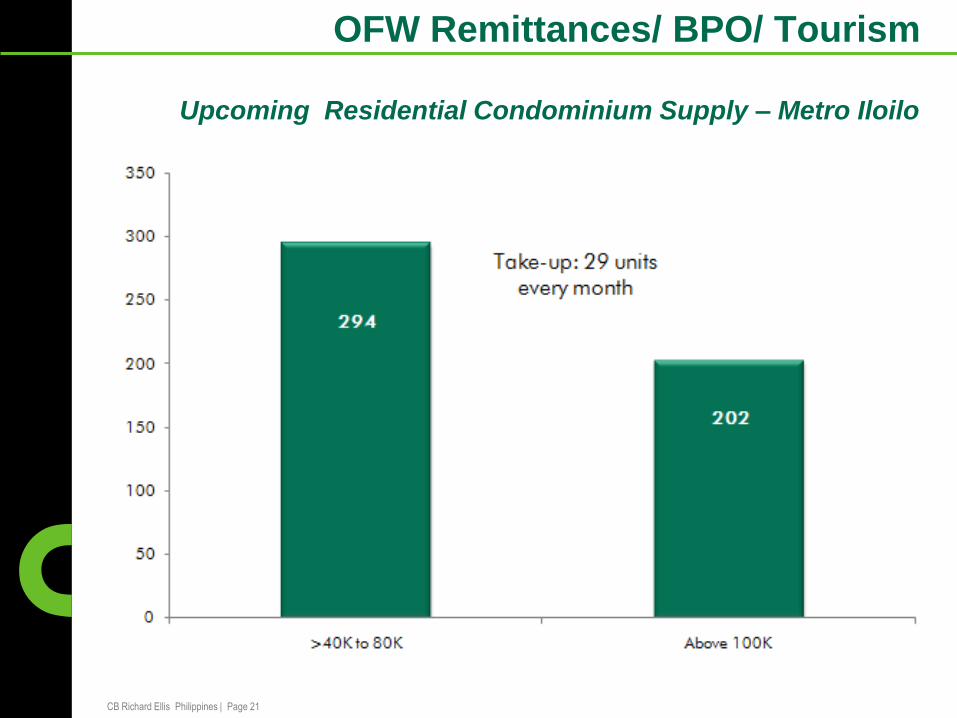

OFW Remittances/ BPO/ Tourism

Upcoming Residential Condominium Supply – Metro Iloilo

Part of the CBRE affiliate network

Philippine

s

Business Process Outsourcing

CB Richard Ellis Philippines | Page 23

Metro Manila Business Districts – Office Sector

MAKATI CENTRAL BUSINESS DISTRICT ORTIGAS CENTER

BONIFACIO GLOBAL CITYEASTWOOD CITY CYBERPARK

Business Process Outsourcing

CB Richard Ellis Philippines | Page 24

Most BPO offices at full

occupancy; 80% to 95% of Take-

up

Tight supply situation with limited

office space turnover

Rising lease rates of BPO offices

resulting from supply pressures

Strong pre-leasing demand

Most cost effective prime office

destination in Asia

Increasing flight-to-quality

demand from traditional offices

Business District

2Q2012 Rents

2Q2011 Rents

Y-o-Y Change

Makati 832 800 4%

Fort

Bonifacio762 688 10.8%

Ortigas 562 554 1.4%

Alabang 562 521 7.9%

Quezon

City572 516 10.9%

Metro Manila Business Districts – Office Sector

Business Process Outsourcing

CB Richard Ellis Philippines | Page 25

Metro Manila Upcoming Office Supply

Business Process Outsourcing

CB Richard Ellis Philippines | Page 26

Business Process Outsourcing

Metro Manila Pre-Leasing Performance

CB Richard Ellis Philippines | Page 27

Source: BPAP and CBRE estimates

Dollar Revenue Performance

Business Process Outsourcing

CB Richard Ellis Philippines | Page 28

Source: BPAP

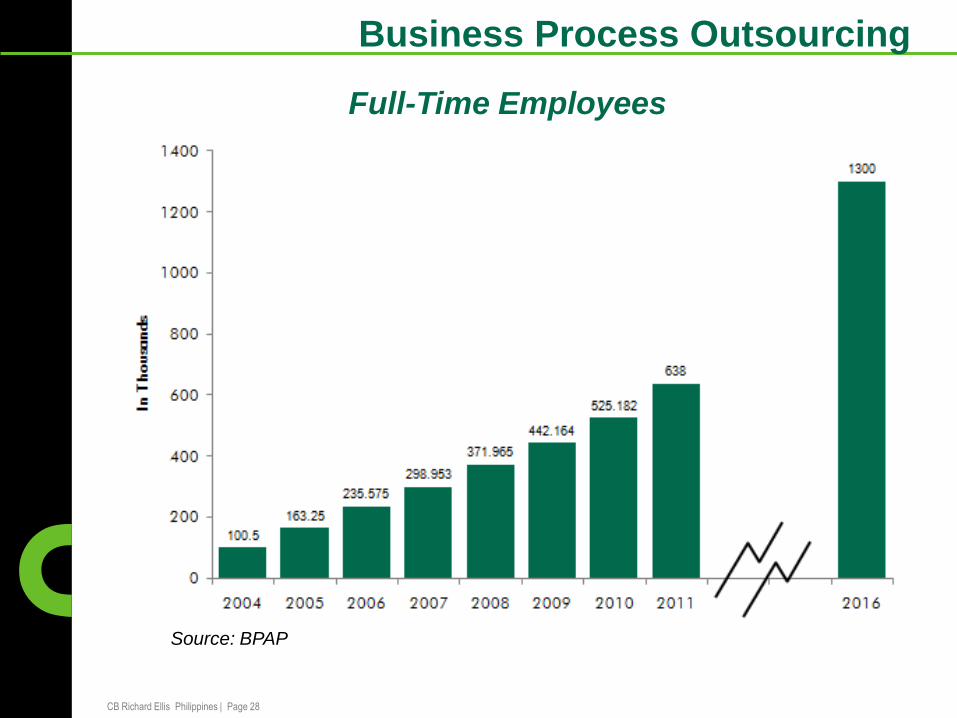

Business Process Outsourcing

Full-Time Employees

CB Richard Ellis Philippines | Page 29

Business Process Outsourcing

PEZA Resolution No. 12-329 (July 2012)

Only Developers/ Operators of New IT Parks and Centers to

be located in Metro Manila and Cebu City including BPO/IT

Facilities Enterprises in such New IT Park shall be entitled to

the special five percent tax on gross income tax (5% GIT)

and other fiscal incentives as maybe provided by PEZA

Previously PEZA registered (before July 2012) Developers

e.g. FBDC, Megaworld, Robinsons Land and Filinvest will

continue to enjoy in perpetuity the tax incentive of PEZA

including new BPO/IT Buildings that they will develop

themselves within the four (4) previously approved IT Park.

Regionalization in aid of the urbanization of the provinces is

the main thrust of this resolution

SOURCE: Elmer San Pascual (PEZA-

PPRG)

Part of the CBRE affiliate network

Philippine

s

Hospitality Sector

CB Richard Ellis Philippines | Page 31

Tourism Industry

TOURIST ARRIVALSCountry 2006 2007 2008 2009 2010 2011 2012*

PHL6.74% 10.71% 1.29% -3.91% 16.68% 11.28% 13.05%

SG9.04% 5.47% -1.64% -4.28% 20.20% 13.17% 12.30%

ID-2.61% 13.02% 13.24% 1.43% 10.74% 9.24% 8.81%

TH19.49% 4.65% 0.50% -2.66% 12.63% 19.84% 7.27%

MY6.10% 20.11% 5.26% 7.27% 4.24% 0.41% 1.20%

*YoY Growth as of May 2012

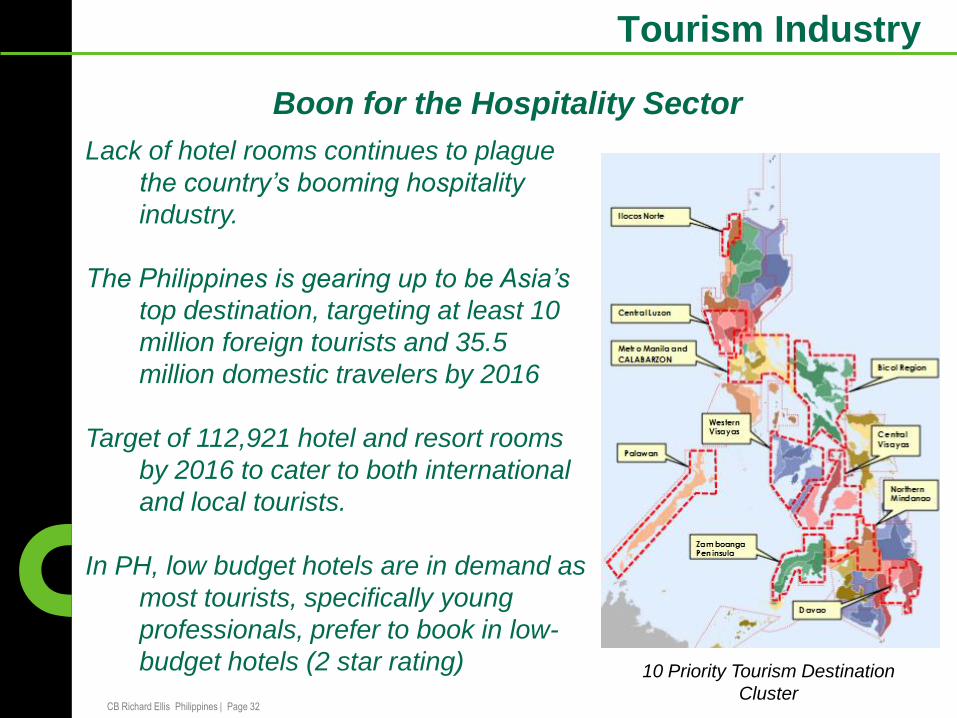

Boon for the Hospitality Sector

CB Richard Ellis Philippines | Page 32

Tourism Industry

Lack of hotel rooms continues to plague

the country’s booming hospitality

industry.

The Philippines is gearing up to be Asia’s

top destination, targeting at least 10

million foreign tourists and 35.5

million domestic travelers by 2016

Target of 112,921 hotel and resort rooms

by 2016 to cater to both international

and local tourists.

In PH, low budget hotels are in demand as

most tourists, specifically young

professionals, prefer to book in low-

budget hotels (2 star rating)

Boon for the Hospitality Sector

10 Priority Tourism Destination

Cluster

CB Richard Ellis Philippines | Page 33

Tourism Industry

Boon for the Hospitality Sector

HOTEL Development Hot Spots

1. Clark/ Angeles City

2. Subic/ Olongapo City

3. Tagaytay City

4. Boracay Island

5. Metro Cebu

6. Cagayan de Oro City

7. Puerto Princesa City

Palawan

8. Davao City

CB Richard Ellis Philippines | Page 34

Tourism Industry

Boon for the Hospitality Sector

Service Portfolio – Local Tourism Industry

CB Richard Ellis Philippines | Page 35

Tourism Industry

Boon for the Hospitality Sector

Philippine CASINO Portfolio

CB Richard Ellis Philippines | Page 36

Tourism Industry

Boon for the Hospitality Sector

Pagcor Entertainment City

CB Richard Ellis Philippines | Page 37

Prognosis

Philippines as consumption-driven economy will persist

motivated by OFW Remittances, BPO and Tourism

Land banking should remain as a major thrust among

developers to keep up property boom

Growth opportunities will focus on housing/ residential

condominium, hospitality and BPO/IT office developments.

Developers should position themselves relative to upcoming

private and public infrastructure projects e.g. PPP

Economic activities would naturally shift towards

regionalization for sustained and strategic property

development

Part of the CBRE affiliate network

Philippine

s

THANK YOU