Embed Size (px)

Citation preview

Real Estate Asset and Investment Management for institutional investors in Switzerland

Prof. Dr. Michael Trübestein ARES-Conference Fort Myers, April 17th 2015

Folie 2, April 17th, 2015

Agenda

1 Introduction and current trends 2 Empirical results for direct real estate investments 3 Empirical results for indirect real estate investments 4 Summary and outlook

Folie 3, April 17th, 2015

Agenda

1 Introduction and current trends 2 Empirical results for direct real estate investments 3 Empirical results for indirect real estate investments 4 Summary and outlook

Folie 4, April 17th, 2015

Pension funds in Switzerland and current trends

- Strong decrease in the number of pension funds to currently 2,000 institutions

- Real estate investments of CHF 120 bn, therefore „only“ CHF 10 bn abroad (of CHF 720 bn)

- Positive macroeconomic conditions might lead to higher investments in real estate (eg. negative interest rates of the SNB, low unemployment rate, economic upturn)

- Challenges with strong currency, regulation of immigration or a possible economic downturn

- Strong increase in the real estate markets in the last years might lead to a suboptimal allocation of real estate investments

- Challenges might be seen in a lack of suitable real estate assets, the future importance/increase of indirect real estate investments, targeting real estate strategies and management of the investments

Folie 5, April 17th, 2015

Targets of the study and empirical approach

n Empirical study with questionnaires sent to pension funds, life insurance companies and foundations.

n Questionnaires were split up in 3 parts with a total of 27 questions, mostly „multiple choice“

n For Switzerland, 126 institutions answered, representing CHF 440 bn of invested assets and CHF 56 bn of investments in real estate

n The survey was conducted between July and September 2014 in Switzerland and the Principality of Liechtenstein (as well as in Germany and Austria)

n Obtain a general overview of real estate investments and real estate asset management of institutional investors

n Analysis of direct and indirect real estate investments and discussion of investment and management trends

n Classification of investors based on their behaviour

Targets of the study

Empirical framework

Fragebogen

„Real Estate Asset Management bei Institutionellen Investoren“

Bitte vom obersten Entscheidungsträger der Immobilienanlage ausfüllen lassen.

Falls es die Abteilung oder den Bereich „Immobilienanlage“ nicht gibt, bitte vom obersten Entscheidungsträger des Verantwortungsbereiches „Immobilienmanagement“ bzw. des Verantwortungsbereiches „Immobilienverwaltung“ oder des Bereiches „Kapitalanlagen“

ausfüllen lassen. Vielen Dank!

ASIP Performance Comparison

Pensionskasse der Muster AG as of 30 June 2013

With the support of the Association of Pension Funds in

Switzerland

Folie 6, April 17th, 2015

Structure of the empirical study of Real Estate Asset Management

Direct real estate

investments: Management and

Investments (11 questions)

Indirect real estate

investments: Management and

Investments (10 questions)

Direct and indirect real estate

investments in Germany and

Austria

Cluster analysis Cluster analysis

General data variables (6 questions)

Folie 7, April 17th, 2015

Structure of the sample: Dominance of pension funds in the sample

- In the sample, pension funds obtain a dominant position with over 80 % of the analyzed questionnaires

- Clustering based on behavioural aspects

Pension'Funds'(101)'

Life'Insurance'Companies'(2)'

Service'Investor'(5)'

Founda=ons'(12)'

Others'(3)'

Various'Ins=tu=ons'(3)'

Folie 8, April 17th, 2015

Agenda

1 Introduction and current trends 2 Empirical results for direct real estate investments 3 Empirical results for indirect real estate investments 4 Summary and outlook

Folie 9, April 17th, 2015

Strategic and operational tasks of a Real Estate Asset Management for direct investments

- Analysis of 15 variables in the area of strategy (4), transaction management(2), management of the assets (7) und reporting/controlling (2)

- Development of different structures of the organization

strategy

• Development of the investment strategy

• Strategic real estate analysis and supervision

• Object-specific investment planning and management

• Structuring of investments (e.g. taxes, financing)

transaction management

• Preparation of (dis-) investments decisions

• Implementation of (dis-) investments decisions

management

• Fiduciary representation • Optimization of operating

expenses • Contract/area

management • Management of external

service providers • Initiation/control of

project development/construction

• Maintenance of data fields • Market and site analysis

controlling

• Reporting and controlling object level

• Reporting and controlling portfolio level

Folie 10, April 17th, 2015

Current organization of real estate asset management tasks

- Tendency towards an internal organization, especially for strategic tasks

- Alternating organizational structures for the management of real estate

(n#=#63#–#66)!!1!=!internal!organiza.on!2!=!in!coopera.on!with!external!services!3!=!external!organiza.on!

*!!!highly!signifcant!**!significant!

1,0$

1,5$

2,0$

2,5$

3,0$

Development$of$the$investm

ent$strategy$

Strategic$real$estate$analysis$and$supervision$

Object@specific$investm

ent$planning$and$management$

Structuring$of$investm

ents$(e.g.$taxes,$financing)$

PreparaGon$of$(dis@)$investm

ents$decisions$

ImplementaGon$of$(dis@)$investm

ents$decisions$

Fiduciary$representaGon$

OpGmizaGon$of$operaGng$expenses$

Contract/$area$m

anagement$

Management$of$external$service$providers$

IniGaGon/control$of$project$development/construcGon$

Maintenance$of$data$fields$

Market$and$site$analysis$

ReporGng$and$controlling$object$level$

ReporGng$and$controlling$porP

olio$level$

Folie 11, April 17th, 2015

Current organization of real estate asset management tasks in diffent clusters

- Clustering in 3 groups with the k-means-method based on the actual organization and the possibility to externalize these tasks

- Different attitudes to internalize and externalize management tasks

1"="internal"organiza.on"2"="in"coopera.on"with"external"services"3"="external"organiza.on"

*"""highly"signifcant"**"significant"

1,0$

1,5$

2,0$

2,5$

3,0$

Development$of$the$investm

ent$strategy*$

Strategic$real$estate$analysis$and$supervision*$

ObjectAspecific$investm

ent$planning$and$management*$

Structuring$of$investm

ents$(e.g.$taxes,$financing)**$

PreparaHon$of$(disA)$investm

ents$decisions*$

ImplementaHon$of$(disA)$investm

ents$decisions*$

Fiduciary$representaHon*$

OpHmizaHon$of$operaHng$expenses*$

Contract/$area$m

anagement*$

Management$of$external$service$providers*$

IniHaHon/$control$of$project$development/$construcHon*$

Maintenance$of$data$fields*$

Market$and$site$analysis*$

ReporHng$and$controlling$object$level*$

ReporHng$and$controlling$porQ

olio$level*$

Strategists$(n$=$15A16)$ Generalists$(n$=$30A32)$ Delegates$(n$=$16A19)$

Folie 12, April 17th, 2015

Evaluation of a (possible) externalization of real estate asset management tasks

1"="very"easy"2"="easy"3"="neutral"4"="difficult"5"="very"difficult"

*"""""highly"significant"**"""significant"

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

4,5$

5,0$

Development$of$the$investm

ent$strategy*$

Strategic$real$estate$analysis$and$supervision*$

ObjectBspecific$investm

ent$planning$and$

Structuring$of$investm

ents$(e.g.$taxes,$financing)**$

PreparaIon$of$(disB)$investm

ents$decisions*$

ImplementaIon$of$(disB)$investm

ents$decisions*$

Fiduciary$representaIon*$

OpImizaIon$of$operaIng$expenses*$

Contract/$area$m

anagement**$

Management$of$external$service$providers*$

IniIaIon/$control$of$project$development/$

Maintenance$of$data$fields*$

Market$and$site$analysis$

ReporIng$and$controlling$object$level*$

ReporIng$and$controlling$porR

olio$level*$

Strategists$(n$=$14B15)$ Generalists$(n$=$32)$ Delegates$(n$=$16B17)$

Folie 13, April 17th, 2015

Investment criteria for direct real estate investments in the clusters

1"="very"important"2"="important"3"="neutral"4"="unimportant"5"="very"unimportant"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1"

1,5"

2"

2,5"

3"

3,5"

4"

4,5"

5"

Long,term"orienta3on***"

Realiza3on"of"a"target"return"

Risk,/"return"ra3on"

Maintenance"of"capital/"inlfa3on"hedge"

Constant"cash,flows"

Diversifica3on***"

Low"vola3lity"

Value"enhancement**"

Realiza3on"of"a"maxim

um"return"

Liquidity"

Social"targets"

Architectural"targets*"

Tax"advantages"

Hidden"reserves**"

Strategists"(n"="15,16)" Generalists"(n"="32,33)" Delegates"(n"="17,19)"

- Long term orientation, security aspects and risk-/return-structures as important criteria for direct real estate investments

- Additional targets are of lower importance

Folie 14, April 17th, 2015

Returns for direct real estate investments

Total return CH in 2012 Total return CH in 2013 Change (in %)Strategists (n = 14) Average 5.70 4.92 -13.62

Deviation 3.66 3.05 -16.68Generalists (n = 27, n = 26) Average 5.40 5.29 -1.97

Deviation 2.06 1.30 -37.02Delegates (n = 17) Average 6.68 5.46 -18.26

Deviation 4.56 1.96 -56.92Total (n = 58, n = 57) Average 5.85 5.25 -10.18

Deviation 3.34 2.02 -39.65

- Returns (total returns) decreased during the last year and fluctuate between 5 and 7 %

- Decrease of the standard deviation implying a homogeneous market with difficulties to find investment opportunities

Folie 15, April 17th, 2015

Criteria for an externalization of real estate asset management tasks

1"="very"important"2"="important"3"="neutral"4"="unimportant"5"="very"unimportant"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

Missing$of$ow

n$know2how$in$real$estate$

Cost$savings$by$contrac>ng$

Confidence$in$quality$of$proper>es$and$m

anagement$

Concentra>on$on$core$compentencies$

Higher$flexibility$

Posi>ve$experiences$with$contrac>ng$

Investments$in$new/$foreign$markets$

Increase$of$value$of$real$estate$assets$

Clear$aKribu>on$and$plannung$of$costs$

Superior$corporate$decisions$

Personnel/$genera>on$change$

Strategists$(n$=$15216)$ Generalists$(n$=$30231)$ Delegates$(n$=$15217)$

- No very important criteria could be observed

- Missing know-how and cost-saving as important criteria

- Missing staff is not seen as a major criteria implying also no tendency towards indirect investments

Folie 16, April 17th, 2015

Criteria against an externalization of real estate asset management tasks

1"="very"important"2"="important"3"="neutral"4"="unimportant"5"="very"unimportant"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

Loss$of$knowledge/competence*$

High$real$estate$know?how$of$staff*$

Outperformance$of$ow

n$teams$(benchmark)**$

Interface$problem

s*$

Risk$of$decreasing$object$quality/unsaKsfied$tenants*$

Intransparency***$

Internal$restricKons/conflicts$of$interests$

Problems/costs$with$later$insourcing*$

Costs$and$controlling$during$the$contract*$

Confidency/sensiKve$informaKon**$

Costs$at$contract$im

plementaKon$

Missing$experience$w

ith$outsourcing$

No$possibility$for$outsourcing/no$real$estate$

Strategists$(n$=$15)$ Generalists$(n$=$30?32)$ Delegates$(n$=$13?14)$

- Competence and know-how in the institution as important criteria

- Risk of decreasing object quality

Folie 17, April 17th, 2015

Criteria for the selection of a real estate asset management

1"="very"important"2"="important"3"="neutral"4"="unimportant"5"="very"unimportant"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1"

1,5"

2"

2,5"

3"

3,5"

4"

4,5"

5"

Experience"of"the"REAM/track"record"

Image/reputa?on"of"the"m

anager"

Geographic"presence"of"the"m

anager"

Costs"of"the"REAM"

Corporate"governance/legal"structures"of"the"REAM

"

Number/type"of"other"mandates"of"REAM

"

Compensa?on"(perform

ance"based)"

Distance"of"the"unit"to"the"REAM**"

Assets"under"management"

Contract"dura?on"

Implementa?on"of"the"contract"in"the"staffMcontracts"

EquityMinvestment"of"the"REAM

***"

Strategists"(n"="15M16)" Generalists"(n"="30M31)" Delegates"(n"="17M19)"

- Experience, image and reputation as well as presence of the managers and costs as important criteria

- Contractual aspects are of minor importance (vs. Principal-Agent-Theory)

- High level of confidence

- Difficulties for new market players

Folie 18, April 17th, 2015

Use of real estate asset management-software for selected tasks

n"="50&54""

0%#

10%#

20%#

30%#

40%#

50%#

60%#

70%#

80%#

90%#

100%#

Por0olio#analysis#and#m

anagement#

Object#analysis#and#m

anagement#

IntegraAon#of#different#data#

Benchmarking#for#new#objects#

ExecuAon#of#scenarioKanalysis#and#forecasts#

Provide#key#figures#

GeneraAon#of#individual#and#standardized#

IntegraAon#of#external#data#(e.g.#leases,#income)#

Alerts#for#budgets#(rentKlosses,#operaAonKcosts)#

Alerts#for#contracts#(indexing,#contract#duraAon)#

Real#estate/por0olio#valuaAon#

ReporAng#for#new#codes#

used# possible,#not#used# not#possible# planned#

- Use of software is of minor importance for the analyzed investors, especially for strategic tasks

- Reasons have to be analyzed – possibly no suitable software products available?

Folie 19, April 17th, 2015

Agenda

1 Introduction and current trends 2 Empirical results for direct real estate investments 3 Empirical results for indirect real estate investments 4 Summary and outlook

Folie 20, April 17th, 2015

Criteria for indirect investments in Switzerland and abroad

1"

1,5"

2"

2,5"

3"

3,5"

4"

Fungibility"

Missing"vol."for"dir."inv."

Investments"in"new"(unknown)"markets"

Tax"reasons"

Transparent"fee"m

odel"

Outsourcing"of"management"

Outsourcing"of"asset"allocaFon"

Savings"of"internal"ressources"

ReporFng/accounFng"

RiskJ/return"structure"

DiversificaFon"

ImplementaFon"

Improved"structuring"

Switzerland" Abroad"

Folie 21, April 17th, 2015

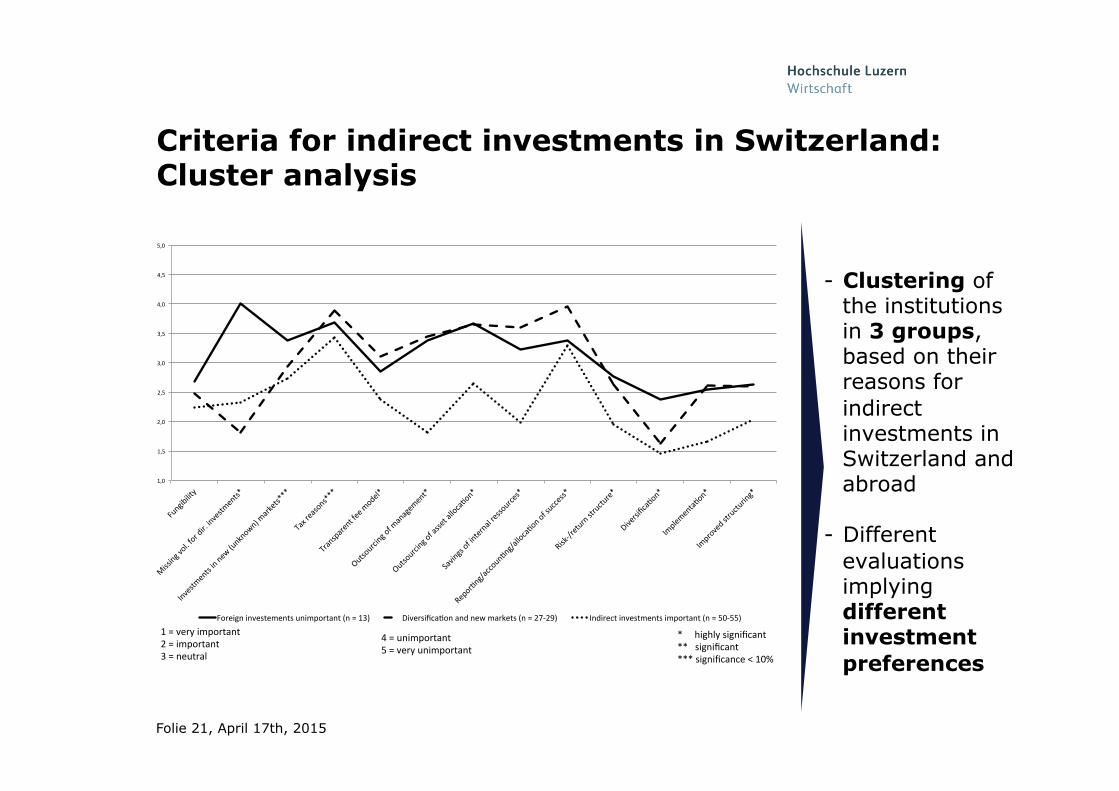

Criteria for indirect investments in Switzerland: Cluster analysis

1"="very"important"2"="important"3"="neutral"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

4,5$

5,0$

Fungibility$

Missing$vol.$for$dir.$investments*$

Investments$in$new$(unknown)$markets***$

Tax$reasons***$

Transparent$fee$model*$

Outsourcing$of$management*$

Outsourcing$of$asset$allocaHon*$

Savings$of$internal$ressources*$

ReporHng/accounHng/allocaHon$of$success*$

RiskL/return$structure*$

DiversificaHon*$

ImplementaHon*$

Improved$structuring*$

Foreign$investements$unimportant$(n$=$13)$ DiversificaHon$and$new$markets$(n$=$27L29)$ Indirect$investments$important$(n$=$50L55)$

4"="unimportant"5"="very"unimportant"

- Clustering of the institutions in 3 groups, based on their reasons for indirect investments in Switzerland and abroad

- Different evaluations implying different investment preferences

Folie 22, April 17th, 2015

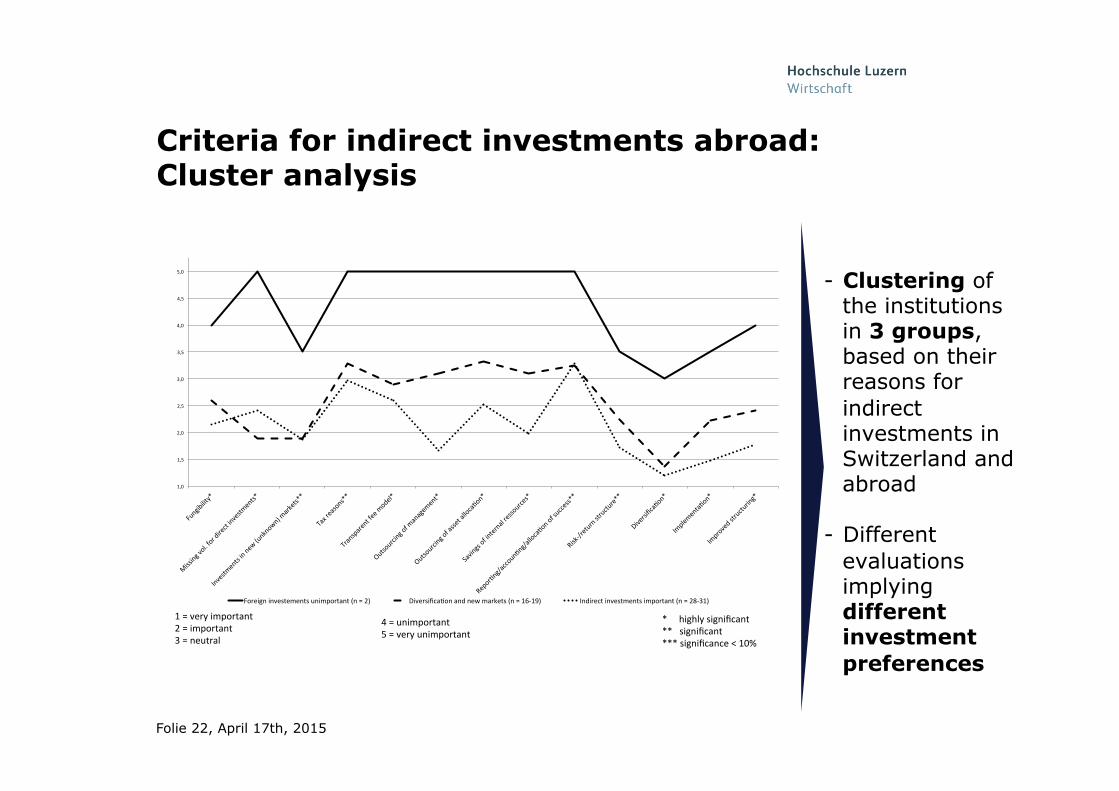

Criteria for indirect investments abroad: Cluster analysis

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

4,5$

5,0$

Fungibility*$

Missing$vol.$for$direct$investments*$

Investments$in$new$(unknown)$markets**$

Tax$reasons**$

Transparent$fee$model*$

Outsourcing$of$management*$

Outsourcing$of$asset$allocaHon*$

Savings$of$internal$ressources*$

ReporHng/accounHng/allocaHon$of$success**$

RiskL/return$structure**$

DiversificaHon*$

ImplementaHon*$

Improved$structuring*$

Foreign$investements$unimportant$(n$=$2)$ DiversificaHon$and$new$markets$(n$=$16L19)$ Indirect$investments$important$(n$=$28L31)$

1"="very"important"2"="important"3"="neutral"

*"""""highly"significant"**"""significant"***"significance"<"10%"

4"="unimportant"5"="very"unimportant"

- Clustering of the institutions in 3 groups, based on their reasons for indirect investments in Switzerland and abroad

- Different evaluations implying different investment preferences

Folie 23, April 17th, 2015

Preferred investement styles in Switzerland and abroad

1"="very"important"2"="important"3"="neutral"4"="unimportant"5"="very"unimportant"

*"""""highly"significant"**"""significant"***"significance"<"10%"

1"

1,5"

2"

2,5"

3"

3,5"

4"

Core,Investm

ents"(cash,flow)"in"CH*"

Core,Plus,Investm

ents"in"CH"

Value,Added,Investm

ents"in"CH"

OpportunisEc,Investm

ents"in"CH"

Core,Investm

ents"(cash,flow)"internaEonal"

Core,Plus,Investm

ents"internaEonal"

Value,Added,Investm

ents"internaEonal"

OpportunisEc,Investm

ents"internaEonal**"

Foreign"investements"unimportant"(CH:"n"="12/int.:"n"="3)"

DiversificaEon"and"new"markets"(CH:"n"="27,28/int.:"n"="17)"

Indirect"investments"important"(CH:"n"="51/int.:"n"="30,31)"

- “normal” behaviour for pension funds

- Higher risks with lower importance

- For investments abroad, higher risks are accepted

Folie 24, April 17th, 2015

Investments in indirect real estate vehicles

CH#In

vestment+

foun

datio

n(dire

ct+re

al+estate)

CH#In

vestment+

foun

datio

n(fu

nd+of+fun

ds)

SICA

Vs

RE+stocks/REITs

Fund

+of+Fun

ds

Open#ended+fund

s

Closed#end

ed+fu

nds

Special+fun

d(open#ended)

Opp

ortunity#Fon

ds/

real+estate+private+

equity#fu

nds+

Infra

structure+fund

s

Others

SwitzerlandTotal 64,94 26,45 7,78 15,54 41,82 42,94 3,00 35,97 5,00 7,50 69,00No.$of$institutions$(n) 76 11 8 31 10 34 1 19 1 2 5Standard#Deviation 30,73 23,11 11,03 12,00 38,27 29,97 . 28,19 . 3,54 36,47AbroadTotal 65,53 42,75 46,55 55,31 57,00 49,58 68,50 49,21 34,43 18,33 31,67No.$of$institutions$(n) 15 13 4 13 5 10 2 11 7 3 3Standard#Deviation 31,31 31,89 38,71 40,04 42,37 37,18 44,55 34,65 28,18 2,89 12,58

- For investments in Switzerland, Swiss Investment Foundations are clearly of highest importance, followed by listed vehicles (stocks and funds)

- For investments abroad, a wide range of investment vehicles can be found

Folie 25, April 17th, 2015

Investments in indirect real estate vehicles

CH#In

vestment+

foun

datio

n(dire

ct+re

al+estate)

CH#In

vestment+

foun

datio

n(fu

nd+of+fun

ds)

SICA

Vs

RE+stocks/REITs

Fund

+of+Fun

ds

Open#ended+fund

s

Closed#end

ed+fu

nds

Special+fun

d(open#ended)

Opp

ortunity#Fon

ds/

real+estate+private+

equity#fu

nds+

Infra

structure+fund

s

Others

SwitzerlandTotal 64,94 26,45 7,78 15,54 41,82 42,94 3,00 35,97 5,00 7,50 69,00No.$of$institutions$(n) 76 11 8 31 10 34 1 19 1 2 5Standard#Deviation 30,73 23,11 11,03 12,00 38,27 29,97 . 28,19 . 3,54 36,47AbroadTotal 65,53 42,75 46,55 55,31 57,00 49,58 68,50 49,21 34,43 18,33 31,67No.$of$institutions$(n) 15 13 4 13 5 10 2 11 7 3 3Standard#Deviation 31,31 31,89 38,71 40,04 42,37 37,18 44,55 34,65 28,18 2,89 12,58

- For investments in Switzerland, Swiss Investment Foundations are clearly of highest importance, followed by listed vehicles (stocks and funds)

- For investments abroad, a wide range of investment vehicles can be found

Folie 26, April 17th, 2015

Situation of Swiss Investment Foundations

Feedback – Mechanismus: Nachfrageüberhang bei Anlagestiftungen

• Die meisten Anlagestiftungen sind seit Jahren für Neugelder geschlossen.

8 © PPCmetrics AG

KGAST Immo-Index Nettovermögen Anteil in % Handel

Adimora Omega (Wohnimmobilien) 114'970'001 0.4% geschlossenASSETIMMO G (Geschäftsliegenschaften) 700'658'997 2.4% geschlossenASSETIMMO W (Wohnliegenschaften) 1'273'134'033 4.4% geschlossenAvadis Immobilien Schweiz Geschäft 662'883'301 2.3% geschlossenAvadis Immobilien Schweiz Wohnen 1'952'060'059 6.7% geschlossenCSA Real Estate Commercial 755'754'578 2.6% geschlossenCSA Real Estate Switzerland 4'657'808'105 16.1% geschlossenCSA Real Estate Switzerland Residential 475'404'114 1.6% geschlossenEcoreal Suissecore Plus 519'209'534 1.8% geschlossenHIG Immobilien Schweiz 643'364'014 2.2% geschlossenImoka Immobilien Schweiz 435'950'012 1.5% geschlossenPatrimonium Wohnimmobilien Schweiz 179'445'297 0.6% offenPensimo Casareal (Wohnimmobilien) 853'179'993 2.9% geschlossenPensimo Proreal (Geschäftsimmobilien) 239'580'002 0.8% geschlossenSarasin Nachhaltig Immobilien Schweiz 302'553'894 1.0% geschlossenSwiss Life Geschäftsimmobilien Schweiz 828'854'492 2.9% geschlossenSwiss Life Immobilien Schweiz 1'000'238'281 3.4% geschlossenSwisscanto Immobilien Schweiz 5'328'999'542 18.4% offenTellco Immobilien Schweiz 661'520'325 2.3% offenTuridomus Casareal (Wohnimmobilien) 2'619'810'059 9.0% geschlossenTuridomus Proreal (Geschäftsimmobilien) 738'950'012 2.5% geschlossenUBS Immobilien Schweiz 1'648'686'890 5.7% geschlossenUBS Kommerzielle Immobilien Schweiz 426'801'239 1.5% geschlossenZürich Immobilien - Geschäft Schweiz 501'866'791 1.7% geschlossenZürich Immobilien - Traditionell Schweiz 476'829'987 1.6% geschlossenZürich Immobilien - Wohnen Schweiz 1'005'689'209 3.5% geschlossenStand: 02.02.2015 29'004'202'761

Quelle: Angaben der Stiftungen, KGAST

– Begründet wird dies u.a. damit, dass zusätzliche Mittel nicht in Liegen-schaften mit gleicher erwarteter Rendite investiert werden können wie die Bestandes-liegenschaften, und die Rendite der bestehenden Anleger «verwässert» wird.

Source: PPCmetrics/KGAST

Folie 27, April 17th, 2015

Future indirect investments by type and country

?

“Real estate investments of CHF 120 bn, therefore „only“ CHF 10 bn abroad (of CHF 720 bn)”

Folie 28, April 17th, 2015

Future indirect investments by type and country

Office Retail Residential Industry Development SumSwitzerland 35 18 63 23 18 157Germany 16 9 12 9 2 48USA 13 9 11 8 5 46Asia 12 10 10 9 4 45Northern?Europe 13 11 8 9 3 44UK 7 5 5 5 3 25Belgium/?Netherlands/Lux. 7 4 6 5 2 24France 5 3 5 4 1 18Others 5 5 3 3 1 17Austria 4 2 4 2 0 12Spain 2 2 3 2 0 9Italy 2 2 3 2 0 9Eastern?Europe 2 1 2 1 1 7Latin?America 1 1 2 2 1 7Sum 124 82 137 84 41 468

Folie 29, April 17th, 2015

Criteria for the selection of an asset management for indirect real estate investments

*"""""highly"significant"**"""significant"***"significance"<"10%"

1,0$

1,5$

2,0$

2,5$

3,0$

3,5$

4,0$

Experience$of$the$REAM/track$record*$

Number/type$of$other$mandates$of$REAM

$

Costs$of$the$REAM$

StructureE/management$compentencies*$

TailorEm

ade$soluIons$

CompensaIon$(perform

ance$based)$

Image/reputaIon$of$the$m

anager$

Geographic$presence$of$the$m

anager***$

Distance$of$the$unit$to$the$REAM$

EquityEinvestment$of$the$REAM

$

Contract$duraIon**$

ImplementaIon$of$the$contract$in$the$staffE

Corporate$governance/legal$structures$of$the$REAM

*$

Foreign$investements$unimportant$(n$=$8)$ DiversificaIon$and$new$markets$(n$=$24E29)$ Indirect$investments$important$(n$=$47E52)$

1"="very"important"2"="important"3"="neutral"

4"="unimportant"5"="very"unimportant"

Folie 30, April 17th, 2015

Characteristics of a “perfect” investment vehicle

*"""""highly"significant"**"""significant"***"significance"<"10%"

1"

1,5"

2"

2,5"

3"

3,5"

4"

4,5"

5"

Leading"market"posi6on"

Cri6cal"mass*"

Focus"on"certain"types"

Focus"on"certain"regions***"

Ac6ve"m

anagement"(buyBandBsell)"

Passive"management"(buyBandBhold)"

Efficient"cost"structure"

Investments"in"developments"

Strong"basis"in"homeBmarket"

Expansion"of"domes6c"m

arket**"

Investments"in"em

erging"markets/loca6ons"

Use"of"real"estate"cycles"

Internal"growth"(via"porOolio)***"

External"grow

th"(M&A)"

Transparency/interna6onal"repor6ng"

Foreign"investements"unimportant"(n"="9B10)"Diversifica6on"and"new"markets"(n"="24B28)"Indirect"investments"important"(n"="50B53)"

1"="very"important"2"="important"3"="neutral"

4"="unimportant"5"="very"unimportant"

Folie 31, April 17th, 2015

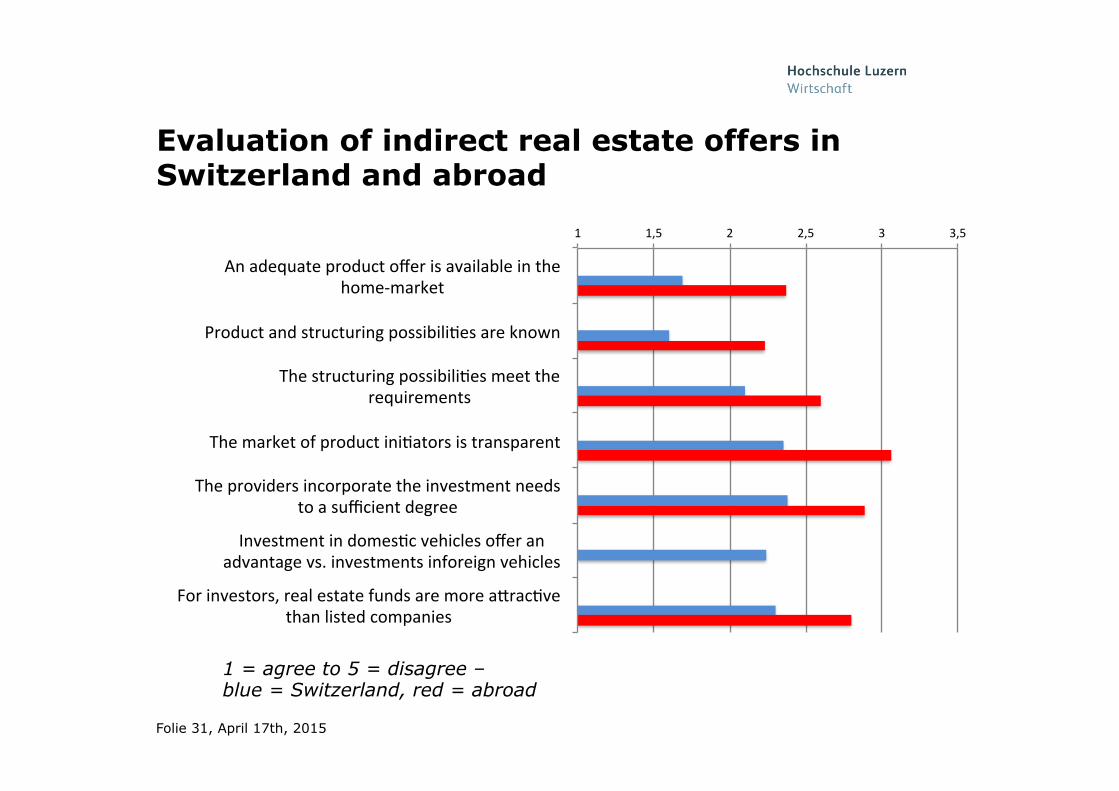

Evaluation of indirect real estate offers in Switzerland and abroad

1" 1,5" 2" 2,5" 3" 3,5"

An"adequate"product"offer"is"available"in"the"home;market"

Product"and"structuring"possibili?es"are"known"

The"structuring"possibili?es"meet"the"requirements"

The"market"of"product"ini?ators"is"transparent"

The"providers"incorporate"the"investment"needs"to"a"sufficient"degree"

Investment"in"domes?c"vehicles"offer"an"advantage"vs."investments"inforeign"vehicles"

For"investors,"real"estate"funds"are"more"aGrac?ve"than"listed"companies"

1 = agree to 5 = disagree – blue = Switzerland, red = abroad

Folie 32, April 17th, 2015

Agenda

1 Introduction and current trends 2 Empirical results for direct real estate investments 3 Empirical results for indirect real estate investments 4 Summary and outlook

Folie 33, April 17th, 2015

Summary

Direct investments - 3 clusters could be derived - Organization of REAM-tasks differ - The use of software is on a („relatively“) low level

Indirect investments - 3 clusters could be derived - Swiss Investment Foundations are preferred for investments in

Switzerland, followed by listed vehicles - Investments abroad are conducted with a multitude of different

vehicles - Swiss institutional investors want to diversify, BUT prefer to

invest in Switzerland – in the past and in the future - The “perfect” vehicle is a cost-efficient and focused vehicle –

growth-aspects are not required - The Swiss market is valued with a higher transparency than

other markets offers many suitable products

Folie 34, April 17th, 2015

Summary: Clusters

indirect

direct

national international

Generalist

Strategists

Delegates

Foreign investments unimportant

Diversification and new markets

Indirect investments important

Folie 35, April 17th, 2015

... literature

Trübestein Hrsg.

Michael Trübestein Hrsg.

Real Estate Asset Management

Das Interesse an direkten und indirekten Immobilieninvestitionen im Inland und Aus-land ist bei institutionellen Investoren seit Jahren ungebrochen. Damit einhergehend nehmen die Strukturierung und das Management der Immobilieninvestitionen einen immer wichtigeren Stellenwert ein bzw. die damit verbundene Auswahl, Führung und Steuerung eines internen und/oder externen Asset Managers. Aufbauend auf den Ergebnissen einer Studie zum Real Estate Asset Management in der Schweiz, Deutschland und Österreich werden der derzeitige Stand des Immobilienmanagements analysiert sowie Handlungsempfehlungen abgeleitet.

Das Fachbuch umfasst neben den detaillierten Studienergebnissen ausgewählte Artikel zu verschiedenen Aspekten der Immobilienanlage und richtet sich gleichermaßen an Investoren, Produktanbieter und Wissenschaftler.

Der Inhalt umfasst u. a. • Struktur und Funktionsweise von Pensionskassen • Herausforderungen bei der direkten und indirekten Immobilienanlage • Internationale Immobilienstrategien • Immobilieninvestitionen und Anlageverhalten institutioneller Investoren • Studienergebnisse zu Immobilienmanagement, Organisationsstrukturen,

Anlagestrategien und Anlageschwerpunkten bei direkten und indirekten Immobilieninvestitionen institutioneller Investoren in der Schweiz, Deutschland und Österreich

Der HerausgeberProfessor Dr. Michael Trübestein ist Professor für Immobilienmanagement an der Hochschule Luzern mit den Schwerpunkten Real Estate Investment und Real Estate Asset Management.

Real Estate Asset Managem

ent

1 Real Estate Asset ManagementStudienergebnisse zu direktenund indirekten Immobilieninvestitionenin der Schweiz, Deutschland und Österreich

ISBN 978-3-658-08783-8

9 783658 087838

Trübestein Hrsg.

Michael Trübestein Hrsg.

Real Estate Asset Management

Das Interesse an direkten und indirekten Immobilieninvestitionen im Inland und Aus-land ist bei institutionellen Investoren seit Jahren ungebrochen. Damit einhergehend nehmen die Strukturierung und das Management der Immobilieninvestitionen einen immer wichtigeren Stellenwert ein bzw. die damit verbundene Auswahl, Führung und Steuerung eines internen und/oder externen Asset Managers. Aufbauend auf den Ergebnissen einer Studie zum Real Estate Asset Management in der Schweiz, Deutschland und Österreich werden der derzeitige Stand des Immobilienmanagements analysiert sowie Handlungsempfehlungen abgeleitet.

Das Fachbuch umfasst neben den detaillierten Studienergebnissen ausgewählte Artikel zu verschiedenen Aspekten der Immobilienanlage und richtet sich gleichermaßen an Investoren, Produktanbieter und Wissenschaftler.

Der Inhalt umfasst u. a. • Struktur und Funktionsweise von Pensionskassen • Herausforderungen bei der direkten und indirekten Immobilienanlage • Internationale Immobilienstrategien • Immobilieninvestitionen und Anlageverhalten institutioneller Investoren • Studienergebnisse zu Immobilienmanagement, Organisationsstrukturen,

Anlagestrategien und Anlageschwerpunkten bei direkten und indirekten Immobilieninvestitionen institutioneller Investoren in der Schweiz, Deutschland und Österreich

Der HerausgeberProfessor Dr. Michael Trübestein ist Professor für Immobilienmanagement an der Hochschule Luzern mit den Schwerpunkten Real Estate Investment und Real Estate Asset Management.

Real Estate Asset Managem

ent

1 Real Estate Asset ManagementStudienergebnisse zu direktenund indirekten Immobilieninvestitionenin der Schweiz, Deutschland und Österreich

ISBN 978-3-658-08783-8

9 783658 087838

UBS Anlagestiftungen

n „Recommendation“: Please send me an email to: [email protected]

Folie 36, April 17th, 2015

Thank you for the support !

Folie 37, April 17th, 2015

Thank you for the support !

UBS Anlagestiungen

Folie 38, April 17th, 2015

Thank you

for your attention!

Questions ?

Folie 39, April 17th, 2015

Backup

Folie 40, April 17th, 2015

Structure of the sample: Dominance of pension funds in the sample

- In the sample, pension funds obtain a dominant position with over 80 % of the analysed quesionnaires

- Clusting based on investment behaviour targeting

Aufteilung der Stichprobe

Institutionen AnzahlPensionskassen

Lebensversicherungsunternehmen

Immobilien-Dienstleister

Stiftungen

Sonstige

Mehrere

Pensionskassen 101Lebensversicherungsunternehmen 2Immobilien-Dienstleister 5Stiftungen 12Sonstige 3Mehrere 3Gesamt 126

Anzahl Mittelwert Minimum Maximum Standard- Abweichung

Gesamte Kapitalanlagen im Jahr 2010 117 2.922 0,18 146.292 13.988Gesamte Kapitalanlagen im Jahr 2013 125 3.525 0,21 133.444 13.617Wachstum Kapitalanlagen bis 2016 (in %) 69 11 –15 100 19Immobilienanlagevermögen im Jahr 2010 114 407 0,1 5.100 841Immobilienanlagevermögen im Jahr 2013 120 473 0,1 6.750 986

Folie 41, April 17th, 2015

Teil A: Immobilienanlagen im Überblick

nein janein 15 49 64ja 20 68 88

35 117 152

direkt

Gesamt

Anzahl

indirekt

Gesamt

Wachstum der Immobilienanlagen (2010 – 2016): Inland direkt (+25%), Inland indirekt (+42%), Ausland indirekt (+39%), aber verlangsamtes Wachstum

Folie 42, April 17th, 2015

General information of the clusters

Total&investments&(2013) (Stand.6Dev.) Investments&in&

real&estate&(2013) (Stand.6Dev.)

Strategists&(n&=&16) 11,559 33,670 698 927Generalists&(n&=&33) 4,531 10,921 901 1,584Delegates&(n&=&19) 1,455 2,353 304 461Total&(n&=&68) 5,325 18,058 686 1,230

- (very) heterogeneous groups - Different capital and real estate volumes in the clusters

Folie 43, April 17th, 2015

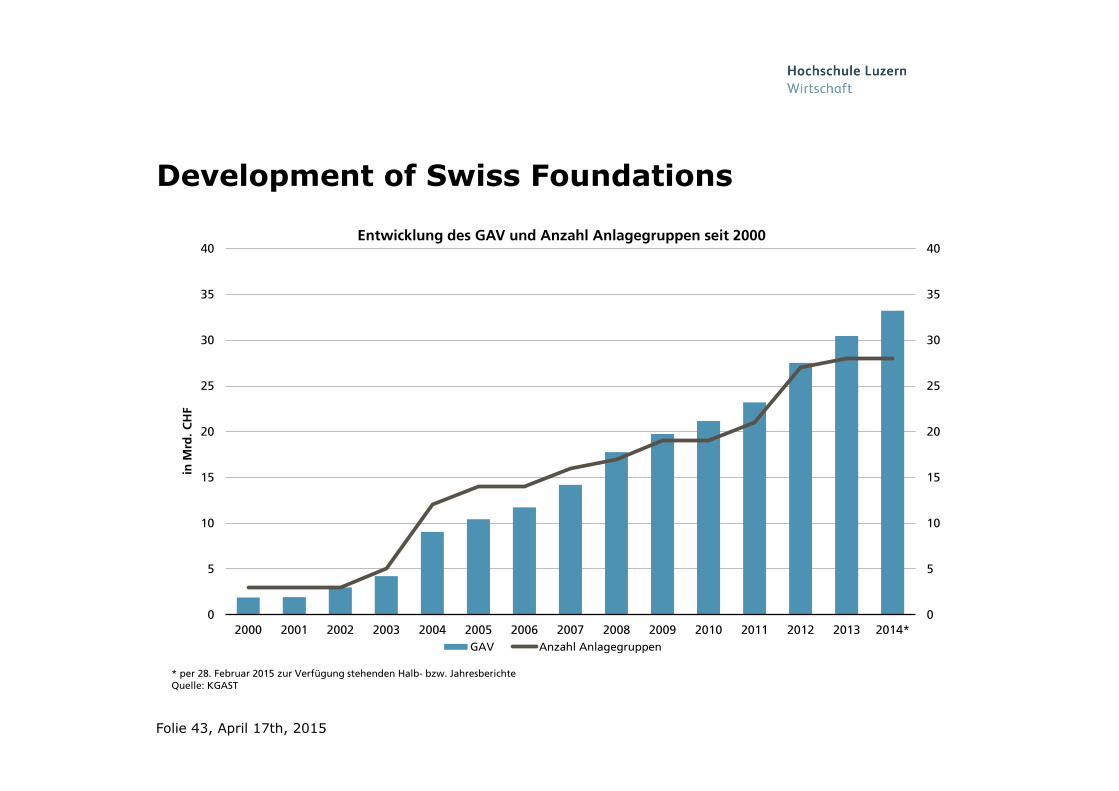

Development of Swiss Foundations

8

Entwicklung der Schweizer Immobilienanlagestiftungen Verdreifachung des GAV seit 2005

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

in M

rd. C

HF

Entwicklung des GAV und Anzahl Anlagegruppen seit 2000

GAV Anzahl Anlagegruppen

* per 28. Februar 2015 zur Verfügung stehenden Halb- bzw. Jahresberichte Quelle: KGAST

8