Embed Size (px)

Citation preview

November 10, 2004 British Columbia Utilities Commission Sixth Floor - 900 Howe Street Vancouver, B.C. V6Z 2N3 Attention: Mr. Robert J. Pellatt, Commission Secretary Dear Sir: RE: Terasen Gas (Vancouver Island) Inc. (“TGVI”)

Review of Resource Plan and an Application for a Certificate of Public Convenience and Necessity (“CPCN”) for a Liquefied Natural Gas Storage Project Hearing Exhibits

Terasen Gas (Vancouver Island) Inc. respectfully submits the following exhibits for the hearing:

• List of Panel Members and Panel Issues • Witness Data • Stakeholder Workshop Presentation for October 22, 2004

Twenty hard copies of the attached will be sent to the Commission office by Friday, November 12, 2004. Yours very truly, TERASEN GAS (VANCOUVER ISLAND) INC. Original signed by Tom Loski

For: Scott A. Thomson Attachment cc. Registered Intervenors

Scott A. ThomsonVice President, Finance & Regulatory Affairs 16705 Fraser Highway Surrey, B.C. V3S 2X7 Tel: (604) 592-7784 Fax: (604) 592-7890 Email: [email protected] www.terasengas.com

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST

APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

WITNESS PANEL MEMBERS

Panel Panel Name Witness Title

Cynthia Des Brisay Director, Business Development

David Bennett Director, Energy Management Services

1 Resource Plan

James Wong Manager, Forecasting

Bill Manery Director,

Project Assessment

Guy Wassick Project Manager, LNG

Gareth Jones Manager, Project Assessment

2 Technical

Mike Davies Manager, Business Development

Douglas Stout Vice President,

Gas Supply and Transmission

Cynthia Des Brisay Director, Business Development

Mike Davies Manager, Business Development

David Bennett Director, Energy Management Services

3 Project Justification

Tom Loski Director, Regulatory Affairs

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

WITNESS PANEL ISSUES

Panel Panel Name Issue

1 Resource Plan

RP1. TGVI Resource Planning Process RP2. Resource Plan Objectives and Measures RP3. Design Day, Design Year and Normal Year Demands for Core Market RP4. Core Market Annual Demand Forecast RP5. Load Forecasts for Other Customers RP7. DSM Programs RP8. Pipeline to Whistler

2 Technical

LNG1. LNG Site Selection LNG2. LNG Facility LNG3. LNG Project LNG6. Development of Resource Addition Portfolios

3 Project Justification

RP6. Industrial Curtailment and Peaking Supply LNG4. System Balancing & Other Benefits LNG5. Contractual Commitments LNG7. Analysis of Resource Addition Portfolios LNG8. Rate Impacts

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Cynthia Des Brisay

TITLE: Director, Business Development; Gas Supply & Transmission

PANEL # 1 and 3

EDUCATION / WORK BACKGROUND B. Engineering in Chemistry, Queen’s University MBA, University of B.C. Employed with Terasen Gas over the past 5 years, with prior experience in the energy sector.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: David Bennett

TITLE: Director, Energy Management Services; Gas Supply & Transmission

PANEL # 1 and 3

EDUCATION / WORK BACKGROUND B. Sc. in Economics and Computer Science, University of Victoria Employed with Terasen Gas and predecessor companies, and held previous positions in Marketing, Planning, and Gas Supply. Previously testified before the British Columbia Utilities Commission.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: James Wong

TITLE: Manager, Forecasting; Marketing

PANEL # 1

EDUCATION / WORK BACKGROUND MBA, Simon Fraser University B. Comm., University of British Columbia Certified General Accountant Employed with Terasen Gas and predecessor companies for 13 years, and held previous positions in Finance, Gas Supply and Marketing.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Bill Manery

TITLE: Director, Project Assessment; Gas Supply & Transmission

PANEL # 2

EDUCATION / WORK BACKGROUND B. Sc. in Mechanical Engineering, University of Calgary, 1969 Professional Engineer, Association of Professional Engineers and Geoscientists of B.C. Employed with Terasen Gas and predecessor companies, and held previous positions in Operations and Engineering. Project Director for the Southern Crossing Pipeline Project completed in 2000. Previously testified before the British Columbia Utilities Commission.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Guy Wassick

TITLE: Project Manager, LNG; Gas Supply & Transmission

PANEL # 2

EDUCATION / WORK BACKGROUND B.A.Sc. in Mechanical Engineering, University of B.C., 1976 Professional Engineer, Association of Professional Engineers and Geoscientists of B.C. Employed with Terasen Gas and predecessor companies, and held previous positions in Operations and Engineering. Project Manager for the compressor installations for the Southern Crossing Pipeline Project and Langley Compressor, both completed in 2000.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Gareth Jones

TITLE: Manager, Project Assessment; Gas Supply & Transmission

PANEL # 2

EDUCATION / WORK BACKGROUND B. Sc. in Mechanical Engineering, University of Alberta, 1981 Queen’s Executive program, Queen’s University, 1998 Professional Engineer, Association of Professional Engineers and Geoscientists of B.C. Professional Engineer, Association of Professional Engineers, Geologists and Geophysicists of Alberta Employed with Terasen Gas and predecessor companies for 14 years, and held previous positions in Operations and Engineering. Previously testified before the British Columbia Utilities Commission.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Michael Davies

TITLE: Manager Business Development

PANEL # 2 and 3

EDUCATION / WORK BACKGROUND MBA, Simon Fraser University B. A. Sc. in Mechanical Engineering, University of B.C. Professional Engineer, Association of Professional Engineers and Geoscientists of B.C. Employed with Terasen Gas and predecessor companies for 14 years.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Douglas Stout

TITLE: Vice President, Gas Supply & Transmission

PANEL # 3

EDUCATION / WORK BACKGROUND MBA, University of Alberta B.Sc. in Civil Engineering, University of Alberta Employed with Terasen Gas over the past 3 years, with prior experience in the energy sector. Previously testified before the British Columbia Utilities Commission.

TERASEN GAS (VANCOUVER ISLAND) INC.

RESOURCE PLAN FOR VANCOUVER ISLAND AND SUNSHINE COAST APPLICATION FOR A CERTIFICATE OF PUBLIC CONVENIENCE AND NECESSITY

FOR A LIQUEFIED NATURAL GAS STORAGE PROJECT

NOVEMBER 17 – 26, 2004 HEARING NANAIMO, BC

Witness Data

NAME: Tom Loski

TITLE: Director, Regulatory Affairs

PANEL # 3

EDUCATION / WORK BACKGROUND

Certified Management Accountant, 1985 Diploma of Technology – Finance Option, BCIT, 1980 Employed with Terasen Gas and predecessor companies for 22 years, and held previous positions in Gas Supply, Finance and Marketing. Previously testified before the British Columbia Utilities Commission.

Contact Information Tom LoskiDirector,Regulatory Affairs

Tel: (604) 592-7464Fax: (604) 592-7890E-mail: [email protected]

Terasen Gas (Vancouver Island) Inc. Resource Plan and LNG Storage

Project CPCN Application

Stakeholder WorkshopFriday, October 22, 2004

Vancouver, B.C.

2

Workshop Agenda Introduction Tom Loski 5 minsOverview Doug Stout 15 minsLNG Plant Bill Manery/Guy Wassick 25 minsQuestions 15 minsResource Planning Process James Wong 10 minsCore Demand Forecast James Wong 20 minsTransport Customer Forecast David Bennett 15 minsQuestions 15 minsResource Portfolios Mike Davies 20 minsGas Supply Benefits & LNG Services David Bennett 20 minsFinancial Justification Cynthia Des Brisay 20 minsQuestions 15 minsNext Steps Tom Loski 10 mins

Guy WassickProject Manager, LNG

Bill ManeryProject Director, LNG

Terasen Gas(Vancouver Island) Inc.

LNG Project

2

Agenda

• LNG Industry in General• Site Selection and Public Consultation• Environmental Assessment• LNG Process and Design• Project Schedule• Project Cost• Project Contracting

3

What Is LNG?

• LNG (liquefied natural gas) is natural gas cooled until it condenses into a clear liquid.

• LNG is stored at -162o Celsius (-260o F) at atmospheric pressure in a “thermos” like storage container.

• LNG takes up far less space – about 1/600th of its original volume as a gas.

• LNG (the liquid itself) is not flammable or explosive.

• When LNG is warmed it evaporates and becomes a lighter-than-air gas and is flammable only when it occurs in a 5% to 15% concentration in air.

4

Types of LNG Storage

• Peak ShavingSmall storage capacity, send out only on peak days, connected to a pipeline with liquefaction and vaporization capability

• Base Load, Import/Export TerminalLarge storage capacity, liquefaction or send out every day, supplied to/by marine tanker with either liquefaction or vaporization capability

• Satellite PlantsFor peaking or smaller base load send out, supplied by truck transport, with vaporization capability only

• Transportation FuelCars, trucks, buses

5

The LNG Industry

• There are over 240 LNG storage facilities operating in the world.

• In North America there are approximately 110 peak shaving facilities (3 located in Canada) and 4 import/export terminals.

• LNG storage tanks are insulated tanks, operating at atmospheric pressure and constructed of 9% nickel steel; no tank of this design has failed in service anywhere in the world.

6

LNG Plants – North America

7

Tilbury Island (Delta, B. C.)“Peak shaving” LNG Plant (1970) - 0.6 bcf

8

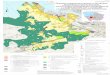

Site Selection Process

• Terasen Gas examined a strip of land 5 km on either side of the main natural gas transmission pipeline from the Courtenay area down to the Langford area to locate a storage facility of up to 1.5 bcf.

• Based on this analysis, 25 potential sites were identified.

• Further analysis of slope, geotechnical characteristics, view sheds and pipeline system hydraulics reduced potential sites to seven, then to three.

9

7 - Short Listed Sites

10

Final Site – Near Ladysmith

LNG Storage

• Proposed facility– Storage 1bcf– Send-out 100

mmcf/d– Liquefaction

5mmcf/d

• 6km NW of Ladysmith, West of Mt. Hayes

• Located near load center on Southern Vancouver Island

11

Storage Plant Location

12

Consultation Process

TGVI undertook a comprehensive public consultation process over a period of 12 months which included the following key elements.

• Letters to stakeholders• Meetings with and presentations to stakeholders• 2 focus groups • 3 Open Houses• CVRD sponsored Public Meeting • Environmental and Social Review (ESR)• CVRD Public Hearing

Site re-zoning approved by CVRD May 26/04

13

Storage Plant Site Details

New zone is U-1, LNG Storage Utility

• 42.7 ha rezoned• 12 ha plant site• 20 ha, western and eastern buffers, beyond

rezoned area will be retained in forestry operations

• Total 82 ha owned or controlled by TGVI

Zoning allows up to 2 – 1.5 bcf tanks; future expansion could occur on the site

14

Private Property Purchased

Property to be purchased

142 ha

15

Rezoned Area

42 ha

Rezoned

Area

16

Proposed Storage Plant Area

Plant area

12 ha

17

Total Land Owned or Controlled

Exclusion Zone

Total area 82 ha

18

Environmental Assessment:Key Human Impact Findings

Location of the site in an isolated area mitigates most human and safety impacts

• 3 km from facility to nearest dwelling• Traffic effects on existing roads limited to

construction period• Little impact on forestry or recreation• Aesthetics and noise impacts minimal

-3 kms to nearest dwelling-Landscape is already heavily disturbed

• Domestic water supplies unaffected-Outside of aquifer recharge areas

19

Environmental Assessment:Key Biophysical Findings

The site is privately owned and has already been disturbed, reducing impacts on physical and biological environment

• Site is mostly clearcut• Site is geologically stable• Aquatic and vegetation impacts can be mitigated• Intermittent streams (non fish bearing) will be

channelized, a pond created, replacing the present bog

• No effect on fish• Little effect on wildlife

20

Economic Impacts

LNG facility will positively impact and help to diversify the existing economy.

Total construction expenditures $94.4 Million• $28.7 M of local expenditures, $41.7 in British

Columbia • 240 local jobs (100 direct, 140 indirect, induced)

Facility operation provides 9 full-time jobs• $150,000/year in goods and services expenditures• $300,000/year in property taxes

21

Site PhotographMt. Hayes in background - view to east

Tank Location

22

Artist Rendering

23

Tilbury Island (Delta, B. C.)“Peak shaving” LNG Plant – 0.6 bcf

24

Major Components OfPeakshaving LNG

• Liquefaction(freezer)

• Storage(thermos)

• Vaporization(hot water tank)

Preheater

Boil-off Compressor

LNG Vaporizers

LNG Tank

LNG TankerUnloading &Loading

to TransmissionPipeline System

LNG Pumps

Feed Gas

Tail Gas

DessicationLiquefaction

25

Design/Safety Features

• Insulated, non pressurized, 9% nickel steel inner tank (like a thermos)

• 100% secondary containment around tank• Controlled buffer zone around facility • Safeguard systems (eg: fire/smoke/gas

detection, automatic/remote control, manned full time) designed for isolation/containment and shut-down

• Fire water system, water deluge and dry chemical extinguishers

LNG facilities are designed to isolate, contain and shut down.

26

Typical 9% Nickel Steel Tank Design

27

Artist Rendering

28

TGVI Project “Pre-approval” Schedule

ID Task Name Duration

1 LNG STORAGE FACILITY 21.82 mons2 GENERAL ENG. & SPEC. DEVELOPMENT 8 mons3 SITE SELECTION incl. ENVIR'N ASSESSMENT 9 mons4 SITING AND ZONING APPROVAL 4.7 mons5 SITE ACQUISITION (Option & Purchase) 2.7 mons6 CONTRACTOR SELECTION 4.8 mons7 CONTRACTOR DESIGN & PRICE 4 mons8 CPCN PROCESS 5.5 mons9 BCUC APPROVAL 0 mons

Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 12004 2005

29

Comparable LNG Storage Project Schedules

Actual peak shaving projects– Memphis Gas – 1996 1.0 bcf 29 mth– Williams (Pine Needle) – 1998 2 X 2.0 bcf 29 mth

Proposed peak shaving projects– BC Gas – 1996 2.0 bcf 25 – 30 mth– PGT – 1996 2.0 bcf 24 – 30 mth– WGSI – 1997 3.0 bcf 28 mth– Williams – 1997 3.0 bcf 24 mth

Other– Contractors 2003 Estimates 28 – 29 mth.– CBI 2004 Negotiated 28 mth.

30

TGVI Project Construction Schedule

ID Task Name Duration

1 LNG STORAGE FACILITY 33.97 mons2 BCUC APPROVAL 0 mons3 AWARD EPC CONTRACT 0.2 mons4 DETAIL DESIGN - TANK 8 mons5 DETAIL DESIGN - PROCESS & CONTROLS 20 mons6 PURCHASE TANK MATERIALS 12 mons7 PURCHASE PROCESS EQUIPMENT 16 mons8 SITE & ROAD PREPARATION 3 mons9 CONSTRUCTION - TANK 22 mons10 CONSTRUCTION - PROCESS & CONTROLS 19 mons11 EPC CONSTRUCTION CONTINGENCY 2 mons12 CONSTRUCTION - POWER LINE 3 mons13 CONSTRUCTION - PIPELINES 3 mons14 COMMISSIONING 2.7 mons15 COMMERCIAL OPERATION 0 mons16 PERFORMANCE TESTING 2 mons17 OPERATION & PARTIAL FILL 3 mons18 RESTORATION 4 mons

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q12005 2006 2007 2008

31

Outstanding Approvals

• OGC Notice to Construct• OGC license of occupation and license to cut• MWLAP Approval to construct pond• MWLAP Air emissions permit • Other minor permits (building, highway access,

etc)

32

TGVI Project Capital Cost – 2004$

Capital Cost, $000

EPC Total $73,800Land $1,600

Interconnects $9,300Proj. Services $7,900

Contingency $1,800CDN$ $94,400

33

Comparable LNG Project Costs

Actual peak shaving projects 2004$million• Memphis Gas–1996 1.0 bcf 81• Williams (Pine Needle)–1998 2 X 2.0 bcf 178

Proposed peak shaving projects• BC Gas – 1996 2.0 bcf 110• PGT – 1996 2.0 bcf 110• WGSI – 1997 3.0 bcf 147• Williams – 1997 3.0 bcf 99

TGVI – 2004 1.0 bcf 94.4

34

EPC Contracting Process

EPC contracting is the norm for process facilities where the construction contractor is also the designer

• 2003 – Contact with 8 potential LNG Contractors• Mar 2004 – Request for Expression of Interest • May 2004 – Evaluation

– 4 teams of interest• Corporate and Financial Strength• Organization• Experience and Performance

– 2 “qualified” contractor teams identified

35

EPC Contracting Process

Decision to Negotiate

EPC Bidding difficult due to;• lack of bidders • high bidders costs• detailed scope and contract leads to non-

compliance, no bids and/or high bids• significant negotiation on scope, price and

contract after bidding

36

EPC Contracting Process

Negotiated contract allows owner to;• Negotiate assignment of project risks (e.g.

insurance, exchange, etc.)• Negotiate pricing fixed elements (e.g. profit,

administration, etc.)• Be part of the scoping and design• View open book bids for equipment/components

and subcontracts• Minimize contractor contingencies

37

EPC Contracting Process

Jun to Aug 2004 – Negotiation– Contract terms– Price development method– Contractor team & execution strategy– Selection of “Chicago Bridge & Iron”

Sep 2004 to Jan 2005 – Design & price development– Document scope and guarantees– Receive EPC price

January 2005 – CPCN Approval– Award EPC Contract

38

EPC Contractor:Chicago Bridge & Iron

One of the worlds leading Low-Temp/LNG design/builders with over 50 years experience. Currently doing US$1.2 billion/yr

• Over 40 LNG Terminals and Peak shaving plants

• Over 120 LNG Tanks• Built last 2 N.A. LNG Peak shaving plants• Awarded Yankee Gas (Oct. 2004 1.2 bcf p/s)• Full Scope of EPC Services In-House• HortonCBI – Canadian Subsidiary

Contact Information James WongManager, Forecasting

Tel: (604) 592-7871E-mail: [email protected]

TGVI Resource Planning Process

2

Evaluating the Portfolio Alternatives

Objective Attribute Measure Ensure reliable and secure supply.

System reliability Security of supply

Risk of outages Gas supply diversity

Provide service to customers at least delivered cost.

Financial evaluation of supply side and demand side resources

Net Present Value Total Resource Cost (TRC) Ratepayer Impact (RIM)

Reduce rate volatility. Expected rates Risk trade-offs Balance socio-economic and environmental impacts.

Social costs / benefits including: Local emissions Greenhouse gas Land use impacts Employment/local

economic impacts Stakeholder consultation

Air pollutants Quantity of CO2 equivalent Area impacted Jobs created

Stakeholder input

3

LNG is the Preferred Resource

• Demand growth presents opportunity to improve energy infrastructure

• LNG Storage is the preferred portfolioImproves security of supplyLowest cost for expected range of demandPart of a phased solution that will support economic growth

TGVI LNG Pipe PipePlanning Storage Compression CompressionObjective Curtailment

Ensure reliable secure supplyLowest delivered costReduce long-term volatilityBalanced impacts

Contact Information James WongManager, Forecasting

Tel: (604) 592-7871E-mail: [email protected]

TGVI Core Market –Peak Demand Forecast

5

Definitions, inputs and drivers

Core Market – residential, commercial and small industrial customers that have gas purchased and delivered to their home or business. Design Year – The year which experienced the coldest day in the last 25 years.Design Day – The coldest day in the last 25 years – i.e. February 2, 1989

Gross Squamish Demand High Base Low High Base Low ICP + 0 ICP + 20 ICP + 45 Yes Yes NoHigh-High ● ● ● ● ●Base + 45 ● ● ● ● ●Base + 20 ● ● ● ● ●Base + 0 ● ● ● ● ●Low-Low ● ● ● ● ●

Core Customers Joint Venture Generation (ICP + CFT) Whistler

Gross Demand Scenarios – Base, High, and Low

6

Definitions, inputs and drivers

Inputs and DriversCustomers• Annual Additions – Customer Growth

• New versus Conversion Customers• Total Number of Customers in a Year

Peak Use Rate per Customer– the maximum demand for natural gas from a customer on a

single day

7

Forecasting Methodology –Customer Growth

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1991 1996 2001 2006 2011 2016 2021 2026

Cus

tom

ers

(Lin

e C

hart

)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Cus

tom

er A

dditi

ons

(Bar

Cha

rt)

Transition

Base - Maintain competitive position and economic growth is stable

High - Competitive position inproves and economy grows

Low - Competitive position worsens and economic growth is poor

ForecastActual

3.1% CAGR

3.8% CAGR

2.4% CAGR

33.4% CAGR

CAGR - Compound Annual Growth Rate

4.7% CAGR

Implementation Maturity

2.0% CAGR

Base – 98,000 cust; 119 TJ/dayHigh – 103,000 cust; 139 TJ/dayLow – 94,000 cust; 107 TJ/day

Base – 132,000 cust; 160 TJ/dayHigh – 140,000 cust; 187 TJ/dayLow – 126,000 cust; 144 TJ/day

Resource Plan reference, page 19 - Figure 3-5. Core Customer New Account Growth in Three Market Phases

8

Forecasting Methodology –Customer Growth

Look at recent years growth experience ~ 3,000 per year

Customer Additions2000 - 2004

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004

# of

Cus

tom

ers

Forecast ~ 2,400/year

OR

55,000 total

FROM

2004-2026

9

Market Segments - Conversions

Conversion Activity – Last Five Years

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1999 2000 2001 2002 2003

# of

Con

vers

ions

10

Market Segments - Conversions

Conversion Potential"On-Main"

Remaining Conversion

Potential27,000

Forecasted Conversions

28,0002004 - 2026

~ 55,000 On-Main Potential Customers

11

Market Segments –New Construction

New Construction Installations to Housing Starts

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1992 1995 1998 2001 2004 2007 2010 2013 2016 2019 2022 2025

New Construction Housing Starts

12

Market Segments –New Construction

Natural Gas Market Capture of New Housing Starts

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

110.0%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

New

Con

stru

ctio

n C

usto

mer

s pe

r New

Hou

sing

Sta

rt

Increased Market capture for forecast horizon

Market capture for forecast horizon

13

Peak Use Rate per Customer

Statistical method –Regression Analysis used

* 1997 to 2001 data used

Scatter(Oct 97 through Dec 01)

y = 0.0377x + 0.1421R2 = 0.9149

0.00.10.20.30.40.50.60.70.80.91.01.11.21.3

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

HDD

UPC

(GJ)

14

Peak Use Rate per Customer

Updated recently –

similar results

* 1997 to 2003 data used

Scatter(Oct 97 through Dec 2003)

y = 0.0362x + 0.144R2 = 0.9109

0.00.10.20.30.40.50.60.70.80.91.01.11.21.3

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

HDD

UPC

(GJ)

Design

15

Peak Use Rate per Customer

Is it a “reasonable” model?

Recent results……. say “Yes”

Regression EquationCore Market Y intercept Slope Heating Forecast Difference Act vs Fcst

Day of Deliveries Non temp sensitive load Temp sensitive load Deg Days Core Market Core Load Act vs Fcst DifferenceDate Week (gigajoules) (UPC) (UPC / DDD) (HDD) (Customers) (gigajoules) (gigajoules) (%)

3-Jan-04 Saturday 76,238 0.1421 0.0377 19.3 76,533 66,488 9,750 14.7%4-Jan-04 Sunday 77,695 0.1421 0.0377 24.0 76,533 79,981 (2,286) -2.9%5-Jan-04 Monday 76,760 0.1421 0.0377 22.9 76,533 77,045 (285) -0.4%6-Jan-04 Tuesday 69,704 0.1421 0.0377 21.2 76,533 72,132 (2,428) -3.4%

Total 4,750

* HDD based on weighted average HDD of three regions; Victoria, Nanaimo, Comox

* BCUC IR #1, 8.5.2

16

Design Day Demand Forecast

Design Day Demand ForecastCore Market

50,000

70,000

90,000

110,000

130,000

150,000

170,000

190,000

210,000

2004 2007 2010 2013 2016 2019 2022 2025

GJs

/ da

y

Low Base High Base + Higher Mkt Capture

Transport Customer Forecast

David A. Bennett

Joint Venture

• Resource Plan Forecast(Based on consultation in the spring)

High – 40 TJ/dMid – 33.6 TJ/dLow – 20 TJ/d

• Current Indications Gas prices are higherHave seen a downward trend in usageTGVI expects energy efficiency initiatives will be more economic10-15 TJ/d longer term

BC Hydro

• ICP45 TJ/d in 2007

• CFT requirements150 MW – 300 MW RequirementBid projects mostly gas firedAnnouncement Tues October 26

• Firm Tenders

Expected Gas Demand Outcome (20 to 45 TJ/d)

BC Hydro

Bidder Name Primary Fuel Location Calpine Island Cogeneration Limited Partnership

Natural Gas Campbell River

Duke Point Power LP Natural Gas Nanaimo ENCO Power Company Natural Gas Nanaimo EPCOR Power Development Corporation Natural Gas Ladysmith EPCOR Power Development Corporation and Calpine Canada Power Ltd.

Natural Gas Nanaimo

Green Island Energy Ltd. Biomass Gold River

Contact Michael DaviesManager, Business DevelopmentTerasen Gas

Tel: (604) 592-7836E-mail: [email protected]

Gross Demand ForecastsSupply Portfolios

RP/CPCN Workshop – October 22, 2004

Summary

• Gross Demand Forecasts• Planning Criteria• Portfolio Description and Comparison Measures

Gross Demand Forecast

• How might VIGJV changes and CFT expectation effect demand?– VIGJV 10 – 15 TJ/d– CFT 20 – 45 TJ/d

• Range of expected demand narrows• New demand forecast comparable to Base+0 to Base+20

Resource PlanForecasts VIGJV BC Hydro TotalTJ/d 2007+

Base +0 34 45 79Base +20 34 65 99Base +45 34 90 124

Base +20 (JV@10) 10 65 75Base +45 (JV@10) 10 90 100

Gross Demand Forecasts

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024 2026

Year

Dem

and

(GJ)

pipeline capacitydemand history

high forecast

base forecast low forecast

Dem

and

GJ/

d

Year

Portfolios – Transmission Planning Criteria

• 20 year planning period beginning 2007 when facilities addedPresent Value of Cost of Service is the main quantitative measureReflects the revenue required to be recovered in customer rates

• Design Day and Normal Peak Day consideredDesign Day – coldest day in 25 years, with curtailmentNormal Peak Day – average coldest day, without curtailment

• Planning based on daily rather than hourly requirementsGeographic/weather diversity, ability to ‘pack’ the transmission lineTransport customers are limited to maximum 5% of daily nomination in one hour

• Construction and operating logistics are also consideredLength and phases of looping for example

Portfolios – Capital Spending Profile

LNGStorage

Base Case + 20millions 2004$

14 26 19 14

94

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

LNGCompressionPipe

14

78

1424 4418 8

34

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

1459

19 22 13 24 44

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

PipeCompression

PipeCompressionCurtailment

Comparison of incremental costs

Table 6.5.1LNG Pipe LNG Pipe

Storage Compression Storage Compression (PV 2004-2026 @ 6%, $M) Incremental Facilities 165 162 250 277 Transport Fuel Differential 4 - 22 - Gas Supply Differential (58) - (58) - LNG Mitigation (36) - (34) - Total (PV@6%) 74 162 180 277

Base +0 TJ/d Base +45 TJ/d

Table 6.5.3LNG Pipe LNG Pipe

Storage Compression Storage Compression (PV 2004-2026 @ 6%, $M) Curtailment Curtailment Incremental Facilities 163 88 245 214 Transport Fuel Differential 4 7 22 8 Gas Supply Differential (58) (35) (58) (28) LNG Mitigation (36) - (34) - Peaking Gas Mitigation (16) - (16) - Total (PV@6%) 56 60 159 195

Base +0 TJ/d Base +45 TJ/d

Gas Supply Benefits and LNG Storage Services

David A. Bennett

Electric Generation

Industrial

Residential and Commercial

1 40 81 120 161 200 241 280 365321

Coldest to Warmest Days of the Year

Nat

ural

Gas

Con

sum

ptio

n

Potential New Electric Generation

Residential and Commercial Growth

Future Requirements

TGVI Annual Load Profile

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

1-Nov

1-Dec

1-Jan

1-Feb

1-Mar

1-Apr

1-May

1-Jun

1-Jul

1-Aug

1-Sep

1-Oct

GJ/

day

Baseload Supply Seasonal Capacity Storage

Curtailment/ Interruption Design Year Demand Gas purchases

Pipeline

StorageStorage

0

10

20

30

40

50

60

70

80

90

100

110

120

1 51 101 151 201 251 301 351Days of the Year

Dem

and

(TJ/

d)

StoragePipeline

Peaking Supply

`

Average Forecast Load Requirements vs Resource Availability

Normal Demand

For illustrative purposes only

Gas Supply Portfolio Planning

Peak Day Demand

TGVI Annual Contracting Plan

2004/05 2005/06 2006/07 2007/08 Stn2 Baseload 20 20 20 20 Stn 2 Winter 5

month9 9 9 9

Hunt 5 month 8 8 10 15 Hunt 3 month 8 8 10 15 Aitken Creek 14 14 14 14 Mist/Peaking 25 30 33

LNG - - - 40 BCHydro Peaking - - - -

VIJV Peaking 18.8 18.8 16.8 -

Peak Day incl fuel 102.8 107.8 112.8 113 Peak Day net of

fuel97.7 100.4 103.9 107.3

TGVI Annual Portfolio(TJ/d)

BCUC IR 23.5

SENDOUT Optimization Model…

• Model OverviewNew Energy Associates - a wholly owned subsidiary of Siemens Westinghouse Power Corporation www.newenergyassoc.com

A Natural Gas Supply Planning Optimization System– Economic model– Optimization types: variable costs only or fixed and variable costs

Linear Programming Network Optimization Algorithm– Minimize total system cost, (the objective function), of flows along a network

subject to physical and contractual constraints (including reliability requirements)– Total System Cost = Fixed + Variable + Un-served Demand Penalty – Revenue– CPLEX Solver Engine – www.ilog.com

Deterministic Model– Optimal solution generated by looking at complete problem all at once– Assumes perfect knowledge…no uncertainty modeling– Optimal solution found via iterative process

Over 100 SENDOUT Clients (90% customers regulated)

SENDOUT Optimization Model…

Graphical Solution of a Two Variable LP

TGVI gas supply model:– 270,000 constraints, 220,000 variables, and 100,000 iterations– Setup time (including input data collection) - 3 to 4 weeks initial setup – Solution time - 15 minutes initial run, 90seconds consequent runs

-8-6-4-202468

10121416

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34

control variable 1

cont

rol v

aria

ble

2

Points at w hich constrains are boundedObjective Function ValuesConstraint Equations 1 & 2Feasible Region

Direction of improvement

TGVI Gas Supply Model…

• SENDOUT Network Structure

* Daily time steps in Chronological order

* Annual resource sizing decisions

* 20 year optimization period

Off System Sales

Storage ContractsSupply Contracts

Term/Day/Peaking

Transport Contracts/

Pipe Segments

Core Load & Temperature

TGVI Gas Supply Model…

• Scenario Structure

Pipe and Compression– Unconstrained pipe capacity to TGVI– Incremental transport (Duke) and/or storage (ACR, Mist)

LNG– Constrained pipe capacity to TGVI– LNG on TGVI (minimum take and optional)

Pipe, Compression, and Curtailment– Constrained pipe capacity to TGVI– Curtailment on TGVI (existing and optional)

TGVI Gas Supply Model…

• Summary of Portfolio Costs – Normal Year Requirements

Total Cost = Variable + Fixed – Resale Revenue – Release RevenueNormal Cost = Variable * Normal Load/Design Load + Fixed

+ (Design Load – Normal Load) * US$0.25/MMBtu

TOTAL COST (BASE + 0) - NORMAL YEAR ($Millions)

PIPE,COMPRESSION LNG

PIPE,COMPRESSION,CURTAILMENT

Fixed 145.77$ 90.32$ 106.26$ Variable 893.73$ 892.01$ 898.88$ Total 1,039.50$ 982.34$ 1,005.12$

Third Party RevenuePotential Customers

• Shippers on TGVIBC Hydro for electrical peakingOthers

• TGI• Others in Region

LDCs, electric producers

Highest value will be to those at Huntingdon or upstream because they avoid pipeline redelivery costsTGI is willing to take all capacity that TGVI does not require

TGI Supply Stack

0

200

400

600

800

1000

1200

1400

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86 91 96 101

106

111

116

121

126

131

136

141

146

151

TJ/d

LNG/Curtailment

Peaking

Stn 2/Alberta Spot / JPS/Mist

Seasonal Storage

Baseload/Seasonal

Design

Normal

Market ValuationAnnual Carrying Costs(1 GJ of Sendout)

Pipeline– 365 days X $0.40 / GJ = $150 per year

Downstream Storage– $3.50 / GJ X 30 days = $115 per year

LNG– $8 / GJ X 10 days = $80 per year

(For illustrative purposes)

Required(days) Pipeline

DSStorage LNG

10 15.00 11.50 8.0030 5.00 3.50 -

150 1.00 - -365 0.40 - -

Costs By Load Duration($/GJ)

Service Comparison Downstream Storage vs. TGVI LNG

Service Downstream Storage TGVI LNG

Reliability Dependent on pipeline grid On-system source of supply

Nomination Notice 4 GISB Cycles over two days 2 hours or less

Nomination Flexibility Subject to intraday proration Infinitely VariableLoad Following

Delivery/Redelivery Dependent on delivery/redelivery by others Firm On-system

Deliverability Declines after 50% No Decline

Injection Up to Max Withdrawal 5% of Max Withdrawal

Cost Certainty Length of contract Yes

Cycling Costs $0.40 /GJ Dependent on IT

~2 X Downstream StorageFirm

• LNG offers unique balancing and storage advantages because of its location

Contact Cynthia Des BrisayDirector, Business DevelopmentTerasen Gas

Tel: (604) 592-7837E-mail: [email protected]

TGVI LNG Storage ProjectCustomer Impacts

October 22, 2004

Introduction

• CPCN Approval sought for LNG Storage Project LNG Storage Portfolio determined to be preferred resource portfolio across range of likely demandMost cost effective portfolio which will support lowest delivered costs to customers

• Cost Allocation of LNG facility to be determined in future rate reviews

• Evaluation of Indicative burnertip and transport costs demonstrates LNG project can supports rate design objectives

Least Cost PortfolioNet Incremental Cost of ServiceBase + 45

0

5

10

15

20

25

30

35

40

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026Calendar Year

Mill

ion

$

Pipe,Compression& Curtailment

LNG Storage

Pipe &Compresion

Least Cost Portfolio

Net Incremental Cost of ServiceBase + 0

0

5

10

15

20

25

30

35

40

2008 2010 2012 2014 2016 2018 2020 2022 2024 2026Calendar Year

Mill

ion

$

Pipe, Compression& Curtailment

LNG Storage

Pipe & Compression

Customer Impacts

• TGVI Rate Design ObjectivesCompetitive Pricing versus alternate energiesLong term financial sustainability

• Centra (TGVI) Rate Design DecisionSoft Cap MechanismRDDA Amortization and Allocation

• Indicative Burner tip costs and Transport CostsBased on current rate design principlesBased on Allocation of LNG Storage Facility in similar fashion as transmission assets

LNG Facility Benefits

➼➼Reliability & Security

➼➼Gas Supply Benefits

➼➼Avoided Facility Costs

➼➼Efficient Use of Existing Transmission System

TransportCoreBenefits

➼ Direct ➼ In-Direct

Indicative Burner Tip Rates

Demand Scenario - Base +0 LNG

$-

$5.00

$10.00

$15.00

$20.00

$25.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

$ pe

r GJ

Del

iver

ed

Average Cost of GasAverage Delivery MarginHeating Oil Equivalent90% Residential Electric

Residential Customer (RGS)Allocated Cost $ per GJ

BCUC IR 47.7

Indicative Transport CostsDemand Scenario - Base + 0 LNG

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Dem

and

Cha

rge

$ pe

r GJ/

d

Allocated Unit Cost / GJ

Allocated Unit Cost x 1.25 R/C

Firm TransportationAllocated Cost $ per GJ/d Capacity

BCUC IR 47.7

Indicative Burner Tip Rates

Demand Scenario - Base + 45 LNG

$-

$5.00

$10.00

$15.00

$20.00

$25.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

$ pe

r GJ

Del

iver

ed

Average Cost of Gas

Average Delivery Margin

Heating Oil Equivalent

90% Residential Electric

Residential Customer (RGS)Allocated $ per GJ

BCUC IR 47.8

Indicative Transport Costs

Demand Scenario - Base + 45 LNG

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Dem

and

Cha

rge

$ pe

r GJ/

d

Allocated Unit Cost / GJAllocated Unit Cost x 1.25 R/C

Firm TransportationAllocated Cost $ per GJ/d Capacity

BCUC IR 47.8

Conclusions

• Given a minimum level of Firm Transport demand as defined in the CPCN as Base + 0, the LNG resource portfolio drives rates that:1. Core service rates that are competitive to

alternative fuels to 2011 2. Provide Core service rates that remain competitive

to alternative fuels in 2012 when royalty relief is lost3. Recover the RDDA by 20114. Transport Rates comparable or less than current

levels

FINANCIAL ANALYSIS UPDATE

• Revised Financial Analysis to be provided before November Hearing

Transport Demand to reflect BC Hydro CFT OutcomeEconomic Parameters – Updated Oil and Gas prices Forecast– BC Hydro Electricity Price forecast – US$/CDN Exchange Rate (from 0.71 to 0.75)

Financial Assumptions– Depreciation Rates– Fed./Prov. Contribution Repayment

Operational– Gas Supply Cost Forecast (Sendout)– Incremental Wheeling Costs

Contact Information Tom LoskiDirector,Regulatory Affairs

Tel: (604) 592-7464Fax: (604) 592-7890E-mail: [email protected]

Review and Approval Process

Next Steps

2

Regulatory Agenda

Workshop Fri, Oct 22

Budget Estimates for Participant Assistance Mon, Oct 25

BC Hydro CFT results made public Tues, Oct 26

Intervenors file Evidence Wed, Oct 27

Information Requests to Intervenors and TGVI Wed, Nov 3

Intervenors & TGVI respond to IR's Wed, Nov 10

Hearing Commences Wed, Nov 17

3

Proposed TGVI Panels for Hearing• Key Considerations in Panel determination

• Primary: Resource Plan and CPCN – subject areas and issues not discrete between the two

• Secondary: Logistics – TGVI personnel involved with Annual Review presentation

• Panel 1• Overview, History, Regional Planning, Resource Planning Process,

Core & Industrial Demand Forecasts, DSM

• Panel 2• LNG Project; Siting, Facility Design, Capital & Operating Costs,

Contracting Practice, Operations, Safety

• Panel 3• Resource Alternatives, Project Justification, Financial Evaluation,

Industrial Curtailment, Customer Rate Impacts, Gas Supply benefits