Embed Size (px)

Citation preview

Re-cap

Charlie wants to set up a chocolate factory. Organise the below costs in to fixed (indirect) and variable (direct) costs.

Raw materials Telephone Bill

Wages Rent

Electricity Bill Council Tax

= 5mins

UNIT TITLE: Unit 2:Finance for BusinessLESSON TITLE: BudgetsLEARNING AIM: B

COMPETENCY FOCUS:

Key Skills (L5): you will be able to develop your numeracy skills to calculate financial transactions of a business and to interpret financial data.

Learning ObjectivesBy the end of the lesson, you should be able to…

LO1) To describe what a budget is and why businesses use budgeting.

LO2) To explain the advantages and limitations of using budgets for planning.

LO3) To calculate variance to determine the accuracy of budgets.

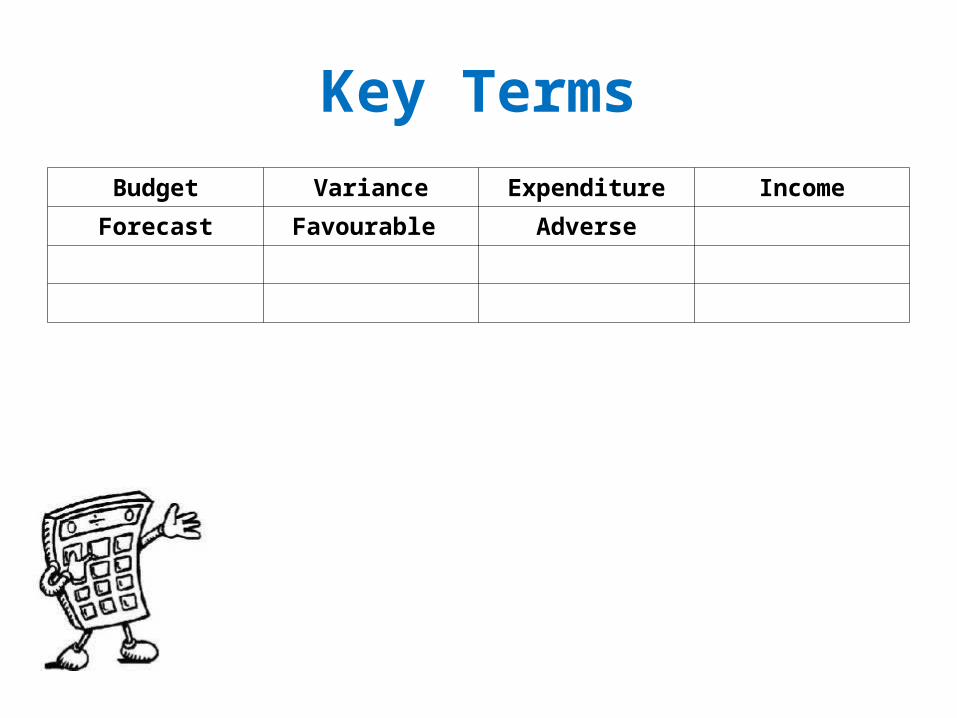

Key Terms

Budget Variance Expenditure Income

Forecast Favourable Adverse

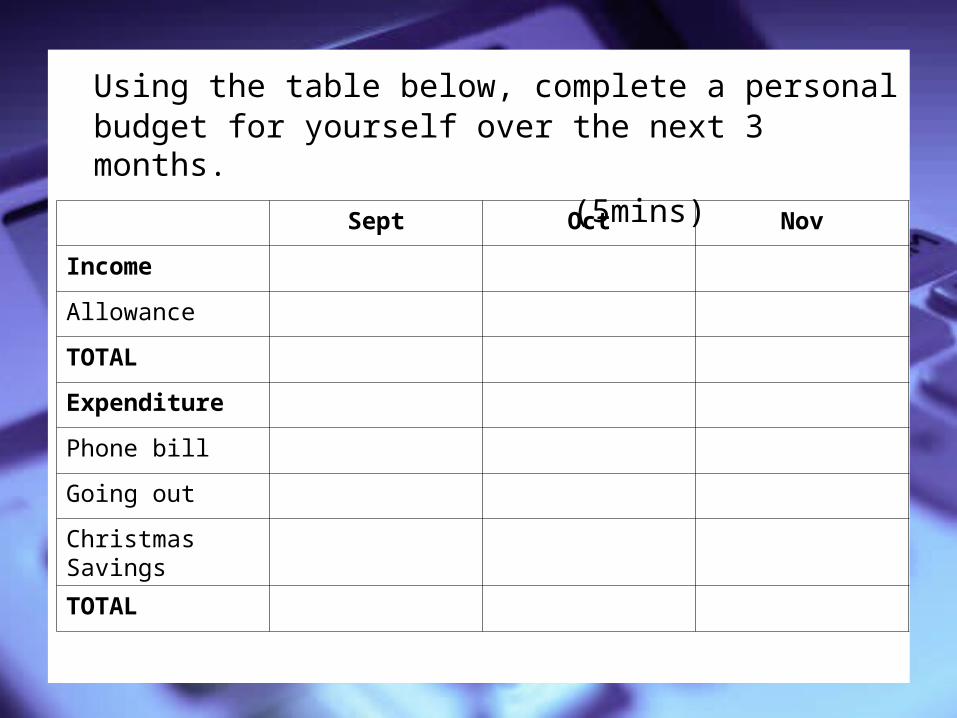

Using the table below, complete a personal budget for yourself over the next 3 months.

(5mins)

Sept Oct Nov

Income

Allowance

TOTAL

Expenditure

Phone bill

Going out

Christmas Savings

TOTAL

Fantasy Football League

You have £40 million pounds to select your football ‘dream team’. You must not go over your budget.

Use the website http://fantasy.premierleague.com/player-list/

to get the names of your players, the position they play and their cost.

Once you have drawn on the following diagram the names and costs, you must then justify why you made the choices that you did and if you had to sacrifice any of your initial ideas.

Why budget?

Planning – anticipate problems and provide solutions early

Measure success and that objectives are being met

Motivation when come in under budget! Prevents overspending

Problems with setting budgets

Time-consuming therefore costly Planned figures therefore often inaccurate Conflict Changes in circumstances therefore

unreliable May de-motivate if budget is unrealistic

Case Study Task

Complete case study task ‘why do businesses budget?’

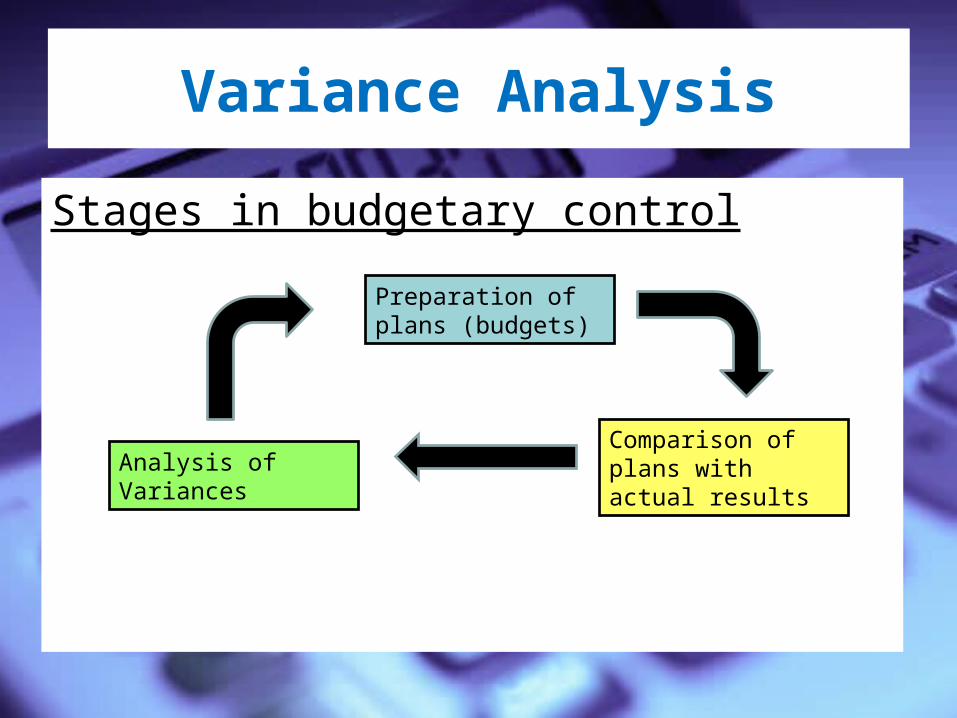

Variance Analysis

Stages in budgetary control

Preparation of plans (budgets)

Analysis of VariancesComparison of plans with actual results

Variance Analysis

Variance = Difference between the predicted and actual figure.- Can be ‘favourable’ (F) or ‘adverse’ (A)

Example:Forecast Actual Variance

Revenue 2,250 2,050 -200

Labour 500 412 -88

Materials 800 900 100

Transport 100 140 40

Profit 850 598 -252 (F)

Variance Analysis

Forecast Profit= 2,250 – 1,400 = 850

Actual Profit = 2,050 – 1,452 = 598

Profit Variance = £252 (F)

Task 2

Variance Analysis Task

Task 3

Produce a factsheet/information leaflet for Business Link to hand out to new business

owners on the advantages of budgeting.

You must include:

What is a budget?Why is budgeting important? What are the advantages and disadvantages of

budgeting?5 Top Tips for budgeting your money

Key Terms

Budget Variance Expenditure Income

Forecast Favourable Adverse

UNIT TITLE: Unit 2:Finance for BusinessLESSON TITLE: BudgetsLEARNING AIM: B

COMPETENCY FOCUS:

Key Skills (L5): you will be able to develop your numeracy skills to calculate financial transactions of a business and to interpret financial data.

Learning ObjectivesBy the end of the lesson, you should be able to…

LO1) To describe what a budget is and why businesses use budgeting.

LO2) To explain the advantages and limitations of using budgets for planning.

LO3) To calculate variance to determine the accuracy of budgets.