Embed Size (px)

Citation preview

RCSA Web Survey

Round 28 – November 2008

Executive Summary

Summary Business confidence has dropped to the lowest since 2001, a drop of 21% while expectations

of growth have become negative for the first time with a drop of 5% to -0.8% There has been a strong increase in the number of applicants for positions and become

considerably easier to find appropriate applicants for positions. Conditions have improved back to those experienced in April 2004

o All locations are finding very similar labour market conditions except NZ is getting more applicants for positions

Staff turnover has remained stable at 36% pa organisations have contracted by 2.1% and become negative for the first time since December 2001

o Qld has 10% higher staff turnover and 7% greater staff loss There has been a substantial drop in permanent full-time placements while on-hire

employment and contractor placements have increased slightly. 12% of on-hired employees converted to permanent positions in the last six months while permanent employees converting to on-hired employment was 5%.

Permanent placements have dropped by 4% to 5% thus on-hired replacements have become proportionally more significant with a rise of 3% to 94% of the total number of placements

Accordingly, the proportion of revenue from on-hired employment has risen by 6% to 54% while that of recruitment services has dropped 3% to 42%

o SA and WA get a larger proportion of revenue from on-hired employees & contractorso NZ gets a larger proportion of from recruitment services

Note: If locational differences are not mentioned, the differences are insufficient for comment

Executive Summary

Summary – issues of most concern Concerns about the state of the economy have jumped again from 84% to 94%

while lack of suitable candidates has dropped to 3rd spot. Concerns about the lack of hiring intentions of clients has jumped again from 3rd place to 2nd with concerns increasing 21% to 88%. Concerns about maintaining profitability/fee levels have also increased 20% to 70% an along with it concerns about price undercutting

o NSW is more financing growth and least about employment legislationo VIC is not substantially different from averageo QLD is more worried industrial relationso SA is more concerned retaining suitable recruitment staff, workers compensation,

employment legislation, and unfair dismissal and less worried about finding suitable candidates, restructuring industries and the cost of advertising

o WA is more concerned legal issues about on-hired staff and immigration issues and less concerned about finding recruitment staff

o NZ is more worried about finding and retaining suitable recruitment staff and restructuring industries and less worried about the cost of advertising and industrial relations

Note: If locational differences are not mentioned, the differences are insufficient for comment

Executive Summary - Skills

The 2 skills with the biggest shortages are non-building professional engineers, associates and technician experiencing a 6% - 8% drop in demand.

The demand for health professionals and nurses remains static while rising to in place.

The demand for business professionals has slumped for the second survey in a row by a further15% to 21% from 4th to 14th place.

The demand for building professionals has also slumped 10% to 18%. Demand for other skills had generally dropped 3% - 8% and is consistent with a

general easing of the economy and labour market conditions The top 12 skills shortages being:

o Non-building professional engineers o Non-building engineering associates and technicians o Health professionals o Nurses o Medical technicians o Electrical trades (building) o Non-building electrical/electronic trades o Mobile plant operators o Building associates and technicians o Carpenters and joiners o Plumbers o Metal trades

Excutive summary cont’d

The majority of respondents (94%) source candidates by approaching passive candidates. A two thirds use niche or specialist internet job boards while nearly two thirds use refer a friend incentives

o NSW is more likely to use social networking sites

o VIC less likely to use internet job boards

o QLD is less likely to use refer a friend

o SA and WA are more likely to use refer a friend incentives

o NZ is more likely to use internet job boards

Nearly two thirds took action to address the market downturn in the last three months and nearly half addressed marketing expenses. The next priority is the number of recruiters per staff member followed by international revenue

Process

Web surveyo E-mail business heads in both NZ and Australia

o 177 responses

o Data collection began early October 2008 and completed 7 November 2008

Demographics of sampleThe number of sole traders in the sample remains stable at16%

Location differences:There are a higher proportion of sole traders in NZ

Sole trader16%

Other84%

Trader status

$1,674

$1,565

$1,346

$331

$577

$1,534

$312

$106

$268

$7,713

38%

34%

39%

13%

17%

21%

7%

8%

19%

0% 10% 20% 30% 40% 50%

NSW

Victoria

Queensland

ACT

South Australia

Western Australia

Tasmania

Northern Territory

New Zealand

(note multiple locations allowed sums to more than 100%)

Location company operates in

22%

20%

17%

4%

7%

20%

4%

1%

3%

0% 10% 20% 30% 40%

NSW

Victoria

Queensland

ACT

South Australia

Western Australia

Tasmania

Northern Territory

New Zealand

Proportion of revenue generated by location

Demographics of sampleThe total annual revenue of respondent companies is $7.7 billion up from $6.0 billion last round.

This large increase is due to an increase in large companies responding

Total

Ann

ual r

even

ue $

m

Total Australia=$7.45bApprox 97% of revenue

Demographics of sampleThe proportion of $100m+ companies increased by 2% from last round to 5%.

22

35

21

8

10

5

0 10 20 30 40

Under $1m

$1M to $5M

$5M to $10M

$10M to $20M

$20M to $100M

$100M and above

% of sample

Annual turnover of companies

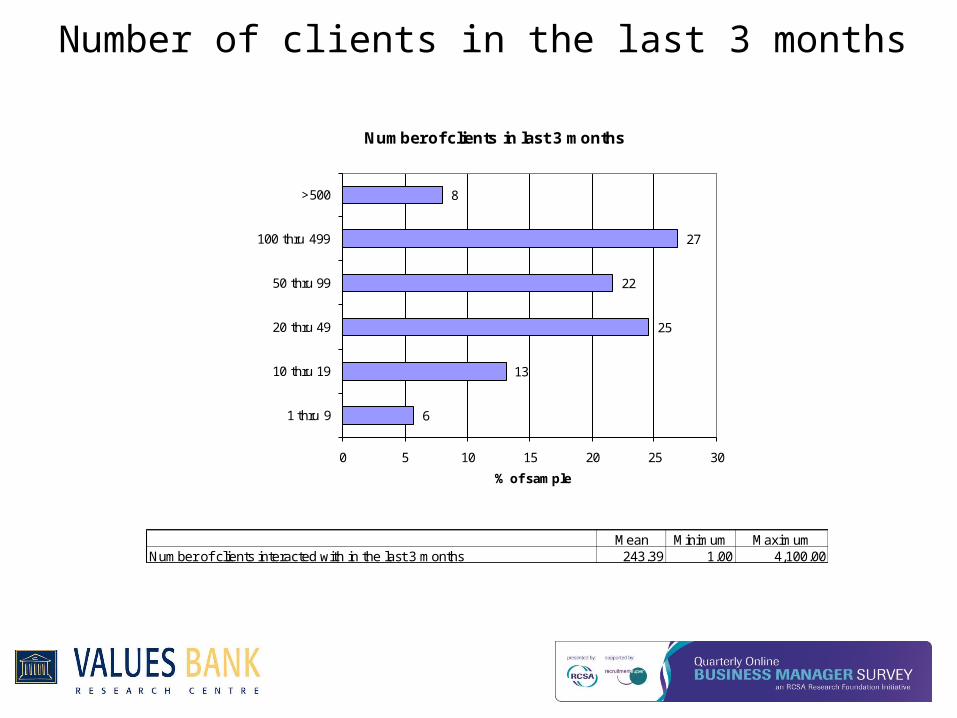

Number of clients in the last 3 months

6

13

25

22

27

8

0 5 10 15 20 25 30

1 thru 9

10 thru 19

20 thru 49

50 thru 99

100 thru 499

>500

% of sample

Number of clients in last 3 months

Mean Minimum MaximumNumber of clients interacted with in the last 3 months 243.39 1.00 4,100.00

Business confidence has dropped to the lowest since 2001, a drop of 21% while expectations of growth have become negative for the first time with a

drop of 5% to -0.8%.

Scale:0=strongly disagree50=neutral100=strongly agree

DifferencesNone Location differences:

NSW and WA are slightly less confident while SA is slightly more confident

40.0

50.0

60.0

70.0

80.0

Av

era

ge

I am confident that our business will improve over the next three months

-1%0%1%2%3%4%5%6%7%8%

Av

era

ge

Volume (%) your business will change next quarter

Staff turnover has remained stable at 36% pa organisations have contracted by 2.1% and become negative for the first time since December 2001

Differences•Qld has 10% higher staff turnover and 7% greater staff loss

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

60%

Sep

t (2001)

Dec (2001)

Feb

(2002)

July (2002)

Sep

t (2002)

Dec (2002)

Mar (2003)

Jun

(2003)

Sep

t (2003)

Dec (2003)

Ap

ril (2004)

Jun

e (2004)

Sep

t (2004)

Dec (2004)

Ap

ril (2005)

Au

g (2005)

No

v (2005)

Feb

(2006)

Jun

(2006)

Sep

t (2006)

Dec(2006)

March

(2007)

Jun

e(2007)

Sep

t(2007)

Dec(2007)

Ap

ril(2008)

Au

g(2008)

No

v(2008)

Ave

rag

e

Staff turnover (% annualised)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Sep

t (2001)

Dec (2001)

Feb

(2002)

July (2002)

Sep

t (2002)

Dec (2002)

Mar (2003)

Jun

(2003)

Sep

t (2003)

Dec (2003)

Ap

ril (2004)

Jun

e (2004)

Sep

t (2004)

Dec (2004)

Ap

ril (2005)

Au

g (2005)

No

v (2005)

Feb

(2006)

Jun

(2006)

Sep

t (2006)

Dec(2006)

March

(2007)

Jun

e(2007)

Sep

t(2007)

Dec(2007)

Ap

ril(2008)

Au

g(2008)

No

v(2008)

Ave

rag

e

Staff growth (% annualised)

There has been a strong increase in the number of applicants for positions and become considerably easier to find appropriate applicants for positions.

Conditions have improved back to those experienced in April 2004.

Scale:0=strongly disagree50=neutral100=strongly agree

Differences•All locations are finding very similar labour market conditions except NZ is getting more applicants for positions

20

30

40

50

60

70

80

Sep

t (2001)D

ec (2001)F

eb (2002)

July (2002)

Sep

t (2002)D

ec (2002)M

ar (2003)Ju

n (2003)

Sep

t (2003)D

ec (2003)A

pril (2004)

Jun

e (2004)S

ept (2004)

Dec (2004)

Ap

ril (2005)A

ug

(2005)N

ov (2005)

Feb

(2006)Ju

n (2006)

Sep

t (2006)D

ec(2006)M

arch(2007)

Jun

e(2007)S

ept(2007)

Dec(2007)

Ap

ril(2008)A

ug

(2008)N

ov(2008)

Av

era

ge

s

Labour market scoresIt is easy to find appropriate applicants for positions

Applicants generally have the appropriate work ready attitudes

Applicants generally have the right mix and level of skills

Applicants generally have the right capabilities

Irrespective of appropriateness there are at least as many applicants for positions as needed

0% 20% 40% 60% 80% 100%

It is easy to find appropriate applicants for positions

Applicants generally have the appropriate work ready attitudes

Applicants generally have the right mix and level of skills

Applicants generally have the right capabilities

Irrespective of appropriateness there are at least as many applicants for positions as there are positions

13%

42%

39%

65%

45%

15%

24%

24%

24%

9%

72%

34%

36%

11%

46%

Labour market

%Agree %Neutral %Disagree

There has been a lift in the capability, skills and attitudes of available applicants

-10%

-7%

+8%

-9%+12%

+12%

+9% -10%

Staff placed and on-hired workersThere has been a substantial drop in permanent full-time placements while on-hire employment and contractor placements have increased slightly. 12% of on-hired

employees converted to permanent positions in the last six months while permanent employees converting to on-hired employment was 5%.

August 2008

Note: variability may arise because of a few large numbers – this is a problem of small data sets

Mean Minimum MaximumPermanent full-time placements 115.23 0 5,406Permanent part-time placements 7.33 0 500On-hire employment & contractors 1,179.62 0 130,000

On-hired employees converting to permanent - last six months% 16.41 0.00 100.00Permanent employees converting to on-hired - last six months% 4.08 0.00 100.00

November 2008

Mean Minimum MaximumPermanent full-time placements 71.14 0 4,500Permanent part-time placements 12.56 0 800On-hire employment & contractors 1,211.54 0 100,000

On-hired employees converting to permanent - last six months% 11.74 0.00 70.00Permanent employees converting to on-hired - last six months% 4.92 0.00 100.00

Permanent placements have dropped by 4% to 5% thus on-hired replacements have become proportionally more significant with a rise of

3% to 94% of the total number of placements

12%4% 7% 4% 5%

9%

14% 11%5% 5%

13%5% 5%

10% 7% 6%13% 15%

9% 5%1% 1% 0% 0% 0% 1%

2% 2% 0% 1% 1% 0% 1% 1% 0% 0% 1% 1% 1% 1%

86%

95%93% 95%

94% 90%85% 87%

94% 95%85%

95% 95%90% 93% 94%

86% 84%91%94%

0%

20%

40%

60%

80%

100%

Ave

rag

ePlacement by type (%)

Permanent full-time placements Permanent part-time placements

On-hire employment & contractor

Accordingly, the proportion of revenue from on-hired employment has risen by 6% to 54% while that of recruitment services has dropped 3% to 42%

Difference from average•SA and WA get a larger proportion of revenue from on-hired employees & contractors•NZ gets a larger proportion of from recruitment services

44%

47%52%57%

48%51%

51%47% 47%

51% 52% 50%45% 43%

47% 48%45%

50%45%

54%

38% 37% 37% 35%

43%

37%

44% 43% 43%45% 45%

42% 43%47%

43% 43%48%

45%49%

42%

0%

10%

20%

30%

40%

50%

60%

70%

Ave

rag

eService revenue (%)

On-hired employee & contractor services Recruitment services

A substantial proportion of companies have neither contractors nor on-hire employees.

19

14

7

9

11

13

17

10

0 5 10 15 20

None

1 thru 19

20 thru 49

50 thru 99

100 thru 199

200 thru 499

500 thru 1999

>2000

% of sample

On-hire & contactor numbers on books

33

24

12

16

19

23

30

17

0 10 20 30 40

None

1 thru 19

20 thru 49

50 thru 99

100 thru 199

200 thru 499

500 thru 1999

>2000

Number

On-hire & contractor numbers on books

4

27

51

63

66

94

0 20 40 60 80 100

Second Life or other virtual worlds

Other

Social networking sites (e.g Facebook LinkedIn

MySpace)

Refer a f riend incentives

Increasing the use of niche/specialist internet

job boards

Approaching passive candidates

% of sample

Media used to source candidates

The majority of respondents (94%) source candidates by approaching passive candidates. A two thirds use niche or

specialist internet job boards while nearly two thirds use refer a friend incentives

Differences•NSW is more likely to use social networking sites•VIC less likely to use internet job boards•QLD is less likely to use refer a friend•SA and WA are more likely to use refer a friend incentives •NZ is more likely to use internet job boards

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Industrial relations

Difficultly in retaining suitable recruitment staff

Financing growth

Restructuring industries

Cost of advertising

Difficultly in finding suitable recruitment staff

Price undercutting in our industry

Maintaining profitability/fee levels

Lack of suitable candidates

Lack of hiring intentions by clients

State of the economy

24%

27%

39%

43%

43%

44%

67%

70%

75%

88%

94%

76%

73%

61%

57%

57%

56%

33%

30%

25%

12%

6%

%Agree %Disagree

Concerns for the present and near future (all respondents)

Concerns about the state of the economy have jumped again from 84% to 94% while lack of suitable candidates has dropped to 3rd spot. Concerns about the lack of hiring intentions of clients has jumped again from 3 rd place to 2nd with

concerns increasing 21% to 88%. Concerns about maintaining profitability/fee levels have also increased 20% to 70% an along with it concerns about price undercutting.

0% 20% 40% 60% 80% 100%

OH&S Issues (Australia)

Workers' compensation legislation (Australia)

Employment legislation (Australia)

Immigration issues (Australia)

Legal issues about on-hired staf f (Australia)

New Zealand

Workers' compensation legislation (Australia)

Unfair dismissal and casuals (Australia)

OH&S Issues (Australia)

Immigration issues (Australia)

Employment legislation (Australia)

Legal issues about on-hired staf f (Australia)

Australia

39%

39%

42%

44%

55%

28%

31%

33%

40%

42%

44%

61%

61%

58%

56%

45%

72%

69%

67%

60%

58%

56%

%Agree %Disagree

Concerns for the present and near future (National issues)

Concerns about national issues remain stable and of relatively low concern compared with the economy. Local concerns range from 44% to 30%.

Location differences have reduced this round

Note: <50=less than neutral50=neutral>50 = greater than neutral

Compared to average•NSW is more financing growth and least about employment legislation•VIC is not substantially different from average•QLD is more worried industrial relations•SA is more concerned retaining suitable recruitment staff, workers compensation, employment legislation, and unfair dismissal and less worried about finding suitable candidates, restructuring industries and the cost of advertising •WA is more concerned legal issues about on-hired staff and immigration issues and less concerned about finding recruitment staff•NZ is more worried about finding and retaining suitable recruitment staff and restructuring industries and less worried about the cost of advertising and industrial relations

Variable NSW VIC Qld SA WA NZWeighted

aveSubstantially less than averageSubstantially more than average

State of the economy 96.00 93.00 95.00 100.00 94.00 100.00 95.81Lack of suitable candidates 67.00 68.00 75.00 61.00 70.00 66.00 68.52Lack of hiring intentions by clients 91.00 92.00 89.00 93.00 92.00 95.00 91.60Difficultly in finding suitable recruitment staff 42.00 43.00 31.00 32.00 28.00 51.00 37.79Difficultly in retaining suitable recruitment staff 34.00 37.00 33.00 51.00 35.00 52.00 38.52Financing growth 45.00 38.00 33.00 31.00 38.00 34.00 37.21Maintaining profitability/fee levels 74.00 71.00 71.00 70.00 78.00 68.00 72.18Price undercutting in our industry 71.00 65.00 65.00 62.00 62.00 67.00 65.77Restructuring industries 39.00 34.00 35.00 29.00 32.00 53.00 36.62Cost of advertising 27.00 31.00 36.00 17.00 27.00 20.00 27.78Industrial relations 27.00 31.00 30.00 35.00 34.00 22.00 29.77Workers' compensation legislation (Australia) 42.00 44.00 43.00 53.00 49.00 45.22Employment legislation (Australia) 42.00 48.00 47.00 61.00 58.00 49.54Legal issues about on-hired staff (Australia) 59.00 65.00 61.00 73.00 76.00 65.33Immigration issues (Australia) 51.00 44.00 52.00 58.00 63.00 52.44OH&S Issues (Australia) 37.00 38.00 39.00 43.00 38.00 38.64Unfair dismissal and casuals (Australia) 26.00 33.00 30.00 38.00 30.00 30.73

Skills shortages by occupation

27%

19%

25%

23%

21%

13%

13%

8%

10%

11%

10%

13%

12%

10%

8%

3%

4%

4%

3%

6%

11%

18%

11%

7%

6%

13%

11%

15%

12%

11%

12%

8%

10%

11%

10%

14%

13%

13%

13%

10%

21%

17%

20%

19%

23%

19%

21%

24%

24%

22%

23%

22%

22%

31%

28%

29%

35%

34%

31%

32%

2%

4%

0%

1%

0%

3%

3%

1%

4%

6%

3%

3%

4%

22%

10%

2%

7%

10%

8%

6%

1%

1%

1%

1%

1%

1%

1%

0%

1%

1%

1%

1%

0%

2%

2%

0%

2%

1%

2%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Non-building professional engineers

Non-building engineering associates and technicians

Health professionals

Nurses

Medical technicians

Electrical trades (building)

Non-building electrical/electronic trades

Mobile plant operators

Building associates and technicians

Carpenters and joiners

Plumbers

Metal trades

Drivers

Business professionals

Building professionals

Machine and stationary plant operators

IT and telecommunications professionals

Receptionists and telephonists

IT and telecommunications technicians

IT and telecommunications trades

Supply of skills by occupation in order of total shortage

Shortage long term

Shortage short term

Neutral

Over supply short term

Over supply long term

Skills shortages by occupation – top 20 The 2 skills with the biggest shortages are non-building professional engineers, associates and technician experiencing a 6% - 8% drop in demand. The demand for health professionals and nurses remains static while rising to in place. The demand for business professionals has slumped for the second survey in a row by a further15% to 21% from 4 th to 14th place. The demand for building

professionals has also slumped 10% to 18%. Demand for other skills had generally dropped 3% - 8% and is consistent with a general easing of the economy and labour market conditions.

To

tal

sho

rtag

e

38%37%35%30%27%26%24%24%22%22%22%22%22%21%18%17%16%16%16%15%

11%

8%

4%

10%

8%

10%

8%

8%

3%

3%

3%

8%

7%

4%

3%

6%

2%

3%

3%

3%

3%

4%

7%

11%

5%

6%

4%

6%

5%

10%

10%

9%

3%

3%

6%

7%

4%

7%

6%

5%

2%

0%

29%

26%

31%

28%

26%

34%

27%

34%

39%

30%

27%

28%

33%

29%

32%

28%

28%

33%

30%

29%

41%

1%

3%

12%

1%

4%

1%

4%

1%

9%

5%

7%

4%

4%

5%

21%

7%

10%

8%

9%

7%

1%

0%

1%

1%

0%

1%

1%

1%

1%

2%

1%

0%

1%

0%

1%

11%

1%

0%

0%

1%

0%

1%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

School teachers

Bricklayers

Sales staf f (not professionals)

Rail drivers

Wall tilers

Scientists

Roofers

Scientif ic technicians

Other clerks

Mining labourers

Trades assistants and factory hands

Agricultural labourers

Social professionals

Food trades

General managers

Vehicle trades

Waiters and restaurant staf f

Other personal service workers

Building & construction labourers

Cleaners

Farm managers

Supply of skills by occupation in order of total shortage

Shortage long term

Shortage short term

Neutral

Over supply short term

Over supply long term

Skills shortages by occupation – bottom 20

To

tal

sho

rtag

e

Top 10 skill shortages by location

NSW1. Non-building professional engineers

2. Non-building engineering associates and technicians

3. Health professionals

4. Nurses

5. Medical technicians

6. Electrical trades (building)

7. Mobile plant operators

8. Non-building electrical/electronic trades

9. Drivers

10. IT and telecommunications technicians

VIC1. Non-building professional engineers

2. Non-building engineering associates and technicians

3. Health professionals

4. Nurses

5. Medical technicians

6. Electrical trades (building)

7. Non-building electrical/electronic trades

8. Metal trades

9. Mobile plant operators

10. Drivers

Top 10 skill shortages by location

Queensland1. Non-building engineering associates and

technicians

2. Non-building professional engineers

3. Health professionals

4. Nurses

5. Medical technicians

6. Electrical trades (building)

7. Non-building electrical/electronic trades

8. Mobile plant operators

9. Plumbers

10. Metal trades

South Australia1. Non-building engineering associates and

technicians

2. Health professionals

3. Non-building professional engineers

4. Mobile plant operators

5. Nurses

6. Electrical trades (building)

7. Medical technicians

8. Non-building electrical/electronic trades

9. Metal trades

10. Machine and stationary plant operators

Top 10 skill shortages by location

Western Australia

1. Non-building engineering associates and technicians

2. Health professionals

3. Non-building professional engineers

4. Nurses

5. Medical technicians

6. Mobile plant operators

7. Electrical trades (building)

8. Non-building electrical/electronic trades

9. Machine and stationary plant operators

10. Metal trades

New Zealand

1. Non-building engineering associates and technicians

2. Health professionals

3. Medical technicians

4. Drivers

5. Non-building professional engineers

6. Nurses

7. Mobile plant operators

8. IT and telecommunications trades

9. IT and telecommunications technicians

10. Electrical trades (building)

Special section

Recruitment and the global economy

Nearly two thirds took action to address the market downturn in the last three months and nearly half addressed marketing expenses. The next

priority is the number of recruiters per staff member followed by international revenue.

MeansLast three

monthsNext three months Difference

Action to address the market downturn 73.25 73.75 -0.50Marketing expenses 55.25 51.25 4.00Number of recruiters per support staff member 52.75 52.00 0.75International revenue 48.25 48.75 -0.50Number of blue collar appointments 47.00 46.25 0.75Total revenue 45.25 43.75 1.50Number of white collar appointments 44.50 47.00 -2.50

0% 20% 40% 60% 80% 100%

Action to address the market downturn

Marketing expenses

Total revenue

Number of white collar appointments

Number of recruiters per support staff member

Number of blue collar appointments

International revenue

71

46

36

22

21

13

12

28

30

14

37

69

64

70

2

25

49

41

10

23

18

Action last three months

%Increase %Neutral %Decrease

0% 20% 40% 60% 80% 100%

Action to address the market downturn

Total revenue

Marketing expenses

Number of white collar appointments

Number of recruiters per support staff member

International revenue

Number of blue collar appointments

74

32

32

27

18

17

16

23

14

40

37

71

61

57

3

53

28

36

11

22

27

Action next three months

%Increase %Neutral %Decrease