Embed Size (px)

Citation preview

R.C. JAIN & ASSOCIATES LLP

Head Office:

622-624, The Corporate Centre, Nirmal Lifestyles, L.B.S. Marg, Mulund (W), Mumbai – 400080. Email: [email protected]

Phone: 25628290/91, 67700107

Website: www. rcjainca.com

NEWSLETTER

R. C. Jain and Associates LLP

INDEX

1. Income Tax ____________________________________________ 1

2. GST___________________________________________________ 10

3. RBI & FEMA ___________________________________________ 18

4. Corporate Law_________________________________________ 20

EDITORIAL TEAM

EDITOR

CA R. C. Jain

MEMBERS SUPPORT TEAM

CA Devangi Thosani Khusbhoo Khatwani Ulhas Jain

Supriya Shelatkar Shivani Thakkar Rohini Veer

Shilka Santhosh Sharadha Hariharan Mangesh Kolekar

Heena Kausar Khan Ekta Pamnani

Ruchika Ravi Hitesh Motwani

The contents provided in this newsletter are for information purpose only and are

intended, but not promised or guaranteed, to be correct, complete and up-to-date. The firm

hereby disclaims any and all liability to any person for any loss or damage caused by errors

or omissions, whether such errors or omissions result from negligence, accident or any

other cause.

1 R. C. Jain and Associates LLP

DIRECT TAX

Income Tax

1. Updating contact details in e-Filing Portal.

Income-Tax Department uses the registered contact details (Mobile number &

E-mail ID) for all communications related to e-Filing. It is mandatory that all

tax payers must have a valid contact details registered in e-Filing portal.

It is noticed that many registered users are not having authenticated contact

details in eFiling or may have provided details of other persons for

convenience. This prevents the Department from interacting directly with

taxpayers on their personal email and Mobile. Further, it has been observed

that in many cases taxpayers are not able to reset their password since the

email communication from the Department may be sent to their registered

email or Mobile which may be different from the taxpayer‟s personal email or

mobile.

Hence, it is requested that all the e-Filing users may immediately update and

authenticate their correct contact details so that the communication can be

sent to the valid Mobile number and E-mail ID

The process of updating and authenticating the contact

New User

Provide the correct Mobile Number and Email ID during the Registration in

the e-Filing portal, Activation link would be sent to the registered E-mail ID

and a One Time Password (OTP also called PIN) is sent to the registered

Mobile Number. User needs to Click on the Link provided in the E-mail and

2 R. C. Jain and Associates LLP

DIRECT TAX

enter the OTP received in the mobile number for Successful activation of the

registered user in e-Filing portal.

Registered User

After the user logs in to the e-filing account, the user is requested to update

the current Mobile number and E-mail ID. The user should update their

personal Mobile number and Email so that the updated contact particulars are

registered with the Department or confirm that the Mobile number and email

ID already registered is their valid personal contacts. Upon submitting the

details, Department would immediately send OTPs (PIN1 & PIN2) to new

mobile number and Email ID. The respective PINsPIN1 and PIN2 received

through Mobile number and E-mail ID should be entered by them in the

respective input fields to authenticate that the email ID and mobile are correct.

Upon successful validation the Mobile numberand email ID would be

updated in the taxpayer‟s profile and the process would be complete. If the

PINs are not received within specified time (say 2 minutes), the taxpayer may

opt for “Resend PINs” option. The PINs once received will be valid for 24

hours. The taxpayers are advised to validate the contact details using the PINs

received within 24 hours. If PINs are not validated within 24 hours, the

taxpayer has to login and follow the same procedure as above again.

3 R. C. Jain and Associates LLP

DIRECT TAX

Note:

One mobile number or email ID can be used for a maximum of 10 user

accounts as the Primary Contact- Mobile Number and Email ID in e-Filing.

This is to ensure that family members (not exceeding 10 separate users) not

having personal email or mobile can be covered under a common email or

mobile, but in general taxpayers should have their own unique email ID and

Mobile registered with the Department.

The taxpayer can enter any other person‟s email or mobile number in addition

as a Secondary Contact (without any restriction on the number of user

accounts linked as a Secondary Contact). Using “Profile Settings - My Profile”

the taxpayer can select to include the Secondary Contact to also receive

emails, alerts etc. Include the emails and SMS from the Income tax

Department in the „safe list‟ or „white list‟ to prevent the communications

from the Department from being blocked or rejected or sent to Spam folder.

As a best practice, please update and authenticate the current contact and

address details under “Profile Settings - My Profile” after login to eFiling

portal.

4 R. C. Jain and Associates LLP

DIRECT TAX

2. I-T Dept to Appoint 7,600 More Experts to Assist Small

Taxpayers in Filing Returns.

Every district of the country will soon have at least one trained personnel to

assist small taxpayers in filing ITRs, with the Income Tax Department

proposing to appoint 7,600 additional experts whose services will also be

available on mobile application.

The Central Board of Direct Taxes (CBDT), the apex policy-making body of

the tax department, has decided to enlarge the ambit of the 2006 Tax Return

Preparer Scheme (TRPS) by making the service "digital" and covering all the

708 districts of the country."

It is proposed to provide sufficient number of Tax Return Preparers (TRPs) in

every district by scaling up of number of TRPs from a total 5,400 to 13,000 in

the country," according to an I-T department blueprint, accessed by PTI. "It is

proposed that every district in the country should have at least three TRPs," it

added.

A senior official working on the project said the aim was to ensure hassle-free

and 'from home' tax filing service to assessees without they taking pains to go

to a Chartered Accountant or a person who has expertise in filing tax

returns.“Filing an ITR is still not easy for many people. The TRP Scheme was

launched about a decade ago with this fact in mind and the view that such

services should be available at a low cost to tax payers,” an officer said.

5 R. C. Jain and Associates LLP

DIRECT TAX

"At present, not every district in the country has a TRP. With the expansion of

the tax base over the years and government's directive to enhance tax payer

services, the new plan has been envisaged," the officer added. He said, "7,600

new TRPs will be trained and appointed by the tax department."

Under the new digital plan for the scheme, he said, a taxpayer will be able to

find his nearest TRP by logging on to the soon-to-be-launched 'Aaykar Mitra'

mobile app, much like the prevalent cab rental apps offered for commuters by

taxi aggregators such as Uber and Ola.

“The taxpayers will be able to send their documents to the TRP in an online

mode and even rate the services of the preparer, much like what is available to

commuters to rate their service providing drivers in the rental cab apps,” he

said.

As per official data, there are 5,400 TRPs in the country at present who have

been trained and appointed by the I-T department over the years. A TRP, as

per official rates, can charge a maximum of Rs 250 for filing one ITR.

6 R. C. Jain and Associates LLP

DIRECT TAX

Case Laws:

1. Issue Involved: Deemed Dividend.

Ravindra R. Fotedar v. Asst. Commissioner of Income-Tax – (ITAT

Mumbai) – (In favour of Assessee)

Section 2(22)(e) of the Income Tax Act, 1961

Gist of the Case:

1) The Assessee is a shareholder of three companies with shareholding of

more than 10% and one of the three companies had granted loans to

remaining two companies.

2) The Assessee contended that such loans were temporary in nature and

asked the Ld. A.O. to consider that these were not loans but were

current accounts of all companies with each other.

3) However, the Ld. A.O. rejected the plea of the Assessee and added the

entire loan to the income of the assessee as deemed dividend.

4) During the course of Tribunal Proceedings, the assessee established the

commercial expediency for granting of temporary loans by the

companies to each other

5) After establishing such expediency, the tribunal deleted the said

additions as deemed dividend from the income of the Assessee.

The entire judicial pronouncement bears Citation No.: [2017] 85

taxmann.com 314 (Mumbai – Trib.) and can be referred accordingly.

.

7 R. C. Jain and Associates LLP

DIRECT TAX

2. Issue Involved: No deduction of TDS on reimbursement of

various charges paid by the Assessee.

Kuloday Technopark (P.) Ltd. v. Income-Tax Officer – (ITAT Mumbai) –

(In favour of Assessee)

Section 194C, 195 and 40(a)(ia) of the Income Tax Act, 1961

Gist of the Case:

1) The Assessee had paid various charges such as Ocean Freight,

Demurrage Charges, Handling Charges and such other charges to

Indian Agents or Authorized Representative of non-resident shipping

company.

2) As no TDS is deducted on the above transactions the same needs to be

disallowed u/s 40(a)(ia). Apart from the stated no exemption certificate

of such party had been submitted by the Assessee so the expenditure

was disallowed.

3) During the course of Assessment Proceedings, the Assessee Company

had relied on CBDT Circular No. 723 dated 19.09.1995 r.w.s. 172 of the

Income Tax Act, 1961.

During the course of First Appeal Proceedings, copies of invoices and

debit notes relating to reimbursement of expenses were provided by the

Assessee for the first time and so the Ld. A.O. objected to the admission

of additional evidences. However, Ld. CIT-(A) considered the claim of

the Assessee and admitted the additional evidences produced by the

Assessee and gave part relief to the Assessee Company.

8 R. C. Jain and Associates LLP

DIRECT TAX

4) The Tribunal remanded back the matter to Ld. A.O. to examine all the

facts freshly and directed the Ld. A.O. to grant reasonable opportunity

to the Assessee to produce all the relevant details before the Ld. A.O.

The entire judicial pronouncement bears Citation No.: [2017] 86 taxmann.com

74 and can be referred accordingly.

3. Issue Involved: Interest free advances and TDS on sales

incentives

Bombay Sales Corporation v. Joint Commissioner of Income Tax – (ITAT

Ahmedabad) – (Partly in favour of Assessee)

Section 36(1)(iii), 40(a)(ia) and 194H of the Income Tax Act, 1961

Gist of the Case:

1) The Assessee is a partnership which had a policy of paying interest on

capital balances of the partners however it had granted interest free

loans to the relatives of the partners and so Ld. A.O. disallowed interest

on capital balances paid by the Assessee Firm. Apart from that the

Assessee firm had also given sales incentives to its dealers and so the

Ld. A.O. contended that the same is in the form of commission to

dealers so TDS u/s 194H of the Income Tax Act, 1961 must be deducted

on said payments and disallowed the expenditure of the assessee firm

u/s 40(a)(ia) of the Income Tax Act, 1961.

9 R. C. Jain and Associates LLP

DIRECT TAX

2) The Ld. CIT-(A) allowed the issue pertaining to interest expenditure in

the favour of Revenue and issue pertaining to non-deduction of TDS in

the favour of Assessee and the order of Ld. CIT-(A) was upheld by the

Tribunal.

The entire judicial pronouncement bears Citation No.: [2017] 86taxmann.com

9 and can be referred accordingly.

10 R. C. Jain and Associates LLP

INDIRECT TAX

GST

1. Extension of Time Limit for filing details in Form Trans-1 for

the month of July 2017

The Central Government vide Order No-03/2017-GST, dated. 21st September,

2017 has extended the time limit for filing of details in form TRANS 1 under

Rule 117 for the month of July 2017 up to 31st October 2017. Prior to this

notification, such details were required to be furnished within 90 days from

the appointed date i.e 28th September

2. Substitution in description of service and tax rates

Central Government vide Notification No. 24/2017-Central Tax (Rate) dated

21st September,2017 and Notification No. 24/2017-Integrated Tax (Rate) dated

21st September,2017 has amended the rates and description of the service

specified in Notification No.11/2017 - Central Tax (Rate) dated the 28th June,

2017 and Notification No. 8/2017- Integrated Tax (Rate), dated the 28th June,

2017 respectively by the following description of service:

11 R. C. Jain and Associates LLP

INDIRECT TAX

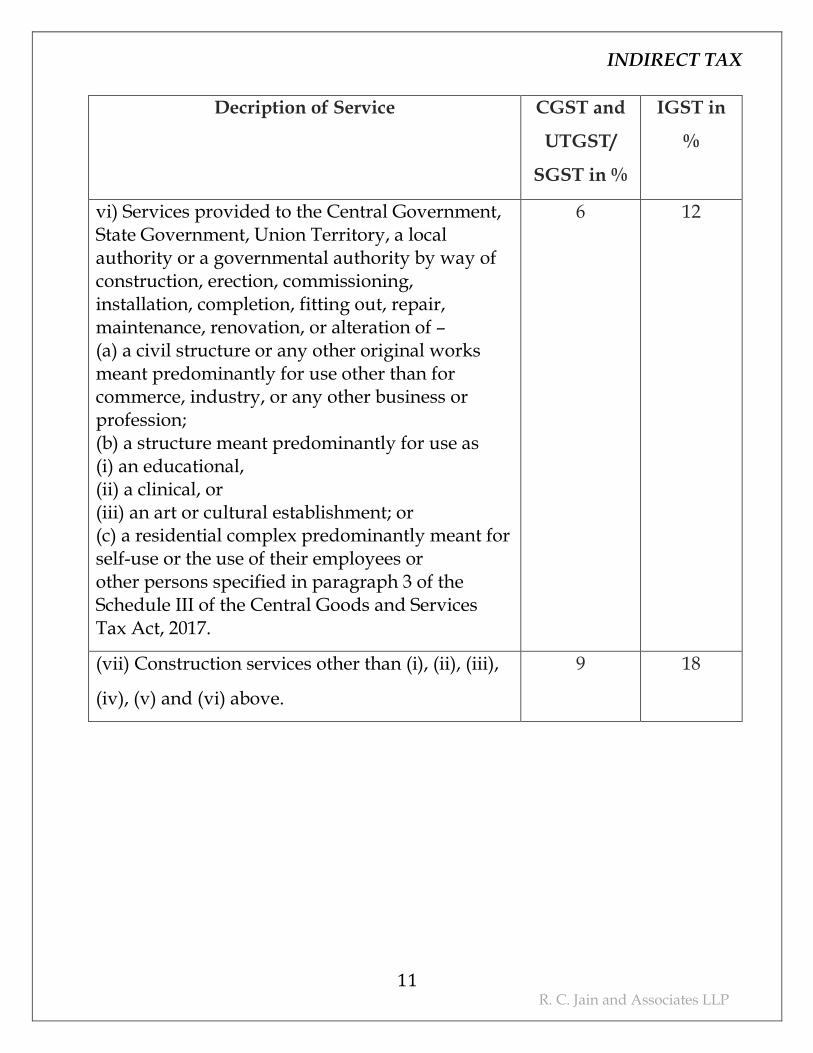

Decription of Service CGST and

UTGST/

SGST in %

IGST in

%

vi) Services provided to the Central Government, State Government, Union Territory, a local authority or a governmental authority by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of – (a) a civil structure or any other original works meant predominantly for use other than for commerce, industry, or any other business or profession; (b) a structure meant predominantly for use as (i) an educational, (ii) a clinical, or (iii) an art or cultural establishment; or (c) a residential complex predominantly meant for self-use or the use of their employees or other persons specified in paragraph 3 of the Schedule III of the Central Goods and Services Tax Act, 2017.

6 12

(vii) Construction services other than (i), (ii), (iii),

(iv), (v) and (vi) above.

9 18

12 R. C. Jain and Associates LLP

INDIRECT TAX

3. Amendment to list of exempted services

Central Government vide Notification No.12/2017- Central Tax (Rate), dated

the 28th June 2017 and Notification No.9/2017- Integrated Tax (Rate), dated

the 28th June, 2017 provided the list of services exempted under GST regime.

In this regard, Central Government vide Notification No. 25/2017- Central

Tax (Rate) dated 21st September, 2017 and Notification No. 25/2017

Integrated Tax (Rate) dated 21st September, 2017 has amended the aforesaid

notification to provide exemption from GST to the following service:

Chapter, Section, Heading, Group or

Service Code (Tariff)

Description of Services Rate %

Chapter 9996

Services by way of right to admission to the events organized under FIFA U-17 World Cup 2017.

Nil

4. Job workers making Inter-State supply of service to a

registered person exempted from obtaining registration.

Central Government vide Notification No. 07/2017-Integrated Tax, dt. 14-09-

2017 has provided that the job workers engaged in making inter-State supply

of services to a registered person are exempted from obtaining registration.

However, said exemption is not available to a job-worker –

(a) who is liable to be registered under sub-section (1) of section 22 or who

opts to take registration voluntarily under sub-section (3) of section 25

of the said Act; or

13 R. C. Jain and Associates LLP

INDIRECT TAX

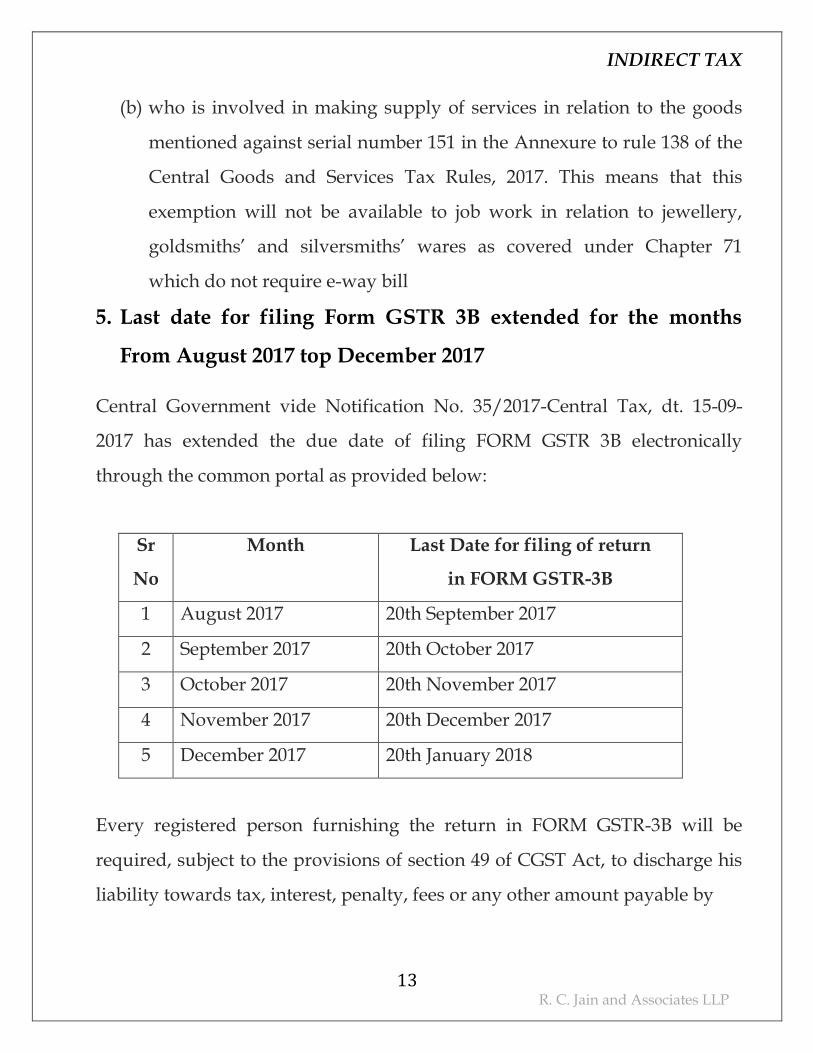

(b) who is involved in making supply of services in relation to the goods

mentioned against serial number 151 in the Annexure to rule 138 of the

Central Goods and Services Tax Rules, 2017. This means that this

exemption will not be available to job work in relation to jewellery,

goldsmiths‟ and silversmiths‟ wares as covered under Chapter 71

which do not require e-way bill

5. Last date for filing Form GSTR 3B extended for the months

From August 2017 top December 2017

Central Government vide Notification No. 35/2017-Central Tax, dt. 15-09-

2017 has extended the due date of filing FORM GSTR 3B electronically

through the common portal as provided below:

Sr

No

Month Last Date for filing of return

in FORM GSTR-3B

1 August 2017 20th September 2017

2 September 2017 20th October 2017

3 October 2017 20th November 2017

4 November 2017 20th December 2017

5 December 2017 20th January 2018

Every registered person furnishing the return in FORM GSTR-3B will be

required, subject to the provisions of section 49 of CGST Act, to discharge his

liability towards tax, interest, penalty, fees or any other amount payable by

14 R. C. Jain and Associates LLP

INDIRECT TAX

debiting the electronic cash ledger or electronic credit ledger, as the case may

be, not later than the last date on which he is required to furnish the said

return.

6. Extension of time limit for filing Return for the month of July,

2017

Central Government vide Notification No. 31/2017- Central Tax dated 11-09-

2017 has extended the time limit for filing the details in form GSTR-1, GSTR-2

and GSTR-3 for the month of July 2017 till the time period as follows:

Sr

No

Details/Returns Class of taxable/registered

persons

Time period for

furnishing of

details/Return

1 Form GSTR 1 Having turnover of more than

one hundred crore rupees

Upto 3rd October,

2017

Having turnover of upto one

hundred crore rupees

Upto 10th October,

2017

2 Form GSTR 2 All Upto 31th October,

2017

3 Form GSTR 3 All Upto 10th

November, 2017

15 R. C. Jain and Associates LLP

INDIRECT TAX

Further, Central Government vide Notification No. 30/2017-Central Tax

dated 11-09-2017 has extended the time limit for furnishing the return by an

Input Service Distributor undersubsection (4) of section 39 of the said Act read

with rule 65 of the Central Goods and Services Tax Rules, 2017, for the month

of July, 2017 upto the 13th October, 2017. However, the extension of the time

limit for furnishing the details or return, as the case may be, for the month of

August, 2017 shall be subsequently notifiedin the Official Gazette.

16 R. C. Jain and Associates LLP

RBI

1. RBI/2017-18/55

DGBA.GBD.No.505/31.02.007/2017-18 Dated 07th September, 2017.

Reimbursement of Merchant Discount Rate (MDR) Charges for

Government transactions up to Rs.1 lakh through debit cards.

i. It is again clarified that the full amount paid to the Government by

the customers / through debit /credit cards should be remitted to the

concerned Government Ministry/Department. The reimbursement of

MDR charges on debit card use (up to Rs.one lakh) can be claimed from

RBI separately as per extant guidelines. Deduction of MDR charges from

the receipts of government is not permissible at all.

ii. MDR charges on debit card transactions above Rs. 1 lakh and on any

credit card transaction are not being absorbed by Government of India

and hence will not be reimbursed by RBI. Accordingly, agency banks

should not deduct MDR charges from the receipts of the government in

these cases also.

iii. It may please be noted that as directed by the O/o the CGA vide its OM

No.S-11012/1(12)/MDR/2017/RBD/824-894 dated May 11, 2017,

agency banks which have remitted the net amount of Government

receipts after deduction of MDR charges to the Ministries/Departments

in contravention of the guidelines referred to above are required to

remit the MDR charges so deducted immediately to the concerned

Ministry/Department under intimation to Reserve bank of India.

17 R. C. Jain and Associates LLP

RBI

2. RBI/2017-18/55

DGBA.GBD.No.505/31.02.007/2017-18 Dated 07th September, 2017

Formation of new districts in the State of West Bengal -

Assignment of Lead Bank Responsibility

The Government of West Bengal vide Gazette Notification dated March 20,

2017 had notified the creation of a new district “Jhargram” with effect from

April 4, 2017 and by Gazette Notification dated March 24, 2017 created a new

district “Paschim Bardhaman” with effect from April 7, 2017 in the State of

West Bengal. It has been decided to assign the lead bank responsibility of the

new districts as detailed below:-

Sr

No

Newly

carved

district

Erstwhile

District

Sub Divisions of newly

created districts

Lead Bank

Responsibility

assigned to

District

Working

Code

allotted

to new

district

1 Paschim

Medinipur

Paschim

Medinipur

Medinipur Sadar,

Kharagpur, Ghatal

United Bank of

India

112

2 Jhargram Paschim

Medinipur

Jhargram Sadar United Bank of

India

398

3 Purba

Bardhaman

Purba

Bardhaman

Bardhaman Sadar North,

Bardhaman Sadar South,

Katwa, Kalna

UCO Bank 399

4 Paschim

Bardhaman

Purba

Bardhaman

Asansol Sadar, Durgapur State Bank of

India

403

The District Working Code of the new districts have been allotted for the purpose of BSR

reporting by banks. There is no change in the lead bank responsibilities of the other

districts in the State of West Bengal.

18 R. C. Jain and Associates LLP

FEMA

RBI/2017-18/64

A.P. (DIR Series) Circular No. 05 Dated 22nd September, 2017.

Investment by Foreign Portfolio Investors in Corporate Debt Securities

Currently, the limit for investment by Foreign Portfolio Investors (FPIs) in

corporate bonds is Rs. 2,44,323 crore. This includes issuance of Rupee

denominated bonds overseas (Masala Bonds) by resident entities of Rs.

44,001 crore (including pipeline). The Masala Bonds are presently reckoned

both under Combined Corporate Debt Limit (CCDL) for FPI and External

Commercial Borrowings (ECBs).

On a review, and to further harmonize norms for Masala Bonds issuance

with the ECB guidelines, the following changes are made:

i. With effect from October 3, 2017, Masala bonds will no longer form a

part of the limit for FPI investments in corporate bonds. They will

form a part of the ECBs and will be monitored accordingly.

ii. The amount of Rs. 44,001 crore arising from shifting of Masala bonds

will be released for FPI investment in corporate bonds over the next

two quarters.

iii. An amount of Rs. 9,500 crore in each quarter will be available only for

investment in infrastructure sector by long term FPIs (i.e., Sovereign

Wealth Funds, Multilateral Agencies, Endowment Funds, Insurance

Funds, Pension Funds and Foreign Central Banks).

19 R. C. Jain and Associates LLP

CORPORATE LAW

1. (Acceptance of Deposits) Second Amendment Rules, 2017.

Notification G.S.R. 1172(E)

A Specified IFSC Public company and a private company may accept from its

members monies not exceeding one hundred percent of aggregate of the paid

up share capital, free reserves and securities premium account and such

company shall file the details of monies so accepted to the Registrar in Form

DPT-3.

A Specified IFSC Public company means an unlisted public company which is

licensed to operate by the Reserve Bank of India or the Securities and

Exchange Board of India or the Insurance Regulatory and Development

Authority of India from the International Financial Services Centre located in

an approved multi services Special Economic Zone set-up under the Special

Economic Zones Act, 2005 (28 of 2005) read with the Special Economic Zones

Rules, 2006:

http://www.mca.gov.in/Ministry/pdf/CompaniesAcceptanceofDepositSeco

ndAmendmentRule_22092017.pdf

2. Restriction on number of layers for certain classes of holding

companies:

On and from the date of commencement of these rules, no company, other

than a company belonging to a class specified in Section 2 clause (87) sub-rule

(2), shall have more than two layers of subsidiaries:

20 R. C. Jain and Associates LLP

CORPORATE LAW

http://www.mca.gov.in/Ministry/pdf/CompaniesRestrictionOnNumberofL

ayersRule_22092017.pdf

http://www.mca.gov.in/Ministry/pdf/CommencementNotification_2209201

7.pdf

3. Exemption given to certain Unlisted Public Companies under the

Companies (Appointment & Qualification of Director) Rules, 2014 from the

appointment of independent directors- reg

The said amended Rule 4 inter-alia provides that an unlisted public company

which is a joint venture, a wholly owned subsidiary or a dormant company

will not be required to appoint Independent Directors.

http://www.mca.gov.in/Ministry/pdf/GeneralCircular_05092017.pdf

Allow us to tell you more!

R.C. JAIN & ASSOCIATES LLP Chartered Accountants Website: www.rcjainca.com Head Office: Mumbai - 622-624, The Corporate Centre,

Nirmal Lifestyles, L.B.S. Marg, Mulund (W), Mumbai – 400080. Email: [email protected] Phone: 25628290/91, 67700107

Branch Offices: Bhopal - 302, Plot No. 75 B, First Floor,

Above Apurti Supermarket, Near Chetak Bridge, Kasturba Nagar, Bhopal. Madhya Pradesh– 462 001 Email: [email protected] Phone: 0755-2600646

Aurangabad - Su-Shobha, Plot No.7,

Mitranagar, Behind Akashwani, Near Maratha Darbar Hotel, Aurangabad - 431001. Email: [email protected]

Phone: 0240-2357556