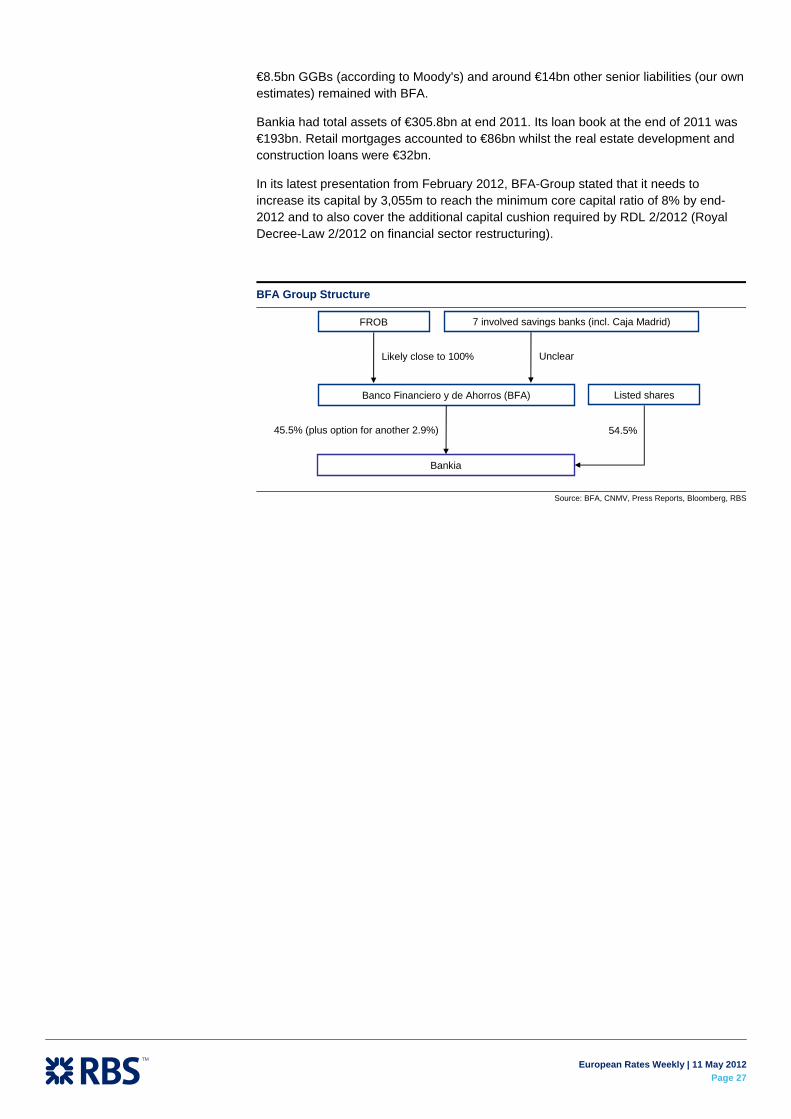

Embed Size (px)

Citation preview

European Rates Research 11 May 2012

Important disclosures can be found on the last page of this publication.

Analysts

Andrew Roberts Head of European Rates Research +44 20 7085 1702 [email protected]

Harvinder Sian Senior European Rates Strategist +44 20 7085 6539 [email protected]

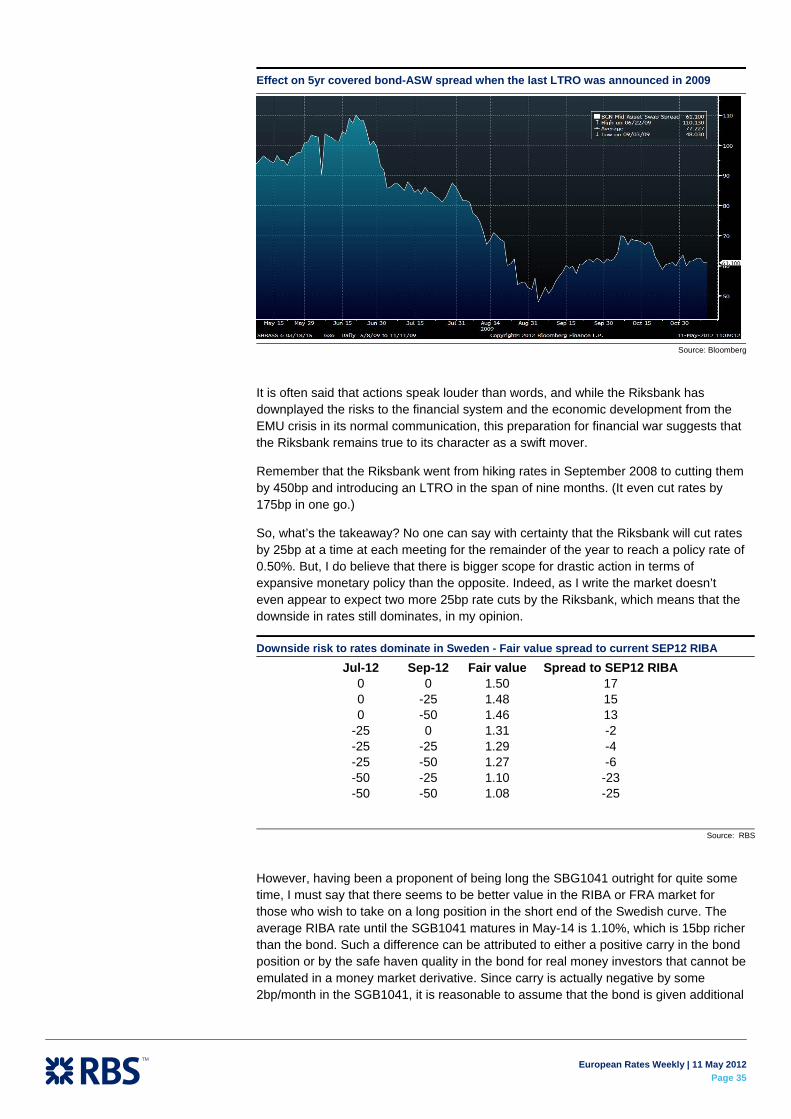

Par Magnusson Chief Analyst Scandinavian Rates Strategy +46 8 506 198 79 [email protected]

Giles Gale European Rates Research +44 207 085 5917 [email protected]

Simon Peck European Rates Research +44 2033611931 [email protected]

Dmytro Bondar European Rates Research +44 20 3361 4160 [email protected]

Biagio Lapolla European Rates Research +44 2033617597 [email protected]

Brian Mangwiro European Rates Research +44 20 3361 3848 [email protected]

Claire Tucker European Rates Research +44 207 085 8480 [email protected]

www.rbsm.com/strategy

European Rates Weekly The exit discussion is now . . . open

Overview (p2): this past week has showed there are few FI longs. I think the risk of a yield plunge is higher than a yield sell-off. Watch now for reversal of those Q1 FI->equity trades. This would make you bullish 30s, but 10s remains safe sweetspot, in bunds. Though everyone wins: witness JGBs. The cat is out of the bag. The EMU exit debate is now finally in the open about whether exits would be devastating for the economy or not. We know what we think - it has been perfectly clear for 2 years how EMU will play through. Next steps: markets will educate on what exits looks like, deposit flight risk is next coming big theme. Euro Area Strategy (p7): Remain bullish core rates for instance still in €3F1Y and at the long end. FRA/OIS basis expected to drift wider but prefer via cheap 1x1 puts in front Euribor or forward basis spreads. The rally to new yield lows in Bunds is not done. Target 10y at 1.25%. €10s30s has flattened back to normal valuations. There is some risk of CVA and Danish long buying. We still like fwd steepeners, with 20y a sweet spot. New Greek elections likely and the hope is disaffected voters back ‘pro-bailout’ parties. If not, Euro exit risks rise. Absent a pro-Euro response, opening up of exit risk means deposit risk across periphery. Spain’s bad bank plan: The headline provisions are more realistic but will still be revised higher in our view which is a risk given market conditions. We do not think this plan is enough around the crisis for SPGBs.

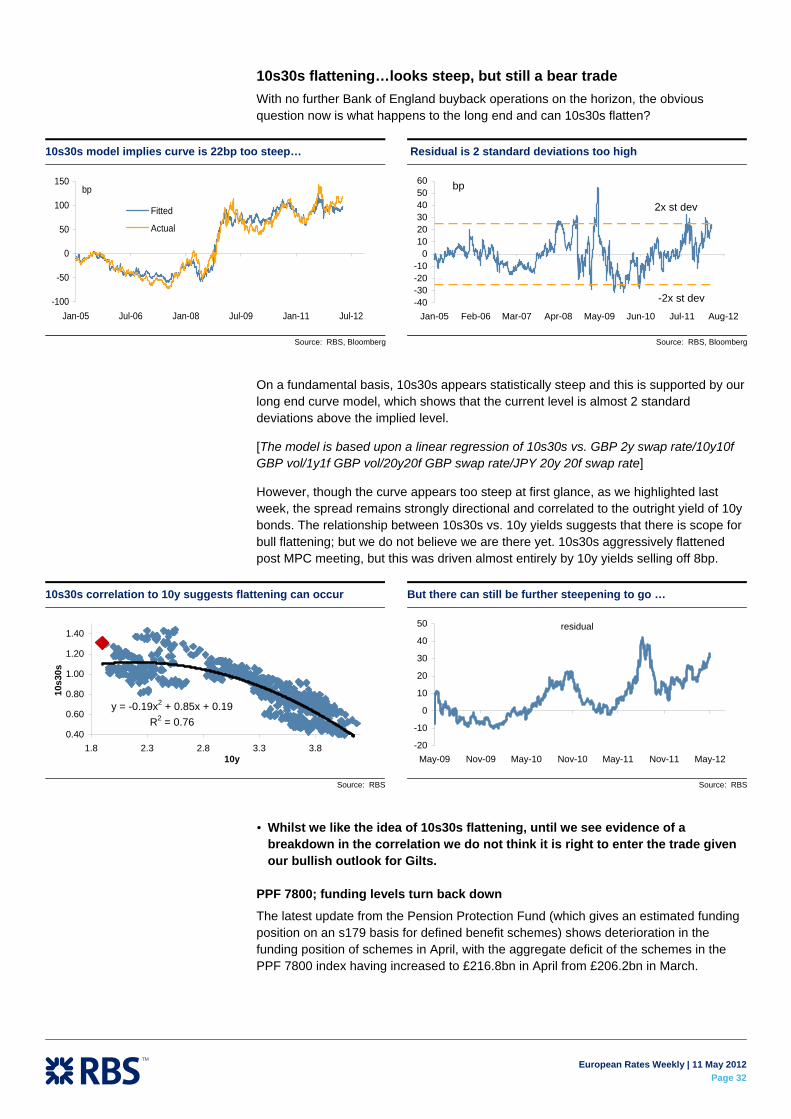

UK Strategy (p31): 10s30s is too steep, and is tempting; but for now this remains a bear trade, 78% correlated to 10y. We look for the BoE Inflation Report on Wednesday to signal that the MPC has made a small move towards a more neutral bias, but this is discounted.

Scandinavian Strategy (p34): The Riksbank prepares for financial war as it establishes a framework for QE and LTRO. Macro data are deplorable in Sweden, so the road to more aggressive monetary policy is paved. We move your profit target levels.

Inflation-Linked Strategy (p38): Euro Area fundamentals suggest sticky inflation and a tight supply side. I argue to use the recent steepening to put on breakeven flatteners in 5s30s. In UK RPI, expect directionality in level and curve to remain until we break at least 10bp higher in real yield. The IL62s syndication makes me less positive on the ultra-longs.

Volatility Strategy (p 44): Euro Area and GBP volatilities have been very well bid, particularly in the top left in GBP and top-right in EUR. Scope for instability over the coming months is high and I would expect that disaster protection will keep volatility relatively supported.

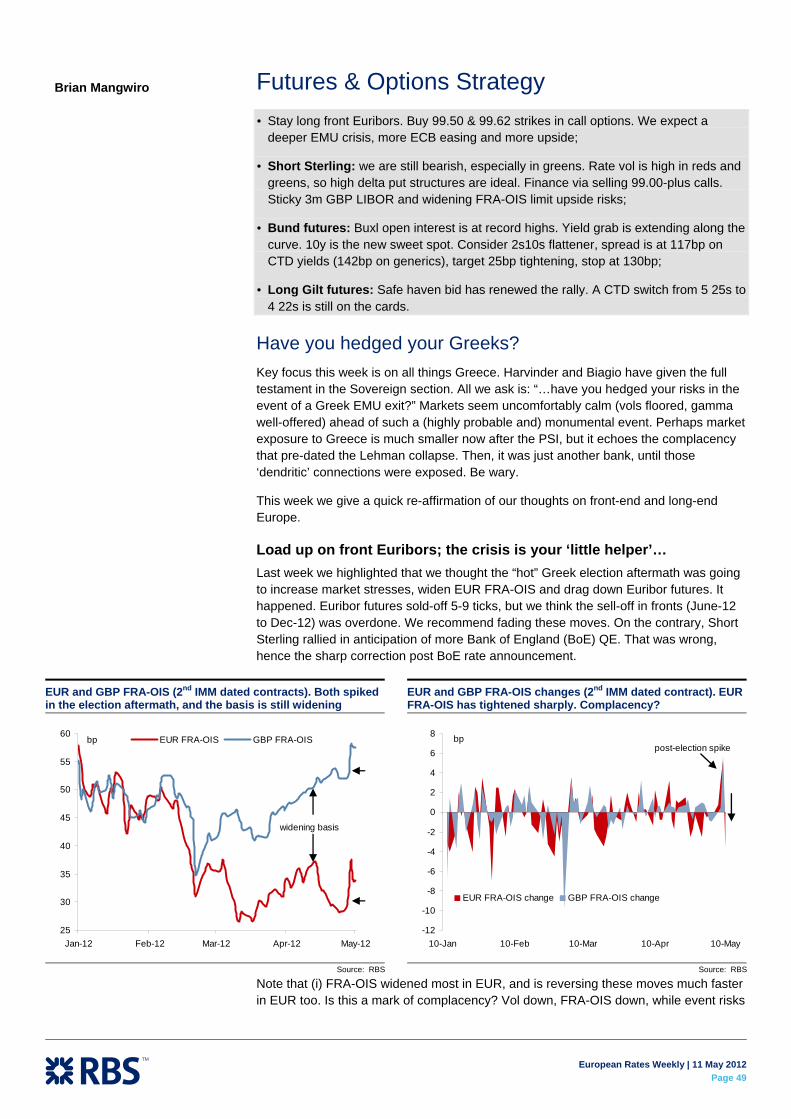

Futures & Options Strategy (p49): Fade the sell-off in front Euribors. Consider EUR 2s10s or 5s30s flatteners. For Short Sterling, prefer high delta put structures in greens vs. selling 99.00-plus calls.

Technical Strategy (p56): Bunds have reached the 142.85 target, but displayed signals of possible short-term correction before continuing to move higher. A similar picture is Sweden.

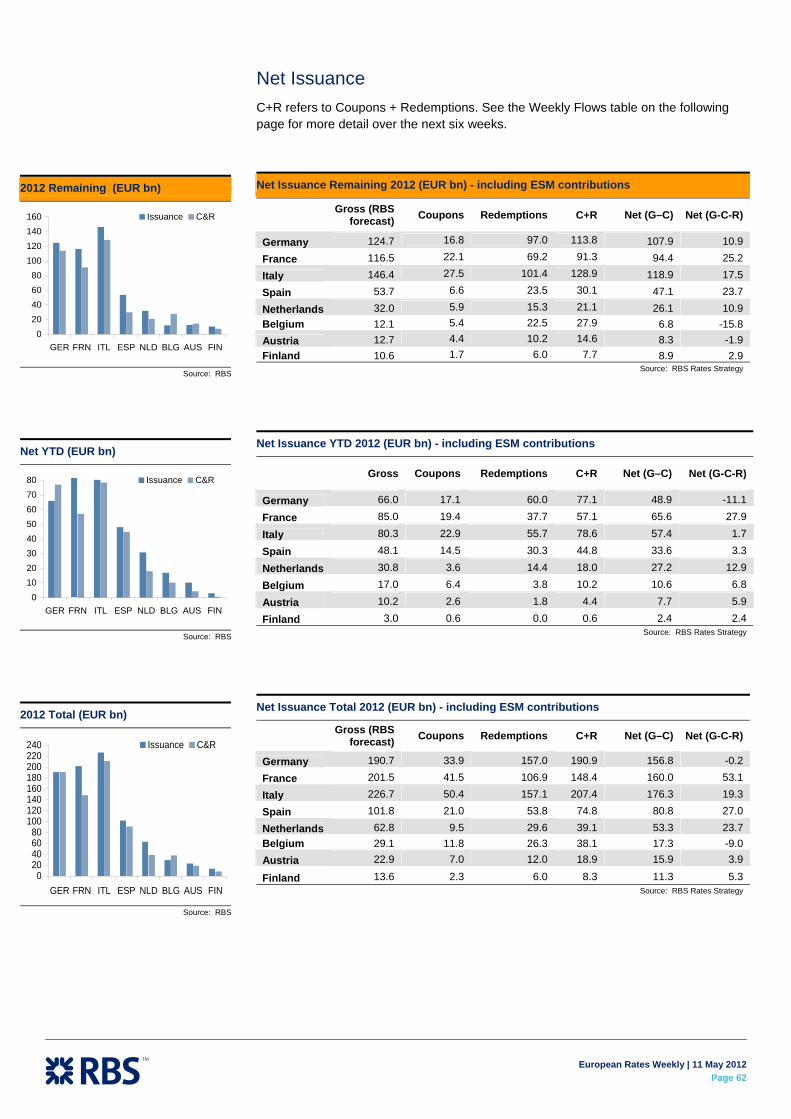

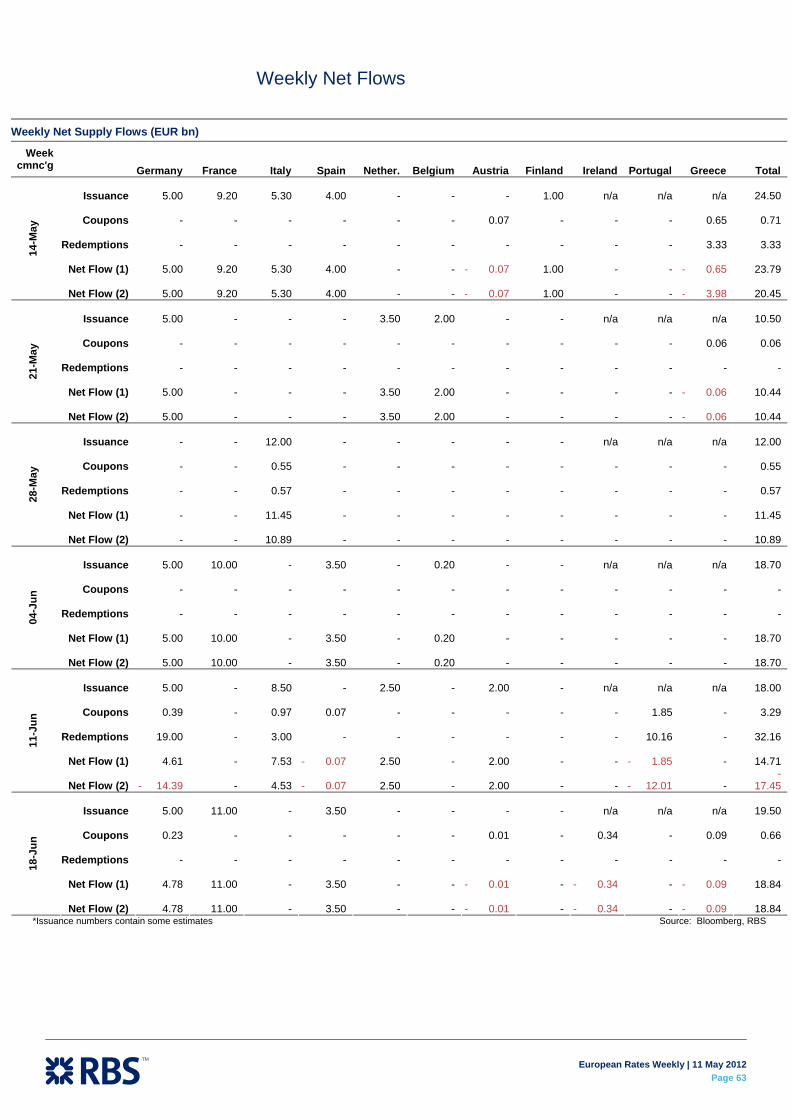

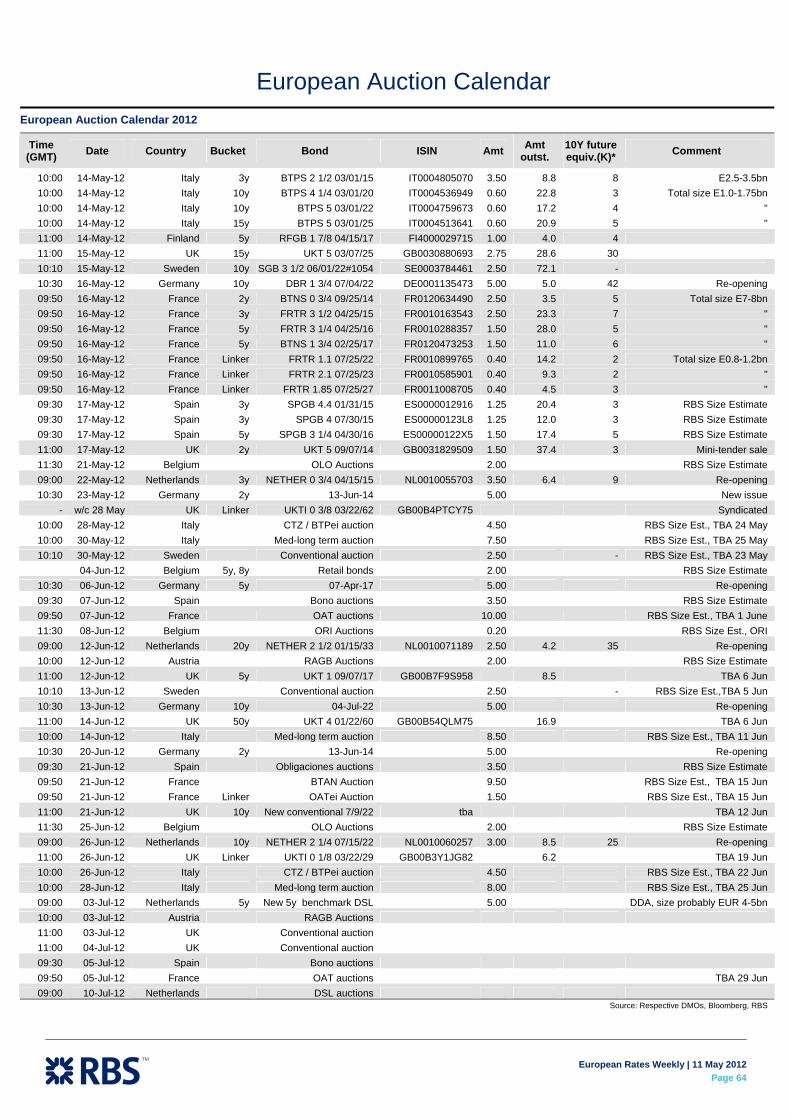

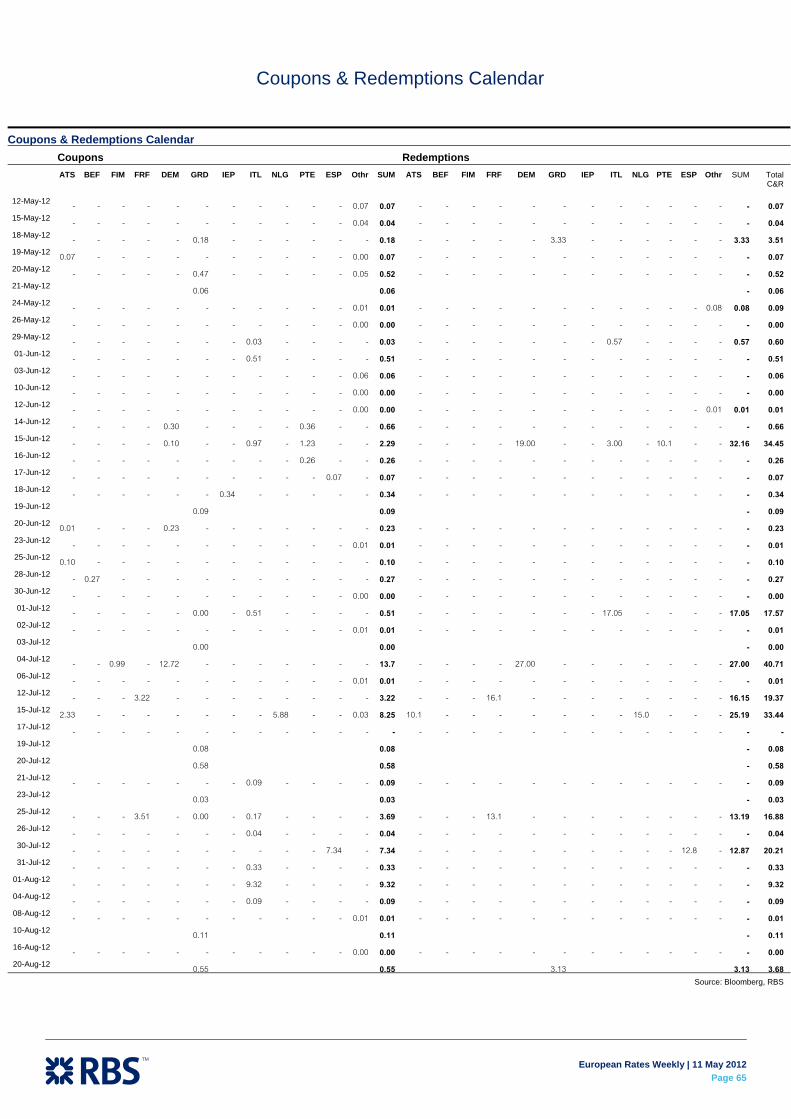

EMU Issuance Update (p57): Weekly bond flows (p63), Auction Calendar (p64), Coupon & Redemption (p65), Portfolio of Trade Ideas (p66), Macro forecasts (p71)

European Rates Weekly | 11 May 2012

Page 2

Overview: the exit discussion is now… open Net: things can only get worse. My key theme of last week – that very few are believers in our scenario and so there are very few who are long, let alone limit long, seems the correct theme. I think the risk of a yield plunge is higher than a yield sell-off, especially since all those FI->equity trades in Q1 (when the world was allegedly fixed), have not been reversed yet. This would make you bullish 30s, but 10s remains safer sweetspot, bunds favoured market. But this is not just about bunds: witness the incredible moves in JGBs where shorts are being squeezed.

The cat is out of the bag. The debate is now – finally - on for Greece, and whether countries can live outside EMU, and whether this would be devastating for the economy or not (I know what I think – I show how Greece is a huge winner in total debt terms, if it left EMU and executed a currency or hard default on its debt, its circumstances would be changed). We are extremely clear on this: it has been obvious for a number of years how EMU will play through. It has worked to plan since Q2 2010, so next steps are a) markets will educate now on what exiting looks like, expect chat on Iceland, Argentina, Uruguay, etc; b) next big theme will be deposit flight risk; which in turn makes c) increasing discussion about others being affected. Short periphery.

I think the risk now is for a yield plunge.

Too many are still looking the wrong way, ie are looking for ‘exit’ trades on the overriding global financial theme of ‘safe havens rallying’.

There are many ways to view this, such as via EMU 5y25f, where you can enter a 1x2 spreads and as long as yields are above -6bp in 25 years, you make money. Note that long end EMU, which has been lagging the 5 & 10yr sectors as we would expect in this lower yield move, has seen a strong end of week performance, leaving 10s30s 2bp flatter on the week. And in forward space, such as EMU 5y25f mentioned above, there have been severe downward yield spikes. At the time of writing (Friday afternoon) this is -26bp on the day. A tempting sell at 1.81%? Perhaps, but I will not be selling it.

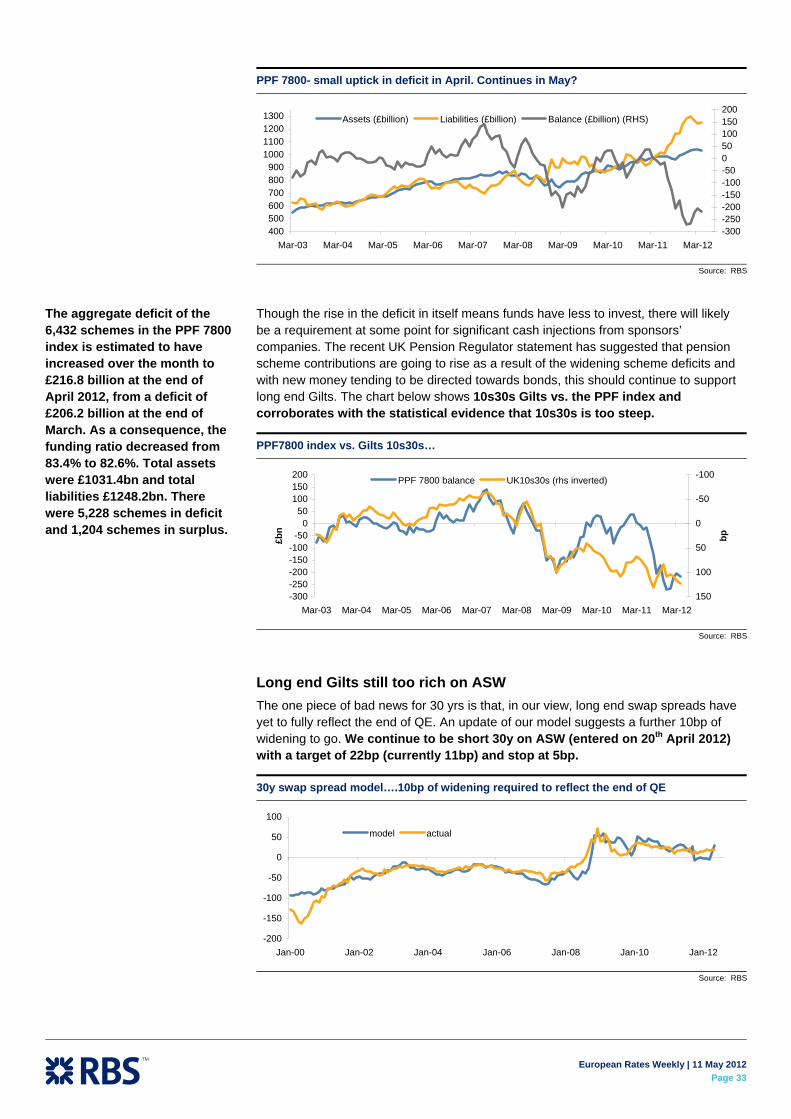

It is clear what is happening – no one is long, and eventually this will become an issue for ALM funds. Impossible to time, but not impossible to call as a theme. Also see Simon Peck’s very timely UK article about the UK pension fund solvency update – this is all very similar to that of EMU, ie, we know there is a mismatch, we know there is a latent bid, and we know that bid will eventually potentially disconnect yields much lower. We want to have such trades onside. We cannot risk a flattener in a bull steepening world, but it does make you more outright bullish.

I discussed last week another 3 pointers that show a marketplace that is underweight risk in our ‘safe haven’ trade (ie long 10y bunds is the sweetspot, or however you wish to position for this, eg 5y5y, or long of lower for longer trades in 1y3f in EMU, or long of 10y UK/US/Canada/Australia/Sweden – we will make or lose our years via absolute market-level bets). To recap, those pointers were the violent reaction to the Australian -50bp rate cut; the fact USTs made strong new highs and broke to new yield lows post payrolls despite our survey showing the highest proportion in a year of clients alleging (in advance) they wanted to sell upticks; and the sharp rally in Gilts two weeks ago as many short positions were squeezed out.

You could argue in the UK’s case that the same has just happened on Friday. After an alleged watershed last Thursday of no more QE from the MPC (merely locking in the move to neutral from Mr Posen/Tucker/MPC minutes – even we were not seeing more QE at that meeting), many jumped on the ‘end of QE’ view, and 10y Gilts took back most of the week’s gains – yet they then immediately bounced back the next day.

Andrew Roberts

European Rates Weekly | 11 May 2012

Page 3

Yet again, the market is causing most pain where it can – there is enough evidence to suck in bond bears for a day, but the overriding theme is still lower yields (for the record, even with that blowout +8bp day, 10y Gilts rallied net -5bp in the past week).

It is dangerous being short any safe haven product given Europe is hastening now to its conclusion.

Is this just about EMU? Not only. Some other very bullish pointers for you before we even start on the biggest theme in Europe – deposit flight – which will soon be everyone’s top theme.

1) Sweden this week followed through on end-April proposals to set up a Swedish gov’t bond portfolio, readying itself for QE if it needs to do so. An SEK10bn fund is not going to excite anyone, and this is just about increasing the available tools to the Riksbank, but the signal it sends is powerful. Well, it is to us - the reaction we were fed back with was ‘old news’ (it had been suggested on 27 April). Yet 10-yr Sweden has this week moved back below 10-yr Germany for the first time since February. Do read Par Magnusson’s piece where he discusses the portfolio in detail.

2) UK construction data was revised from -3% to -4.8%, which cuts GDP by an extra -0.14%, which means a revision down in UK Q1 GDP at next print from -0.2% to at least -0.3%.

3) Japan is not on everyone’s radar screens. We suspect this is partly because yields have been so low for so long that there has been an unwillingness to invest. I remember an old boss, 10 years ago, making the point that global investors had been underweight JGBs in their global gov’t portfolios for 15 years. Well, not much has changed. Being short JGBs has been a more popular trade in Q4 2011 with growing fears about lack of household sponsorship – I certainly had numerous conversations about it in November/December. I can see the reasons why Japan is inevitably a terrible credit in a few years time, but I would not consider that a trade for now. We have just updated our RBS sovereign risk index (which takes into account total debt levels, rule of law, bank assets, loan to deposit ratios, etc), and Japan is now the worst credit in the developed world. Last time – published in the year ahead - it was 2nd worst, after Greece. But the idea they sell-off now misses the large corporate surpluses which can and will be put to work, or the policy flexibility to keep JGB yields low (ie, it becomes a yen trade, not an FI trade – we will return to this in a year or perhaps longer). Anyway, the point is that all the payer swaptions were entered at 1-1.1% on 10y JGB equivalent, and Japan is showing one of the world’s most violent bond rallies. This is an absolute value world, do not be short any safe havens.

On that subject, read an ECB paper in the monthly bulletin which compares Europe to Japan. My new catchword is Japanification (of Europe). See Giles Gale’s volatility articles for more (especially last week’s). 1y forwards have converged from 20yrs onwards, but EMU forwards sit substantially higher than Japan further up the curve (eg 1y10f in EMU is 3.06%, over 100bp above the 2.01% in Japan). In my view, another strong support for longs in bunds at 5-10yr sector.

My website of the week: www.thecurrencycollector.com

For a great look at how money circulates on a currency exit, click on ‘stamps on notes’

European Rates Weekly | 11 May 2012

Page 4

Leaving aside the interesting charts above, which show that Japan did not start its recession/deleveraging period with terrible numbers, it was the ongoing lack of credit creation, and devastating cut to trend GDP that had such long lasting corrosive effect. One of my big themes some years ago was that trend GDP in Japan had moved from 4.1% in 1990 to sub 1% by the mid 2000s. This is a primary support for much lower structural bond yields in developed majors – trend GDP is on its way down once you overlay deleveraging and demographics, the 2 overriding themes in my opinion. The below chart shows how the US is going some way to getting through its deleveraging (well, only in a private sector sense), but EMU has done …nothing.

House prices. Adjustments can take a long time

Source: RBS; ECB monthly bulletin; S&P; Fiserv; MacroMarkets LLC; Japan Real Estate Research Institute

We apologise if this does not seem very ‘weekly’, but it is absolutely relevant as your big overarching theme. And it goes a long way to explaining why bonds are not rich right now. Sure, they may be close to the rich end of our fair value models for bunds and Gilts, but I would not describe them as over-expensive. It just requires an adoption of the concept of JAPANIFICATION to see that perhaps rates stay long forever (it was only a month ago that many were seeing early Fed & MPC exits etc), and term premia are too high along the curve out to 10 years.

Gross debt/GDP ratio: EMU is following the identical path to Japan. US and EMU have some optimistic forecasts

Source: IMF Word Economic Outlook, October 2011; RBS; ECB Monthly bulletin

. . . and Japan started with a far better primary balance than EMU (& US)

Source: IMF Word Economic Outlook, October 2011; RBS; ECB monthly bulletin

European Rates Weekly | 11 May 2012

Page 5

Back to Europe

I introduced last week’s overview with the following view on Greece

“Greece’s elections are woefully under focused on, a no result/weak majority is very possible, we are sceptical of the idea that PASOK/ND are an easy done deal (in financial market estimate terms), and suspect that immediate talk come the week ahead will be about exit & renegotiations.”

Why was Greece so underdiscussed? This past week has suddenly seen all those telling us that Greece was a one-off with no effect on anything else (well, 10yr Spain is net +28bp on the week) being replaced with the media now starting to talk about the most relevant point as far as I can see it: if a country exits, you have a blueprint, and it risks a bushfire across some European countries.

Why? Whether you believe or not that any other country will follow the path that Greece is about to tread (I personally believe they will, but have never wanted to be seen as stoking the fire of the crisis by writing such over the past two years), the prospect of the private sector removing their deposits risks making events self-fulfilling.

We suspect many will start discussing Argentina a lot more in coming weeks. Harvinder Sian and Biagio Lapolla write about it at length in this document. Remember that under exits from currency unions, you will not necessarily leave all your debts in other currencies – could Hellenic Telecom be paid in new drachmas but have its debt still in euros? – which is why Argentina, with its dollarized economy (90% of its mortgages were in USD), just passed a law converting everything to pesos.

Once you take this on board, you realise that the key numbers to be following are bank deposit data, which we have been discussing in every meeting for some months. It is not falling off dramatically yet in Italy, but it is doing so in Spain.

We have a responsibility not to be overly aggressive in this debate, which we hope you will feel we have not been, and there are many sensitive parties out there, but we have finally reached the point at which a sensible debate can start, about the economic viability of certain countries membership of EMU.

I focus on total debt all the time. For me, we are in a debt deleveraging world, and it is ludicrous to just look at government debt. I do not understand why the market concentrates on just government debt. For starters, as Spain showed last week, and everyone did in 2008, bank debts can quickly become government debts! As can household & corporate debts if you turn into recession and bad debts start to rise etc.

Total Debt: Greece is a big winner. Major implications for the economy post-EMU . . .

Source: RBS; McKinsey; Haver Analytics

European Rates Weekly | 11 May 2012

Page 6

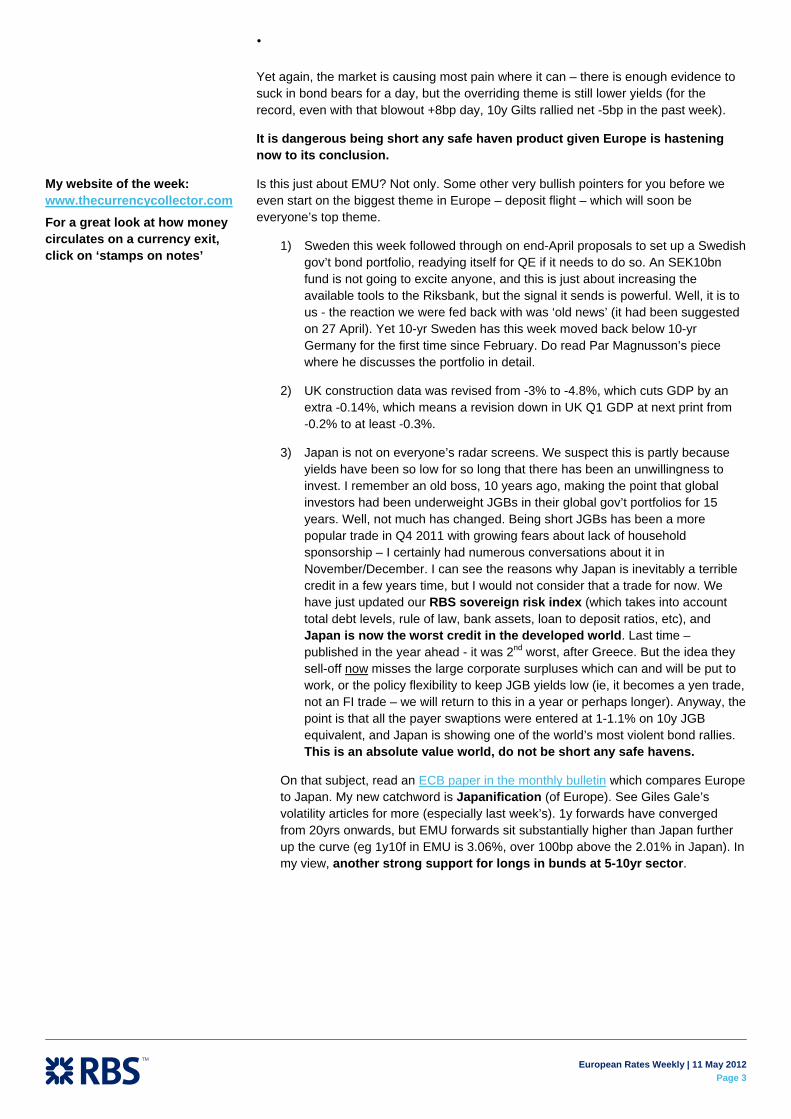

As such, the chart above is a favourite in my presentation. Greece is actually a net winner, once you take off the cloud hanging over the country of its un-surmountable government debt mountain. This has major implications for risky asset performance there once they leave the currency zone.

This also, sadly, has implications for those who wrongly see Greece as a one-off.

2012 real GDP, change in forecast from Autumn 2011 to May 2012. Spain…and EMU…

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

Slo

vaki

a

US

A

Pol

and

L

uxem

bour

g

Jap

an

Ger

man

y

Fra

nce

M

alta

A

ustri

a

Uni

ted

Kin

gdom

C

hina

P

ortu

gal

Den

mar

k

Lat

via

I

rela

nd

Fin

land

C

zech

Rep

ublic

R

oman

ia

Cyp

rus

E

uro

area

H

unga

ry

Bel

gium

L

ithua

nia

S

wed

en

Net

herla

nds

I

taly

E

ston

ia

Bul

garia

G

reec

e

Cro

atia

S

love

nia

S

pain

Source: RBS; European Commission

If global growth were to take off, my theme here would be less powerful. But we are still in a woeful growth environment across EMU (see the growth chart above, still falling, momentum is downward, not upward), debt is being paid down, and we still hold a E5trn forecast cut to total European bank assets.

Total debt is without any question going to haunt many economies – and Spain’s total debt is 100% greater than that of Greece. (As an aside, if of interest, the USA does exceedingly well in this regard, total debt is <300%, other winners are Canada and Australia, both at the same level as the USA). This is the essence, for me, of why I do not agree with the idea that Greece is a one-off. Low and weakening growth + high debt levels = continuing upgrades for expected write-downs (such as the E98bn we see for further Spanish bank write-downs under our credit specialist, Alberto Gallo’s, ‘adverse scenario’).

One last point. In the week ahead the Eco-fin may ease the fiscal adjustment process, and there is much chat about whether this makes the periphery short trade less solid, since it does throw the sovereigns a life-line? No. The key point is that this is happening in response to some terrible growth forecast revisions, visible in the chart above. Spain is in the unenviable position of having had its 2012 GDP forecast cut by 0.8% even from the last update in February. Harvinder Sian is expressing this via short 10-yr Spain.

European Rates Weekly | 11 May 2012

Page 7

Euro Area Rates Strategy There is no change in strategy or tactics from last week. We remain bullish in core rates with lower for long seen as favouring ongoing exposure to rates such as €3F1Y and also at the long end.

FRA/OIS basis is expected to drift wider but ability of the ECB to restrain bank risk is an important variable and means that we prefer to take on only cheap 1x1 puts in front Euribor or longer dated forward basis spreads.

In German bonds, the rally to new yield lows is not done. We continue to target 10y at 1.25% and below, if the Euro exit risk is for real, which we think is the case.

New Trade: Receive EUR 18m forward starting of the 7y tenor versus paying EUR 3F 2y.

€ 10s30s has flattened back to normal valuations and there is some risk of CVA activity and Danish ALM but not Dutch ALM. We continue to see forward steepeners, with 20y as the new sweet spot on the curve, as attractive.

Sovereign Strategy

The volatility and higher spreads that we expect come from two sources. Firstly, the Greece Euro exit risk and secondly, the prospect that the ESM will subordinate SPGB and BTPs will see these markets have more self-fulfilling crisis features.

New Greek elections are likely and the hope is that disaffected voters come back to ‘pro-bailout’ parties. If not, then Euro exit risks rise as Europe can not offer a gift sizeable enough to bribe Greek voters to stay the course. This means, on another hung parliament, that Greek government IOUs could trade as proxy currency as early as July. If this does not galvanise a large pro-euro vote intention into accepting Troika demands the actual exit looms. Opening up the Pandora’s box of exit means deposit risk across the periphery. The future of the euro would then be dictated by the subsequent policy response.

Spain’s new bad bank plan: We assess the news and the risks for SPGBs. The overall headline provisions are more realistic but will still be revised higher in our view which is a risk given that market conditions are not benign. We think that the provisions for small banks means more private to public sector risk transfer and this will also be necessary to make the bad bank plan work. Ultimately, we do not think this plan is enough around the crisis for SPGBs.

Harvinder Sian

Biagio Lapolla

European Rates Weekly | 11 May 2012

Page 8

Lower core rates set to push lower still The rally in core rates has continued with Bund yields hitting new lows. The near term bias from here is determined largely by the flow of events from Greece (on which we think the markets underestimate risk). Perhaps the most surprising feature of the rally is just how many investors have been looking to fight the move despite the fact that long 10y Bund has been one of the best trending performers with volatility low enough to deliver some attractive Sharpe ratios.

Our trading plan for the crisis and the macro data remains vanilla in that both call for

Much more ECB accommodation near term (policy easing and further large scale ECB balance sheet expansion).

Accommodation to be maintained medium term (lower for longer).

Portfolio rebalancing towards core markets favours Bunds, as evidenced in the fact that non resident exposure is rising and this data maps well the decline in Bund yields.

Our targets in 2y Schatz remain at negative yields and 10y Bund at 1.25%. Given the heightened risk of a Greek Euro exit (see the Sovereign section) we do not think that 1.25% is a floor for Bunds with levels below 1% feasible on flow.

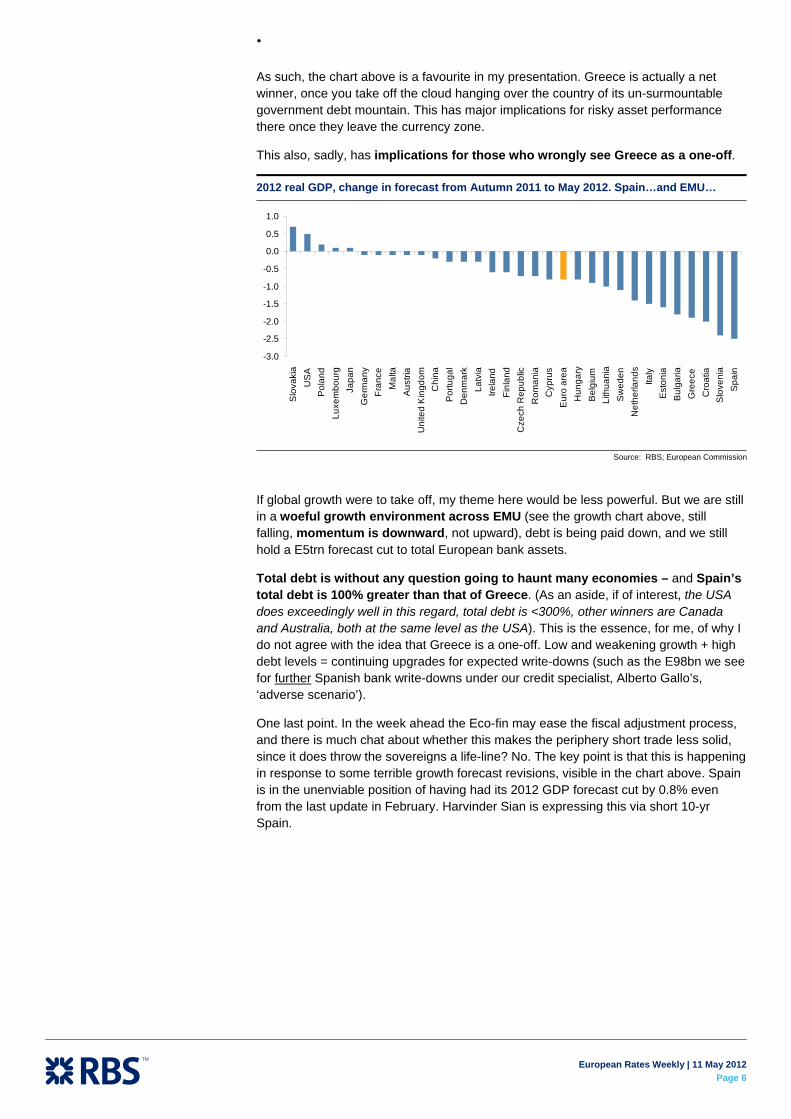

Is FRA/OIS basis turning higher? The past few sessions have seen front futures push lower. This partly reflects the long positioning (bullish trades) and the subsequent unwinding but there has also been a hiatus in the lower 3m Euribor fixings.

Our models of the 3m FRA/OIS have focused on the correlation with the average Euribor panel banks’ CDS (our series trims the mean CDS in line with the Euribor fixing calculation). This shows a good broad directionality of the basis but this has broken down since the end of last year. Not so coincidentally this was the period of large ECB balance sheet expansion following the 3y LTRO – an operation that Draghi has said is meant to ensure the ECB’s lender-of-last-resort functioning.

There are various ways that this could be corrected to arrive at a fair value calculation – such as removing the weaker banks and concentrating on only the Prime banks that are the focus of the Euribor question on the lending rate to other Prime banks. The chart below shows a model using the above banks CDS index and the YoY% rise in the ECB balance sheet.

The inference is that FRA/OIS risks are still to the upside and that there is cheap optionality in forward basis spreads such as 2y2y and even further out. Alternatively, buy the ERU2 99.25/99.125.

FRA/OIS versus the trimmed mean Euribor bank panel CDS

050

100150200250300350400450

Oct

-09

Dec

-09

Feb-

10

Apr

-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb-

11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb-

12

Apr

-12

0102030405060708090Bank CDS (left)

3x6 FRA/OIS

Source: RBS

ECB balance sheet expansion has underpinned banks

1500

1800

2100

2400

2700

3000

3300

Oct-09 Apr-10 Oct-10 Apr-11 Oct-11 Apr-12

ECB Bal Sheet size

EUR mn

Source: RBS

European Rates Weekly | 11 May 2012

Page 9

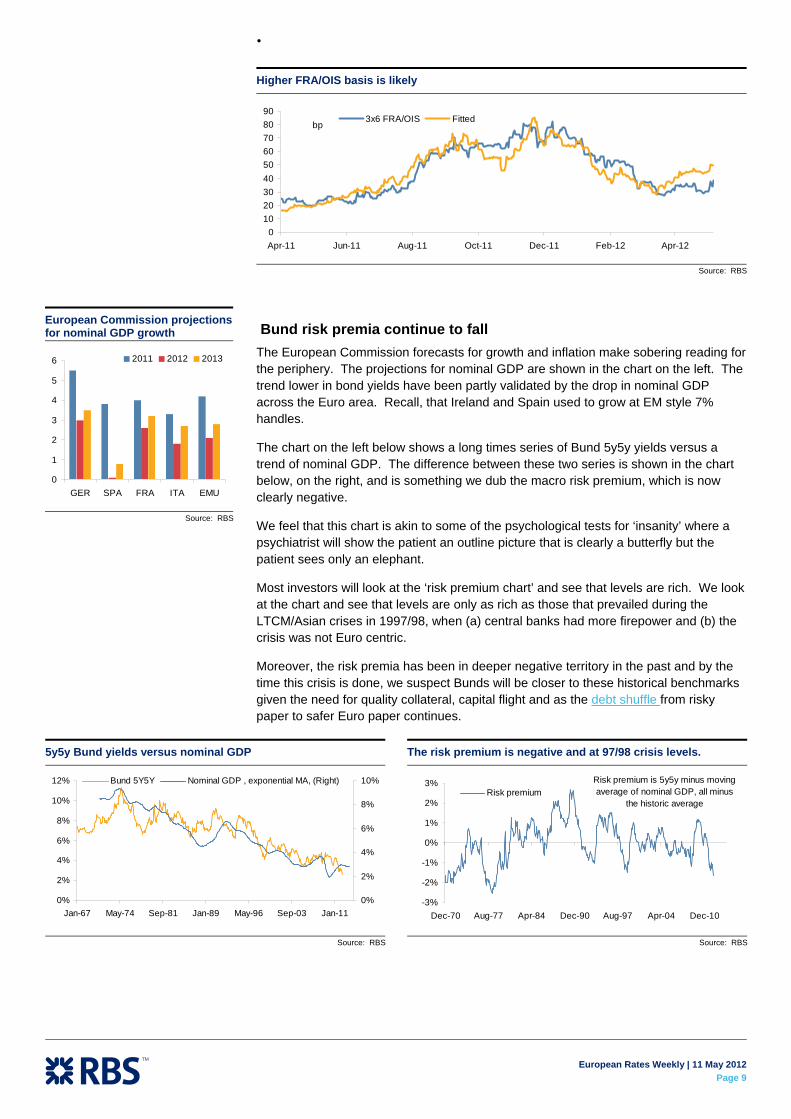

Higher FRA/OIS basis is likely

0102030405060708090

Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12

3x6 FRA/OIS Fittedbp

Source: RBS

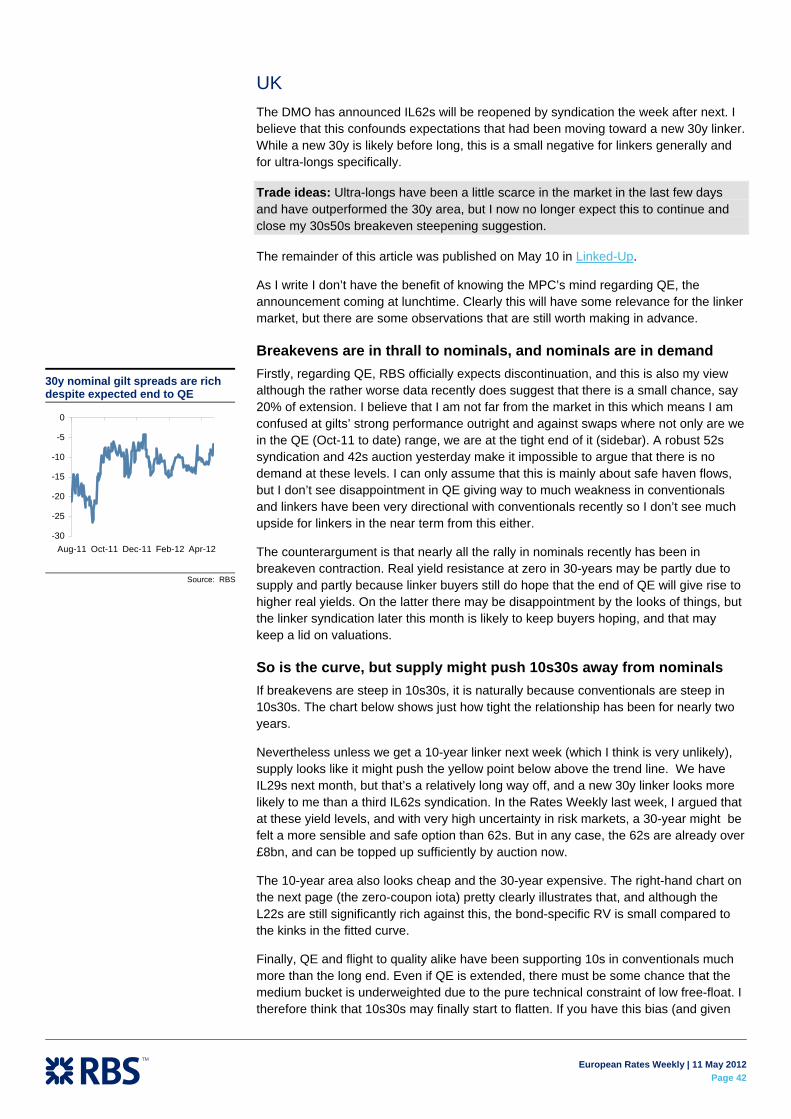

Bund risk premia continue to fall The European Commission forecasts for growth and inflation make sobering reading for the periphery. The projections for nominal GDP are shown in the chart on the left. The trend lower in bond yields have been partly validated by the drop in nominal GDP across the Euro area. Recall, that Ireland and Spain used to grow at EM style 7% handles.

The chart on the left below shows a long times series of Bund 5y5y yields versus a trend of nominal GDP. The difference between these two series is shown in the chart below, on the right, and is something we dub the macro risk premium, which is now clearly negative.

We feel that this chart is akin to some of the psychological tests for ‘insanity’ where a psychiatrist will show the patient an outline picture that is clearly a butterfly but the patient sees only an elephant.

Most investors will look at the ‘risk premium chart’ and see that levels are rich. We look at the chart and see that levels are only as rich as those that prevailed during the LTCM/Asian crises in 1997/98, when (a) central banks had more firepower and (b) the crisis was not Euro centric.

Moreover, the risk premia has been in deeper negative territory in the past and by the time this crisis is done, we suspect Bunds will be closer to these historical benchmarks given the need for quality collateral, capital flight and as the debt shuffle from risky paper to safer Euro paper continues.

European Commission projections for nominal GDP growth

0

1

2

3

4

5

6

GER SPA FRA ITA EMU

2011 2012 2013

Source: RBS

5y5y Bund yields versus nominal GDP

0%

2%

4%

6%

8%

10%

12%

Jan-67 May-74 Sep-81 Jan-89 May-96 Sep-03 Jan-110%

2%

4%

6%

8%

10%Bund 5Y5Y Nominal GDP , exponential MA, (Right)

Source: RBS

The risk premium is negative and at 97/98 crisis levels.

-3%

-2%

-1%

0%

1%

2%

3%

Dec-70 Aug-77 Apr-84 Dec-90 Aug-97 Apr-04 Dec-10

Risk premium Risk premium is 5y5y minus moving average of nominal GDP, all minus

the historic average

Source: RBS

European Rates Weekly | 11 May 2012

Page 10

Richer term premium Our expectation that core rates will continue to push lower is obviously synonymous with flattening risk and lower curvature. To date the lower for longer theme has been played out to 5y but we are expecting longer tenors to 10y to also gain and this throws up some interesting trades.

For instance, the spread between EUR 18m forward start 7y and EUR 3F 2y looks attractive versus historical levels. The spread shows some long term mean-reverting features and the fact this spread has crossed the lower two-standard deviations band (based on an eight-year history) makes the risk reward compelling at these levels.

The trade shows some directionality, evident when looking at the correlation with 10y swaps. That said, the 32% R-squared is hardly impressive and secondly, the scatter chart on the right suggests that even if rates drop from here, the fact current levels are well below the fair value implied by the OLS regression, makes the trade compelling.

New Trade:

Receive EUR 18m forward starting of the 7y tenor versus paying EUR 3F 2y from current -26bp to target -11bp. Place stop loss at -32bp. The carry and roll is negative by 1 bp per month.

Long end swaps reach new lows: will there be an ALM push The all time low in swaps is causing some concern that forced buying at the long end of the curve may be seen by ALM. This has been partly behind the recent flattening in 10s30s swaps though fast money exiting steepeners has also been very prominent.

EUR 2Y Swap, 3Y Forward - EUR 7Y Swap, 18M Forward

-35-30-25-20-15-10

-505

1015

Jun-04 Sep-05 Dec-06 Mar-08 Jun-09 Sep-10 Dec-11

Rec EUR 18m 7Y vs 3F 2y

bp

Source: RBS

Scatter of EUR 18m 7y and EUR 3F 2y vs. 10y Swaps

R2 = 32%

-35-30-25-20-15-10

-505

1015

1.9 2.4 2.9 3.4 3.9 4.4 4.9 5.4

EUR 10y SwapRec

EU

R 1

8m 7

Y v

s 3F

2y

Source: RBS

Long end swap rates have hit new lows

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

May-07 Feb-08 Nov-08 Aug-09 May-10 Feb-11 Nov-11

30y swap 50y swap

Source: RBS

EUR 10s30s versus 30y swap rate

R2 = 0.0223

0

5

10

15

20

25

30

35

40

2.20 2.40 2.60 2.80 3.00 3.20 3.40

bp

30y rate

Source: RBS

European Rates Weekly | 11 May 2012

Page 11

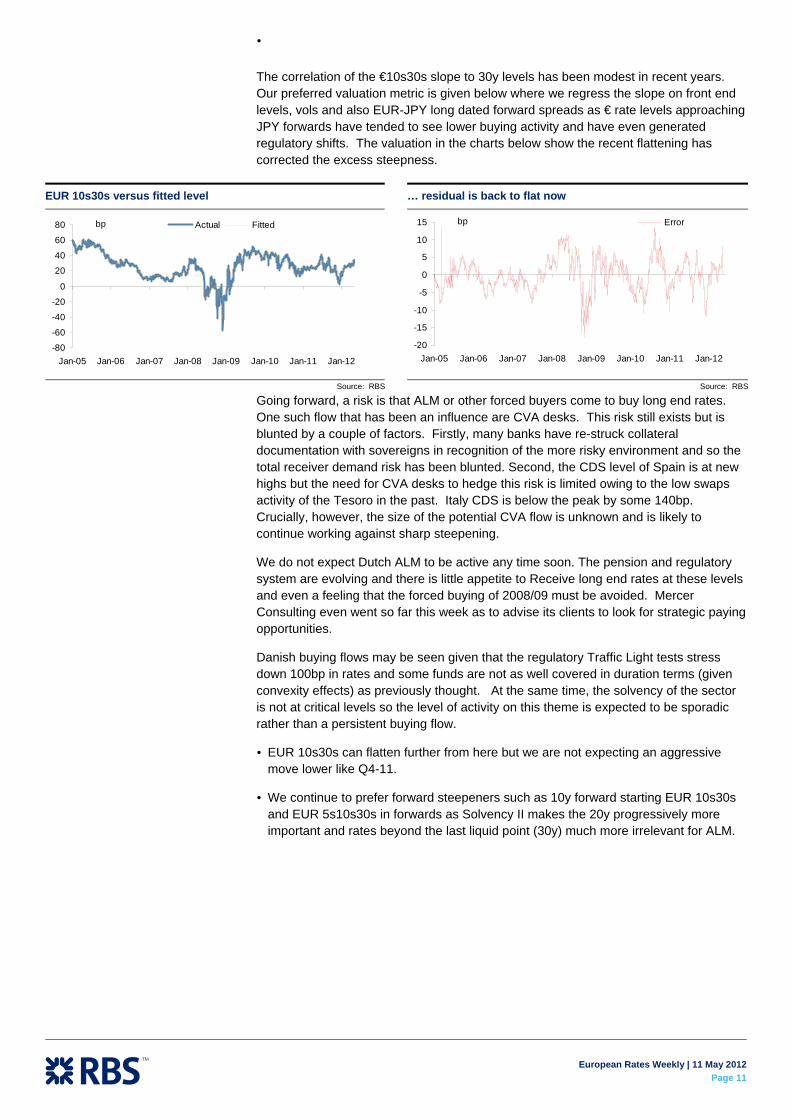

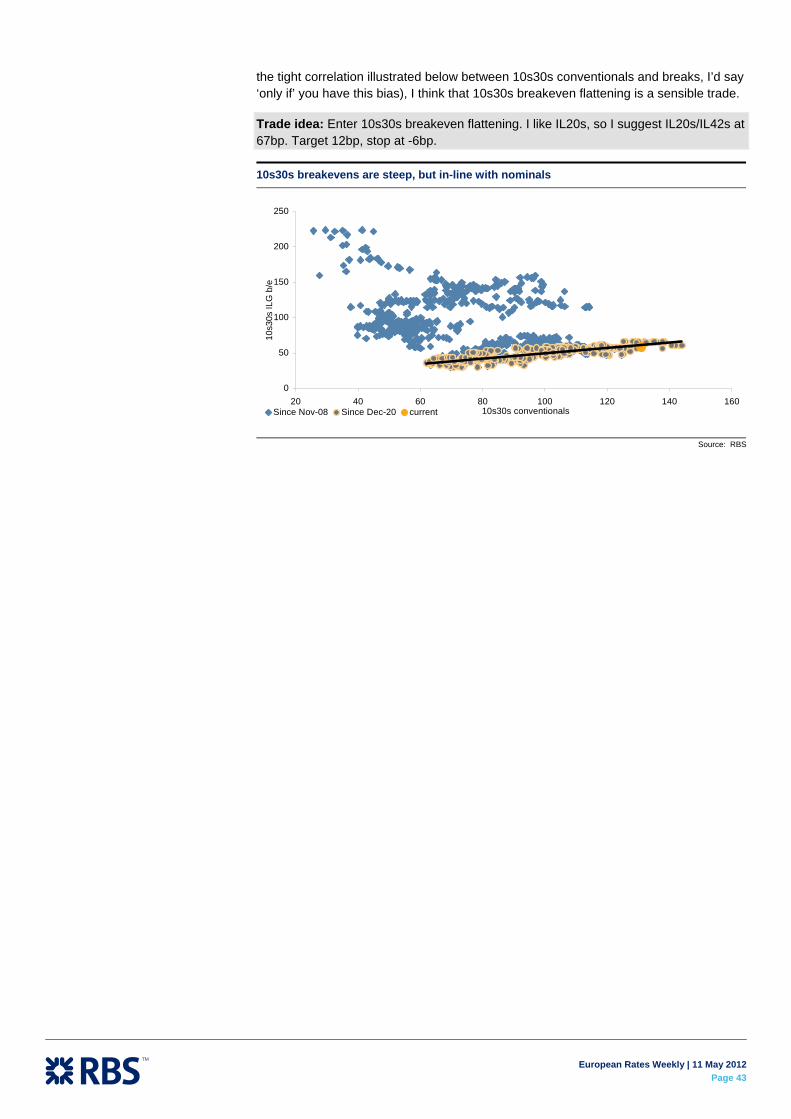

The correlation of the €10s30s slope to 30y levels has been modest in recent years. Our preferred valuation metric is given below where we regress the slope on front end levels, vols and also EUR-JPY long dated forward spreads as € rate levels approaching JPY forwards have tended to see lower buying activity and have even generated regulatory shifts. The valuation in the charts below show the recent flattening has corrected the excess steepness.

Going forward, a risk is that ALM or other forced buyers come to buy long end rates. One such flow that has been an influence are CVA desks. This risk still exists but is blunted by a couple of factors. Firstly, many banks have re-struck collateral documentation with sovereigns in recognition of the more risky environment and so the total receiver demand risk has been blunted. Second, the CDS level of Spain is at new highs but the need for CVA desks to hedge this risk is limited owing to the low swaps activity of the Tesoro in the past. Italy CDS is below the peak by some 140bp. Crucially, however, the size of the potential CVA flow is unknown and is likely to continue working against sharp steepening.

We do not expect Dutch ALM to be active any time soon. The pension and regulatory system are evolving and there is little appetite to Receive long end rates at these levels and even a feeling that the forced buying of 2008/09 must be avoided. Mercer Consulting even went so far this week as to advise its clients to look for strategic paying opportunities.

Danish buying flows may be seen given that the regulatory Traffic Light tests stress down 100bp in rates and some funds are not as well covered in duration terms (given convexity effects) as previously thought. At the same time, the solvency of the sector is not at critical levels so the level of activity on this theme is expected to be sporadic rather than a persistent buying flow.

EUR 10s30s can flatten further from here but we are not expecting an aggressive move lower like Q4-11.

We continue to prefer forward steepeners such as 10y forward starting EUR 10s30s and EUR 5s10s30s in forwards as Solvency II makes the 20y progressively more important and rates beyond the last liquid point (30y) much more irrelevant for ALM.

EUR 10s30s versus fitted level

-80

-60

-40

-20

0

20

40

60

80

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Actual Fittedbp

Source: RBS

… residual is back to flat now

-20

-15

-10

-5

0

5

10

15

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Errorbp

Source: RBS

European Rates Weekly | 11 May 2012

Page 12

Harvinder Sian

Biagio Lapolla

Sovereign Strategy The volatility and higher spreads that we expect come from two sources. Firstly, the Greece Euro exit risk and secondly, the prospect that the ESM will subordinate SPGB and BTPs will see these markets have more self-fulfilling crisis features.

New Greek elections are likely and the hope is that disaffected voters come back to ‘pro-bailout’ parties. If not, then Euro exit risks rise as Europe can not offer a gift sizeable enough to bribe Greek voters to stay the course. This means, on another hung parliament, that Greek government IOUs could trade as proxy currency as early as July. If this does not galvanise a large pro-euro vote intention into accepting Troika demands the actual exit looms. Opening up the Pandora’s box of exit means deposit risk across the periphery. The future of the euro would then be dictated by the subsequent policy response.

Spain’s new bad bank plan: We assess the news and the risks for SPGBs. The overall headline provisions are more realistic but will still be revised higher in our view which is a risk given that market conditions are not benign. We think that the provisions for small banks means more private to public sector risk transfer and this will also be necessary to make the bad bank plan work. Ultimately, we do not think this plan is enough around the crisis for SPGBs.

Trading plan update There is little new in the tactical game plan as we are maximum long Bunds and short periphery. If anything, we would want to raise sizes on the periphery shorts into the likely Greek election as exit risk is deemed higher than the market thinks. Moreover, we continue to think the ESM is a crisis accelerator.

As such, we still think our risk and trading calendar timing motivates moving from tactical risk to structural stress trades. What is the biggest near term positive? If this weekend’s German NRW election brings a federal government containing the SPD closer.

We remain in full size risk in BTP 2s10s flattener using BTP 2.25% Nov-13 and 5% Mar-22s, with a target of 150 bp initially.

Stay outright short SPGB 3.15% Jan16s. The initial target was 4.50% and then 5.0%. We are approaching our anticipated summer risk-off moves so target now 7%+.

Stay long DBR2 01/22 versus FRTR3 04/22 (DV01 weighted) from 135 bp to target 200 bp initially and place stop below 100 bp.

Short Italy versus Spain in 2026 paper. The fate of Italy and Spain is unlikely to be separated as far as the ESM is concerned and so current spreads at this point of the curve look attractive.

Remain in Bund ASW widening box versus Bobl;

Remain in Dutch 5s10s steepening versus France;

Remain in short DSL versus RFGB in 2028 bonds.

We are also long German 5y CDS protection from our Year Ahead publication and keep the trade. The long Bunds view is driven by a flow argument but that does not mean Germany is impervious to the crisis. The heatmaps of cross-market bond spreads and EGB slope spreads presented below show some potential interesting trades.

European Rates Weekly | 11 May 2012

Page 13

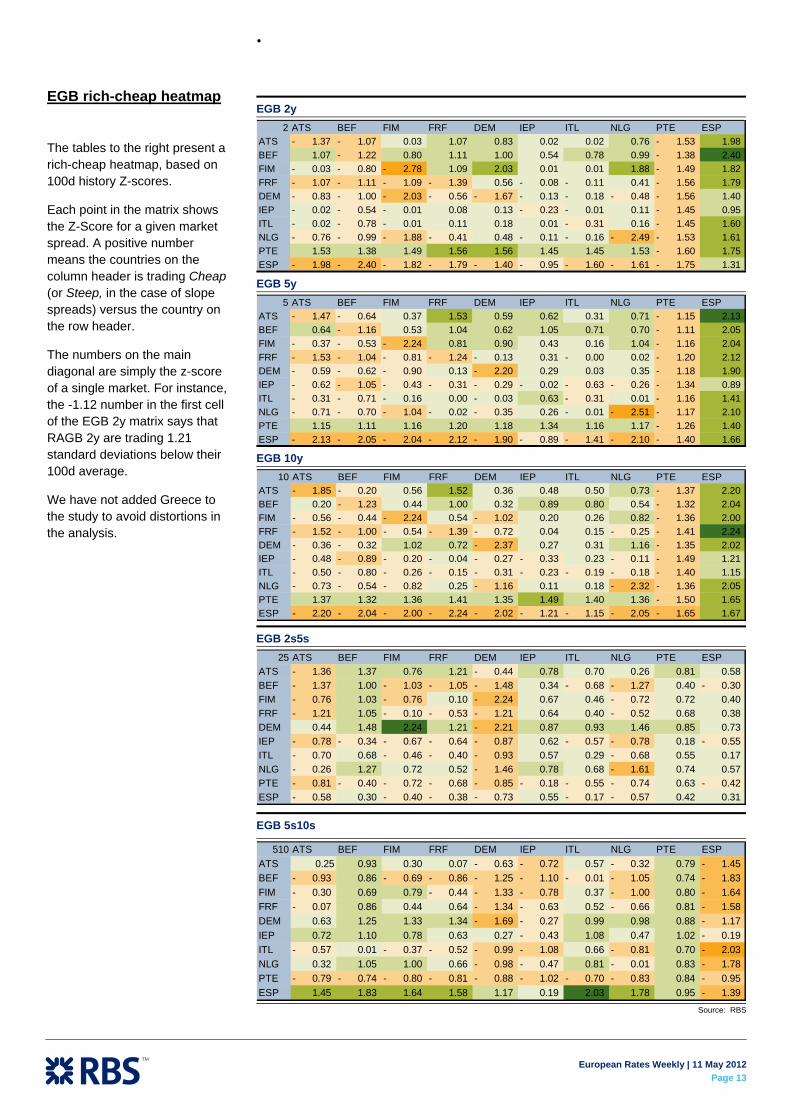

EGB rich-cheap heatmap

The tables to the right present a rich-cheap heatmap, based on 100d history Z-scores.

Each point in the matrix shows the Z-Score for a given market spread. A positive number means the countries on the column header is trading Cheap (or Steep, in the case of slope spreads) versus the country on the row header.

The numbers on the main diagonal are simply the z-score of a single market. For instance, the -1.12 number in the first cell of the EGB 2y matrix says that RAGB 2y are trading 1.21 standard deviations below their 100d average.

We have not added Greece to the study to avoid distortions in the analysis.

EGB 2y 2 ATS BEF FIM FRF DEM IEP ITL NLG PTE ESP

ATS 1.37- 1.07- 0.03 1.07 0.83 0.02 0.02 0.76 1.53- 1.98 BEF 1.07 1.22- 0.80 1.11 1.00 0.54 0.78 0.99 1.38- 2.40 FIM 0.03- 0.80- 2.78- 1.09 2.03 0.01 0.01 1.88 1.49- 1.82 FRF 1.07- 1.11- 1.09- 1.39- 0.56 0.08- 0.11- 0.41 1.56- 1.79 DEM 0.83- 1.00- 2.03- 0.56- 1.67- 0.13- 0.18- 0.48- 1.56- 1.40 IEP 0.02- 0.54- 0.01- 0.08 0.13 0.23- 0.01- 0.11 1.45- 0.95 ITL 0.02- 0.78- 0.01- 0.11 0.18 0.01 0.31- 0.16 1.45- 1.60 NLG 0.76- 0.99- 1.88- 0.41- 0.48 0.11- 0.16- 2.49- 1.53- 1.61 PTE 1.53 1.38 1.49 1.56 1.56 1.45 1.45 1.53 1.60- 1.75 ESP 1.98- 2.40- 1.82- 1.79- 1.40- 0.95- 1.60- 1.61- 1.75- 1.31

EGB 5y 5 ATS BEF FIM FRF DEM IEP ITL NLG PTE ESP

ATS 1.47- 0.64- 0.37 1.53 0.59 0.62 0.31 0.71 1.15- 2.13 BEF 0.64 1.16- 0.53 1.04 0.62 1.05 0.71 0.70 1.11- 2.05 FIM 0.37- 0.53- 2.24- 0.81 0.90 0.43 0.16 1.04 1.16- 2.04 FRF 1.53- 1.04- 0.81- 1.24- 0.13- 0.31 0.00- 0.02 1.20- 2.12 DEM 0.59- 0.62- 0.90- 0.13 2.20- 0.29 0.03 0.35 1.18- 1.90 IEP 0.62- 1.05- 0.43- 0.31- 0.29- 0.02- 0.63- 0.26- 1.34- 0.89 ITL 0.31- 0.71- 0.16- 0.00 0.03- 0.63 0.31- 0.01 1.16- 1.41 NLG 0.71- 0.70- 1.04- 0.02- 0.35- 0.26 0.01- 2.51- 1.17- 2.10 PTE 1.15 1.11 1.16 1.20 1.18 1.34 1.16 1.17 1.26- 1.40 ESP 2.13- 2.05- 2.04- 2.12- 1.90- 0.89- 1.41- 2.10- 1.40- 1.66

EGB 10y 10 ATS BEF FIM FRF DEM IEP ITL NLG PTE ESP

ATS 1.85- 0.20- 0.56 1.52 0.36 0.48 0.50 0.73 1.37- 2.20 BEF 0.20 1.23- 0.44 1.00 0.32 0.89 0.80 0.54 1.32- 2.04 FIM 0.56- 0.44- 2.24- 0.54 1.02- 0.20 0.26 0.82 1.36- 2.00 FRF 1.52- 1.00- 0.54- 1.39- 0.72- 0.04 0.15 0.25- 1.41- 2.24 DEM 0.36- 0.32- 1.02 0.72 2.37- 0.27 0.31 1.16 1.35- 2.02 IEP 0.48- 0.89- 0.20- 0.04- 0.27- 0.33- 0.23 0.11- 1.49- 1.21 ITL 0.50- 0.80- 0.26- 0.15- 0.31- 0.23- 0.19- 0.18- 1.40- 1.15 NLG 0.73- 0.54- 0.82- 0.25 1.16- 0.11 0.18 2.32- 1.36- 2.05 PTE 1.37 1.32 1.36 1.41 1.35 1.49 1.40 1.36 1.50- 1.65 ESP 2.20- 2.04- 2.00- 2.24- 2.02- 1.21- 1.15- 2.05- 1.65- 1.67

EGB 2s5s 25 ATS BEF FIM FRF DEM IEP ITL NLG PTE ESP

ATS 1.36- 1.37 0.76 1.21 0.44- 0.78 0.70 0.26 0.81 0.58 BEF 1.37- 1.00 1.03- 1.05- 1.48- 0.34 0.68- 1.27- 0.40 0.30- FIM 0.76- 1.03 0.76- 0.10 2.24- 0.67 0.46 0.72- 0.72 0.40 FRF 1.21- 1.05 0.10- 0.53- 1.21- 0.64 0.40 0.52- 0.68 0.38 DEM 0.44 1.48 2.24 1.21 2.21- 0.87 0.93 1.46 0.85 0.73 IEP 0.78- 0.34- 0.67- 0.64- 0.87- 0.62 0.57- 0.78- 0.18 0.55- ITL 0.70- 0.68 0.46- 0.40- 0.93- 0.57 0.29 0.68- 0.55 0.17 NLG 0.26- 1.27 0.72 0.52 1.46- 0.78 0.68 1.61- 0.74 0.57 PTE 0.81- 0.40- 0.72- 0.68- 0.85- 0.18- 0.55- 0.74- 0.63 0.42- ESP 0.58- 0.30 0.40- 0.38- 0.73- 0.55 0.17- 0.57- 0.42 0.31

EGB 5s10s

510 ATS BEF FIM FRF DEM IEP ITL NLG PTE ESPATS 0.25 0.93 0.30 0.07 0.63- 0.72- 0.57 0.32- 0.79 1.45- BEF 0.93- 0.86 0.69- 0.86- 1.25- 1.10- 0.01- 1.05- 0.74 1.83- FIM 0.30- 0.69 0.79 0.44- 1.33- 0.78- 0.37 1.00- 0.80 1.64- FRF 0.07- 0.86 0.44 0.64 1.34- 0.63- 0.52 0.66- 0.81 1.58- DEM 0.63 1.25 1.33 1.34 1.69- 0.27- 0.99 0.98 0.88 1.17- IEP 0.72 1.10 0.78 0.63 0.27 0.43- 1.08 0.47 1.02 0.19- ITL 0.57- 0.01 0.37- 0.52- 0.99- 1.08- 0.66 0.81- 0.70 2.03- NLG 0.32 1.05 1.00 0.66 0.98- 0.47- 0.81 0.01- 0.83 1.78- PTE 0.79- 0.74- 0.80- 0.81- 0.88- 1.02- 0.70- 0.83- 0.84 0.95- ESP 1.45 1.83 1.64 1.58 1.17 0.19 2.03 1.78 0.95 1.39-

Source: RBS

European Rates Weekly | 11 May 2012

Page 14

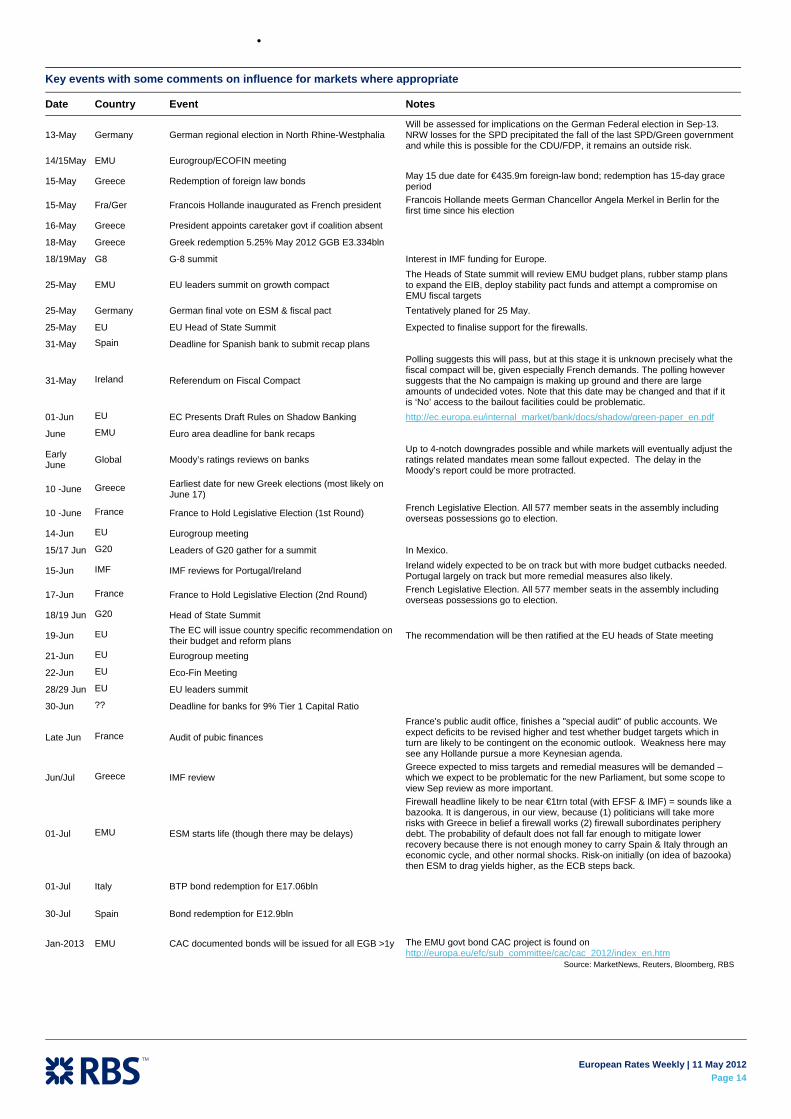

Key events with some comments on influence for markets where appropriate

Date Country Event Notes

13-May Germany German regional election in North Rhine-Westphalia Will be assessed for implications on the German Federal election in Sep-13. NRW losses for the SPD precipitated the fall of the last SPD/Green government and while this is possible for the CDU/FDP, it remains an outside risk.

14/15May EMU Eurogroup/ECOFIN meeting

15-May Greece Redemption of foreign law bonds May 15 due date for €435.9m foreign-law bond; redemption has 15-day grace period

15-May Fra/Ger Francois Hollande inaugurated as French president Francois Hollande meets German Chancellor Angela Merkel in Berlin for the first time since his election

16-May Greece President appoints caretaker govt if coalition absent

18-May Greece Greek redemption 5.25% May 2012 GGB E3.334bln

18/19May G8 G-8 summit Interest in IMF funding for Europe.

25-May EMU EU leaders summit on growth compact The Heads of State summit will review EMU budget plans, rubber stamp plans to expand the EIB, deploy stability pact funds and attempt a compromise on EMU fiscal targets

25-May Germany German final vote on ESM & fiscal pact Tentatively planed for 25 May.

25-May EU EU Head of State Summit Expected to finalise support for the firewalls.

31-May Spain Deadline for Spanish bank to submit recap plans

31-May Ireland Referendum on Fiscal Compact

Polling suggests this will pass, but at this stage it is unknown precisely what the fiscal compact will be, given especially French demands. The polling however suggests that the No campaign is making up ground and there are large amounts of undecided votes. Note that this date may be changed and that if it is ‘No’ access to the bailout facilities could be problematic.

01-Jun EU EC Presents Draft Rules on Shadow Banking http://ec.europa.eu/internal_market/bank/docs/shadow/green-paper_en.pdf

June EMU Euro area deadline for bank recaps

Early June Global Moody’s ratings reviews on banks

Up to 4-notch downgrades possible and while markets will eventually adjust the ratings related mandates mean some fallout expected. The delay in the Moody’s report could be more protracted.

10 -June Greece Earliest date for new Greek elections (most likely on June 17)

10 -June France France to Hold Legislative Election (1st Round) French Legislative Election. All 577 member seats in the assembly including overseas possessions go to election.

14-Jun EU Eurogroup meeting

15/17 Jun G20 Leaders of G20 gather for a summit In Mexico.

15-Jun IMF IMF reviews for Portugal/Ireland Ireland widely expected to be on track but with more budget cutbacks needed. Portugal largely on track but more remedial measures also likely.

17-Jun France France to Hold Legislative Election (2nd Round) French Legislative Election. All 577 member seats in the assembly including overseas possessions go to election.

18/19 Jun G20 Head of State Summit

19-Jun EU The EC will issue country specific recommendation on their budget and reform plans The recommendation will be then ratified at the EU heads of State meeting

21-Jun EU Eurogroup meeting

22-Jun EU Eco-Fin Meeting

28/29 Jun EU EU leaders summit

30-Jun ?? Deadline for banks for 9% Tier 1 Capital Ratio

Late Jun France Audit of pubic finances

France's public audit office, finishes a "special audit" of public accounts. We expect deficits to be revised higher and test whether budget targets which in turn are likely to be contingent on the economic outlook. Weakness here may see any Hollande pursue a more Keynesian agenda.

Jun/Jul Greece IMF review Greece expected to miss targets and remedial measures will be demanded – which we expect to be problematic for the new Parliament, but some scope to view Sep review as more important.

01-Jul EMU ESM starts life (though there may be delays)

Firewall headline likely to be near €1trn total (with EFSF & IMF) = sounds like a bazooka. It is dangerous, in our view, because (1) politicians will take more risks with Greece in belief a firewall works (2) firewall subordinates periphery debt. The probability of default does not fall far enough to mitigate lower recovery because there is not enough money to carry Spain & Italy through an economic cycle, and other normal shocks. Risk-on initially (on idea of bazooka) then ESM to drag yields higher, as the ECB steps back.

01-Jul Italy BTP bond redemption for E17.06bln

30-Jul Spain Bond redemption for E12.9bln

Jan-2013 EMU CAC documented bonds will be issued for all EGB >1y The EMU govt bond CAC project is found on http://europa.eu/efc/sub_committee/cac/cac_2012/index_en.htm

Source: MarketNews, Reuters, Bloomberg, RBS

European Rates Weekly | 11 May 2012

Page 15

Paths towards a Greek end-game New Greek elections are likely. The hope is that disaffected voters come back to ‘pro-bailout’ parties. If not, Euro exit risks rise. We do not think Europe can offer a gift sizeable enough to bribe Greek voters to stay the course. This means, on another hung parliament, that Greek government IOUs could trade as proxy currency as early as July. This may then galvanise a large pro-euro vote intention into accepting Troika demands. If not, exit looms. Opening up the Pandora’s box of exit means deposit risk across the periphery. The future of the euro would then be dictated by the subsequent policy response.

New Greek elections will be a referendum on the Euro

The Greek political establishment is trying to cobble together a coalition and while the leading parties, New Democracy and SYRIZA, have attempted and failed, there is a residual hope that PASOK may be successful. Its leader, Evangelos Venizelos, is courting the Democratic Left leader Fotis Kouvelis – though this also includes the negotiation of a gradual ‘disengagement’ from bailout austerity measures.

No party in Greece has a mandate to rewrite the bailout austerity measures and the comments from EU officials suggest there is little scope for large changes – a point we made in Greece: updated thoughts (7 May) when we argued that it is hard to see anything other than token efforts to relieve some of the austerity pain for Greece.

In terms of commentary: the rhetoric from core Europe, there is little confusion over what Greece needs to do:

ECB’s Jörg Asmussen: “Greece needs to be aware that there is no alternative to the agreed reform programme if it wants to remain a member of the Eurozone.”

German Foreign Minister Westerwelle: “If Greece ends the reform process it has undertaken, then I can’t see that the respective tranches [of aid] can be paid out.”

German Chancellor Merkel: “It is of utmost importance that the programs that we agreed on with Greece continue to be implemented. The process is a difficult one, but despite that it should go on.”

German Finance Minister Schäuble: “If Greece does not decide to stay in the Eurozone we can't force them to stay in it.”

Former SPD Finance Minister Steinbrück: “If I had political responsibility, I would want to prepare myself for a plan B in which the Eurozone is no longer necessarily composed of 17 members.”

(Bloomberg)

European Rates Weekly | 11 May 2012

Page 16

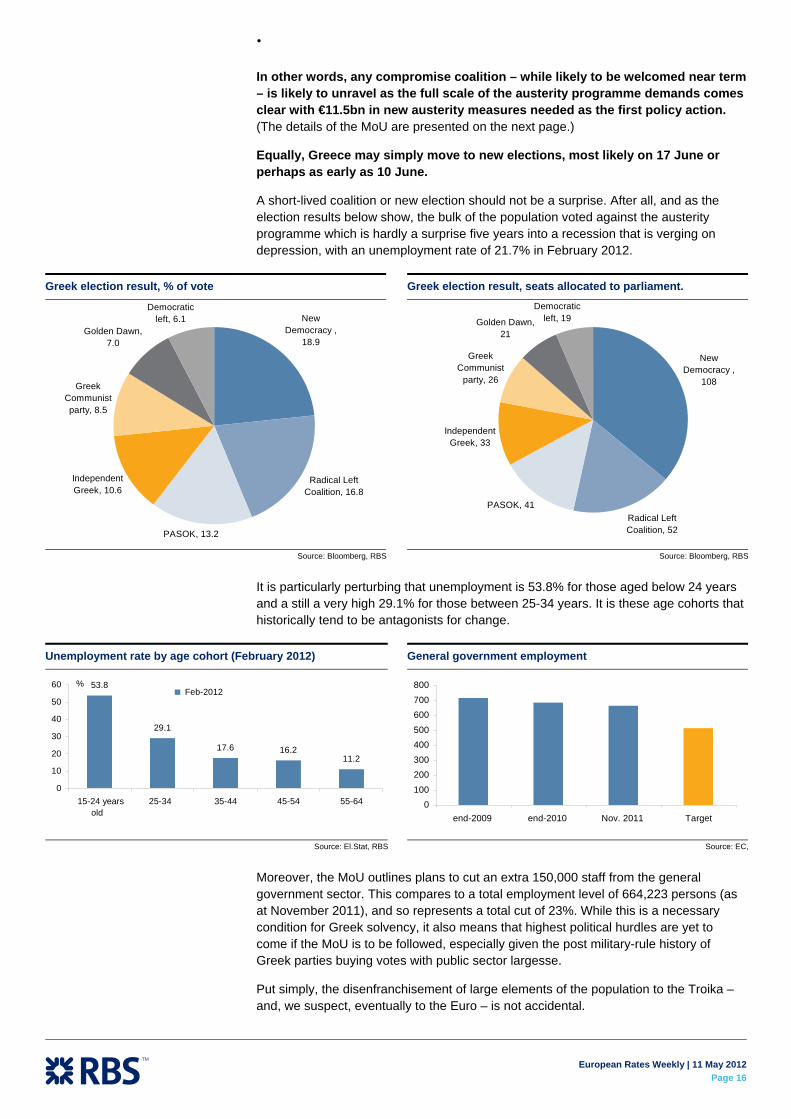

In other words, any compromise coalition – while likely to be welcomed near term – is likely to unravel as the full scale of the austerity programme demands comes clear with €11.5bn in new austerity measures needed as the first policy action. (The details of the MoU are presented on the next page.)

Equally, Greece may simply move to new elections, most likely on 17 June or perhaps as early as 10 June.

A short-lived coalition or new election should not be a surprise. After all, and as the election results below show, the bulk of the population voted against the austerity programme which is hardly a surprise five years into a recession that is verging on depression, with an unemployment rate of 21.7% in February 2012.

It is particularly perturbing that unemployment is 53.8% for those aged below 24 years and a still a very high 29.1% for those between 25-34 years. It is these age cohorts that historically tend to be antagonists for change.

Moreover, the MoU outlines plans to cut an extra 150,000 staff from the general government sector. This compares to a total employment level of 664,223 persons (as at November 2011), and so represents a total cut of 23%. While this is a necessary condition for Greek solvency, it also means that highest political hurdles are yet to come if the MoU is to be followed, especially given the post military-rule history of Greek parties buying votes with public sector largesse.

Put simply, the disenfranchisement of large elements of the population to the Troika – and, we suspect, eventually to the Euro – is not accidental.

Greek election result, % of vote

New Democracy ,

18.9

Radical Left Coalition, 16.8

PASOK, 13.2

Independent Greek, 10.6

Greek Communist party, 8.5

Golden Dawn, 7.0

Democratic left, 6.1

Source: Bloomberg, RBS

Greek election result, seats allocated to parliament.

New Democracy ,

108

Radical Left Coalition, 52

PASOK, 41

Independent Greek, 33

Greek Communist

party, 26

Golden Dawn, 21

Democratic left, 19

Source: Bloomberg, RBS

Unemployment rate by age cohort (February 2012)

53.8

29.1

17.6 16.211.2

0

10

20

30

40

50

60

15-24 yearsold

25-34 35-44 45-54 55-64

Feb-2012 %

Source: El.Stat, RBS

General government employment

0100200300400500600700800

end-2009 end-2010 Nov. 2011 Target

Source: EC,

European Rates Weekly | 11 May 2012

Page 17

Prior to first disbursement of the new programme, the government is to adopt the following measures, according to the latest MoU: • Reduction in pharmaceutical expenditure by at least €1.076bn in 2012. • Reduction in overtime pay for doctors in hospitals by at least €50m. • Reduction in the procurement of military material by €300m (cash and deliveries). • Reduction by 10% in the remuneration of elected and related staff at the local level and reduction in the number of deputy mayors and associated staff in 2013 with the aim of saving at least €9m in 2012 and €28m in 2013 and onwards. • Reduction in the central government's operational expenditure and election-related spending by at least €370m (compared to the 2012 budget), of which at least €100m is to come from military-related operational expenditure, and at least €70m from electoral spending. • Reduction in operational expenditure by local government with the aim of saving at least €50m. • Frontloading cuts in subsidies to residents in remote areas, and cuts in grants to several entities supervised by the several ministries, with the aim of reducing expenditure in 2012 by at least €190m. • Reduction in the public investment budget of €400m. • Changes in supplementary pension funds and pension funds with high average pensions or which receive high subsidies from the budget and cuts in other high pensions, with the aim of saving at least €450m (net after taking into account the impact on taxes and social contributions). • Cuts in family allowances for high-income households, with the aim of saving €43m. Prior to the disbursement, the government also is to adopt the following pending acts: • Ministerial Decisions for the implementation of the business tax (minimum levy on the self-employed) provided for in Article 31 of Law 3986/2011; • Ministerial Decisions to complete the full implementation of the new wage grid in all the pertinent entities, and legislation on the modalities for the recovery of wages paid in excess from November 2011 on. By end-June 2012, the government is to legislate an average reduction by 12% in the so-called 'special wages' of the public sector, to which the new wage grid does not apply. This will apply from 1 July 2012 and deliver savings of at least €205m (net after taking into account the impact on taxes and social contributions).

Source: IMF, EC

Exit threat: the only bargaining chip We had expected a mixed election result and one that would begin to test markets on the idea of the Greek EMU exit risk. The rationale for this view (which alongside the activation of the ESM) is seen as a key structural story behind wider EGB spreads this summer). On Greece the situation is clear.

The threat of another default from core EMU to Greece makes little sense as the bulk of loans to Greece are now in official hands and the PSI bonds are pari passu.

Greece would embrace a default that means less pain and reform – but markets would question just how it can remain in the Euro long term given that competitiveness and governance issues have not been addressed.

Given the weak bargaining position of core EMU to Greece, in the likely event of Troika non-compliance, the only feasible threat that may work in motivating real reform is the threat of exit from the Euro. Core Europe will have noted that 80% of the population wants to remain in the Euro but there is an equally high portion of the population that is against the austerity programme.

The exit threat is credible, a priori

We believe if there is a time in which core EMU may play the Greek exit card, it is when the ECB is backstopping banks and the ESM/EFSF/IMF firewall is in place. The latter is intended from July 2012. Given this, politicians may reason that contagion costs will be limited or at the least would be more inclined to take that gamble.

Second, the ability of Greece to survive in the Euro, even on a larger debt relief, is limited in the absence of economic restructuring.

Third, politicians have hinted at this threat before and the distrust is high enough to mean Greek bondholders get paid from an escrow account separate to other Greek bailout money.

The main argument against core EMU exercising the exit threat is the contagion it poses to other periphery countries, something that we explore below. Note that this does not prevent the a priori threat of exit.

The ex post action of core EMU will surely depend on the scale of the contagion to the rest of Europe, but there will be no easy choices here for the political elite as caving in to the fear of a Greek exit by offering Greece fiscal gifts will lead to huge moral hazard and a race to the bottom. If this were to be the case, then we would expect to hear about new bailout discussions which would involve more money for Greece.

European Rates Weekly | 11 May 2012

Page 18

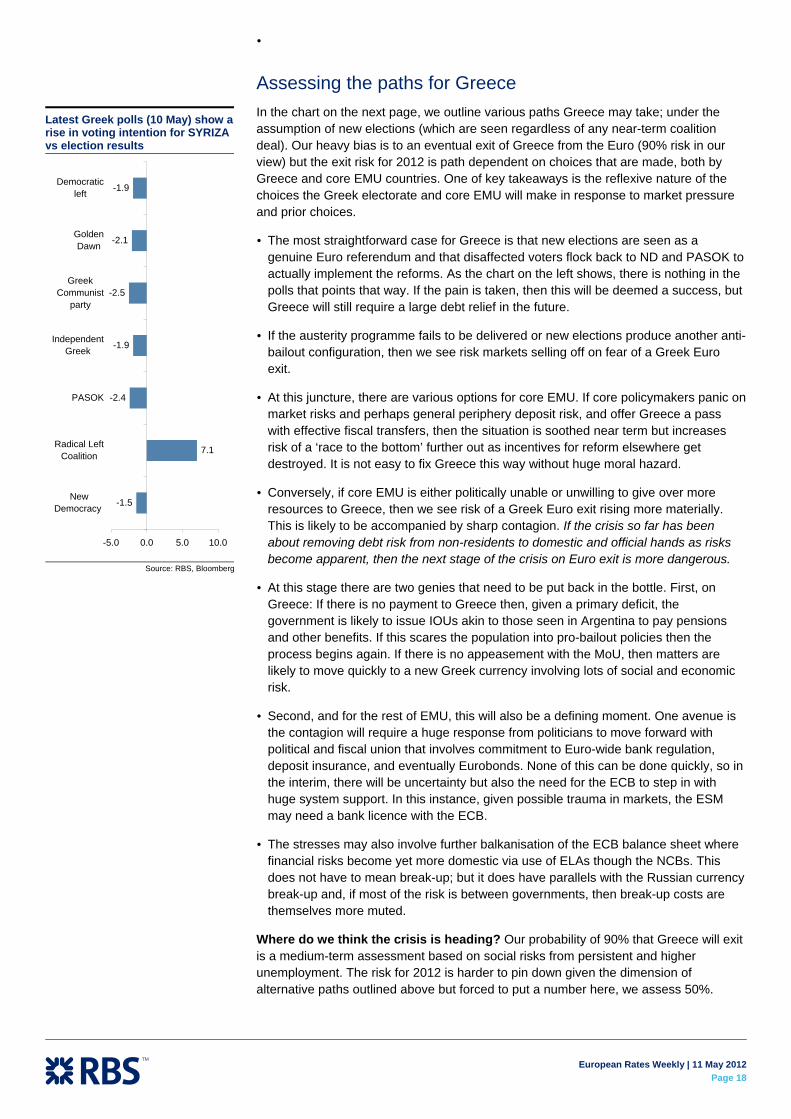

Assessing the paths for Greece In the chart on the next page, we outline various paths Greece may take; under the assumption of new elections (which are seen regardless of any near-term coalition deal). Our heavy bias is to an eventual exit of Greece from the Euro (90% risk in our view) but the exit risk for 2012 is path dependent on choices that are made, both by Greece and core EMU countries. One of key takeaways is the reflexive nature of the choices the Greek electorate and core EMU will make in response to market pressure and prior choices.

The most straightforward case for Greece is that new elections are seen as a genuine Euro referendum and that disaffected voters flock back to ND and PASOK to actually implement the reforms. As the chart on the left shows, there is nothing in the polls that points that way. If the pain is taken, then this will be deemed a success, but Greece will still require a large debt relief in the future.

If the austerity programme fails to be delivered or new elections produce another anti-bailout configuration, then we see risk markets selling off on fear of a Greek Euro exit.

At this juncture, there are various options for core EMU. If core policymakers panic on market risks and perhaps general periphery deposit risk, and offer Greece a pass with effective fiscal transfers, then the situation is soothed near term but increases risk of a ‘race to the bottom’ further out as incentives for reform elsewhere get destroyed. It is not easy to fix Greece this way without huge moral hazard.

Conversely, if core EMU is either politically unable or unwilling to give over more resources to Greece, then we see risk of a Greek Euro exit rising more materially. This is likely to be accompanied by sharp contagion. If the crisis so far has been about removing debt risk from non-residents to domestic and official hands as risks become apparent, then the next stage of the crisis on Euro exit is more dangerous.

At this stage there are two genies that need to be put back in the bottle. First, on Greece: If there is no payment to Greece then, given a primary deficit, the government is likely to issue IOUs akin to those seen in Argentina to pay pensions and other benefits. If this scares the population into pro-bailout policies then the process begins again. If there is no appeasement with the MoU, then matters are likely to move quickly to a new Greek currency involving lots of social and economic risk.

Second, and for the rest of EMU, this will also be a defining moment. One avenue is the contagion will require a huge response from politicians to move forward with political and fiscal union that involves commitment to Euro-wide bank regulation, deposit insurance, and eventually Eurobonds. None of this can be done quickly, so in the interim, there will be uncertainty but also the need for the ECB to step in with huge system support. In this instance, given possible trauma in markets, the ESM may need a bank licence with the ECB.

The stresses may also involve further balkanisation of the ECB balance sheet where financial risks become yet more domestic via use of ELAs though the NCBs. This does not have to mean break-up; but it does have parallels with the Russian currency break-up and, if most of the risk is between governments, then break-up costs are themselves more muted.

Where do we think the crisis is heading? Our probability of 90% that Greece will exit is a medium-term assessment based on social risks from persistent and higher unemployment. The risk for 2012 is harder to pin down given the dimension of alternative paths outlined above but forced to put a number here, we assess 50%.

Latest Greek polls (10 May) show a rise in voting intention for SYRIZA vs election results

-1.5

7.1

-2.4

-1.9

-2.5

-2.1

-1.9

-5.0 0.0 5.0 10.0

NewDemocracy

Radical LeftCoalition

PASOK

IndependentGreek

GreekCommunist

party

GoldenDawn

Democraticleft

Source: RBS, Bloomberg

European Rates W

eekly | 11 May 2012Page 19

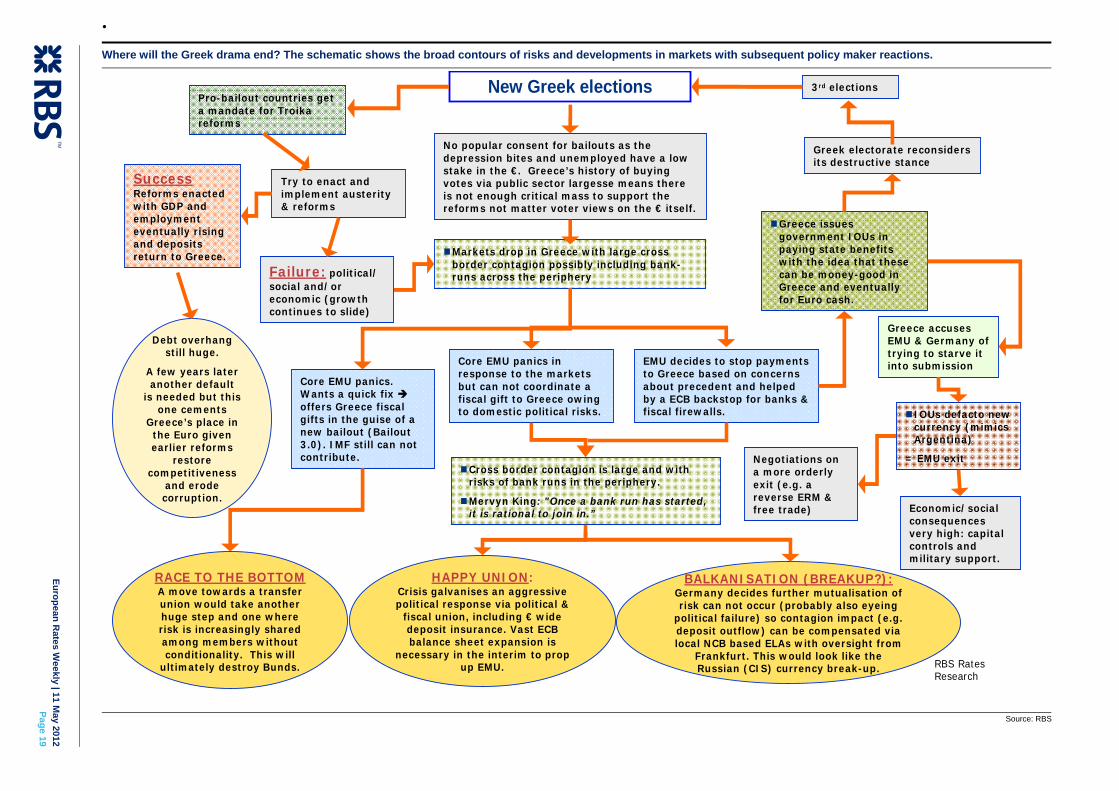

Where will the Greek drama end? The schematic shows the broad contours of risks and developments in markets with subsequent policy maker reactions.

Pro-bailout countries get a mandate for Troika reforms

New Greek elections

Markets drop in Greece with large cross border contagion possibly including bank-runs across the periphery

No popular consent for bailouts as the depression bites and unemployed have a low stake in the €. Greece’s history of buying votes via public sector largesse means there is not enough critical mass to support the reforms not matter voter views on the € itself.

Try to enact and implement austerity & reforms

Failure: political/ social and/or economic (growth continues to slide)

SuccessReforms enacted with GDP and employment eventually rising and deposits return to Greece.

Core EMU panics. Wants a quick fix offers Greece fiscal gifts in the guise of a new bailout (Bailout 3.0). IMF still can not contribute.

3rd elections

Greece accuses EMU & Germany of trying to starve it into submission Core EMU panics in

response to the markets but can not coordinate a fiscal gift to Greece owing to domestic political risks.

EMU decides to stop payments to Greece based on concerns about precedent and helped by a ECB backstop for banks & fiscal firewalls.

Greece issues government IOUs in paying state benefits with the idea that these can be money-good in Greece and eventually for Euro cash.

Greek electorate reconsiders its destructive stance

Cross border contagion is large and with risks of bank runs in the periphery.

Mervyn King: "Once a bank run has started, it is rational to join in.”

RACE TO THE BOTTOMA move towards a transfer union would take another huge step and one where risk is increasingly shared among members without conditionality. This will

ultimately destroy Bunds.

HAPPY UNION:Crisis galvanises an aggressive political response via political &

fiscal union, including € wide deposit insurance. Vast ECB balance sheet expansion is

necessary in the interim to prop up EMU.

BALKANISATION (BREAKUP?):Germany decides further mutualisation of risk can not occur (probably also eyeing

political failure) so contagion impact (e.g. deposit outflow) can be compensated via local NCB based ELAs with oversight from

Frankfurt. This would look like the Russian (CIS) currency break-up.

IOUs defacto new currency (mimics Argentina)

= EMU exit Negotiations on a more orderly exit (e.g. a reverse ERM & free trade) Economic/social

consequences very high: capital controls and military support.

Debt overhang still huge.

A few years later another default

is needed but this one cements

Greece’s place in the Euro given earlier reforms

restore competitiveness

and erode corruption.

RBS Rates Research

Source: RBS

European Rates Weekly | 11 May 2012

Page 20

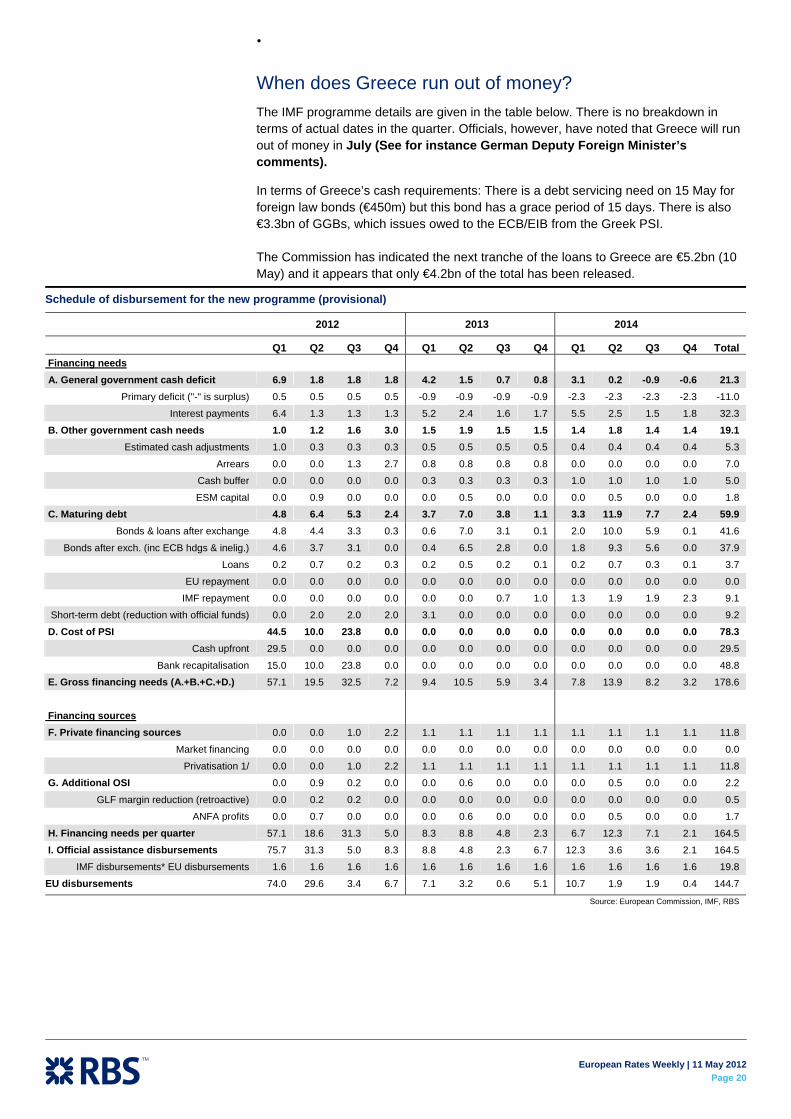

When does Greece run out of money? The IMF programme details are given in the table below. There is no breakdown in terms of actual dates in the quarter. Officials, however, have noted that Greece will run out of money in July (See for instance German Deputy Foreign Minister’s comments).

In terms of Greece’s cash requirements: There is a debt servicing need on 15 May for foreign law bonds (€450m) but this bond has a grace period of 15 days. There is also €3.3bn of GGBs, which issues owed to the ECB/EIB from the Greek PSI.

The Commission has indicated the next tranche of the loans to Greece are €5.2bn (10 May) and it appears that only €4.2bn of the total has been released.

Schedule of disbursement for the new programme (provisional)

2012 2013 2014

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Total Financing needs

A. General government cash deficit 6.9 1.8 1.8 1.8 4.2 1.5 0.7 0.8 3.1 0.2 -0.9 -0.6 21.3 Primary deficit ("-" is surplus) 0.5 0.5 0.5 0.5 -0.9 -0.9 -0.9 -0.9 -2.3 -2.3 -2.3 -2.3 -11.0

Interest payments 6.4 1.3 1.3 1.3 5.2 2.4 1.6 1.7 5.5 2.5 1.5 1.8 32.3

B. Other government cash needs 1.0 1.2 1.6 3.0 1.5 1.9 1.5 1.5 1.4 1.8 1.4 1.4 19.1 Estimated cash adjustments 1.0 0.3 0.3 0.3 0.5 0.5 0.5 0.5 0.4 0.4 0.4 0.4 5.3

Arrears 0.0 0.0 1.3 2.7 0.8 0.8 0.8 0.8 0.0 0.0 0.0 0.0 7.0

Cash buffer 0.0 0.0 0.0 0.0 0.3 0.3 0.3 0.3 1.0 1.0 1.0 1.0 5.0

ESM capital 0.0 0.9 0.0 0.0 0.0 0.5 0.0 0.0 0.0 0.5 0.0 0.0 1.8

C. Maturing debt 4.8 6.4 5.3 2.4 3.7 7.0 3.8 1.1 3.3 11.9 7.7 2.4 59.9 Bonds & loans after exchange 4.8 4.4 3.3 0.3 0.6 7.0 3.1 0.1 2.0 10.0 5.9 0.1 41.6

Bonds after exch. (inc ECB hdgs & inelig.) 4.6 3.7 3.1 0.0 0.4 6.5 2.8 0.0 1.8 9.3 5.6 0.0 37.9

Loans 0.2 0.7 0.2 0.3 0.2 0.5 0.2 0.1 0.2 0.7 0.3 0.1 3.7

EU repayment 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

IMF repayment 0.0 0.0 0.0 0.0 0.0 0.0 0.7 1.0 1.3 1.9 1.9 2.3 9.1

Short-term debt (reduction with official funds) 0.0 2.0 2.0 2.0 3.1 0.0 0.0 0.0 0.0 0.0 0.0 0.0 9.2

D. Cost of PSI 44.5 10.0 23.8 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 78.3 Cash upfront 29.5 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 29.5

Bank recapitalisation 15.0 10.0 23.8 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 48.8

E. Gross financing needs (A.+B.+C.+D.) 57.1 19.5 32.5 7.2 9.4 10.5 5.9 3.4 7.8 13.9 8.2 3.2 178.6

Financing sources

F. Private financing sources 0.0 0.0 1.0 2.2 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 11.8

Market financing 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Privatisation 1/ 0.0 0.0 1.0 2.2 1.1 1.1 1.1 1.1 1.1 1.1 1.1 1.1 11.8

G. Additional OSI 0.0 0.9 0.2 0.0 0.0 0.6 0.0 0.0 0.0 0.5 0.0 0.0 2.2

GLF margin reduction (retroactive) 0.0 0.2 0.2 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.5

ANFA profits 0.0 0.7 0.0 0.0 0.0 0.6 0.0 0.0 0.0 0.5 0.0 0.0 1.7

H. Financing needs per quarter 57.1 18.6 31.3 5.0 8.3 8.8 4.8 2.3 6.7 12.3 7.1 2.1 164.5

I. Official assistance disbursements 75.7 31.3 5.0 8.3 8.8 4.8 2.3 6.7 12.3 3.6 3.6 2.1 164.5

IMF disbursements* EU disbursements 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.6 1.6 19.8

EU disbursements 74.0 29.6 3.4 6.7 7.1 3.2 0.6 5.1 10.7 1.9 1.9 0.4 144.7

Source: European Commission, IMF, RBS

European Rates Weekly | 11 May 2012

Page 21

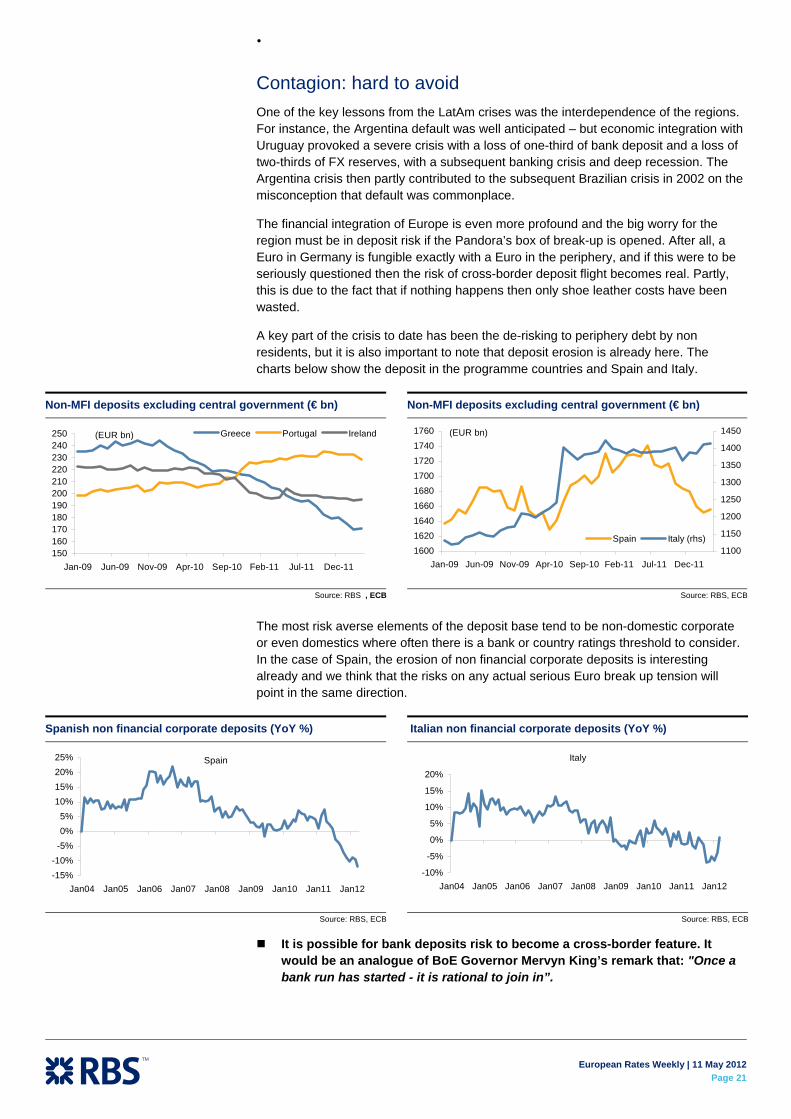

Contagion: hard to avoid One of the key lessons from the LatAm crises was the interdependence of the regions. For instance, the Argentina default was well anticipated – but economic integration with Uruguay provoked a severe crisis with a loss of one-third of bank deposit and a loss of two-thirds of FX reserves, with a subsequent banking crisis and deep recession. The Argentina crisis then partly contributed to the subsequent Brazilian crisis in 2002 on the misconception that default was commonplace.

The financial integration of Europe is even more profound and the big worry for the region must be in deposit risk if the Pandora’s box of break-up is opened. After all, a Euro in Germany is fungible exactly with a Euro in the periphery, and if this were to be seriously questioned then the risk of cross-border deposit flight becomes real. Partly, this is due to the fact that if nothing happens then only shoe leather costs have been wasted.

A key part of the crisis to date has been the de-risking to periphery debt by non residents, but it is also important to note that deposit erosion is already here. The charts below show the deposit in the programme countries and Spain and Italy.

The most risk averse elements of the deposit base tend to be non-domestic corporate or even domestics where often there is a bank or country ratings threshold to consider. In the case of Spain, the erosion of non financial corporate deposits is interesting already and we think that the risks on any actual serious Euro break up tension will point in the same direction.

It is possible for bank deposits risk to become a cross-border feature. It would be an analogue of BoE Governor Mervyn King’s remark that: "Once a bank run has started - it is rational to join in”.

Non-MFI deposits excluding central government (€ bn)

150160170180190200210220230240250

Jan-09 Jun-09 Nov-09 Apr-10 Sep-10 Feb-11 Jul-11 Dec-11

Greece Portugal Ireland(EUR bn)

Source: RBS , ECB

Non-MFI deposits excluding central government (€ bn)

160016201640

1660168017001720

17401760

Jan-09 Jun-09 Nov-09 Apr-10 Sep-10 Feb-11 Jul-11 Dec-111100

1150

1200

1250

1300

1350

1400

1450

Spain Italy (rhs)

(EUR bn)

Source: RBS, ECB

Spanish non financial corporate deposits (YoY %)

Spain

-15%-10%

-5%0%5%

10%15%20%25%

Jan04 Jan05 Jan06 Jan07 Jan08 Jan09 Jan10 Jan11 Jan12

Source: RBS, ECB

Italian non financial corporate deposits (YoY %)

Italy

-10%

-5%

0%

5%

10%

15%

20%

Jan04 Jan05 Jan06 Jan07 Jan08 Jan09 Jan10 Jan11 Jan12

Source: RBS, ECB

European Rates Weekly | 11 May 2012

Page 22

Summing up We have been expecting Greek exit risk to rise. The austerity push is getting to a tipping point for the social and electoral fabric of the country.

We are convinced that any new election will clearly be seen as a referendum on the Euro as core EMU countries will have no other way to impress upon Greece the need to stay the course.

This may work – but there is little basis to make that judgement at present.

If the anti-austerity vote remains strong – and in the absence of large fiscal gifts to Greece that 1) may not be politically feasible to deliver and 2) would encourage huge moral hazard – then the risk of a Greek Euro exit in 2012 rises notably.

A failure to make the bailout payments could see IOUs trade as proxy Greek currency as early as July. If these IOUs remain, because the electorate still is not willing to observe the reforms, then the exit will be cemented.

Just how the rest of Europe reacts here will dictate no less than the future of the Euro. The ECB will have a role to play in propping up the system to a far larger degree than now, but it will be political decisions on integration or balkanisation that should be most closely watched.

In terms of trades – and given that the Greek exit risk has been part of our trading plan – we stick to the themes and risk outlined in the last Rates Weekly and indeed much before that. Namely, remain limit long 10yr bunds (target 1.25% and perhaps below 1%), own 'lower for longer' (e.g. 1y3f) but also consider that the sweet spot can be 10yrs, while butterfly trades such as 5s10s30s in forward space are also excellent carry and performance vehicles. We expect the periphery crisis to take a turn for the worse and remain short Spain outright and France versus Bunds, with BTP flatteners and some other macro/RV switch ideas.

European Rates Weekly | 11 May 2012

Page 23

Appendix: A stylised history of currency break-ups for EMU investors Currency crises and currency break-ups are rare but not without precedent. In fact, there have been over 100 currency break-ups and exits from currency unions over the last hundred years (Checking Out: Exits from currency unions, A.K. Rose, 2007). While most of these events are not directly comparable with the EMU, they do provide a useful guide. The scope of this section is not to conduct an in-depth analysis into previous episodes of currency break-ups, but a glimpse into past experiences that might present useful similarities with the Euro crisis.

1. Argentina: from IOUs to Lecop burgers Argentina’s experience is one of the most interesting cases from which to draw comparisons with the Euro crisis. In fact, Argentina’s crisis unfolded around similar dimensions to those seen in the EMU: a partly self-inflicted economic grief linked to an artificially overvalued currency and exacerbated growing debt strains (especially external debt) that eventually filtered into the banking system.

Following a series of shocks that hit the country (starting with the 1999 recession), Argentina found itself trapped. Its choices: break the dollar currency board arrangement would be at the cost of bankrupting many domestic institutions (including the government) or muddle through a deflationary backdrop which could ultimately lead to an identical outcome.

In November 2001, Argentina converted domestically held international bonds into loans. Although the loans were issued under Argentine law and carried a lower interest rate, they were backed, at least in theory, by revenues from a financial transactions tax.

By end-2001, the economy and public finances were in deep crisis. In December, activity collapsed, with industrial production falling by 18% (year-on-year), construction by 36% and imports by more than 50%. Tax revenues plummeted 17% (year-on-year) in the final quarter of 2001 (in December, tax collections fell by almost 30% year-on year), and despite across-the-board spending cuts, the federal government ran an overall deficit of 4.5% of GDP in 2001 against a (revised) programme target of 2.5%.

Provincial finances also deteriorated. Out of Arg$17bn of federal transfers to the provinces, about Arg$1bn were in the form of federal guarantees of provincial T-bills (Lecops).

As the crisis progressed, provincial governments issued about Arg$1.6bn in bills (quasi-monies) to pay wages and suppliers – in the liquidity crunch – and this ‘money’ was also acceptable by the federal government in lieu of tax payments. The movement towards regional money is neatly captured by the fact that McDonald’s started selling Lecop burgers.

An example of Argentina’s Lecop (Letras de Cancelacion de Obligaciones Provinciales)

Source: Google Images

European Rates Weekly | 11 May 2012

Page 24

On 3 January 2002, President Duhalde – the fifth president in three weeks – confirmed the debt moratorium (as well as the intention to negotiate with private creditors) and announced the end of the convertibility regime. Three days later, Congress effectively replaced the convertibility regime with a dual exchange-rate system based on an official exchange rate of Arg$1.40 per US dollar for the public sector and most trade-related transactions (except luxury imports); all other transactions would take place at prevailing market rates.

At the same time, the monthly deposit withdrawal limit was raised to 1,500 pesos (previous limit: Arg$1,000), coupled with a freezing of term-deposits. US dollar deposits would remain frozen until at least 2003. To dampen inflation pressure, prices of privatised utilities (gas, electricity, telephones and water) were frozen indefinitely. Congress approved an emergency law that severely curtailed creditors’ rights.

USSR to the CIS

Following the break up of the Soviet Union and despite the independence of many post-Soviet states, the money supply was still officially controlled by the new Central Bank of Russia (CBR), which took over the role of the old Soviet central bank (Gosbank). Gosbank branches in the other post-USSR countries (now the Commonwealth of Independent States) became 14 independent central banks.

The old Soviet system was based on a dual monetary circuit: enterprises could convert Rubles in the bank into cash only for specified purposes – chiefly the payment of wages, which were paid in cash. All inter-enterprise transactions were required to be in non-cash Rubles to facilitate central planning and control. This dual circuit continued in the post-soviet Ruble zone. The implication was that while the CBR had monopoly on cash Rubles, the other central banks could and did create non-cash Rubles. This institutional structure not only led to a competition for seigniorage among post-Soviet states but the non-Russian states also found that they could finance their trade deficits with Russia by issuing credit to local commercial banks, which could extend it to local importers, with the resulting Ruble credit balances ending up in the accounts of the CBR.

The obvious flaw in this system was that credit creation was feasibly unlimited and created a free-rider problem, which eventually created much higher inflation that progressively saw the independent states abandon this monetary arrangement. The parallel with the Euro area is simply that if NCBs are allowed to extend local collateral rules and perhaps some form of ELA (to prop up local banking systems), then the free-rider/inflationary risk will also be apparent.

The CBR in July 1993 announced, without warning, that all Ruble notes printed between 1961 and 1992 would no longer be legal tender, leading to a crisis of Russians’ confidence in their monetary system. The behaviour of the second director of the CBR, Viktor Gerashchenko, led the Harvard economist Jeffrey Sachs to call him, famously, “the world’s worst central banker.” The Ruble fared little better outside Russia. The currency was subject to severe exchange-rate instability, and to repeated speculative attacks. Several post-Soviet governments rejected the “occupation Ruble” in early 1992 and introduced their own national currencies.

Czechoslovakia

During late 1992 and throughout January 1993, many Slovak firms and individuals transferred funds to Czech commercial banks in expectation of Slovak devaluation shortly after the political split. This was reflected in the apparent undervaluation of the Czech currency as the Czech exports to Slovakia rose 25% YoY at 1992 while Slovak exports to the Czech Republic increased by only 16%.

European Rates Weekly | 11 May 2012

Page 25

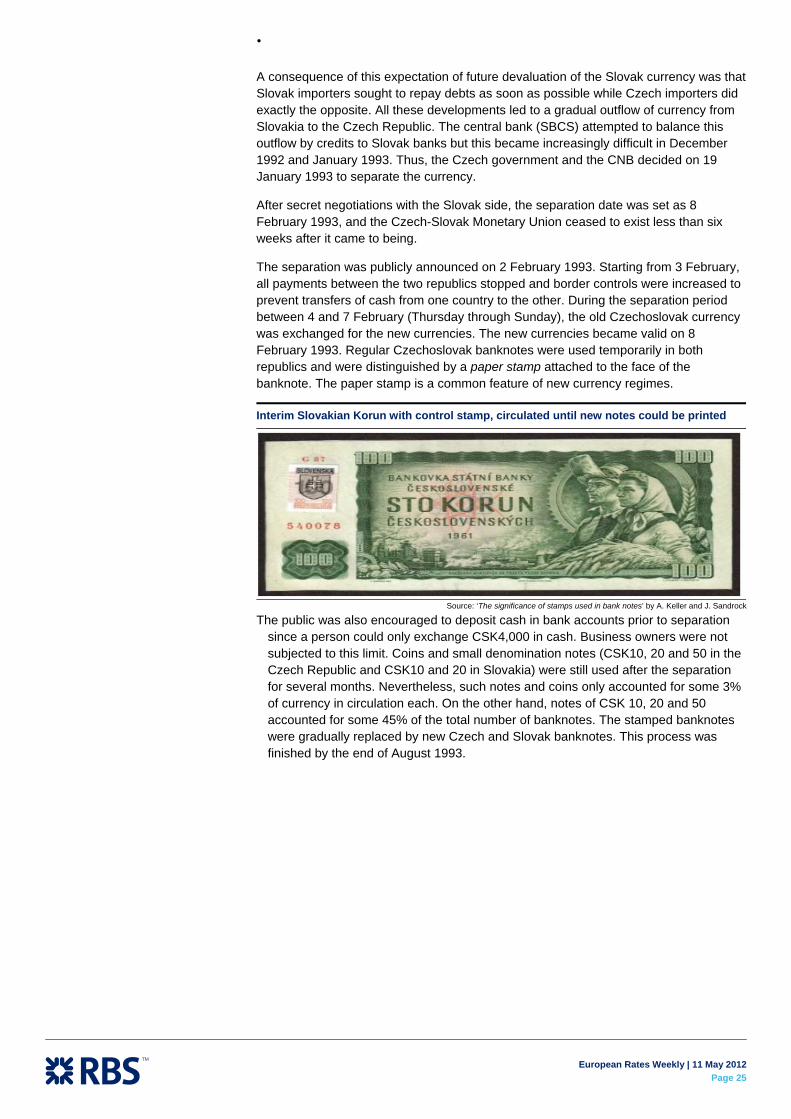

A consequence of this expectation of future devaluation of the Slovak currency was that Slovak importers sought to repay debts as soon as possible while Czech importers did exactly the opposite. All these developments led to a gradual outflow of currency from Slovakia to the Czech Republic. The central bank (SBCS) attempted to balance this outflow by credits to Slovak banks but this became increasingly difficult in December 1992 and January 1993. Thus, the Czech government and the CNB decided on 19 January 1993 to separate the currency.

After secret negotiations with the Slovak side, the separation date was set as 8 February 1993, and the Czech-Slovak Monetary Union ceased to exist less than six weeks after it came to being.

The separation was publicly announced on 2 February 1993. Starting from 3 February, all payments between the two republics stopped and border controls were increased to prevent transfers of cash from one country to the other. During the separation period between 4 and 7 February (Thursday through Sunday), the old Czechoslovak currency was exchanged for the new currencies. The new currencies became valid on 8 February 1993. Regular Czechoslovak banknotes were used temporarily in both republics and were distinguished by a paper stamp attached to the face of the banknote. The paper stamp is a common feature of new currency regimes.

Interim Slovakian Korun with control stamp, circulated until new notes could be printed

Source: ‘The significance of stamps used in bank notes’ by A. Keller and J. Sandrock

The public was also encouraged to deposit cash in bank accounts prior to separation since a person could only exchange CSK4,000 in cash. Business owners were not subjected to this limit. Coins and small denomination notes (CSK10, 20 and 50 in the Czech Republic and CSK10 and 20 in Slovakia) were still used after the separation for several months. Nevertheless, such notes and coins only accounted for some 3% of currency in circulation each. On the other hand, notes of CSK 10, 20 and 50 accounted for some 45% of the total number of banknotes. The stamped banknotes were gradually replaced by new Czech and Slovak banknotes. This process was finished by the end of August 1993.

European Rates Weekly | 11 May 2012

Page 26

Spain's bad bank plan The Spanish government announced the second phase of the Royal-Decree-Law of 3 February, which details the plan to resolve the banking crisis in the country. The measures discussed today are as follows:

The government will hire two auditors to undertake the valuation of all banks' entire loan portfolios.