Embed Size (px)

Citation preview

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 1/8

Equity Structured Products and Warrants

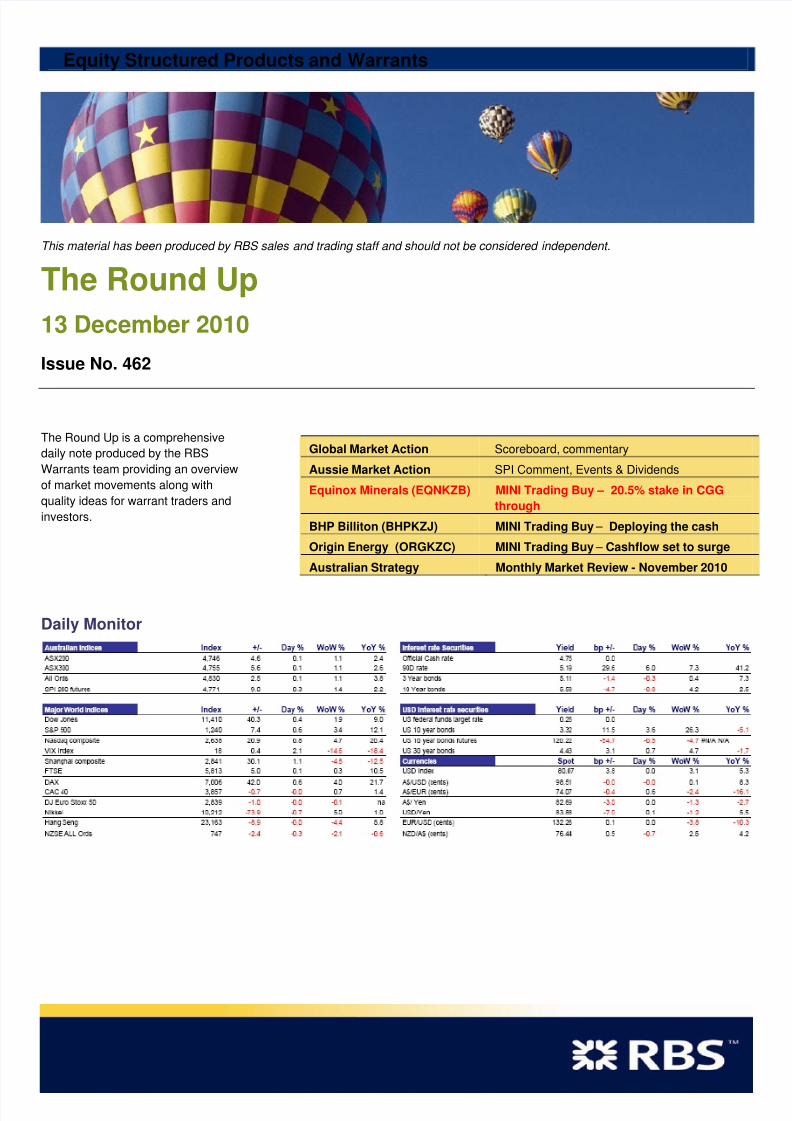

This material has been produced by RBS sales and trading staff and should not be considered independent.

The Round Up

13 December 2010 Issue No. 462

The Round Up is a comprehensive

daily note produced by the RBS

Warrants team providing an overview

of market movements along with

quality ideas for warrant traders and

investors.

Daily Monitor

Global Market Action Scoreboard, commentary

Aussie Market Action SPI Comment, Events & Dividends

Equinox Minerals (EQNKZB) MINI Trading Buy – 20.5% stake in CGG

through

BHP Billiton (BHPKZJ) MINI Trading Buy – Deploying the cash

Origin Energy (ORGKZC) MINI Trading Buy – Cashflow set to surge

Australian Strategy Monthly Market Review - November 2010

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 2/8

Equity Structured Products and Warrants

Overnight Commentary United States Commentary

Better than expected eco data from both on and offshore coupled with comments from the Commerce Department that

the US trade deficit had narrowed saw US indices stronger across the board Friday. GE added 3.4% after raising its

dividend for the second time this year while JPMorgan, BOA and Amex added 1% to 1.5%. National Semiconductor shed

7.8% after reporting weaker than expected sales numbers while a number of stocks rallied into their addition to the 500

on Friday. Volumes were lower than average which will continue to be a theme as we near Christmas.

United Kingdom and Europe Commentary

UK - The FTSE managed a slight gain Friday as strong Chinese import data sparked demand for miners. However

volumes were lower than average with fears of further Chinese interest rate rises setting a cautious undertone.

Vedanta was best on ground, adding 3.2%, as copper hovered near all time highs while ENRC, Xstrata and RIO added0.4% to 2.9%. Banks returned some of the previous sessions gains with Barclays and Standard Chartered shedding

1.4% and 2.6% with the latter hampered by broker downgrade. Diageo added 1% as it was rumoured they were in talks

with a Turkish firm in hopes of capturing some earnings within the emerging markets.

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 3/8

Equity Structured Products and Warrants

Commodities Commentary

Last % Move

GOLD 1391 0.50%OIL 87.79 -0.70%

NI 23919 1.60%

AL 2289 -1.30%

ZN 2274 -1.10%

CU 8990 0.40%

CRB -0.40%

SPI Commentary

The SPI traded up 4 pts to 4759. Open at 4755 with a high of 4763 and a low of 4730. Volume 31,786. Overnight the SPI traded up 12

pts to 4771.

SPI Intraday SPI Daily

*SPI report taken from the 9:50am open to the 4:30pm close on the previous trading day. Charts taken from IRESS

Upcoming Economic Events for the Week

Monday AUS

US

Tuesday AUS NAB Business Confidence US PPI, FOMC Rates decision

Wednesday AUS Westpac Consumer Confidence

US CPI

Thursday AUS Consumer Inflation Expectation

US Housing Starts, Initial Jobless

Friday AUS

US

*Dates are indicative only and may change

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 4/8

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 5/8

Equity Structured Products and Warrants

MINI Trading Buy: BHP Billiton (BHP.AX): Deploying the cash

We have come off research restriction following BHP's withdrawal of the PotashCorp bid. In

our view the stock offers a compelling investment case and we have reinstated our Buyrecommendation.

Source: IRESS Capital management a positive and probably only the start, in our view BHP has reinstated its US$13bn buyback program, which has US$4.2bn to be completed. The buyback will be on marketand for Plc shares (at this stage there is no off-market purchase of Ltd shares). When completed the buyback willincrease RBS Research’s FY11F and FY12F EPS by 2%. We view the reinstatement as an interim measure in terms ofcapital management. We believe the BHP board will review further capital management initiatives ahead of the interimresults in February 2011. RBS Research forecast BHP will be in a net-cash position by the end of FY11, leaving directorswith the options of reinvesting in the business, increasing dividends, buying back shares or all of the above.

We see plenty of room to increase dividends We believe BHP has the capacity to increase dividends substantially. Currently, RBS Research estimate BHP is on an

FY11 dividend yield of only c2%. The US$0.93 dividend equates to about US$5.1bn, which compares to operating cashflow of about US$29bn. In our view, BHP could materially increase this amount on a sustainable basis. We believe thiswould be another positive and that it would demonstrate management's confidence in future cash flow.

Options for M&A appear limited now that PotashCorp is off the agenda Opportunities for BHP to acquire a company that would make a meaningful impact now look limited. It seems that an oil &gas acquisition might be the easiest option for assets material to BHP. We see no reason for such a deal to be pursuedstraight away and we believe any such transaction would likely be six months away to allow for adequate due diligence.

Investment view - Buy - we think BHP offers a compelling investment case BHP is trading at a 15% discount to RBS Research’s NPV and on a PE of 10x FY12F. We advise investors to beoverweight BHP going into the next reporting season, as further capital management initiatives may provide anotherpositive catalyst for a re-rating. RBS Research reinstate full research coverage with a Buy recommendation and A$51.15

target price (was A$51.48).

RBS MINIs over BHP

Security ExPrc Stop Loss CP ConvFac Delta Description

BHPKZJ 32.1971 35.28 Long 1 1 MINI Long

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 6/8

Equity Structured Products and Warrants

MINI Trading Buy: Origin Energy (ORGKZC) – Cashflow set to surge ORG's FY10 earnings fell a little short of our forecasts, but, importantly, FY11 is on track to be a bigyear on the earnings front. With cashflows set to surge over the coming years, on our estimates, we

think the market is underestimating ORG's financial flexibility and optionality. Buy maintained.Buy maintained with RBS Target Price of $18.25

Source: IRESS

Underlying NPAT of A$585m was behind our A$611m forecast EBITDA of A$1,304m (incl associates) was the main variance to RBS Research numbers (A$1,321m forecast) but D&A(variance of A$9m) and minorities (variance of A$9m) also impacted. Operationally, the generation and E&P contributionswere lower than we expected with retail offsetting. Management has suggested it would have hit its 15% growth target ifnot for the overseas exploration write-downs, although RBS Research had these in the numbers already. OPCF ofA$789m was a little below RBS Research’s expectations (A$840m), but the 25c dividend was in line.

ORG has guided for 15% NPAT growth in FY11 FY11 guidance has been set at +35% EBITDAF growth and +15% NPAT growth in FY11. Importantly, the guidance now

includes a reasonably aggressive A$170m exploration programme and RBS Research have pushed up forecasts forexploration write-offs to about A$65m (from A$40m). This has been the sole driver of RBS Research’s earningsdowngrade. Importantly, the valuation impact is negligible.

APLNG - is consolidation lurking? Today ORG appeared the most open to collaborating with another project proponent since the Conoco deal was struckalmost two years ago and we continue to believe that any news on that front would be well received by the market. Likeall investors, we would like to see an off-take arrangement done before we get too excited about the project, but, in ourview, an investor is not paying a dime for any LNG upside.

Buy maintained, ORG's balance sheet about to go to work ORG's major capex programme is taking a breather and the company will have very substantial cashflow over the comingyears. Throw in an under-geared balance sheet and we believe the market is under-estimating the opportunities ahead.

The NSW energy sell-down and APLNG are the obvious candidates, but we wouldn't be surprised to see some accretiveacquisition from left field that could create shareholder value.BUY ORGKZC for 1-for-1 upside towards RBS Target Price of $18.25

RBS MINIs over ORG Security ExPrc Stop Loss CP ConvFac Delta Description

ORGKZC 1116.75 12.20 Call 1 1 MINI Long

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 7/8

Equity Structured Products and Warrants

RBS Round Up Corner: Monthly Market Review - November 2010

Australian equities fell 1.7% in November, as risk aversion dominated capital markets as

European sovereign risk re-emerged along with concerns that China may over-tighten as itworks to quell inflation. The defensive sectors outperformed, Health Care by 7.4% andTelecoms by 6.6%.

Australia's performance vs the world In local currency, the All Ordinaries (-1.2%) underperformed the US S&P 500 (-0.2%) but outperformed theWorld MSCI ex Australia Index (-1.7%) and the regional MSCI ex Japan Index (-1.6%).

The best- and worst-performing sectors The best performers for the month were Health Care (+5.7%), Telecommunication Services (+5.0%) andEnergy (+1.3%). The worst performers were Consumer Staples (-5.3%), Financials ex Property (-4.2%) andConsumer Discretionary (-4.2%).

The top-five and bottom-five performing S&P/ASX 200 stocks The top-five performers from the S&P/ASX 200 (price) Index for the month were Cudeco (+55.6%), IntrepidMines (+37.8%), Linc Energy (+34.0%), Riversdale Mining (+27.3%) and Sundance Resources (+24.1%). Thebottom-five performers were Hastie Group (-29.0%), Aristocrat Leisure (-25.9%), Infigen Energy (-21.8%),Karoon Gas Australia (-21.3%) and Murchison Metals (-20.3%).

Consensus earnings revisions

The top-five upgrades were Intoll Group (+18.1%), Iluka Resources (+15.1%), Alumina (+13.9%), Incitec Pivot(+8.1%) and Caltex Australia (+6.5%). The top-five downgrades were BlueScope Steel (-31.8%), AristocratLeisure (-31.2%), CSR (-12.1%), AWE (-11.8%) and OneSteel (-8.9%).

8/8/2019 RBS Round Up: 13 December 2010

http://slidepdf.com/reader/full/rbs-round-up-13-december-2010 8/8

Equity Structured Products and Warrants

For further information please do not hesitate to contact us on the details below

Equities Structured Products & Warrants

Toll free 1800 450 005 www.rbs.com.au/warrants

Trading Products Team

Ben Smoker 02 8259 2085 [email protected]

Ryan Corrigan 02 8259 2425 [email protected]

Investment Products Team

Elizabeth Tian 02 8259 2017 [email protected]

Tania Smyth 02 8259 2023 [email protected]

Robert Deutsch 02 8259 2065 [email protected]

Mark Tisdell 02 8259 6951 [email protected]

Disclaimer

The information contained in this report has been prepared by RBS Equities (Australia) Limited (“RBS Equities”) (ABN 84 002 768 701) (AFS Licence No 240530) and hasbeen taken from sources believed to be reliable. RBS Equities does not make representations that the information is accurate or complete and it should not be relied on assuch. Any opinions, forecasts and estimates contained in this report are the views of RBS Equities at the date of issue and are subject to change without notice. RBSEquities and its affiliated companies may make markets in the securities discussed. RBS Equities, its affiliated companies and their employees from time to time may holdshares, options, rights and warrants on any issue contained in this report and may, as principal or agent, sell such securities. RBS Equities may have acted as manager orco-manager of a public offering of any such securities in the past three years. RBS Equities’ affiliates may provide, or have provided banking services or corporate finance tothe companies referred to in this report. The knowledge of affiliates concerning such services may not be reflected in this report. This report does not constitute an offer orinvitation to purchase any securities and should not be relied upon in connection with any contract or commitment. RBS Equities, in preparing this report, has not taken intoaccount an individual client’s investment objectives, financial situation or particular needs. Before a client makes an investment decision, a client should consider whether anyadvice contained in this report is appropriate in light of their particular investment needs, objectives and financial circumstances. It is unreasonable to rely on anyrecommendation without first having consulted with your advisor for a personal securities recommendation. The information contained in this report is general advice only.RBS Equities, its officers, directors, employees and agents accept no liability for any loss or damage arising out of the use of all or any part of the information contained in thisreport. This Information is not intended for distribution to, or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to locallaw or regulation. If you are located outside Australia and use this Information, you are responsible for compliance with applicable local laws and regulation. This report maynot be taken or distributed, directly or indirectly into the United States, or to any U.S. person (as defined in Regulation S under the U.S. Securities Act of 1993, as amended).

The warrants contained in this report are issued by RBS Group (Australia) Pty Limited (“RBS”) (ABN 78 000 862 797, AFS Licence No. 247013). The Product DisclosureStatements relating to these warrants are available upon request from RBS Equities or on our website www.rbs.com.au/warrants

RBS Group (Australia) Pty Limited is not an Authorised Deposit-Taking Institution and these products do not form deposits or other liabilities of The Royal Bank of ScotlandN.V. or The Royal Bank of Scotland plc. The Royal Bank of Scotland plc does not guarantee the obligations of RBS Group (Australia) Pty Limited.

© Copyright 2009. RBS Equities. A Participant of the ASX Group.

Explanation of Warrant Tables

Security – refers to the code ascribed to the warrant, ExDate – refers to the date on which the warrant expires or is reset, ExPrc – refers to the exercise price, or second

instalment payment, CP – tells you whether the warrant is a call or a put, ConvFac – the conversion factor of the warrant which tells you how many warrants you need to

exercise in order to take possession of 1 share,Delta

– tells you how much the warrant will move for a 1c move in the underlying security,Description

– Tells you the typeof warrant.

All charts taken from IRESS unless indicated otherwise