Embed Size (px)

Citation preview

Ras Al Khaimah- The Emirate of Opportunities

March 2016

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

Table of Contents

2

INTRODUCTION

DEMAND DRIVERS

DEMAND CHARACTERISTICS

HOSPITALITY SUPPLY

MARKET TRENDS

GUEST EXPERIENCE INDEXTM

RETURN ON INVESTMENT

ANALYSIS

3

4

5

6

7

8

9

CONCLUSION 10

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

IntroductionMACRO LOCATION OF RAS AL KHAIMAH

3

REPORT OVERVIEW

Ras Al Khaimah (RAK), the fourth largest and northern

most emirate of the United Arab Emirates, has

experienced rapid economic growth in recent years.

The emirate is strategically located within proximity to

several major routes and demand generators and only

45 minutes from Dubai International Airport. The

emirate is renowned for its unique topography and

landscapes from the highest mountain in the UAE,

terracotta deserts to lush mangroves, white sandy

beaches and the longest stretch of coastline in the UAE.

In this paper, we examine the hospitality market of Ras

Al Khaimah, paying particular attention to upcoming

demand drivers, the characteristics of supply, key

performance indicators and return on investment.

TOURISM IN RAS AL KHAIMAH

Tourism is one of Ras Al Khaimah s most important

economic sectors and is considered a key engine for

continued GDP growth and job creation. In 2015, Ras Al

Khaimah welcomed 740,383 visitors and recorded a

13% rise in total tourism revenues.

As the emirate continues expansion plans to meet its

growth targets, several large-scale developments have

been announced which are expected to raise its tourism

profile and further build Ras Al Khaimah s position as a

leading leisure destination.

RAS AL KHAIMAH TOURISM DEVELOPMENT

AUTHORITY

Ras Al Khaimah Tourism Development Authority (RAK

TDA), was established in May 2011 as a government

entity to develop and promote the emirates tourism

infrastructure, both domestically and abroad.

RAK TDA has recently launched its three year tourism

strategy Destination Ras Al Khaimah 2019 , which sets

out a new agenda to ensure the long-term success and

viability of this rising sector.

Source: Colliers International

Dubai

Abu Dhabi

Mega Projects

Natural Beaches Luxury HotelsN

E

S

W

Population 416,600

Size 1,684 sq km

Coastline 64 km

Ras Al Khaimah

Rich Heritage

KEY MESSAGE• Dedicated tourism authority aiming to grow tourism into

the leading socio-economic driver under the Destination

Ras Al Khaimah 2019 strategic plan

Source: RAKTDA, Colliers International

MISSIONAdvance the development of a

sustainable and competitive

tourism industry to achieve 2018

targets

VISIONCompelling destination for visitors

seeking authentic, cultural,

historical and natural Arabian

experiences

RAKTDA STRATEGIC TARGETS FOR 2018

1 millionTotal Visitors

15,000 employeesTourism Employment

AED 2.4 billionTourism Revenues

Diverse Landscape

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

Roads Under Development / Partially Developed

Al Marjan Island

Al Hamra Village

Mina Al Arab

Al Hamra

Industrial Area

Al Jazira Al Hamra

Khor Al Jazira

Qawasim Corniche

80 km to Dubai International Airport 40 km to Oman

Ras Al Khaimah

International Airport

RAK City

Khor Hulaylah

67 km to Sharjah International Airport

Ice Land

Water Park

RAK Mall

RAK Shooting Club

Tower Links

Golf Club

Leisure Demand Generators

Falcon Island

RAK Museum

Al Hamra

Golf Club

N

ES

W

Jabel Jais

Wadi KhadijaKhatt Springs

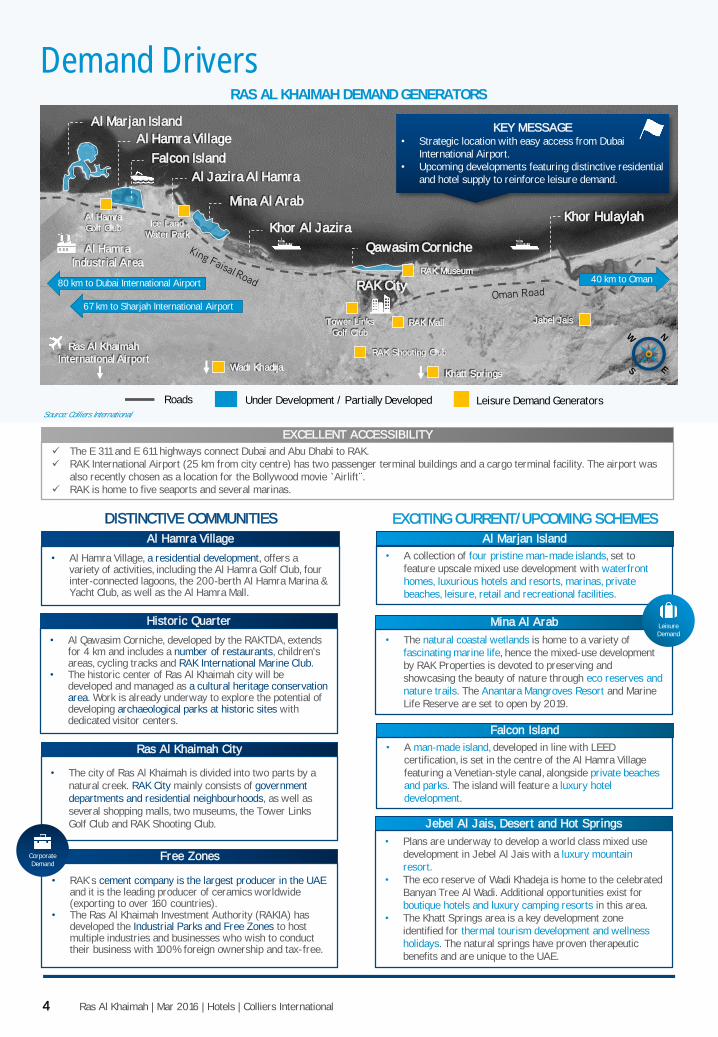

Demand Drivers

4

Source: Colliers International

RAS AL KHAIMAH DEMAND GENERATORS

The E 311 and E 611 highways connect Dubai and Abu Dhabi to RAK.

RAK International Airport (25 km from city centre) has two passenger terminal buildings and a cargo terminal facility. The airport was

also recently chosen as a location for the Bollywood movie Airlift .

RAK is home to five seaports and several marinas.

EXCELLENT ACCESSIBILITY

Al Marjan Island

• A collection of four pristine man-made islands, set to

feature upscale mixed use development with waterfront

homes, luxurious hotels and resorts, marinas, private

beaches, leisure, retail and recreational facilities.

Mina Al Arab

• The natural coastal wetlands is home to a variety of

fascinating marine life, hence the mixed-use development

by RAK Properties is devoted to preserving and

showcasing the beauty of nature through eco reserves and

nature trails. The Anantara Mangroves Resort and Marine

Life Reserve are set to open by 2019.

Falcon Island

• A man‐made island, developed in line with LEED

certification, is set in the centre of the Al Hamra Village

featuring a Venetian‐style canal, alongside private beaches

and parks. The island will feature a luxury hotel

development.

Leisure

Demand

• The city of Ras Al Khaimah is divided into two parts by a

natural creek. RAK City mainly consists of government

departments and residential neighbourhoods, as well as

several shopping malls, two museums, the Tower Links

Golf Club and RAK Shooting Club.

Ras Al Khaimah City

• Al Hamra Village, a residential development, offers a variety of activities, including the Al Hamra Golf Club, four inter‐connected lagoons, the 200‐berth Al Hamra Marina & Yacht Club, as well as the Al Hamra Mall.

Al Hamra Village

• RAK s cement company is the largest producer in the UAE and it is the leading producer of ceramics worldwide (exporting to over 160 countries).

• The Ras Al Khaimah Investment Authority (RAKIA) has developed the Industrial Parks and Free Zones to host multiple industries and businesses who wish to conduct their business with 100% foreign ownership and tax-free.

Free Zones

• Al Qawasim Corniche, developed by the RAKTDA, extends for 4 km and includes a number of restaurants, children's areas, cycling tracks and RAK International Marine Club.

• The historic center of Ras Al Khaimah city will be developed and managed as a cultural heritage conservation area. Work is already underway to explore the potential of developing archaeological parks at historic sites with dedicated visitor centers.

Historic Quarter

DISTINCTIVE COMMUNITIES EXCITING CURRENT/UPCOMING SCHEMES

Corporate

Demand

KEY MESSAGE• Strategic location with easy access from Dubai

International Airport.

• Upcoming developments featuring distinctive residential

and hotel supply to reinforce leisure demand.

Jebel Al Jais, Desert and Hot Springs

• Plans are underway to develop a world class mixed use

development in Jebel Al Jais with a luxury mountain

resort.

• The eco reserve of Wadi Khadeja is home to the celebrated

Banyan Tree Al Wadi. Additional opportunities exist for

boutique hotels and luxury camping resorts in this area.

• The Khatt Springs area is a key development zone

identified for thermal tourism development and wellness

holidays. The natural springs have proven therapeutic

benefits and are unique to the UAE.

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

20%

30%

40%

50%

60%

70%

80%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Occupancy%

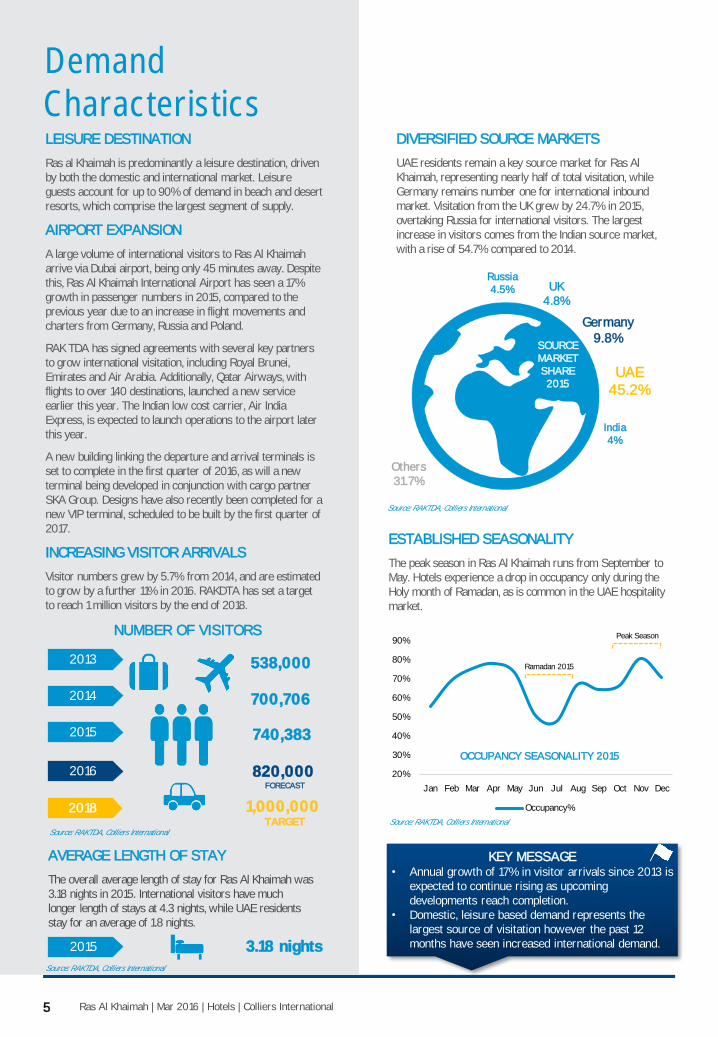

Demand

CharacteristicsLEISURE DESTINATION

Ras al Khaimah is predominantly a leisure destination, driven

by both the domestic and international market. Leisure

guests account for up to 90% of demand in beach and desert

resorts, which comprise the largest segment of supply.

AIRPORT EXPANSION

A large volume of international visitors to Ras Al Khaimah

arrive via Dubai airport, being only 45 minutes away. Despite

this, Ras Al Khaimah International Airport has seen a 17%

growth in passenger numbers in 2015, compared to the

previous year due to an increase in flight movements and

charters from Germany, Russia and Poland.

RAK TDA has signed agreements with several key partners

to grow international visitation, including Royal Brunei,

Emirates and Air Arabia. Additionally, Qatar Airways, with

flights to over 140 destinations, launched a new service

earlier this year. The Indian low cost carrier, Air India

Express, is expected to launch operations to the airport later

this year.

A new building linking the departure and arrival terminals is

set to complete in the first quarter of 2016, as will a new

terminal being developed in conjunction with cargo partner

SKA Group. Designs have also recently been completed for a

new VIP terminal, scheduled to be built by the first quarter of

2017.

INCREASING VISITOR ARRIVALS

Visitor numbers grew by 5.7% from 2014, and are estimated

to grow by a further 11% in 2016. RAKDTA has set a target

to reach 1 million visitors by the end of 2018.

5

UAE

45.2%

Germany

9.8%

India

4%

UK

4.8%

Russia

4.5%

Source: RAKTDA, Colliers International

Source: RAKTDA, Colliers International

OCCUPANCY SEASONALITY 2015

Source: RAKTDA, Colliers International

Others

31.7%

ESTABLISHED SEASONALITY

The peak season in Ras Al Khaimah runs from September to

May. Hotels experience a drop in occupancy only during the

Holy month of Ramadan, as is common in the UAE hospitality

market.

AVERAGE LENGTH OF STAY

The overall average length of stay for Ras Al Khaimah was

3.18 nights in 2015. International visitors have much

longer length of stays at 4.3 nights, while UAE residents

stay for an average of 1.8 nights.

Ramadan 2015

Peak SeasonNUMBER OF VISITORS

2013

2014

2015 740,383

538,000

700,706

2016

2018

820,000

1,000,000

FORECAST

TARGET

2015 3.18 nights

DIVERSIFIED SOURCE MARKETS

UAE residents remain a key source market for Ras Al

Khaimah, representing nearly half of total visitation, while

Germany remains number one for international inbound

market. Visitation from the UK grew by 24.7% in 2015,

overtaking Russia for international visitors. The largest

increase in visitors comes from the Indian source market,

with a rise of 54.7% compared to 2014.

KEY MESSAGE• Annual growth of 17% in visitor arrivals since 2013 is

expected to continue rising as upcoming

developments reach completion.

• Domestic, leisure based demand represents the

largest source of visitation however the past 12

months have seen increased international demand.

SOURCE

MARKET

SHARE

2015

Source: RAKTDA, Colliers International

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

0% 20% 40% 60% 80% 100%

5-Star 4-Star 3-Star 2-Star 1-Star Standard SA

Hospitality SupplyCURRENT SUPPLY

The Ras Al Khaimah hospitality market consists of a

mixture of hotels and resorts, serviced apartments and

guest houses. The majority of guest houses, serviced

apartments and city hotels are located in or in close

proximity to RAK City. Resorts, which dominate the

market, are typically located towards the south of the

coastline as part of upcoming developments, as well as

two desert resorts.

The 5-star segment accounts for the highest volume of

properties and keys (58% of total supply), of which 87%

are internationally branded, resort properties. Hotels in

the 4-star segment are a mixture of city hotels and

resorts, whereas all 3-star hotels are located in the city

and are owner operated.

Resort properties (5-star) have an average of 314 keys,

while city hotels have an average of 55 keys.

SERVICED APARTMENTS

The serviced apartment sector in Ras Al Khaimah is

limited, with 7 properties currently in operation. Majority

of the properties are located in RAK City, with an

average size of 45 keys. No new supply has been

announced in this segment, suggesting a possible

market gap.

GROWTH IN SUPPLY

The hospitality market witnessed the largest increase in

supply in 2014, with a 42% increase in keys compared

to 2013, due to the opening of new properties, such as

the Waldorf Astoria and resort properties on Marjan

Island.

RAKTDA expects the market size to reach 12,000 keys

by 2020. Approximately 4,040 keys have already been

announced to open in the next 5 years and an additional

2,841 keys are expected to be announced shortly

according to the RAKTDA.

The hotel market is led by Hilton Worldwide, which

currently operates 5 properties. InterContinental Hotels

Group (IHG) is expected to make a strong entrance in

the market with the InterContinental Mina Al Arab and

the Crowne Plaza Resort, expected to open before

2020. Other notable entries to the market include the

expected opening of the Marriott Resort and Uniqorn

Resort Marjan Island.

Source: RAKTDANote: The graph includes forthcoming supply according to RAKTDA, part of which is yet to be announced.

6

By Rating

HOSPITALITY SUPPLY CHARACTERISTICS

Beach &

Desert Resorts

3,274 keys

Serviced

Apartments

316 keys

Guest

Houses

241 keys

City

Hotels

1,553 keys

EVOLUTION OF SUPPLY

Total Hospitality Supply 5,384 keys

By Operator

By Property

58% 32% 2% 2% 6%1%

0 1,000 2,000

Current Supply (No. of Keys) Future Supply (No. of Keys)

Source: RAKTDA, STR, Colliers InternationalNote: Current supply does not take into consideration properties currently under renovation, future supply only includes announced supply as of February 2016

KEY MESSAGE• Presence of internationally branded, 5-star resort

properties with opportunities to develop further

as mega projects reach completion.

• Limited number of quality hotels and serviced

apartments in city centre and desert resorts.

• Market gap for serviced apartment component

within resort properties to cater to families.

• Opportunity to develop eco-friendly desert

resorts and luxury mountain resorts.

SA

5,384 5,9326,729 6,954

9,122

12,000

2015 2016(f) 2017(f) 2018(f) 2019(f) 2020(f)

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

Market Trends

Source: Colliers International

REVENUE MIX

% contribution to total property revenue

F&B

4

8 %

ANCILLARY

ROOMS

5 8 -6 3 %3 5 -3 8 %

2 4%

7

CURRENT PERFORMANCE

In 2014, the Ras Al Khaimah hospitality market

experienced a softening in performance due to the

increase in supply entering the market and the changing

source market conditions.

In 2015, however, the hotel market demonstrated an

impressive progression compared to 2014 as visitation

increased and performance of new hotel openings

stabilised. Consequently, hotels in Ras Al Khaimah

reported:

• A 3.3% increase in occupancy rates, reaching

64.7% in 2015

• Average daily rate growth of 7% on 2014

• Highest increase in RevPAR in five years, up by 10%

• 12.1% increase in room revenues

• A 14.4% increase in F&B revenues

The growth in performance was demonstrated across

both types of properties resorts and city hotels. Ras

Al Khaimah resorts achieve a higher ADR due to the

large concentration of internationally, branded 5-star

supply in the resort segment, while city hotels, the

majority of which are unbranded, tend to target

corporate demand and price sensitive customers.

• Large room sizes to accommodate GCC source

market demand.

• Greater proportion of suites and connected rooms.

KEY PERFORMANCE INDICATORS

OCC%

ADR (USD)

RevPAR(USD)

RESORTS CITY HOTELS

2014 2015 2014 2015

62% 65%

164.6 169.2

103.5 110.1

62% 64%

70.5 72.2

46.644.4

Source: RAKTDA, Colliers International

FACILITY MIX

KEY MESSAGE• Hotel performance has withstood increases in

hotel supply and changing source market

conditions.

• Resort performance indicates further

opportunities to develop destination hotels with

extensive range of leisure and wellness facilities.

• Opportunities exist to develop luxury mountain

resorts, serviced apartments and additional city

hotels.

• High F&B contribution due to lack of significant food and beverage

offerings outside of hotels

• Meeting facilities predominately in city hotels while resorts tend to

offer large banqueting space.

• Resort hotels feature luxurious spas with an average of 8 treatment

rooms and extensive leisure facilities.

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International7

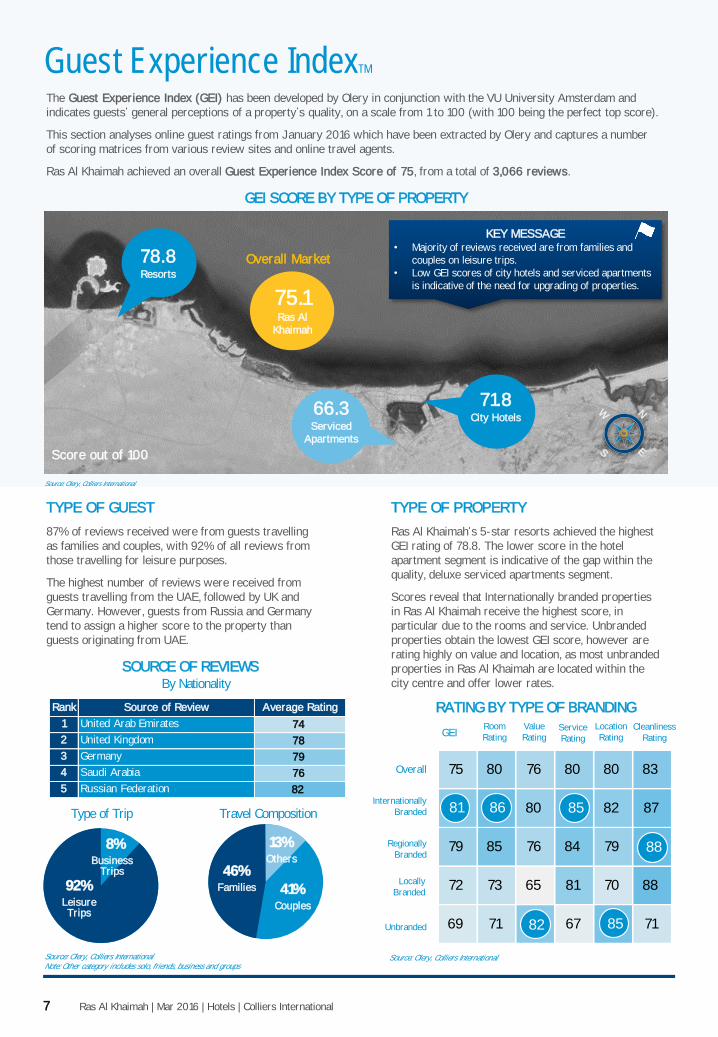

Guest Experience IndexTM

The Guest Experience Index (GEI) has been developed by Olery in conjunction with the VU University Amsterdam and

indicates guests general perceptions of a property s quality, on a scale from 1 to 100 (with 100 being the perfect top score).

This section analyses online guest ratings from January 2016 which have been extracted by Olery and captures a number

of scoring matrices from various review sites and online travel agents.

Ras Al Khaimah achieved an overall Guest Experience Index Score of 75, from a total of 3,066 reviews.

Source: Olery, Colliers InternationalSource: Olery, Colliers InternationalNote: Other category includes solo, friends, business and groups

By Nationality

RATING BY TYPE OF BRANDING

Overall

Unbranded

Locally

Branded

Regionally

Branded

Internationally

Branded

GEIRoom

Rating

Value

RatingService

Rating

Location

Rating

Cleanliness

Rating

92%Leisure Trips

8%Business

Trips

N

ES

W

78.8Resorts

75.1Ras Al

Khaimah

71.8City Hotels

66.3Serviced

Apartments

Score out of 100

Overall Market

N

ES

W

46%Families 41%

Couples

13%Others

SOURCE OF REVIEWS

Type of Trip Travel Composition

TYPE OF GUEST

87% of reviews received were from guests travelling

as families and couples, with 92% of all reviews from

those travelling for leisure purposes.

The highest number of reviews were received from

guests travelling from the UAE, followed by UK and

Germany. However, guests from Russia and Germany

tend to assign a higher score to the property than

guests originating from UAE.

TYPE OF PROPERTY

Ras Al Khaimah s 5-star resorts achieved the highest

GEI rating of 78.8. The lower score in the hotel

apartment segment is indicative of the gap within the

quality, deluxe serviced apartments segment.

Scores reveal that Internationally branded properties

in Ras Al Khaimah receive the highest score, in

particular due to the rooms and service. Unbranded

properties obtain the lowest GEI score, however are

rating highly on value and location, as most unbranded

properties in Ras Al Khaimah are located within the

city centre and offer lower rates.

GEI SCORE BY TYPE OF PROPERTY

Source: Olery, Colliers International

KEY MESSAGE• Majority of reviews received are from families and

couples on leisure trips.

• Low GEI scores of city hotels and serviced apartments

is indicative of the need for upgrading of properties.

75 80 76 80 80 83

82 86 80 85 82 87

79 85 76 84 79 87

72 73 65 81 70 88

69 71 82 67 85 71

81 86 85

8582

88

Rank Source of Review Average Rating

1 United Arab Emirates 74

2 United Kingdom 78

3 Germany 79

4 Saudi Arabia 76

5 Russian Federation 82

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

Return on Investment Analysis

8

Occupancy

(%)

Average Daily

Rate

(USD)

RevPAR

(USD)

Profit Conversion

(%)

Site Acquisition

and Construction

Cost

( 000 USD)

Equity IRR

(%)

ESTIMATE OF POTENTIAL RETURNS FOR A HYPOTHETICAL 200 KEY HOTEL INVESTMENT

Al Marjan Island

Ras Al Khaimah

Palm Jumeirah

Dubai

Saadiyat Island

Abu Dhabi

70% 78% 73%

232 381 272

162 298 199

40% 32% 32%

75,777 106,948 79,700

16.1% 16.2% 14.9%

Al Marjan Island Palm Jumeirah Saadiyat Island

Notes:1. Based on a 200 key hypothetical hotel in each of the mentioned locations

2. Assumed the hotels are managed by an International Hotel Operator3. Assumed Upper Upscale Positioning4. IRR has been calculated using a 50:50 Debt to Equity assumption

Disclaimer:The Projections provided with respect to each of the hypothetical hotels areestimates only, and are based upon Colliers opinion on how each of thehypothetical hotels could perform within the respective markets. Estimateshave also been made regarding land acquisition and construction costs persubmarket.

In this section we explore the potential return on investment that exists from hotel development within the Emirate of RAK at

present. Our analysis focuses on the Marjan Island development within RAK, which is well known for being home to a

number of high-end beach hotels. For comparison purposes, we have also carried out a similar exercise on two other well

known resort areas within the UAE, namely, Palm Jumeirah, Dubai and Saadiyat Island, Abu Dhabi.

KEY MESSAGE• Although not as well known internationally as the Emirates of Dubai

and Abu Dhabi, Ras Al Khaimah can offer similar attractive hotel

investment returns for Owners/ Developers.

• In RAK, beach resorts (in particular), have shown high profit

conversion when compared to other similar regional markets.

• Good levels of profitability, along with more affordable land prices,

offer hotel investors in RAK the opportunity to achieve attractive

returns.

Source: Colliers International

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International

Conclusion

• Ras Al Khaimah s free trade zone has zero tax on income and capital gains as well as no property transfer or value-added tax.

• Although not as well known internationally as the Emirates of Dubai and Abu Dhabi, Ras Al Khaimah can offer similar attractive hotel

investment returns for Owners/ Developers

• Good levels of profitability, along with more affordable land prices, offer hotel investors in RAK the opportunity to achieve attractive

returns

• RAK benefits from leisure demand, nearly half of which generates from the domestic market.

• The emirate offers a variety of unique features, with the longest stretch of coastline and tallest mountain in the UAE, cultural and heritage

sites and diverse landscapes.

• Upcoming mega projects, including further development of the popular Al Marjan Island and Mina Al Arab developments.

• RAK International Airport, 25 km from the city centre, services a diverse range of source markets and is set for expansion.

• 45 mins from Dubai International Airport.

• The emirate has 5 seaports and several marinas.

10

DEVELOPMENT OPPORTUNITIES

Focus on unique F&B

concepts to act as a

draw factor for the

hotel

Trendy F&B Offers

Branded City Hotels

Simple and efficient in

design, with modern

amenities and meeting

facilities

• Increase in guest visitation by 6% and tourism revenues by 13% in 2015.

• Dedicated tourism authority aiming to grow tourism into the leading socio-economic driver under the Destination Ras Al Khaimah 2019

strategic plan.

• Existing and forthcoming supply of quality, internationally branded resorts along the coastline.

• Hotel performance has withstood increases in hotel supply and changing source market conditions.

• Strong performance of Ras Al Khaimah hospitality market, with the highest RevPAR recorded in 2015 over the last five years.

Ecotourism

Opportunity to further

develop sustainable, eco-

friendly desert and mountain

resorts and luxury camping

Destination Hotels

Opportunity to further

develop resort properties

offering an extensive range of

leisure and wellness facilities

Serviced Apartments

Serviced apartment

component within

resort properties to

cater to families

Opportunity to

introduce new F&B

concepts through

leasing or franchises

Market gap for

branded serviced

apartments in the

city-centre

FOCUS ON TOURISM

EASE OF ACCESSIBILITY

LEISURE DEMAND

GROWTH IN HOSPITALITY PERFORMANCE

INVESTOR FRIENDLY & ATTRACTIVE POTENTIAL RETURNS

Source: Colliers International

Resort development

zones include coastal,

desert and mountain

areas

Opportunity to further

develop wellness resorts

around natural thermal

springs

Ras Al Khaimah | Mar 2016 | Hotels | Colliers International11

Colliers International Hotels

Colliers International Hotels division is a global network of specialist consultants in hotel, resort,

marina, golf, leisure and spa sectors, dedicated to providing strategic advisory services to owners,

developers and government institutions to extract best values from projects and assets. The

foundation of our service is the hands-on experience of our team combined with the intelligence and

resources of global practice. Through effective management of the hospitality process, Colliers

delivers tangible financial benefits to clients. With offices in Dubai, Abu Dhabi, Jeddah, Riyadh and

Cairo, Colliers International Hotels combines global expertise with local market knowledge.

SERVICES AT A GLANCE

The team can advise throughout the key phases and lifecycle of projects

• Destination / Tourism / Resort / Brand Strategy

• Market and Financial Feasibility Study

• Development Consultancy & Highest and Best Use Analysis

• Operator Search, Selection and Contract Negotiation

• Pre-Opening Budget Analysis and Operational Business Plan

• Owner Representative / Asset Management / Lenders Asset Monitoring

• Site and Asset Investment Sale and Acquisition/Due Diligence

• RICS Valuations for Finance Purposes and IPOs

Our hotels team in the MENA region:

$9 39,200 8,880billion keys Hotel keys

investment value of valued under asset management

projects advised

About Colliers InternationalColliers International is a global leader in commercial real estate services, with over 16,300 professionals operating out of more than 502 offices in 67 countries. Colliers International delivers a full range of services to real estate users, owners and investors worldwide, including global corporate solutions, brokerage, property and asset management, hotel investment sales and consulting, valuation, consulting and appraisal services and insightful research. The latest annual survey by the LipseyCompany ranked Colliers International as the second-most recognized commercial real estate firm in the world. In MENA Colliers International has provided leading advisory services through its regional offices since 1996. Colliers International currently has four corporate offices in the region located in Dubai, Abu Dhabi, Riyadh and Jeddah.

colliers.com

Colliers International, 2016

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to

ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their

professional advisors prior to acting on any of the material contained in this report.

$2.3billion in

annual revenue

1.7billion square feet

under management

16,300professionals

and staff

502 offices in

67 countries on

6 continentsUnited States: 151

Canada: 46

Latin America: 26

Asia Pacific: 190

EMEA: 89

Colliers International | MENA Region

Dubai | United Arab Emirates

+971 4 453 7400

For further information,

please contact:

Filippo Sona

Director | Head of Hotels | MENA Region

Main +971 4 453 7400

Mobile +971 55 899 6102

Selim El Zein

Associate Director | Hotels | MENA Region

Main +971 4 453 7400

Mobile +971 55 899 6103