Embed Size (px)

Citation preview

Southern European Insight Day

Barcelona May 2015

Randstad Spain

Index

2

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Index

3

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

4

• Dramatic change of trend started in 2008 coming to an end in 2014

• Main stoppers for

recovery are Public Debt and Strong Unemployment (+ Activity Rate)

• Unemployment Rate is

linked to a high volume of informal economy

• Stabilization has come

through salaries devaluation & trade balance (Internal Demand still to improve)

Source: National Institute of Statistics and Central Bank of Spain

Economy & Labour Market Positive economic cycle impacting labour market…

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

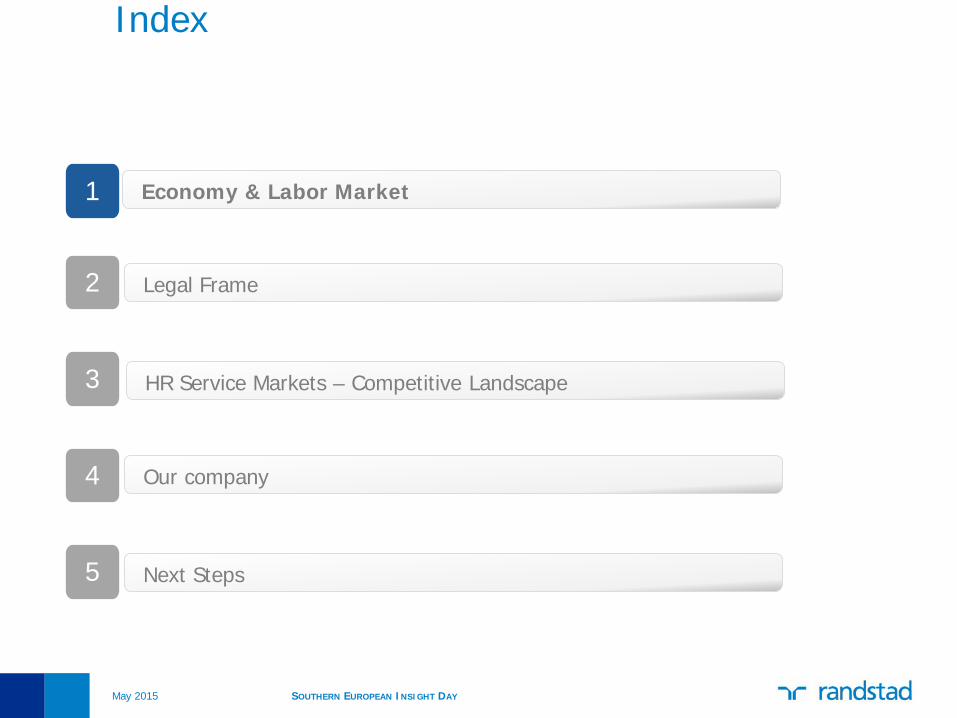

Economy & Labour Market CLUs give sustainability to the positive trend…

5

• Internal & External

devaluation

• Right evolution of ULC vs. Europe

• Global decisions about production already affecting positively

Source: Eurostat, OECD

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

6

•Source: National Institute of Statistics , EPA 2015 / Q1

Actives Employed17.454.800

22.899.400 Unemployed5.444.600

Activity rate = 59,45 Unemployment rate = 23,78(Actives/Population>16 years x 100) (Unemployed / Actives x 100)

Population > 16 years

38.517.200

Inactives15.617.800

Economy & Labour Market …Although the Labour Market is still very weak

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

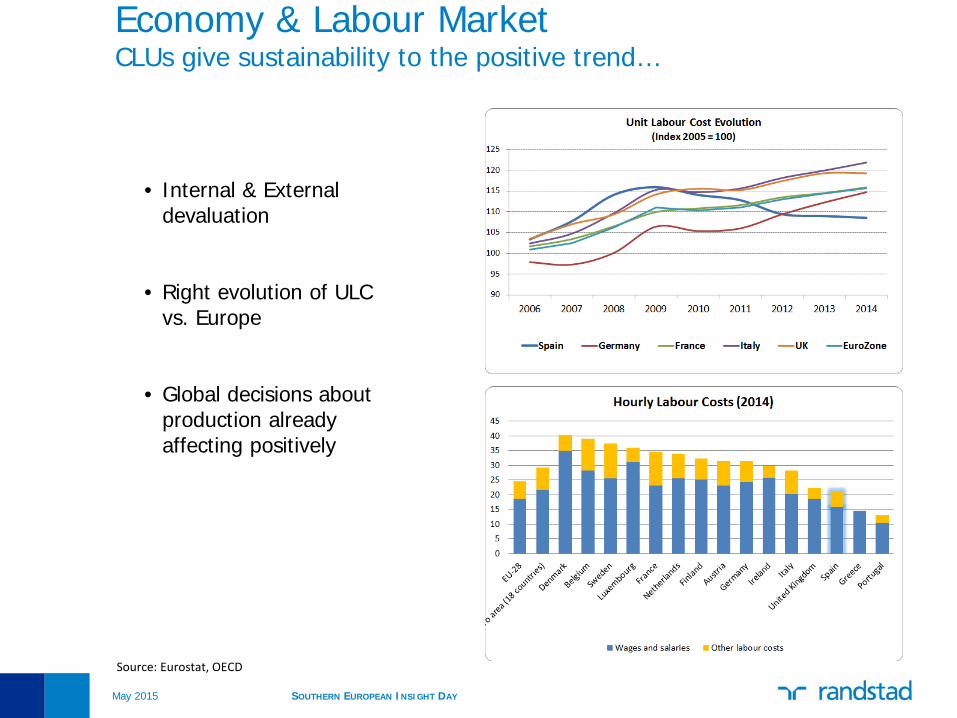

7

*Source: Eurostat 2013, Eurociett 2014

Temporary Rate Penetration Rate

Economy & Labour Market …And penetration & temporary rates Benchmark are not attractive

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

8

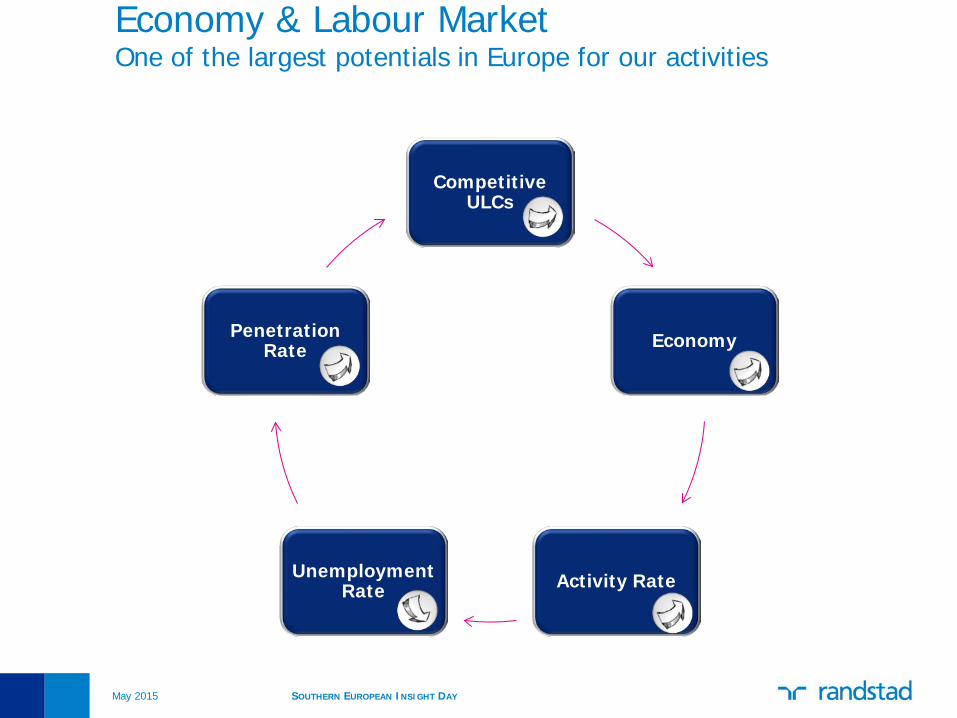

Economy & Labour Market One of the largest potentials in Europe for our activities

Competitive ULCs

Economy

Activity Rate Unemployment Rate

Penetration Rate

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Index

9

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

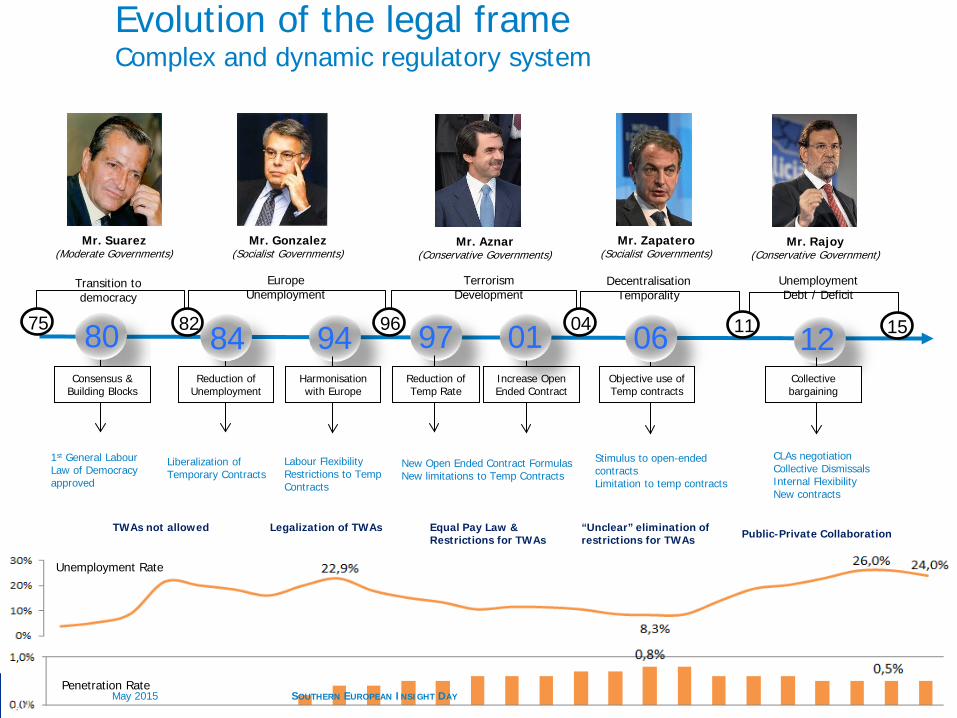

94 97 06 12

Transition to democracy

1st General Labour Law of Democracy approved

Liberalization of Temporary Contracts

Equal Pay Law & Restrictions for TWAs

Stimulus to open-ended contracts Limitation to temp contracts

Mr. Suarez (Moderate Governments)

Mr. Gonzalez (Socialist Governments)

Mr. Aznar (Conservative Governments)

Mr. Zapatero (Socialist Governments)

Mr. Rajoy (Conservative Government)

Europe Unemployment

Terrorism Development

Decentralisation Temporality

Unemployment Debt / Deficit

CLAs negotiation Collective Dismissals Internal Flexibility New contracts

Unemployment Rate

Penetration Rate

10

80 84 75 82 96 04 11 15

Consensus & Building Blocks

Reduction of Unemployment

TWAs not allowed

Harmonisation with Europe

Labour Flexibility Restrictions to Temp Contracts

Legalization of TWAs

Reduction of Temp Rate

Increase Open Ended Contract

New Open Ended Contract Formulas New limitations to Temp Contracts

Objective use of Temp contracts

“Unclear” elimination of restrictions for TWAs

Collective bargaining

Public-Private Collaboration

Evolution of the legal frame Complex and dynamic regulatory system

01

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

11

• No major legal frame changes in the coming future expected

• Penetration Rate to increase up to 0.8% just with positive Economic Trend

• Staffing Market to double from >2.0 bio to >4.0bio

• Penetration Rate in existing markets

• New markets (Closed Activities) • Salaries Increase

Legal Frame Hot Topics: Threats & Opportunities

High

High

Real opening of restricted sectors

Prosecution of Informal Work and bad practices Public – Private Collaboration

New limitation to Temporary Contracts

Limitation of applicability of Outsourcing CLAs.

Public competition in staffing market

Main Threats

Low

Med

?

Impact

Main Opportunities Impa

ct

Low

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Index

12

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

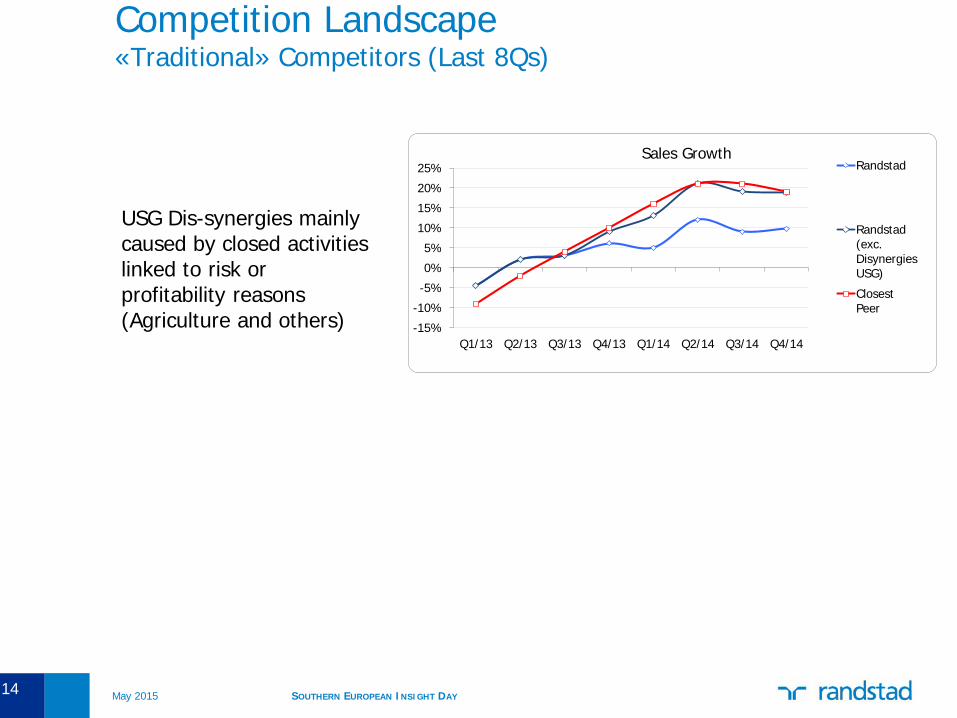

Competition Landscape «Traditional» Competitors (based in 2013 figures*)

* Randstad estimation based in last public annual accounts projections

# 1 Position in the HR Services Market (total portfolio) # 1 Position in the Staffing Activities

661579

263

65 60 57 54

Randstad Adecco Manpower Flexiplan Eurofirms Synergie Iman

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 13

14

Ambition

Competition Landscape «Traditional» Competitors (Last 8Qs)

USG Dis-synergies mainly caused by closed activities linked to risk or profitability reasons (Agriculture and others)

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Q1/13 Q2/13 Q3/13 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14

Sales Growth Randstad

Randstad(exc.DisynergiesUSG)

ClosestPeer

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

15

Competition Landscape Perm Professionals Competitors*

* Randstad estimation based in last public annual accounts projections and market information

2% 4%

6% 8,5%

24 48

48

80

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Market Trend Employer driven vs. Candidate driven

Employer Driven Market

Employer Driven Market Candidate Driven Market

Employer Driven Market

2014 2020

Professionals

Staffing

Outsourcing

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 16

Index

17

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

18

93 97

Start Operations in Barcelona

Incorporation of Randstad Spain

(Staffing)

99

1st Acquisition: Tempo Grup

(Staffing)

00

Acquisition of Umano

(Outsourcing)

04

Boost Plan

07

Divestment in Logistics & Call

Centres

09

Integration Vedior

10

Strong Recession

12

GAP Professionals (Perm)

Integration USG

14

Outplacement HR Solutions

Company Lifeline Total History

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

13 11 12 14

19

Company Lifeline Zoom-In Last 5 years strategy

• Focus in Core Products

• Efficiency & Control

• Manage Downturn (Recovery Rates)

• Technology working for efficiency

• Investment in Talent Development

• Outside-In Approach (Differentiation)

• Service Culture

• Focus in Active Customers

• Total HR Offering (Product Mix)

• Different Approach per product (segmentation adapted: New Service Delivery Models vs. New USPs)

• Central Functions: Accountability & SLAs

• Technology working for service level

• Further Investment in Talent Development and Employee Engagement

• Outside-In Approach

• Service Culture

GAP1 GAP2 GAP3

Efficiency & Control From Staffing to Total HR

Offering

10

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Product

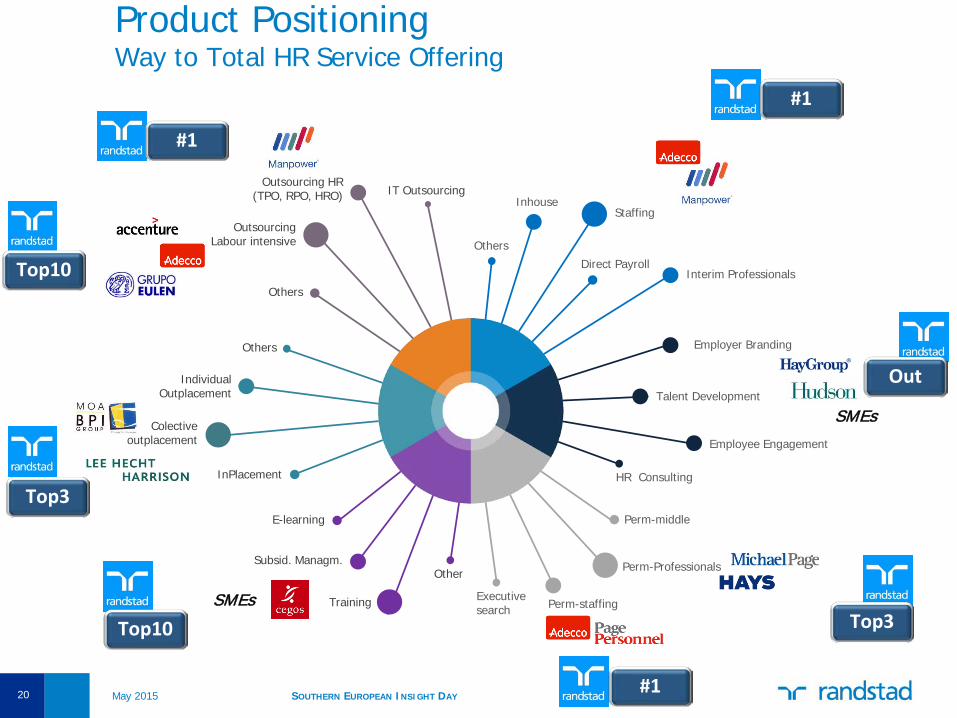

Product Positioning Way to Total HR Service Offering

Others

Outsourcing HR(TPO, RPO, HRO) IT Outsourcing

Outsourcing Labour intensive

InPlacement

Others

IndividualOutplacement

Colectiveoutplacement

Subsid. Managm.

E-learning

Other

Training Executivesearch

Perm-middle

Perm-staffing

Perm-Professionals

Inhouse

Direct Payroll

Others

Staffing

Interim Professionals

HR Consulting

Talent Development

Employee Engagement

Employer Branding

SMEs

SMEs

#1

#1

Top3

Top10

Top3

Top10

Out

#1 May 2015 SOUTHERN EUROPEAN INSIGHT DAY 20

Product Positioning Different approach per product

Inhouse

Direct Payroll Others

HR Consulting

Individual Outplacement

InPlacement

Others

Others

Subsid. Managm.

E-learning

Other

Executive search

Perm-middle

Perm-staffing

Talent Development

Employee Engagement

Outsourcing HR (TPO, RPO, HRO)

IT Outsourcing

Employer Branding

Outsourcing Labour intensive

Training

Perm-Professionals

Staffing

Interim Professionals

Collective outplacement

Productivity (tools)

Positioning

Reactive

Analysis

“Productization”

Markettshare Growth

“e” end to end

Risk Control

Positioning Out Growth-ABFS

Blended approach

Boost

Organization

Specialized Unit

Consultancy

Appraisal Systems Development Centers Talent Pools

Leverage

Growth Platform

Efficiency (SDMs) Differentiation SME

Exit barriers

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 21

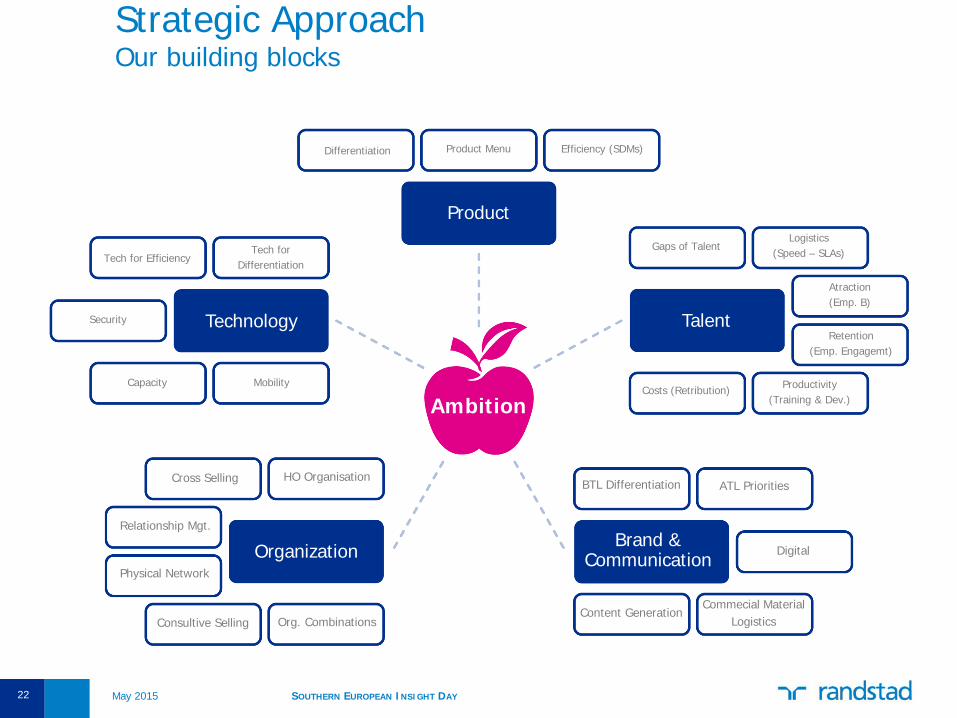

Strategic Approach Our building blocks

Technology

Organization Brand & Communication

Product

Talent

Gaps of Talent Logistics

(Speed – SLAs)

Atraction (Emp. B)

Retention (Emp. Engagemt)

Productivity (Training & Dev.)

Costs (Retribution)

Differentiation Efficiency (SDMs) Product Menu

Tech for Differentiation

Tech for Efficiency

Security

Capacity Mobility

Cross Selling HO Organisation

Relationship Mgt.

Physical Network

Consultive Selling Org. Combinations Content Generation

Digital

Commecial Material Logistics

ATL Priorities BTL Differentiation

Ambition

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 22

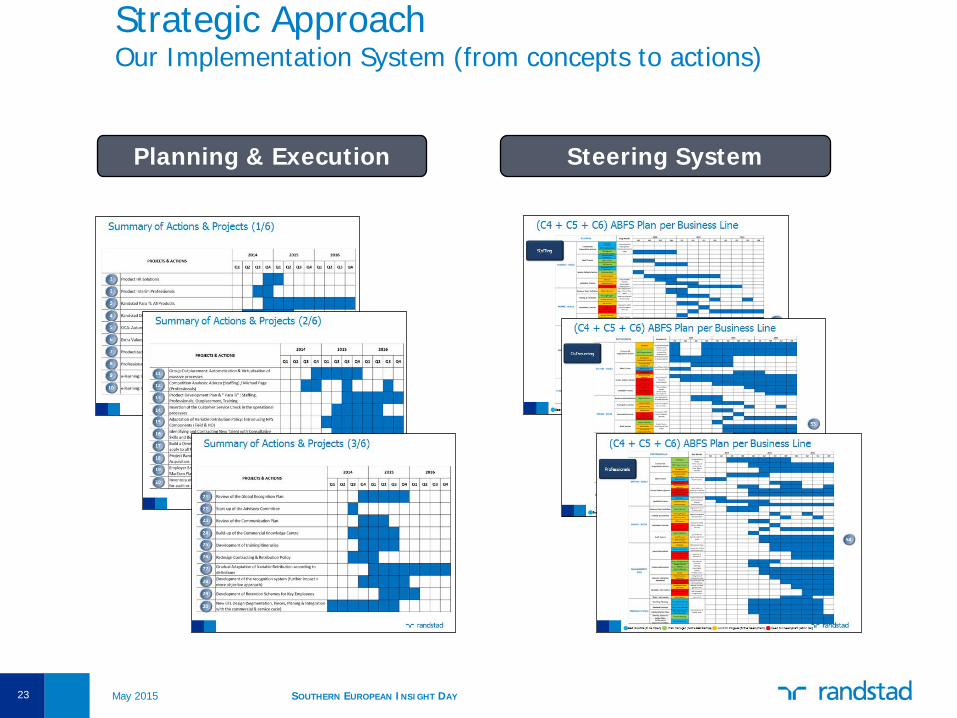

Strategic Approach Our Implementation System (from concepts to actions)

Planning & Execution Steering System

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 23

STI QR Code OCA Center (e-contracting)

24

Increase Capacity Tools for Internal Efficiency & SDMs Tools for Customer Service

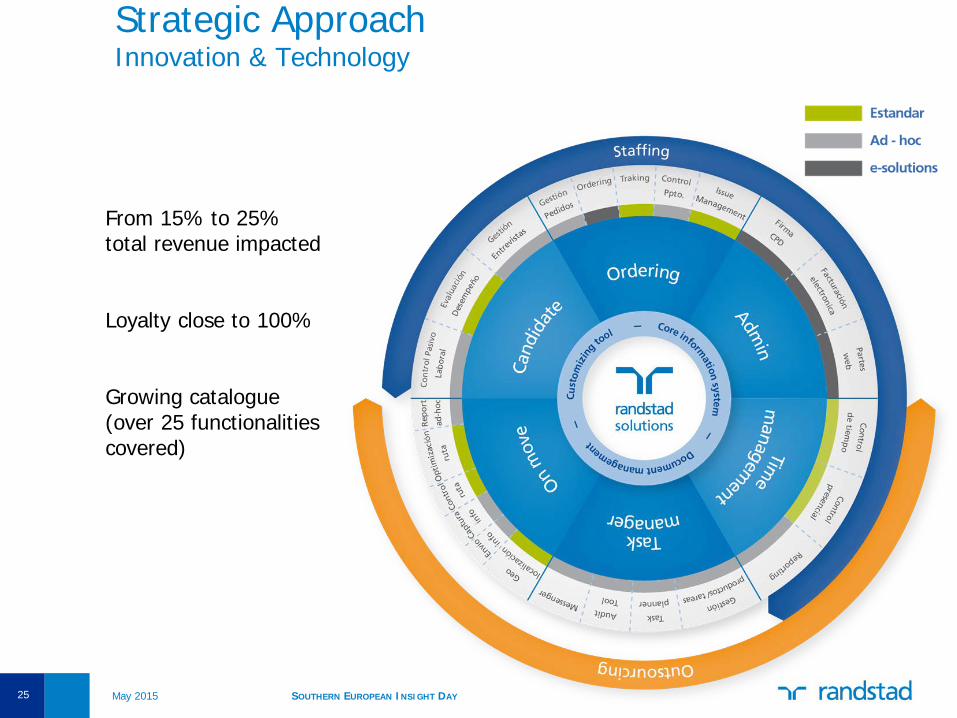

Strategic Approach Innovation & Technology

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Strategic Approach Innovation & Technology

From 15% to 25% total revenue impacted Loyalty close to 100% Growing catalogue (over 25 functionalities covered)

May 2015 SOUTHERN EUROPEAN INSIGHT DAY 25

Index

26

1

2

4

5

3

Economy & Labor Market

Legal Frame

HR Service Markets – Competitive Landscape

Our company

Next Steps

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Next Steps

27

1. Completing the Product Portfolio

2. Developing Consultative Knowledge Capacity

3. Widening ICT delivery capacity

4. Avoiding turnover of staff in the upper cycle

5. Finishing the implementation of the Outside-In approach

6. Adapting the distribution model

7. Developing our new SDMs for Staffing, Training & Perm

8. Leverage Cross-Selling

9. Reaching our profitability targets

10.Influencing the legal development

May 2015 SOUTHERN EUROPEAN INSIGHT DAY

Key Take Aways

28

1. Positive Economy trend sustainable – Competitive economy

2. Strong Potential of the market (Penetration rate + Economic Growth)

3. Reduced impact of potential legal changes

4. Concentration of the HR Markets

5. Good trend of Randstad to Total HR Service Supplier

6. Solid strategy and methodology of implementation and steering

May 2015 SOUTHERN EUROPEAN INSIGHT DAY