Embed Size (px)

Citation preview

FINANCIAL REPORTING

Rajeev Pai,Chief Financial Officer

JSW Steel Limited

Setting of Enterprise Resource Planning (ERP) based system and key challenges

Accounting Standards and Regulatory compliance and Challenges thereof

Reporting to owners / shareholders

Contents

Setting of ERP based Financial system and challenges

An ERP system is an attempt to integrate all functions

across a company to a single computer system to serve

all functions’ specific needs.

It provides integrated database and custom-designed

report systems.

It adopts a set of “best practices” for carrying out all

business processes.

What is ERP?

Integrated financial information

Integrated customer order information

Standardization and optimization of operational processes

Standardization of various information and report

Major Reasons for Adopting ERP

Internal Benefits◦ Integration of information enhances financial and internal

controls◦ A real-time system◦ Increased productivity and reduced operating costs◦ Improved internal communication◦ Foundation for future improvement

Benefits of ERP

External Benefits

◦ Improved customer service and order fulfillment

◦ Improved communication with suppliers and customers

◦ Enhanced competitive position

◦ Increased sales and profits

Benefits of ERP

Resistance to change Limitation on customization of ERP system due to

inconsistency with existing business processes Cost of implementation (hardware, software, training,

consulting) and maintenance Impact on organizational structure (front office vs. back

office, product lines, etc.) Interface to other software systems Implementation timelines Availability of internal technical knowledge and resources Education and training Implementation strategy and execution

Major Challenges to ERP Implementation

Accounting Standards (AS), Regulatory compliance and Key

Challenges

Why Accounting Standards?

- To harmonize the diverse accounting policies and practices in use in India

- To enables the users to interpret the reported information in a better way.

- Uniform adoption and disclosure of accounting policies

AS consists of detailed rules to be adopted for accounting treatment of various items before the presentation of financial statements.

Accounting Standards (AS)

Accounting Standards issued by ICAI

AS 1 to 15 1979 to 1995

AS 16 to 29

As 30 to 32

2000 to 2007 (7)

After 2007 (Yet to be notified)

Statutes e.g. Companies Act, etc. - Schedule VI, Companies (Accounting Standards) Rules, 2006, etc. SEBI / RBI Regulations , etc. Accounting Standard Board (ASB) of Institute of Chartered Accountants of

India (ICAI)◦ Framework◦ Accounting Standards (AS)◦ Accounting Standard Interpretations (ASI)◦ Guidance notes (GN)◦ Various accounting announcements ◦ Expert Advisory Opinion (EAC)◦ ICAI Technical Guides◦ ICAI Monographs◦ ICAI Research publications

Sources of Indian GAAP

Accounting Standards – ICAI -> NACAS Section 210A – Constitution of National Advisory Committee on

Accounting Standards (NACAS) Section 211

◦ P&L, Balance Sheet to comply with the Accounting Standards◦ Accounting Standards as may be prescribed by the Central

Government ◦ Till that time, standards issued by ICAI to be followed

Formation of NACAS Committee - Headed by Shri Y. H. Malegam as Chairman and representatives from various bodies viz. ICAI, ICSI, RBI, SEBI etc.

NACAS recommended Standards 1 to 7 and 9 to 29 (AS 8 – R&D part of AS 26)

IND-AS accounting standard equivalent to IFRS have been issued by NACAS in India however the adoption of these standards have been postponed.

Companies Act has amended the presentation of financials statements by issuing Revised Schedule VI for the financial years beginning from 1.4.2011. Revised Schedule VI has brought the disclosure of financial statements more or less in accordance with IFRS.

Accounting Standards (AS)

Other Regulatory compliances

Key Compliances:- Adoption of audited annual accounts at AGM and filing (XBRL)

thereof within 30 days of AGM- Maintenance of register under various section of the Companies Act

(example - register of investments, charges etc)- Filing of various forms with ROC (like appointment of directors,

allotment of shares etc)- Compliance with minimum number of board meetings, audit

committee (if applicable), shareholder meetings etc. and maintenance of various records thereof

- Defines power within which Board of directors to act upon- Cost Audit Report, if applicable, to be filed within 180 days from end

of financial year.

Companies Act :

Key Compliances:

- Transfer pricing – International & Domestic Transfer Pricing

- Tax audit and Filing of Annual Income Tax return

- Payment of Advance Tax

- TDS Compliance

Direct Tax

Transfer Pricing

19

Scope of International Transfer Pricing Regulations

Transfer Pricing

20

Transfer Pricing

• The process of determining what is the arm’s length price for a transaction (or a group of similar transactions)

What is Transfer Pricing Analysis

TP was earlier limited to ‘International Transactions’

The Finance Act 2012, extends the scope of TP provision to ‘Specified Domestic Transactions’ between related parties w.e.f. 1 April 2012

Obligation now on taxpayer to report/ document and substantiate the arm’s length nature of such transactions

Transfer Pricing - Domestic

22

Intent of Indian TP Regulations…(Domestic transactions)

Indian Co.Tax Holiday undertaking

Related Enterprise in Domestic Tariff Area

(DTA)

Shifting of expenses/losses

Shifting of income/profits

India

Tax Exemption

Tax Saving for the Group – Loss to Indian revenue

India

Tax @33.99%

Transfer Pricing - Domestic

23

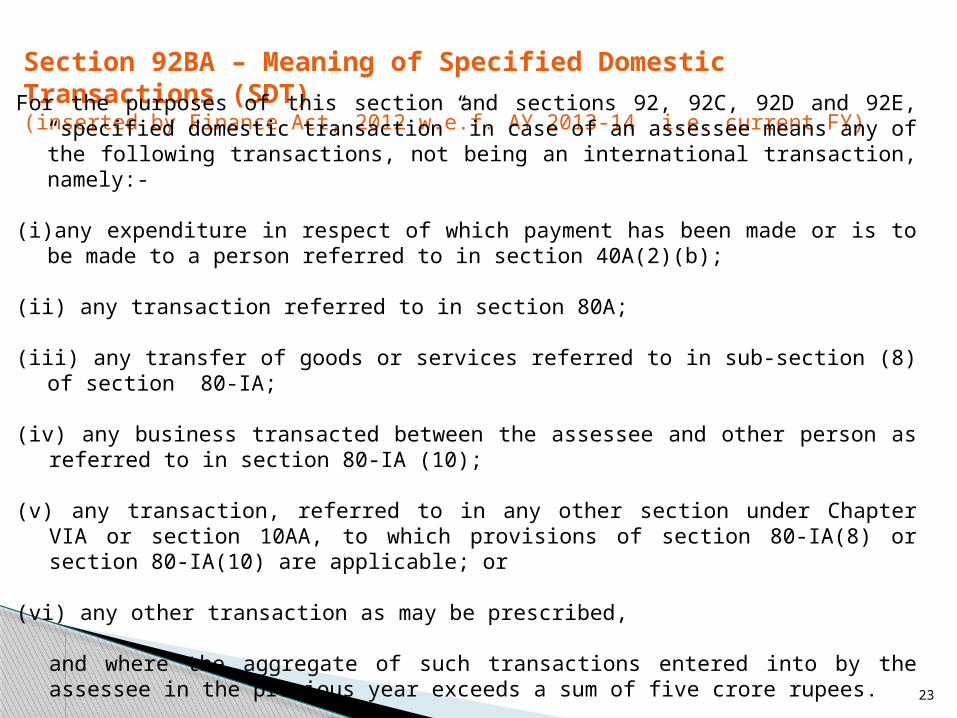

Section 92BA – Meaning of Specified Domestic Transactions (SDT)(inserted by Finance Act, 2012 w.e.f. AY 2013-14 i.e. current FY)

For the purposes of this section and sections 92, 92C, 92D and 92E, “specified domestic transaction” in case of an assessee means any of the following transactions, not being an international transaction, namely:-

(i) any expenditure in respect of which payment has been made or is to be made to a person referred to in section 40A(2)(b);

(ii) any transaction referred to in section 80A;

(iii) any transfer of goods or services referred to in sub-section (8) of section 80-IA;

(iv) any business transacted between the assessee and other person as referred to in section 80-IA (10);

(v) any transaction, referred to in any other section under Chapter VIA or section 10AA, to which provisions of section 80-IA(8) or section 80-IA(10) are applicable; or

(vi) any other transaction as may be prescribed,

and where the aggregate of such transactions entered into by the assessee in the previous year exceeds a sum of five crore rupees.

Transfer Pricing

• Computation of Arm’s Length Price by applying the ‘most appropriate’ method out of

– Comparable Uncontrolled Price (CUP)

– Resale Price Method (RPM)

– Cost Plus Method (CPM)

– Transaction Net Margin Method (TNMM)

– Profit Split Method (PSM)

25

Transfer Pricing – Domestic

Type of payments/ transactions Challenges• Salary and Bonuses paid to the

partners

• Remuneration paid to the Directors

• Transfer of land

• Joint Development agreements

• Project management fees

• Allocation of expenses between the same taxpayer having an eligible unit and non-eligible unit

• Definition of Related Party

• Benchmarking?• Whether the limit as mentioned in section

40 (b) would be the ALP?

• Benchmarking?• Whether the limit as mentioned in

Schedule XIII would be the ALP?

• Whether the rates mentioned in the ready reckoner be considered as ALP?

• Benchmarking?

• Benchmarking?

• Whether these allocation would be SDT – Sec 80-IA(10)?

• Directly v/s Indirectly

Challenges

Key Compliances• Service Tax – Applicable on all services except negative list

• Excise Duty – Applicable on goods manufactured

• Custom Duty – Applicable on import of goods

• Sales Tax/VAT – Applicable on Sale of goods (inter state and intra state)

Compliance includes timely filing of returns, payment of taxes etc

Indirect Tax

Payment of Service Tax

- by 5th of succeeding month

- For March month by 31st March

ST 3 Returns has to be e-filed half-yearly

27

Service Tax

Period Due Date

April to September 25th October

October to March 25th April

Form Description Who is require to file Time limit

ER-1 Monthly return by large units

Manufacturers not eligible for SSI concession

10th of following mth.

ER-2 Return by EOU EOU units 10th of following mth.

ER-3 Quarterly return by SSI Assesses availing SSI concession

20th of following qtr.

ER-4 Annual financial information statement

Assesses paying duty of Rs. One crore or more per annum through PLA .

Annually, by 30th Nov. of succeeding year.

ER-5 Information relating to principal inputs

Assesses paying duty of Rs. One crore or more per annum through PLA and manufacturing goods under specified tariff heading

Annually, by 30th April of current year.

ER-6 Monthly return of receipts & consumption of each of Principal Inputs

Assesses who is required to submit ER-5 return

10th of following month

ER-7 Annual Install capacity statement

All assessee Annually on or before 30th April.

28

Excise duty : Periodical returns

SEBI Act (Applicable to listed entities )

- Corporate Governance Report (Clause 49)- Quarterly standalone and consolidated financial statements (clause

41)- Shareholding pattern (Clause 35)

Others

- Compliance with respect to compliance with Factories Act and other applicable labor legislations.

- Compliance with Foreign Exchange Management Act.- Compliance with Environment Laws.- Compliance with Employers Provident Fund and Miscellaneous

Provisions Act, 1952, Payment of Bonus Act, Payment of Gratuity Act etc.

Other Regulatory compliances

- Ensuring that the financials are prepared in accordance with the measurement and disclosures requirement of accounting standards

- Various Assumptions made in preparation of financial statements

- Frequent changes in rules and regulations

- Multiple Acts/ regulators increase cost of compliance and litigations. For example in case indirect tax, tax is levied at various instances such excise on manufactured, service tax on services and VAT/Sales Tax on sale of goods which can be substituted by a single act like Goods and Service Tax (GST) Act. Govt. of India is already contemplating for implementation of the same.

Key Challenges:

To submit annual report containing Corporate Governance, Business Sustainability Report, Management Discussion and Analysis alongwith audited financial statements.

Intimation to shareholders on key updates through press release, advertisement in newspapers etc

Maintenance and making available to shareholders of various statutory registers and documents as defined under various laws.

Reporting to owners / shareholders

Voluntary disclosures like

◦ Guidance on profitability of the company ◦ Current status and key updates to Investor and

Analyst through meet.

Reporting to owners / shareholders

Thank You.