Embed Size (px)

Citation preview

Queensland region construction

supply and demand analysis:

1995-2026 and quarterly

indicators to June 2018

A report for the

DEPARTMENT OF HOUSING AND PUBLIC WORKS

Prepared by the

National Institute of Economic and Industry Research (NIEIR)

ABN: 72 006 234 626

416 Queens Parade, Clifton Hill, Victoria, 3068

Telephone: (03) 9488 8444; Facsimile: (03) 9482 3262

Email: [email protected]

July 2016

PJB1197-QDH&PW-Annual report/QldDPW/2016/July

While the National Institute endeavours to provide reliable forecasts and believes the material is accurate it will not be liable for any claim by any party acting on such information.

Contents

Page no.

Executive summary i

1. Introduction 1

2. The economic outlook for the world, Australia and Queensland 2

2.1 The world economy 2 2.2 The Australian economic outlook 4 2.3 The Queensland economic outlook 11 2.4 Queensland housing affordability 15

3. Queensland construction activity in the Australian context 23

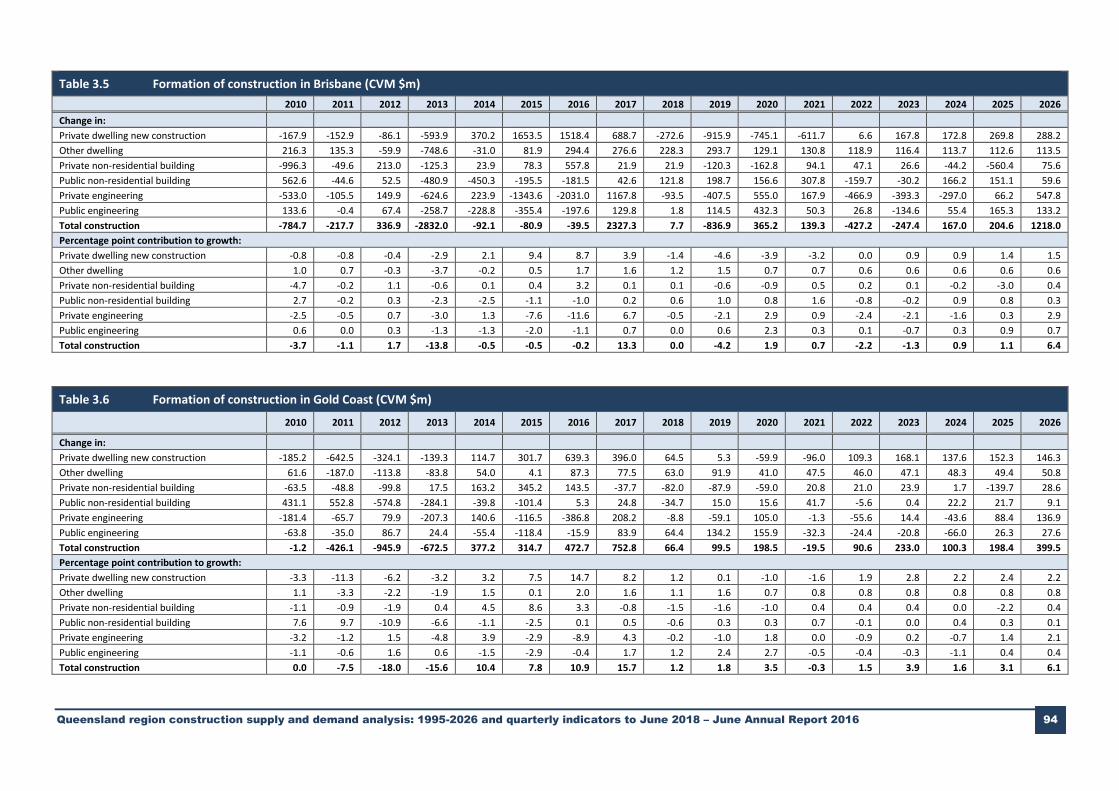

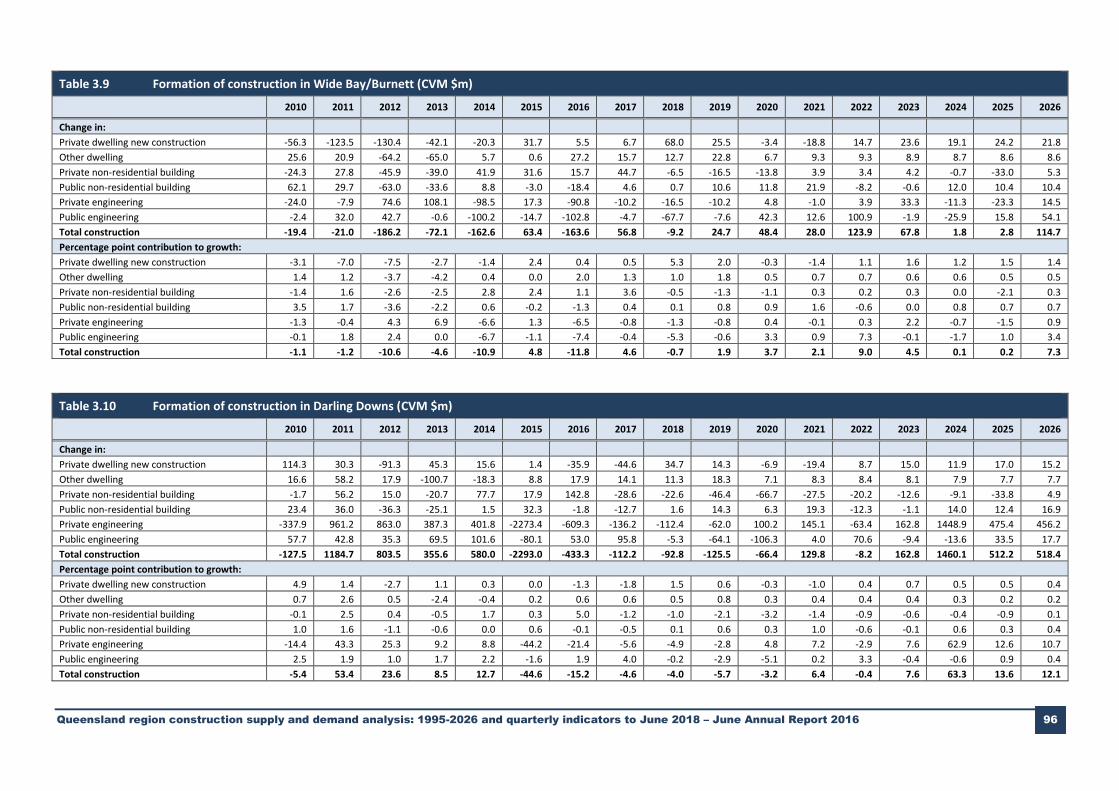

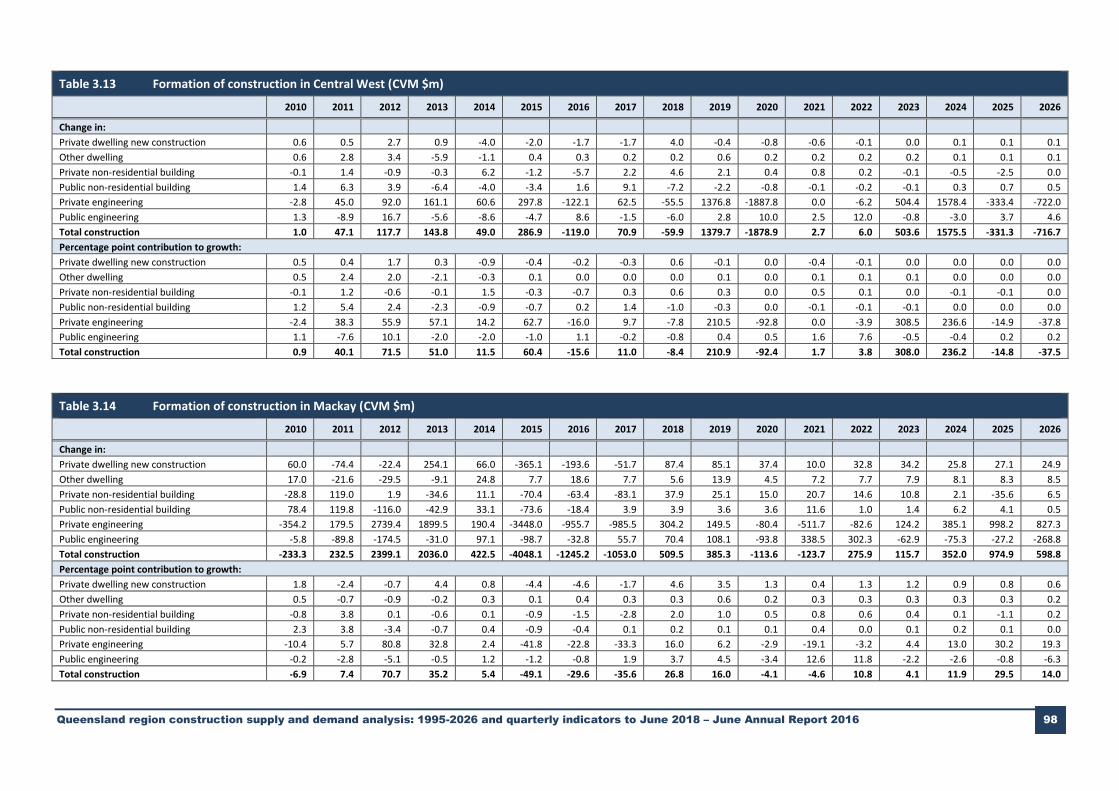

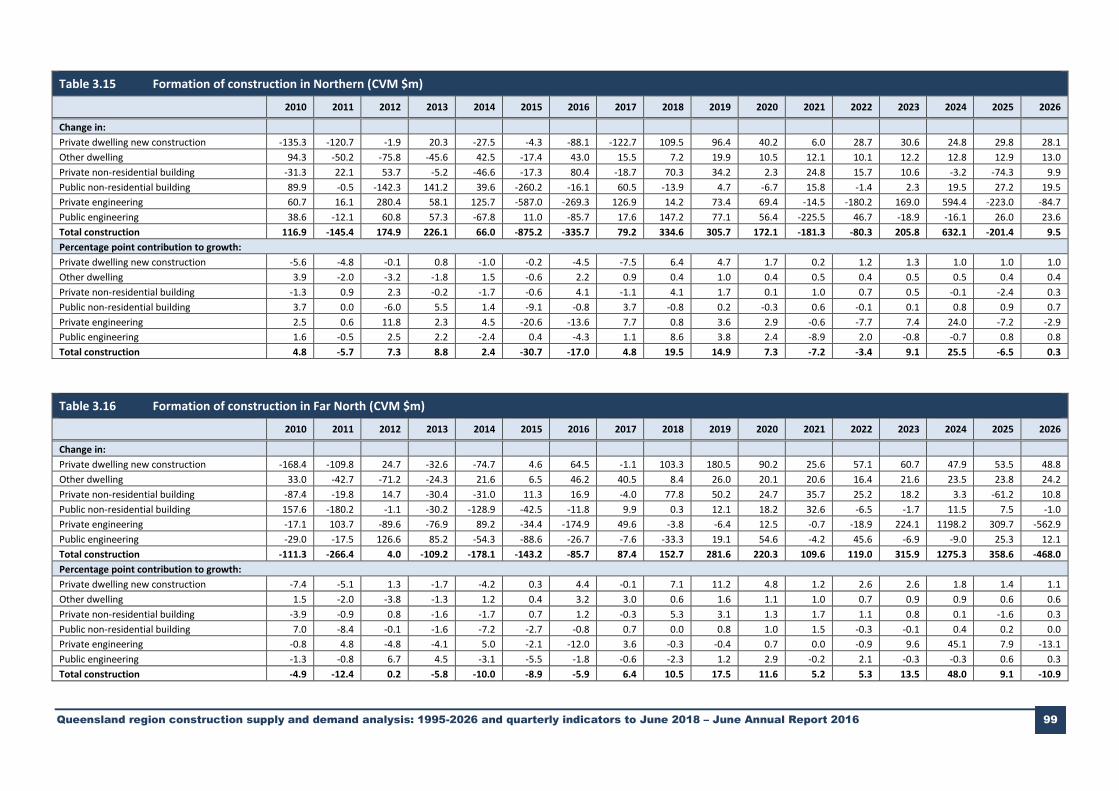

3.1 Queensland construction: The headline outcomes 23 3.2 Total construction: A comparison with last year’s Annual Report 23 3.3 The Queensland dwelling market 24 3.3.1 New dwelling construction 24 3.3.2 Other dwelling expenditure 24 3.3.3 Total Queensland private dwelling construction expenditures 24 3.3.4 Dwelling commencements 25 3.4 Non-residential building 28 3.4.1 Private non-residential building 28 3.4.2 Public non-residential building activity 30 3.4.3 Major Queensland non-residential building projects 31 3.4.4 Total non-residential building activity 32 3.5 Engineering construction 32 3.5.1 Engineering: The segment drivers 33 3.5.2 Mining investment and output 33 3.5.3 Engineering construction: The outlook 33 3.5.4 Major Queensland engineering projects 36 3.6 Queensland’s construction share of total Australian construction 38 3.7 The regional dimension 47 3.7.1 Brisbane 47 3.7.2 Gold Coast 50 3.7.3 Sunshine Coast 54 3.7.4 West Moreton 58 3.7.5 Wide Bay/Burnett 61 3.7.6 Darling Downs 65 3.7.7 South West 69 3.7.8 Fitzroy 72 3.7.9 Central West 76 3.7.10 Mackay 79 3.7.11 Northern 83 3.7.12 Far North 86 3.7.13 North West 90

Contents (cont.)

Page no.

4. Queensland construction: Resources, capacity and price pressures 103

4.1 Utilisation of capacity 103 4.2 Labour shortages 103 4.3 Queensland construction sector unemployment rates 103 4.4 Construction cost inflation 104

5. Quarterly profiles 111

Appendix A: Additional annual tables 120

Appendix B: Additional quarterly tables 133

List of tables

Page no.

E.1 Australia and Queensland gross product and construction activity indicators vi E.2 Annual growth and % contribution to construction activity by major construction segment vi E.3 Construction activity by Queensland region vii E.4 Share of total construction activity by Queensland region vii E.5 Total construction – average annual growth rates by Queensland regions viii E.6 Drivers of construction growth by Queensland region 2012-2023 viii E.7 Shortage of construction labour by Queensland region ix E.8 Queensland construction industry – real quarterly price growth at annual rates ix

2.1 Australian economy: Population and labour market 8 2.2 Australian economy: Formation of real GDP – Demand side 9 2.3 Australian economy: Commodity prices, terms of trade and the balance of payment 10 2.4 Formation of Queensland Gross State Product 12 2.5 Formation of Queensland population 14 2.6 Average annual population change by region 15 2.7 Housing affordability – Brisbane City 16 2.8 Housing affordability – Gold Coast 17 2.9 Housing affordability – West Moreton 17 2.10 Housing affordability – Logan Redland 18 2.11 Housing affordability – Moreton Bay 18 2.12 Housing affordability – Sunshine Coast 19 2.13 Housing affordability – Darling Downs South West 19 2.14 Housing affordability – Far North Torres 20 2.15 Housing affordability – Fitzroy Central West 20 2.16 Housing affordability – Mackay 21 2.17 Housing affordability – Townsville North West 21 2.18 Housing affordability – Wide Bay Burnett 22

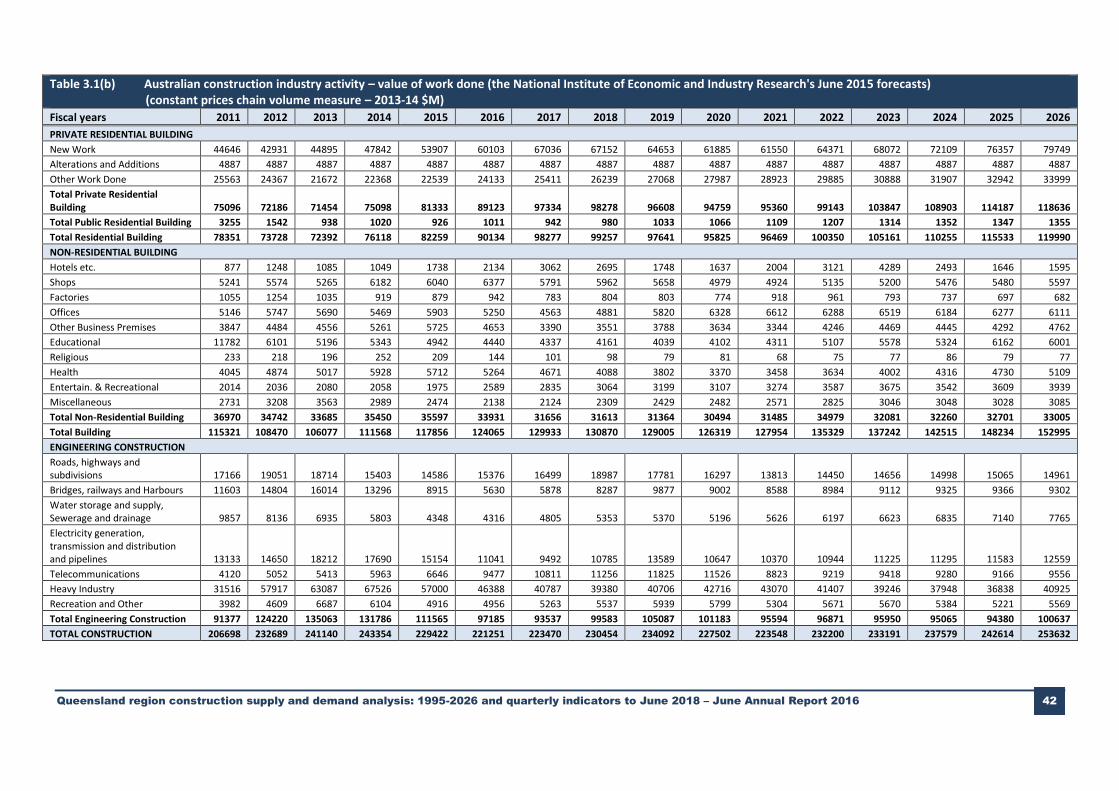

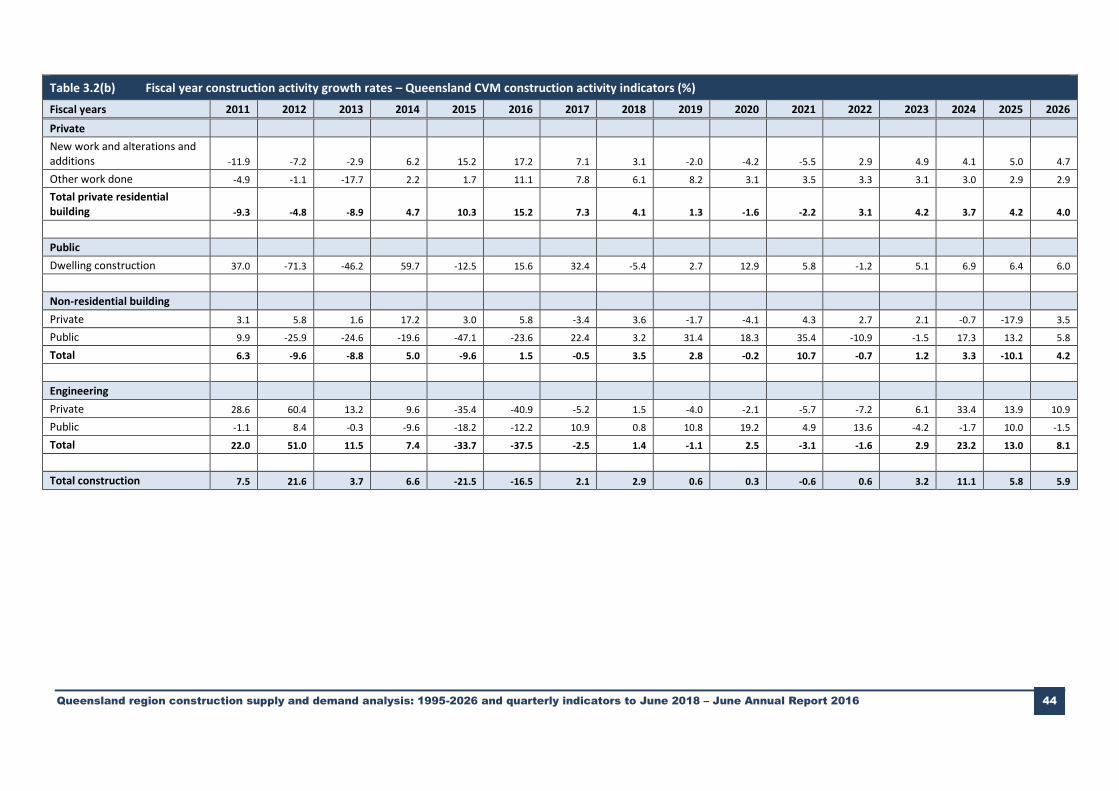

3.1(a) Australia and Queensland construction industry activity 41 3.1(b) Australian construction industry activity 42 3.2(a) Queensland construction industry activity 43 3.2(b) Fiscal year construction activity growth rates – Queensland CVM construction activity indicators 44 3.2(c) Fiscal year construction activity indicator contribution to total Queensland construction growth rate 45 3.3 Annual growth and % contribution to Queensland construction activity by major construction segment 46 3.4 Sector contribution to Queensland engineering construction growth 46 3.5 Formation of construction in Brisbane 94 3.6 Formation of construction in Gold Coast 94 3.7 Formation of construction in Sunshine Coast 95 3.8 Formation of construction in West Moreton 95 3.9 Formation of construction in Wide Bay/Burnett 96

List of tables (cont’d)

Page no.

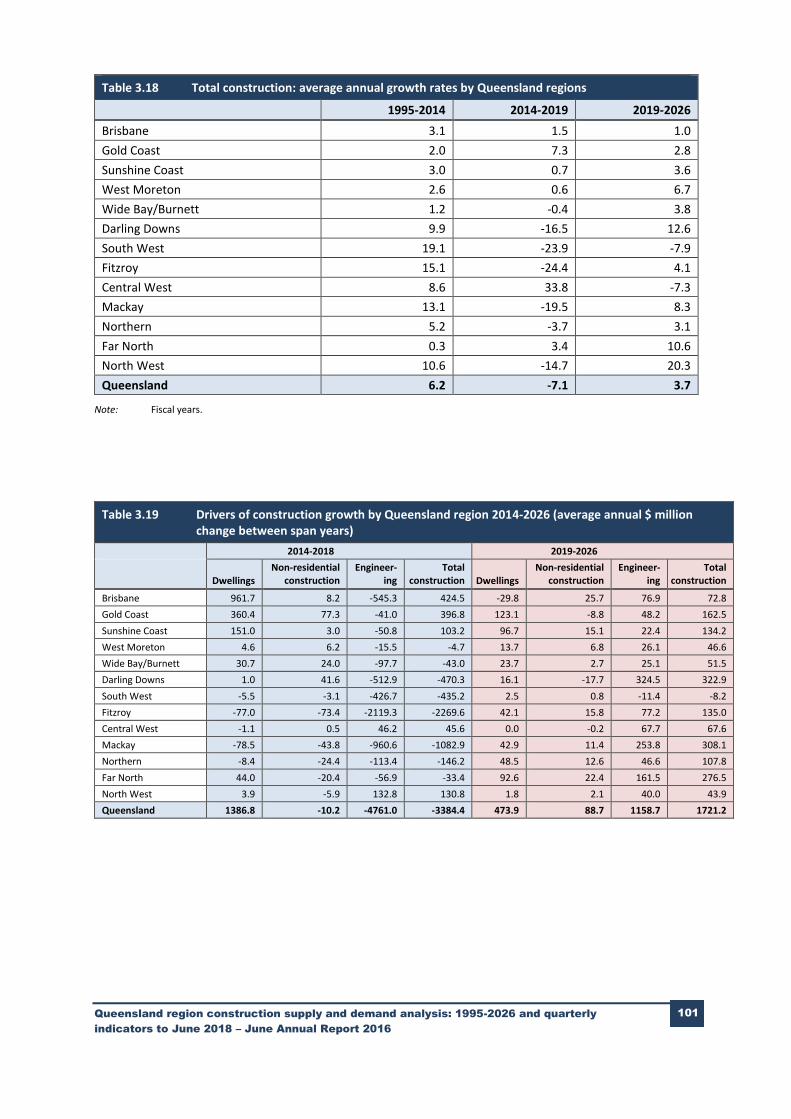

3.10 Formation of construction in Darling Downs 96 3.11 Formation of construction in South West 97 3.12 Formation of construction in Fitzroy 97 3.13 Formation of construction in Central West 98 3.14 Formation of construction in Mackay 98 3.15 Formation of construction in Northern 99 3.16 Formation of construction in Far North 99 3.17 Formation of construction in North West 100 3.18 Total construction: average annual growth rates by Queensland regions 101 3.19 Drivers of construction growth by Queensland region 2012-2023 101 3.20 Contribution of each region to Queensland construction growth 102

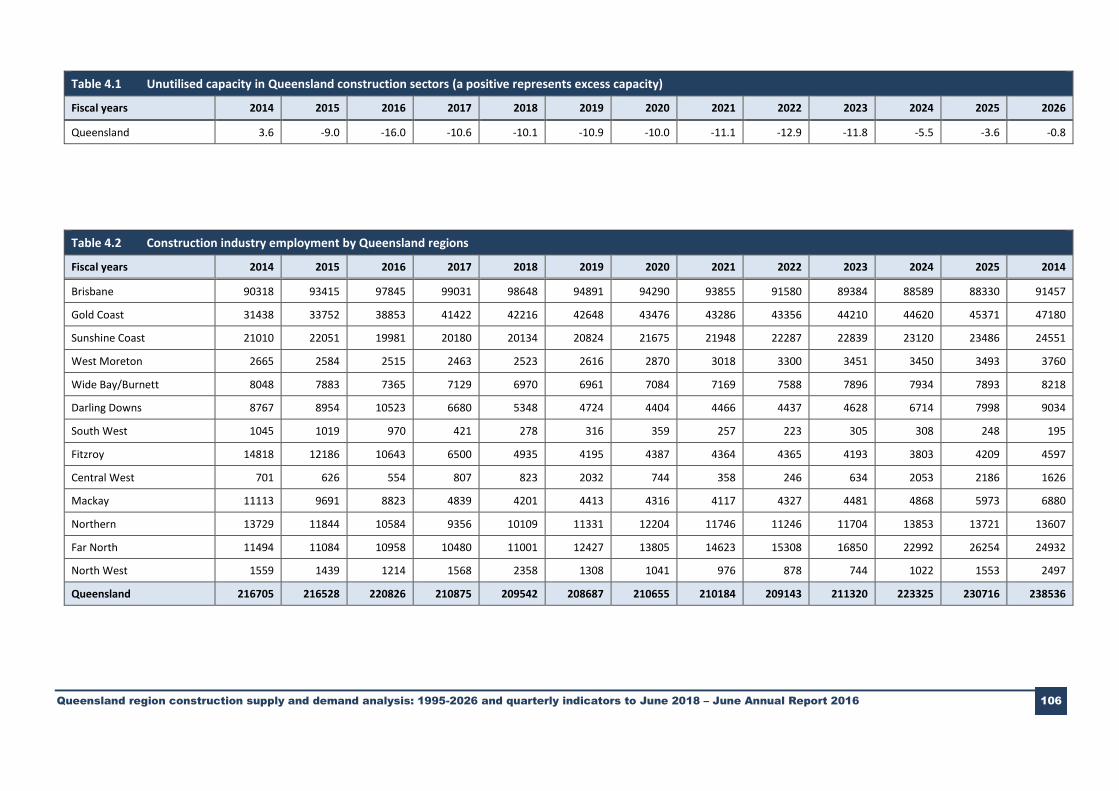

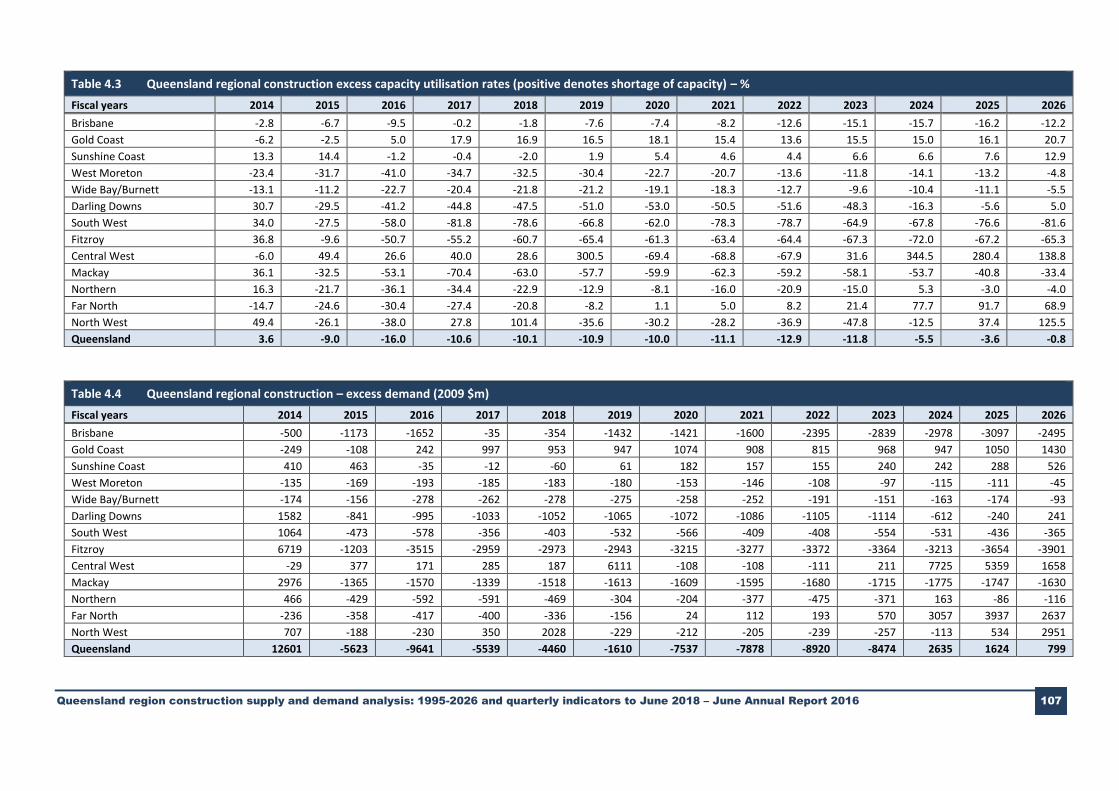

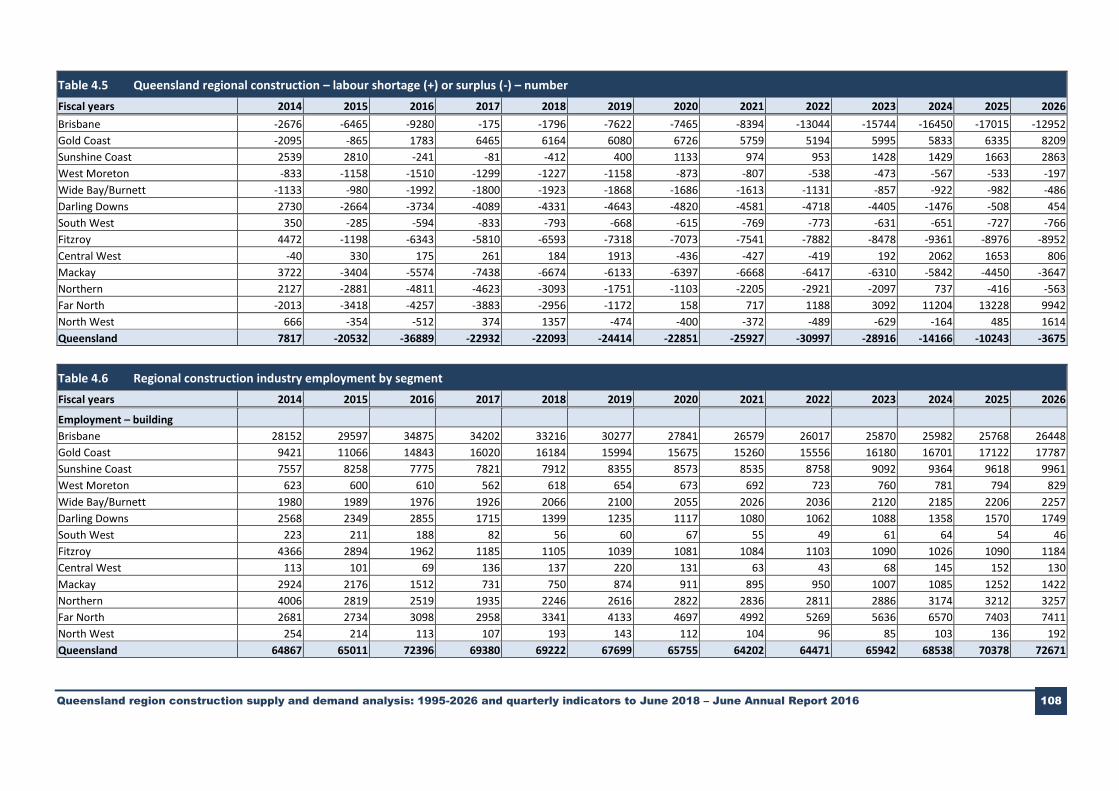

4.1 Unutilised capacity in Queensland construction sectors 106 4.2 Construction industry employment by Queensland regions 106 4.3 Queensland regional construction excess capacity utilisation rates 107 4.4 Queensland regional construction – excess demand 107 4.5 Queensland regional construction – labour shortage (+) or surplus (–) 108 4.6 Regional construction industry employment by segment 108

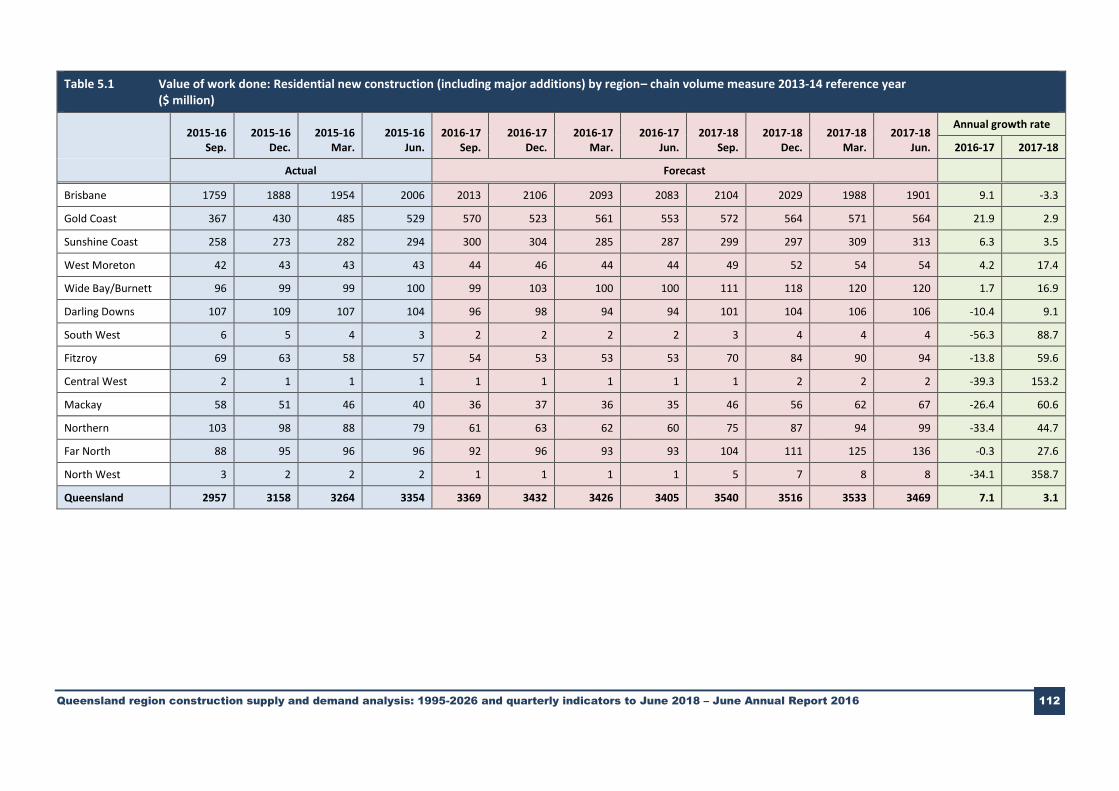

5.1 Value of work done: Residential new construction (including major additions) by region 112 5.2 Value of work done: Non-residential building by region 113 5.3 Value of work done: Residential other renovations by region 114 5.4 Value of work done: Residential building by region 115 5.5 Value of work done: Total engineering construction activity by region 116 5.6 Value of work done: Total construction activity by region – chain volume measure 2012-13 reference year ($ million) 117 5.7 Value of work done: Total construction activity by region – chain volume measures 2012-13 reference year – Qtr. 3 2014-15 = 100 118 5.8 Queensland construction industry 119 5.9 Shortage of construction labour by Queensland region 119

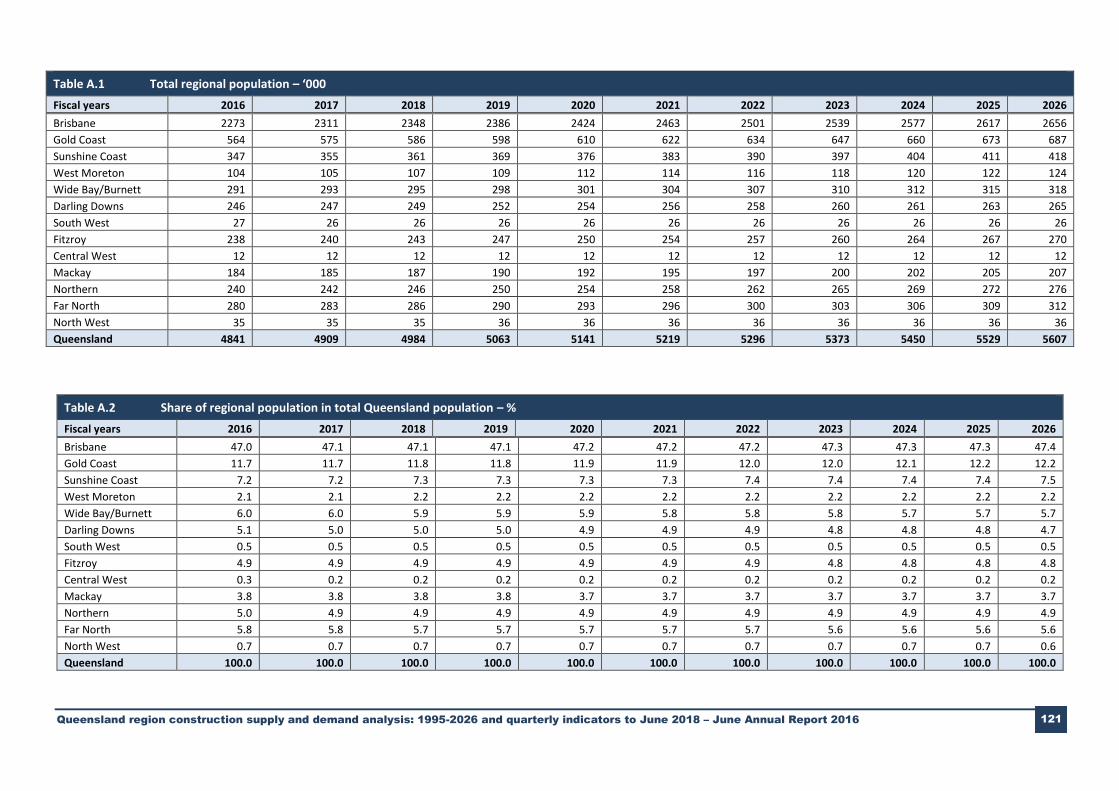

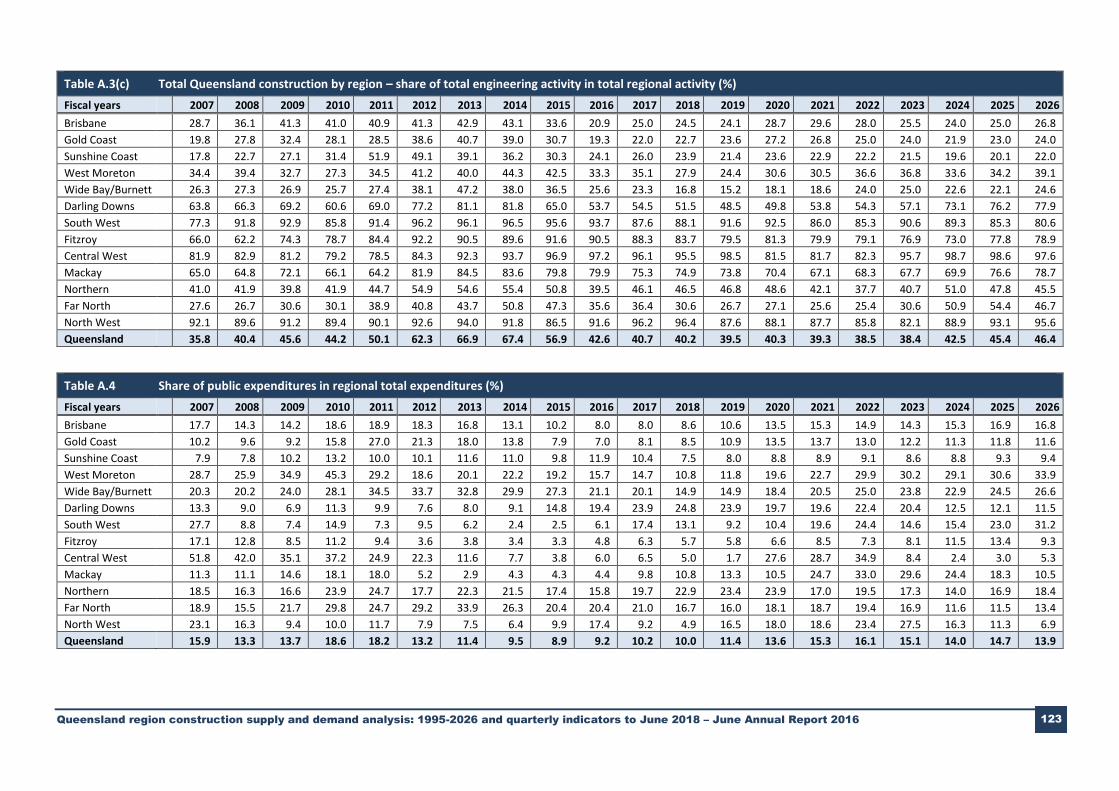

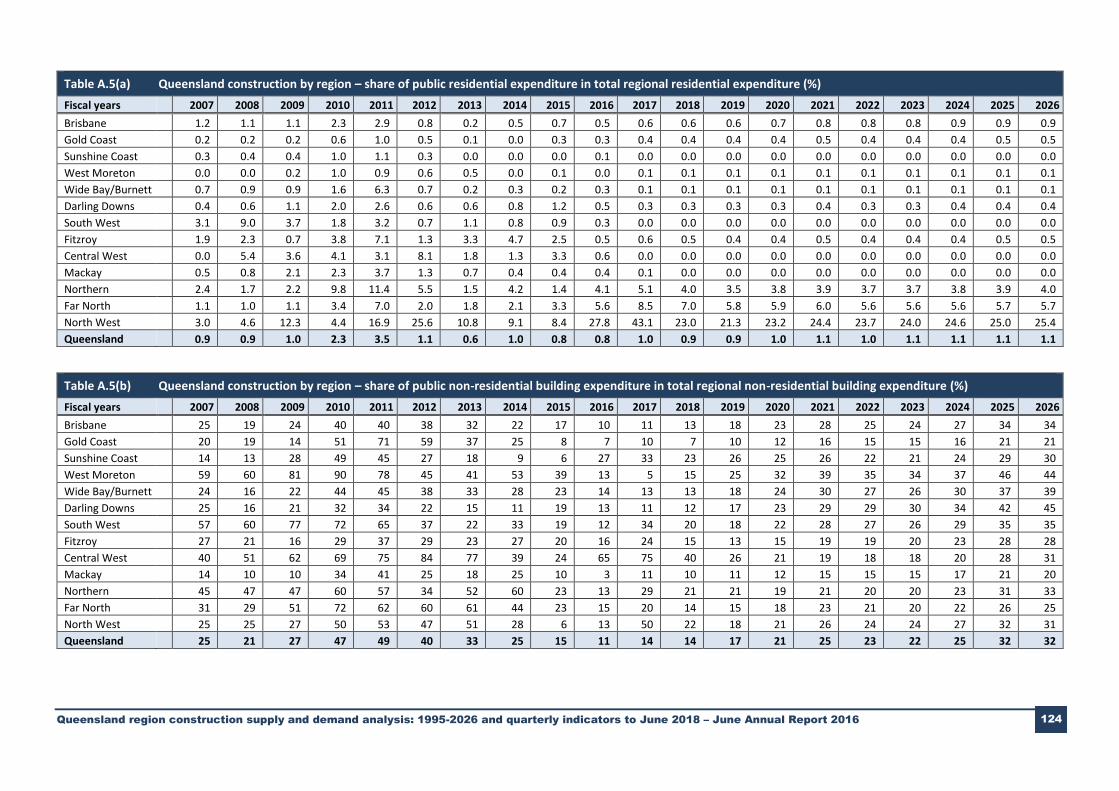

A.1 Total regional population 121 A.2 Share of regional population in total Queensland population 121 A.3(a) Total Queensland construction by region – share of residential activity in total regional activity 122 A.3(b) Total Queensland construction by region – share of non-residential activity in total regional activity 122 A.3(c) Total Queensland construction by region – share of total engineering activity in total regional activity 123 A.4 Share of public expenditures in regional total expenditures 123 A.5(a) Queensland construction by region – share of public residential expenditure in total regional residential expenditure 124 A.5(b) Queensland construction by region – share of public non-residential building expenditure in total regional non-residential building expenditure 124

List of tables (cont’d)

Page no.

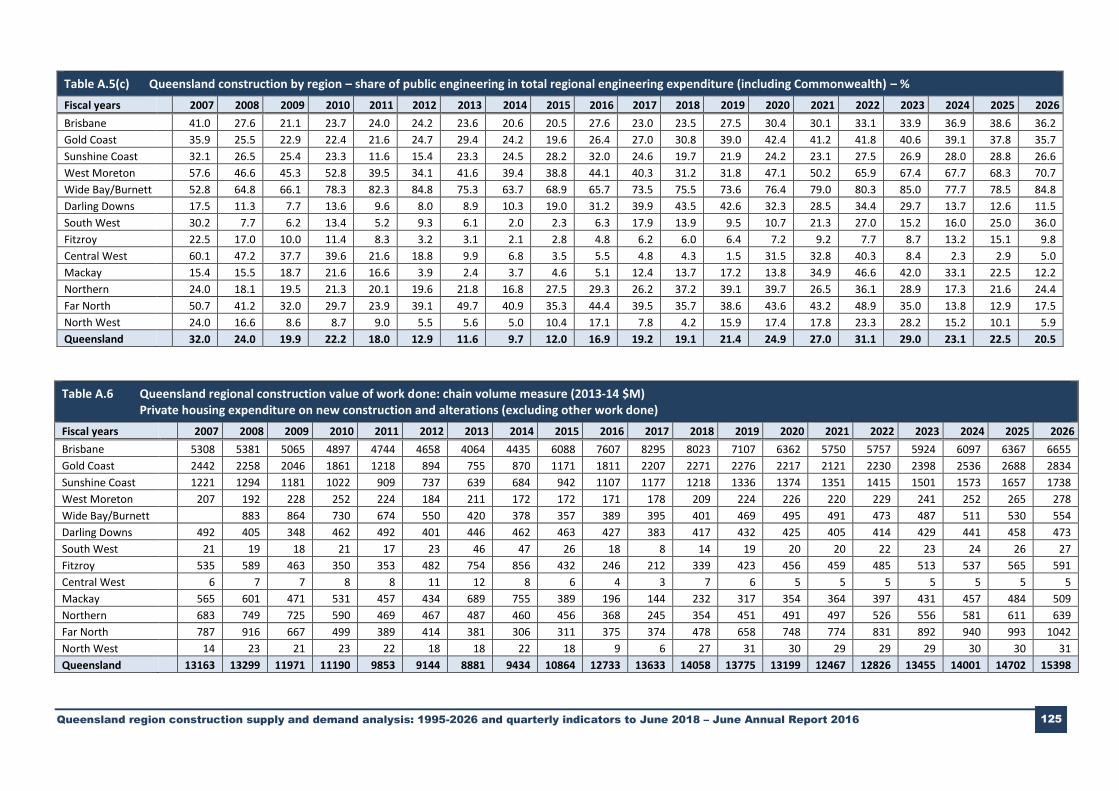

A.5(c) Queensland construction by region – share of public engineering in total regional engineering expenditure (including Commonwealth) 125 A.6 Queensland regional construction value of work done: chain volume measure – Private housing expenditure on new construction and alterations (excluding other work done) 125 A.7 Queensland regional construction value of work done: chain volu28 measure – Public housing 126 A.8 Queensland regional construction value of work done: chain volume measure – Non-residential building private 126 A.9 Queensland regional construction value of work done: chain volume measure – Non-residential building public 127 A.10 Queensland regional construction value of work done: chain volume measure – Private engineering 127 A.11 Queensland regional construction value of work done: chain volume measure – Public engineering 128 A.12 Queensland regional construction value of work done: chain volume measure – Non-residential building total 128 A.13 Queensland regional construction value of work done: chain volume measure – Engineering total 129 A.14 Queensland regional construction value of work done: chain volume measure – Total residential (excluding other work done) 129 A.15 Queensland regional construction value of work done: chain volume measure – Total public sector engineering (including Commonwealth) 130 A.16 Queensland regional construction value of work done: chain volume measure – Private residential (other work done) 130 A.17 Queensland regional construction value of work done: chain volume measure – Total construction 131 A.18 Queensland regional construction value of work done: chain volume measure – Total construction expenditure share of State total 131 A.19 Queensland regional dwelling units commenced – Total residential units 132

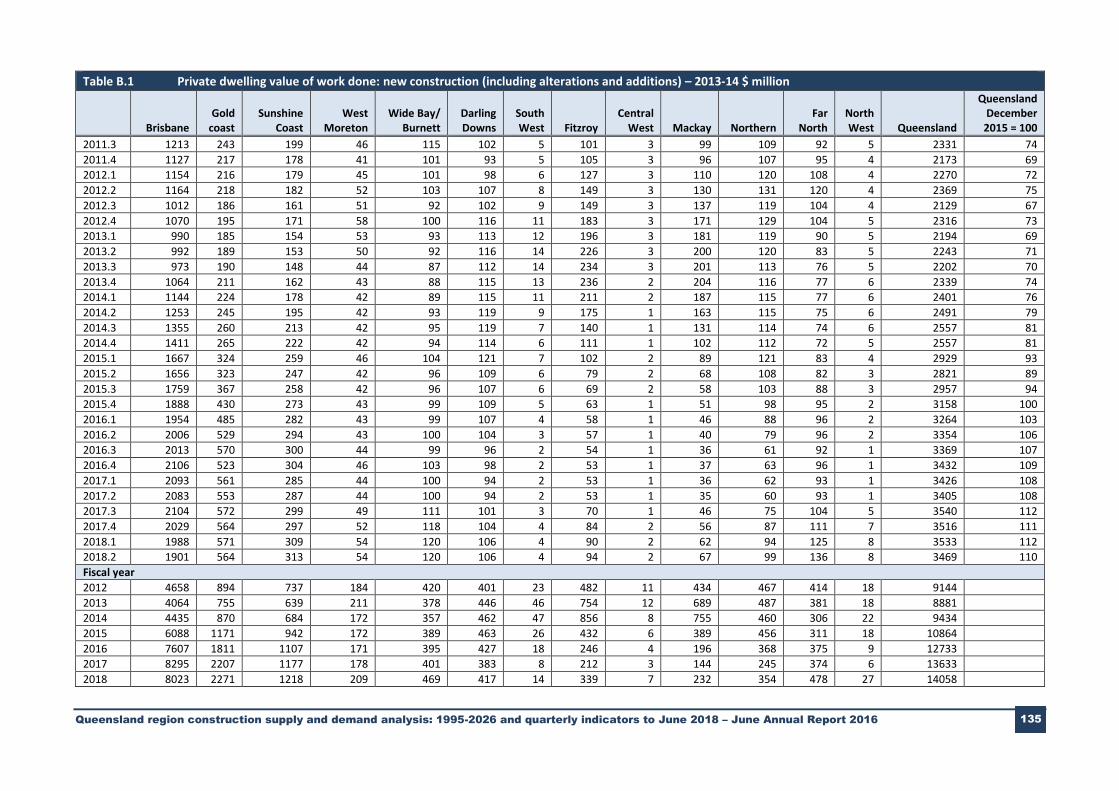

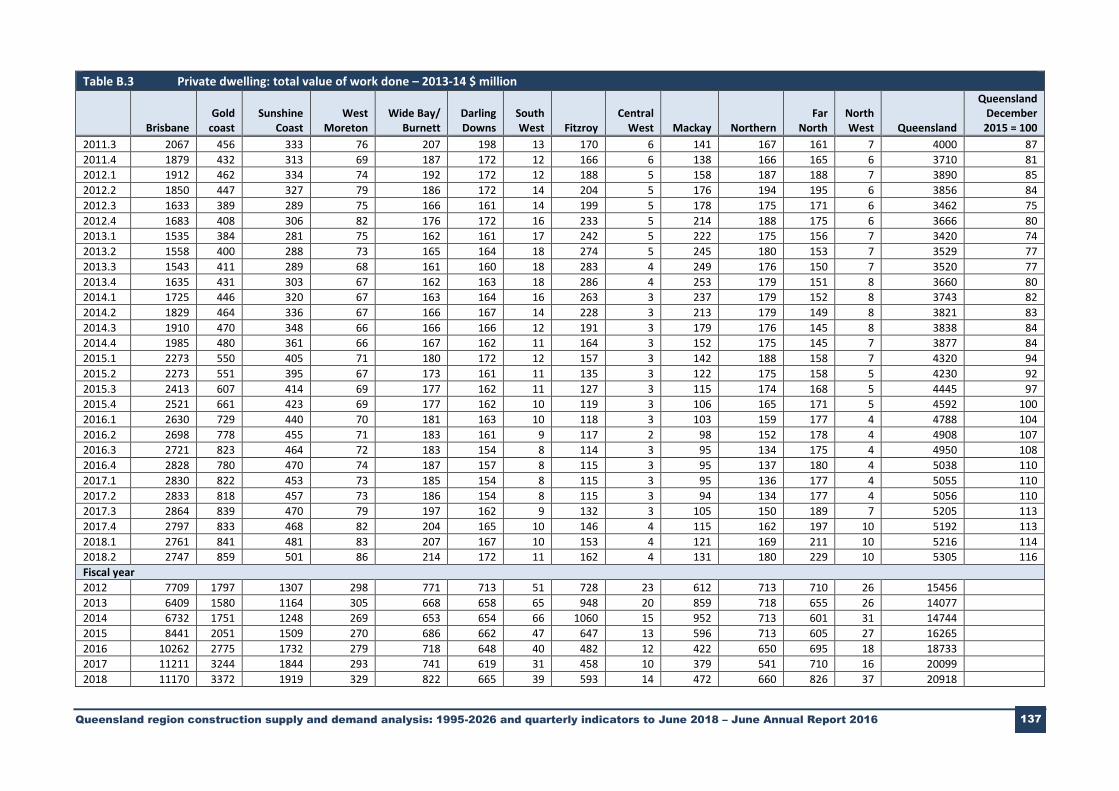

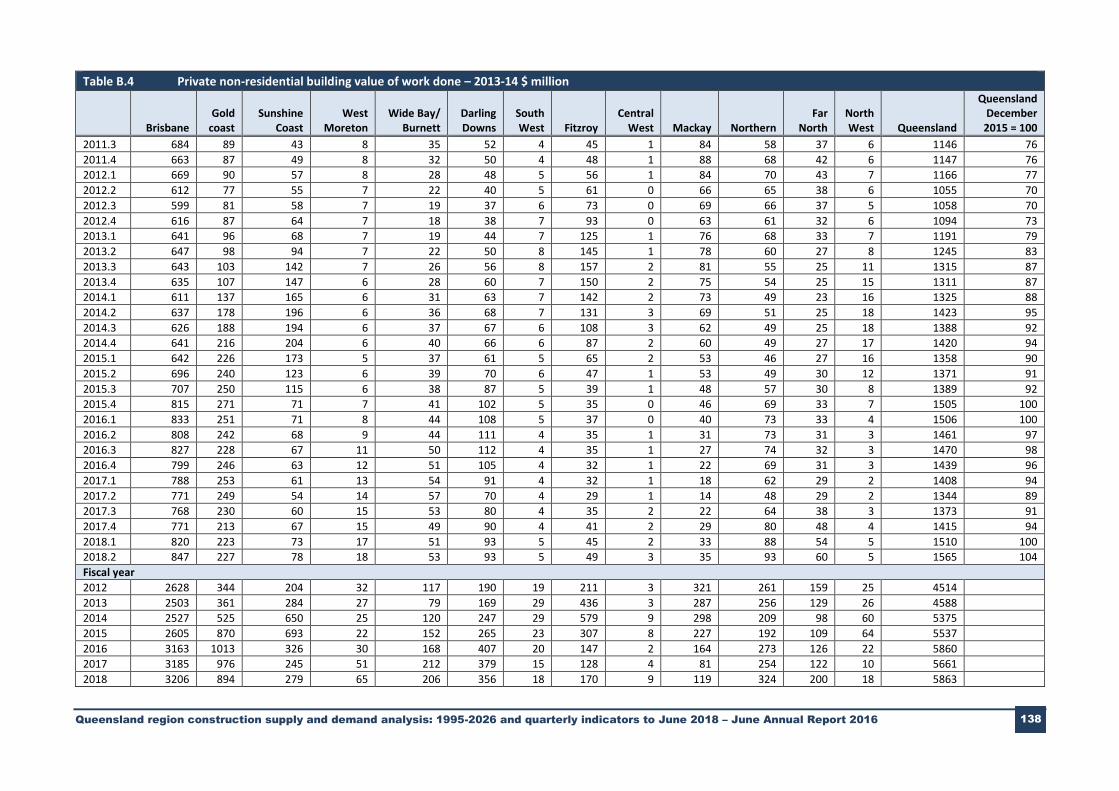

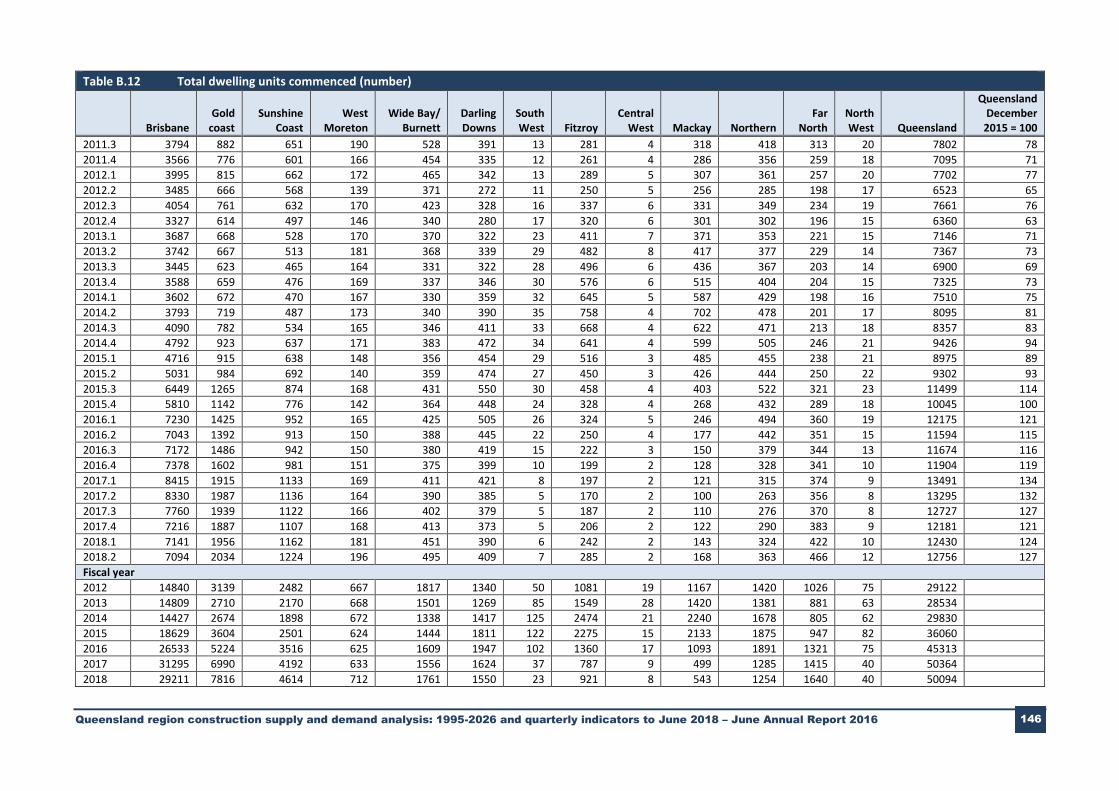

B.1 Private dwelling value of work done: new construction (including alterations and additions) 134 B.2 Private dwelling: other value of work done 135 B.3 Private dwelling: total value of work done 136 B.4 Private non-residential building value of work done 137 B.5 Public non-residential building value of work done 138 B.6 Total non-residential building value of work done 139 B.7 Public sector engineering value of work done 140 B.8 Private sector engineering value of work done 141 B.9 Total engineering value of work done 142 B.10 Public dwelling value of work done 143 B.11 Total construction: value of work done 144 B.12 Total dwelling units commenced 145

List of tables (cont’d)

Page no.

C.1 New residential dwelling construction by LGA 148 C.2 Housing affordability by LGA: Average established dwelling price 151 C.3 Housing affordability by LGA: Average household income from labour market 153 C.4 Housing affordability by LGA: Ratio of average mortgage costs on established dwellings to average household catchment income 155 C.5 Housing affordability by LGA: Ratio of average mortgage costs on new dwellings to average household catchment income 157

List of figures

Page no.

E.1 Australian GDP and Queensland GSP v

2.1 World GDP growth rate 4 2.2 Australia’s international borrowing requirement 6 2.3 Australia – Real GDP growth rate 7

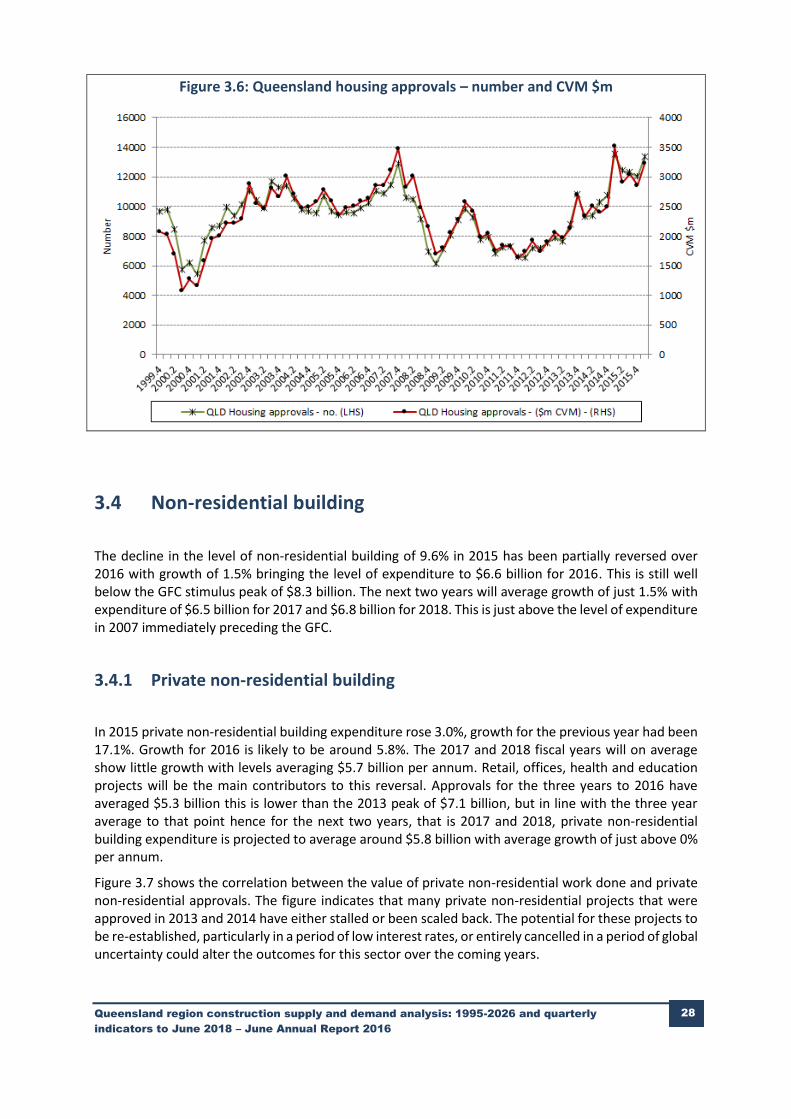

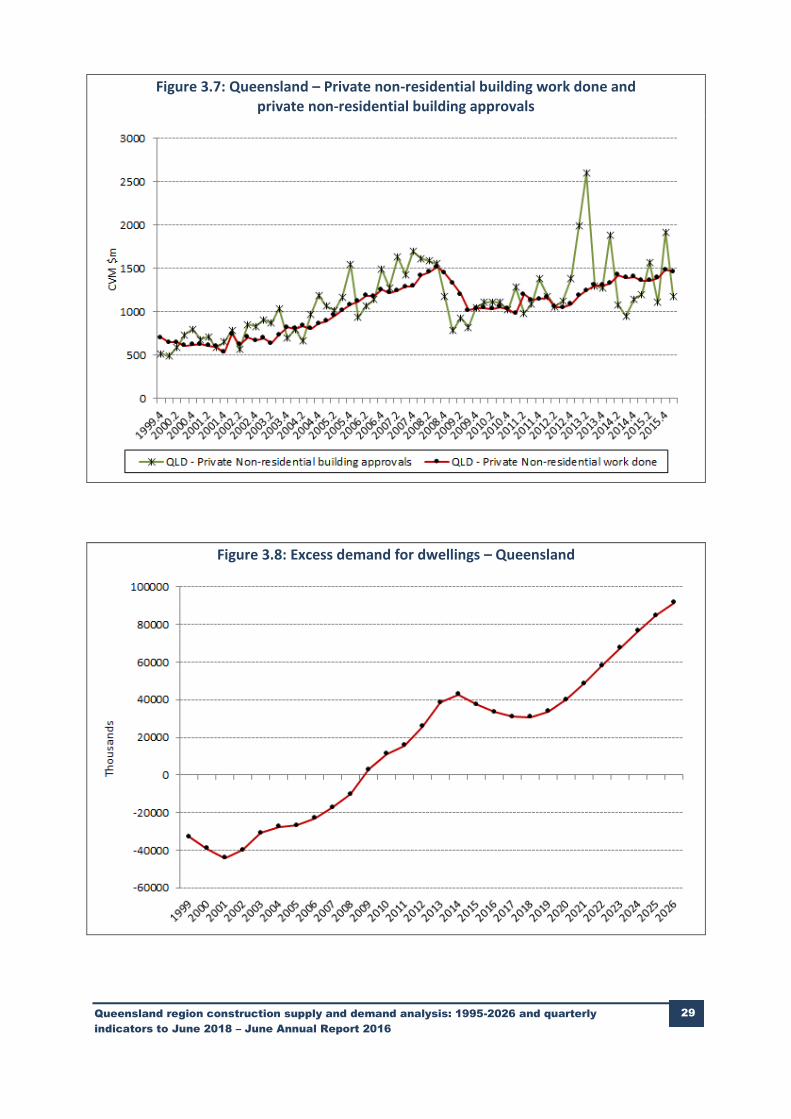

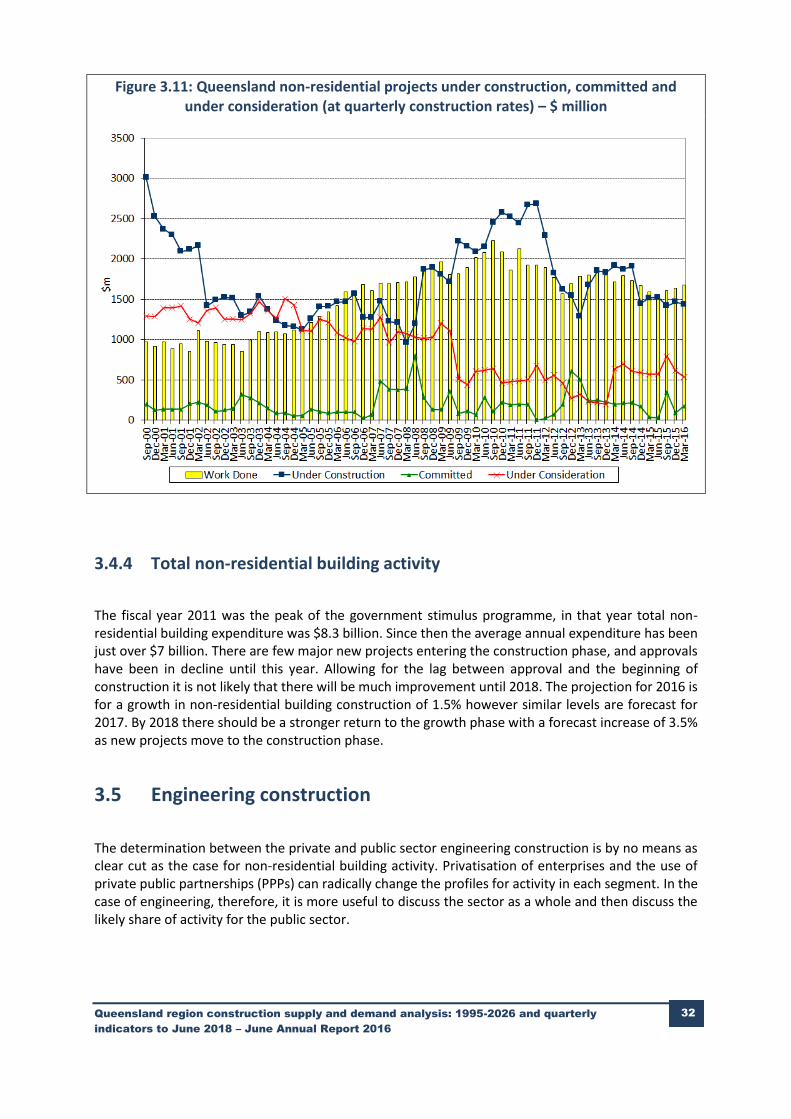

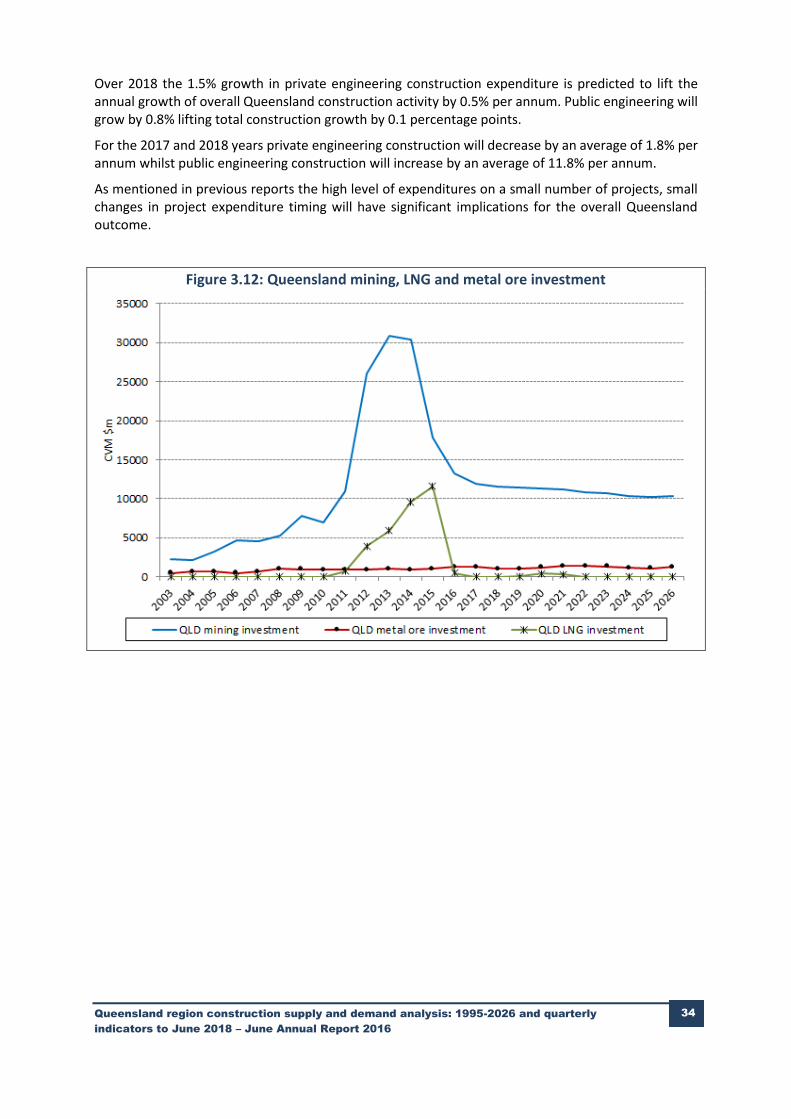

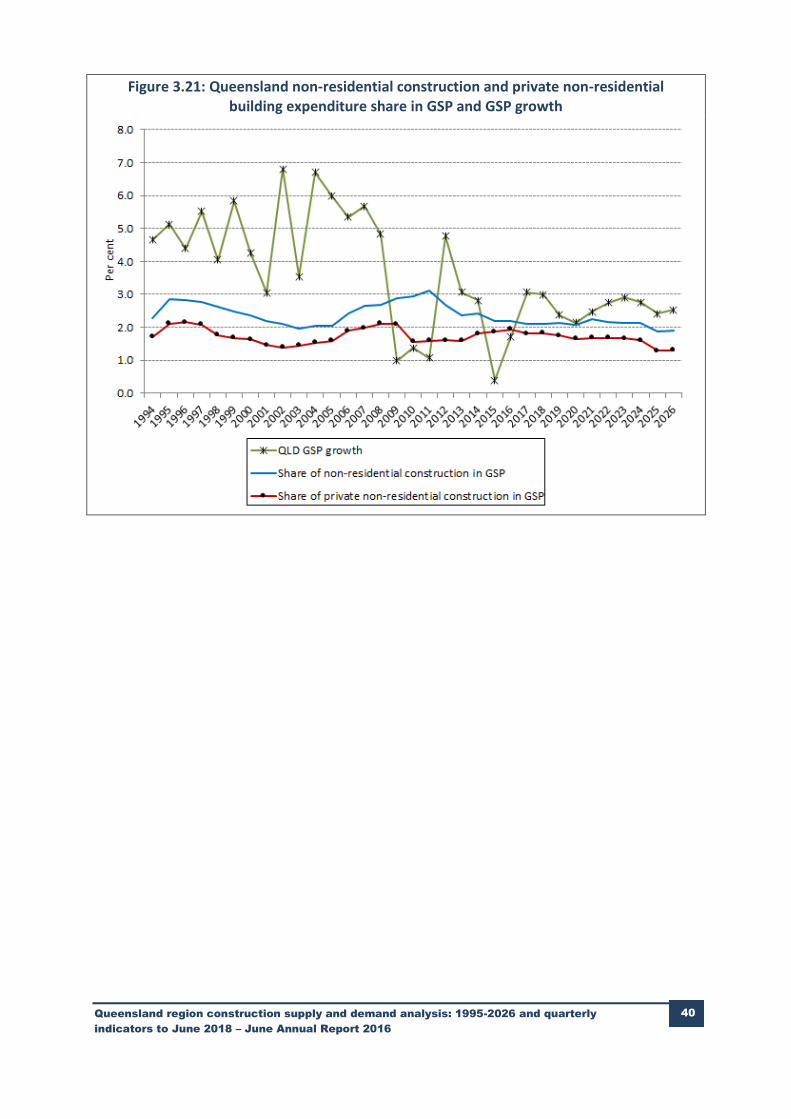

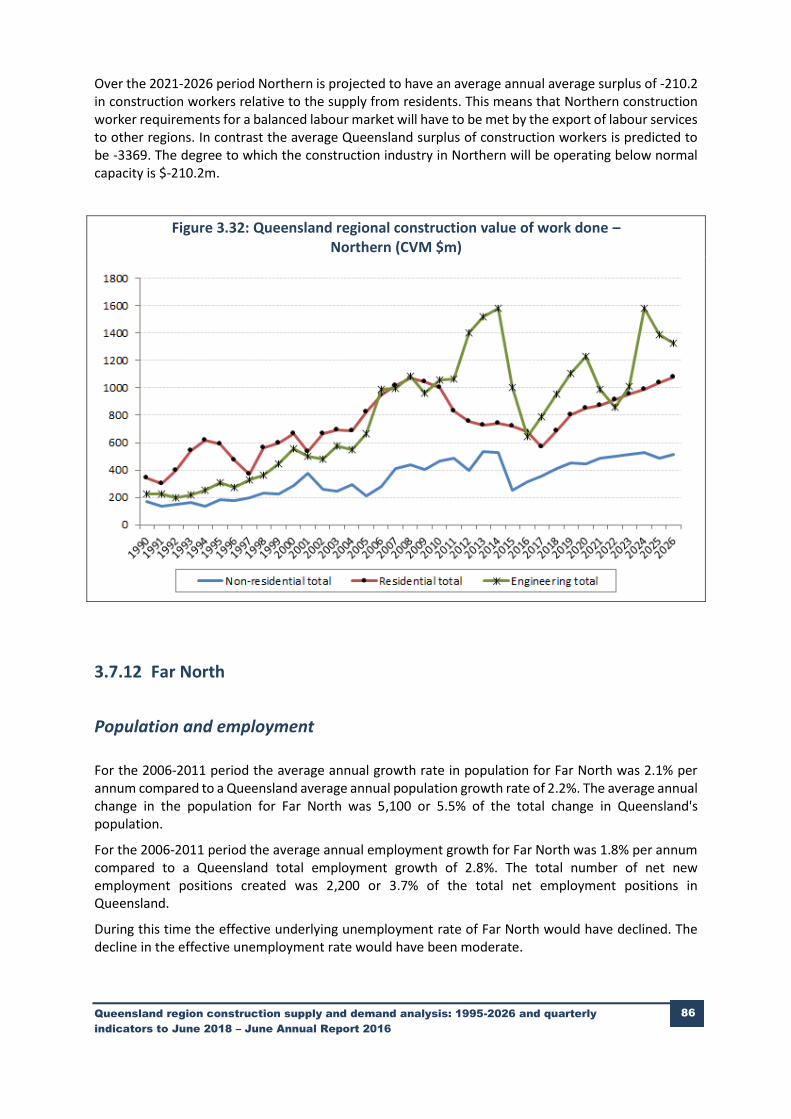

3.1 Queensland dwelling – new construction approvals ($ million) 25 3.2 Queensland dwelling – new construction approvals (number) 26 3.3 Queensland non-residential building approvals 26 3.4 Real Queensland established house prices 27 3.5 Queensland housing rental vacancy rate 27 3.6 Queensland housing approvals 28 3.7 Queensland – Private non-residential building work done and private non-residential building approvals 29 3.8 Excess demand for dwellings – Queensland 29 3.9 Queensland share of national population increase and national approvals 30 3.10 Queensland non-residential building approvals and work done 31 3.11 Queensland non-residential projects under construction, committed and under consideration 32 3.12 Queensland mining, LNG and metal ore investment 34 3.13 Queensland real mining output % rate of growth 35 3.14 Queensland mining investment 35 3.15 LNG expansion 36 3.16 Queensland engineering – work done 37 3.17 Queensland total engineering – work yet to be done 37 3.18 Queensland engineering projects under construction, committed and under consideration 38 3.19 Share of public engineering in total engineering 39 3.20 Share of Queensland construction industry in GSP 39 3.21 Queensland non-residential construction and private non-residential building expenditure share in GSP and GSP growth 40 3.22 Queensland regional construction value of work done – Brisbane 50 3.23 Queensland regional construction value of work done – Gold Coast 54 3.24 Queensland regional construction value of work done – Sunshine Coast 57 3.25 Queensland regional construction value of work done – West Moreton 61 3.26 Queensland regional construction value of work done – Wide Bay-Burnett 65 3.27 Queensland regional construction value of work done – Darling Downs 68 3.28 Queensland regional construction value of work done – South West 72 3.29 Queensland regional construction value of work done – Fitzroy 75 3.30 Queensland regional construction value of work done – Central West 79 3.31 Queensland regional construction value of work done – Mackay 82 3.32 Queensland regional construction value of work done – Northern 86 3.33 Queensland regional construction value of work done – Far North 90 3.34 Queensland regional construction value of work done – North West 93

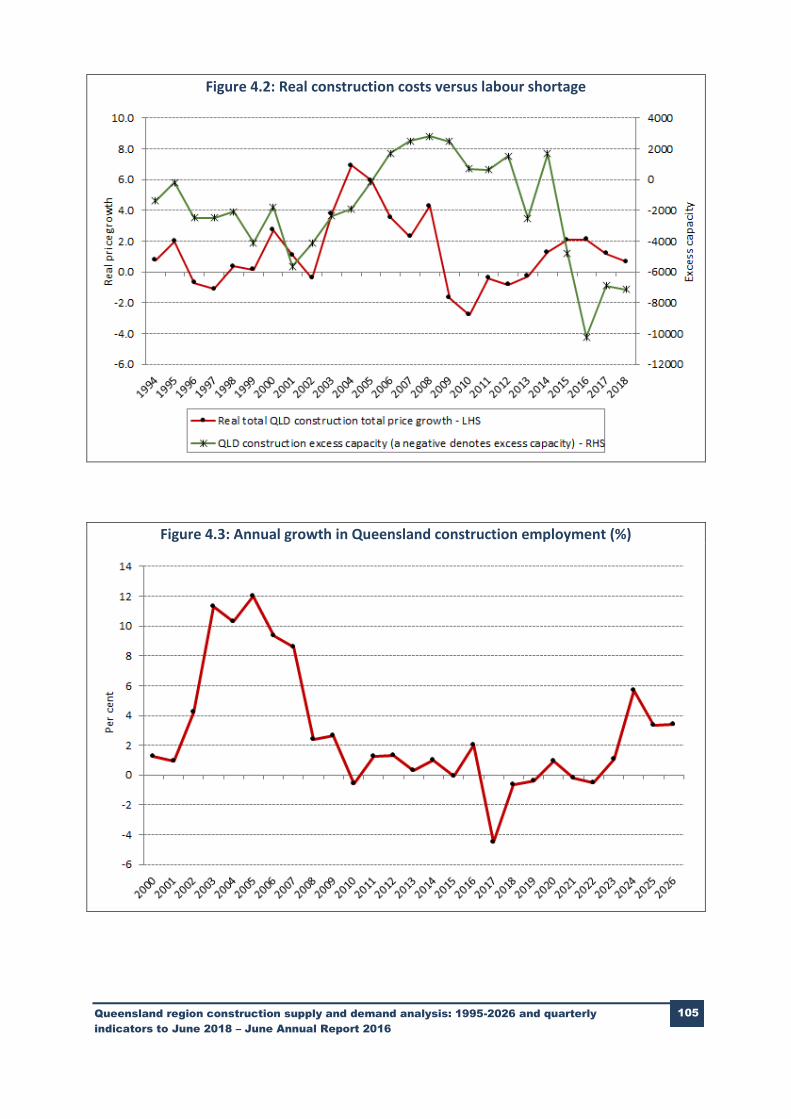

4.1 Unused capacity in Queensland’s construction sector 104 4.2 Real construction costs versus labour shortage 105 4.3 Annual growth in Queensland construction employment 105

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

i

Executive summary

A review of the core findings

In the 2016 fiscal year the Queensland economy is projected to be growing in the vicinity of 3% per annum. Despite a large subtraction from growth coming from the fall in mining investment this is being offset by the recovery in dwelling investment and the production effects of completed mining projects in general and LNG projects in particular. This state of affairs is projected to continue for at least another 18 months to two years.

As in the two previous annual reports, Australia’s economic growth is projected to be relatively strong over the 2016 to 2017 period, with Queensland’s economic growth, despite further large falls in private investment expenditure, projected to be higher than the Australian growth. That is, a little over 3% per annum. The reason for this expectation is the contribution of:

(i) current low interest rates which could go lower;

(ii) an exchange rate that will track down to levels where Australian cost competitiveness is established (an exchange rate of around 66 to 70 cents for the US$); and

(iii) high house prices maintaining net household wealth and therefore supporting high levels of consumption expenditure.

It goes without saying that the highest risk component is the exchange rate projection. However unless the policy authorities can engineer a lower exchange rate over the next 12 to 18 months Australia’s sources of growth post 2018 will be particularly weak.

For Queensland economic growth, as measured by gross state product (GSP), growth is returning to levels which if not normal compared to historical benchmarks pre-2009 will at least be similar to the national average outcomes in terms of the key economic and demographic aggregates.

Looking beyond 2018 the current drivers of Queensland economic growth, namely dwelling investment and mining production will come to an end in terms of their current high relative contribution. To maintain a growth rate similar to the national average Queensland will nead a lower Australian exchange rate to drive service exports in general and tourism exports in particular.

1. Currently (as measured by the indicators of the March Quarter 2016) the growth rate of the world is near 2.8%.

The world economy is at the crossroads. Politicians and advanced economies only made to realise that their legitimacy depends very much on their ability to deliver quality employment opportunities for their citizens in proportion to the growth in the working age population. How the current political backlash in North America and Europe translates into influencing economic activity nobody can state with certainty. All that can be said is that the solution lies with coordinated fiscal expansion across a number of key economies financed by supportive central bank policies in terms of public sector debt management. That is financing by so-called “helicopter money”. Quality political leadership needs to emerge across a number of countries which at this stage appears unlikely with instead political leadership adopting narrow protectionist policies framed purely in the national interest akin to what happened in the 1930s. A key assumption of the projections in this report is that in effect the world does manage to “muddle through” with enough positive action taken to sustain world growth near the 3% per annum range. Hopefully this assumption does not prove to be hopelessly optimistic.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

ii

2. Provided China continues to grow at least at moderate growth rates (that is, in excess of 5.5%), then Australia will not meltdown with a financial/balance of payments crisis as would otherwise have been possible given the world difficulties. There are macroeconomic imbalances in the Chinese economy but the extensive public sector ownership of assets of all types, and especially financial enterprises, the Chinese government control of vast array of economic policy instruments coupled with a $US trillion international reserves renders it highly likely that China will “muddle through” with the maintenance of reasonable economic performance.

The largest threat to the Australian and Queensland economy from China is likely to stem from geopolitical considerations rather than the performance of the Chinese economy. Tensions in the China seas if not contained is likely to see China exercise her long stated position that Australia cannot expect to successfully exploit the opportunities of the Chinese economy and remain in alliance with United States. This could at the very least result in discrimination against Australia imports and for Queensland discrimination against cold imports. Alternatively if China maintains its aggressive position in relation to the China seas it may well be that the nations of the regions will have no option but to implement at the very least a gradual build-up in an informal trade embargo against China based on a platform around the proposed TPP treaty. The current projections assume that these eventualities are not realise to a significant extent.

3. After reaching 300,000 over the 2008 and 2009 period, Australia’s immigration intake fell to an average of 178,000 over the 2014 to 2015 period with an average population growth rate of 1.4% per annum. Over the next four years that is between 2016 and 2019 the average net immigration intake is projected 186,000 with the population growth rate maintaining the 1.4% per annum growth rate. Subdued economic conditions and in particular the maintenance of relatively high unemployment rates at near 6% will constrain the immigration rate from increasing significantly above current levels forcing the National population growth rate falling to 1.3% per annum.

Over 2014 and 2015 the level of foreign net migration into Queensland has averaged in the vicinity of 20,000. This represents approximately half the level of net foreign migration into Queensland that prevailed in the five years preceding 2014. The level of net interstate migration into Queensland has remained reasonably stable over the last few years at approximately 7000 per annum. As a result the Queensland population growth rate over the last two years has fallen slightly to below the national average.

4. After growing between 4% and 6% over the years prior to the GFC, Queensland’s gross state product has averaged 12.1% per annum for the fiscal years 2009 to 2015. For the 2015 fiscal year the Queensland growth rate was 0.5% per annum which was the same outcome for 2011. Despite the fall in mining investment for 2016 and 2017 the Queensland GSP growth rate is projected to average around 3% per annum due to the recovery in dwelling investment and the production effect of completed mining projects in general and LNG projects in particular. If the weakening of the current drivers of growth and any substantial recovery in mining investment delayed until the mid-2020s at the earliest the Queensland economic growth rate should fall to around 2.4% per annum for the remainder of the projection period.

The mining production effect from the completed mining projects will come to an end by 2018 with the dwelling cycle turning down by 2020. At this stage the downside of the current dwelling cycle is projected to be reasonably mild with further growth in renovation expenditures partially offsetting the decline in new construction expenditures.

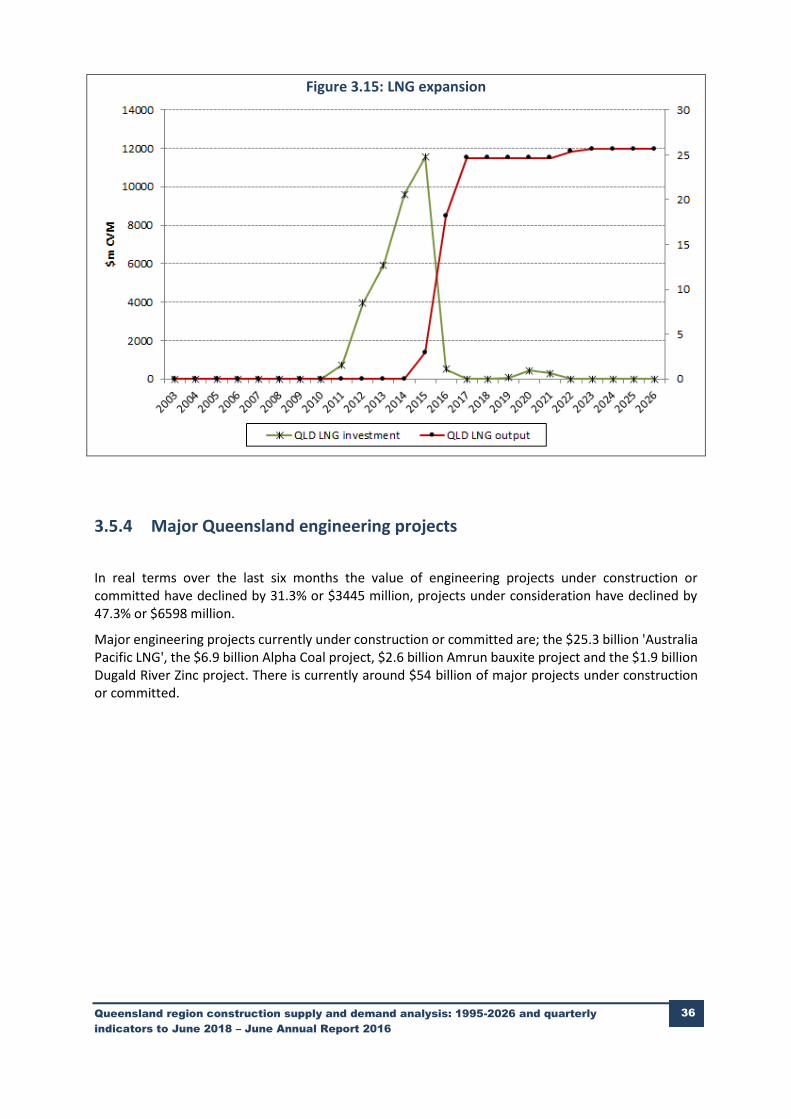

5. The Queensland construction industry has been dominated by engineering construction for the last eight years. The engineering construction share of total construction rose from just 40% in 2008 to a peak of 67% in 2014 due to the strong investment in mining and LNG projects

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

iii

over that period. In 2008 engineering work done was valued at $18 billion by 2014 it had peaked at almost $46 billion. Engineering construction has now returned to 2008 levels. This LNG construction phase is now finished. The next phase in the LNG story is LNG production, this has begun, but low world commodity prices have meant that there is no urgency to bring the established plant on line. Lack of demand for LNG in the short to medium term will delay further investment in new LNG plant.

The low commodity prices are also affecting investment in other engineering construction sectors, such as coal mining, with large projects now delayed, or cancelled. Global uncertainties, such as the economic cycles of our major trading partners such as China, conflict across the globe, US presidential elections, BREXIT, low commodity prices and fluctuating exchange rates all have the effect of discouraging investment in commodities for the global market. The result of all this uncertainty is that over the next two years engineering investment will remain at similar levels to those that occurred in 2008.

Over the last eight years, when total engineering construction was reaching record heights, the public sector investment in engineering was just over $4 billion, this was not dissimilar to the levels of investment in the eight years prior to 2008 when public sector engineering investment was $3.7 billion.

Residential construction is comprised of; the building of dwellings, alterations and additions to dwellings and other work done. The latter figure is measured in the National Accounts and covers various types of work such as odd jobs, painting, plumbing or works not requiring a permit. Until 2008 residential construction dominated the Queensland construction sector. Over the period 1990 to 2008 the average residential share of total construction was 53%. Over that period the share was never below 40%. Around 2008 two things happened; one was the global financial crisis, which lowered consumer confidence, the other was the economic rise of China, which had been begun earlier in the decade but by 2008 had reached the point where the need for coal, iron ore, other minerals and other energy sources was almost insatiable. The double effect was that the investment in dwellings was falling at the same time as the investment in engineering such as LNG plant and coal mines was booming. Hence from 2009 residential construction was no longer the major construction industry.

However the Queensland population has continued to grow. Perhaps not as fast as had been expected. The Queensland government recently revised its long term projections, with around 200,000 less people residing in Queensland in 2021 than expected in the 2013 medium projection. NIEIR has similarly adjusted the structure of the population projections used in this report. Between 2008 and 2016 the population of Queensland grew by over 600,000. This combined with declining residential construction investment since 2008 have led to a shortfall in the number of dwellings available to meet the needs of the expanding population. This shortfall and the record low interest rates that Australia is experiencing have provided the impetus needed for the dwelling construction cycle to return to the growth phase. The dwelling cycle trough occurred in 2013 when dwelling investment was just $14 billion. Currently dwelling investment is worth almost $19 billion per year. The peak in the cycle will occur around 2019, when the current shortfall has been met.

Public sector dwelling expenditure has historically averaged 2% of total expenditure in the residential sector. The last five years have seen levels of expenditure consistently below this average, this is partly because the private sector has performed reasonably well over this period, that is, the relative share of investment has increased for the private sector. However the long term average expenditure in public sector dwelling investment has be around $200 million per annum, the average for 2010 and 2011 was $500 million per annum. The average figure for 2012 to 2016 is just $135 million.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

iv

Over the first five years of the Twenty-first century the value of non-residential construction was averaging $4 billion per annum. Over the three years to the Global Financial Crisis in 2008 in response to the flow-on effects of the beginning of the mining boom, the value of non-residential construction averaged $6 billion per annum. Post GFC the expected decline in non-residential investment didn’t occur. An average of $8 billion a year was invested from 2009 to 2012, twice the pre-GFC level. The reasons for this are well documented. From 1990 until 2008 public sector investment in non-residential projects averaged around $1 billion per year, that is 26% of the total non-residential investment. For the period 2009 to 2013 the value of public sector investment steadily rose to reach $4 billion in 2011, this was largely due to the Australian Government’s stimulus packages. This stimulus was worth a total of at least $8 billion above the average long term expenditure for those four years. The types of projects included school buildings and hospitals. In the short term such spending helped prevent the Queensland economy from slipping into recession. In the longer term the bringing forward of these projects has meant that public sector non-residential investment in Queensland has had a long period of decline. From the peak of $4 billion in 2011, public sector non-residential construction expenditure was just $0.7 billion in 2016. However, population demands are ever present and in the long term public sector expenditure must return to more normal levels.

Summarising the current situation in the Queensland residential building and non-residential building sector.

■ The residential building and non-residential building sectors together make up the building sector.

■ In 2015-16 building sector activity contributed 8.1% to Queensland Gross State Product.

■ The $25 billion sector contributes one in every 12 dollars to the state's economic activity.

■ A steady recovery in the building sector is under way with average annual growth over the last two financial years of 7.4%.

■ Growth in residential building activity for the 2015/16 financial year was 15.2%. New South Wales and Tasmania were the only states to experience faster growth in dwelling expenditure over this period.

■ In the 12 months ended May 2016 the number of new dwellings approved was 11% above the corresponding period in the previous year.

■ There were 505,000 new dwellings approved in the year to the end of May 2016.

■ The Building and Construction Services sector, which is comprised of residential building, non-residential building, and construction services, is one of the largest employing industries in Queensland.

■ On average over 2015-16 the building and construction services sector employed one in every 13 jobs or 7.8% of the state's total workforce, making it the state's third biggest employing industry behind Health Care and Social Assistance (13.6%), and Retail Trade (10.7%).

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

v

■ Trend figures for the June quarter 2016 show that 228,000 persons were employed on average in construction in Queensland, with 206,000 employed in construction services and building, of these, 11.5% were employed in residential building, 5% were employed in non-residential building and 83.4% were employed in construction services.

■ Persons employed in the building industry in Queensland worked and average of 38.3 hours per week in 2014-15, compared to 38.1 hours per week nationally.

6. Historically prior to 2011, the region with the largest share of Queensland construction expenditure has been Brisbane with a long term average of 43% of the total. Whilst Brisbane still has the highest proportion of construction expenditure its share fell over the period of the mining boom so that the average share of Queensland construction for Brisbane was 33% for 2011 to 2016. In contrast the mining regions have seen their share of the state’s construction rise over this same period. The share for Fitzroy has risen from a long term average of 6% to a post 2011 average of 21%, similarly Mackay’s long term average to 2010 of 4% has risen to a 9% share of the state’s construction expenditure. Longer term it is to be expected that the distribution across the state of construction expenditure will return to the more normal pattern, where the most populous regions experience the bulk of the growth in the construction sector. However the mining regions will revert to levels that are lower than the recent past but higher than the long term trend. The total effect looking forward is that Brisbane’s construction expenditure levels should average just under $20 billion per annum over the next ten years, Gold Coast and Fitzroy between $5 billion and $6 billion per annum, Sunshine Coast and Mackay should average around $3 billion per annum. Darling Downs, Northern and Far North will all average between $2.5 billion and $3.0 billion per year.

Figure E.1: Australian GDP and Queensland GSP

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

vi

Table E.1 Australia and Queensland gross product and construction activity indicators

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Average 2019-2026

Gross product

Australia (2013-14 =100) 95.2 97.6 100.0 102.4 104.7 107.3 110.9 123.8

Queensland (2013-14 =100) 94.9 97.3 100.0 100.5 103.3 106.6 109.5 122.2

Dwelling expenditure

Australia (2013-14 =100) 98.7 95.0 100.0 108.3 119.9 131.2 132.5 140.4

Queensland (2013-14 =100) 104.9 95.2 100.0 110.1 126.8 136.3 141.7 149.6

Non-residential building expenditure

Australia (2013-14 =100) 98.6 95.0 100.0 99.9 94.8 98.2 98.2 101.0

Queensland (2013-14 =100) 104.4 95.2 100.0 90.4 91.8 91.3 94.5 86.9

Engineering construction

Australia (2013-14 =100) 94.0 105.9 100.0 84.9 80.0 81.0 88.1 87.3

Queensland (2013-14 =100) 83.6 93.1 100.0 66.3 41.5 40.4 41.0 47.2

Total construction expenditure

Australia (2013-14 =100) 96.2 100.7 100.0 94.8 95.3 100.0 104.1 106.7

Queensland (2013-14 =100) 90.5 93.8 100.0 78.5 65.6 66.9 68.8 75.2

Table E.2 Annual growth and % contribution to construction activity by major construction segment

2009-10

2010-11

2011-12

2012-13

2013-14

2014- 15

2015- 16

2016- 17

2017- 18

Annual percentage rate of change (%)

Dwellings -1.3 -8.2 -7.1 -9.3 5.1 10.1 15.2 7.5 4.0

Total non-residential building 4.2 6.3 -9.6 -8.8 5.0 -9.6 1.5 -0.5 3.5

Total engineering construction -5.1 22.0 51.0 11.5 7.4 -33.7 -37.5 -2.5 1.4

Total construction -2.2 7.5 21.6 3.7 6.6 -21.5 -16.5 2.1 2.9

Contribution to total construction growth (%)

Dwellings -0.5 -2.8 -1.8 -2.1 1.1 3.1 6.5 3.4 1.8

Total non-residential building 0.7 1.0 -1.2 -0.9 0.5 -1.2 0.2 -0.1 0.5

Total engineering construction -2.2 11.0 31.8 7.7 5.0 -19.2 -16.0 -1.0 0.6

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

vii

Table E.3 Construction activity by Queensland region – 2013-14 = 100

2010- 11

2011- 12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Average 2019-26

Brisbane 115 117 101 100 100 99 113 113 109

Gold Coast 131 107 91 100 108 120 138 140 150

Sunshine Coast 126 102 81 100 105 93 97 97 112

West Moreton 128 105 102 100 92 82 92 98 126

Wide Bay/Burnett 132 118 112 100 105 92 97 96 108

Darling Downs 66 82 89 100 55 47 45 43 51

South West 28 68 86 100 55 32 14 16 22

Fitzroy 31 72 89 100 68 38 29 27 27

Central West 35 59 90 100 160 135 150 138 210

Mackay 41 70 95 100 51 36 23 29 36

Northern 84 90 98 100 69 58 60 72 88

Far North 118 118 111 100 91 86 91 101 164

North West 56 78 94 100 50 42 88 140 66

Queensland 74 90 94 100 78 66 67 69 73

Table E.4 Share of total construction activity by Queensland region (%)

2010- 11

2011- 12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Average 2019-26

Brisbane 40.0 33.5 27.8 26.0 32.9 39.3 43.7 42.5 38.1

Gold Coast 10.4 7.0 5.7 5.9 8.2 10.8 12.3 12.1 12.2

Sunshine Coast 7.7 5.1 3.9 4.5 6.1 6.5 6.6 6.4 7.1

West Moreton 1.5 1.0 0.9 0.9 1.0 1.1 1.2 1.2 1.5

Wide Bay/Burnett 3.5 2.6 2.3 2.0 2.6 2.8 2.8 2.7 2.9

Darling Downs 6.8 6.9 7.2 7.6 5.4 5.4 5.1 4.7 5.6

South West 1.7 3.5 4.2 4.6 3.2 2.2 1.0 1.1 1.4

Fitzroy 11.3 21.5 25.6 27.0 23.5 15.6 11.8 10.5 10.1

Central West 0.3 0.5 0.7 0.7 1.4 1.4 1.6 1.4 2.0

Mackay 6.7 9.4 12.3 12.2 7.9 6.7 4.2 5.2 6.4

Northern 4.7 4.2 4.4 4.2 3.7 3.7 3.8 4.4 5.1

Far North 3.7 3.1 2.8 2.4 2.7 3.1 3.2 3.5 5.6

North West 1.6 1.8 2.1 2.1 1.4 1.4 2.8 4.3 1.9

Queensland 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

viii

Table E.5 Total construction – average annual growth rates by Queensland regions (%)

1995-2014 2014-2019 2019-2026

Brisbane 3.1 1.5 1.0

Gold Coast 2.0 7.3 2.8

Sunshine Coast 3.0 0.7 3.6

West Moreton 2.6 0.6 6.7

Wide Bay/Burnett 1.2 -0.4 3.8

Darling Downs 9.9 -16.5 12.6

South West 19.1 -23.9 -7.9

Fitzroy 15.1 -24.4 4.1

Central West 8.6 33.8 -7.3

Mackay 13.1 -19.5 8.3

Northern 5.2 -3.7 3.1

Far North 0.3 3.4 10.6

North West 10.6 -14.7 20.3

Queensland 6.2 -7.1 3.7

Table E.6 Drivers of construction growth by Queensland region 2014-2026 (average annual $ million change between span years)

2013-2018 2018-2026

Dwellings

Non-residential

con-struction

Engineer- ing

Total con-struction Dwellings

Non-residential

con-struction

Engineer- ing

Total con-struction

Brisbane 961.7 8.2 -545.3 424.5 -29.8 25.7 76.9 72.8

Gold Coast 360.4 77.3 -41.0 396.8 123.1 -8.8 48.2 162.5

Sunshine Coast 151.0 3.0 -50.8 103.2 96.7 15.1 22.4 134.2

West Moreton 4.6 6.2 -15.5 -4.7 13.7 6.8 26.1 46.6

Wide Bay/Burnett 30.7 24.0 -97.7 -43.0 23.7 2.7 25.1 51.5

Darling Downs 1.0 41.6 -512.9 -470.3 16.1 -17.7 324.5 322.9

South West -5.5 -3.1 -426.7 -435.2 2.5 0.8 -11.4 -8.2

Fitzroy -77.0 -73.4 -2119.3 -2269.6 42.1 15.8 77.2 135.0

Central West -1.1 0.5 46.2 45.6 0.0 -0.2 67.7 67.6

Mackay -78.5 -43.8 -960.6 -1082.9 42.9 11.4 253.8 308.1

Northern -8.4 -24.4 -113.4 -146.2 48.5 12.6 46.6 107.8

Far North 44.0 -20.4 -56.9 -33.4 92.6 22.4 161.5 276.5

North West 3.9 -5.9 132.8 130.8 1.8 2.1 40.0 43.9

Queensland 1386.8 -10.2 -4761.0 -3384.4 473.9 88.7 1158.7 1721.2

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

ix

Table E.7 Shortage of construction labour by Queensland region – number (shortage is denoted by +/surplus -)

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

Average 2019-26

Brisbane 53 3670 -6554 -2676 -6465 -9280 -175 -1796 -12336

Gold Coast 1264 -2479 -5484 -2095 -865 1783 6465 6164 6266

Sunshine Coast 2667 -657 -2477 2539 2810 -241 -81 -412 1355

West Moreton -582 -1230 -816 -833 -1158 -1510 -1299 -1227 -643

Wide Bay/Burnett -252 -1261 -550 -1133 -980 -1992 -1800 -1923 -1193

Darling Downs 1185 377 -280 2730 -2664 -3734 -4089 -4331 -3087

South West 131 384 45 350 -285 -594 -833 -793 -700

Fitzroy -89 5902 2728 4472 -1198 -6343 -5810 -6593 -8198

Central West 35 189 155 -40 330 175 261 184 668

Mackay -678 2053 1736 3722 -3404 -5574 -7438 -6674 -5733

Northern 51 730 1023 2127 -2881 -4811 -4623 -3093 -1290

Far North -755 -747 -999 -2013 -3418 -4257 -3883 -2956 4795

North West 168 269 229 666 -354 -512 374 1357 -54

Queensland 3198 7199 -11246 7817 -20532 -36889 -22932 -22093 -20149

Table E.8 Queensland construction industry – real quarterly price growth at annual rates (%)

2015-16 Jun.

2016-17 Sep.

2016-17 Dec.

2016-17 Mar.

2016-17 Jun.

2017-18 Sep.

2017-18 Dec.

2017-18 Mar.

2017-18 Jun.

Average 2015-16

and 2017-18

Actual Forecast

Non-residential building 7.8 -2.6 -1.6 3.8 3.8 2.5 2.5 1.1 0.1 2.4

Residential building 4.3 -0.2 0.2 3.1 3.5 1.6 1.8 1.5 1.0 2.1

Engineering construction 4.3 3.7 -1.3 4.9 -1.1 6.1 3.1 0.1 0.1 1.5

Total construction 5.0 0.5 -0.6 3.8 2.2 3.1 2.3 1.0 0.5 1.9

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

1 1 1

1. Introduction

This study has the following objectives:

(i) to undertake an historical analysis of Queensland regional construction activity to 2016;

(ii) to project Queensland regional construction activity to 2026; and

(iii) to analyse both historically and to project the capacity of Queensland regions to meet construction demands.

The Queensland regional analysis is undertaken at the Australian Bureau of Statistics’ Statistical Division level.

Section 2 overviews the Australian and Queensland economies for the next few years. Section 3 analyses the construction sector from the Queensland and Queensland regions’ perspective.

Section 4 analyses capacity utilisation and cost pressures in the Queensland construction sector as well as by region.

There are two very important points to remember when reading the text. There are no nominal values used in the study. All dollar million or dollar billion values referred to are in constant prices or technically chain volume measure (CVM) prices which in this report is the prices of the 2013-14 fiscal year. Also in terms of the domestic economy the calendar years are not in general referred to unless otherwise explicitly noted. That is all years are fiscal years so 2016 would refer to the 2015-16 fiscal year. The exception is for the world economy section where all years referred to are calendar years.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

2 2 2

2. The economic outlook for the world, Australia and Queensland

This chapter is divided into three segments. Each segment considers the macroeconomic environment for the world, Australia and Queensland.

2.1 The world economy

The world economy continues on in its sluggish growth rate recovery from the Global Financial Crisis (GFC). The current world economic growth rate is running in the order of 2.8% per annum.

The key reasons for this outcome is what, in current economic analyses, is termed ‘hysteresis. Hysteresis is commonly interpreted as if there is a sharp increase in the unemployment rate which is not quickly reversed by expansionary monetary and fiscal policies the future unemployment rate is likely to remain close to its initial elevated value. The main reason for this given by US economists is explained in terms of the fact that the longer the initially retrenched workers remain out of employment the less they are likely to be re-employed because skills degrade and experience becomes more remote to current labour market requirements. In short, the capacity of economy declines from what otherwise would have been the case.

The problem with this interpretation of hysteresis is that the US post GFC unemployment rate has fallen largely as a result of the decline in the participation rate. However, the trend rate of growth since the GFC (Global Financial Crisis) has been well below pre-GFC trends. An alternative, more realistic, explanation of hysteresis would run along the following lines:

(i) the post-GFC fiscal and monetary expansion was not maintained long enough to restore quickly pre-GFC capacity utilisation rates;

(ii) as a result investment continued to fall past 2010 or, at the very least, was held below the share necessary to maintain pre-GFC capacity growth rates;

(iii) as new investment is the main conduit by which new technology was introduced into the economy the result was not only a decline in capacity growth rates but also the rate of productivity growth. Normal capacity utilisation rates have been restored at relatively low levels of capacity output; and

(iv) the economy, therefore, becomes locked into a low trend growth rate (based on the past 5 to 10 year trend) because firstly, the capacity of the economy to accommodate a sharp increase in investment to restore pre-GFC capacity growth rates has evaporated and secondly, because expectations used for investment formation is based on subdued growth realised outcomes of the recent past.

Hence the concept of hysteresis is best thought of as meaning that the longer an economy experiences a growth rate that is below historical benchmarks the greater the probability that growth rate will become the future growth rate without further positive or negative external shocks. This is in evidence throughout the projection tables with the key driver being investment.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

3 3 3

Because many economies have been impacted by hysteresis over the past decade, this has led to the concept of secular stagnation from the world perspective. That is, the world is locked in to a period of relatively low economic growth because of the wide-spread Hysteresis. This means that once a country attempts to lift its capacity growth rate by expansionary fiscal and monetary policies it would quickly run into balance of payments constraints to growth because the failure of trading parties to expand means that imports would grow rapidly compared to exports forcing downward pressure on the exchange rate and upward pressure on interest rates. Unless the country had a strong balance of payments position before expansion, that is, low foreign debt and current account surplus, the expansionary policies would have to be curtailed.

The fundamental cause of this outcome is the failure to sustain expansionary fiscal policies post-2010 and reliance on ineffective/inefficient monetary policies leading to rapid expansions in liquidity, but not expenditures. This overhang of liquidity, in conjunction with circumstances demanding control of this liquidity, such as a sharp upward movement in the US and/or Euro inflation rate, would threaten a second GFC.

The term ‘secular stagnation’ was coined in 1938 just as the Second World War forced massive co-ordinated expansion in military expenditures which elevated the balance of payments constraint to growth and rendered the concept irrelevant for 80 years.

There are signs that the developed economies in general, and the European and Japanese economies in particular, are slowly moving towards acceptance that coordinated fiscal expansion financed by the Central Bank issuing irredeemable assets is going to be required for any acceleration in the world economic growth rate.

Such a policy approach would at least place a floor under the world economic growth rate and, therefore, justify a medium-term growth rate in the range of 2.8% to 3.3% per annum.

However, there are significant downside risks. The following are not assumed to have a significant impact on the world economy:

(i) in exiting from quantitative easing policies and the gradual return to more normal interest rates, the resulting capital losses on bonds does not trigger a herd like exit from bond markets forcing up market interest rates compared to official interest rates plunging the United States in particular into a recession;

(ii) the rise in United States interest rates does not trigger a large outflow of capital from emerging economies (the reverse of the capital inflows 2011-2013) forcing defaults in one or more of these countries;

(iii) Brexit does not force further breakup of the EU. Given the full election cycle, this probability requires the United Kingdom to slide into a recession over 2017 and 2018 and exhibit a great deal of political instability to ensure stable election cycle outcomes in Europe over 2017-2018;

(iv) the political tension in the South China Sea does not result in a new cold war with trade sanctions imposed on China;

(v) quality political leadership in the United States and Europe is maintained; and

(vi) domestically Australia does not lose the confidence of international investors that it can service and repay its two trillion dollar gross foreign debt.

Time will tell if disregarding these possibilities or assuming that they can be offset by policy reaction is justified or not.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

4 4 4

Figure 2.1: World GDP growth rate (%)

2.2 The Australian economic outlook

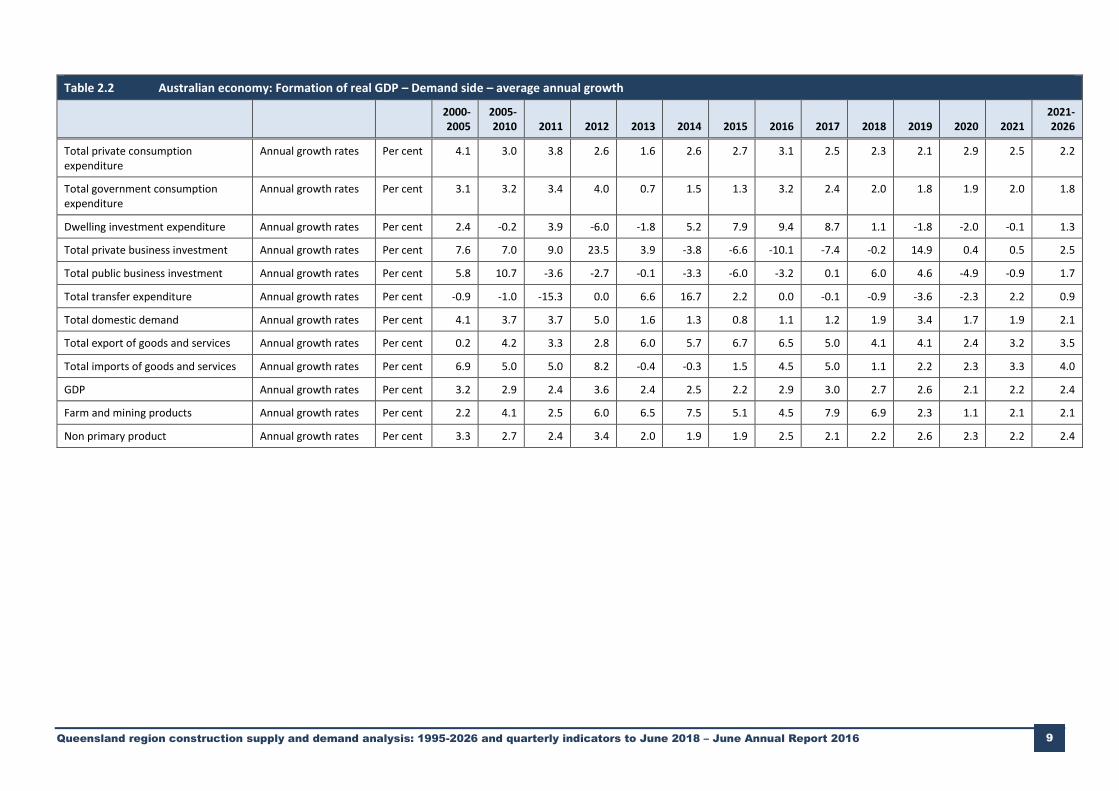

Tables 2.1 to 2.3 profile the projected outcome for key indicators of Australian economic performance. In the short-term, that is, over 2016 and 2017, Australia’s economic growth is likely to be in the vicinity of 3% per annum. However, this acceleration in the Australian growth rate from the 2014-2015 average of 2.4% will be largely due to the sustained growth in exports driven by the completion of mining projects in general, and LNG projects in particular, as well as the recovery in dwelling investment.

After 2017, these sources of growth will decline. This is especially the case for dwelling investment. Any significant extension of the current dwelling investment recovery beyond 2017, for example by adopting ultra-low interest rates, will simply be reflected by offsetting negative contributions of dwelling investment to economic growth in 2021 or 2022. This would take the Australian economic growth rate to near 1.5% in these years.

It can be seen from the tables that exports also continue to grow by in excess of 4% over 2018 and 2019. This is due to the exchange rate profile. The exchange rate is projected to decline to around the 65 cent rating for the US dollar and maintains a rate near that level for a considerable period of time. If this occurs, then continued export expansion and import replacement will make a significant positive contribution to economic growth. If, on the other hand, the exchange rate remains high at close to current levels, then for the 2018 to 2020 period Australia’s economic growth is likely to again fall to 1.5% or lower.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

5 5 5

Little more can be expected from the other drivers of economic activity. Government consumption expenditure growth is constrained by government deficit reduction objectives while private consumption expenditure growth is constrained by debt saturation, that is, upper limits of current household debt to income ratios. The downward pressure on household consumption will be aggravated by real declines in established dwelling prices which is likely to happen from 2019 onwards from the natural dynamics of the current housing price cycle. That is, increased housing supply and reductions in the population growth rate place downward pressure on house prices. The loss of household wealth will force households to increase savings rates by reducing expenditure to reduce relative debt levels.

The exchange rate and the balance of payments

At the centre of the reasons for the subdued economic outlook is Australia’s deteriorating current account deficit. The fall, in terms of trade, over the last two years means that Australia will be facing a period when the current account deficit will return to the 4% to 5% of GDP range for a considerable period of time. In part this is because the terms of trade are likely to remain relatively low over the medium-term due to:

(i) continued oversupply in iron ore and coal markets;

(ii) subdued world economic growth; and

(iii) more aggressive CO2 reduction strategies by India and China reducing coal requirements below what was previously expected.

The current account balance will also deteriorate as the expected increase in US interest rates over the next three years will directly increase as Australia’s foreign debt interest burden.

Australia’s international borrowing requirement

With the return of high current account deficits Australia’s annual international borrowing requirement will move to centre stage of policy focus. Figure 2.2 shows Australia’s short-term borrowing requirement as a percentage of GDP. The short-term borrowing requirement is defined as the level of foreign debt that falls due over the next 12 months from a given quarter less current foreign reserves plus the expected current account deficit over the next 12 months.

It can be seen from Figure 2.2 that Australia’s international borrowing requirement has gone from 35% of GDP in March 2014 to 46% by the September quarter. It has returned to GFC peaks. In 2009 it was China’s stimulus package that restored Australia’s international borrowing requirement to sustainable levels by 2012. There is no prospect of this happening now and if anything the probability is a further deterioration so that by 2017, with further devaluation of the currency, the borrowing requirement will be approaching $900 billion. Any substantial negative shocks may make it difficult for Australia to maintain the confidence of international investors and therefore avoid an international debt default. This of course result in a very different economic scenario.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

6 6 6

Figure 2.2: Australia’s international borrowing requirement (per cent of GDP)

Interest rates

The projection outlook is built around the assumption that the US will increase interest rates by at least between 1 and 2 percentage points over the next two to three years. This is likely to occur irrespective of the contraction of subdued economic growth in the US. This is because the policy of quantitative easing in the US since 2011 has led to a situation where the excess revenues of the US banking system are around US$2.6 trillion, which could be quickly mobilised to significantly expand credit to accommodate an inflation threatening unexpected acceleration in the US real economic growth rate, or an unexpected direct positive shock to inflate inflationary expenditures. Prudent monetary policy would be one which reduced the incentive to mobilise the excess reserves by increasing interest rates as well as to enable large-scale Central Bank sale of securities to reduce the level of reserves.

Given Australia’s high current international borrowing requirement, Australia will be forced to follow any increase in US interest rates despite the fact that in the short-run Australia’s interest rates are likely to fall further.

Population and migration

The subdued Australian outlook is reinforced by the fact that the lower the economy’s growth rate the lower will be the employment growth rate, which will force a reduction in the net foreign immigration rate to stabilise the unemployment rate at around 6%. Accordingly, over the medium-term the Australian net foreign immigration intake is likely to remain in the 170,000 to 200,000 range.

As a result, the population growth rate is held to a growth rate in the range of 1.3% to 1.5% per annum. That is, this will be the maximum growth rate the economy can support given the economic outlook.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

7 7 7

The inflation rate

The current general policy concern is the rate of inflation. That is, its low level. For the projections the rate of inflation returns to the 2% to 3% range. The key driver of this outcome is the low exchange rate. This reinforces the point that Australia’s and Queensland’s economic outlook depends critically on a long-term low exchange rate regime being successfully realised. Post the mining boom, with a debt saturated household sector by choice, a deficit constrained government sector and a subdued world economy there is no other credible driver of growth

Figure 2.3: Australia – Real GDP growth rate (%)

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 8

Table 2.1 Australian economy: Population and labour market

2000-2005

2005-2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2021-2026

Total population Annual growth rates Per cent 1.2 1.8 1.4 1.6 1.8 1.6 1.4 1.4 1.5 1.4 1.4 1.3 1.3 1.3

Net foreign arrivals Annual level Ths. 115.6 230.6 180.4 229.4 227.1 186.4 176.5 184.8 192.0 184.0 184.0 176.0 172.0 202.9

Population 18 and over Annual growth rates Per cent 1.5 2.0 1.6 1.8 1.9 1.7 1.6 1.8 1.7 1.4 1.4 1.3 1.3 1.4

Total hours worked Annual growth rates Per cent 1.3 1.8 2.8 1.4 -0.9 0.8 1.0 2.4 1.5 1.1 1.2 1.4 1.3 0.8

Average hours worked per working age population per week

Annual level Ths. 21.1 21.4 21.2 21.2 20.6 20.4 20.3 20.4 20.4 20.3 20.3 20.3 20.3 20.0

Total employment Annual growth rates Per cent 2.0 2.3 2.4 1.2 1.2 0.5 1.2 2.2 1.7 1.5 1.5 1.6 1.6 1.3

Total employed per working age population

Annual growth rates Per cent 0.6 0.3 0.8 -0.6 -0.6 -1.1 -0.5 0.5 -0.2 0.0 0.1 0.2 0.2 -0.1

Total workforce Annual growth rates Per cent 1.7 2.4 1.9 1.3 1.5 1.0 1.5 2.3 1.4 1.5 1.4 1.5 1.4 1.3

Number unemployed Annual level Ths. 597.9 532.0 590.6 614.0 655.2 710.7 762.4 760.1 779.2 801.7 807.3 806.0 804.1 855.1

Unemployment rate Annual level Per cent 6.1 4.8 5.0 5.2 5.4 5.8 6.2 5.9 6.1 6.2 6.1 6.0 5.9 6.0

Participation rate Annual level Per cent 63.4 65.1 65.5 65.3 65.1 64.7 64.7 65.1 64.9 64.9 65.0 65.1 65.1 65.1

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 9

Table 2.2 Australian economy: Formation of real GDP – Demand side – average annual growth

2000-2005

2005-2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2021-2026

Total private consumption expenditure

Annual growth rates Per cent 4.1 3.0 3.8 2.6 1.6 2.6 2.7 3.1 2.5 2.3 2.1 2.9 2.5 2.2

Total government consumption expenditure

Annual growth rates Per cent 3.1 3.2 3.4 4.0 0.7 1.5 1.3 3.2 2.4 2.0 1.8 1.9 2.0 1.8

Dwelling investment expenditure Annual growth rates Per cent 2.4 -0.2 3.9 -6.0 -1.8 5.2 7.9 9.4 8.7 1.1 -1.8 -2.0 -0.1 1.3

Total private business investment Annual growth rates Per cent 7.6 7.0 9.0 23.5 3.9 -3.8 -6.6 -10.1 -7.4 -0.2 14.9 0.4 0.5 2.5

Total public business investment Annual growth rates Per cent 5.8 10.7 -3.6 -2.7 -0.1 -3.3 -6.0 -3.2 0.1 6.0 4.6 -4.9 -0.9 1.7

Total transfer expenditure Annual growth rates Per cent -0.9 -1.0 -15.3 0.0 6.6 16.7 2.2 0.0 -0.1 -0.9 -3.6 -2.3 2.2 0.9

Total domestic demand Annual growth rates Per cent 4.1 3.7 3.7 5.0 1.6 1.3 0.8 1.1 1.2 1.9 3.4 1.7 1.9 2.1

Total export of goods and services Annual growth rates Per cent 0.2 4.2 3.3 2.8 6.0 5.7 6.7 6.5 5.0 4.1 4.1 2.4 3.2 3.5

Total imports of goods and services Annual growth rates Per cent 6.9 5.0 5.0 8.2 -0.4 -0.3 1.5 4.5 5.0 1.1 2.2 2.3 3.3 4.0

GDP Annual growth rates Per cent 3.2 2.9 2.4 3.6 2.4 2.5 2.2 2.9 3.0 2.7 2.6 2.1 2.2 2.4

Farm and mining products Annual growth rates Per cent 2.2 4.1 2.5 6.0 6.5 7.5 5.1 4.5 7.9 6.9 2.3 1.1 2.1 2.1

Non primary product Annual growth rates Per cent 3.3 2.7 2.4 3.4 2.0 1.9 1.9 2.5 2.1 2.2 2.6 2.3 2.2 2.4

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 10

Table 2.3 Australian economy: Commodity prices, terms of trade and the balance of payments

2000-2005

2005-2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2021-2026

Terms of trade Annual level Index 0.6 0.9 1.1 1.1 1.0 1.0 0.9 0.8 0.8 0.8 0.8 0.8 0.8 0.8

Balance of trade Annual level $Billion -12.9 -15.5 14.2 -3.0 -18.9 -7.0 -23.0 -42.0 -56.9 -61.2 -72.1 -73.5 -80.7 -86.5

Net income paid overseas Annual level $Billion -23.1 -46.5 -58.4 -47.3 -40.5 -44.1 -35.8 -35.3 -41.2 -42.4 -43.1 -43.5 -45.2 -34.9

Current account balance Annual level $Billion -35.9 -62.0 -44.1 -50.3 -59.4 -51.1 -58.7 -77.3 -98.3 -103.6 -115.2 -117.0 125.9 -121.4

Current account balance – % of GDP Annual level Index -4.5 -5.4 -3.1 -3.4 -3.9 -3.2 -3.6 -4.8 -5.8 -5.8 -6.1 -6.0 -6.3 -4.9

International debt – % of GDP Annual level Index 41.7 49.4 46.8 49.0 50.9 54.6 59.1 62.7 68.0 73.2 73.9 78.2 85.0 88.8

90 day rate Annual level Index 5.3 5.6 4.9 4.4 3.2 2.6 2.5 2.2 2.0 2.4 3.0 3.0 3.1 3.4

10 year bond rate Annual level Index 5.0 4.8 4.6 3.5 2.9 3.8 3.0 2.8 2.9 3.5 3.9 3.9 3.8 4.2

Oil price Annual growth rates $US 29.9 72.4 92.7 105.4 102.3 105.5 69.5 50.8 52.4 57.2 62.2 66.5 70.1 79.7

World GDP Annual growth rates Per cent 3.7 3.6 4.4 3.2 2.5 2.6 2.9 3.1 3.2 3.1 3.1 2.8 3.0 3.3

Exchange rate Annual level Index 0.62 0.81 0.99 1.04 1.03 0.92 0.84 0.73 0.70 0.65 0.64 0.64 0.63 0.68

Implicit consumption deflator Annual growth rates Per cent 2.6 3.0 2.1 2.5 2.7 2.4 1.6 1.4 1.9 2.2 1.9 1.3 1.4 2.2

$ per hour wage and mixed income Annual growth rates Per cent 5.6 4.6 5.7 5.2 4.2 1.8 2.1 2.1 2.1 2.2 2.5 2.6 2.8 3.4

Average weekly earnings Annual growth rates Per cent 5.0 4.5 4.3 4.6 4.6 2.9 2.2 2.2 2.1 2.2 2.3 2.3 2.2 2.7

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

11 11 11 11

2.3 The Queensland economic outlook

Queensland Gross State Product was $240 billion in 2006, by 2015 it had grown to $300 billion. In 2006 the Queensland economy was growing at 6%. The impact of the Global Financial Crisis can be seen in the slower growth of the economy over the 2009 to 2011 period. At that time dwelling investment was falling rapidly at an average of 7% per annum. Private investment fell dramatically in 2010. However public expenditure was maintained over this period through economic stimulus. Economic growth was slowest in 2011 at just 0.5%, this was in spite of strong growth in private investment, particularly engineering construction due to LNG and mining investment. In 2012 engineering construction growth was again strong, resulting in growth of 39.5% in private investment, this contributed to the 5% growth in GSP in that year. Between 2013 and 2016 GSP growth has ranged between 1.1% and 2.8%. Large declines in public investment have occurred in 2015 and 2016 as the LNG projects are completed. These have been partially offset by growth in dwelling investment.

Further winding down of the engineering sector occurs over 2017, as indicated in the 16% decline in private investment. However dwelling investment is still exhibiting strong growth in 2017 due to population growth and record low interest rates. The low interest rates and rising property values ensure that private consumption will grow at around 2.8% over 2017 and 2018.

Falling commodity prices will slow growth in mining exports over 2018, never the less GSP growth for 2018 is still above 3%. In the longer term Queensland GSP growth will average just under 3% reflecting the subdued outlook for coal with low commodity prices and China’s slow but steady move to greener fuel sources or local energy sources.

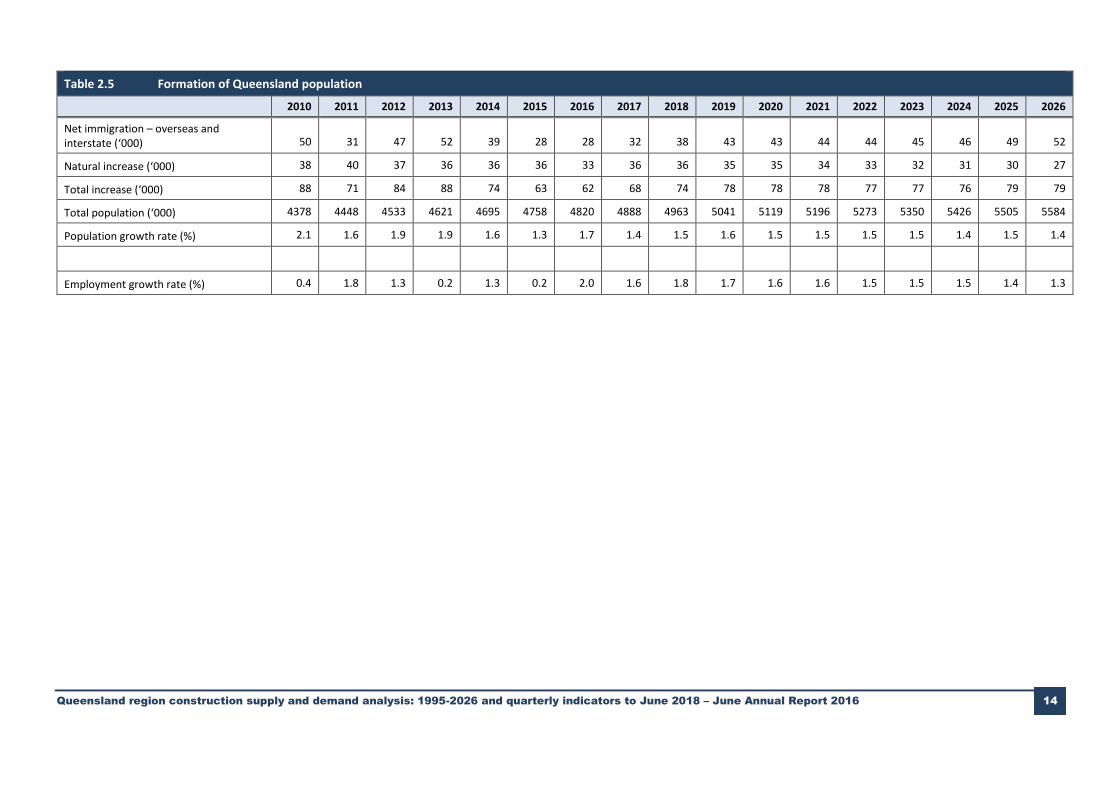

Net immigration into Queensland has averaged around 26,000 over the last two years. This is less than half of the value for the 2006 to 2014 period. Net interstate migration stood at around 27,000 in 2006, whilst net overseas migration was around 33,000 for the same year. Net interstate migration was trending down from 2003, whereas net overseas migration reached a peak of 60,000 in 2009. Bye 2015 net interstate migration was 6,400 and net overseas migration was 21,000. The winding up of the mining construction cycle has had a two-fold effect on net immigration, the more mobile of the construction workers, will have flown out in search of construction work elsewhere, and the slow employment growth over the 2010 to 2014 period when investment was concentrated in the mining sectors has failed to lure migrants from interstate and overseas. However the long term projection is for Queensland population growth to average 1.5% per annum as the relatively high cost of dwellings in Sydney and Melbourne in particular will push migration flows from these centres towards Queensland. Employment growth averages around 2% per annum until 2020, in the long term employment growth slows to average 1% over the 2021 to 2026 period. This is lower than the Australian growth rate. Across the state Brisbane, Gold Coast and Sunshine Coast can expect the largest increase in population.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 12

Table 2.4 Formation of Queensland Gross State Product

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Annual growth – $CVM m (%)

Private consumption expenditure 1.3 3.6 3.4 2.0 2.7 2.4 2.9 2.6 2.9 2.2 2.9 2.7 2.0 2.4 2.7 2.7 2.7

Government expenditure 1.1 5.0 4.1 0.0 0.8 1.7 3.8 1.7 1.3 1.4 1.3 1.7 2.0 2.1 1.8 2.0 1.8

Dwelling investment -2.9 -9.4 -4.8 -8.8 4.7 8.6 15.2 7.5 4.0 1.4 -1.5 -2.1 3.0 4.2 3.7 4.2 4.1

Private investment -15.0 22.1 39.5 5.4 -3.5 -21.7 -22.7 -16.5 -1.1 10.8 -4.3 4.3 3.5 3.7 -2.0 -0.5 8.2

Public investment 6.5 -7.3 -3.4 -7.4 0.1 -8.5 -6.3 2.3 0.9 4.1 2.5 5.3 6.0 7.6 6.6 4.7 0.9

Total state final demand -1.3 4.4 8.6 1.3 1.1 -3.0 -0.9 1.2 1.2 2.4 1.3 2.5 2.2 2.6 2.0 2.3 3.1

Net trade and stocks – percentage point contribution 2.7 -4.0 -3.5 1.0 1.6 3.7 3.8 2.1 1.5 0.0 1.0 0.2 0.4 0.0 0.4 -0.1 -0.5

Gross State Product 1.3 0.5 5.8 2.4 2.8 0.5 2.8 3.3 2.7 2.4 2.3 2.6 2.6 2.5 2.3 2.1 2.5

Percentage point contribution to Queensland GSP growth

Private consumption expenditure 0.8 2.1 2.0 1.2 1.5 1.4 1.7 1.5 1.7 1.3 1.7 1.6 1.1 1.4 1.6 1.6 1.6

Government expenditure 0.2 0.9 0.7 0.0 0.1 0.3 0.6 0.3 0.2 0.2 0.2 0.3 0.3 0.3 0.3 0.3 0.3

Dwelling investment -0.2 -0.6 -0.3 -0.5 0.2 0.4 0.8 0.4 0.2 0.1 -0.1 -0.1 0.2 0.2 0.2 0.3 0.2

Private investment -2.6 3.1 6.8 1.2 -0.8 -4.8 -3.9 -2.1 -0.1 1.1 -0.5 0.4 0.4 0.4 -0.2 -0.1 0.8

Public investment 0.5 -0.6 -0.3 -0.5 0.0 -0.5 -0.4 0.1 0.0 0.2 0.1 0.3 0.3 0.4 0.4 0.3 0.1

Total state final demand -1.4 4.5 9.3 1.4 1.2 -3.2 -1.0 1.2 1.2 2.4 1.3 2.4 2.2 2.5 2.0 2.2 3.0

Net trade and stocks - percentage point contribution 2.7 -4.0 -3.5 1.0 1.6 3.7 3.8 2.1 1.5 0.0 1.0 0.2 0.4 0.0 0.4 -0.1 -0.5

Gross State product 1.3 0.5 5.8 2.4 2.8 0.5 2.8 3.3 2.7 2.4 2.3 2.6 2.6 2.5 2.3 2.1 2.5

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 13

Table 2.4 Formation of Queensland Gross State Product (continued)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Supply side contribution to GSP growth – average annual growth rate $CVM

Agriculture -0.5 4.6 2.9 -4.3 -4.0 0.5 4.6 5.6 4.4 3.6 3.0 2.7 2.5 2.4 2.2 2.1 2.1

Mining 14.0 -10.0 5.9 5.0 9.9 6.7 11.0 9.8 3.4 2.1 2.5 2.8 2.8 1.5 1.8 1.0 0.8

Manufacturing -4.2 -1.5 4.2 -1.4 0.7 -0.3 -0.4 2.2 3.9 4.8 5.1 5.7 6.5 6.9 6.5 5.0 5.3

Construction -4.6 6.9 14.4 6.2 10.3 -21.1 -9.3 2.1 2.9 0.6 0.3 -0.6 0.6 3.2 11.1 5.8 5.9

Distribution -2.0 2.0 6.0 5.3 1.3 9.7 2.1 4.6 2.0 1.3 0.6 0.6 1.4 2.0 1.3 1.5 2.5

Finance 1.3 1.0 3.4 4.5 5.2 8.1 5.8 3.5 3.5 3.8 3.8 3.2 2.8 3.0 2.3 1.8 1.9

Business services -0.8 2.0 3.8 1.8 2.6 0.4 1.6 5.7 3.5 3.3 2.6 2.6 2.8 3.1 2.6 2.5 3.5

Community services 4.2 1.6 4.1 2.3 5.3 3.6 5.4 4.6 3.0 2.6 2.6 2.9 3.3 3.4 3.2 3.2 3.0

Ownership of dwellings -1.9 -1.9 0.9 1.6 2.0 2.3 2.2 2.9 3.1 3.0 2.9 2.8 2.7 2.6 2.6 2.7 2.7

Indirect taxes and other 1.4 -0.3 1.0 -0.2 -0.9 -0.1 0.9 -1.0 -0.2 -0.1 0.1 0.4 0.0 -0.3 -0.8 -0.5 -0.5

GDP 1.3 0.5 5.8 2.4 2.8 0.5 2.8 3.3 2.7 2.4 2.3 2.6 2.6 2.5 2.3 2.1 2.5

Supply side contribution to GSP growth – percentage point contribution to growth

Agriculture 0.0 0.1 0.1 -0.1 -0.1 0.0 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1

Mining 0.9 -0.7 0.4 0.3 0.7 0.5 0.8 0.8 0.3 0.2 0.2 0.2 0.2 0.1 0.2 0.1 0.1

Manufacturing -0.3 -0.1 0.3 -0.1 0.1 0.0 0.0 0.1 0.2 0.3 0.3 0.4 0.4 0.5 0.5 0.4 0.4

Construction -0.5 0.6 1.4 0.7 1.1 -2.5 -0.9 0.2 0.2 0.0 0.0 0.0 0.0 0.2 0.8 0.5 0.5

Distribution -0.3 0.3 0.9 0.8 0.2 1.5 0.3 0.6 0.3 0.2 0.1 0.1 0.2 0.3 0.2 0.2 0.3

Finance 0.1 0.1 0.2 0.3 0.3 0.5 0.4 0.2 0.2 0.2 0.3 0.2 0.2 0.2 0.2 0.1 0.1

Business services -0.2 0.5 1.0 0.5 0.7 0.1 0.4 1.5 0.9 0.9 0.7 0.7 0.7 0.8 0.7 0.7 0.9

Community services 0.4 0.2 0.4 0.2 0.6 0.4 0.6 0.5 0.4 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4

Ownership of dwellings -0.2 -0.2 0.1 0.1 0.2 0.2 0.2 0.2 0.3 0.3 0.3 0.2 0.2 0.2 0.2 0.2 0.2

Indirect taxes and other 1.4 -0.3 1.0 -0.2 -0.9 -0.1 0.9 -1.0 -0.2 -0.1 0.1 0.4 0.0 -0.3 -0.8 -0.5 -0.5

GDP 1.3 0.5 5.8 2.4 2.8 0.5 2.8 3.3 2.7 2.4 2.3 2.6 2.6 2.5 2.3 2.1 2.5

Queensland region construction supply and demand analysis: 1995-2026 and quarterly indicators to June 2018 – June Annual Report 2016 14

Table 2.5 Formation of Queensland population

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Net immigration – overseas and interstate (‘000) 50 31 47 52 39 28 28 32 38 43 43 44 44 45 46 49 52

Natural increase (‘000) 38 40 37 36 36 36 33 36 36 35 35 34 33 32 31 30 27

Total increase (‘000) 88 71 84 88 74 63 62 68 74 78 78 78 77 77 76 79 79

Total population (‘000) 4378 4448 4533 4621 4695 4758 4820 4888 4963 5041 5119 5196 5273 5350 5426 5505 5584

Population growth rate (%) 2.1 1.6 1.9 1.9 1.6 1.3 1.7 1.4 1.5 1.6 1.5 1.5 1.5 1.5 1.4 1.5 1.4

Employment growth rate (%) 0.4 1.8 1.3 0.2 1.3 0.2 2.0 1.6 1.8 1.7 1.6 1.6 1.5 1.5 1.5 1.4 1.3

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

15 15 15 15

Table 2.6 Average annual population change by region (‘000)

2001-2005 2005-2015 2015-2018 2018-2026

Brisbane 42.5 42.5 37.3 38.6

Gold Coast 14.6 11.9 10.7 12.6

Sunshine Coast 9.0 6.3 7.0 7.1

West Moreton 1.6 2.0 1.5 2.1

Wide Bay/Burnett 4.9 4.3 1.7 2.8

Darling Downs 2.5 2.9 1.6 2.0

South West -0.2 0.1 -0.1 0.0

Fitzroy 2.9 4.0 2.3 3.4

Central West -0.2 0.0 -0.1 -0.1

Mackay 3.2 3.5 1.4 2.5

Northern 2.9 4.0 2.4 3.7

Far North 3.3 4.4 2.8 3.3

North West -0.3 0.3 0.0 0.1

Queensland 86.8 86.0 68.3 78.0

2.4 Queensland housing affordability

In the annual ALGA/NIEIR “State of the Regions” reports NIEIR has developed a range of indicators to assess the affordability of housing in Australian regions. The results for the Queensland regions are attached. The regions referred to in this section of the report are those used in the ALGA report, however as their names suggest they can be in this context, broadly compared to the regions used elsewhere in this report. For brevity only a selection of years are included the tables. Appendix C contains LGA level data for some of these series and further commentary.

As discussed in previous reports sustainable dwelling markets are those that are able to where dwelling construction keeps pace with population growth. Regions that achieve this generally meet the two criteria listed below;

1. a construction cost for new dwellings that is not significantly below the average market prices for established dwellings; and

2. the expected average income from the labour market catchment must be able to support the average mortgage on new dwelling construction.

If criteria (1) is not satisfied in that the cost of new dwelling construction is well above the average established dwelling prices, then new construction will be discouraged because of the risk of capital losses if the dwelling is on-sold within the first few years of completion.

If condition (2) is not satisfied then new households relying on income to support mortgage payments will not be able to afford new dwellings. In other words, a region that is attractive to new residents will have average household incomes in the catchment region, that are able to support the mortgage levels required to build new dwellings.

The attached tables have a range of indicators that drive local housing markets. It should also be noted that the mortgage costs are calculated on a long-run average mortgage interest rates. In the short-run, mortgage costs may well be below the estimates in the tables.

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

16 16 16 16

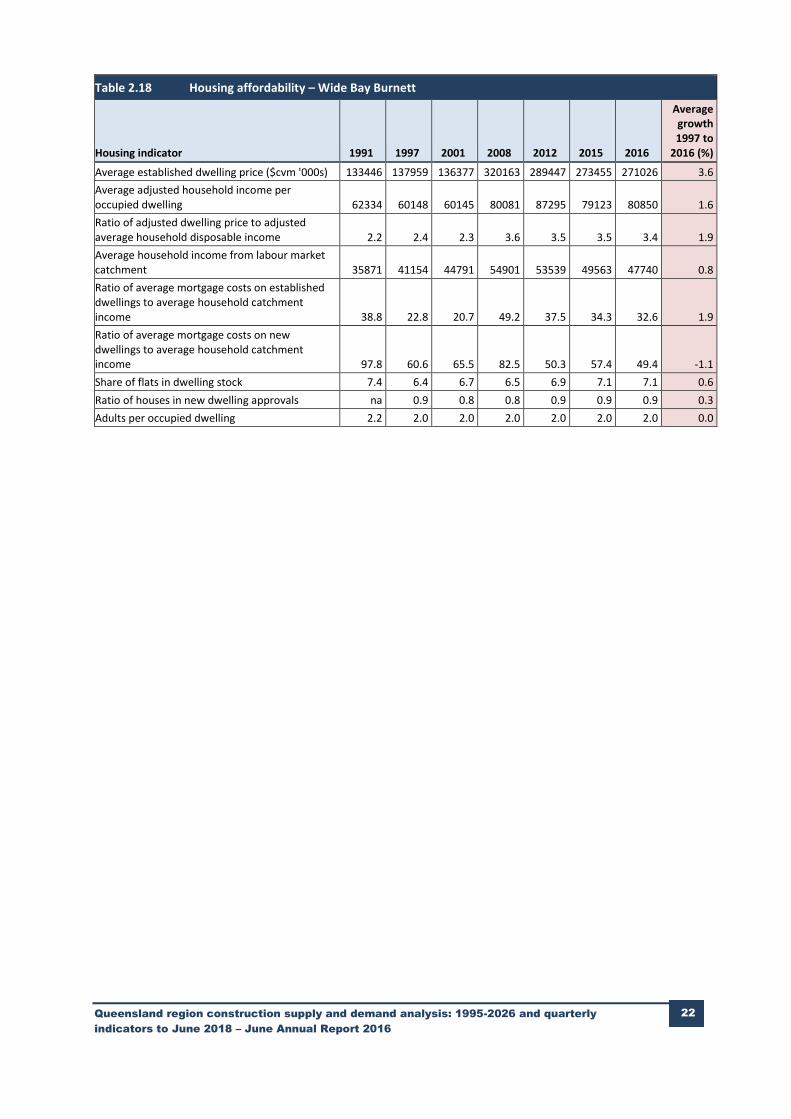

Ideally, the average ratio of new dwelling costs to established house prices should be less than 85% to 90%, while the mortgage costs for new dwelling construction to labour market catchment average income should be no more than 35% to 40%. Sydney has mortgage costs for new dwelling construction to labour market catchment average income of around 44%, although in 2008 it was over 60%. The figure for the greater Brisbane region is 23% down from 37% in 2008.

A comparison across the regions of the indicators in the tables can be informative. At a glance it can be seen that the Brisbane region has the highest average established dwelling price at $560,000. The Gold Coast has the second highest at just over $500,000, with Sunshine Coast, Logan Redland and Moreton Bay all having values between $400,000 and $500,000. The remaining ALGA regions have values of less than $400,000 but greater than $270,000. All else being equal one could assume that housing affordability in Queensland follows this pattern. However it is important to consider the other indicators in the tables.

The figures for adjusted income per dwelling indicate that it is not Brisbane that has the highest incomes but Mackay, with $132,000 compared to Brisbane with $130,000. However as Mackay house prices are less than $317,000 the ratio of adjusted dwelling price to adjusted average household disposable income is only 2.9 for Mackay but 4.1 for Brisbane. The region with the highest ratio is Gold Coast.

Looking more broadly at catchment incomes, that is the incomes obtainable within commuting distance, Mackay and Brisbane have the highest catchment incomes and Moreton Bay has the lowest. However although Moreton Bay has mid-range dwelling values, the catchment income is low.

The next two indicators show that Moreton Bay residents are the hardest pressed in regards to the two ratios of average mortgage costs on dwellings to average household catchment income. The large values these ratios for Moreton Bay show that in spite of the relatively low housing prices, the ability for the region to attract new residents is hampered by lack of opportunity to earn high incomes within commuting distance.

Table 2.7 Housing affordability – Brisbane City

Housing indicator 1991 1997 2001 2008 2012 2015 2016

Average growth 1997 to

2016 (%)

Average established dwelling price ($cvm '000s) 208725 227618 270438 531375 509386 549130 559976 4.9

Average adjusted household income per occupied dwelling

76746 78339 78329 118612 142509 130944 130444 2.7

Ratio of adjusted dwelling price to adjusted average household disposable income

2.7 2.8 2.9 3.7 3.8 4.0 4.1 2.1

Average household income from labour market catchment

59342 68048 79887 104966 105462 95672 89687 1.5

Ratio of average mortgage costs on established dwellings to average household catchment income

36.5 22.3 22.3 42.1 33.0 33.8 35.3 2.4

Ratio of average mortgage costs on new dwellings to average household catchment income

78.4 42.1 35.5 37.3 27.6 23.8 23.2 -3.1

Share of flats in dwelling stock 18.4 17.2 17.7 19.7 20.5 23.6 25.5 2.1

Ratio of houses in new dwelling approvals na 0.6 0.6 0.4 0.4 0.2 0.2 -6.1

Adults per occupied dwelling 2.2 2.1 2.1 2.1 2.2 2.2 2.1 0.2

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

17 17 17 17

Table 2.8 Housing affordability – Gold Coast

Housing indicator 1991 1997 2001 2008 2012 2015 2016

Average growth 1997 to

2016 (%)

Average established dwelling price ($cvm '000s) 225947 255717 284090 550014 469038 492548 504667 3.6

Average adjusted household income per occupied dwelling 51490 52617 53417 89194 108205 106704 110361 4.0

Ratio of adjusted dwelling price to adjusted average household disposable income 4.4 4.8 4.8 5.4 4.7 4.4 4.3 -0.5

Average household income from labour market catchment 51654 54609 62032 77894 76403 69692 66364 1.0

Ratio of average mortgage costs on established dwellings to average household catchment income 45.3 31.3 30.1 58.7 41.9 41.5 43.0 1.7

Ratio of average mortgage costs on new dwellings to average household catchment income 70.8 42.7 38.8 53.6 44.0 39.6 41.1 -0.2

Share of flats in dwelling stock 33.0 23.6 24.2 23.2 21.6 22.2 22.8 -0.2

Ratio of houses in new dwelling approvals na 0.5 0.6 0.5 0.6 0.4 0.5 -0.5

Adults per occupied dwelling 1.9 1.9 1.9 2.0 2.1 2.2 2.2 0.8

Table 2.9 Housing affordability – West Moreton

Housing indicator 1991 1997 2001 2008 2012 2015 2016

Average growth 1997 to

2016 (%)

Average established dwelling price ($cvm '000s) 132112 135990 136730 356165 330125 328259 327502 4.7

Average adjusted household income per occupied dwelling 65201 64559 64457 93560 107753 102175 103129 2.5

Ratio of adjusted dwelling price to adjusted average household disposable income 2.0 2.1 2.1 3.3 3.3 3.2 3.1 2.2

Average household income from labour market catchment 52758 59960 68115 87443 88673 81416 77262 1.3

Ratio of average mortgage costs on established dwellings to average household catchment income 26.7 15.6 14.0 36.8 27.4 25.6 25.3 2.6

Ratio of average mortgage costs on new dwellings to average household catchment income 56.1 31.7 28.3 42.3 31.9 29.3 28.0 -0.6

Share of flats in dwelling stock 3.2 3.1 3.5 3.3 3.2 3.7 4.2 1.7

Ratio of houses in new dwelling approvals na 0.9 0.9 0.9 0.9 0.9 0.8 -0.6

Adults per occupied dwelling 2.3 2.1 2.1 2.1 2.1 2.2 2.2 0.2

Queensland region construction supply and demand analysis: 1995-2026 and quarterly

indicators to June 2018 – June Annual Report 2016

18 18 18 18

Table 2.10 Housing affordability – Logan Redland

Housing indicator 1991 1997 2001 2008 2012 2015 2016

Average growth 1997 to

2016 (%)

Average established dwelling price ($cvm '000s) 173398 182663 196305 431379 403651 400876 401817 4.2

Average adjusted household income per occupied dwelling 72372 71854 71960 99544 115206 102441 102091 1.9

Ratio of adjusted dwelling price to adjusted average household disposable income 2.4 2.5 2.5 3.6 3.7 3.8 3.9 2.3

Average household income from labour market catchment 33829 38494 43652 56049 56350 50567 47606 1.1

Ratio of average mortgage costs on established dwellings to average household catchment income 54.4 32.2 30.0 66.0 50.5 48.6 49.1 2.2

Ratio of average mortgage costs on new dwellings to average household catchment income 89.2 50.6 44.7 67.3 51.7 52.9 52.9 0.2

Share of flats in dwelling stock 4.2 3.4 3.5 3.7 3.7 4.6 4.9 2.0

Ratio of houses in new dwelling approvals na 0.8 0.9 0.7 0.7 0.8 0.8 0.0

Adults per occupied dwelling 2.2 2.1 2.1 2.2 2.2 2.2 2.2 0.2

Table 2.11 Housing affordability – Moreton Bay

Housing indicator 1991 1997 2001 2008 2012 2015 2016

Average growth 1997 to

2016 (%)

Average established dwelling price ($cvm '000s) 163391 180763 196393 423551 396282 400143 402095 4.3

Average adjusted household income per occupied dwelling 65553 64067 64489 94031 112728 108045 109416 2.9

Ratio of adjusted dwelling price to adjusted average household disposable income 2.5 2.8 2.8 3.9 3.8 3.7 3.6 1.4

Average household income from labour market catchment 27694 29714 31413 38782 39791 35306 33432 0.6