Embed Size (px)

Citation preview

In this issue:

7 The Investment Roundtable:Recasting the Municipal Story

A Letter From Marc D. Stern, Chief Investment Officer

Dear Client,

Sometimes it’s the smaller things that move markets.

To be sure, the enormity of the events in Japan, Egypt, Libya, andNew Zealand caused widespread turmoil and human suffering,appropriately garnering worldwide news coverage in the first fewmonths of 2011. But it was resilient corporate profits that quietlypowered equity markets higher.

Asset prices could fall substantially if the news gets bad enough in the Middle East (e.g., Saudi oil supply interruption) or Japan (e.g., widespread nuclear contamination). But if the worst-case scenarios are avoided, we see ample justification for the S&P 500Index to achieve our full-year target of 1400 (up from 1257 at year-end 2010).

Our investment objective is to participate in these gains by emphasizingglobal securities we see as underpriced, while limiting downside riskalong the way by employing various diversifying strategies.

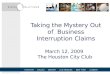

Companies Sharing the Wealth The global economy has healed from its devastating seizure two years ago. Indeed, world trade has risen 30% since 2009 to a recordhigh. Quarter-to-quarter growth figures will fluctuate widely, and first-quarter U.S. GDP will likely come in on the weaker side in the face of higher gasoline prices. But we remain convinced a double-dip recession is unlikely. Particularly encouraging is the substantial improvement we have seen in corporate sentiment, asshown in Exhibit 1, where readings have signaled global expansionsince mid-2009.

April 2011

Quarterly Investment PerspectiveState of Affairs

Visit us on the web at www.bessemer.com.

Exhibit 1: Continued Improvement in CorporateSentimentGlobal Purchasing Managers Index

As of March 31, 2011.Source: Institute for Supply Management, JP Morgan Chase & Co., Bloomberg

It is easy to see why corporate leaders are feelingbetter. Helped by growing global economic activity,rising productivity, and ready funding for majorcompanies, corporate profitability appears ontrack for a third consecutive year of strong gains.What was initially a bounce sparked by zealouscost cutting has migrated into a full-fledged profitboom characterized by meaningful revenue growth.

This earnings strength has surprised most investors.Indeed, consensus analyst estimates have beenrevised upward for 21 consecutive months.

It has also surprised business leaders, who didn’tbudget for big profit gains in an uncertain economicenvironment. As a result, most industries wereunusually slow to deploy their increased cash flow. But rebounding business activity eventuallynecessitates increases in production capacity to fulfill customer orders and maintain competitiveposition. That day appears to have arrived. Capitalspending has increased 13% over the last 12months, with additional advances likely for thenext several quarters.

Will this translate into more jobs? Evidence ismounting that the overall employment picture hasmeaningfully improved since the darkest days in

mid-2009. Layoffs have fallen 39%, the unemploy-ment rate has dropped from 10.2% to 8.8%, andprivate-sector payrolls have expanded by 1.5 million.Moreover, corporate surveys reveal a pickup in hiring intentions. Nevertheless, the unemploymentrate will likely remain elevated for at least the nextfew years, in part because the extended joblessnessof many former workers dims their prospects oflanding an acceptable position.

Rebounding boardroom confidence has alsorewarded investors with rising payouts. In the firstquarter, companies repurchased 140% more of theirown stock than in the same period one year ago. Weare even more gratified by another development:the number of dividend hikes has returned to thehigh levels last seen five years ago (Exhibit 2).

Exhibit 2: Boardrooms Boost PayoutsNumber of S&P 500 Companies Raising Dividends

As of March 31, 2011.Source: Standard & Poor’s

Even as stock prices have appreciated, corporateprofit growth has enabled valuations to remainattractive. Most global equity markets trade atabout 13 times expected earnings, somewhatbelow historical norms. This figure translates intoa 71/2% stock earnings yield, which represents an unusual premium versus government bondyields of about 31/2%. At current prices, moststocks will likely generate meaningfully higherreturns than most bonds over the next few years.

A Letter From Marc D. Stern, Chief Investment Officer

2 Bessemer Trust Quarterly Investment Perspective

30

35

45

40

55

50

60

65

2004 111005 06 07 08 09

Inde

x

Growth

Contraction

90

Q1 2004

116

Q1 2005

111

Q1 2006

103

Q1 2007

95

Q1 2008

55

Q1 2009

78

Q1 2010

117

Q1 2011

A Letter From Marc D. Stern, Chief Investment Officer

Lurking Hazards While we see abundant sources of strength, this isno time for unrestrained optimism. Numeroustrouble spots are evident.

Middle East/North Africa turmoil. It is impossible topinpoint all of the eventual implications of develop-ments unfolding in this troubled region. At thisstage, though, the rising oil prices sparked bytumult in Egypt and Libya appear unlikely to derailglobal economic expansion. For example, as shownin Exhibit 3, U.S. consumer spending on energycurrently remains within historical norms. Butpotential for greater trouble exists, including thepossibility of armed conflict across the region. Aspike in oil prices to the $145 per barrel levelreached in 2008, if sustained, would likely lead to recession. Critical to avoiding this outcome isstability in Saudi Arabia, home to 20% of knownglobal oil reserves and one of the few countries withspare production capacity. High unemploymentamong young Saudis suggests the need for changesbeyond the benefit packages announced recently bySaudi leaders, but we expect the country’s policiesto evolve gradually.

Exhibit 3: Increasing U.S. Energy SpendingEnergy Costs as a Percentage of Personal Income

As of December 31, 2010.Cost of energy consists of gasoline, electricity, gas, and other energygoods as percentage of personal income.Source: Bureau of Economic Analysis

Japan disaster. Beyond the tragic human implicationsof the earthquake and tsunami, power interruptionsand physical damage have caused shortages of certain products, including electronic componentsused in automobiles and cellphones. These eco-nomic disruptions will likely prove manageable,provided the crippled Fukushima electric plants donot inflict widespread damage on the country’slargest cities. Nevertheless, we foresee two lastingimplications. First, openness to expanding nuclearpower will likely diminish globally, potentiallyraising demand for coal, oil, and natural gas. Second,while Japan has the ability and commitment torebuild and recover, the cost of reconstruction will add significantly to the country’s fiscal woes.Government debt as a percentage of GDP, alreadyamong the world’s highest, appears sure to increasefurther, intensifying the risk of a fiscal crisis over time.

Europe debt concerns. The region continues to wrestle with sovereign debt problems and widedivergences among the 17 euro-zone countries. Thefirst quarter saw additional credit-rating down-grades, higher bank loan-loss projections, politicalturmoil in Ireland and Portugal, and an electoralsetback for Germany’s ruling party, raising the risk of a euro breakup. Yet incentives remain forpreserving the monetary union. These includeheightened economic clout for the region, as wellas substantial interconnections such as $700 billionin loans to Greece, Ireland, Portugal, and Spain onthe books of German banks. The region’s economicdata modestly improved in the first quarter, andgovernment leaders made some progress toward aunified crisis resolution program. But a favorableoutcome for the euro is unlikely unless Europeanpolicymakers adopt far-reaching policy changesthat place regional interests over those of individualcountries. In our view, necessary actions includeincreased fiscal restraint, greater fiscal union, mark-downs on bonds where issuers no longer can affordfull repayment, and a possible reduction in the sizeof the euro zone to save it.

April 2011 3

%

2.5

3.5

4.5

5.5

6.5

7.5

101975 80 85 90 95 00 05

Inflationary pressures. Even as the case for deflationis bolstered by the many lenders who don’t wish to lend and the many borrowers who don’t wish to borrow, we believe inflationary pressures areincreasingly gaining the upper hand. We don’t foresee hyperinflation, but inflation rates will likelymove somewhat higher over the next few years. TheFederal Reserve faces enormously difficult questionsabout when and how to withdraw its extraordinarystimulus efforts. While acting abruptly couldprompt an economic slowdown, waiting too longcould spur even more painful adjustments later. We’reon the side of gradual tightening that commences in2011 and plays out over the next two years or so.Policymakers’ challenges are even greater in manyemerging-market countries, where consumers areespecially vulnerable to rising food costs. A 50%increase in grain prices over the last year has raisedthe risk of civil unrest and compelled many centralbankers outside the U.S. to raise interest rates tolimit inflation.

China property bubble. Runaway bank lending hasled to unhealthy levels of speculation, including a35% increase in real-estate development last year.Many uneconomic projects have been funded, likelyleading to substantial write-offs down the road.While we shouldn’t underestimate the ample skilland flexibility of Chinese policymakers who haveoverseen the country’s remarkable economicgrowth, they now face the difficult task of coolingoff frenzied activity while maintaining necessarygrowth to create needed jobs. First-quarter eco-nomic data suggests that tightened rules on banksand homebuyers have begun to temper speculation.But further policy tightening is likely. Indeed, weexpect periodic scares as policies appear to over-shoot before being adjusted, especially with addeduncertainty accompanying the selection next yearof a new leader to replace President Hu Jintao.

U.S. housing weakness. Home prices fell another4% over the last six months, bringing their cumulative drop since 2007 to 30%. While new

delinquencies are slowing, a housing recovery willbe delayed by a substantial overhang of excessinventory. Indeed, the home vacancy rate hasdropped only slightly since peaking in 2008, suggesting that new construction will remaindepressed for several more years. These realitieswill continue to restrain U.S. economic growth,but they are unlikely to crush it. After all, residentialinvestment has come down to the lowest percent-age of GDP since 1933, and financial institutionshave already marked down their mortgage assets.

U.S. budget woes. Federal debt in relation to overallGDP is at its highest level in 50 years. At somepoint, legislators will act. The only question iswhether they will do so before a financial crisisdevelops, or afterwards. Much of the debate duringthe first quarter centered on discretionary categoriesincluding education, housing, research, and publichealth, which comprise just 14% of total spending.Lasting solutions will require adjustments to bigger categories like defense, healthcare, andSocial Security, which total two-thirds of totalspending. Headed by Erskine Bowles and AlanSimpson, the president’s deficit commission provid-ed a thoughtful roadmap in December, includingreduced government spending and a restructuredtax code. Representative Paul Ryan and PresidentObama proposed separate plans in early April.Restoring the country’s long-term fiscal health isachievable, but it represents a big test for the U.S.system of government, which often acts after a crisis compels a response. Perhaps both partieshave gotten the message from voters that it is timeto take appropriate action. If not, we foresee theTreasury bond and currency markets delivering astern warning to legislators within the next two years.

None of these risks are likely to deliver a knockoutblow to the markets. But upside return potentialwill likely be capped by higher interest rates, lingering European debt problems, heated debate in the U.S. Congress about fiscal reform, and upsand downs in China’s growth trajectory. As these

A Letter From Marc D. Stern, Chief Investment Officer

4 Bessemer Trust Quarterly Investment Perspective

issues play out, investor unease is bound to remainhigh. Indeed, a lengthy period when investors feelunusually dependent on global policymakers takingreasonable steps will likely restrain the valuationsthey feel comfortable paying for growth-orientedassets. The current setting reinforces our longstandingcommitment to absorbing volatility through broaddiversification that avoids concentrating investmentsin any one company, sector, geography, or asset class.

Positioning Portfolios Coming into 2011, our expectations for the investinglandscape led us to four priorities:• protect against a potential interest rate rise;• broaden global currency diversification;• achieve greater inflation protection; and• emphasize global growth prospects.

As a result, we shifted our recommended asset allocation by reducing fixed income, initiatingStrategic Currency, increasing Real Return, andtrimming U.S. equities in favor of non-U.S. small-cap stocks managed by London-based firmMondrian Investment Partners Limited.

We are convinced our current positioning is consistentwith our objective of participating in potential marketgains over time, while limiting downside risk.

At the center of our aggressive investments areglobal equities, which make up 43% of our flag-ship Balanced Growth allocation. Among ourlargest equity holdings are industrial and technologycompanies with strong competitive positions inrapidly growing emerging-market countries.

We achieve substantial diversification in the fol-lowing ways:• Cash and high-quality bonds (represents 23% ofBalanced Growth);

• Strategic Currency1 (5%), which emphasizescountries with sound fiscal policies, strong tradepositions, and favorable growth prospects;

• Inflation-linked investments (8%), includingcommodities and commodity-related equities,particularly in agricultural products, energy, andindustrial materials; and

• Investments that we believe offer attractive return potential with meaningfully less volatilitythan the equity markets (21%), such as creditinvestments (e.g., corporate bonds including convertibles and high-yield, mortgage-backedsecurities, and emerging-market governmentbonds) and hedge funds.

All three of our overall model portfolios deliveredpositive returns in the first quarter. During thethree-month period when equity markets delivereda winning performance, our more protective holdingsacross diverse asset classes restrained our gains.Overall, our flagship Balanced Growth model portfolio returned 3.2% for the quarter, in line withthe Global Balanced Growth Index return.

Each of the components of our model portfoliosdelivered positive returns in the first quarter. The largest gains were in Global Small & Mid Cap, Global Opportunities, U.S. Large Cap, RealReturn, and Non-U.S. Large Cap. Smaller returnscame in Strategic Currency and Fixed Income. Thesereturns were generally in line with their respectivebenchmarks, although Global Opportunities outper-formed (helped by strength in corporate credit)while U.S. and Non-U.S. Large Cap underperformed(hurt by weakness in technology holdings).

Ultimately, though, our focus is on delivering superior long-term returns with controlled volatility,as reflected in Exhibit 4.

It is particularly important in today’s complexinvestment environment to maintain a broad perspective. We rely on three sources to help usunderstand the interconnections at play around theworld, whether relating to economic activity, policy

A Letter From Marc D. Stern, Chief Investment Officer

April 2011 5

1As of March 31, 2011, Strategic Currency was invested in the Norwegian krone, Hong Kong dollar, Singapore dollar, and South African rand. While theseinvestments are currently implemented through bank deposits at The Bank of New York Mellon, they are subject to significant fluctuations in value andare not FDIC insured.

decisions, or corporate profits: 1) our analysts whoperform independent global research; 2) third-partyspecialists such as independent economists, politicalanalysts, and firms trading physical commodities;and 3) the external managers on whom we rely fortheir expertise in certain specialized asset classes.The timely and valuable insights we garner fromthe combination of these sources ensure we have afull perspective on the broad investment landscape.I look forward to updating you on our strategiesand results in the coming quarters.

Sincerely,

Marc D. SternChief Investment Officer

A Letter From Marc D. Stern, Chief Investment Officer

6 Bessemer Trust Quarterly Investment Perspective

The Bessemer Balanced Growth Portfolio represents a model portfolio comprised of U.S. Large Cap, Non-U.S. Large Cap, Global Opportunities, Global Small& Mid Cap, Real Return, Fixed Income, Strategic Currency, and three Bessemer hedge funds of funds. Investments cannot be made directly in this modelportfolio. Relative weightings vary over time. Returns for Old Westbury Global Opportunities Fund, Old Westbury Global Small & Mid Cap Fund, Old WestburyReal Return Fund, and Bessemer hedge funds of funds are after all fees and expenses. All other returns reflect performance of Bessemer Common TrustFunds and are before fees and expenses. The results also include the reinvestment of all dividends and capital gains. Returns for hedge fund of funds arepreliminary and subject to change.

The Global Balanced Growth Index represents a mix of the Barclays Capital U.S. Government/Credit Index (25%), S&P 500 Index (15%), S&P Global Largeex-U.S. Index (10%), S&P Global Small & Mid Cap Index (14%), S&P Global Large & Mid Cap Index (14%), Real Assets (7% consisting of Dow Jones-UBSCommodity Index [5%] and Barclays Capital U.S. TIPS Index [2%]), Hedge Funds (10% consisting of S&P Global Broad Market Index (Hedged) [7%] andBarclays Capital U.S. Government Index [3%]), and 3-Month Treasury bills (5%) after 12/31/2010 and a mix of the S&P 500 Index (25%), S&P Mid Cap400 Index (10%), MSCI EAFE Index (14%), MSCI World Small Cap Index (5%), MSCI Emerging Markets Index (3%), HedgeFund.net Fund of FundsAggregate Index (10%), Dow Jones-UBS Commodity Index (2.5%), Barclays Capital U.S. Government/Credit Index (25%), Barclays Capital U.S. TIPS Index(2.5%), and 3-Month Treasury bills (3%) before 1/1/2011.

The U.S. Stock/Bond Mix (70/30) is a composite of 70% S&P 500 Index and 30% Barclays Government/Credit Bond Index.

Index information is included herein to show the general trend in the securities markets during the periods indicated and is not intended to imply that anyreferenced portfolio is similar to the indices in either composition or volatility. Index returns are not an exact representation of any particular investment,as you cannot invest directly in an index.

Exhibit 4: Performance Overview Annualized Returns

Ended March 31, 2011 Volatility

First Quarter2011 1 Year 3 Years 5 Years 3 Years 5 Years

Bessemer Balanced Growth Portfolio 3.2% 12.8% 4.0% 5.0% 13.2% 10.9%Global Balanced Growth Index 3.1 12.3 3.3 4.3 15.1 12.2

U.S. Stock/Bond Mix (70/30) 4.2 12.9 3.6 3.9 15.7 12.7

S&P 500 Index 5.9 15.6 2.4 2.6 21.9 17.9As of March 31, 2011. Past performance is no guarantee of future results.See below for a complete description of Bessemer’s Balanced Growth Portfolio and benchmarks. Volatility is measured by annualized standard deviation of monthly returns. This figure is most meaningful over multiyear periods. Source: Barclays Capital, Dow Jones, Federal Reserve, HedgeFund.net, Morgan Stanley Capital International, Standard & Poor’s, UBS

April 2011 7

The Investment Roundtable: Recasting the Municipal Story

Phyllis E. King, Fixed Income Credit Analyst

David W. Rossmiller, Head of Fixed Income

Bruce A. Whiteford,Municipal Bond Portfolio Manager

The $3 trillion municipal bond market has received afair amount of notoriety lately, with some commentatorspredicting a surge of defaults and harrowing losses forinvestors. Three members of Bessemer’s fixed incometeam discuss the current state of municipal finances,the outlook for municipal bonds, and why the press isgetting much of the story wrong.

Q: Why have municipal bonds been getting so muchattention lately?

Rossmiller: Because many of the state and local gov-ernments that have issued these bonds are in difficultfinancial straits. Tax revenues, which decreasedsharply during the recent recession, remain below2008 levels. Healthcare and pension costs — amongthe largest liabilities for these governments — contin-ue to rise. And proposed spending cuts have attracteda firestorm of controversy in states such as New Jerseyand Wisconsin. To make matters worse, states are nolonger able to rely on the roughly $150 billion theyreceived in aid from the federal government over thepast two years as part of the 2009 stimulus package.For the 2012 fiscal year, 44 states are projectingbudget deficits of a collective $125 billion.

Several notable commentators and members of themedia have taken the story and run with it. MeredithWhitney — a bank analyst most well known for heraccurate prediction in 2007 of an impending banking-sector collapse — appeared on CBS’s “60 Minutes”in December forecasting a coming municipal crisischaracterized by hundreds of billions of dollars worthof defaults. She called the issue the largest threat tothe U.S. economy. Meanwhile, other media reportshave been dire or sensational. One recent headline

likened the municipal-bond market to a “Molotovcocktail” that “could explode,” while another issuedthe warning: “Muni Bond Chaos Imminent.”

Q: Some commentators have called the situation formunicipal bonds “the next subprime crisis.” Wouldtroubles in the municipal market reverberate to the restof the economy like the last financial crisis?

Rossmiller: It’s not likely. Banks’ exposure to theseinvestments is much less than it was to mortgagesduring the subprime debacle. In fact, according tothe Federal Deposit Insurance Corporation, onlyabout 1.4% of banks’ total assets are tied up inmunicipal bonds, compared to roughly 10% formortgage-backed securities in 2007 at the beginningof the financial crisis. This suggests that municipalbonds pose less systemic risk to the broader economy.

Also, because municipal bonds are tax exempt,roughly two-thirds of all these bonds are held by individuals. Among the remaining third ofbondholders, insurance companies are one of thelargest constituents. These firms aren’t particularlyhard-hit by falling municipal bond prices becausethey almost always hold these bonds to maturityand therefore aren’t required to take a paper lossin the interim.

Q: How have investors reacted to the news reports?

Whiteford: With their feet. From early November2010 to the end of February 2011, investors pulleda net $25 billion from municipal bond funds, withover $9 billion of that coming in December alone(Exhibit 5). Though the pace of outflows hasrecently begun to ease, the flow of funds is still neg-ative. In fact, according to the Investment CompanyInstitute, the week of March 23 represented the 20thconsecutive week that investors had withdrawnmore from muni-bond funds than they had added.

Exhibit 5: Investors Are Fleeing Municipal Bond Mutual Fund Flows

As of February 28, 2011.Source: Investment Company Institute

Q: Are state and local governments indeed on the pathto insolvency?

Rossmiller: It doesn’t appear so. For all of the negative news surrounding the municipal-bondmarket, there are many positive signs being overlooked. Take tax revenues, for instance. Stateand local collections have increased for each of the past four quarters (Exhibit 6). Improvementsin the retail environment, higher employment levels, and strong corporate earnings — as well asincreased tax rates in some cases — have broughtabout a corresponding rise in sales, income, andcorporate tax revenues.

Equally important has been policymakers’ reneweddetermination to cut spending — something thatwould have been much more difficult in previousyears before there were more obvious signs of fiscal crisis. For example, California’s Democraticgovernor recently proposed a budget 17% lowerthan the state’s 2008 peak, and nationwide, stategeneral-fund spending in 2010 was down an averageof 11% — helped in part by federal stimulus funds.

Exhibit 6: Revenues Are ImprovingState Personal Income Taxes

As of December 31, 2010 (updated quarterly). Reflects year-over-yearcalculation for quarterly change in revenues.Source: National Association of State Budget Officers, Strategas ResearchPartners, U.S. Census Bureau

As unpleasant as some of these austerity measuresare for local governments, social service recipients,and other groups, they nonetheless demonstratethat policymakers are willing to make the difficultdecisions to address financial problems that havebeen festering for years.

Whiteford: Another important thing to keep in mindis that municipal debts are relatively small whencompared to the debts of sovereign countries. To putit in perspective, Illinois, which is considered one ofthe most financially troubled states in the countryright now, has outstanding debt equal to roughly13% of its GDP. Greece’s debt, by contrast, is over 140% of its GDP — and that doesn’t includeits pension liabilities.

Rossmiller:None of this takes away from the fact thatmany governments face daunting challenges today.Indeed, it will take time for them to sort out lingeringfinancial problems — but for the vast majority ofthem, that likely won’t mean becoming insolvent.

The Investment Roundtable: Recasting the Municipal Story

8 Bessemer Trust Quarterly Investment Perspective

2007 10 110908(12)

(6)

(4)

(2)

0

2

4

6

8

(10)

(8)

10

$ B

illio

ns

1Q08 4Q103Q102Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10(30)

(25)

(20)

(15)

(5)

(10)

0

5

10

15%

Q: What about pension and healthcare liabilities?

King: There’s no denying they represent a seriouschallenge. The combination of recent stock marketdeclines, an aging workforce, and a lower number ofnew government employees paying into the systemis making it difficult for many state and local governments to keep the promises they’ve made to workers. Estimates of state and local unfundedpension liabilities go as high as $3 trillion.

But it’s important to remember that pensions arelong-term obligations. Although addressing annualoperating deficits requires near-term solutions,pensions can be addressed over years and evendecades. The pension problem doesn’t warrant anemergency response but rather a series of definitivesteps over a number of years.

And many states are beginning to take the necessaryaction, including creating new-employee tiers thatrequire higher retirement age and service require-ments, increasing employee contributions, prohibitingpost-retirement benefit increases, and limiting cost-of-living adjustments. For example, New Mexicoand Mississippi have sought to require higher pension contributions from existing employees, andColorado, Minnesota, and South Dakota have votedto tone down cost-of-living increases for pensioners.

Some governments are also moving away fromdefined-benefit plans toward defined-contributionplans — meaning 401(k)-type plans. Moreover,Congress has introduced legislation potentiallyrequiring state and local governments to use more conservative rates of return when estimating their public pension liabilities. All of this points to the fact that policymakers are beginning todemonstrate a willingness to confront the problemhead-on — something too often ignored in previous years.

Q: For those state and local governments that arestruggling, is bankruptcy a viable option?

Rossmiller: No. In fact, states cannot file for bankruptcy, and many states don’t allow local governments to file. Even those municipalities thatcan file rarely do for the following reasons:

Limited benefits. Bankruptcy courts do not permit amunicipality to override state laws (such as lawsrequiring voter approval for new or increased taxes).Moreover, courts cannot simply impose a workoutplan. If a workout plan cannot be agreed upon, thecase is dismissed, and the municipality retains itspre-bankruptcy problems.

Tarnished credit. Typically, bankruptcy severelycompromises a municipality’s much-needed accessto the capital markets. Even in the best case, themarket would likely exact a large penalty for yearsto come, increasing costs for taxpayers. Whereas abankrupt corporation may cease to exist after it hassettled with bondholders, a city can’t liquidate anddisappear. It will still need to raise money to pay forprojects in years to come. That gives governmentsextra incentive to prove to bondholders that they arecommitted to honoring their debt commitments.

Deference to states. Many states have their ownmeans of dealing with insolvent or fiscally stressedmunicipalities. Through control boards, receivers,and other means, states can impose control overmunicipalities (including their budgets) much moredirectly than a bankruptcy court can — and statesmost often become involved before financial stresstranslates into bond defaults.

Bankruptcy is rarely a good way for municipalitiesto cut costs or avoid dealing directly with their fiscal problems. It is nearly always better — andcheaper — to continue operating and negotiatesolutions, as difficult and headline-grabbing as this process tends to be.

The Investment Roundtable: Recasting the Municipal Story

April 2011 9

Q: Are the forecasts for massive bond defaults exag-gerated, then?

Whiteford:Yes. Defaults in municipal bonds are rare.No state has defaulted on a bond since the GreatDepression. As for local governments, from 1970 to2009, only 54 issuers rated by Moody’s defaulted.Furthermore, 42 of these defaults were in the higher-risk healthcare and housing project financesectors — sectors in which Bessemer’s municipalbond team does not invest. The reason these sectorstend to have higher default rates is that their projectsare often a) more subject to competition from theprivate sector, and b) easier for a city to walk awayfrom than, say, a project to finance a school oressential water system.

King: Historically, the 10-year cumulative defaultrate for investment-grade municipal bonds (ratedsingle-A or better) is a miniscule 0.06%; the figurefor corporate debt of equal rating is a much higher2.50% (Exhibit 7). Even in the event of a default,all is not lost: the recovery rate for bondholders historically is in the range of 85 cents on the dollar,twice that for corporate bondholders.

Exhibit 7: Default Risk Has Been Miniscule

Based on Moody’s study of 1970-2009 corporate and municipal defaultrates as well as 1987-2010 recovery rates for corporate bonds and1970-2009 recovery rates for municipal bonds.“Investment-Grade Default Rates” represents 10-Year Cumulative DefaultRates during 1970-2009.Source: Moody’s Investor Service

Whiteford: After Orange County, CA, defaulted andeventually filed for bankruptcy in the 1990s, it ulti-mately paid back every dime owed to bondholders.The reason the recovery rate is so high is becausemunicipalities know they can’t leave bondholders inthe lurch and expect to sell new debt in the future.

Q: But haven’t there been some notable bond defaultsrecently?

King:Yes, there have been. But if you look more close-ly at these bonds, it becomes apparent that many ofthem were on thin ice to begin with. Here’s a quicksummary of a few of the higher-profile defaults:

Las Vegas Monorail Corporation, Nevada. In 2000, aNevada state business agency sold $650 million ofbonds to finance an air-conditioned monorail thatwould take riders to different tourist spots in LasVegas. The bonds are secured by monorail fares andadvertising revenues, although bondholders arepaid after operating expenses for the monorail havebeen met. The project was fraught with difficultieswell before the recession struck, including a delayedopening, severe mechanical problems, and a three-month shutdown in 2004. Despite projections for21.6 million riders by 2010, only 5.2 million peopleactually rode the monorail that year. In 2009, themonorail generated $27 million in revenue andfaced $23 million in cash expenses — which left $4 million to cover $34 million in debt payments.In 2010, the corporation declared bankruptcy.

The Harrisburg Authority, Pennsylvania.An agency forthe City of Harrisburg (the capital of Pennsylvania),the authority issued municipal bonds to refurbish anincinerator designed to convert trash to energy. Tofinance this high-risk project at a lower cost, the cityguaranteed the bonds. In order to entice DauphinCounty — the county in which Harrisburg lies — touse the incinerator and therefore have its garbagehaulers pay the corresponding trash collection fees,

The Investment Roundtable: Recasting the Municipal Story

10 Bessemer Trust Quarterly Investment Perspective

Investment-Grade Default Rates Recovery Rates After Default

85%

Municipal

41%

Corporate

0.06%

Municipal

2.50%

Corporate

Harrisburg relinquished the right to raise feeswithout county approval except under “uncontrol-lable circumstances” — a definition still in dispute.When the project faced substantial delays and itscosts grew, the authority was forced to issue morebonds (over $200 million are outstanding) — whichincreased debt costs. However, the city had nopower to raise collection fees when the countyrefused to allow it, leaving the authority withoutenough revenue to pay principal and interest tobondholders. Faced with this situation — alongwith other financial problems stemming from highunemployment, poor management, and a stagnanttax base — Harrisburg refused to raise propertytaxes and defaulted on its guaranty to pay debtservice on the bonds. This forced Dauphin Countyand the bonds’ insurer to step in to make principaland interest payments.

Jefferson County, Alabama. The Alabama countyhousing the City of Birmingham recently defaulted onits obligation to make payments on $3.2 billion ofbonds issued to finance a massive, regulatory-drivencapital plan. The bonds are secured by fees paid byusers of a sewer system. Because of the actions ofseveral dishonest and incompetent city officials, thedebt was structured to involve complex interest-ratederivatives, which added strain to the county’sfinances when financial markets collapsed andinterest rates moved unfavorably. The county thenrefused to increase sewer rates to cover higher debtservice costs — thereby reneging on its obligation tobondholders. As a result, the bonds are currently indefault, and a massive stream of lawsuits suggests itwill be years before the situation is resolved.

Though these bonds have their differences, they allhave one thing in common: the financial difficultieseach issuer is facing can be attributed to flawed economic assumptions and poor decision makingon the part of municipal officials — well before theeconomic downturn began.

Q: How can Bessemer avoid troubled municipal bondssuch as these?

Whiteford: We rely on our disciplined, independentresearch. The following are some of the criteria thathelp us select bonds that are unlikely to be stressedby the problems in recent headlines.

Essential service bonds. We focus on bonds thatfinance essential governmental functions, such asthe provision of water services. These types ofbonds have a miniscule historic default rate. That’sbecause a municipality is more likely to shutter anonessential project like a monorail system than itwould stop the reconstruction of pipes deliveringwater to households.

Favorable bond provisions. We carefully examineeach bond’s legal provisions. For example, theremay be a limit on the dollar amount of bonds thatmay be issued per dollar of revenue pledged to repaybondholders. This type of provision determineshow much of a cushion bondholders have — thatis, to what extent pledged revenues would have tofall for debt service not to be paid back in full.

State-specific analysis. We develop our investmentpolicies on a state-by-state basis, taking into accounteconomic fundamentals, revenue diversity, flexibilityto raise revenues and make budgetary adjustments,the ability of voters to enact statutes or amend astate’s constitution via initiative, and the quality of management.

Attention to disclosures. We evaluate the timelinessand the quality of all the issuer’s financial disclosures.If there is a delay or the information provided isinadequate, we won’t approve the bond.

King: The municipal market cannot be painted witha broad brush because it’s enormously diverse.Municipal bonds finance everything from essentialgovernment functions such as roads or schools toprojects that are more prone to competition, such as

The Investment Roundtable: Recasting the Municipal Story

April 2011 11

the construction of a nursing home. This breadthmakes it possible to find high-quality bonds with theproper research and analysis — even in difficulttimes or troubled regions.

Q: Can you give any examples of bonds Bessemer findsattractive?

Whiteford: Sure. Although we invest in many typesof securities, the ones below illustrate the spirit ofwhat we look for in new purchases.

Special Tax Bonds. These bonds are secured by agross pledge of a selected revenue stream, in whichbond principal and interest must be paid before the revenues can be released for other purposes.Take, for instance, a bond secured by the MichiganState Trunk Line Fund, a state fund that collectsmotor vehicle-related taxes and fees. Despite thestate’s fiscal challenges, we like these bonds for several reasons. First, the bonds are backed bymotor-vehicle taxes and fees that have provided anice cushion for bondholders in boom and bustperiods alike. Second, the bonds’ legal provisionsrequire the state to use these revenues to pay bond-holders before other expenses. And third, the stateisn’t allowed to issue any additional bonds unlessthere are at least $2 of pledged taxes and fees onhand for every dollar of debt service due on thebonds. Currently, revenues are more than fourtimes what is needed to service the debt. In otherwords, these tax revenues would have to fall bymore than 75% from today’s levels for bondholdersnot to be paid in full.

Public Higher Education Bonds.We like many publichigher education bonds because a) these universitiesserve an important economic function, and b) theyhave a wide range of revenues at their disposal to

cover debts. One example is a bond issued by theUniversity of Montana. One of only two major stateuniversities in Montana, the school receives rev-enues from tuition, dining halls, parking facilities,dormitories, bookstores, state funding, and othersources. Importantly, the school can increase manyof these fees at will. Plus, current revenues are morethan double debt service.

Single Purpose District Bonds. Single purpose districtstypically have limited responsibilities, a broad baseof fees or taxes supporting them, and flexibleexpenditure bases that are relatively easy to adjustif revenues decline. Two current examples includegeneral obligation bonds issued by East Bay RegionalPark District, California, and Chicago Park District,Illinois. Both districts are responsible for maintain-ing parks and related facilities in their respectiveareas. While both face strict limits on how muchrevenue they can raise via property taxes, each hasbeen very proactive about controlling expenditures.As a result, both districts have maintained a solidfinancial profile despite the budgetary disarray inCalifornia and Illinois.

Enterprise Revenue Bonds. These bonds are issuedto finance essential government functions such asthe provision of water or electric services. Generally,the issuer can increase user charges to coverexpenses including debt service. In this sector, welike the Tallahassee Consolidated Utility SystemRevenue Bonds, which are secured by revenuesfrom water and sewer fees. Not only do the bondsbenefit from a relatively stable economy, but the cityregularly increases the rates it charges to customersto keep up with inflation and to service debt — a signof proactive management committed to maintainingsolid financial standing.

The Investment Roundtable: Recasting the Municipal Story

12 Bessemer Trust Quarterly Investment Perspective

Q: Are state and local government finances the only rea-sons behind recent weakness in the muni-bond market?

Rossmiller:No — in fact, there are two other factorshaving a greater effect on the market.

Monetary policy. Since 2008, the U.S. FederalReserve has flooded the U.S. economy with liquiditythrough “quantitative easing,” its program of purchasing bonds from banks using cash, with thehopes that banks would in turn lend this cash toconsumers and companies. Though the program’sgoal was to lower interest rates, after two roundsof quantitative easing totaling $1.5 trillion, 10-year interest rates are almost a full percentagepoint higher (Exhibit 8). Many bond investors aregrowing increasingly worried that this much excessmoney in the system will lead to inflation — whichbodes poorly for long-term bonds. That’s whythey’re demanding higher yields for municipal and taxable bonds alike — which has driven theirprices down.

Exhibit 8: Unintended Consequences10-Year Treasury Yield

As of March 31, 2011.Source: Federal Reserve

Build America Bonds. As part of the 2009 stimuluspackage, the federal government allowed state and local governments to issue special taxablebonds for which the federal government subsidized

interest payments. In 2009 and 2010, states tookadvantage of the program by issuing a flurry ofthese securities instead of tax-exempt bonds, whichlowered the supply of municipals (and raised theirprices). However, when this program was about to expire in late 2010, investors began to fear thata new wave of municipal bonds would flood themarket once governments could no longer rely on the federal subsidy. Anticipating this comingoversupply, many investors sold their muni-bondpositions late in the year and pushed up interestrates, which have remained elevated since.

Q: Has Bessemer made any changes to its bond portfo-lios in light of the evolving situation for bond markets?

Whiteford: Concern over an environment of risinginterest rates and inflation was one of the reasonswhy the team decided to lower the average durationof municipal portfolios from 8.2 in December 2010to 4.2 today. Duration is the measure of how mucha bond’s price will change given a 1% change ininterest rates. A lower duration will help protect ourclients’ capital and reduce volatility by making theportfolio less sensitive to downside price pressure asyields rise.

Q: What should investors bear in mind most aboutmunicipal bonds in the coming months?

Rossmiller: First, the muni-bond market is not onlyvast but also inefficient. Because these bonds don’ttrade on a centralized exchange as stocks do, unwaryinvestors can get shortchanged easily if they don’tunderstand each bond’s underlying credit qualityor the corresponding price it should fetch in theopen market. Also, the market’s enormous sizemeans that, even in distressed times, there areattractive opportunities for those investors with the experience and diligence to conduct in-depthresearch. That’s why we carefully research each bond,factoring in the issuer’s credit history, sources of

The Investment Roundtable: Recasting the Municipal Story

April 2011 13

Second round of quantitative easing announced2.0

2.5

3.0

3.5

4.0

Aug 10 Mar 11Sep 10 Oct 10 Nov 10 Dec 10 Jan 11 Feb 11

%

revenue, employment base, legal structure, and thequality of its disclosures, along with current marketconditions and monetary policy developments.

The second thing to remember is that, as interestrates and inflationary pressures begin to rise,municipal bonds as an asset class are likely to provide lower-than-usual returns in the periodahead. Yet despite these macroeconomic forces andfinancial challenges for state and local governments,we believe high-quality municipal bonds remain an important diversifier in an overall portfolio,providing a strong buffer during equity-marketsetbacks while offering attractive tax advantagesfor individual investors.

The Investment Roundtable: Recasting the Municipal Story

14 Bessemer Trust Quarterly Investment Perspective

Past performance is no guarantee of future results. This material is provided for your general information. It does not take into account the particularinvestment objectives, financial situation, or needs of individual clients. This material has been prepared based on information that Bessemer Trustbelieves to be reliable, but Bessemer Trust makes no representation or warranty with respect to the accuracy or completeness of such information. Thispresentation does not include a complete description of any fund or portfolio mentioned herein. Investors should consider the investment objectives, risks,charges, and expenses of each fund or portfolio before investing. Views expressed herein are current opinions only as of the date indicated, and are subjectto change without notice. Forecasts may not be realized due to a variety of factors, including changes in economic growth, corporate profitability, geopoliticalconditions, and inflation. The mention of a particular security is not intended to represent a stock-specific or other investment recommendation, andour view of these holdings may change at any time based on stock price movements, new research conclusions, or changes in risk preference. Indexinformation is included herein to show the general trend in the securities markets during the periods indicated and is not intended to imply that anyreferenced portfolio is similar to the indices in either composition or volatility.

THIS PAGE INTENTIONALLY LEFT BLANK

Atlanta • Boston • Chicago • Dallas • Denver • Los Angeles • Miami • NaplesNew York • Palm Beach • San Francisco • Washington, D.C. • Wilmington • Woodbridge

Cayman Islands • New Zealand • United KingdomVisit us at www.bessemer.com.

Copyright © Bessemer Trust Company, N.A. All rights reserved.