Embed Size (px)

Citation preview

Quaker Council for European Affairs – A Quaker Voice in Europe

The European Union Budget

Overview and Income

Quaker Council for European Affairs – A Quaker Voice in Europe

2

What we will look at

• Income sources

• Correction Mechanisms

• Alternative Income Sources

Quaker Council for European Affairs – A Quaker Voice in Europe

3

Income

Quaker Council for European Affairs – A Quaker Voice in Europe

4

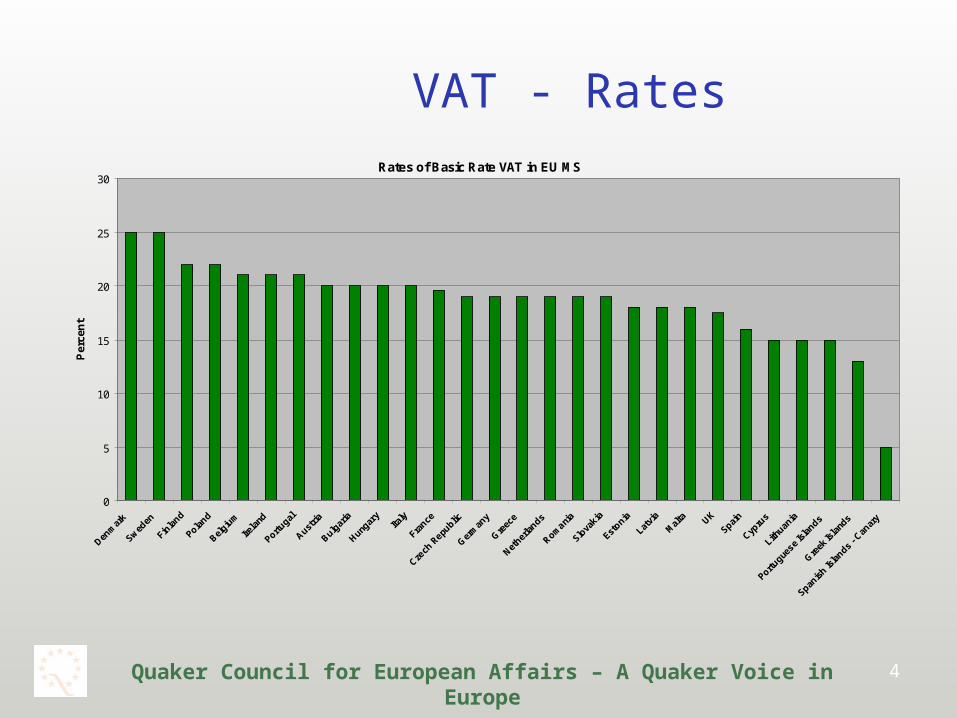

VAT - RatesRates of Basic Rate VAT in EU MS

0

5

10

15

20

25

30

Denm

ark

Swed

en

Finla

nd

Poland

Belgiu

m

Irela

nd

Portugal

Austria

Bulgar

ia

Hungar

yIta

ly

France

Czech

Repu

blic

Ger

man

y

Gre

ece

Nether

lands

Romani

a

Slova

kia

Estonia

Latvi

a

Mal

ta UK

Spain

Cypru

s

Lithuan

ia

Portugue

se Is

lands

Gre

ek Is

land

s

Spanis

h Isla

nds - C

anar

y

Per

cen

t

Quaker Council for European Affairs – A Quaker Voice in Europe

5

VAT – How many ratesNumber of

RatesCountries

6 Greece, Portugal, Spain (NB: each of them have three rates on the mainland and 3 different rates for their Islands – in Spain the Island rates apply in the Canary Islands but not in the Balearics

5 Lithuania

4 Ireland, Italy, Poland

3 Austria, Belgium, Bulgaria, Finland, France, theNetherlands, Sweden, UK

2 Cyprus, Czech Republic, Estonia, Germany, Hungary,

Latvia, Malta, Romania, Slovakia

1 Denmark

Quaker Council for European Affairs – A Quaker Voice in Europe

6

GNI

• Why GNI and not GDP?

• Flaws of GDP

• Is it an ‘own resource’?

Quaker Council for European Affairs – A Quaker Voice in Europe

7

Income

Quaker Council for European Affairs – A Quaker Voice in Europe

8

What does it all cost?

EU B as Budget as Percentage of GNI

0.96%

0.98%

1.00%

1.02%

1.04%

1.06%

1.08%

1.10%

1.12%

2007 2008 2009 2010 2011 2012 2013

Quaker Council for European Affairs – A Quaker Voice in Europe

9

Who pays and who gains?

• Flows from each country to EU

• Flows from EU to each country

• Is it a relevant question?

Quaker Council for European Affairs – A Quaker Voice in Europe

10

What does it all cost?Net contribution/ benefit per head of population

-200.00

-100.00

0.00

100.00

200.00

300.00

400.00

500.00

Net

herlan

ds

Swed

en

Den

mar

k

Ger

man

y

Belg

ium

Luxe

mbo

urg

Fran

ce

Finl

and

Aus

tria

Uni

ted

Kin

gdom

I tal

y

Czec

h Rep

ublic

Slov

akia

Slov

enia

Pola

nd

Spai

n

Hun

gary

Latv

ia

Cypr

us

Esto

nia

Lith

uani

a

Portug

al

Mal

ta

I rel

and

Gre

ece

Quaker Council for European Affairs – A Quaker Voice in Europe

11

Who pays and who gains

• Net contributors 1997 to 2006– Germany– Netherlands– United Kingdom– France– Italy– Sweden– Belgium– Austria– Denmark– Luxembourg– Finland

Quaker Council for European Affairs – A Quaker Voice in Europe

12

Who pays and who gains?

• Net Recipients 1997 to 2006– Ireland– Portugal– Greece– Spain

Quaker Council for European Affairs – A Quaker Voice in Europe

13

New Member StatesNew Member States - Net Revenue from EU 2004 to 2006

0.0 500.0 1,000.0 1,500.0 2,000.0 2,500.0 3,000.0 3,500.0

2004

2005

2006

Malta Cyprus Slovenia Estonia Latvia Slovakia Czech Republic Lithuania Hungary Poland

Quaker Council for European Affairs – A Quaker Voice in Europe

14

What is fair?Comparison between purchasing power and net contribution/ receipt - 2006

-200

-100

0

100

200

300

400

500

600

700

Luxe

mbo

urg

I rel

and

Denm

ark

Nethe

rland

s

Austria

Belg

ium

Unite

d Kin

gdom

Finl

and

Swed

en

Germ

any

Fran

ceI t

aly

Spai

n

Cypr

us

Greec

e

Slov

enia

Czec

h Rep

ublic

Portug

al

Mal

ta

Esto

nia

Hunga

ry

Slov

akia

Lith

uani

a

Latv

ia

Pola

nd

Purchasing Power Net contribution/receipt per head of population

Quaker Council for European Affairs – A Quaker Voice in Europe

15

Corrective Measures?

• UK Rebate and how it is financed – two different issues

Quaker Council for European Affairs – A Quaker Voice in Europe

16

Corrective Measures

Why a UK Rebate?• Small agricultural sector (comparatively)• High VAT base• High net contributor• Rebate = € 4.6 bn average per annum• UK contribution after rebate = € 2 bn pa• UK 3rd highest net contributor (total)• UK 10th highest net contributor (per capita)

Quaker Council for European Affairs – A Quaker Voice in Europe

17

How is it financed?

Quaker Council for European Affairs – A Quaker Voice in Europe

18

What has changed?

• Rebate in place since 1982• CAP now smaller part of budget• VAT now smaller part of income

calculation• New Member States – different

balance of economic power• UK economy very strong• Rebate predated German reunification

Quaker Council for European Affairs – A Quaker Voice in Europe

19

Alternative Sources of Income

Principles

• Based on EU values• Transparency• Based on EU priorities• Link to citizens – accountability

Quaker Council for European Affairs – A Quaker Voice in Europe

20

More of the same?

• Keep current own resources

• Increase the share of VAT that goes to the EU

• Top up with a GNI based formula

Quaker Council for European Affairs – A Quaker Voice in Europe

21

Something new – an EU Tax?

Principles of good taxation:• simple and transparent• buoyant • broad based• low marginal rate• It should deliver ‘horizontal equity’• It should deliver ‘vertical equity’

Quaker Council for European Affairs – A Quaker Voice in Europe

22

Something new – an EU Tax?

Issues at EU level with national taxation:• Horizontal tax competition. • Vertical tax competition • Can distort investment decisions• Can distort decisions on location of

employment• Can distort shopping decisions

especially in border regions

Quaker Council for European Affairs – A Quaker Voice in Europe

23

Principles

Tax

Simple Buoyant

Broad Base

Low Marginal Rate

Horizontal Equity

Vertical Equity

VAT Depends on rate

No - regressive

Excise Duty Depends on other policies

Depends on rate

No - regressive

Eco taxes Depends on specifics

Depends on specifics

Depends on specifics

Depends on specifics

Depends on specifics

Communication Tax

No - regressive

Corporate Tax

Depends on rate

Personal Income Tax

Could be

Savings Tax Depends on specifics

Could be