Embed Size (px)

Citation preview

Ithaca Energy Inc. Q3 2014 Financial Statements

Q3 2014CONSOLIDATED FINANCIAL STATEMENTS

1

Ithaca Energy Inc. Q3 2014 Financial Statements

Consolidated Statement of IncomeFor the three and nine months ended 30 September 2014 and 2013

(unaudited)

Restated* Restated*

Three months ended 30 Sept Nine months ended 30 Sept

Note

Revenue 5

- Operating costs 6

- Oil purchases

- Movement in oil and gas inventory 6

- Depletion, depreciation and amortisation EXP04

Cost of sales

Gross (Loss)/Profit

Exploration and evaluation expenses 12

Impairment of assets

- Administrative expenses

- Non-recurring Valiant acquisition costs

Total Administrative expenses 7

Operating (Loss)/Profit

Foreign exchange

Gain/(Loss) on financial instruments 29

Release of exploration obligation 19

Negative goodwill

Profit Before Interest and Tax

Finance costs 8

Interest income

Profit Before Tax

Taxation 27

Profit After Tax

Earnings per share

Basic 26

Diluted 26

* Refer to Note 2, Basis of Preparation for further details on the nature of the restatement.

The accompanying notes on pages 6 to 24 are an integral part of the financial statements.

-

27,038

114,112

30,866

2,212

(1,518)

(81,219)

(4,956)

(15,814)

32,893

(509)

(1,518)

-

8,183

-

24,98243,143

46

31,989

5,978

(10,866)

(21,865)

-

3

34,960

39,913

12,092

5,219

19,763

0.34

0.08

0.08 0.13

0.14

45

107,937

100,445

55,333

No separate statement of comprehensive income has been prepared as all such gains and losses have been incorporated in the

consolidated statement of income above.

39,229

22,649

120,125

(7,492)

0.34

(12,233)

(277,573)

(5,472)

(612)

US$'000

0.02

0.02

289,665

US$'000

2014

US$'000

2013

US$'000

2013 2014

(10,235)

-

137

22,649 2,190

47,478

(3,067)

302,241

(235,979)

(7,971)

(3,734)

66,262

(11,278)

(13,119)

(953)

(17,831)

(7,596)(11,278)

-

90,094

(25,809)

4,147

(3,734)

(103,586)

-

(13,492)

(270)

(68,819)

17,567

7,727

227

7,954

4

(9,844)

-

-

(111,925)

(981)

(108,275)

(121,580)

(161,979)

(46,207)

6,915

(34)

(41,893)

7,047

(1,061)

(37,809)

3,312 (14,798)

2

Ithaca Energy Inc. Q3 2014 Financial Statements

(unaudited)

Note

Current assets

Cash and cash equivalents CAS01

Restricted cash 9 CAS03

Accounts receivable 10 CAS02

Deposits, prepaid expenses and other CAS04

Inventory 11 CAS06

Derivative financial instruments 30 CAS10

Non current assets

Long-term receivable 32

Long-term inventory 11

Investment in associate 16

Exploration and evaluation assets 12

Property, plant & equipment 13

Goodwill 15

Total assets

LIABILITIES AND EQUITY

Current Liabilities

Trade and other payables 18 CLB01

Exploration obligations 19

Non current liabilities

Borrowings 17

Decommissioning liabilities 20 CLB04

Other long term liabilities 21 CLB03

Contingent consideration 23 CLB06

Derivative financial instruments 30 CLB07

Deferred tax liability 27

Net Assets

Equity attributable to equity holders

Share capital 24 SEQ01

Share based payment reserve 25 SEQ02

Retained earnings SEQ03

Shareholders' Equity

The accompanying notes on pages 6 to 24 are an integral part of the financial statements.

The financial statements were approved by the Board of Directors on 12 November 2014 and signed on its behalf by:

49,938

57,405

80,729

18,337

1,821,513

(491,938)

31,655

18,337

8,126

(486,345)

137,114

(199)

1,423,712

1,540,443

2,618,904

(17,820)

(323,658)

(893,110)

57,628

495,680

(5,593)

2,123,224

2014

Consolidated Statement of Financial Position

30 September

21,150

21,632

63,435

355,185

6,311

-

(1,233,856)

(143,964)

(551,632)

(4,000)

25,198

US$'000

59,048

(222,890)

US$'000

985

(12,859)

(485,255)

(472,396)

8,126

12,198

314,727

5,102

(6,037)

1,978,687

853,646

31 December

2013

(19,254)

"Jay Zammit"

Director

Director

"Les Thomas"

ASSETS

(830,681)

893,110

(32,122)

(535,716)

(853,646)

(298,676)

(432,243)

(15,550)

(4,000)

(9,909)

(639,786)

(172,047)

438,244

3

Ithaca Energy Inc. Q3 2014 Financial Statements

Consolidated Statement of Changes in Equity(unaudited)

Balance, 1 Jan 2013

Net income for the period

Total comprehensive income

Shares issued

Share based payment

Options exercised

Balance, 30 September 2013

Balance, 1 Jan 2014

Share based payment

Options exercised

Net income for the period

Balance, 30 September 2014

The accompanying notes on pages 6 to 24 are an integral part of the financial statements.

19,254

551,632 17,820

9,672-

323,658

(6,244)

-- 4,810

20,340

Retained

Earnings

US$'000

524,908

-

15,916

23,000

2,917

535,716

-

-

Share Based

Payment Reserve

100,445

153,990

93,005

298,676 853,646

Share Capital Total

605,648

US$'000US$'000

431,318

US$'000

20,340 - 100,445-

-585

254,435

93,005

431,318

-

(257)

-

802,343

328

254,435

-893,110

4,810

706,093

24,982 24,982

2,917

4

Ithaca Energy Inc. Q3 2014 Financial Statements

Consolidated Statement of Cash FlowFor the three and nine months ended 30 September 2014 and 2013

(unaudited)Restated* Restated*

Three months ended 30 Sept Nine months ended 30 Sept

Operating activities

Profit Before Tax

Adjustments for:

Depletion, depreciation and amortisation

Exploration and evaluation expenses

Impairment

Share based payment

Loan fee amortisation

Revaluation of financial instruments

Movement in goodwill

Gain on disposal

Gain on exploration obligation release

Accretion

Bank interest & charges

Valiant acquisition fees

Cashflow from operations

Net cash from operating activities

Investing activitiesAcquisition of Valiant

Cash acquired on acquisition of Valiant

Valiant acquisition fees

Acquisition of Cook

Acquisition of Summit

Capital expenditureLoan to associate

Proceeds on disposal

Net cash used in investing activities

Financing activitiesProceeds from issuance of shares

(Increase) / decrease in restricted cash

Derivatives

Loan (repayment)/draw down

Senior notes

Bank interest & charges

Net cash from financing activities

Currency translation differences relating to cash

Increase / (decrease) in cash & cash equiv.

Cash and cash equivalents, beginning of period

Cash and cash equivalents, end of period

The accompanying notes on pages 6 to 24 are an integral part of the financial statements.

* Refer to Note 2, Basis of Preparation for further details on the nature of the restatement.

-

-

161,549

-

33,390

-

69,860

- -

(7,925)

2014

- -

612

7,727

(22,321)

203

(25,931)

(569,678) (446,503)

2,190

9,673

(1,050) (3,249)

-

(22,133)

98,726

400,087

73,770

3,655

(73,139)

(200,636)

198,229

19,950

-

1,777

(22,321)

121,580

865

-

(33,495)

(55,333)

-

(2,190)

7,405

5,032

4,162

(196,943)

11,611

178,279

(305,638)

2013

107,937

- 12,60812,608 -

2,106

(2,365)

52,058

31,374

(18,555)

50,753

(865)

63,435

-

(139,304)

-

CASH PROVIDED BY (USED IN):

(163,541)

(16,787)

128,159

3,052

US$'000

34,960

63,136

US$'000

2014 2013

- -

13,312

550

37,809

(38,189)

26,325

11,242

77,785

7,0991,3751,543

-

46,206

(5,077)

37,567

(163,541)

-

-

-

-

1,316

5921,203

17,074

509 953

111,925 3,067

US$'000

5,219

US$'000

27,091

8,295

-

- (76,758)

(76,168)(260,562)

294,946

42,396

(4,275)

319,041

(3,226)

(12,876)

(8,321)

328

-

2,965

73,770

-

(8,370)

(75,157)

-

Changes in inventory, receivables and

payables relating to operating activities

Changes in receivables and payables relating

to investing activities

59,048

(2,816)232,155

46,679

929

-

-

2,949

-

(4,387)

59,048

58,123

-

(5,032)

(33,370)

-

7,971

300,000 300,000-

14,582

-

- 10,866

5

Ithaca Energy Inc. Q3 2014 Financial Statements

1. NATURE OF OPERATIONS

2. BASIS OF PREPARATION

3. SIGNIFICANT ACCOUNTING POLICIES, JUDGEMENTS AND ESTIMATION UNCERTAINTY

Basis of measurement

Basis of consolidation

A subsidiary is an entity which the Corporation controls by having the power to govern the financial and operating policies. The

existence and effect of potential voting rights that are currently exercisable or convertible are considered when assessing whether

Ithaca controls another entity. A subsidiary is fully consolidated from the date on which control is obtained by Ithaca and is de-

consolidated from the date that control ceases.

The consolidated financial statements have been prepared under the historical cost convention, except for the revaluation of

certain financial assets and financial liabilities (under IFRS) to fair value, including derivative instruments.

Ithaca Energy Inc. (the “Corporation” or “Ithaca”), incorporated and domiciled in Alberta, Canada on 27 April 2004, is a publicly

traded company involved in the exploration, development and production of oil and gas in the North Sea. The Corporation's

registered office is 1600, 333 - 7th Avenue S.W., Calgary, Alberta, Canada, T2P 2Z1. The Corporation's shares trade on the

Toronto Stock Exchange in Canada and the London Stock Exchange’s Alternative Investment Market in the United Kingdom under

the symbol “IAE”.

Business combinations are accounted for using the acquisition method. The cost of an acquisition is measured as the fair value of

the assets acquired, equity instruments issued and liabilities incurred or assumed at the date of completion of the acquisition.

Acquisition costs incurred are expensed and included in administrative expenses. Identifiable assets acquired and liabilities and

contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. The

excess of the cost of acquisition over the fair value of the Corporation's share of the identifiable net assets acquired is recorded as

goodwill. If the cost of the acquisition is less than the Corporation's share of the net assets acquired, the difference is recognised

directly in the statement of income as negative goodwill.

These interim consolidated financial statements have been prepared in accordance with International Financial Reporting

Standards (IFRS) applicable to the preparation of interim financial statements, including IAS 34 Interim Financial Reporting. These

interim consolidated financial statements do not include all the necessary annual disclosures in accordance with IFRS.

The consolidated financial statements of the Corporation include the accounts of Ithaca Energy Inc. and all wholly-owned

subsidiaries as listed per note 32. Ithaca has twenty-one wholly-owned subsidiaries, thirteen of which were acquired on 19 April

2013 as part of the acquisition of Valiant Petroleum PLC ("Valiant"), and four of which were acquired on 31 July 2014 as part of the

acquisition of Summit Petroleum Limited ("Summit"). The consolidated financial statements include the Valiant group of companies

from 19 April 2013 only and the Summit group of companies from 31 July 2014 only (being the respective acquisition dates.). All

inter-company transactions and balances have been eliminated on consolidation.

The condensed interim consolidated financial statements should be read in conjunction with the Corporation’s annual financial

statements for the year ended 31 December 2013.

The policies applied in these condensed interim consolidated financial statements are based on IFRS issued and outstanding as

of 12 November 2014, the date the Board of Directors approved the statements. Any subsequent changes to IFRS that are given

effect in the Corporation’s annual consolidated financial statements for the year ending 31 December 2014 could result in

restatement of these interim consolidated financial statements.

The financial statements for the period ended 30 September 2013 have been restated to reflect adjustments to the provisional fair

values attributed to the business combination accounting for the acquisition of Valiant Petroleum PLC in 2Q 2013. Subsequent

revisions disclosed within the 3Q 2013 and 31 December 2013 year end accounts are now reflected through 2Q 2013 (the time of

acquisition). Restatements have been reflected through negative goodwill and cost of sales.

Business Combinations

6

Ithaca Energy Inc. Q3 2014 Financial Statements

Goodwill

Capitalisation

Impairment

Interest in joint operations

Revenue

Foreign currency translation

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the

transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at

year end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in the statement of

income.

Goodwill acquired through business combinations is initially measured at cost, being the excess of the aggregate of the

consideration transferred and the amount recognised as the fair value of the Corporation's share of the identifiable net assets

acquired and liabilities assumed. If this consideration is lower than the fair value of the identifiable assets acquired, the difference

is recognised in the statement of income.

Goodwill is tested annually for impairment and also when circumstances indicate that the carrying value may be at risk of being

impaired. Impairment is determined for goodwill by assessing the recoverable amount of each cash generating unit ("CGU") to

which the goodwill relates. Where the recoverable amount of the CGU is less than its carrying amount, an impairment loss is

recognised in the statement of income. Impairment losses relating to goodwill cannot be reversed in future periods.

Items included in the financial statements are measured using the currency of the primary economic environment in which the

Corporation and its subsidiaries operate (the ‘functional currency’). The consolidated financial statements are presented in United

States Dollars, which is the Corporation’s functional and presentation currency.

The Corporation's interests in joint operations (eg exploration and production arrangements) are accounted for by recognising its

assets (including its share of assets held jointly), its liabilities (including its share of liabilities incurred jointly), its revenue from the

sale of its share of the output arising from the joint operation, its share of revenue from the sale of output by the joint operation and

its expenses (including its share of any expenses incurred jointly).

Interest income is recognised on an accruals basis and is separately recorded on the face of the statement of income.

Oil, gas and condensate revenues associated with the sale of the Corporation’s crude oil and natural gas are recognised when title

passes to the customer. This generally occurs when the product is physically transferred into a vessel, pipe or other delivery

mechanism. Revenues from the production of oil and natural gas properties in which the Corporation has an interest with joint

venture partners are recognised on the basis of the Corporation’s working interest in those properties (the entitlement method).

Differences between the production sold and the Corporation’s share of production are recognised within cost of sales at market

value.

Under the equity method, investments are carried at cost plus post-acquisition changes in the Corporation's share of net assets,

less any impairment in value in individual investments. The consolidated statement of income reflects the Corporation's share of

the results and operations after tax and interest.

Under IFRS 11, joint arrangements are those that convey joint control which exists only when decisions about the relevant

activities require the unanimous consent of the parties sharing control. Investments in joint arrangements are classified as either

joint operations or joint ventures depending on the contractual rights and obligations of each investor. Associates are investments

over which the Corporation has significant influence but not control or joint control, and generally holds between 20% and 50% of

the voting rights.

7

Ithaca Energy Inc. Q3 2014 Financial Statements

Share based payments

Cash and cash equivalents

Restricted cash

Financial instruments

Senior notes

Inventory

Trade receivables

Trade payables

Senior notes are measured at amortised cost.

Inventories of materials and product inventory supplies, other than oil and gas inventories, are stated at the lower of cost and net

realisable value. Cost is determined on the first-in, first-out method. Oil and gas inventories are stated at fair value less cost to sell.

Cash that is held for security for bank guarantees is reported in the balance sheet and cash flow statements separately. If the

expected duration of the restriction is less than twelve months then it is shown in current assets.

The Corporation has a share based payment plan as described in note 24 (c). The expense is recorded in the statement of income

or capitalised for all options granted in the year, with the gross increase recorded in the share based payment reserve.

Compensation costs are based on the estimated fair values at the time of the grant and the expense or capitalised amount is

recognised over the vesting period of the options. Upon the exercise of the stock options, consideration paid together with the

amount previously recognised in share based payment reserve is recorded as an increase in share capital. In the event that vested

options expire unexercised, previously recognised compensation expense associated with such stock options is not reversed. In

the event that unvested options are forfeited or expired, previously recognised compensation expense associated with the

unvested portion of such stock options is reversed.

Analysis of the fair values of financial instruments and further details as to how they are measured are provided in notes 29 to 31.

For the purpose of the statement of cash flow, cash and cash equivalents include investments with an original maturity of three

months or less.

Trade receivables are recognised and carried at the original invoiced amount, less any provision for estimated irrecoverable

Trade payables are measured at cost.

Transaction costs that are directly attributable to the acquisition or issue of a financial asset or liability and original issue discounts

on long-term debt have been included in the carrying value of the related financial asset or liability and are amortised to

consolidated net earnings over the life of the financial instrument using the effective interest method.

Held-for-trading financial instruments are subsequently measured at fair value with changes in fair value recognised in net

earnings. All other categories of financial instruments are measured at amortised cost using the effective interest method. Cash

and cash equivalents are classified as held-for-trading and are measured at fair value. Accounts receivable are classified as loans

and receivables. Accounts payable, accrued liabilities, certain other long-term liabilities, and long-term debt are classified as other

financial liabilities. Although the Corporation does not intend to trade its derivative financial instruments, they are classified as held-

for-trading for accounting purposes.

All financial instruments, other than those designated as effective hedging instruments, are initially recognised at fair value in the

statement of financial position. The Corporation’s financial instruments consist of cash, restricted cash, accounts receivable,

deposits, derivatives, accounts payable, accrued liabilities, contingent consideration and the current liability on the Beatrice

acquisition. The Corporation classifies its financial instruments into one of the following categories: held-for-trading financial assets

and financial liabilities; held-to-maturity investments; loans and receivables; and other financial liabilities. All financial instruments

are required to be measured at fair value on initial recognition. Measurement in subsequent periods is dependent on the

classification of the respective financial instrument.

8

Ithaca Energy Inc. Q3 2014 Financial Statements

Property, plant and equipment

Oil and gas expenditure – exploration and evaluation assets

Capitalisation

Impairment

Oil and gas expenditure – development and production assets

Capitalisation

Depreciation

Impairment

Costs of bringing a field into production, including the cost of facilities, wells and sub-sea equipment, direct costs including staff

costs and share based payment expense together with E&E assets reclassified in accordance with the above policy, are

capitalised as a D&P asset. Normally each individual field development will form an individual D&P asset but there may be cases,

such as phased developments, or multiple fields around a single production facility when fields are grouped together to form a

single D&P asset.

The Corporation’s oil and gas assets are analysed into CGUs for impairment review purposes, with E&E asset impairment testing

being performed at a grouped CGU level. The current E&E CGU consists of the Corporation’s whole E&E portfolio. E&E assets

are reviewed for impairment when circumstances arise which indicate that the carrying value of an E&E asset exceeds the

recoverable amount. When reviewing E&E assets for impairment, the combined carrying value of the grouped CGU is compared

with the grouped CGU's recoverable amount. The recoverable amount of a grouped CGU is determined as the higher of its fair

value less costs to sell and value in use. Impairment losses resulting from an impairment review are written off to the statement of

income.

E&E costs are not amortised prior to the conclusion of evaluation activities. At completion of evaluation activities, if technical

feasibility is demonstrated and commercial reserves are discovered then, following development sanction, the carrying value of the

E&E asset is reclassified as a development and production (“D&P”) asset, but only after the carrying value is assessed for

impairment and where appropriate its carrying value adjusted. If after completion of evaluation activities in an area, it is not

possible to determine technical feasibility and commercial viability or if the legal right to explore expires or if the Corporation

decides not to continue exploration and evaluation activity, then the costs of such unsuccessful exploration and evaluation is

written off to the statement of income in the period the relevant events occur.

A review is carried out each reporting date for any indication that the carrying value of the Corporation’s D&P assets may be

impaired. For D&P assets where there are such indications, an impairment test is carried out on the CGU. Each CGU is identified

in accordance with IAS 36. The Corporation’s CGUs are those assets which generate largely independent cash flows and are

normally, but not always, single developments or production areas. The impairment test involves comparing the carrying value

with the recoverable value of an asset. The recoverable amount of an asset is determined as the higher of its fair value less costs

to sell and value in use, where the value in use is determined from estimated future net cash flows. Any additional depreciation

resulting from the impairment testing is charged to the statement of income.

Pre-acquisition costs on oil and gas assets are recognised in the statement of income when incurred. Costs incurred after rights to

explore have been obtained, such as geological and geophysical surveys, drilling and commercial appraisal costs and other

directly attributable costs of exploration and evaluation including technical, administrative and share based payment expenses

are capitalised as intangible exploration and evaluation (“E&E”) assets.

All costs relating to a development are accumulated and not depreciated until the commencement of production. Depreciation is

calculated on a unit of production basis based on the proved and probable reserves of the asset. Any re-assessment of reserves

affects the depreciation rate prospectively. Significant items of plant and equipment will normally be fully depreciated over the life

of the field. However, these items are assessed to consider if their useful lives differ from the expected life of the D&P asset and

should this occur a different depreciation rate would be charged.

9

Ithaca Energy Inc. Q3 2014 Financial Statements

Non oil and natural gas operations

Decommissioning liabilities

Contingent consideration

Taxation

Operating leases

Finance leases

Maintenance expenditure

Recent accounting pronouncements

Finance leases that transfer substantially all the risks and benefits incidental to ownership of the leased item to the Corporation,

are capitalised at the commencement of the lease at the fair value of the leased property or, if lower, at the present value of the

minimum lease payments. Lease payments are apportioned between finance charges and reduction of the lease liability so as to

achieve a constant rate of interest on the remaining balance of the liability. Finance charges are recognised in finance costs in the

income statement. A leased asset is depreciated over the useful life of the asset. A486However, if there is no reasonable certainty

that the Corporation will obtain ownership by the end of the lease term, the asset is depreciated over the shorter of the estimated

useful life of the asset and the lease term.

Current income tax

Rentals under operating leases are charged to the statement of income on a straight line basis over the period of the lease.

Expenditure on major maintenance refits or repairs is capitalised where it enhances the life or performance of an asset above its

originally assessed standard of performance; replaces an asset or part of an asset which was separately depreciated and which is

then written off, or restores the economic benefits of an asset which has been fully depreciated. All other maintenance expenditure

is charged to the statement of income as incurred.

Deferred income tax

Current income tax assets and liabilities are measured at the amount expected to be recovered from or paid to the taxation

authorities. The tax rates and tax laws used to compute the amounts are those that are enacted or substantively enacted by the

reporting date.

The Corporation records the present value of legal obligations associated with the retirement of long term tangible assets, such as

producing well sites and processing plants, in the period in which they are incurred with a corresponding increase in the carrying

amount of the related long term asset. The obligation generally arises when the asset is installed or the ground/environment is

disturbed at the field location. In subsequent periods, the asset is adjusted for any changes in the estimated amount or timing of

the settlement of the obligations. The carrying amounts of the associated assets are depleted using the unit of production method,

in accordance with the depreciation policy for development and production assets. Actual costs to retire tangible assets are

deducted from the liability as incurred.

Contingent consideration is accounted for as a financial liability and measured at fair value at the date of acquisition with any

subsequent remeasurements recognised either in the statement of income or in other comprehensive income in accordance with

IAS 39.

Deferred tax is recognised for all deductible temporary differences and the carry-forward of unused tax losses. Deferred tax assets

and liabilities are measured using enacted or substantively enacted income tax rates expected to apply to taxable income in the

years in which temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a

change in rates is included in earnings in the period of the enactment date. Deferred tax assets are recorded in the consolidated

financial statements if realisation is considered more likely than not.

Computer and office equipment is recorded at cost and depreciated over its estimated useful life on a straight-line basis over three

years. Furniture and fixtures are recorded at cost and depreciated over their estimated useful lives on a straight-line basis over five

years.

New and amended standards and interpretations need to be adopted in the first interim financial statements issued after their

effective date (or date of early adoption). There are no new IFRSs or IFRICs that are effective for the first time for this interim

period that would be expected to have a material impact on the Corporation.

10

Ithaca Energy Inc. Q3 2014 Financial Statements

Significant accounting judgements and estimation uncertainties

4. SEGMENTAL REPORTING

5. REVENUE

Three months ended 30 Sept Nine months ended 30 Sept

Oil sales REV01

Gas sales REV02

Condensate sales REV03

Other income REV04

6. COST OF SALES

7. ADMINISTRATIVE EXPENSES

Three months ended 30 Sept Nine months ended 30 Sept

General & administrative EXP01

Non-recurring Valiant acquisition related costsShare based payment EXP16

8. FINANCE COSTS

Three months ended 30 Sept Nine months ended 30 Sept

Accretion

Bank charges

Senior notes interest

Finance lease interest

Non-operated asset finance fees

Prepayment interestLoan fee amortisation

The 3Q 2014 movement in inventory figure represents a positive movement in volumes of $8.9 million partially offset by a negative

movement due to revaluation of oil inventory at the period end of $5.6 million due to the low Brent price at 30 September 2014.

The preparation of financial statements in conformity with IFRS requires management to make estimates and assumptions

regarding certain assets, liabilities, revenues and expenses. Such estimates must often be made based on unsettled transactions

and other events and a precise determination of many assets and liabilities is dependent upon future events. Actual results may

differ from estimated amounts.

374

US$'000

289,665

(592)

56

(3,052)

(17,831)

(10,235)

1,060

US$'000

4,579

2014

(82)

(12,233)

2,533

(3,184)

114,112

2013

(6,731)

US$'00020142013

US$'000

(9,962)

(865)

88,347 292,506

(1,777)-

-

(7,409)

US$'0002013

(21,865)(4,956)

-

2014

(2,965)

(1,316)

282,179

2013

The amounts recorded for depletion, depreciation of property and equipment, long-term liability, stock-based compensation,

contingent consideration, decommissioning liabilities, derivatives and deferred taxes are based on estimates. The depreciation

charge and any impairment tests are based on estimates of proved and probable reserves, production rates, prices, future costs

and other relevant assumptions. By their nature, these estimates are subject to measurement uncertainty and the effect on the

financial statements of changes in such estimates in future periods could be material. Further information on each of these

estimates is included within the notes to the financial statements.

2014US$'000

2013

(11,278)

US$'000

(4,162)

2014

2014US$'000

(9,883)(2,949)

(1,518)

US$'000

7,231

(550) (203)

(1,315)

90,094

US$'000

238 328

111,289

2,176

302,241

2,007

(1,375)

2013US$'000

- -

(3,734)

(1,543)

449 760

US$'000

(2,743)

(1,203)

(9,844)

(22)

The Company operates a single class of business being oil and gas exploration, development and production and related activities

in a single geographical area presently being the North Sea.

-

(3,862)

-

- (3,862)

(174)(174)

Included within 3Q operating costs is $12 million associated with the Sullom Voe Terminal 2013 reconciliation charge previously

reported as a contingent liability in Q2 2014 as a result of the late notification from the operator. Following a full audit this non-

recurring exceptional item has been recognised as a cost and settled in Q3 2014.

(608)

(124)

(297)(40)

-

11

Ithaca Energy Inc. Q3 2014 Financial Statements

9. RESTRICTED CASH

Letters of credit

10. ACCOUNTS RECEIVABLE

Trade debtors

Norwegian tax receivableAccrued income

11. INVENTORY

Crude oil inventory - current

Crude oil inventory - non-current

Materials inventory

The non-current portion of inventory relates to long term stocks at the Sullom Voe Terminal

12. EXPLORATION AND EVALUATION ASSETS

At 1 January 2013

Additions

Write offs/relinquishmentsDisposals

At 31 December 2013

Additions

Transfer from E&E to D&P

Release of exploration obligationsWrite offs/relinquishments

At 30 September 2014

30 Sept

12,198

US$'000

2,247

(7,266)

31 Dec

US$'000

12,198

2013

2013

34,800

The cash letters of credit collateralised in place as at 30 June 2014 were issued under the Reserved Based Lending Facility in Q3

and therefore the restricted cash was released.

2014

31 Dec

Following completion of geotechnical evaluation activity, certain licences were declared unsuccessful and certain prospects were

declared non-commercial and therefore the related expenditure of $3 million was expensed in the nine months to 30 September

2014.

(1,366)

US$'000

58,064

2014

-

-

30 Sept

47,691

US$'000

47,390

60,145

(31,170)(18,737)

80,729

The above also includes the release of the exploration obligation provision against expenditure incurred (see note 19).

77,589

US$'000 US$'0002014 2013

8,126

29,758

215

21,417

355,185

31,371

8,126

31 Dec

US$'000

30 Sept

194,442

57,628

(3,067)

246,225

314,727

58,88861,397

12

Ithaca Energy Inc. Q3 2014 Financial Statements

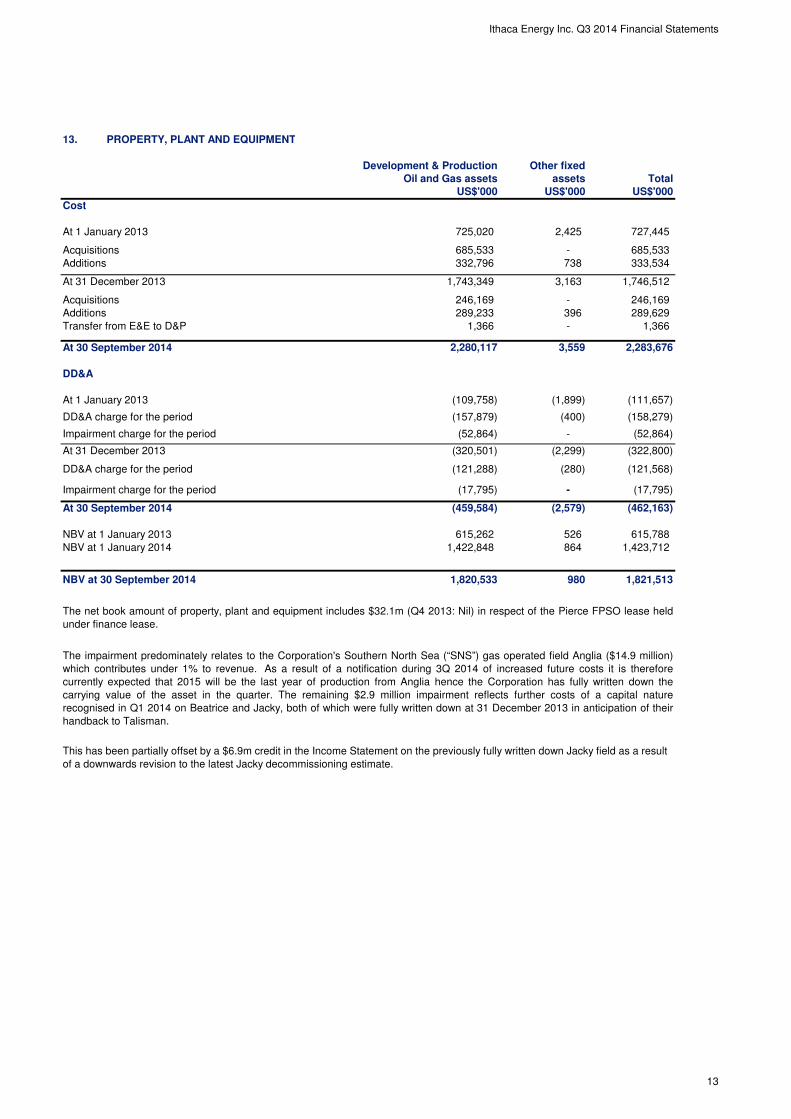

13. PROPERTY, PLANT AND EQUIPMENT

Development & Production Other fixed

Cost

At 1 January 2013

Acquisitions

Additions

At 31 December 2013

Acquisitions

Additions

Transfer from E&E to D&P

At 30 September 2014

DD&A

At 1 January 2013

DD&A charge for the period

Impairment charge for the period

At 31 December 2013

DD&A charge for the period

Impairment charge for the period

At 30 September 2014

NBV at 1 January 2013

NBV at 1 January 2014

NBV at 30 September 2014

1,366

1,423,712

1,820,533

1,422,848

(459,584)

615,262

(2,579)

-

(462,163)

332,796

-

(320,501)

(52,864)

333,534

-

685,533 685,533

(158,279)

725,020

1,743,349

-

The impairment predominately relates to the Corporation's Southern North Sea (“SNS”) gas operated field Anglia ($14.9 million)

which contributes under 1% to revenue. As a result of a notification during 3Q 2014 of increased future costs it is therefore

currently expected that 2015 will be the last year of production from Anglia hence the Corporation has fully written down the

carrying value of the asset in the quarter. The remaining $2.9 million impairment reflects further costs of a capital nature

recognised in Q1 2014 on Beatrice and Jacky, both of which were fully written down at 31 December 2013 in anticipation of their

handback to Talisman.

289,629

2,283,676

(280)

US$'000

615,788

(2,299)

US$'000

3,163 1,746,512

727,445 2,425

738

526

Oil and Gas assets assets

1,821,513980

864

(322,800)

289,233

(121,288)

(1,899)

1,366 -

3,559

Total

396

(109,758)

246,169 246,169

US$'000

(17,795)

The net book amount of property, plant and equipment includes $32.1m (Q4 2013: Nil) in respect of the Pierce FPSO lease held

under finance lease.

(157,879)

(111,657)

(400)

2,280,117

(17,795)

(121,568)

(52,864)

This has been partially offset by a $6.9m credit in the Income Statement on the previously fully written down Jacky field as a result

of a downwards revision to the latest Jacky decommissioning estimate.

13

Ithaca Energy Inc. Q3 2014 Financial Statements

14. BUSINESS COMBINATION

ProvisionalFair value

US$'000

PP&EPierce lease asset

InventoryTrade and other receivables

Trade and other payablesPierce lease liabilityDeferred tax liabilities

Provisions

Total identifiable net assets at fair value

Positive goodwill arising on acquisition

Total consideration

The cash outflow on acquisition is as follows:Net cash acquiredCash paid

Net consolidated cash flow

15. GOODWILL

At 1 January 2014Addition in the period

At 30 September 2014

(178,402)

(43,772)

214,000

178,402

The fair values of the acquired identifiable assets are provisional due to the proximity of the acquisition to the quarter end and to

allow for any further information received to be taken into account.

16,563

(136,903)

On 31 July 2014 the Corporation completed the acquisition of 100% of the issued shares of Summit Petroleum Limited and its

subsidiaries ("Summit"), The acquisition further broadens the Corporation's producing asset base with high quality, long-life oil

assets with clear upsides and enables acceleration in the monetisation of existing UK tax allowance. The assets that were

acquired were: a further 20% interest in the Cook field in which the Company already had a 41.346% interest; a 7.48% interest in

the Pierce field; and, a 7.43% interest in the Wytch Farm field. The transaction was completed on 31 July 2014 for a net

consideration of $163 million. The total acquisition consideration was $178.4 million, paid in cash. These interim condensed

consolidated financial statements include the results of Summit from the acquisition date.

The provisional fair values of the identifiable assets and liabilities of Summit as at the acquisition date were:

(25,245)

17,630

32,169

(32,169)

$136.1 million represents a goodwill asset recognised on the acquisition of Summit Petroleum limited as a result of recognising a

$136.9million deferred tax liability as required under IFRS 3 fair value accounting for business combinations. Absent the deferred

tax liability the price paid for the Summit assets equates to the fair value of the assets. $0.9 million represents goodwill recognised

on the acquisition of gas assets from GDF in December 2010. As at 30 September 2014, the recoverable amount of oil and gas

assets was sufficiently high to support the carrying value of this goodwill.

136,129

42,273

From the date of acquisition, Summit has contributed $9 million of revenue and approximately $2.5 million to the net profit before

tax. If the combination had taken place at the beginning of the year, the profit before tax from continuing operations for the period

would have been approximately $39.4 million and revenue contribution of the Summit assets to the continuing operations would

have been approximately $57 million.

14,861

(163,541)

US$'000

985136,129

137,114

14

Ithaca Energy Inc. Q3 2014 Financial Statements

16. INVESTMENT IN ASSOCIATES

Investment in FPF-1 and FPU Services

17. BORROWINGS30 Sept

RBL facility

Corporate facility

Senior notes

Norwegian facility

Long term bank feesLong term senior notes fees

The key covenants in the RBL are:

- A corporate cashflow projection showing total sources of funds must exceed total forecast uses of funds for the following 12

months.

- The ratio of the net present value of cashflows secured under the RBL for the economic life of the fields to the amount drawn

under the facility must not fall below 1.15:1

- The ratio of the net present value of cashflows secured under the RBL for the life of the debt facility to the amount drawn under

the facility must not fall below 1.05:1.

The Corporation is in compliance with all its financial and operating covenants.

Investment in associates comprises shares, acquired by Ithaca Energy (Holdings) Limited, in FPF-1 Limited and FPU Services

Limited as part of the completion of the Greater Stella Area transactions in 2012. There has been no change in value during the

period with the above investment reflecting the Company's share of the associates' results.

8,948

US$'000

18,337

The Corporation is subject to financial and operating covenants related to the facilities. Failure to meet the terms of one or more of

these covenants may constitute an event of default as defined in the facility agreements, potentially resulting in accelerated

repayment of the debt obligations.

On 1 July 2013, the Corporation signed a NOK 450 million Norwegian Tax Rebate Facility (the "Norwegian Facility"). Under the

Norwegian tax regime, 78% of exploration, appraisal and supporting expenditure resulting from operations on the Norwegian

Continental Shelf is refunded by the Government in the December of the year following the year the costs were incurred. This is a

conventional tax refund facility on industry standard terms. On 30 September 2014, this facility was increased to NOK 600 million

(~$100 million) and tenure to 31 December 2016. Any drawings under this facility will be fully offset by a receivable tax refund from

the Norwegian government within a maximum of 24 months.

20132014

30 Sept 31 Dec

US$'000

18,337

In October 2013, the Corporation increased its existing RBL (Reserved Based Lending) Facility to $610 million with enhanced

terms including reduced margin costs (LIBOR plus 2.75%-3%) and greater flexibility over future unallocated capital with a loan

term until June 2017.

The Corporation also established a new five year $100 million corporate facility in October 2013 with a term of up to 5 years which

attracts interest at LIBOR plus 4.15%.

- 5,538

(432,243)

-

US$'000 US$'000

(33,985)

11,660

-

(409,918)

(69,044)

(300,000)

-

(476,123)

2014 2013

31 Dec

(830,681)

On 3 July 2014, the Company completed an offering of $300 million 8.125% senior unsecured notes due July 2019, with interest

payable semi-annually. The net proceeds of the notes were used to partially repay (without cancelling) the Company’s senior

secured RBL Facility, with a portion of it subsequently redrawn to finance the acquisition of the Summit assets on 31 July 2014.

15

Ithaca Energy Inc. Q3 2014 Financial Statements

18. TRADE AND OTHER PAYABLES30 Sept

Trade payablesAccruals and deferred income

19. EXPLORATION OBLIGATIONS

Exploration obligations

The RBL and Corporate facilities are secured by the assets of the guarantor member of the Ithaca Group, such security including

share pledges, floating charges and/or debentures.

The Norwegian Facility is secured by the assets of Ithaca Petroleum Norge AS, such security including a share pledge,

assignment of insurance and tax refund proceeds and pledges of participation interests in licences.

The Senior notes are unsecured senior debt of Ithaca Energy Inc, guaranteed by certain members of the Ithaca Group and

subordinated to existing and future secured obligations.

There are no financial maintenance covenants tests under the senior notes.

The principle covenants under the undrawn Corporate Facility are:

- The ratio of total debt to earnings before interest, tax, DD&A, impairment, exceptional or extraordinary expenditure and E&E

writeoffs ("EBITDAX"), calculated quarterly on a trailing 12-month basis as of the last day of each quarter, must not exceed 3.0:1 or

3.5:1 if any one of the two previously tested ratios have been at or below 3.0:1

- The ratio of EBITDAX to total debt costs, calculated quarterly on a trailing 12-month basis as of the last day of each quarter,

must not be less than 4.0:1

The key covenant in the Norwegian Tax Rebate Facility is Norwegian subsidiaries must have available funds to execute planned

activities for the year to December in each calendar year.

Note no funds have or are forecast to be drawn under the Corporate facility.

Security provided against the loan

US$'000

As at 30 September 2014, $476 million (31 December 2013: $410 million) was drawn down under the RBL Facility and

approximately $70 million (31 December 2013: $34million) was drawn under the Norwegian Tax Rebate Facility. $8 million (31

December 2013: $12 million) of loan fees relating to the RBL and $5.4 million relating to the Senior Notes have been capitalised

and remain to be amortised.

31 Dec

2014

30 Sept

2013

(5,593) (12,859)

(206,194)

31 Dec

US$'000

The above reflects the fair value of E&E commitments assumed as part of the Valiant transaction. During the period to 30

September 2014, $7.3 million was released reflecting expenditure incurred in the period.

(280,151)

(472,396)(486,345)

US$'000

(299,344)

2013US$'000

(173,052)

2014

16

Ithaca Energy Inc. Q3 2014 Financial Statements

20. DECOMMISSIONING LIABILITIES

30 Sept 31 Dec

US$'000 US$'000

Balance, beginning of period

Acquisitions

Additions

AccretionRevision to estimates

Balance, end of period

21. OTHER LONG TERM LIABILITIES 30 Sept 31 Dec

US$'000 US$'000

Balance, beginning of period

Revaluation in the period

Reclassed to trade payables

Finance lease

Balance, end of period

22. FINANCE LEASE LIABILITIES

30 Sept 31 Dec

US$'000 US$'000

Total minimum lease payments

Less than 1 year

Between 1 and 5 years

5 years and later

Interest

Less than 1 year

Between 1 and 5 years

5 years and later

Present value of minimum lease payments

Less than 1 year

Between 1 and 5 years5 years and later

The finance lease relates to the Pierce FPSO asset acquired as part of the Summit acquisition in the period. (Note 21)

2014

(43,772)

2013

(32,123)

(4,162)

-

The total future decommissioning liability was calculated by management based on its net ownership interest in all wells and

facilities, estimated costs to reclaim and abandon wells and facilities and the estimated timing of the costs to be incurred in future

periods. The Corporation uses a risk free rate of 3.0 percent (31 December 2013: 3.0 percent) and an inflation rate of 2.0 percent

(31 December 2013: 2.0 percent) over the varying lives of the assets to calculate the present value of the decommissioning

liabilities. These costs are expected to be incurred at various intervals over the next 13 years.

The economic life and the timing of the obligations are dependent on Government legislation, commodity price and the future

production profiles of the respective production and development facilities. Note that upon the acquisition of the Beatrice Field in

November 2008, the Corporation did not assume the decommissioning liabilities.

(6,037)

5,691

(172,047)

2014

The opening balance relates to volumes of oil at the Nigg terminal which must be settled on re-transfer to Talisman, expected to

take place in early 2015. This has been transferred to current liabilities and is now included within trade and other payables (Note

18). The finance lease relates to the Pierce FPSO asset acquired as part of the Summit acquisition in the period (Note 22).

347

(966)

(1,943)

(32,122)

(3,018)

(4,509)

(6,037)

- (3,019)

-

-

-

-

(4,541)

(172,047)

(52,834)

(18,891)

(9,475)

2013

(222,890)

2014 2013

(2,595) -

-

(21,967)

-

-

(12,958)

(26,370)

(1,061)

-

(1,534)

(8,417)

-

(86,338)

(4,403)

17

Ithaca Energy Inc. Q3 2014 Financial Statements

23. CONTINGENT CONSIDERATION

30 Sept 31 Dec

US$'000 US$'000

Balance 31 December 2013 & 30 September 2014

24. SHARE CAPITAL

Amount

Authorised share capital 000 US$'000

At 31 December 2013 and 30 September 2014 Unlimited -

(a) Issued

The issued share capital is as follows:

Issued Number of common shares Amount US$'000

Balance 1 January 2013

Share issue

Issued for cash - options exercised 6,574 Transfer from Share based payment reserve on options exercised

Balance 1 January 2014

Issued for cash - options exercisedTransfer from Share based payment reserve on options exercised

Balance 30 September 2014

(b) Stock options

Balance, beginning of period

Granted $2.43

Forfeited / expiredExercised

$2.01

2014 2013

11,090

$2.31

(5,885,000)

329,518,620

4,819

Changes to the Corporation’s stock options are summarised as follows:

No. of Options

30 September 2014

$2.37$1.79

The contingent consideration at the end of the period relates to the acquisition of the Stella field and is payable subsequent to first

oil.

$2.47

* The weighted average exercise price has been converted into U.S. dollars based on the foreign exchange rate in effect at the

date of issuance.

$2.18

15,682,164

No. of Options

7,260,000

Options

Wt. Avg Exercise

Price *

14,593,567

(286,403)

56,952,321 93,005

31 December 2013

Wt. Avg Exercise

Price *

No. of ordinary

20,347,964

In the nine months ended 30 September 2014, the Corporation's Board of Directors granted 95,000 options at a weighted average

exercise price of $2.51 (C$2.68) and 7,165,000 options at a weighted average exercise price of $2.47 (C$2.71)

(4,000)(4,000)

431,318 259,920,003

323,633,620

6,761,296 -

535,716

5,885,000

$2.01

(813,333)(6,761,296)

1,820,232

$0.95

14,593,567

551,632

4,826

The Corporation’s stock options and exercise prices are denominated in Canadian Dollars when granted. As at 30 September

2014, 15,682,164 stock options to purchase common shares were outstanding, having an exercise price range of $2.00 to $2.51

(C$1.97 to C$2.71) per share and a vesting period of up to 3 years in the future.

$1.63

-

18

Ithaca Energy Inc. Q3 2014 Financial Statements

The following is a summary of stock options as at 30 September 2014

Options Outstanding Options Exercisable

Wt. Avg. Wt. Avg. Wt. Avg. Wt. Avg.

Life Exercise Life Exercise

(Years) Price * (Years) Price *

2.5 $2.41 0.9 $2.28

2.0 $2.03 2.0 $2.03

2.4 $2.31 1.2 $2.21

The following is a summary of stock options as at 31 December 2013

Options Exercisable

Wt. Avg. Wt. Avg. Wt. Avg. Wt. Avg.

Life Exercise Life Exercise

(Years) Price * (Years) Price *

1.8 $2.29 1.0 $2.22

2.1 $1.90 1.4 $1.77

0.1 $0.17 0.1 $0.20

1.9 $2.01 1.1 $1.95

(c) Share based payment

Risk free interest rate

Expected stock volatility

Expected life of options

Weighted Average Fair Value

25. SHARE BASED PAYMENT RESERVE

30 Sept 31 Dec

Balance, beginning of period

Share based payment cost

Transfer to share capital on exercise of options (6,244)

Balance, end of period

4,810

2014

$2.00-$2.03

(C$1.97-C$1.99)

Range of

Exercise Price

2013

2 years

1.37%

56%

3,733

US$’000

1,144,999

11,560,496

$2.22-$2.51

(C$2.25-C$2.71)

Options granted are accounted for using the fair value method. The compensation cost during the three months and nine months

ended 30 September 2014 for total stock options granted was $1.5 million and $4.8 million respectively (Q3 2013: $1.0 million, Q3

YTD: $3.0 million). $0.6 million and $1.3 million were charged through the income statement for share based payment for the three

and nine months ended 30 September 2014 respectively, being the Corporation’s share of share based payment chargeable

through the income statement. The remainder of the Corporation’s share of share based payment has been capitalised. The fair

value of each stock option granted was estimated at the date of grant, using the Black-Scholes option pricing model with the

following assumptions:

51%

19,254

No. of Options

4,673,333

$2.22-$2.46

(C$2.25-$2.53)

$1.08

US$’000

3,367,163

15,682,164

For the year ended 31

December 2013

14,593,567

$2.22-$2.51

(C$2.25-C$2.71)

Range of

Exercise PriceNo. of Options

4,121,668

$2.00-$2.03

(C$1.97-C$1.99)

Options Outstanding

For the nine months ended 30

September 2014

$0.82

4,512,162

8,989,999

17,820

1.27%

3 years

471,668

19,254

471,668$0.20 (C$0.25)

7,451,667

$1.49-$2.03

(C$1.54-C$1.99)

Range of

Exercise Price

$0.20 (C$0.25)

$1.49-$2.03

(C$1.54-C$1.99) 3,844,998

No. of Options

Range of

Exercise Price

$2.22-$2.46

(C$2.25-$2.53)

20,340

6,670,232

No. of Options

(4,819)

19

Ithaca Energy Inc. Q3 2014 Financial Statements

26. EARNINGS PER SHARE

Three months ended 30 Sept Nine months ended 30 Sept

Wtd av. number of common shares (basic)

Wtd av. number of common shares (diluted)

27. TAXATION

Three months ended 30 Sept Nine months ended 30 Sept

UK Corporation Tax

Norwegian Corporation TaxUK Petroleum Revenue Tax

Total Taxation Credit/(Charge)

The movement in deferred taxation primarily results from business combination as per note 14.

28. COMMITMENTS

30 Sept 31 Dec

Operating lease commitments

Within one year

Two to five years

Capital commitments 30 Sept 31 Dec

Capital commitments incurred jointly with other venturers (Ithaca's share)

29. FINANCIAL INSTRUMENTS

1

272 4,253-

16,959

299,807,995

(1,449)

2014

• Level 1 – inputs represent quoted prices in active markets for identical assets or liabilities (for example, exchange-traded

commodity derivatives). Active markets are those in which transactions occur in sufficient frequency and volume to provide pricing

information on an ongoing basis.

7,911

19,763

2014 2013

2014

324,563,406

294,617,969

1,675

12,528

14,389

The calculation of basic earnings per share is based on the profit after tax and the weighted average number of common shares in

issue during the period. The calculation of diluted earnings per share is based on the profit after tax and the weighted average

number of potential common shares in issue during the period.

- 1,214

(8,706)

(1,449)

To estimate fair value of financial instruments, the Corporation uses quoted market prices when available, or industry accepted

third-party models and valuation methodologies that utilise observable market data. In addition to market information, the

Corporation incorporates transaction specific details that market participants would utilise in a fair value measurement, including

the impact of non-performance risk. The Corporation characterises inputs used in determining fair value using a hierarchy that

prioritises inputs depending on the degree to which they are observable. However, these fair value estimates may not necessarily

be indicative of the amounts that could be realised or settled in a current market transaction. The three levels of the fair value

hierarchy are as follows:

66,841

(7,492)

US$'000

317,365,658329,954,910

327,997,027

330,098,302

2014

329,409,055

2013 2013

2013

111,747

2014US$000 US$000

8,183 227

US$'000

2014 2013US$'000 US$'000

US$000

• Level 2 – inputs other than quoted prices included within Level 1 that are observable, either directly or indirectly, as of the

reporting date. Level 2 valuations are based on inputs, including quoted forward prices for commodities, market interest rates, and

volatility factors, which can be observed or corroborated in the marketplace. The Corporation obtains information from sources

such as the New York Mercantile Exchange and independent price publications.

2013US$000

• Level 3 – inputs that are less observable, unavailable or where the observable data does not support the majority of the

instrument’s fair value.

8,149

13,262

20

Ithaca Energy Inc. Q3 2014 Financial Statements

Derivative financial instrument assets

Long term liability on Beatrice acquisition

Contingent considerationDerivative financial instrument liability

Three months ended 30 Sept Nine months ended 30 Sept

Revaluation of forex forward contracts

Revaluation of other long term liability

Revaluation of commodity hedges

Revaluation of interest rate swaps

Realised gain/(loss) on commodity hedges

Realised gain/(loss) on forex contracts

Realised (loss)/gain on interest rate swaps

Total (loss)/gain on financial instruments

The Corporation has identified that it is exposed principally to these areas of market risk.

i) Commodity Risk

Three months ended 30 Sept

Revaluation of commodity hedgesRealised gain/(loss) on commodity hedges

(4,171)

(82)

US$'000

2014

In forming estimates, the Corporation utilises the most observable inputs available for valuation purposes. If a fair value

measurement reflects inputs of different levels within the hierarchy, the measurement is categorised based upon the lowest level

of input that is significant to the fair value measurement. The valuation of over-the-counter financial swaps and collars is based on

similar transactions observable in active markets or industry standard models that primarily rely on market observable inputs.

Substantially all of the assumptions for industry standard models are observable in active markets throughout the full term of the

instrument. These are categorised as Level 2.

US$'000

-

US$'000

US$'000

(199)

The table below presents the total gain / (loss) on commodity hedges that has been disclosed through the statement of

comprehensive income:

(199)

- -

Level 3

(5,691)

25,198

-

-

Level 1

-

2013

(5,691)

US$'000

25,198

US$'000Total Fair ValueLevel 2

The following table presents the Corporation’s material financial instruments measured at fair value for each hierarchy level as of

30 September 2014:

(4,000)

US$'000

US$'000

2014 2013

US$'000

Total gain/(loss) on commodity hedges

37,373

2013

38,189 33,486

11,602

(15,814)

1,185 -

Commodity price risk related to crude oil prices is the Corporation’s most significant market risk exposure. Crude oil prices and

quality differentials are influenced by worldwide factors such as OPEC actions, political events and supply and demand

fundamentals. The Corporation is also exposed to natural gas price movements on uncontracted gas sales. Natural gas prices, in

addition to the worldwide factors noted above, can also be influenced by local market conditions. The Corporation’s expenditures

are subject to the effects of inflation, and prices received for the product sold are not readily adjustable to cover any increase in

expenses from inflation. The Corporation may periodically use different types of derivative instruments to manage its exposure to

price volatility, thus mitigating fluctuations in commodity-related cash flows.

- -

1,729 4,028

(306)

9,873 1,122 (3,687) (5,219)

39,229

(25,389)37,373

100

1,040

716 3468,251- 9,723

64

-

(13,312)

37,445

38,495

1,122 (3,687)(22,945)

(26,632)

(5,472)

The table below presents the total gain / (loss) on financial instruments that has been disclosed through the statement of

comprehensive income:

-

(90)

US$'000

31,989

(1,497)

(17,074)

(2,502)

(134)(22,945)

(4,000)

2014

- -

21

Ithaca Energy Inc. Q3 2014 Financial Statements

Derivative Term Volume Average price

bbls

bbls

therms

therms

ii) Interest Risk

Derivative Value Rate

0.44%

Three months ended 30 September

Revaluation of foreign exchange forward contractsRealised gain on foreign exchange forward contracts

Oct 15 - Jun 17 187,300,000 63p/therm

Oil swaps Oct 14 - Jun 16

Oct 14 - Dec 14 404,800

$103/bbl

2,774,205 $102/bbl

1,225,835

9,723

10,908

The Corporation’s accounts receivable with customers in the oil and gas industry are subject to normal industry credit risks and are

unsecured. All of its oil production from the Beatrice, Jacky and Athena fields is sold to BP Oil International Limited. Oil production

from Cook, Broom, Dons, Causeway and Fionn is sold to Shell Trading International Ltd. Anglia and Topaz gas production is

currently sold through three contracts to RWE NPower PLC and Hess Energy Gas Power (UK) Ltd. Cook gas is sold to Shell UK

Ltd and Esso Exploration & Production UK Ltd.

1,185

Gas puts

Oil puts Oct 14 - Jun 16

67p/thermGas swaps

-

US$'000

The below represents commodity hedges in place:

The Corporation also has credit risk arising from cash and cash equivalents held with banks and financial institutions. The

maximum credit exposure associated with financial assets is the carrying values.

The Corporation assesses partners’ credit worthiness before entering into farm-in or joint venture agreements. In the past, the

Corporation has not experienced credit loss in the collection of accounts receivable. As the Corporation’s exploration, drilling and

development activities expand with existing and new joint venture partners, the Corporation will assess and continuously update its

management of associated credit risk and related procedures.

The Corporation may be exposed to certain losses in the event that counterparties to derivative financial instruments are unable to

meet the terms of the contracts. The Corporation’s exposure is limited to those counterparties holding derivative contracts with

positive fair values at the reporting date. As at 30 September 2014, exposure is $25.2 million (31 December 2013: $5.1 million).

The Corporation is exposed to foreign exchange risks to the extent it transacts in various currencies, while measuring and

reporting its results in US Dollars. Since time passes between the recording of a receivable or payable transaction and its

collection or payment, the Corporation is exposed to gains or losses on non USD amounts and on balance sheet translation of

monetary accounts denominated in non USD amounts upon spot rate fluctuations from quarter to quarter. The Corporation

evaluates its foreign exchange instrument requirements on a rolling monthly basis.

US$'000

-

2014 2013

Total gain/(loss) on forex forward contracts

The Corporation regularly monitors all customer receivable balances outstanding in excess of 90 days. As at 30 September 2014

substantially all accounts receivables are current, being defined as less than 90 days. The Corporation has no allowance for

doubtful accounts as at 30 September 2014 (31 December 2013: $Nil).

-

Interest rate swap

Calculation of interest payments for the RBL agreement incorporates LIBOR. The Corporation is therefore exposed to interest rate

risk to the extent that LIBOR may fluctuate. The Corporation evaluates its annual forward cash flow requirements on a rolling

monthly basis.

iv) Credit Risk

$200 million

The table below presents the total gain on foreign exchange financial instruments that has been disclosed through the statement

of comprehensive income:

iii) Foreign Exchange Rate Risk

Term

Oct 14 - Dec 15

22

Ithaca Energy Inc. Q3 2014 Financial Statements

Accounts payable and accrued liabilitiesBorrowings

30. DERIVATIVE FINANCIAL INSTRUMENTS

30 Sept 31 December

US$'000 US$'000

Oil swaps

Oil puts

Gas swaps

Gas puts

Interest rate swapsForeign exchange forward contract

31. FAIR VALUES OF FINANCIAL ASSETS AND LIABILITIES

Classification

Cash and cash equivalents (Held for trading)

Restricted cash

Derivative financial instruments (Held for trading)

Accounts receivable (Loans and Receivables)

Deposits

Long-term receivable (Loans and Receivables)

Borrowings (Loans and Receivables)

Contingent consideration

Derivative financial instruments (Held for trading)

Other long term liabilities

Accounts payable (Other financial liabilities)

Liquidity risk includes the risk that as a result of its operational liquidity requirements the Corporation will not have sufficient funds

to settle a transaction on the due date. The Corporation manages liquidity risk by maintaining adequate cash reserves, banking

facilities, and by considering medium and future requirements by continuously monitoring forecast and actual cash flows. The

Corporation considers the maturity profiles of its financial assets and liabilities. As at 30 September 2014, substantially all accounts

payable are current.

US$'000

63,435

-

13,042

5,179

3

24,999

-

31 December 2013

Fair Value

314,727

5,102

31,655

-

12,198

314,727355,185

57,405

(6,037)

31,655

5,102

(830,681)

25,198

21,150 21,150

(15,550)

(4,000)(432,243)

(4,000)

(472,396)(472,396)

(830,681)

(32,122)

(4,000)

(6,037)

(15,550)

(830,681)

59,048

25,198

6,311

355,185

US$'0001 to 5 yearsWithin 1 year

2014 2013

-

(486,345)

(486,345) -

597

-

(15,349)

4,304

The following table shows the timing of cash outflows relating to trade and other payables.

59,048

(830,681)

(486,345) (486,345)

79

63,435

US$'000

US$'000

v) Liquidity Risk

6,696

(199)

30 September 2014

Carrying

Amount Carrying Amount

Financial instruments of the Corporation consist mainly of cash and cash equivalents, receivables, payables, loans and financial

derivative contracts, all of which are included in these financial statements. At 30 September 2014, the classification of financial

instruments and the carrying amounts reported on the balance sheet and their estimated fair values are as follows:

(432,243)

12,198

(32,122)

(199)

- -

Fair Value

(10,448)

(4,000)

57,405

6,311

23

Ithaca Energy Inc. Q3 2014 Financial Statements

32. RELATED PARTY TRANSACTIONS

Country of incorporation % equity interest at 30 Sep

Ithaca Energy (UK) Limited Scotland 100% 100%

Ithaca Minerals (North Sea) Limited Scotland 100% 100%

Ithaca Energy (Holdings) Limited Bermuda 100% 100%

Ithaca Energy Holdings (UK) Limited Scotland 100% 100%

Ithaca petroleum PLC England and Wales 100% 100%

Ithaca North Sea Limited England and Wales 100% 100%

Ithaca Exploration Limited England and Wales 100% 100%

Ithaca Causeway Limited England and Wales 100% 100%

Ithaca Gamma Limited England and Wales 100% 100%

Ithaca Alpha Limited Northern Ireland 100% 100%

Ithaca Epsilon Limited England and Wales 100% 100%

Ithaca Delta Limited England and Wales 100% 100%

Ithaca Petroleum Holdings AS Norway 100% 100%

Ithaca Petroleum Norge AS Norway 100% 100%

Ithaca Technology AS Norway 100% 100%

Ithaca AS Norway 100% 100%

Ithaca Petroleum EHF Iceland 100% 100%

Ithaca SPL Limited England and Wales 100% Nil

Ithaca Dorset Limited England and Wales 100% Nil

Ithaca SP UK Limited England and Wales 100% Nil

Ithaca Pipeline Limited England and Wales 100% Nil

Burstall Winger Zammit LLP 2014 - 111 -

2013 - 323 -

Loans to related parties Amounts owed from related parties

FPF-1 Limited

33. SEASONALITY

(127)

(18)

31,655

20132014

The effect of seasonality on the Corporation's financial results for any individual quarter is not material.

31 Dec

The consolidated financial statements include the financial statements of Ithaca Energy Inc and the subsidiaries listed in the

following table:

20132014

30 Sept

US$'000US$'000

57,405

Purchases

Accounts

Receivable

Accounts

Payable

US$'000

Sales

US$'000 US$'000 US$'000

The following table provides the total amount of transactions that have been entered into with related parties during the nine month

period ending 30 September 2014 and 30 September 2013, as well as balances with related parties as of 30 September 2014 and

31 December 2013:

Transactions between subsidiaries are eliminated on consolidation.

24