Embed Size (px)

Citation preview

Q1

• Use the growing annuity formula and solve for C.

• Plug in PV=50, r=0.1, g=0.07, T=30.• C=4.06

Q2

• Use the variance of a portfolio formula

• Plug in values remembering covariance is zero, so the last term drops out.

• Take the square root of the variance to find the standard deviation.(0.7^2*0.03^2+0.03^2*0.08^2)^0.5=0.0318

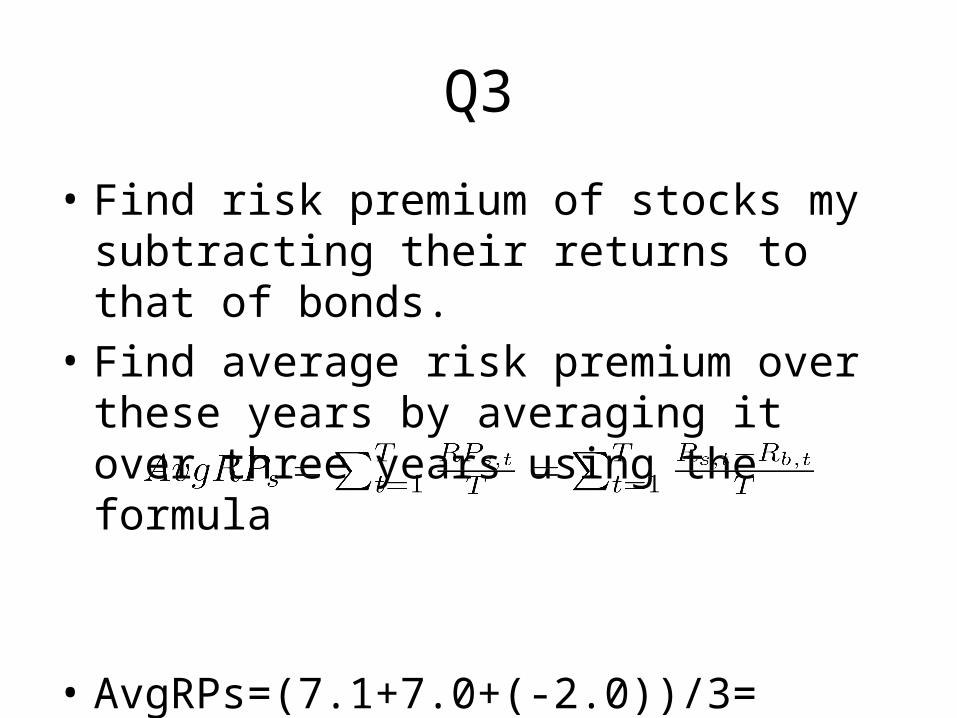

Q3

• Find risk premium of stocks my subtracting their returns to that of bonds.

• Find average risk premium over these years by averaging it over three years using the formula

• AvgRPs=(7.1+7.0+(-2.0))/3= 0.0403

Q4

• Find the present value at year 5 using the growing perpetuity formula with C=1, r=0.08, g=-0.1:

• Discount this result to year zero by dividing it by (1+r)^5

• PV=1/(0.08+0.1)*1/(1.08)^5=3.78

Q5

• The formula for the expected return of a stock is

• Solve for Rf and plug in for beta=3.5, Rs=0.31 and Rm=0.1

• Rf=(0.31-0.35)/(1-3.5)=0.016

Q6

• Find the rate of returns for each year using

• The geometric average return is

• Solution: plug return values into formula and T=3, and you get 0.087

Q7

• Use PV formulas for discounted future cash flows. The desired present value of the stock today is $40. The current value of the stock is the perpetuity paying $5 per period. Add an expression for an unknown dividend value x at the end of 8.5 periods, and solve for x.

• 40=5/0.15 + x/1.15^8.5• x=21.86

Q8

• Use PV formula:

• Solve for r, and plug in FV=550, PV=200, t=6.5• r= (550/200)^(1/6.5)-1= 0.1683

Q9

• Plug in those rates of return into the geometric average return formula for T=8:

Q10

• The variance of a sample is:

• In this case, the expected value of X is simply the arithmetic average of the returns for those three years. Plug this value as E(x) and each years returns as the xi, and N=3.

• Var=0.5(0.04-0.06)^2+(0.06-0.06)^2+(0.08-0.06)^2=0.0004, Std=Var^0.5=0.02

Q11

• Use annuity PV formula for coupon payments and face value at date 15.

• Adjust value by 3 months.

Q12

• Change this problem to bi-yearly periods

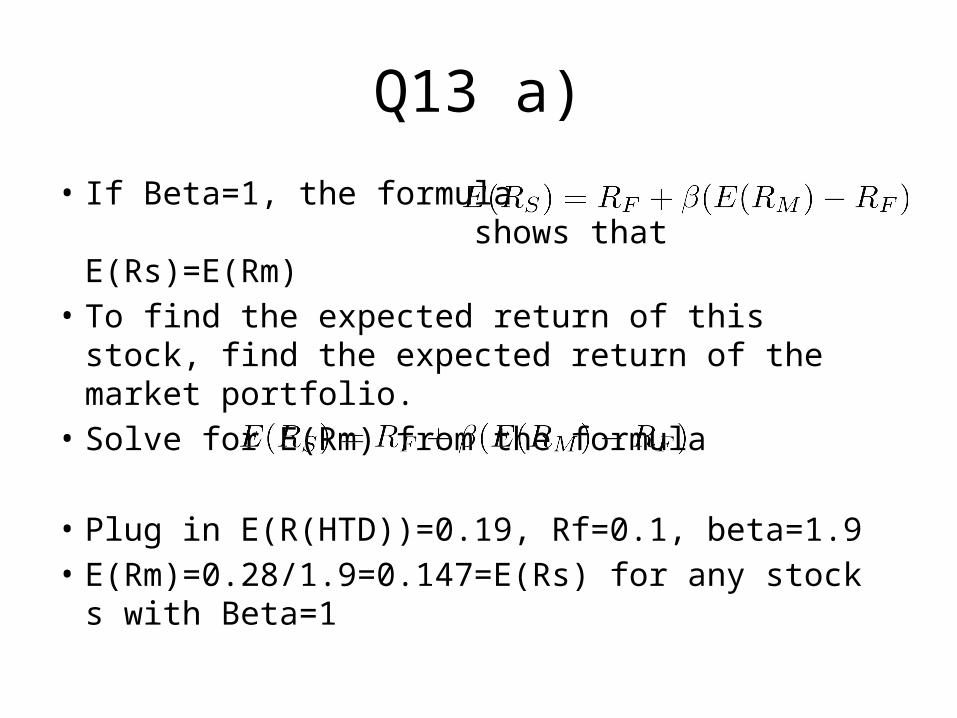

Q13 a)

• If Beta=1, the formula shows that E(Rs)=E(Rm)

• To find the expected return of this stock, find the expected return of the market portfolio.

• Solve for E(Rm) from the formula

• Plug in E(R(HTD))=0.19, Rf=0.1, beta=1.9• E(Rm)=0.28/1.9=0.147=E(Rs) for any stock s

with Beta=1

Q13 b)

• Use the formula for variance of a portfolio

• Note that the variance of a risk free bond is zero, there is no covariance either. So find the square root of the first term to find the variance of the portfolio. The variance of the risky asset is found with the following formula:

• Std=0.333(0.5(0-0.19)^2+0.5(0.38-0.19^2))^(1/2)=0.063

Q14

• Find the effective yearly rate using for m=3

• Plug in that value to find the effective rate over 6 months and one month

• Now change the problem to be semi-annual and discount an extra month at the beginning: