Embed Size (px)

Citation preview

Summer 2009

pwc: china compass News for experts

pwc

Hot topic China as global player? Chinese direct investment in Germany China’s health reform Implications for the pharma industry Investment and financing Business valuations in China Tax and legal New rules for restructuring and liquidation Economic spotlight: Asia Foreign direct investment in India

Contents

Editorial 3

Hot topic 4 China invests in Germany ............................................................ 4

Investment and financing 7 Investment: new powers to provincial governments should speed up process ......................................................................... 7 Business valuation in China: getting to grips with the problems and finding a solution.................................................... 9 Health care reform in China: what it means for the pharmaceutical industry.............................................................. 12 Acquisitions in China: effective protection against typical traps ........................................................................................... 14

Reporting and controlling 17 China introduces corporate governance regulations .................. 17 Economic crime during economic crisis: how to protect your firm ..................................................................................... 20

Tax and legal 22 Tax planning in the pharmaceutical industry � approach of increasing importance ................................................................ 22 Transfer pricing: Chinese administrative regulation sets new standards (Part 1) ............................................................... 25 New tax rules for corporate restructuring and liquidation in China.......................................................................................... 29 Driving � and taxing � vehicles in China..................................... 32 Tax presence in China: practical variations and applications ................................................................................ 35

Economic spotlight: Asia 38 Foreign direct investment in India: new rules for more transparency?............................................................................. 38

Portrait 40 Marc Wintermantel ..................................................................... 40

Publications 41 Investing in the Chinese pharmaceutical industry after health reform .............................................................................. 41 Economic crime during economic crisis...................................... 41 China news on the PwC Portal................................................... 41

PwC China Business Group 42

Imprint 43

2 pwc:china compass | Summer 2009

Editorial

Following the global economic crisis, we will be faced with a wave of crises in public finance. As a result, all sorts of creative answers to taxation questions are making the rounds in political circles. Jens-Peter Otto reveals what we can learn from the taxation of luxury cars in China � and what we shouldn�t do � in Driving � and taxing � vehicles in China (page 32).

Dear reader, You probably see it every day in the news. China�s interest in investing in Europe is steadily growing. Our colleague in Beijing, Dr Roland Spahr, brings you the latest on this hot topic, including a close look at current developments and difficulties, in his article China invests in Germany (from p. 4).

Do you know why a lucky bamboo plant should adorn the desk of every manager? Because it represents wealth, prosperity, health and success in business. With this in mind, I hope you enjoy this issue of pwc:china compass and wish you great success throughout the world!

China�s desire to invest in Germany follows a general trend that poses several important questions: Will China reshape the world economy as a global player? And how can we best work with Chinese investors? These questions are increasingly crucial for Western industrial nations as China is no longer just a seller�s market or an outsourcer�s paradise � it�s a strategic investor. Experience has shown that acquisitions by Chinese investors don�t always go smoothly. Not only do cultural differences affect negotiations, but so do different expectations of the outcome. For China, a nation with a long tradition of trade, the price of the target company is often the main concern. In contrast, strategy, risk management or a clear business plan as seen in the West are given less consideration. China has certainly grown from a trader into a global player, but its ambitious political goals are still a way off.

Yours, Franz Nienborg Member of the Executive Board PricewaterhouseCoopers AG Wirtschaftsprüfungsgesellschaft

There is some good news for foreign direct investment in China, as Jens-Peter Otto in Shanghai reports in his article Investment: new powers to provincial governments should speed up process on page 7. In direct comparison to these new measures in China, we also take a look at India in a piece by our colleague in the India Business Group, Iris Winkler, titled Foreign direct investment in India: will new regulations equal more transparency? (from page 38). On 30 April 2009, China�s Ministry of Finance published a much anticipated circular on restructuring, which follows on the heels of corporate tax reform in 2008. Two of our tax experts in Düsseldorf and Shanghai, Lea Gebhardt and Claus Schuermann, explain how this will affect your business activities in their article New tax rules for corporate restructuring and liquidation in China on page 29. Those of you who know China know that the country�s health care system is not up to par when it comes to efficiency. A health system reform aims to remedy the situation. Major investments and the development of comprehensive medical insurance should guarantee basic health care for the population of China. In addition, Beijing wants to reign in health spending. While this opens opportunities for international pharmaceutical companies and medical technology manufacturers, it also carries various risks. For more see the article by Dr Volker Fitzner, Health care reform in China: what it means for the pharmaceutical industry, on page 9.

pwc:china compass | Summer 2009 3

Hot topic

4 pwc:china compass | Summer 2009

China invests in Germany China has long been a popular investment location but as it develops into a global player, it is becoming an active investor as well – reason enough for us to look at Germany from a new perspective: how does the country appear to potential Chinese investors? – For the answers to this exciting question, read on. The political and economic environment beyond the Great Wall In the late 1970s, when China began to open up and launch its first economic reform, Chinese investment abroad was limited to just a few countries and regions. Due to its strong economic standing, (West) Germany was one of the five initial target destinations. Since the end of the 1990s, however, the number of Chinese enterprises investing overseas has risen significantly – a direct result of the ‘go abroad’ policy advocated by the Central Committee of China’s Communist Party. In 2004, the Chinese Ministry of Commerce (MOFCOM) and Ministry of Foreign Affairs jointly published an industry-specific guide for investors, the Catalogue for the Guidance of Foreign Investment Industries. In issuing these guidelines, the Chinese government once again underscored the importance of Chinese investment activities abroad. The catalogue contained official recommendations for investments in particular economic sectors in various countries. Investment projects which followed these specifications and obtained official authorisation were entitled to tax deductions, subsidies and further privileges. In Germany, the following industries and sectors were recommended: electrical industry, mechanical and plant engineering, pharmaceuticals and chemicals, trade, logistics, transport (ships, aircraft, lorries, cars), finance, and research and development. On 16 March of this year, MOFCOM issued its Measures for the Administration of Outbound Investment, which became effective on 1 May 2009. According to MOFCOM, the new regulation aims to introduce further reform to China’s outbound investment system. For example, lower-level government bodies will now be responsible for authorising Chinese companies to invest abroad. In addition, the approval process will be simplified so that the majority of outbound investment applications will only require a single standard application form and can be approved within three working days. The new regulation places great emphasis on simplification and expeditiousness, and serves to encourage Chinese companies to increasingly ‘go abroad’. In addition to the new regulation, MOFCOM reported on the potential for foreign investment in different geographical locations. Germany was among the first 20 countries selected from around the world, including five in Europe. By choosing to include Germany, the Chinese government clearly emphasised its strategic importance as an investment destination.

This article explains: ● how Beijing is encouraging Chinese outbound investment. ● which obstacles potential Chinese investors must overcome. ● why the number of Chinese acquisitions will rise.

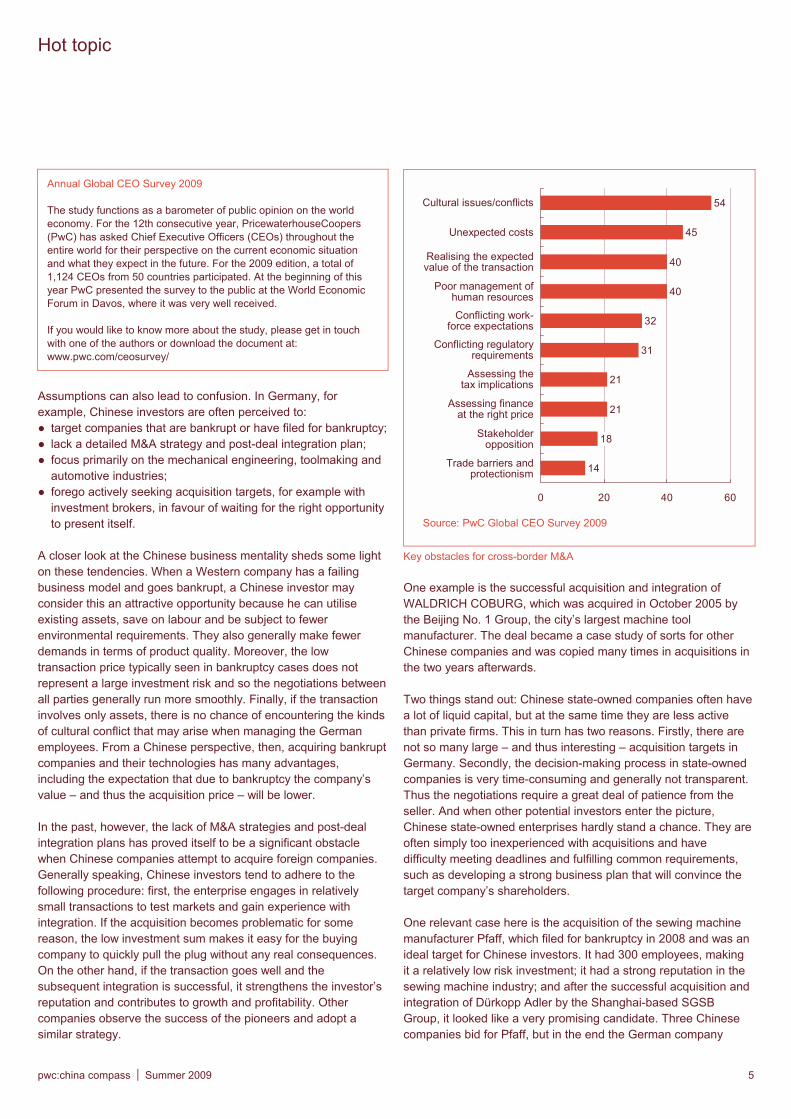

The report outlines Germany’s political, economic and social structures as well as giving practical advice for Chinese companies wanting to invest in Germany. By providing this information, MOFCOM aims to help Chinese companies better understand the German market and investment environment and take advantage of investment opportunities while avoiding potential risks. Although global financial flows have slowed dramatically since the beginning of the current economic crisis, China has continued to advance outbound investment. Finance industry data provider Dealogic reports that in 2008, the country’s M&A activities reached a staggering $52.1 billion. In the first two months of 2009 alone, Chinese domestic companies invested $16.3 billion abroad. If this pace continues, Chinese direct investment will double that of the previous year. The ongoing development of regulations for foreign investment coupled with investor education regarding activities abroad leaves no doubt that China is pursuing a long-term strategy. MOFCOM has also stepped up efforts to encourage Chinese companies to invest overseas, as Wu Xilin, a senior ministry official, stressed at a recent conference. By doing so, the Chinese government hopes to keep the country’s economy on course despite the global financial crisis. Chinese investments in Germany Economic strategies are not always easy to implement. And while governments can create a supportive legal framework, the decision to invest ultimately rests with individual companies. When it comes to engaging in transactions, many companies have learned from experience that differing cultural and historical backgrounds often present a significant stumbling block for a successful deal. Furthermore, it is not uncommon for each party to have completely different business practices and expectations. The Annual Global CEO Survey published by PricewaterhouseCoopers in 2009 identified cultural issues and conflicts as the most significant obstacle in cross-border M&A transactions. The managers participating in the survey named unexpected costs and failure to achieve expected value as the second-largest obstacle, suggesting that many companies – and Chinese enterprises in particular – often lack the experience needed to accomplish a complex merger or acquisition. Respondents also named post-deal integration issues, such as poor management of human resources, as a further challenge. It is likely that cultural differences and conflicting staff expectations play a large role here as well.

Hot topic

Hot topic

21

21

31

32

40

40

45

54

18

14

0 20 40 6

Unexpected costs

Trade barriers andprotectionism

Stakeholder opposition

Assessing financeat the right price

Assessing thetax implications

Conflicting regulatory requirements

Conflicting work-force expectations

Poor management of human resources

Realising the expected value of the transaction

Cultural issues/conflicts

Source: PwC Global CEO Survey 2009

0

Annual Global CEO Survey 2009 The study functions as a barometer of public opinion on the world economy. For the 12th consecutive year, PricewaterhouseCoopers (PwC) has asked Chief Executive Officers (CEOs) throughout the entire world for their perspective on the current economic situation and what they expect in the future. For the 2009 edition, a total of 1,124 CEOs from 50 countries participated. At the beginning of this year PwC presented the survey to the public at the World Economic Forum in Davos, where it was very well received. If you would like to know more about the study, please get in touch with one of the authors or download the document at: www.pwc.com/ceosurvey/

Assumptions can also lead to confusion. In Germany, for example, Chinese investors are often perceived to: ● ● ●

●

target companies that are bankrupt or have filed for bankruptcy; lack a detailed M&A strategy and post-deal integration plan; focus primarily on the mechanical engineering, toolmaking and automotive industries; forego actively seeking acquisition targets, for example with investment brokers, in favour of waiting for the right opportunity to present itself.

A closer look at the Chinese business mentality sheds some light on these tendencies. When a Western company has a failing business model and goes bankrupt, a Chinese investor may consider this an attractive opportunity because he can utilise existing assets, save on labour and be subject to fewer environmental requirements. They also generally make fewer demands in terms of product quality. Moreover, the low transaction price typically seen in bankruptcy cases does not represent a large investment risk and so the negotiations between all parties generally run more smoothly. Finally, if the transaction involves only assets, there is no chance of encountering the kinds of cultural conflict that may arise when managing the German employees. From a Chinese perspective, then, acquiring bankrupt companies and their technologies has many advantages, including the expectation that due to bankruptcy the company�s value � and thus the acquisition price � will be lower.

Key obstacles for cross-border M&A One example is the successful acquisition and integration of WALDRICH COBURG, which was acquired in October 2005 by the Beijing No. 1 Group, the city�s largest machine tool manufacturer. The deal became a case study of sorts for other Chinese companies and was copied many times in acquisitions in the two years afterwards. Two things stand out: Chinese state-owned companies often have a lot of liquid capital, but at the same time they are less active than private firms. This in turn has two reasons. Firstly, there are not so many large � and thus interesting � acquisition targets in Germany. Secondly, the decision-making process in state-owned companies is very time-consuming and generally not transparent. Thus the negotiations require a great deal of patience from the seller. And when other potential investors enter the picture, Chinese state-owned enterprises hardly stand a chance. They are often simply too inexperienced with acquisitions and have difficulty meeting deadlines and fulfilling common requirements, such as developing a strong business plan that will convince the target company�s shareholders.

In the past, however, the lack of M&A strategies and post-deal integration plans has proved itself to be a significant obstacle when Chinese companies attempt to acquire foreign companies. Generally speaking, Chinese investors tend to adhere to the following procedure: first, the enterprise engages in relatively small transactions to test markets and gain experience with integration. If the acquisition becomes problematic for some reason, the low investment sum makes it easy for the buying company to quickly pull the plug without any real consequences. On the other hand, if the transaction goes well and the subsequent integration is successful, it strengthens the investor�s reputation and contributes to growth and profitability. Other companies observe the success of the pioneers and adopt a similar strategy.

One relevant case here is the acquisition of the sewing machine manufacturer Pfaff, which filed for bankruptcy in 2008 and was an ideal target for Chinese investors. It had 300 employees, making it a relatively low risk investment; it had a strong reputation in the sewing machine industry; and after the successful acquisition and integration of Dürkopp Adler by the Shanghai-based SGSB Group, it looked like a very promising candidate. Three Chinese companies bid for Pfaff, but in the end the German company

pwc:china compass | Summer 2009 5

Hot topic

Joachim Richter Systeme und Maschinen e.K. won in spite of a higher Chinese bid. The decisive factor was the German company�s convincing long-term strategy and more solid and transparent business plan. Chinese companies have only recently started to show interest in larger and more complex acquisitions in Germany. Last year, for example, China Development Bank announced its intentions to acquire Dresdner Bank, and since the end of May this year, the Beijing Automotive Industry Company has been attempting to purchase Opel. Conclusion Careful observation of more recent M&A activities gives us good reason to believe that Chinese companies will continue to focus on uncomplicated, low-risk deals and probably ignore long-term investment analyses. At the same time, they are gradually starting to enter the market for more complex and large-scale transactions. Judging by the development dynamics seen in the past few years, we expect Chinese companies to quickly learn how to handle the transaction process more effectively, resulting in a rising number of successful acquisitions as well as the development of increasingly sophisticated acquisition strategies and concepts for long-term growth and profitability. The most crucial issue, however, remains: how can Chinese companies manage cultural differences and improve the integration process? The answer can be observed in companies from other Asian countries, such as Japan and Korea. Their experience has shown that while the differences arising from different approaches, business conduct and expectations may not be resolved completely, they can be overcome � something which Chinese companies with global aspirations will achieve, just as their Japanese and Korean counterparts have. Outlook Change is coming to the market and Chinese investors have become important participants. With time, cultural conflicts will certainly be transcended. Lots of signs point to increased Chinese investment in Germany, including the low valuations of many German companies resulting from the current tense financial situation. These companies offer China the opportunity to acquire new knowledge and technologies and gain access to international brands. It remains to be seen, however, how well Chinese companies will cope with the question of integration. Looking at the past 30 years, China has made great strides in opening up and becoming part of the world economy. Chinese companies are now on the cusp of understanding the essential aspects of developing sustainable business concepts and successfully closing deals. And in the current environment of relatively low-cost German companies available for purchase, the conditions for Chinese

investment are better than ever � the opportunity is simply too good to pass up. If you have any questions or would like more individualised information, please give us a call or send us an e-mail.

Contacts [email protected] Phone: +86 10 6533-7124 [email protected] Phone: +86 10 6533-5736 [email protected] Phone: +49 711 25034-3226

6 pwc:china compass | Summer 2009

Investment and financing

pwc:china compass | Summer 2009 7

Investment: new powers to provincial governments should speed up process The resourcefulness of the Chinese and their ability to adapt to new circumstances are legendary. Yet today routine approvals for businesses are burdened with conditions reminiscent of the Ming Dynasty. For this reason five new administrative directives with which the Ministry of Commerce recently delegated new powers to provincial governments deserve attention. They have two major goals: to revive the high level of foreign investment that China formerly enjoyed and to make it easier for the Chinese to invest abroad. Can the directives do this? In a free-market economy one of the most important prerequisites for successful entrepreneurship is the ability to make free and fast decisions about investments. Just how little decision-making freedom entrepreneurs have in China is reflected in the numerous approval hurdles potential investors must clear. One lesson to be learned from this is that China is still a long way from ridding itself of the fetters of the planned economy. Entrepreneurs need a great deal of patience to struggle through the bureaucratic restrictions China has placed on its economy. The 2007 edition of the Catalogue Guiding Foreign Investment in Industry ranks high among these. It divides the economic activities of foreign businesses into four categories: encouraged, permitted, restricted and prohibited. These categories determine in which industries foreign investments are possible and actively supported. Here it is important to take note of the restrictive foreign exchange controls for businesses with foreign and domestic investors. – More on this issue can be found in the article by Jens-Peter Otto and Anselm Stolte in the fall/winter 2008 edition of pwc:china compass (available in German only). Faster approvals by way of directive? Rendered wary by the cumbersome approval process and a flood of guidelines, businesses regard all undertakings of the Chinese economic authorities with a certain scepticism. – Whether or not the most recent steps in support of quicker investment decisions on the part of the Chinese ministerial bureaucracy will have the intended effect is best determined by taking a look at the regulations themselves. By means of five administrative directives the Ministry of Commerce recently transferred foreign investment approval authority to the provincial governments. What does this mean in practice? – Perhaps most importantly, threshold amounts have been introduced that determine whether an investment must be approved by the central government in Beijing. All investment projects that fall short of these amounts will be subject to the provincial authorities. With these measures Beijing is seeking to reduce administrative burden and thereby significantly cut down the time it takes for businesses to go through the approval process. Another goal is to encourage foreign companies to

This article explains: ● what approvals provincial governments will assume from the central

government. ● what lawmakers expect to achieve with this delegation of authority. ● what exceptions there are.

invest strongly in China again, as the level of foreign investment in China has dropped significantly since the end of 2008. All of the provisions of the directives discussed below are already in effect. Circular 50/2008 Increases in capital registered when establishing a foreign-invested enterprise (FIE) originally approved by the Ministry of Commerce can now be dealt with by provincial authorities as long as they do not exceed the following thresholds: ● up to $100 million for FIEs that had been approved by the

Ministry (this only applies to enterprises in the encouraged and permitted industries)

● up to $50 million for FIEs in the restricted industries Until now all capital increases had to be approved by the same authorities who approved the founding of the FIE. Circular 7/2009 The power of provincial governments to grant approval has been extended to the following: ● imported machinery and other equipment ● the establishment of FIE branches in and outside China ● increases in registered capital in order to expand the capacity

of automobile manufacturers (In China foreign automobile manufacturers – but not their suppliers – are limited by the provision that foreign ownership may not exceed 50 percent. Automobile manufacturing is generally included in the encouraged category of industries.)

● all other business matters, except changes in registered capital exceeding the aforementioned thresholds and the sale of a controlling share of an FIE from a Chinese entity to a foreign entity

● merger and acquisition transactions with a transaction value equal to or less than 100 million renminbi (RMB, about €10.9 million; in industries identified as encouraged and permitted) or RMB50 million (in the restricted industries).

Certain industry sectors have their own regulations, which are not affected by the new provisions and must still be adhered to. Circular 51/2008 The establishment of a commercial FIE will now fall under provincial jurisdiction. However this only applies if the commercial FIE does not deal in certain media (eg, televisions, audiovisual materials, telephones and the Internet) or distribute its products through these media.

Investment and financing

Investment and financing

Do you know that Baron de Rothschild is opening a vineyard in China?

The French wine producer is planning a 25-hectare vineyard on the Penglai peninsula in Shandong province. The Chinese will surely enjoy the wine, not only because of the tannins which are also found in their beloved tees, but because of its colour. For the Chinese, red is the colour of good luck.

Weinwelt, June 2009, Meininger Verlag (pub.)

你知道了吗

Circular 8/2009 Provincial governments are now responsible for approving the establishment and changes in registered capital of foreign-invested holding companies (FIHCs) that do not fall under the restricted and prohibited categories, as long as: ●

●

the initial capital or one-off changes in registered capital amount to less than $100 million changes in registered capital amount to less than $100 million for FIHCs originally approved by the Ministry of Commerce.

Circular 23/2008 The issuance of various approvals to real estate FIEs was simplified in June 2008 by the transfer of this authority to the provinces. Analysis and prospects

Any change that improves the climate for foreign-invested enterprises in China must be welcomed. However if Beijing really wants to create a level playing field for both foreign and domestic investors, it must do away with approval requirements as well as with the Catalogue Guiding Foreign Investment in Industry. Moreover, as in any other country, but especially in China, one has to wait and see how developments unfold in real life. Only this will show whether processing times actually become shorter under provincial jurisdiction. The new provisions do not contain any specifications on shorter time periods. But in many instances the delegation of power to provincial governments removes a level of bureaucracy, as provincial authorities and provincial departments of the Ministry of Commerce were previously involved in preparing for decisions.

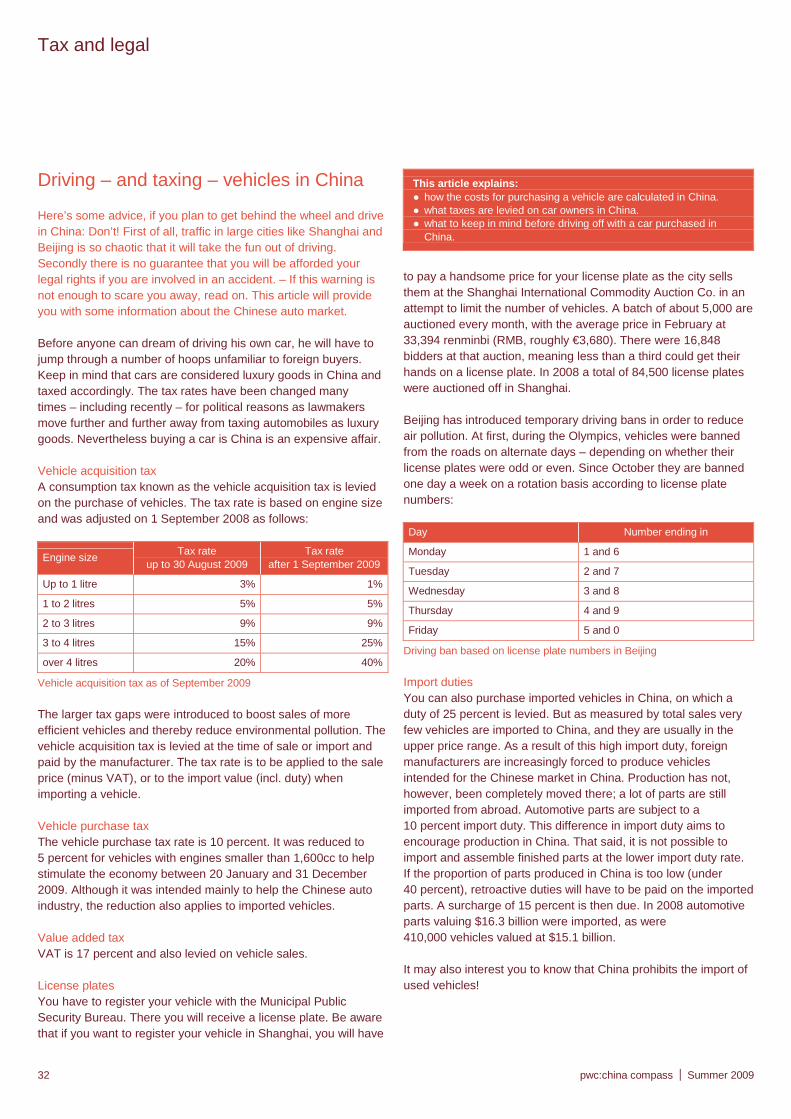

Foreign investment by Chinese companies China�s currency reserves currently add up to over $2 trillion. Around $700 billion of this is invested in US government bonds (as of 31 December 2008). By contrast Chinese foreign direct investment was barely $52 billion in 2008. By delegating the approval of Chinese investments abroad not exceeding $100 million, the Ministry of Commerce hopes to stimulate foreign investment by Chinese companies. Prices for businesses have sunk considerably around the world as a result of the current economic crisis, making investment attractive despite the risks involved. Do you have questions or would you like to learn more about the new directives? Then call us or simply send us an e-mail.

Contact [email protected] Phone: +86 21 2323-3350

8 pwc:china compass | Summer 2009

Investment and financing

pwc:china compass | Summer 2009 9

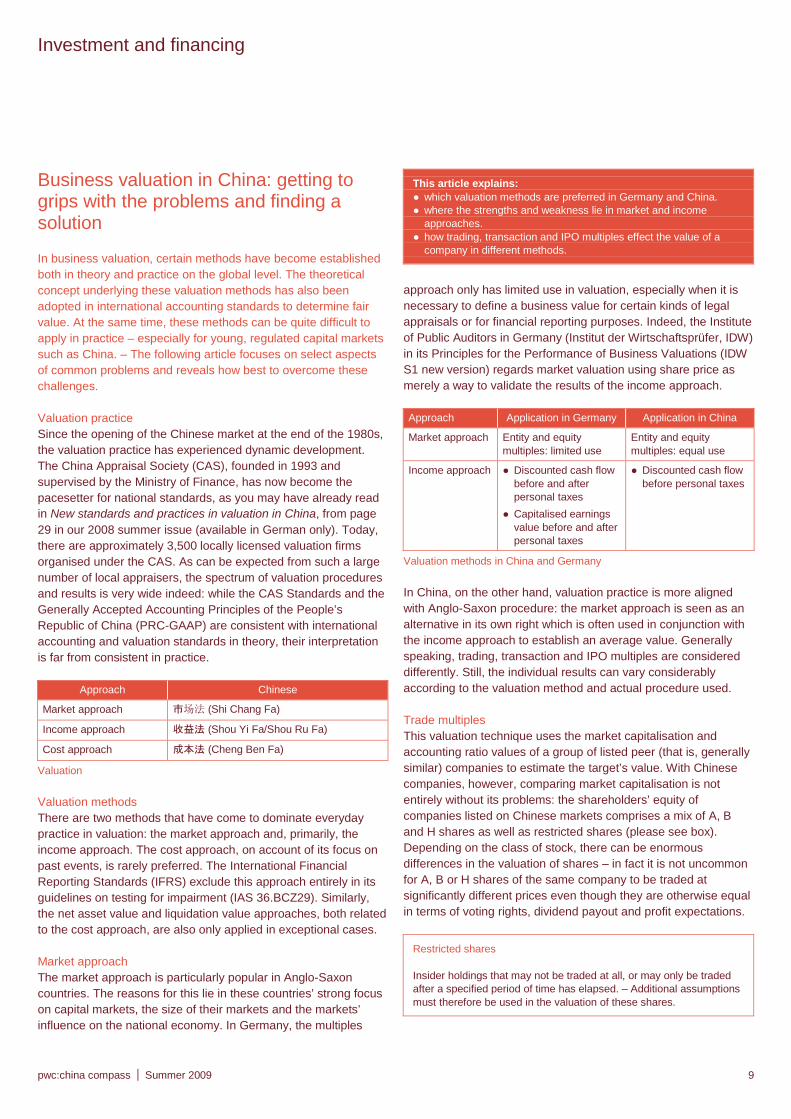

Business valuation in China: getting to grips with the problems and finding a solution In business valuation, certain methods have become established both in theory and practice on the global level. The theoretical concept underlying these valuation methods has also been adopted in international accounting standards to determine fair value. At the same time, these methods can be quite difficult to apply in practice – especially for young, regulated capital markets such as China. – The following article focuses on select aspects of common problems and reveals how best to overcome these challenges. Valuation practice Since the opening of the Chinese market at the end of the 1980s, the valuation practice has experienced dynamic development. The China Appraisal Society (CAS), founded in 1993 and supervised by the Ministry of Finance, has now become the pacesetter for national standards, as you may have already read in New standards and practices in valuation in China, from page 29 in our 2008 summer issue (available in German only). Today, there are approximately 3,500 locally licensed valuation firms organised under the CAS. As can be expected from such a large number of local appraisers, the spectrum of valuation procedures and results is very wide indeed: while the CAS Standards and the Generally Accepted Accounting Principles of the People’s Republic of China (PRC-GAAP) are consistent with international accounting and valuation standards in theory, their interpretation is far from consistent in practice.

Approach Chinese

Market approach 市场法 (Shi Chang Fa)

Income approach 收益法 (Shou Yi Fa/Shou Ru Fa)

Cost approach 成本法 (Cheng Ben Fa)

Valuation Valuation methods There are two methods that have come to dominate everyday practice in valuation: the market approach and, primarily, the income approach. The cost approach, on account of its focus on past events, is rarely preferred. The International Financial Reporting Standards (IFRS) exclude this approach entirely in its guidelines on testing for impairment (IAS 36.BCZ29). Similarly, the net asset value and liquidation value approaches, both related to the cost approach, are also only applied in exceptional cases. Market approach The market approach is particularly popular in Anglo-Saxon countries. The reasons for this lie in these countries’ strong focus on capital markets, the size of their markets and the markets’ influence on the national economy. In Germany, the multiples

This article explains: ● which valuation methods are preferred in Germany and China. ● where the strengths and weakness lie in market and income

approaches. ● how trading, transaction and IPO multiples effect the value of a

company in different methods.

approach only has limited use in valuation, especially when it is necessary to define a business value for certain kinds of legal appraisals or for financial reporting purposes. Indeed, the Institute of Public Auditors in Germany (Institut der Wirtschaftsprüfer, IDW) in its Principles for the Performance of Business Valuations (IDW S1 new version) regards market valuation using share price as merely a way to validate the results of the income approach. Approach Application in Germany Application in China

Market approach Entity and equity multiples: limited use

Entity and equity multiples: equal use

Income approach ● Discounted cash flow before and after personal taxes

● Capitalised earnings value before and after personal taxes

● Discounted cash flow before personal taxes

Valuation methods in China and Germany In China, on the other hand, valuation practice is more aligned with Anglo-Saxon procedure: the market approach is seen as an alternative in its own right which is often used in conjunction with the income approach to establish an average value. Generally speaking, trading, transaction and IPO multiples are considered differently. Still, the individual results can vary considerably according to the valuation method and actual procedure used. Trade multiples This valuation technique uses the market capitalisation and accounting ratio values of a group of listed peer (that is, generally similar) companies to estimate the target’s value. With Chinese companies, however, comparing market capitalisation is not entirely without its problems: the shareholders’ equity of companies listed on Chinese markets comprises a mix of A, B and H shares as well as restricted shares (please see box). Depending on the class of stock, there can be enormous differences in the valuation of shares – in fact it is not uncommon for A, B or H shares of the same company to be traded at significantly different prices even though they are otherwise equal in terms of voting rights, dividend payout and profit expectations.

Restricted shares Insider holdings that may not be traded at all, or may only be traded after a specified period of time has elapsed. – Additional assumptions must therefore be used in the valuation of these shares.

Investment and financing

Shares are classified A, B and H according to the currency they are traded in and which stock market they are traded on. A shares are traded in Renminbi and B shares in US dollars or Hong Kong dollars (HK dollars) on the Shanghai and Shenzhen exchanges; H shares are only traded in HK dollars on the Hong Kong exchange. A and B shares are often traded at a (sometimes large) premium to H shares. Still, the difference in pricing is not a result of the different currencies or markets but rather of capital market restrictions for investors: Chinese citizens are only allowed to invest in A and B shares while foreigners were, for a long time, restricted solely to H shares; several years ago, the regulations were altered to include B shares as well. Transaction multiples When performing valuations using transaction multiples, it is important to remember that detailed information about the transactions is often not available. In addition to this general limitation, transactions in China are often executed according to political motives, making it essential for appraisers to carefully scrutinise the published price of a transaction before using it as the basis for comparison. Furthermore, in the majority of cases the purchase price reflects a value that includes buyer-specific synergies, which may not be considered in the financial reporting. IPO multiples Valuation using IPO multiples is largely dependent on the date of the IPO in question. In view of the extremely volatile stock markets of the last years, peer groups for comparison should only include companies with IPOs which occurred at approximately the same time. Furthermore, the admission of shares is controlled by the Chinese exchange supervisory authority and the influence of political interests cannot be discounted entirely. This is especially true for the IPOs of state-owned enterprises. In the past years, the first stock market valuations were sometimes far higher than the issue price � and that was not due to the high demand alone. In this type of environment IPO multiples can produce low business values and therefore should be interpreted as a lower value limit. In all three approaches the denominator is taken from reference values based on accounting information. These include turnover, earnings before interest, taxes, depreciation and amortisation (EBITDA), or earnings before interest and taxes (EBIT) for the gross method, based on the total business value including liabilities (entity multiples); or on the annual net income for the net method, based on the shareholder�s equity used (equity multiples). In order for the multiples to provide an accurate estimation, it is imperative that the object of valuation and the peer companies use the same accounting policies. All the same, the different options for drawing up the balance sheet and profit and loss account allowed by PRC-GAAP, IFRS and US-GAAP do complicate a comparison across the group, making it necessary to adjust or reconcile the values to the actual balance sheet and profit and loss account. Of course, this step assumes that all

necessary information is available from the peer companies. If it is not, then the differences in accounting policy can produce business values that are not suitable for comparison. Financial crisis As the financial crisis has thrown capital markets throughout the world into a downward spiral, additional limitations of the market approach have surfaced in the past few months. A tightening of the credit approval process, dwindling liquidity and steep drops on the stock markets have caused slumps and, in many places, total stagnancy in transactions and IPOs, making a prompt valuation using transaction and IPO multiples temporarily impossible. Sharply declining prices on the stock exchanges in Shanghai and Shenzhen often resulted in a market capitalisation value which was beneath the equity book value of the companies. The figure below shows the development of the Shanghai Composite Index over the last 10 years.

1.000

2.000

3.000

4.000

5.000

6.000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0

16

32

48

64

80

Shanghai Composite IndexPrice-earnings multiple

Sha

ngha

i Com

posi

te In

dex

Pric

e-ea

rnin

gs m

ultip

le

+482

.38%

+60.

18%

�70.

71%

Shanghai Composite Index, 1999�2009 Income approach In addition to the internationally accepted discounted cash flow (DCF) analysis, the income approach is generally preferred in Germany and is also applied in the majority of valuations performed for corporate or general law purposes. Both of these approaches focus on the future profitability of the company where the business value is calculated as the net present value of the future expected surplus. Income tax is � without exception � taken into account when calculating the company�s surplus. When appraising the business at shareholder level (equity value), it has become established in German theory and practice to consider the net inflows after personal taxes at shareholder level (and consequently to proceed in the same manner for the discount rate). For the valuation of equity holdings and other investments for the annual financial statements as required by commercial

10 pwc:china compass | Summer 2009

Investment and financing

Balancing approaches and valuation law, IDW RS HFA 10 still stipulates that surpluses be considered before personal income tax. In the past, the Chinese GAAP have come close to agreeing with

the IFRS. For listed companies the new PRC-GAAP went into force on 1 January 2007; exactly one year later, they were also made applicable to large state or financial service companies. This harmonisation implies some changes that could be relevant for valuation, for example, development costs can now be capitalised and amortised for the rest of their useful life. Furthermore, fixed assets can now be given a residual value of zero; previously this value was fixed as 10 percent of the acquisition costs. Both of these changes effect the income statement of a company and, particularly in the market approach, will lead to different valuation results. The introduction of balancing sheet accounting at fair value for receivable and liabilities will raise or lower the net current assets of a company, something which must be considered when calculating the free cash flows in the DCF approach.

As mentioned earlier, Chinese valuation follows the Anglo-Saxon approach to valuation, which, in turn, in the application of the income approach is confined to DCF analysis. Generally speaking, the income approach is not applied. In addition, the personal income taxes of the shareholders are not considered during valuation. In calculating the future surplus, called free cash flow in the DCF method, the underlying budget review should be carefully checked against the annual financial statements of the past fiscal years to confirm its feasibility. In doing so, it is important to remember that, just like in the market approach, different accounting policies and interpretation can result in different value assessments. In quickly growing industries and businesses like those in China, for example, a different interpretation of revenue recognition can produce a misleading value.

Moreover, not all companies in China have implemented the new standards. Some companies, for example, record advance payments as sales revenue, which means they are reporting inflated revenues and results. Consequently it is necessary to perform a critical analysis of the company�s historical performance and make any necessary adjustments to arrive at an accurate assessment of the budget review.

In checking the feasibility of budget reviews, particular attention must be paid to the consideration of revenue growth, profit margin, and capital requirements for current assets and investments. Here it is important to note that in China expectations are significantly higher and companies often expect to see a two-figure growth rate for the next three to five years. For appraisers, it is then important to make sure that these expectations are in line with both the company�s historical growth and the middle-term expectations for individual sectors and the market as a whole. Then they must also verify that the company�s budget review appropriately reflects the capital requirements for current assets and investments which would be necessary to achieve the targeted growth. Finally, it is important to discuss with the company which long-term expectations are to be applied in terms of perpetuity. Experience has shown that growth assumptions for perpetuity are often 2 to 3 percent higher than in longer established economies in, for example, Central Europe or North America.

Conclusion Business valuations are extremely important: they influence the pricing and value assessment for transactions or any other case where a valuation is required by corporate law; and they also become relevant in financial reporting when fair value-oriented accounting standards are applied. Theoretically, many different valuation methods can be used. In practice, however, certain methods have by now come to the fore in China (as shown in the figure). For this reason, the question of which valuation method to use is not of central importance. Instead, priority should be given to compiling the necessary information and ensuring its reliability. In addition, it always important to take into consideration the different classes of stocks owned by a company when performing a valuation. And finally, when evaluating the cost of capital, it should be kept in mind that the Chinese market is still relatively young and regulated.

A further challenge in the income approach is the calculation of a risk-adequate discount rate. In practice, no other parameter is more critically regarded than this one: its leveraging effect means that even minor adjustments can disproportionately influence the business value.

Our experts are happy to help you further. You can reach them by phone or e-mail.

In calculating the cost of capital in China, country-specific capital market risks, currency exchange risks and differences in inflation rates must be considered. Reflecting these risks regularly leads to higher capital costs that in, for example, Western Europe or North America � the market risk premium for China has proved to be 3 to 4 percent higher than in Western Europe of North America. Additionally, it is important to determine how much inflation expectations have been reflected in the planned cash flows and, if necessary, to adjust the discount rate.

Contacts [email protected] Phone: +65 6236-7378 [email protected] Phone: +86 21 2323-2632

pwc:china compass | Summer 2009 11

Investment and financing

12 pwc:china compass | Summer 2009

Health care reform in China: what it means for the pharmaceutical industry The Chinese government has announced sweeping reforms of the country’s ailing health care system. Two major steps are being taken to insure affordable basic health care for all Chinese: a high level of investment in the medical infrastructure and the development of comprehensive medical insurance. At the same time the government wants to exercise more supervision of and control over health care expenditures. These reforms offer both opportunities and risks for pharmaceutical manufacturers. Only those companies that adapt quickly to the new distribution and pricing policies will profit from growth in this area. The Chinese government has been grappling with the weaknesses of the health care system for some time. The current medical infrastructure is insufficient in large part because when the state greatly reduced its involvement in health care during the 1980s, it did not take steps to set up private financing of the system. A major problem is that there are few doctors and hospitals to be found in rural areas. Moreover, only a small portion of the Chinese population has medical insurance. According to the Ministry of Health, patients have to pay for almost 50 percent of treatment and drug costs out of their own pockets. Key aspects of the reform programme 2020 is the target set by the government and the Central Committee of the Communist Party for completing reforms that will lead to an effective nationwide health care system. The first stage alone – through 2011 – will cost the government the equivalent of about $124 billion. The blueprint for this reform (Opinions on Deepening Pharmaceutical and Health System Reform, draft dated 14 October 2008, as well as Implementation Plan of the Ministry of Health dated 21 January 2009) put forth five major initiatives: ● providing some form of medical insurance for 90 percent of the

urban and rural population by 2011 ● developing a national system to regulate drug selection,

prescription, distribution and reimbursement ● building a nationwide infrastructure to provide basic health care ● promoting equal access to basic medical services in rural and

urban areas ● increased government funding of hospitals If the reforms are successful, the demand for medical services and drugs will undoubtedly rise. However this does not necessarily mean increased turnover for pharmaceutical manufacturers. This is because it is still unclear what regulations will be implemented to govern the allocation, control and pricing of drugs, and what the relationship will be between traditional Chinese medicine and Western pharmaceuticals.

This article explains: ● what is wrong with China’s current health care system. ● what role traditional medicine plays in China today. ● how the reforms will affect the pharmaceutical industry.

Greater transparency in distribution The distribution of pharmaceuticals in China is highly complex. There are few pharmacies, and generally only in the cities. Patients buy about 80 percent of Western drugs from hospitals, which in turn are supplied by thousands of intermediaries. Clinics refinance themselves primarily through the profits they make from selling medicine, so they often prescribe more – and more expensive – medications than necessary. In addition, the system is susceptible to corruption. The temptation is great for manufacturers to pay doctors to prescribe their products over those of their competitors as much as possible.

Pharmaceutical manufacturers

Intermediaries

Clinics (share of turnover:

about 80%)

Pharmacies (share of turnover:

about 20%)

Patients

Source: Business Monitor International

Distribution of drugs and pharmaceuticals in China To combat this problem, the government wants to wean hospitals off their reliance on drug sales revenue. Doctors are to earn more money from actually treating patients and the costs that arise are to be covered by medical insurance. Pharmacies will take on new importance as the government tries to restructure hospital financing and separate drug prescription from drug dispensation. Companies in the pharmaceutical industry must prepare themselves for these developments. The biggest task will be making necessary changes in distribution networks. One the one hand, they must secure market access. On the other, they must overcome logistical challenges such as, for example, uninterrupted cooling of medication transported over long distances to rural regions. Prices will continue to be regulated Even after the reforms, manufacturers and distributors of pharmaceuticals will have to abide by government price controls. While exceptions will certainly be made for innovative new drugs,

Investment and financing

there are as of yet no concrete proposals or regulations that could provide guidance. The state currently regulates the price of around 2,400 pharma-ceuticals. About 60 percent of drug sales are subject to such controls. In practice, however, they have not led to a drop in prices. Although there have been 24 rounds of price-cutting in the past 10 years � with categories of drugs reduced in price by around 20 percent � the average price of medication only dropped 2.8 percent between 1996 and 2007. What actually happens is that price controls lead to lower revenues for the pharmaceutical manufacturers affected. When the sale price for a particular drug is lowered, the intermediaries and hospitals switch to other, more expensive ones. Moreover, many manufacturers respond to price controls simply by taking the respective drug off the market. They then introduce a slightly altered version under a new name, one that is no longer subject to price controls. The National Development and Reform Commission is responsible for drug price controls and aims to implement more effective rules by 2011. In all likelihood the authorities will set maximum drug prices for each step of the supply chain � from manufacturers to clinics and pharmacies. In addition, there is talk of introducing a flat rate dispensing fee instead of the price-based reimbursement that pharmacies can currently claim for the sale of medications. With the introduction of this reform, doctors in clinics would no longer have incentive to prescribe unnecessarily expensive medications. Competition from traditional medicine The Chinese pharmaceutical market will remain a special challenge for foreign drug manufacturers, even if health care reform eventually leads to a distribution and payment system similar to that found in Western industrial nations. This is due primarily to the popularity enjoyed by treatments used in traditional Chinese medicine (TCM). Two out of every three medications sold now come from TCM. Turnover from TCM in 2007 was around $21 billion; that amounts to 40 percent of all turnover in Chinese pharmaceuticals. According to some experts, the market volume for such treatments could increase to $28 million by 2010. One factor to take into account in such predictions is the explicit support given to TCM prescriptions within the reform programme. Until now foreign manufacturers have hardly been represented in the TCM segment. Things may well change if Western investors take advantage of the expected consolidation of this sector as a way into the market. At present the market for traditional Chinese medications is fragmented. Around 1,100 providers are registered with the Chinese authorities, of which only 300 meet official quality standards. Many manufacturers lack the capital to

modernise production equipment and introduce control processes. This situation offers Western companies numerous opportunities to invest. The next edition of pwc:china compass will keep you up-to-date on further developments. � To learn how corporate tax reform will affect the pharmaceutical industry please read the article by Claus Schuermann und Ralph Dreher on page 22 of this issue. If you would like further information, please call us or simply send an e-mail.

Contacts [email protected] Phone: +49 69 9585-5602 [email protected] Phone: +49 69 9585-5604

Do you know what �Chinoiseries� are?

In the 18th century, an art form became popular in Europe that was modeled on Chinese examples and influenced by motifs of a supposed Chinese utopia. The image of a massive yet peaceful empire whose population - down to the lowest classes - was educated in literature and philosophy triggered a considerable pro-China zeal in many European countries.

China Takeaway, Hans Hauenschield, Ullstein (pub.), 2007

你知道了吗

pwc:china compass | Summer 2009 13

Investment and financing

14 pwc:china compass | Summer 2009

Acquisitions in China: effective protection against typical traps Local and international companies are trying ever harder to position themselves as best they can on the rapidly expanding Chinese market, and consequently the number of mergers and acquisitions are on the rise. Nevertheless, most European investors still find Chinese transactions hugely challenging. – This article by our Swiss expert team Ralph Schlaepfer and Jia Ye You sheds light on the background as well as the stumbling blocks for European investors planning an acquisition in China’s incredibly dynamic marketplace. 1. The marketplace Challenging and conservative Although the Chinese government is anxious to reconcile the needs and issues of parties in a transaction, the latest amendments to merger and acquisition (M&A) regulations and their strict implementation have only served to increase the parties’ sense of insecurity. Furthermore, official regulations are constantly evolving, providing a steady stream of questions the Chinese government needs to address. Finally, many initiatives in this area are influenced by national interests, which tend to give them a more conservative character. As a result, European investors need to closely monitor developments in the regulatory environment, as well as any amendments to regulatory statutes arising from these developments, and integrate the changes into their decision-making processes. It is highly beneficial to have a flexible attitude which allows for quick adaptation to the latest regulatory developments. Discrepancy between local and national interpretations of law Even though China has a reputation for being very centralised, the Chinese administrative system grants local authorities considerable leeway when it comes to the implementation of national directives at the local level. Local officials sometimes interpret official laws in a manner that benefits one party over another, or enforce national legislation in a way that is not always entirely appropriate. European investors need to realise that the national government always has precedence in the interpretation of law. Should there be any discrepancies, this can lead to high follow-up tax demands or even fines. Compliance Chinese companies of particular local significance occasionally engage in certain business practices that, strictly interpreted, violate the already loosely enforced laws. Well-intentioned advice from business partners and other industry insiders on how to best exploit such grey areas is to be treated carefully. European investors must always remember that just because a practice is common in a local market does not mean it is legal or not subject

This article explains: ● what typical traps can befall foreign companies trying to acquire a

holding in a Chinese company. ● how Chinese and European expectations differ during acquisition

negotiations. ● why due diligence is almost always advantageous.

to penalty. It is therefore very important to determine whether a custom is simply tolerated or whether it is actually in compliance with Chinese law. In addition, European investors need to carefully consider their own domestic legal system before deciding to take advantage of more dubious interpretations of Chinese law. Personal relationships: ‘guanxi’ We should never underestimate the extent to which cultural differences can effect our interactions. Personal relationships are a central aspect of Chinese business culture. Without them, it is almost impossible to successfully close a deal. All the same, one should never rely entirely on personal relationships during a transaction – the terms of any agreement reached orally should always be put in writing. Integrity of local business partners China is sometimes referred to as the ‘Wild East’ on account of the questionable practices adopted by some individuals to close transactions or achieve personal gain. When working with local business partners a certain level of caution is necessary to keep risks to a minimum. 2. Systemic inefficiency Processes Compared to their European counterparts, Chinese companies do not place as much emphasis on such topics as confidentiality, privacy and due diligence. Declarations of intent are usually signed relatively early on and are often based on vague and non-binding ideas. In light of this, parties should not expect their Chinese transaction partners to place much importance on written agreements; even signed memorandums of understanding are still not viewed as binding. Before a transaction can be carried out the partners also have to obtain regulatory approval from various authorities, which makes the entire process very time-consuming. European investors have to realise that it is very important to maintain continuous communication with the authorities. Chinese companies may also change their mind at the drop of a hat. The resulting delay in a project can be very stressful for Europeans. Perseverance is therefore one of the most important factors in the successful closing of a transaction.

Investment and financing

Information In many aspects, the quality and availability of information is often poor and does not live up to the standards that European investors have come to expect. This is accentuated by two additional factors: ●

●

● ● ●

3.

● ● ●

●

●

●

There are hardly any public sources that can be used to verify information. Many companies either have never been audited, or have merely had a poor quality audit.

Chinese companies traditionally tend to concentrate on day-to-day operations rather than on administrative processes and proper accounting. Consequently, business decisions are seldom made based on accounting records. Poor accounting systems may also contribute to insufficient budgeting or a complete lack of budgetary controls. Moreover, many Chinese companies keep two or even three different books:

one for the tax authorities one for internal use one for the bank

Financial statements may also be manipulated for several reasons. Europeans can minimise the resulting risk with an early and extensive implementation of due diligence processes. Since many Chinese companies tend to emphasise daily operations, they often do not understand or even know about due diligence, making it absolutely vital to thoroughly explain the process to the Chinese seller. Experience has shown that it is best to focus due diligence on the most important factors for the viability of the company after the acquisition. Valuations Buyers and sellers often have very different price expectations for entirely different reasons. One reason is that differing valuation methods are used. The Chinese prefer valuation methods which diverge from international standards, for example the net asset valuation method compared to the internationally preferred discounted cash flow method. Chinese sellers with little experience in transactions also tend to have price expectations that are more closely related to general market conditions than to their company�s actual facts and figures. According to Chinese law, state-owned enterprises are also subject to a statutory valuation, which is conducted by a state-licensed expert appraiser usually selected by the target company. While the qualifications of these �experts� are often dubious, their valuations are very significant since the Chinese government must approve sales prices that are below 90 percent of the statutory valuation. Two further circumstances make it difficult for European investors to determine the value of a company. There is usually neither

reliable data for comparison nor key figures for the market. Therefore buyers, especially those who do not know much about doing business in China, are at risk of paying too much for their acquisition. European investors thus need to remain involved in the complete valuation process and follow it closely.

Typical problems Accounting practices Although Chinese accounting principles increasingly adhere to the International Financial Reporting Standards (IFRS), they are sometimes incorrectly applied in practice � whether out of ignorance or intentionally. The most common deviations are:

incorrect revenue recognition policy; sales which were not invoiced or recorded; inadequate recording of accruals and deferrals (eg, of discounts granted, product guarantees or severance payments).

The financial implications of such irregularities are often difficult to estimate since the information needed to do so is generally unavailable. Group transactions Many Chinese companies are bound up in complicated corporate structures and often earn a large percentage of their revenue from sales to affiliated companies. Should a company be acquired from this type of affiliated group, it is very important for the European investor to be able to precisely follow transactions with affiliated companies, the fundamental agreements behind these transactions and their financial impact. Assets

Unclear ownership: It is often difficult to discern property rights to assets in China, which is why they should be thoroughly analysed. For example, the same assets could be used as collateral to back up obligations to several third parties. Land-use rights: The transfer of land-use rights needs to be closely examined during due diligence because, depending on the nature of the land-use rights (whether land was granted to the company, or allocated, or is collectively owned by the groups of farmers), the state can demand significant or financial compensation for authorising a transaction or completely refuse the rights transfer. External assets: Domestic companies, especially state-owned enterprises, often function as a sort of social community and thus frequently own assets such as employee accommodation, hospitals, schools and restaurants. Their value is usually fairly low for the buyer; however the Chinese transaction partner will sometimes expect the foreign investor to purchase them and continue providing the social services.

pwc:china compass | Summer 2009 15

Investment and financing

Liabilities Chinese companies� books often do not include all of the debts and other liabilities. This is especially true for the disclosure of contingent liabilities and bank guarantees, which were issued for other companies within the group or for third parties. Chinese companies, especially state-owned enterprises, often have higher reserves than are needed in order to cover such employee-related obligations as contributions to social security, pension obligations or obligations arising from the conversion of a non-cancellable employment contract into a cancellable one. In addition tax law violations may lead to higher taxation risks for which no reserves are available. For that reason it is important to perform an extensive audit of the company being acquired to uncover all possible hidden or contingent liabilities. Based on the due diligence results and the buyer�s readiness to assume risk, a decision must be made as to whether the company should be acquired through equity or asset acquisition.

Equity and asset deals Equity is capital brought into a company by one or several proprietors. An asset deal is a basic form of acquiring a company where the assets are individually transferred.

Further aspects A few other issues pose typical problems for M&A transactions in China. When dealing with Chinese companies it is very important to keep an eye on: ●

● ● ● ●

4.

●

●

●

non-compliance with safety, health and environmental regulations; unnecessary personnel (especially in state-owned enterprises); unclear sales channels; diverging business interests for the joint venture partners; how much the commercial success of the company is dependent on key personnel (ie, because of their relationships).

Conclusion

Chinese M&A transactions follow their own rules. That is why PricewaterhousCoopers recommends that all companies planning such a transaction proceed systematically and align their transaction goals with those of local interest groups from the very beginning. It is especially important to:

emphasise the advantages of the transaction for all stakeholders from the get-go; quickly take control of the acquired company after the transaction is finalised; quickly introduce one�s own business culture.

Most European investors appreciate receiving regular advice from a qualified, locally based team which understands the industry of the target company as well as the M&A market in general, and

can closely follow negotiations to guarantee a successful acquisition. If you have any questions or would like advice, please feel free to contact us by phone or e-mail.

Contacts [email protected] Phone: +49 69 9585-5666 [email protected] Phone: +86 10 6533-7124

16 pwc:china compass | Summer 2009

Reporting and controlling

pwc:china compass | Summer 2009 17

China introduces corporate governance regulations As of 1 July 2009, China’s Basic Standard for Enterprise Internal Control (‘China SOX’ or ‘C-SOX’) is in effect. For more background, see the article China introduces legislation on internal controls in the spring edition of your pwc:china compass. While C-SOX applies to all companies listed on Chinese stock exchanges, all large and mid-sized non-listed companies are also being encouraged to adopt the Standard. Foreign companies active in China are no exception, meaning that joint ventures with domestic-listed companies are now subject to the regulations as well. To find out what all companies should keep in mind, read this article by Roland Spahr and co-author Anna-Katharina Viessmann . In 2002 the US government set new standards for corporate governance when it passed the Sarbanes-Oxley Act (SOX) in the wake of several major accounting scandals. Mandating a system of internal controls in companies, SOX places additional responsibility on both executive boards and auditors and obligates them to improve the company’s financial reporting practices. Other countries have followed America’s lead in the mean time: ● South Africa passed The King Code in 2002. ● Hong Kong issued the Hong Kong Code of Governance

Practice in 2004. ● Japan enacted its Financial Instruments and Exchange Law

(J-SOX) in 2006. ● Canada introduced National Instrument 52-109 in 2008. ● In March 2004, the European Commission published a

proposal, known as E-SOX, to modernise the 8th EU Directive and set down basic principles similar to those of the Sarbanes-Oxley Act. The bill has yet to be passed, meaning that German companies are still subject only to the German Corporate Governance Code of 2002, which covers similar content but is less extensive in scope.

Purpose After the fall of Guangxia Industry Co. Ltd., dubbed ‘China’s Enron’, and a string of other corporate scandals in 2001, the Chinese government also took a stand against corruption. In accordance with the instructions of China’s State Council, the Enterprise Internal Control Standard Committee was founded in 2006. It consists of the Ministry of Finance (MOF) and several other important government authorities. The Basic Standard was jointly released on 28 June 2008 by: ● the MOF; ● the National Audit Office; ● three of the largest economic regulatory authorities; ● the China Banking Regulatory Commission; ● the China Securities Regulatory Commission; ● the China Insurance Regulatory Commission; ● the Ministry of Commerce.

This article explains: ● which documents detail the new Standard. ● what C-SOX does and which companies it affects. ● how the regulations differ from those in other countries.

The Standard was officially published on 22 May 2008 in Caikuai No.7 (The Circular), which contained instructions for facilitating the introduction of C-SOX and outlined its regulatory requirements for internal controls. To further assist companies in implementing the Standard, three more documents were issued in September 2008: ● Guidelines for Evaluation and Assessment of Effectiveness of

Enterprise Internal Control ● Implementation Guidelines for Enterprise Internal Control ● Guidelines for Performing Assurance Engagements in Relation

to Assessing Effectiveness of Enterprise Internal Control Please refer to the appendix for more on these three documents and other documents which helped prepare for and guide the implementation of C-SOX. Structure and Applicability C-SOX contains seven chapters, a total of 50 articles. The first chapter defines the purpose and applicability of the regulations and lays down the guidelines for a company’s annual audit. Chapters 2 to 6 address the five elements of internal controls, such as risk assessment. The last chapter contains the date when the regulations come into force and advises of possible future amendments that may be added by the financial authority or other government-related organisations in addition to the Standard. C-SOX is in effect since 1 July 2009, initially applies to approximately 1,700 companies: 900 companies listed on the Shanghai Stock Exchange and about 800 listed on the Shenzhen Stock Exchange. C-SOX aims to protect stock market investors and to this end demands the provision of more precise information and specifies stricter regulations for corporate financial reporting. In light of the extensive and complex scope of the Standard it seems very likely that it will be implemented in unlisted large and mid-sized companies in the long term, even though the Enterprise Internal Control Standard Committee has not set a specific date. As such, businesses are well advised to integrate the Standard into company policy as soon as possible – and since the regulations do not differentiate between domestic and foreign enterprises, compliance is also mandatory for German companies that are traded on Chinese exchanges. US role models C-SOX combines the basic principles from both of the following publications issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO): ● Internal Control – Integrated Framework (1992) ● Enterprise Risk Management Framework (2004)

Reporting and controlling

Reporting and controlling

While the 2004 publication focuses on processes, most notably the steps in registering a stock corporation, the 1992 publication was chiefly concerned with establishing definitions for fundamental concepts such as the five elements of internal control. These elements � internal environment, risk assessment, control activities, information and communication and internal monitoring � also form the backbone of the Chinese Basic Standard, meaning they must also be included in any effective internal control. Furthermore, the Standard requires that every company listed in China establish the conditions necessary to introduce embezzlement controls and draft a company procedural code for the case that any fraud does surface. International comparison C-SOX is significantly more complex than its foreign equivalents. One of the most fundamental differences is the very definition of �internal control�: China�s Standard clearly and precisely defines it by listing the five elements. SOX and J-SOX, on the other hand, name no specific points, instead leaving it up to the companies to establish their own relevant areas. Another central difference is the scope of the companies affected: SOX focuses on external accounting procedures, an aspect of the regulation that was developed primarily for listed companies. In China, however, the Standard is designed to make possible the later implementation in unlisted companies as well. To this end C-SOX not only regulates external accounting but also transactions, and specifies the procedures to be followed. The safeguarding of assets and implementation of fraud prevention controls are described in particular detail. Other elements are similar to the international SOX standards: ●

●

●

The Board of Directors is responsible for implementing and monitoring C-SOX compliance. The supervisory board in turn shall monitor the Board of Directors� actions in those areas. Company management is responsible for organising controls in daily operations.

Furthermore, the Standard also requires the implementation of an auditing committee to monitor compliance and effectiveness. Focal points China�s Standard supports the use of information technology and automated monitoring. This also includes the monitoring of electronic information, as has occurred in the United States since 2002, and in particular the archiving of e-mail. Possible remuneration, bonuses and penalties are to be clearly defined beforehand and anchored in company guidelines to facilitate the further integration of the Standard into internal enterprise controls. A second focal point is the role of external consulting firms. The Standard obligates every company listed on a Chinese stock exchange to engage an external consultancy to monitor internal

controls and, just as in the United States, statutory and tax audits must be conducted by two different organisations, namely an auditing firm and the tax authority. Neither the Circular nor the Standard requires an auditor�s report on the effectiveness of internal controls, so this point remains a matter of personal preference. Deadlines and required actions All companies are encouraged to implement C-SOX as soon as possible so that it can take effect in all areas. Starting in the summer of 2009, listed companies are obligated to submit on annual report on the progress and handling of the Standard. As you have already read, the rules will affect very broad operational areas in companies and in light of the experience gained during the introduction of the American equivalent, the implementation period for C-SOX seems extremely optimistic, at least if the goal is an effective application of the new rules. Many experts have already voiced their doubts about the punctual introduction of C-SOX in July 2009. In contrast to the United States, where companies had a lead-time of almost four years, Chinese enterprises have only had about one year between the publication of the Standard and its compliance date. It is absolutely vital that executives are supported in the process by having relevant, high-quality information about their companies. To ease implementation, we recommend a staggered introduction of the new guidelines. It is also advisable for companies to avoid implementing completely new rules and instead build upon those already in place. If companies are interested in proceeding in this manner, then they should become familiar with the subject as soon as possible, both for their own information and to quickly set up special training courses in external account management and IT. Outlook With C-SOX, China has made a clear statement on how it plans to introduce international standards of governance in Chinese companies. It is designed to lower the risk posed to companies by poor or absent governance and thus protect investors and improve the stability of Chinese companies and markets. C-SOX is an important step in introducing international governance standards in Chinese companies and the regulatory authorities are called upon to carefully monitor the implementation of the rules. The companies in questions have been asked to comply with C-SOX regulations by this summer, although unconfirmed information indicates that this date will be pushed back. A delay in introduction, however, should not detract from the importance of these rules: with the Chinese government currently supporting a �go abroad� strategy, C-SOX definitely has full political support. Nevertheless, it will realistically take some time before the new rules can take full effect. On the one hand, experienced foreign companies may have an easier time implementing C-SOX since

18 pwc:china compass | Summer 2009

Reporting and controlling

they are already familiar with similar regulations in other countries. On the other hand, foreign companies will have to deal with Chinese regulators without the benefit of having the state � as a supportive owner � behind them. In any case, PricewaterhouseCoopers is looking forward to support you and your company in meeting full compliance with C-SOX. If you have any questions or would like advice, please feel free to contact us by phone or e-mail.

Contact [email protected] Phone: +86 10 6533-7124

Three guidelines to help with the introduction of the Basic Standard ●

● ●

●

●

●

●

●

●

●

Guidelines for Evaluation and Assessment of Effectiveness of Enterprise Internal Control Implementation Guidelines for Enterprise Internal Control Guidelines for Performing Assurance Engagements in Relation to Assessing Effectiveness of Enterprise Internal Control

Other relevant restrictions for enterprise control in China

Guidance on Internal Accounting Control Basic Standards (six documents covering money stock, procurement and payment, sales and income, expansion projects, foreign investments and notes of surety; MOF, 2001 to 2004) Guidance on Initial Public Offerings of Listed Companies (Article; China Security Regulation Commission, 29 May 2006) SSE Guidelines for Internal Control of Listed Companies (Draft; Shanghai Stock Exchange, June 2006) Central State-owned Enterprises Comprehensive Risk Management Guidance (China�s State-owned Asset Supervision and Administration Commission, June 2006) SZSE Listed Companies Internal Controls Guidance (Draft; Shenzhen Stock Exchange, September 2006) Insurance Risk Management Guidance (China Insurance Regulatory Commission, April 2007) Commercial Banks Internal Control Guidance (China Banking Regulatory Commission, July 2007)

pwc:china compass | Summer 2009 19

Reporting and controlling

20 pwc:china compass | Summer 2009