Embed Size (px)

Citation preview

Implementing Integrated Energy PolicyExpanding of Options for Power*26,July 2006

Integrated Research and Action for DevelopmentNew Delhi

*connectedthinking

Contents

ContextRequirements & Key IssuesOptions for Expanding Power

ContextDefining Energy Security for India

Current Energy Mix, Intensity & SecurityDevelopment & Growth RequirementsRole of Power in Energy Security

“The country is energy Secure when we can supply lifeline energy to all our citizens as well as meet their effective demand for their safe and convenient energy to satisfy various needs at affordable costs at all times with a prescribed confidence level considering shocks and disruptions that can be reasonably expected”

- Expert Committee on Integrated Energy Policy

Slide 4Expanding PowerPricewaterhouseCoopers

July 2006

EDI and components for select countries

0

0.25

0.5

0.75

1

EDI Commercial energyuse per capita

Commercial energyto total energy

ElectrificationIndex

BrazilChinaIndonesiaIndia

India Energy Needs: Energy Development Index

• IEA has developed a simple composite measure of a country’s progress in transition to modern fuels & the degree of maturity of energy end-use

• It has been calculated for 75 developing countries only.

• It is a simple average of the following three sub-indicators

1. Per capita commercial energy consumption.

2. Share of commercial energy in total final energy use.

3. Share of population with access to electricity.

India ranks a poor 53rd and fares very poorly in all three sub-indicators

EDI and components for select countries

Slide 5Expanding PowerPricewaterhouseCoopers

July 2006

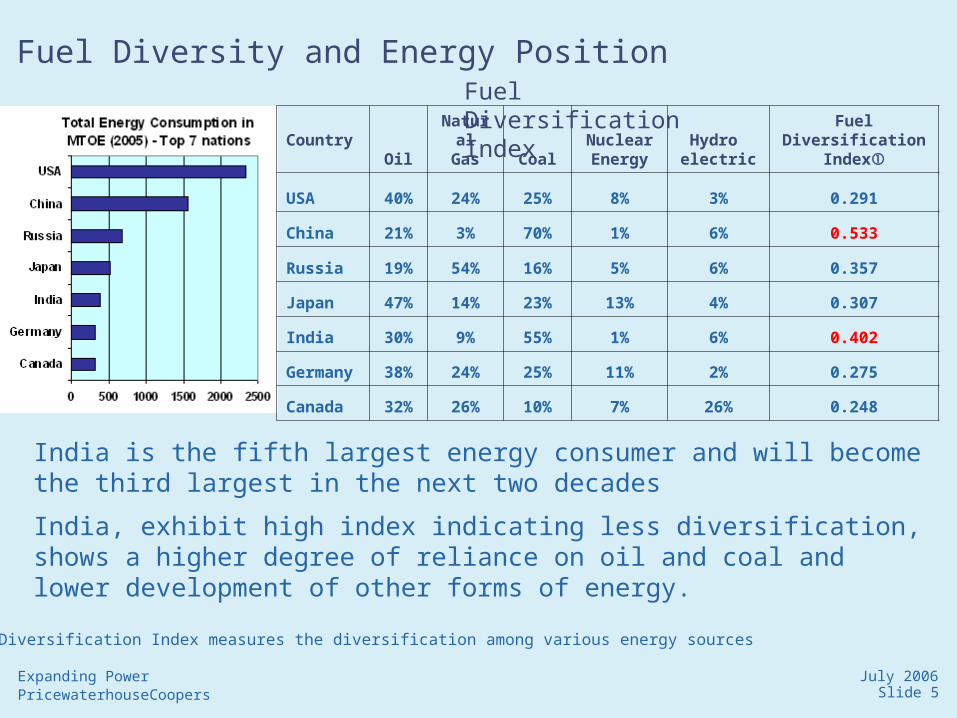

Fuel Diversity and Energy Position

Country OilNatural

Gas CoalNuclear Energy

Hydro electric

Fuel Diversification Index

USA 40% 24% 25% 8% 3% 0.291

China 21% 3% 70% 1% 6% 0.533

Russia 19% 54% 16% 5% 6% 0.357

Japan 47% 14% 23% 13% 4% 0.307

India 30% 9% 55% 1% 6% 0.402

Germany 38% 24% 25% 11% 2% 0.275

Canada 32% 26% 10% 7% 26% 0.248

India is the fifth largest energy consumer and will become the third largest in the next two decades

India, exhibit high index indicating less diversification, shows a higher degree of reliance on oil and coal and lower development of other forms of energy.

Fuel Diversification Index

Fuel Diversification Index measures the diversification among various energy sources

Slide 6Expanding PowerPricewaterhouseCoopers

July 2006

Energy Security Strategy Vulnerability to external shocks

• India, despite the improvement, is three times more energy intense when compared to developed nations making the economic growth energy dependent

•India because of higher import dependence relative to the exports remains vulnerable

•India has a lonely position in a quadrant which is high dependence and vulnerability

•It is imperative that India chalks an energy security strategy to lessen the external shocks and sustain its economic growth

USA, 246

Japan, 112

Brazil, 11

India, 39

China, 52

Canada, 23UK, 30

France, 46Germany, 59

0%

5%

10%

15%

20%

25%

30%

0 0.2 0.4 0.6 0.8 1 1.2

Energy Intensity

En

erg

y Im

po

rts

as %

of

Exp

ort

s

Bubble size indicates Oil Import Bill in 2003 USD

High Risk - Vulnerable & Dependant

Competitive - Low Dependence & Vulnerability

India’s Energy Security- Requirements & Key Issues

Learning from other countriesDiversification of Energy Supply

Energy Security : Equity, efficiency, diversity & sustainability

Slide 8Expanding PowerPricewaterhouseCoopers

July 2006

Need to alter the source of energy for householdsEquity component of energy security

Total Final Consumption: By Source

Gas2%

Electricity9%

Coal9%

Petroleum26%

Combustible & Waste54%

Quantum of Biomass & waste (Fuel wood, straw, charcoal, agricultural residue & cow dung) consumption at 54% is very high.

Dependence on Petroleum is significantly high

The changes in energy mix in residential use will help to address equity issues

There is huge potential to improve overall energy efficiency in industrial and transport sector

The Challenge is related to governance of the large dispersed rural system

Total Final Consumption: By sector

Residential57%

Industry27%

Non energy3%

Transport9%

Other2%

Agriculture2%

Source: IEA

Slide 9Expanding PowerPricewaterhouseCoopers

July 2006

End-Use Oil (2004-05) LPG

Kerosene Naphta Diesel LDO

Furnace Oil LSHS MS

Total Consumed (MMT) 9.9 9.4 14.0 39.7 1.5 9.4 4.4 8.3Domestic 95.4% 98.9% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Transport 0.0% 0.0% 0.0% 56.8% 3.3% 2.7% 0.0% 100.0%Power Gen 0.0% 0.0% 6.9% 7.0% 5.9% 3.3% 28.1% 0.0%Agri 0.0% 0.0% 0.0% 18.9% 2.5% 0.0% 0.0% 0.0%Industrial/Comm 4.6% 1.1% 93.1% 17.4% 88.3% 94.0% 71.9% 0.0%

Source: MoPNG

Improving energy efficiency & reducing oil dependency Opportunity for expanding power

Improved Access to Electricity could significantly reduce Kerosene for domestic use

Appropriate Supply of Power for Irrigation will reduce Diesel in Agriculture

Improved Mass Transportation based on Electricity can arrest rapid growth of the Motor Spirits

Slide 10Expanding PowerPricewaterhouseCoopers

July 2006

Expanding Power in Transportation A case of INDIAN RAILWAYS

• Total energy consumption of transport sector only 1.5% met through electricity and remaining about 98.5 % through petroleum products

• IR consumes about 5.1% of total energy consumed by transport sector (and 1.1% of total energy consumption)

Within Railways energy consumption- 77.5% consumed in the form of diesel (HSD)- 22.5% consumed in the form of electricity

As a proportion to the total energy consumption by the Nation: - 1.8% of total electric energy- 4.4% of total diesel consumption

• Had there been no electrification IR would have been using additional 2.25 million tonnes of diesel oil per annum- This would have raised consumption of oil in Rail sector from 4% to 9%

• If entire IR was electrified there would have been saving of 1.7 million tonnes of diesel oil per annum - This would have reduced the nation’s requirement of diesel oil by 4%

Slide 11Expanding PowerPricewaterhouseCoopers

July 2006

Increase Mass Urban Transport

• Savings in fuel costs is potentially high with introduction of electrified Metro (EIA study for Bangalore estimates savings of Rs.876 cr./yr on a price of Rs.35/ltr of petrol for just 2 & 3 wheelers for just 32 km of metro length)

• In the Delhi Metro project phase-II, the estimated foreign exchange savings due to reduced consumption of 7 Mn lts of Diesel, 31.5 Mn lts of Petrol and 18.6 Mn kg of CNG is Rs. 1.722 Bn, in addition to reduced CO2, travel time and decongestion of roads

• With a fully integrated Metro, Bus and Rail network, only 13% use personal motorised transport to travel into central London

Expected reduction of fuel consumption in 2011

Category of Vehicles

No of vehicles without Metro

No of vehicles with

Metro

Fuel consumption without Metro (litres)

Fuel consumption with Metro (litres)

Fuel Saved (litres)

Two Wheelers 2,394,075 1,676,137 1,795,556 1,257,102 538,454Three Wheelers 157,224 125,829 786,120 629,145 156,975

Total Saving in Fuel, litres per day 695,429

Urban Mass TransportEnhancing energy efficiency & Expanding power

Slide 12Expanding PowerPricewaterhouseCoopers

July 2006

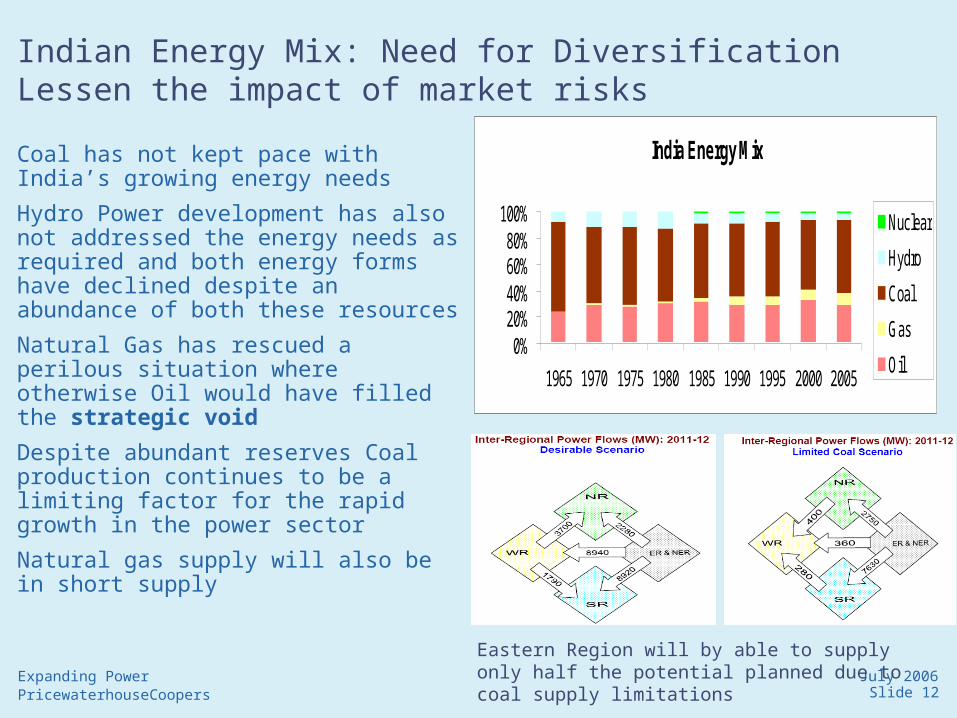

Indian Energy Mix: Need for DiversificationLessen the impact of market risks

Coal has not kept pace with India’s growing energy needs

Hydro Power development has also not addressed the energy needs as required and both energy forms have declined despite an abundance of both these resources

Natural Gas has rescued a perilous situation where otherwise Oil would have filled the strategic void

Despite abundant reserves Coal production continues to be a limiting factor for the rapid growth in the power sector

Natural gas supply will also be in short supply

India Energy Mix

0%20%40%60%80%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005

Nuclear

Hydro

Coal

Gas

Oil

Eastern Region will by able to supply only half the potential planned due to coal supply limitations

Slide 13Expanding PowerPricewaterhouseCoopers

July 2006

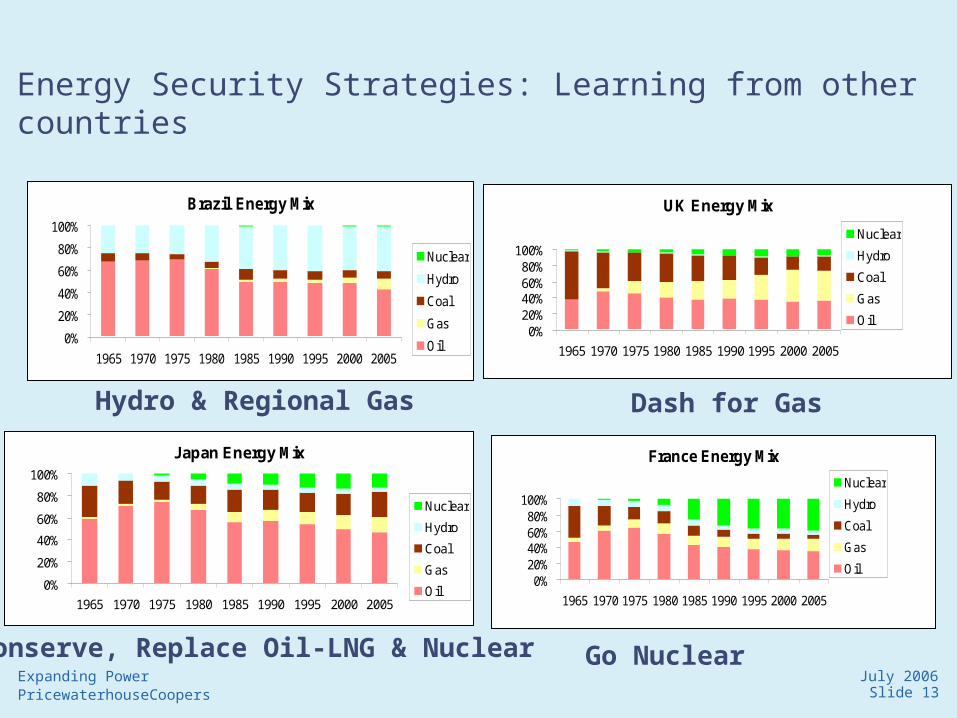

Energy Security Strategies: Learning from other countries

UK Energy Mix

0%20%40%60%80%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005

Nuclear

Hydro

Coal

Gas

Oil

France Energy Mix

0%20%40%60%80%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005

Nuclear

Hydro

Coal

Gas

Oil

Brazil Energy Mix

0%

20%

40%

60%

80%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005

Nuclear

Hydro

Coal

Gas

Oil

Japan Energy Mix

0%

20%

40%

60%

80%

100%

1965 1970 1975 1980 1985 1990 1995 2000 2005

Nuclear

Hydro

Coal

Gas

Oil

Hydro & Regional Gas Dash for Gas

Go Nuclear Conserve, Replace Oil-LNG & Nuclear

Slide 14Expanding PowerPricewaterhouseCoopers

July 2006

Diversification - International lessons

Local/Regional resources play a critical role in meeting the energy needs (E.g. USA– Coal & Oil, China– Coal, Russia– Nat. Gas)

For Developed Economies, reliance on Combustibles, renewables and wastes decreases, almost disappears – India would need to find commercial energy for all

Transportation and Industrial Sector increases its share in sectoral mix vis-à-vis residential sector requiring a multiplier to the energy needs. The next decade will require India to review its transportation growth options in view of the energy needs

Source : IEA 2003

Comparison of Total Final Consumption

Total Final Consumption - by source

0% 20% 40% 60% 80% 100%

India

Indonesia

China

Brazil

Russia

USACombustible& wastesPetroleumProductsElectricity

Coal

Gas

Others

Total Final Consumption: by sector

0% 20% 40% 60% 80% 100%

India

Indonesia

China

Brazil

Russia

USAResidential

Industry sector

TransportationsectorAgriculture

Other sectors

Non-Energy Use

MTOE1571418162885116394

Options for Expanding Power

Expanding of Regional MarketsExpanding Internal Resources

Options for Expanding PowerExpanding Regional Markets

Energy Resources of the RegionsDevelopment of Regional Power MarketsBilateral and Regional Energy Market Development

Slide 17Expanding PowerPricewaterhouseCoopers

July 2006

Why Regional Resources for power?Generation Based on Imported Fuel

• Imported fuel poses significant cost implication for power generation

• Light area shows price at which gas is competitive vis-à-vis coal, while dark area coal is competitive

• Spot prices and freight rates indicate $ 45/ton of delivered cost of coal and gas prices is considered at $6.2 MMBTU – bus-bar cost of generation at these levels is Rs. 3.0/kwh and Rs. 3.39 per kwh respectively

• Current levels are however ruling at their highs and recent long term deals are showing signs of softening prices

Slide 18Expanding PowerPricewaterhouseCoopers

July 2006

Energy Resources of the RegionNepal

Nepal’s topography and hydro sources emanating from snows and glaciers provides scope for hydroelectric development

India has assisted in a limited way Nepal to develop its hydro resources: • HE schemes: Pokhra (1 MW), Trisuli (21

MW), Western Gandak (15 MW) and Devighat (14.1 MW)

• Projects under consideration:- Karnali (10,800 MW)- Pancheshwar (5,600 MW) - Sapta Koshi (3,300 MW)

• NHPC considering Upper Karnali Project (300 MW) as an IPP

• DPR of Burhi Gandaki (600 MW) by WAPCOS under consideration

River Basin

Major (MW)

Small (MW)

Total (MW)

Kosi 18,750 360 22,530

Gandak 17,950 270 20,650

Karnali (Ghaghra)

28,840 3,170 32,010

Mahakali 3,840 320 4,160

Southern Rivers

3,070 1,040 4,110

Total 72,450 10,830 83,280

Total Hydro Potential of Nepal

Improving political situation in Nepal could facilitate development of some of the above potential.

Slide 19Expanding PowerPricewaterhouseCoopers

July 2006

Nepal – Interconnections with India

India Nepal Voltage

Anand Nagar Bhairahawa 33 kV

Itawa Krishna Nagar 33 kV

Nanpara Nepalganj 33 kV

Pallia Dhangadhi 33 kV

Tulsipur Koliabas 11 kV

Lohiahead Mahendranagar 33 kV

Pithoragarh Baitadi 11 kV

Dharchula Jaljibe 11 kV

Dharchula Pipale 11 kV

Gandak East Surajpura 132 kV

Raxaul Birganj 33 kV

Jogbani Biratnagar 11 kV

Thakurganj Bhadrapur 33 kV

Balmikinagar Surajpura 11 kV

Kataiya Duhabi 132 kV

Kataiya Biratnagar 33 kV

Kataiya Rajbiraj 33 kV

Bargania Gaur 11 kV

Sitamarhi Jaleswar 33 kV

Transmission links at 132 kV, 33 kV and 11 kV – Low capacity for energy exchange

Slide 20Expanding PowerPricewaterhouseCoopers

July 2006

Energy Resources of the RegionBhutan

Bhutan’s hydro power potential is assessed to be 30,000 MW, of which 23,500 MW is considered techno-economically feasible.

Developed hydro capacity of 469 MW constitutes ~2% of the potential

The upcoming Tala Project will add 1020 MW of new capacity on commencement (July 06) and increase the capacity threefold

Tala is expected to produce 4865 MU

Hydro Projects to be taken up on Priority basis have been identified

Tala Transmission System Developed by Powerlinks, a JV between Tata Power & PGCIL (51:49) provides a secure infrastructure for Bhutan power to reach more power deficit Northern Indian States. Indirectly it provides also access to western Indian market

3000 MW Capacity, 1200 km length (2384 Ckt Km) BOOT project is integrated into Eastern Transmission system.

Slide 21Expanding PowerPricewaterhouseCoopers

July 2006

Regional Energy Cooperation

There is a need and potential for higher level of energy co-operation within the region to promote energy security

•SAARC Initiatives

•BIMSTEC Initiatives• Strengthen bi-lateral agreements• Allow of more access to Indian market segments• Integration & Strengthening of transmission network• Developing commercial framework for trading: framework

trading agreements, model power purchase agreements

Cross-border energy exchanges through trans-national oil & gas pipelines and transnational grids for transmission of power.

Options for Expanding PowerExpanding Internal Resources

Energy Resources & DemandTransmission InfrastructurePower Trading ArrangementsTechnology Improvements

Slide 23Expanding PowerPricewaterhouseCoopers

July 2006

Energy Resources & Demand

• Energy resources are concentrated in Eastern region

• North East India ranked highest in unexploited hydro potential

• The Northern, Western and Southern are expected face the maximum shortages in energy, while the eastern region is expected remain surplus and export power

Energy & Power Requirement

78037 81492

115705

157107

50700 5450071900

97500

0

50000

100000

150000

FY 01 FY 03 FY 07 FY 12

MU

Peak Requirement (MW) Energy Requirement (MU)

Slide 24Expanding PowerPricewaterhouseCoopers

July 2006

Hydro Power Potential in India

• India itself has significant hydro-power capability undeveloped and has targeted 50 GW for development

• Significant potential for development in N-E and North India.

• These states see hydro power as the main strategy for development of their economies

• South India and Western India has diminishing HEP opportunity. These states are facing energy and peak power shortages

CEA Ranking Study on River Basins

Uttaranchal & HP have focused plans for Hydro power development through involvement of private sector.

State Assessed (MW)

In Operation

Under Construction

Balance (MW)

Arunchal Pradesh

50,328 11 405 49,913

Uttaranchal 18,898 1,610 3,453 13,835

Himachal Pradesh

18,820 3,823 1,926 13,071

Jammu & Kashmir

14,146 1,394 469 12,283

Sikkim 4,286 84 519 3,683

Karnataka 6,602 2,789 222 3,591

Meghalaya 2,394 185 - 2,209

Mizoram 2,196 - 60 2,136

MP/ Chattisgarth

4,485 899 30 1,684

Kerala 3,514 1,800 30 1,684

West Bengal

2,841 301 936 1,605

Manipur 1,784 105 90 1,589

Nagaland 1,574 75 24 1,475

Orissa 2,999 1,838 66 1,096

Total 134,867 14,912 8,231 109,852

Slide 25Expanding PowerPricewaterhouseCoopers

July 2006

Requirements for meeting demand

Year ER-SR

ER-NR

ER-WR

ER-NER

NR-WR

WR-SR NER-NR

Total

2002 600 100 400 1,250 1,000 1,700 0 5,050

2007 3,600 5,000 2,800 1,250 2,100 1,700 0 16,450

2012 3,600 8,500 8,500 2,250 7,600 2,700 4,000 37,150

Transmission system• To facilitate evacuation of power from

eastern region to rest of India• The capacity of the transmission

system needs multi fold increase• JVs similar to Tala system would help

to speed up

Development of Power Market

•Incentives for eastern region states to attract investments in Generation

• Country wide consistent Open Access regime to provide choice and competition

•Third party supplies with credible open access is essential prerequisite as payment security mechanism

•Need to remove both tariff and non-tariff barriers

Slide 26Expanding PowerPricewaterhouseCoopers

July 2006

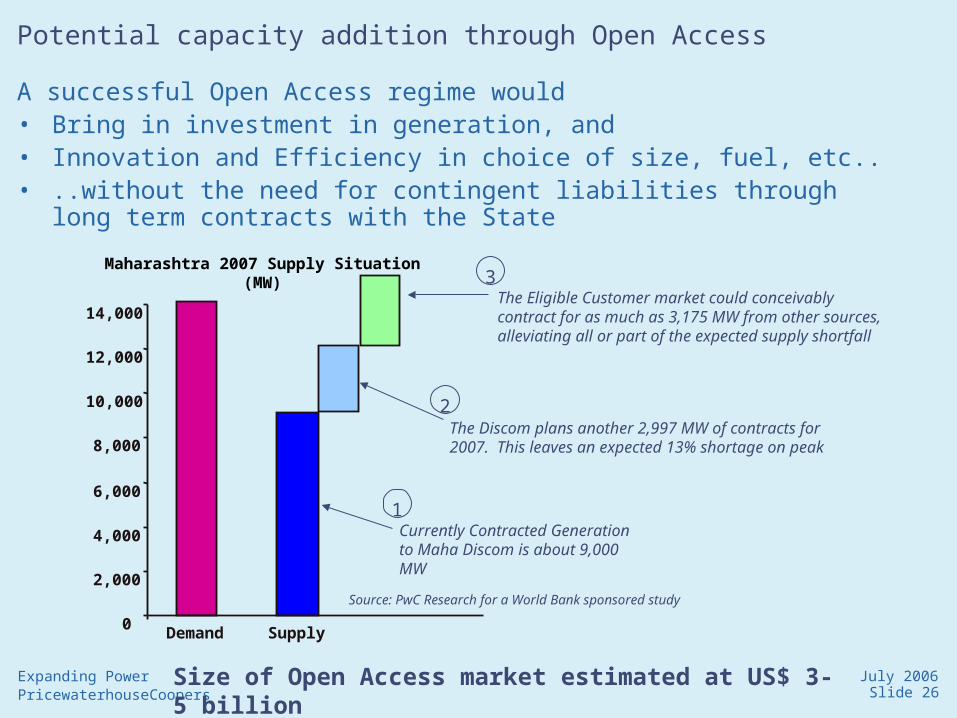

Potential capacity addition through Open Access

A successful Open Access regime would• Bring in investment in generation, and• Innovation and Efficiency in choice of size, fuel, etc..• ..without the need for contingent liabilities through long term contracts

with the State

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Deman

d

Supply

Currently Contracted Generation to Maha Discom is about 9,000 MW

Maharashtra 2007 Supply Situation(MW)

1

The Discom plans another 2,997 MW of contracts for 2007. This leaves an expected 13% shortage on peak

2

The Eligible Customer market could conceivably contract for as much as 3,175 MW from other sources, alleviating all or part of the expected supply shortfall

3

Source: PwC Research for a World Bank sponsored study

Size of Open Access market estimated at US$ 3-5 billion

Slide 27Expanding PowerPricewaterhouseCoopers

July 2006

The change challenge

Nearly 60% of respondents thought the industry needed to have a strong 10-year focus on reducing environmental damage, developing new technologies and improving customer service relationships.

The importance of technology is highlighted by utility companies’ identification of coal, alongside piped gas, as the key fuel in meeting much of future demand growth. Nuclear has grown in favour and finds fifth rank. Hydro-Carbons (LNG and Oil) are low on the rankings of CEOs

The Big Leap: PwC Utilities Survey 2006 - Inside the boardroom

Slide 28Expanding PowerPricewaterhouseCoopers

July 2006

Big Leap – Where would technology Investment yield results

Slide 29Expanding PowerPricewaterhouseCoopers

July 2006

Summary

• Energy Security challenges are Global in nature but we need to develop India specific strategy and action plans

• Oil intensity of our economy has to be reduced in favour of Electricity • Coal & Hydro potential of the nation and the region could help alter the

energy balance• Energy Security Plans have to be developed at the State level progressing

further from Expert Committee Recommendations• Indian supply resources have to be augmented through national

transmission network development & connectivity• Regional Power resources could be developed through appropriate

development of regional power markets and Framework Agreements on trade & energy cooperation

Expanding options for Power

Slide 30Expanding PowerPricewaterhouseCoopers

July 2006

Thank You

![ESIA - Services Architecture Enterprise Services Integrated Architecture [ESIA] Viv Noot PwC](https://img.dokumen.tips/doc/110x75/56649e715503460f94b70588/esia-services-architecture-enterprise-services-integrated-architecture-esia.jpg)