Embed Size (px)

Citation preview

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

June 30, 2010 Actuarial Valuation Report

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

1550 Liberty Ridge Drive Suite 200 Wayne, PA 19087-5572 Tel +1 610 687.5644 Fax +1 610.687.4236 www.milliman.com

March 8, 2011 Mr. Héctor M. Mayol Kauffman Administrator Puerto Rico Government Employees and Judiciary Retirement System Administration 437 Ponce de León Avenue Hato Rey, PR 00918 Dear Mr. Mayol: This report presents the results of the actuarial valuation of the Puerto Rico Government Employees Retirement System (PRGERS) as of June 30, 2010. Section I contains highlights of the valuation including a general discussion and comments on the various schedules included in the report. The subsequent Sections contain schedules summarizing the underlying calculations, asset information, participant data, plan benefits and actuarial assumptions and methods. Purpose The main purposes of this report are: • to provide the Annual Required Contribution and Annual Pension Cost for

the Fiscal Year ending June 30, 2011 based on relevant Statements of the Government Accounting Standards Board (GASB);

• to review the experience under the plan since the previous valuation; • to present information pertaining to the operation of the plan for inclusion

in financial statements; and • to assess the relative funded position of the plan.

The use of this report for purposes other than those stated above may not be appropriate and should be reviewed with Milliman. The report was prepared solely to provide assistance to the Commonwealth of Puerto Rico Government Employees Retirement System for a specific and limited purpose. It is a complex, technical analysis that assumes a high level of knowledge concerning

Mr. Héctor M. Mayol March 8, 2011 Page 2

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

PRGERS’ operations, and uses PRGERS’ data, which Milliman has not audited. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this report. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report. Data Reliance In performing this analysis, we relied on the census data, asset information, and other information (both written and oral) provided by the System. We have not audited or verified the census data, asset information, or other information. To the extent that any of these are inaccurate or incomplete, the results of this valuation may likewise be inaccurate or incomplete. We did not audit the data used in our analysis, but did review it for reasonableness and consistency and have not found material defects in the data. It is possible that material defects in the data would be uncovered by a detailed, systematic review and comparison of the data to search for data values that are questionable or for relationships that are materially inconsistent. Such a review was beyond the scope of our assignment. Future Measurements Future actuarial measurements may differ significantly from the current measurements presented in this report due to factors such as the following: plan experience differing from the actuarial assumptions; future changes in the actuarial assumptions; increases or decreases expected as part of the natural operation of the methodology used for these measurements (such as potential additional contribution requirements due to changes in the plan’s funded status); and, changes in the plan provisions or accounting standards. Due to the limited scope of our assignment, we did not perform an analysis of the potential range of such measurements. Certification We hereby certify that, to the best of our knowledge, this report is complete and accurate and all costs and liabilities were determined in conformance with generally accepted actuarial principles and practices which are consistent with the Actuarial Standards of Practice promulgated by the Actuarial Standards Board and the applicable Guides to Professional Conduct, amplifying Opinions, and supporting recommendations

Mr. Héctor M. Mayol March 8, 2011 Page 3

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

of the American Academy of Actuaries and are based on actuarial assumptions and methods adopted by the System. All of the actuarial assumptions were developed by Milliman in consultation with PRGERS. Actuarial computations presented in this report are for purposes of fulfilling financial accounting requirements under the GASB Statements 25, 27, and 45. The calculations in the enclosed report have been made on a basis consistent with our understanding of the plan provisions described in Section VIII of this report, and of the applicable GASB Statements. Determinations for purposes other than meeting these requirements may be significantly different from the results contained in this report. Accordingly, additional determinations may be needed for other purposes. Qualifications We are members of the Society of Actuaries and meet the qualification standards of the American Academy of Actuaries to render this actuarial opinion. Respectfully submitted, MILLIMAN, INC. By:

Glenn D. Bowen, F.S.A. Member American Academy of Actuaries

Timothy J. Nugent, F.S.A. Member American Academy of Actuaries

Katherine A. Warren, F.S.A. Member American Academy of Actuaries GDB:TJN:KAW:mlm\PRG01-10 g:\corr11\prg\PRGERS_Val_June302010.doc

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

TABLE OF CONTENTS

Page

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

SECTION I - SUMMARY 1 Subsection A - Summary of Principal Results 1 Subsection B - General Discussion 4 Subsection C - Discussion of Supporting Exhibits 12 SECTION II - SYSTEM ASSETS 16 Subsection A - Market Value of Assets 16 Subsection B - Reconciliation of Market Value of Assets 17 Subsection C - Development of Actuarial Value of Assets 17 Subsection D - Estimated Annual Rate of Return 18 Subsection E - Estimated Historical Rates of Return 18 SECTION III - MANAGEMENT INFORMATION 19 Subsection A - Allocation of Actuarial Liability by Pension Law and System Entity 19 Subsection B - Accumulated Member Contributions for Active Members 20 Subsection C - Projected Cash Flows for Basic System Benefits 21 SECTION IV - BASIC SYSTEM BENEFITS INFORMATION 22 Subsection A - Development of Actuarial Accrued Liability 22 Subsection B - Development of Employer Normal Cost 23 Subsection C - Development of Unfunded Actuarial Accrued Liability and Amortization Payment 24 Subsection D - Development of Annual Required Contribution 24 SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION 25 Subsection A - Benefit Obligations 25 Subsection B - Development of Unfunded Actuarial Accrued Liability and Amortization Payment 26 Subsection C - Development of Annual Required Contribution 26 Subsection D - Schedule of Employer Contributions 27 Subsection E - Schedule of Funding Progress 28 Subsection F - Additional Information 29

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

TABLE OF CONTENTS

Page

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

SECTION VI - GASB 45 ACCOUNTING INFORMATION 30 Subsection A - Benefit Obligations 30 Subsection B - Development of Unfunded Actuarial Accrued Liability and Amortization Payment 31 Subsection C - Development of Annual Required Contribution 31 Subsection D - Schedule of Employer Contributions 32 Subsection E - Schedule of Funding Progress 33 Subsection F - Additional Information 34 SECTION VII - CENSUS DATA 35 Subsection A - Summary of Members 35 SECTION VIII - SUMMARY OF PRINCIPAL PLAN PROVISIONS 36 SECTION IX - ACTUARIAL ASSUMPTIONS 67 SECTION X - ACTUARIAL METHODS 75

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

1

A. Summary of Principal Results of June 30, 2010 Actuarial Valuation ($ amounts in thousands)

Basic System

Pension Benefits only

System Administered Pension Benefits only

GASB 25 & 27 Accounting (Basic System and

System Administered Pension Benefits)

GASB 45 Accounting

(Other Postemployment Benefits)

Actuarial Accrued Liability $17,264,874 $2,236,887 $19,501,761 $1,646,148 Actuarial Value of Assets 1,667,358 0 1,667,358 0 Unfunded Actuarial Accrued Liability 15,597,516 2,236,887 17,834,403 1,646,148 Normal Cost (A) Gross Normal Cost 304,187 9,139 313,326 28,722 (B) Expected Member Contributions 302,666 0 302,666 0 (C) Administrative Expenses 33,000 0 33,000 0 (D) Net Employer Normal Cost 34,521 9,139 43,660 28,722 (D) = (A) – (B) + (C) Annual Required Contribution (ARC) (A) Normal Cost 34,521 9,139 43,660 28,722 (B) Amortization of Unfunded Liability 1,314,838 188,565 1,503,403 98,850 (C) ARC 1,349,359 197,704 1,547,063 127,572 (A) + (B) Employer Contributions (estimated) 391,181 151,036 542,217 89,690

A discussion of the benefits included in the respective Actuarial Accrued Liability begins on page 4 of this section. Please see page 19 for an allocation of Actuarial Accrued Liability by Pension Law and System Entity.

(Numbers shown may not add due to rounding.)

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

2

June 30, 2009 June 30, 2010 Valuation Valuation

GASB 25 & 27 Accounting ($ amounts in thousands) Actuarial Accrued Liability $18,943,586 $19,501,761 Actuarial Value of Assets 1,851,223 1,667,358 Unfunded Actuarial Accrued Liability 17,092,363 17,834,403 Employer Normal Cost 35,357 43,660 Annual Required Contribution for upcoming fiscal year 1,459,774 1,547,063

GASB 45 Accounting ($ amounts in thousands) Actuarial Accrued Liability $1,633,159 $1,646,148 Actuarial Value of Assets 0 0 Unfunded Actuarial Accrued Liability 1,633,159 1,646,148 Employer Normal Cost 32,187 28,722 Annual Required Contribution for upcoming fiscal year 128,294 127,572 A discussion of the benefits included in the respective Actuarial Accrued Liability begins on page 4 of this section.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

3

June 30, 2009 June 30, 2010 Valuation Valuation

Participant Data Active Members Number 160,053 140,642 Average Salary $26,820 $27,149 Total Annual Salary $4,292,552,000 $3,818,332,000 Retirees Number 75,697 77,528 Average Monthly Basic System Benefit $1,011 $1,037 Average Monthly System Administered Benefit $77 $74 Disabled Members Number 17,073 16,839 Average Monthly Basic System Benefit $427 $431 Average Monthly System Administered Benefit $116 $115 Beneficiaries Number 12,201 12,171 Average Monthly Basic System Benefit $267 $275 Average Monthly System Administered Benefit $21 $20 Basic System Benefit and System Administered Benefit amounts shown above are for pension benefits, including minimum benefits and COLAs. Special Law "bonus" benefits are not reflected.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

4

B. General Discussion

Basic System Benefits As summarized in Section VIII, the Puerto Rico Government Employees Retirement System (PRGERS) provides benefits to Act 447 and Act 1 members, or their beneficiaries, upon:

• Retirement • Disability • Vested withdrawal • Death • Nonvested withdrawal (return of contributions) • Christmas bonus ($200)

These benefits will be referred to as the “Basic System Benefits” throughout this report. Basic System Benefits for members of System 2000 consist of the accumulated member contribution account. The contributions required by statute to fund the basic system benefits listed above total 17.55% of payroll, comprising 8.275% from members and 9.275% from employers. These contribution rates are not actuarially determined. Annuity benefits are subject to a $400 monthly minimum. The amount in excess of $200 and less than $300 is a System Administered Benefit (see below) for all employees. The amount in excess of $300 and less than $400 is a System Administered Benefit for Public Corporation and County employees. System Administered Benefits Also summarized in Section VIII are benefits granted under a series of special laws that are administered by PRGERS, including:

• Additional minimum pension benefits • Additional minimum death benefits • Ad-hoc cost-of-living adjustments (COLAs) provided in past years • Additional benefits due to death or disability for reasons specified in Act 127 • Medical insurance plan contribution • Summer bonus • Medication bonus • Christmas bonus ($400)

System 2000 participants do not receive any System Administered Benefits other than those available under Act 127.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

5

These benefits are funded on a pay-as-you-go basis from the General Fund or specific entity of the Commonwealth of Puerto Rico and will be referred to as “System Administered Benefits” throughout this report. These benefits are not an obligation of the PRGERS assets. Other Benefits The disability benefits provided by a private insurance long term disability program to active members of System 2000 who voluntarily elect to enroll are not considered to be a Basic System Benefit nor a System Administered Benefit for purposes of the actuarial valuation since these benefits are financed solely by employees. As a result, these benefits are not reflected in this report. (Please see Management’s Discussion and Analysis on page 8 of the System’s June 30, 2009 Basic Financial Statements.) Moreover, this report does not address the guarantee insurance reserve for life insurance on loans to plan members. (Please see Notes to Basic Financial Statements on page 38 and Statements of Plan Net Assets on page 12 of the System’s June 30, 2009 Basic Financial Statements.) GASB Accounting Information Basic System Benefits and System Administered Benefits have been valued under Governmental Accounting Standards Board Statement No. 25, “Financial Reporting for Defined Benefit Pension Plans and Note Disclosures for Defined Contribution Plans” (GASB 25) and Statement No. 27, “Accounting for Pensions by State and Local Governmental Employers” (GASB 27). The Medical Insurance Plan Contribution has been valued under Governmental Accounting Standards Board Statement No. 45, “Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions” (GASB 45). Accounting results under GASB 25, 27, and 45 are presented in Sections IV, V and VI of this report and are discussed below. Basic System Benefits Information alone We have performed a June 30, 2010 actuarial valuation of the Basic System Benefits alone and have prepared accounting results for them based on GASB 25 and 27 rules.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

6

The FY 2010-11 Annual Required Contribution (ARC) for the Basic System Benefits only based on GASB 25 and 27 rules would be $1.349 billion. The ARC represents the portion of the cost of PRGERS’ Basic System Benefits that employers should pay in order for PRGERS to be actuarially funded in accordance with GASB’s required minimum parameters. The actual employer contributions are based on the statutory funding requirement, which is 9.275% of payroll and which is not actuarially determined. Contributions for prior early retirement incentive programs are also included. Employer contributions for Basic System Benefits are estimated to be $391.2 million for FY 2010-11, which is less than the ARC by $958 million. Note the above ARC has been reduced to reflect the fact that active members contribute 8.275% of pay to the system. The ARC represents the additional contributions required from employers. As shown in Subsection C of Section IV, PRGERS has Unfunded Actuarial Accrued Liabilities (UAAL) of $15.6 billion on behalf of Basic System Benefits, which should be amortized over a period not to exceed 30 years in accordance with GASB 25 and 27 rules. Based on the current statutory member and employer funding requirements, the UAAL is expected to grow indefinitely into the future instead of being amortized. Effectively, this means that the statutory member and employer contributions to PRGERS are not adequate to fund PRGERS’ Basic System Benefits. Instead, PRGERS is being rapidly disfunded. As a result, the future scheduled contributions equal to the statutory funding requirement will not be adequate to accumulate sufficient assets to make future benefit payments when due. GASB 25 and 27 Accounting Information for Basic plus System Administered Benefits We have performed a June 30, 2010 actuarial valuation of the Basic System Benefits and the System Administered Benefits (excluding the Medical Insurance Plan Contribution, which will be discussed separately under GASB 45 below) and have prepared accounting results under GASB 25 for the financial statements of the System and under GASB 27 for the Commonwealth of Puerto Rico’s financial statements. The System Administered Benefits are financed on a pay-as-you-go basis from the General Fund of the Commonwealth of Puerto Rico and contributions from municipalities and public corporations.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

7

The FY 2010-11 employer ARC under GASB 25 and 27 for these combined benefits is $1.547 billion. The estimated FY 2010-11 combined employer contributions are only $542.2 million, which is $1.005 billion less than the ARC. This includes the Basic System Benefits and the System Administered Benefits (excluding the Medical Insurance Plan Contribution). As shown in Subsection B of Section V, the Unfunded Actuarial Accrued Liability for these combined benefits is $17.8 billion. As noted above, future scheduled contributions equal to the statutory funding requirements will not be adequate to accumulate sufficient assets to make future benefit payments when due. GASB 45 Accounting Information We have performed a June 30, 2010 actuarial valuation of the Medical Insurance Plan Contribution and have prepared accounting results for the Commonwealth of Puerto Rico’s financial statements under GASB 45. (Note that the Medication Bonus has been included in the GASB 25 and 27 results as a Pension Benefit because members can receive the bonus without submitting documentation to substantiate medication expenses.) The FY 2010-11 ARC for the Medical Insurance Plan Contribution under GASB 45 is $127.6 million. There are no member or employer contributions on behalf of the Medical Insurance Plan Contribution. This benefit is financed on a pay-as-you-go basis from the General Fund of the Commonwealth of Puerto Rico. Since this is an Other Postemployment Benefit that is not funded in advance, the ARC for this benefit has been calculated based on an assumed investment return rate of 4.0%, instead of the 7.5% rate used for the Pension Benefits. As shown in Subsection B of Section VI, the Unfunded Actuarial Accrued Liability on a GASB 45 basis for this benefit is $1.6 billion. Allocation of Actuarial Accrued Liability Subsection A of Section III shows the Actuarial Accrued Liability as of June 30, 2010 by Pension Law (Act 447, Act 1, and System 2000) within each System Entity (Government, Public Corporation, and County).

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

8

Gain/Loss Analysis Our analysis of System experience from June 30, 2009 to June 30, 2010 resulted in a liability gain of $0.2 billion for Basic System Benefits (e.g. – the June 30, 2009 liability of $16.7 billion was expected to increase to $17.1 billion as of June 30, 2010, and instead increased to $16.9 billion prior to the increase in the loading for deferred vested participants). Major sources of gains and losses are as follows:

1. $40 million loss on new entrants 2. $80 million loss on roughly 860 “pop-up” retirees who were not in the June 30,

2009 census data 3. $20 million loss on retiree and beneficiary mortality and other data changes 4. $200 million loss on roughly 2,700 active members who retired during the one-

year period; a large portion of this loss is due to members retiring with benefits larger than expected

5. $100 million gain on continuing active members due to salary and other data changes

6. $200 million gain on active members exiting the System; a portion of this gain is due to the impact of Law 7 (a large reduction in force among government employees, primarily from System 2000)

7. $240 million gain from all other sources, including data changes Further discussion is warranted on Items 2 and 4. For Item 2, the entire $80 million is not a loss to the extent that these new retirees were included in the deferred vested liability on June 30, 2009. However, we cannot determine what portion of the 860 retirees emerged from deferred vested status since deferred vested census data is not available and the deferred vested liability is developed by placing a loading assumption on the Act 447 and Act 1 liabilities to account for deferred vested members. (Please see the discussion of assumption changes later in this section for further discussion.) For Item 4, possible explanations for losses attributable to individual members include purchases of service (which are offset to some extent by the member’s purchase price), retirement incentives, and data clean-up that occurred during the benefit calculation process when the member retired. Many members experienced significant actuarial

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

9

losses from the previous valuation due to the retirement benefit in the 2010 census data far exceeding what would have expected based on the service and salary amounts reported in the 2009 census data. The information provided in the census data does not allow us to determine which if any of the above-mentioned explanations may apply to a particular member. Changes in Actuarial Assumptions since Prior Valuation The loading on the actuarial accrued liabilities for Act 447 and Act 1 members to approximate the value of the liability on behalf of deferred vested participants has been increased from 3% to 5%. After this change the resulting actuarial accrued liability for Basic System Benefits on behalf of vested terminated members is $790 million. This increase is based on the liability for “pop-up” retirees in this valuation and the 2009 valuation. Over the three-year period (2007 to 2010), about $100 million in liability has been added each year for “pop-up” retirees – most of which may be retiring deferred vested participants (see discussion above). The increase is also based on the number of Act 447 members who were reported as active in the 2009 valuation and did not appear in the census data for the 2010 valuation because they are no longer active employees but they have not yet applied for retirement benefits. FY 2009-2010 Employer Contribution In the June 30, 2009 valuation, the expected employer contribution under GASB 25 accounting for the fiscal year ending June 30, 2010 was $590.7 million. This amount assumed contributions of 9.275% of expected payroll for Basic System Benefits ($398.1 million), $149.9 million for Special Law pension benefits, and $42.7 million for early retirement incentives. The actual employer contribution under GASB 25 accounting for the 2009-2010 fiscal year was $534.3 million. This amount equals $381.2 million for the 9.275% payroll contribution for Basic System Benefits, $149.6 for Special Law pension benefits, and $3.4 million for early retirement incentives. The actual contribution of $534.3 million is lower than the expected $590.7 million because the payroll contribution was less than anticipated due to the Law 7 reductions in the active membership and the actual early retirement incentive contributions were only $3.4 million versus the $42.7 million expected.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

10

Census Data Overview and Potential Additional Liability During the valuation process, significant effort was made to reconcile the current 2010 census data with the prior 2009 census data and to examine the individual data components. The examination of individual data components year over year is simpler for members who do not change employment status between valuations. For members whose status changes, different data components are reported. For instance, members who retire between valuations have service and salary reported in the prior census data and have a retirement benefit reported in the current data. Based on the census data reported, the System experienced a $200 million liability loss on behalf of members who retired between June 30, 2009 and June 30, 2010. This loss is approximately 1% of the total Basic System Benefit liability. We will provide PRGERS with a file that will allow PRGERS to examine both the 2009 (active) and 2010 (retired) data for the individual members who retired between valuations. While the $200 million loss that occurred in 2009-10 was significantly less than the $800 million loss over the preceding 2 years, as discussed above, we cannot determine the validity of the census data for any individual member of PRGERS. Therefore, we cannot determine if there may be additional data clean-up that will occur in future years as more of the current active members retire. For example, if there exists another potential $1 billion liability due to data clean-up that may occur in the future but that is not included in the current liability, reflecting such a potential liability would increase the unfunded liability for Basic System Benefits reported in this valuation from $17.3 billion to $18.3 billion, would increase the ARC from $1.35 billion to $1.43 billion, and the additional unanticipated cash flows would hasten the exhaustion of the System assets that is discussed in the following section and illustrated on Exhibit C in Section III. Cash Flow Projection for Basic System Benefits PRGERS is a mature retirement system with a significant retiree population. Based on the current statutory funding requirements, the annual benefit payments and administrative expenses paid by the system are significantly larger than the member and employer contributions made to the system. Thus investment income must be used to cover this negative cash flow. As a result, system assets can be expected to decline

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

11

as negative cash flow (contributions less benefit payments) exceeds expected investment income. PRGERS’ liabilities for the Basic System Benefits will continue to increase significantly over time as Act 447 and Act 1 employees approach retirement. Thus the funded status can also be expected to decline, based on the actuarial assumptions used to prepare this actuarial valuation. The table shown in Subsection C of Section III illustrates the expected negative net cash flows over the next 10 years. Annual payroll growth of 2.5% is assumed, as future members are assumed to replace current members who terminate or retire. (Note, we did not attempt to include in the expected benefit payments any benefit payments attributable to new members in preparing this table. Members who join PRGERS in the future will generate some cash outflow during the next 10 years due to refunds of their contributions, death and disability benefits, and immediate annuities due to service purchases, etc. We expect that these amounts will be relatively modest and they have not been included in the results shown. Doing so would increase the expected negative net cash flow.) We recommend that the statutory funding requirements be significantly increased in excess of the employer contribution rate of 9.275% in light of:

• the expected negative net cash flows which are expected to exhaust net System assets in FY 2013-2014 (assuming the investment return assumption of 7.5% is met);

• the expected negative net cash flows which are expected to exhaust gross System assets in FY 2018-2019 (assuming the investment return assumption of 7.5% is met)

• the forecast decrease in funded status; • the market value of assets as of June 30, 2010 which is significantly less

than the Accumulated Member Contributions for active members as of June 30, 2010; and,

• the Annual Required Contribution based on GASB 25 and 27. Note that in the period from FY 2013-2014 to FY 2018-2019, benefits are expected to be paid with pension obligation bond proceeds, i.e. – borrowed money. Once gross assets are exhausted there would be no System assets remaining to pay pension benefits to members nor to pay debt service to bondholders.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

12

C. Discussion of Supporting Exhibits System Assets Section II summarizes the plan assets taken into account in the preparation of the GASB 27 Employer Accounting results for PRGERS. Subsection A summarizes the Market Value of Assets as of June 30, 2010, including the additional amounts due to the contribution receivables, if any. Subsection B summarizes the reconciliation of the Market Value of Assets from June 30, 2009 to June 30, 2010. Subsection C summarizes the development of the Actuarial Value of Assets as of June 30, 2010. The Actuarial Value of Assets is equal to the Market Value of Assets. Subsection D develops an estimated rate of return on plan assets for the previous plan year. The estimated rate of return from June 30, 2009 to June 30, 2010 was 27.87% on the Market Value of Assets. Subsection E summarizes the historical estimated rate of return on plan assets on a market value basis. The asset information used for the valuation was taken from financial statements provided by PRGERS as of June 30, 2010. Management Information Section III presents additional information that has been derived from the valuation process. Subsection A shows the allocation of Actuarial Accrued Liability as of June 30, 2010 for Basic System Benefits by Pension Law (Act 447, Act 1, and System 2000) within each System Entity (Government, Public Corporation, and County). Subsection B shows the allocation of the Accumulated Member Contributions with interest for active members as of June 30, 2010 by Pension Law (Act 447, Act 1, and

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

13

System 2000) within each System Entity (Government, Public Corporation, and County). Subsection C shows a projected cash flow for the current fiscal year and the next ten fiscal years for Basic System Benefits and is illustrative of the expected future decline in funded status. Please see Subsection B of Section I for a description of this projection. Basic System Benefits Information Section IV summarizes the Actuarial Accrued Liability and the development of the Annual Required Contribution for just the Basic System Benefits under GASB 25 and 27 for the fiscal year ending June 30, 2011 (please see Subsection B of Section I for a description of the benefits included in this valuation). Subsection A summarizes the development of the Actuarial Accrued Liability as of June 30, 2010. Subsection B summarizes the development of the Employer Normal Cost. The Employer Normal Cost is the total normal cost under the Projected Unit Credit Actuarial Cost Method adjusted for interest to mid-year, increased by expected administrative expenses paid from the fund, and reduced by expected member contributions. Subsection C summarizes the development of the amortization payment of the Unfunded Actuarial Accrued liability. The amortization period used to calculate the ARC is 30 years from June 30, 2007, with level annual payments. 27 years remain as of June 30, 2010. Subsection D summarizes the development of the Annual Required Contribution (ARC). The ARC is the sum of the employer normal cost and the amortization payments, adjusted to mid-year to reflect that payments are made throughout the year. GASB 25 and 27 Accounting Information Section V summarizes the Actuarial Accrued Liability and the development of the Annual Required Contribution and Annual Pension Cost under GASB 25 and 27 for the fiscal year ending June 30, 2011 (please see Subsection B of Section I for a description of the benefits included in these valuation results). Results are shown in total for GASB

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

14

25 and 27, with the Actuarial Accrued Liability and Employer Normal Cost presented for the underlying Basic System Benefits and for the underlying System Administered Benefits that are included in this valuation. Subsection A summarizes the development of the Actuarial Accrued Liability as of June 30, 2010 and Employer Normal Cost as of December 31, 2010. Subsection B summarizes the development of the amortization payment of the Unfunded Actuarial Accrued liability. The amortization period used to calculate the ARC is 30 years from June 30, 2007 with level annual payments each year. 27 years remain as of June 30, 2010. Subsection C summarizes the development of the Annual Required Contribution (ARC). The ARC is the sum of the employer normal cost and the amortization payments, adjusted to mid-year to reflect that payments are made throughout the year. Subsection D shows a seven-year history of the ARC and the percentage contributed. This schedule is required by GASB Statements No. 25 and 27. The FY 2010-11 contribution percentage assumes that employer contributions for Basic System Benefits will remain at the statutory level of 9.275% of payroll and that employer contributions for the applicable System Administered Benefits will be the anticipated pay-as-you-go payments as reported by the System. The amounts shown for the fiscal year ending June 30, 2007 and earlier are from the audited financial statements for the System and for the Commonwealth of Puerto Rico. As indicated on the exhibit, we restated the ARC for FY 2005-06 and FY2006-07 based on information available in the June 30, 2005 valuation report prepared by Buck Consultants. Based on our understanding of prior valuations, the ARC for 2004-05 does not include the liability for any System Administered Benefits, and the Actual Employer Contributions for FY 2004-05 does not include contributions for the System Administered Benefits. Subsection E shows a six-year history of the funding progress of the plan. This schedule is required by GASB Statements No. 25 and 27. The amounts shown for the fiscal year ending June 30, 2007 and earlier are from the audited financial statements for the System (adjusted as discussed in the paragraph above). Schedule F summarizes information used to determine the Annual Required Contribution for the fiscal year ending June 30, 2011.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION I – SUMMARY

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

15

GASB 45 Accounting Information Section VI summarizes the Actuarial Accrued Liability and the development of the Annual Required Contribution for the fiscal year ending June 30, 2011 for the Medical Insurance Plan Contribution. Subsection A summarizes the development of the Actuarial Accrued Liability as of June 30, 2010 and Employer Normal Cost as of December 31, 2010. Subsection B summarizes the development of the amortization payment of the Unfunded Actuarial Accrued liability. The amortization period used to calculate the ARC is 30 years from June 30, 2007 with level annual payments each year. 27 years remain as of June 30, 2010. Subsection C summarizes the development of the Annual Required Contribution (ARC). The ARC is the sum of the employer normal cost and the amortization payments, adjusted to mid-year to reflect that payments are made throughout the year. Census Data Section VII summarizes the census data provided by the System and utilized in the preparation of the actuarial valuation. Subsection A provides a profile of active and inactive participants, summarized by pension law. Special data adjustments are discussed in Section IX. Summary of Principal Plan Provisions Section VIII summarizes the principal plan provisions as of the valuation date and denotes any changes from the previous valuation. Actuarial Assumptions and Methods Sections IX and X summarize the actuarial assumptions and methods that were utilized in the preparation of this actuarial valuation and denote any changes from the previous valuation.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

A. Market Value of Assets as of June 30, 2010

1. Assets Cash $ 1,129,860,000 Bonds 563,454,000 Stocks 1,492,386,000 Private Equity Investments 55,307,000 Total Loans to Plan Members 1,226,155,000 Accounts Receivable 326,178,000 Capital Assets 8,964,000 Other Assets 7,224,000 Prepaid Bond Cost 33,267,000 Total $ 4,842,795,000 2. Total Liabilities Bonds Payable $ 2,981,775,000 Other Liabilities 193,662,000 Total $ 3,175,437,000

3. Market Value of Assets as of June 30, 2010: (1) - (2) $ 1,667,358,000

16

SECTION II - SYSTEM ASSETS

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intendto benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

B. Reconciliation of Market Value of Assets from June 30, 2009 to June 30, 2010

1. Market Value of Assets as of June 30, 2009 $ 1,851,223,000

2. Additions a. Contributions Employer Contributions $ 381,243,000 Member Contributions 345,265,000 Early Retirement Programs 3,399,000 Appropriations for Special Laws 188,843,000 Total Contributions $ 918,750,000

b. Investment Income Interest Income $ 179,585,000 Dividend Income 10,663,000 Net Appreciation of Investments 216,011,000 Other Income 31,783,000 Investment Related Expenses (7,649,000) Net Investment Income $ 430,393,000

Total Additions $ 1,349,143,000

3. Decreases Refund of Contributions $ 45,146,000 Annuities and Death Benefits 1,060,933,000 Special Law Benefits 188,843,000 Administrative Expenses 33,063,000 Other Expenses 16,968,000 Cost of Bonds 188,055,000 Total $ 1,533,008,000

4. Net Increase (Decrease) in Market Value of Assets $ (183,865,000)

5. Market Value of Assets as of June 30, 2010 $ 1,667,358,000

C. Development of Actuarial Value of Assets as of June 30, 2010

17

SECTION II - SYSTEM ASSETS

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

The Actuarial Value of Assets as of June 30, 2010 is equal to the Market Value of Assets as of June 30, 2010 of $1,667,358,000.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

D. Estimated Annual Rate of Return for year ending June 30, 2010Market Value

1. Value of Assets as of June 30, 2009 $ 1,851,223,000

2. Total Contributions 918,750,000

3. Benefit Payments and Expenses 1,533,008,000

4. Value of Assets as of June 30, 2010 1,667,358,000

5. Non-Investment Increment: (2) - (3) (614,258,000)

6. Investment Increment: (4) - (1) - (5) 430,393,000

7. Time Weighted Value: (1) +.5 * (5) 1,544,094,000

8. Estimated Annual Rate of Return: (6) / (7) 27.87%

E. Estimated Historical Rates of Return

Plan Year Ending Market Value

June 30, 2010 27.87%June 30, 2009 -13.23%June 30, 2008 -2.26%June 30, 2007 18.23%June 30, 2006 13.88%

5-year Compounded Annual Return 7.86%

Prior year returns were calculated by Milliman using the methodology in Section D above, based on asset amounts and cash flows shown in PRGERS audited financial statements.

18

SECTION II - SYSTEM ASSETS

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

A. Allocation of Actuarial Accrued Liability by Pension Law and System Entity

Basic SystemBasic System and System

System Administered Administered GASB 45Benefits Benefits Benefits Benefits

GovernmentAct 447 9,187,746,000 1,155,769,000 10,343,515,000 905,420,000Act 1 1,458,374,000 175,938,000 1,634,312,000 183,432,000System 2000 317,717,000 160,453,000 478,170,000 3,582,000

10,963,838,000 1,492,160,000 12,455,998,000 1,092,434,000

CorporationAct 447 4,181,349,000 472,657,000 4,654,006,000 280,847,000Act 1 361,977,000 15,312,000 377,289,000 35,885,000System 2000 92,180,000 341,000 92,521,000 4,000

4,635,507,000 488,310,000 5,123,817,000 316,736,000

CountiesAct 447 1,200,583,000 209,543,000 1,410,126,000 175,771,000Act 1 349,856,000 33,693,000 383,549,000 60,836,000System 2000 115,090,000 13,181,000 128,271,000 371,000

1,665,530,000 256,416,000 1,921,946,000 236,978,000

TotalAct 447 14,569,678,000 1,837,968,000 16,407,646,000 1,362,038,000Act 1 2,170,208,000 224,943,000 2,395,151,000 280,153,000System 2000 524,988,000 173,976,000 698,964,000 3,957,000

17,264,874,000 2,236,887,000 19,501,761,000 1,646,148,000

(Numbers shown may not add due to rounding.)

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume noduty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this reportbe aided by its own actuary or qualified professional when reviewing the Milliman report.

19

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION III - MANAGEMENT INFORMATION

B. Accumulated Member Contributions for Active Members as of June 30, 2010

Contribution Account Balances

Government Act 447 803,561,000 Act 1 926,244,000 System 2000 310,792,000

2,040,597,000

Corporation Act 447 296,078,000 Act 1 235,618,000 System 2000 88,537,000

620,233,000

Counties Act 447 117,855,000 Act 1 194,738,000 System 2000 111,429,000

424,022,000

Total Act 447 1,217,494,000 Act 1 1,356,600,000 System 2000 510,758,000

3,084,852,000

Market Value of Assets as of June 30, 2010 1,667,358,000

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

20

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION III - MANAGEMENT INFORMATION

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION III - MANAGEMENT INFORMATION

C. Projected Cash Flows for Basic System Benefits

(Amounts in Millions)

EstimatedEstimated Benefit Pension Estimated Estimated

Member and Payments and Obligation Net GrossPlan Year Estimated Employer Administrative Bond Net Plan Assets Plan Assets

Ending Payroll Contributions Expenses Debt Service Cash Flow at Year-End at Year-End

06/30/2011 3,818 670 1,252 167 (749) 1,189 4,43006/30/2012 3,913 687 1,261 167 (741) 683 3,99406/30/2013 4,011 704 1,278 167 (741) 139 3,52606/30/2014 4,111 721 1,298 167 (744) (449) 3,02006/30/2015 4,214 740 1,328 167 (755) (1,092) 2,46406/30/2016 4,319 758 1,359 167 (768) (1,797) 1,85306/30/2017 4,427 777 1,395 167 (785) (2,573) 1,17806/30/2018 4,538 796 1,434 167 (805) (3,427) 43306/30/2019 4,651 816 1,478 167 (829) (4,370) (394)06/30/2020 4,767 837 1,524 167 (854) (5,410) (1,308)06/30/2021 4,886 857 1,570 167 (880) (6,556) (2,318)

Notes:- Estimated Net and Gross Plan Assets at Year-End assumes that the investment return assumption of 7.5% is met.- Estimated Payroll is assumed to grow 2.5% annually.- Member and Employer Contributions were estimated to be 17.55% of Estimated Payroll for plan year ending 06/30/2011 and each year thereafter.- The Estimated Benefit Payments do not include amounts expected to be made to future participants, such as: - refund of contributions to terminated nonvested participants, - disability benefits, - death benefits, - retirement benefits due to service purchase, and thus are slightly understated.- Administrative Expenses are assumed to grow 2.5% annually.- Contributions on behalf of and benefit payments to members of System 2000 are included in the table above

21

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability toother parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary orqualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION IV - BASIC SYSTEM BENEFITS INFORMATION

A. Development of Actuarial Accrued Liability as of June 30, 2010

1. Projected Benefits Payable to Retirees and Beneficiaries Retirees $ 9,445,627,000 Disabled Members 731,003,000 Beneficiaries 324,131,000 Total $ 10,500,761,000

2. Projected Benefits for Vested Terminated Members 789,418,000

3. Actuarial Accrued Liability for Active Members 5,974,695,000

4. Total Actuarial Accrued Liability: (1) + (2) + (3) $ 17,264,874,000

22

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

The above liabilities are for Basic System Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION IV - BASIC SYSTEM BENEFITS INFORMATION

B. Development of Employer Normal Cost Payable as of December 31, 2010

1. Total Normal Cost as of June 30, 2010 $ 293,384,000

2. Expected Member Contributions $ 302,666,000

3. Load for Administrative Expenses: $ 33,000,000

4. Total Employer Normal Cost as of December 31, 2010: (1) * ( 1.075 ^ 0.5 ) - (2) + (3) $ 34,521,000

23

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intendto benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualifiedprofessional when reviewing the Milliman report.

The above liabilities are for Basic System Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION IV - BASIC SYSTEM BENEFITS INFORMATION

C. Development of Unfunded Actuarial Accrued Liability and Amortization Payment Payable as of December 31, 2010

1. Actuarial Accrued Liability as of June 30, 2010 $ 17,264,874,000

2. Actuarial Value of Assets as of June 30, 2010 $ 1,667,358,000

3. Unfunded Actuarial Accrued Liability as of June 30, 2010: (1) - (2) $ 15,597,516,000

4. Amortization Period in years 27

5. Amortization Factor at beginning of year 12.2995

6. Amortization Amount Payable as of December 31, 2010: [ (3) / (5) ] * ( 1.075 ^ 0.5 ) $ 1,314,838,000

D. Development of Annual Required Contribution

1. Total Employer Normal Cost as of December 31, 2010 $ 34,521,000

2. Amortization Payment as of December 31, 2010 $ 1,314,838,000

3. Annual Required Contribution*: (1) + (2) $ 1,349,359,000

* Assumes payments made throughout the year.

24

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefitand assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that anythird party recipient of this report be aided by its own actuary or qualified professional when reviewing the Millimanreport.

The above liabilities are for Basic System Benefits. See Section I for more information.

A. Benefit ObligationsBasic System

System AdministeredBenefits Benefits Total

1. Projected Benefits Payable to Retirees and Beneficiairies: Retirees $ 9,445,627,000 $ 1,168,652,000 $ 10,614,279,000 Disabled Members 731,003,000 326,294,000 1,057,297,000 Beneficiaries 324,131,000 75,856,000 399,987,000 Total $ 10,500,761,000 $ 1,570,802,000 $ 12,071,563,000

2. Projected Benefits Payable to Vested Terminated Members: $ 789,418,000 $ 98,160,000 $ 887,578,000

3. Actuarial Accrued Liability for Active Members $ 5,974,695,000 $ 567,925,000 $ 6,542,620,000

4. Actuarial Accrued Liability as of June 30, 2010: $ 17,264,874,000 $ 2,236,887,000 $ 19,501,761,000 (1) + (2) + (3)

5. Gross Normal Cost as of December 31, 2010: $ 304,187,000 $ 9,139,000 $ 313,326,000

6. Expected Member Contributions $ 302,666,000 $ 0 $ 302,666,000

7. Administrative Expenses $ 33,000,000 $ 0 $ 33,000,000

8. Net Employer Normal Cost as of December 31, 2010: $ 34,521,000 $ 9,139,000 $ 43,660,000 (5) - (6) + (7)

25

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties whoreceive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or qualified professional when reviewingthe Milliman report.

The above liabilities are for Basic System Benefits and selected System Administered Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

B. Development of Unfunded Actuarial Accrued Liability and Amortization Payment Payable as of December 31, 2010

1. Actuarial Accrued Liability as of June 30, 2010 $ 19,501,761,000

2. Actuarial Value of Assets as of June 30, 2010 $ 1,667,358,000

3. Unfunded Actuarial Accrued Liability as of June 30, 2010 (1) - (2): $ 17,834,403,000

4. Amortization Period in years 27

5. Amortization Factor at beginning of year 12.2995

6. Amortization Amount Payable as of $ 1,503,403,000 December 31, 2010: [ (3) / (5) ] * (1.075 ^ 0.5)

C. Development of Annual Required Contribution

1. Total Employer Normal Cost as of December 31, 2010 $ 43,660,000

2. Amortization Payment as of December 31, 2010 $ 1,503,403,000

3. Annual Required Contribution*: (1) + (2) $ 1,547,063,000

* Assumes payments made throughout the year.

26

SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

The above liabilities are for Basic System Benefits and selected System Administered Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

D. Schedule of Employer Contributions

Year Actual AnnualEnded Employer Required Percent

June 30 Contribution Contribution Contributed

2011 * $542,217,000 $1,547,063,000 35.05%2010 534,275,000 1,459,774,000 36.602009 594,509,000 1,258,695,000 47.23

2008 ** 581,285,000 1,191,275,000 48.80 2007 *** 566,524,000 816,472,000 69.39 2006 *** 559,198,000 816,472,000 68.49

2005 374,823,000 578,387,000 64.80

* Actual Employer Contribution for the year ended June 30, 2011 assumes: - contribution of 9.275% of expected payroll for the Basic System Benefits, plus - contribution of $151.0 million for Special Law pension benefits, plus - contribution of $37.0 million for early retirement incentives.

** In the development of the Fiscal Year 2007-2008 Annual Required Contribution the System has adopted a level dollar amortization method with a 30-year period to reflect the closing of the defined benefit plan to new entrants under System 2000 (the Retirement Savings Account Program).

*** Annual Required Contribution for the years ended June 30, 2007 and June 30, 2006 is restated to remove the offset of employer contributions on behalf of System 2000 members that was applied to the normal cost, and to include the Special Law Benefits. Actual Employer Contributions are restated to include receipts for Special Law pension benefits and early retirement incentives. These adjustments were made to allow for better comparability between the results of the later and the earlier valuations.

27

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION

The above liabilities are for Basic System Benefits and selected System Administered Benefits. See Section I for more information.

E. Schedule of Funding Progress

(a) (b) (c)=(b)-(a) (d)=(a)/(b) (e) (f)=(c)/(e)

UnfundedActuarial Actuarial Liability as aValuation Value of Accrued Unfunded Funded Annual % of Annual

Date Assets Liability Liability Ratio Salary Salary

06/30/2010 $1,667,358,000 $19,501,761,000 $17,834,403,000 8.5% $3,818,332,000 467.1%06/30/2009 1,851,223,000 18,943,586,000 17,092,363,000 9.8% 4,292,552,000 398.2%06/30/2008 2,607,086,00006/30/2007 2,891,501,000 16,769,512,000 13,878,011,000 17.2% 4,246,409,000 326.8%06/30/2006 2,541,331,000

* 06/30/2005 2,327,871,000 13,969,000,000 11,641,129,000 16.7% 4,125,866,000 282.2%

* Accrued liability for June 30, 2005 is restated to include the Special Law benefits. This adjustment was made to allow for better comparability between the results of the current and the prior valuation.

28

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty orliability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its ownactuary or qualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION

The above liabilities are for Basic System Benefits and selected System Administered Benefits. See Section I for more information.

------------------------------------------- not determined -------------------------------------------

------------------------------------------- not determined -------------------------------------------

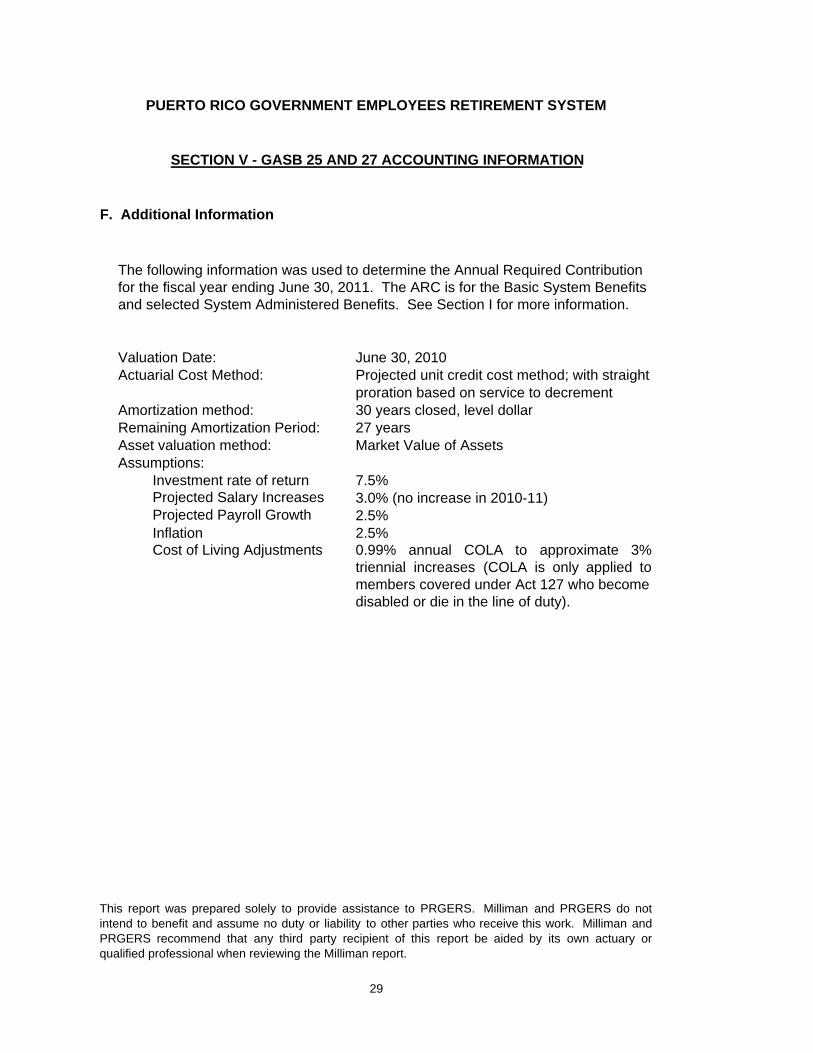

F. Additional Information

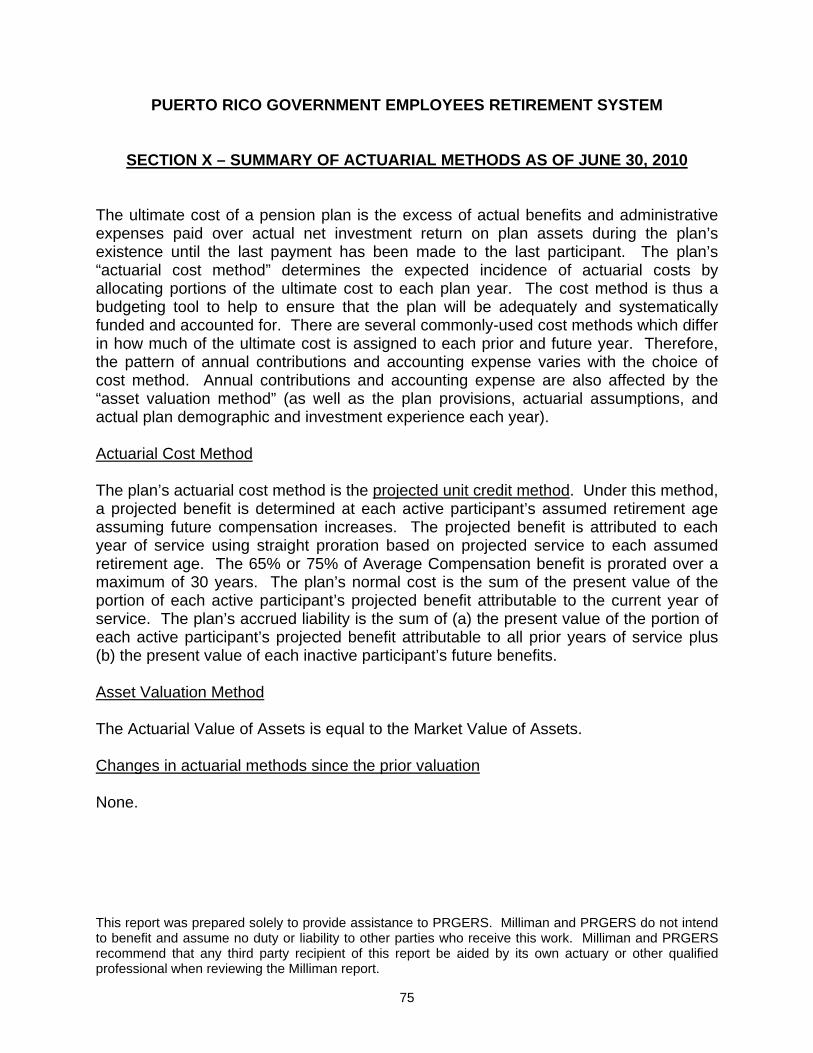

Valuation Date: June 30, 2010Actuarial Cost Method: Projected unit credit cost method; with straight

proration based on service to decrementAmortization method: 30 years closed, level dollarRemaining Amortization Period: 27 yearsAsset valuation method: Market Value of AssetsAssumptions:

Investment rate of return 7.5%Projected Salary Increases 3.0% (no increase in 2010-11)Projected Payroll Growth 2.5%Inflation 2.5%Cost of Living Adjustments 0.99% annual COLA to approximate 3%

triennial increases (COLA is only applied tomembers covered under Act 127 who become disabled or die in the line of duty).

29

The following information was used to determine the Annual Required Contribution for the fiscal year ending June 30, 2011. The ARC is for the Basic System Benefits and selected System Administered Benefits. See Section I for more information.

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do notintend to benefit and assume no duty or liability to other parties who receive this work. Milliman andPRGERS recommend that any third party recipient of this report be aided by its own actuary orqualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION V - GASB 25 AND 27 ACCOUNTING INFORMATION

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

A. Benefit Obligations

1. Projected Benefits Payable to Retirees and Beneficiaries: Retirees $ 903,468,000 Disabled Members 151,943,000 Beneficiaries 0 Total $ 1,055,411,000

2. Projected Benefits Payable to Vested Terminated Members: $ 78,200,000

3. Actuarial Accrued Liability for Active Members $ 512,537,000

4. Total Actuarial Accrued Liability as of June 30, 2010: $ 1,646,148,000

5. Total Employer Normal Cost as of December 31, 2010: $ 28,722,000

30

SECTION VI - GASB 45 ACCOUNTING INFORMATION

The above liabilities are for the Medical Insurance Plan Contribution portion of the System Administered Benefits. See Section I for more information.

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VI - GASB 45 ACCOUNTING INFORMATION

B. Development of Unfunded Actuarial Accrued Liability and Amortization Payment Payable as of December 31, 2010:

1. Actuarial Accrued Liability as of June 30, 2010: $ 1,646,148,000

2. Actuarial Value of Assets as of June 30, 2010: $ 0

3. Unfunded Actuarial Accrued Liability as of June 30, 2010: (1) - (2) $ 1,646,148,000

4. Amortization Period in years 27

5. Amortization Factor at beginning of year 16.9828

6. Amortization Amount Payable as of December 31, 2010: [ (3) / (5) ] * ( 1.04 ^ 0.5 ) $ 98,850,000

C. Development of Annual Required Contribution

1. Total Employer Normal Cost as of December 31, 2010: $ 28,722,000

2. Amortization Payment as of December 31, 2010: $ 98,850,000

3. Annual Required Contribution*: (1) + (2) $ 127,572,000

* Assumes payments made throughout the year.

31

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

The above liabilities are for the Medical Insurance Plan Contribution portion of the System Administered Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

D. Schedule of Employer Contributions

Year Actual AnnualEnded Employer Required Percent

June 30 Contribution Contribution Contributed

2011 * $89,690,000 $127,572,000 70.31%2010 85,460,000 128,294,000 66.612009 86,739,000 111,683,000 77.672008 79,793,607 110,650,000 72.11

* Actual Employer Contribution for the year ended June 30, 2011 assumes: - contribution of $89.690 million for Special Law OPEB benefits.

32

SECTION VI - GASB 45 ACCOUNTING INFORMATION

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend tobenefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERSrecommend that any third party recipient of this report be aided by its own actuary or qualified professionalwhen reviewing the Milliman report.

The above liabilities are for the Medical Insurance Plan Contribution portion of the System Administered Benefits. See Section I for more information

E. Schedule of Funding Progress

(a) (b) (c)=(b)-(a) (d)=(a)/(b) (e) (f)=(c)/(e)

UnfundedActuarial Actuarial Liability as aValuation Value of Accrued Unfunded Funded Annual % of Annual

Date Assets Liability Liability Ratio Salary Salary

06/30/2010 $0 $1,646,148,000 $1,646,148,000 0.0% $3,818,332,000 43.1%06/30/2009 0 1,633,159,000 1,633,159,000 0.0% 4,292,552,000 38.0%06/30/2008 006/30/2007 0 1,556,809,000 1,556,809,000 0.0% 4,246,409,000 36.7%

33

The above liabilities are for the Medical Insurance Plan Contribution portion of the System Administered Benefits. See Section I for more information.

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty orliability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its ownactuary or qualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VI - GASB 45 ACCOUNTING INFORMATION

------------------------------------------- not determined -------------------------------------------

F. Additional Information

Valuation Date: June 30, 2010Actuarial Cost Method: Projected unit credit cost method; with straight

proration based on service to decrementAmortization method: 30 years closed, level dollarRemaining Amortization Period: 27 yearsAsset valuation method: not applicableAssumptions:

Investment rate of return 4.0%Projected Salary Increases not applicableProjected Payroll Growth not applicableInflation not applicableCost of Living Adjustments not applicable

34

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do notintend to benefit and assume no duty or liability to other parties who receive this work. Milliman andPRGERS recommend that any third party recipient of this report be aided by its own actuary orqualified professional when reviewing the Milliman report.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VI - GASB 45 ACCOUNTING INFORMATION

The following information was used to determine the Annual Required Contribution for the fiscal year ending June 30, 2011. The ARC is for the Basic System Benefits and selected System Administered Benefits. See Section I for more information.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VII - CENSUS DATA

A. Summary of Member Data as of June 30, 2010:

Act 447 Act 1 System 2000 TotalActive Members

Count 34,079 51,284 55,279 140,642Average Age 53.2 46.8 40.2 45.8Average Salary $31,465 $27,928 $23,766 $27,149Average Creditable Service 20.5 14.4 6.0 12.6

Retired MembersCount 75,100 2,428 N/A 77,528Average Age 69.2 68.4 N/A 69.2Average Monthly Basic System Benefit $1,047 $748 N/A $1,037Average Monthly System Administered Benefit $76 $16 N/A $74

Disabled MembersCount 16,521 318 N/A 16,839Average Age 67.7 52.1 N/A 67.4Average Monthly Basic System Benefit $429 $515 N/A $431Average Monthly System Administered Benefit $117 $16 N/A $115

Beneficiaries in paymentCount 12,157 14 N/A 12,171Average Age 71.4 58.4 N/A 71.4Average Monthly Basic System Benefit $275 $508 N/A $275Average Monthly System Administered Benefit $20 $0 N/A $20

35

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other partieswho receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or qualified professional whenreviewing the Milliman report.

Basic System Benefit and System Administered Benefit amounts shown above are for pension benefits, including minimumbenefits and COLAs. Special Law "bonus" benefits are not reflected.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VIII – SUMMARY OF PRINCIPAL PLAN PROVISIONS

AS OF JUNE 30, 2010

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

36

Three main sets of benefit provisions apply to various members of PRGERS depending on the member’s date of hire. In general, the benefits under Act 447 of 1951 (as amended) apply to members hired before April 1, 1990. The benefits under Act 1 of 1990 (as amended) apply to members hired on or after April 1, 1990 and on or before December 31, 1999. The benefits under Act 305 of 1999 (as amended), known as System 2000, apply to members hired on or after January 1, 2000. This summary of plan provisions, with separate descriptions for the three sets of benefits, is intended only to describe the essential features of the plan for valuation purposes. All eligibility requirements and benefit amounts shall be determined in strict accordance with the plan document itself. Act 447 of 1951 as amended 1. Type of Plan The System is a contributory, defined benefit plan. 2. Effective Date The System was established in 1951 by Act 447 to be effective January 1, 1952.

The plan was last amended under Act 7, approved February 15, 2008. 3. Eligibility for Membership Members of the Employees Retirement System of the Government of Puerto Rico

and its Instrumentalities include all regular full-time employees who are not contributing to other Retirement Systems (Articles 1-104 and 1-105) and who were initially hired full-time prior to April 1, 1990. Employees include those in the following categories:

• Police of Puerto Rico, • Firefighters of Puerto Rico, • Elective officers and the employees of the Legislature, • Officers and employees of the Government of Puerto Rico, • Officers and employees of public enterprises, • Officers and employees, including mayors, of the municipalities, and • Irregular personnel fulfilling the requirements of regular employee.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VIII – SUMMARY OF PRINCIPAL PLAN PROVISIONS

AS OF JUNE 30, 2010

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

37

Membership is mandatory, except for the Governor of Puerto Rico, Government Secretaries, heads of public agencies and instrumentalities, the Governor’s aides, gubernatorial appointees of commissions and boards, members of the Legislature, the Controller of Puerto Rico, the employees of the Agricultural Extension Service of the U.P.R., the Ombudsman and the Commonwealth Election Board employees (Article 1-105). In addition, membership is optional for eligible employees while working and residing outside the territorial limits of the Commonwealth of Puerto Rico (Act 112 of 2004).

4. Definitions a. Fiscal Year: A Fiscal Year is a 12-month period beginning on July 1 and ending

on June 30 (Article 1-104). b. General Fund: The General Expenses Budget of the Government of the

Commonwealth of Puerto Rico. c. Government of Puerto Rico or Government: The Government of the

Commonwealth of Puerto Rico, its departments, divisions, bureaus, offices, agencies and dependencies (Article 1-104).

d. Public Enterprise: Any government instrumentality of the People of Puerto Rico

(Article 1-104). e. Municipality: The Municipality of San Juan (Article 1-104). f. Employer: The Government of Puerto Rico, any public enterprise that has

elected to participate in the System, or any municipality that has elected to participate in the System (Articles 1-104 and 1-110).

g. Employee: Any officer or employee of the Employer regularly employed on a full

time basis (Article 1-104). h. Creditable Service: The years and months of plan participation, during which

contribution have been made, beginning on the later of date of hire or January 1, 1952 and ending on date of separation from service. For purposes of calculating Creditable Service, the following schedule shall apply:

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VIII – SUMMARY OF PRINCIPAL PLAN PROVISIONS

AS OF JUNE 30, 2010

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

38

Service During a Fiscal Year Creditable Service Earned

15 days during the same month 1 month

2 months and 15 days to 5 months and 14 days ½ year

5 months and 15 days to 8 months and 14 days ¾ year

8 months and 15 days to 12 months 1 year

Note: All of the days have to be during the same month.

Months in which less than 15 days of service are rendered do not count towards

Creditable Service. (Article 1-106) In general, Creditable Service may be earned for any period of employment

during which no contributions were made if Accumulated Contributions for such periods are paid to the System. The same rules hold for rehired employees who previously received a refund of Accumulated Contributions at separation. (Article 1-106)

Creditable Service also includes purchased service, if any (Article 1-106). i. Compensation: The gross cash compensation, excluding bonuses and overtime,

upon which contributions by a Member to the Fund are based (Article 1-104). j. Average Compensation: The average of the 3 highest years (36 highest months)

of compensation that the participant has received for Creditable Service (Article 1-104).

k. Contributions: The amount deducted from the compensation of a Member and

the employer (Section 781). l. Regular Interest: The interest rate as prescribed by the Board of Trustees

(Article 1-104). The rate of 2.50% has always been in effect.

PUERTO RICO GOVERNMENT EMPLOYEES RETIREMENT SYSTEM

SECTION VIII – SUMMARY OF PRINCIPAL PLAN PROVISIONS

AS OF JUNE 30, 2010

This report was prepared solely to provide assistance to PRGERS. Milliman and PRGERS do not intend to benefit and assume no duty or liability to other parties who receive this work. Milliman and PRGERS recommend that any third party recipient of this report be aided by its own actuary or other qualified professional when reviewing the Milliman report.

39

m. Accumulated Contributions: The sum of all amounts deducted from the compensation of a Member with regular interest (Article 1-104).

n. Actuarial Equivalent: Equality in value such that the present value of the amount