Embed Size (px)

Citation preview

Published by BUSINESS MONITOR INTERNATIONAL LTD

Including 5-year and 10-year industry forecasts

© 2009 Business Monitor International. All rights reserved.All information, analysis, forecasts and data provided by Business Monitor International Ltd is for the exclusive use of subscribing persons or organisations (including those using the service on a trial basis). All such content is copyrighted in the name of Business Monitor International, and as such no part of this content may be reproduced, repackaged, copied or redistributed without the express consent of Business Monitor International Ltd.

All content, including forecasts, analysis and opinion, has been based on information and sources believed to be accurate and reliable at the time of publishing. Business Monitor International Ltd makes no representation of warranty of any kind as to the accuracy or completeness of any information provided, and accepts no liability whatsoever for any loss or damage resulting from opinion, errors, inaccuracies or omissions affecting any part of the content.

Business Monitor InternationalMermaid House, 2 Puddle DockLondon EC4V 3DS UKTel: +44 (0)20 7248 0468Fax: +44 (0)20 7248 0467email: [email protected]: http://www.businessmonitor.com

United Arab EmiratesOil & GasReport Q3 2009 ISSN: 1748-4332

Business Monitor International Mermaid House, 2 Puddle Dock, London, EC4V 3DS, UK Tel: +44 (0) 20 7248 0468 Fax: +44 (0) 20 7248 0467 email: [email protected] web: http://www.businessmonitor.com

© 2009 Business Monitor International. All rights reserved. All information contained in this publication is copyrighted in the name of Business Monitor International, and as such no part of this publication may be reproduced, repackaged, redistributed, resold in whole or in any part, or used in any form or by any means graphic, electronic or mechanical, including photocopying, recording, taping, or by information storage or retrieval, or by any other means, without the express written consent of the publisher.

DISCLAIMER All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor International accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the publication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind as to the accuracy or completeness of any information hereto contained.

UAE Oil & Gas Report Q3 2009 Including 5-year and 10-year industry forecasts by BMI

Part of BMI's Industry Survey & Forecasts Series

Published by: Business Monitor International

Publication date: July 2009

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 2

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 3

CONTENTS

Executive Summary .........................................................................................................................................7

SWOT Analysis.................................................................................................................................................9

United Arab Emirates Political SWOT .................................................................................................................................................................. 9 United Arab Emirates Economic SWOT .............................................................................................................................................................. 10 United Arab Emirates Business Environment SWOT........................................................................................................................................... 11

UAE Energy Market Overview.......................................................................................................................12

Regional Energy Market Overview ...............................................................................................................14

Oil Supply And Demand............................................................................................................................................................................................ 14 Table: Middle East Oil Consumption (000b/d) .................................................................................................................................................... 15 Table: Middle East Oil Production (000b/d) ....................................................................................................................................................... 16

Oil: Downstream ...................................................................................................................................................................................................... 17 Table: Middle East Oil Refining Capacity (000b/d)............................................................................................................................................. 17

Gas Supply And Demand .......................................................................................................................................................................................... 18 Table: Middle East Gas Consumption (bcm) ....................................................................................................................................................... 18 Table: Middle East Gas Production (bcm) .......................................................................................................................................................... 19

Liquefied Natural Gas............................................................................................................................................................................................... 20 Table: Middle East LNG Exports/(Imports) (bcm)............................................................................................................................................... 20

Business Environment Ranking ...................................................................................................................21

Middle East Region................................................................................................................................................................................................... 21 Composite Scores................................................................................................................................................................................................. 21 Table: Regional Upstream Business Environment Rating.................................................................................................................................... 22 Table: Regional Downstream Business Environment Rating ............................................................................................................................... 23 Upstream Scores.................................................................................................................................................................................................. 23 Downstream Scores ............................................................................................................................................................................................. 23 UAE Upstream Rating – Overview ...................................................................................................................................................................... 24 UAE Upstream Rating – Potential Returns.......................................................................................................................................................... 24 UAE Upstream Rating – Risks to Potential Returns............................................................................................................................................. 24 UAE Downstream Rating – Overview.................................................................................................................................................................. 24 UAE Downstream Rating – Potential Returns ..................................................................................................................................................... 25 UAE Downstream Rating – Risks to Potential Returns........................................................................................................................................ 25

Business Environment ..................................................................................................................................26

Legal Framework...................................................................................................................................................................................................... 26 Infrastructure....................................................................................................................................................................................................... 28

Labour Force............................................................................................................................................................................................................ 28 Foreign Investment Policy ........................................................................................................................................................................................ 30

Tax Regime .......................................................................................................................................................................................................... 31 Security Risk ........................................................................................................................................................................................................ 31

Industry Forecast Scenario...........................................................................................................................32

Oil and Gas Reserves................................................................................................................................................................................................ 32 Oil Supply and Demand............................................................................................................................................................................................ 32 Gas Supply and Demand........................................................................................................................................................................................... 34 LNG .......................................................................................................................................................................................................................... 35

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 4

Refining and Oil Products Trade .............................................................................................................................................................................. 36 Revenues/Import Costs.............................................................................................................................................................................................. 37

Table: UAE Oil & Gas – Historical Data & Forecasts ....................................................................................................................................... 38 Other Energy ............................................................................................................................................................................................................ 39

Table: UAE Other Energy – Historical Data & Forecasts .................................................................................................................................. 40 Key Risks To BMI’s Forecast Scenario..................................................................................................................................................................... 40 Long-Term Oil & Gas Outlook ................................................................................................................................................................................. 41

Macroeconomic Outlook ...............................................................................................................................42

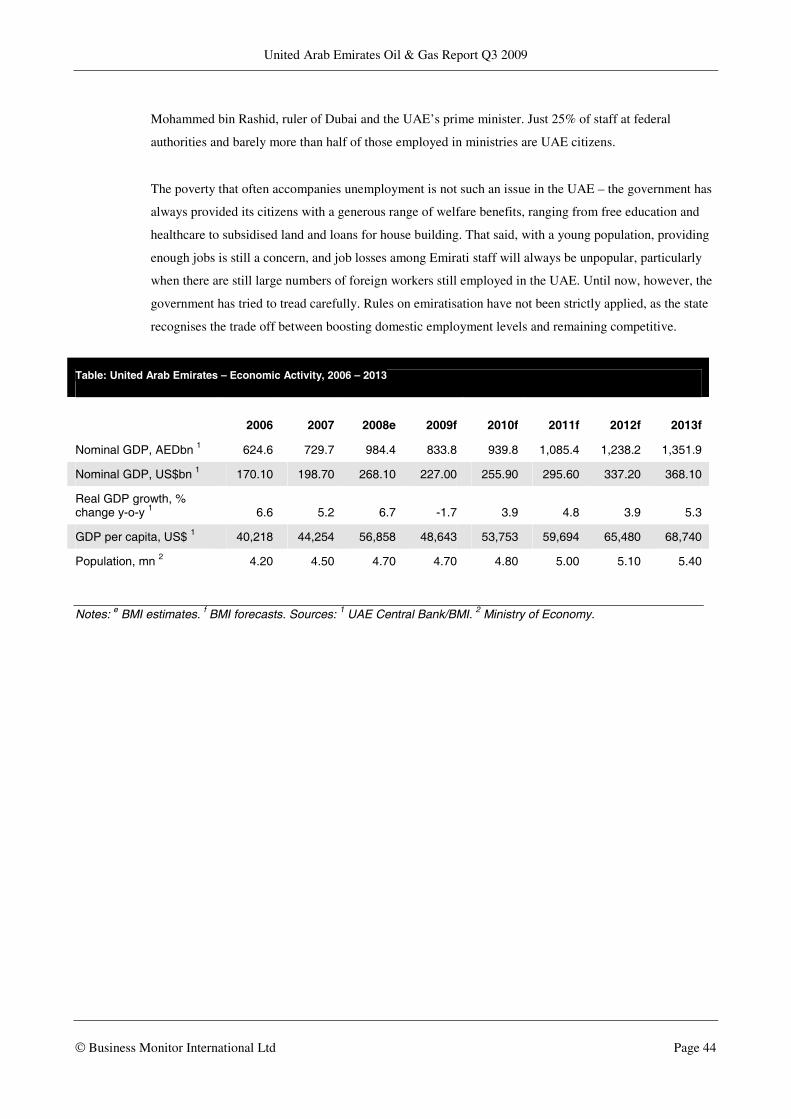

Table: United Arab Emirates – Economic Activity, 2006 – 2013......................................................................................................................... 44

Competitive Landscape .................................................................................................................................45

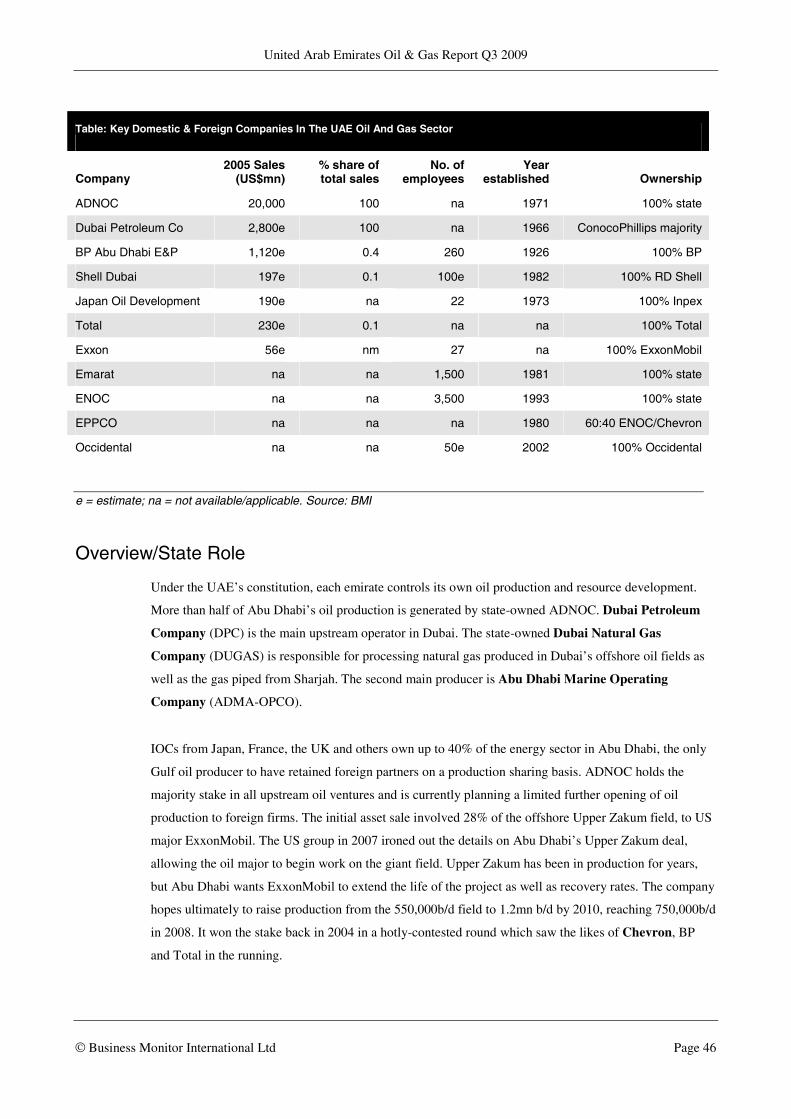

Table: Key Domestic & Foreign Companies In The UAE Oil And Gas Sector .................................................................................................... 46 Overview/State Role.................................................................................................................................................................................................. 46

Table: Key Upstream Players .............................................................................................................................................................................. 47 Table: Key Downstream Players ......................................................................................................................................................................... 48

Company Monitor...........................................................................................................................................49

Abu Dhabi National Oil Company (ADNOC) ........................................................................................................................................................... 49 Dolphin Energy Ltd (DEL) ....................................................................................................................................................................................... 53 Emarat – Emirates General Petroleum Corporation ................................................................................................................................................ 56 Emirates National Oil Company Limited (ENOC).................................................................................................................................................... 58

BP – Summary ..................................................................................................................................................................................................... 60 Total – Summary.................................................................................................................................................................................................. 60 ConocoPhillips – Summary.................................................................................................................................................................................. 60 ExxonMobil – Summary....................................................................................................................................................................................... 61 Shell – Summary .................................................................................................................................................................................................. 61 Dana Gas – Summary .......................................................................................................................................................................................... 62 Occidental Petroleum – Summary........................................................................................................................................................................ 62 Japan Oil Development Co (JODCO) – Summary............................................................................................................................................... 63 Cosmo Oil – Summary ......................................................................................................................................................................................... 63 Abu Dhabi National Energy Company (TAQA) – Summary................................................................................................................................. 63

Glossary of Terms..........................................................................................................................................65

Oil & Gas Ratings: Revised Methodology ...................................................................................................66

Introduction .............................................................................................................................................................................................................. 66 Ratings Overview...................................................................................................................................................................................................... 66

Table: BMI Oil & Gas Business Environment Ratings: Structure ....................................................................................................................... 67 Indicators.................................................................................................................................................................................................................. 68

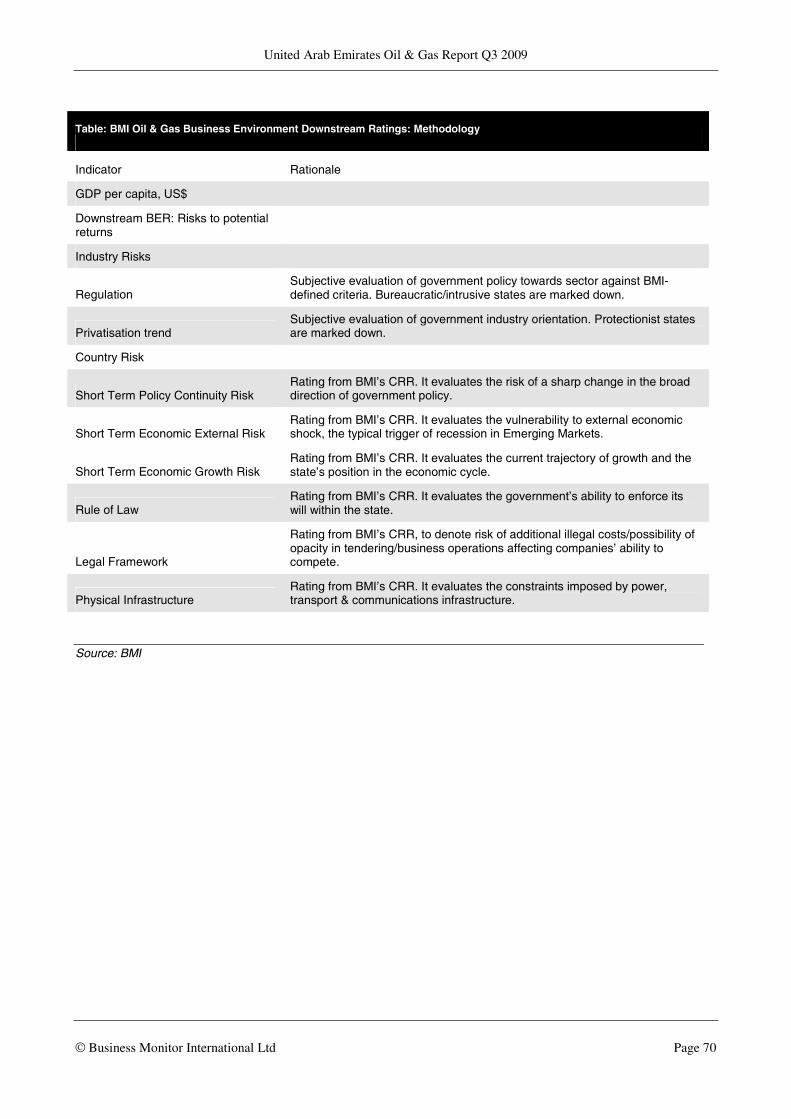

Table: BMI Oil & Gas Business Environment Upstream Ratings: Methodology................................................................................................. 68 Table: BMI Oil & Gas Business Environment Downstream Ratings: Methodology ............................................................................................ 69

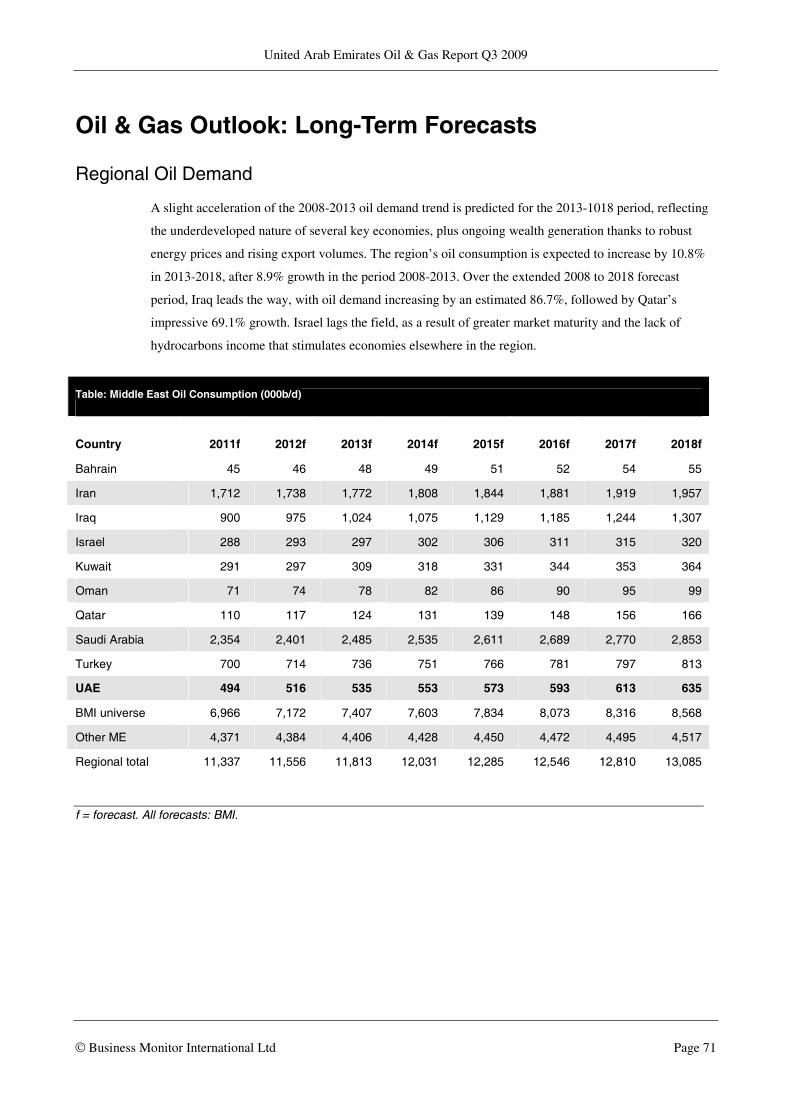

Oil & Gas Outlook: Long-Term Forecasts ...................................................................................................71

Regional Oil Demand ............................................................................................................................................................................................... 71 Table: Middle East Oil Consumption (000b/d) .................................................................................................................................................... 71

Regional Oil Supply .................................................................................................................................................................................................. 72 Table: Middle East Oil Production (000b/d) ....................................................................................................................................................... 72

Regional Refining Capacity ...................................................................................................................................................................................... 73 Table: Middle East Oil Refining Capacity (000b/d)............................................................................................................................................. 73

Regional Gas Demand .............................................................................................................................................................................................. 74 Table: Middle East Gas Consumption (bcm) ....................................................................................................................................................... 74

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 5

Regional Gas Supply................................................................................................................................................................................................. 75 Table: Middle East Gas Production (bcm) .......................................................................................................................................................... 75

UAE Country Overview ............................................................................................................................................................................................ 75 Methodology & Risks To Forecasts .......................................................................................................................................................................... 76

BMI Forecast Modelling.................................................................................................................................77

How we generate our industry forecasts ................................................................................................................................................................... 77 Energy Industry ........................................................................................................................................................................................................ 78 Cross checks ............................................................................................................................................................................................................. 78 Sources ..................................................................................................................................................................................................................... 78

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 6

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 7

Executive Summary

The latest United Arab Emirates (UAE) Oil & Gas Report from BMI forecasts that the country will

account for 4.52% of Middle Eastern (ME) regional oil demand by 2013, while providing 11.36% of

supply. Regional oil use of 8.24mn barrels per day (b/d) in 2001 rose to an estimated 10.86mn b/d in

2008. It should average 11.09mn b/d in 2009 and then rise to around 12.08mn b/d by 2013. Regional oil

production was 22.87mn b/d in 2001, and in 2008 averaged an estimated 25.94mn b/d. It is set to rise to

28.99mn b/d by 2013. Oil exports are growing steadily, because demand growth is lagging the pace of

supply expansion. In 2001, the region was exporting an average 14.63mn b/d. This total had risen to an

estimated 15.18mn b/d in 2008 and is forecast to reach 16.58mn b/d by 2013. Iraq has the greatest

production growth potential, followed by Qatar.

As regards natural gas, the region in 2008 consumed an estimated 386bn cubic metres (bcm), with

demand of 511bcm targeted for 2013, representing 32.3% growth. Production of an estimated 407bcm in

2008 should reach 625bcm in 2013 (+53.8%), which implies net exports rising to 115bcm by the end of

the period. The UAE in 2008 consumed an estimated 12.44% of the region’s gas, with its market share

forecast at 12.35% by 2013. It contributed an estimated 14.26% to 2008 regional gas production and, by

2013, will account for 14.39% of supply.

In terms of the OPEC basket of crudes, the average price in Q109 was an estimated US$45.78 per barrel

(bbl), down 13% from the US$52.51/bbl recorded during the previous three months. During the second

quarter, there has been little change to our view of oil market developments. BMI is forecasting an

average OPEC basket price of US$51.30/bbl, with the March gains being retained in April, before further

recovery to a possible US$57.00 is seen by June. For 2009, we are still assuming an average OPEC basket

price of US$52.00/bbl (-45% year-on-year). The BMI full year forecast implies Brent crude at US$53.73,

WTI averaging US$54.90/bbl and Urals at US$52.66 for 2009.

For the whole of 2009, the BMI assumption for gasoline is an average US$56.89/bbl, with the price

peaking at a forecast monthly average of US$64.75 in December 2009. The overall y-o-y fall in 2009

gasoline prices is put at 44.1%. For gasoil in 2009, the BMI forecast is for an average price of

US$69.35/bbl, assuming a monthly high of US$94.48/bbl in December. The full-year outturn represents a

42.8% fall from the 2008 level. The monthly average jet fuel price is forecast to range from US$53.75 in

February to US$96.76/bbl in December, proving an annual level of US$71.78/bbl. This compares with

US$124.95/bbl in 2008.

The UAE’s real GDP is forecast by BMI to fall by 1.7% in 2009, following growth of 6.7% in 2008. We

are assuming 3.9% growth in 2010, 4.8% in 2011, 3.9% in 2012, followed by 5.3% in 2013. We expect

oil demand to rise from an estimated 468,000b/d in 2008 to 535,000b/d in 2013, lagging our underlying

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 8

economic assumptions. State-owned Abu Dhabi National Oil Company (ADNOC) is the biggest

national oil company, working in partnership with major international oil companies (IOCs) to deliver an

estimated 2.80mn b/d of 2009 oil and liquids production, rising to 3.23mn b/d by the end of the forecast

period – subject to OPEC quota policy. Gas production should reach at least 90bcm by 2013, up from an

estimated 58bcm in 2008. Consumption is expected to rise from 48bcm to 63bcm by the end of the

forecast period, allowing exports of 27bcm.

Between 2008 and 2018, we are forecasting an increase in UAE oil production of 24.0%, with volumes

rising steadily to 3.70mn b/d by the end of the 10-year forecast period. Oil consumption between 2008

and 2018 is set to increase by 35.7%, with growth slowing to an assumed 3.0% per annum towards the

end of the period and the country using 635,000b/d by 2018. Gas production is expected to rise from

58bcm to 110bcm by the end of the period. With 2008-2018 demand growth of 83.4%, this provides

export potential rising from 10bcm to 22bcm over the period. Details of BMI’s 10-year forecasts can be

found in the appendix to this report.

UAE is ranked a relatively close second place in BMI’s updated Upstream Business Environment rating,

thanks largely to its significant oil and gas resource base, and investor-friendly climate. It stands seven

points clear of Iraq, so appears secure at least over the medium term. It is unlikely, however, to mount a

near-term challenge on Qatar, four points above it. UAE’s score reflects the country’s gas reserves, high

RPR, plus non-state competition, established licensing framework and generally encouraging country risk

factors. The country is well up the league table in BMI’s Downstream Business Environment rating, with

several high scores and further progress up the rankings possible over the longer term. It is ranked second

behind only Turkey, thanks largely to high scores for oil and gas demand, refining capacity expansion,

and nominal GDP.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 9

SWOT Analysis

United Arab Emirates Political SWOT

Strengths Standards of living are high for nationals, which has dampened any demands for greater political representation.

The monarchy enjoys strong support nationwide.

Weaknesses Lack of democracy poses long-term risks given trends towards greater popular participation elsewhere in the region.

Sheikh Khalifa bin Zayed assumed the presidency after the death of Sheikh Zayed al-Nahayan. He is equally conservative and is unlikely to make concerted efforts to address constitutional issues.

The succession lineage is somewhat opaque, raising concerns about longer-term stability.

Opportunities The UAE co-operates closely with other GCC states in security and economic policy.

The UAE is typically a 'dove' within OPEC, sympathetic to the needs of consumer states, which is good for its relations with the West.

Dubai enjoyed a smooth political succession following the death of former ruler Sheikh Maktoum bin Rashid al-Maktoum in January 2006, with new ruler Sheikh Mohammed bin Rashid al-Maktoum welcomed by most of the public.

Threats There is a long-running territorial dispute with Iran, which continues to affect bilateral relations.

Relatively poor living conditions among some foreign workers have led to strikes and demonstrations. Given the size of the expatriate community, this poses some threat to domestic stability.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 10

United Arab Emirates Economic SWOT

Strengths The UAE is a member of the Gulf Co-operation Council, which, as well as being a common market, is targeting a common currency by 2010.

The UAE has one of the most liberal trade regimes in the Gulf, and attracts strong capital flows from across the region.

In common with most Gulf states, there are a high number of expatriate workers at all levels of the economy, making up for the otherwise small workforce.

The UAE is progressively diversifying its economy, minimising vulnerability to oil price movements

Weaknesses The UAE's currency is pegged to the dollar, giving it minimal control over monetary policy and reducing its ability to tackle inflationary pressure.

The state's location in a volatile region means that its risk profile is, to some extent, affected by events elsewhere. US concerns about regional militant groups and Iranian WMD programmes could affect investor perceptions.

Opportunities Oil prices are expected to stay high (by historical standards) over the forecast period.

Economic diversification into gas, tourism, financial services and high-tech industry offers some protection against volatile oil prices.

The construction, tourism and financial sectors are growing rapidly, driven by domestic and foreign investment.

Threats Heavy subsidies on utilities and agriculture and an outdated tax system have contributed to persistent fiscal deficits in the past, although rising oil revenues have masked the problem in recent years.

Some bottlenecks have been forming in the construction sector and there is a chance of delays in several high-profile construction projects.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 11

United Arab Emirates Business Environment SWOT

Strengths The UAE is a member of the Gulf Co-operation Council, a six member common market, and has been a member of the WTO since 1996.

The state has invested large amounts in infrastructure, and will continue to do so over the next 10 years.

The UAE's diversified economy reduces risks from volatile oil prices. Oil and gas reserves are vast and under-utilised, providing a high reserves-

to-production ratio (RPR) that facilitates medium- to long-term production growth.

Weaknesses Due to the state's federal nature, regulations can vary considerably across

the emirates. The regional economy is oil-dependent. This has historically been very

cyclical, which increases risks for long-term projects. Growth in oil production is subject to OPEC policy and substantial ongoing

investment that can be guaranteed only with continuing IOC participation.

Opportunities Large number of free trade zones offering tax holidays and full foreign ownership.

Comparatively relaxed rules on expatriate employment. The UAE's social stability and relative prosperity means that there is far less

concern for security than in some other Gulf states. The UAE is set to upgrade two refineries by end-2011 in order to meet rising

domestic demand for refined products.

Threats The state is bureaucratic relative to regional peers. Strong oil prices have massively increased liquidity in the region. This has

resulted in strong financial inflows, increasing risks that projects of lower investment potential are currently being funded.

Abu Dhabi in particular has less near- to medium-term oil and gas production upside potential than other Gulf States and investment opportunities elsewhere in the region could make IOCs less enthusiastic regarding longer-term UAE participation.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 12

UAE Energy Market Overview

The collection of states that forms the UAE has proven oil reserves estimated at 97.8bn barrels (bbl) (BP

Statistical Review of World Energy, June 2008), or nearly 10% of the world total. The same total is

recorded in the December 2008 Oil & Gas Journal (OGJ) survey. It also houses the world’s fifth largest

natural gas reserves at 6,090bcm at end-2007 and exports significant amounts of liquefied natural gas

(LNG) to Japan. It is also importing gas from Qatar. Abu Dhabi dominates the UAE oil and gas sector,

with 94% of its oil (over 92bn bbl). Dubai contains just 4bn bbl of reserves, followed by Sharjah and Ras

al-Khaimah, with 1.5bn bbl and 100mn bbl respectively.

The UAE is a member of OPEC and it has recently (March 2009) been producing 2.25mn b/d, against

sustainable productive capacity estimated at 2.85mn b/d. Output was reduced in support of OPEC policy,

with the December 2008 meeting allocating a quota of 2.22mn b/d to the Gulf producer. There are also

significant volumes of gas liquids that are exempt from OPEC quotas. Foreign minister Sheikh Abdullah

bin Zayed al-Nahyan announced in April 2007 that UAE oil production capacity will increase to 5mn b/d

by 2014, increasing the UAE’s profile in the Gulf region. Given the probable impact of lower oil prices

on spending plans, this target is unlikely to be met.

There are five operational refineries providing end-2008 capacity of approximately 781,000b/d, according

to the December 2008 OGJ annual survey. UAE oil consumption is estimated at 468,000b/d, while its gas

demand of 48bcm falls short of production at an estimated 58bcm.

For the UAE, gas was in 2007 the dominant fuel, accounting for 63.8% of primary energy demand (PED),

followed by oil at 36.2%. Regional energy demand is forecast to reach 853mn tonnes of oil equivalent

(toe) by 2013, representing 19.6% growth over the period since 2008. The UAE’s estimated 2008 market

share of 9.26% is set to climb to 9.70% by 2013. Electricity generation in the UAE is based on gas and

oil. Gas provides an estimated 97.8% and oil 2.2% of generated electricity.

It is estimated that the UAE electricity sector will require about US$8bn in investment over the next eight

years to meet growing demand, and the government has plans to expand its approximate 10 gigawatts

(GW) of installed capacity by more than 50% during the next decade. It is believed that Dubai alone will

have to invest to boost its power generating capacity to 9.5GW by 2010.

According to BMI calculations, end-2008 installed generating capacity in UAE was around 9GW, all of

which came from conventional thermal sources. In 2008, UAE generated an estimated 78TWh and

consumed an estimated 72TWh of electricity. Since 2000, electricity generation has risen by 50% and

consumption by almost 70%.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 13

Under the UAE’s constitution, each emirate controls its own oil production and resource development.

Although Abu Dhabi joined OPEC in 1967 (four years before the UAE was formed), Dubai does not

consider itself part of OPEC or bound by its quotas.

The UAE is considering revising its system of oil and gas concessions to spur technological development

and introduce more competition into its upstream segment. Having concluded its sour gas licensing round

with IOCs, it is expected that ADNOC will focus on reforming the concessions system as it seeks to boost

production capacity.

Several options are being considered for the concessions, including splitting them into their individual

fields and issuing competitive tenders for the fields’ development. Although the concessions are not due

to expire until 2014 at the earliest, it is expected that renegotiations will begin early. This may provide the

opportunity for smaller players to get a toehold into the UAE’s upstream segment and may open the door

for national oil companies (NOCs), particularly from Asia, to get involved. Nevertheless, the UAE is

unlikely to take any action which will put at risk its solid relationship with existing IOC partners.

Pipelines

The start-up of a planned 320km oil pipeline from the Habshan fields to the port of Fujairah has been

delayed by two years, according to a May 2009 statement by Dieter Blauberg, the director of the project.

The project was originally due to come onstream in 2009, but start-up had already been delayed until

2010. Blauberg said in early May 2009 that the project had now been pushed back to August 2011. The

delays have been attributed to the current ‘market conditions’. The pipeline is aimed at bypassing the

Strait of Hormuz. It will initially have a capacity of 1.5mn b/d, which could be increased to 1.8mn b/d at a

later stage. The pipeline will be supplied with oil from the Habshan fields, which are operated by

ADNOC.

China National Petroleum Corporation (CNPC) signed a US$3.29bn deal in November 2008 with the

IPIC to build the oil pipeline. Under the EPC contract for the Abu Dhabi Crude Oil Pipeline, CNPC’s two

pipeline engineering and construction units China Petroleum Pipeline Bureau (CPPB) and China

Petroleum Engineering & Construction Corporation (CPECC) will jointly build the 48-inch diameter

pipeline. The pipeline project will also include the construction of a 12mn bbl oil storage facility at

Fujairah and export terminal facilities. Further, the construction of a refinery at Fujairah is also being

considered by International Petroleum Investment Company (IPIC), but such plans are still at an early

stage, according to Blauberg.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 14

Regional Energy Market Overview

The Arabian Gulf states will continue to dominate oil supply, backed by huge and largely untapped

reserves. Gas is another important export product for the region, mainly in the form of LNG. The Gulf

plays a growing role in the supply of the world’s gas. Large parts of the region remain off limits to IOCs,

thanks to state control in the major Gulf states. Iraq is formulating oil laws that may result in foreign

partnerships, however. Investment in Iran by IOCs has come under increasing pressure thanks to the

nuclear standoff. Refinery investment opportunities do exist for IOC partners, with the region building a

substantial surplus with which to meet demand growth in Asia, Europe and North America.

Oil Supply And Demand

Thanks to the Gulf producers, this remains the key region in terms of supply – and has an increasingly

significant role to play as a consumer of oil. Oil- and gas-based wealth creation has stimulated regional

economies, triggering an unwelcome surge in fuel demand that could ultimately have a negative impact

on the export capabilities of Iran and others. The recent fall in crude prices may undermine investment

plans, with some risk of capacity expansion targets being missed. OPEC policy and a relatively high level

of quota adherence points to a meaningful downturn in 2009 regional supply.

Iraq remains the region’s ‘wild card’, having medium-term production potential of at least 3.30mn b/d,

with the government still targeting longer-term supply of up to 6.0mn b/d. For the immediate future,

volumes look set to continue recovering in spite of the uncertain political climate – as well as a lack of

investment in developing new reserves. For the region as a whole, we expect to see output reach 28.39mn

b/d by 2013, representing a gain of 9.04% over 2008. Apart from likely dramatic growth in Iraq, the big

supply winner will be Qatar, with Egypt the most significant loser. With regional consumption set to

reach 11.81mn b/d in 2013, the growing export capability is clearly vast. Some 16.58mn b/d is likely to

be exported in 2013, up from an estimated 13.70mn b/d in 2009.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 15

Table: Middle East Oil Consumption (000b/d)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Bahrain 39 40 41 42 44 45 46 48

Iran 1,625 1,621 1,675 1,670 1,687 1,712 1,738 1,772

Iraq 570 620 700 780 850 900 975 1,024

Israel 281 285 285 280 284 288 293 297

Kuwait 275 276 282 284 287 291 297 309

Oman 59 62 63 64 67 71 74 78

Qatar 79 95 98 100 104 110 117 124

Saudi Arabia 2,005 2,154 2,218 2,240 2,285 2,354 2,401 2,485

Turkey 655 666 673 670 683 700 714 736

UAE 419 450 468 473 482 494 516 535

BMI universe 6,007 6,269 6,503 6,604 6,774 6,966 7,172 7,407

Other ME 4,319 4,336 4,345 4,345 4,358 4,371 4,384 4,406

Regional total 10,326 10,605 10,848 10,949 11,132 11,337 11,556 11,813

e/f = estimate/forecast. Historical data: BP Statistical Review of World Energy, June 2008/BMI. All forecasts: BMI.

Middle East regional oil use of 8.24mn b/d in 2001 rose to an estimated 10.85mn b/d in 2008. It should

average 10.95mn b/d in 2009 and then rise to around 11.81mn b/d by 2013. The UAE accounted for an

estimated 4.31% of 2008 regional consumption, with its market share expected to be 4.52% by 2013.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 16

Table: Middle East Oil Production (000b/d)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Bahrain 50 49 48 50 55 58 60 57

Iran 4,388 4,401 4,300 4,100 4,200 4,250 4,300 4,450

Israel na na na na na na na na

Kuwait 2,682 2,626 2,750 2,600 2,650 2,750 2,900 3,050

Oman 752 718 730 730 730 725 720 710

Qatar 1,110 1,197 1,280 1,365 1,499 1,609 1,648 1,656

Saudi Arabia 10,853 10,413 10,830 9,850 10,100 10,500 11,000 11,350

Turkey 42 40 41 37 35 33 30 27

UAE 2,971 2,915 2,985 2,800 2,850 2,950 3,100 3,225

BMI universe 22,848 22,359 22,964 21,532 22,119 22,875 23,758 24,525

Iraq 1,999 2,145 2,350 2,400 2,550 2,700 2,950 3,100

Syria 417 397 377 358 340 323 307 292

Yemen 390 317 310 326 374 393 413 433

Other ME 32 33 34 34 35 36 37 38

Regional total 25,687 25,251 26,034 24,650 25,419 26,327 27,465 28,389

e/f = estimate/forecast. na = not applicable. Historical data: BP Statistical Review of World Energy, June 2008/BMI. Forecasts: BMI.

Regional oil production was 22.87mn b/d in 2001, and in 2008 averaged an estimated 26.03mn b/d. It is

set to rise to 28.39mn b/d by 2013. The UAE in 2008 accounted for an estimated 11.47% of regional oil

supply, and its market share is expected to be 11.36% by the end of the forecast period.

Oil exports are growing steadily, because demand growth is lagging the pace of supply expansion. In

2001, the region was exporting an average 14.63mn b/d. This total had risen to an estimated 15.18mn b/d

in 2008 and is forecast to reach 16.58mn b/d by 2013. Iraq has the greatest production growth potential,

followed by Qatar.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 17

Oil: Downstream

Table: Middle East Oil Refining Capacity (000b/d)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Bahrain 249 262 262 262 262 262 262 262

Iran 1,732 1,857 1,857 1,900 2,000 2,000 2,000 2,000

Iraq 666 674 674 750 750 1,000 1,150 1,200

Israel 220 220 220 220 220 220 320 320

Kuwait 905 905 905 990 990 990 1,150 1,150

Oman 85 85 85 235 235 235 235 235

Qatar 200 200 350 350 350 550 720 720

Saudi Arabia 2,100 2,100 2,100 2,450 2,530 2,630 2,630 3,430

Turkey 613 613 613 613 613 763 763 800

UAE 620 620 781 1,000 1,000 1,000 1,000 1,150

BMI universe 7,390 7,536 7,847 8,770 8,950 9,650 10,230 11,267

Other ME 694 729 729 765 765 765 803 843

Regional total 8,084 8,265 8,576 9,535 9,715 10,415 11,033 12,110

e/f = estimate/forecast. Historical data: BP Statistical Review of World Energy, June 2008/BMI. All forecasts: BMI.

Refining capacity for the region was 7.46mn b/d in 2001, rising gradually to an estimated 8.58mn b/d in

2008. Oman, Qatar, Iraq, Saudi Arabia, the UAE are all expected to increase significantly their domestic

refining capacity, with the region’s total capacity forecast to reach 12.11mn b/d by 2013 – well ahead of

oil demand, therefore implying substantial net exports of refined products. The UAE’s share of regional

refining capacity in 2008 was an estimated 9.11%, and its market share is set to rise to 9.50% by 2013.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 18

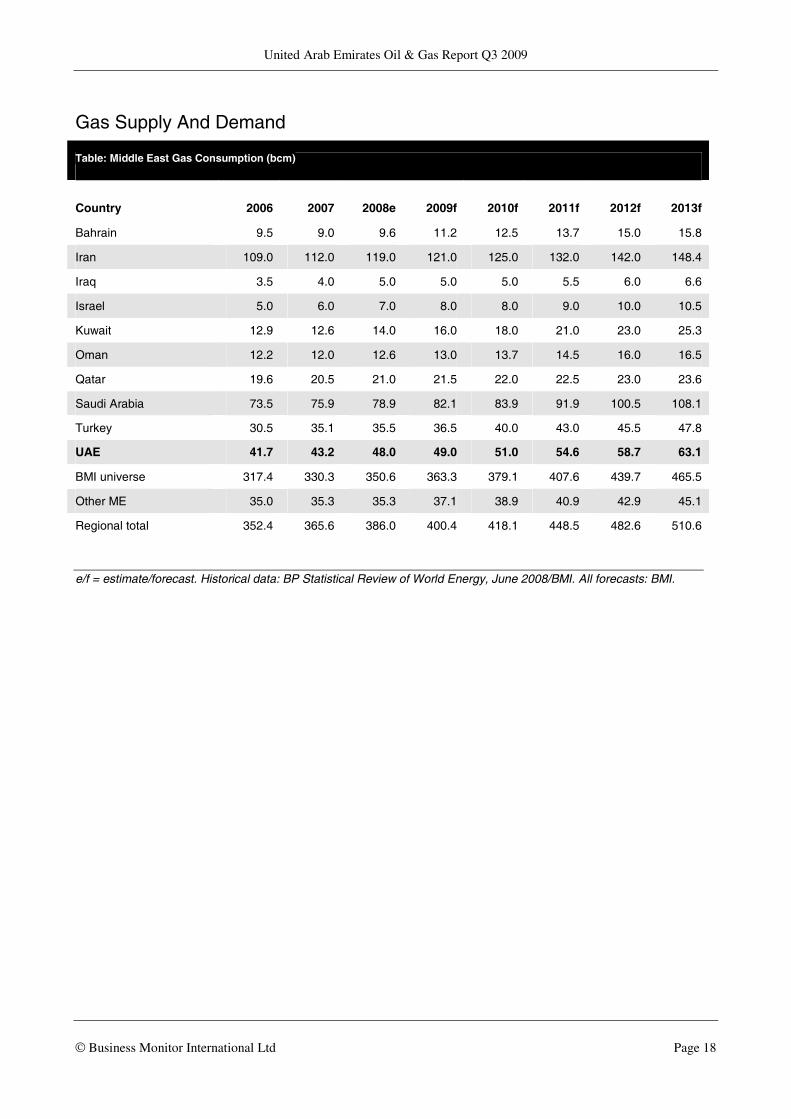

Gas Supply And Demand

Table: Middle East Gas Consumption (bcm)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Bahrain 9.5 9.0 9.6 11.2 12.5 13.7 15.0 15.8

Iran 109.0 112.0 119.0 121.0 125.0 132.0 142.0 148.4

Iraq 3.5 4.0 5.0 5.0 5.0 5.5 6.0 6.6

Israel 5.0 6.0 7.0 8.0 8.0 9.0 10.0 10.5

Kuwait 12.9 12.6 14.0 16.0 18.0 21.0 23.0 25.3

Oman 12.2 12.0 12.6 13.0 13.7 14.5 16.0 16.5

Qatar 19.6 20.5 21.0 21.5 22.0 22.5 23.0 23.6

Saudi Arabia 73.5 75.9 78.9 82.1 83.9 91.9 100.5 108.1

Turkey 30.5 35.1 35.5 36.5 40.0 43.0 45.5 47.8

UAE 41.7 43.2 48.0 49.0 51.0 54.6 58.7 63.1

BMI universe 317.4 330.3 350.6 363.3 379.1 407.6 439.7 465.5

Other ME 35.0 35.3 35.3 37.1 38.9 40.9 42.9 45.1

Regional total 352.4 365.6 386.0 400.4 418.1 448.5 482.6 510.6

e/f = estimate/forecast. Historical data: BP Statistical Review of World Energy, June 2008/BMI. All forecasts: BMI.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 19

Table: Middle East Gas Production (bcm)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Bahrain 11.1 11.5 10.6 10.0 10.0 11.0 11.0 13.0

Iran 109.0 112.0 130.0 135.0 142.0 155.0 165.0 190.0

Iraq 3.5 4.0 5.0 8.0 10.0 13.0 15.0 17.0

Israel 5.0 6.0 7.0 7.0 7.0 7.0 7.0 7.0

Kuwait 12.9 12.6 14.1 14.3 14.5 16.2 19.9 20.6

Oman 23.7 24.1 27.0 30.0 30.0 30.0 33.0 35.0

Qatar 50.7 59.8 70.0 88.0 110.0 125.0 133.0 135.0

Saudi Arabia 73.5 75.9 78.9 82.1 83.9 91.9 100.5 108.1

Turkey na na na na na na na na

UAE 47.4 49.2 58.0 63.0 70.0 80.0 85.0 90.0

BMI universe 336.8 355.1 400.6 437.4 477.4 529.0 569.4 615.7

Other ME 5.6 5.5 6.0 6.6 7.3 8.0 8.8 9.7

Regional total 342.4 360.6 406.7 444.0 484.7 537.1 578.3 625.4

e/f = estimate/forecast. na = not applicable. Historical data: BP Statistical Review of World Energy, June 2008/BMI. Forecasts: BMI.

In terms of natural gas, the region in 2008 consumed an estimated 386bcm, with demand of 511bcm

targeted for 2013, representing 32.3% growth. Production of an estimated 407bcm in 2008 should reach

625bcm in 2013 (+53.8%), which implies net exports rising to 115bcm by the end of the period. The

UAE in 2008 consumed an estimated 12.44% of the region’s gas, with its market share forecast at 12.35%

by 2013. It contributed an estimated 14.26% to 2008 regional gas production and, by 2013, will account

for 14.39% of supply.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 20

Liquefied Natural Gas

Table: Middle East LNG Exports/(Imports) (bcm)

Country 2006 2007 2008e 2009f 2010f 2011f 2012f 2013f

Iran na na na na na na na 10.0

Oman 11.5 12.2 13.0 15.5 15.0 14.0 16.0 17.0

Qatar 31.0 38.5 43.0 49.5 69.5 82.5 90.0 91.4

Turkey (5.7) (6.0) (6.5) (6.5) (6.5) (6.5) (6.5) (12.0)

UAE 7.1 7.6 8.0 8.0 8.0 9.0 10.0 10.0

Regional total 43.9 52.3 57.5 66.5 86.0 99.0 109.5 116.4

e/f = estimate/forecast. na = not applicable. Historical data: BP Statistical Review of World Energy, June 2008/BMI. All forecasts: BMI.

The leading LNG exporter by 2013 will be Qatar (+112.6% from 2008). Iran has significant longer-term

gas export potential, although the first volumes have yet to flow. The country is signing gas supply deals,

which point to rising LNG sales from 2013. Turkey is set to be a key gas importer, although LNG

volumes will be modest as the country raises pipeline supplies from the likes of Azerbaijan and Iran.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 21

Business Environment Ranking

Middle East Region

This updated regional Business Environment scoring system incorporates many more industry-specific

elements and a more sophisticated approach to political and economic risk assessment. The enlarged

scoring matrix is broken down into Upstream and Downstream segments, providing a more detailed

analysis of the growth outlook and market conditions for both major elements of the oil and gas industry.

The Middle East region comprises 10 countries, including all key Gulf states. State influence remains

very high, with limited privatisation activity. Oil production growth for the period to 2013 ranges from a

negative 34% for Turkey (where absolute numbers are already small) to a positive 54% in Iraq, while oil

demand growth ranges from 6% to 46% across the region. Increases in gas output range from zero to

240% across the region over the period to 2013. The spread of gas demand growth estimates ranges from

10% to 64%. The political and economic environment varies, depending partly on market maturity and

specific factors such as the uncertainty in Iraq and the nuclear-inspired stand-off in Iran.

Composite Scores

The UAE and Saudi Arabia now occupy the top and bottom slots of the regional league table. The

composite Upstream and Downstream combined scores are 62 points and 45 points respectively, out of a

possible 100. Qatar now shares first place with the UAE, having as expected retaken Turkey. Turkey

remains well clear of the midfield pack, which comprises Iraq, Israel, Oman and Iran. Iraq is clearly

capable of moving much higher once licensing terms have been established and IOC activity picks up.

Kuwait has remained ahead of Saudi Arabia near the foot of the table. Bahrain has eased away from the

bottom slot, but still appears vulnerable.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 22

Table: Regional Upstream Business Environment Rating

Limits of Potential Returns Risks to the Realisation of

Potential Returns

Upstream

Market Country

Structure Limits Industry

Risks Country

Risk Risks Upstream

Rating Rank

Qatar 70 85 74 65 78 69 72 1

UAE 61 80 66 70 80 74 68 2

Iraq 90 35 76 30 14 24 61 3

Turkey 26 90 42 85 61 77 53 4

Iran 69 35 60 20 53 31 52 5

Oman 26 55 33 90 80 86 49 6

Israel 16 75 31 90 77 85 47 7=

Bahrain 21 60 31 85 81 84 47 7=

Kuwait 63 15 51 10 84 36 46 9

Saudi Arabia 56 10 45 10 67 30 40 10

Scores are out of 100 for all categories, with 100 the best. The Upstream Business Environment Rating is the principal rating. It comprises two sub-ratings 'Limits of potential returns' and 'Risks to realisation of returns', which have a 70% and 30% weighting, respectively. In turn, the 'Limits' rating comprises 'Upstream market' and 'Country structure', which have a 75% and 25% weighting, respectively. They are based on the oil and gas resource base/growth outlook and sector maturity (Upstream) and the broader industry competitive environment (Country). The 'Risks' rating comprises 'Industry risks' and 'Country risk', which have a 65% and 35% weighting, respectively, and are based on a subjective evaluation of licensing terms and liberalisation (Industry) and the industry's broader country risk exposure (Country), which is based on BMI's proprietary Country Risk Ratings. The ratings structure is aligned across all the industries for which BMI provides Business Environment Ratings, and is designed to enable clients to consider each rating individually or as a composite. For a list of the data/indicators used, please consult the Methodology section at the end of the report. Source: BMI

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 23

Table: Regional Downstream Business Environment Rating

Limits of Potential Returns Risks to the Realisation of

Potential Returns

Downstream

Market Country

Structure Limits Industry

Risks Country

Risk Risks Downstream

Rating Rank

Turkey 47 88 57 80 51 69 60 1

UAE 58 46 55 50 72 59 56 2

Israel 33 60 40 100 69 87 54 3

Oman 48 42 46 60 73 65 52 4

Qatar 62 32 55 20 80 44 51 5

Saudi Arabia 61 48 58 10 67 33 50 6

Bahrain 41 48 43 60 71 64 49 7=

Iran 61 48 58 10 58 29 49 7=

Kuwait 52 46 51 15 83 42 48 9

Iraq 56 40 52 10 31 18 42 10

Scores are out of 100 for all categories, with 100 the best. The Downstream Business Environment Rating is the principal rating. It comprises two sub-ratings 'Limits of potential returns' and 'Risks to realisation of returns', which have a 70% and 30% weighting, respectively. In turn, the 'Limits' rating comprises 'Downstream market' and 'Country structure', which have a 75% and 25% weighting, respectively. They are based on the downstream refining capacity/product growth outlook/import dependence (Downstream) and the broader socio-demographic and economic context (Country). The 'Risks' rating comprises 'Industry risks' and 'Country risk', which have a 60% and 40% weighting, respectively, and are based on a subjective evaluation of regulation and liberalisation (Industry) and the industry's broader country risk exposure (Country), which is based on BMI's proprietary Country Risk Ratings. The ratings structure is aligned across all the industries for which BMI provides Business Environment Ratings, and is designed to enable clients to consider each rating individually or as a composite. For a list of the data/indicators used, please consult the Methodology section at the end of the report. Source: BMI

Upstream Scores

Qatar and Saudi Arabia remain the best and worst performers in this segment, showing that the overall

pecking order is quite different to that for combined scores. The UAE is a comfortable second, itself

having a useful seven-point lead over Iraq. However, Iraq has the long-term potential to overtake the

UAE. Turkey, Iran and Oman vie for the middle ground, with Iran having the greatest potential to break

free if the risk outlook improves. The foot of the table is dominated by Bahrain, Kuwait and Saudi Arabia,

in spite of the epic hydrocarbon resources of two of these state-dominated laggards. Saudi has

accumulated less than 60% of the points allocated to Qatar.

Downstream Scores

Turkey and Iraq still bracket the remaining eight ME states in the Downstream rankings, with the former

driven by the size of the fuels market, privatisation moves and the competitive landscape, plus a

reasonable Country Risk rating. Israel has slipped back behind the UAE, in spite of its privatised and

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 24

deregulated oil market. Oman is now only one point clear of Qatar in fourth place, with the latter under

long-term threat from Saudi Arabia below. There is currently little to choose between Bahrain and Iran,

although either could ultimately be displaced by Kuwait.

UAE Upstream Rating – Overview

UAE is ranked a relatively close second place in BMI’s updated Upstream Business Environment rating,

thanks largely to its significant oil and gas resource base, and investor-friendly climate. It stands seven

points clear of Iraq, so appears secure at least over the medium term. It is unlikely, however, to mount a

near-term challenge on Qatar, four points above it. UAE’s score reflects the country’s gas reserves, high

RPR, plus non-state competition, established licensing framework and generally encouraging country risk

factors.

UAE Upstream Rating – Potential Returns

Upstream Market: On the basis of upstream data alone, UAE ranks fifth, just behind Kuwait, in the ME

region. The country ranks fifth and fourth respectively in terms of proven oil and gas reserves. Its oil and

gas production growth outlook are third and fourth, while the oil and gas RPR are third and fifth

respectively.

Country Structure: Influencing UAE’s third place in the ‘Limits to Potential Returns’ section is the

third-placed country structure, behind Qatar. UAE ranks third by the number of non-state operators in the

upstream sector, and equal third in terms of state ownership of assets.

UAE Upstream Rating – Risks to Potential Returns

Industry Risks: UAE is ranked fifth in the ‘Risks to Realisation of Potential Returns’ section of our

ratings, behind Turkey. Its fifth position for ‘Industry Risks’ is due to a joint first-placed licensing

environment and fifth-placed privatisation trend.

Country Risks: Its broader Country Risk environment is more impressive, ranking UAE equal third with

Oman. The best score is for long-term policy continuity, while corruption fares relatively well. Would-be

investors are also faced with respectable scores for physical infrastructure and rule of law.

UAE Downstream Rating – Overview

The UAE is well up the league table in BMI’s Downstream Business Environment rating, with several

high scores and further progress up the rankings possible over the longer term. It is ranked second behind

only Turkey, thanks largely to high scores for oil and gas demand, refining capacity expansion, and

nominal GDP.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 25

UAE Downstream Rating – Potential Returns

Downstream Market: On the basis of downstream data alone, the UAE ranks fourth among the region’s

10 countries, behind Iraq. This score reflects the region’s fifth-ranked refining capacity and oil demand,

third-placed gas consumption and third-placed refining capacity expansion plans.

Country Structure: UAE ranks equal fourth with Qatar in terms of the ‘Limits to Potential Returns’

section, although its Country Structure holds equal sixth place in the region, alongside Kuwait.

Population and nominal GDP rank the country sixth and fourth respectively, while growth in GDP per

capita is the third-highest. State ownership of assets is ranked equal fourth.

UAE Downstream Rating – Risks to Potential Returns

Industry Risks: In the ‘Risks to Realisation of Potential Returns’ section of our ratings, UAE is ranked

fifth, behind Bahrain. Its fifth place for ‘Industry Risks’ reflects the fifth-placed regulatory regime and

fifth-ranked score for privatisation of government-held assets.

Country Risks: Its broader Country Risk environment is good, ranked fourth just behind Oman. The best

and optimum score is for short-term economic external risk, followed closely by short-term policy

continuity. High scores are awarded for rule of law, short-term economic growth risk and physical

infrastructure. Operational risks for private companies are raised only by the state’s legal framework.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 26

Business Environment

Legal Framework

The UAE legal system is based on civil law concepts and common law principles – such as adopting

previous court judgments as legal precedent – are usually not recognised.

The legal system follows the federal structure of the UAE, but the constitution acknowledges the right of

individual emirates to opt out of the federal court system, which Dubai and Ras al-Khaimah have done.

These two emirates have their own court systems, which are not subject to the federal Supreme Court.

There are three main branches within the court structure: civil, criminal and shari’a law. The court

structure comprises the following:

The Court of First Instance – which includes the Civil Court, the Criminal Court and the shari’a Court.

This hears all claims, including commercial matters. Commercial disputes involving foreign parties tend

to come before the civil courts, although shari’a law is applicable in all kinds of cases involving both

Muslims and non-Muslims.

The Court of Appeal.

The Court of Cassation – whose judgment is final. Dubai has its own Court of Cassation.

The 1971 constitution established the independence of judiciary. However, in practice, independence is

minimal as all judges are appointed by the government. The five judges of the Federal Supreme Court, for

example, are appointed by the Supreme Council of Rulers, while other judges are appointed by the

Ministry of Justice. Furthermore, judges’ decisions are subject to review by the executive, meaning that

any politically unpopular rulings can be overturned.

Commercial disputes involving foreign companies are usually heard before the federal civil courts, with a

panel of three judges presiding. All cases involving banks and financial institutions must be heard by civil

courts. In Abu Dhabi, all non-arbitration commercial disputes are first taken to the Abu Dhabi

Conciliation Department and if the parties cannot settle, they start legal proceedings in the court of first

instance.

With the UAE now firmly established as a regional business hub, arbitration is now the preferred mode of

dispute resolution involving foreign companies. Yet dispute resolution can be an arduous and uncertain

process and enforcing arbitration judgments can be difficult since court certification is also required. The

judicial process can sometimes take years to conclude. Some companies are reportedly unwilling to resort

to arbitration out of concern that it could affect their future business opportunities in the UAE.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 27

In 2006, the UAE ratified the 1958 New York Convention on the Recognition and Enforcement of

Foreign Arbitral Awards – one of the last countries in the region to become a signatory to the convention.

This enables UAE courts to enforce arbitration decisions made in a foreign country. However, the federal

Supreme Court says that a foreign arbitration clause in a registered commercial agency agreement is

invalid, since the Commercial Agency Law states that UAE courts have jurisdiction over commercial

agency disputes. Nevertheless, smoother arbitration should ensure that disputes are handled more quickly

than in the court system.

Although investment laws and regulations are undergoing a period of evolution and becoming more

conducive to foreign investment, at present the regulatory and legal framework still favours local over

foreign nationals. Foreign ownership of land and stocks is restricted, although specific rules vary between

emirates. Dubai and Abu Dhabi have opened up some areas for freehold and leasehold property

investments. Ras al-Khaimah also offers freehold land to offshore companies in designated areas. In Abu

Dhabi, non-GCC nationals can own buildings in certain investment areas but cannot own the land.

However, investors should be aware of impediments to the exercise of rights over property. In Dubai, for

example, foreign owners of ‘freeholds’ cannot register titles with the Dubai Land Department, which

would allow them access to the full range of legal protections and transactions that property ownership

requires. Freeholds are a new phenomenon in Dubai and very few court precedents exist, so there is still

considerable ambiguity concerning property rights and inheritance laws.

The UAE is a regional leader in the protection of intellectual property rights (IPR), with improving

enforcement of copyright, trademark, and patent laws. Anecdotal evidence suggests that the federal

government is enforcing these laws, which were passed in 2002. The rate of software piracy in the UAE

is regarded as one of the lowest in the Middle East. However, enforcement of anti-piracy measures can

vary between emirates, with Dubai seen as the best performer. More could be done in other emirates,

while the UAE still remains a major centre for the trans-shipment of counterfeit goods.

Corruption is not endemic to UAE business life and the country ranks 35th out of 180 states in

Transparency International’s 2008 Corruption Perception Index, second only to Qatar in the Middle East.

Nevertheless, large state-owned enterprises continue to control large swathes of the economy and are not

subject to extensive scrutiny. Furthermore, those convicted of corruption have often escaped effective

punishment – in 2001, the former head of the Dubai Customs and Port Authority was convicted of

corruption and embezzlement and sentenced to 27 years in prison, but was quickly pardoned by the Dubai

government and released. A law passed in 2005 now stipulates minimum sentencing requirements for

public officials found guilty of corruption.

Under its WTO membership obligations, the UAE has undertaken measures to reduce red tape

surrounding the foreign investment approval process. Investors are now exempt from obtaining a Ministry

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 28

of Labour card in addition to an Immigration Department visa and investors no longer need to appear in

person to inquire about the status of business applications; a new automated service allows them to

receive information about their business licences over the telephone.

Infrastructure

The UAE has around 1,000km of paved roads linking all the emirates, mainly along the coast. The

motorway between Abu Dhabi and the Al-Ain oasis has been upgraded and sections of the road linking

Abu Dhabi and Dubai are also being upgraded. Road is the major means of transport between the

emirates given that there is no railway system.

However, much of the UAE’s international trade is done by sea and all seven emirates have modern port

facilities. Dubai dominates the cargo and re-export markets thanks to the size of its two ports, Port Rashid

and Jebel Ali Port. The former is one of the busiest ports in the Gulf region and has 35 berths, while the

latter has 63 berths and is part of a free economic zone. Abu Dhabi’s Mina Zayed port has been upgraded

to 21 deepwater berths, which has helped eliminate waiting times. All three aforementioned ports have

warehouse facilities that provide storage for imports, with no storage charges for the first 20 days.

Other emirates are seeking a share of the re-export business, although their facilities are currently smaller

than those available in Dubai or Abu Dhabi. Sharjah is the only emirate with ports on both the Persian

Gulf and the Indian Ocean, which offers it significant advantages; international cargo ships can save

around 24 hours in a trip from East Asia to Europe by not having to join the queue to enter the busy Gulf.

Avoiding the Gulf also results in significant insurance savings.

The UAE is home to two major airline carriers; Gulf Air (owned jointly by Abu Dhabi, Bahrain, Oman

and Qatar) and Emirates Air (owned by Dubai). The latter flies to around 80 destinations across Europe,

the Middle East, Australia, Africa and the Indian subcontinent.

Mobile phone use in the UAE is among the highest in the Middle East and indeed the world, with services

provided by two carriers: Etisalat and newcomer Du. Fixed-line services are less popular and although it

is now gaining in popularity – broadband penetration grew from under 3% in 2005 to 5.1% in 2006 –

broadband networks are not as developed as in some neighbouring states, such as Bahrain. Customers

have complained of high prices and poor service quality, although this should improve as Du expands its

services nationwide (the newcomer is currently present only in the free zones).

Labour Force

The total population exceeded 5mn in 2007. A census has been carried out which will determine the

actual size of the labour force, but estimates put it at about 60% of the total population.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 29

Exact data on the number of foreign workers in the UAE is not available from the federal government, but

it is estimated that more than 80% of the UAE workforce is expatriate, with as much as 98% of private

sector workers thought to be non-UAE nationals. Most UAE nationals seek employment opportunities in

the public sector, due to the higher salaries, greater benefits, shorter working hours and job security on

offer. The construction sector is a major employer of foreign labour, mainly from the Indian subcontinent.

In recent years, the federal and emirate governments have implemented a number of measures to increase

the cost of hiring expatriate workers, as part of an effort to bring more UAE nationals into the private

sector. ‘Emiratisation’ of the UAE workforce is a government objective, though less rigorously enforced

than in other Gulf States. Compulsory hiring of nationals has been limited to sectors such as banking

(which has a 4% quota), insurance (5%) and trade (2% for companies employing 50 workers or more). In

2006, the government added Emiratisation requirements that all secretaries and PR officers must also be

UAE nationals.

The government continues to try and regulate the labour market, in mid-2007 granting a three-month

amnesty to illegal expatriate workers and their employers, who had either to adjust their status or to leave

the country without incurring penalties. By mid-July, 74,800 people had applied for the amnesty. Calls for

reform of labour laws, including the right to create trade unions, are growing louder. The US insisted on

this during negotiations over its free trade agreement with the UAE. The current law does not specifically

give workers the right to engage in collective bargaining neither do labour laws cover government

employees, domestic servants, and agricultural workers.

Industrial unrest is growing, particularly amongst construction workers, the vast majority of whom come

from the Indian subcontinent. In November 2007, nearly 40,000 labourers working for the country’s

largest construction firm Arabtec went on strike, in a high-profile protest. Whereas previous protests had

called for better living conditions, the most recent wave of unrest has centred on the falling real value of

wages, in light of high UAE inflation and the falling value of the dirham against Asian currencies.

In the wake of those protests, the labour ministry has drawn up new laws, which should come into force

in early 2008. These include the mandatory use of electronic payment systems for unskilled workers,

increased fines for companies found to be employing illegal workers, and compulsory health cover, which

is already in place in Abu Dhabi but will be extended to the other emirates. The ministry has also drawn

up a series of standards for worker accommodation to cover all industry sectors. It is unclear whether the

new rules will extend to domestic servants and agricultural workers. The former currently face

considerable difficulty in negotiating employment contracts because mandatory requirements in the

labour law do not apply to them.

Nevertheless, the minister of labour, Dr Ali bin Abdullah al-Ka’abi, has ruled out any possibility of

expatriates being awarded citizenship, no matter how long they have worked in the emirates or their level

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 30

of expertise in their field. Furthermore, the UAE is one of the main supporters of the 3+3 labour law that

will be discussed by the GCC in 2008. The law proposes that expatriates’ term of residency within any

GCC country be limited to three years, with a possible three-year extension.

Foreign Investment Policy

The UAE’s investment climate is becoming more clement for foreign direct investors: the federal

government, led by Abu Dhabi, has made significant headway in the past five years in increasing the role

of the private sector. Yet the overall legal framework continues to favour local over foreign investors – a

fact that partly reflects the benign macro environment in light of the country’s substantial oil revenue

windfall. This has endowed local and regional Gulf investors with substantial liquidity, discouraging the

search for new FDI sources from outside the region.

Change may be on the way. In June 2008, the government said a new companies’ law would open some

areas within the services sector to full foreign ownership while also allowing greater foreign participation

in other areas – up to 100% – such as financial services. This is likely to be enacted in 2008. At present,

foreign shareholders may only hold up to a 49% equity interest in limited liability companies; indeed, all

companies established in the UAE are required to have a minimum of 51% national ownership, although

profits may be divided differently. In the insurance sector, companies must be 75%-owned by a UAE

national or 100% by a UAE corporation.

Full foreign ownership is generally only allowed within economic free zones. In order to do business in

the UAE outside the free zones, a foreign business must usually have a UAE national sponsor, agent or

distributor which, once chosen, has exclusive rights. In order to bid for federal projects, a contractor must

be at least 51%-owned by UAE nationals, and tenders must be accompanied by a bid bond – an

unconditional bank guarantee for 5% of the value of the bid. However, government tendering practices do

not live up to international standards and re-tendering is common.

On the positive side, the absence of income tax compensates for the restrictive investment environment.

FDI figures remain difficult to verify, though data from UNCTAD claims that FDI inflows totalled

US$8.4bn in 2006, with much of it attracted to the booming real estate and construction sectors. The UAE

is now the Gulf’s second biggest FDI destination after Saudi Arabia. Perhaps even more impressive,

given the massive investments made by UAE firms and individuals outside the emirates, the country has

more inward FDI stock by foreigners than nationals’ outward FDI stock in foreign countries. According

to a Dubai Chamber of Commerce & Industry report in 2007, during 1997-2006, the average net inward

FDI flows as percentage of gross fixed capital formation was 17% for UAE.

Until now, the main destinations for FDI have been ICT and software, tourism and textiles. The main

sources of FDI are the UK, the US and India.

United Arab Emirates Oil & Gas Report Q3 2009

© Business Monitor International Ltd Page 31

Tax Regime

The UAE’s substantial hydrocarbons resource revenues means government has no pressing need to raise

income via direct taxes.

Only banks and oil companies pay corporate tax, at a rate of 50% (55% in Dubai) for oil companies. Oil

companies also pay royalties on oil and gas they produce. Net taxable income of foreign banks is subject

to tax at a flat rate of 20%, implemented in Abu Dhabi and Dubai. Alongside all the other benefits

enjoyed by companies operating in the free trade zones, there is no corporate tax for 15 years, renewable

for an additional 15 years.

There is no income tax on individuals resident in the UAE. There is no VAT in the UAE, but the federal

government, under the advice of the IMF, is discussing the introduction of a VAT system. This is unlikely

to be introduced in the near term, however. There are no withholding or capital taxes. Business properties

pay a municipal tax set at 10% of annual rental value. Double taxation agreements exist with France,

Pakistan, Poland, Turkey, China, Romania, Italy, Egypt, Germany, Singapore, Malaysia, Indonesia and

India.

Security Risk

While there remains a generalised threat of terrorism throughout the Middle East, the UAE has not yet