Embed Size (px)

Citation preview

PUBLIC EXPOSE TAHUNAN

PT INTAN BARUPRANA FINANCE TBK

Auditorium 5th Floor, INTA HQ Building

Jakarta, 27 Oktober 2015

VISION

MISSION

STRATEGY

To be Tier 1 Finance Company in the financial industry

in Indonesia

To create job and prosperity, and build and grow with

aspiring local entrepreneurs

To have Capital Rp. 1 trillion or higher and rating single A or better.

Through upholding Good Corporate Governance, respecting all

stakeholders, practicing highest professionalism and having honest

character.

Key Company HighlightsVision, Mission, Strategy

1991 2010 2014

\

2003 2013

On September 4, 1991,

the Company was

established with a name

PT Intan Baruprana

Finance

The Company’s business

activities were expanded,

namely moving into

financing based on syariah

principles on April 8, 2010

The Company listed (go public) its

shares on the Indonesian Stock

Exchange with code:IBFN on

December 22, 2014

On February 14, 2003,

PT Inta Finance and

Employee Cooperative

of PT Intraco Penta, Tbk

become shareholders

(acquired by INTA)

On August 15, 2013,

Phillip Asia Pacific

Opportunity Fund, Ltd

became a shareholder of

the Company by holding

9.71% shares.

Key Company HighlightsMilestones

Overview of the CompanyAwards and Achievements

September 2011

The 12th best

multifinance

company (Total

Assets between

Rp500bn – Rp1tn)

October 2012

The 3rd best

multifinance

company (Total

Assets between

Rp1tn – Rp2tn)

Investor Magazine Awards Infobank Magazine Awards

“The company is well recognized in the Indonesian multifinance sector, having been given

numerous awards from Investor and Infobank magazines.”

September 2013

The 5th best

multifinance

company (Total

Assets between

Rp1tn – Rp2tn)

August 2011

Rated “Very Good”

and ranked 35th

(Assets category

between Rp 100

billion – Rp 1 trillion)

August 2012

Rated “Very Good”

and ranked 17th

(Assets category

above Rp 1 trillion)

August 2013

Rated “Very Good”

and ranked 37th

(Assets category

above Rp 1 trillion)

August 2014

Rated “Very Good” and

ranked 9th

(Assets category above

Rp 1 trillion)

September 2015

The 2nd best

multifinance company

(Total Assets between

Rp2tn – Rp5tn)

August 2015

Rated “Very Good” and

ranked 8th

(Assets category between

Rp1tn – 5tn)

October 2014

The 9th best

multifinance

company (Total

Assets between

Rp2tn – Rp5tn)

Business Strategy

• Prioritize to provide financing services for INTA customers

Maintaining captive market

• Provide financing for non-INTA products

• Target to have 50:50 captive and non-captive portfolio in the near future

Expanding the non-captive market

• Understand client’s needs

• Knowing client’s business

• Assess payment capabilities

Improving the assets quality

• Diversify portfolio to construction & infrastructure, agribusiness, transportation (land,sea), oil & gas, hospitality, healthcare and various sector

Penetrating new industry sectors

• Establish a joint-financing /channeling scheme

• issue MTN, BondsLowering cost of fund

• Provide tailor made financing

• Have skilled and experienced personnel

• Have depth knowledge in heavy equipments industry

Focusing on the customer

FinancialRevenue

Revenue from FY10A – FY14A; Sept 14UA – 15UA (in Rp mn)

Source: AFS 2010, 2011, 2012, 2013 ,2014 & UAFS Sept 2014, 2015

47.784

111.628

173.443

258.738

398.420

278.379

352.224

FY10A FY11A FY12A FY13A FY14A Sept14 Sept15

5.866

17.555

24.721

31.825

60.545

50.361 47.267

FY10A FY11A FY12A FY13A FY14A Sept14UA Sept15UA

12,28%

15,73%14,25%

12,30%

15,20%

18,09%

13,42%

FY10A FY11A FY12A FY13A FY14A Sept14UA Sept15UA

Net Profit Margin FY10A – FY14A; Sept 14UA – 15UA (%)

Net Income FY10A – FY14A; Sept 14UA – 15UA (in Rp Mn)

FinancialNet Income

FinancialNew Booking

New Booking from FY10 – FY14; Sept 14– 15 (in Rp mn)

Source: FS 2010, 2011, 2012, 2013 ,2014 & FS Sept 2014, 2015

440.983

985.244 1.041.619

997.275

1.071.313

715.798

847.707

Dec 10 Dec 11 Dec 12 Dec 13 Dec 14 Sept 14 Sept 15

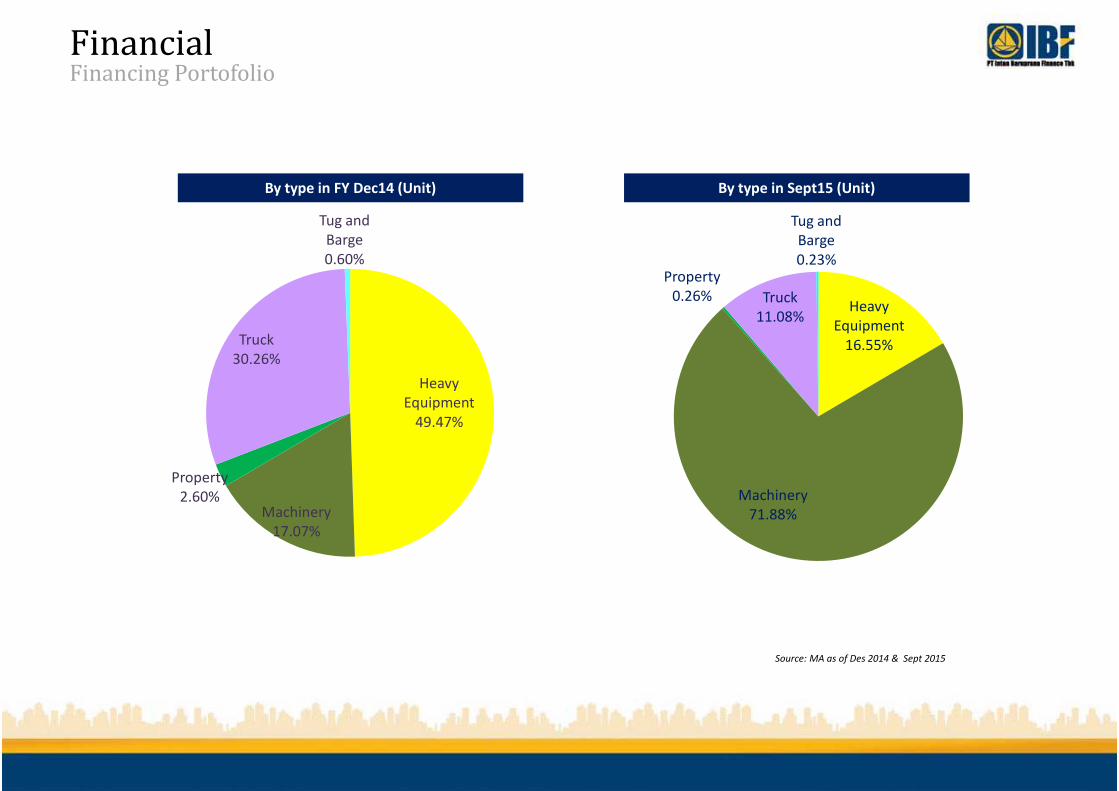

FinancialFinancing Portofolio

By type in FY Dec14 (Value) By type in Sept15 (Value)

Heavy

Equipment

55.83%

Machinery

14.22%

Property

0.34%

Truck

19.62%

Tug and

Barge

8.02%

Others

1.96%

Heavy

Equipment

46.33%

Machinery

25.59%

Property

0.16%

Truck

17.66%

Tug and

Barge

7.65%

Others

2.61%

Source: MA as of Des 2014 & Sept 2015

Source: MA as of Des 2014 & Sept 2015

By type in FY Dec14 (Unit) By type in Sept15 (Unit)

Heavy

Equipment

49.47%

Machinery

17.07%

Property

2.60%

Truck

30.26%

Tug and

Barge

0.60%

Heavy

Equipment

16.55%

Machinery

71.88%

Property

0.26% Truck

11.08%

Tug and

Barge

0.23%

FinancialFinancing Portofolio

Source: MA as of Des 2014 & Sept 2015

By sector industry in Sept15 (Value)

Coal Mining

43%

Nickel

3%Gold

2%Bauxite

2%

Oil &

Gas

9%Quarry

2%

Agribusiness

4%

Transport &

Logistic

26%

Construction

6%

Other

3%

Coal Mining

40%

Nickel

3%Gold

1%Bauxite

0%

Logam

1%

Oil & Gas

11%Quarry

2%

Agribusiness

3%

Transport &

Logistic

22%

Construction

6%

Other

11%

By sector industry in FY Dec14 (Value)

FinancialFinancing Portofolio

Source: MA as of Des 2014 & Sept 2015

By sector industry in FY Dec14 (Unit) By sector industry in Sept15 (Unit)

Coal Mining

29%

Nickel

4%

Gold

1%Bauxite

2%

Oil & Gas

12%

Quarry

1%

Agribusiness

9%

Transport &

Logistic

31%

Construction

8%

Other

3%

Coal Mining

10%

Nickel

1%

Gold

1%Bauxite

0%Logam

0%

Oil & Gas

22%

Quarry

1%Agribusiness

3%Transport &

Logistic

10%

Construction

3%

Other

49%

FinancialFinancing Portofolio

FinancialFunding

Outstanding loans per bank & financial institutions Bank loans+Financial institutions+MTN at Dec14A & Sept15UA

Conventional vs Sharia

IDR vs USD

Currency: Rp bn Dec14A Sept15UA

Bank Artha Graha 67 29

BPD Jabar dan Banten 19 1

BNI 292 243

Bank SBI Indonesia 25 48

Bank MNC (ICB Bumiputera) 96 163

Bank Mestika 74 75

Indonesia Eximbank - 158

Total Conventional Loans 581 717

Unamortized transaction cost (2) (2)

BSM 159 76

Bank Muamalat Indonesia 312 328

BNI Syariah 189 185

Bank Maybank Syariah Indonesia 78 91

Bank Jabar Banten Syariah 37 10

BCA Syariah 17 7

Bank Bukopin Syariah 3 1

Bank Rakyat Indonesia Syariah 3 2

ICD (The Islamic Corp. For The

Development Of The Private Sector) - 77

Total Sharia Loans 798 777

Bank loans & financial institutions 1.377 1.492

MTN (Medium Terms Notes) 300 300

Convent

52%Sharia

48%

IDR 79%

USD 21%

Convent

57%Sharia

43%

IDR;

82%

USD;

18%

Source: AFS 2010, 2011, 2012, 2013, 2014 & Sept 2015UA (ROA & ROE Sept 2015UA disetahunkan)

Assets (Rp billion) Equity (Rp billion)

ROA & ROE (%) Gearing Ratio (%)

295%

408%

557%

336%

286% 289%

Dec10A Dec11A Dec12A Dec13A Des14A Sept15UA

120

187 212

394

565 612

Dec 10A Dec 11A Dec 12A Dec 13A Dec 14A Sept 15UA

570

1.378

1.795

2.355

3.040

3.576

Dec 10A Dec 11A Dec 12A Dec 13A Dec 14A Sept 15UA

1,03% 1,27% 1,38% 1,35%1,99% 1,78%

4,91%

9,38%

11,69%

8,08%

10,73%10,04%

Dec10A Dec11A Dec12A Dec13A Dec14A Sept15UA

ROA

ROE

FinancialAssets, Equity & Ratios

Opportunities and Potentials

� Huge and growing middle class

� Very young population

� Infrastructure is the main theme of the current

government namely toll road, power plant,

airport, and seaport. These are the areas where

leasing can contribute and play big role.

� Healthcare and alternative energy.

Challenges

� Growth is dependent and limited by availability of

bank lines

� Investment grade is BBB- but in practice investors

look for A flat

� Capital market is robust but favor the big names,

big sharehlders, and big market cap

Q & A

THANK YOU

![Berkilau di Usia Intan TAHUNAN LAPORAN 2014 · yang mengutamakan penggunaan obat generik [OGB]—Perseroan berhasil membukukan pertumbuhan Penjualan Bersih 10,8%, jauh di atas pertumbuhan](https://img.dokumen.tips/doc/110x75/5e2651b60e2b6f71072eb733/berkilau-di-usia-intan-tahunan-laporan-yang-mengutamakan-penggunaan-obat-generik.jpg)