Embed Size (px)

Citation preview

PSYCHOLOGY OF IRP PRESENTATION

Script and Training Notes

Trained by:

Marlon Antonio

Lead Mentor

August 24, 2017

Developed by: Jaan Raj I. Barrera

“From the beginning, Presentation has always been my Passion”

~ Marlon Antonio, CEO and President

WHY IS IT VERY IMPORTANT TO UNDERSTAND THE PSYCHOLOGY OF THE PRESENTATION?

If you master the psychology of presentation, 80 – 100% you will close because the presentation is

designed that way. The presentation is based on Architectural presentation – small step by step process

to have the desired result at the end.

This presentation is also based on the Psychology of Selling. Understanding why people buy and why

people don’t buy.

Psychology of Selling: Why people buy and why people don’t buy?

People buy because they want to feel good. The Presentation is designed for your client to feel good. Your

business is to make them feel good professionally. Client also buys into your preparedness, confidence

and beliefs. Do you believe?

People don’t buy because they don’t feel good.

WHAT IS THE RESULT YOU WANT TO ACHIEVE?

Informed Educated Decision for the Client so that they can decide properly.

Responsibility to Save Money. Client who sticks in the plan are becoming financially better than those

who don’t.

WHAT IS THE PURPOSE OF THE PRESENTATION?

To Change their Financial Destiny. When they applied but not settled, nothing changes. If the policy is

settled, there is peace of mind about money. When Clients die, there’s inheritance and the next

generation will be financially better

Are you presenting because of the product or because you have a purpose? Be a purpose-driven Financial

Advisor. Every time you see someone, you have the opportunity to change someone’s financial destiny.

Present only 35-45 minutes (properly controlled presentation) Illustration is not part of the presentation,

it is creating a plan for them. Your clients will be tired of listening to you if more than that. You must time

yourself and practice. If more than one hour of presentation, then you talk too much. Remember… you

have 2 Ears and 1 mouth.

“Greatway is created for people to become a better person. Always think good, say good and do good

all the time.”

~ Marlon Antonio, CEO and President

HOW DO YOU KNOW IF YOU HAVE AN AMAZING PRESENTATION?

When clients call you back or text you, “when do I get approved? They are excited to save money and they

keep texting or calling you back.

Sometimes when you are not done presenting, they already want to apply.

WHAT TO DO BEFORE PRESENTATION?

PRACTICE

Perfect practice makes perfect results. The more you practice, the more you gain confidence. Remember

that your client buys into your confidence. Nobody started at 80 – 100% closing rate, but if you were

guided properly and improve 1% everyday, overtime you become better. You practice and practice and

please do not practice in front of the client.

FOLLOW-UP

Make sure they are in the house. Call and text them that you are on your way. Never call or text them that

will give them reason to cancel.

PRAY

In this business you need a partner, you cannot do this on your own. Your partner is God. Volunteer

yourself to help more and more of His people. Volunteer yourself to glorify and serve God.

On your way to their house, pray… “If God is with me, who is against me?” Even during presentation pray

in the silence of your heart.. “God please help me help this people understand.”

RITUALS

You must be in the zone when you present! Always prepare your state and make this in the highest level.

Make sure you are excited and feel good through rituals (music, chocolates etc.) Always feel good when

you are going to an appointment, never present if you have an argument with your spouse or children.

When you leave your home make sure you family is happy.

CREATE A MENTAL MOVIE

You must know exactly what you want and the ending that you want. You have to picture out the end

result of the presentation. When you feel great and think about what you want, you attract it.

PREPAREDNESS

Remember that your client buys into your preparedness. Make sure you have the following before

going to your client:

a. Know Your Client (KYC) Form

b. Application forms ( As much as possible bring 10)

c. 6 Step Duplication Process forms

• SAT Program kit

• Prospect list

d. Travel Rewards Program

WHAT TO DO WHEN YOU ARE ON THE DOOR?

Always try to see the goodness of everyone.

Don’t talk about what we do right away, always try to look for an opportunity to praise them, and make

them feel good. Importantly, make them feel good about you, your identity must not be a life insurance

agent.

Find that connection.

Ask where they came from and talk about what’s good about the province. Your client is the star, not you.

A good AGA will help you find someone that you can connect in the office.

If they asked you to eat, please don’t say no. If blessings come to you, don’t refuse it. It’s best to eat a

little bit before you go to your client’s house, so that you’re not full when they offer food and if there’s no

food, you’re not hungry while presenting.

Always think good, say good and do good all the time.

Other companies there are like our brothers and sisters. We have a common goal of helping people. Our

competition is not them, our real competition is the bank. We don't have to compete against anyone.

HOW TO START THE PRESENTATION?

Keep in mind and heart that the presentation is based on a PURPOSE, Change someone’s financial destiny.

Always thank your client for the opportunity of allowing you to share your blessings. The opportunity to

share the information that helped you and your family.

WHERE TO PRESENT?

Always present in the KITCHEN, because this is where most family decisions are made. Don’t present in

the living room because people are relaxed and out of focus. Then properly position yourself in the

kitchen table.

TIPS:

a. Eliminate distractions as much as possible, “is it okay if we turn off the television?”

b. Sit where you believe the head of the family sits. Don’t ask but simply put your bag or jacket.

c. If it’s a couple, make sure you present on both. Find the dominant person and sit beside that

person (it is usually the wife).

d. Properly position your laptop. It’s ok if only one person responds to your questions, as long as

both sees the presentation.

e. Observe their body language.

While talking and thanking your client, this slide

is already in your laptop and is shown to your

client. Before the presentation, start with your

Advisor Story. Your advisor story is your

experience before and during Greatway and if

you share this energy, you excite and intrigue

your client.

Just leave this, never talk anything about this

page. This is like a curtain of a show.

This page will intrigue your client. They’ll be

intrigued with the pictures and once they are

intrigued, you have engaged them.

Again, while presenting, you are praying silently... “God please help me help these people understand”

“Thank you very much for giving me this opportunity to share this information that helped me and my

family”

Q: “Is it okay to ask you questions while I present?”

A good presenter is before you click, you are already talking about it.

Table The Advisor

The couple The dominant person

First question is the most important question:

“Would you like to save more money?”

a. You can control the answer.

b. Make sure that they agree with you.

c. They feel good when they answer “YES!”

d. Most people also feel good if they hear the word “save”

e. This question will prepare you from the last question.

f. What we do is help people save money.

if they don’t answer, keep asking them. They have to say YES.

It is important for me to explain you this “Chinese proverb.”

The Best time to plant a tree was 20 years ago. If you’ve planted 20 years

ago, by now you’ll have a tree.

But what if you’ve never planted? (Wait for their answer)

Right, no tree or nothing to harvest

So the next best time now so that if you’ll plant today, in the future

you’ll have a tree. What you sow is what you reap, you have to plant so

you can harvest.

People tend to forget about words, but remember pictures. Always create a mental image in your client’s

mind. Connect with pictures, not language. Don’t use language that are complicated.

It’s true that the more you attend training the more technical you can become. When in front of the

client, be simple as possible. People don’t care how much you know, they want to know how much you

care.

It is also important for me to explain this Canadian statistics.

When they say green, say “that’s good, what we are going to do tonight is to show you, where the 9% invest

their money, and where the 53% invest their money. Is that okay with you?”

53% are financially broke

14% are still working

Do you want to be here someday?

These people, love their work and

they’re not poor. Some just realized

that their savings are not enough

that’s why some of them are still

working

Do you want to be here someday?

Only 9% are financially

secure. Imagine if there

are 100 of us here, only 9

are financially secure at

age 65

Where do you want to be in the future?

Don’t show them yet the 24% dead. Ask them first “where do

you want to be in the future” before you show the 24% dead.

When you’ll show them 24% dead, say…

Then 24% are dead at the age of 65.

Don’t talk too much about the 24% and do not focus on life

insurance.

Do you have life insurance?

(The reason why we asked this because we want to know

what company they have so we can offer the right company

for their IRP application)

That’s good, please keep it. You already have that peace of mind

that when something bad happens, you can still protect your family

The purpose of this slide is to remove the insurance mindset and have

the client focused on saving or investing for retirement.

We have a different approach to our clients, we will not approach them as insurance agents.

Our topic for tonight is Lifetime income, but before we talk about let me share how life works

You must make sure you use good quality words so that your client will feel good.

Our topic for tonight is not life insurance, because

you actually have 76% chance of living longer than

65, so instead of life insurance, our topic will be Tax

Free Life-Time Income.

Is it ok to talk about lifetime income?

Let’s imagine we are 30 years old today

Are we young forever?

Eventually we’ll become old,

Is that a good thing or a bad thing?

To us, it’s good, because you didn’t die young

and get to enjoy life.

Would you agree that when we’re

young, we are physically strong?

Are we strong forever?

Eventually we’ll become physically weak

Can you do anything about this?

Would you agree that most young people

today live paycheque to paycheque?

If we save and invest money properly,

someday we will become financially strong

This is how Life works, when we are young we

work hard for our money, but as we grow old

we should stop working hard and our money

should work hard for us

The sad part is at a young age, we are financially weak, and

we work hard and as we grow old still are financially weak.

But according to statistics, only 9%

are financially secure

53% are financially broker, 14% are still working, that

makes 67% of people here in Canada are financially weak.

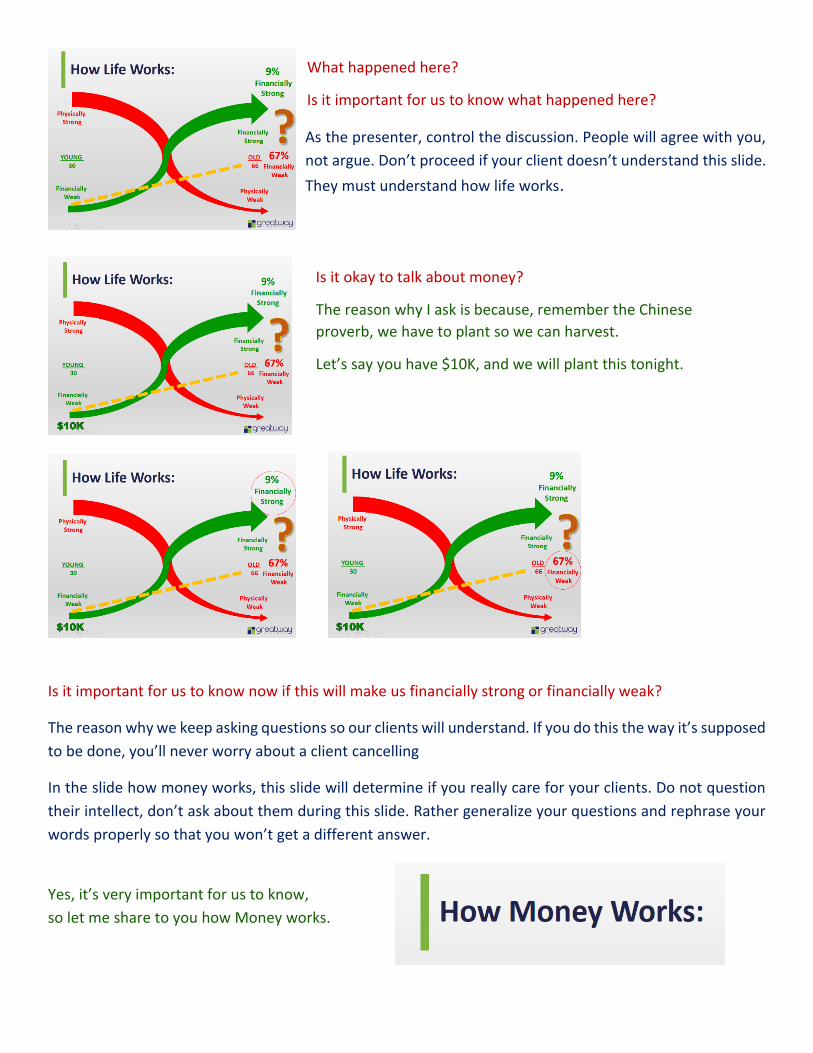

As the presenter, control the discussion. People will agree with you,

not argue. Don’t proceed if your client doesn’t understand this slide.

They must understand how life works.

Is it important for us to know now if this will make us financially strong or financially weak?

The reason why we keep asking questions so our clients will understand. If you do this the way it’s supposed

to be done, you’ll never worry about a client cancelling

In the slide how money works, this slide will determine if you really care for your clients. Do not question

their intellect, don’t ask about them during this slide. Rather generalize your questions and rephrase your

words properly so that you won’t get a different answer.

Yes, it’s very important for us to know,

so let me share to you how Money works.

What happened here?

Is it important for us to know what happened here?

Is it okay to talk about money?

The reason why I ask is because, remember the Chinese

proverb, we have to plant so we can harvest.

Let’s say you have $10K, and we will plant this tonight.

Let’s say this is you and have money. Where do most people put their money?

Someday, the bank will give you back money and that’s good.

How much is the typical interest rate?

The biggest is around 2.00% let’s say this bank gives 4%

Do you know any bank that will tell you how much you’ll get back someday?

But is it important for you to know?

We will know that through the rule of 72, this is a simple formula that will determine how many

years our money will double in the bank

72 divided by the number of the interest rate which is 4.

Equals how many years? (Use your finger to point and let your client answer)

18 years! You said your interest is 2%, 72 divided 2 is how many years?

Do they advertise that? You mentioned 1%, 72 divided 1, how many years? Will you invest

there?

Why do you answer bank?

It’s safe, secure and they give us something back.. interest

Would you agree that most people put their money in the bank because they give us

peace of mind?

At the age of 30, you deposited $10K. You have to celebrate your birthday 18 times

before money doubles. By 48 it doubled to $20,000 and by 66 the bank will be obligated

to pay you back around $40,000

Is this enough for people to stop working?

Would you agree this is the reason why people are still working?

The bank will invest somewhere SAFER. Would you agree that McDonalds, Apple

Tim Hortons are safer than people? Every time we eat, is someone making money?

Every time we drive to work is someone making money?

What does the bank do to our money?

Invest because they are obligated to pay you back. What I like here in Canada is that we have one

of the best banking system in the world. They will pay us back,

But, have you heard of the saying being cooked by your own oil?

Who is giving us credit cards?

They invest to us through credit cards. How much is the typical interest rate?

The biggest are in-store credit cards, 29.99%. Let’s say it’s 18%. 72 divided by 18 is how much?

(Point your finger and let your client answer)

Look how faster our debt doubles compared to our savings

Is this the reason why people are financially broke?

Mismanaging credit cards?

Credit cards are good as long as we don’t abuse it.

But would you agree, PEOPLE ARE

RISKY?

Is our jobs guaranteed?

Is our health guaranteed?

Is marriage guaranteed?

There are two important lessons here… one is we can work hard for our money and second one is money

can work hard for us. If you can do both, you become financially strong much faster

72 divided by 12 equals how much? (Point your

finger and let your client answer)

By 60, the bank has $320,000. Are they

obligated to pay you back $40,000 now?

You actually have to wait 6 more years and by

that time their money has doubled to $640,000!

The bank is earning 640K, while they will only

give you back how much? What do you feel

right now?

Remember what I said a while ago that this

information helped me and my family. The first

time I saw this, I realized the rich are becoming

________ (let them finish this statement)

Big companies are safer than people because if

they’re not earning well, what do they do to their

employees? They Lay them off.

The Bank has this simple philosophy. It’s ok for

them to earn less, as long as it is safer. To them

12% is less than 18% but SAFER

I am not here for the bank or for the big

companies, I’m here for you. This is about you.

Which would you like to see in your bank

account someday? $40K or $640K? Why?

Instead of planting your seed in the bank, we will plant that in big companies. That’ what a Financial Advisor

do… share to people how to grow their money. So that in the future, instead of the bank you will be

receiving $640K.

Is this a good idea? But how come banks don’t teach

us? Do schools teach us how to become a financial

Advisor?

There’s a big shortage of financial advisors here in

Canada and later I’ll show to you how to become one.

What I meant about big companies is really about

STOCK MARKET.

What do you remember back in 2009? So is investing in big companies risky?

Let me share about what is the risk

The purpose of the WHAT IS THE RISK slide is to eliminate the objection of “is this guaranteed?” This is

what the slide is designed for. Every part of this is purposely created so we can have a solid presentation

without any holes.

I asked you awhile ago, and you wanted to be here, but how do these

people become financially secure? I just want to share something and I

hope it make sense.

What if we can bypass the bank?

I don’t mean your chequing or savings account, those are

important for our bills, what I meant is the money you set aside

for the future or retirement

So what is the risk

So you were expecting $640,000. I cannot

guarantee your money, remember 2009? The

market dropped around 50% if it happens again,

you will only have $320,000.

Is it still better that $40,000?

The Riskiest thing in life is not taking the risk.

I love Canada, you can earn more if you want to. The challenge is the more you earn the bigger

____________ (let your client answer this, “taxes you pay”)

If I can grow your money someday. How much tax would you like to pay?

Now you want peace of mind, let’s see the worst

scenario, what if 90% of the market went down?

You’ll lose 90%, you’ll only have 10% which is

$64,000. Is this still better than $40,000?

100%, 50% or No Tax?

No Tax, would you agree this is too good to be

true?

There are plans out there that are tax-free and let

me share to you the typical retirement plans in

Canada.

What’s the most famous retirement plan in Canada?

We also have TFSA and IRP, Insured Retirement Plan.

All these plans are good plans, but they have

advantages and disadvantages

We will compare them, first is Tax Deduction. Is there tax

deduction in RRSP? That’s the good thing in RRSP.

Is there tax deduction in TFSA? None, also in IRP

How about when we ACCESS the money, do we get taxed

when we WITHDRAW money from RRSP?

Do we get taxed when we access money in TFSA?

In IRP, if we ACCESS the money there’s no tax. This is

Canada, we cannot escape taxes. Either we enjoy now and

pay later or pay tax now then enjoy later

BE CAREFUL in using the words ACCESS and Withdraw. Because IRP is taxable when withdrawn, but if IRP

Strategy (Collateral Bank Loan) is implemented there are no taxes.

Which among the following can provide Tax-free Lifetime income…

Is RRSP designed for lifetime income?

For most people, RRSP is not designed for lifetime income

because of the taxes when withdrawn. Also TFSA, for most

people it is not lifetime.

What does letter “S” stands for? And how much is the typical

interest rate of savings account?

IRP is designed to provide lifetime income.

among the following which can provide tax-free survivor benefit for your family…

Let’s say something bad happens to you 2 weeks from

now knock on wood, (Please knock on wood) and you put

$200 in RRSP…

Does RRSP provide a survivor benefit?

Your family will receive how much? 200 minus tax

Where would you like to see yourself someday? How we

would know if we are financially secure?

Would you like to have peace of mind that you will have

life-time income?

What is the problem when you die?

Would you agree that when you die, problem

stops?

You don’t have problems when you die but

your family will, SURVIVOR BENEFIT can

provide that peace mind.

How about you put 200 in TFSA then knock on wood something bad happens to you 2 weeks from now,

Does TFSA provide a survivor benefit? Your family will receive how much? 200

Is 200 enough for our family? Would you agree people saving in RRSP and TFSA still have to buy life

Insurance? Would you agree that’s additional cost?

IRP is a very unique plan, even if you only put 200 then something bad happens to you (knock on wood),

we can qualify you for $500K survivor benefit, Tax-free!

Survivor benefit can vary from client to client, $200 with a survivor benefit of $500K is based on 35-year-

old female. Say, “Survivor Benefit depends on the savings and age, we can qualify you for more or less”

What if this is you and you have $200, would you like less financial benefits or more Financial Benefits?

Paint pictures in their mind. Make it clear to them so they can

relate

The next slide is an example so that clients can relate during

presentation. We have to provide CLARITY to our clients.

Example, 35 year old female, most of them are married has

children and every family’s dream is to become a home owner.

Would you agree this is a good plan?

Would you agree this is what most people are

doing?

Would you like to see something better?

Same person, same goals and same budget.

But instead of RRSP or TFSA, she’s putting it in

IRP. Lets see what happens

Remember cellphones 10 years ago? How is it now?

Would you agree that cellphones today are better 10 years ago?

The next slide is designed to remove the objection and doubts that what if the financial institution

becomes bankrupt.

We’ve talked about how life works, and how

money works, I’d like to share to you how

safe is our money. Is that important for us to

know?

I asked you a while ago and you wanted to

save more, how much are you saving more?

Would you like to pay more or less?

Let’s imagine you are 65 today and you were

saving in the bank. By 65 you have

$1,000,000. Can we control what will happen

tomorrow?

How do you know if your money is safe? Is it

important to know the guarantee?

Explain CDIC and the guaranteed amount to the client

Let’s say you also have $1,000,000 in IRP. What if the Insurance company will be bankrupt?

If your financial company becomes bankrupt, would you like

to be safe or sorry?

How much did you lose?

How do you feel losing that money?

IRP is offered under the insurance industry, and it

surprises me because my understanding of insurance

before is that something has to happen before they

pay. I did not know that they will pay retirement.

Assuris is the counterpart of CDIC and protects

the insurance industry. If your life insurance

company fails, Assuris GUARANTEES that you

will retain $60,000 or 85% of the savings in the

investment account whichever is higher

Because $1,000,000 is bigger than 60,000 so

you will retain 85% which is $850,000.

How much did you lose?

Would you agree this is better than losing

900,000?

We are almost done…

IRP is out there, and please GOOGLE Insured Retirement Plan

If IRP is out there, how come only few people know about IRP?

Let me share to you what one of the banks say…

Emphasize the contribution… 25,000! 20,000! 25,000!

According to Manulife Bank, many

affluent Canadians use Insured

Retirement

What is affluent to you?

Rich, but how rich is rich?

Would you agree to some people, these are their annual income?

This part will give your client Hope…

Then proceed to using the BMO Software and create a plan for your client.

After you have created a plan and showed it to your client then say..

I know you like the plan, but there’s one challenge with IRP, not everyone can qualify… because of the

Survivor benefit.

If you would like to know if you can qualify, it’s free to apply.

Would you agree that rich people are using IRP

because of the financial benefits? Let me share

again those benefits… Tax-free when you access

the money, designed for lifetime income and if

something happens, there’s a survivor benefit