Embed Size (px)

Citation preview

Band of Angels: Protecting the Seed Investor Convertible Notes, Capped Notes, Series Seed and Preferred Stock Investment Structures

October 16, 2013

James C. Chapman,Partner, Bingham McCutchen LLP

2

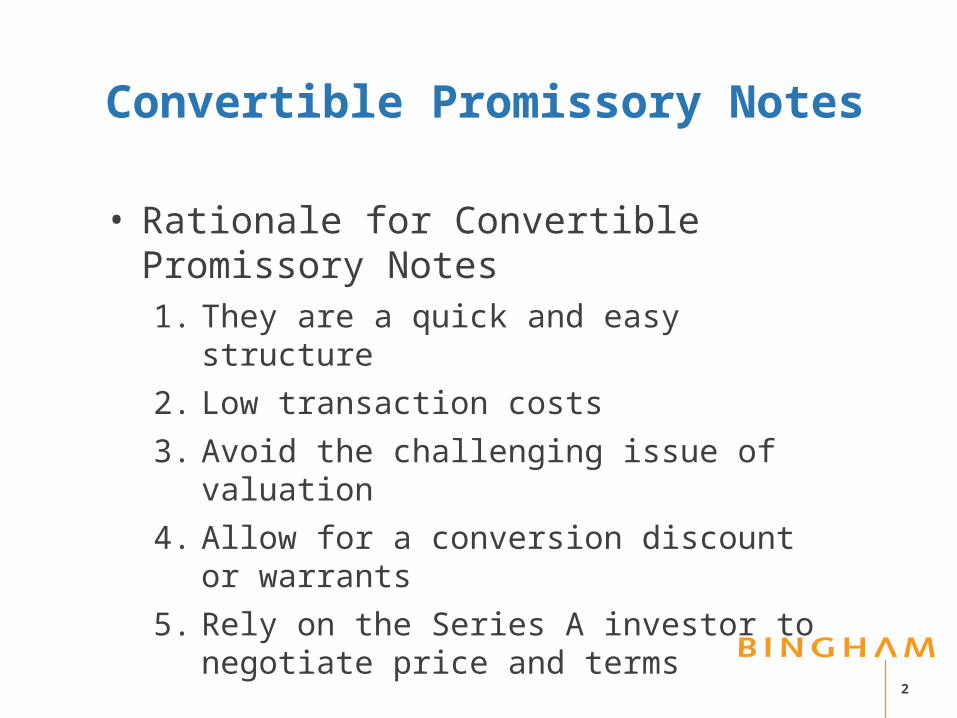

Convertible Promissory Notes

• Rationale for Convertible Promissory Notes1. They are a quick and easy structure

2. Low transaction costs

3. Avoid the challenging issue of valuation

4. Allow for a conversion discount or warrants

5. Rely on the Series A investor to negotiate price and terms

3

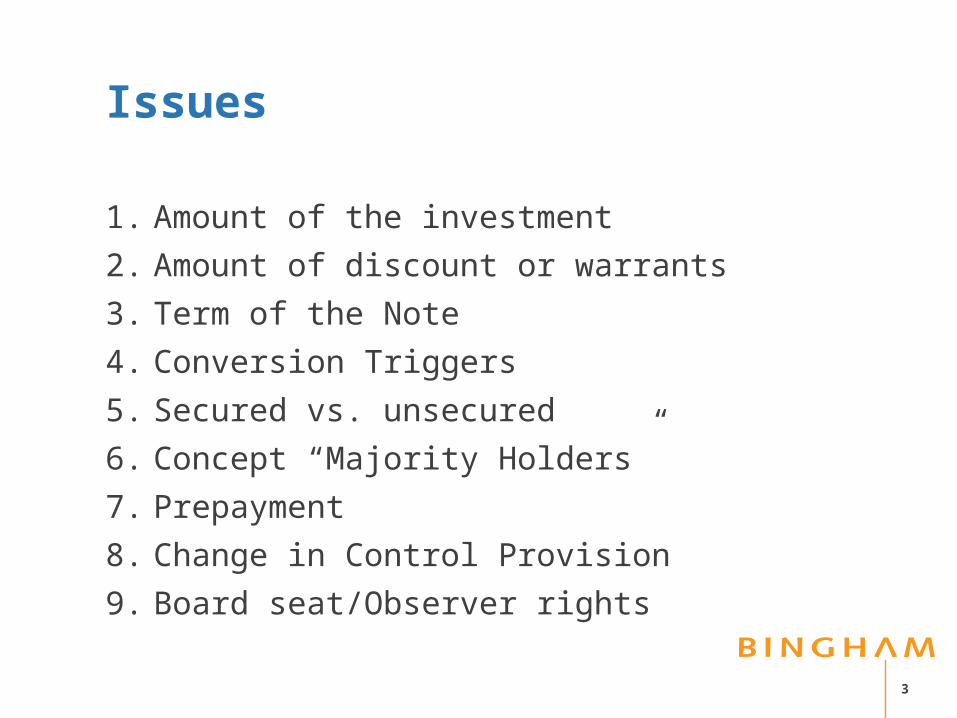

Issues

1. Amount of the investment

2. Amount of discount or warrants

3. Term of the Note

4. Conversion Triggers

5. Secured vs. unsecured

6. Concept “Majority Holders”

7. Prepayment

8. Change in Control Provision

9. Board seat/Observer rights

4

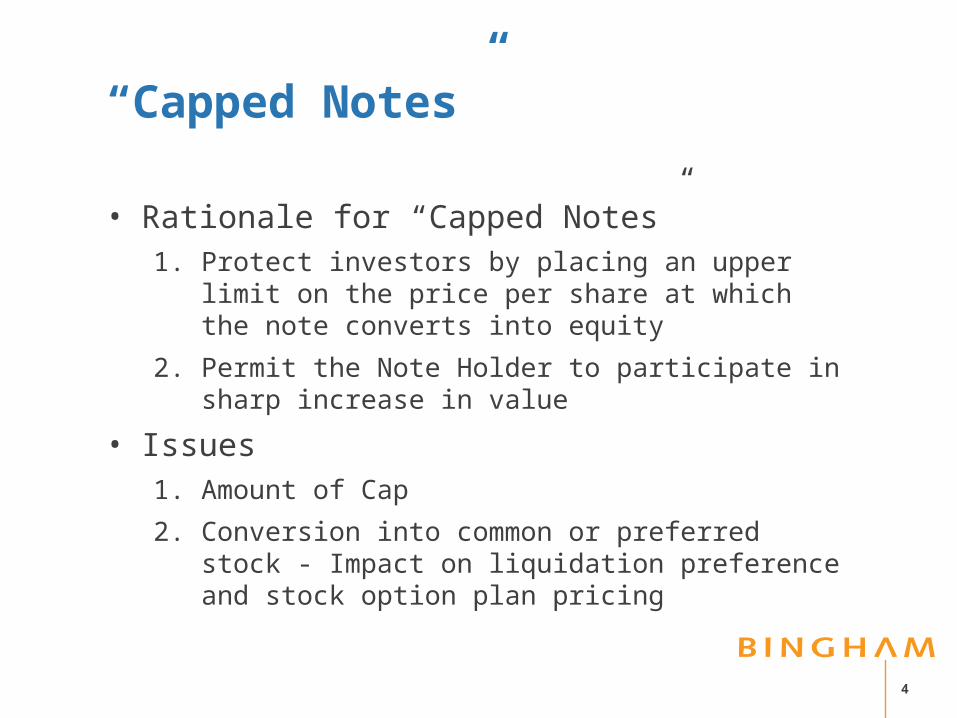

“Capped Notes”

• Rationale for “Capped Notes”1. Protect investors by placing an upper limit on the price

per share at which the note converts into equity

2. Permit the Note Holder to participate in sharp increase in value

• Issues1. Amount of Cap

2. Conversion into common or preferred stock - Impact on liquidation preference and stock option plan pricing

5

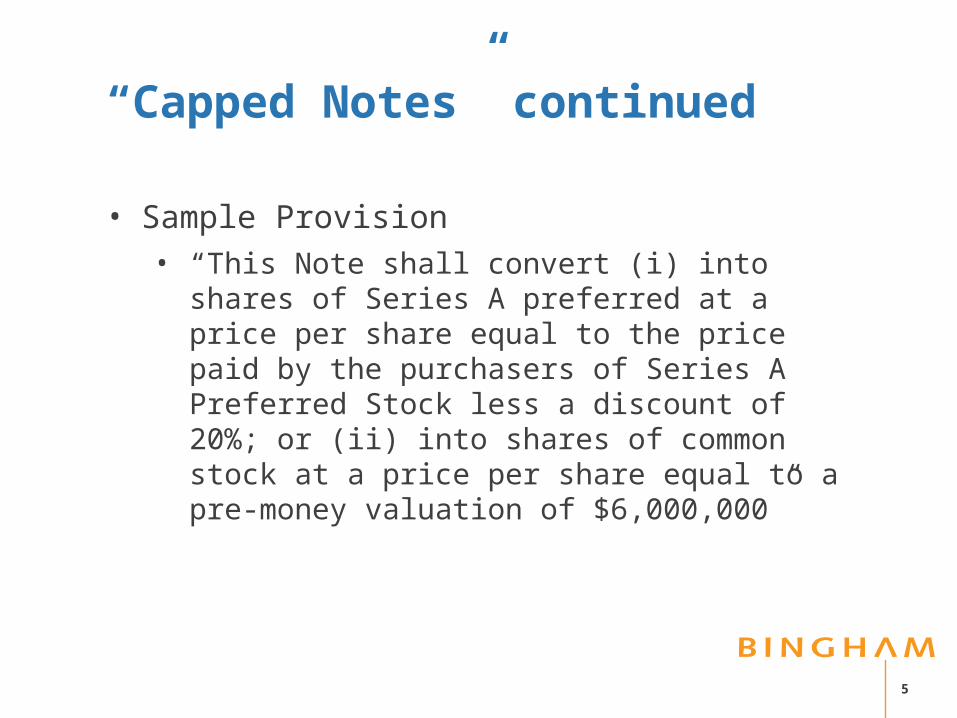

“Capped Notes” continued

• Sample Provision• “This Note shall convert (i) into shares of Series A

preferred at a price per share equal to the price paid by the purchasers of Series A Preferred Stock less a discount of 20%; or (ii) into shares of common stock at a price per share equal to a pre-money valuation of $6,000,000”

6

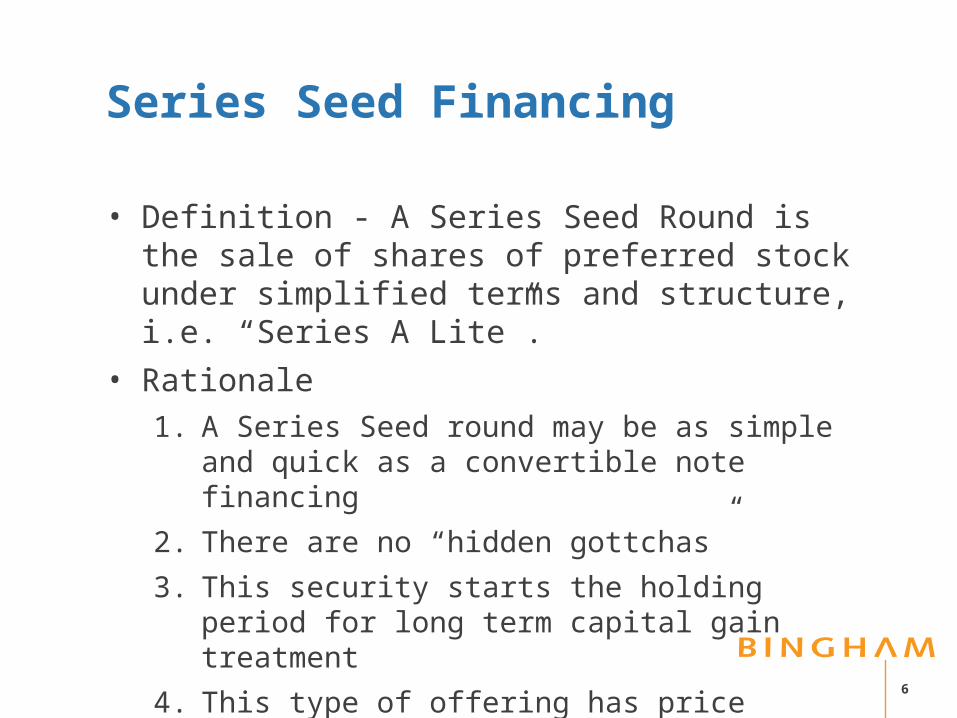

Series Seed Financing

• Definition - A Series Seed Round is the sale of shares of preferred stock under simplified terms and structure, i.e. “Series A Lite”.

• Rationale

1. A Series Seed round may be as simple and quick as a convertible note financing

2. There are no “hidden gottchas”

3. This security starts the holding period for long term capital gain treatment

4. This type of offering has price certainty as opposed to capped notes

7

Series Seed Financing continued

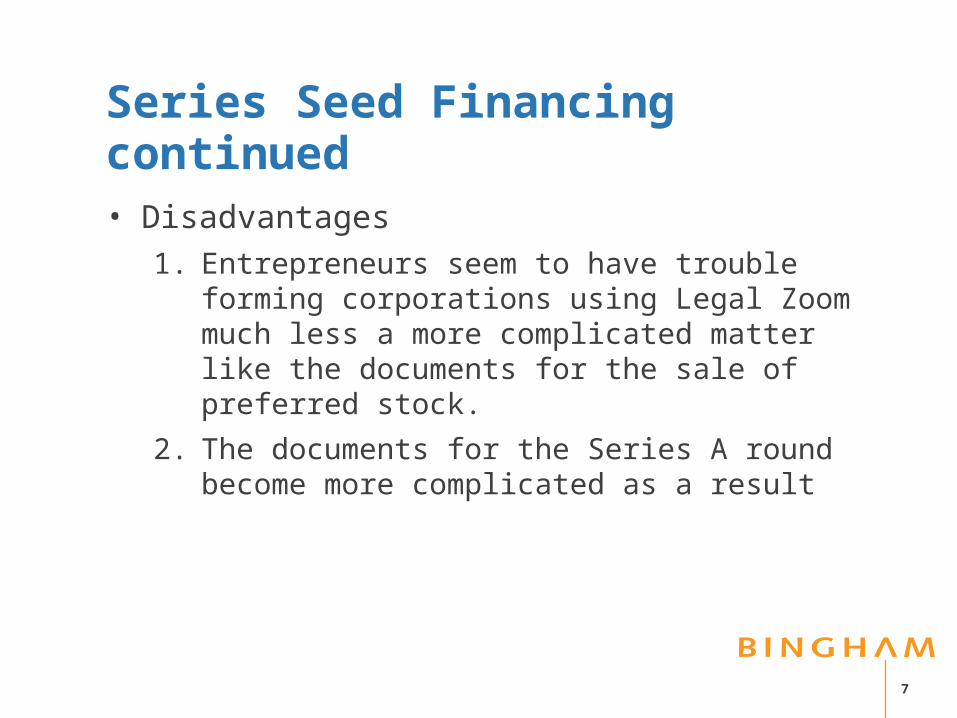

• Disadvantages

1. Entrepreneurs seem to have trouble forming corporations using Legal Zoom much less a more complicated matter like the documents for the sale of preferred stock.

2. The documents for the Series A round become more complicated as a result

8

Series Seed Financing continued

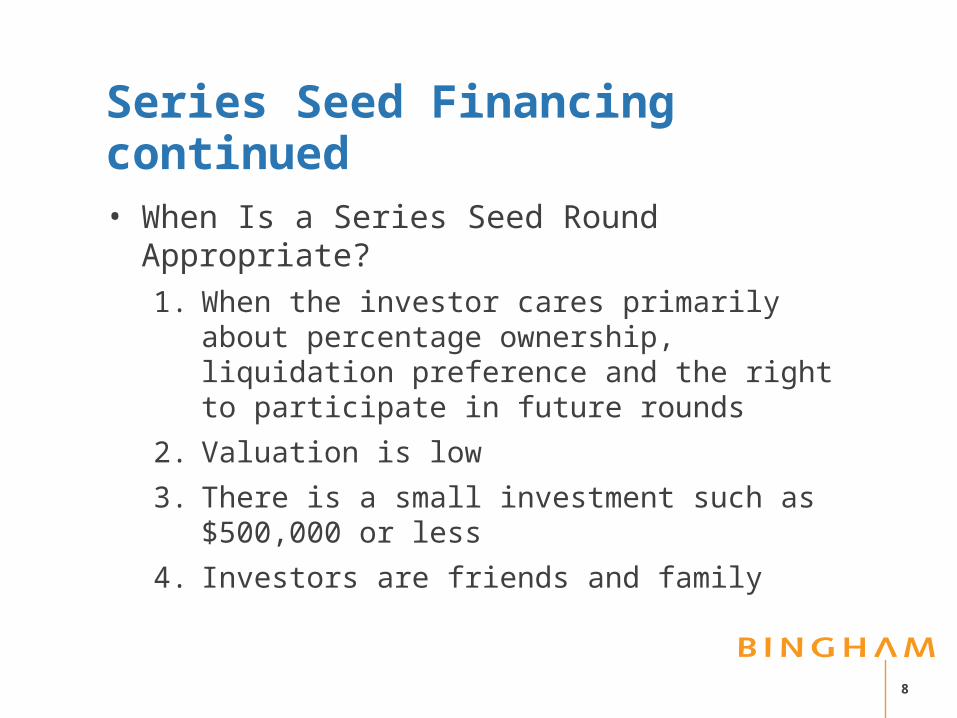

• When Is a Series Seed Round Appropriate?

1. When the investor cares primarily about percentage ownership, liquidation preference and the right to participate in future rounds

2. Valuation is low

3. There is a small investment such as $500,000 or less

4. Investors are friends and family

9

Series A Preferred Stock Financing

• Typical Issues

1. Amount of investment

2. Valuation

3. Right Preferences and Privileges

• Dividends - only 5% are cumulative dividends

• Liquidation - 34% are participating preferred (43% of these are not capped)

• Conversion -voluntary and mandatory

• Anti-dilution -98% of deals use weighted average

• Voting - with the common stockholders or as a separate class

10

Series A Preferred Stock Financing continued

• Protective Provisions - negative covenants

• Registration Rights- Demand, Piggyback, S-3

4. Board Seats/Observer Rights

5. Information Rights

6. Right of First Refusal and Co-Sale Rights

7. Right to Participate in Future Round of Financing - 8% have pay to play provisions.

• When is a Series A Round Appropriate?

1. $1,000,000 of investment or more.

2. Institutional investor

11

Differences Between Series Seed and Series A Preferred1. No dividend preference

2. No anti-dilution protection

3. No registration rights

4. No comprehensive protective provisions

5. No co-sale rights

6. No voting agreement

7. The representations and warranties are limited

8. No legal opinion

Beijing

Boston

Frankfurt

Hartford

Hong Kong

London

Los Angeles

New York

Orange County

San Francisco

Santa Monica

Silicon Valley

Tokyo

Washington

bingham.com

Bingham McCutchen®

© 2013 Bingham McCutchen LLP One Federal Street, Boston, MA 02110-1726 ATTORNEY ADVERTISING

To communicate with us regarding protection of your personal information or to subscribe or unsubscribe to some or all of Bingham McCutchen LLP’s electronic and mail communications, notify our privacy administrator at

[email protected] or [email protected] (privacy policy available at www.bingham.com/privacy.aspx). We can be reached by mail (ATT: Privacy Administrator) in the US at One Federal Street, Boston, MA

02110-1726 or at 41 Lothbury, London EC2R 7HF, UK, or at 866.749.3064 (US) or +08 (08) 234.4626 (international).

Bingham McCutchen (London) LLP, a Massachusetts limited liability partnership authorised and regulated by the Solicitors Regulation Authority (registered number: 00328388), is the legal entity which operates in the UK

as Bingham. A list of the names of its partners and their qualification is open for inspection at the address above. All partners of Bingham McCutchen (London) LLP are either solicitors or registered foreign lawyers.

This communication is being circulated to Bingham McCutchen LLP’s clients and friends. It is not intended to provide legal advice addressed to a particular situation. Prior results do not guarantee a similar outcome.

Circular 230 Disclosure: Internal Revenue Service regulations provide that, for the purpose of avoiding certain penalties under the Internal Revenue Code, taxpayers may rely only on opinions of counsel that meet

specific requirements set forth in the regulations, including a requirement that such opinions contain extensive factual and legal discussion and analysis. Any tax advice that may be contained herein does not constitute an

opinion that meets the requirements of the regulations. Any such tax advice therefore cannot be used, and was not intended or written to be used, for the purpose of avoiding any federal tax penalties that the Internal

Revenue Service may attempt to impose.

12