Embed Size (px)

Citation preview

PROSPECTIVE FINANCIALSTATEMENTS: GUIDELINES FORA OROWINO PRACTICE AREAHow a newAICPA ED would beapplied in practice.by Don Pallais* and Robert K. Elliott

A client wants help in estimating his personalincome taxes for next year. Another clientwants help in order to decide whether to leaseor buy a new machine. A condominium asso-ciation needs assistance in developing a bud-get. A promoter needs help in putting togetheran offering to sell a real estate limited partner-ship to a group of doctors.

What do these engagements have in com-mon? Each one may involve prospective fi-nancial statements, the subject of a newAmerican Institute of CPAs Exposure Draft(ED), Proposed Guide for Prospective Finan-cial Statements."^

The ED proposes guidelines for the ser-vices accountants may provide concerningprospective financial statements. It is an am-bitious document in that, to accomplish this, itwould affect all of the traditional disciplinesof the profession—not only auditors and ac-countants but also management advisory ser-vices and tax practitioners. The ED probablywould affect more types of practitioners per-forming more types of services than any othertechnical pronouncement.

This article describes the ED. explains therationale behind it and shows how the EDwould be applied in practice. Readers should

*Mr. Pallais is an etnplnyec of the American Instilule ofCPAs, and his views, as expressed in this article, do notneces,sarily reflect the views of the AICPA. Official positionsof the AICPA are detetniincd through certain procedures, dueprocess and deliberation.AICPA Exposure Drafl, Proposed Guide for Prospective

Financial Statements (New York: AICPA, September 20.1983).

keep in mind, however, that the document isan exposure draft and. therefore, is subject tochange. Until a final guide is published, prac-titioners should consult for guidance theGuide for a Review of a Financial Forecast,^Statement of Position (SOP) no, 75-4, Pre-sentation and Disclosure of Financial Fore-casts,^ the AICPA auditing standards divi-sion SOP entitled Report on a FinancialFeasibility Stiidy^ and Rule 201{e)—GeneralStandards (Forecasts) of the Code of Profes-sional Ethics and related interpretation.

Types of Prospective FinancialStatements Covered by the EDProspective financial statements, as defined inthe ED, arc presentations of future-orientedfinancial information that contain, at a mini-mum, certain items (see exhibit 1, page 58).Presentations that omit one or more of theseitems are called "partial presentations" andare not covered by the ED. The ED alsodoesn't apply to pro forma presentations(which are essentially historical financialstatements adjusted for a prospective transac-tion) nor does it apply to prospective financialstatements covering wholly expired periods(for example, last year's budget wouldn't becovered by the ED because the infonnation isno longer prospective; but this year's budgetwould be covered if any unexpired portion ofthe year remains).

DON PALLAIS, CPA. is dircetor-audil and accounting guidesat the American Inslitute of CPAs. He is a member ol'the NewYork State Society of CPAs and ihe AICPA. ROBERT K.ELLIOTT, CPA, is a partner of Peal, Marwick, Mitchell &Co.. New York Cily. Chairman of the Institute"s financialforeeasts and projections task force, he is a former member ofthe AICPA auditing standards hoard and has served on numer-ous other Institute task forces and eommiltecs, Mr. Elliott alsois viee-president of the American Accounting Association,

Financial Forecasts and Projeetions Task Force. Guide for aReview of a Financial Forecast (New York: AICPA. 1980).Statement of Position no. 75-4. Pre.sentation and Disclosure

of Financial Forecasts (New York: AICPA, 1975).Auditing Standards Division SOP. Report on a Financial

Feasibilit\' Study (New York: AICPA. 1982).

56 Journal of Accountancy, January 1984

The ED classifies prospective financialstatements into three types: forecasts, projec-tions and multiple projections. The types ofpresentations and what they are intended topresent differ somewhat from both current lit-erature and practice and thus require someexplanation.

The Guide for a Review of a Financial Fore-cast defines a forecast as an estimate of themost probable financial position, results ofoperations and changes in financial positionfor one or more future periods. It defines afinancial projection as an estimate of financialresults that are not necessarily the most like-ly.*

In the nine years since these definitionswere established, issuers of prospective finan-cial statements have had increasing difficultywith them. They have become reluctant tocharacterize any estimate about the future as"most probable" (for example, they arguethat it is not possible to estimate any rate ofinflation as most probable). In addition someissuers' attomeys have been similarly reluc-tant to have their clients characterize theseestimates as most probable. As a result, somecompanies whose objectives were to issueprospective financial statements depictingtheir best estimates of results have issued pro-jections (where no assettions about probabil-ity are made) rather than issue forecasts.

The ED attempts to encourage entities topresent their estimates of future results by re-vising the definition of forecast to eliminatethe troublesome most-probable concept. TheED defines a forecast as a presentation thatdepicts, to the best of management's knowl-edge and belief, the entity's expected futurefinancial position, results of operations andchanges in financial position based oti condi-tiotis tnanagement expects to exist and actionsit expects to take. It defines a financial projec-tion as a presentation that depicts, to the bestof management's knowledge and belief, ex-pected future financial position, results of op-erations and changes in financial position giv-en the occurrence of one or more hypothetical(that is, not expected) assumptions, based on

'These definitions were first developed by the managementadvisory services executive committee in MAS Guideline Se-ries no. 3, Guidelines for Systems for the Preparation of Fi-nancial Foretasis (New York: AICPA, 1975).

conditions it expects would exist and actions itwould take if the hypothetical assumptionsmaterialized.

Thus, as revised, a forecast would be man-agement's best estimate of what it expects tohappen and a projection would be a presenta-tion intended to answer the question "Whatwould happen if . . . ? " This differentiationappears to be easier to understand and applythan one based on judgments about probabil-ity of future occurrence.

Based on the revised definitions, forecastswould be useful for any class of users and forany purpose because they depict what man-agement thinks will happen; for example,they would be useful for general offerings ofdebt or equity, negotiations or internal analy-sis. Projections, on the other hand, becausethey would depict something managemetitdoes not expect to happen, would only beuseful for management or outsiders who areevaluating the same "what ifs" as manage-ment and with whom management can discussthe presentation and underlying assumptions.

Journal of Accountancy, January 1984 57

Thus, projections wouldn't be useful to a pas-sive user, but only to users able to evaluateand challenge the hypothetical assumptions.Typically, the users of financial projectionswould be parties in negotiations with the issu-er, such as banks, or the issuer itself.

In some cases, management wants to pre-pare a forecast but is unable to because it can'tdevelop a single point estimate relating to oneor more conditions or courses of action. Forexample, a real estate developer may not beable to provide a single point estimate of theoccupancy rate of a new apartment buildingalthough he believes occupancy will be higherthan 70 percent but lower than 90 percent. Toaddress this situation, the ED provides for a

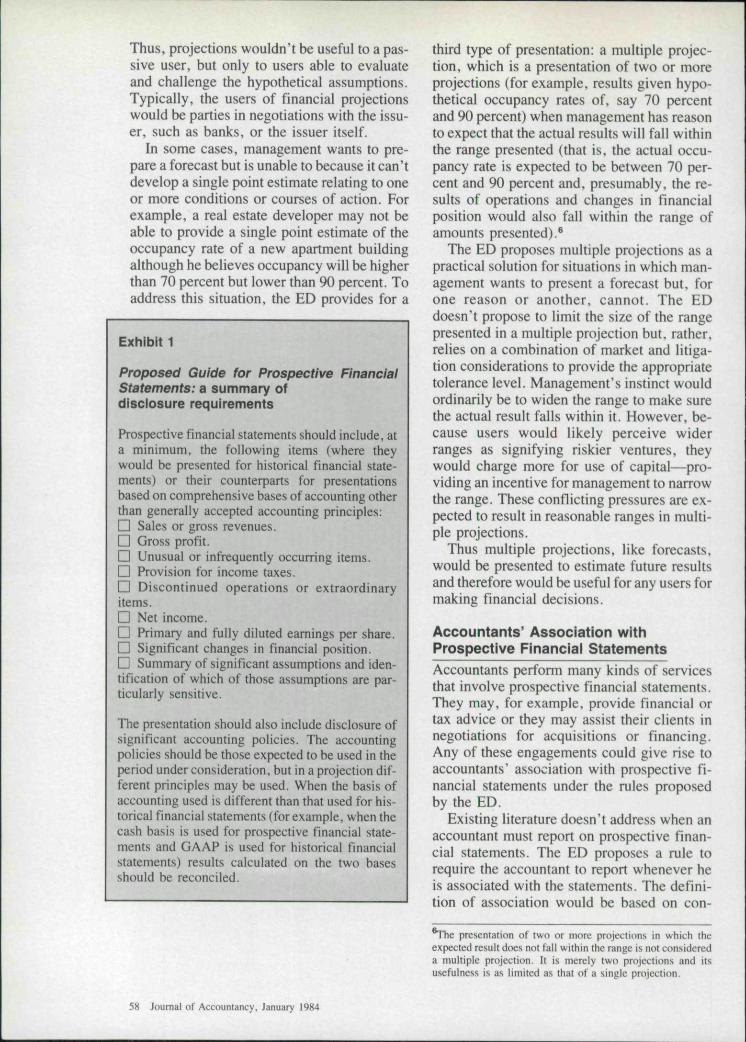

Exhibit 1

Proposed Guide for Prospective FinancialStatements: a summary ofdisclosure requirements

Prospective financial statements should include, ata minimum, the following items (where theywould be presented for historical fmancial state-ments) or their counterparts for presentationsbased on comprehensive bases of accounting otherthan generally accepted accounting principles:D Sales or gross revenues.D Gross profit.n Unusual or infrequently occurring items.n Provision for income taxes.n Discontinued operations or extraordinaryitems.D Net income.D Primary and fully diluted earnings per share.D Significant changes in financial position.n Summary of significant assumptions and iden-tification of which of those assumptions are par-ticularly sensitive.

The presentation should also include disclosure ofsignificant accounting policies. The accountingpolicies should be those expected to be used in theperiod under consideration, but in a projection dif-ferent principles may be used. When the basis ofaccounting used is different than that used for his-torical financial statements (forexample. when thecash basis is used for prospective financial state-ments and GAAP is used for historical financialstatements) results calculated on the two basesshould be reconciled.

third type of presentation: a multiple projec-tion, which is a presentation of two or moreprojections (for example, results given hypo-thetical occupancy rates of, say 70 percentand 90 percent) when management has reasonto expect that the actual results will fall withinthe range presented (that is. the actual occu-pancy rate is expected to be between 70 per-cent and 90 percent and. presumably, the re-sults of operations and changes in financialposition would also fall within the range ofamounts presented).*

The ED proposes multiple projections as apractical solution for situations in which man-agement wants to present a forecast but, forone reason or another, cannot. The EDdoesn't propose to limit the size of the rangepresented in a multiple projection but, rather,relies on a combination of market and litiga-tion considerations to provide the appropriatetolerance level. Management's instinct wouldordinarily be to widen the range to make surethe actual result falls within it. However, be-cause users would likely perceive widerranges as signifying riskier ventures, theywould charge more for use of capital—pro-viding an incentive for management to narrowthe range. These conflicting pressures are ex-pected to result in reasonable ranges in multi-ple projections.

Thus multiple projections, like forecasts,would be presented to estimate future resultsand therefore would be useful for any users formaking fmancial decisions.

Accountants' Association withProspective Financial StatementsAccountants perform many kinds of servicesthat involve prospective financial statements.They may, for example, provide financial ortax advice or they may assist their clients innegotiations for acquisitions or financing.Any of these engagements could give rise toaccountants' association with prospective fi-nancial statements under the rules proposedby the ED.

Existing literature doesn*t address when anaccountant must report on prospective finan-cial statements. The ED proposes a rule torequire the accountant to report whenever heis associated with the statements. The defini-tion of association would be based on con-

^Tie presentation of two or more projections in which theexpected result does not fall within the range is not con.sidereda multiple projection. It is merely two projections and itsusefulness Is as limited as that of a single projection.

58 Joumal of Accountancy. January 1984

cepts in Statement on Auditing Standards no.26, Association with Financial Statements^and Statement on Standards for Accountingand Review Services no. I, Compilation andReview of Financial Statements,^ and wouldread as follows:

' ' An accountant is associated . . . when hehas consented to the use of his name in con-junction with the [prospective financial state-ments] in a report, document, or written com-munication containing [them]. Also, when anaccountant submits to his client or others[prospective financial statements] that he hasassembled® or assisted in assembling, he isdeemed to be associated even though an ac-countant does not append his name to [them].The accountant who is associated . . , should. . . report. . .; however, he is not deemedto be associated with [prospective financialstatements] that, prior to the issuance of hisreport, [are] clearly identified as a draft."'®

Thus, association with prospective finan-cial statements would depend on two majorfactors; (1) whether the accountant's namewas used in conjunction with the presentationor he or she assembled it or assisted in itsassembly and (2) whether the service was pro-vided on prospective financial statements.

To demonstrate the first factor: an accoun-tant who uses microcomputer software to pro-cess client data to produce his client's budgetwould be associated with prospective finan-cial statements because he assembled them.An accountant who makes software availableto his client through time-sharing would notbe associated with the statements because theclient assembled them (unless his client usedhis name in conjunction with the statements ina document).

To demonstrate the second factor: the ac-countant's services with regard to partial pre-

Statement on Auditing Standards no. 26, Association withFinancial Statements (New York: AICPA, 1979), See alsoAICPA Professional Standards, vol.1 (Chicago: CommerceClearing House), AU section 504.Statement on Standards for Accounting and Review Services

no. 1, Compilation and Review of Financial Statements (NewYork: AtCPA. 1979). See also AICPA Professional Stan-dards, vol. 2. AR sec. 100.^Tie exposure draft defines assembly as the perfonnance ofmathematical or other clerical functions related to the presen-tation of the prospective tlnancial statements. Assemblywouldn't refer to the mere reproduction and collation of such.statements.

AICPA ED. Proposed Guide for Prospective FinancialStatements, sec. 500.01.

sentations wouldn't be covered by the pro-posed association rule" because partial pre-sentations wouldn't be prospective financialstatements as defined in the ED. Similarly,the accountant who helps his client identifykey factors or assumptions or who developssoftware for the client to do its own modelingwould not, on that account, be associated withthe resulting prospective financial statementsbecause, although he provided a valuable ser-vice, the service didn't encompass the pros-pective financial statements. He would onlybe associated with them if, in addition to pro-viding the software, he assembled, or assistedin assembling, the statements. (For example,if he not only provided the modeling softwarebut also used it to produce prospective finan-cial statements, he would be associated withthe statements and would have to report onthem.)

The accountant who is associated with theprospective financial statements would be re-quired to report on them for the same reasonsthe accountant is required to report on histori-cal financial statements. That is, users are bet-ter informed and the accountant is better pro-tected if the accountant explicitly identifiesthe scope of his services and the degree ofresponsibility he is taking.

The ED states that the form of the accoun-tant's report would depend on two factors: thepotential users (third-party users or internalusers) and the nature of service provided.

The primary objective of an accountant'sinvolvement with prospective financial state-ments for use by third parties is similar to thatof the accountant's services with respect tohistorical financial statements—to add credi-bility to those statements. Accordingly, theED provides that, just as in the case of histori-cal financial statements, the accountant's ser-vices and reports for prospective financialstatements would be standardized when in-tended for third-party use. Standardization ofservices and reports would increase their use-fulness to third-party users because the userswould be able to easily identify and under-stand the services and reports.

The ED defines two levels of service onprospective financial statements for use bythird parties. The services are reviews (orig-inally defined in the Guide for a Review of aFinancial Forecast), which would provide ex-

However. the accountant should be aware of Rule 201 (e)—General Standards (Forecasts) and related interpretation.

60 Joumat of Accountancy, January 1984

pHcit assurance as to the presentation of thestatements and the reasonableness of the as-sumptions; and compilations, which, similarto SSARS no. 1, would provide no explicitassurance on either the presentation or as-sumptions.

The objective of a service for intemal-use-only prospective financial statements may bethe same as for third-party-use statements, butprobably more often it is not. Often, the ob-jective of the service is to consult with theclient, to give advice or to help the client

"The ED indicates that there wouldbe instances in which the accountant

shouldn't be associated withprospective financial statements."

make a decision. Thus, although the standardcompilation and review services would be ap-propriate for intemal-use-only prospective fi-nancial statements, the circumstances oftencall for a different form of service and a reportthat is responsive to the service rendered.

To provide the flexibility required for en-gagements with varying objectives, the EDproposes a spectrum of services to be per-formed on intemal-use-only prospective fi-nancial statements. At the low end of the spec-trum would be mere assembly, the lowestlevel of service resulting in the accountant'sassociation, while at the otber end of the spec-trum would be a review. In between would benumerous services, including not only compi-lation but also services not identified in theED resulting in reports expressing varioustypes of assurances as to the presentation ofthe statements and underlying assumptions.

The association rule would apply to ser-vices on intemal-use-only statements as itdoes for statements intended for third-partyuse, so the accountant would have to reportwhenever he is associated with the state-ments. However, if the accountant is satisfiedthat the statements and reports are not going tooutsiders he wouldn't need to use a standardreport as long as the level of assurance ex-pressed is supported by the work performedand his report clearly states that its distribu-tion is limited to intemal use.

The ED proposes that the accountant berequired to report on intemal-use-only state-ments even when distribution of the state-ments would be restricted to management be-

cause physical restrictions may not be effec-tive and prospective fmancial statements maybe improperly shown to outsiders. The ac-countant's report would provide him withsome measure of protection against outsiders,who might incorrectly attribute too high a lev-el of responsibility to him. It would also pro-tect outsiders from misinterpreting the ac-countant's responsibility.

When the Accountant Should NotBe Associated with the StatementsThe ED indicates that there would be in-stances in which the accountant shouldn't beassociated with prospective fmancial state-ments. One of these is when prospective fi-nancial statements omit the summary of sig-nificant assumptions. This prohibition isbased on the concem that prospective fman-cial statements without assumptions won't beunderstandable and will result in useless ormisleading presentations.

Certain microcomputer software can printout, in one form or other, the factors used incomputing the prospective amounts. As longas this information is understandable to theuser, it would ordinarily meet the ED's re-quirements. Obviously, some software doesthis more neatly than others and presumablyaccountants will keep this in mind in order toachieve a balance between the benefits of use-ful microcomputer printouts and the cost tosearch out or modify software to achieve thisusefulness.

The ED would also prohibit an accountantfrom being associated with a financial projec-tion (not a multiple projection) to be used in ageneral offering (unless it supplements a fore-cast or multiple projection) because, as pre-viously mentioned, a financial projectionwouldn't be useful to passive investors. Toinclude a projection that doesn't supplement aforecast or multiple projection in a documentgoing to such users would likely be mislead-ing, and the accountant wouldn't ordinarily beassociated witb a presentation that couid mis-lead outsiders."

Reviews and CompiiationsThe review level of service was established inthe Guide for a Financial Forecast. The ED

In a review service the accountant might be associated witha misleading presentation but issue an adverse report.

62 Journal of Accountancy. January 1984

doesn't propose any significant changes tothis service except that it would extend theservice to financial projections and multipleprojections.

The ED identifies compilation as the lowestlevel of service an accountant could provideon prospective financial statements for out-side use. The service would be similar to aSSARS no. 1 compilation—an informed read-ing of the statements, realizing that the ac-countant may have to help his client putamounts on paper. The procedures in the EDgenerally parallel those in SSARS no. 1 ex-cept where the nature of prospective data re-quires them to be different.

The procedures required for a compilationof prospective financial statements would pri-marily ben Obtaining background knowledge.n Assembling the statements.D Reading the statements.n Considering any actual results for an ex-pired portion of the period.n Attempting to correct any problems en-countered.n Obtaining signed representations.n Reporting.

The accountant would be required to obtainknowledge of the client's industry and its ac-counting, just as he is under SSARS no. 1.Acquiring this knowledge about the entity andits industry gives the accountant a basis forconsidering the form of presentation and as-sumptions used.

Assembly of the prospective financial state-ments refers to the mathematical translation ofmanagement's expectations into prospectivefinancial statements. If the client were to handthe accountant a complete financial forecast,this step wouldn't be necessary, just as inSSARS no. 1 the accountant (theoretically)need not put pencil to paper to compile finan-cial statements. In the real world, however,clients often engage accountants primarily forthis step. The ED contemplates that outsideusers relying on an accountant's compilationreport probably would believe they have theright to expect the prospective financial state-ments to be mathematically accurate and sothe ED would make assembly a distinct com-pilation procedure. (As stated earlier, an ac-countant who assembles prospective financialstatements would be associated with thosestatements under the ED and would have toreport on them.)

To be of value as a professional service, acompilation must imply certain things about

which the accountant has special knowledgeor expertise. Even though the compilation re-port would express no assurance, the publicmay be likely to assume that, in addition tobeing mathematically accurate, the compiledstatements are based on acceptable accountingprinciples, presented in the proper form andnot intended to mislead. Thus the ED pro-poses that the accountant be required to askwhat accounting principles are used in the pre-sentation (and compare these to his knowl-edge of the principles normally used) andwhere the assumptions came from (to consid-er whether management needs help in devel-oping assumptions or whether it is unwise tobe associated with the statements).

The accountant would then consider, basedon this knowledge, whether the assumptionsor the presentation are obviously inappropri-ate, incomplete or otherwise misleading. Thisconsideration wouldn't require the type ofanalytical work done in a review (unless theaccountant believed it necessary for his com-pilation) but. rather, can be considered a"smell test." If, based on his knowledge ofthe entity and of accounting and business ingeneral, nothing strikes the accountant as ob-viously wrong with the presentation, he

"In a significant departure fromSSARS no. 1, the compiler ofprospective financiai statements wouldbe required to obtain signedrepresentations from management."wouldn't need to perform any analytical pro-cedures or further inquiries to comp-lete hiscompilation.

When part of the prospective period hasexpired (for example, a 1983 budget done inMarch 1983) the ED proposes that the accoun-tant be required to consider the historical re-sults to date (that is, results for January andEebruary 1983). The method and level of de-tail of this consideration would depend on thecircumstances, but as the year goes on thehistorical results would tend to become moresignificant and the accountant would be moreinclined to look at them closely. As an ex-treme case, a one year forecast done on the364th day of the year would normally be ex-pected to look very much like the historicalresults to date; if it did not, the accountant

would be very concerned that the forecast wasmisleading.

In a significant departure from SSARS no.1, the compiler of prospective financial state-ments would be required to obtain signed rep-resentations from management. Unlike his-torical financial statements, which are basedon records of completed transactions, pros-pective financial statements are based onmanagement's thoughts and expectations. Be-cause the accountant can't see into manage-ment's mind the way he can look into a gener-al ledger, the signed representations are hisassurance that the statements are based on theappropriate assumptions and that manage-ment accepts responsibility for the assump-tions. The ED specifies certain representa-tions that the accountant would be required toobtain in writing and provides illustrative rep-resentation letters to show one way of obtain-ing them.

The ED proposes that the accountant berequired to issue a standard report at the com-pletion of the compilation engagement (unlessthe statements were for internal use only). Thestandard compilation report would give no as-surance as to presentation or the assumptionsand would be similar to a SSARS no. 1 com-

"The ED recognizes that the objectiveof an engagement done for internal useis often different than for engagements

contemplating third-party reliance."pilation report. (The report on prospective fi-nancial statements, however, would carrywarnings and descriptions relating to the factthat the statements depict the results of eventsthat have not occurred and therefore may notcome true.)

The standard compilation report would readas follows (in this example, a forecast wascompiled):

"The accompanying forecasted balancesheet, statements of income, retained earn-ings, and changes in financial position andsummaries of significant assumptions and ac-counting policies of XYZ Company as of De-cember 31, I9XX, and for the year then end-ing, present, to the best of management'sknowledge and belief, the Company's expect-ed financial position, results of operations,and changes in financial position for the fore-cast period. Accordingly, the financial fore-

cast refiects its judgment, based on presentcircumstances, of the expected conditions andits expected course of action. However, someassumptions inevitably will not materializeand unanticipated events and circumstancesmay occur; therefore, the actual resultsachieved during the forecast period will varyfrom the forecast and the variations may bematerial.

"We have compiled the forecast in accor-dance with applicable guidelines establishedby the American Institute of Certified PublicAccotintants. A compilation of a forecast doesnot include evaluation of the support for theassumptions underlying the forecast. Becausea compilation of a forecast is limited as de-scribed above, we do not express a conclusionor any other form of assurance on the accom-panying statements or assumptions. We haveno responsibility to update this report forevents and circumstances occurring after thedate of this report.""

When the accountant encounters a problemwith the assumptions, his first step would beto get the matter corrected (assuming it's ma-terial). If management was unwilling to revisethe assumptions (or was unable to justifythem), the ED proposes that the accountant berequired to withdraw from the engagement.The ED specifies this action rather than dis-closing the problem in the accountant's reportfor two reasons: (1) modifying the report forone assumption might imply some unintendedlevel of assurance regarding the other assump-tions and (2) the assumptions are often depen-dent on each other and users might not be ableto understand the effect of a qualification onthe presentation taken as a whole. Since theaccountant often works closely with manage-ment when compiling statements, it isn't an-ticipated that it would be difficult for him tohave misleading assumptions corrected.Therefore, it is expected that accountantswould rarely have to withdraw from compila-tion engagements.

When prospective financial statementsomit certain disclosures—other than those re-lating to assumptions—the accountant woulddescribe the omission in his report. For exam-

AICPA ED, Proposed Guide for Prospective FinancialStatements, sec. 620.04.

54 Joumal of Accountancy, January 1984

pie, if the presentation omits disclosure of theaccounting policies (see exhibit 1), the ac-countant would describe the omission in hisreport but would not normally be required towithdraw from the engagement, limit distri-bution of his report or provide the missingdisclosure.

Statements for Internal Use OnlyThe ED recognizes that the objective of anengagement done for intemal use is often dif-ferent from that of an engagement contem-plating third-party reliance. Thus, the proce-dures and reporting designed to meet theneeds of third-party users wouldn't always berequired for internal-use-only engagements.

As previously mentioned, many differenttypes of engagements would be done for inter-nal use, bounded by reviews as the highestlevel of service and assembly as the lowest. Itis anticipated that there would be two generaltypes of engagements that come under thisumbrella. One is the consulting engagement,in which the accountant is engaged to giveadvice to his client regarding future oper-ations and is expected to give some type ofassurance regarding the assumptions. The EDrecognizes that, because of the differing cir-cumstances, flexibility is needed in reporting.It doesn't illustrate a report so as not to sug-gest that one type of report is preferable toanother in this type of engagement. (Howev-er, the ED proposes that certain items be re-quired in the report including identification ofthe prospective financial statements; a de-scription of the accountant's service and thelevel of assurance he is giving; and a state-ment restricting the use of his report to inter-nal use.)

The other general type of internal-use en-gagement relates to processing a client's bud-gets or other prospective data on the accoun-tant's computer. The ED proposes that onlytwo procedures be required for such a service:(1) the establishment of an understanding withthe client, which may be especially importantbecause of the limited procedures involvedand the distribution restriction and (2) assem-bly. Since the accountant would be associatedwith the assembled statements, he would haveto report on them, and the ED provides a sam-ple report on this level of service. An accoun-tant could use this example in practice by pro-gramming the report into his computer or byhaving it reproduced, leaving blanks for theclient's name and the date of the statements.

As the accountant completes the assembly, hecould fill in the date and client's name andattach the report to the computer printout,meeting the ED's requirements without an ap-preciable increase in cost.

Because the client may expect that the ac-countant's involvement ensures proper disclo-sure, the ED proposes that an accountant'sreport on any internal-use-only service be re-quired to describe the omission of requireddisclosures that come to his attention. Theaccountant wouldn't, however, be required towithdraw from the engagement or to modifyhis report because of a bad assumption—aslong as the assumption is disclosed in thestatement—because the statements wouldn'tbe distributed to outsiders.

The accountant would still be prohibitedfrom being associated with prospective finan-cial statements that omit the summary of sig-nificant assumptions. This disclosure is im-portant even for intemal-use-only statements.For example, if no assumptions are disclosedand management refers to the statements aweek later, it may not remember the assump-tions used—rendering the statements use-less—or it may remember them incorrectly—rendering them misleading. However, the ac-countant wouldn't need to be concerned ifsensitive assumptions aren't separately identi-fied; presumably management would knowwhich assumptions are sensitive.

The accountant would perform internal-useservices on prospective financial statementsonly if he had no reason to believe they wereintended for outsiders. If he believed theywere intended for outsiders, he would com-pile or review the statements.

Putting the ED into PracticeIf issued as exposed, here's how the ED mightapply in practice in the four situations men-tioned in the first paragraph of this article.

Situation I. The president of a corporateclient wants a forecast of his personal taxes fornext year. The accountant has a form 1040software package that, based on the assump-tions input, calculates and pfints a forecast inthe form of a 1040. Because a 1040 doesn'tinclude significant changes in financial posi-tion, the printout is a partial presentation.

66 Journal of Accountancy, January 1984

which isn't covered by the ED. The accoun-tant would do whatever he believes appropri-ate considering the situation and Rule 201(e)and related interpretation. (If the softwarealso provided the significant changes in finan-cial position, the accountant would apply theED and probably issue an intemal-use-onlyreport on the presentation,)

Situation 2. A corporate client needs adviceto help it decide whether to lease or buy anasset and wants to know how the two alterna-tives would affect operations. Pro forma fi-nancial statements could be prepared in thissituation to see what last year's operationswould have looked like if the asset had beenbought or leased, (Pro forma presentationsaren't covered by the ED.) However, in thisinstance, the client is also contemplating other

"The ED is an important documentwhich, if issued as exposed, should

have a considerable effect on arelatively new area of practice and,thus, will benefit the profession and

the public."operating changes and believes it would bemore meaningful to analyze the effect on cashin the following year, when the asset would beacquired. Two projections are prepared, oneassuming the asset is purchased and one as-suming the asset is leased.^*

After discussion of the intended use of thepresentation with the client, the accountantbelieves he can perform an intemal-use-onlyservice, (The client doesn't intend to use thepresentation to get financing for the acquisi-tion.) The accountant inputs the data into hismicrocomputer and applies to the assumptionswhatever procedures he thinks appropriate inthe circumstances. In looking at the results,the accountant notices that, under the assump-tions used, the lease would be capital-

^*rhis situation can be used to illustrate the difference be-tween a multiple projection and two single projections. If theclient expected that he would either buy the asset or lease it, hecould present a multiple projection, but in this case because heis unsure whether he will obtain the asset at all, this presenta-tion would be two projections; it Isn't a multiple projectionbecause his expectation does not necessatily fall within therange.

izable under Financial Accounting StandardsBoard Statement no, 13, Accounting forLeases.^^ Because the client is primarily in-terested in his cash flow, he doesn't want thelease capitalized in the projection.

The ED's disclosure requirements call forthe reconciliation of the basis of accountingused (in this case, cash) with the basis theclient historically uses for financial statements(in this case, generally accepted accountingprinciples) but since the client doesn't want orneed this disclosure, the accountant merelymentions its omission (as well as the omissionof the rest of the accounting policies) in hisreport. The accountant completes the reportillustrated in the ED and attaches it to theprintout of the two projections and assump-tions and gives it to the client.

Situation 3. A condominium associationengages an accountant to help it develop itsannual budget. The accountant can't performan intemal-use-only engagement because heknows that the budget must be distributed toall unit owners (who, like shareholders, areconsidered outsiders). So, the accountantcompiles the budget (a forecast). The accoun-tant, after establishing his understanding withthe association, acquires knowledge about theclient and its industry. If he previously audit-ed, reviewed or compiled historical financialstatements for the client, he already wouldhave the required background knowledge of itand the industry. If not, he could rely on hisknowledge gained from other clients in theindustry and by inquiry of this new client.

In doing the compilation the accountantasks where the assumptions come from and istold that they are based on the previous year'sresults, which have been adjusted for infla-tion. The approach seems reasonable and theaccountant has no reason to ask further ques-tions about the assumptions at this point.

In reading the assumptions for intemal con-sistency, the accountant notices that althoughthe condominium association expects to takeout a mortgage for its new athletic facilities,no interest expense has been budgeted. Theaccountant has this inconsistency corrected(or finds out where the interest expense isincluded); otherwise he would withdraw fromthe engagement if the amount was material.

Because the budget is for calendar year1984 and the accountant is doing the work inNovember 1983, there are no historical results

Financial Accounting Standards Board Statement no. 13,Accounting for Leases (SVdmfoTd: FASB, 1976).

68 Journal of Accountancy, January 1984

for an expired portion of the prospective peri-od and he needn't perform the compilationprocedure relating to those results. The ac-countant obtains signed representations andgives the standard report on a compilation of aforecast.

Situation4. A client wants to promote a realestate limited partnership—a professionalbuilding—to 20 doctors. The client can't pre-pare a forecast because he is too unsure aboutcertain assumptions. Instead, he decides toissue a multiple projection, which he is confi-dent will encompass the results that will oc-cur. A single projection, or even two projec-tions that are not a multiple projection, wouldbe inappropriate for this type of offering,which amounts to a general offering of equity.

The client originally requested a review,but decided that the size of the offeringcouldn't justify the cost of a review; accord-ingly, the accountant is engaged to compilethe multiple projection. The accountant com-piles the presentation and notes no problems.

Although the prospective financial statementsare presented on the tax basis of accounting,there is no requirement to reconcile the resultsto GAAP, provided that the historical resultsof the entity will also be reported on the taxbasis. The accountant applies the standardprocedures and gives the standard report for acompilation of a multiple projection.

Conclusion

The ED is an important document which, ifissued as exposed, should have a considerableeffect on a relatively new area of practice and,thus, will benefit the profession and the pub-lic. Still, the draft should be considered by ailpractitioners who would be affected—ac-counting, auditing, tax and MAS practition-ers—all of whom are encouraged to respondto the draft (by May 4, 1984) in order to devel-op the best guidance for the profession. •

Trailing the economy

Not surprisingly, trying to gauge an economy the size of that ofthe U.S. hasalways introduced errors into the data. The consumer price index, until it wasrevised . . . after a decade of debate, had overstated inflation during periods ofrising interest rate.s. And the growth of a huge underground economy has causedthe gross national product, personal income, and savings to be understated.

But now economists recognize that a more fundamental problem is distortingthe numbers. Increasingly, economic statistics have failed to keep up with thedizzying pace of an economy in flux. At a time when the economy is beingshaped by high-technology industries and the fast-growing service sector, thedata tend to emphasize older, mature, or declining industries. This tnakes itdifficult to get a clear picture of the structure of the economy and producesdistortions about economic growth and inflation.

Generally, economists maintain that most of the indicators are adequate forshort-run analysis and policymaking. because by and large they track develop-ments over the business cycle reasonably we!!. When policymakers and busi-nessmen attempt to devise longer-term plans, however, they run into serioustrouble. The deficiencies in the data wil! prove most dangerous if the governmentmoves to take a more interventionist role in t!ie economy, as favored by advo-cates of industria! policy. "I shudder every time I think of industrial planning,"says Pierre A. Rinfret, president of . . .a New York consulting firm. "The firstrule of such an effort is that you have to know where you are starting from. Howcan we hope to plan if we don't even know where we are!?]"

From "Why Economic IndicatorsAre Often Wrong"

Business Week, October 17, 1983

Journal of Accountancy. January 1984 69