Embed Size (px)

Citation preview

Real Estate

Deloitte Insight

Q2 2014

Rental growth set to boost returns

Property IQ

AuthorsJames GriggsInformation Unit [email protected]+44 (0)20 7303 3158

Will MatthewsResearch and [email protected]+44 (0)20 7303 4776

Property IQ is a brief snapshot of some of the most pertinent charts from the UK Property Handbook, our comprehensive quarterly review of UK property markets.

As the recovery continues, the drivers of property performance are now gradually starting to rebalance.

Yields are expected to compress further, particularly for regional and secondary property as investors look to these markets for returns. But prime yields are still under pressure too: for example, industrial space has been in notably strong demand by different investor types, and yields have fallen by around 50bps in a range of industrial and office sub-sectors since the start of the year.

UK institutional funds are playing a growing role in the investment market, spurred on by improving expectations for the economy and by the still-substantial gap between real estate and bond yields.

However, purchasing by Middle Eastern investors has been more restrained during recent months. US funds, in contrast, have become more active.

In broad terms though we expect capital growth fuelled by yield movement to slow over the next two years. Rental growth will start to become a more important driver of commercial property performance.

Take-up of new space in the central London office markets was strong last year, suppoting rental growth, while the picture is improving in the South East and most regional office centres.

Although still not visible across large parts of the sector, retail rental growth is gradually returning, and will be underpinned by improving demand from occupiers.

Sector Category Jun

‑09

Jul‑

09

Au

g‑0

9Se

p‑0

9O

ct‑0

9N

ov‑

09

Dec

‑09

Jan

‑10

Feb

‑10

Mar

‑10

Ap

r‑10

May

‑10

Jun

‑10

Jul‑

10A

ug

‑10

Sep

‑10

Oct

‑10

No

v‑10

Dec

‑10

Jan

‑11

Feb

‑11

Mar

‑11

Ap

r‑11

May

‑11

Jun

‑11

Jul‑

11A

ug

‑11

Sep

‑11

Oct

‑11

No

v‑11

Dec

‑11

Jan

‑12

Feb

‑12

Mar

‑12

Ap

r‑12

May

‑12

Jun

‑12

Jul‑

12A

ug

‑12

Sep

‑12

Oct

‑12

No

v‑12

Dec

‑12

Jan

‑13

Feb

‑13

Mar

‑13

Ap

r‑13

May

‑13

Jun

‑13

Jul‑

13A

ug

‑13

Sep

‑13

Oct

‑13

No

v‑13

Dec

‑13

Jan

‑14

Feb

‑14

Mar

‑14

Ap

ri‑1

4

Shops

Prime major cities

Cathedral cities

Market town

Shopping centres

Regional dominant

Sub‑regional

Major town centre schemes

Smaller urban schemes

Retail warehouses

Parks (open A1)

Parks (bulky)

Solus

Car showrooms

Let to dealership

Let to manufacturer

Leisure parks

Supermarkets Standalone superstore

Industrial

Distribution (15 year term)

Distribution (inside M25)

Modern ind. est. (outside M25)

Modern ind. est. (inside M25)

Offices

City

West End

Midtown

West London

South East

Major cities

Out‑of‑town

Deloitte Real Estate Yield Matrix – changing sentiment towards yields on prime propertySentiment remains positive across virtually all sectors of the market

Source: Deloitte Real Estate

Sentiment indicator: n Sentiment weakening n No change in sentiment n Sentiment strengthening

The economy

GDP growth expectations rise furtherExpansion broadening out

• The economy continued to expand at an annual rate of 3.1% in the first quarter of the year and the consensus view for GDP growth over 2014 has now reached 2.9%. More encouraging still is the increased contribution coming from business investment as consumer spending loses some momentum.

• Although inflation is well below the Bank of England’s target, rapid falls in unemployment are increasing pressure to raise the base rate.

Credit availability improving, but mainly for large firms

• Recent survey results for both large and smaller firms suggest expansion is uppermost in directors’ minds. Deloitte’s latest quarterly CFO Survey shows a record 71% of corporates in favour of taking greater risk onto their balance sheets.

• The availability of credit continues to improve, although it is less of an issue for large firms than for SMEs. The Bank of England’s Q1 Credit Conditions Survey points to a weaker increase in availability of credit for small businesses. However the survey reports that the availability of lending to the commercial real estate sector rose over Q1 and is expected to grow further.

Activity grows faster in Southern regions

• Regional economic performance is also improving. PMI figures measuring private sector firms’ workloads show that activity is increasing (index above 50) in all regions. However, it is clear that regions in the southern half of the country are enjoying faster growth, and this is expected to continue as these regions contain a greater share of the job-creating sectors in financial and business services.

Changing consensus forecasts for GDP growth

GD

P gr

owth

%

2013 2014 2015

Source: HM Treasury consensus forcasts

Nov-13Jun-13

Dec-13

Jul-13

Jan-14

Aug-13

Feb-14

Sep-13

Mar-14

Oct-13

Apr-14 May-14

Forecasts made in:

0.0

1.0

2.0

3.0

4.0

North West

East Midlands

Scotland, 56.4

North East, 56.6

Yorkshire & Humber, 55.8

East Midlands, 58.2

West Midlands,58.2

Wales, 60.5

North West, 56.1

NorthernIreland,56.6

East, 58.2

London, 59.5

South East, 58.0South West, 58.8

Source: Markit

PMI Business Activity Index, March 2014

2 | Property IQ Rental growth set to boost returns

UK commercial property

Investor demand for property remains firmAppetite for investment still strong

• Over the first four months of the year, £12.9bn of investment purchases were recorded, fractionally ahead of the same period last year. Cash flows from domestic savers into property funds continue to increase steadily, reaching almost £300m in February according to the Investment Managers Association, and we see little let up in demand from across the range of investors over the rest of the year.

• Auction sales have an increasingly important role in the market; there has been a visible shift to larger lot sizes and the sold rate is up over 5% on last year.

UK funds eager to build exposure

• UK institutional funds have been notable in raising their purchasing activity over the last two quarters, and, along with UK property companies, accounted for 53% of purchases in Q1 against 43% for 2013 as a whole.

• Overseas investors, particularly those from the Middle East, have been more subdued this year, but US buyers have been significantly more active in the market.

Yields remain under downward pressure

• The weight of this demand has meant that prime yields have fallen, by a further 50bps since the start of the year for some prime office sub-markets as well as for distribution warehouses and industrial estates. Although now at a low level, we expect to see further small falls this year, particularly in the regional markets.

• Shopping centres have been in high demand, accounting for the three largest single-asset deals in Q1. In contrast to the previous quarter which saw two £1.7bn central London office purchases, the largest office deal in Q1 was Hines’ £245m purchase of 60 Holborn Viaduct in central London.

Property investment by quarter (£ million)

Q1 Q2 Q3 Q4

Source: Property Data

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Share of investment by investor type Q1 2014

Source: Property Data

Owner occupiers

Overseas investors

Private investors

UK institutions

UK property companies

Others

4% 3%

33%

7%31%

21%

Offices – major cities

Offices – South East

Offices – West London

Prime distribution 15 year term

Offices – Midtown

Modern ind estate – regional

Offices – out-of-town

Supermarkets

Leisure partks

Car showrooms

Shopping centres – major

Shopping centres – regional

Shops – market townO�ces – City

Retail parks

Shops – major cities

Fall in prime yields, year to date % (selected)

Source: Deloitte Real Estate

0.00 0.25 0.50

0

0

0

| 3Property IQ Rental growth set to boost returns

UK commercial property

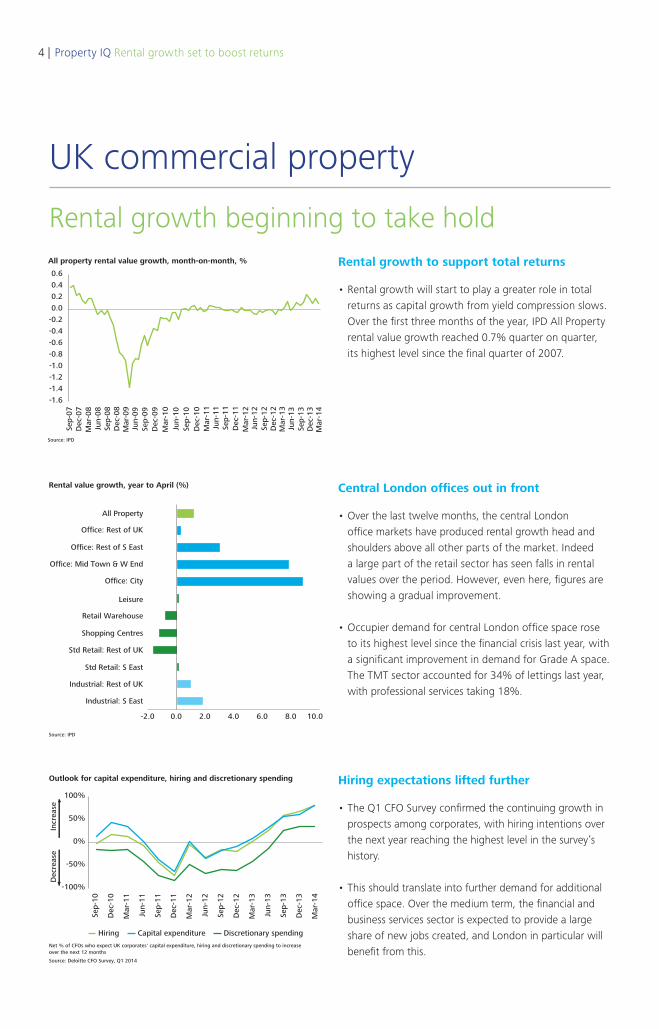

Rental growth beginning to take holdRental growth to support total returns

• Rental growth will start to play a greater role in total returns as capital growth from yield compression slows. Over the first three months of the year, IPD All Property rental value growth reached 0.7% quarter on quarter, its highest level since the final quarter of 2007.

Central London offices out in front

• Over the last twelve months, the central London office markets have produced rental growth head and shoulders above all other parts of the market. Indeed a large part of the retail sector has seen falls in rental values over the period. However, even here, figures are showing a gradual improvement.

• Occupier demand for central London office space rose to its highest level since the financial crisis last year, with a significant improvement in demand for Grade A space. The TMT sector accounted for 34% of lettings last year, with professional services taking 18%.

Hiring expectations lifted further

• The Q1 CFO Survey confirmed the continuing growth in prospects among corporates, with hiring intentions over the next year reaching the highest level in the survey’s history.

• This should translate into further demand for additional office space. Over the medium term, the financial and business services sector is expected to provide a large share of new jobs created, and London in particular will benefit from this.

-1.6

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

All property rental value growth, month-on-month, %

Source: IPD

Mar

-14

Dec

-13

Sep-

13Ju

n-13

Mar

-13

Dec

-12

Sep-

12Ju

n-12

Mar

-12

Dec

-11

Sep-

11Ju

n-11

Mar

-11

Dec

-10

Sep-

10Ju

n-10

Mar

-10

Dec

-09

Sep-

09Ju

n-09

Mar

-09

Dec

-08

Sep-

08Ju

n-08

Mar

-08

Dec

-07

Sep-

07

Rental value growth, year to April (%)

All Property

Office: Rest of UK

Office: Rest of S East

Office: Mid Town & W End

Office: City

Leisure

Retail Warehouse

Shopping Centres

Std Retail: Rest of UK

Std Retail: S East

Industrial: Rest of UK

Industrial: S East

Source: IPD

-2.0 0.0 2.0 4.0 6.0 8.0 10.0

Outlook for capital expenditure, hiring and discretionary spending

Source: Deloitte CFO Survey, Q1 2014

-100%

-50%

0%

50%

100%

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Dec

reas

e

I

ncre

ase

Net % of CFOs who expect UK corporates' capital expenditure, hiring and discretionary spending to increase over the next 12 months

Hiring Capital expenditure Discretionary spending

4 | Property IQ Rental growth set to boost returns

UK commercial property

Retail sector provides some encouragement

High street message improving

• The office sector does not have a monopoly on good news. Recent research by Deloitte suggests that the health of the high street may not be in as critical a condition as widely claimed. An analysis of the reoccupation rates of units formerly held by retailers that had gone into administration shows that those on high streets have fared better than those in shopping centres or on retail parks.

• Furthermore a significant proportion of reoccupied space on the high street has been taken by discount stores and supermarkets seeking to increase their presence in the convenience sector, and not just by bookmakers and charity shops.

Industrials in favour over the medium term

• Returns continue to improve: the average prediction for all property total returns in the May IPF Consensus Forecasts report was 13.7%, up from 12.1% in February.

• Supported by a superior income return element, the industrial sector is expected to produce the strongest total returns over the next five years, at 9.1% per annum according to the latest IPF consensus forecasts.

• Capital growth is expected to be highest in the office sector, bringing total returns to 8.6% per annum.

Changing demands on distribution

• Our new research paper, The Shed of the Future, discusses the impact of e-commerce on the retail logistics network. Higher customer expectations for stock availability, delivery times and collection options are forcing retailers to reassess their optimum distribution arrangements.

• As a consequence we see additional demand for mega sheds from some operators, heavy competition for urban warehousing, and changes in the type of functions warehouses are expected to accommodate.

Of the shops that were vacated

Reoccupied

Reoccupied Reoccupied

Total occupancy

occupancy

High Street

Retail Park

occupancy63%

occupancy71%

Shopping Centre

Source: Deloitte

New logistics model

Source: Deloitte

Total return outlook by sectorIPF consensus forecasts: annualised total returns 2014-18 (%)

Source: IPF Consensus Forecasts Q2 2014

Total return Income return Capital growth

0.0

2.0

4.0

6.0

8.0

10.0

IndustrialStandard RetailOfficeAll property

| 5Property IQ Rental growth set to boost returns

UK residential property

Signs of the market starting to easeHouse price rises continue

• Most regions saw a further acceleration in house prices in Q1, with notable pick-ups recorded in Scotland and the North. London has moved further away from other areas of the county, with annual house price growth of over 18% in Q1.

• Unlike in Q4, however, there are a small number of regions where price growth has fallen back.

Pace of demand growth slows

• The latest data from RICS shows that the level of enquires from new buyers is growing at a much slower rate than during the second half of last year.

• At the same time, the number of properties available to buy remains low, keeping upward pressure on house prices.

• The latest data from the British Bankers Association shows that the number of new mortgages taken out in April was 42,000, a steady fall from the recent peak of 48,000 in January. However the volume remains higher than for the same period last year.

• Market interest rates suggest new loans will become gradually more expensive, while regulations introduced in April will make them more onerous to acquire.

Construction volumes show little sign of taking off

• Improvements in the number of new homes being built have been modest and remain well below the volume in 2007.

• Demand for new houses remains firm, buoyed up by the Help to Buy scheme, but house builders are citing increasing costs – of labour and materials – as well as the lengthy planning process for holding back construction volumes.

Annual house price growth by region %

Q4 2013 Q1 2014

Source: Nationwide

0 2 4 6 8 10 12 14 16 18 20Wales

Northern IrelandNorth

Yorks & HumberWest Midlands

North WestEast Midlands

South WestScotland

East AngliaOuter South East

Outer MetropolitanLondon

Demand indicators

New buyer enquiries (LHS) Sales to stock ratio (RHS)

Dec

reas

in

Incr

easi

ng

Source: RICS

-80

-60

-40

-20

0

20

40

60

80

Mar

-07

Jun-

07Se

p-07

Dec

-07

Mar-08

Jun-

08Sep-08

Dec

-08

Mar-09

Jun-

09Sep-09

Dec

-09

Mar-10

Jun-

10Sep-10

Dec

-10

Mar-11

Jun-

11Sep-11

Dec

-11

Mar-12

Jun-

12Sep-12

Dec

-12

Mar-13

Jun-

13Sep-13

Dec

-13

Mar-14

0%5%10%15%20%25%30%35%40%45%50%

Source: NHBC

New homes started

0

10,000

20,000

30,000

40,000

50,000

60,000

Jun-

07Se

p-07

Dec

-07

Mar

-08

Jun-

08Se

p-08

Dec

-08

Mar

-09

Jun-

09Se

p-09

Dec

-09

Mar

-10

Jun-

10Se

p-10

Dec

-10

Mar

-11

Jun-

11Se

p-11

Dec

-11

Mar

-12

Jun-

12Se

p-12

Dec

-12

Mar

-13

Jun-

13Se

p-13

Dec

-13

Mar

-14

6 | Property IQ Rental growth set to boost returns

Recent publications

A Deloitte Insight report

The Deloitte Consumer ReviewDigital Predictions 2014

Consumer Review: Digital predictions 2014

Q1 2014

April 2014

Record risk appetiteRisk appetite among the Chief Financial Officers of the UK’s largest companies rose to a six-and-a-half-year high in the first quarter of 2014. 71% of CFOs say now is a good time to take risk onto their balance sheet, more than twice the level of a year ago and higher than the levels prevailing before the onset of the financial crisis in late 2007.

Significantly reduced economic uncertainty and much improved financing conditions have helped drive corporate risk appetite higher.

Our economic and financial uncertainty index has fallen by one-third over the last year. Easy monetary policy and favourable financing conditions have created a capital-rich environment for big UK corporates. Buoyant risk appetite means that CFOs are likely to draw down on that capital. CFOs report that credit is more available, and more keenly priced, than at any time in the last six-and-a-half years. Expectations for equity issuance and bank borrowing have seen a strong recovery since the lows in late 2011.

The default position of large corporates in the past six years – bullish on emerging markets, cautious on developed markets – seems to be reversing.

CFOs have become more confident about growth in developed economies, particularly the UK. CFOs increasingly see growth here in the UK, and established markets such as the US and euro area, as the key drivers of their corporate investment plans.

Plans for all forms of corporate spending – hiring, capital spending and discretionary spending – are at new three-and-a-half-year highs. A record 95% of CFOs expect merger and acquisition activity to rise over the next year.

CFOs have become markedly more confident about the outlook for UK inflation. Last quarter a majority expected inflation to overshoot significantly its 2.0% target in two years’ time. Most now expect inflation to be around 2.0%. On average CFOs expect interest rates to rise by 0.25% over the next year.

Consumer spending has been a significant driver of the UK recovery so far. This quarter’s CFO Survey suggests that corporate spending will play an increasingly prominent role as the recovery matures.

The Deloitte CFO Survey

AuthorsIan StewartChief Economist020 7007 [email protected]

Debapratim DeSenior Economic Analyst020 7303 [email protected]

Alex ColeEconomic Analyst020 7007 [email protected]

ContactsIan StewartChief Economist020 7007 [email protected]

Mark FitzPatrickVice Chairman and CFO Programme Leader020 7303 [email protected]

To access current and past copies of the survey, historical data and media coverage, please visit:

www.deloitte.co.uk/cfosurvey

0%

10%

20%

30%

40%

50%

60%

70%

80%

2014Q1

2013Q3

2013Q1

2012Q3

2012Q1

2011Q3

2011Q1

2010Q3

2010Q1

2009Q3

2009Q1

2008Q3

2008Q1

2007Q3

Chart 1. Risk appetite% of CFOs who think this is a good time to take greater risk onto their balance sheets

CFO Survey Q1 2014

Retail thought leadership series

The changing face of retailWhere did all the shops go?

The changing face of retail: Where did all the shops go?

To start a new section, hold down the apple+shift keys and click

to release this object and type the section title in the box below.

UK real estate predictions 2014Expansion mode

Real EstatePredictions 2014

M&AIndex Q2 2014

The Deloitte

Growth is back on the corporate agenda

About the Deloitte M&A IndexThe Deloitte M&A Index is a forward‑looking indicator that forecasts future global M&A deal volumes and identifies the factors influencing conditions for dealmaking. The Deloitte M&A Index has an accuracy rate of over 90 per cent dating back to Q1 2008.

>

Contacts

Iain MacmillanHead of UK M&A020 7007 [email protected]

Sriram PrakashHead of M&A Insight020 7303 [email protected]

Key points

• Deloitte forecasts a strong resurgence in deal volumes for Q2 2014, bolstered by strong economic figures from the US and Europe.

• We expect the global deal volumes to reach nearly 8,000 deals by the end of Q2 2014, up by 10% for the same period in 2013.

• More than $500 billion worth of deals were announced just in the first two months of 2014. It appears growth is firmly back on the corporate agenda.

• The S&P 1200 share price index currently stands close to its pre‑crisis high, however revenue growth has been declining since 2012. With confidence levels recovering, M&A activity provides a compelling way to enhance revenues and profits.

Figure 1. The Deloitte M&A Index

Global M&A deal volumes

Q2 2014 M&Adeal forecast

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

9,500

Q22014

Q12014

Q42013

Q32013

Q22013

Q12013

Q42012

Q32012

Q22012

Q12012

Q42011

Q32011

Q22011

Q12011

Q42010

Q32010

Q22010

Q12010

Quarter

Deloitte M&A Index (projection) Actual M&A deal volume (actuals)

7850

8200

M&A Index Q2 2014

To start a new section, hold down the apple+shift keys and click

to release this object and type the section title in the box below.

The Self Storage Association UK Annual Survey2014

34307A ra Self Storage Report.indd 1 25/04/2014 15:41

The Self Storage Association UK Annual Survey 2014

London industrialTaking stock of the capital

A Deloitte Insight Report2014

London Industrial: Taking stock of the capital

London Office Crane SurveyGearing up for the next phase of construction

Summer 2014

A

London Office Crane SurveySummer 2014

Recent research

London Office Crane Survey Gearing up for the next phase of construction

www.deloitte.co.uk/cranesurvey

2014 will see a spike in the delivery of new space but there is a very limited pipeline thereafter

45% of the space under construction is already let

The West End and Midtown are the only markets to see a rise in construction levels

There was just one new construction start in the City

Office construction is down 5% over the past six months

to 9.2 million sq ft

This survey has recorded15 new starts; lowest number since 2010

Total volume under construction by submarketMillion sq ft

0Paddington

9.2Total

0.5Docklands

0.7King’s Cross 1.3

Midtown1.6West End

0.3Southbank

4.7City

Ann IbrahimResearch Manager+44 (0) 20 7303 [email protected]

Largest available building currently under construction:

317,000 sq ft

Aldgate Tower, City

Largest building currently under construction:

700,000 sq ft5 Broadgate, City

| 7Property IQ Rental growth set to boost returns

Key contacts

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2014 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Designed and produced by The Creative Studio at Deloitte, London. 35712A

Alex BellPublic Sector – Local [email protected]+44 (0)20 7303 3405

Victoria SmithPublic Sector – Central [email protected]+44 (0)20 7007 8597

James GriggsInformation Unit [email protected]+44 0(20) 7303 3158

Will MatthewsResearch & [email protected]+44 0(20) 7303 4776

Anthony DugganHead of Real Estate Research & [email protected]+44 (0)20 7303 3134

Philip ParnellHead of Management and [email protected]+44 (0)20 7303 3898

Chris LewisCorporate [email protected]+44 0(20) 7303 3201

Stephen PeersHead of [email protected]+44 0(20) 7303 3260

Andy RotheryHead of Deloitte Real [email protected]+44 (0)20 7007 1847

Nigel ShiltonHead of Corporate FinanceReal [email protected]+44 0(20) 7007 7934

Russell McMillanCorporate [email protected]+44 0(20) 7303 2381

David BrownHead of Real Estate [email protected]+44 (0)20 7007 2954

8 | Property IQ Rental growth set to boost returns