Embed Size (px)

Citation preview

“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”

UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.

NORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITY

TOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OF

BACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATION

BACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATION

{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}

AAAA

PROJECT REPORTPROJECT REPORTPROJECT REPORTPROJECT REPORT

ONONONON

“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”

ININININ

UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.

DONDAICHA.DONDAICHA.DONDAICHA.DONDAICHA.

SUBMITTED TOSUBMITTED TOSUBMITTED TOSUBMITTED TO

NORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITY

TOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OF

BACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATION

SUBMITTED BYSUBMITTED BYSUBMITTED BYSUBMITTED BY

A$HWIN CHOUHANA$HWIN CHOUHANA$HWIN CHOUHANA$HWIN CHOUHAN

BACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATION

{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}{FINANCIAL MANAGEMENT}

{2010{2010{2010{2010----11}11}11}11}

FROMFROMFROMFROM

“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”“WORKING CAPITAL MANAGEMENT”

UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.UNIVERSAL STARCH CHEM. ALLIED LTD.

NORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITYNORTH MAHARASHTRA UNIVERSITY

TOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OFTOWARDS PARTIAL FULFILLMENT OF

BACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATIONBACHELOR DEGREE IN BUSINESS ADMINISTRATION

BACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATIONBACHELOR IN BUSINESS ADMINISTRATION

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 2

ACKNOWLEDGEMENT Words are indeed inadequate to convey my deep sense of gratitude to all those who have helped me in completing this project to the best of my ability. Being a part of this project has certainly been a unique and a very productive experience on my part. First of all I would like to thank North Maharashtra University, Jalgoan for providing me an opportunity to undertake a project as a partly fulfillment of BBA degree. I am really thankful to my mentor Mr. Ankush Agrawal Sir, for guiding and helping me to solve all kinds of queries regarding the project work. His systematic way of working and incomparable guidance has inspired the pace of the project to a great extent. I would also like to thank my project coordinator Mr. Sachin Surana Sir for guiding me about preparing project report and very thankful to all lecturers, office staff and library staff of Institute of Management Research And Development, Shirpur for their useful guidance and advise. I am very grateful to Mr. J.S Patil Sir (Sr. Administration Manager) UNIV ERSAL STARCH-CHEM ALLIED LTD. Who has given me the opportunity to do this project in their esteemed organization. This project would not have been successful without the help of Mr. Altaf Sheikh Sir (Finance Manager) and Mr. Devendrasingh Rawal (A.C Maintenance Dept.) of UNIVERSAL STARCH-CHEM ALLIED LTD. Last but not least I would like to thank all the employees of UNIVERSAL STARCH-CHEM ALLIED LTD. who have directly and indirectly helped me with their moral support for the completion of my project Finally I would to express sincere thanks to my Dad & Mom for their blessings and appreciation which helped me some or other way in making my project successful. ( Ashwin Chouhan )

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 3

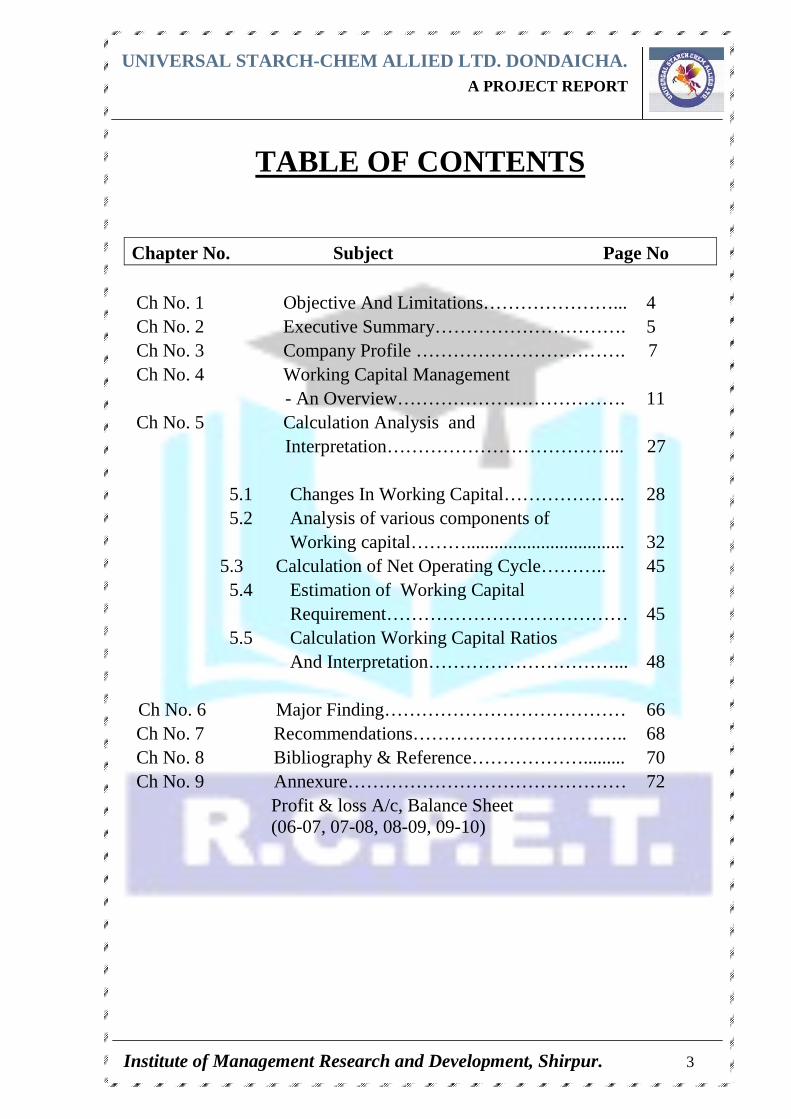

TABLE OF CONTENTS

Chapter No. Subject Page No Ch No. 1 Objective And Limitations…………………... 4 Ch No. 2 Executive Summary…………………………. 5 Ch No. 3 Company Profile ……………………………. 7 Ch No. 4 Working Capital Management - An Overview………………………………. 11 Ch No. 5 Calculation Analysis and Interpretation………………………………... 27 5.1 Changes In Working Capital……………….. 28 5.2 Analysis of various components of Working capital……….................................. 32 5.3 Calculation of Net Operating Cycle……….. 45 5.4 Estimation of Working Capital Requirement………………………………… 45 5.5 Calculation Working Capital Ratios And Interpretation…………………………... 48

Ch No. 6 Major Finding………………………………… 66 Ch No. 7 Recommendations…………………………….. 68 Ch No. 8 Bibliography & Reference………………......... 70 Ch No. 9 Annexure……………………………………… 72 Profit & loss A/c, Balance Sheet (06-07, 07-08, 08-09, 09-10)

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 4

OBJECTIVES & LIMITATIONS

It is compulsory that under three year full time course of B.B.A. degree, a student has to

undergo different training programs so as to establish himself capable of managing at the

place of his work after the completion of this degree. Thus project work is an unique way

of studying an organization.

The main purpose of assigning this task of project report is to keep new practical

knowledge, establishing relations with different persons outside the organization and to

obtain first hand and factual information.

The project helps to draw out the differences and similarities between the theoretical

knowledge with the actual job conditions, this helps the students to persuade and activate

strategy decision-making when they start their carriers. It provides an opportunity to

develop communication skill and analytical skills.

The project provides the opportunity to understand the working capital management of

Universal Starch-Chem Allied Ltd.

Limitations:

This project focuses only on certain factors, which are important to discuss. But tool of

ratio analysis has certain fundamental and conceptual limitations, this project as well.

The study is only made on one organization so it does not provide any scope of

comparison with other organization.

� The study is based only on last 4-year records.

� The study is restricted to financial position of the company with on attention

given to loans and advances and deposit mobilization.

� While computing ratios, average, percentage, the figures are appropriated to two

decimal places. Therefore sometimes the total may not exactly tally

� Sometime round figures are taken on place of accurate figures.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 5

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 6

EXECUTIVE SUMMARY

The group was founded in the year 1973 by Hon'ble Shri Dadasaheb Rawal, the Ex-Ruler, Ex-MLA & Freedom Fighter. This visionary personality thought of bringing industry, power & water works to his town of Dondaicha, which was otherwise an under-developed region of North Maharashtra. In his vision he selected an agro- based industry to process Maize into value-added products. The project entitled “Working Capital Management and Analysis” deals with brief of management of their day to day expenses, inflow as well as outflow of cash in UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. which is an agro-based industry to process Maize into value-added products. The term of study was kept limited to make the title true. The purpose of the report is to get the in depth understanding of the process of working capital management. The Company has successfully enhanced the production capacity of Maize Refining from 60 MT to 400 MT per day. The objective of this project work is to focus on the working capital of the STARCH-CHEM ALLIED LTD. DONDAICHA. And exploring its potential in the company. The project contain the basic postulates of working capital, procedure of analysis of working capital, ratio being used to define the working capital and the impact of working capital in the company in case of excess or inadequacy. Also, the project contains analysis of estimation of working capital requirement and the procedure to estimate working capital requirement in manufacturing and trading concern. and from the data available it can be concluded that it holds a very strong position in the market. The total turnover of company is around `̀̀̀.85 crores and still counting. Company showing good ratios which indicate sound efficiency , liquidity , and structural health of company.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 7

� Founder � Vision � Mission � Company History � Structure � Capacities � Products

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 8

A well-read, widely traveled, highly educated Law Graduate who has dedicated his life for the upliftment of human society beyond the boundaries of nation, caste & creed. The group was founded in the year 1973 by Hon'ble Shri Dadasaheb Rawal, the Ex-Ruler, Ex-MLA & Freedom Fighter. This visionary personality thought of bringing industry, power & water works to his town of Dondaicha, which was otherwise an under-developed region of North Maharashtra. In his vision he selected an agro- based industry to process Maize into value-added products. His two young sons assisted him to set up this industry. He being a progressive minded person took the lead in updating technology, products, quality, system and transportation and delivery of the liquid products etc. In his efforts he has been first in many spheres in India like introduction of tankerisation for transport of Liquid Glucose and Dextrose Syrup. In the fields of Education and Training, he started a Diploma Engineering College at Dhule, in 1945 the district headquarters, which was the first technical institute in the region. It followed by starting Science Colleges, Agriculture Schools and ITI training institutes under the inspiring guidance of Dadasaheb Rawal. He was the first person to introduce Rural Electric Power Company at Dondaicha before the SEB (State Electricity Board) could lay lines here. He is also the first to start reforestation of this area with Juliflora Prosopis to make fuel wood available to villagers and also to ensure protection of the soil from erosion.

Vision:

It is UNIVERSAL truth that maize is amazing and, we are committed to excellence

giving products of UNIQUE quality to customer satisfaction.

Mission:

Our plant and machinery has been established on the strong foundation of modern

technology for refining of Maize and to manufacture finished products conforming to

the international quality standards. The plant and machinery are being operated by highly

qualified, experienced & dedicated people who monitor continuously the day-to-day

operations in maintaining the consistency of results in all the operations. The total

administrative and technical manpower is working under the guidelines of dynamic and

forward thinking Management.

Founder:

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 9

Company History

M/s. UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. Has achieved remarkable milestones during the history of last 30 years since its incorporation in 1973. The Company has successfully enhanced the production capacity of Maize Refining from 60 MT to 400 MT per day.

The product range has been also successfully expanded to cater the requirements of Food, Pharmaceutical, Textile, Paper & Adhesive industries. The process of new product development has been accomplished through the instantaneous efforts of different teams like Marketing, R & D, Engineering & Production. The Company’s R and D Laboratory is recognized by D.S.I.R., Govt. of India. The Company was awarded by OPPI as the “BEST VENDOR’ in the category of ‘Excipient Supplier” for the year 1998-99. The Company has a H.R.D. Centre for training the staff and workers on Total Quality Management, Productivity and ISO 9000.

The Company is thriving in sectors of Energy, Environment under the dynamic leadership of Management. The Company has sophisticated and full-fledged Effluent Treatment Plant along with Bio-Digestors in which Biogas is generated from the factory effluents. The Biogas is being utilized as the fuel for by-product driers and boilers and actively participating in the National Campaign of “SAVE ENERGY SAVE NATION”. The Company has also established Wind Mill to generate 0.6 M.W. power and also succeeded in establishing a Co-Generation Power plant for captive consumption. The Management is dedicated in the service of Mankind with the production and supply of quality products through Maize Refining industry.

Structure:

Chairman & Managing Director : USA -- Universal Starch-Chem Allied Ltd.

Hon'ble Shri.Sarkarsaheb Rawal

Director - Business Development Shri. Jaykumar J. Rawal - M.L.A.

Director - Business Administration

Shri. Rishikesh Rawal

Director Shri. Vikrant Rawal Chief Executive Officer Finance Advisor Mr. M.N. Patwari General Manager - R & D Mr. D.A. Patil General Manager - Q.A. Mr. G.P. Chaudhary General Manager – Engg

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 10

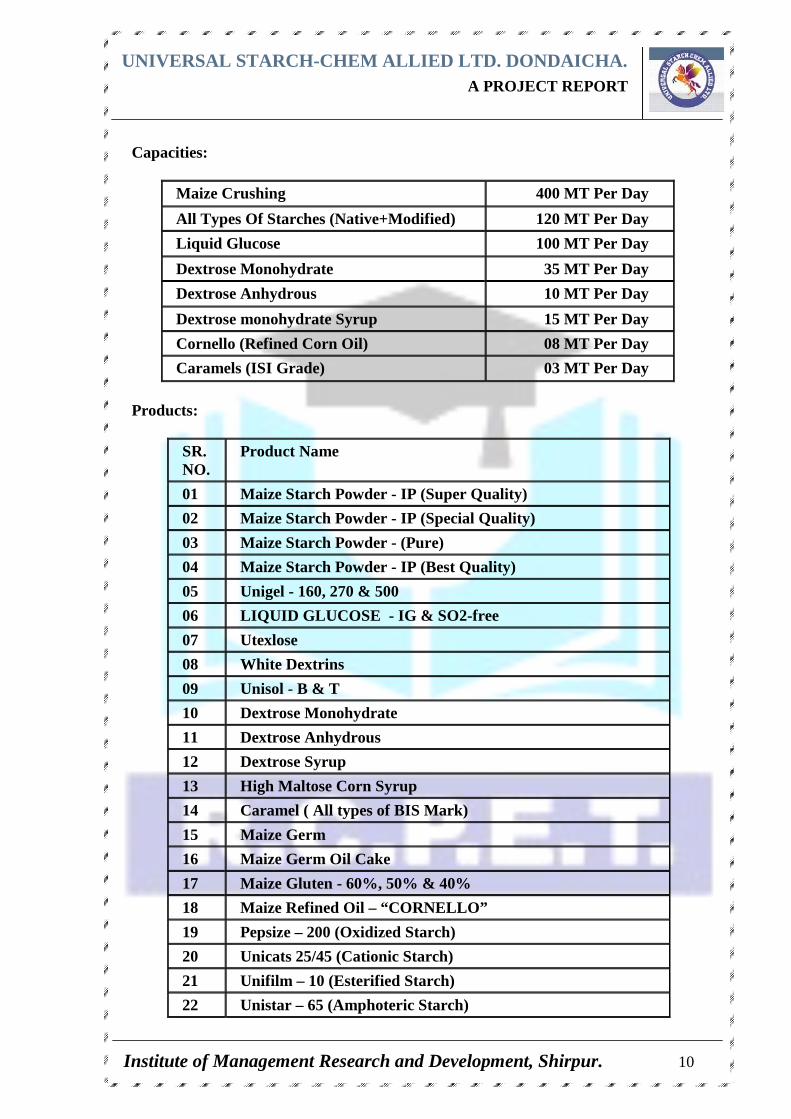

Capacities:

Maize Crushing 400 MT Per Day

All Types Of Starches (Native+Modified) 120 MT Per Day

Liquid Glucose 100 MT Per Day

Dextrose Monohydrate 35 MT Per Day

Dextrose Anhydrous 10 MT Per Day

Dextrose monohydrate Syrup 15 MT Per Day

Cornello (Refined Corn Oil) 08 MT Per Day

Caramels (ISI Grade) 03 MT Per Day

Products:

SR. NO.

Product Name

01 Maize Starch Powder - IP (Super Quality)

02 Maize Starch Powder - IP (Special Quality)

03 Maize Starch Powder - (Pure)

04 Maize Starch Powder - IP (Best Quality)

05 Unigel - 160, 270 & 500

06 LIQUID GLUCOSE - IG & SO2-free

07 Utexlose

08 White Dextrins

09 Unisol - B & T

10 Dextrose Monohydrate

11 Dextrose Anhydrous

12 Dextrose Syrup

13 High Maltose Corn Syrup

14 Caramel ( All types of BIS Mark)

15 Maize Germ

16 Maize Germ Oil Cake

17 Maize Gluten - 60%, 50% & 40%

18 Maize Refined Oil – “CORNELLO”

19 Pepsize – 200 (Oxidized Starch)

20 Unicats 25/45 (Cationic Starch)

21 Unifilm – 10 (Esterified Starch)

22 Unistar – 65 (Amphoteric Starch)

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 11

Working capital has been described as the

“Life blood of any business which is apt because it

constitutes a cyclically flowing stream through the

business.”

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 12

This section includes: INTRODUCTION :

The term working capital is commonly used for the capital required for day-to-day working in a business concern, such as for purchasing raw material, for meeting day-to-day expenditure on salaries, wages, rents rates, advertising etc. But there are much disagreement among various financial authorities (Financiers, accountants, businessmen and economists) as to the exact meaning of the term working capital.

DEFINITION AND CLASSIFICATION OF WORKING CAPITAL:

Working capital refers to the circulating capital required to meet the day to day operations of a business firm. Working capital may be defined by various authors as follows: 1. According to Weston & Brigham - “Working capital refers to a firm’s investment in short term assets, such as cash amounts receivables, inventories etc. 2. Working capital means current assets. - Mead, Baker and Malott 3. “The sum of the current assets is the working capital of the business” - J.S.Mill Working capital is defined as “the excess of current assets over current liabilities and provisions”. But as per accounting terminology, it is difference between the inflow and outflow of funds. In the Annual Survey of Industries (1961), working capital is defined to include “Stocks of materials, fuels, semi-finished goods including work-in-progress and finished goods and by-products; cash in hand and bank and the algebraic sum of sundry creditors as represented by (a) outstanding factory payments e.g. rent, wages, interest and dividend; b)purchase of goods and services; c) short-term loans and advances and sundry debtors comprising amounts due to the factory on account of sale of goods and services and advances towards tax payments”.

The term “working capital” is often referred to “circulating capital” which is frequently used to denote those assets which are changed with relative speed from one form to another i.e., starting from cash, changing to raw materials, converting into work-in-progress and finished products, sale of finished products and ending with realization of cash from debtors.

Working capital has been described as the “life blood of any business which is apt because it constitutes a cyclically flowing stream through the business”.

Working Capital may be classified in two ways a) Concept based working capital b) Time based working capital

Concepts of working capital

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 13

1. Gross Working Capital: It refers to the firm’s investment in total current or circulating assets. 2. Net Working Capital: The term “Net Working Capital” has been defined in two different ways: i. It is the excess of current assets over current liabilities. This is, as a matter of fact,

the most commonly accepted definition. Some people define it as only the difference between current assets and current liabilities. The former seems to be a better definition as compared to the latter.

ii. It is that portion of a firm’s current assets which is financed by long-term funds. 3. Permanent Working Capital: This refers to that minimum amount of investment in all current assets which is required at all times to carry out minimum level of business activities. In other words, it represents the current assets required on a continuing basis over the entire year. Tandon Committee has referred to this type of working capital as “Core current assets”. The following are the characteristics of this type of working capital:

1. Amount of permanent working capital remains in the business in one form or another. This is particularly important from the point of view of financing. The suppliers of such working capital should not expect its return during the life-time of the firm.

2. It also grows with the size of the business. In other words, greater the size of the business, greater is the amount of such working capital and vice versa. Permanent working capital is permanently needed for the business and therefore it should be financed out of long-term funds.

4. Temporary Working Capital : The amount of such working capital keeps on fluctuating from time to time on the basis of business activities. In other words, it represents additional current assets required at different times during the operating year. For example, extra inventory has to be maintained to support sales during peak sales period. Similarly, receivable also increase and must be financed during period of high sales. On the other hand investment in inventories, receivables, etc., will decrease in periods of depression.Suppliers of temporary working capital can expect its return during off season when it is not required by the firm. Hence, temporary working capital is generally financed from shortterm sources of finance such as bank credit. 5. Negative Working Capital: This situation occurs when the current liabilities exceed the current assets. It is an indication of crisis to the firm. Need for Working Capital Working capital is needed till a firm gets cash on sale of finished products. It depends on two factors: i. Manufacturing cycle i.e. time required for converting the raw material into finished

product; and ii. Credit policy i.e. credit period given to Customers and credit period allowed by

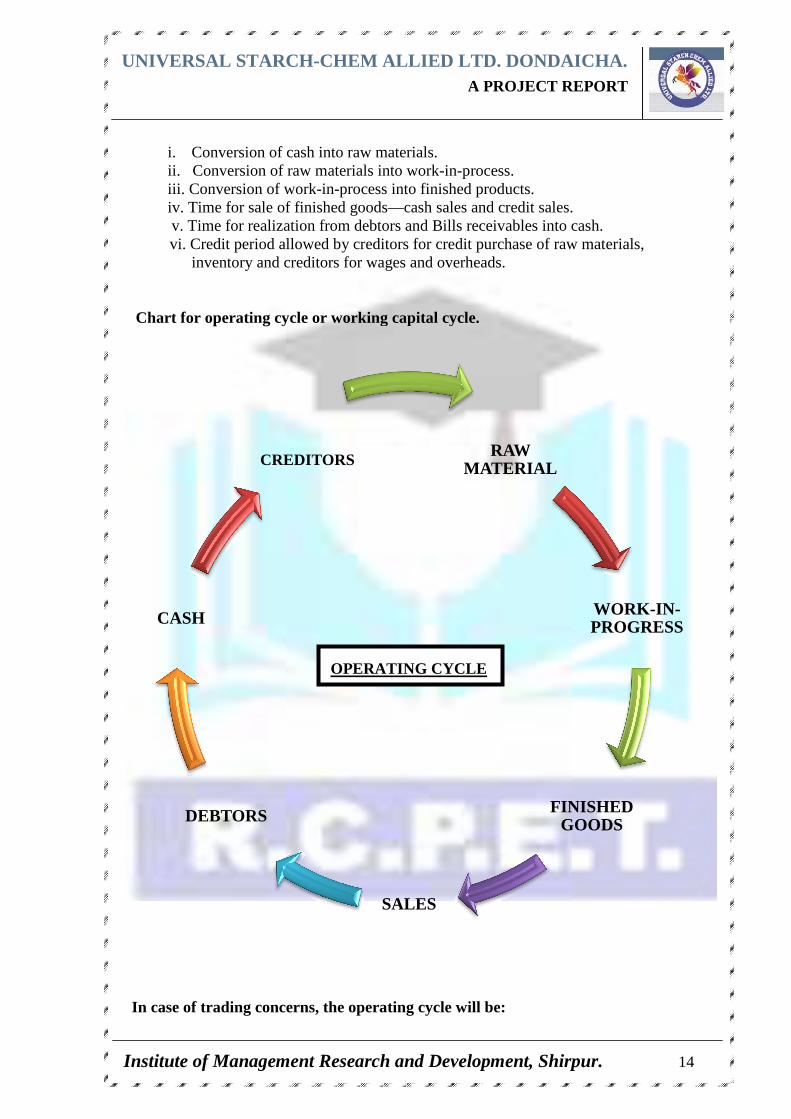

creditors. Thus, the sum total of these times is called an “Operating cycle” and it consists of the following six steps:

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

i. Conversion of cash into raw materials.ii. Conversion of raw materials into work

iii. Conversion of work iv. Time for sale of finished goods v. Time for realization

vi. Credit period allowed by creditors for credit purchase of raw materials, inventory and creditors for wages and overheads.

Chart for operating cycle or working capital cycle.

In case of trading concerns, the operating cycle will be:

DEBTORS

CASH

CREDITORS

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Conversion of cash into raw materials. Conversion of raw materials into work-in-process.

of work-in-process into finished products. for sale of finished goods—cash sales and credit sales.

realization from debtors and Bills receivables into cash.period allowed by creditors for credit purchase of raw materials,

creditors for wages and overheads.

cycle or working capital cycle.

In case of trading concerns, the operating cycle will be:

RAW MATERIAL

FINISHED GOODS

SALES

CREDITORS

OPERATING CYCLE

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 14

s. from debtors and Bills receivables into cash.

period allowed by creditors for credit purchase of raw materials,

WORK-IN-PROGRESS

FINISHED GOODS

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

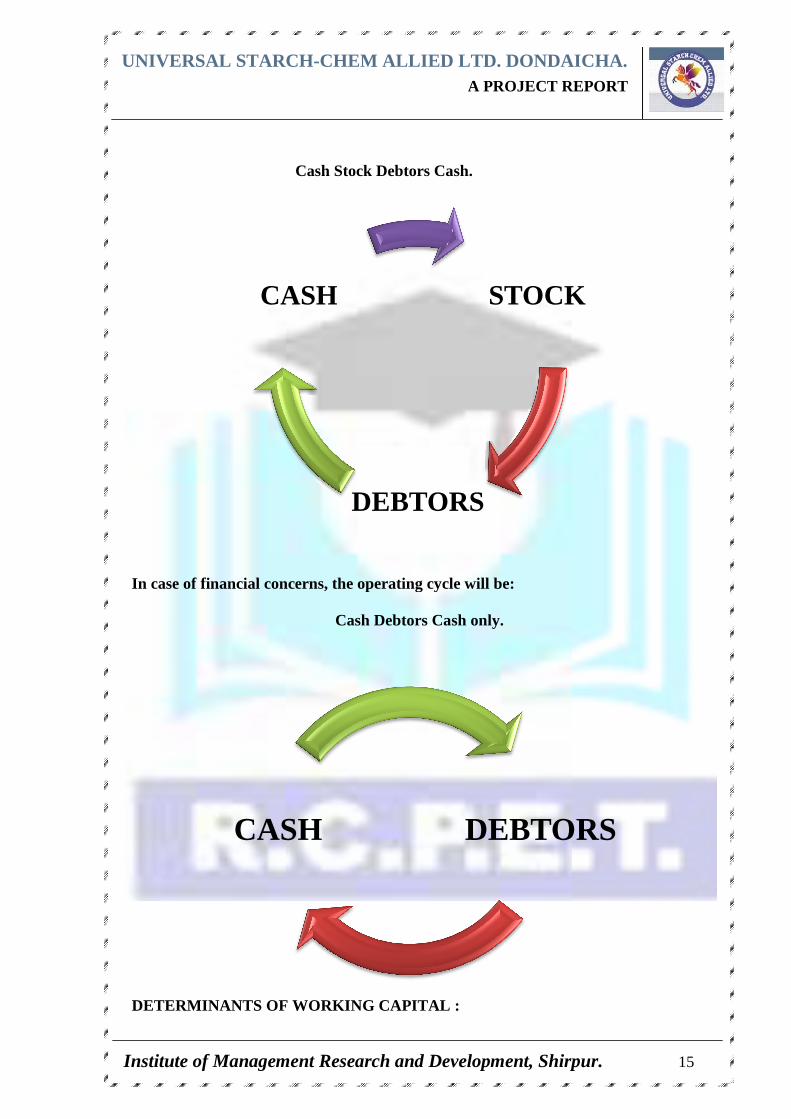

In case of financial concerns, the operating cycle will be:

DETERMINANTS OF WORKING CAPITAL :

CASH

CASH

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Cash Stock Debtors Cash.

In case of financial concerns, the operating cycle will be:

Cash Debtors Cash only.

DETERMINANTS OF WORKING CAPITAL :

STOCK

DEBTORS

CASH

DEBTORSCASH

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 15

STOCK

DEBTORS

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 16

The factors influencing the working capital decisions of a firm may be classified as two groups, such as internal factors and external factors. The internal factors includes, nature of business size of business, firm’s product policy, credit policy, dividend policy, and access to money and capital markets, growth and expansion of business etc. The external factors include business fluctuations, changes in the technology, infrastructural facilities, import policy and the taxation policy etc. These factors are discussed in brief in the following lines. I. Internal Factors 1. Nature and size of the business The working capital requirements of a firm are basically influenced by the nature and size of the business. Size may be measured in terms of the scale of operations. A firm with larger scale of operations will need more working capital than a small firm. Similarly, the nature of the business - influence the working capital decisions. Trading and financial firms have less investment in fixed assets. But require a large sum of money to be invested in working capital. Retail stores, business units require larger amount of working capital, whereas, public utilities need less working capital and more funds to invest in fixed assets. 2. Firm’s production policy The firm’s production policy (manufacturing cycle) is an important factor to decide the working capital requirement of a firm. The production cycle starts with the purchase and use of raw material and completes with the production of finished goods. On the other hand production policy is uniform production policy or seasonal production policy etc., also influences the working capital decisions. Larger the manufacturing cycle and uniform production policy – larger will be the requirement of working capital. The working capital requirement will be higher with varying production schedules in accordance with the changing demand. 3. Firm’s credit policy The credit policy of a firm influences credit policy of working capital. A firm following liberal credit policy to all customers requires funds. On the other hand, the firm adopting strict credit policy and grant credit facilities to few potential customers will require less amount of working capital. 4. Availability of credit The working capital requirements of a firm are also affected by credit terms granted by its suppliers – i.e. creditors. A firm will need less working capital if liberal credit terms are available to it. Similarly, the availability of credit from banks also influences the working capital needs of the firm. A firm, which can get bank credit easily on favorable conditions, will be operated with less working capital than a firm without such a facility. 5. Growth and expansion of business Working capital requirement of a business firm tend to increase in correspondence with growth in sales volume and fixed assets. A growing firm may need funds to invest in fixed assets in order to sustain its growing production and sales. This will, in turn,

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 17

increase investment in current assets to support increased scale of operations. Thus, a growing firm needs additional funds continuously. 6. Profit margin and dividend policy The magnitude of working capital in a firm is dependent upon its profit margin and dividend policy. A high net profit margin contributes towards the working capital pool. To the extent the net profit has been earned in cash, it becomes a source of working capital. This depends upon the dividend policy of the firm. Distribution of high proportion of profits in the form of cash dividends results in a drain on cash resources and thus reduces company’s working capital to that extent. The working capital position of the firm is strengthened if the management follows conservative dividend policy and vice versa. 7. Operating efficiency of the firm Operating efficiency means the optimum utilisation of a firm’s resources at minimum cost. If a firm successfully controls operating cost, it will be able to improve net profit margin which, will, in turn, release greater funds for working capital purposes. 8. Co-ordinating activities in firm The working capital requirements of a firm are depend upon the co-ordination between production and distribution activities. The greater and effective the co-ordinations, the pressure on the working capital will be minimized. In the absence of co-ordination, demand for working capital is reduced. II. External Factors 1. Business fluctuations Most firms experience fluctuations in demand for their products and services. These business variations affect the working capital requirements. When there is an upward swing in the economy, sales will increase, correspondingly, the firm’s investment in inventories and book debts will also increase. Under boom, additional investment in fixed assets may be made by some firms to increase their productive capacity. This act of the firm will require additional funds. On the other hand when, there is a decline in economy, sales will come down and consequently the conditions, the firm try to reduce their short-term borrowings. Similarly the seasonal fluctuations may also affect the requirement of working capital of a firm. 2. Changes in the technology The technological changes and developments in the area of production can have immediate effects on the need for working capital. If the firm wish to install a new machine in the place of old system, the new system can utilise less expensive raw materials, the inventory needs may be reduced there by working capital needs. 3. Import policy Import policy of the Government may also affect the levels of working capital of a firm since they have to arrange funds for importing goods at specified times.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 18

4. Infrastructural facilities The firms may require additional funds to maintain the levels of inventory and other current assets, when there is good infrastructural facilities in the company like, transportation and communications. 5. Taxation policy The tax policies of the Government will influence the working capital decisions. If the Government follow regressive taxation policy, i.e. imposing heavy tax burdens on business firms, they are left with very little profits for distribution and retention purpose. Consequently the firm has to borrow additional funds to meet their increased working capital needs. When there is a liberalized tax policy, the pressure on working capital requirement is minimized. Thus the working capital requirements of a firm are influenced by the internal and external factors. MEASUREMENT OF WORKING CAPITAL : There are 3 methods for assessing the working capital requirement as explained below: a) Percent of Sales Method Based on the past experience, some percentage of sale may be taken for determining the quantum of working capital b) Regression Analysis Method The relationship between sales and working capital and its various components may be plotted on Scatter diagram and the average percentage of past 5 years may be ascertained. This average percentage of sales may be taken as working capital. Similar exercise may be carried out at the beginning of the year for assessing the working capital requirement. This method is suitable for simple as well as complex situations. c) Operating Cycle Method As a first step, we have to compute the operating cycle as follows: i) Inventory period: Number of days consumption in stock = I + M_ 365 Where I = Average inventory during the year. M = Materials consumed during the year. ii) Work-in-process: Number of days of work-in-process = W + _ K_ 365 Where W = Average work-in-process during the year. K = Cost of work-in-process i.e., Material + Labour + Factory overheads. iii) Finished products inventory period: G ÷ F_ 365 Where G = Average finished products inventory during the year F = Cost of finished goods sold during the year.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 19

iv) Average collection period of Debtors: D ÷ F_ 365 Where D = Average Debtors balances during the year. S = Credit sales during the year. v) Credit period allowed by Suppliers: C ÷ P_ 365 Where C= Average creditors’ balances during the year. P = credit purchases during the year. vi) Minimum cash balance to be kept daily. Formula: O.C. = M + W + F + D – C Note: It is also known as working capital cycle. Operating cycle is the total time gap between the purchase of raw material and the receipt from Debtors. Importance or Advantages of Adequate Working Capital Working capital is the life blood and nerve centre of a business. Just as circulation of blood is essential in the human body for maintaining life, working capital is very essential to maintain the smooth running of a business. No business can run successfully without an adequate amount of working capital. The main advantages of maintaining adequate amount of working capital are as follows: 1. Solvency of the business: Adequate working capital helps in maintaining solvency of the business by providing uninterrupted flow of production. 2. Goodwill: Sufficient working capital enables a business concern to make prompt payments and hence helps in creating and maintaining goodwill. 3. Easy loans: A concern having adequate working capital, high solvency and good

credit standing can arrange loans from banks and other on easy and favourable terms. 4. Cash Discounts: Adequate working capital also enables a concern to avail cash discounts on the purchases and hence it reduces costs. 5. Regular supply of raw materials: Sufficient working capital ensures regular supply of raw materials and continuous production. 6. Regular payment of salaries, wages and other day-to-day commitments:

A company which has ample working capital can make regular payment of salaries, wages and other day-to-day commitments which raises the morale of its employees, increases their efficiency, reduces wastages and costs and enhances production and profits.

7. Exploitation of favorable market conditions: Only concerns with adequate working capital can exploit favorable market conditions such as purchasing its requirements in bulk when the prices are lower and by holding its inventories for higher prices.

8. Ability to face Crisis: Adequate working capital enables a concern to face business crisis in emergencies such as depression because during such periods, generally, there is much pressure on working capital.

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

9.Quick and Regular return on Investments:return on his investments. Sufficiency of working capital enables a concern to pay quick and regular dividends to its investors as there may not be much pressure toplough back profits. This gains the confidence of its investors and creates a favourablemarket to raise additional funds i.e., the future.

10. High morale: Adequacy of working capital creates an environment of security, confidence, high morale and creates overall efficiency in a business.

Importance or Advanta

Excess or Inadequate Working Capital

from Banks

Efficient

Supply Chain

Management

Regular

Payments of

Salaries &

Wages

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Quick and Regular return on Investments: Every Investor wants a quick and return on his investments. Sufficiency of working capital enables a concern to pay quick and regular dividends to its investors as there may not be much pressure toplough back profits. This gains the confidence of its investors and creates a favourable

rket to raise additional funds i.e., the future. Adequacy of working capital creates an environment of security,

confidence, high morale and creates overall efficiency in a business.

Importance or Advantages of Adequate Working Capital

Excess or Inadequate Working Capital

Working

Capital

Payments to

Suppliers

Planning and

Forecasting

Increase in

Efficiency

Easy Loan

from Banks

Payments of

Salaries &

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 20

Every Investor wants a quick and regular return on his investments. Sufficiency of working capital enables a concern to pay quick and regular dividends to its investors as there may not be much pressure to plough back profits. This gains the confidence of its investors and creates a favourable

Adequacy of working capital creates an environment of security, confidence, high morale and creates overall efficiency in a business.

ges of Adequate Working Capital

Planning and

Forecasting

Creates

Goodwill

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 21

Every business concern should have adequate working capital to run its business operations. It should have neither redundant or excess working capital nor inadequate nor shortage of working capital. Both excess as well as short working capital positions are bad for any business. However, out of the two, it is the inadequacy of working capital which is more dangerous from the point of view of the firm. Disadvantages of Redundant or Excessive Working Capital 1. Excessive Working Capital means ideal funds which earn no profits for the business

and hence the business cannot earn a proper rate of return on its investments. 2. When there is a redundant working capital, it may lead to unnecessary purchasing and

accumulation of inventories causing more chances of theft, waste and losses. 3. Excessive working capital implies excessive debtors and defective credit policy

which may cause higher incidence of bad debts. 4. It may result into overall inefficiency in the organization. 5. When there is excessive working capital, relations with banks and other financial

institutions may not be maintained. 6. Due to low rate of return on investments, the value of shares may also fall. 7. The redundant working capital gives rise to speculative transactions. Disadvantages or Dangers of Inadequate Working Capital 1. A concern which has inadequate working capital cannot pay its short-term liabilities

in time. Thus, it will lose its reputation and shall not be able to get good credit facilities.

2. It cannot buy its requirements in bulk and cannot avail of discounts, etc. 3. It becomes difficult for the firm to exploit favourable market conditions and undertake

profitable projects due to lack of working capital. 4. The firm cannot pay day-to-day expenses of its operations and its creates

inefficiencies, increases costs and reduces the profits of the business. 5. It becomes impossible to utilize efficiently the fixed assets due to non-availability of

liquid funds. 6. The rate of return on investments also falls with the shortage of working capital. MANAGEMENT OF WORKING CAPITAL: Working Capital Management involves management of different components of working capital such as cash, inventories, accounts receivable, creditors etc. A brief description follows regarding the various issues involved in the management of each of the above components of working capital. INVENTORY MANAGEMENT: Inventory constitutes an important item in the working capital of many business concerns.Net working capital is the difference between current assets and current liabilities. Inventory is a major item of current assets. The term inventory refers to the stocks of the product of a firm is offering for sale and the components that make up the product Inventory is stores of goods and stocks. This includes raw materials, work-in-process and finished goods. Raw materials consist of those units or input which are used to manufactured goods that require further processing to become finished goods. Finished

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 22

goods are products ready for sale. The classification of inventories and the levels of the components vary from organisaion to organisation depending upon the nature of business. For example steel is a finished product for a steel industry, but raw material for an automobile manufacturer. Thus, inventory may be defined as “Stock of goods that is held for future use”. Since inventories constitute about 50 to 60 percent of current assets, the management of inventories is crucial to successful working capital management. Working capital requirements are influenced by inventory holding. Hence, the need for effective and efficient management of inventories. A good inventory management is important to the successful operations of most organisaions, unfortunately the importance of inventory is not always appreciated by top management. This may be due to a failure to recognize the link between inventories and achievement of organizational goals or due to ignorance of the impact that inventories can have on costs and profits. Inventory management refers to an optimum investment in inventories. It should neither be too low to effect the production adversely nor too high to block the funds unnecessarily. Excess investment in inventories is unprofitable for the business. Both excess and inadequate investment in inventories is not desirable. The firm should operate within the two danger points. The purpose of inventory management is to determine and maintain the optimum level of inventory investment. Techniques of Inventory Control The following are the various measures of selective control of inventory: F. Inventory Turnover Ratio i) Inventory Turnover Ratio: __ Cost of goods sold __ average total inventories. The higher the ratio, more the efficiency of the firm ii) Work in process turnover ratio = Cost of goods sold ________ Average inventory of finished goods at costs Here, in this ratio also higher the ratio, more the efficiency of the firm. iii) Weeks inventory finished goods on hand = _________Finished Goods______ Weekly of finished sales goods The ratio reveals that the lower the ratio, the higher the efficiency of the firm iv) Weeks raw material on order = ______Raw material on order_______ Weekly consumption of raw material This ratio indicates that the lower the ratio, the higher the efficiency of the firm. v) Average age of raw material inventory = _Average raw material inventory at cost_ Average daily purchases of raw material This ratio says that the lower the ratio the higher the efficiency of the firm.

vi) Average age of finished goods inventory

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

This ratio comes that the lower

i) Out of stock index =

This ratio indicates the lower the ratio higher the efficiency of the firm.

ii) Spare parts index = Value of This ratio reveals that the higher the ratio the more the efficiency of the firm.

CASH MANAGEMENT :

Cash management is one of the key areas of working capital management. Cash is the most liquid current assets. Cash is the common denominator to which all current assets can be reduced because the other major liquid assets, i.e. receivable and inventory geeventually converted into cash. This underlines the importance of cash management. The term “Cash” with reference to management of cash is used in two ways. In a narrow sense cash refers coins, currency, cheques, drafts and deposits in banks. The broader view of cash includes near cash assets such as marketable securities and time deposits in banks.The reason why these near cash assets are included in cash is that they can readily be converted into cash. Usually, excess cash is invested in marketable securities as it contributes to profitability.of current assets. Every firm should have adequate cash, neither more nor less. Inadequate cash will lead to production interruptions, while excessive cash remains iimpair profitability. Hence, the need for cash management. The cash management assumes significance for the following reasons. Significance: 1. Cash planning - Cash is the most important as well as the least unproductive of all

current assets. Though, it is necessary to meet the firm’s obligations, yet idle cash earns nothing. Therefore, it is essential to have a sound cash planning neither excess nor inadequate.

2. Management of cash flowsSynchronization between cash inflows and cash outflows rarely happens. Sometimes, the cash inflows will be more than outflows because of receipts from debtors, and cash sales in huge amounts. At other times, cash outflows exceed inflows due to payment of taxes, interest and dividends cash management.

3. Maintaining optimum cash balancebalance. The management should also consider the factors determining and influencing the cash balances at various point of time. The cost of excess cash and danger of

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

= __ Average finished goods invetory at cost_____ Average cost of finished goods manufactured per day

This ratio comes that the lower the ratio the higher the efficiency of the firm.

_No. of times out of stock_ No. of items requisitioned This ratio indicates the lower the ratio higher the efficiency of the firm.

Value of spare parts inventory Value of capital equipment

This ratio reveals that the higher the ratio the more the efficiency of the firm.

CASH MANAGEMENT :

Cash management is one of the key areas of working capital management. Cash is the most liquid current assets. Cash is the common denominator to which all current assets can be reduced because the other major liquid

receivable and inventory get eventually converted into cash. This underlines the importance of cash management. The term “Cash” with reference to management of cash is used in two ways. In a narrow sense cash refers coins, currency, cheques, drafts and deposits in

der view of cash includes near cash assets such as marketable securities and time deposits in banks.The reason why these near cash assets are included in cash is that they can readily be converted into cash. Usually, excess cash is invested in marketable ecurities as it contributes to profitability. Cash is one of the most important components

of current assets. Every firm should have adequate cash, neither more nor less. Inadequate cash will lead to production interruptions, while excessive cash remains iimpair profitability. Hence, the need for cash management. The cash management assumes significance for the following reasons.

Cash is the most important as well as the least unproductive of all current assets. Though, it is necessary to meet the firm’s obligations, yet idle cash earns nothing. Therefore, it is essential to have a sound cash planning neither excess

2. Management of cash flows - This is another important aspect of cash management. between cash inflows and cash outflows rarely happens. Sometimes,

the cash inflows will be more than outflows because of receipts from debtors, and cash ales in huge amounts. At other times, cash outflows exceed inflows due to payment of

taxes, interest and dividends etc. Hence, the cash flows should be managed for better

3. Maintaining optimum cash balance - Every firm should maintain optThe management should also consider the factors determining and influencing

the cash balances at various point of time. The cost of excess cash and danger of

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 23

Average finished goods invetory at cost_____ Average cost of finished goods manufactured per day

the ratio the higher the efficiency of the firm.

This ratio indicates the lower the ratio higher the efficiency of the firm.

This ratio reveals that the higher the ratio the more the efficiency of the firm.

Cash management is one of the key areas of working capital management. Cash is the most liquid current assets. Cash is the common denominator to which all current assets

to

time deposits in banks.The reason why these near cash assets are included in cash is that they can readily be converted into cash. Usually, excess cash is invested in marketable

Cash is one of the most important components of current assets. Every firm should have adequate cash, neither more nor less. Inadequate cash will lead to production interruptions, while excessive cash remains idle and will impair profitability. Hence, the need for cash management. The cash management

Cash is the most important as well as the least unproductive of all current assets. Though, it is necessary to meet the firm’s obligations, yet idle cash earns nothing. Therefore, it is essential to have a sound cash planning neither excess

This is another important aspect of cash management. between cash inflows and cash outflows rarely happens. Sometimes,

the cash inflows will be more than outflows because of receipts from debtors, and cash ales in huge amounts. At other times, cash outflows exceed inflows due to payment of

Hence, the cash flows should be managed for better

Every firm should maintain optimum cash The management should also consider the factors determining and influencing

the cash balances at various point of time. The cost of excess cash and danger of

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 24

inadequate cash should be matched to determine the optimum level of cash balances. 4. Investment of excess cash - The firm has to invest the excess or idle funds in short

term securities or investments to earn profits as idle funds earn nothing. This is one of the important aspects of management of cash. Thus, the aim of cash management is to maintain adequate cash balances at one hand and to use excess cash in some profitable way on the other hand.

Motives Motives or desires for holding cash refer to various purposes. The purpose may be different from person to person and situation to situation. There are four important motives to hold cash. a. Transactions motive - This motive refers to the holding of cash, to meet routine cash requirements in the ordinary course of business. A firm enters into a number of transactions which requires cash payment. For example, purchase of materials, payment of wages, salaries, taxes, interest etc. Similarly, a firm receives cash from cash sales, collections from debtors, return on investments etc. But the cash inflows and cash outflows do not perfectly synchronize. Sometimes, cash receipts are more than payments while at other times payments exceed receipts. The firm must have to maintain sufficient (funds) cash balance if the payments are more than receipts. Thus, the transactions motive refers to the holding of cash to meet expected obligations whose timing is not perfectly matched with cash receipts. Though, a large portion of cash held for transactions motive is in the form of cash, a part of it may be invested in marketable securities whose maturity conform to the timing of expected payments such as dividends, taxes etc. b. Precautionary motive - Apart from the non-synchronization of expected cash receipts and payments in the ordinary course of business, a firm may be failed to pay cash for unexpected contingencies. For example, strikes, sudden increase in cost of raw materials etc. Cash held to meet these unforeseen situations is known as precautionary cash balance and it provides a caution against them. The amount of cash balance under precautionary motive is influenced by two factors i.e. predictability of cash flows and the availability of short term credit. The more unpredictable the cash flows, the greater the need for such cash balances and vice versa. If the firm can borrow at short-notice, it will need a relatively small balance to meet contingencies and vice versa. Usually precautionary cash balances are invested in marketable securities so that they contribute something to profitability. c. Speculative motive - Sometimes firms would like to hold cash in order to exploit, the profitable opportunities as and when they arise. This motive is called as speculative motive. For example, if the firm expects that the material prices will fall, it can delay the purchases and make purchases in future when price actually declines. Similarly, with the hope of buying securities when the interest rate is expected to decline, the firm will hold cash. By and large, firms rarely hold cash for speculative purposes. d. Compensation motive - This motive to hold cash balances is to compensate banks and other financial institutes for providing certain services and loans. Banks provide a variety of services to business firms like clearance of cheques, drafts, transfer of funds etc. Banks charge a commission or fee for their services to the customers as indirect compensation.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 25

Customers are required to maintain a minimum cash balance at the bank. This balance cannot be used for transaction purposes. Banks can utilise the balances to earn a return to compensate their cost of services to the customers. Such balances are compensating balances. These balances are also required by some loan agreements between a bank and its customers. Banks require a chest to maintain a minimum cash balance in his account to compensate the bank when the supply of credit is restricted and interest rates are rising. Thus cash is required to fulfill the above motives. Out of the four motives of holding cash balances, transaction motive and compensation motives are very important. Business firms usually do not speculate and need not have speculative balances. The requirement of precautionary balances can be met out of short-term borrowings. Objectives The basic objectives of cash management are (i) to make the payments when they become due and (ii) to minimize the cash balances. The task before the cash management is to reconcile

the two conflicting nature of objectives. 1. Meeting the payments schedule - The basic objective of cash management is to meet the payment schedule. In the normal course of business, firms have to make payments of cash to suppliers of raw materials, employees and so on regularly. At the same time firm will be receiving cash on a regular basis from cash sales and debtors. Thus, every firm should have adequate cash to meet the payments schedule. In other words, the firm should be able to meet the obligations when they become due. The firm can enjoy certain advantages associated with maintaining adequate cash. They are: a. Insolvency - The question of insolvency does not arise as the firm will be able to meet

its obligations. b. Good relations - Adequate cash balance in the business firm helps in developing good

relations with creditors and suppliers of raw materials. c. Credit worthiness - The maintenance of adequate cash balances increase the credit

worthiness of the firm. Consequently it will be able to purchase raw materials and procure credit with favorable terms and conditions.

d. Availing discount facilities - The firm can avail the discounts offered by the creditors for payments before the due date.

e. To meet unexpected facilities - The firm can easily meet the unexpected cash expenditure in situations like strikes, competition from customers etc. with little strain. So, every firm should have adequate cash balances for effective cash management.

2. Minimising funds committed to cash balances - The second important objective of cash management is to minimise cash balance. In minimizing the cash balances two conflicting aspects have to be reconciled. A high level of cash balances will ensure prompt payment together with all advantages, but at the same time, cash is a non-earning asset and the larger balances of cash impair profitability. On the other hand, a low level of cash balance may lead to the inability of the firm to meet the payment schedule. Thus the objective of cash management would be to have an optimum cash balance. Factors determining cash needs - Maintenance of optimum level of cash is the main problem of cash management. The level of cash holding differs from industry to industry,

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 26

organization to organisation. The factors determining the cash needs of the industry is explained as follows: i. Matching of cash flows - The first and very important factor determining the level of

cash requirement is matching cash inflows with cash outflows. If the receipts and payments are perfectly coincide or balance each other, there would be no need for cash balances. The need for cash management therefore, due to the non-synchronization of cash receipts and disbursements. For this purpose, the cash inflows and outflows have to be forecast over a period of time say 12 months with the help of cash budget. The cash budget will pin point the months when the firm will have an excess or shortage of cash.

ii. Short costs - Short costs are defined as the expenses incurred as a result of shortfall of cash such as unexpected or expected shortage of cash balances to meet the requirements. The short costs includes, transaction costs associated with raising cash to overcome the shortage, borrowing costs associated with borrowing to cover the shortage i.e. interest on loan, loss of trade-discount, penalty rates by banks to meet a shortfall in compensating, cash balances and costs associated with deterioration of the firm’s credit rating etc. which is reflected in higher bank charges on loans, decline in sales and profits.

iii. Cost of cash on excess balances - One of the important factors determining the cash needs is the cost of maintaining cash balances i.e. excess or idle cash balances. The cost of maintaining excess cash balance is called excess cash balance cost. If large funds are idle, the implication is that the firm has missed opportunities to invest and thereby lost interest. This is known as excess cost. Hence the cash management is necessary to maintain an optimum balance of cash.

iv. Uncertainty in business - Uncertainty plays a key role in cash management, because cash flows cannot be predicted with complete accuracy. The first requirement of cash management is a precautionary cushion to cope with irregularities in cash flows, unexpected delays in collections and disbursements, defaults and expected cash needs the uncertainty can be overcome through accurate forecasting of tax payments, dividends, capital expenditure etc. and ability of the firm to borrow funds through over draft facility.

v. Cost of procurement and management of cash - The costs associated with establishing and operating cash management staff and activities determining the cash needs of a business firm. These costs are generally fixed and are accounted for by salary, storage and handling of securities etc. The above factors are considered to determine the cash needs of a business firm.

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 27

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 28

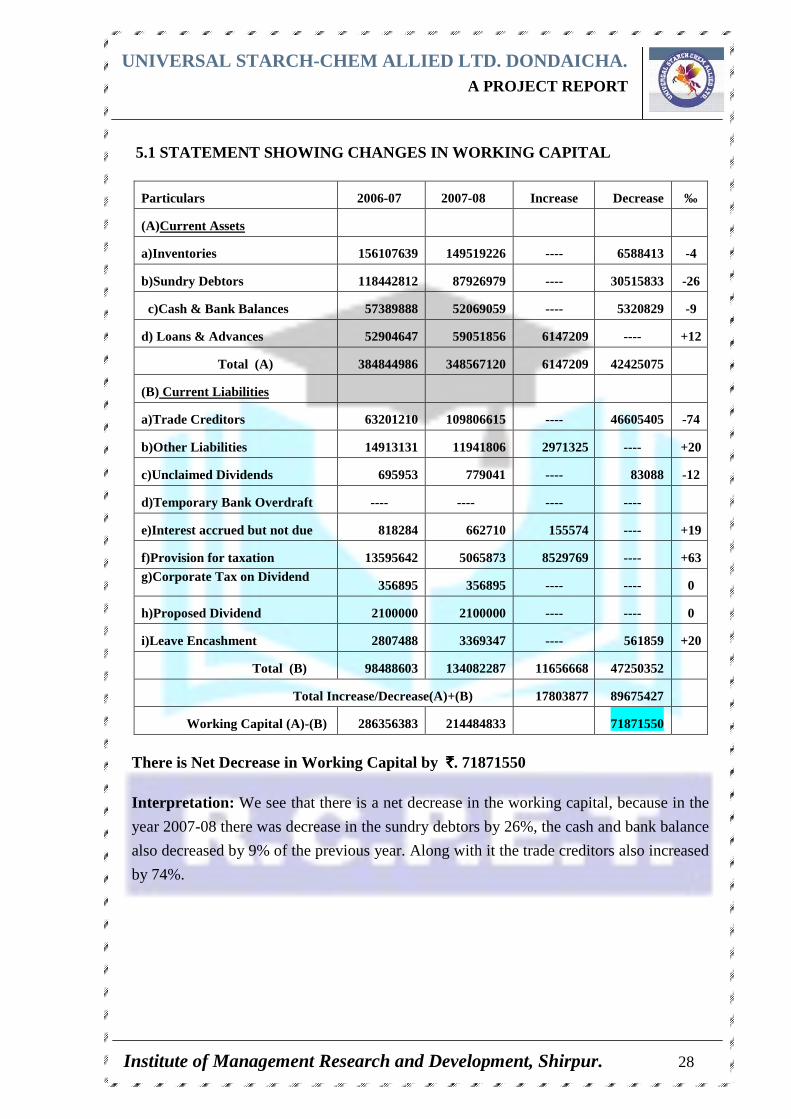

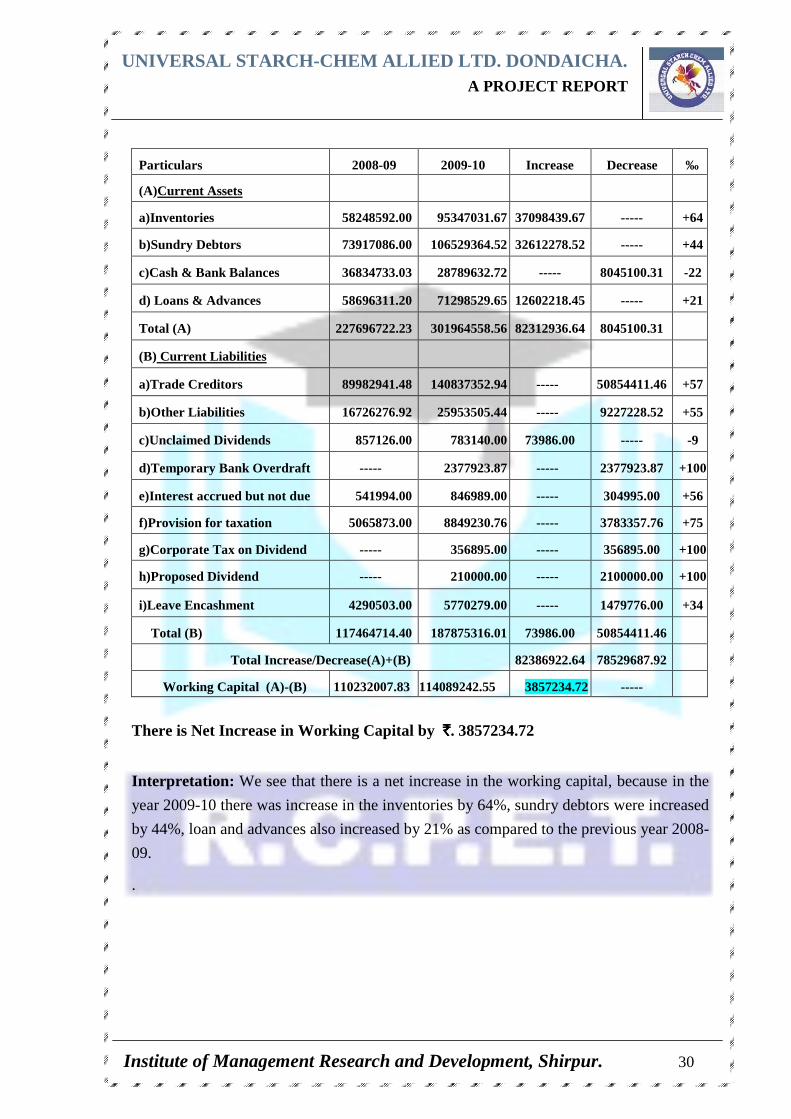

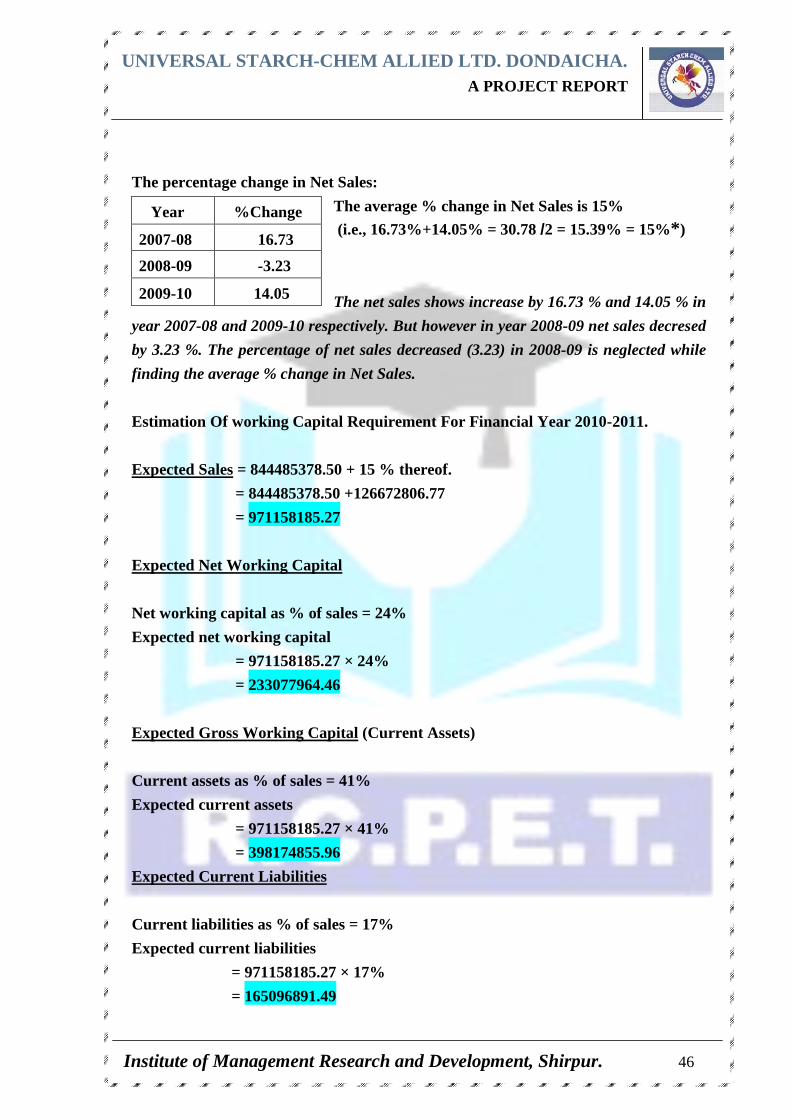

5.1 STATEMENT SHOWING CHANGES IN WORKING CAPITA L

There is Net Decrease in Working Capital by ̀̀̀̀. 71871550

Interpretation: We see that there is a net decrease in the working capital, because in the

year 2007-08 there was decrease in the sundry debtors by 26%, the cash and bank balance

also decreased by 9% of the previous year. Along with it the trade creditors also increased

by 74%.

Particulars 2006-07 2007-08 Increase Decrease ‰

(A)Current Assets

a)Inventories 156107639 149519226 ---- 6588413 -4

b)Sundry Debtors 118442812 87926979 ---- 30515833 -26

c)Cash & Bank Balances 57389888 52069059 ---- 5320829 -9

d) Loans & Advances 52904647 59051856 6147209 ---- +12

Total (A) 384844986 348567120 6147209 42425075

(B) Current Liabilities

a)Trade Creditors 63201210 109806615 ---- 46605405 -74

b)Other Liabilities 14913131 11941806 2971325 ---- +20

c)Unclaimed Dividends 695953 779041 ---- 83088 -12

d)Temporary Bank Overdraft ---- ---- ---- ----

e)Interest accrued but not due 818284 662710 155574 ---- +19

f)Provision for taxation 13595642 5065873 8529769 ---- +63 g)Corporate Tax on Dividend

356895 356895 ---- ---- 0

h)Proposed Dividend 2100000 2100000 ---- ---- 0

i)Leave Encashment 2807488 3369347 ---- 561859 +20

Total (B) 98488603 134082287 11656668 47250352

Total Increase/Decrease(A)+(B) 17803877 89675427

Working Capital (A)-(B) 286356383 214484833 71871550

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 29

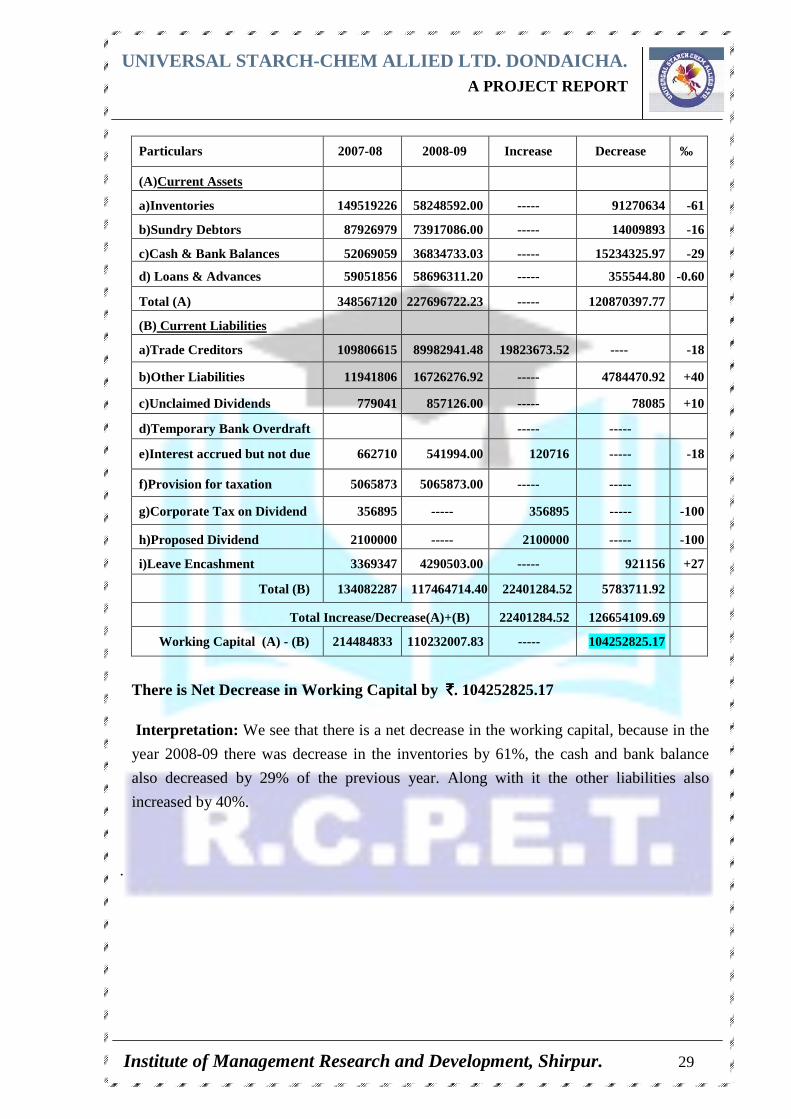

There is Net Decrease in Working Capital by ̀̀̀̀. 104252825.17

Interpretation: We see that there is a net decrease in the working capital, because in the

year 2008-09 there was decrease in the inventories by 61%, the cash and bank balance

also decreased by 29% of the previous year. Along with it the other liabilities also

increased by 40%.

.

Particulars 2007-08 2008-09 Increase Decrease ‰

(A)Current Assets

a)Inventories 149519226 58248592.00 ----- 91270634 -61

b)Sundry Debtors 87926979 73917086.00 ----- 14009893 -16

c)Cash & Bank Balances 52069059 36834733.03 ----- 15234325.97 -29

d) Loans & Advances 59051856 58696311.20 ----- 355544.80 -0.60

Total (A) 348567120 227696722.23 ----- 120870397.77

(B) Current Liabilities

a)Trade Creditors 109806615 89982941.48 19823673.52 ---- -18

b)Other Liabilities 11941806 16726276.92 ----- 4784470.92 +40

c)Unclaimed Dividends 779041 857126.00 ----- 78085 +10

d)Temporary Bank Overdraft ----- -----

e)Interest accrued but not due 662710 541994.00 120716 ----- -18

f)Provision for taxation 5065873 5065873.00 ----- -----

g)Corporate Tax on Dividend 356895 ----- 356895 ----- -100

h)Proposed Dividend 2100000 ----- 2100000 ----- -100

i)Leave Encashment 3369347 4290503.00 ----- 921156 +27

Total (B) 134082287 117464714.40 22401284.52 5783711.92

Total Increase/Decrease(A)+(B) 22401284.52 126654109.69

Working Capital (A) - (B) 214484833 110232007.83 ----- 104252825.17

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 30

There is Net Increase in Working Capital by ̀̀̀̀ . 3857234.72

Interpretation: We see that there is a net increase in the working capital, because in the

year 2009-10 there was increase in the inventories by 64%, sundry debtors were increased

by 44%, loan and advances also increased by 21% as compared to the previous year 2008-

09.

.

Particulars 2008-09 2009-10 Increase Decrease ‰

(A)Current Assets

a)Inventories 58248592.00 95347031.67 37098439.67 ----- +64

b)Sundry Debtors 73917086.00 106529364.52 32612278.52 ----- +44

c)Cash & Bank Balances 36834733.03 28789632.72 ----- 8045100.31 -22

d) Loans & Advances 58696311.20 71298529.65 12602218.45 ----- +21

Total (A) 227696722.23 301964558.56 82312936.64 8045100.31

(B) Current Liabilities

a)Trade Creditors 89982941.48 140837352.94 ----- 50854411.46 +57

b)Other Liabilities 16726276.92 25953505.44 ----- 9227228.52 +55

c)Unclaimed Dividends 857126.00 783140.00 73986.00 ----- -9

d)Temporary Bank Overdraft ----- 2377923.87 ----- 2377923.87 +100

e)Interest accrued but not due 541994.00 846989.00 ----- 304995.00 +56

f)Provision for taxation 5065873.00 8849230.76 ----- 3783357.76 +75

g)Corporate Tax on Dividend ----- 356895.00 ----- 356895.00 +100

h)Proposed Dividend ----- 210000.00 ----- 2100000.00 +100

i)Leave Encashment 4290503.00 5770279.00 ----- 1479776.00 +34

Total (B) 117464714.40 187875316.01 73986.00 50854411.46

Total Increase/Decrease(A)+(B) 82386922.64 78529687.92

Working Capital (A)-(B) 110232007.83 114089242.55 3857234.72 -----

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

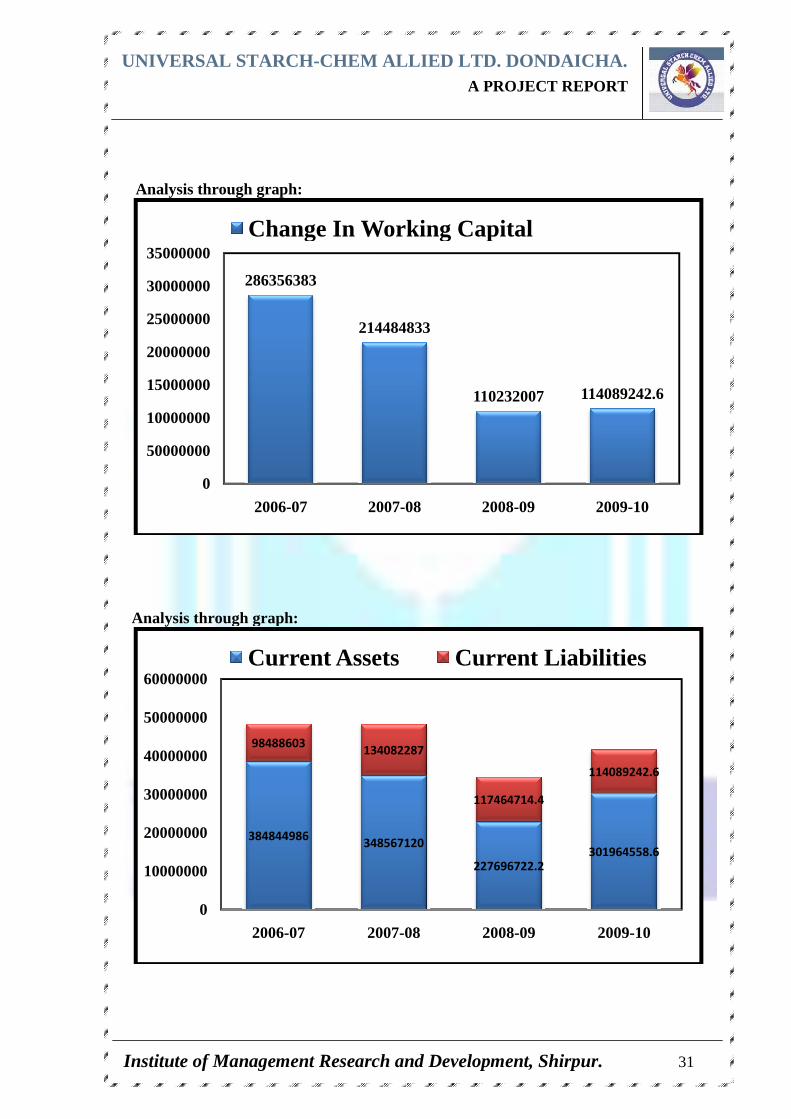

Analysis through graph

Analysis through graph:

286356383

0

50000000

10000000

15000000

20000000

25000000

30000000

35000000

2006

Change In Working Capital

384844986

98488603

0

10000000

20000000

30000000

40000000

50000000

60000000

2006-

Current Assets

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

graph:

through graph:

286356383

214484833

110232007

-07 2007-08 2008-09

Change In Working Capital

384844986348567120

227696722.2

98488603134082287

117464714.4

-07 2007-08 2008-09

Current Assets Current Liabilities

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 31

114089242.6

2009-10

301964558.6

114089242.6

2009-10

Current Liabilities

UNIVERSAL STARCH-CHEM ALLIED LTD. DONDAICHA. A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 32

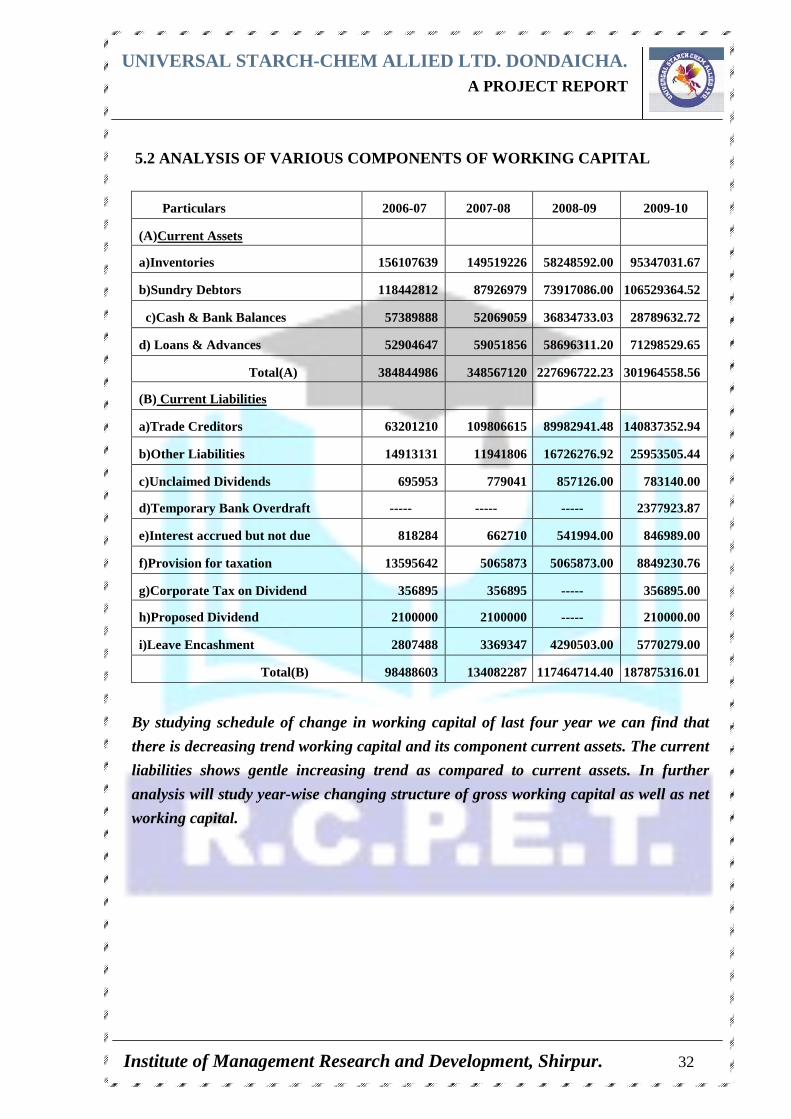

5.2 ANALYSIS OF VARIOUS COMPONENTS OF WORKING CAPIT AL

Particulars 2006-07 2007-08 2008-09 2009-10

(A)Current Assets

a)Inventories 156107639 149519226 58248592.00 95347031.67

b)Sundry Debtors 118442812 87926979 73917086.00 106529364.52

c)Cash & Bank Balances 57389888 52069059 36834733.03 28789632.72

d) Loans & Advances 52904647 59051856 58696311.20 71298529.65

Total(A) 384844986 348567120 227696722.23 301964558.56

(B) Current Liabilities

a)Trade Creditors 63201210 109806615 89982941.48 140837352.94

b)Other Liabilities 14913131 11941806 16726276.92 25953505.44

c)Unclaimed Dividends 695953 779041 857126.00 783140.00

d)Temporary Bank Overdraft ----- ----- ----- 2377923.87

e)Interest accrued but not due 818284 662710 541994.00 846989.00

f)Provision for taxation 13595642 5065873 5065873.00 8849230.76

g)Corporate Tax on Dividend 356895 356895 ----- 356895.00

h)Proposed Dividend 2100000 2100000 ----- 210000.00

i)Leave Encashment 2807488 3369347 4290503.00 5770279.00

Total(B) 98488603 134082287 117464714.40 187875316.01

By studying schedule of change in working capital of last four year we can find that

there is decreasing trend working capital and its component current assets. The current

liabilities shows gentle increasing trend as compared to current assets. In further

analysis will study year-wise changing structure of gross working capital as well as net

working capital.

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

Current Liabilities98488603

20%

2006

Composition of Current Assets & Current Liabilities

Current Liabilitie

s13408228

728%

2007

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Current Assets

38484498780%

2006-07

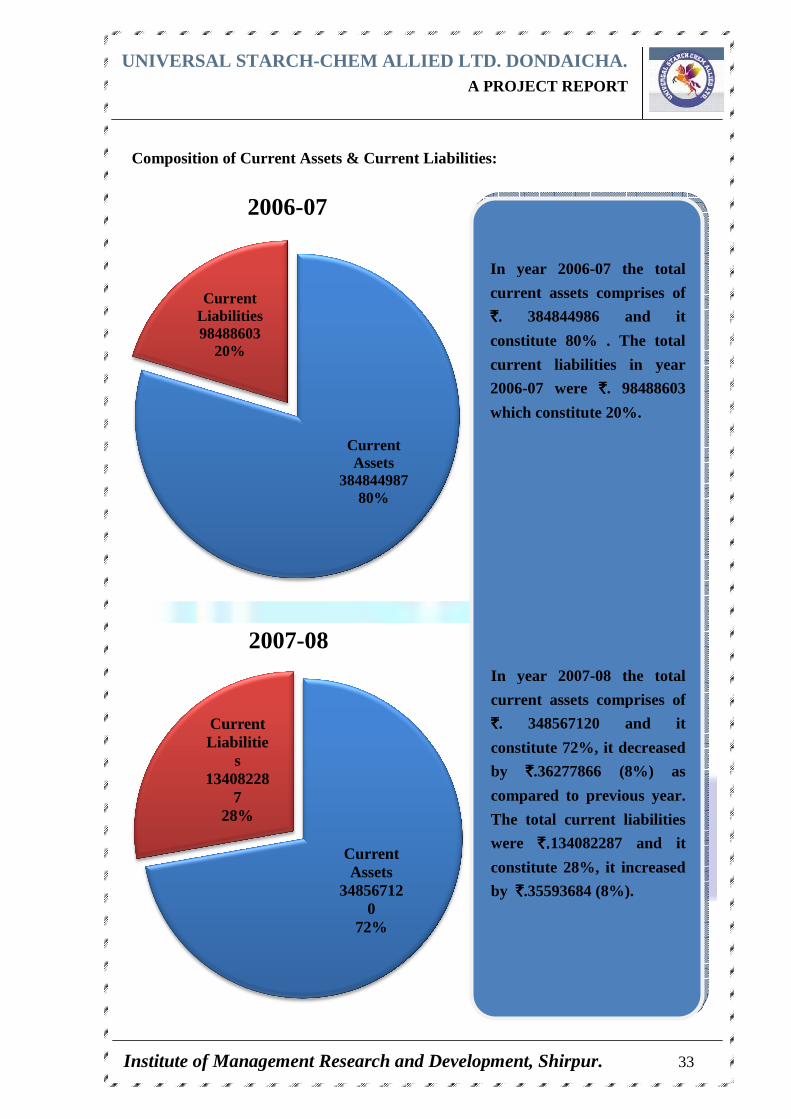

Composition of Current Assets & Current Liabilities:

Current Assets

348567120

72%

2007-08

In year 2006

current assets comprises of

`̀̀̀. 384844986 and it

constitute 80% . The total

current liabilities in year

2006-07 were

which constitute 20%.

In year 2007

current assets comprises of

`̀̀̀. 348567120 and it

constitute 72%, it decreased

by `̀̀̀.36277866 (8%) as

compared to previous year.

The total current liabilities

were `.`.`.`.134082287 and it

constitute 28%, it increased

by ̀̀̀̀ .35593684 (8%).

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 33

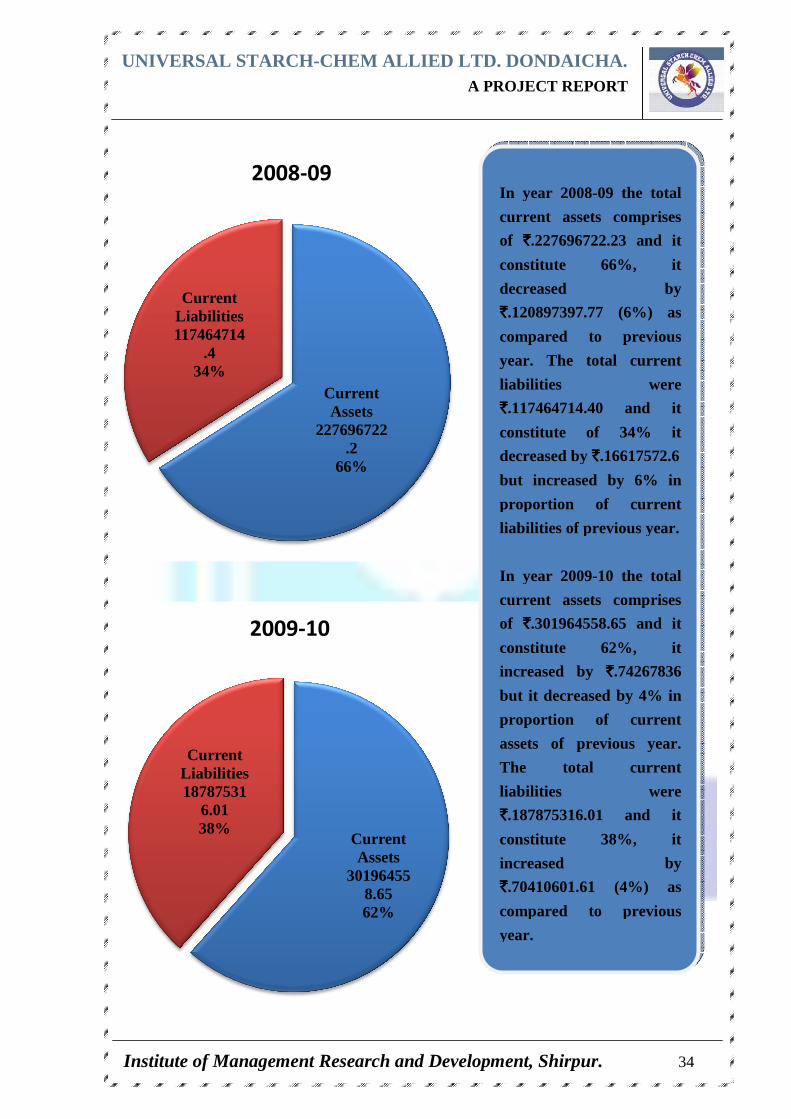

In year 2006-07 the total

current assets comprises of

. 384844986 and it

constitute 80% . The total

current liabilities in year

07 were `̀̀̀. 98488603

which constitute 20%.

In year 2007-08 the total

current assets comprises of

. 348567120 and it

constitute 72%, it decreased

.36277866 (8%) as

compared to previous year.

The total current liabilities

134082287 and it

constitute 28%, it increased

.35593684 (8%).

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

Current Liabilities18787531

6.0138%

2009

Current Liabilities117464714

.434%

2008

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Current Assets

301964558.6562%

2009-10

Current Assets

227696722.2

66%

2008-09In year 2008

current assets comprises

of `̀̀̀.227696722.23 and it

constitute 66%, it

decreased by

`̀̀̀.120897397.77 (6%) as

compared to previous

year. The total current

liabilities were

`̀̀̀.117464714.40 and it

constitute of 34% it

decreased by

but increased by 6% in

proportion of current

liabilities of previous year.

In year 2009

current assets comprises

of `̀̀̀.301964558.65 and it

constitute 62%, it

increased by

but it decreased by 4% in

proportion of current

assets of previous year.

The total current

liabilities were

`̀̀̀.187875316.01 and it

constitute 38%, it

increased by

`̀̀̀.70410601.61 (4%) as

compared to previous

year.

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 34

In year 2008-09 the total

current assets comprises

.227696722.23 and it

constitute 66%, it

decreased by

.120897397.77 (6%) as

compared to previous

year. The total current

liabilities were

.117464714.40 and it

constitute of 34% it

decreased by ̀̀̀̀.16617572.6

but increased by 6% in

proportion of current

liabilities of previous year.

In year 2009-10 the total

current assets comprises

.301964558.65 and it

constitute 62%, it

increased by `̀̀̀.74267836

but it decreased by 4% in

proportion of current

assets of previous year.

The total current

liabilities were

.187875316.01 and it

ute 38%, it

increased by

.70410601.61 (4%) as

compared to previous

UNIVERSAL STARCH

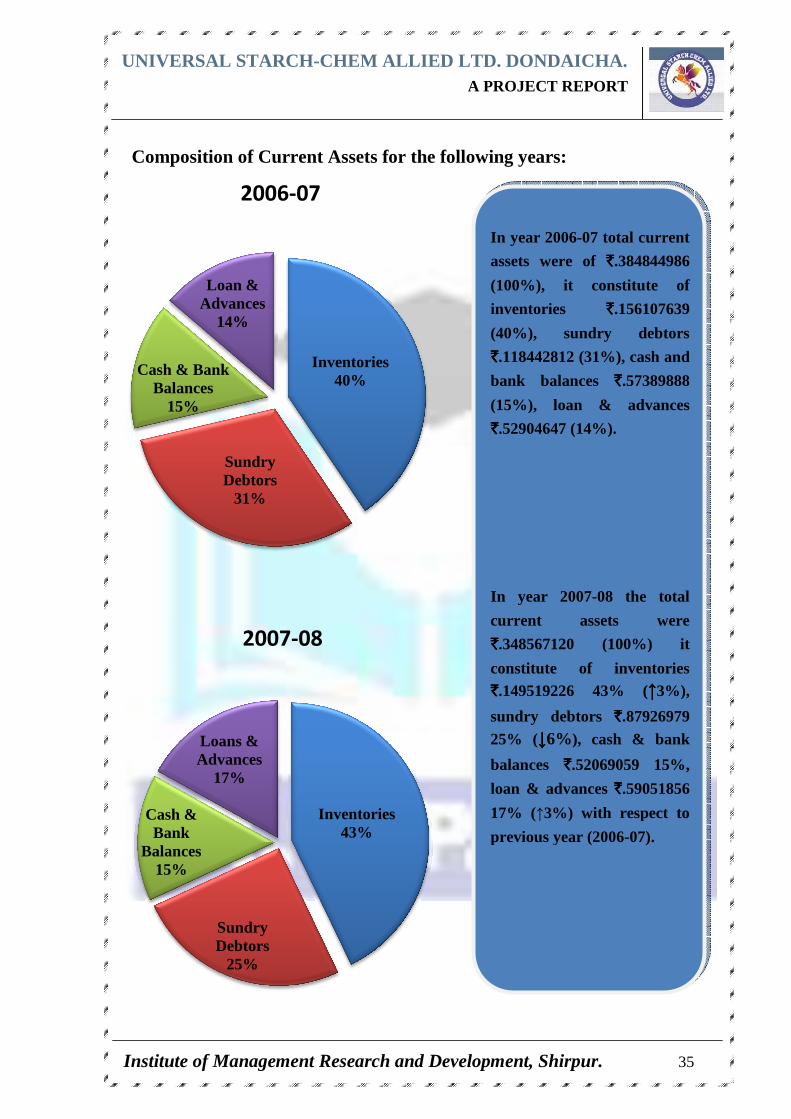

Institute of Management Research and Development, Shirpur.

Sundry Debtors

25%

Cash & Bank

Balances15%

Loans & Advances

17%

2007

Composition of Current Assets for the following years:

Sundry Debtors

31%

Cash & Bank Balances

15%

Loan & Advances

14%

2006

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Inventories43%

2007-08

Composition of Current Assets for the following years:

Inventories40%

2006-07

In year 2006

assets were of

(100%), it constitute of

inventories

(40%), sundry debtors

`̀̀̀.118442812 (31%), cash and

bank balances

(15%), loan & advances

`̀̀̀.52904647 (14%).

In year 2007

current assets were

`̀̀̀.348567120 (100%) it

constitute of inventories `̀̀̀.149519226 43% (

sundry debtors 25% (↓↓↓↓6%), cash & bank

balances `̀̀̀.52069059 15%,

loan & advances

17% (↑3%) with respect to

previous year (2006

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 35

In year 2006-07 total current

assets were of ̀̀̀̀ .384844986

(100%), it constitute of

inventories `̀̀̀.156107639

(40%), sundry debtors

.118442812 (31%), cash and

bank balances `̀̀̀.57389888

(15%), loan & advances

.52904647 (14%).

In year 2007-08 the total

current assets were

.348567120 (100%) it

constitute of inventories .149519226 43% (↑↑↑↑3%),

sundry debtors `̀̀̀.87926979 ), cash & bank

.52069059 15%,

& advances ̀̀̀̀ .59051856

3%) with respect to

previous year (2006-07).

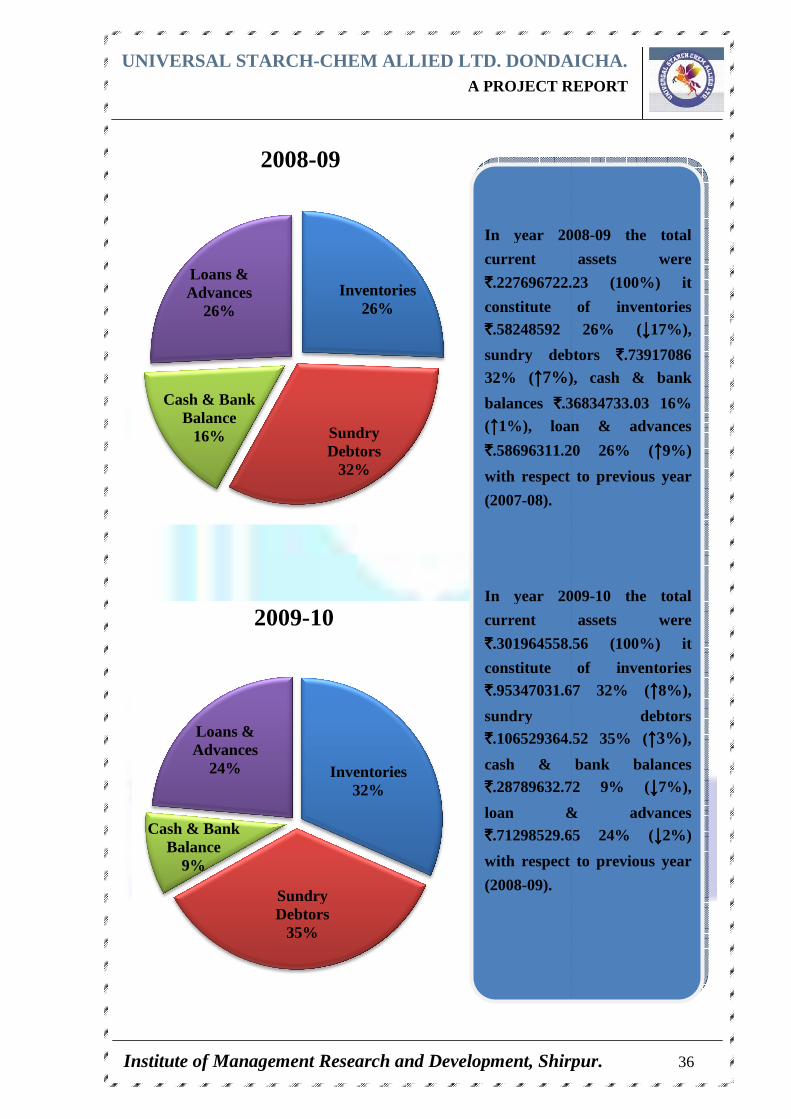

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

Sundry Debtors

Cash & Bank Balance

9%

Loans & Advances

24%

2009

Cash & Bank Balance

16%

Loans & Advances

26%

2008

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Inventories32%

Sundry Debtors

35%

2009-10

Inventories26%

Sundry Debtors

32%

2008-09

In year 2008

current assets were

`̀̀̀.227696722.23 (100%) it

constitute of inventories `̀̀̀.58248592 26% (

sundry debtors 32% (↑↑↑↑7%), cash & bank

balances `̀̀̀.36834733.03 16% (↑↑↑↑1%), loan & advances

`̀̀̀.58696311.20 26% (

with respect to previous year

(2007-08).

In year 2009

current assets were

`̀̀̀.301964558.56 (100%) it

constitute o`̀̀̀.95347031.67 32% (

sundry debtors `̀̀̀.106529364.52 35% (

cash & bank balances `̀̀̀.28789632.72 9% (

loan & advances `̀̀̀.71298529.65 24% (

with respect to previous year

(2008-09).

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 36

In year 2008-09 the total

current assets were

.227696722.23 (100%) it

constitute of inventories .58248592 26% (↓↓↓↓17%),

sundry debtors `̀̀̀.73917086 ), cash & bank

.36834733.03 16% 1%), loan & advances

.58696311.20 26% (↑↑↑↑9%)

with respect to previous year

In year 2009-10 the total

current assets were

.301964558.56 (100%) it

constitute of inventories .95347031.67 32% (↑↑↑↑8%),

sundry debtors .106529364.52 35% (↑↑↑↑3%),

cash & bank balances .28789632.72 9% (↓↓↓↓7%),

loan & advances .71298529.65 24% (↓↓↓↓2%)

with respect to previous year

UNIVERSAL STARCH

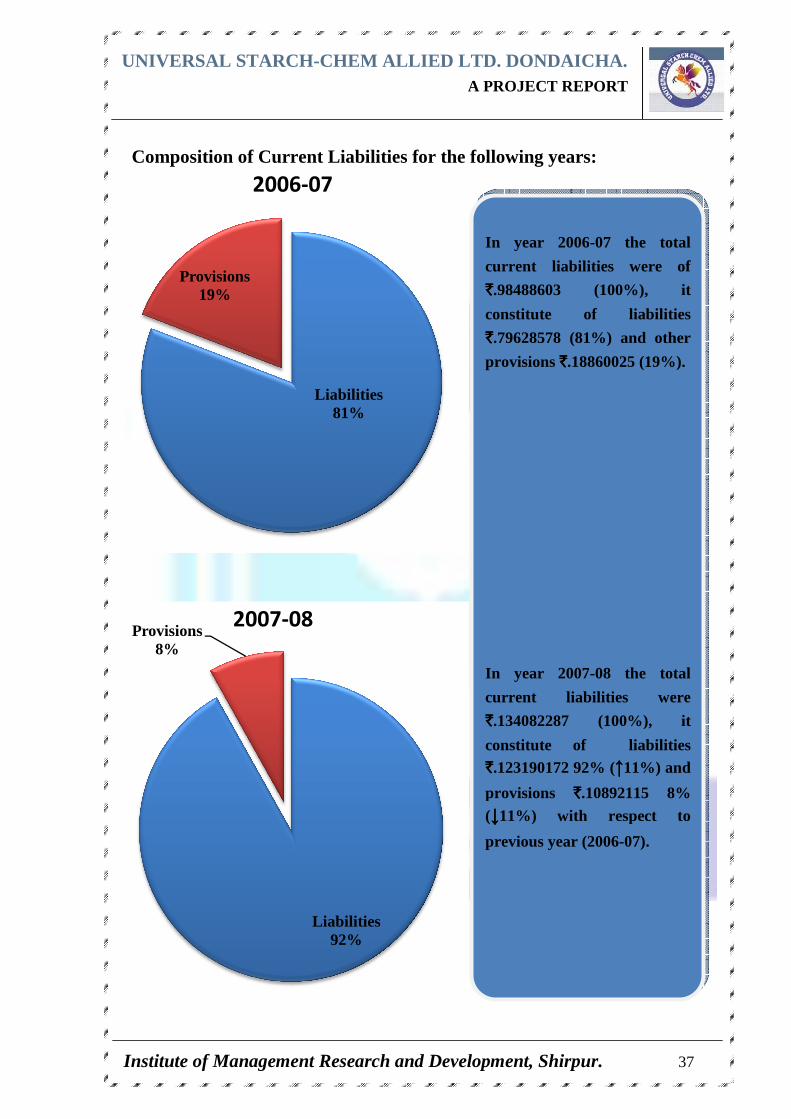

Institute of Management Research and Development, Shirpur.

Composition of Current Liabilities

Provisions19%

2006

Provisions8%

2007-

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Composition of Current Liabilities for the following years:

Liabilities81%

2006-07

Liabilities92%

-08

In year 2006

current liabilities were of

`̀̀̀.98488603 (100%), it

constitute of liabilities

`̀̀̀.79628578 (81%) and other

provisions ̀̀̀̀ .18860025 (19%).

In year 2007

current liabilities were

`̀̀̀.134082287 (100%), it

constitute of liabilities `̀̀̀.123190172 92% (

provisions (↓↓↓↓11%) with respect to

previous year (2006

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 37

for the following years:

In year 2006-07 the total

current liabilities were of

.98488603 (100%), it

constitute of liabilities

.79628578 (81%) and other

.18860025 (19%).

In year 2007-08 the total

current liabilities were

82287 (100%), it

constitute of liabilities .123190172 92% (↑↑↑↑11%) and

provisions `̀̀̀.10892115 8% 11%) with respect to

previous year (2006-07).

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

Provisions4%

2008

Provisions9%

2009

NIVERSAL STARCH -CHEM ALLIED LTD. DONDAICHA A PROJECT REPORT

Institute of Management Research and Development, Shirpur.

Liabilities96%

2008-09

Liabilities91%

2009-10

In year 2008

current liabilities were

`̀̀̀.117464714.40 (100%), it

constitute of liabilities `̀̀̀.108108338.40 96% (

and provisions 4% (↓↓↓↓4%) with respect to

previous year (2007

In year 2009

current liabilities were

`̀̀̀.187875316.01 (100%), it

constitute of liabilities `̀̀̀.170798911.25 91% (

and provisions 9% (↑↑↑↑5%) with respect to

previous year (2007

DONDAICHA . A PROJECT REPORT

Institute of Management Research and Development, Shirpur. 38

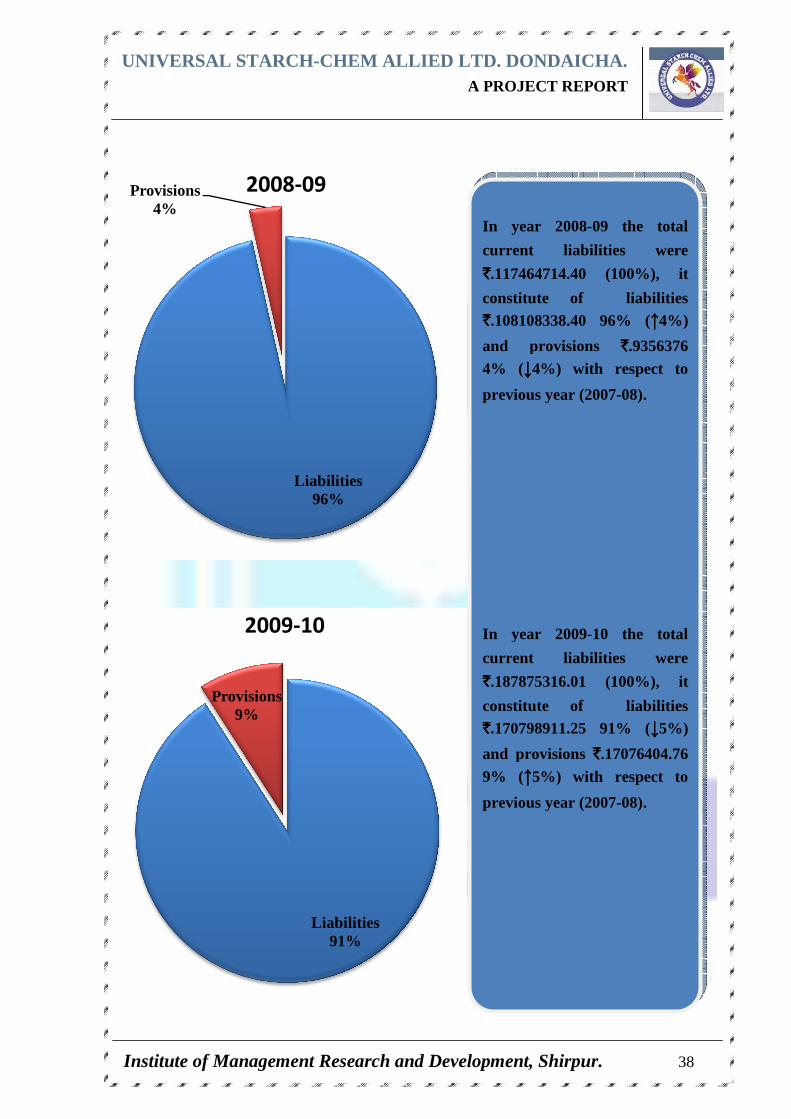

In year 2008-09 the total

current liabilities were

.117464714.40 (100%), it

constitute of liabilities .108108338.40 96% (↑↑↑↑4%)

and provisions `̀̀̀.9356376 4%) with respect to

previous year (2007-08).

In year 2009-10 the total

current liabilities were

.187875316.01 (100%), it

titute of liabilities .170798911.25 91% (↓↓↓↓5%)

and provisions `̀̀̀.17076404.76 5%) with respect to

previous year (2007-08).

UNIVERSAL STARCH

Institute of Management Research and Development, Shirpur.

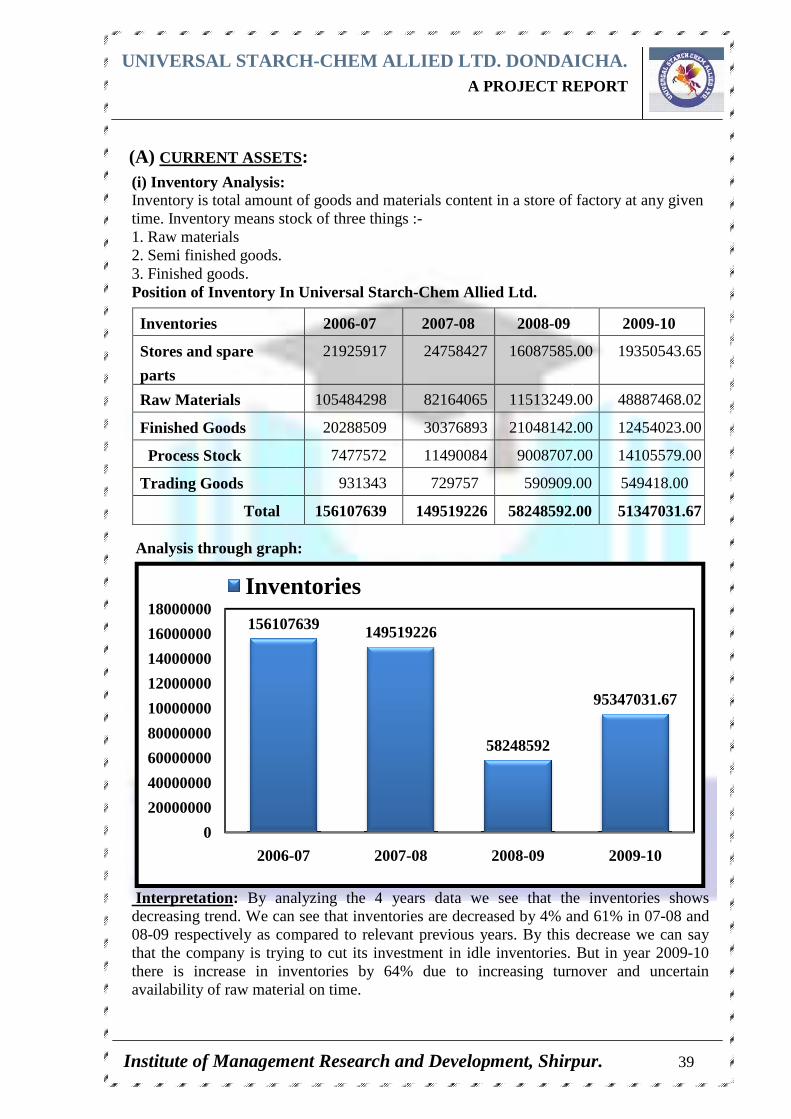

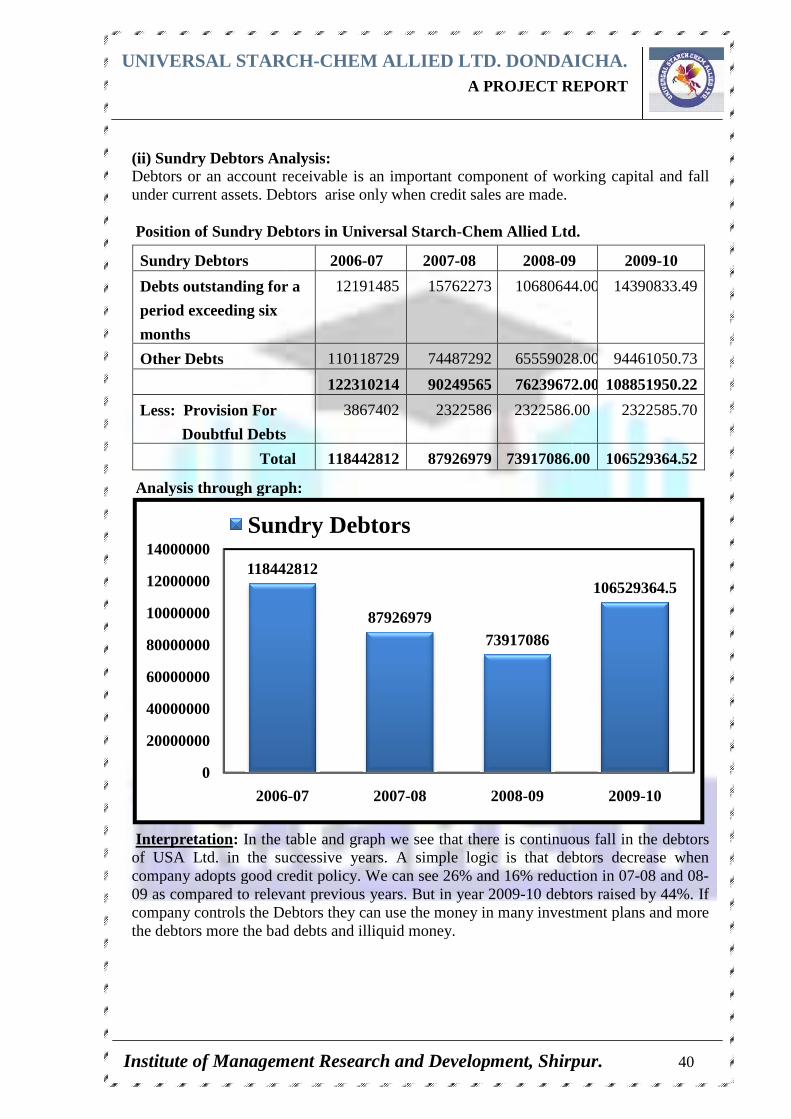

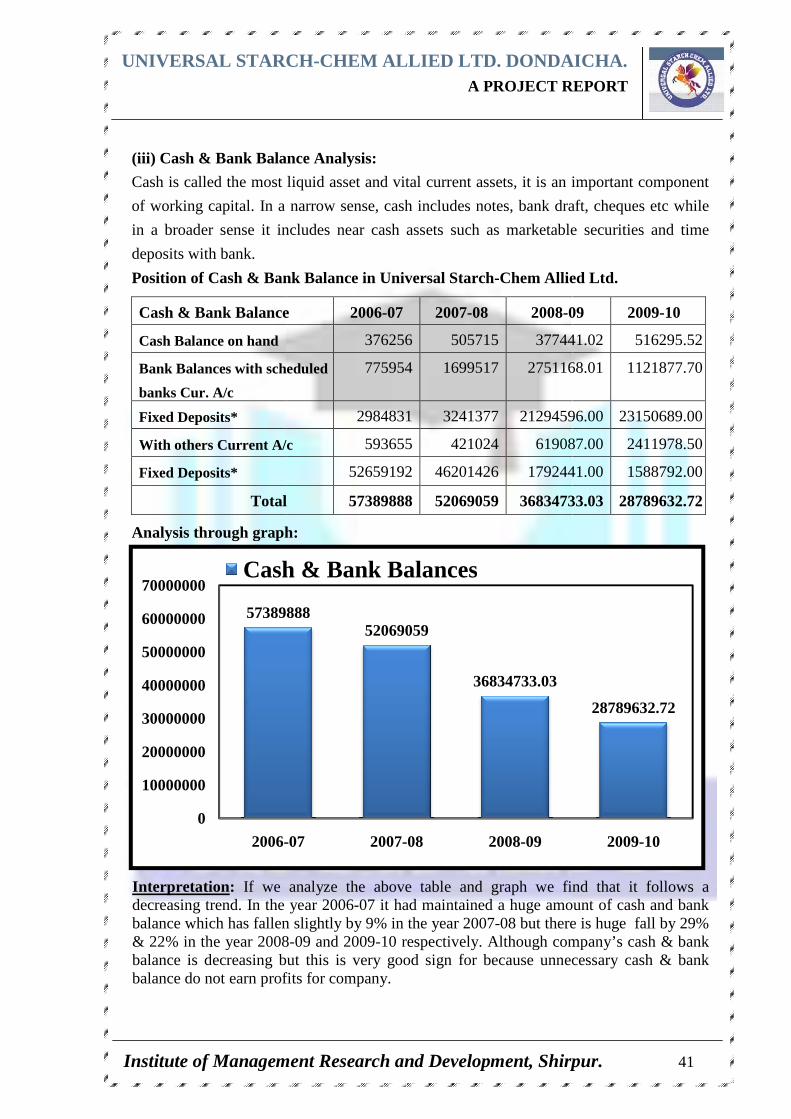

(A) CURRENT ASSETS

(i) Inventory Analysis: Inventory is total amount of goods and materials content in a store of factory at any given time. Inventory means stock of three things :1. Raw materials 2. Semi finished goods. 3. Finished goods. Position of Inventory In Universal Starch

Analysis through graph

Interpretation : By analyzing the 4decreasing trend. We ca08-09 respectively as compared to relevant previous yearthat the company is tryingthere is increase in inventories byavailability of raw material on time.

Inventories

Stores and spare

parts

Raw Materials

Finished Goods

Process Stock

Trading Goods

Total

156107639

0

20000000

40000000

60000000

80000000

10000000

12000000