Embed Size (px)

Citation preview

PROGRAMME

PUBLIC CONSULTATION ON TRANSFER PRICING DISCUSSION DRAFTS

12-14 NOVEMBER 2012

OECD CONFERENCE CENTRE

2 RUE ANDRÉ PASCAL, PARIS 16TH, FRANCE

MONDAY 12 NOVEMBER

08:30-09:30 REGISTRATION

09:30-10:00 OPENING REMARKS AND GROUND RULES

Speakers:

Michelle LEVAC, Chair of Working Party No. 6

William MORRIS, BIAC

10:00-11:00 I: DISCUSSION DRAFT ON TRANSFER PRICING SAFE HARBOURS

Speakers: Page No.

Patricia LEWIS, Caplin & Drysdale ............................................................................................................... 6

- The general approach of the Discussion Draft

- The usefulness of bilateral safe harbours

Michael HECKEL, True Partners Consulting

- The optional nature of safe harbours for taxpayers and the provisions on

rebuttable presumptions;

- The specific OECD proposals for bilateral MOUs

An THEEUWES, Tax Executives Institute ................................................................................................... 10

- The usefulness of bilateral safe harbours; and

- The proposed guidance on unilateral safe harbours

11:00-11:30 Refreshment Break

11:30-13:00 II: SECRETARIAT REQUEST FOR COMMENTS ON TIMING ISSUES

Speakers:

Duncan NOTT, BDO .................................................................................................................................... 14

- The arm’s length price-setting and the arm’s length outcome-testing approaches;

- The need for further direction on year-end adjustments or “true ups”

Brigitte BAUMGARTNER, Plansee Group Services GmbH ...................................................................... 19

- The relative merits of the arm’s length price-setting and the arm’s length

outcome-testing approaches

Matthew WALL, MDW Consulting Inc. ...................................................................................................... 24

- The determination of transfer prices when valuation is uncertain

- Paragraphs 171 – 178 of the Discussion Draft and Examples 20 – 22

Jutta MENNINGER, BSH/PwC ................................................................................................................... 31

- The determination of transfer prices when valuation is uncertain

13:00-14:30 Lunch break

Page 1 of 180

MONDAY 12 NOVEMBER (CONT’D)

14:30-15:15 III: GENERAL DEFINITIONAL APPROACH FOR INTANGIBLES

Speakers:

Jennifer RHEE, Richter Consulting ............................................................................................................. 38

- The definition of intangibles in Section A of the Discussion Draft

Vanessa DE SAINT BLANQUAT, MEDEF ............................................................................................... 45

- General definitional approach for intangibles

Anne QUENEDEY, SALANS ...................................................................................................................... 49

- Intangibles: the relevance of property law definitions, accounting definitions

and separate transferability

15:15-16:00 IV: CATEGORIES OF INTANGIBLES

Ronald VAN DEN BREKEL, Ernst & Young ............................................................................................. 54

- The usefulness of the concept defined as “D.1. (vi) Intangibles”

Wendy NICHOLLS, Grant Thornton UK ................................................................................................... 60

- Should the Discussion Draft distinguish between Routine vs. Unique and

Valuable Intangibles?

16:00-16:30 Refreshment Break

16:30-18:00 V: TREATMENT OF GOODWILL AND WORKFORCE IN PLACE

Speakers:

Caroline SILBERZTEIN, Baker & McKenzie ............................................................................................. 65

- The treatment of goodwill (and related examples in the Annex)

Agata UCEDA, International Tax Centre, Leiden ....................................................................................... 70

- The treatment of goodwill (and related examples in the Annex)

Laurence DELORME, A3F ......................................................................................................................... 74

- The Discussion Draft provisions on assembled workforce

Page 2 of 180

TUESDAY 13 NOVEMBER

09:30-10:15 VI. DOES THE DISCUSSION DRAFT FOCUS TOO HEAVILY ON RESTRAINING ABUSIVE

BEHAVIOUR?

Speakers:

Georg GEBERTH, BIAC ............................................................................................................................. 79

- Does the Discussion Draft focus too heavily on restraining abusive behaviour?

James PHILLIPS ........................................................................................................................................... 83

- Does the Discussion Draft focus too heavily on restraining abusive behaviour?

10:15-11:00 VII: DOES THE DISCUSSION DRAFT PLACE TOO MUCH EMPHASIS ON PROFIT SPLIT

APPROACHES?

Speakers:

Gary SPRAGUE, Treaty Policy Working Group ......................................................................................... 88

- Does the Discussion Draft place too much emphasis on profit split approaches?

Arnaud LE BOULANGER, CMS Bureau Francis Lefebvre ....................................................................... 93

- Does the Discussion Draft place too much emphasis on profit split approaches?

11:00-11:30 Refreshment Break

11:30-13:00 VIII: INTANGIBLES: ENTITLEMENT TO INTANGIBLE RELATED RETURNS

Speakers:

Alison LOBB and John HENSHALL, Deloitte ........................................................................................... 98

- The treatment of risk and control of risk, including the consistency of the draft with

Chapter IX of the TPG

Linda FERNANDEZ, Transfer Pricing Discussion Group ....................................................................... 103

- The general usefulness of the intangible related return concept and its definition

13:00-14:30 Lunch

14:30-16:00 IX: INTANGIBLES: ENTITLEMENT TO INTANGIBLE RELATED RETURNS (CONTINUED)

Speakers:

Catherine SCHULTZ, National Foreign Trade Council ........................................................................... 108

- The role of registrations and contractual arrangements;

- Disregard of transactions, registrations and contracts

Kate NOAKES, Fidal International Direction .......................................................................................... 111 - Compensation for marketing activities performed by associated enterprises related to

the development, enhancement, maintenance or protection of Intangibles,

including examples 3 through 8

Ian BRIMICOMBE, AstraZeneca .............................................................................................................. 114 - Entitlement to intangible related returns: The importance of performance of

important functions and control

16:00-16:30 Refreshment Break

Page 3 of 180

TUESDAY 13 NOVEMBER (CONT’D)

16:30-18:00 X: OPTIONS REALISTICALLY AVAILABLE AND PERSPECTIVES OF THE PARTIES

Speakers:

Isabel VERLINDEN, PriceWaterhouseCoopers ....................................................................................... 130 - Options realistically available and perspectives of the parties and example 19

Carol Doran KLEIN, USCIB ..................................................................................................................... 136

- Options realistically available and perspectives of the parties and example 19

Patrick BRESLIN, Bates White, LLC ........................................................................................................ 140

- Options realistically available and perspectives of the parties and example 19

WEDNESDAY 14 NOVEMBER

9:30-11:00 XI: INTANGIBLES: USE OF FINANCIAL VALUATION TECHNIQUES

Speakers:

Jochem QUAAK and Dick DE BOER, Duff & Phelps .............................................................................. 145

- The relevance of accounting valuations and purchase price allocations

for transfer pricing purposes

Richard GINSBERG, Canadian Institute of Chartered Business Valuators ............................................. 150

- Use of financial valuation techniques and expressly adopting a standard of value

Emmanuel LLINARES, NERA Economic Consulting ............................................................................... 161 - Use of financial valuation techniques for transfer pricing purposes

11:00-11:30 Refreshment Break

11:30-12:45 XII: DETERMINING ARM’S LENGTH ROYALTY RATES FOR LICENSING TRANSACTIONS

Speakers:

Brian CODY, KPMG ................................................................................................................................. 167

- Determining arm’s length royalty rates for licensing transactions and

comparability standards for intangibles

Ednaldo SILVA, RoyaltyStat LLC ............................................................................................................. 173

- Use of information from databases

David JARCZYK, ktMINE ........................................................................................................................ 177

- Intangibles: comparability standards and use of information from databases

12:45-13:00 CONCLUDING REMARKS

Speakers:

Michelle LEVAC, Chair of Working Party No. 6

William MORRIS, BIAC

13:00 ADJOURN

Page 4 of 180

SESSION I

DISCUSSION DRAFT ON TRANSFER PRICING SAFE HARBOURS

Speakers:

Patricia LEWIS, Caplin & Drysdale

Michael HECKEL, True Partners Consulting

An THEEUWES, Tax Executives Institute

Page 5 of 180

1

November 12, 2012

-- Safe Harbours -- Comments on

OECD Discussion Draft

Patricia Gimbel Lewis

Caplin & Drysdale One Thomas Circle, N.W. Washington, DC 20005

O: 202.862.5000 F: 202.429.3301

www.caplindrysdale.com

Page 6 of 180

2

-- Safe Harbours -- General Approach of

Discussion Draft

#1

BILATERAL TRANSFER

PRICING SAFE HARBOURS

Acute Taxpayer and Government

Resource Considerations

Treaty-Based Desires to Respect Arm’s Length Standard, Minimize Double

Taxation, and Increase Certainty

Concern with Potential Adverse

Selection

MOUs

#2 UNILATERAL

SAFE HARBOURS, WITH MAP

Page 7 of 180

3

Particular Usefulness of Bilateral Safe Harbours

Test-drive solutions

Emulate arm’s length result via government negotiation;

reduce adverse selection

Efficiently multiply benefit

Minimize double taxation risk

Enhance compliance

Increase government revenues

Enable customized MOUs for specific-country situations

Reduce impediments to cross-border enterprise

Eliminate inadvertent Permanent Establishment exposure

MOU = Many Ought to Use

Overall: A+

Page 8 of 180

4

Suggested Enhancements

1. Make MOUs simpler and broader o Rough justice

o Anti-abuse rule

2. Provide model MOU for Headquarters/centralized services;

tackle “benefit” aspect

3. Reduce adverse selection potential via advance election or

multi-year requirement

4. Include dynamic safe-harbor updating mechanisms

5. Permit post-year-end adjustments

6. Preclude or limit safe harbors for transactions with tax havens

7. Combine with short-cut APA process for unclear cases

********

Page 9 of 180

1

OECD Public Consultation

Safe Harbours for Transfer Pricing

Paris, 12-14 November 2012

Represented by Anna Theeuwes and Alexander Koelbl

Page 10 of 180

2

TEI welcomes the Draft’s focus on using safe harbours for non-

entrepreneurial, routine tasks; such an approach will make taxpayer

transfer pricing compliance less burdensome

TEI agrees that the use of safe harbours should be optional (i.e.,

taxpayer may use the arm’s length principle or a safe harbour)

tax authorities should not treat a safe harbour as a rebuttable

presumption of the “correct” arm’s length price

TEI recommends working with ranges for safe harbours

Coordination with the Timing Issues Draft, TEI recommends:

that IP valuation should be done ex ante

that any ex post approach approved in the Guidelines be used only in

conjunction with safe harbour rules, and that taxpayers be permitted to

select either the safe harbour or the standard arm’s length approach

Safe Harbours – General considerations

Page 11 of 180

3

OECD should promote the use of safe harbour rules for interest rates,

low value-added services, and shared services

Unilateral safe harbour:

Set in local legislation - easy for member states

Helpful for businesses - for centralised activities out of a country

Bilateral safe harbour:

Set in tax treaty – not so easy for member states

Complex to manage given the multinational character of MNE transactions

OECD should not encourage the use of bilateral memorandum of

understanding (MOUs) too complex to manage given the multinational

character of MNEs transactions.

Multilateral safe harbour:

Basis to be range in OECD commentaries – member states to translate in

DTT or local legislation

Supportive of development of international standards - This would promote

uniformity across MOUs, further decreasing transfer pricing compliance

costs and disputes

Safe Harbours – Type of Safe Harbour

Page 12 of 180

SESSION II

SECRETARIAT REQUEST FOR COMMENTS ON TIMING ISSUES

Speakers:

Duncan NOTT, BDO

Brigitte BAUMGARTNER, Plansee Group Services GmbH

Matthew WALL, MDW Consulting Inc.

Jutta MENNINGER, BSH / PwC

Page 13 of 180

TIMING ISSUES RELATING TO TRANSFER

PRICING Overview

OECD Consultation

DUNCAN NOTT - BDO

8 November 2012

Copyright © November 12 BDO LLP. All rights reserved. Page 14 of 180

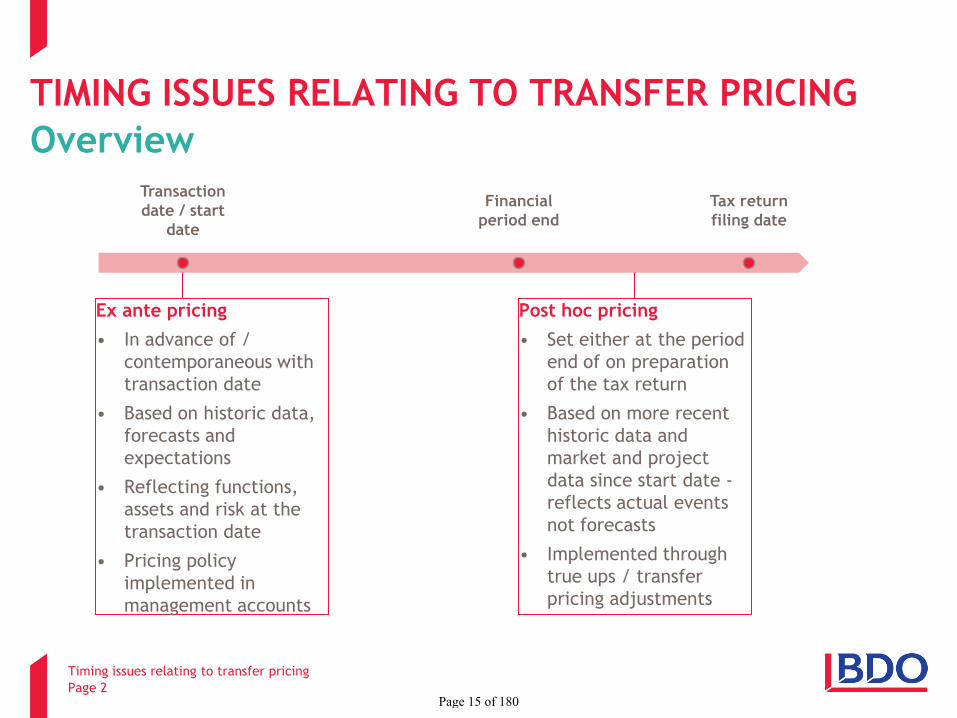

TIMING ISSUES RELATING TO TRANSFER PRICING

Overview

Ex ante pricing

• In advance of /

contemporaneous with

transaction date

• Based on historic data,

forecasts and

expectations

• Reflecting functions,

assets and risk at the

transaction date

• Pricing policy

implemented in

management accounts

Timing issues relating to transfer pricing

Page 2

Transaction

date / start

date

Financial

period end

Tax return

filing date

Post hoc pricing

• Set either at the period

end of on preparation

of the tax return

• Based on more recent

historic data and

market and project

data since start date -

reflects actual events

not forecasts

• Implemented through

true ups / transfer

pricing adjustments

Page 15 of 180

TIMING ISSUES RELATING TO TRANSFER PRICING

Practical problems

Key areas for consideration

The existence of two approaches to price setting – ex ante and post hoc – can give

rise to practical problems, including:

• Nature of information regarding potentially comparable transactions that may

be relied upon

• Taxpayer initiated adjustment and whether/how these will be respected by

different taxing authorities

• Use and impact of post-transaction date developments

• Application of these circumstances to transfers of intangibles of highly uncertain

valuation and the ability to assume the existence of a post-transaction risk

sharing mechanism

Timing issues relating to transfer pricing

Page 3

Ex post

Greater flexibility Ex ante

Third party approach

Page 16 of 180

TIMING ISSUES RELATING TO TRANSFER PRICING

Comments and areas for discussion

Clear theory

• Clarifying terms

- Using ex ante pricing over a period of

years – can a forward looking standpoint

be maintained?

• Does a ‘hybrid’ approach exist in

practice?

• Usefulness of ex ante approach for

profit based methods

• Extent (or limit) of incidence of price

adjustment clauses in third party

situations

• Expressing a preference for ex ante or

post hoc pricing in the Guidelines

Timing issues relating to transfer pricing

Page 4

Effective practice

• Clarity on what is appropriate available

information for ex ante pricing

• Identifying a reasonable level for

contemporaneous documentation of ex

ante pricing

• When and how to interpose

retrospective pricing adjustment

- A place for bad business decisions in

transfer pricing policy?

• Enabling the ‘right kind’ of true up

• Creating transparency for tax

authorities without increasing

administrative burden on business

Reflecting the outcome of these areas in the Guidelines

Page 17 of 180

DUNCAN NOTT Director - Transfer Pricing

BDO LLP

+44(0)20 7893 3389 (DDI)

+44(0)780 580 8969 (Mobile)

+44(0)20 7893 2418 (Fax)

Page 18 of 180

1

Timing issues: The relative merits of arm’s length price-setting and the arm’s length outcome-testing approaches

LL.M. Brigitte Baumgartner International Tax Manager Plansee Group

October 2012

Page 19 of 180

Plansee Group 2

Plansee Group Example

Hardmetals

& Tools

High Performance

Materials

Tungsten

& Powders

Kolkata

Tianjin

Vista

Franklin

Towanda

Warren

Gabrovo

Hitzacker

Lechbruck

Liezen

Reutte

Alserio Seon

St. Pierre en Faucigny

Biel

Niederkorn

Empfingen

Livange

Mamer

Bruntál

Esashi

Sakura

Sales companies

and sales partners

in 50 countries

Mysore

Shanghai

Tamsui

Wugu Zhangzhou Xiamen

Seoul

Page 20 of 180

Plansee Group 3

What are we looking for?

Page 21 of 180

Plansee Group 4

Certainty: We want to know if we are doing things right! Clarity on: when should be the ex post approach acceptable and

appropriate and adjustments (timing & consequences on VAT and Customs)

Simplicity: regarding the applicability of TPG

Minimization: of possible disputes with the tax authorities and double taxation issues

Examples

Page 22 of 180

Plansee Group 5

THANK YOU

Page 23 of 180

Working Party No. 6

Public Consultation on the Transfer Pricing Discussion Drafts 12 - 14 November 2012

OECD Conference Centre, Paris

The determination of transfer prices when valuation is uncertain

Presentation by: Matthew Wall CA CBV

MDW CONSULTING INC.

Page 24 of 180

MDW CONSULTING INC. Page 1

Draft Paragraphs 171 - 178(currently Paragraphs 6.28 - 6.35)

Draft Examples 20 - 22 give More Guidance needed

clearer meaning and purpose to restrict the use of hindsight for

to Paragraphs 171 - 178 "exceptional circumstances"

Draft Examples 20 - 22 Draft Paragraphs 3.67 - 3.71(currently Annex to Chapte VI) (currently Paragraphs 3.67 - 3.71)

Certain changes (e.g., Examples) and more Guidance (e.g., Paragraphs 3.67 - 3.71)

needed to mitigate the risk of misunderstanding, misuse and dispute.

1

2 3

Page 25 of 180

Paragraph 171 – 178 of the Intangibles Draft

• Information should be both relevant and reliable for arm’s length pricing. This might be information at the time of the transaction, in the year of the transaction, or at the year-end or tax filing.

Example Product A Product B

Transfer price at the time of the transaction $13.50 $10.00

Transfer pricing adjustment in the year of the transaction 1.50 5.00

Transfer price at the year-end or tax filing $15.00 $15.00

• More Guidance is needed to restrict the use of information after the year-end or tax filing for “exceptional circumstances only” to avoid the potential for misuse, dispute and double taxation.

MDW CONSULTING INC. Page 2

Page 26 of 180

MDW CONSULTING INC. Page 3

Key Facts and Assumptions Ex. 20 Ex. 21 Ex. 22

a) Fundamental change in the facts? Yes Yes Yes

b) Foreseeable at the time of the agreement? No No No

c) Following third party terms and conditions? Yes No No

OECD Guidance per Discussion Draft

d) Example adjusts the royalty payment? No Yes Yes

e) Example uses a price adjustment clause? No Yes Yes

f) Example uses hindsight? No Yes Yes

SUMMARY CHART of EXAMPLES 20 - 22 from the Intangibles Draft

(This chart is for discussion purposes only and does not reflect MDW's views or comments.)

Page 27 of 180

Hindsight

The Tax Court of Canada has many cases that consistently state each case must be decided based on the facts and circumstances at the time without the benefit of hindsight.

... the Court must not second-guess the business judgment of the taxpayer ... should not use the benefit of 20-20 hindsight to substitute its judgment for the taxpayer’s judgment ...

... the determination ... was made not with the benefit of hindsight. When expenditures are being incurred by a person, that person does not know what the future will hold. Expenses should not be denied simply because a person, with the benefit of hindsight, made a poor business decision.

... This is easy to say in hindsight but not reasonable ...

MDW CONSULTING INC. Page 4

Page 28 of 180

Recommendation

Please consider the following guidance to be included: a) A tax administration’s examination of a controlled transaction ordinarily should be

based on the transaction actually undertaken by the associated enterprises as it has been structured by them, using the methods applied by the taxpayer insofar as these are consistent with the methods described in Chapter III.

b) If the contractual arrangements between the related parties include a price adjustment clause or other terms that require the use of information after the fiscal year or tax filing of the transaction, the tax authority should then be allowed to consider and use this information as it relates to the contractual arrangements.

c) If the economic substance of a transaction differs from its form, the tax authorities should then be allowed to consider the actual facts and circumstances (i.e., not assumptions) involving independent enterprises in the same or similar circumstances, and compare this to a transaction between related parties.

d) In other than the exceptional circumstances described above, information after the fiscal year or tax filing of the transaction should not be used to determine or adjust the arm’s length price of a controlled transaction.

MDW CONSULTING INC. Page 5

Page 29 of 180

References

For further details, please consider:

a) MDW’s comments on the OECD’s Discussion Draft on Intangibles.

b) MDW’s comments on the OECD’s Discussion Draft on Timing Issues.

c) Contacting the presenter at:

Matthew Wall CA CBV MDW Consulting Inc. 416.737.2276 [email protected]

MDW CONSULTING INC. Page 6

Page 30 of 180

OECD - WP 6 - Special Session on the Transfer Pricing Aspects of Intangibles

Paris, November 12, 2012

www.pwc.de

Dr. Jutta Menninger

Page 31 of 180

PwC

Determination of Transfer Prices when valuation is uncertain: What is “highly uncertain”?

• Current Discussion Draft on Intangibles (DDI): paragraphs 171 - 178

• Par. 171 DDI: When valuation of intangible property at the time of the transaction is highly uncertain. See par. 9.87 TPG

• Par. 9.87 TPG: Transaction of an intangible when it does not have an established value (e.g. pre-exploitation).

• Several disciplines (economics, physics, natural science) provide support, how to deal with risk and uncertainty via statistical tools.

• Valuation practice uses methods like the Monte Carlo Simulation:

- Sensitivity analysis to understand the effect of uncertainty,

- Numerical estimation of probability distribution,

- Random number generators with certain statistical properties.

2

November 2012

Page 32 of 180

PwC

Determination of Transfer Prices when valuation is uncertain: Steps to deal with high uncertainty

• Par. 172 DDI: In determining the anticipated benefits, financial valuation techniques, particularly those based on the discounted value of projected cash flows, may be helpful tools.

• Par. 173 DDI: Shorter-Term agreements or price adjustment clauses

• Par. 174 DDI: Renegotiation of pricing agreements by mutual agreement of the parties

• Par. 175 DDI: The arrangements that would have been made in comparable circumstances by independent enterprises should be followed without using hindsight.

3

November 2012

Page 33 of 180

PwC

Determination of Transfer Prices when valuation is uncertain: Suggested changes to DDI

• Define, what is meant by “highly uncertain”.

• Introduce statistical tools as a means to deal with risk and uncertainty, e.g. in par. 172 and maybe also in example 21.

• In most cases performing a sensitivity analysis based on statistical tools should be sufficient to determine a reliable transfer price at the time of the transaction.

• Alternatively the taxpayer might be allowed to agree a price adjustment clause at the time of the transaction; although it should be noted, that in third party transactions this is not very often the case.

4

November 2012

Page 34 of 180

PwC

Contact WP/StB Dr. Jutta Menninger Partner Transfer Pricing and Valuation Services PwC Munich, Bernhard-Wicki-Str. 8 Phone: +49 89 5790-6400 E-Mail: [email protected]

5

November 2012

Page 35 of 180

Thank you…

© 2011 PricewaterhouseCoopers AG Wirtschaftsprüfungsgesellschaft. Alle Rechte

vorbehalten. In diesem Dokument bezieht sich "PwC" auf die PricewaterhouseCoopers

Aktiengesellschaft Wirtschaftsprüfungsgesellschaft, Frankfurt am Main, die eine

Mitgliedsgesellschaft der PricewaterhouseCoopers International Limited (PwCIL) ist. Jede der

Mitgliedsgesellschaften der PwCIL ist eine rechtlich und wirtschaftlich selbständige

Gesellschaft.

Page 36 of 180

SESSION III

GENERAL DEFINITIONAL APPROACH FOR INTANGIBLES

Speakers:

Jennifer RHEE, Richter Consulting

Vanessa. DE SAINT BLANQUAT, MEDEF

Anne QUENEDEY, SALANS

Page 37 of 180

WWW.RICHTERCONSULTING.COM

Public Consultation with the OECD Definitional Aspects of Intangibles

Paris

November 12 - 14, 2012

Page 38 of 180

OECD Invites Comments on the Scoping of its Project on

Intangibles - 2010

• Need for a clear definition and criteria of “intangibles” for transfer pricing purposes:

– Accounting, legal, economic, or transfer pricing definition.

• Categorization of intangibles:

– “Soft” vs. “hard” intangibles;

– Routine vs. non-routine intangibles;

– Legally vs. non-legally owned intangibles.

• Further guidance on specific types of intangibles:

– Marketing intangibles;

– Know-how and trade secrets.

1 Page 39 of 180

The Scoping Document on Intangibles is Released by the

OECD - 2011

• Specific areas identified for further work in terms of definitional aspects related to intangibles:

– Usefulness of language related to payment for transfers of “something of value” from Chapter IX;

– Relevance and usefulness of accounting, financial valuation, and legal definitions;

– Factors to consider in determining whether or not an intangible is used or transferred:

• Future economic benefits;

• Legal protection;

• Separate transferability.

– Relevance and usefulness of the categorization of intangibles:

• Routine and non-routine intangibles;

• Marketing and trade intangibles.

2 Page 40 of 180

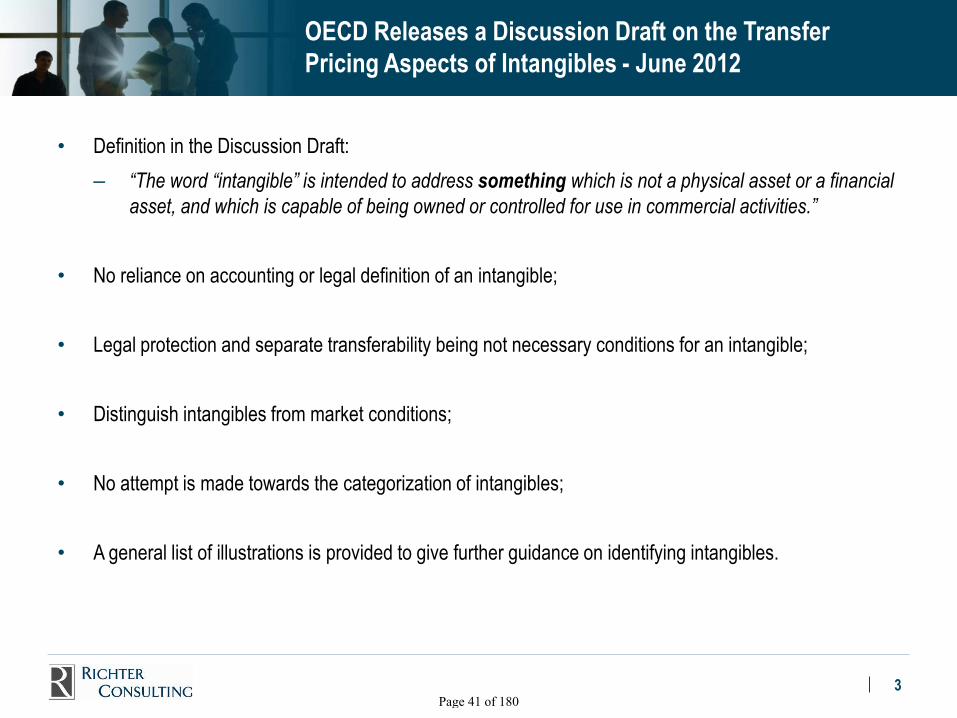

OECD Releases a Discussion Draft on the Transfer

Pricing Aspects of Intangibles - June 2012

• Definition in the Discussion Draft:

– “The word “intangible” is intended to address something which is not a physical asset or a financial

asset, and which is capable of being owned or controlled for use in commercial activities.”

• No reliance on accounting or legal definition of an intangible;

• Legal protection and separate transferability being not necessary conditions for an intangible;

• Distinguish intangibles from market conditions;

• No attempt is made towards the categorization of intangibles;

• A general list of illustrations is provided to give further guidance on identifying intangibles.

3 Page 41 of 180

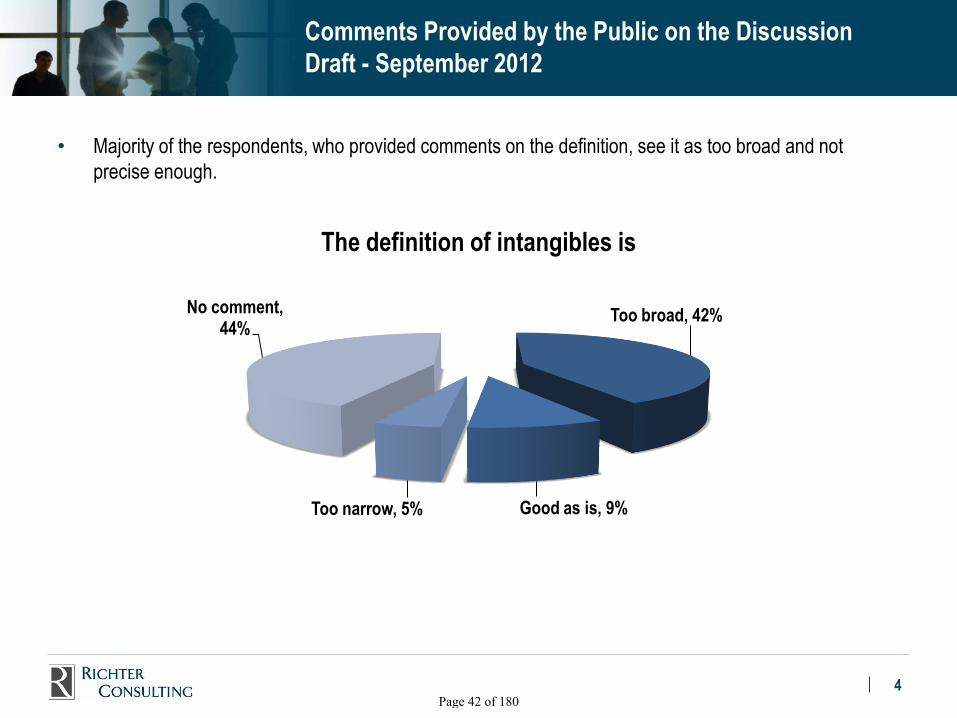

Comments Provided by the Public on the Discussion

Draft - September 2012

• Majority of the respondents, who provided comments on the definition, see it as too broad and not

precise enough.

4

Too broad, 42%

Good as is, 9% Too narrow, 5%

No comment, 44%

The definition of intangibles is

Page 42 of 180

Comments Provided by the Public on the Discussion

Draft - September 2012

• Major areas of concern of the public with respect to the definition of intangibles:

– An intangible is defined as “something”, and not as an “asset” or as a “property”;

– Transferability of an intangible;

– Legal and/or contractual protection of an intangible.

• Other concerns:

– Categorization of intangibles;

– Goodwill and going concern as intangibles;

– Assembled workforce viewed primarily as non-intangible;

– Group synergies.

5 Page 43 of 180

Questions

• Does the Discussion Draft achieve the objectives established in the scoping document?

• Does the definition of intangibles assist in the following:

– Identify when an intangible asset has been transferred between related companies; or

– Identify the existence of an intangible asset in determining intercompany pricing?

6 Page 44 of 180

General definitional approach for intangibles

Vanessa de Saint-Blanquat

OECD – 12th November 2012

Page 45 of 180

2

Why is a clear definition of intangibles necessary in the area of transfer pricing?

Key concerns:

1. Intangible assets resulting from a subjective view (ex-post analysis, vague definition, valuation, related return, residual profit split …) a) will create intangibles that might not be internationally recognised as such

b) contradicts the aim of the OECD TP Guidelines that transaction and its price can only be determined if its nature is previously and clearly identified

c) creates insecurity for both taxpayers and tax administrations + increases double taxation risks

2. Solution should be based on simple definition and formal process

3. Objective : to protect administration and MNE’s interests (proper allocation of profits & facilitating business economic activities)

Page 46 of 180

What is an asset? What is an intangible? What is an intangible asset?

ASSET

Recognised by legal, contractual or accounting principles and subject to

ownership, control and transferability

INTANGIBLE

3 cumulative factors : protection (ex ante or ex post),

functions (creation, maintenance and management),

costs

INTANGIBLE ASSET

Meets both criteria of an intangible and an asset

(all assets are not intangibles and all intangibles are not assets)

3

Not an asset if not transferrable (excluded : “something”)

Not an intangible if only “right of income”, added-value or expense

Page 47 of 180

What about in practice?

An intangible that is not an

asset

A company owns an intangible and licenses it to its subsidiary, which sells and commercialises the goods or services developed by its parent company. The subsidiary indeed contributes to local market development and needs to earn sufficient margin to reflect this, but does not “co-own” its parent’s intangible because it solely plays a normal role in the value chain

An asset that is not an intangible

If a company restructures its business and ceases to carry out an activity that is transferred to another company in the group (eg: a local company is closed as another company handles its activity with more synergies at a regional level from another country), some assets may be transferred from one company to the other, but such transfer of assets does not imply the transfer of an intangible

4

Process : 2 step analysis 1. Does an intangible exist? (according to the aforementioned definition) 2. How is it included in the TP policy ? (according to economic & functional analysis)

Page 48 of 180

Intangibles : the relevance of property law

definitions, accounting definitions and

separate transferability

Anne Quenedey

Partner

Email : [email protected]

12 November 2012

Page 49 of 180

Relevance of property law definitions

Most detailed comments not in Part A “Identifying Intangibles” (paragraph

7) of the Discussion Draft but in Part B “Identification of Parties Entitled to

Intangible Related Returns” (paragraphs 30 to 36)

What is already acknowledged in the Discussion Draft:

Intangibles protectable under intellectual property registration systems

Intangibles legally protected via unfair competition legislation or other

unforceable laws or by means of employment contracts

“There may also be intangibles whose use is not protected under any

applicable law” (paragraph 32)

However : “Because legal registrations and relevant contracts form the

starting point for an analysis of which members of an MNE group are

entitled to intangible related returns, it is good practice for associated

enterprises to document in writing their decisions to allocate significant

rights in intangibles […].” (paragraph 36)

Page 50 of 180

Relevance of accounting definitions

“Intangibles that are important to consider for transfer pricing purposes

are not always recognised as intangible assets for accounting purposes.”

(paragraph 6)

Comments on the example of research and development costs:

Research and development costs are not always booked as an asset for

accounting purposes (paragraph 6)

Not all research and development expenditures produce or enhance an

intangible (paragraph 10)

accounted : YES = INTANGIBLE

R & D

accounted : NO

accountable : YES = INTANGIBLE ?

accountable : NO

Page 51 of 180

Relevance of separate transferability

Discussion Draft:

“while some intangibles may be identified separately and transferred on

a segregated basis, other intangibles may be transferred only in

combination with other business assets. Therefore, separate

transferability is not a necessary condition for an item to be characterised

as an intangible for transfer pricing purposes.” (paragraph 7)

“It may sometimes be difficult or impossible to segregate or separately

transfer the various intangibles contributing to brand value.” (paragraph

19)

“It is generally recognized that goodwill and ongoing concern value

cannot be segregated or transferred separately from other business

assets.” (paragraph 21)

Transferability separate or not is a necessary condition

Page 52 of 180

SESSION IV

CATEGORIES OF INTANGIBLES

Speakers:

Ronald VAN DEN BREKEL, Ernst & Young

Wendy NICHOLLS, Grant Thornton UK

Page 53 of 180

Discussion Draft on Intangibles

OECD Public Consultation 12 November 2012

Ronald van den Brekel, Ernst & Young

Page 54 of 180

Agenda

► Introduction

► Use of concept

► Points of attention

Page 55 of 180

Introduction

► Section D.1.(vi) Intangibles: ► An intangible (i) that is not similar to intangibles used by or

available to parties to potentially comparable transactions, (ii)

whose use in business operations (e.g. in manufacturing, provision

of services, marketing, sales, or administration) is expected to yield

greater future economic benefits than would be expected in the

absence of the intangible, and (iii) whose use or transfer would be

remunerated in dealings between independent parties, will be

referred to as a Section D.1.(vi) intangible.

► Unique and valuable intangibles vs. routine intangibles in

context of comparability

► Relationship with profit split

Page 56 of 180

Use of having a definition of a unique and valuable intangible

► Welcome attempt to clarify “unique and valuable”

► DD par 121: “only where the intangibles in question can be clearly and distinctly identified and where the intangibles are manifestly section D.1.(vi) intangibles.

► Relationship with “unique and valuable contributions”

► Comparability ► 1) tested party = “routine” function -> avoid (routine) rejection of

comparables

► 2) tested party = intangible owner -> proposed concept might lead to (routinely) rejecting CUT’s

Page 57 of 180

Points of attention

► Concept

► Avoid “artificially” splitting an intangible into several “micro

intangibles” or otherwise “unbundling” or “atomizing” intangibles

► To distinct between unique/valuable and routine. However: risk

that comparability factors by “backdoor” are promoted to

intangibles -> to be clarified

► Definition in draft

► Replace by more natural term

► Subjective and circular -> to be further elaborated

Page 58 of 180

Ernst & Young

Assurance | Tax | Transactions | Advisory

Ernst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 167,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

© 2012 EYGM Limited.

All Rights Reserved.

This publication contains information in summary form and is therefore intended for general guidance only. It is not

intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYG Limited nor any

other member firm of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person

acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be

made to the appropriate advisor.

Page 59 of 180

© 2012 Grant Thornton UK LLP. All rights reserved.

Categorisation of Intangibles: Should the Discussion

Draft Distinguish Between Routine vs. Unique and

Valuable Intangibles?

Wendy Nicholls

Partner, Head of Transfer Pricing

Grant Thornton UK LLP

Page 60 of 180

© 2012 Grant Thornton UK LLP. All rights reserved.

Routine vs Non-routine: not helpful; not clear; not useful?

• Are 'routine' intangibles something that protects the business from competition

but do not create super profits?

• If so, 'routine' intangibles are presumably assets or rights used in the ordinary

course of business, for example brought into being by

'normal' levels of expenditure on marketing (by distributors) or

know-how that is widely available in the market (by a manufacturer or

service provider)

• Our (and some other contributors') views are that intangibles must be capable of

separate transferability for a consideration

• Hence, we do not consider that most 'routine' intangibles would be intangibles

and the distinction would be moot

• The Draft suggests 'separate transferability is not a necessary condition...' (para

7) but does seem to agree that the routine vs non-routine distinction is not

necessary and the approach should 'not turn on these categorisations' (para 13)

Page 61 of 180

© 2012 Grant Thornton UK LLP. All rights reserved.

Routine vs Non-routine: are they terms used by business?

• Is a 'routine' intangible actually an intangible at all?

• Is it an arbitrary distinction? Are these terms used by businesses?

• Is there a 'bright line' between what is routine and what is not?

• Does one extra euro of marketing spend require the parties to share the

intangible related returns? Is that consistent with third party behaviour?

• We agree not all intangibles, even unique ones, are valuable (consider all the

redundant patents that gather dust on shelves) or consistently maintain that

value throughout their lives.

• We also agree that the distinction between valuable intangibles (which would

generate extra profit potential and which one might be able to sell) and other

intangibles is vital to get the transfer pricing right

• The concept of 'unique and valuable' is therefore a helpful distinction (see para

128 regarding profit split and para 2.109). Distinguishing the term 'unique and

valuable' reduces the need for inclusion of the term 'routine'.

Page 62 of 180

© 2012 Grant Thornton UK LLP. All rights reserved.

Routine vs Non-routine: suggested way forward

• Whilst para 13 suggests that WP6 has not relied on the routine vs non-routine

distinction, references are made to it in para 108 (residual profit split), para 148

(financial projections) and again in para 166 (useful life)

• If, as we and presumably WP6, believe, the routine vs non-routine distinction is

arbitrary, tends towards over simplistic assumptions and does not add clarity to

the analysis of who should get 'intangible related returns', then these

inconsistent references should be removed

• In conclusion:

We agree with WP6's view that there should not be a distinction between

routine and non-routine intangibles

We consider that the distinction between 'unique and valuable' intangibles

and other intangibles is vital to get the transfer pricing right

Further guidance on comparability is needed in this area (especially

qualitative factors) and work is required to make the wording in the Draft

more internally consistent

Page 63 of 180

SESSION V

TREATMENT OF GOODWILL AND WORKFORCE IN PLACE

Speakers:

Caroline SILBERZTEIN, Baker & McKenzie

Agata UCEDA, International Tax Centre, Leiden

Laurence DELORME, A3F

Page 64 of 180

BAKER & MCKENZIE GLOBAL TRANSFER PRICING AND GLOBAL TAX

POLICY GROUPS

Goodwill and transfer pricing

OECD consultation, 12-14 November 2012

Caroline Silberztein, Partner

Page 65 of 180

Need clear definition(s) for an "important and monetarily

significant" TP intangible: different words for fundamentally

differing concepts (not a mere question of “context”):

Name Proposed definition Reference

Goodwill Portion of the purchase price, paid in

the context of an acquisition of an

entire business, which is not allocable

to any identified asset of said

acquired business

Accounting

Going concern A business or activity which is not

about to be liquidated

Accounting

Common law

goodwill

Clientele, activity Legal

Profit potential Expected future profits / losses Not an intangible asset but

a concept used for

valuation purposes; see

Glossary and TPG 9.66

Reputational

characteristics

Reputational characteristics of

otherwise existing assets

Comparability factors

2

Page 66 of 180

Examples could be improved if it was made clear

what notion they are referring to:

– Example 13 : “… over the years of its operation in branch form,

Ilcha developed substantial goodwill and ongoing concern value

in country B. The transfer of the going business to Company S…

implicitly conveys the value of that continuing goodwill to

Company S” => Valuation of assets transferred in combination?

– Example 14: Whether Company S is or is not ”entitled to

intangible related returns associated with goodwill in respect of

Product Y created through the advertising costs it has borne.”

=> Product-related marketing intangible?

– Example 15: “Depending on the facts, a substantial portion of the

value described in the purchase price allocation as goodwill of

Company T may have been transferred to Company S together

with the other Company T intangibles… may have been retained

by Company T.” => Premium paid above identified asset value? 3

Page 67 of 180

Goodwill (accounting definition, “survaleur”) may

arise from a number of factors, for instance:

– Intangible assets which are not identified or are specifically allocated

to goodwill for accounting purposes

– Control premium paid by the acquirer,

– Premium to exclude competitors from the acquisition

– Premium paid because of anticipated synergies with the

acquirer's other assets or activities (may or may not materialise)

– Over-optimistic evaluation by an acquirer who has imperfect

information on the assets and liabilities of the acquired entity

(as is always the case in arm's length acquisitions)

– Etc.

Goodwill should therefore not be assumed to systematically

correspond to the value of assets of the acquired entity;

Goodwill value may or may not disappear, depending on the

facts and circumstances of each case.

4

Page 68 of 180

BAKER & MCKENZIE GLOBAL TRANSFER PRICING AND GLOBAL TAX

POLICY GROUPS

Thank you for the opportunity to share

our views and contribute to the debate

on this important OECD project.

Page 69 of 180

Goodwill definition Accounting: purchase price minus fair market value of assets

Psychology (buyer): bigger ego of the CEO -> bigger goodwill

Commercial/Legal: good reputation, clientele and established (assembled) well run business

Other languages: fondo de comercio (well established, synergies of the business)

Etymology: hope that "good will" come and several religious meanings

Synergy and established/assembled business common factor in all definitions

In all cases the concept has an objective/intrinsic component and (often more dominant) subjective/external component

Date of presentation Insert filename here 1 Page 70 of 180

Goodwill measurement Value, like beauty, is in the eye of the beholder

Aggregate value of assets vs. sum of separate tangibles and intangibles (definition in draft par. 20) ~ what is the difference to synergies?

If all intangibles assets are already identified and valued AND synergies, market circumstances, assembled workforce and other factors are considered in the comparability analysis: is there anything left?

Is there really anything left?

Most likely not, but if there is, that must be "goodwill"

Proposition: goodwill for transfer pricing purposes as the synergies resulting from having certain Functions Risks and Assets established

Date of presentation Insert filename here 2 Page 71 of 180

Can you count the black dots?

Date of presentation Insert filename here 3

Page 72 of 180

Why does it matter? For transfer pricing purposes goodwill matters primarily when

buying/selling assets intercompany: is there any goodwill? where? how do we account for it?

Possible scenarios: When selling going concern (full business): what happens to goodwill?

When selling only some fixed or intangible assets whereas rest of the business stays: what happens to goodwill?

When selling a combination of Functions Risks and Assets ("FRAs") while some FRAs stay locally: what happens to goodwill?

Date of presentation Insert filename here 4 Page 73 of 180

The OECD public consultation on the Discussion Drafts on issues related to Transfer Pricing Safe Harbours, Timing Issues and Intangibles

The OECD Conference Centre, Paris

12-14 November 2012

Discussion Draft (« DD ») on Intangibles Provisions on Assembled Workforce

Laurence Delorme

Page 74 of 180

Assembled Workforce in DD Section A paragraphs 25 & 26, and section D paragraph 124

Comparability factor

impacting arm’s length price for services

(25) Existence of a uniquely qualified/experienced employee group may affect arm’s length price for services provided or goods produced

(26) Transfer of an existing assembled workforce may provide a benefit to the transferee by saving it expense/difficulty of hiring and training new workforce

(26) Transfer or secondment of isolated employees does not, in and of itself, constitute the transfer of an intangible

(124) Comparability adjustments may be required for matters such as assembled workforce. While such factors may not be intangibles (within meaning of section A.1.), they can nevertheless have important effects on arm’s length prices in matters involving the use of intangibles.

Intangible

capable of being transferred for a price

(26) Contractual rights and obligations MAY be intangibles within meaning of section A.1, so that a long term contractual commitment to make available the services of uniquely qualified employees MAY constitute an intangible

(26) As a factual matter, a transfer or secondment of employees MAY result in the transfer of valuable know-how or trade secrets for which compensation MAY be required in arm’s length dealings.

12 November 2012 A3F Association Française des Femmes Fiscalistes 2 Page 75 of 180

Business comments (1/2)

• Ambiguities in DD

(i) what is meant under “transfer of an assembled workforce”, and

(ii) whether “assembled workforce” qualifies as an intangible (within the meaning of section A.1 of the DD), or comparability factor (paragraph 124)

• Clarifications needed

Circumstances when “a long term contractual commitment to make available the services of

uniquely qualified employees may constitute an intangible”

– Employer entitled to claim compensation from an employee, based on e.g. unfair competition legislation or labour law, employment contract restricting employee’s freedom (non compete, non disclosure agreement, star athletes’ contracts)

– Where this is the case based upon legal rights and obligations, transaction to be valued would relate to know-how and trade secrets themselves (or to value provided in the contract), and not to group of employees

• Clarifications and practical guidance needed

– How in practice to undertake comparability adjustments for differences in factors such as assembled workforce

12 November 2012 A3F Association Française des Femmes Fiscalistes 3 Page 76 of 180

Business comments (2/2)

• Employee secondments (international mobility within MNEs)

– Globalization, division and specialization of labour within MNEs – Economic necessity for cooperation on an international basis => extensive secondment

programs for engineers and management executives – Seconded employees retain employment contract with home office and remain on home

payroll – Service transactions, appropriately compensated with a cost or cost plus method – Skills and expertise as comparability factors only, not intangibles

• Assembled workforce

– Cannot be “owned or controlled” by the employer, hence cannot be sold or licensed independently of the entire business to which the workforce relates, i.e. issue of “transfer of an assembled workforce” arises only as part of a business transfer

– As such, to be considered as business attribute that influence the value of an MNE’s assets, but not to be qualified as an intangible asset

– Assembled workforce is NOT an intangible within the meaning of section A.1 – Assembled workforce can contribute to the development of intangibles (e.g. know-how and

other legally protectable intangibles), and should be taken into consideration in transfer pricing comparability analysis

12 November 2012 A3F Association Française des Femmes Fiscalistes 4 Page 77 of 180

SESSION VI

DOES THE DISCUSSION DRAFT FOCUS TOO HEAVILY ON

RESTRAINING ABUSIVE BEHAVIOUR?

Speakers:

Georg GEBERTH, BIAC

James PHILLIPS

Page 78 of 180

Seite 1/5 November 2012 Georg Geberth (Siemens AG)

Public Hearing on the treatment of Intangible

Assets

12th November 2012

Paris

Does the Discussion Draft focus too heavily on

Restraining Abusive Behaviour?

Page 79 of 180

Seite 2/5 November 2012 Georg Geberth (Siemens AG)

Businesses need a clear Definition of „Intangible“ not driven by Anti-Abuse

The draft definition (« something ») is too vague and clearly driven by

anti-abuse thoughts. Businesses need more clarity.

Foundation of a Definition of Intangibles

• Legal principles

• Accounting Principles

• Contractual arrangements

Possible elements of a definition

• An asset

• Being capable of being owned and controlled

• Separately transferrable

Page 80 of 180

Seite 3/5 November 2012 Georg Geberth (Siemens AG)

Business concerns over Anti-Abuse Language

The draft implicitely focuses on abuse by mentioning numerous times

that legal consequences apply only « where the parties’ conduct is

aligned with contracts » etc.

Examples:

• In total this or a similar wording is being used in at least 13 Paragraphs (29,

35, 37, 38, 40, 41, 42, 44, 46, 48, 55, 66, 180)

• It would be better to have a clear wording, without mentioning the possibility

of an abusive behaviour in all those cases

• Instead, a general clause could be added at the end of the text

Page 81 of 180

Seite 4/5 November 2012 Georg Geberth (Siemens AG)

Instead, Businesses need a clear Allocation Process

The draft does not define a clear and reliable process for the Allocation

of Intangible Assets. Businesses need more certainty.

Allocation of Intangibles:

• Who owns legal protection?

• Who performs functions in relation to the ownership, the maintenance or the

management of the intangible?

• Who incurs costs in relation to the intangible?

• Right to earn income from exploiting the asset

• Right to exclude others from exploiting the asset

• Right to transfer ownership or use of the asset to another owner

Page 82 of 180

Does the Discussion Draft focus too heavily on restraining abusive

behaviour?

Tuesday 13 November

James Phillips Comments are provided in a personal capacity only

Page 83 of 180

• The purpose of the OECD Guidelines should be to provide a common and objective framework, acceptable to both businesses and tax administrations, multilaterally, to help reduce the risk, and the incidence, of double or less than single taxation.

• The purpose of the OECD Guidelines is not to provide, or substitute for domestic, anti-avoidance or anti-abuse guidance or legislation.

• Unfortunately, the general tone of the current draft, no doubt a reflection of governments under domestic political pressure to increase tax yields from MNEs, seems to emphasise a preconception of, certain, tax administrations that the OECD Guidelines are an avoidance tool used by multinationals to avoid taxation which is their due.

• Whilst it may seem self-evident, it does bear repeating that MNEs are just as worried about double taxation as Tax Administrations and their governments are about less than single taxation, and this dynamic can impact investment decisions.

• This is most particularly true at the interface between Developed and Emerging Economies and intangibles are a frequent source of concern on such issues.

Introductory comments

Page 84 of 180

• The organisation and structuring of IP by an MNE is often done for wholly legitimate business reasons and it should not be seen as some form of automatic indication of aggressive tax planning.

• It is best practice for businesses to ensure strong control, which can often mean centralised control, of all of their high-value assets and this is even more true of intangible assets which are at particular risk of being exploited in an unauthorised manner.

• Businesses are required to respect the arm’s length principle, including for their intangibles - it is not a choice and correct transfer pricing is, in nature, a compliance obligation.

• Whilst profit splits for intangibles may superficially appear tempting, their current emphasis in Chapter VI is likely to generate serious unwanted consequences, particularly in relation to materially higher compliance burdens and costs for MNEs and significantly greater incidences of double taxation.

• Chapter VI, once finalized, should strive to continue the OECD’s solid track record in guiding Tax Administrations and MNEs alike in their interpretation of Article 9, particularly in such a difficult topic area as intangibles.

Introductory comments

Page 85 of 180

• The OECD Guidelines and Chapter VI must therefore continue to be fundamentally based around what independent parties would do in unrelated transactions – i.e., they must reaffirm the pre-eminence of the arm’s length principle in the context of the transfer pricing of intangibles.

• More specifically, the Guidelines should focus around their primary and founding purpose – to provide an acceptable structure for taxpayers and tax administrations to work within in order to help avoid double and less than single taxation and, by so doing, allow international trade to grow and do its part to help rebuild the world economy.

• Using the OECD Guidelines other than for determining the arm’s length principle is to render the consensus weakened for increased international trade which has been so important in helping deliver economic growth, and reducing global poverty, over the last 20 years.

• The current financial crisis will, eventually, pass - it is far from historically unique. If, however, an additional long-term impact of the Great Recession is to retrench cross-border trade by reducing opportunities for profitable gain via the institutionalisation of double taxation, its legacy will be even more negative than it already is.

Introductory comments

Page 86 of 180

SESSION VII

DOES THE DISCUSSION DRAFT PLACE TOO MUCH EMPHASIS ON

PROFIT SPLIT APPROACHES?

Speakers:

Gary SPRAGUE, Treaty Policy Working Group

Arnaud LE BOULANGER, CMS Bureau Francis Lefebvre

Page 87 of 180

TREATY POLICY WORKING GROUP

Does the Discussion Draft Place Too Much

Emphasis on Profit Split Approaches?

OECD WP6 Consultation, 12-14 November 2012

Gary D. Sprague, Partner ([email protected])

Holly E. Glenn, Principal Economist ([email protected])

Page 88 of 180

Discussion Draft Does Place Too Much Emphasis

on Profit Split Approaches

– Under the most reliable method requirement of the TPG, a method other than

the PSM normally is the most appropriate method to apply to many

transactions involving rights in or use of intangibles.

– All other methods (except CUP) are based directly on comparable entities

which themselves own and exploit the important intangibles necessary for

their business.

Comparable distribution entities may own client lists, operate in fast growing

markets, employ an experienced sales force, and have experience in branded

goods distribution.

Comparable manufacturing entities may own process technology, employ a

skilled workforce, and own highly sophisticated production assets.

Comparable R&D entities may employ highly skilled engineers, have deep

expertise in the industry, and have a long track record of developing successful

products.

– “Comparable” does not mean “identical”. It means no material differences, or

that material differences can be addressed with “reasonably accurate

adjustments”. TPG 1.33.

– Assuming reliable comparables (with comparability adjustments when

needed), a one-sided method is appropriate in most cases and a CUP method

also normally is more reliable than a PSM.

2 Page 89 of 180

Existing TPG Guidance on Selection of Methods

Normally Can Apply

– One-sided methods normally should apply when local entity is not making

unique contributions. TPG 2.59, 3.18, 3.19.

TPG 2.109 refers expressly to contract manufacturing and contract service

activities.

– The use of intangibles that are normal to the function is not a reason to use a

two-sided method. TPG 2.60.

Examples: distribution of branded goods, deployment of experienced

development team, manufacturing using process intangibles.

We agree with DD para. 87 on this point.

– Comparability adjustments can be made as necessary. TPG 2.68.

Example: adjustments can account for differences in technology in product,

barriers to entry, growing market share, etc. TPG 2.72.

– The TPG provide additional tools to increase reliability.

Use of the arm’s length range. TPG 2.73.

Choice among different possible net profit indicators. TPG 2.76.

3 Page 90 of 180

Discussion Draft Should Focus on Reliability

– PSM frequently is an appropriate method when exploitation and further

development rights are transferred, as both sides to the transaction typically

are making unique and valuable contributions.

– PSM is not the most appropriate method when reliable comparables exist to

used a one-sided method.

Use of PSM, usually without comparable data, generally requires economically

complex and frequently controversial assumptions.

Fact that a group is profitable or that “something of value” may exist in an

entity’s business is not a principled reason to employ PSM.

PSM will also require loss sharing, if method is applied consistently.

– Recommendations:

Discussion Draft should acknowledge cases where one-sided methods normally

are appropriate.

Further guidance could be provided on comparability factors and on use of

comparability adjustments to improve reliability of one-sided methods in

transactions involving the use of intangibles.

Further guidance could be provided in TPG 3.38 and 3.39 for cases where

availability of local comparables is limited.

Paras. 128, 136 and 141 should be reconsidered.

4 Page 91 of 180

TREATY POLICY WORKING GROUP

Thank you for the opportunity to share our

views and contribute to the debate on this

important OECD project.

Page 92 of 180

|

OECD – Public consultation on transfer pricing discussion

drafts - Intangibles

Does the Discussion Draft Place Too Much Emphasis

on Profit Split Approaches?

Arnaud Le Boulanger, CMS Bureau Francis Lefebvre

Partner, Chief Economist

13 November 2012

OECD Conference Centre, Paris

Page 93 of 180

|

Does the Discussion Draft Place Too Much Emphasis on

Profit Split Approaches?

– Many commentators (more than 25) discuss in their response the fact that

the discussion draft places too much emphasis on Profit Split approaches, or

at least present drawbacks of this method that may not be sufficiently

addressed in the document

• Why do respondents largely appear to express the same general comments?

• Recommendations to better balance the merits and drawbacks of the Profit Split

method compared to others

13/11/2012 2 Page 94 of 180

|

Why do so many respondents believe that the discussion

draft places too much emphasis on Profit Split approaches?

– The proposed guidelines set quite significant restrictions to the use of

any methods…

– Standards required for comparability purposes have been raised again to a level

that may disregard the concept of reasonableness expressed in Chapter I of the

OECD Guidelines

– The draft includes a very interesting discussion on valuation techniques.

However, the draft is largely focused on the drawbacks of these methods and on

the degree of subjectivity required to apply them

– Other methods, such as some one-sided ones as the TNMM, are not specifically

discussed in the draft

– … except to the use of the Profit Split method

13/11/2012 3 Page 95 of 180

|

Recommendations to better balance the merits and

drawbacks of the Profit Split method compared to others

– Does the Discussion draft miss some drawbacks of the Profit Split method?

• Is this really a method that unrelated parties would use for intangibles?

– Unrelated parties only rarely share any information regarding their profits, in transactions involving strategic assets such as intangibles

– In what circumstances would unrelated parties use it for intangibles?

– How to minimize possible debates between taxpayers and tax administrations over Profit Split approaches when applied to transactions involving intangibles?

• In our experience, Profit Split methods that create less debates between taxpayers and tax administrations are generally those based on allocation keys using obvious, quantitative data readily available such as costs or workforce.

• Is this applicable to transactions involving intangibles?

13/11/2012 4 Page 96 of 180

SESSION VIII

INTANGIBLES:

ENTITLEMENT TO INTANGIBLE RELATED RETURNS

Speakers:

Alison LOBB and John HENSHALL, Deloitte

Linda FERNANDEZ, Transfer Pricing Discussion Group

Page 97 of 180

© 2012 Deloitte LLP. Private and confidential.

The treatment of risk and control of risk, including the consistency of the draft with Chapter IX TPG

Revision of Chapter VI Special Considerations for Intangibles

WP6 Public Consultation

13 November 2012

John Henshall, Partner, Deloitte

Page 98 of 180

© 2012 Deloitte LLP. Private and confidential.

Recognition of the arm’s length principle • Intangible property rights are commercial assets; a form of monopoly granted

by law.

• The arm’s length principle requires that MNEs follow what happens between

unrelated parties according to IP laws and commercial practice.

• The Guidelines need to help MNEs and tax authorities to understand what

happens between unrelated parties and how to gather evidence to show

compliance with the arm’s length principle. The level of functional control

required is therefore that which an independent party would be expected to

have in comparable circumstances.

• Where comparable data exists to show the allocation of risk associated with

intangible-related activity, this is the best material that MNEs and tax authorities

can provide to evidence compliance with the arm’s length principle. If such

evidence is available, and comparability adequately assessed, then compliance

with the arm’s length principle has been satisfied.

• Where such third party evidence is not available, then, as for functions, the

guidance should take into account the allocation of risk when allocating

intangible related returns. In that case, is there consistency with Chapter IX?

2 OECD WP6 Public Consultation Nov. 2012 Page 99 of 180

© 2012 Deloitte LLP. Private and confidential.

Consistency with Chapter IX (Business Restructuring) • Inconsistency can arise between Chapter VI and Chapter IX only if the

guidance in either one would lead to a non-arm’s length result.

• Per Chapter IX the examination of risks should start with the contractual

arrangements between the parties. The three additional questions that should

be asked also apply to intangibles: ‒ Is the allocation of risks in the controlled transaction arm’s length?

‒ Does the conduct conform to the contractual allocation?

‒ What are the consequences of the risk allocation?

• The impact of the allocation of risk, and conduct of the parties, is decided for

independent parties by IP law. Chapter VI must respect that position under the

arm’s length principle.

• Commercial court cases around the world provide one source of evidence of

how third parties should agree the impact of risk and activity allocation on the

right to enjoy a return from intangibles. This material should be used when

available to provide factual evidence of arm’s length behaviour, and in particular

takes into account the relative bargaining power of the parties.

• See for example • Jay-Lor International Inc et Al v Penta Farm Systems Ltd et Al 2007 FC358,

• Allied Signal Inc v Dupont Canada Inc (1998) 78 CPR (3d) 129,

• Uniloc USA Inc v Microsoft Corp., 632 F.3d 1292 (Fed. Cir. Jan 4, 2011) and

• Meridian International Services Limited v Richardson &ors (08) EWCA Civ 09

3 OECD WP6 Public Consultation Nov. 2012 Page 100 of 180

© 2012 Deloitte LLP. Private and confidential.

Treatment of risk if no arm’s length evidence available

• Relevant (but not conclusive) factors to consider in determining whether

arrangements are arm’s length are

• functional control of and capability to undertake risks; and

• financial capacity to bear the associated risks; and

• commercial “reality” of the transaction, including evidence of arm’s length behaviour in

a commercial setting or dispute.

This is consistent with Paragraph 9.22 of Chapter IX:

• It is only in the absence of comparable transactions evidencing the consistency

with the arm’s length principle of the risk allocation in a controlled transaction

that the examination of which party has greater control over that risk is relevant;

• In such circumstances, the examination of which party would have greater

control over the risk “...can be a relevant factor”, meaning both that it need not

be a relevant factor and that even if it is, it is not the only (or determinative)

factor; and

• The financial wherewithal to bear risk is also a relevant but not determinative

factor.

4 OECD WP6 Public Consultation Nov. 2012 Page 101 of 180

© 2012 Deloitte LLP. Private and confidential.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms,

each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and

its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will

depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of

the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific

circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any

material in this publication.

© 2012 Deloitte LLP. All rights reserved.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street

Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

Member of Deloitte Touche Tohmatsu Limited

Page 102 of 180

Topic: Entitlement to Intangible-

Related Returns Under DDI

Transfer Pricing Discussion Group (“TPDG”) Founded and Chaired by Steven Hannes,

McDermott Will & Emery

Presentation for TPDG by Linda H. Fernandez, J.D.

Eli Lilly

OECD Business Consultation on 2012 Discussion Draft on Transfer Pricing For

Intangibles (“DDI”) November 12-14, 2012

Page 103 of 180

2

Return Entitlement

• TPDG supports DDI’s introductory statement: where relevant registrations and contractual arrangements align with the conduct of the parties, the party entitled to use the intangible (and exclude others from using it) is the party entitled to intangible returns.

• TPDG strongly disagrees with (a) the DDI’s extreme “expectation” that entity claiming entitlement to returns from intangibles will perform, through its own employees, the important functions for development, enhancement, maintenance and protection of intangibles and (b) the DDI’s proposed requirement that the entity “control” important functions.

• TPDG’s objections to the “expectation” and control requirement.

– Inconsistent with third party conduct in the marketplace; an inappropriate, theoretical substitute for the arm’s length standard’s traditional reliance on facts.

– Third parties are often hired to provide services related to intangibles (R&D, marketing, and so forth); the hiring party does not control the services provider.

– Inconsistent with principles of OECD’s Transfer Pricing Guidelines (“TPG”) allowing outsourcing, whereby hiring party has capacity to decide to put its capital at risk.

– Conflicts with the fact-based and commercially-realistic standard in the DDI (e.g., Example 11) and OECD TPG for return entitlement for intangibles that are licensed.

• TPDG’s other objections to DDI’s “control” proposal.

– “Control” is not defined nor easily definable; it is not an administrable standard.

– A hiring party does not “control” a third party service provider, but it does have the capacity and expertise to enter into the contract and to bear its own risks.

Page 104 of 180

3

Return Entitlement

• Issue of Risk – The hiring party bears risks on discovery, development, enhancement, etc., but the service

provider has its own risks & opportunities.

– The OECD TPG need to clarify and recognize the different types of risk borne by the hiring

party and the service provider.

• TPDG Proposals

– The legal or contractual owner of the intangible asset that bears risks and owns opportunities should be entitled to claim intangible returns for tax purposes.

– Outsourcing of functions related to intangible discovery, development, enhancement, etc. by an “informed hiring party” with financial capacity and expertise should not jeopardize its ownership of intangibles or its entitlement to intangible-related returns.

– To the extent the intangible owner outsources many or most functions related to discovery, development, enhancement, etc., its status as intangible owner entitled to returns can be questioned by the tax authority, but the taxpayer will have the opportunity to establish as a fact that it is an “informed hiring party.” In other words, that it has the financial capacity and expertise to agree to a budget or other contractual terms with the service provider as well as to determine that the contract’s terms are followed.

Page 105 of 180

4

Return Entitlement

• Concluding TPDG Observations

– Chapter VI should use fact-based approaches anchored in the marketplace for determining entitlement to intangible related returns for both licensed intangibles and intangibles that are discovered, developed, enhanced, etc. by way of services performed by others, whether related or unrelated.

– In general, OECD TPG for intangibles (and other) pricing should avoid the DDI’s proposed reliance on speculation and theories about how either the related parties or unrelated parties “should” or “would” structure transactions or otherwise behave. Chapter VI should consistently rely on the related parties’ facts and the facts of the chosen comparables.

– Courts make decisions based on facts, not theories of behavior. Tax authorities should do the same to determine entitlement to intangible-related returns.

– The OECD TPG should consistently emphasize that before rejecting transactions or companies as “insufficiently reliable” to be used (perhaps with adjustments) as “comparables” in connection with intangibles (and other pricing matters), one must consider the relative (un)reliability of the theoretical alternatives (e.g., almost all profit splits of the residual).

* * *

Page 106 of 180

SESSION IX

INTANGIBLES:

ENTITLEMENT TO INTANGIBLE RELATED RETURNS

(CONTINUED)

Speakers:

Catherine SCHULTZ, National Foreign Trade Council

Kate NOAKES, Fidal International Direction

Ian BRIMICOMBE, AstraZeneca

Page 107 of 180