Embed Size (px)

Citation preview

Profile of International Home Buyers in Florida

2015 Report

Prepared for the Florida REALTORS®

By the Research Division, National Association of REALTORS®

September 2015

1

Profile of International Home Buyers in Florida

2015 Report The Research Division of the National Association of REALTORS®, in cooperation with the Florida REALTORS®, has conducted an annual survey of purchases of existing homes by international clients since 2005. The term international (or foreign) client refers to clients who are “citizens of another country”. This definition covers both non-resident and resident clients1:

Non-Resident Foreigners (Type A): Foreign clients with permanent residences outside the U.S. These clients typically purchase property as an investment, or for vacations or visits of less than six months to the U.S.

Resident Foreigners (Type B): Clients who are recent immigrants (in the country less than two years) or temporary visa holders residing for more than six months in the U.S. for professional, educational, or other reasons. The Florida REALTORS® issued the invitation to its members to participate in the online survey, conducted over the time period July 7 - August 9, 2015. There were 1,203 Florida REALTORS® respondents to this year’s survey who provided information on their client interaction during the 12 months ended June 2015 and on the characteristics of their most recent sale during this period.2

NAR Research Division Lawrence Yun, Ph.D., Senior Vice President & Chief Economist

Paul Bishop, Ph.D., Vice President, Research

Jed Smith, Ph.D., Managing Director, Quantitative Research

Gay Cororaton, Research Economist

1 The 2005, 2007, 2008 Florida surveys covered only non-resident international clients. Starting 2009, the Florida

surveys asked about international clients “who are citizens of another country” so this definition covers resident and non-resident international clients, both citizens of another country. NAR did not conduct a survey in 2006. 2 Some care should be taken when comparing certain results of the 2015 Florida survey to those of the 2014

Florida survey—the latter of which had a lower-than-typical response rate in Miami-Dade and Broward counties.

2

Table of Contents

I. EXECUTIVE SUMMARY AND OVERVIEW ........................................................................ 3

II. FLORIDA’S INTERNATIONAL SALES, 12 MONTHS ENDED JUNE 2015 ................................. 4

III. TRENDS IN REALTOR® TRANSACTIONS WITH INTERNATIONAL CLIENTS ................... 8

Share of REALTORS® who worked with an international client ............................................................... 8

Number of International Clients ............................................................................................................... 8

Number of Clients Who Purchased Property ............................................................................................ 9

Source of Client Contact ......................................................................................................................... 10

Most Important Factor Affecting Decision to Purchase ......................................................................... 11

Client’s Perception of Florida Property Prices and Exchange Rate Changes .......................................... 11

Reasons for Not Purchasing Property ..................................................................................................... 13

Change in the Percentage of International Clients ................................................................................. 13

Retirees as a Potential Market ................................................................................................................ 14

Number of Years as a REALTOR® ........................................................................................................... 15

Extent of Language or Cultural Problems ............................................................................................... 16

IV. INTERNATIONAL BUYERS: ORIGINS AND PREFERENCES ............................................ 17

Origin of Foreign Buyers ......................................................................................................................... 17

Destination of Foreign Buyers ................................................................................................................. 19

Top Buyers by Metro Area ...................................................................................................................... 22

Prices and Financing................................................................................................................................ 24

Intended Use of Property ....................................................................................................................... 26

Location Preference ................................................................................................................................ 27

Type of Property ..................................................................................................................................... 28

New and Existing Home Sales ................................................................................................................. 30

Intended Months’ Use of Property ......................................................................................................... 30

V. CONCLUDING COMMENTS ........................................................................................... 31

VI. APPENDICES .................................................................................................................................... 33

Appendix 1: Computation of Market Share ........................................................................................... 33

Appendix 2: Some Comments Received From 2015 Florida Survey ...................................................... 34

3

I. EXECUTIVE SUMMARY AND OVERVIEW

Florida is one of the major U.S. destinations of international residential real estate

buyers. Approximately 25 percent of foreign home buyers purchasing U.S. property buy Florida

properties.3 The 2015 survey shows that foreign sales remain an important segment of Florida’s

residential market:

International unit sales totaled 44,000 properties, 12 percent of Florida’s residential market

(15 percent a year ago), compared to four percent nationally.

The dollar volume of international sales totaled $23.7 billion, 24 percent of Florida’s

residential dollar volume of sales (19 percent a year ago), compared to eight percent

nationally.

69 percent of Florida REALTORS® have international clients (52 percent a year ago),

compared to the national average of 35 percent.

31 percent of Florida REALTORS® reported having more than five clients (19 percent a year

ago), compared to the national average of 15 percent

Among respondents who worked with a client, 78 percent reported having closed at least

one sale (75 percent a year ago), compared to the national average of 56 percent for those

working with an international client.

Respondents reported a significant increase in the share of buyers from Latin America to 56

percent (23 percent a year ago).

Approximately 50 percent of foreign buyers purchased in Miami-Miami Beach (36 percent)

and Fort Lauderdale (14 percent).

Foreigners purchased property at the average price of $538,600 ($300,600 in 2014),

compared to the median price of Florida’s residential sales of $258,200. The substantial

change in average price appears to be due to market mix.

Approximately 63 percent reported that their clients found Florida properties less expensive

than comparable properties in their home country (76 percent a year ago).

Approximately 29 percent reported that an increase in the percentage of business that is

international in the past year (45 percent a year ago), compared to the national average of

13 percent.

Florida’s real estate market continues to attract new REALTORS®: 16 percent of Florida

respondents reported that they have been in business for less than one year (12 percent a

year ago), compared to 10 percent at the national level.

3 Data are from NAR’s Profile of International Home Buyers surveys, 2009 through 2015. The percentages fluctuate

year to year. In the 2015 survey, Florida accounted for 21 percent of all foreign buyers purchasing in the U.S.

4

II. FLORIDA’S INTERNATIONAL SALES, 12 MONTHS ENDED JUNE

2015

In the 12-month period ended June 2015, sales to foreign buyers accounted for 12

percent of Florida’s residential unit sales of single-family, townhome, and condominium

properties, a decrease from the 15 percent share in the same period last year.4 In terms of

dollar volume, sales to foreign buyers accounted for 24 percent of Florida’s residential dollar

volume of sales, an increase from the 19 percent share in the same period last year. For

comparison, all purchases of foreign buyers in the U.S. accounted for four percent of U.S. total

existing home sales, while the corresponding dollar volume of such sales accounted for eight

percent of the U.S. dollar volume of existing home sales.5

The market share of foreign buyers in Florida’s residential existing home markets

significantly increased in the wake of the housing downturn, accounting for about half of the

dollar volume of sales and about a fifth of Florida unit sales in 2009 -2011. With the recovery of

the U.S. economy and increased participation of domestic buyers, the share of foreign buyers

to Florida’s residential market has decreased. Still, the 24 percent share of purchases by foreign

buyers in Florida’s existing home sales market is substantial when compared to the national

figure of eight percent in the 2015.

4 12 months ended June 2014.

5 NAR’s Survey of International Homebuyers. NAR’s reference period in estimating the national level of

international sales is from April of the previous year to March of the current year. The Florida survey’s reference period is from July of the previous year to June of the current year.

12% 14% 19% 17%

27% 23%

17% 14% 15% 12%

19% 27%

38% 41%

57% 51%

43%

28%

19% 24%

0%

10%

20%

30%

40%

50%

60%

70%

2005 2007 2008 2009 2010 2011 2012 2013 2014 2015

Share of International Sales to Florida's Residential Market in Past 12 Months*

As percent of unit sales As percent of dollar sales

*Source: NAR. Past 12 months generally covers the period July of previous year to June of current year. No survey was held in 2006. The 2005-, 2007, 2008 surveys covered only non-resident foreign

5

Measured in numbers of purchases, foreigners purchased 44,000 properties in the 12-

month period ended June 2015, a decrease from the level of 52,300 units in the same period

last year. These transactions accounted for about 12 percent of Florida’s residential unit sales, a

decrease compared to the 15 percent share in the previous period.6 The decrease in Florida’s

residential unit sales to foreigners is in line with the decrease in international sales at the

national level and the lower share of Florida to the national level of international sales.

Nationally, international sales decreased to 209,000 in 2015 from 232,600 in 2014. Florida’s

share to total international sales decreased to 21 percent in 2015 from 23 percent in 2014.

Increases in home prices across the U.S. and in Florida, changes in foreign exchange

rates, and adverse economic conditions in some countries appear to have been the major

factors that dampened the demand for existing homes by foreign buyers. The average price of a

residential property in Florida rose to $258,200 in the past 12 months ended June 2015, a six

percent increase from $245,500 in the same period last year. The weakening of most currencies

against the U.S. dollar (e.g., the Canadian dollar, the Brazilian real, and the euro) further made

Florida prices more expensive in terms of the local currency. In this year’s survey, respondents

reported that the primary reason cited for not making a sale was “cost of property” (18 percent

in 2015, 11 percent in 2014); previously “could not find property” was the major reason. Also, a

higher share of respondents cited that the exchange rate movement had an impact on foreign

purchases (90 percent in 2015, 85 percent in 2014). In addition, a lower percentage of

respondents cited that Florida prices were less expensive compared to their home country (63

percent in 2015, 76 percent in 2014).

6 Based on closed sales and mean prices for single-family homes and condo/townhouses from July 2014-June 2015

reported by Florida REALTORS®, downloaded from http://media.floridarealtors.org.

39,800

24,500 30,600

36,200

66,100 65,300

53,600

44,300

52,300

44,000

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2005 2007 2008 2009 2010 2011 2012 2013 2014 2015

Number of International Sales in Florida in Past 12 Months*

*Source: NAR. Past 12 months generally covers the period July of previous year to June of current year. No survey was held in 2006. The 2005, 2007, 2008 surveys covered only non-resident foreign buyers.

6

Measured in dollar volume, sales to foreigners increased to $23.7 billion from the

previous 12-month period’s level of $15.7 billion. International sales accounted for about 24

percent of Florida’s residential market, compared to a 19 percent share in the preceding

period.7

The dollar volume of sales increased even as unit sales decreased as those international

clients who decided to purchase property did so for properties at the upper price range

compared to domestic buyers in Florida. Foreign buyers in Florida purchased properties at the

average price of $538,600 compared to $300,600 from the same period last year. The average

price of homes purchased by foreign buyers in Florida was higher compared to the price of

homes purchased by all foreign buyers in the U.S. ($499,600), to the price of residential homes

sold in Florida ($258,200), and to the price of U.S. existing home sales ($255,600).8 The median

price of properties purchased by foreign buyers in Florida also increased to $297,300 compared

to $209,600 in the same period last year.

7 See Appendix 1 for computations.

8 This is the average price for single-family, townhomes, and condominiums based on data reported by the Florida

Realtors® downloaded at http://www.floridarealtors.org/ResearchAndStatistics/Florida-Market-Reports/Index.cfm.

$14.5

$10.3 $11.2 $12.0

$17.1 $17.3 $17.4

$14.5 $15.7

$23.7

$-

$5

$10

$15

$20

$25

2005 2007 2008 2009 2010 2011 2012 2013 2014 2015

Dollar Volume of International Sales in Florida in Past 12 Months* In Billion Dollars

Source: NAR. Past 12 months generally covers the period July of previous year to June of current year. No survey was held in 2006. The 2005, 2007, 2008 surveys covered only non-resident foreign buyers.

7

$300,600

$396,000

$245,500 $249,500

$538,600 $499,600

$258,200 $255,600

Florida internationalclients

All internationalclients

Florida existinghome sales

U.S. existing homesales

Average(Mean) Home Prices of International and Domestic Clients in Florida and U.S. Market*

2014 2015

*Past 12 months in the Florida survey covers the period July 2014-June 2015. In the National survey, the period is from April 2015-March 2015.

$209,600

$268,000

$161,800

$201,800

$297,300 $265,100

$174,600

$208,900

Florida internationalclients

All internationalclients

Florida existinghome sales

U.S. existing homesales

Median Home Prices of International and Domestic Clients in Florida and U.S. Market*

2014 2015

*Past 12 months in the Florida survey covers the period July 2014-June 2015. In the National survey, the period is from April 2015-March 2015.

8

III. TRENDS IN REALTOR® TRANSACTIONS WITH INTERNATIONAL CLIENTS

Share of REALTORS® who worked with an international client International transactions account for a larger share of transactions in Florida

compared to international transactions at the national level. About 69 percent of Florida

REALTORS® worked with an international client for the 12 months ended June 2015.

Nationally, only 35 percent of REALTORS® had an international client. Last year, 52 percent of

Florida respondents reported working with an international client.

Number of International Clients

Among respondents who reported dealing with an international client, approximately

69 percent reported one to five clients (whether purchased or not), compared to 85 percent

nationally. Last year, 81 percent reported one to five clients.

53% 54% 61%

77%

61% 63% 52%

69%

26% 23% 28% 28% 27% 27% 28%

35%

0%10%20%30%40%50%60%70%80%90%

2008 2009 2010 2011 2012 2013 2014 2015

Share of Florida REALTOR® Respondents Who Had an International Client in the Past Twelve Months*

Florida National

*Past 12 months in the Florida survey generally covers the period July of previous year to June of current year. In the National survey, the period is from April of previous year to March of current year.

9

Number of Clients Who Purchased Property

Among respondents who reported working with an international client, 78 percent reported that they had at least one client who purchased a property, compared 56 percent nationally.

82% 79% 76% 72% 75% 76% 81% 69%

10% 11% 14% 17% 15% 13% 12%

17%

8% 10% 9% 11% 10% 11% 7% 13%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Number of International Clients Among FLORIDA REALTOR® Respondents With International Clients

(Percentage distribution)

1 to 5 6 to 10 more than 10

38% 33% 26% 22% 23% 19% 25% 22%

28% 26%

25% 22% 24% 26%

28% 28%

15% 18%

16% 17% 18% 21%

17% 18%

7% 8%

9% 12% 11% 11%

11% 8%

3% 5%

6% 7% 6% 7% 6%

6%

3% 4% 6% 6% 6% 6% 5%

6%

4% 4% 8% 9% 8% 6% 6%

6%

2% 3% 4% 5% 3% 5% 3% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Number of International Clients Who Purchased Property from Florida REALTOR® Respondents With International Clients

(Percentage Distribution)

0 1 2 3 4 5 6 to 10 more than 10

10

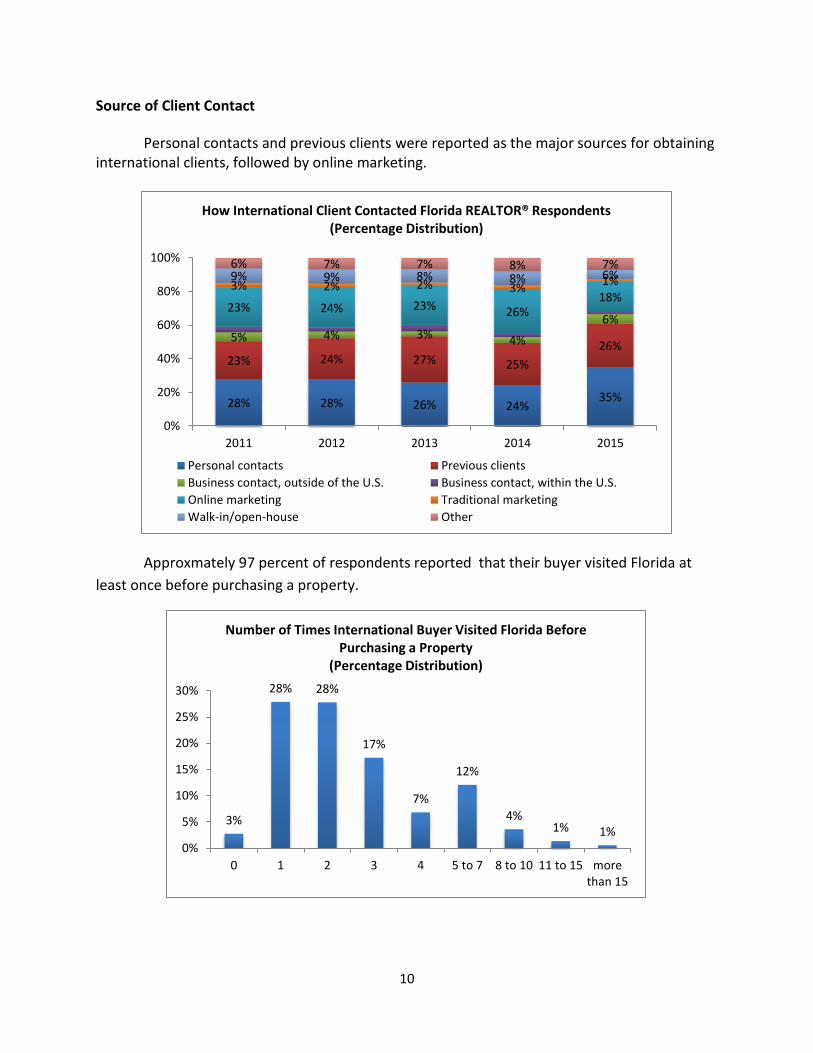

Source of Client Contact

Personal contacts and previous clients were reported as the major sources for obtaining international clients, followed by online marketing.

Approxmately 97 percent of respondents reported that their buyer visited Florida at

least once before purchasing a property.

28% 28% 26% 24% 35%

23% 24% 27% 25%

26% 5% 4% 3% 4%

6% 23% 24% 23% 26%

18% 3% 2% 2% 3%

1% 9% 9% 8% 8% 6% 6% 7% 7% 8% 7%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

How International Client Contacted Florida REALTOR® Respondents (Percentage Distribution)

Personal contacts Previous clients

Business contact, outside of the U.S. Business contact, within the U.S.

Online marketing Traditional marketing

Walk-in/open-house Other

3%

28% 28%

17%

7%

12%

4% 1% 1%

0%

5%

10%

15%

20%

25%

30%

0 1 2 3 4 5 to 7 8 to 10 11 to 15 morethan 15

Number of Times International Buyer Visited Florida Before Purchasing a Property

(Percentage Distribution)

11

Most Important Factor Affecting Decision to Purchase

The most important factor influencing a client’s decision to purchase Florida property

appears to be primarily tied to the security and profitability of investing in Florida property,

cited by 51 percent of respondents. This is consistent with the findings of this and past surveys

that show majority of buyers are purchasing property for rental purposes. About 41 percent of

Florida REALTORS® respondents reported Florida’s desirable location as the most important

factor, also consistent with the finding that majority of foreign buyers purchase property for

vacation use.

Client’s Perception of Florida Property Prices and Exchange Rate Changes

International clients also purchase property in Florida because of their perception about

the value they get for their money. About 63 percent of Florida REALTORS® responding to the

survey reported that their clients found Florida properties less expensive than comparable

properties in their home country. However, this is a decline from the previous years’ shares of

about 76 to 81 percent. The average price of a residential property in Florida rose to $258,200

in the past 12 months ended June 2015, a six percent increase from $245,500 in the same

period last year.

Secure investment

30%

Profitable investment

21%

Desirable location

41%

Other/don't know

8%

Most Important Factor Influencing Client's Decision to Purchase Real Estate in Florida

(Percentage Distribution)

12

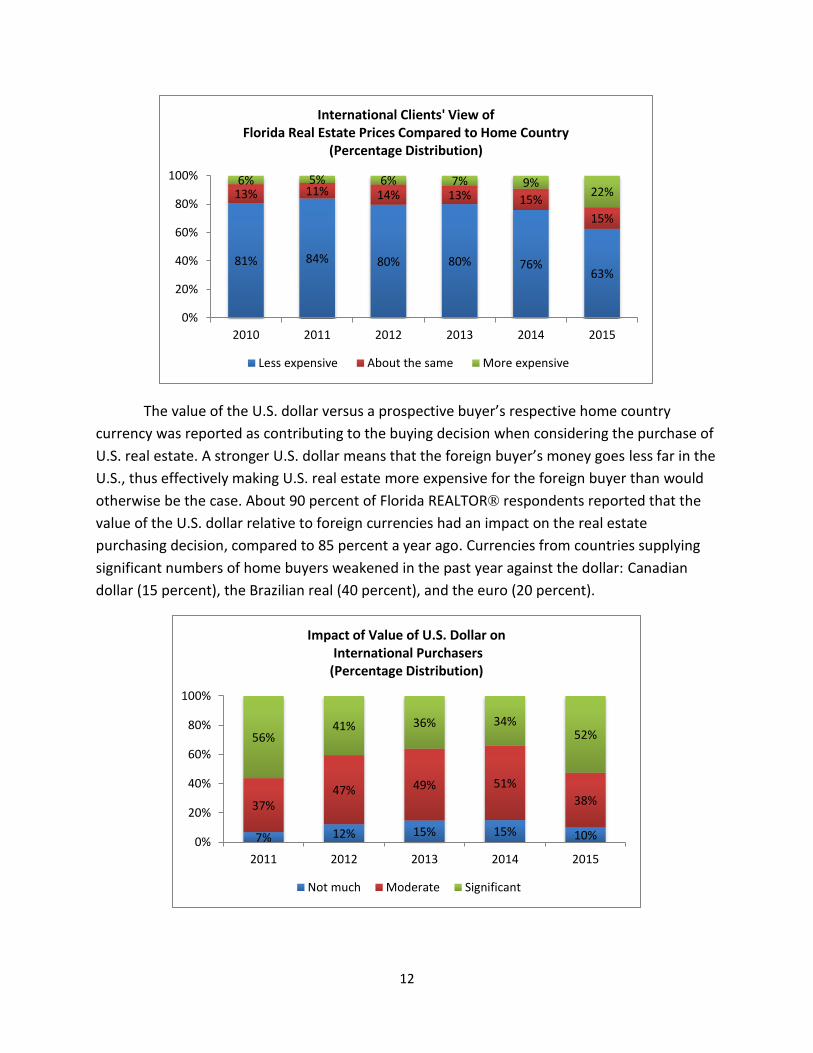

The value of the U.S. dollar versus a prospective buyer’s respective home country

currency was reported as contributing to the buying decision when considering the purchase of

U.S. real estate. A stronger U.S. dollar means that the foreign buyer’s money goes less far in the

U.S., thus effectively making U.S. real estate more expensive for the foreign buyer than would

otherwise be the case. About 90 percent of Florida REALTOR® respondents reported that the

value of the U.S. dollar relative to foreign currencies had an impact on the real estate

purchasing decision, compared to 85 percent a year ago. Currencies from countries supplying

significant numbers of home buyers weakened in the past year against the dollar: Canadian

dollar (15 percent), the Brazilian real (40 percent), and the euro (20 percent).

81% 84% 80% 80% 76% 63%

13% 11% 14% 13% 15%

15%

6% 5% 6% 7% 9% 22%

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015

International Clients' View of Florida Real Estate Prices Compared to Home Country

(Percentage Distribution)

Less expensive About the same More expensive

7% 12% 15% 15% 10%

37% 47% 49% 51%

38%

56% 41% 36% 34%

52%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

Impact of Value of U.S. Dollar on International Purchasers (Percentage Distribution)

Not much Moderate Significant

13

Reasons for Not Purchasing Property

Not every transaction resulted in a sale. Approximately 43 percent of respondents with

an international client had at least one client who decided not to purchase. There were a

variety of reasons that explain why a client did not purchase a property. ”Cost of property” was

cited as the major reason in 2015, mentioned by 18 percent of Florida REALTORS®

respondents, up from 11 percent a year ago. Rising property prices and the weakening of most

currencies against the dollar might have accounted for this increase. In addition, foreigners are

reported to be frequently surprised by the levels of condo fees, property taxes, and insurance

costs. There are differences in real estate markets between countries, and foreigners frequently

need additional information on U.S. practices compared to their country of origin. “Could not

find property” was another reason, mentioned by ten percent of respondents. REALTORS® may

need to work more closely with foreign buyers who are looking for properties that meet their

financial requirements, individual preferences, and cultural lifestyle.

Change in the Percentage of International Clients

Approximately 29 percent of respondents reported an increase in the percentage of

clients in the past year, a decrease from the 45 percent share who reported an increase in

2014. The majority of respondents reported no change. Approximately one in five did not

provide an opinion because they had been in business for less than one year.

11% 11%

20%

11%

5% 7%

8%

3%

18%

11% 11% 10%

7% 7% 5% 4%

1%

6%

Reasons For Not Purchasing Property in Past 12 Months (Percentage Distribution)

2014 2015

* Not included as a response option in 2014 survey.

14

Over a five-year period, 37 percent of respondents reported an increase in the share of

international clients to their business, compared to 29 percent in 2014. About a third of

respondents had no opinion because they have been in business for less than five years.

Retirees as a Potential Market

Approximately half of respondents have reported in the surveys that have been

conducted that foreign retirees are a potential pool of buyers in their market.

45% 32% 31%

45% 29%

38% 48% 49%

38%

40%

8% 8% 7% 8% 14%

9% 12% 13% 9% 18%

0%

50%

100%

2011 2012 2013 2014 2015

How Has the Percentage Of Clients Who Are International Changed in the Past Year? (Percentage Distribution)

Not applicable, less than 1 yr in businessDecreasedStayed about the sameIncreased

27% 27% 31% 46% 38% 39%

29% 37%

36% 38% 33%

29% 35% 35%

40% 21%

11% 14% 17% 9% 8% 5% 8%

9%

26% 22% 19% 16% 20% 21% 23% 32%

0%

50%

100%

2008 2009 2010 2011 2012 2013 2014 2015

How Has the Percentage Of Clients Who Are International Changed in the Past 5 Years?

(Percentage Distribution)

Not applicable, less than 5 yrs in businessDecreasedStayed about the sameIncreased

15

Number of Years as a REALTOR®

The share of REALTORS ® who have less than one year of experience continued to

increase in 2015, as reported in the surveys conducted in recent years, rising from six percent in

2008 to 16 percent in 2015. The rising share is an indicator of the growth potential for growth

of the Florida’s market. An examination of reasons for why foreigners have not purchased

property may be of interest to individuals building their practice. “Could not find property” and

“cost of property” were major reasons why foreign clients did not purchase properties,

indicating that REALTORS® will need to work more closely with clients to meet their financial

requirements, individual needs, and cultural preferences.

46% 49% 52% 54% 47% 52% 47%

22% 23% 21% 25% 23% 22% 23%

32% 28% 27% 21% 30% 27% 30%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014

Are Foreign Retirees A Potential Pool of Buyers In Your Market?

(Percentage Distribution)

Yes No Don’t know

6% 8% 8% 10% 12% 11% 12% 16%

42% 32% 26% 22% 19% 19% 19%

31%

18% 21% 28% 28% 28% 25% 17%

18%

9% 10% 12% 13% 13% 16%

19%

16% 8%

8% 9% 8% 8% 10% 9%

5% 17% 21% 19% 20% 20% 19% 25%

13%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Years as a REALTOR® Among Florida REALTOR® Respondents (Percentage Distribution)

Less than 1 1 to 5 6 to 10 11 to 15 16 to 20 more than 20

16

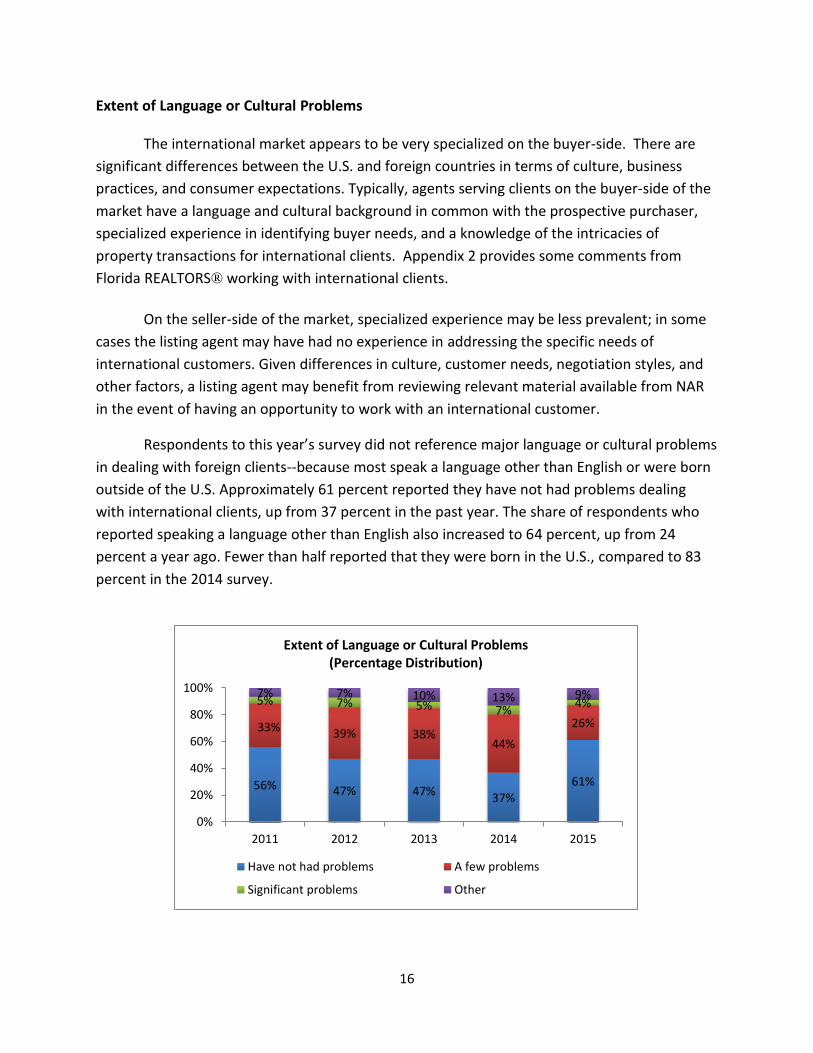

Extent of Language or Cultural Problems

The international market appears to be very specialized on the buyer-side. There are

significant differences between the U.S. and foreign countries in terms of culture, business

practices, and consumer expectations. Typically, agents serving clients on the buyer-side of the

market have a language and cultural background in common with the prospective purchaser,

specialized experience in identifying buyer needs, and a knowledge of the intricacies of

property transactions for international clients. Appendix 2 provides some comments from

Florida REALTORS® working with international clients.

On the seller-side of the market, specialized experience may be less prevalent; in some

cases the listing agent may have had no experience in addressing the specific needs of

international customers. Given differences in culture, customer needs, negotiation styles, and

other factors, a listing agent may benefit from reviewing relevant material available from NAR

in the event of having an opportunity to work with an international customer.

Respondents to this year’s survey did not reference major language or cultural problems

in dealing with foreign clients--because most speak a language other than English or were born

outside of the U.S. Approximately 61 percent reported they have not had problems dealing

with international clients, up from 37 percent in the past year. The share of respondents who

reported speaking a language other than English also increased to 64 percent, up from 24

percent a year ago. Fewer than half reported that they were born in the U.S., compared to 83

percent in the 2014 survey.

56% 47% 47% 37%

61%

33% 39% 38% 44%

26%

5% 7% 5% 7% 4%

7% 7% 10% 13% 9%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

Extent of Language or Cultural Problems (Percentage Distribution)

Have not had problems A few problems

Significant problems Other

17

IV. INTERNATIONAL BUYERS: ORIGINS AND PREFERENCES

Origin of Foreign Buyers

Foreign home buyers in Florida come from a wide variety of countries. In the 12 months

ended June 2015, Florida REALTORS® respondents reported a significant increase in the share

of purchases from Latin America and a decrease from Canada and Europe. The majority of

buyers from Latin America came from Venezuela (18 percent in 2015, 3 percent in 2014), Brazil

(9 percent in 2015, 6 percent in 2014), Colombia (7 percent in 2015, 4 percent in 2014), and

Argentina (7 percent in 2015, 3 percent in 2014). The share of buyers from Canada and Europe

30% 33% 33%

41% 39% 33%

24%

64%

0%

10%

20%

30%

40%

50%

60%

70%

2008 2009 2010 2011 2012 2013 2014 2015

Percent of Florida REALTOR® Respondents Who are Fluent in a Language Other than English

63% 69% 73% 83%

48%

10% 10% 8% 6%

14%

27% 21% 19% 11% 38%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 2015

Where You Born in the U.S.? (Percentage Distribution)

No, but came to the U.S. at least 18 years old

No, but came to the U.S. before 18 years old

Yes

18

decreased, particularly from Canada (11 percent in 2015, 32 percent in 2014). The share of

purchases from the United Kingdom has declined significantly from a share of 21 percent in

2008 to five percent in 2015. Meanwhile, the share of purchases from China has been generally

trending up from an insignificant level in 2008 to four percent in 2015.

By region of origin, Latin America/Caribbean accounted for 56 percent of international

buyers, a jump from 23 percent in 2014. Buyers from Europe accounted for 19 percent. Buyers

from Canada declined from about a third to about a tenth.

3% 5% 6% 4% 6% 8% 11% 8%

27% 26% 35% 38% 31% 30%

32%

11%

50% 42% 37%

28% 24% 27%

29%

19%

17% 25% 17% 28% 36% 32% 23%

56%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Region of Origin

Asia/Oceania AfricaCanada EuropeLatin America/Caribbean Middle EastUnknown

19

Destination of Foreign Buyers

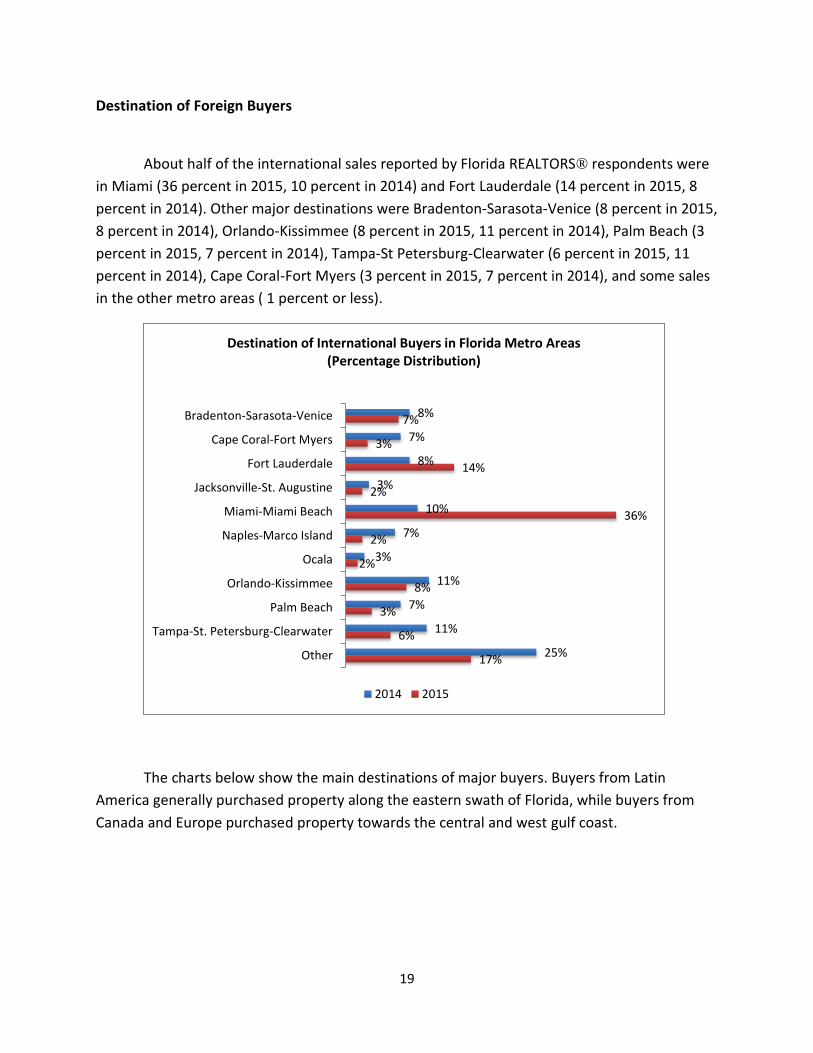

About half of the international sales reported by Florida REALTORS® respondents were

in Miami (36 percent in 2015, 10 percent in 2014) and Fort Lauderdale (14 percent in 2015, 8

percent in 2014). Other major destinations were Bradenton-Sarasota-Venice (8 percent in 2015,

8 percent in 2014), Orlando-Kissimmee (8 percent in 2015, 11 percent in 2014), Palm Beach (3

percent in 2015, 7 percent in 2014), Tampa-St Petersburg-Clearwater (6 percent in 2015, 11

percent in 2014), Cape Coral-Fort Myers (3 percent in 2015, 7 percent in 2014), and some sales

in the other metro areas ( 1 percent or less).

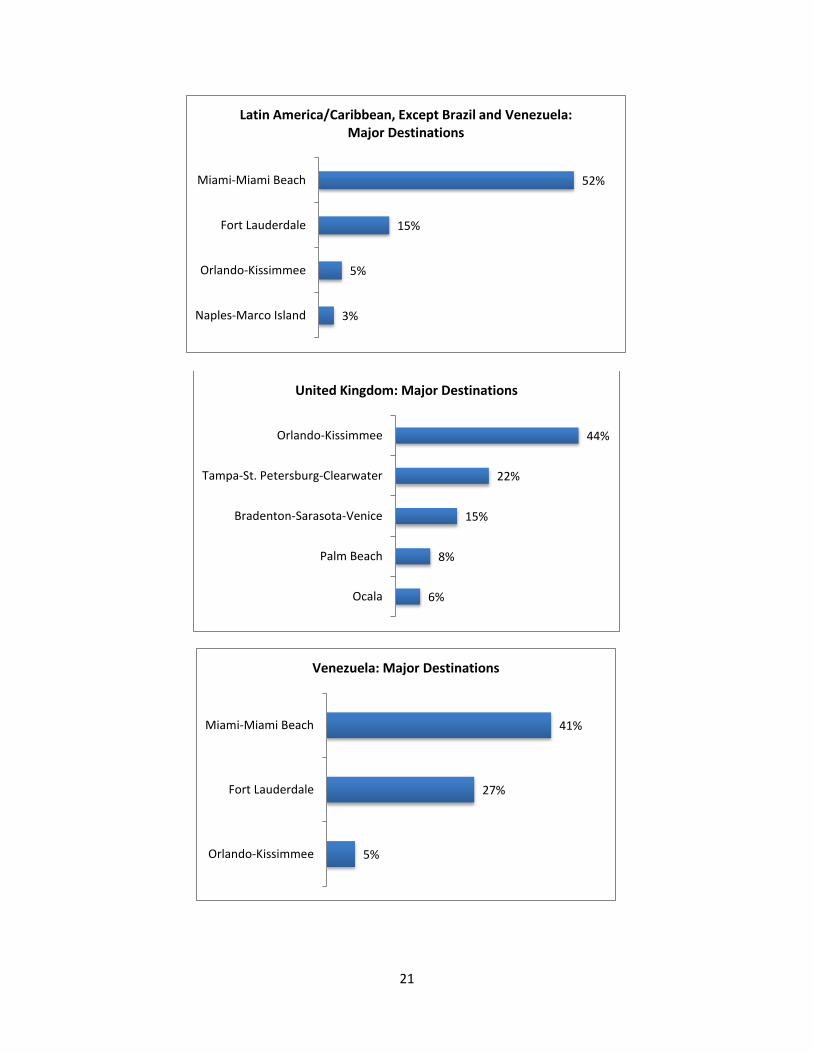

The charts below show the main destinations of major buyers. Buyers from Latin

America generally purchased property along the eastern swath of Florida, while buyers from

Canada and Europe purchased property towards the central and west gulf coast.

8%

7%

8%

3%

10%

7%

3%

11%

7%

11%

25%

7%

3%

14%

2%

36%

2%

2%

8%

3%

6%

17%

Bradenton-Sarasota-Venice

Cape Coral-Fort Myers

Fort Lauderdale

Jacksonville-St. Augustine

Miami-Miami Beach

Naples-Marco Island

Ocala

Orlando-Kissimmee

Palm Beach

Tampa-St. Petersburg-Clearwater

Other

Destination of International Buyers in Florida Metro Areas (Percentage Distribution)

2014 2015

20

44%

18%

16%

Miami-Miami Beach

Fort Lauderdale

Orlando-Kissimmee

Brazil: Major Destinations

29%

19%

17%

9%

9%

6%

4%

Bradenton-Sarasota-Venice

Palm Beach

Tampa-St. Petersburg-Clearwater

Fort Lauderdale

Cape Coral-Fort Myers

Naples-Marco Island

Miami-Miami Beach

Canada: Major Destinations

42%

27%

9%

6%

5%

3%

3%

Miami-Miami Beach

Bradenton-Sarasota-Venice

Orlando-Kissimmee

Tallahassee

Gainesville

Fort Lauderdale

Ocala

China: Major Destinations

21

52%

15%

5%

3%

Miami-Miami Beach

Fort Lauderdale

Orlando-Kissimmee

Naples-Marco Island

Latin America/Caribbean, Except Brazil and Venezuela: Major Destinations

44%

22%

15%

8%

6%

Orlando-Kissimmee

Tampa-St. Petersburg-Clearwater

Bradenton-Sarasota-Venice

Palm Beach

Ocala

United Kingdom: Major Destinations

41%

27%

5%

Miami-Miami Beach

Fort Lauderdale

Orlando-Kissimmee

Venezuela: Major Destinations

22

Top Buyers by Metro Area

Miami-Miami Beach, Fort Lauderdale, Orlando-Kissimmee, Palm Beach, and Tampa-St.

Petersburg-Clearwater were the major destinations of foreign buyers. The next charts show the

top countries of origin for these areas.

27%

13%

12%

10%

7%

6%

4%

3%

Miami-Miami Beach

Cape Coral-Fort Myers

Fort Lauderdale

Tampa-St. Petersburg-Clearwater

Bradenton-Sarasota-Venice

Orlando-Kissimmee

Naples-Marco Island

Palm Beach

Western Europe, Except United Kingdom: Major Destinations

46%

14%

11%

3%

3%

Canada

China

United Kingdom

Italy

Czech Republic

Bradenton-Sarasota-Venice: Top Foreign Buyers in Past 12 Months Ended June 2015

23

34%

12%

7%

6%

5%

5%

4%

4%

3%

Venezuela

Brazil

Canada

Colombia

Argentina

Mexico

France

Cuba

Ecuador

Fort Lauderdale: Top Foreign Buyers in Past 12 Months Ended June 2015

21%

13%

12%

8%

4%

4%

3%

Venezuela

Argentina

Brazil

Colombia

Mexico

China

France

Miami: Top Foreign Buyers in Past 12 Months Ended June 2015

28%

19%

12%

7%

5%

4%

4%

4%

4%

3%

United Kingdom

Brazil

Venezuela

Peru

Colombia

China

Ecuador

Germany

Sweden

Canada

Orlando-Kissimmee: Top Foreign Buyers in Past 12 Months Ended June 2015

24

Prices and Financing

Foreign buyers typically purchased properties that were more expensive than those

purchased by the typical Florida domestic buyer. The average price of a property purchased by

the foreign buyer was $538,600, compared to the average price of $258,200 in Florida’s

residential market.9

9 NAR computed the median price for single-family, townhouse, and condominium properties based on Florida

REALTORS® market data, downloaded from http://www.floridarealtors.org/ResearchAndStatistics/Florida-Market-Reports/Index.cfm

62%

12%

8%

6%

Canada

United Kingdom

Colombia

Germany

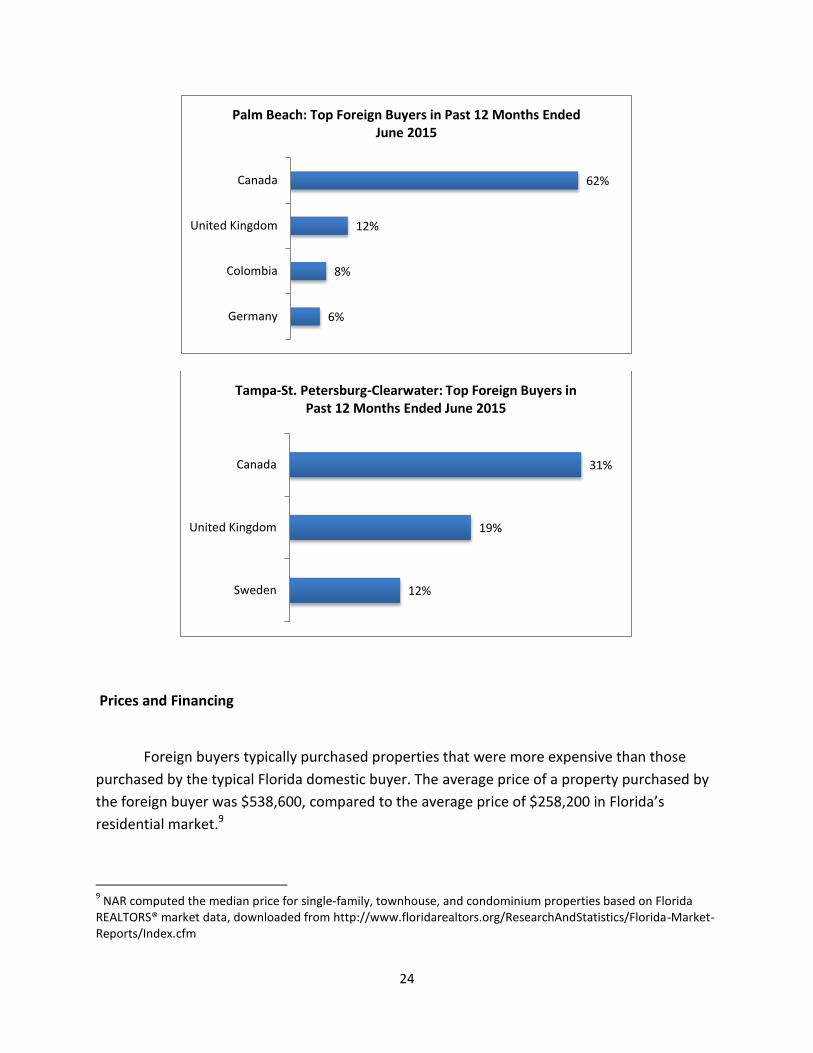

Palm Beach: Top Foreign Buyers in Past 12 Months Ended June 2015

31%

19%

12%

Canada

United Kingdom

Sweden

Tampa-St. Petersburg-Clearwater: Top Foreign Buyers in Past 12 Months Ended June 2015

25

Buyers from Western Europe except the United Kingdom and from China purchased the

more expensive properties, while buyers from the United Kingdom and Canada purchased less

expensive properties. This is related to the survey’s findings that majority of these buyers

purchased properties in Miami-Miami Beach area where home prices are higher.

About 74 percent of Florida REALTORS® respondents reported all cash sales to foreign

buyers. Among recent foreign buyers in Florida, the use of mortgage financing was much less

frequent at 20 percent compared with the overall national share of 70 percent of

transactions.10 This disparity in the use of mortgages appears to have been due to differences in

credit reporting between the U.S. and foreign countries, and difficulties in confirming credit

worthiness internationally. Foreign buyers typically don’t have credit ratings that are computed

on scales similar to U.S. practices, don’t have Social Security numbers, and have credit and asset

10

Based on data from NAR’s REALTORS® Confidence Index surveys from April 2014-March 2015.

$264,400 $323,800 $326,500 $300,600

$538,600

$190,000 $198,800 $224,100 $245,500 $258,200

2011 2012 2013 2014 2015

Average (Mean) Home Prices of International and Domestic Clients in Florida and U.S. Market

Florida - foreign buyer Florida - residential market

Average Price of Property Purchased in Florida by Foreign Buyer, 12 months ended June 2015

Average (Mean) Price

Brazil $587,700

Canada $376,800

China $1,064,800

Latin America/Caribbean Except Brazil & Venezuela $593,600

United Kingdom $289,600

Venezuela $390,400

Western Europe Except United Kingdom $844,500

All foreign buyers $538,600

26

profiles significantly different from those typically experienced in standard U.S. credit profiles.

This makes obtaining a mortgage difficult for the foreign buyer.

Buyers from Canada were more likely to pay cash for the property.

Intended Use of Property

Approximately 66 percent of Florida’s foreign buyers purchased property for use as

vacation, residential rental, or both.

82% 84% 82% 74%

14% 13% 14% 21%

0%

50%

100%

2012 2013 2014 2015

Financing of International Buyers Purchasing Property in Florida

(Percentage Distribution)

Don’t know Investors/OtherMortgage financing - buyer's home countryMortgage financing - U.S. sourcesAll cash

Cash sales, as Percent of Purchases Made by Foreign Buyer in Florida, 12 months ended June 2015

Percent of buyers

Brazil 65%

Canada 92%

China 79%

Latin America/Caribbean Except Brazil & Venezuela 69%

United Kingdom 82%

Venezuela 82%

Western Europe Except United Kingdom 80%

All foreign buyers 74%

27

Buyers from the United Kingdom were the most likely to purchase the property for

vacation, residential rental, or both. Buyers from China tended to use the property for primary

residence and student housing.

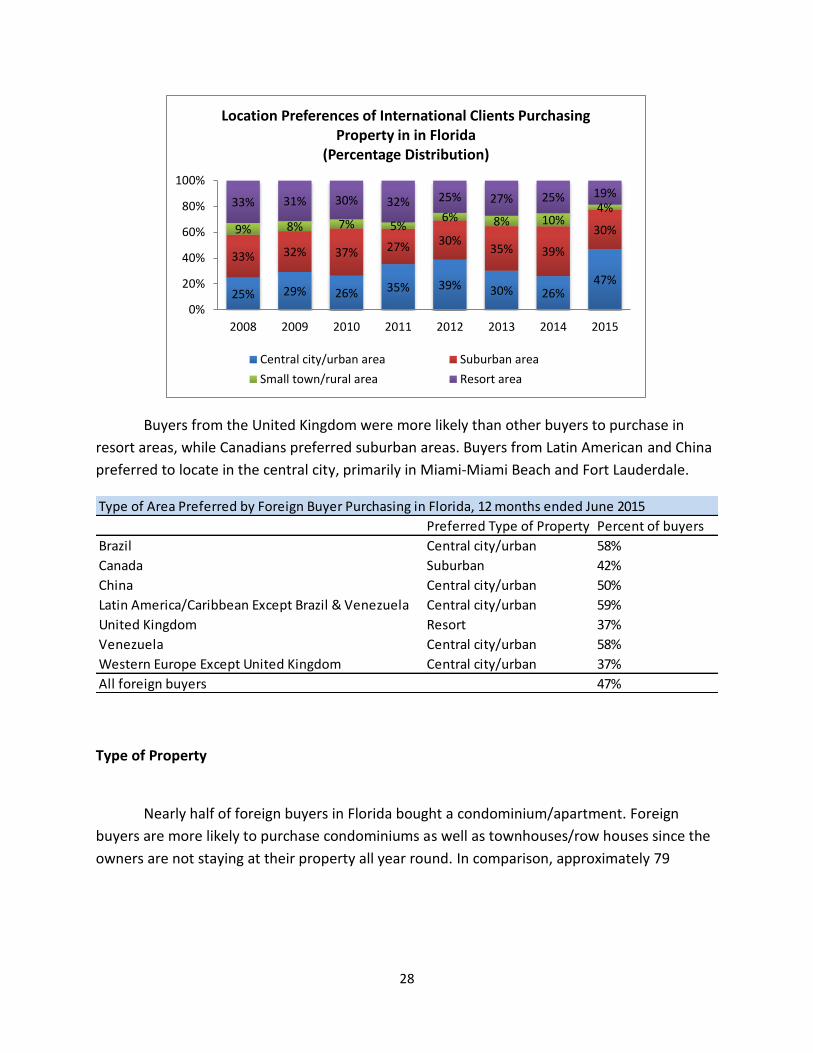

Location Preference

Florida REALTOR® respondents reported that 47 percent of foreign buyers purchased

property in the central city/urban area. This is in line with the finding that the share of buyers

from Latin America increased, and that these buyers tend to purchase condominium properties

for vacation and residential rental use.

27% 24% 20%

16%

4% 4% 5%

15% 20%

46%

11%

3% 2% 3%

0%5%

10%15%20%25%30%35%40%45%50%

Intended Use Property Purchased By International Clients (Percentage Distribution)

Florida National

Use of Property for Vacation, Rental, or Both by Foreign Buyer, 12 months ended June 2015

Percent of buyers

Brazil 63%

Canada 73%

China 57%

Latin America/Caribbean Except Brazil & Venezuela 69%

United Kingdom 81%

Venezuela 72%

Western Europe Except United Kingdom 72%

All foreign buyers 66%

28

Buyers from the United Kingdom were more likely than other buyers to purchase in

resort areas, while Canadians preferred suburban areas. Buyers from Latin American and China

preferred to locate in the central city, primarily in Miami-Miami Beach and Fort Lauderdale.

Type of Property

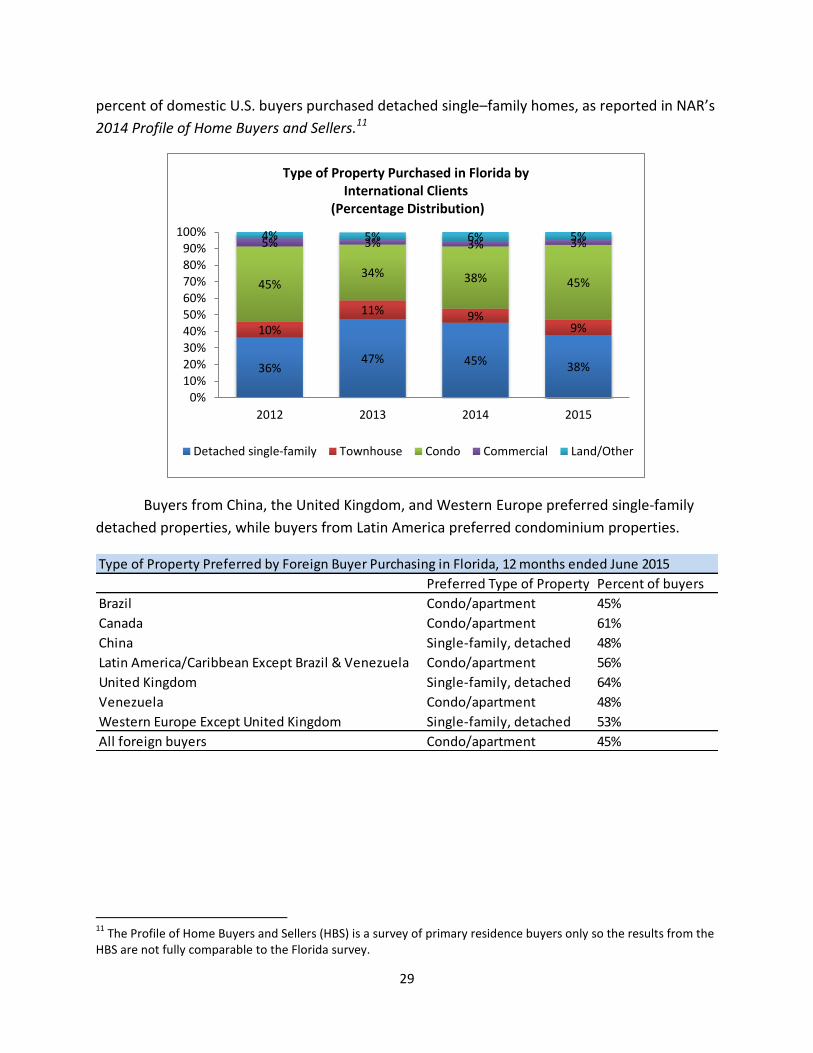

Nearly half of foreign buyers in Florida bought a condominium/apartment. Foreign

buyers are more likely to purchase condominiums as well as townhouses/row houses since the

owners are not staying at their property all year round. In comparison, approximately 79

25% 29% 26% 35% 39% 30% 26% 47%

33% 32% 37% 27% 30% 35% 39%

30% 9% 8% 7% 5% 6% 8% 10%

4% 33% 31% 30% 32% 25% 27% 25% 19%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Location Preferences of International Clients Purchasing Property in in Florida

(Percentage Distribution)

Central city/urban area Suburban area

Small town/rural area Resort area

Type of Area Preferred by Foreign Buyer Purchasing in Florida, 12 months ended June 2015

Preferred Type of Property Percent of buyers

Brazil Central city/urban 58%

Canada Suburban 42%

China Central city/urban 50%

Latin America/Caribbean Except Brazil & Venezuela Central city/urban 59%

United Kingdom Resort 37%

Venezuela Central city/urban 58%

Western Europe Except United Kingdom Central city/urban 37%

All foreign buyers 47%

29

percent of domestic U.S. buyers purchased detached single–family homes, as reported in NAR’s

2014 Profile of Home Buyers and Sellers.11

Buyers from China, the United Kingdom, and Western Europe preferred single-family

detached properties, while buyers from Latin America preferred condominium properties.

11

The Profile of Home Buyers and Sellers (HBS) is a survey of primary residence buyers only so the results from the HBS are not fully comparable to the Florida survey.

36% 47% 45% 38%

10%

11% 9% 9%

45% 34% 38% 45%

5% 3% 3% 3% 4% 5% 6% 5%

0%10%

20%30%

40%

50%

60%

70%

80%

90%100%

2012 2013 2014 2015

Type of Property Purchased in Florida by International Clients

(Percentage Distribution)

Detached single-family Townhouse Condo Commercial Land/Other

Type of Property Preferred by Foreign Buyer Purchasing in Florida, 12 months ended June 2015

Preferred Type of Property Percent of buyers

Brazil Condo/apartment 45%

Canada Condo/apartment 61%

China Single-family, detached 48%

Latin America/Caribbean Except Brazil & Venezuela Condo/apartment 56%

United Kingdom Single-family, detached 64%

Venezuela Condo/apartment 48%

Western Europe Except United Kingdom Single-family, detached 53%

All foreign buyers Condo/apartment 45%

30

New and Existing Home Sales

About 81 percent of foreign buyers who purchased a home in Florida bought an existing

home, lower than the share reported last year. The national share is 84 percent reported in

NAR’s 2014 Profile of Home Buyers and Sellers.

Buyers from Canada were the most likely to buy existing homes than any other group,

while buyers from China were the most likely to buy new homes.

Intended Months’ Use of Property

The likelihood that properties may have a dual use is also reflected in the length of time

that buyers plan to personally use them, with shorter intended use among those who also plan

22% 14% 11% 11% 12% 11% 10% 19%

78% 86% 89% 89% 88% 89% 90% 81%

0%

20%

40%

60%

80%

100%

2008 2009 2010 2011 2012 2013 2014 2015

New vs. Previously Owned Units Purchased in Florida By International Clients

(Percentage Distribution)

New Previously owned

Share of New and Existing Home Sales by Foreign Buyer in Florida, 12 months ended June 2015

New Existing

Brazil 19% 81%

Canada 7% 93%

China 40% 60%

Latin America/Caribbean Except Brazil & Venezuela 20% 80%

United Kingdom 27% 73%

Venezuela 15% 85%

Western Europe Except United Kingdom 19% 81%

All foreign buyers 19% 81%

31

to rent their property to others. Historically, about half of buyers have intended to use their

property for at most six months.

Most buyers were likely to stay at most six months. The high share of “don’t know”

responses especially about buyers from China and Venezuela does not enable the researchers

to make strong conclusions about the intended length of stay of foreign buyers.

V. CONCLUDING COMMENTS

The international market for the sale of existing residential homes to non-resident

foreigners remains an important part of the total Florida real estate market, comprising

approximately 12 percent of sales transactions and 24 percent of dollar volume in Florida in the

15% 16% 16% 18% 16% 14%

21% 23% 17% 22%

15% 16%

34% 34% 32%

31% 32%

23%

15% 12% 15%

13% 18%

22%

16% 16% 20% 16% 20% 25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015

Months International Buyer Plans to Use Property (Percentage Distribution)

Less than 1 1 to 2 3 to 6 more than 6 Don’t know

Intended Months' Use of Property of Foreign Buyer Purchasing in Florida, 12 months ended June 2015

Up to six months Don't know

Brazil 64% 20%

Canada 74% 17%

China 27% 46%

Latin America/Caribbean Except Brazil & Venezuela 50% 24%

United Kingdom 83% 3%

Venezuela 40% 40%

Western Europe Except United Kingdom 66% 15%

All foreign buyers 53% 25%

Percent of buyers

32

12 month time period ending June 2015. Although the role of foreign buyers has declined

compared to the years in the wake of the Great Recession, foreign buyers continue to be a

significant source of business in Florida, especially when compared against the national

performance.

A wide diversity of purchasers is attracted to Florida for investment and vacation

purposes. Respondents did express concern about the “cost of property” in Florida. This is

expected to be a continuing concern given the steep increase of properties amid tight inventory

that has pushed up prices.

In general, Florida REALTORS® responding to the survey have seen their international

practices expand over the past five years, and the increasing entry of new agents indicate that

further growth could be expected in the future. The future growth of international sales to

foreigners will be strongly dependent on the economic outlook in the countries of origin as well

as the other factors that typically drive residential markets.

33

VI. APPENDICES

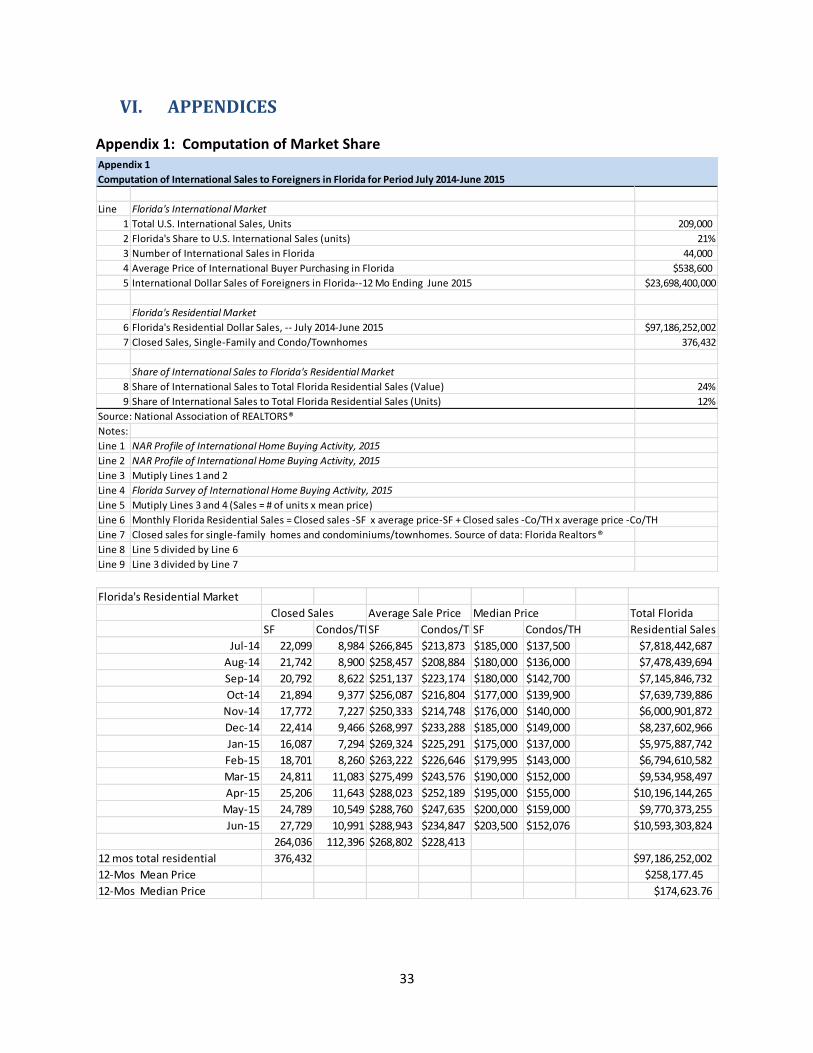

Appendix 1: Computation of Market Share

Appendix 1

Computation of International Sales to Foreigners in Florida for Period July 2014-June 2015

Line Florida's International Market

1 Total U.S. International Sales, Units 209,000

2 Florida's Share to U.S. International Sales (units) 21%

3 Number of International Sales in Florida 44,000

4 Average Price of International Buyer Purchasing in Florida $538,600

5 International Dollar Sales of Foreigners in Florida--12 Mo Ending June 2015 $23,698,400,000

Florida's Residential Market

6 Florida's Residential Dollar Sales, -- July 2014-June 2015 $97,186,252,002

7 Closed Sales, Single-Family and Condo/Townhomes 376,432

Share of International Sales to Florida's Residential Market

8 Share of International Sales to Total Florida Residential Sales (Value) 24%

9 Share of International Sales to Total Florida Residential Sales (Units) 12%

Source: National Association of REALTORS®

Notes:

Line 1 NAR Profile of International Home Buying Activity, 2015

Line 2 NAR Profile of International Home Buying Activity, 2015

Line 3 Mutiply Lines 1 and 2

Line 4 Florida Survey of International Home Buying Activity, 2015

Line 5 Mutiply Lines 3 and 4 (Sales = # of units x mean price)

Line 6 Monthly Florida Residential Sales = Closed sales -SF x average price-SF + Closed sales -Co/TH x average price -Co/TH

Line 7 Closed sales for single-family homes and condominiums/townhomes. Source of data: Florida Realtors®

Line 8 Line 5 divided by Line 6

Line 9 Line 3 divided by Line 7

Florida's Residential Market

Closed Sales Average Sale Price Median Price Total Florida

SF Condos/THSF Condos/THSF Condos/TH Residential Sales

Jul-14 22,099 8,984 $266,845 $213,873 $185,000 $137,500 $7,818,442,687

Aug-14 21,742 8,900 $258,457 $208,884 $180,000 $136,000 $7,478,439,694

Sep-14 20,792 8,622 $251,137 $223,174 $180,000 $142,700 $7,145,846,732

Oct-14 21,894 9,377 $256,087 $216,804 $177,000 $139,900 $7,639,739,886

Nov-14 17,772 7,227 $250,333 $214,748 $176,000 $140,000 $6,000,901,872

Dec-14 22,414 9,466 $268,997 $233,288 $185,000 $149,000 $8,237,602,966

Jan-15 16,087 7,294 $269,324 $225,291 $175,000 $137,000 $5,975,887,742

Feb-15 18,701 8,260 $263,222 $226,646 $179,995 $143,000 $6,794,610,582

Mar-15 24,811 11,083 $275,499 $243,576 $190,000 $152,000 $9,534,958,497

Apr-15 25,206 11,643 $288,023 $252,189 $195,000 $155,000 $10,196,144,265

May-15 24,789 10,549 $288,760 $247,635 $200,000 $159,000 $9,770,373,255

Jun-15 27,729 10,991 $288,943 $234,847 $203,500 $152,076 $10,593,303,824

264,036 112,396 $268,802 $228,413

12 mos total residential 376,432 $97,186,252,002

12-Mos Mean Price $258,177.45

12-Mos Median Price $174,623.76

34

Appendix 2: Some Comments Received From 2015 Florida Survey

Market Trends/Factors Influencing Purchase

o The dollar is strengthening and we will see a significant drop in foreign investment; rising prices will also deter investment.

o The strong dollar is affecting the purchase power of the international clients. o Exchange rates have stopped a couple of clients from overseas from purchasing. o A big decrease in Canadian interest in the past several months. o The rebound of the US market and home price has driven away the Canadian buyers who were

scooping up the deals a few years ago. They are still looking but there are not many bargains any more.

o The decline of the euro has had the most impact on the foreign buyer. o Brazil still our best market but new economic challenges is beginning to have effect on new

transactions. o Chinese market seems to be the biggest investor. o European clients are interested in the US market, also Middle Eastern clients. o Foreign market is hot. Two years ago it was Russia and Brazil. Now it is China. o I think that the next pool of people who is going to buy here in South Florida is going to be

Chinese (besides those from Latin America, Canadians and Russians). o I am finding that foreign clients are selling their properties and not rebuying. I have sold three

homes and going to list another four in next month. All My clients are from the UK. o It is a market geared to Spanish speaking Realtors®. o In my city of Dunedin, Canadian buyers abound due to our winter home of the Toronto Blue

Jays, but they concentrate on mobile homes and very inexpensive condos. o I've had several inquiries from German customers. o Many Australians are drawn to Florida for the investment prices, since it is much more

affordable here, but the dollar has an influence. o Most of my buyers and renters have been international. My Brickell tenants are 90% relocating

for professional reasons. Foreign buyers tend to have more cash available and less time to make decisions on purchasing a property.

o My dealings have been more with listings so I do have customers both buyers and sellers from Canada, UK, Argentina & China.

o The Venezuelan investors dominate the South Florida market. o The investors are taking advantage of the low interest rates. I am also a Property Manager. o Most international buyers are now purchasing pre-construction in my opinion. o There is lot of new homes and prices are high. o I like work with international buyer because they come to USA with cash to buy. o The buyer I had were a young professional buyer. I feel global trade, export, and manufacturing

business are going to be a great impact in our market. Young professional want a secure vacation home.

o Out of 200 leads that come in, three percent are international and that is what I have right now working.

o My career is about to become obsolete because I am a Miami Beach native and the international market is significantly pushing out my local clientele making my job very difficult. It is becoming impossible for my clients to purchase real estate in their hometown and they feel like they are being driven out do to the significant influx of internationals. This is just not feeling

35

like a home to them anymore and it has been very sad not only for my clients, but my real estate business that has been here for over 50 years. Yes, the city is booming but we need to have a more even mix of locals and internationals or we are going to have a major issue. We need subsidized housing for locals or this city is going to fall apart.

o Our property prices and lack of inventory are hurting our international market as well as lack of good financing for foreign buyers.

o My foreign buyers haven't bought yet, but are still looking. All three are multi-millionaires. o I'm an experienced businessman in dealing with internationals clients and believe that this

market will grow in desirability as Florida represents a location well known worldwide as a destination point which most international clients value as important in considering the security of a real estate investment beyond their home country.

Visa/Immigration/Business

o The two limiting factors are the lack of long-stay visa for retirees and the almost-impossibility for foreigners to get a mortgage.

o If we didn't have the rental restrictions on condo in Miami Beach, we could sell three times what we do to international buyers. They all want to buy to use the place and rent when they are not in town and this is not possible in Miami Beach!

o I would like to see an alliance with the Palm Beach International Airport to increase flight traffic to our area from regions around the world.

o We thought the new international airport in Panama City Beach would bring in more international buyers. The aircraft carriers are not there.

o Immigration attitude and taxes draw many potential investors away. Bank/Mortgage/Financing

o We need more local banks with programs for foreign national buyers. o We need to improve in offering foreign national loans. We need to have a more reliable source

of attorneys and accountants able to deal with international buyers. o International buyers are having trouble and or prohibited from pulling large amounts of cash out

of their home country. Last two Brazilian buyers failed to close. Homeowner Association Fees/Taxes/Procedures

o Some international buyers are not aware of our tax laws, therefore, as a Realtor®, we need to help educate these potential buyers.

o The inheritance taxes and taxes in general are scaring international customers. They are becoming savvy on taxes and they are holding back.

Language/Culture

o The biggest challenge I have had is that there are many Realtors® that do not speak English very well. Because of this, my workload on an average transaction has been more than it should have been.

o We Realtors® should be more prepared in giving clear and understandable explanations to our foreign buyers. This way they can easily understand the buying process before, during and after their purchase is completed.

36

Association Assistance/Support

o Maybe more education in other languages about international buyers. o More class in Spanish. o More information and capacity in Spanish and Italian. o More nice videos about all Miami each different- areas, life-style like Brickell Aventura edge

water south beach etc...should be made separately and posted on YouTube. We should sell Miami lifestyle first.

o More oversees marketing. o Would like to see more classes on working with international buyers and the implications. o Need more info on immigration status to own a property because the info for financing or tax

related charges are well explained.